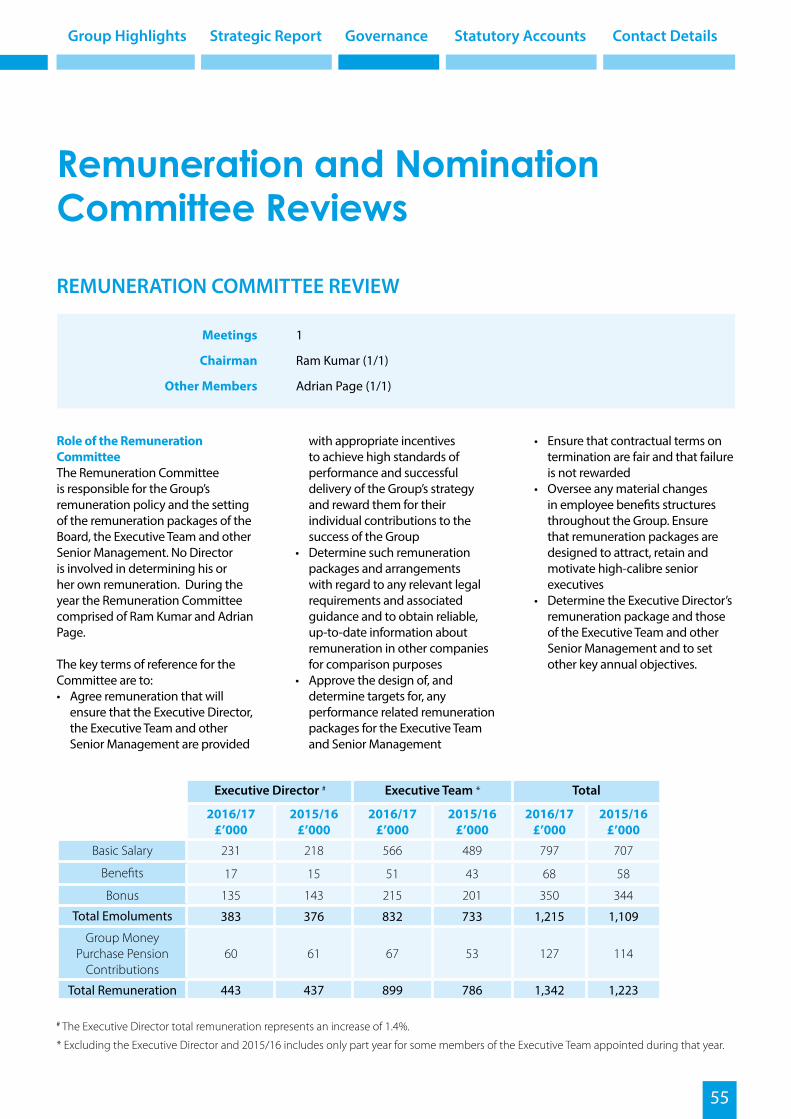

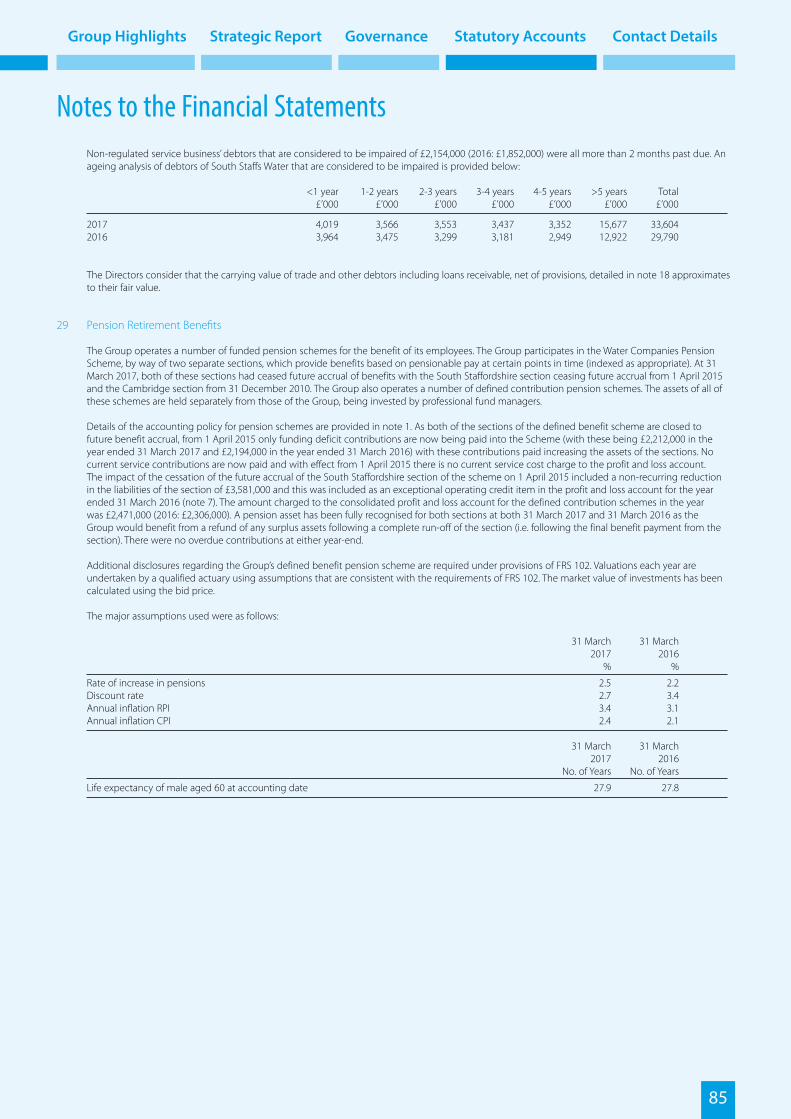

ANNUAL REPORT 2017 - South Staffordshire · Welcome to South Staffordshire Plc’s Annual Report...

92

ANNUAL REPORT 2017

-

Upload

trinhduong -

Category

Documents

-

view

214 -

download

0

Transcript of ANNUAL REPORT 2017 - South Staffordshire · Welcome to South Staffordshire Plc’s Annual Report...

ANNUAL REPORT 2017

2

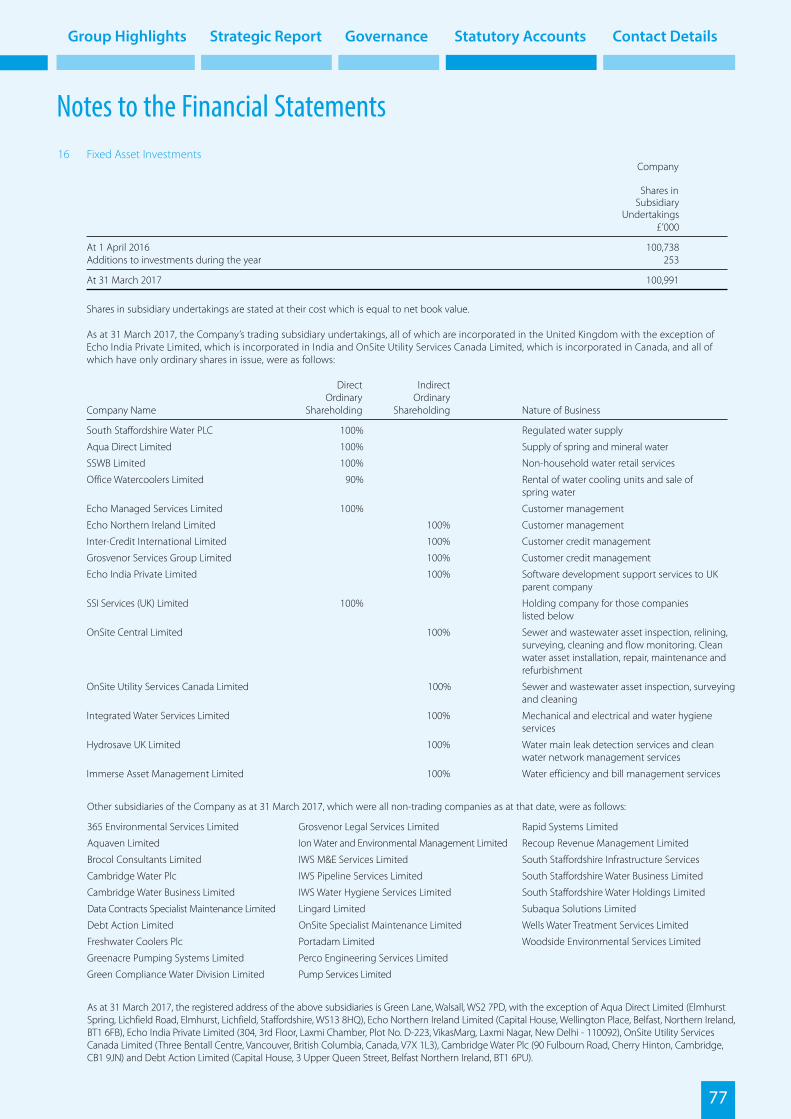

Front cover and aboveSeedy Mill UV Treatment Plant project

South Staffs Water, supported by its partners including SSI Services, completed the installation of one of the UK’s largest UV clean water treatment plants at Seedy Mill Treatment Works.

Underground wet contact tanks were converted into two dry chambers, each housing two UV reactors. The project was completed to schedule whilst still ensuring that Seedy Mill remained operational, with all water leaving the site now being treated by UV.

More details about this project can be found in the Strategic Report on pages 13 and 21.

Welcome to South Staffordshire Plc’s

Annual Report 2017

Group Highlights 4

Strategic Report 6Executive SummarySouth Staffs WaterSSI ServicesEchoCorporate Social ResponsibilityFinancial Review

Governance 44Board of Directors and Executive TeamDirectors’ ReportCorporate Governance Report and Committee ReviewsDirectors’ Responsibilities Statement

