ANNUAL REPORT 2014 - Home – Aamal/media/Files/A/Aamal-V2/reports-and-presentations... · Aamal...

45

ANNUAL REPORT 2014

Transcript of ANNUAL REPORT 2014 - Home – Aamal/media/Files/A/Aamal-V2/reports-and-presentations... · Aamal...

ANNUALREPORT2014

٢٠١٤

His Highness

Sheikh Tamim Bin Hamad Bin Khalifa Al-Thani

Emir of the State of Qatar

CONTENT

Company Profile

Financial Highlights

Investment Rationale

Chairman’s Report

Vice Chairman’s Report

Managing Director’s Report

Corporate Governance

Board of Directors

Executive Management and General Managers

Organisational Chart

Functional Chart

Corporate Social Responsibility

Operations Review

Industrial Manufacturing Division

Trading and Distribution Division

Property Division

Managed Services Division

Financial Statements

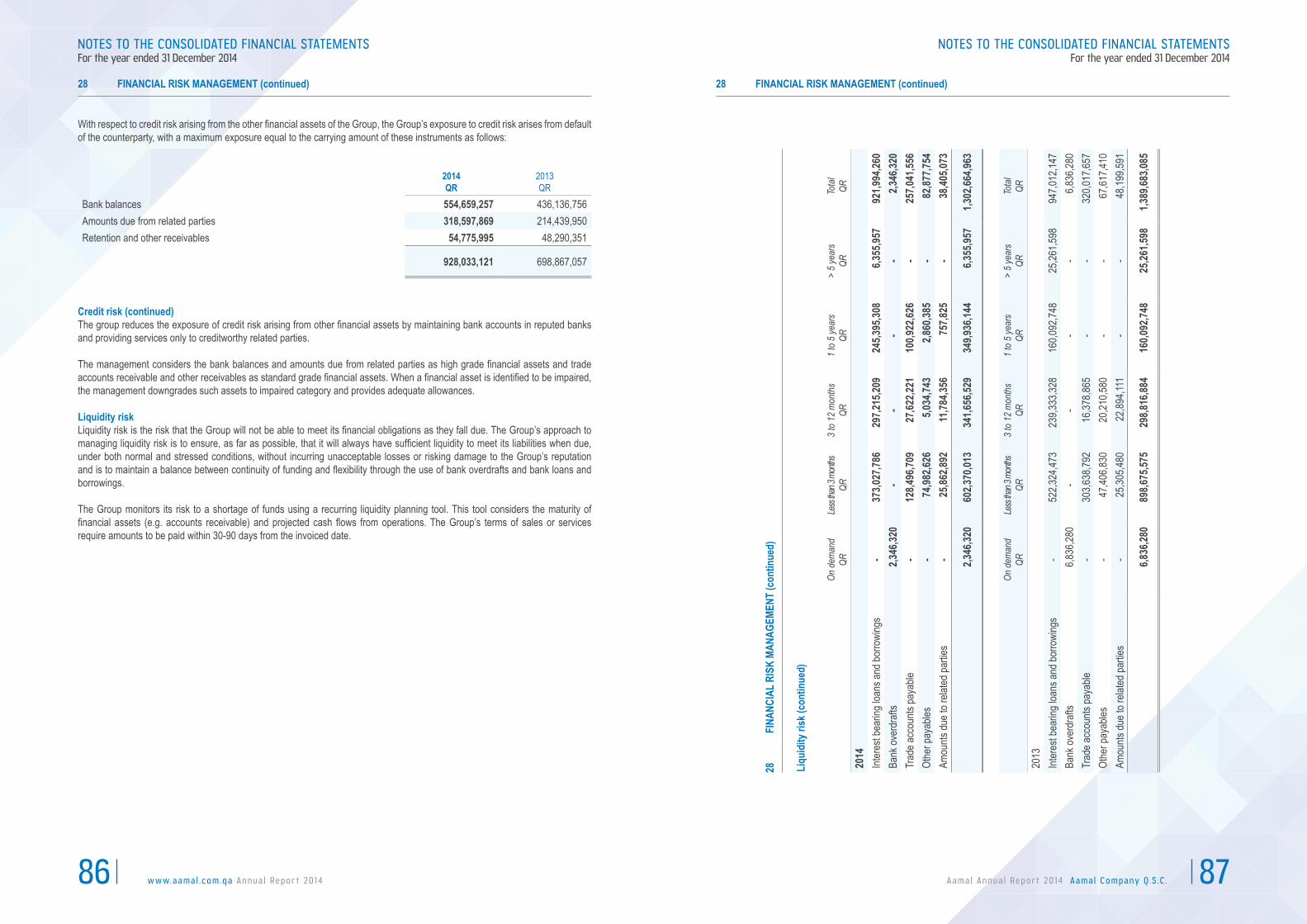

060810121416182022242526283034404246

A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 9

Company Snapshot

x Incorporated in 2001 in Qatar and listed on the Qatar Exchange in 2007

x Geographical focus on Qatar at present with intentions to expand further in the Gulf region

x Operations across 23 business units with market leading positions in key sectors including: industrial manufacturing, property, trading in pharmaceuticals and medical equipment and managed services

x Strategy focused on three pillars for sustained, profitable growth: i) Increasing focus on industrial manufacturing and related high growth sectors ii) Continued growth, diversification and innovation across other existing businesses to enhance market position and optimise performance iii) Continued application of clear and disciplined operational and financial principles underlying our strategic growth initiatives

x Uniquely positioned to benefit from increased private and public sector demand, particularly for infrastructure development, as Qatar is transformed into an advanced and self-sustaining economy. The award of the 2022 FIFA World Cup to Qatar and the National Vision 2030 is anticipated to accelerate this capital investment as infrastructure projects are commissioned and new projects come on stream

x Current market capitalisation of QAR 11bn* (US$ 3bn), making Aamal Company one of the largest diversified companies listed on the Qatar Exchange

x Al Faisal Holding Company is the major shareholder

*As on 3 March 2015

COMPANY PROFILE“Generating revenues of QAR 2,139m (US$ 588m) in 2014, Aamal Company is one of the largest, most

diversified and fastest-growing companies in Qatar offering investors a high quality and balanced

exposure to the remarkable Qatar growth story.”

A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 11

FINANCIAL HIGHLIGHTS

QARm FY 2014 FY 2013 Change%

Revenue 2,139.1 2,122.6 0.8%Gross Profit 506.0 420.5 20.3%Gross Profit Margin % 23.7% 19.8% 390 basis pointsNet Profit Before Value Gains on Investment Properties 348.5 267.2 30.4%Net Underlying Profit Margin2 Before Fair Value Gain % 15.4% 11.7% 370 basis pointsFair Value Gains on Investment Properties 251.7 245.1 2.7%Net Profit 600.2 512.3 17.2%Reported EPS 0.96 0.85 13.9%Adjusted EPS3 0.54 0.44 24.3%

1 There may be slight calculation discrepancies due to rounding2 Excluding share of profit from equity accounted for investments in associates and joint ventures3 EPS adjusted to show underlying profitability (i.e. excluding fair value gains on investment properties)

2014: Revenue and Net Profit breakdown by division (QARm)

Division

Revenue1 Net Profit Before Fair Value Gains on

Investment Properties2

Industrial Manufacturing 1,134.2 51.7Trading and Distribution 728.8 114.9Property 288.8 223.3Managed Services 64.2 8.3Total 2,215.9 398.2

1 Revenue shown before deduction of inter divisional revenue2 Net Profit shown before deduction of Head Office costs

Revenue* by division Net Profit* by division

Industrial Manufacturing (51%)

Trading and Distribution (33%)

Property (13%)

Managed Services (3%)

Industrial Manufacturing (13%)

Trading and Distribution (29%)

Property (56%)

Managed Services (2%)

*Before deduction of inter divisional revenue *Before fair value gains on investment properties and deduction of Head Office Costs

33%

13%3%

51% 29% 56%

13%2%

A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C 13

INVESTMENT RATIONALE

1) A powerful, cohesive growth platform

x One of the fastest growing diversified companies, offering high quality exposure to the Qatar growth story x Diversified for balanced exposure across the Qatari economy x Strong market positions in key sectors x Superior combination of high quality asset base, strong operating profitability and earnings visibility (delivering a compound

annual growth rate in net profit excluding fair value gains on investment properties in excess of 13% from 2006-2014, and generating revenues of QAR 2,139m (US$ 588m) in 2014.

