ANNUAL REPORT 2010/11 - ca.go.ke · HRA Human Resources and Administration HSPA High Speed Packet...

76

REPORT ANNUAL Financial Year 2010/11 Opening your world

-

Upload

nguyenphuc -

Category

Documents

-

view

216 -

download

0

Transcript of ANNUAL REPORT 2010/11 - ca.go.ke · HRA Human Resources and Administration HSPA High Speed Packet...

REPORTANNUAL Financial Year

2010/11

Opening your world

OUR MISSIONTo facilitate access to communications

services through enabling regulation and catalyze the country’s socio-economic

development.

OUR VISIONAcess to communications services by

all in Kenya by 2030.

1

Acronyms and Abbreviations

Board of Directors

Chairman’s Overview

Director General’s Word

Corporate Governance

Organizational Structure

Commission’s Mandate

02

04

08

10

13

15

16

CONTENTSTABLE OF

Pg

Macro-economic Environment

Management of Scarce Resources

Promoting Competition and Innovation

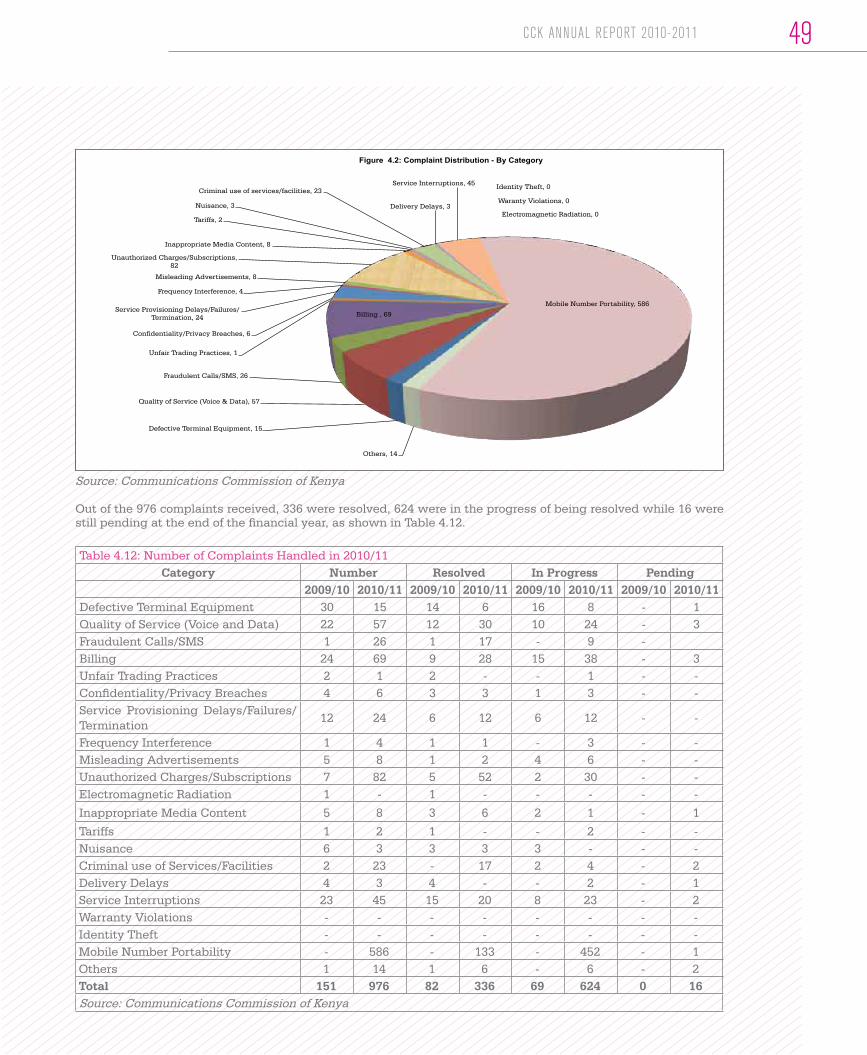

Ensuring Compliance and Empowering Consumers

Roadmap to Universal Access

Capacity Building, Improvement of Systems and Working Environment

Corporate Communication and International Liaison

Financial Information

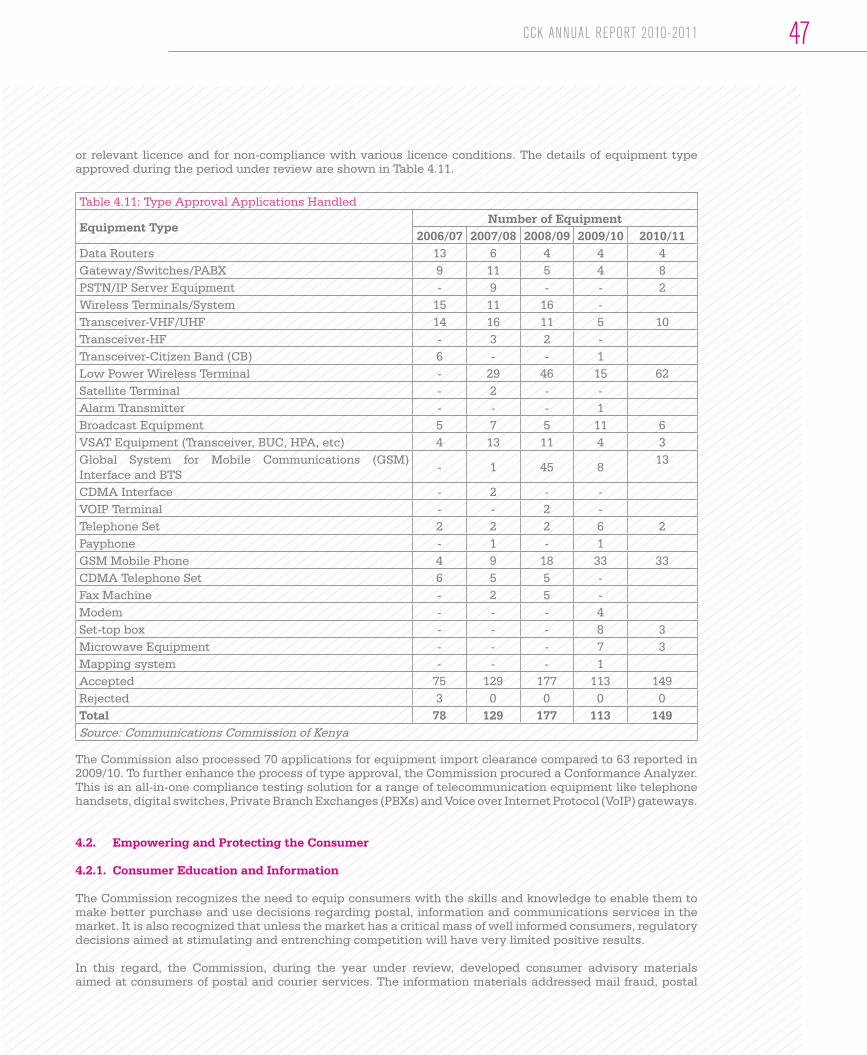

17

22

28

40

53

56

61

65

Chapter 1

Chapter 2

Chapter 3

Chapter 4

Chapter 5

Chapter 6

Chapter 7

Chapter 8

2G Second Generation3G Third Generation4G Fourth GenerationAIDS Acquired Immune Deficiency SyndromeARICEA Association of Regulators of Information

and Communications for Eastern and Southern Africa

ASK Agricultural Society of KenyaASP Application Service ProviderATU African Telecommunications UnionBCAC Broadcasting Content Advisory CouncilBPO Business Process OutsourcingBTS Base Transmitter StationsBUC Block Up ConverterCA Consumer AffairsCAP ChapterCB Citizen BandCCK Communications Commission of KenyaccTLD country code Top Level DomainCDMA Code Division Multiple AccessCEOs Chief Executive OfficersCIIP Critical Information Infrastructure

ProtectionCIRT Computer Incident Response TeamCPI Consumer Price IndexCPR Communication and Public RelationsCS Commission SecretaryCSP Content Service ProvidersCSR Corporate Social ResponsibilityCTMA Competition, Tariffs and Market

AnalysisCTO Commonwealth Telecommunications

OrganizationdBm Decibels (dB) measurement (m)DCNO Data Carrier Network OperatorDG Director-GeneralDMP Dominant Market PowerDPM Directorate of Personnel ManagementDR Disaster RecoveryDSL Digital Subscriber LineDTC Digital Television CommitteeDVB-T2 Digital Video Broadcast – Terrestrial 2nd

GenerationEAC East African CommunityEACO East African Communications

OrganizationEA-IGF East Africa Internet Governance ForumEASSY East African Sub-marine Cable SystemEDGE Enhanced Data Rates for GSM EvolutionESA European Space AgencyF&A Finance and AccountsFSM Frequency Spectrum ManagementFTR Fixed Termination RateFWA Fixed Wireless AccessGAAP Generally Accepted Accounting PracticeGbps Giga Bits Per SecondGDP Gross Domestic ProductGHz Giga HertzGIXP Government Internet Exchange PointGMPCS Global Mobile Personal Communications

by SatelliteGPRS General Packet Radio Service

GSM Global System For Mobile Communication

GSR Global Symposium for RegulatorsHF High FrequencyHIV Human Immuno-deficiency VirusHPA High Power AmplifierHR4ICT Human Resource for Information and

Communication TechnologyHRA Human Resources and AdministrationHSPA High Speed Packet AccessIAS Internal Audit ServiceIASs International Accounting StandardsIBC International Broadcasting ConventionIBGO Internet Backbone and Gateway

OperatorICANN Internet Corporation for Assigned

Names and NumbersICT Information and Communications

TechnologyIGF Internet Governance ForumIGS International Gateway Systems &

ServicesIMIS Integrated Management Information

SystemIP Internal ProtocolISO International Organization for

StandardizationISS International System and ServicesIT Information TechnologyITU International Telecommunication UnionIXP Internet Exchange PointKACC Kenya Anti Corruption CommissionKCCT Kenya College of Communications

TechnologyKE-CIRT Kenya national Computer Incident

Response TeamKECOSO Kenya Communications Sports

OrganizationKENIC Kenya Network Information CentreKES Kenya ShillingKIA Kenya Institute of AdministrationKICA Kenya Information and Communications

Act, Cap 411AK-IGF Kenya Internet Governance ForumKNBS Kenya National Bureau of StatisticsKNLS Kenya National Library ServicesKPIs Key Performance IndicatorsLA Legal AffairsLAN Local Area NetworkLCS Licensing, Compliance StandardsLLOs Local Loop OperatorsLRIC Long Run Incremental CostLTE Long Term EvolutionMACRA Malawi Communications Regulatory

AuthorityMbps Mega Bits Per SecondMHz Mega HertzMNDC Mobile National Destination CodesMNP Mobile Number PortabilityMOS Mean Opinion ScoreMOU Minutes of UseMoU Memorandum of Understanding

Acronyms and Abbreviations2

MSK Marketing Society of KenyaMTR Mobile Termination RateNACADAA National Campaign Against Drug Abuse AuthorityNACC National Aids Control CouncilNCPWDs National Council for Persons with DisabilitiesNFP Network Facility ProviderNFP T1 Network Facility Provider Tier 1NFP T2 Network Facility Provider Tier 2NFP T3 Network Facility Provider Tier 3NGN Next Generation NetworksNPC National Preparatory CommitteeNSS National Space SecretariatPAPU Pan African Postal UnionPBXs Private Branch ExchangesPCK Postal Corporation of KenyaPDNO Public Data Network OperatorPKI Public Key InfrastructurePOC Postal Operations CouncilPROC ProcurementPRS Premium Rate ServicesPRSK Public Relations Society of KenyaPSTN Public Switched Telephone NetworkPWDs Persons with DisabilitiesQMS Quality Management SystemQoS Quality of ServiceRRB Radio Regulations BoardRxLev Received signal levelSCR Submarine Cable Landing RightsSDR Software Defined RadiosSEACOM Sea Submarine CommunicationsSHF Super High FrequencySMS Short Message ServiceSOYA Sports Personality of the Year AwardSP-B&DM Special Projects, Broadcasting and Digital MigrationSSA Sub-Saharan AfricaTbps Tera Bits Per SecondTCRA Tanzania Communications Regulatory AuthorityTEAMS The East African Marine SystemTEC Telecommunications ContractorsTEV Telecommunications VendorsTKL Telkom Kenya LimitedTNA Training Needs AssessmentTP Technical PersonnelTV TelevisionUCC Uganda Communications CommissionUDPK United Disabled Persons of KenyaUHF Ultra High FrequencyUK United KingdomULF Unified Licensing FrameworkUN United NationsUPU Universal Postal UnionUSD United States DollarUSF Universal Service FundVAS Value Added ServicesVHF Very High FrequencyVOIP Voice over Internet ProtocolVSAT Very Small Aperture TerminalWIMAX Worldwide Interoperability for Microwave AccessWRC-12 World Radio Conference 2012WSIS World Summit on the Information SocietyWTDC World Telecommunications Development ConferenceZICTA Zambia Information and Communication Technology Authority

3CCK ANNUAL REPORT 2010-2011 3

Hon. Eng. Philip O. Okundi, EBS, HSC

CHAIRMANKariithi Njogu DIRECTOR

Eunice M. Ombati *DIRECTOREunice M. Ombati *DIRECTOR

Aloys .O. Ang’asa DIRECTOR

Charles J.K Njoroge, EBSDIRECTOR GENERAL

Joseph K. Kinyua, CBS DIRECTOR

Dr. Bitange Ndemo, EBS DIRECTOR

Peter L. Simani DIRECTOR

Dr. Monica Kerretts -Makau DIRECTOR

John Omo COMMISSION SECRETARY

Shakaba C. Induli, MBS ALTERNATE DIRECTOR(Ministry of Finance)

Henry Mungasia ALTERNATE DIRECTOR(Ministry of Information & Communications)

Francis W. WangusiAg. DIRECTORGENERAL(August 2011 to date)

Francis Kimemia, CBS DIRECTOR

Matei M. Ndeti DIRECTOR

Joe Kamau *DIRECTOR

Alice Munyua * DIRECTOR

* Retired before the end of the year under review. See profiles overleaf.