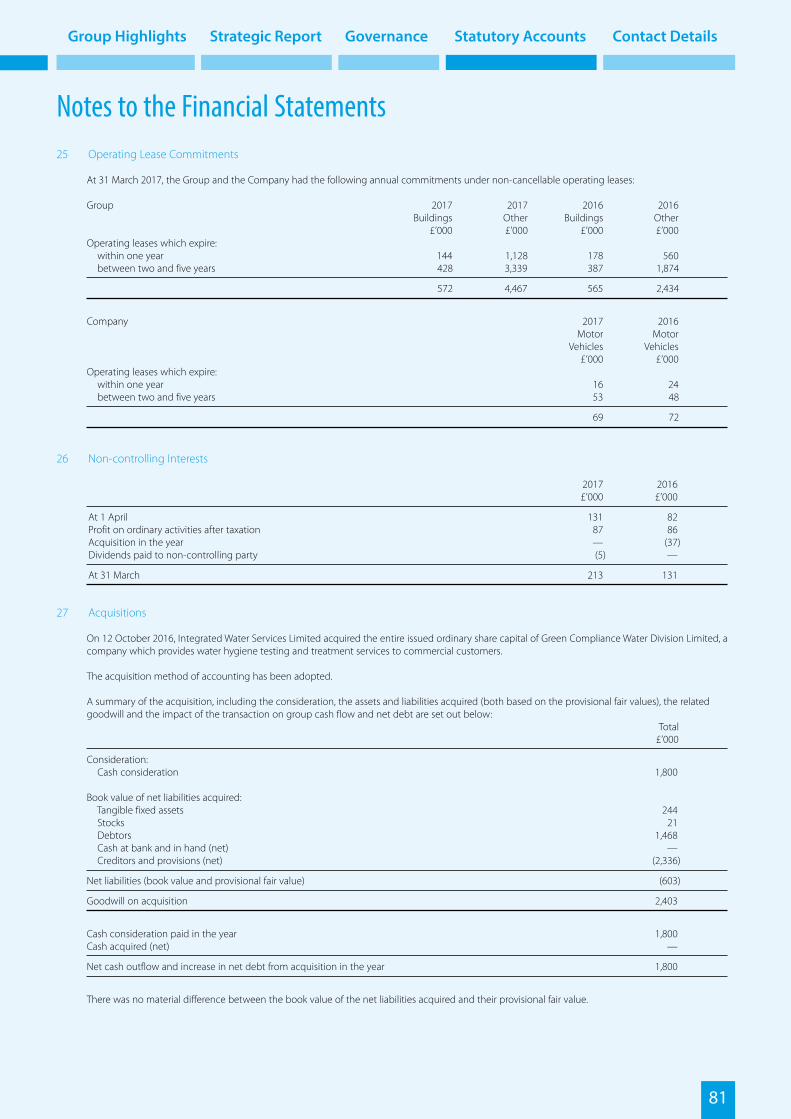

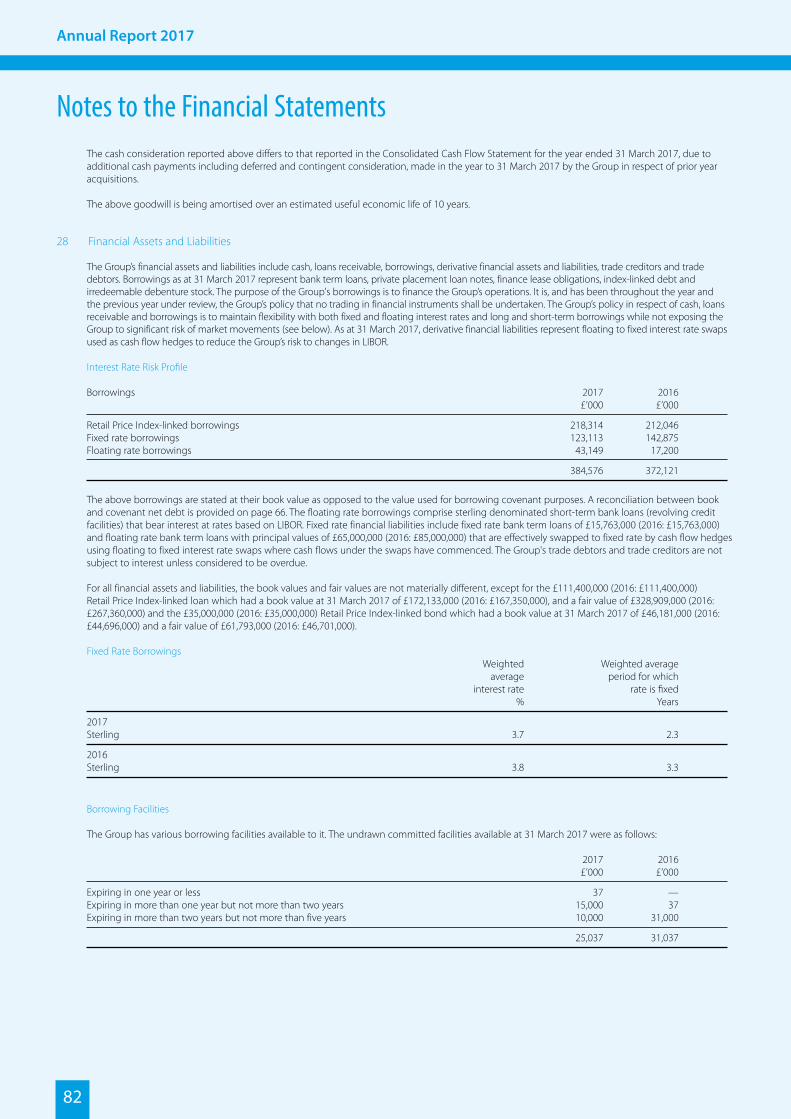

Statutory Accounts 58Independent Auditor’s ReportConsolidated Profit & Loss AccountConsolidated Balance SheetCompany Balance SheetConsolidated Statement of Changes in EquityCompany Statement of Changes in EquityConsolidated Statement of Comprehensive IncomeConsolidated Cash Flow StatementNotes to the Consolidated Cash Flow StatementNotes to the Financial Statements

Contact Details 88

4

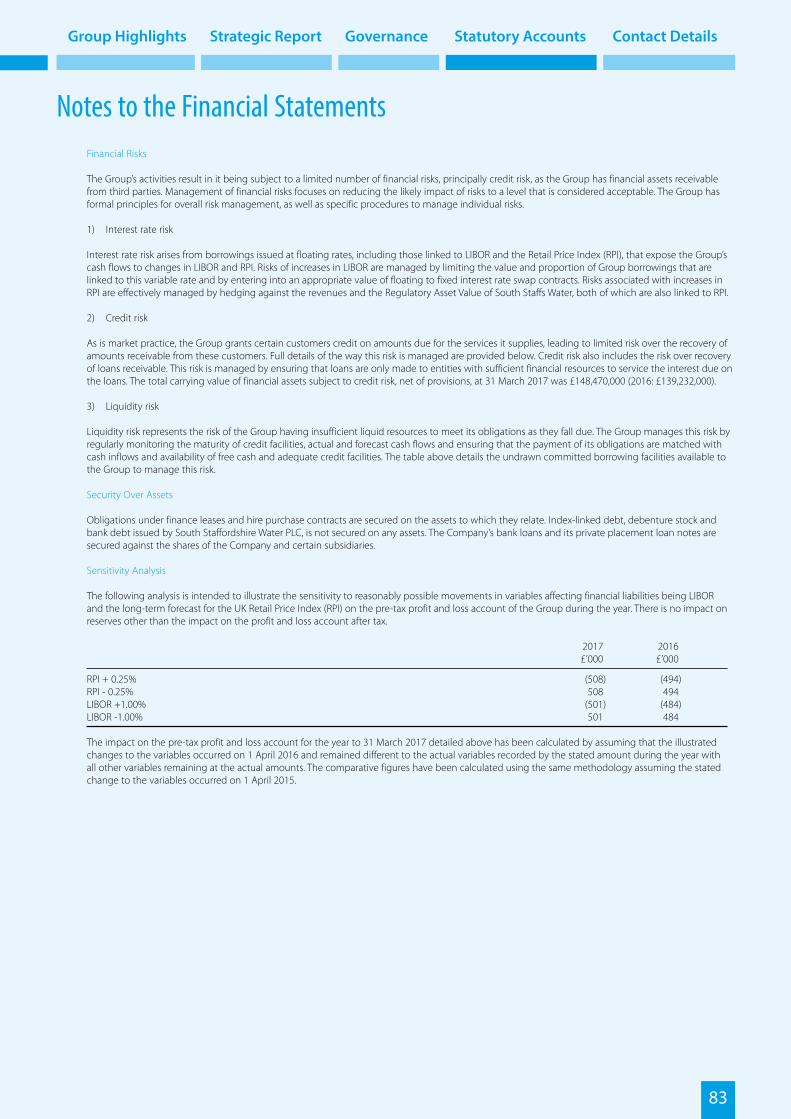

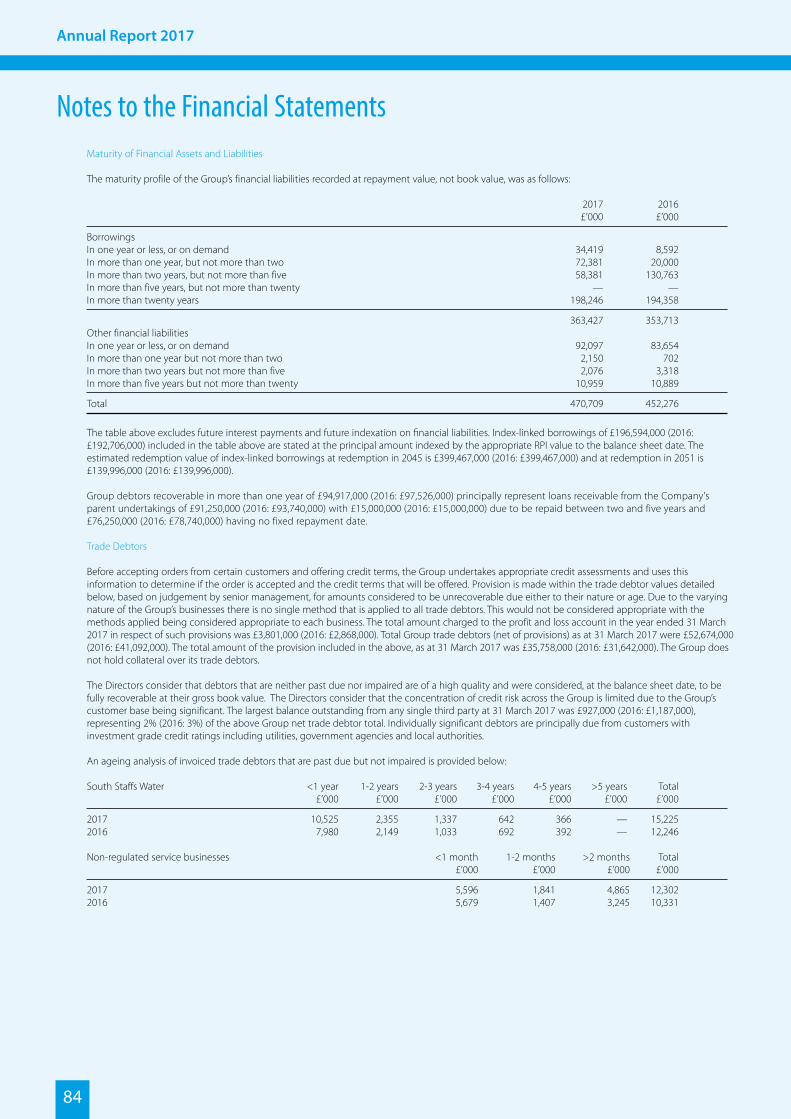

Annual Report 2017

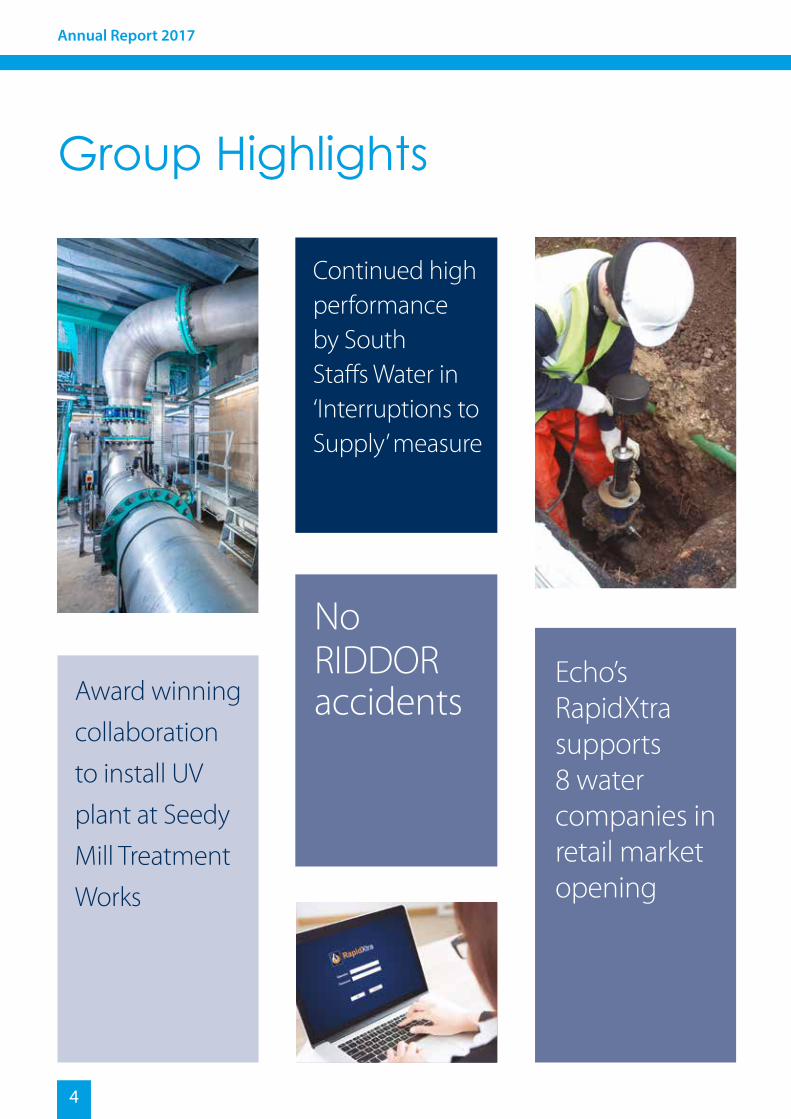

Group Highlights

Award winning collaboration to install UV plant at Seedy Mill Treatment Works

Echo’s RapidXtra supports 8 water companies in retail market opening

Continued high performance by South Staffs Water in ‘Interruptions to Supply’ measure

No RIDDOR accidents

5

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

Echo shortlisted for 19 Industry awards, winning four All Group

Health and Safety targets again met or exceeded

Disappointing performance on complaints in South Staffs Water

Over £60k raised for WaterAid

Strong organic growth across SSI Services

Turnover increased by 5.6% to £248m

6

Annual Report 2017

Strategic ReportExecutive Summary

Group overview, strategy and business modelSouth Staffordshire Plc is a highly respected integrated services group of businesses. The Group includes a regulated water supply company, South Staffs Water, comprising two operational regions, South Staffs and Cambridge, and also two non-regulated service divisions, SSI Services and Echo.

The Group’s strategy remains to continue to grow by providing high levels of service quality, while remaining price competitive in all of its operations, through driving continuing business improvement and operational efficiency, as well as maintaining a safe and enjoyable working environment. Details of how this strategy is implemented across the Group and the individual divisional strategies, business models and plans are provided throughout the Strategic Report.

South Staffs WaterSouth Staffs Water has again achieved good performance against most of its Outcome Delivery Incentives, with pleasing results in water quality, interruptions to supply, encouraging and enhancing biodiversity, as well as providing support for customers in debt. There was also the successful completion of a significant investment in a water quality enhancing UV plant at one of its main treatment works.