2) Balance sheet strength – strong backing of major shareholders

x Strong asset backing x Readily available access to debt capital markets, which in addition to strong cash flow generation, provides strong liquidity

for future growth x Low gearing x Al Faisal Holding Company and Sheikh Faisal Al Thani are the major shareholders

3) Experienced, proven senior management team

x Strength in strategic asset allocation, corporate governance and risk control x Proven track record of historical profit growth and value creation driven by clear focus on returns on capital and capital

discipline x Highly effective corporate decision-making with short lines of communication with operational management

4) Strength in depth

x Development of shared services policy, allowing divisional management to focus on core business x Each subsidiary managed as an individual entity, optimising management’s operational focus and transparency x Talented and motivated managers with significant experience and excellent customer relationships in their respective areas x Clear segregation between management and ownership, reinforcing best practice corporate governance guidelines

20.00

19.00

18.00

17.00

16.00

15.00

Esteemed Shareholders

On behalf of the Board of Directors, I am very pleased to report excellent results for 2014. We have managed to grow our total net profit by over 17% to exceed QAR 600 million for the first time, with

earnings per share rising by almost 14%. Excluding the net fair value gains on investment properties which were largely flat at QAR 251.7 million, net profit was up by 30%. Today’s results extend Aamal’s proud and

long-established track record of profit growth and value creation underpinned by a clear focus on efficient capital allocations and returns.

Summary of financial results - breakdown by division:(nb. there may be slight differences due to rounding)

QAR m 2014 2013 Change %

Industrial Manufacturing 1,134.2 1,261.2 (10.1)%Trading and Distribution 728.8 585.8 24.4%Property 288.8 261.6 10.4%Managed Services 64.2 86.3 (25.6)%less: inter-divisional revenue (76.8) (72.2)

TOTAL 2,139.1 2,122.7 0.8%

QAR m 2014 2013 Change %

Industrial Manufacturing 51.7 22.6 128.3%Trading and Distribution 114.9 86.5 32.8%Property (ex-fair value gains on investment properties) 223.3 200.8 11.2%Fair value gains on investment properties 251.7 245.1 2.7%Managed Services 8.3 5.2 60.1%less: Head Office costs (49.7) (47.9) 3.8%

TOTAL 600.2 512.3 17.2%

As well as a record year for financial performance, we achieved a number of significant operational milestones. First, we established Aamal Optical Supplies in partnership with Qatar Optics, one of the leading companies in this sector, which is involved in the import, manufacture and distribution of prescription lenses and contact lenses. It is also the intention to open a specialised optical medical center in the near future that will diversify operations and revenue channels further, and allow us to capitalise on opportunities in this fast-growing sector.

Another important milestone was the start of commercial production at Advanced Pipes Company following construction of its state of the art factory in Mesaieed. A total of QAR 200 million (US$ 55m) has been invested in establishing this new facility which specialises in the manufacture of concrete pipe products to supply infrastructure and pipeline projects both in Qatar and across the region.

As Qatar continues to prosper and diversify its industrial base under the wise leadership of H.H. the Emir of Qatar Sheikh, Tamim Bin Hamad Al Thani, Aamal remains very much at the vanguard of this growth. It is the ‘best in class’ in terms of the products and services it is able to offer, and continues to be the partner of choice for those blue chip companies wishing to enter Qatar, bringing market leading knowledge and skills with them.

Faisal Bin Qassim Al ThaniChairman

REVENUE

NET PROFIT

CHAIRMAN’S REPORT

Aamal has achieved exemplary financial and operational results for 2014, evidencing the Company’s ability to seize opportunities offered by Qatar’s growing and flourishing economy, as well as its ability to do so profitably by focusing on revenue growth alongside operational efficiency and cost control, and in line with the Company’s balanced strategy for risk assessment and management. Aamal’s key strengths lie in its clear vision and strategy that are closely aligned with Qatar’s national strategy for economic development. Aamal has succeeded in building a solid base with its industrial manufacturing division, whilst developing further the other sectors in which it operates. Looking at the Company’s performance alongside the performance of the overall Qatari economy, we believe that our strategy of diversifying revenue sources is in line with the country’s strategy for economic growth and plans for development; that is, aiming to diversify the economy away from over-dependence on the hydrocarbon sector towards transforming Qatar into a center for manufacturing and services which will help to underpin the country’s long term prosperity. Besides, Aamal seeks to build on opportunities resulting from the MSCI upgrade of Qatar from frontier market to emerging market status. This upgrade has undoubtedly raised the appeal of those companies listed on the Qatar Exchange to international investors, leading to an enhancement in investor confidence and an increase in liquidity. Accordingly, Aamal has applied to raise the level of permitted foreign ownership to 49%, aiming to attract private capital from non-Qatari nationals both abroad and from the increasing number resident within Qatar, who may wish to participate in a company that is able to offer directly, a high quality and balanced exposure to the remarkable Qatar growth story. Together, these factors give cause for continuing confidence in the Company’s future performance. I am sure that Aamal will continue to prosper whilst focusing on delivering the best results for all stakeholders first and foremost. Our leading positions in the sectors in which we operate as well as our strong financial position enable us to offer comprehensive and balanced growth opportunities within Qatar, one of the fastest growing economies in the world.

Mohammed Bin Faisal Al ThaniVice Chairman

VICE CHAIRMAN’S REPORT

MANAGING DIRECTOR’SREPORT

I am pleased to present another positive set of results as the Company continues to grow and develop in line with the expansion of the broader Qatari economy.

I would like to emphasize two key points that our strong 2014 performance clearly bears out. The first is the importance of diversifying the Company’s revenue streams and the impact this has on reducing risk and

achieving sustainable growth. The second is the quality of Aamal’s activities and investments.

Although Aamal is positioned as a leading industrial company, as it continues to build a solid industrial base across a range of businesses that benefit from Qatar’s significant infrastructure programme, it has also built a prominent market

positions in other key sectors that are meeting the demand for increasingly sophisticated products and services as Qatar’s economy continues to evolve at a rapid pace.

Investment in the industrial manufacturing sector is at the heart of Aamal’s long-term growth strategy.

The success of our core focus on this sector is evident from its growing contribution to the Company’s net profit, which continues to increase - in 2014, it made up 13% of overall net profit compared to 7% the previous year. More importantly, our long term approach to this sector is starting to deliver increasing profitability as production continues to increase in line with the anticipated acceleration in infrastructure project build, as evidenced by the tenfold year-on-year increase in the net profit margin for the Industrial Manufacturing division.

However, we continue to ensure that the growth that our industrial manufacturing activities deliver for the Company is balanced against the growth of Aamal’s other activities (whether by establishing new projects or through developing existing activities), as their positive cash flow underpins our expansion plans. Balanced and sustained diversification also enhances our overall strength, reducing our exposure to the impact of market conditions that might affect one particular sector more than others from time to time.

Across all of our businesses in each of our four core sectors, delivering the highest quality of products, services and investments is a fundamental principle on which we never compromise. This principle underpins the strength of our market positions, customer reputation and our track record in attracting the best global expertise and partners, and in creating jobs opportunities in new fields. Our investment commitment to maintaining our leadership in this respect is reflected in our sector operational performance throughout the year.

To highlight a number of examples, in 2014, production began at the Advanced Pipes and Casts factory, the largest factory in Qatar with an area of 85,000 square metres and a production capacity of 450,000 tonnes per year. It will produce a range of infrastructure and construction products including jacking pipes, reinforced concrete pipes, circular precast concrete manholes and precast concrete box culverts, which is considered a new product that will be manufactured in Qatar for the first time.

At our core Aamal ready mix operation, we completed a significant investment in new equipment and the complete overhaul of its batching and ice plants that will enable us to deliver further growth in production at the highest standards of quality and efficiency. And in our trading and distribution sector, we have established “Aamal Optical Supplies” in partnership with Qatar Optics, a leading company in the optical care field. The Company will be involved in the import, manufacture and distribution of prescription lenses and eyeglasses, the import and distribution of contact lenses, and other eye care products and services. There are also other projects under consideration that will be announced in due time.

Looking ahead, we continually appraise potential new investment opportunities and we expect a number of these to be announced over the course of the next 12 months as we continue to capitalise on opportunities for balanced and profitable growth.