Profiles of CCK Board Members

Hon. Eng. Philip O. Okundi, EBS, HSC - Chairman Hon. Eng. Philip O. Okundi is the Chairman of the Board of Directors of the Communications Commission of Kenya. He was appointed to the position in October 2008. He holds a Msc. in Telecommunications Systems Engineering from the University of Essex and a BSc. in Electrical and Telecommunications Engineering from the University of Westminster. He is a fellow of the Institution of Engineers of Kenya and the UK, a registered Engineer and a Chartered Electrical Engineer (UK).

Mr. Charles J.K. Njoroge, EBS – Director-GeneralMr. Charles J.K. Njoroge is the Director-General and Chief Executive Officer of the Communications Commission of Kenya (CCK). He holds an M.A in Development Economics from Dalhousie University, Canada, a B.A in Economics from the University of Nairobi, Kenya, and a Postgraduate Certificate in Telecommunications Regulation from the University of Westminster, United Kingdom (UK). Mr. Njoroge was appointed to the position on 21st July 2008.

Dr. Bitange Ndemo, EBS - Permanent Secretary, Ministry of Information and CommunicationsDr. Bitange Ndemo is the Permanent Secretary in the Ministry of Information and Communications. He holds a PhD in Industrial Economics from the University of Sheffield in the UK, an MBA and Bachelor’s degree in Finance and Accounting from the University of Minnesota.

Mr. Joseph Kanja Kinyua, CBS - Permanent Secretary, Ministry of FinanceMr. Joseph K. Kinyua is the Permanent Secretary in the Ministry of Finance. He holds Bachelor’s and Master’s degrees in Economics from the University of Nairobi.

Mr. Francis T. Kimemia, CBS - Permanent Secretary Ministry of State for Provincial Administration & Internal SecurityMr. Kimemia is the Permanent Secretary in the Ministry of State in charge of Provincial Administration and Internal Security.

Ms. Alice Munyua – DirectorMs Munyua holds an M.A. in Social Communications from the Pontifical Gregorian University in Rome, Italy, and has also trained in gender mainstreaming, Internet law and negotiation skills at various reputable institutions. She joined the CCK Board

on 11th May 2005 and her second three-year term ended on 10th May 2011.

Mr. Kariithi Njogu – DirectorMr Kariithi holds two MSc. degrees in Human Biology and in Management and Organization Development from Loughborough University of Technology in the UK. He is serving his second term in the CCK Board, which he joined on 1st October 2006.

Ms. Eunice Maranya-Ombati – DirectorMs. Maranya-Ombati holds an MBA from USIU-San Diego and a BSC in Agriculture from University of Nairobi. She was appointed to the CCK Board on 19th November 2007 for a three-year term which ended on 30th October 2010.

Mr. Joe Kamau – DirectorMr. Joe Kamau holds an MBA in Finance from William Paterson University, USA, and a Bachelor of Business Administration of the University of Nairobi. He also has done various postgraduate courses in International Business. Mr. Kamau was appointed to the CCK Board on 19th November 2007 for a three-year term which ended on 30th October 2010.

Mr. Matei Mulili Ndeti – Director Mr. Ndeti holds a Msc. in Electrical Engineering from North Carolina A&T State University, USA, and a Bsc. in Systems Engineering from Wright State University in the USA. He was appointed to the CCK Board on 7th November 2008 for a three-year term.

Mr. Aloys .O. Ang’asa – Director Mr. Ang’asa holds a B.Ed (Economics) and MSc (Agricultural Economics) from the University of Nairobi. He has worked in the communications sector in various capacities for over 30 years and was appointed to the CCK Board on 21st February 2011 for a three-year term.

Dr. Monica Kerretts-Makau – Director Dr. Monicah Kerretts-Makau holds a Doctoral degree in Policy and Regulation with specialization in the Telecom sector from the University of New South, Wales, Sydney, Australia, an MSc in Business and Information Technology from Salford University – Greater Manchester in the UK, and a BA in Communications (Major) Cum Laude Honors from Daystar University, Kenya. She was appointed to the CCK Board on 21st February 2011 for a three-year term.

PROFILES OF CCK BOARD MEMBERS6

Mr. Peter Ldhituachi Simani - DirectorMr. Peter Ldhituachi Simani holds a Bachelor of Laws degree from the University of Nairobi, Diploma in Law from the Kenya School of Law and a Certificate of Proficiency in French. He is a member of the Law Society of Kenya, Commonwealth Lawyers Association, International Bar Association, International Commission of Jurists and the Association of European Lawyers. He was appointed to the CCK Board on 21st February 2011 for a three-year term.

Mr. Shakaba Chiboli Induli, MBS – Alternate DirectorMr. Shakaba Chiboli is the Director of Administration in the Ministry of Finance. He holds a Bachelor of Arts ( B.A. Hons) degree in Political Science, Literature and Linguistics from the University of Nairobi and a Master in Public Administration ( MPA) from Harvard University. He is the alternate Director to the Permanent Secretary in the Ministry of Finance.

Mr. Henry M. Mungasia – Alternate DirectorMr. Henry M. Mungasia is the Deputy Secretary in the Ministry of Information and Communications. He is a Bachelor of Arts ( Hons) graduate of the University of Nairobi. Mr. Mungasia has undertaken courses in Advanced Public Administration (APA) and in National Defence at the Kenya Institute of Administration and the National Defence College respectively. He is the alternate Director to the Permanent Secretary in the Ministry of Information and Communications.

Mr. John Omo – Commission SecretaryMr. John Omo holds a Master of Laws degree from the University of Sheffield, UK, and a first degree in Law from the University of Nairobi. He is the Secretary to the Board and Head of the Legal Affairs Division at CCK.

Francis W. Wangusi – Ag. Director GeneralMr. Wangusi holds a Master of Space Science (Satellite Communications) from the International Space University, France, and a Bachelor of Technology (Telecoms Engineering) from the University of Rome, Italy. He also holds a Chartered Engineering Certificate from the Engineering Council, United Kingdom. He was appointed to the position of Ag. Director General of CCK in August 2011.

7CCK ANNUAL REPORT 2010-2011

CHAIRMAN’SOVERVIEW

We facilitate access to communications services

through enabling regulation and catalyze the country’s

socio-economic development.

Hon. Eng. Philip O. OKundi, EBS, HSC

Chairman’s Overview

On behalf of the Board of Directors, I am greatly honoured to present to you the Commission’s annual report for the year ended 30th June 2011 as required under Section 22(1) of the Kenya Information and Communications Act, CAP 411A.

It has been yet another year of considerable achievement and progress in our quest to facilitate access to communications services through enabling regulation and catalysing the country’s socio economic development. The ICT sector has been driving economic growth over the last decade and is poised to continue doing so in the coming years.

The pace of growth in the ICT sector continued to surge during the year review. The mobile telecommunications subsector registered a 25% growth in service subscription to record 25.2million subscribers by 30th June 2011 up from 20.1 million the previous year.

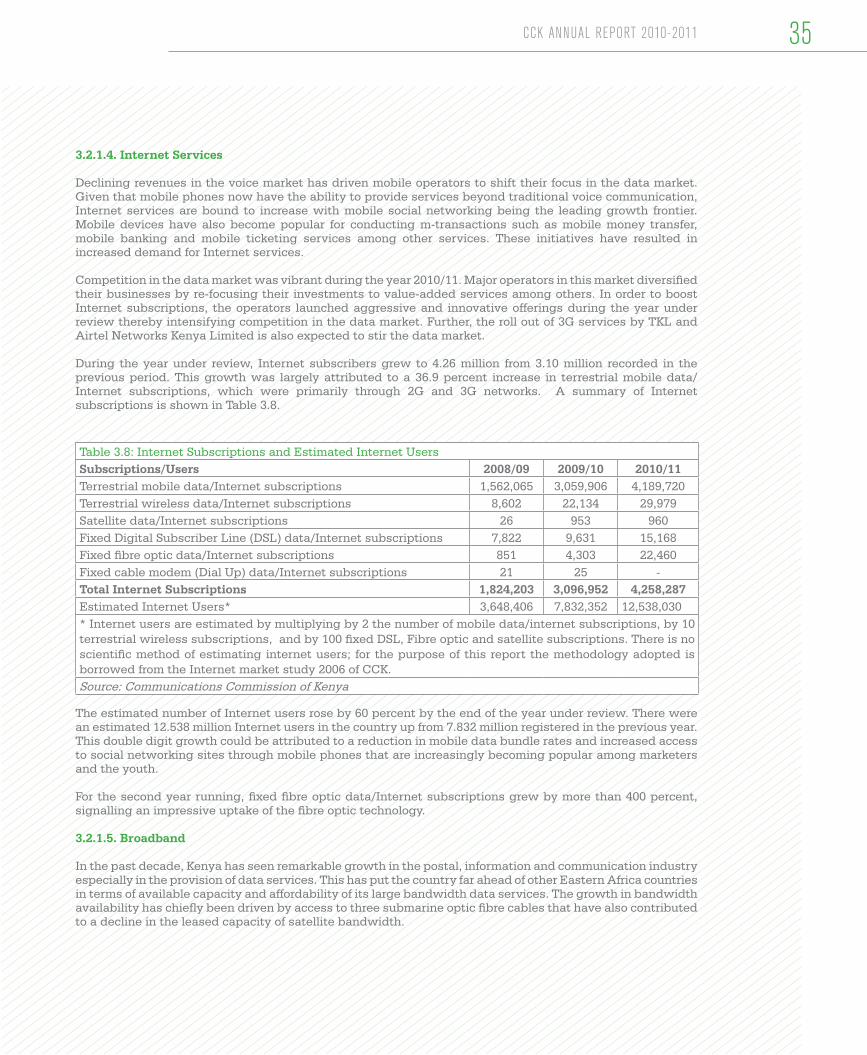

The availability of the three sub-marine fibre optic cables has resulted in increased Internet speeds and amount of broadband available for users at reduced cost. The cables have provided numerous investment opportunities in the country and present great prospects for spurring economic growth. As at 30th June 2011, there were an estimated 12.538 million Internet users in the country up from 7.832 million the previous year.

To promote effective competition in the mobile sub-sector, the Commission developed guidelines on the implementation of Mobile Number Portability (MNP), paving way for implementation of the service in the country. The MNP service went live on 1st April 2011, according mobile service consumers the flexibility and convenience to retain subscriber numbers upon switching service providers.

During the year under review, the financial services sector adopted ICT-based innovations resulting in increased competition and efficiency gains. Mobile money transfer service offered by the four mobile networks and two of the licensed Content Service Providers (CSPs) has revolutionized the banking industry in Kenya, considerably reducing transaction costs and deepening financial inclusion. The country is now recognized globally as the innovation hub in the mobile finances market.

During the year under review, the Commission reviewed and updated the Network Cost Study, resulting in further reduction in interconnection rates for mobile, fixed and fixed transit termination. Subsequently, there has been considerable reduction of retail tariffs both for voice services and SMS, which has resulted in a significant increase in minutes of use on the mobile networks in the country.