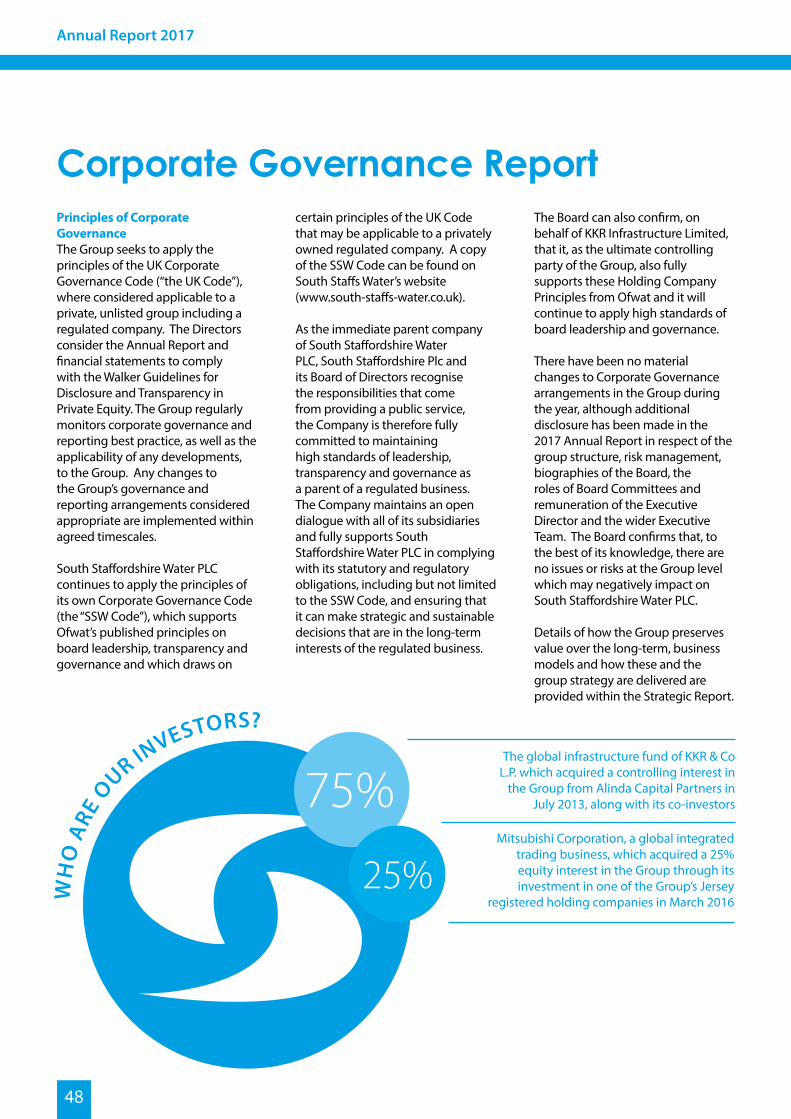

The business has, however, encountered some disappointments during the year, particularly in its Service Incentive Mechanism (SIM) score – the water industry customer service measure. Efforts to drive efficiency to ensure that customers continue to experience great service at a fair price have had an unfortunate impact on the overall customer experience, in this period resulting in an increase in complaints. South Staffs Water is making significant efforts to reverse this, the benefits of which can already be seen so far in the 2017/18 year, with improvements in the SIM score achieved.

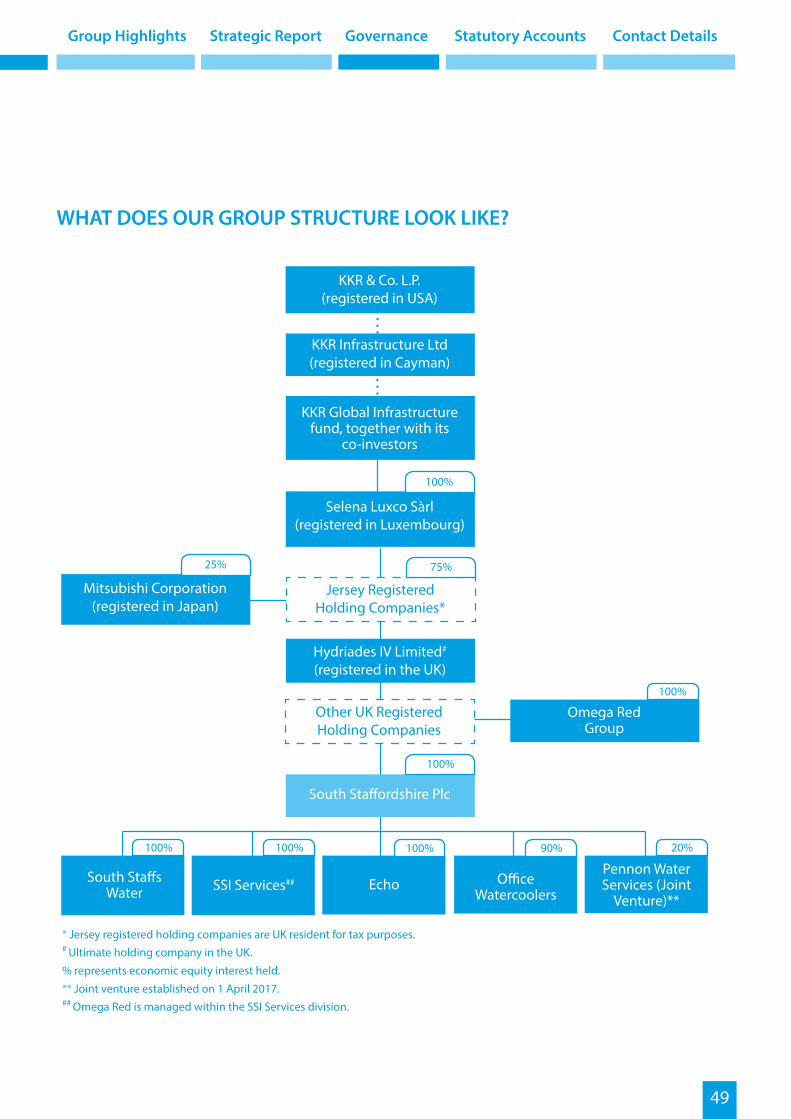

During the year, preparations for the launch of the Non-Household retail market were a key area of focus for the business. A readiness program was delivered, to ensure that our operations were in place for the 1 April 2017 ‘go live’; when South Staffs Water exited the Non-Household retail market by transferring its related assets and operations to a sister company SSWB Limited. This company was then transferred to Pennon Water Services, as part of a joint venture between South Staffordshire Plc and Pennon Group Plc.

South Staffs Water is now working to deliver the remainder of its AMP6 commitments, as well as preparing for PR19, which demands a level of innovation, flexibility and responsiveness not previously seen in the water industry.

EchoThroughout the year, Echo’s Rapid business has helped all of its clients, both retail and wholesale, to successfully comply with the new requirements for Non-Household retail competition, as well as interact with the market operator and compete effectively in the new environment. However, whilst this was a significant success for Echo, our clients understandable focus on Non-Household retail competition led to reductions in other work for Rapid. Echo continues to monitor developments to ensure its clients remain compliant and competitive.

Echo’s debt recovery solution focuses on the customer experience, and the business continues to be awarded new contracts, putting the business in a strong position within its core sector, UK utilities.

The business is particularly proud to have been shortlisted for 19 industry awards across a variety of customer service and debt collection award programmes, four of which it won.

7

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

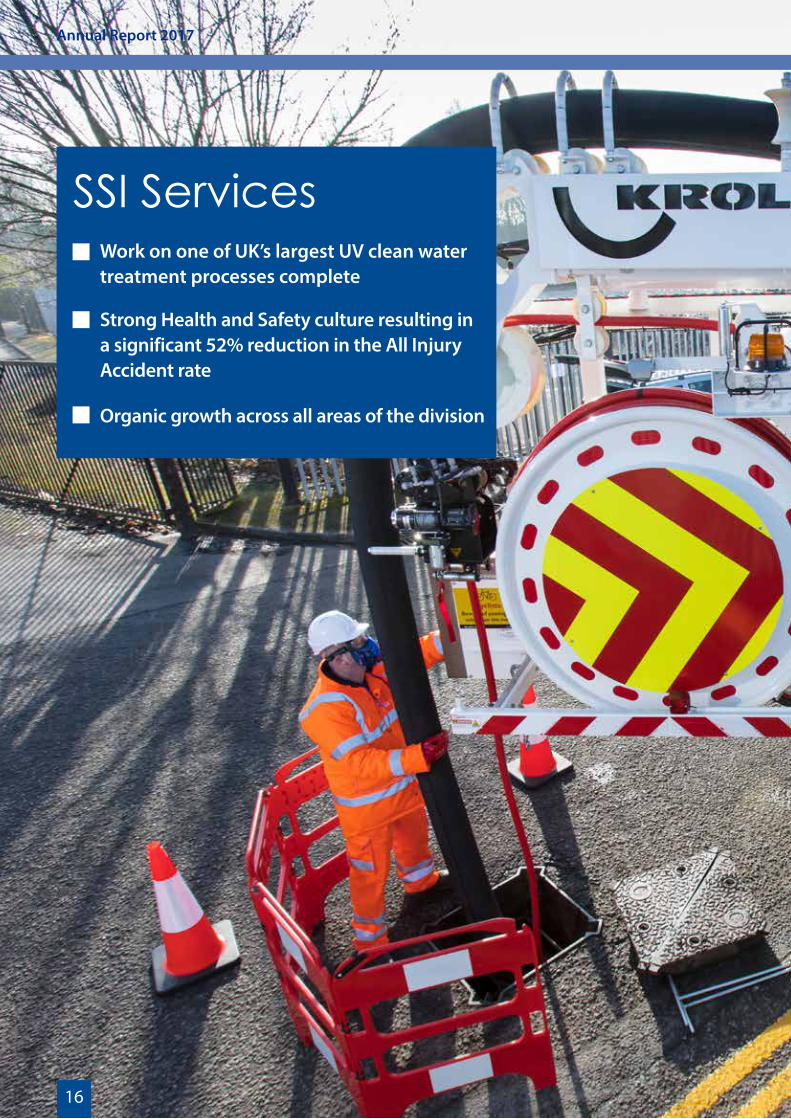

SSI ServicesOverall, the division has experienced an encouraging year, seeing organic growth; including an increase in demand for its specialist skills and technologies, along with the successful completion of some important client projects. The division is now seeing the benefits of its risk management plan and is less reliant on individual customers and the water industry five-year AMP cycle. The division’s excellent Health and Safety performance saw a reduction in the All Injury Accident rate by 52%, reflecting the significance the divison, and the Group as a whole, places on Health and Safety.

The Mechanical and Electrical business had an excellent year, securing four new frameworks that mean the business now has twelve secured frameworks with eight major clients.

During the year, a decision was taken to integrate the businesses of Onsite Specialist Maintenance, Perco and IWS’s Pipeline Services into OnSite, which is intended to bring economies of scale, greater clarity surrounding the business’ market offering, improved customer experience and brand awareness.

Real benefits are expected be realised in the future, as the new structure is established.

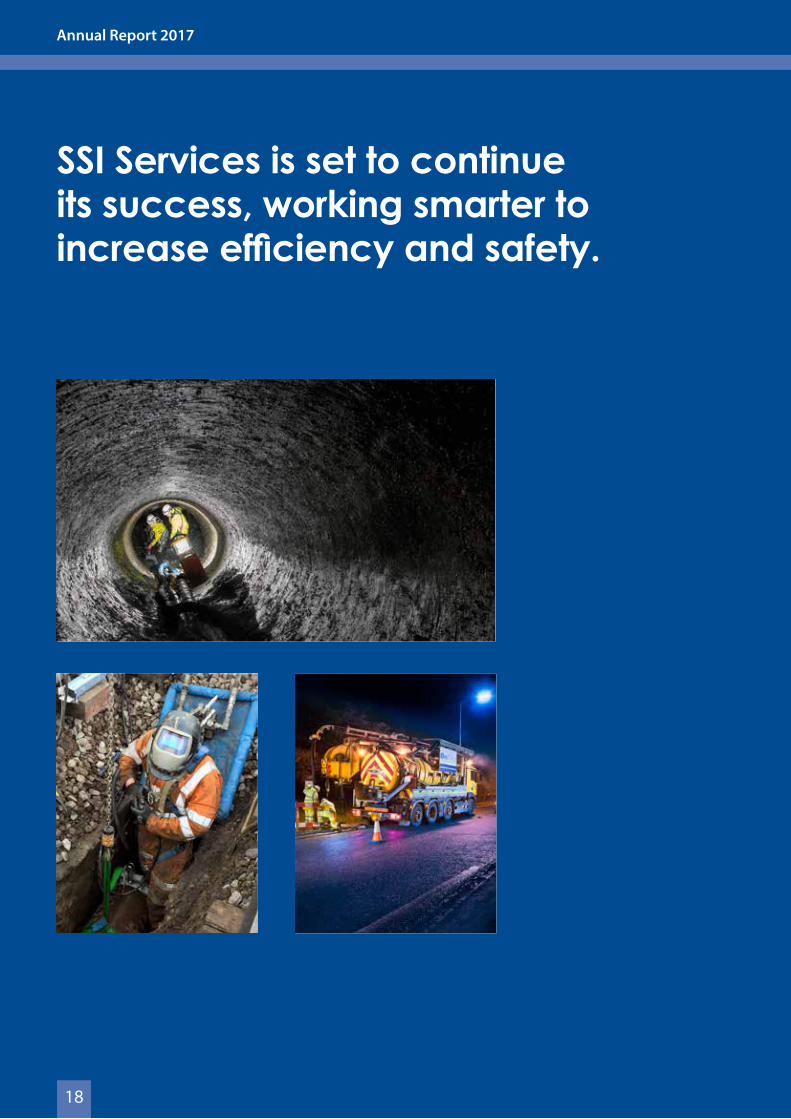

SSI Services is set to continue its success and grow in the existing markets in which it operates, targeting further organic revenue growth whilst seeking further cost efficiencies, including smarter working processes and systems through continuing investment in technology.

FinancialThe Group outperformed key financial targets, including challenging budgets for turnover, profitability, cash flow and net debt. Overall, Group turnover increased by 5.6% in the year to £248.0m, with as budgeted, EBITDA of £81.9m (before infrastructure renewals - see reconciliation on page 37) remaining largely in line with the previous year. Operating profit for the year was £43.8m (2016: £47.5m before exceptionals). Capital investment of £44.2m (2016: £35.9m) was completed in addition to investment in infrastructure renewals of £8.7m (2016: £7.5m) in the year.