Tarek M. El SayedManaging Director

A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C 21

Board committees

The Board of Directors has formed five committees: 1) Audit Committee; 2) Nomination Committee; 3) Corporate Governance Committee; 4) Compensation Committee; and 5) Executive Committee. The dedicated committees meet regularly to assess operational effectiveness and ensure that the Company is performing in line with the set objectives.

Segregation of responsibility

In accordance with the highest standards of good Corporate Governance, the Board has decided to segregate the executive management duties from the Board.

The executives operate from a well-defined rule authorisation matrix and have various quantitative and qualitative targets set for them.

The executive management acts upon authorities approved by the Board of Directors. The Company policies and procedures are reviewed and updated regularly.

Relations with shareholders

Aamal Company is committed to maintaining an active and open dialogue with its shareholders through a planned programme of investor relations activities centred on the financial reporting calendar. Our website has a dedicated Investor Relations section to provide further information for all investors or potential investors while our Investor Relations team provides a channel for any other queries to be answered.

Support systems

The Company uses the Oracle system as the primary Group IT System.

“Aamal’s Board and Management are committed to meeting the expectations of

stakeholders in practicing sound corporate governance. Aamal Company views

corporate governance as an important factor in delivering success.”

CORPORATE GOVERNANCE

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 422 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C 23

Mr. Bader A. Al FehaniBoard Member

Sheikh Faisal Bin Qassim Al ThaniChairman

Sheikh Mohamed Bin Faisal Al ThaniVice-Chairman

Sheikh Abdullah Al ThaniBoard Member

Mr. Tarek M. El SayedManaging Director

Sheikh Turki Bin Faisal Al ThaniBoard Member

BOARD OF DIRECTORS

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 424 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C 25

Sameer Abu HannunAdvanced Pipes and Casts Company

GENERAL MANAGERS

Mr. Tarek M. El SayedManaging Director

Mohamed RamahiChief Financial Officer

Maha Jadallah HarperChief Legal Advisor

Parveez AslamAamal Readymix

Sherif ShehataAamal Medical

Ayman MorrarAamal Travel and Tourism

Ahmed El SewedyEl Sewedy Cables Qatar, Doha Cables

Hesham KaoudGulf Rocks

Keith SmithAamal Cement Industries

Osama Al HajjAamal Real Estate

Amr GoherECCO Gulf

Jorg HarengerdCity Center - Doha

Homok ChunggInnovative Lighting QLEDs

Samy HannaEbn Sina Medical

Samy IbrahimAl Farazdaq Company

EXECUTIVE MANAGEMENT

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 426 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 27

Aamal Readymix

Advanced Pipesand Casts Company

Senyar IndustriesQatar Holding

Doha Cables

Elsewedy CablesQatar

Doha Transformers

Innovative Lighting

Ci-San Trading

Gulf Rocks

Aamal CementIndustries

INDUSTRIAL MANUFACTURING

TRADING AND DISTRIBUTION

Aamal Tradingand Distribution

Aamal Medical

Ebn SinaMedical

Ebn Sina Health CareSolutions

Foot Care Centre

Al Farazdaq Company

Aamal OpticalSupplies

PROPERTY

City Center Doha

Aamal Real Estate

MANAGED SERVICES

Aamal Travel and Tourism

Aamal Services

ECCO Gulf

Johnson ControlsQatar

Aamal Company Q.S.C.

ORGANISATIONAL CHART FUNCTIONAL CHART

Corporate GovernanceCommittee

Chairman

Managing Director

Board of Directors

CompensationCommittee

Executive Committee

Audit Committee

NominationCommittee

Chief OperatingOfficer

Chief BusinessDevelopment Officer

Business DevelopmentDepartment

Aamal BranchesGeneral Managers

Human CapitalDepartment

CorporateCommunications

ProcurementDepartment

Legal Department

Chief Financial Officer

Finance DepartmentHead Office, Branches

and Subsidiaries

Treasury Department

Subsidiaries Operations

Chief Legal Adviser

AdministrationDepartment

A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C 29

CORPORATE SOCIAL RESPONSIBILITY (CSR)

Aamal continued its partnership with The Qatar Football Association for the third consecutive year as part of its commitment to play a proactive and responsible role in promoting sport which is one of the key elements of Qatar’s National Vision 2030.

Key CSR activities by division:

INDUSTRIAL MANUFACTURING DIVISION

Doha Cables x Established a summer internship programme where aspiring engineers can attend full training programmes to help them

prepare for a career in electrical engineering x Continuing to expand the Doha Cables Academy by organising various workshops for a number of engineering organisations,

such as the Institute of Integrated Electrical Engineers, as well as a number of educational seminars for consultants and contractors in Qatar

x Doha Cables is an affiliate member of The Gulf Organization for Research and Development (GORD)

Aamal Readymix x Renewed its Green Building certification to re-emphasize its commitment for the study and achievement of reduced carbon

footprints in the readymix industry x In the process of finalizing the installation of new recycling plant at its industrial area factory. This will enable the branch to

recycle all the unused and scrap quantities of the Readymix concrete, thereby minimising waste x Aamal Readymix was honoured for its participation in a recent blood donation campaign

Aamal Cement Industries x Continued to focus on in-house recycling, and dust suppression to improve the environmental impacts on site x Joined the Green Building Council, adding support to the green building lobby in Qatar that is leading the drive for greater

environmental controls

TRADING AND DISTRIBUTION DIVISION

Ebn Sina Medical x Continued focus on education through the adoption of two programmes:

a) Support of pharmacy students at the University of Qatar and the College of the North Atlantic, through the provision of collaborative training work experience opportunities within the Ebn Sina pharmacy chain

b) Support of the scholarship programme for the Bachelor’s, Master’s and PhD Pharmacy students at Qatar University x Continuing to substitute environmentally harmful plastic bags with d2w oxo-biodegradable bags throughout its pharmacy

chain

Aamal Medical x Organised an AED Awareness and Training Programme in Shopping Centres and Residence Towers. AED (Automated

External Defibrillator) is a portable electronic device that automatically diagnoses the life-threatening cardiac arrhythmias of ventricular fibrillation and ventricular tachycardia in patients

Aamal Trading & Distribution x Annual hosting of the ‘Bridgestone Tyre Safety and Eco Station Campaign’ to promote road safety and environmental

awareness

PROPERTY DIVISION

City Center Doha x Continued to support various awareness campaigns in collaboration with the Government and other non-profit organisations

Aamal Real Estate x Organised blood donation event at Souq Al Harraj with coordination with Hamad Medical Cooperation

Aamal will continue to build upon its core values of responsibility and sustainability implementing strategies that address environmental issues, empower people and provide training and safety awareness programmes to all its employees.

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 430 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C 31

QAR m 2014 2013 Change %

Revenue 1,134.2 1,261.2 (10.1)%Net profit: fully consolidated activities 33.6 4.1 711.4%Net underlying profit margin % 3.0% 0.3% +270 bpsNet profit: share of equity accounted for investee net profits 18.1 18.5 (2.0)%Total net profit 51.7 22.6 128.3 %

For the year ended 31 December 2014, the Industrial Manufacturing Division generated 51% of the Company's revenues, and 13% of its net profit. Net profit grew by 128.3% to QAR 51.7 million, driven principally by a 270 basis point improvement in the net margin to 3.0%

The improvement was due mainly to an acceleration in infrastructure project build in Qatar, translating into an increase in demand for various products offered by this division.

An important milestone reached was the start of the commercial production at the Advanced Pipes and Casts Company in the last quarter of 2014; initial trading signs have been very positive with the winning of several key orders and we foresee positive performance for this unit during 2015.

Aamal Industrial Manufacturing operations currently include:

a. Senyar Industries Qatar Holding: production and distribution of electric cables, equipment and tools, as well as the distribution of electro-mechanical equipment;

b. Aamal Readymix: production of high quality ready-mixed concrete;c. Aamal Cement Industries: production of interlocking paving stones, concrete blocks and tiles;d. Ci-San Trading: importation and supply of high quality gabbro aggregates through Gulf Rocks; e. Innovative Lighting Company: trading and supplying of LED and other lighting products; andf. Advanced Pipes and Casts Company: manufacturer of pipes

Senyar Industries Qatar Holding

A 50:50 joint venture between Aamal and El Sewedy Electric Company, an Egyptian company listed on the Egyptian Exchange and producer of integrated cables and electrical products (such as transformers, tools and energy and water measurement and management). Senyar’s operations include:

Doha CablesThe first and largest cables manufacturing facility in Qatar, Doha Cables commenced operations in May 2010 specialising in the manufacturing of power cables, special cables, winding wires and cables accessories. Annual manufacturing production capacity is 40,000 tonnes of cable. Doha Cables is 85% interest owned by Senyar (El Sewedy Cables Qatar (of which Senyar owns 55%) owns a 12.5% interest, with an unaffiliated third party the remaining 2.5%). Effective ownership by Aamal in Doha Cables is thus 45.9%).