Following the expansion of the mandate of the Commission vide the Kenya Communications Act, CAP 411A, the Commission commenced implementation of the Kenya Communications (Broadcasting)

Regulations, 2009. During the year under review, the Commission developed Broadcasting Guidelines, the Broadcasting Code of Practice and licensing framework for broadcasting services. The new regulatory framework shall be used to streamline and infuse order into the broadcasting industry.

In addition, the Commission continued coordinating seamless migration from analogue to digital TV broadcasting. The transition to digital TV broadcasting, scheduled to be completed by 2012, is expected to increase efficiency in the use of radio spectrum, increase content plurality and diversity and provide high quality digital signals. To enhance competition in the digital TV signal distribution in Kenya, the Commission commenced the process of licensing two additional national digital TV broadcasting signal distributors. The Commission also developed minimum technical specifications for DVB-T2 set-top boxes that will be used to access digital TV broadcast services.

In line with the provisions of the Kenya Information and Communications (Universal Access and Service) Regulations, 2010, the Commission set 1st January 2011 as the commencement date of receipt of contributions to the Universal Service Fund (USF) from the commercial licensees. In order to achieve transparency and promote accountability in the management and administration of the USF, the Commission initiated the development of an operations manual. The manual will provide the administrative framework and guidelines on processes such as selection criteria for USF projects and Fund disbursement mechanisms.

On the international scene, Kenya continued participating actively in relevant meetings and forums hosted by international organizations to which the country is affiliated. As a result of the goodwill cultivated over the years, the country was re-elected to the ITU Council and elected to the ITU Radio Regulations Board (RRB) during the ITU Plenipotentiary Conference 2010 held in Mexico. The Commission will continue to engage actively at the international arena with a view to ensuring that our regulatory regime in attuned to the international treaties and global best practice.

In conclusion, I would like to thank the Government, our stakeholders and the general public for the overwhelming support during the year. I would also like to commend the management and staff for their diligence and commitment under the stewardship of the Director-General. My deep appreciation is also extended to my fellow Board members for the invaluable guidance they have extended to the Commission’s leadership.

Hon. Eng. Philip OKundi, EBS, HSCChairman

9CCK ANNUAL REPORT 2010-2011

DIRECTOR GENERAL’SWORD

We facilitate access to communications services

through enabling regulation and catalyze the country’s

socio-economic development.

Francis W. Wangusi

Director General’s Word

The year under review witnessed positive growth in the postal, information and communication sector as an essential part of business and social life in the country. The growth was in tandem with the growth of the Kenyan economy which expanded by 5.6 percent in 2010 compared to 2.6 percent in 2009. The improved performance was as a result of consistent macroeconomic stability, increased credit to the private sector, low inflationary pressure and improved weather conditions.

The Transport and Communications sector recorded a 5.9 percent growth compared to 6.4 percent in 2009. The total output value for the sector grew by 9.5 percent to KES 594.6 billion in 2010. The telecommunications industry continued to post considerable growth spearheaded mainly by the mobile telephony segment which saw subscriber growth register a 15.9 percent increase. Overall, however, the postal and telecommunications sub-sector experienced a marginal decline in percentage contribution to GDP to 2.5 down from 2.6 in 2009.

Rapid changes and developments in Information and Communications Technology (ICT) have blurred the traditional lines between specific technologies and rendered technology based licensing untenable. With this in mind, the Commission introduced Unified Licensing Framework (ULF) in 2007, allowing licensees the benefits of expanded scope and flexibility. During the year under review, the number of licensees under the ULF increased to 844 from 610 the previous year, representing 38.4 percent growth.

The mobile market segment continued to thrive during the year under review. Mobile subscriptions grew significantly to stand at 25.2 million subscribers from 20.1 million recorded the previous year. This represented a growth of 25.6 percent.

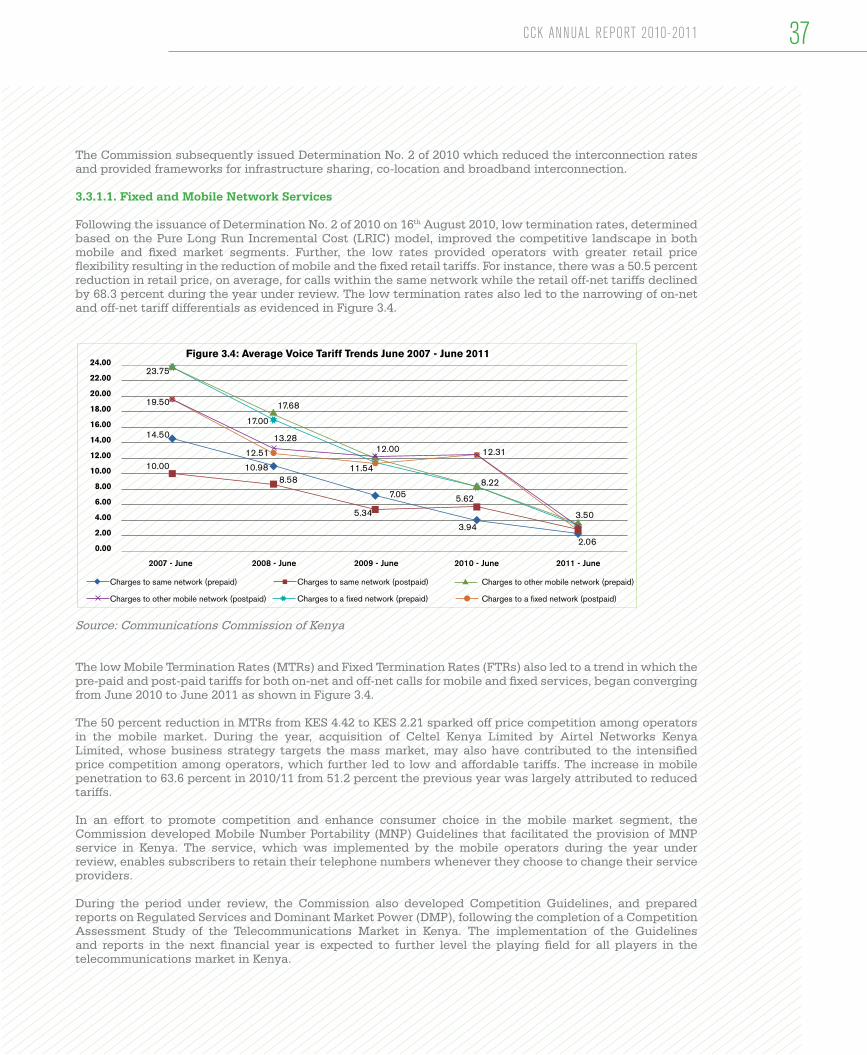

Following the review of the mobile termination rates, the operators reduced both on-net and off-net tariffs in a bid to attract and retain customers on their respective networks. Mobile penetration increased from 51.2 percent in June 2010 to 63.6 percent as at 30th June 2011. This penetration rate was above the African penetration rate estimated by the International Telecommunication Union (ITU) to be 41 percent during the same period. During the year under review, mobile the number of money service subscribers were at 17,395,727 up from 10,615,386 the previous year, with Safaricom’s M-Pesa being the largest system, accounting for 82.4 per cent of mobile money transfer service subscriptions.

During the year under review, the Commission introduced Mobile Number Portability services which kicked off on 1stApril 2011. ‘Number yangu milele’ was the tagline of the media consumer awareness campaign that was funded and coordinated by the Commission. The campaign was aimed at sensitizing consumers on the porting procedures and the associated benefits. Using the porting service, consumers have the freedom of moving from one network to another while retaining their individual subscriber numbers.

Internet use in the country remained on an upward trend as more Kenyans relied on the service to conduct business and social activities. As at 30th June 2011, there were an estimated 12.538 million Internet users in the country up from 7.832 million the previous year. The growth in the data market is attributed to three mobile operators having rolled out 3G services. Mobile data/Internet subscriptions continued to dominate the Internet market, accounting for 98.4 percent of the total subscriptions during the period under review.

Demand for both television and radio frequencies remained high during the year under review. The Commission’s mandate in respect to regulating the broadcasting sector is relatively new having come under our ambit in 2009. To better understand competition within the sector, the Commission, during the year under review, requested for proposals for a competition study of the broadcasting sector in Kenya. The findings will be presented in the next financial year.

Further, the Commission developed a regulatory framework for the broadcasting sector, including licensing procedures as well as the Broadcasting Code and Broadcasting Guidelines. Migration to digital television is on course and the Commission continued to actively take part in the process by providing secretariat and logistical support to the Digital Television Committee (DTC). In the wake of the adoption of DVB T2 as the technology of choice in the migration to digital TV broadcasting, the Commission published the minimum technical specifications for the DVB-T2 standard and commenced the process of licensing two additional national digital TV broadcast signal distributors.

In the postal/courier sub-sector, the Commission licensed 17 new operators during the year under review, increasing the total number of licensees to 176 from 159 the previous year. The increase was attributed to enhanced monitoring

11CCK ANNUAL REPORT 2010-2011

and enforcement as well as sustained public awareness campaigns on the regulatory requirements. Intra-country postal/courier operators remained the largest category of operators at 99 accounting for 56.3 percent of the total number of licensed operators. The Commission also hosted the 3rd Postal/Courier Stakeholders Forum which emphasised the need for the postal/courier sector to adopt ICTs in their businesses.

The Commission continued to empower and equip consumers with skills and knowledge to enable them make better decisions regarding postal, information and communications services. During the year under review, the Commission developed consumer advisory materials and distributed them through universities, Mombasa International Show, Nairobi International Trade Fair and during other corporate events. In addition, the Commission engaged child online protection stakeholders in a workshop whose findings will further enrich the consumer advisory information.

The Kenya Information and Communications Act, Cap 411A, vests the Commission with the responsibility of managing and administering the Universal Service Fund (USF). During the year under review, the Commission undertook a number of initiatives aimed at achieving universal access to postal, information and communications services. These initiatives included the institutionalization and operationalization of the USF, identification of access gaps through studies and the implementation of universal access projects on a pilot basis.

During the year under review, the Commission continued to build capacity for its employees with 92.7 percent of the workforce being trained compared to 80.3 percent the previous year. The Commission staff were further sensitized on Behaviour Change and Prevention of Mother to Child Transmission of HIV/AIDS as well as on provision of services to Persons with Disabilities (PWDs) and Disability Mainstreaming. Capacity in the industry was also increased through courses offered in collaboration with partners such as International Telecommunication Union (ITU), Commonwealth Telecommunications Organization (CTO) and Universal Postal Union (UPU). Further, the Commission facilitated training for institutions and schools for PWDs under its Universal Service programmes.

During the year under review, the Commission upgraded its Quality Management System to the ISO 9001:2008 Standard. Awareness training for all staff was carried out following the upgrade.

As a responsible corporate citizen, the Commission carried out a number of CSR activities. During the festive season, the Commission spread cheer by giving food supplies and basic necessities to Shangilia Mtoto wa Africa Children’s Home, Muthaiga North Hospital (formerly Mathari Hospital) and the Missionaries of Charity Mother Teresa’s Home. The Commission also sponsored the Mater Heart Run, Sports Personality of the Year Award (SOYA) and Kalasha Awards.

The Commission continued to represent the Government of Kenya in international and regional meetings organised by affiliated intergovernmental organizations dealing with postal, and ICT matters. As the designated Government representative to affiliated international and regional bodies dealing with ICTs, the Commission met all its obligations to these organizations. The Commission also hosted a number of meetings, conferences, study group meetings and workshops in conjunction with the organizations affiliated to it. Most notable was the hosting, for the first time in Africa, of the UPU Conference in September 2010.

The year under review has been one of accomplishment for the postal and ICT industry. These achievements which would not have been possible without the Commission’s dedicated staff, partners and investors. I also wish to express my appreciation to the Commission’s Board of Directors and the Ministry for Information and Communications for their continued support.

Francis W. WangusiAg. Director General

DIRECTOR GENERAL’S WORD12

Corporate Governance

Corporate governance is critical to the success or failure of any organization. The Commission’s governance is vested in its Board of Directors whose powers are set out in the Kenya Information and Communications Act, CAP 411A. The Board is tasked, under the Act, with the twin functions of decision making and oversight.

The Board acknowledges the importance of good corporate governance in building a competitive postal and ICT industry, and enhancing stakeholder confidence in the regulatory environment. To this end, the Board provides the requisite leadership and strategic direction for the fulfilment of the Commisiion’s statutory mandate.

The Board conducts its business in accordance with best regulatory practice anchored in principles of accountability and transparency as well as compliance with relevant laws and regulations. In this regard, the Commission discharges its mandate based on strong corporate governance principles through application of high and consistent ethical standards.