EmployeesAs always, the success of the Group could not be achieved without the hard work and dedication of our employees. We thank them for their continued support and commitment to the Group.

The Health and Safety of our employees is of prime importance, and we are pleased to once again report that each business met, or exceeded, their targets for reduction in accidents. It is pleasing to note that no RIDDOR accidents were recorded across the Group, compared to seven during the previous year. Going forward, each business unit has been tasked with setting a business plan to achieve a minimum of 10% improvement on 2016/17’s Health and Safety performance.

OutlookOverall, through its ability to efficiently provide high quality services at competitive prices, the Group remains in a strong position to continue its work in maximising the opportunities available to it, while preparing for the undoubted challenges ahead.

8

South Staffs WaterContinued high performance in Interruptions to Supply

Successful completion of one of the UK’s largest UV clean water treatment plants

Annual Report 2017

Introduction of a new social tariff, ‘Assure’

9

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

In a year of challenge, South Staffs Water continues its focus on providing the highest quality water, while remaining affordable, to our customers.

Annual Report 2017

10

11

OverviewSouth Staffs Water is a water only company, supplying around 1.6 million customers in the South Staffordshire and Cambridge regions.

The water industry is undergoing unprecedented transformation. With complex challenges including deregulation, environmental pressures and significant changes in the demands of the UK population the business is developing a new flexibility in how it operates that means it can respond quickly and adapt as necessary to take full advantage of the new landscape.

Underpinned by significant customer engagement, the new Outcome Delivery Incentive (ODI) targets included in the plan have been designed to deliver what is important to our customers. This is captured within five Outcomes and 15 specific ODIs, covering all aspects of operations from water quality, secure and reliable supplies, customer services and environmentally sustainable operations to fair customer bills.

Alongside the ODIs, there are seven business targets, including a focus on readiness for competition, employee satisfaction, as well as safety and wellbeing.

of these was undertaken at the Seedy Mill treatment works. A multimillion pound investment created the second largest clean water UV (Ultraviolet) treatment plant in the UK. The resulting benefit of enhanced water quality and compliance will be replicated with additional investment in the coming year, including the installation of UV treatment at our largest treatment works.

Fair and affordable bills for all of our customersSouth Staffs Water’s household customers continue to enjoy some of the lowest bills in England and Wales. We are committed to maintaining affordability of bills, as well as supporting our most vulnerable customers with a range of help when they need it most. During the year, we exceeded our performance commitment in providing extra help to over 23,000 customers in debt, helping them to manage their water accounts and take control of their consumption.

Our range of solutions for customers that struggle with bills expanded with the introduction of the new “Assure” social tariff. It offers a discount of up to 80% on bills, subject to eligibility which is based on income and expenditure. During the year 4,066 customers were signed up to the Assure tariff. In addition, we are seeing real benefit to some of our most

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

Together, they provide a real focus for delivery as we meet the challenges and opportunities this five year period presents, while still ensuring that excellent customer service, alongside a reliable, high quality water supply with affordable bills, remains at the heart of everything we do.

The highest quality water, today and tomorrowThe single most important area of our operation is ensuring the water we supply to customers every day is of the highest quality. Improving the quality of our water beyond simply meeting regulatory commitments is a principal objective for the business, with an aim to achieve 100% water quality compliance and an improved customer perception of our water through appearance, taste and odour. The business aspires to an unrestricted, uninterrupted supply of water of the highest possible quality.

Following a challenging period in the previous year, we have seen an improvement in our acceptability of water measure, both in terms of our compliance score and in a reduced number of customer contacts about water quality, driven by investments in the business’ assets and processes.

Quality driven investment was undertaken across our assets including a number of borehole refurbishments. The most significant

12

“We continue to find better ways to listen to our customers and respond to what we hear from them.”

91%satisfaction score for value for money

and affordability

vulnerable customers in providing sensitive face to face assistance to them in their own homes. We plan to expand on this valuable work in the year ahead.

Excellent customer service, every timeAt South Staffs Water we recognise the importance of responding to lifestyle changes, offering greater choice and flexibility in how customers can access information and make contact with us. The expansion of the online account management service, MyAccount, into our Cambridge region was a key stage in the continued expansion of our digital offering.

However, in the last year there has been some negative impact on the customer experience as a result of changes in billing services, as well as some of our operations in the field and contact centre. Whilst these changes will deliver long-term sustainable efficiencies and improvements, the short-term effect in the first half of the year was a deterioration in our level of customer service. As a result, we were not in our targeted upper quartile position of Ofwat’s SIM measure for the year. As a result of this, significant efforts in training of staff, along with a review of our processes and systems, were made to reverse this trend and ensure that we are consistently delivering the quality of service our customers expect. We were pleased to see our SIM performance start to improve in the latter half of the year, and correspondingly complaint numbers began to glide back towards their traditional low levels.

We continue to find ways to better listen to our customers and respond to what we hear from them. More in-depth, regular research has been put in place to better understand customers’ current and future needs, as well as their views of our services.

The results are being used to inform business decisions which match with what customers have told us they value. We will also involve them in the shaping and creation of a future services.

These research findings are being complemented by contributions from the new Independent Water Customer Panel, who meet quarterly. On the panel there are representatives from the Environment Agency, CCW water and other members with a variety of skills and expertise within public and private sectors. They use their skills and expertise to actively challenge how we as a Company, engage with our customers and perform as a business. This has been a significant achievement for us this year. In addition, one of the South Staffs Water Independent Non-Executive Directors attends the panel to compliment attendance by Senior Management and to ensure that the appropriate actions are being taken based on the meeting outcomes. We welcome the independent and challenging contribution the panel brings.

South Staffs Water has commenced publishing in year performance results, initially for our South Staffordshire region, on our website. These are unaudited but in a format which customers can easily follow.

Secure and reliable supplies, now and in the futureWater efficiency is fundamental to safeguarding supplies and the business remains committed to helping customers change the way they value and use water every day through an ongoing programme of educational engagement.

We have maintained a strong performance on minimising supply interruptions, and will continue to focus on ensuring that our pipes and networks are well maintained

Annual Report 2017

13

Completion of one of the UK’s largest UV clean water treatment plantsSeedy Mill is South Staffs Water’s second largest surface water treatment works. There have been numerous modifications and extensions to the facility but it was still principally operating using the same technology and processes since its initial construction in the 1950s.

As part of our commitment to the highest water quality standards, we chose to design and retro-fit a state-of-the-art UV treatment technology into the existing structure, in collaboration with Integrated Water Services and the UV technology supplier, atg UV Technology, whilst keeping the works operational. The proven, regulated and environmentally friendly UV

technology ensures water is free from harmful organisms, and means less chlorine is needed, reducing the risk of issues with taste and odour.

Underground wet contact tanks were converted into two dry chambers in separate phases to keep the plant operational, each housing two UV reactors, with each containing 30 glass tubes, making the facility one of the

“We have maintained a strong performance on minimising supply interruptions this year.”

and that decisions regarding our infrastructure place us in the best possible position to provide secure and reliable supplies.

The benefits of addressing challenges in this area are increasingly evident. We will continue to work closely with the Environment Agency to maintain practices that are environmentally responsible, as well as develop appropriate partnerships that will provide innovative solutions.

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

Successful collaboration with the University of Cambridge will, this coming year, see completion of Phase 1 of the award-winning £1 billion North West Cambridge development, supplying 3,000 homes, 2,000 student rooms and other community facilities from the UK’s largest rainwater recycling scheme. We see this as a living example of how future developments in a water scarce area which is also seeing continued and significant population growth should be approached.

largest UV water treatment plants in the UK. A project of this scale would normally take two and a half years but it was completed in just ten months. The speed of the construction did not negatively impact on Health and Safety, with eight main contractors and sub-contractors, over 90 suppliers and 200 plus craftsmen and technicians on site with no lost time injuries.

14

“The recruitment of seven apprentices in the year represents a commitment to investing in future talent.”

99.98%water quality

compliance

Connecting with our communitiesSouth Staffs Water aims to make a positive difference, developing strong and lasting partnerships with the communities in which we live and work through education about water usage and efficiency, as well as enhancing biodiversity and charitable support.

We have an ambitious target to deliver at least 400 days of support in our communities through initiatives including an education programme, biodiversity projects and our employee volunteering scheme. This remains a challenge as, whilst we have made a difference in supporting schools, charities and other organisations, we ended the year on a total of 222 days.

A change in how we approach engagement with schools has been introduced during the year. We believe that by switching from a location based offering in the South Staffs region alone to an outreach service in both regions, we are better placed to meet the demands of educational institutions, allowing us to increase our work in this area.

Environmentally sustainable operationsThe business understands and recognises the impact of its operations and is dedicated to protecting our environment. We work hard to maintain our good long-term track record on leakage and ensure we continue to meet our targets. This includes fitting additional flow meters to automatically monitor consumption, and so support our leak detection performance improvements.

Our active approach to catchment management as a long-term solution to improving the quality of raw water includes developing partnerships with key stakeholders, undertaking relevant research, participating in initiatives, and acting as an education resource.

Our new SPRING Environmental Protection Scheme has built on previous success to further support arable farmers in the Blithe catchment area. Grants are made available by the Company towards the costs of voluntary on-farm infrastructural improvements and agricultural management schemes designed to protect the environment and improve water quality, such as contour cropping and pesticide sprayer washdown.

We also work to deliver innovative projects that will enhance biodiversity across our region. The first round of funding from our PEBBLE fund (Projects that Explore Biodiversity Benefits in the Local Environment) has rewarded applications ranging from creating a wildlife walk, and clearing scrubland, to supporting a school keen to raise awareness of the environment and local wildlife among pupils.

Valuing our peopleWe are committed to making South Staffs Water a great place to work with a safe, positive, and rewarding working environment. We maintained our performance on accidents in the workplace last year and continue to place a strong focus on ensuring the highest employee safety standards, with a target to further reduce accidents in the coming year.

The recruitment of seven apprentices in this year represents a commitment to investing in future talent and a recognition of the importance of succession planning. The apprentices each have a mentor to support them as they gain experience from rotating across the wholesale division of the business alongside gaining formal qualifications.

Annual Report 2017

15

Our annual employee survey plays an important role in helping us to understand the feelings and motivations of our people, with the results providing direction for change and improvement in areas such as training and development.

Readiness for Open WaterThis year saw a focus on ensuring our systems, processes and organisational structures were in place for Non-Household retail business opening up for competition in April 2017. Robust preparation ensured both the risks and opportunities associated with the significant changes were identified and planned for appropriately, with the business meeting all compliance requirements at Go Live.

On 1 April 2017, South Staffs Water transferred its Non-Household retail operations and related assets to SSWB, a fellow Group company. On the same day, South Staffordshire Plc transferred its shares in SSWB to Pennon Water Services (PWS), in return for a 20% equity share in PWS. South West Water transferred its Non-Household retail operations to PWS on the same day, therefore forming a joint venture between South Staffordshire and the quoted Pennon Group to operate in the Non-Household retail market.

Our Future FocusMuch of our future activity is mapped out, and so, we must continue to focus on ensuring that the predicted benefits of our planned investments are fully realised. However, AMP6 and the period beyond demand a degree of flexibility and responsiveness not previously seen in the water industry. To meet our commitments, we need to demonstrate a combination of collaboration, innovation, long-term planning and careful investment.

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

The biggest single challenge we face is finding the best way to consistently deliver high quality water at great value with excellent service for future generations, as well as today’s customers, in a sustainable way. We have to consider this whilst not ignoring the significant economic, social and environmental challenges this presents. We have begun significant planning to be able to submit our next five year business plan to the economic regulator, Ofwat, in September 2018. Amongst other matters, it will lay out what we plan to do to ensure our network of pipes, reservoirs, pumping stations and water treatment facilities are fit for the future, as well as how this will be paid for.

To ensure we get it right, we will need to work with everyone who is affected by water use in our region – from big business owners and housing developers to customers in our communities and other stakeholders. We will work to share our ideas, listen to the opinions and ideas of other, learning from them to form a plan together. That way, we can be sure that the commitments and measures we include in our plan truly reflect what is important to our customers.

“To meet our commitments, we need to be collaborative, innovative and flexible.”

New ‘Assure’ social tariff introduced to support vulnerable customers

16

SSI ServicesWork on one of UK’s largest UV clean water treatment processes complete

Strong Health and Safety culture resulting in a significant 52% reduction in the All Injury Accident rate

Organic growth across all areas of the division

Annual Report 2017

17

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

18

SSI Services is set to continue its success, working smarter to increase efficiency and safety.

Annual Report 2017

19

OverviewSSI Services is the Group’s specialist infrastructure contracting division. We provide a broad range of specialist infrastructure based services, including design and installation, testing and repair, as well as long-term maintenance. Our main focus is on the management of client risk and legislative needs, principally in regulated environments, providing added value using specialist skills, equipment and technologies.

We have developed a very broad customer base across both the public and private sectors, from all major water utilities, industrial processing companies, infrastructure providers, government agencies and local authorities through to major contractors and facilities management (FM) companies. Historically, we have mainly worked in the water and wastewater sector, however to diversify, as well as to manage risk and demand we are now increasingly operating in the water hygiene, rail, power generation, industrial and construction markets. Our strategy continues to be to deliver these services through a number of specialist operating companies using a nationwide mobile operation, along with maintaining strong, long-term relationships with our customers by providing value for money with quality services at competitive prices.

A successful yearOur objective in 2016/17 was to build on the growth and stability of the successful trading concluded in the previous year, whilst also restructuring the division so as to create a consistent team approach. The substantial growth in both revenue and profit has been achieved organically, with only one small acquisition, that of Green Compliance Water Division by IWS, Water Hygiene being completed in October 2016.