In 2014, Doha Cables has achieved LPCB certification for Fire Resistant Cables, and it has been approved by Kahramaa up to 66kV and has successfully passed the 132kV loop type test held at KEMA laboratories, the world renowned testing, inspection and certification organisation.

INDUSTRIAL MANUFACTURINGDIVISION

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 432 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 33

El Sewedy Cables Qatar commenced operations in 2006, specialising in the distribution of electro-mechanical equipment and cables for Doha Cables and third party manufacturers. A 49% stake (with 55% share of profits/losses) was acquired by Senyar from El Sewedy Electric Company in January 2010 with unaffiliated third parties owning the remaining 51%. Effective ownership by Aamal in El Sewedy Cables Qatar is 27.5% and is equity accounted for as an Associate.

Aamal Readymix

An entity 100% owned by Aamal. It commenced operations in 1994 and is one of the largest producers of quality ready-mixed concrete in Qatar with an annual production capacity of 600,000 cubic metres.

In 2014, Aamal Readymix has acquired 60 pieces of new equipment and fleet including trailer heads, trailer boxes, transit mixers, concrete pumps (62 metres in boom length), wheel loaders and water tankers

The branch re-opened its batching plants at Lusail after the complete renovation and overhaul of its batching plant and ice plant. Also, a new office and new Quality Control lab was built at the Lusail plant. Certifications of compliance with IMS standards, TUV ISO 9001:2008, ISO 14001:2004 and BS OHSAS 18001:2007 were renewed. The batching plants at the industrial area and Lusail were certified by NRCMA (National Readymix Concrete Association) for its compliance with the international standards of readymix concrete production and quality control.

Aamal Cement Industries W.L.L.

Aamal Company owns 99%. It commenced production of decorative interlocking paving stones and concrete blocks in 2010 with an annual production capacity of approximately 25 million blocks or two million square metres of paving stones. The plant has one of the largest block and pavement making machines in Qatar.

In 2014, Aamal Cement Industries continued to its increase its product offering as it successfully introduced four new curb stone products to the market and is expected to add six more in 2015.

Established in 2009 to build a transformers factory to produce primarily oil-filled and dry transformers. This project is still under development.

El Sewedy Cables Qatar

Doha Transformers

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 434 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 35

Ci-San Trading W.L.L.

Innovative Lighting W.L.L.

Gulf Rocks is the sole trading entity of this joint venture established in 2008 with Masraf Al Rayyan, to evaluate investments in various sectors such as industrial, real estate, and trading opportunities in both local and international markets. Effective ownership by Aamal is 74.5%; in 2012, Ci-San Trading purchased 51% with Aamal directly acquiring the remaining 49%.

Gulf Rocks itself was established in 2000 by Al Faisal Holding, and is a leading importer and provider of high quality gabbro aggregates, which is widely used in concrete products.

Aamal owns 70% of Innovative Lighting ‘QLEDs’. Established in 2012 as a joint venture with C&C Lightway of South Korea, Innovative Lighting currently trades in and distributes light emitting diodes (“LEDs”) and other lighting products (indoor, outdoor and façade) for the Qatari market and other GCC countries.

Advanced Pipes & Casts Company W.L.L.

Aamal owns 50% of Advanced Pipes and Casts Company. Established in July 2010 as a joint venture between the Company and a Saudi Arabian subsidiary of the Lokma Group, a leading pipe manufacturer in the Middle East.

In 2014, the factory commenced commercial production at its 85,000 square metre facility at Mesaieed with an annual production capacity of 450,000 tonnes. It produces a range of infrastructure and construction products including jacking pipes, reinforced concrete pipes, circular precast concrete manholes and precast concrete box culverts, a first for Qatar in manufacturing terms.

A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 37w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 436

QAR m 2014 2013 Change %

Revenue 728.8 585.8 24.4%Net Profit 114.9 86.5 32.8%Net Profit Margin 15.8% 14.8% +100 basis points

For the year ended 31 December 2014, the Trading and Distribution generated 33% of the Company's revenues, and 29% of its net profit. The Trading and Distribution division net profit rose by 32.8% to QAR 114.9m along with an improvement of 100 basis points in the net margin to 15.8%.

The major contributors to this growth have been Aamal Medical and to a lesser degree, Ebn Sina Medical, due to increased demand from both the private and public medical sectors, underpinned by the significant increase in government spending to develop the medical sector in Qatar.

During 2014, a new business entity was established called Aamal Optical Supplies, a joint venture with Qatar Optics, one of Qatar’s leading companies in the optometry industry, in which Aamal has a 51% interest. The establishment of this new business is in keeping with the development of Qatar’s healthcare system through the setting-up of the Qatar National Health Strategy for 2011-2016, designed to ensure that the population has increasing access to world-class treatment facilities.

Aamal Trading and Distribution operations currently include:

a. Ebn Sina Medical: the leading pharmaceutical distribution company in Qatarb. Aamal Medical: a leading medical equipment supplierc. Aamal Trading & Distribution: a leading distributor of automotive products d. Foot Care Centre: provider of a range of foot care services and productse. Ebn Sina Health Care Solutions: a modern chain of pharmacies located in City Center Dohaf. Aamal Optical Supplies W.L.L.: an importer, manufacturer and supplier of optical supplies and servicesg. Al Farazdaq Company: provider of printing solutions and trader of office supply products

Ebn Sina Medical

Aamal owns 100% of Ebn Sina Medical, the Qatari leading provider of pharmaceutical, hospital supplies and consumer health products, representing 50+ international reputable healthcare manufacturers from more than 20 countries including Roche, AstraZeneca, Novartis Pharma, B-Braun, Boston Scientific and Nuxe. Ebn Sina Medical also operates a retail chain including a pharmacy and three Foot Care Centre that provide a range of clinical foot care services, foot care products and specialist footwear. In 2014, Ebn Sina Medical has signed four contracts with leading multinational pharmaceuticals and consumer companies. Also, it has registered with the Supreme Council of Health, eight new pharmaceutical and herbal companies as well as more than 45 new products. Despite price reductions of 30% to 40% for medicines during 2014, Ebn Sina Medical managed to achieve more than 8% growth in the private market and more than 12% growth in both the retail pharmacy and the Foot Care Centers. Ebn Sina Medical has succeeded to complete the renewal of ISO 9001- 2008 Certification, up to June 2017.

Ebn Sina Health Care Solutions

Aamal has a 100% interest in Ebn Sina Health Care Solutions and was formerly known as Good Life Pharmacy. The renaming was done in order to capitalise on the strong Ebn Sina brand as expansion plans for this pharmacy chain are undertaken.

TRADING & DISTRIBUTIONDIVISION

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 438 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 39

Aamal has a 100% interest in Foot Care Centre, offering a broad range of biomechanical, orthopaedic and therapeutic services for feet along with a variety of foot care products from the well-known brand SCHOLL. Foot Care Centre is considered an important addition to the local market offering several popular therapeutic services. Foot Care Centre is a registered trademark in Qatar.

There are currently two Foot Care Centres operating in Qatar with a third one due to open in the Pearl Madina Centrale during the first half of 2015

Foot Care Centre Aamal Medical

Aamal owns 100% of Aamal Medical, a leading medical equipment supplier in Qatar. Aamal Medical has exclusive distribution agreements with a number of leading international medical equipment suppliers. In addition to sales of medical equipment, Aamal Medical also provides consultancy on, and builds, operating room theatres, and installs hospital information systems. In 2014, the branch has signed multiple distribution agreements with leading companies providing diverse products such as a) surgical ceiling pendants, operating lights and operating tables; b) Non-invasive patient monitoring technologies; c) emergency defibrillation and automated CPR equipment; d) communicable disease management system that has been designed by health professionals to meet specific population health needs; and e) patient monitoring, infotainment, nursing care and medical record tracking that also helps to ensure the safety, accuracy and reliability of medical data.