The Board of Directors

1. Oversight Role of the Board of Directors In fulfilling its mandate, the Board of Directors is guided by a Board Charter which outlines its functions and responsibilities. The Charter outlines, among others, the Board’s obligations, Directors’ Code of Conduct and Ethics, and establishment of Board Committees.

The principal role and responsibility of the Board is to establish long-term goals of the Commission and ensure that effective plans are developed and implemented within a commonly agreed organizational structure. This entails among others:

(i) Exercising leadership, integrity and judgement in directing the Commission;

(ii) Setting the vision, mission and values of the Commission;

(iii) Developing strategies to achieve the Commission’s mandate;

(iv) Determining key performance indicators of the Commission, setting targets and monitoring performance;

(v) Ensuring that internal structures and policies are in place;

(vi) Identifying and managing key risk areas; and (vii) Ensuring preparation of annual financial

statements and reports, and disclosure of information to stakeholders.

2. Composition of the Board

During the year under review, the Commission’s Board comprised nine Directors, who possess knowledge and experience in matters relating to postal, broadcasting, radiocommunications, Information Technology, telecommunications, computer science, economics, ICT regulation and consumer protection.

The Director General is the Chief Executive Officer of the Commission and an ex-officio member of the Board. The Director General, therefore, provides the link between the Board of Directors and Staff.

3. Board Meetings

The Board is required to meet at least four times a year. Additional Board meetings are convened when necessary. During the year under review, the Board held 15 meetings.

4. Board Committees

Section 9 of the Kenya Information and Communications Act, Cap 411A, empowers the Board to form standing or ad hoc Committees and to delegate the exercise of any of its powers and performance of its functions or duties to such committees, member, officer, employee or agent of the Commission to enhance efficiency. To this end, the Board has four standing committees namely Finance, Technical, Staff and Audit committees.

The Finance Committee is responsible for, among others, accounting and financial management policies of the Commission. This Committee met four times in the year under review.

13CCK ANNUAL REPORT 2010-2011

The Technical Committee deals with regulatory issues including granting of licences, review of the market structure and regulatory interventions. During the year under review, this Committee met seven times.

The Staff Committee is responsible for development of human resources and related policies and their implementation. This Committee met three times during the year under review.

The Audit Committee reviews internal and external audit reports and recommendations thereof and ensures that appropriate remedial actions are promptly taken by management where necessary. This Committee met four times during the year.

5. Capacity Building

On appointment, Directors of the Board are taken through an induction programme aimed at enhancing their understanding of the Commission, its mandate and the business environment. Directors attend local, regional and international conferences, workshops and benchmark visits to other jurisdictions to gain better insights into global best practices in ICT regulation. The Commission facilitates training on corporate governance and further encourages the Directors to attend relevant training programmes aimed at broadening their knowledge.

During the year under review, the Directors participated in the following local and international training, conferences and exhibitions:

• SevendirectorsweretrainedinstrategicleadershipandchangemanagementattheKenyaInstituteof Administration (KIA), Nairobi;

• TwodirectorsattendedtheInternationalBroadcastingConvention(IBC2010)andExhibitioninAmsterdam, Netherlands;

• Twodirectorsattendedthe5thAnnualInternetGovernanceForuminVilnius,Lithuania;• TwodirectorsparticipatedinthePOST–EXPOandWorldPostalBusinessForuminCopenhagen,

Denmark; and• Twodirectorsattendedthe10thGlobalSymposiumforRegulators(GSR10)inDakar,Senegal.

BOARD OF DIRECTORS14

Organizational Structure

CPR Communication and Public Relations

IT Information Technology

IAS Internal Audit Services

PROC Procurement

CTMA Competition, Tariffs and Market Analysis

FSM Frequency Spectrum Management

LCS Licensing, Compliance and Standards

HRA Human Resource and Administration

F&A Finance and Accounts

CA Consumer Affairs

LA Legal Affairs

SP&B Special Projects and Broadcasting

BOARD

DIRECTOR GENERAL

ASSISTANTDIRECTOR

CPR

ASSISTANTDIRECTOR

IT

ASSISTANTDIRECTOR

IAS

MANAGERPROC

DIRECTORCTMA

DIRECTORFSM

DIRECTORLCS

DIRECTORHRA

DIRECTORF&A

DIRECTORCA

DIRECTORSP&B

COMMISSIONSECRETARY

LA

Commission’s Mandate

The Communications Commission of Kenya is the regulatory authority for the communications sector in Kenya. Established in 1999 by the Kenya Information and Communications Act, (KICA) No. 2 of 1998, the Commission’s initial mandate was regulation of the telecommunications and postal/courier sub-sectors, and the management of the country’s radiofrequency spectrum.

In recognition of the rapid changes and developments in technology which have blurred the traditional distinctions between telecommunications, Information Technology (IT) and broadcasting, the Government in January 2009 enacted the Kenya Communications (Amendment) Act, 2009. This statute enhanced the regulatory scope and jurisdiction of the Commission and effectively transformed it to a converged regulator. The Commission is now responsible for facilitating the development of the information and communications sectors (including broadcasting, multimedia, telecommunications and postal services) and electronic commerce through proper regulation.

The Kenya Communications Act, 1998, and the Kenya Communications (Amendment) Act, 2008, have been amalgamated into the Kenya Information and Communications Act, CAP 411A. This piece of legislation removes barriers to electronic transactions and introduces penalties to cybercrimes with the aim of minimizing fraud in electronic commerce. It also enhances some penalties for offences committed under the Act. It formally recognizes Internet domain resources within the regulatory framework. In addition, the Act provides for the establishment of Universal Service Fund (USF) to support widespread access to ICT services. It also establishes a Universal Service Advisory Council to manage and administer the Fund. The Act also enhances the competition framework in the ICT sector.

The responsibilities of the Commission include:

• Licensingallsystemsandservicesinthecommunicationsindustry,includingtelecommunications,postal/courier and broadcasting.

• Managingthecountry’sfrequencyspectrumandnumberingresources.• Facilitatingthedevelopmentofe-commerce.• Typeapproving/acceptingcommunicationsequipmentmeantforuseinthecountry.• Protectingconsumerrightswithinthecommunicationsenvironment.• Managingcompetitioninthesectortoensurealevelplayinggroundforallplayers.• Regulatingretailandwholesaletariffsforcommunicationsservices.• ManagingtheUniversalServiceFund.• Monitoringtheactivitiesoflicenseestoenforcecompliancewiththelicencetermsandconditions

as well as the law.

The Kenya Communications Regulations, 2001, were reviewed in 2009/2010 to bring them up to date with technological developments and changes in the policy and law. The Kenya Information and Communications Regulations, 2010, clarify and expound on the Act and cover the following areas: Electronic Transactions, Universal Access and Service, Consumer Protection, Dispute Resolution, Radio Communications and Frequency Spectrum Management, Licensing and Quality of Service, Postal and Courier Services, Fair Competition and Equality of Treatment, Broadcasting, Compliance Monitoring, Inspection and Enforcement, Type Approval, Tariff, Interconnection and Provision of Fixed Links, Access and Numbering.

COMMISSION’S MANDATE16

CHAPTER 1Macro-Economic Environment

1.1 Global Economy

During the period under review, the global economy continued to recover as the world Gross Domestic Product (GDP) grew by 4.6 percent in 2010 compared to a contraction of 1.0 percent recorded in 2009. The recovery was as a result of austerity measures put in place to counter the effects of the recession which commenced in 2008 coupled with stimulus policies; a rebound in demand for consumer goods; and increased trade. Emerging and developing economies continued with upward growth driven by vibrant domestic demand while advanced economies recovered and experienced positive growth in 2010 as a result of a recovering financial sector and improved labour market conditions. However, this growth is expected to decline in 2011 as a result of gradual tightening of monetary and fiscal policies; rising commodity prices; political turmoil in North Africa and Middle-East and the natural disaster and nuclear catastrophe in Japan.

In Sub-Saharan Africa (SSA), the real GDP is estimated to have expanded by 5.0 percent in 2010 compared to 2.8 percent in 2009. This was attributed to favourable economic climate, increased commodity demand from emerging economies and increased trade. The abundance of harvests led to a deceleration in consumer prices in SSA to stand at 7.5 percent compared to 10.4 percent in 2009. In the East African Community (EAC), the total real GDP for the five EAC Member countries increased by 5.4 percent in 2010 compared to 4.8 percent in 2009.

1.2 Global Postal, Information and Communication Technology Industry

The rapid uptake of mobile telephony, even in remote locations of low-income countries, has radically increased the potential for Information and Communication Technologies (ICTs) to play a constructive role in the fight against poverty. The scope for ICTs to improve the lives of the poor has expanded thanks to the emergence of many new and innovative applications and services, especially those linked to mobile telephony. The penetration level of the mobile telephony in the developing countries is much higher than it is for other competing services, such as fixed telephony, Internet, and broadband.

Traditional fixed telephony is facing growing economic pressure in finding new income streams as consumers take up competing wireless and cable

connections to access more and more services. In some countries, including Portugal and the United States, traditional fixed line operators have responded by investing in fibre access technologies and have seen their revenues increase as a result.

The Internet arena is expected to transform from one dominated by advanced countries to one where emerging economies are predominant. As more businesses and citizens in these economies go online and connectivity levels approach those of advanced markets, the global shares of Internet activity and transactions will increasingly shift toward the former. With the improvement in the speed and quality of broadband and the introduction of Web 2.0 technologies and applications, economic and social dynamics across the world are expected to change dramatically. These are anticipated to have massive implications in terms of productivity gains and new opportunities for individuals and businesses. This inflection point presents an opportunity for economies all over the globe to take decisive steps to gain competitive advantage that can be derived from widespread use of broadband networks.

ICT markets, such as international gateway, wireless local loop and the 3G markets, around the world are generally becoming more competitive. However, the fixed line market continues to lag behind other ICT markets in terms of competitiveness. Nevertheless, there has been an increase in the percentage of countries that have opened their fixed line markets to competition, although teledensity has remained relatively flat over the past 10 years. This stands in contrast to the exponential growth in mobile penetration over the same period and the continued growth of mobile broadband services, (Trends in Telecommunication Reform, 2010/11).

While the average penetration level of mobile broadband services was 5.4 subscriptions per 100 inhabitants in developing countries, it is 10 times higher in the developed world, at 51.1 per 100 inhabitants. The ongoing deployment of higher speed Third Generation (3G) mobile broadband networks such as Worldwide Interoperability for Microwave Access (WIMAX) and more recently High Speed Packet Access (HSPA+) and Long Term Evolution (LTE) systems will certainly contribute to greater levels of mobile broadband services uptake worldwide. Regulatory measures taken in selected countries such as spectrum re-farming (reallocation of a frequency band for a different use) and the licensing of 3G services, will also contribute to the

CHAPTER 1: MACRO-ECONOMIC ENVIRONMENT

Macro-economic Environment

18

accelerated growth of mobile broadband penetration. These regulatory measures have been complemented at the industry level by a move towards developing Next Generation Networks such as Fourth Generation (4G).

ICT revolution and market liberalization has had a considerable impact on the postal and courier industry. This has resulted in the reduction of postal monopolies and increased competition in this market segment. This has also convinced many governments that public postal operators must have autonomy and financial viability to compete effectively while at the same time providing universal postal service. To this end, governments have gone on to sponsor regulatory reforms and targeted investments in the public postal operator. The results of such reforms can be remarkable in terms of improving financial and operational performance and overall contribution to national economic growth.

Growing globalization and falling trade barriers have sparked off competition that goes beyond national postal marketplaces. Globally, many postal operators are taking advantage of more competitive and liberalized international postal services to establish mergers, alliances and joint ventures with their fellow operators and with the private sector. These joint efforts, if properly structured, can utilize the combined strengths of one or more players to produce a comprehensive service that is greater than the sum of its parts. It is noted that access to outside expertise and financing through such cooperative arrangements can be a significant element in rebuilding the postal business in developing countries.

Finally, the rapid advance of electronic Information Technologies poses the greatest threat to the traditional postal world. The increasing demand for faster, more affordable and flexible communications services means that postal services must embrace ICTs, electronic commerce and innovations to remain relevant in the global environment and keep up with today’s customer.

1.3 Local Environment

On the local scene, the economy recorded a growth of 5.6 percent in 2010 compared to 2.6 percent recorded in 2009. The improved performance was as a result of consistent macroeconomic stability, increased credit to the private sector, low inflationary pressure and improved weather conditions. The country also benefited from improved prices of the main exports and increased remittances from abroad as a result the global economic recovery. Despite the political campaigns associated with the 2010 constitutional referendum, business and customer confidence remained largely intact thereby boosting economic growth.