The division is now less reliant on the water industry five-year AMP expenditure cycle, with increased revenue now being generated outside of this sector, in line with our risk mitigation plan. This is set to continue and makes the division more resilient.

Clean Water ServicesThe Clean Water business includes two operating units – IWS Mechanical and Electrical (M&E) Services and Hydrosave, which provides water management services, with a number of common clients across the two businesses.

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

The division has around 1,900 employees, all of whom are key to our success, with the majority operating remotely and in often challenging environments. Health and Safety is therefore at the heart of our businesses, and we continue to focus on developing a strong Health and Safety based culture across all of our businesses. The hard work and commitment of all of our employees has enabled the division to achieve all of its safety targets, whilst noting that further improvement can still be made. Importantly, the division suffered no RIDDOR reportable events during the year, compared to three in 2015/16, with the All Injury Accident rate reducing by 52%.

SSI Services is made up of three business areas, Clean Water, OnSite and Water Hygiene. In addition, Omega Red, which provides lighting protection and electrical earthing services, also trades as part of SSI Services. During the year, a decision was taken to integrate Onsite Specialist Maintenance, Perco and IWS’s Pipeline Services into OnSite, which was completed in August 2016. This integration will bring economies of scale, greater clarity surrounding our market offering, improved customer experience and brand awareness.

20

“OnSite’s Rail division is now recognised as a highly respected operator in this specialist sector.”

52%reduction in All Injury Accident rate

The M&E business has had an excellent year with significant growth mainly attributable to the full year impact of the Essex and Suffolk Water framework contract and growth at both our Accrington and Dorchester depots. Throughout the year, the business has managed to secure four new frameworks, meaning that it now has twelve secured frameworks with eight major clients from which to source work, reducing reliance on any single client.

Hydrosave also had a very good trading year. The mainstream Leak Detection contracts have performed strongly, and the newly formed Test Inspect Consult consultancy arm has also performed well during the year, being set to enter the Gas sector in the coming year, providing access into this highly specialised area as we aim to grow our consultancy offering.

OnSiteOnSite, which offers specialist wastewater services, including flow monitoring, sewer rehabilitation and CCTV surveys, had a very busy year. The Rail division that was formed organically in 2014/15 delivered a number of schemes throughtout the year and is now recognised as a highly respected operator in this very specialist sector. The Flow Monitoring department contributed to the year-on-year growth by securing a significant project from a new client, that is set to continue into 2017/18. Further capital has been invested into the business to purchase new plant and equipment so as to support this growth, taking full advantage of years 3 and 4 of the water sector’s AMP period, when activity levels are anticipated to be high.

The Sewer Lining division experienced a good year whilst also targeting increased revenue outside of the traditional water sector market in order to lessen the impact of the water sector’s AMP cycle on the business.

OnSite Specialist Maintenance had a challenging year, due to varying work types. However, a new 3-year framework has been secured within the year, with activity levels increasing at the end of 2016/17, which is encouraging for the year ahead. OnSite Trenchless also experienced a challenging year, due to two schemes that did not deliver in line with expectations. However, the introduction of additional management resource towards the end of the year has yielded positive results.

The changes made within Pipeline Services during previous years have proved to be successful. The five-year contract with South Staffs Water continues to perform well and in line with our expectations. Additional projects with various clients also performed in line with our plan. With the integration into OnSite completed in August 2016, real benefits should be realised in the future as the new structure takes hold.

Water HygieneIWS Water Hygiene is a market leading provider of legionella control services and water hygiene risk assessment, maintenance and remedial works, together with a comprehensive water treatment service, servicing a wide range of customers including local authorities, housing associations and FM companies. The business offers a 24 hours a day, 365 days a year national mobile service supported by the use of technology, which we continue to invest in.

Annual Report 2017

21

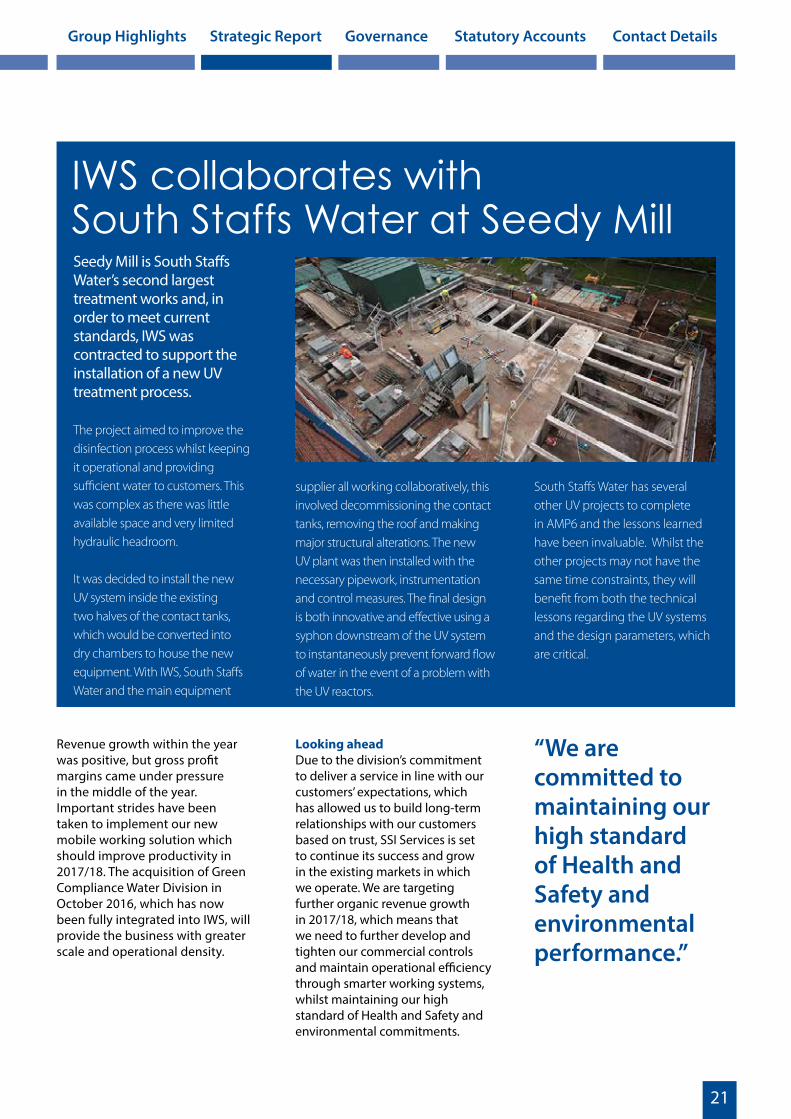

IWS collaborates with South Staffs Water at Seedy MillSeedy Mill is South Staffs Water’s second largest treatment works and, in order to meet current standards, IWS was contracted to support the installation of a new UV treatment process.

The project aimed to improve the disinfection process whilst keeping it operational and providing sufficient water to customers. This was complex as there was little available space and very limited hydraulic headroom.

It was decided to install the new UV system inside the existing two halves of the contact tanks, which would be converted into dry chambers to house the new equipment. With IWS, South Staffs Water and the main equipment

supplier all working collaboratively, this involved decommissioning the contact tanks, removing the roof and making major structural alterations. The new UV plant was then installed with the necessary pipework, instrumentation and control measures. The final design is both innovative and effective using a syphon downstream of the UV system to instantaneously prevent forward flow of water in the event of a problem with the UV reactors.

“We are committed to maintaining our high standard of Health and Safety and environmental performance.”

Revenue growth within the year was positive, but gross profit margins came under pressure in the middle of the year. Important strides have been taken to implement our new mobile working solution which should improve productivity in 2017/18. The acquisition of Green Compliance Water Division in October 2016, which has now been fully integrated into IWS, will provide the business with greater scale and operational density.

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

Looking aheadDue to the division’s commitment to deliver a service in line with our customers’ expectations, which has allowed us to build long-term relationships with our customers based on trust, SSI Services is set to continue its success and grow in the existing markets in which we operate. We are targeting further organic revenue growth in 2017/18, which means that we need to further develop and tighten our commercial controls and maintain operational efficiency through smarter working systems, whilst maintaining our high standard of Health and Safety and environmental commitments.

South Staffs Water has several other UV projects to complete in AMP6 and the lessons learned have been invaluable. Whilst the other projects may not have the same time constraints, they will benefit from both the technical lessons regarding the UV systems and the design parameters, which are critical.

22

Echo13 contract awards including new clients and existing client extensions

RapidXtra supports all eight clients to be compliant and ready on time for the Non-Household water retail market opening

Annual Report 2017

Shortlisted for 19 industry awards, winning four

23

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

Annual Report 2017

Echo’s innovative and cost effective solutions have supported new and existing clients, both within and outside the water sector.

24

25

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

OverviewEcho is a specialist outsourced provider of complex multi-channel customer contact services, comprehensive debt and revenue management solutions, as well as being the developer of the UK’s market leading water billing and customer information software, RapidXtra. Echo’s strength is combining best practice specialist services and solutions with highly skilled and knowledgeable people.

The past year has seen both changing and challenging market conditions. In the water industry, companies have focused on delivery and compliance with the opening of the new Non-Household retail market. In the household market, high customer service aspirations, along with protecting revenues, remain pressing against a backdrop of cost to serve constraints and increased regulatory scrutiny around customer affordability and vulnerability. This changing landscape, characterised by consolidation among incumbents, new market entrants and the first steps towards a multi-utility market, has led to both challenge and opportunity for Echo.

Tightening regulations within the debt services sector and the growing focus on treating customers fairly continue to change the debt market. As debt levels continue to rise across the UK, customers’ ability to pay this debt has reduced, making it more difficult for companies to collect what is owed to them.

In the outsourced contact centre industry, competition remains fierce, placing pressure on profit margins. The marketplace is increasingly polarised, with those that innovate, embrace new technologies and become customer-centric continuing to prosper, while others face further challenges. The trend of returning contact centre services on-shore continues, as businesses seek competitive advantage through service excellence.

Despite these conditions, Echo’s ability to offer innovative and cost-effective solutions to meet client challenges has led to both new business and extended relationships with existing clients.

Our expertise once again received recognition, with the division shortlisted for 19 awards across a variety of customer service and debt collection award programmes. Winning four of these is a particular highlight, including the Utility Sector’s Customer Facing Team of the Year and the South West’s Outsourced Contact Centre of the Year.

Our people, our greatest assetPeople are key to delivering great service on behalf of our clients. During the year, we focused on engagement and communication, with our annual employee engagement survey incorporating Echo’s values for the first time to measure how they have started to become embedded within the business. Results were shared

with employees, with focus groups meeting across all sites to deliver any required improvements. The Employee Voice forum was created, with elected employee representatives meeting Senior Management bi-monthly to help make Echo an even better place to work.

Market leading customer billing in an evolving marketEcho’s billing and customer information solution, RapidXtra, continues to hold a market leading position within the UK water sector. The past year was challenging and extremely busy as we navigated evolving market and regulatory requirements to successfully assist all eight of our water company clients, including both wholesalers and retailers to become fully compliant with and ready on time for the opening of the Non-Household retail market.

RapidXtra Retail successfully provided all the additional required functionality to comply with the new regulations, interact with the market operator and compete effectively in the new environment. As the Non-Household retail market evolves, we are closely monitoring developments, reacting swiftly to any regulatory changes, allowing our clients to remain compliant and competitive. Planned upgrade releases will add yet more enhancements to our clients’ customer service and billing

26

“Echo’s offering leverages the importance of the customer experience throughout the debt recovery process.”

19 industry

awardshortlistings

capabilities, ensuring RapidXtra remains the solution of choice to service our customers.

With vast experience in retail billing programme deployment and delivery, as well as a deep understanding of the water sector and its regulatory requirements, RapidXtra is perfectly placed to be the first choice option for any new market entrants, and we continue to monitor the market closely and engage with new entrants, offering expert support and services to meet their market entry strategies.

Innovative end-to-end customer-centric collections servicesThe challenges of supporting vulnerable customers, ascertaining customers’ ability to pay and ensuring fair outcomes for all are key concerns, as well as to the sector and to Echo. Strong data, tailored strategies and positive customer engagement are all key debt recovery strategies. We are in a strong position here with the business able to provide both debt management expertise and customer service excellence.

The last year has seen both innovation and growth, as we continued to build on the strength of our end-to-end debt recovery service. As well as being successfully authorised by the Financial Conduct Authority, Echo’s office-based debt operations were successfully integrated into our Bristol site, aligning customer experience and debt activities closer than ever before.

Recognising that debt is just another part of the customer journey, Echo’s offering leverages the importance of customer experience, with a customer service mind-set throughout the debt recovery process, championing the importance of early intervention and a collaborative approach between in-house teams and external providers. This provides a strong platform for growth, with a continued focus on customer service excellence.

We continue to expand our field-based propositions, with activities widening beyond traditional debt collection work to include revenue protection activities and customer affordability, as well as vulnerability visits, focused around building long-term sustainable relationships with customers.

As our solution continues to strengthen, it places us in a strong position in our core sector, UK Utilities. Echo secured a number of new clients during the year, including a strategically important contract with a ‘big six’ energy provider to provide field-based meter tampering and energy theft investigation services. Also, our first energy client award in Ireland, providing field-based debt collection services, provides a solid foundation to support our strategic objective of growth in both Northern Ireland and the Republic of Ireland.

Customer contact service excellenceThe English water sector has seen a year of challenge and evolution as water companies balanced service performance in the household sector with the operational demands of readiness for the opening of the Non-Household retail market.