Aamal has a 51% interest in Aamal Optical Supplies

A partnership agreement between Aamal Company and Qatar Optics was signed in 2014 establishing Aamal Optical Supplies W.L.L.. The Company will be involved in the import, manufacture and distribution of prescription lenses, the import and distribution of contact lenses and other eye care products and services, and the opening of a specialised optical medical centre in the near term.

Aamal Optical Supplies W.L.L.

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 440 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 41

Aamal Trading & Distribution

Aamal owns 100% of Aamal Trading and Distribution, the exclusive distributor in Qatar of Bridgestone tyres since 1971 and a non-exclusive distributor of TOTAL oil and lubricant products since 1990 and is also involved with the supply, installation, commissioning of ‘GETTCO’ home appliances and maintenance of air conditioning and refrigeration equipment.

In addition, Aamal Trading and Distribution has the sole Qatari distribution rights to supply Energizer Automotive Batteries, under license from Johnson Controls Battery Group.

Al Farazdaq Company

Aamal Company holds 65% of Al Farazdaq Company which started its operations in 2013 to provide printing solutions and trade in various office supplies products. The printing press is equipped with state of the art printing machines, offering innovative digital printing solutions to the business community.

Al Farazdaq is also the sole agent of ‘Gettco Office Supplies’, offering a wide range of a high quality stationery that is durable, innovative reliable and competitively priced.In 2014, Al Farazdaq has added more printing machines in order to increase its offerings and cater to a wider customer base

A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 43w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 442

City Center Doha

Aamal owns 100% of City Center Doha, inaugurated in 2000, one of the first shopping malls in Doha and remains the largest, based upon its net leasable area. Widely regarded as the premier mall in Qatar, City Center Doha has 372 shops, 62 kiosks, a 14-screen cinema, family entertainment facility and an indoor ice skating rink.

In 2014, good progress had been made towards securing the necessary permissions for Phase 2 of the redevelopment of the mall.

Aamal Real Estate

Aamal owns 100% of Aamal Real Estate which comprises a) the Souq Najma (Al Haraj) which was built in 1993 as a traditional Middle Eastern souq comprising of 347 shops, 25 kiosks and 24 residential flats; b) the Markhiya residential complex; and c) four other residential buildings.

In 2014, Aamal Real Estate completed the renovation of three of these four residential buildings, comprising a total of 30 apartments in the Bin Mahmoud area, that were all successfully rented out to new tenants.

QAR m 2014 2013 Change %

Revenue 288.8 261.6 10.4%Net Profit* 223.3 200.8 11.2%Net profit margin 77.3% 76.8% +50 basis points

*Net profit before fair value gains on investment properties

For the year ended 31 December 2014, the Property Division generated 13% of the Company's revenues, and 56% of its net profit, excluding fair value gains on investment properties. Net profit for the Property division rose by 11.2% to QAR 223.3 million year-on-year with the net margin increasing by 50 basis points to 77.3%.

Main components to this growth were first, the completion of renovations to three buildings owned by Aamal Real Estate, comprising 30 apartments, which have now all subsequently been rented out; and secondly, the annual rental increases for properties owned by the Company.

Occupancy rate at both City Center and Aamal Real Estate remained at a high level of 95%, with 5% held back as a strategic reserve in order to allow for active management

Fair value gains on investment properties for the year were QAR 251.7 million (2013: QAR 245.1million).

Aamal Property division owns and leases retail and residential properties through two subsidiaries: City Center Doha, the largest shopping mall in Doha, and Aamal Real Estate.

PROPERTY DIVISION

A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 45w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 444

QAR m 2014 2013 Change %

Revenue 64.2 86.3 (25.6)%Net Profit 8.3 5.2 60.1%Net profits margin 12.9% 6.0% +690 basis points

For the year ended 31 December 2014, the Managed Services Division generated 3% of the Group's revenues and 2% of its net profit. Net profit for the Managed Services division rose by over 60% to QAR 8.3m over the course of the year, principally due to the 690 basis point increase in the net margin to 12.9%

The major factor behind this growth is a greater focus on cost control, along with the curtailment of several low margin contracts which also helps to explain the 25.6% drop in revenues.

The Managed Services operations focus primarily on providing commercial facilities management, outsourcing and other business support services, and currently include:

Johnson Controls Qatar W.L.L.

Aamal Company owns 51% of Johnson Controls Qatar which provides facility improvement and energy solutions to customers in Qatar. Johnson Controls Qatar offers green building and building efficiency solutions using eco-friendly materials and techniques that help lower carbon emissions and lower electricity consumption by approximately 30%. This is in line with Aamal’s strategy to offer environmentally-friendly products and services.

ECCO Gulf W.L.L.

Aamal Company owns 51% of ECCO Gulf which is a joint venture with ECCO Outsourcing, the leading Egyptian contact centre operator and business process outsourcer. ECCO Gulf commenced operations in 2010 offering Business Process Outsourcing, professional service outsourcing and human resources outsourcing to clients in Qatar.

In 2014, ECCO Gulf has introduced new services and successfully diversified its client sectors to include banking, real estate, insurance and shipping.

MANAGED SERVICESDIVISION

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 446 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 47

Aamal Services

Aamal owns 100% of Aamal Services which provides a wide range of services, including cleaning, hotel and hospitality services, waste collection and disposal (including medical waste and solid waste), ground maintenance and landscaping, pest control and fleet/car washing.

Aamal Travel and Tourism

Aamal owns 100% of Aamal Travel and Tourism, which is an International Air Transport Association (IATA) accredited travel agency providing a range of travel services, including airline reservations and ticketing, worldwide hotel bookings and holiday packages.

Aamal Travel has officially joined “Lufthansa City Center International” network of 688 Travel Agencies in 88 countries around the world; this strategic move will enable Aamal Travel to exchange knowledge and business with the network partners around the world.

Accordingly, the branch trade name was rebranded to “Aamal Travel Lufthansa City Center”, becoming the first Lufthansa City Center partner in Qatar.

AAMAL COMPANY Q.S.C.Consolidated Financial Statements31 December 2014

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 450 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 51

INDEPENDENT AUDITORS’ REPORTTO THE SHAREHOLDERS OF AAMAL COMPANY Q.S.C.

Report on the consolidated financial statementsWe have audited the accompanying consolidated financial statements of Aamal Company Q.S.C. (the “Company”), which comprise the consolidated statement of financial position as at 31 December 2014, and the consolidated statements of income, profit or loss and other comprehensive income, cash flows and changes in equity for the year then ended, and notes, comprising a summary of significant accounting policies and other explanatory information.

Board of Directors’ responsibility for the consolidated financial statementsThe Board of Directors is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards and, for such internal control as the Board of Directors determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ responsibilityOur responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on our judgement, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Board of Directors, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the consolidated financial statements present fairly, in all material respects, the consolidated financial position of the Company as at 31 December 2014 and its consolidated financial performance and consolidated cash flows for the year then ended in accordance with International Financial Reporting Standards.

Report on other legal and regulatory requirementsWe have obtained all the information and explanations which we consider necessary for the purposes of our audit. The Company has maintained proper accounting records and its consolidated financial statements are in agreement therewith. We confirm that physical count of inventories was carried out in accordance with established principles. We have reviewed the accompanying report of the Board of Directors and confirm that the financial information contained therein is in agreement with the books and records of the Company. We are not aware of any violations of the provisions of the Qatar Commercial Companies Law No. 5 of 2002 or the terms of the Company’s Articles of Association during the year which might have had a material adverse effect on the business of the Company or on its consolidated financial position as at 31 December 2014.