Real Gross Domestic Product (GDP) per capita increased by 2.7 percent from KES 35,470 in 2009 to KES 36,419 in 2010. This can be attributed to varying positive growth in all the sectors of the economy. Electricity and Water Supply, Mining and Quarrying, and Financial Intermediation showed most significant growth during the same period. Key sectors in the economy also performed well, with Agriculture and Forestry posting a significant growth of 6.3 percent in 2010 after two consecutive declines of 4.1 percent and 2.6 percent in 2008 and 2009, respectively.

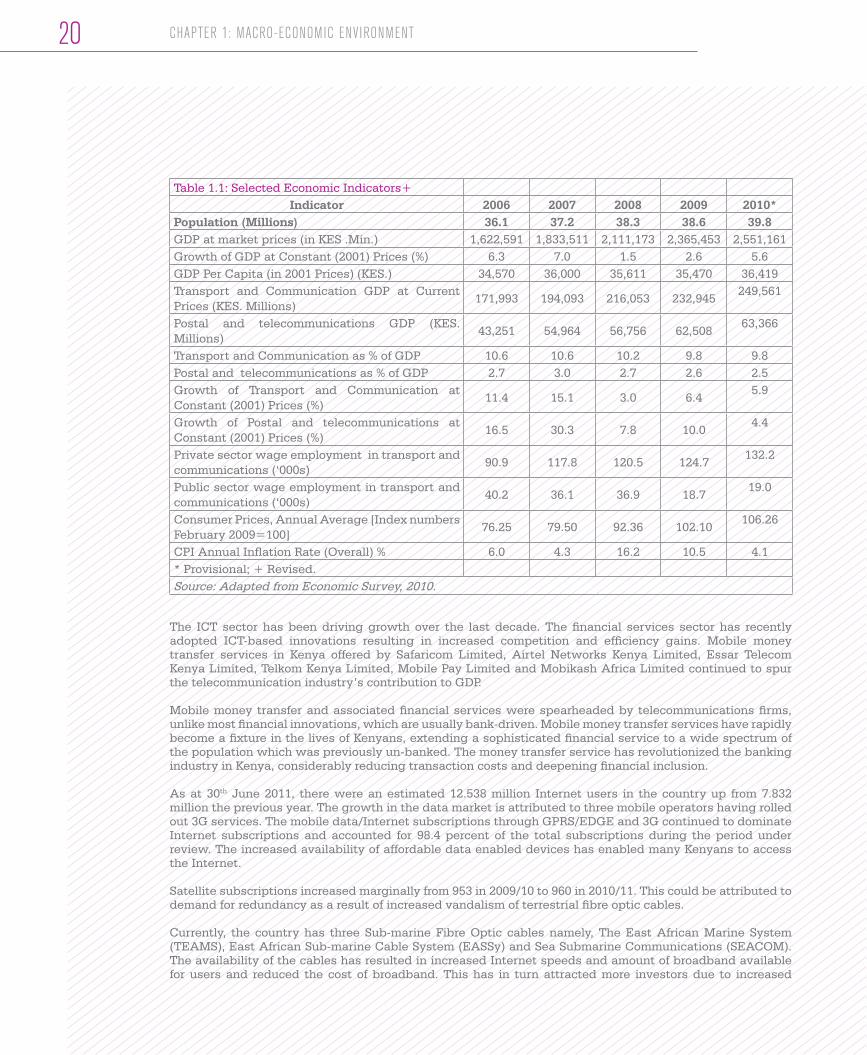

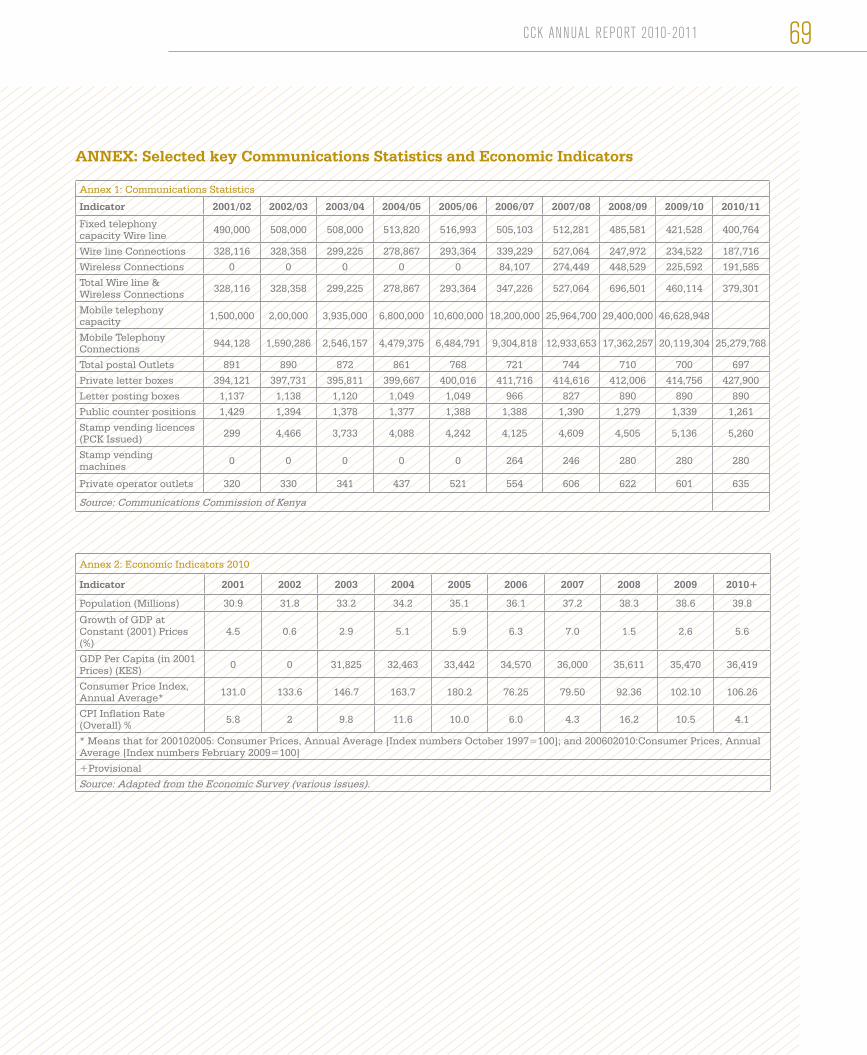

The Transport and Communications sector recorded a 5.9 percent growth compared to 6.4 percent in 2009, with the total output value for the sector growing by 9.5 percent to KES 594.6 billion in 2010. The telecommunications industry continued to post considerable growth spearheaded mainly by the mobile telephony segment which saw subscriber growth register a 15.9 percent increase. Overall, however, the postal and telecommunications sub-sector experienced a marginal decline in percentage contribution to GDP to 2.5 down from 2.6 in 2009. This is shown in Table 1.1.

19CCK ANNUAL REPORT 2010-2011

Table 1.1: Selected Economic Indicators+Indicator 2006 2007 2008 2009 2010*

Population (Millions) 36.1 37.2 38.3 38.6 39.8GDP at market prices (in KES .Min.) 1,622,591 1,833,511 2,111,173 2,365,453 2,551,161Growth of GDP at Constant (2001) Prices (%) 6.3 7.0 1.5 2.6 5.6GDP Per Capita (in 2001 Prices) (KES.) 34,570 36,000 35,611 35,470 36,419Transport and Communication GDP at Current Prices (KES. Millions)

171,993 194,093 216,053 232,945249,561

Postal and telecommunications GDP (KES. Millions)

43,251 54,964 56,756 62,50863,366

Transport and Communication as % of GDP 10.6 10.6 10.2 9.8 9.8Postal and telecommunications as % of GDP 2.7 3.0 2.7 2.6 2.5Growth of Transport and Communication at Constant (2001) Prices (%)

11.4 15.1 3.0 6.45.9

Growth of Postal and telecommunications at Constant (2001) Prices (%)

16.5 30.3 7.8 10.04.4

Private sector wage employment in transport and communications (‘000s)

90.9 117.8 120.5 124.7132.2

Public sector wage employment in transport and communications (‘000s)

40.2 36.1 36.9 18.719.0

Consumer Prices, Annual Average [Index numbers February 2009=100]

76.25 79.50 92.36 102.10106.26

CPI Annual Inflation Rate (Overall) % 6.0 4.3 16.2 10.5 4.1* Provisional; + Revised.Source: Adapted from Economic Survey, 2010.

The ICT sector has been driving growth over the last decade. The financial services sector has recently adopted ICT-based innovations resulting in increased competition and efficiency gains. Mobile money transfer services in Kenya offered by Safaricom Limited, Airtel Networks Kenya Limited, Essar Telecom Kenya Limited, Telkom Kenya Limited, Mobile Pay Limited and Mobikash Africa Limited continued to spur the telecommunication industry’s contribution to GDP.

Mobile money transfer and associated financial services were spearheaded by telecommunications firms, unlike most financial innovations, which are usually bank-driven. Mobile money transfer services have rapidly become a fixture in the lives of Kenyans, extending a sophisticated financial service to a wide spectrum of the population which was previously un-banked. The money transfer service has revolutionized the banking industry in Kenya, considerably reducing transaction costs and deepening financial inclusion.

As at 30th June 2011, there were an estimated 12.538 million Internet users in the country up from 7.832 million the previous year. The growth in the data market is attributed to three mobile operators having rolled out 3G services. The mobile data/Internet subscriptions through GPRS/EDGE and 3G continued to dominate Internet subscriptions and accounted for 98.4 percent of the total subscriptions during the period under review. The increased availability of affordable data enabled devices has enabled many Kenyans to access the Internet.

Satellite subscriptions increased marginally from 953 in 2009/10 to 960 in 2010/11. This could be attributed to demand for redundancy as a result of increased vandalism of terrestrial fibre optic cables.

Currently, the country has three Sub-marine Fibre Optic cables namely, The East African Marine System (TEAMS), East African Sub-marine Cable System (EASSy) and Sea Submarine Communications (SEACOM). The availability of the cables has resulted in increased Internet speeds and amount of broadband available for users and reduced the cost of broadband. This has in turn attracted more investors due to increased

CHAPTER 1: MACRO-ECONOMIC ENVIRONMENT20

international connectivity and created employment opportunities in the country.

The liberalized broadcasting sub-sector remained competitive with increased demand for both television and radio broadcasting frequencies and channels. In an effort to ensure a smooth transition from analogue to digital TV broadcasting, the Commission continued to provide secretariat services, budgetary and logistical support to the Digital Television Committee (DTC). The Commission also meet the cost of consumer awareness campaign on digital migration.

The Commission also commenced the process of licensing additional broadcast signal distributors. It also developed material for consumer education campaign, and published the minimum technical specifications for the Digital Video Broadcast – Terrestrial 2nd Generation (DVB-T2) standard. The transition from analogue to digital TV broadcasting scheduled to be completed by 2012 is expected to increase efficiency in the use of radio spectrum, increase content plurality and diversity and provide high quality digital signals.

Within the EAC, Kenya is largest economy contributing 40 percent to EAC’s total GDP. The coming into force of the EAC Common Market protocol in July 2010 widened the market and has helped Kenya expand trade with other EAC Member countries. The Common Market is further expected to boost trade within the region by removing tariff barriers to trade.

Economic performance indicators for the 2011/12 point to a possibility of suppressed level of economic activities as a result of escalating oil prices arising from political unrest in oil producing nations of North Africa and the Middle East; insufficient rains and drought; high food prices; and instability and volatility in the foreign exchange market.

The growth momentum experienced in 2010/11 is, therefore, likely to be slowed down by the aforementioned factors and as a result, the domestic economy is projected to grow by between 3.5 percent and 4.5 percent in the 2011/12. This growth is expected to be driven by successful implementation of the constitutional reforms which will send positive signals to the private sector and, therefore, boost business and investor confidence; large EAC common market and increased investment in infrastructure. The EAC common market is likely to increase its talent pool and, thus, could evolve into an ICT hub for the Continent.

21CCK ANNUAL REPORT 2010-2011

CHAPTER 2Management of Scarce Resources

The Commission is mandated to manage scarce radio frequency spectrum and numbering resources, which are essential for the provision of postal, information and communications services. As the postal, information and communications sector expanded, the Commission continued to receive and respond to the changing demands for public resources.