Echo continued to assist South Staffs Water to embed and promote their customer digital service offerings, as well as supporting and developing a number of innovative offerings such as the ‘Assure’ social tariff. In Northern Ireland, we successfully implemented the last of three key contract project milestones for Northern Ireland Water, delivering new technologies and functionality. Echo also secured a new metering and billing contract with Northern Ireland Water to undertake field and office based data reconciliation activities.

Echo Bristol continues to provide multi-channel customer contact services to public and private sector organisations; offering end-to-

Annual Report 2017

27

end capabilities, from entry level bureau through to comprehensive, analytics-enabled multi-channel programmes. Despite the highly competitive landscape, we won a number of new clients during the year, as well as maintaining and expanding relationships with existing clients. The Bristol operation focuses on service excellence, using insight, experience and expertise to add further value; evolving and improving customer experience and exceeding clients’ expectations.

Looking to the futureThis next year promises, once again, to be rich in opportunities across Echo’s core divisions. We remain focused on sustainable growth within core markets, as well as across our service and software portfolio.

As UK water follows energy into deregulation, with the possibility

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

RapidXtra Retail supports water market opening RapidXtra is already used by over one third of water companies across England and Wales. In the past year, Echo has supported the water sector to ensure that each of its Rapidxtra clients’ billing systems was capable of communicating with the market and was compliant with the new Non-Household market regulations.

Our RapidXtra team successfully navigated evolving market requirements whilst delivering the Retail Ready Roadmap; supporting both wholesale and retail clients to operate and compete effectively in the new environment.

Echo worked closely with retailers Anglian Water Business, South Staffs Water Business, Yorkshire Water, Source for Business (the trading brand for Pennon Water Services), WaterPLus and Water2Business, as well as wholesalers Pelican Business Services, South Staffs Water and South West Water; assisting them successfully through to full market go-live in April 2017.

The hard work does not stop there, with the RapidXtra team continuing to keep a close eye on the evolving market in order to react quickly to any regulatory changes, enabling clients to remain compliant and competitive. Planned upgrade releases of RapidXtra Retail will continue to add yet further enhancements to clients’ customer service and billing capabilities.

of household market opening on the horizon, the opportunity for companies to offer a true multi-utility customer proposition has arrived. New partnerships within the water sector, cross-utility developments and the growing demand for white labelled solutions all present opportunities for Echo. We will continue to develop products and services, positioning ourselves as the true customer engagement specialist for the new sector; delivering both customer engagement improvements and cost efficiencies.

Continued investment in, and the development of, RapidXtra remains a key focus; ensuring our solution continues to lead the way in the market. Echo will continue to grow its debt collection and revenue management proposition, widening field-based services and targeting deeper market penetration across

key industry sectors. For contact centre services, the focus remains on developing and delivering multi-channel value driven propositions.

Echo’s new Leadership Behaviour Framework will be rolled out into the employee performance management lifecycle, placing equal emphasis on how we do things as well as what we do. By staying true to our values, we will provide customer-led solutions for clients. Through the expertise, knowledge and understanding of our people, we will collaborate to deliver an enriched customer experience; protecting clients’ brands as if they were our own. Echo will pursue opportunities to add new clients, expand services provided to existing clients, as well as identify and acquire businesses aligned with Echo’s strategy, ultimately adding value to its client base.

28

Corporate SocialResponsibility

Record-breaking fundraising for WaterAid at annual ball

No RIDDOR accidents across the Group

New PEBBLE biodiversity scheme launched

Annual Report 2017

29

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

30

Annual Report 2017

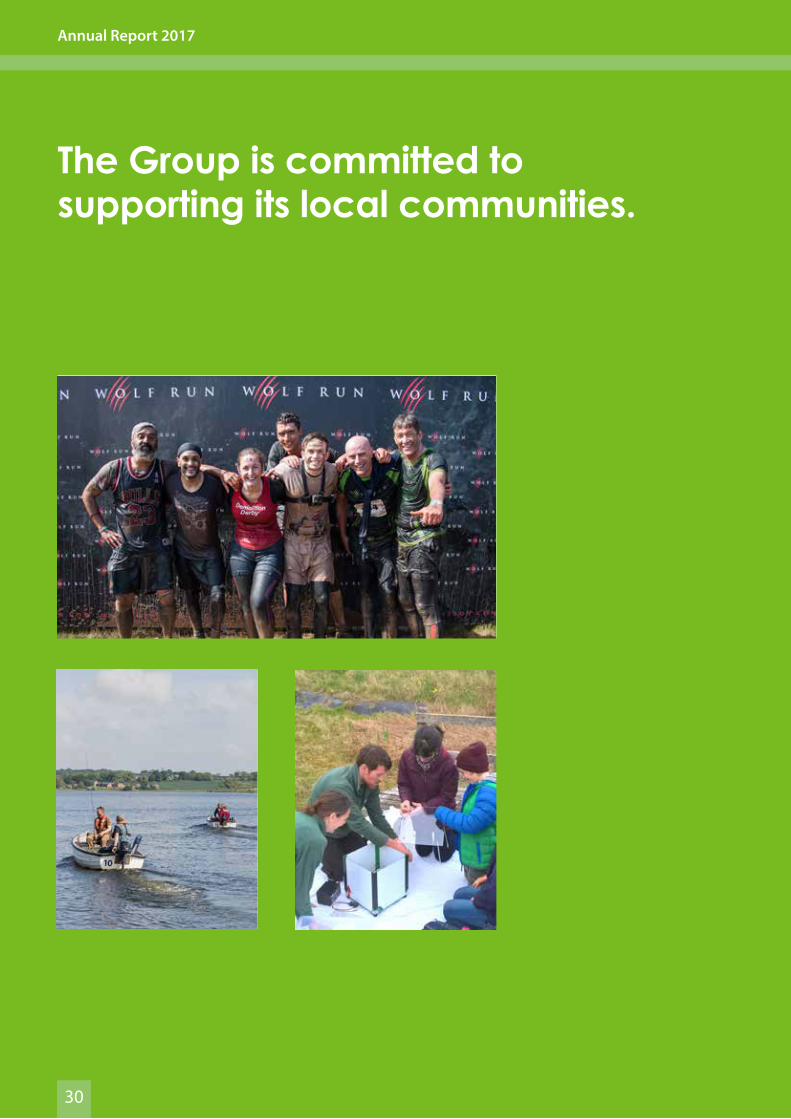

The Group is committed to supporting its local communities.

31

OverviewThe Group has had a particularly successful year in managing the Health and Safety of its employees, and continuing to focus on the environment and prevention of pollution. The Group is committed to supporting it’s local communities and supporting fundraising events. Customers are also at the centre of the Group’s activities. CSR has and remains a priority for the Group.

EmployeesThe health, safety and wellbeing of our employees is central to the growth and success of South Staffordshire Plc. We ensure it remains a safe and enjoyable Group to work for, by providing a positive and inclusive working environment.

- Health and SafetyGood progress has been made to steer the Group to further develop the Health and Safety culture, and each business met or improved their targets for reduction in accidents. The headline figure being, no RIDDOR accidents, compared to seven in the previous year.

The Health and Safety Strategy Forum led by the Group Chief Executive and supported by the Head of Group Health and Safety, continues to oversee activities in this important area of the business.

The success is due to each business closely monitoring their own performance, against their own

Business Safety Plan, which contains business specific targets for, different measures of accidents, accident rates, hazards identified, Director and Line Manager Audits, as well as local initiatives aimed at addressing identified areas of risk.

New Business Safety Plans have been developed for 2017/18 and focus on accountability. These plans are divided into departmental plans and managers are responsible for the delivery of specific parts of the overall plan.

The accident/incident database has been further developed to include Hazard Reporting, and accident investigation training has been rolled out to approximately 300 managers and supervisors, these are just a couple of the initiatives which were undertaken during the year.

Effective leadership, commitment and employee engagement enabled us to achieve our Health and Safety milestones, which were met or improved on for the third year in succession. In order to maintain the momentum, annual milestones have been set for 2017/18, with a minimum of 10% improvement on 2016/17’s performance.

The majority of our businesses have external accreditation for their health, safety and environmental management systems. Many Group companies also hold ISO 9001 quality management and OHSAS 18001 Occupational Health and

Safety management accreditations, and are part of the Safe Contractor schemes.

Employees have access to specialist occupational health advisors, who can provide proactive health surveillance and advice in order to keep our employees fit and healthy. Employee assistance programmes are also available across the Group; our employees can get free advice and counselling on any issues, whether its work related or personal.

- Training, development and engagementSouth Staffs Water is committed to providing a safe, positive and rewarding working environment. The annual employee survey plays an important role in helping understand the feelings and motivations of the employees. The results provide direction for change and improvement in areas such as, training and development and the working environment.The recruitment of seven apprentices, each with a mentor, during the year, represents a commitment to investing in future talent.

Echo launched an Employee Voice Forum to drive communication and engagement, in addition to driving actions to make Echo a great place to work, the forum also focuses on local and national charity days/events. So far they have supported, Depression Awareness Week, No Smoking Day, Learning at Work Week and National

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

32

Walking Month. A wellness policy has also been launched, to support employees in promoting a happier healthier wellbeing.

SSI Services have periodic reviews of individuals, to identify and ensure that appropriate qualifications and accreditations are in place to carry out their duties, in accordance with legislation and customer requirements. Approximately 120 managers and supervisors have completed the Training for Success programme, which covers all aspects of leadership and management. Existing apprentice programmes will be strengthened by the development of an Engineering Apprenticeship Programme in late 2017.

- Equality and fair treatmentWe are committed to providing a positive working environment, free from discrimination and/or unfair treatment. Every effort is made to provide equal opportunities for employment, training and promotion, having regard to employees’ particular aptitudes and abilities, regardless of their gender, race, age or disability. If an employee were to become disabled, we would endeavour to keep them in the workforce, by making reasonable adjustments to their role or working environment, or looking for redeployment opportunities within the Group.

Human rights are not considered to be a material risk for the business, due to existing regulatory requirements in the UK and the nature of our supply chain.

EnvironmentAs a Group, we have several environmental projects on going. South Staffs Water continues management of the previously established wildflower meadow areas at Sedgley Beacon, and the translocated grassland area at Fleam Dyke. It launched the PEBBLE fund, awarding grants totalling £26,500

to ten projects aiming to improve biodiversity across the South Staffs and Cambridge regions. SSI Services is ISO 14001 accredited, which covers the environmental aspects and impacts that relevant to the activities it carries out. The division is working towards reducing its carbon footprint and that of its customers, by the regionalisation of the business and the minimisation of fuel usage.

CommunitiesThe key event in our fundraising calendar was WaterAid’s Sparkles & Suits Ball. More than 200 guests attended from across the Group, the wider supply chain and other stakeholders. A total of nearly £44,000 was raised as a result of sponsorship, monetary and gift donations and fundraising on the night, significantly beating last year’s total. Support for the charity continued during their ‘GoBlue4Water’ activity on World Water Day in March 2017.

Each of our businesses have provided support to their local communities and organised or attended fundraising events:

• Group Services provided 13 days of employee time to support a local hospice (Acorns)

• South Staffs Water Employee Volunteer Scheme provides staff with up to three days’ paid time per year to participate in work that will make a positive difference in their communities. They also encourage communities to access their sites that are open to the public, to help increase knowledge of the work the company does. A highlight of the year was opening the Maplebrook pumping station in Burntwood as part of the national initiative, Heritage Open Days. Although no longer functioning, the Grade II listed building is one of the few remaining pumping stations in England to retain original triple expansion steam engines in situ.

Annual Report 2017

Male 18

Female 5

Directors and Executives

Senior Management

Male 32

Female 8

Other Employees

Male 2108

Female 646

Analysis of Group employees by gender

33

• Echo supported the Macmillan Cancer cake sale, Children in Need and Save the Children, to name a few. They also participated in events for local charities, their Belfast site continues to support local animal shelters, and in Walsall, food is regularly donated from our contact centre to a local homeless shelter. Finally, Echo launched an employee volunteering scheme, piloting the scheme in Bristol, giving employees a paid day off to support local volunteering programmes.

• SSI Services is a nationwide division, and so it encourages employees to support their local charities, specifically in areas relating to schools and learning. SSI Services also supports the Robert Harley award, which is made once a year to employees who have shown commitment to delivering great service and who have gone the extra mile for the success of the division. The winner is awarded with £500 to donate to a charity of their choice.

CustomersThe Group is concentrating on customer satisfaction, service quality and building long-term relationships with customers, all of which are imperative to the future success of the Group.

The Water Customer panel is made up of an impartial board of customers. Stakeholders and experts who act on behalf of customers to keep check on how South Staffs Water operates. They are responsible for looking at communication, ensuring the commitments outlined in the business plan are met and challenging performance to be sustainable, affordable and cost-effective.

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

Sparkles & Suits ball is a record-breaking successSouth Staffs Water’s key fundraising event in support of WaterAid, the Sparkles & Suits Ball, enjoyed fantastic support with over 200 guests from businesses across the Group and the wider supply chain.

As a result of sponsorship, monetary and gift donations and fundraising on the night, a total of nearly £44,000 was raised, significantly beating last year’s total of £25,000.

Support for the charity has continued, with businesses from across the Group getting involved in the annual Fly Fishing competition at Blithfield, as well

as WaterAid’s ‘GoBlue4Water’ activity, marking World Water Day in March 2017.