3 February 2015 Gopal BalasubramaniamDoha KPMGState of Qatar Qatar Auditors Registry Number 251

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 452 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 53

Sheikh Faisal Bin Qassim Al-ThaniChairman

Tarek Mahmoud El SayedManaging Director

Mohammad RamahiChief Financial Officer

CONSOLIDATED STATEMENT OF FINANCIAL POSITIONAt 31 December 2014

Note2014QR

2013QR

ASSETSCurrent AssetsCash and bank balances 4 554,659,257 436,136,756Accounts receivable and prepayments 5 518,412,487 510,089,839Amounts due from related parties 6 318,597,869 214,439,950Inventories 7 300,570,431 316,699,545

1,692,240,044 1,477,366,090

Non-current assetsAvailable-for-sale investments - 24,983Equity-accounted investees 8 150,304,676 133,106,907Investment properties 9 6,669,136,000 6,402,486,000Property, plant and equipment 10 553,338,058 519,970,890

7,372,778,734 7,055,588,780

TOTAL ASSETS 9,065,018,778 8,532,954,870

LIABILITIES AND EQUITYCurrent liabilitiesBank overdrafts 4 2,346,320 6,836,280Accounts payable and accruals 11 413,573,770 445,046,573Amounts due to related parties 12 38,405,073 48,199,591Interest bearing loans and borrowings 13 671,682,995 749,520,820

1,126,008,158 1,249,603,264

Non-current liabilitiesInterest bearing loans and borrowings 13 232,698,286 165,384,481

Employees’ end of service benefits 14 22,011,182 19,957,976254,709,468 185,342,457

TOTAL LIABILITIES 1,380,717,626 1,434,945,721

EQUITYShare capital 15 6,000,000,000 6,000,000,000Legal reserve 16 435,842,111 378,132,552Treasury shares (2,075,865) (2,075,865)Cumulative change in fair value - 4,069Retained earnings 1,031,009,690 526,628,214

Equity attributable to equity holders of the parent 7,464,775,936 6,902,688,970

Non-controlling interests 219,525,216 195,320,179Total equity 7,684,301,152 7,098,009,149

TOTAL LIABILITIES AND EQUITY 9,065,018,778 8,532,954,870

CONSOLIDATED STATEMENT OF INCOMEFor the year ended 31 December 2014

2014 2013

Note QR QR

Revenue 17 2,139,104,614 2,122,595,133Direct costs 18 (1,633,072,684) (1,702,139,177)

GROSS PROFIT 506,031,930 420,455,956

Other income 19 11,785,913 11,516,688Marketing and promotion expenses (23,508,622) (18,995,918)General and administrative expenses 20 (125,134,749) (109,981,101)Depreciation (8,569,845) (9,331,067)Finance costs 21 (30,238,041) (44,930,877)Share of profits of equity-accounted investees 8 18,122,554 18,499,901

PROFIT BEFORE FAIR VALUE GAINS ON INVESTMENT PROPERTIES 348,489,140 267,233,582

Net fair value gains on investment properties 9 251,692,874 245,051,107

PROFIT FOR THE YEAR 600,182,014 512,284,689

Profit attributable to:Equity holders of the parent 577,095,585 506,874,507Non-controlling interests 23,086,429 5,410,182

600,182,014 512,284,689

Basic and diluted earnings per share (QR)(attributable to equity holders of the parent) 22 0.96 0.85

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOMEFor the year ended 31 December 2014

2014 2013QR QR

Profit for the year 600,182,014 512,284,689Other comprehensive incomeItems that are or may be reclassified to profit or lossUnrealised (loss)/gain on available-for-sale investments (5,461) 6,020

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 600,176,553 512,290,709

Total comprehensive income attributable to:Equity holders of the parent 577,091,516 506,878,992Non-controlling interests 23,085,037 5,411,717

600,176,553 512,290,709

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 454 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 55

CONSOLIDATED STATEMENT OF CASH FLOWSFor the year ended 31 December 2014

2014 2013Note QR QR

OPERATING ACTIVITIESProfit for the year 600,182,014 512,284,689Adjustment for:

Net fair value gains on investment properties 9 (251,692,874) (245,051,107)Depreciation 10 44,137,864 42,495,449Provision for employees’ end of service benefits 14 4,520,855 4,056,969Allowance for impairment of trade accounts receivable 20 2,694,547 2,294,590Profit on disposal of property, plant and equipment 19 (287,032) (737,647)Provision for slow moving inventories 7 78,431 2,380,617Interest income 19 (3,315,399) (2,824,216)Finance costs 21 30,238,041 44,930,877Gain on sale of available-for-sale investments (6,550) -Share of profit of equity-accounted investees 8 (18,122,554) (18,499,901)

Operating profit before working capital changes: 408,427,343 341,330,320Inventories 16,050,683 82,822,711Accounts receivable and prepayments (11,017,195) (30,102,654)Accounts payable and accruals (46,477,353) 53,120,387Net movement in amounts due from and due to related parties (113,952,437) (44,382,753)

Cash from operations 253,031,041 402,788,011Finance costs paid (30,540,830) (45,056,522)End of service benefits paid 14 (2,467,649) (2,210,756)

Net cash from operating activities 220,022,562 355,520,733

INVESTING ACTIVITIESInterest income received 19 3,315,399 2,824,216Proceeds from disposal of property, plant and equipment 1,036,890 1,274,457Proceeds from sale of available-for-sale investments 26,072 -Dividends received from a joint venture 924,785 11,992,985Additions to investment properties 9 (14,957,126) (9,568,047)Additions to property, plant and equipment 10 (77,952,101) (147,870,074)

Net cash used in investing activities (87,606,081) (141,346,463)

FINANCING ACTIVITIESNet movement in interest bearing loans and borrowings (10,524,020) (149,939,995)Contributions from non-controlling interests 1,120,000 70,000

Net cash used in financing activities (9,404,020) (149,869,995)

INCREASE IN CASH AND CASH EQUIVALENTS 123,012,461 64,304,275Cash and cash equivalents at 1 January 429,300,476 364,996,201

CASH AND CASH EQUIVALENTS AT 31 DECEMBER 4 552,312,937 429,300,476

Shar

eca

pital

Lega

lre

serv

eTr

easu

ry

shar

es

Cum

ulativ

e ch

ange

in fa

ir va

lue

Reta

ined

earn

ings

Tota

lNo

n-co

ntro

lling

inter

ests

Tota

lEq

uity

QRQR

QRQR

QRQR

QRQR

Balan

ce at

31 D

ecem

ber 2

012

5,445

,000,0

0032

7,445

,101

(2,07

5,865

)(4

16)

638,2

48,27

56,4

08,61

7,095

189,8

38,46

26,5

98,45

5,557

Bonu

s sha

res i

ssue

d55

5,000

,000

--

-(5

55,00

0,000

)-

--

Profi

t for t

he ye

ar

--

--

506,8

74,50

750

6,874

,507

5,410

,182

512,2

84,68

9Ot

her c

ompr

ehen

sive i

ncom

e for

the y

ear

--

-4,4

85-

4,485

1,535

6,020

Tran

sfer t

o leg

al re

serve

-50

,687,4

51-

-(5

0,687

,451)

--

-Co

ntribu

tion f

rom

non-

contr

olling

inter

est

--

--

--

70,00

070

,000

Contr

ibutio

n to s

ocial

and s

ports

activ

ities f

und

--

--

(12,8

07,11

7)(1

2,807

,117)

-(1

2,807

,117)

Balan

ce at

31 D

ecem

ber 2

013

6,000

,000,0

0037

8,132

,552

(2,07

5,865

)4,0

6952

6,628

,214

6,902

,688,9

7019

5,320

,179

7,098

,009,1

49Pr

ofit fo

r the

year

-

--

-57

7,095

,585

577,0

95,58

523

,086,4

2960

0,182

,014

Othe

r com

preh

ensiv

e inc

ome f

or th

e yea

r-

--

(4,06

9)-

(4,06

9)(1

,392)

(5,46

1)Tr

ansfe

r to l

egal

rese

rve-

57,70

9,559

--

(57,7

09,55

9)-

--

Contr

ibutio

n fro

m no

n-co

ntroll

ing in

teres

t-

--

--

-1,1

20,00

01,1

20,00

0Co

ntribu

tion t

o soc

ial an

d spo

rts ac

tivitie

s fun

d -

--

-(1

5,004

,550)

(15,0

04,55

0)-

(15,0

04,55

0)

Balan

ce at

31 D

ecem

ber 2

014

6,000

,000,0

0043

5,842

,111

(2,07

5,865

)-

1,031

,009,6

907,4

64,77

5,936

219,5

25,21

67,6

84,30

1,152

Attri

buta

ble to

equ

ity h

older

s of t

he p

aren

t

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY For the year ended 31 December 2014

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 456 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 57

1 CORPORATE INFORMATION AND PRINCIPAL ACTIVITIES

Aamal was formed on 13 January 2001 as a private shareholding company with limited liability (W.L.L.) under the Commercial Registration Number 23245 in the State of Qatar. On 12 July 2007, the private shareholders resolved to transform Aamal into a Qatari Shareholding Company (Q.S.C.) (the “Company”). Accordingly, the Company was listed on Qatar Exchange on 5 December 2007. The Company’s registered office is at P.O. Box 22477, Doha, State of Qatar.