2.1 Frequency Management

The Commission plans, licenses, assigns, monitors, and coordinates the usage of the scarce frequency spectrum resources to ensure efficient utilization. During the year under review, the Commission assigned frequencies for various systems/services as follows:

2.1.1. Fixed Links

The Commission assigned a total of 1,994 frequencies to various operators for deployment of new links to facilitate provision of diverse communications services. A total of 229 fixed links were decommissioned mainly due to increased availability of optic fibre networks. Overall, the number of fixed links increased by 1,765, mainly as a result of expansion of mobile networks and increased vandalism of the core fibre network largely in urban areas. These are shown in Table 2.1.

Table 2.1: Fixed Links Frequency

BandNumber of new links

No. of decommissioned links

Growth in the No. of fixed links

Cumulative No. of fixed links

2009/10 2010/11 2009/10 2010/11 2009/10 2010/11 2010/11400MHz 28 0 0 0 28 0 01.5 GHz 0 0 70 0 -70 0 02GHz 0 0 6 0 -6 0 0

2.5GHz 0 0 4 0 -4 0 04GHz 0 0 11 0 -11 0 06GHz 8 2 48 0 -40 2 105

7/8GHz 208 382 143 50 65 332 1,16210.5GHz 0 0 9 0 -9 0 011 GHz 9 0 8 0 1 0 013GHz 347 144 207 71 140 73 73615GHz 157 1,181 1 86 156 1,095 2,24218GHz 0 2 2 1 -2 1 823GHz 63 232 3 21 60 211 32138GHz 3 51 0 0 3 51 43Total 823 1,994 512 229 311 1,765 4,617

Source: Communications Commission of Kenya

23CCK ANNUAL REPORT 2010-2011

Management of Scarce Resources

24

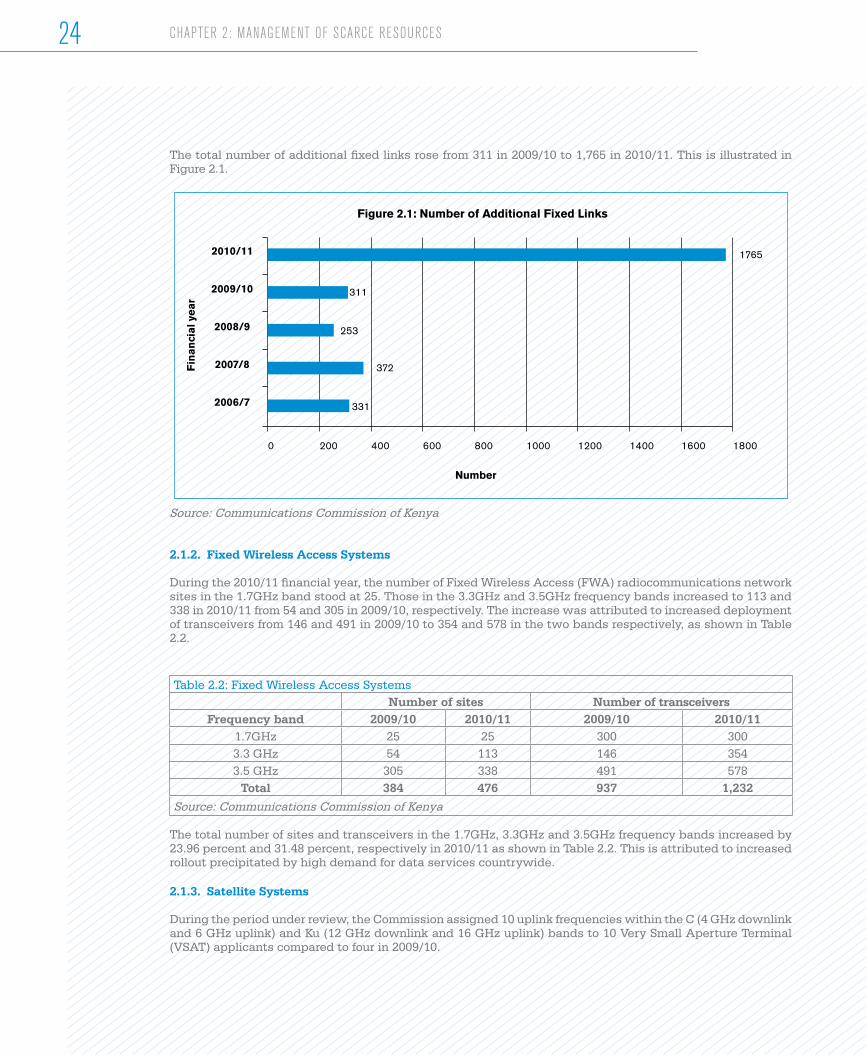

The total number of additional fixed links rose from 311 in 2009/10 to 1,765 in 2010/11. This is illustrated in Figure 2.1.

2006/7

2007/8

2008/9

2009/10

2010/11

Figure 2.1: Number of Additional Fixed Links

Fin

anci

al y

ear

Number

1765

311

253

372

331

0 200 400 600 800 1000 1200 1400 1600 1800

Source: Communications Commission of Kenya

2.1.2. Fixed Wireless Access Systems

During the 2010/11 financial year, the number of Fixed Wireless Access (FWA) radiocommunications network sites in the 1.7GHz band stood at 25. Those in the 3.3GHz and 3.5GHz frequency bands increased to 113 and 338 in 2010/11 from 54 and 305 in 2009/10, respectively. The increase was attributed to increased deployment of transceivers from 146 and 491 in 2009/10 to 354 and 578 in the two bands respectively, as shown in Table 2.2.

Table 2.2: Fixed Wireless Access SystemsNumber of sites Number of transceivers

Frequency band 2009/10 2010/11 2009/10 2010/111.7GHz 25 25 300 3003.3 GHz 54 113 146 3543.5 GHz 305 338 491 578

Total 384 476 937 1,232Source: Communications Commission of Kenya

The total number of sites and transceivers in the 1.7GHz, 3.3GHz and 3.5GHz frequency bands increased by 23.96 percent and 31.48 percent, respectively in 2010/11 as shown in Table 2.2. This is attributed to increased rollout precipitated by high demand for data services countrywide.

2.1.3. Satellite Systems

During the period under review, the Commission assigned 10 uplink frequencies within the C (4 GHz downlink and 6 GHz uplink) and Ku (12 GHz downlink and 16 GHz uplink) bands to 10 Very Small Aperture Terminal (VSAT) applicants compared to four in 2009/10.

CHAPTER 2: MANAGEMENT OF SCARCE RESOURCES

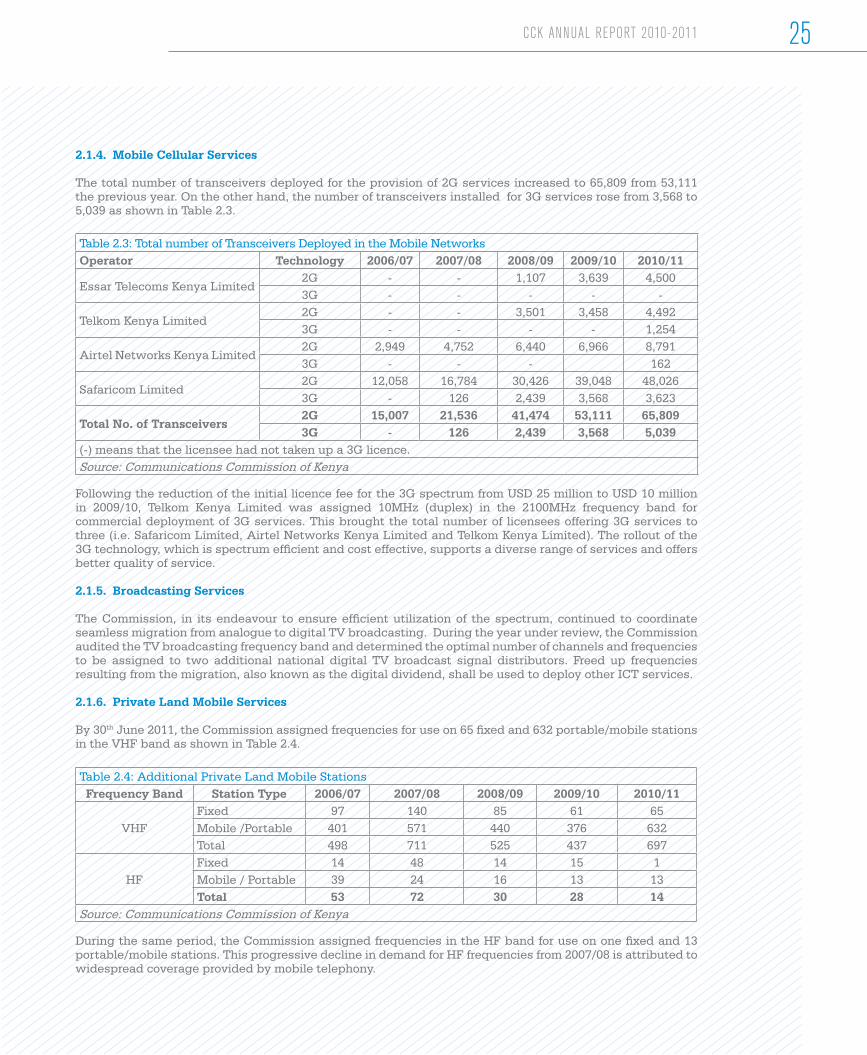

2.1.4. Mobile Cellular Services

The total number of transceivers deployed for the provision of 2G services increased to 65,809 from 53,111 the previous year. On the other hand, the number of transceivers installed for 3G services rose from 3,568 to 5,039 as shown in Table 2.3.

Table 2.3: Total number of Transceivers Deployed in the Mobile NetworksOperator Technology 2006/07 2007/08 2008/09 2009/10 2010/11

Essar Telecoms Kenya Limited2G - - 1,107 3,639 4,5003G - - - - -

Telkom Kenya Limited 2G - - 3,501 3,458 4,4923G - - - - 1,254

Airtel Networks Kenya Limited 2G 2,949 4,752 6,440 6,966 8,7913G - - - 162

Safaricom Limited2G 12,058 16,784 30,426 39,048 48,0263G - 126 2,439 3,568 3,623

Total No. of Transceivers2G 15,007 21,536 41,474 53,111 65,8093G - 126 2,439 3,568 5,039

(-) means that the licensee had not taken up a 3G licence.Source: Communications Commission of Kenya

Following the reduction of the initial licence fee for the 3G spectrum from USD 25 million to USD 10 million in 2009/10, Telkom Kenya Limited was assigned 10MHz (duplex) in the 2100MHz frequency band for commercial deployment of 3G services. This brought the total number of licensees offering 3G services to three (i.e. Safaricom Limited, Airtel Networks Kenya Limited and Telkom Kenya Limited). The rollout of the 3G technology, which is spectrum efficient and cost effective, supports a diverse range of services and offers better quality of service.

2.1.5. Broadcasting Services

The Commission, in its endeavour to ensure efficient utilization of the spectrum, continued to coordinate seamless migration from analogue to digital TV broadcasting. During the year under review, the Commission audited the TV broadcasting frequency band and determined the optimal number of channels and frequencies to be assigned to two additional national digital TV broadcast signal distributors. Freed up frequencies resulting from the migration, also known as the digital dividend, shall be used to deploy other ICT services.

2.1.6. Private Land Mobile Services

By 30th June 2011, the Commission assigned frequencies for use on 65 fixed and 632 portable/mobile stations in the VHF band as shown in Table 2.4.

Table 2.4: Additional Private Land Mobile Stations Frequency Band Station Type 2006/07 2007/08 2008/09 2009/10 2010/11

VHFFixed 97 140 85 61 65Mobile /Portable 401 571 440 376 632Total 498 711 525 437 697

HFFixed 14 48 14 15 1Mobile / Portable 39 24 16 13 13Total 53 72 30 28 14

Source: Communications Commission of Kenya

During the same period, the Commission assigned frequencies in the HF band for use on one fixed and 13 portable/mobile stations. This progressive decline in demand for HF frequencies from 2007/08 is attributed to widespread coverage provided by mobile telephony.

25CCK ANNUAL REPORT 2010-2011

In addition, the Commission issued licences for 115 existing network expansions and downsizing. It also renewed 641 Land Mobile licences comprising 567 VHF and 74 HF networks, 714 Aircraft and 41 Amateur radio networks. In addition, the Commission cancelled 46 Land Mobile radio networks, comprising 18 VHF and 28 HF networks.

By 30th June 2011, the cumulative total of the number of authorised private radiocommunications networks is as shown in Table 2.5.