Echo took part in the Institute of Customer Service’s (ICS) National Customer Service Week in October 2016; the ICS spent an engagement day in the Bristol Operation. This was to embed the ICS principles and values within the operation with this focus on customer service by Echo being rewarded with a number of awards.

34

Financial ReviewChallenging budgets for turnover, profitability, cash flow and net debt outperformed

Increase in capital investment by £7m

Annual Report 2017

Significant liquidity headroom maintained

35

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

Annual Report 2017

The Group again exceeded its challenging financial targets, indicating another strong and disciplined financial performance.

36

GROUP TURNOVER

£205m£225m

£239m £235m£248m

2013 2014 2015 2016 2017

37

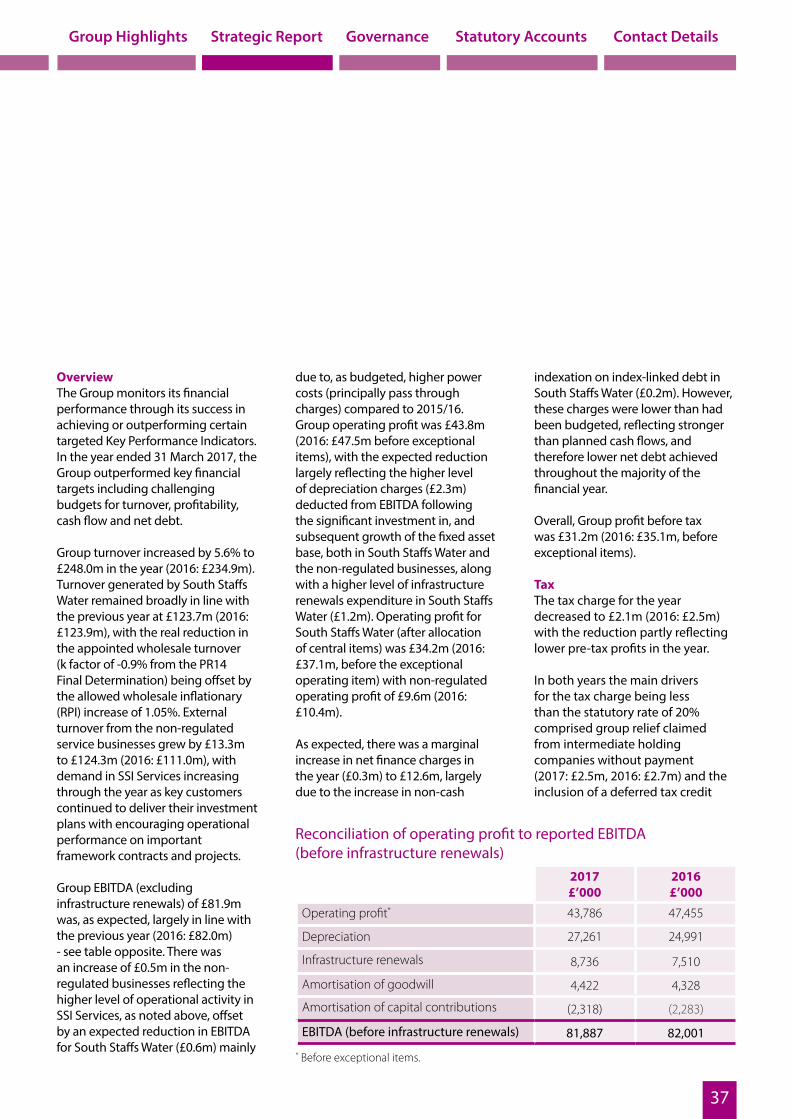

OverviewThe Group monitors its financial performance through its success in achieving or outperforming certain targeted Key Performance Indicators. In the year ended 31 March 2017, the Group outperformed key financial targets including challenging budgets for turnover, profitability, cash flow and net debt.

Group turnover increased by 5.6% to £248.0m in the year (2016: £234.9m). Turnover generated by South Staffs Water remained broadly in line with the previous year at £123.7m (2016: £123.9m), with the real reduction in the appointed wholesale turnover (k factor of -0.9% from the PR14 Final Determination) being offset by the allowed wholesale inflationary (RPI) increase of 1.05%. External turnover from the non-regulated service businesses grew by £13.3m to £124.3m (2016: £111.0m), with demand in SSI Services increasing through the year as key customers continued to deliver their investment plans with encouraging operational performance on important framework contracts and projects.

Group EBITDA (excluding infrastructure renewals) of £81.9m was, as expected, largely in line with the previous year (2016: £82.0m) - see table opposite. There was an increase of £0.5m in the non-regulated businesses reflecting the higher level of operational activity in SSI Services, as noted above, offset by an expected reduction in EBITDA for South Staffs Water (£0.6m) mainly

due to, as budgeted, higher power costs (principally pass through charges) compared to 2015/16. Group operating profit was £43.8m (2016: £47.5m before exceptional items), with the expected reduction largely reflecting the higher level of depreciation charges (£2.3m) deducted from EBITDA following the significant investment in, and subsequent growth of the fixed asset base, both in South Staffs Water and the non-regulated businesses, along with a higher level of infrastructure renewals expenditure in South Staffs Water (£1.2m). Operating profit for South Staffs Water (after allocation of central items) was £34.2m (2016: £37.1m, before the exceptional operating item) with non-regulated operating profit of £9.6m (2016: £10.4m).

As expected, there was a marginal increase in net finance charges in the year (£0.3m) to £12.6m, largely due to the increase in non-cash

indexation on index-linked debt in South Staffs Water (£0.2m). However, these charges were lower than had been budgeted, reflecting stronger than planned cash flows, and therefore lower net debt achieved throughout the majority of the financial year.

Overall, Group profit before tax was £31.2m (2016: £35.1m, before exceptional items).

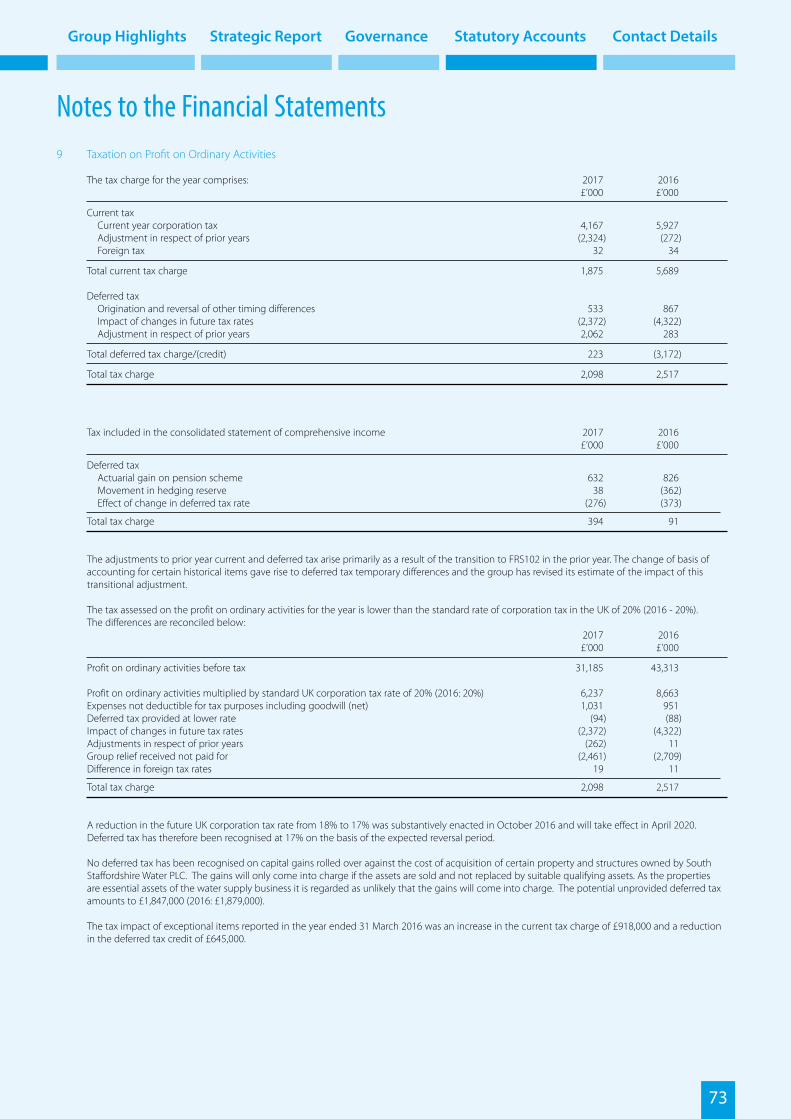

TaxThe tax charge for the year decreased to £2.1m (2016: £2.5m) with the reduction partly reflecting lower pre-tax profits in the year.

In both years the main drivers for the tax charge being less than the statutory rate of 20% comprised group relief claimed from intermediate holding companies without payment (2017: £2.5m, 2016: £2.7m) and the inclusion of a deferred tax credit

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

2017£’000

2016£’000

Operating profit* 43,786 47,455

Depreciation 27,261 24,991

Infrastructure renewals 8,736 7,510

Amortisation of goodwill 4,422 4,328

Amortisation of capital contributions (2,318) (2,283)

EBITDA (before infrastructure renewals) 81,887 82,001

Reconciliation of operating profit to reported EBITDA(before infrastructure renewals)

* Before exceptional items.

38

(2017: £2.4m, 2016: £4.3m) arising from the revaluation of deferred tax liabilities for future tax rate changes. A reduction in the future UK corporation tax rate from 18% to 17% was substantively enacted in October 2016 and will take effect in April 2020, and therefore deferred tax balances were reduced accordingly during the year ended 31 March 2017. Reductions in the rate of corporation tax from 20% to 18% were enacted in the year ended 31 March 2016 and in that year deferred tax balances were reduced accordingly.

The Group’s approach to tax is explained on page 42.

Prior Year Exceptional ItemsIncluded within the total Group operating profit for the previous year was a non-cash exceptional operating cost credit of £3.6m relating to the reduction in the 2015/16 year in the book value of liabilities relating to the South Staffordshire Section of the Water Companies Pension Scheme. This non-recurring and significant reduction in the liabilities arose as a result of the cessation of future accrual of the defined benefits within the scheme during the 2015/16 year.

Also, during the previous year, South Staffs Water sold the contractual rights to future rental income relating to a number of its sites. This sale generated proceeds, as well as a profit of £4.6m which has also been disclosed in the comparative profit and loss account as exceptional as it is not of an operating nature and due to the non-recurring nature of the sale and the significance of the proceeds and the profit generated.

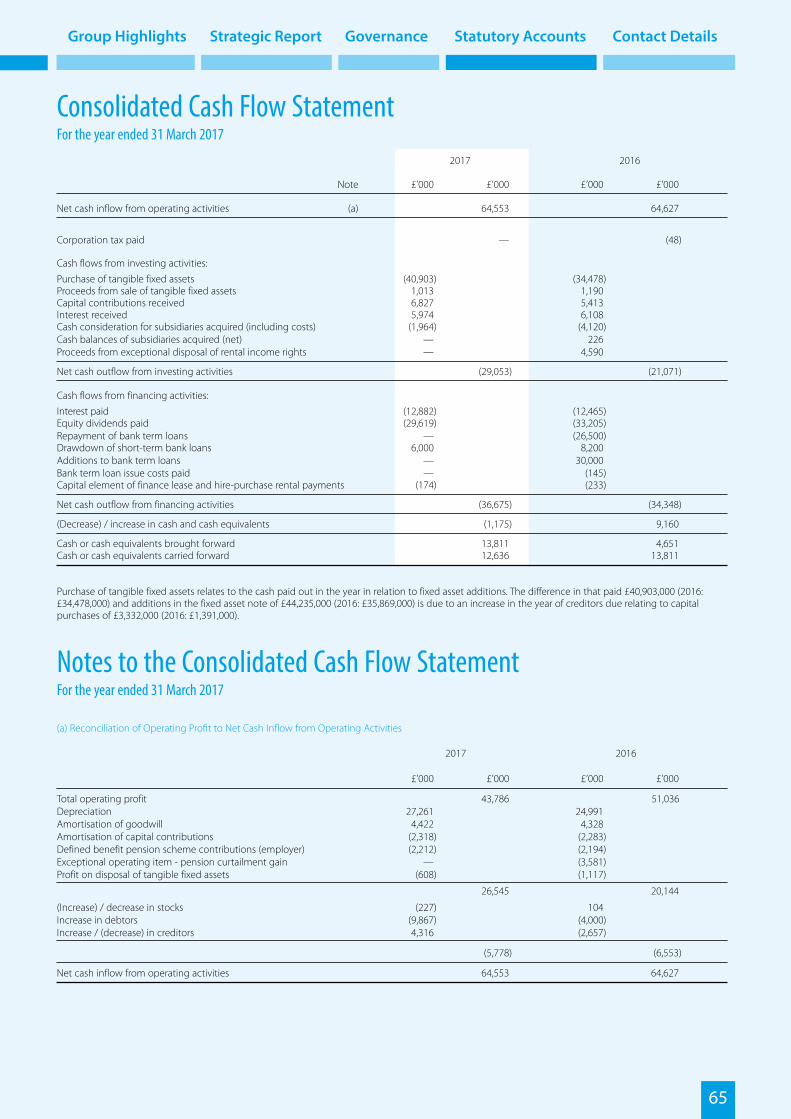

Cash flow and DividendsThe Group continues to place significant emphasis on its cash flow. Group cash flow from operating activities was £64.6m

(2016: £64.6m), including lower year-on-year investment required in working capital, which was also lower than the budget set at the start of the year, offset by the expected year-on-year increase in infrastructure renewals expenditure. Capital investment (excluding infrastructure renewals, net of contributions, disposals and capital creditor movements) increased to £33.1m (2016: 27.9m) due mainly to increased capital investment by South Staffs Water in the second year of the new AMP6 investment period, along with increased investment in the non-regulated businesses to support the sales growth in the year and the expected further growth in this new financial year. Overall, free cash flow (cash flow from operations less interest, tax and capital expenditure) of £24.6m (2016: £30.3m), was ahead of our target. Total dividends paid and proposed in the year were £29.6m (2016: £33.2m) with the reduction from 2015/16 largely reflecting the prior year distribution of the exceptional proceeds on disposal of rental income rights received during that year (£4.6m).