The Company is organised into a head office (Aamal) and branches and operates in the State of Qatar. The following table sets out the principal activities of the branches:

The consolidated financial statements were authorised for issue by the representatives of the Board of Directors of Aamal Company Q.S.C. on 3 February 2015.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the year ended 31 December 2014

Branch Principal activitiesCity Center Qatar Branch Leasing the facilities of the retail outlet complex in City Center Doha.Aamal Real Estate Branch Residential and commercial real estate investment and property rental.Aamal Readymix Branch Production and sale of readymix concrete.Ebn Sina Medical Branch Wholesale and retail distribution of pharmaceuticals and general consumable

products.Aamal Medical Branch Wholesale distribution of medical equipment.Aamal Trading and Distribution Branch Sale of tyres, lubricants, batteries and home appliances.Aamal Services Branch Providing facilities management and cleaning services. Aamal Travels Branch Operating a travel agency.Aamal for Industrial Projects Branch Industrial investments.Ebn Sina Heath Care Solutions City Center Pharmacy (Good Life Pharmacy Branch)

Sale of pharmaceuticals, baby care products, medicine and general consum-able products.

Foot Care Centre Branch Sale of footwear, clinical activities and general commercial trading products.

2 BASIS OF CONSOLIDATION

The consolidated financial statements comprise the financial statements of Aamal Company Q.S.C. (the “Company”) and its subsidiaries, associates and joint controlled entity (together referred to as the “Group”).

SubsidiariesSubsidiaries are entities controlled by the Group. The Group controls an entity when it is exposed to, or has rights to, variable returns of its involvement with the entity and has the ability to affect those returns through its power over the entity. The financial statements of subsidiaries are included in the consolidated financial statements from the date on which control commences until the date on which control ceases. When the Group loses control over a subsidiary, it dereognises the assets and liabilities of the subsidiary, and any related non-controlling interest and other components of equity. Any resulting gain or loss is recognised in consolidated statement of income. Any interest retained in the former subsidiary is measured at fair value when control is lost.

Set out below are the Group’s principal subsidiaries at 31 December 2014. Unless otherwise stated, the subsidiaries as listed below have share capital consisting solely of ordinary shares, which are held directly by the group and the proportion of ownership interests held equals to the voting rights held by Group. The country of incorporation or registration is also their principal place of business:

2 BASIS OF CONSOLIDATION (continued)

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the year ended 31 December 2014

Company name Country of incorporation Principal activity

Proportion of ownership held by the

GroupNon controllinginterest

Aamal Cement Industries W.L.L.

Qatar Development and management of factories and the production of curb stone, interlock slabs and cement bricks.

99% 1%

IMO Qatar Company W.L.L. Qatar Construction and repair of power plant, establishment and management of industrial enterprises and acting as a representative for the international companies.

60% 40%

Senyar Industries Qatar Holding W.L.L.

Qatar Management of subsidiaries and associates, owning of patents, businesses and subletting them and provision of investment portfolio management for its subsidiaries and associates. Under the shareholders agreement signed between the Group and the other shareholders, the Group is able to appoint the chairman and two other members to the Board of Directors (out of six members) and is able to govern the financial and operating policies of Senyar Industries Qatar Holding W.L.L. Accordingly, the company is considered as a subsidiary of the Group.

50% 50%

Doha Cables Qatar W.L.L. Qatar Maintenance and manufacture of electric cables, equipment and tools. Doha Cables Qatar W.L.L. is 91.875% (effectively) owned by Senyar Industries Qatar Holding W.L.L., a subsidiary of the Group. The Group has the power, indirectly through Senyar Industries Qatar Holding W.L.L., to govern financial and operating policies of Doha Cables Qatar W.L.L. and accordingly the company was considered as a subsidiary of the Group.

45.9% 54.1%

Ecco Gulf Company W.L.L. Qatar Offers professional and business process outsourcing and call center services.

51% 49%

Advanced Pipes and Casts Company W.L.L.

Qatar Manufacturing of wide cement and glass reinforced pipes systems for infrastructure and pipeline projects. The Group has the power to govern the financial and operating policies of Advanced Pipes and Casts Company W.L.L. by virtue of a shareholders’ agreement. Thus the Company has been considered as a subsidiary of the Group.

50% 50%

Johnson Controls Qatar W.L.L.

Qatar Provision of facilities management services, energy services and building maintenance and cleaning services to corporate clients.

51% 49%

Ci-San Trading W.L.L. Qatar Selling, buying, renting and developing real estate, investment in shares, management of real estate properties, owning the patent and trademark and trading in equipment and vehicles. The Group has the power to govern the financial and operating policies of Ci-San by virtue of a shareholders’ agreement.

50% 50%

Gulf Rocks Qatar Retail distribution of aggregates. 74.5% 25.5%Innovative Lighting Company W.L.L.

Qatar Trading of Light Emitting Diode (LED) Lamps and other lighting products.

70% 30%

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 458 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 59

2 BASIS OF CONSOLIDATION (continued)

Subsidiaries (continued)

Company name Country of incorporation Principal activity

Proportion of ownership held by the

GroupNon controllinginterest

Al Farazdaq Company W.L.L. Qatar Trading of office supplies and providing printing and laminating services.

65% 35%

Aamal Optical Supplies W.L.L.

Qatar Trading of optical supplies 51% 49%

Non-controlling interestsNon-controlling interests are measured at their proportionate share of the acquiree’s identifiable net assets at the acquision date. Changes in the Group’s interest in a subsidiary that do not result in a loss of control are accounted for as equity transactions.

Transactions eliminated on consolidationIntra-group balances and transactions, and any unrealised income and expenses arising from intra-group transactions, are eliminated. Unrealised gains arising from transactions with equity-accounted investees are eliminated against the investment to the extent of the Group’s interest in the investee. Unreaslised losses are eliminated in the same way as unrealised gains, but only to the extent that there is no evidence of impairment.

Interests in joint arrangements and associatesDetails of each of the Group’s material joint ventures and associates at the end of the reporting period are as follows

Company name Country of incorporation Principal activity

Proportion of ownership and voting power held by the Group

El Sewedy Cables Qatar W.L.L.

Qatar Trading in electro-mechanical equipment and providing related services. El Sewedy Cables Qatar W.L.L. is 49% owned (with 55% share of profits / (losses) by Senyar Industries Qatar Holding W.L.L., a subsidiary of the Group. However due to a revised shareholders agreement, the entity has become a joint venture effective from 1 January 2012 which is accounted for under the equity method.

55%

Frijns Structural Steel Middle East W.L.L.

Qatar Entity is engaged in steel fabrications. Group measure the associate under equity method.

20%

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the year ended 31 December 2014

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the year ended 31 December 2014

3.2 CHANGES IN ACCOUNTING POLICIES

The accounting policies adopted are consistent with those of the previous financial year except for the following standards effective for the annual period beginning on or after 1 January 2014. These standards and amendments, did not have any material impact to the Group.

Amendments to IFRS 10, IFRS 12 and IAS 27 “Investment Entities”The amendments to IFRS 10 define an investment entity and require a reporting entity that meets the definition of an investment entity not to consolidate its subsidiaries but instead to measure its subsidiaries at fair value through profit or loss in its consolidated and separate financial statements.

Consequential amendments have been made to IFRS 12 and IAS 27 to introduce new disclosure requirements for investment entities.

Amendments to IAS 32 Offsetting Financial Assets and Financial LiabilitiesThe amendments to IAS 32 clarify the requirements relating to the offset of financial assets and financial liabilities. Specifically, the amendments clarify the meaning of ‘currently has a legally enforceable right of set-off’ and ‘simultaneous realisation and settlement’. The amendments have been applied retrospectively.

Amendments to IAS 36 Recoverable Amount Disclosures for Non-Financial AssetsThe amendments to IAS 36 remove the requirement to disclose the recoverable amount of a cash-generating unit (CGU) to which goodwill or other intangible assets with indefinite useful lives had been allocated when there has been no impairment or reversal of impairment of the related CGU. Furthermore, the amendments introduce additional disclosure requirements applicable to when the recoverable amount of an asset or a CGU is measured at fair value less costs of disposal. These new disclosures include the fair value hierarchy, key assumptions and valuation techniques used which are in line with the disclosure required by IFRS 13 Fair Value Measurements.