Table 2.5: Number of Private Radiocommunication StationsFrequency Band No. of Fixed Stations No. of Mobile/Portable Stations

2009/10 2010/11 2009/10 2010/1130-136 MHz 211 211 843 883

138-170 MHz 2,774 2,784 18,228 18,336170-470 MHz 411 428 7,627 7,720

Total 3,396 3,423 26,698 26,939Source: Communications Commission of Kenya

2.1.7. Radio Alarm Services

During the year under review, the Commission licensed 39 new alarm networks compared to four the previous year. As shown in Table 2.6, the total number of alarm units in the country increased from 30,429 in 2009/10 to 32,068 in 2010/11 as a result of increased demand for the alarm services.

Table 2.6: Number of Alarm Networks and UnitsFinancial Year No. of Alarm Networks No. of Alarm Units

2007/08 171 28,3962008/09 175 31,6802009/10 179 30,4292010/11 218 32,068

Source: Communications Commission of Kenya

The increased demand for alarm network units was more pronounced in major towns in Western and Central regions such as Nakuru, Eldoret, Kisumu, Kakamega, Bungoma, Nyeri and Embu due to a rise in the level of economic activities.

2.2. Management of Numbering Resources

The Commission manages numbering resources by planning and assigning these scarce resources to licensed telecommunication service providers. During the review period, the Commission assigned a total of 11,020,054 numbers to facilitate the rollout of various services. The numbering resources assigned, by category, are shown in Table 2.7.

Table 2.7: Numbering Resources Assigned Category 2006/07 2007/08 2008/09 2009/10 2010/11Mobile National Destination Codes 16 24 8 4 11Mobile Subscriber Number Capacity 16,000,000 24,000,000 8,000,000 4,000,000 11,000,000Numbers for Fixed Telephony 1,629,000 1,729,000 50,000 900,025 20,000Toll Free Numbers 5,010 15,010 50 1 20Premium Rate Numbers - - - 1,000 16National Signalling Point Codes 233 361 1 1 2International Signalling Point Codes 6 6 2 1 -Network Colour Codes - - 1 - -Short Codes for Voice - - - - 5Source: Communications Commission of Kenya

CHAPTER 2: MANAGEMENT OF SCARCE RESOURCES 26

During the review period, 11 Mobile National Destination Codes (MNDC), each with a capacity of 1 million numbers, were assigned up from four the previous year. This increase could be attributed to a rise in the number of new services and products, reduction in calling tariffs and increased offers by operators. The anticipated introduction of Mobile Number Portability (MNP) in the period under review might also have contributed to the application for more MNDCs by telecommunication operators.

The numbers assigned for fixed telephony dropped to 20,000 in 2010/11 from 900,025 the previous year. This was due to depressed demand for fixed line numbers. Toll free numbers (0800 range) assigned increased from one in 2009/10 to 20 in 2010/11. This was attributed to the increase in the number of Content Service Providers (CSPs) that required these numbers for their clientele. There was a decline in the premium rate numbers (0900 range) assigned from 1,000 recorded the previous year to 16 in 2010/11 due to shrinking demand for these numbers. CSPs source these numbers directly from mobile operators.

To ensure efficient utilization of the numbering resources, the Commission carried out a numbering audit in order to establish the level of usage. Out of a total of 58,283,418 assigned numbers, 40,221,940 were being utilized as at 30th June 2011, representing a utilization rate of 69.0 percent compared to 61.8 percent recorded the previous year. The increase in utilization rate by 7.2 percentage points could be attributed to the launch of various products and services by mobile operators.

The continued development of the postal, information and communications industry in Kenya is crucial to Kenya’s economic prosperity and international competitiveness. Recognising the importance of competition as a driver of good market outcomes such as low prices, affordability, growth, investment and innovation, the Commission continued to issue licences in various market segments. During the year under review, the Commission undertook various initiatives aimed at stimulating competition and innovation. The initiatives included studies on emerging issues in the industry and the review of the interconnection and infrastructure sharing framework.

CCK’s Brain Wangila takes delegates from AFRALTI through the Radio Spectrum Monitoring System

27CCK ANNUAL REPORT 2010-2011

CHAPTER 3Promoting Competition and Innovation

3.1. Licensing and Network Expansions

The Commission continued to issue licences to new and existing players in the postal, information and telecommunications industry. As a result, there was an increase in the number of players, offering a diverse range of products and services thus expanding consumer choice. Further, during the year under review, the Commission commenced the process of evaluating the performance of some licensees whose licences were due for renewal. The Commission also reviewed the licence conditions of the Public Data Network Operators (PDNOs). 3.1.1. Telecommunications Licensing

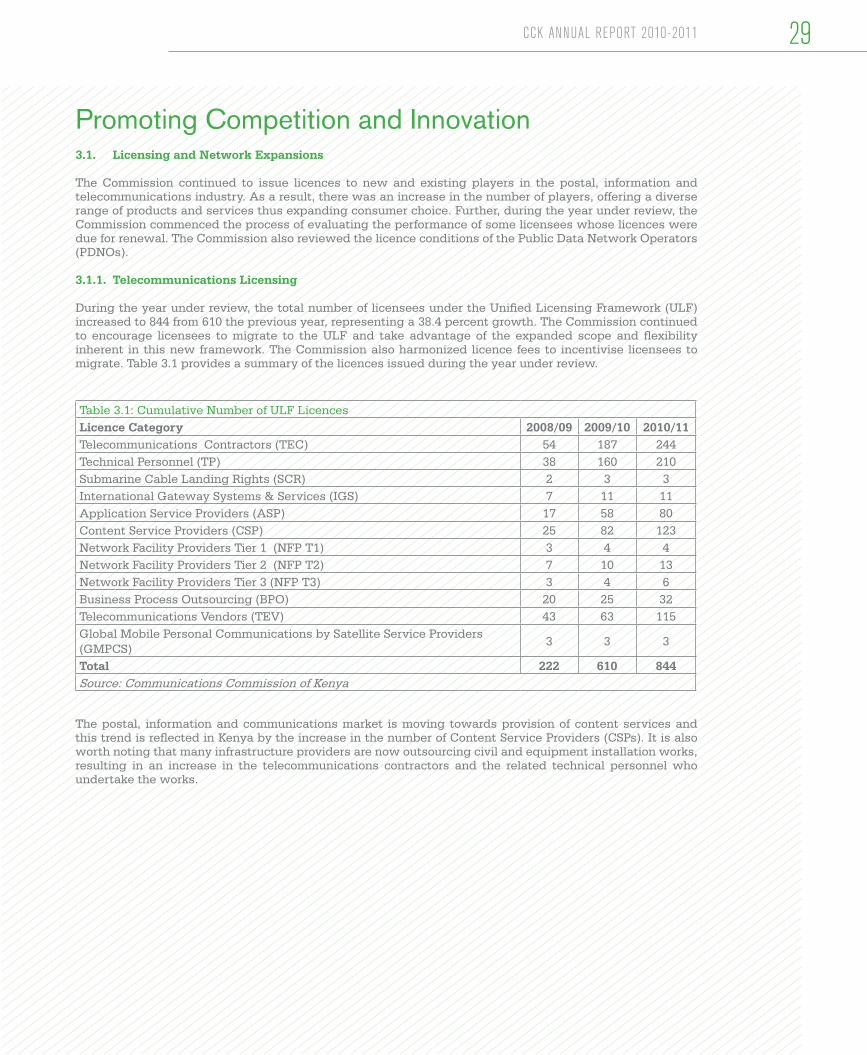

During the year under review, the total number of licensees under the Unified Licensing Framework (ULF) increased to 844 from 610 the previous year, representing a 38.4 percent growth. The Commission continued to encourage licensees to migrate to the ULF and take advantage of the expanded scope and flexibility inherent in this new framework. The Commission also harmonized licence fees to incentivise licensees to migrate. Table 3.1 provides a summary of the licences issued during the year under review.

Table 3.1: Cumulative Number of ULF Licences Licence Category 2008/09 2009/10 2010/11Telecommunications Contractors (TEC) 54 187 244Technical Personnel (TP) 38 160 210Submarine Cable Landing Rights (SCR) 2 3 3International Gateway Systems & Services (IGS) 7 11 11Application Service Providers (ASP) 17 58 80Content Service Providers (CSP) 25 82 123Network Facility Providers Tier 1 (NFP T1) 3 4 4Network Facility Providers Tier 2 (NFP T2) 7 10 13Network Facility Providers Tier 3 (NFP T3) 3 4 6Business Process Outsourcing (BPO) 20 25 32Telecommunications Vendors (TEV) 43 63 115Global Mobile Personal Communications by Satellite Service Providers (GMPCS)

3 3 3

Total 222 610 844Source: Communications Commission of Kenya

The postal, information and communications market is moving towards provision of content services and this trend is reflected in Kenya by the increase in the number of Content Service Providers (CSPs). It is also worth noting that many infrastructure providers are now outsourcing civil and equipment installation works, resulting in an increase in the telecommunications contractors and the related technical personnel who undertake the works.

29CCK ANNUAL REPORT 2010-2011

Promoting Competition and Innovation

30

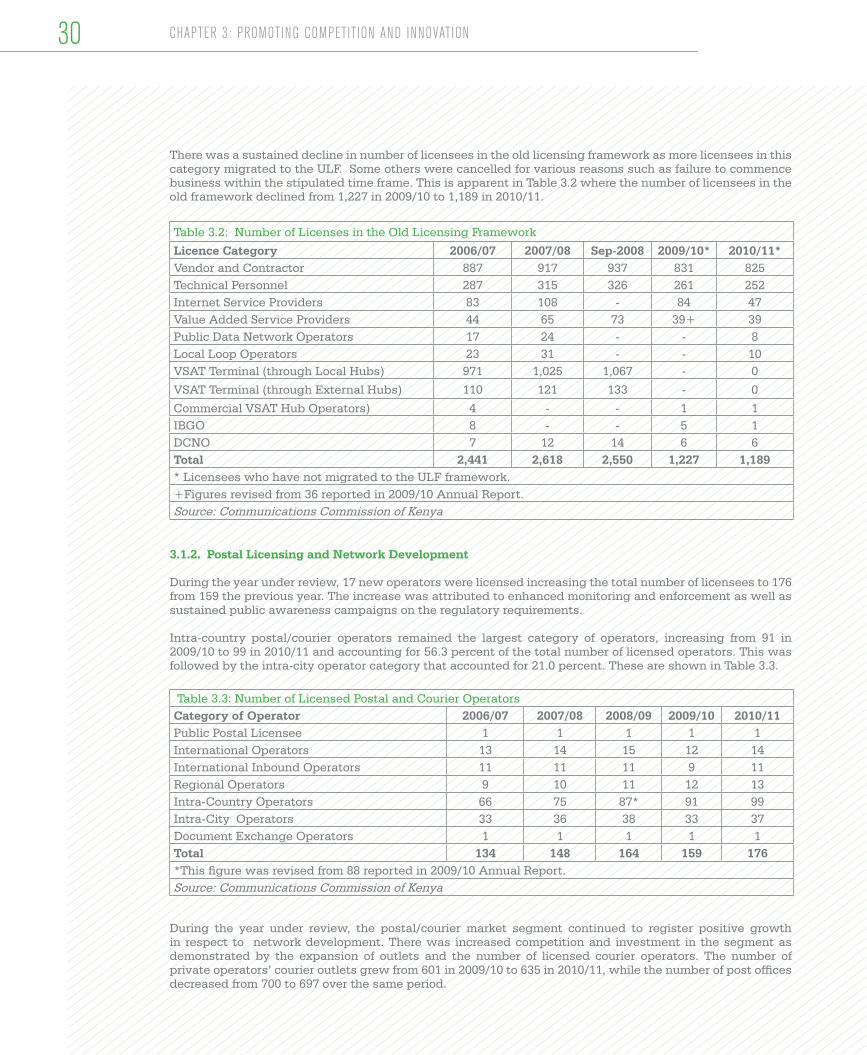

There was a sustained decline in number of licensees in the old licensing framework as more licensees in this category migrated to the ULF. Some others were cancelled for various reasons such as failure to commence business within the stipulated time frame. This is apparent in Table 3.2 where the number of licensees in the old framework declined from 1,227 in 2009/10 to 1,189 in 2010/11.