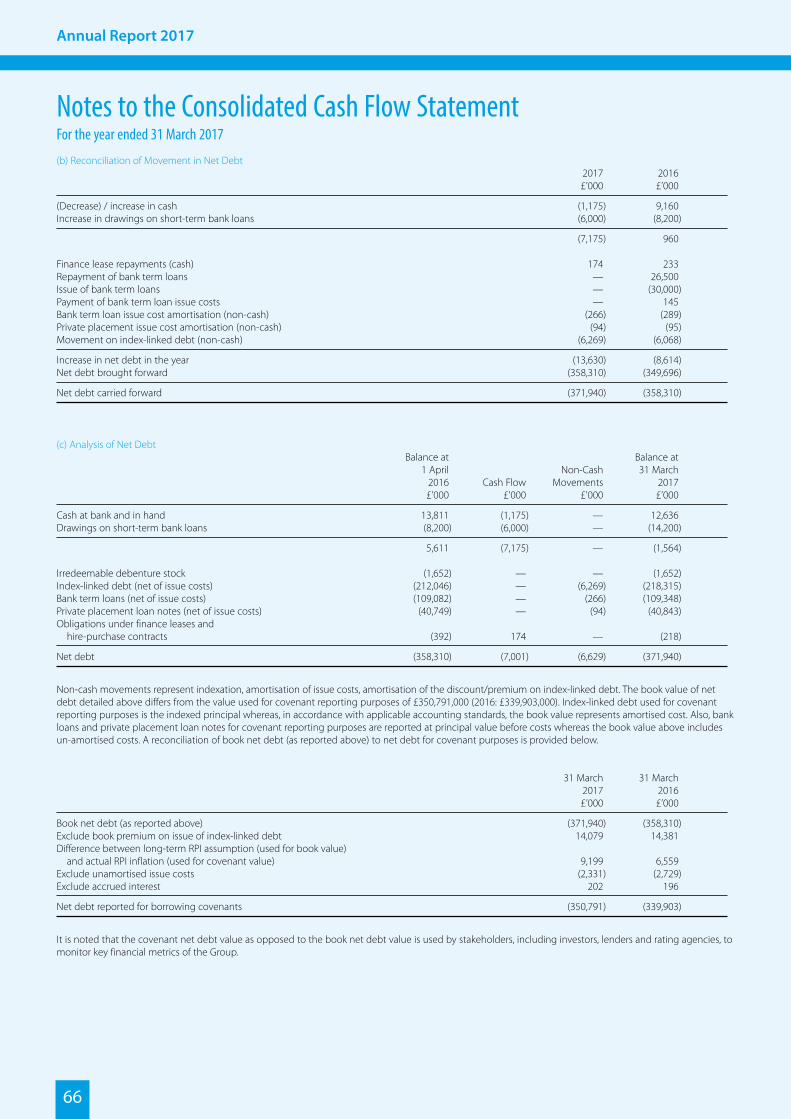

Financing, Net Debt and LiquidityGroup net debt reported for covenant purposes at 31 March 2017 amounted to £350.8m with the increase from 31 March 2016 (£339.9m) being largely due to the increase in the value of index-linked debt in South Staffs Water due to indexation for the year of £3.9m and higher levels of net capital investment of £7.0m (net of contributions and before infrastructure renewals). This net debt value is fully reconcilled to the value used for statutory accounting reporting purposes in the notes to the consolidated cash flow statement on page 66 along with a detailed analysis of the Group’s net debt.

In South Staffs Water, net debt for covenant reporting purposes was £219.7m (2016: £213.4m) being 63.2% (2016: 64.3%) of its Regulated

“Group invests over £44m in its capital base.”

Turnover

increasedby 5.6% to £248m

Annual Report 2017

39

Asset Value (RAV) of £347.6m (2016: £332.0m), representing the PR14 Final Determination RAV uplifted for actual inflation. This ratio reflects the impact of better than expected free cash generation in the year and higher than anticipated inflation (RPI) at the end of the year, which impacts the value of RAV. The expectation for this ratio is in the region of 66%.

The Group and South Staffs Water have maintained, and continue to forecast to maintain, significant headroom in respect of all borrowing covenants which include both interest cover and leverage covenants. Standard and Poor’s continues to rate South Staffs Water as BBB+, well within investment grade.

At 31 March 2017, the Group had available £25.0m of undrawn bank facilities (2016: £31.0m), in addition to its cash balances of £12.6m (2016: £13.8m), providing significant liquidity headroom of £37.6m (2016: £44.8m).

On 18 July 2017, South Staffordshire Plc refinanced a bank facility of £20m that was due to mature in December 2017 with a new five-year £20m bank facility.

Risk ManagementThe Directors acknowledge that risks exist in all businesses with the Group’s approach to risk reflecting its status as a Group comprising a regulated business, with a long-term water supply license, and also non-regulated activities operating in regulated markets.

As part of its normal activities, the Board of Directors, assisted by the Senior Management team, regularly carry out robust assessments of the principal risks facing the Group, including those risks that have the potential to threaten individual business models, future operational

or financial performance, solvency and liquidity. There is regular monitoring of the Group’s risk management and material internal control systems to review their continuing relevance to the Group’s businesses and their effectiveness, ensuring that appropriate risk management activities are in place or are planned to mitigate the risks identified. It is accepted that risks can emerge and change quickly, therefore risk identification and mitigation activities will need to be able to respond to this and that, at any given point in time, enhancements to mitigating actions may be required in response to changes.

Risks are assessed both on a gross basis (likelihood and consequence before mitigating controls) and a net basis (likelihood and consequence after mitigating controls) so that the Directors and the Senior Management team can properly assess the overall significance of the risk and the estimated effectiveness of mitigating actions, as well as if further actions are required.

The Directors accept that not all risks can be mitigated entirely, but aim to ensure that risk management activities reduce the overall estimated impact of risks, on a net basis, to a level that is considered to be acceptable and that do not impact on the long-term viability of the Group and its businesses. The Directors believe that the most significant risk areas currently faced by the Group along with the related mitigating actions are summarised below with no significant changes in the ratings assigned to each risk from the previous year.

Details of the Group’s principal financial risks are provided in note 28 to the accounts.

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

Non-regulated Service Businesses 22%

South Staffs Water 78%

Analysis of Group operating profit

40

Annual Report 2017

Hea

lth a

nd s

afet

y*

The risks to the health, safety and wellbeing of the Group’s employees, contractors and members of the public that may be impacted by the Group’s operations.

Continuing to improve Health and Safety in a practical and sensible manner is a top priority for the Group, and is regularly reported to both the Board and Executive Management.

A Group Health and Safety Executive Committee is in place to drive Health and Safety strategy and culture, encouraging training, targeted focus on identifying hazards, prompt reporting, best practice policy and improving behaviours.

On a day-to-day basis, Health and Safety is operated and managed within each of the Group’s businesses. Annual plans including targets are produced, which focus operational efforts on areas which have the greatest impact on or risk to Health and Safety performance in each business. Monthly Health and Safety statistics are published and discussed to further drive focus and performance.

Wat

er q

ualit

y#

The risk that South Staffs Water is unable to meet its legal and regulatory obligations for the supply of clean, safe drinking water or that water quality is not of an acceptable standard.

Each year South Staffs Water carries out thousands of water samples taken from treatment works, reservoirs and homes across its areas of supply to monitor quality and respond to any matters arising from the sample results. As part of our Drinking Water Safety Plan activities we undertake catchment monitoring. The results of water quality testing are regularly reported to both the Board and Executive Management.

South Staffs Water has sought to mitigate the risk of water quality failures at one of its key operational sites, Seedy Mill Treatment Works through investment in a multi-million pound project to install a new UV water treatment facility. Since April 2016, all water leaving Seedy Mill has been subject to this additional treatment process.

Investigations as to the most appropriate long-term solution have been carried out at our Hampton Loade water treatment facility during the year, with another UV treatment solution planned to commence in this new 2017/18 year. Alongside this is a continued commitment to invest in our borehole facilities across our estate.

Regu

lato

ry e

nviro

nmen

t an

d co

mpe

titio

n#

The risk for South Staffs Water of non-compliance with, or the inability to respond to, a regulatory environment which is complex and changing, and the risk of these changes having a detrimental impact on the success and financial position of the business and the Group.

The business has a dedicated regulation team that is focused on keeping abreast of regulatory changes, compliance with regulations, and advising the business of changes so that it can respond effectively. This team, along with members of the Board and Executive Management regularly attend focused water sector briefings and technical events to ensure that knowledge in this important area is up to date. Professional advice is taken on matters where it is considered that this will add value. Regulatory matters and changes are regularly reported to the Board and Executive Management.

Ass

et q

ualit

y an

d m

aint

enan

ce#

The risk of failure of key infrastructure and other assets or processes which may result in South Staffs Water’s inability to provide a continuous supply of clean, safe drinking water.

The business is committed to a major investment programme over the five year asset management period (AMP) to continue to maintain and enhance its asset and infrastructure base so that it is able to meet demand and ensure customers continue to receive a high quality, reliable water supply and very high standards of customer service.

Risks Description Mitigation

PRINCIPAL GROUP RISKS

41

Group Highlights Strategic Report Governance Statutory Accounts Contact Details

Avai

labi

lity

of a

dequ

ate

wat

er re

sour

ces#

The risk that, due to inadequate water resources, South Staffs Water is unable to meet its legal and regulatory obligations for the secure and resilient supply of water.

South Staffs Water is creating the next version of its Water Resources Management Plan for the period 2020 to 2045, and beyond. This considers the impact that housing and industrial development, climate change and the potential for drought may have on both the water supply and the local environment.

The business is actively involved in the design process for the new “Water Resources” price control to be introduced in April 2020, which introduces “upstream” market reform and abstraction reform. Data is being collected to determine the environmental impact of increasing abstraction at sources where licences are due to be renewed in 2018.

Long-term planning is underway to identify options for the future of Hampton Loade and Seedy Mill in the West Midlands. This includes a full range of demand management, resources and trading options. A similar review is underway in Cambridge to address growth and licence restriction.

South Staffs Water has invited customers to share opinions on how they think water resources should be managed in the future. These views will form part of future water resource plans. The business is actively engaging with WREA (Water Resources East Anglia) to identify regional water resource solutions. Exploration of more extreme drought impacts has commenced which may identify the need for wider and more innovative options to be developed.

Cust

omer

ser

vice

# The risk of failure to maintain industry leading customer service levels to ensure that our operations are delivering what customers require.

An action plan is in place to deliver continued improvements to customer service (measured primarily by SIM scores) in South Staffs Water. These scores are used as the measure of performance in this important area, with the target being to be in the top quartile of the sector for SIM performance.

Customer engagement is continuing with a new Customer Challenge Group (Customer Panel). This was launched in April 2016 providing scrutiny and challenge to South Staffs Water.

Secu

rity

and

ava

ilabi

lity

of

info

rmat

ion

and

syst

ems*

The risk that the security over the Group’s information and assets is breached, and the risk to the Group of the loss of key systems.

Risk mitigation initiatives include:• Segmentation of information system infrastructure.• Removing single points of failure from within systems, processes and

infrastructure.• Moving from a disaster recovery to a business continuity infrastructure.• Raising staff awareness of the risks and how to respond to them.

Controls in these important areas are being progressively improved, with a Group-wide initiative to develop information security policies, controls, practices, procedures and awareness. The Group IT operation, which is responsible for the security of the Group’s IT networks, is currently going through the process of becoming ISO 27001 certified, and is also seeking to become accredited against the Cyber Essentials technical controls. The Group IT operation has been strengthened by the appointment of a Group Information Security Controller to further drive risk identification, management and mitigation in information security. Monitoring practices are also being enhanced to identify unusual behaviour or activity that could indicate a security risk.

Risks Description Mitigation

* Affects all of the Group’s operations.# Affects South Staffs Water’s operations.

42

Annual Report 2017

Group Approach to TaxThe following statement complies with the requirements of Finance Act 2016 for large groups to make their tax strategies available to the public.

The South Staffordshire Plc Group (‘the Group’) takes seriously its legal and social responsibilities for meeting its tax obligations. The Group currently has no material operations outside the United Kingdom, and therefore the following has specific reference to UK taxation, although the same principles are applied in other jurisdictions where applicable.

The Group is committed to complying with tax laws in a responsible manner, balancing its obligations to the Government and the public with its duty to manage its affairs efficiently in order to deliver cost-effective services to its customers while generating an economic return to its investors. The Group makes timely and accurate tax returns that reflect its fiscal obligations to the Government.

In particular, the Group:• Will not engage in aggressive

tax planning that is not linked with commercial and economic activity;

• Will not engage in artificial tax arrangements;

• Will seek to maintain a transparent and collaborative relationship with HM Revenue & Customs, principally through the Group’s Customer Relationship Manager;

• Will seek independent professional tax advice on material matters where the application of tax law is complex or uncertain.