Amendments to IAS 39 Novation of Derivatives and Continuation of Hedge AccountingThe amendments to IAS 39 provide relief from the requirement to discontinue hedge accounting when a derivative designated as a hedging instrument is novated under certain circumstances. The amendments also clarify that any change to the fair value of the derivative designated as a hedging instrument arising from the novation should be included in the assessment and measurement of hedge effectiveness. The amendments have been applied retrospectively.

IFRIC 21 LeviesIFRIC 21 on Levies (amendments to IAS 32) provide guidance on the accounting for levies in the financial statements of the entity that is paying the levy.

3 BASIS OF PREPARATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS), and the applicable requirements of Qatar Commercial Companies’ Law No. 5 of 2002.

The consolidated financial statements have been presented in Qatari Riyals (QR), which is the Company’s functional and presentation currency and have been rounded to the nearest Qatari Riyal. The consolidated financial statements are prepared under the historical cost convention modified to include the measurement at fair value of investment properties and available-for-sale investments.

3.1 BASIS OF PREPARATION

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 460 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 61

3.3 IASB STANDARDS AND INTERPRETATIONS ISSUED BUT NOT ADOPTED

The following IASB standards/amendments have been issued but are not yet mandatory, and have not been early adopted by the Group:

The Group is considering the implications of the above standards, and the timing of adoption by the Group.

3.4 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Business combinationsThe Group accounts for business combinations using the acquisition method when control is trnasferred to the Group. The consideration transferred in the acquisition is generally measured at fair value, as are the identifiable net assets acquired. Any goodwill that arises is tested annually for impairment. Any gain on a bargain purchase is recognised in profit or loss immediately. Transaction costs are expensed as incurred, except if reltated to the issue of debt or equity securities.

The consideration transferred does not include amounts related to the settlement of pre-existing relationships. Such amounts are recognised in profit or loss.

Any contingent consideration payable is measured at fair value at the acquisition date. If the contingent consdieration is classified as equity, then it is not remeasured and settlement is accounted for within equity. Otherwise, subsequent changes in the fair value of the contingent consderation are recognised in profit or loss.

Cash and cash equivalents For the purpose of the consolidated statement of cash flows, cash and cash equivalents consist of cash and bank balances and short term bank deposits with an original maturity of three months or less, net of outstanding bank overdrafts.

Accounts receivableAccounts receivable are stated at original invoice amount less an allowance for any uncollectible amounts. An estimate for doubtful debts is made when collection of the full amount is no longer probable. Bad debts are written off when there is no possibility of recovery.

InventoriesInventories are stated at the lower of cost and net realisable value. Costs are those expenses incurred in bringing each product to its present location and condition.

3 BASIS OF PREPARATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Standard/Interpretation Content Effective date

IFRS 9 Financial Instruments (new standard) 1 January 2018IFRS 15 Revenue from Contracts with Customers (new standard) 1 January 2017IFRS 11 Accounting for Acquisitions of Interests in Joint Operations (amendment) 1 January 2016IAS 16 and IAS 38 Clarification of Acceptable Methods of Depreciation and Amortisation

(amendments)1 January 2016

Goods for resale/work in progress - Cost of direct materials and labour plus attributable overheads based on a normal level of activity.

Raw material and spare parts - Purchase cost on a weighted average basis.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the year ended 31 December 2014

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the year ended 31 December 2014

Net realisable value is based on estimated selling price less any further costs expected to be incurred to completion and disposal.

Interests in equity-accounted investeesThe Groups, interest in equity-accounted investees comprise interest in associates and joint venture.

Associates are those entities in which the Group has significant influence, but not control or joint control, over the financial and operating policies. A joint venture is an arrangement in which the Group has joint control, whereby the Group has rights to the net assets of the arrangement, rather than rights to its assets and obligations for its liabilities.

Interests in associates and the joint venture are accounted for using the equity method. They are recognised initially at cost, which includes transaction costs. Subsequent to initial recognition, the consolidated financial statements include the Group’s share of the profit or loss and other comprehensive income of equity-accounted investees, until the date on which significant influence or joint control ceases.

The reporting dates of the equity-accounted investees and the Group are identical and the equity-accounted investees’ accounting policies conform to those used by the Group for like transactions and events in similar circumstances.

Investment propertiesLand and buildings are considered as investment properties only when they are being held to earn rentals or for capital appreciation or for both.

Investment properties are measured initially at cost, including transaction costs and borrowing costs that are directly attributable to construction of the asset. The carrying amount includes the cost of replacing part of an existing investment property at the time that cost is incurred if the recognition criteria are met; and excludes the costs of day-to-day servicing of an investment property. Subsequent to initial recognition, investment properties are stated at fair value, which reflects market conditions at the reporting date. Gains or losses arising from changes in the fair values of investment properties are included in the consolidated statement of income in the year in which they arise.

Investment properties are derecognised when either they have been disposed off or when the investment property is permanently withdrawn from use and no future economic benefit is expected from its disposal. Any gains or losses on the retirement or disposal of an investment property are recognised in the consolidated statement of income in the year of retirement or disposal.

Property under construction is dealt with under IAS 40 and recorded at cost less accumulated impairment losses until either its fair value becomes reliably determinable or construction is completed (whichever is earlier). At that time, it is reclassified as investment property and a fair value adjustment is recognised in the consolidated statement of income.

Transfers are made to or from investment property only when there is a change in use. For a transfer from investment property to owner occupied property, the deemed cost for subsequent accounting is the fair value at the date of change in use. If owner occupied property becomes an investment property, the difference between the carrying value and the fair value at the date of transfer is recognised as a revaluation reserve in the equity and is released to the consolidated statement of income upon disposal of such property.

3.4 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

3 BASIS OF PREPARATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

w w w.a a m a l . c o m .q a A n n u a l R e p o r t 2 0 1 462 A a m a l A n n u a l R e p o r t 2 0 1 4 A a m a l C o m p a n y Q . S . C . 63

Property, plant and equipmentProperty, plant and equipment is stated at cost including borrowing costs that are eligible for capitalisation and excluding the costs of day-to-day servicing, less accumulated depreciation and any impairment in value.

Depreciation is provided on a straight-line basis on all property, plant and equipment. The rates of depreciation are based upon the following estimated useful lives:

The carrying amounts are reviewed for impairment when events or changes in circumstances indicate that the carrying value may not be recoverable. If any such indication exists and where the carrying values exceed the estimated recoverable amount, the assets are written down to their recoverable amount, being the higher of their fair value less costs to sell and their value in use.

Expenditure incurred to replace a component of an item of property, plant and equipment that is accounted for separately is capitalised and the carrying amount of the component that is replaced is written off. Other subsequent expenditure is capitalised only when it increases future economic benefits of the related item of property, plant and equipment. All other expenditure is recognised in the consolidated statement of income as the expense is incurred.

An item of property, plant and equipment is derecognised upon disposal or when no future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset is included in the consolidated statement of income in the year the asset is derecognised.

The asset’s residual values, useful lives and method of depreciation are reviewed, and adjusted if appropriate, at each financial year end.

Borrowing costsBorrowing costs directly attributable to the acquisition, construction or production of an asset that necessarily takes substantial period of time to get ready for its intended use or sale are capitalised as part of the cost of the respective assets. All other borrowing costs are expensed in the year they incur. Borrowing costs consist of the interest and other costs that the Group incurs in connection with the borrowing of funds.

Accounts payable and accrualsLiabilities are recognised for amounts to be paid in the future for goods or services received, whether billed by the supplier or not.

Interest bearing loans and borrowingsInterest bearing loans and borrowings are recognised initially at fair value of the amounts borrowed, less directly attributable transaction costs. Subsequent to initial recognition, interest bearing loans and borrowings are measured at amortised cost using the effective interest method, with any differences between the cost and final settlement values being recognized in the consolidated statement of income over the period of borrowings. Instalments due within one year at amortised cost are shown as a current liability.

Gains or losses are recognised in the consolidated statement of income when the liabilities are derecognised. Interest relating to interest bearing loans and borrowings is expensed in the year in which it is incurred except those qualify for capitalisation.

3 BASIS OF PREPARATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

3.4 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)