Table 3.2: Number of Licenses in the Old Licensing Framework

Licence Category 2006/07 2007/08 Sep-2008 2009/10* 2010/11*Vendor and Contractor 887 917 937 831 825Technical Personnel 287 315 326 261 252Internet Service Providers 83 108 - 84 47Value Added Service Providers 44 65 73 39+ 39Public Data Network Operators 17 24 - - 8Local Loop Operators 23 31 - - 10VSAT Terminal (through Local Hubs) 971 1,025 1,067 - 0

VSAT Terminal (through External Hubs) 110 121 133 - 0

Commercial VSAT Hub Operators) 4 - - 1 1IBGO 8 - - 5 1DCNO 7 12 14 6 6Total 2,441 2,618 2,550 1,227 1,189* Licensees who have not migrated to the ULF framework.+Figures revised from 36 reported in 2009/10 Annual Report. Source: Communications Commission of Kenya

3.1.2. Postal Licensing and Network Development

During the year under review, 17 new operators were licensed increasing the total number of licensees to 176 from 159 the previous year. The increase was attributed to enhanced monitoring and enforcement as well as sustained public awareness campaigns on the regulatory requirements.

Intra-country postal/courier operators remained the largest category of operators, increasing from 91 in 2009/10 to 99 in 2010/11 and accounting for 56.3 percent of the total number of licensed operators. This was followed by the intra-city operator category that accounted for 21.0 percent. These are shown in Table 3.3.

Table 3.3: Number of Licensed Postal and Courier OperatorsCategory of Operator 2006/07 2007/08 2008/09 2009/10 2010/11Public Postal Licensee 1 1 1 1 1International Operators 13 14 15 12 14International Inbound Operators 11 11 11 9 11Regional Operators 9 10 11 12 13Intra-Country Operators 66 75 87* 91 99Intra-City Operators 33 36 38 33 37Document Exchange Operators 1 1 1 1 1Total 134 148 164 159 176*This figure was revised from 88 reported in 2009/10 Annual Report.Source: Communications Commission of Kenya

During the year under review, the postal/courier market segment continued to register positive growth in respect to network development. There was increased competition and investment in the segment as demonstrated by the expansion of outlets and the number of licensed courier operators. The number of private operators’ courier outlets grew from 601 in 2009/10 to 635 in 2010/11, while the number of post offices decreased from 700 to 697 over the same period.

CHAPTER 3: PROMOTING COMPETITION AND INNOVATION

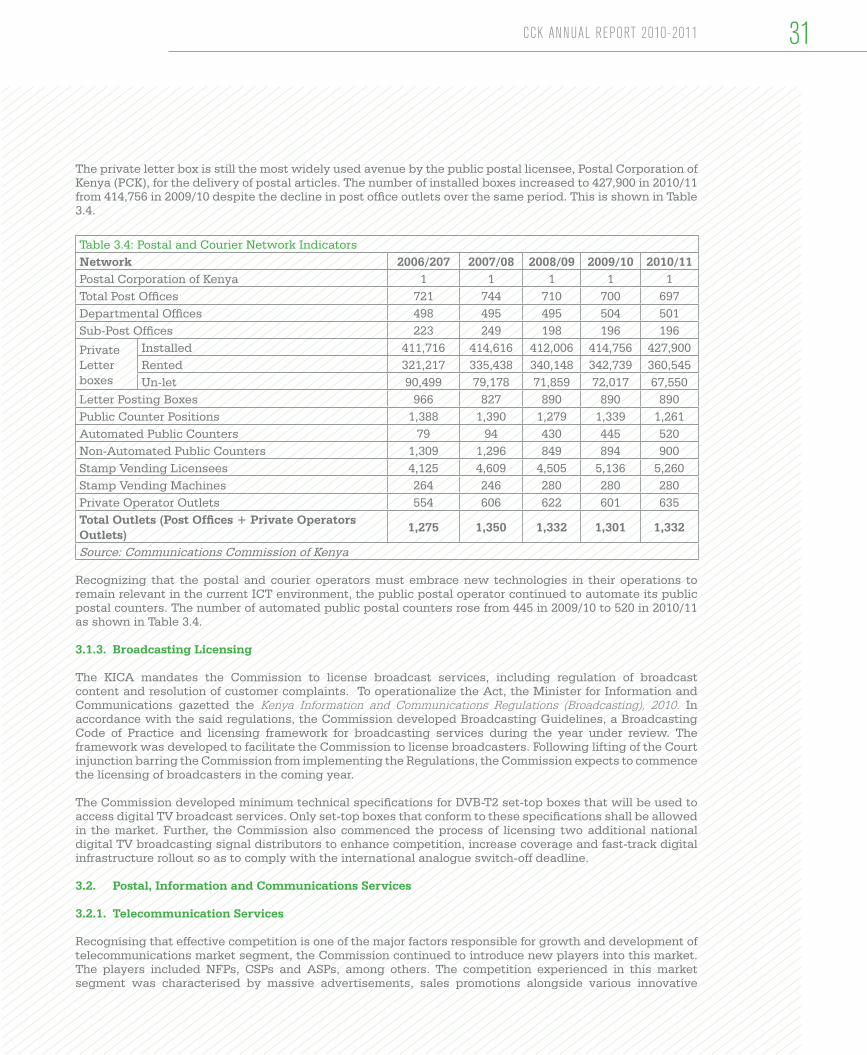

The private letter box is still the most widely used avenue by the public postal licensee, Postal Corporation of Kenya (PCK), for the delivery of postal articles. The number of installed boxes increased to 427,900 in 2010/11 from 414,756 in 2009/10 despite the decline in post office outlets over the same period. This is shown in Table 3.4.

Table 3.4: Postal and Courier Network IndicatorsNetwork 2006/207 2007/08 2008/09 2009/10 2010/11Postal Corporation of Kenya 1 1 1 1 1Total Post Offices 721 744 710 700 697Departmental Offices 498 495 495 504 501Sub-Post Offices 223 249 198 196 196

Private Letter boxes

Installed 411,716 414,616 412,006 414,756 427,900Rented 321,217 335,438 340,148 342,739 360,545Un-let 90,499 79,178 71,859 72,017 67,550

Letter Posting Boxes 966 827 890 890 890Public Counter Positions 1,388 1,390 1,279 1,339 1,261Automated Public Counters 79 94 430 445 520Non-Automated Public Counters 1,309 1,296 849 894 900Stamp Vending Licensees 4,125 4,609 4,505 5,136 5,260Stamp Vending Machines 264 246 280 280 280Private Operator Outlets 554 606 622 601 635Total Outlets (Post Offices + Private Operators Outlets)

1,275 1,350 1,332 1,301 1,332

Source: Communications Commission of Kenya

Recognizing that the postal and courier operators must embrace new technologies in their operations to remain relevant in the current ICT environment, the public postal operator continued to automate its public postal counters. The number of automated public postal counters rose from 445 in 2009/10 to 520 in 2010/11 as shown in Table 3.4.

3.1.3. Broadcasting Licensing

The KICA mandates the Commission to license broadcast services, including regulation of broadcast content and resolution of customer complaints. To operationalize the Act, the Minister for Information and Communications gazetted the Kenya Information and Communications Regulations (Broadcasting), 2010. In accordance with the said regulations, the Commission developed Broadcasting Guidelines, a Broadcasting Code of Practice and licensing framework for broadcasting services during the year under review. The framework was developed to facilitate the Commission to license broadcasters. Following lifting of the Court injunction barring the Commission from implementing the Regulations, the Commission expects to commence the licensing of broadcasters in the coming year.

The Commission developed minimum technical specifications for DVB-T2 set-top boxes that will be used to access digital TV broadcast services. Only set-top boxes that conform to these specifications shall be allowed in the market. Further, the Commission also commenced the process of licensing two additional national digital TV broadcasting signal distributors to enhance competition, increase coverage and fast-track digital infrastructure rollout so as to comply with the international analogue switch-off deadline.

3.2. Postal, Information and Communications Services

3.2.1. Telecommunication Services

Recognising that effective competition is one of the major factors responsible for growth and development of telecommunications market segment, the Commission continued to introduce new players into this market. The players included NFPs, CSPs and ASPs, among others. The competition experienced in this market segment was characterised by massive advertisements, sales promotions alongside various innovative

CCK ANNUAL REPORT 2010-2011 31

32

product and service offerings by both new and existing players.

3.2.1.1. Fixed Network Voice Services

Telkom Kenya Limited (TKL) and Flashcom Kenya Limited [a Local Loop Operator (LLO)] continued to be the only players in the fixed network voice services market in Kenya, with TKL holding 99 percent of the market share. During the year under review, the total fixed line (including wireless) subscribers shrank from 460,114 recorded in June 2010 to 379,301 in June 2011. This translated to a decrease in teledensity from 1.2 percent in 2009/10 to 0.95 percent in 2010/11. The fixed wireline capacity decreased from 421,528 to 400,764 during the same period as shown in Table 3.5.

Table 3.5: Fixed Network Growth Indicators

Financial Year 2006/07 2007/08 2008/09 2009/10 2010/11Wireline Capacity 505,103 512,281 485,581 421,528 400,764Wireline Connections 263,122 252,615 247,972 234,522 187,716Wireless Connections (Include LLO subscribers)

84,104 274,449 419,047 225,592 191,585

Total Connections (Wireline and Wireless)

347,226 527,064 696,501 460,114 379,301

Urban Wireline Connections 251,924 246,927 240,533 227,486 182,084Rural Wireline Connections 11,198 5,688 7,439 7,036 5,632International Outgoing Traffic (Minutes)

27,363,876 15,582,304 14,471,643 14,761,211 11,455,952

International Incoming Traffic (Minutes)

85,672,270 83,148,332 88,538,230 38,550,399 31,866,685

Traffic to Mobile networks (Minutes) 124,378,826 98,238,064 34,103,924 31,024,688 59,301,227Source: Communications Commission of Kenya

The fixed wireline connections in both urban and rural areas declined by 20 percent to stand at 182,084 and 5,632 in 2010/11 compared to 227,486 and 7,036, respectively recorded the previous year. The reduction in fixed line services could be attributable to increased competition from mobile service providers and high cost of maintaining fixed lines as a result of cable vandalism. Declining trends in wireline and fixed wireless connections are shown in Figure 3.1.

450,000

400,000

350,000

300,000

250,000

150,000

50,000

2006/7 2007/8 2008/9 2009/10 2010/11

0

100,000

200,000

Figure 3.1: Fixed Subscriber Growth Trend in the last Five Years

263,122

84,104

252,615

247,449

234,522

225,592

187,716

191,585

419,047

247,972

Wireline Connections Wireless Connections

Source: Communication Commission of Kenya

CHAPTER 3: PROMOTING COMPETITION AND INNOVATION

Fixed international voice traffic, both outgoing and incoming, continued to decline from 2008/09 to 2010/11. The decline in fixed international call traffic could be attributed to a decline in consumers’ ability to pay for fixed international telephone calls. It could also be ascribed to reduced mobile international voice calling charges and other competing alternatives such as Skype, Google talk as well as video and instant messaging over the Internet. The trend in outgoing and incoming traffic is shown in Figure 3.2.

2006/7

2007/8

2008/9

2009/10

2010/11

Figure 3.2: Fixed Network International Traffic

Fin

anci

al Y

ear

Traffic Volume

20,000,000 40,000,000 60,000,000 80,000,000 100,000,000 120,000,000

International Incoming Traffic (Minutes) International Outgoing Traffic (Minutes)

31,866,68511,455,952

38,550,39914,761,211

88,538,23014,471,643

83,148,33215,582,304

85,672,27027,363,876

0

Source: Communications Commission of Kenya

3.2.1.2. Mobile Network Services

Competition amongst the four mobile network operators namely Airtel Networks Kenya Limited (Airtel), Safaricom Limited (Safaricom), Essar Telecoms Kenya Limited (yu), and Telkom Kenya Limited (Orange) in the mobile market segment continued to thrive during the year under review. Mobile subscriptions grew significantly, recording a growth of 25.6 percent to stand at 25.2 million subscribers at the end of the year from 20.1 million recorded the previous year. Mobile capacity grew from 46,628,948 million to 51,677,000 as shown in Figure 3.3.

2006/7 2007/8 2008/9 2009/10 2010/11

Figure 3.3: Mobile Operator’s Capacity and Subscribers

52,000,000

47,000,000

42,000,000

37,000,000

32,000,000

27,000,000

22,000,000

17,000,000

12,000,000

7,000,000

2,000,000

Capacity Connections (Mobile Subscribers)

18,200,000

9,304,818

25,964,700

12,933,653

29,400,000

17,362,257

46,628,948

20,119,304

51,677,000

25,279,768

Source: Communications Commission of Kenya

33CCK ANNUAL REPORT 2010-2011

34

The operators reduced both on-net and off-net tariffs in a bid to attract and retain customers on their respective networks following the Commission’s intervention in lowering mobile termination rates. Subsequently, mobile penetration increased from 51.2 percent in June 2010 to 63.6 percent as at 30th June 2011. This penetration was above the African penetration rates estimated by ITU at 41 percent during the same period.