Annual Report 2007 MAN Ferrostaal AG · 2010. 8. 20. · ROS (%) 14.4 12.7 * including temporary...

62

Annual Report 2007 MAN Ferrostaal AG TURNING IDEAS INTO REALITY

Transcript of Annual Report 2007 MAN Ferrostaal AG · 2010. 8. 20. · ROS (%) 14.4 12.7 * including temporary...

Annual Report 2007MAN Ferrostaal AG

T u R n i n g i d e A s i n T o R e A l i T y

MAN Ferrostaal Subgroup 2007 2006 Change in %

in mill. €

Order Intake 1,556 1,982 – 21.5

Germany 380 283 34.3

Abroad 1,176 1,699 – 30.8

Sales 1,445 1,379 4.8

Germany 270 247 9.3

Abroad 1,175 1,132 3.8

Orders on hand 31/12 2,415 2,342 3.1

Germany 332 233 42.5

Abroad 2,083 2,109 – 1.2

Employees (Number as of 31/12) 4,687 4,879 – 3.9

of which temporary staff 512 589 – 13.1

Germany 2,648 2,715 – 2.5

Abroad 2,039 2,164 – 5.8

Change in mill. €

Operating Profit 179 119 60

Earnings Before Tax (EBT) 173 81 92

Net Income after Taxes 156 – 15 171

Return on Sales ROS (in %) 12.4 8.6 -

Return on Capital Employed ROCE (in %) 36.9 31.2 -

MAN Value Added (MVA) 126 77 49

Investments 45 22 23

Depreciation 28 26 2

Cash Earnings 102 40 62

Cashflow from Business Operations 260 – 94 354

Free Cashflow 257 – 90 347

Liquid Assets 628 447 181

Net Liquid Assets 601 415 186

Equity 334 255 79

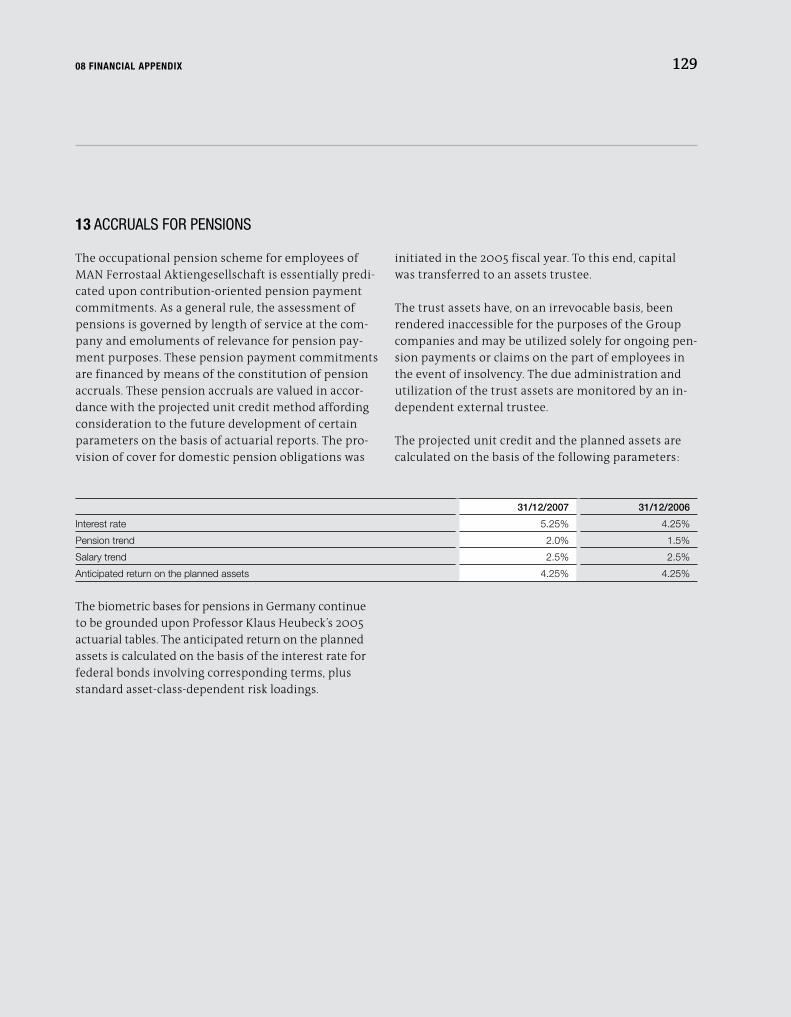

At a glance

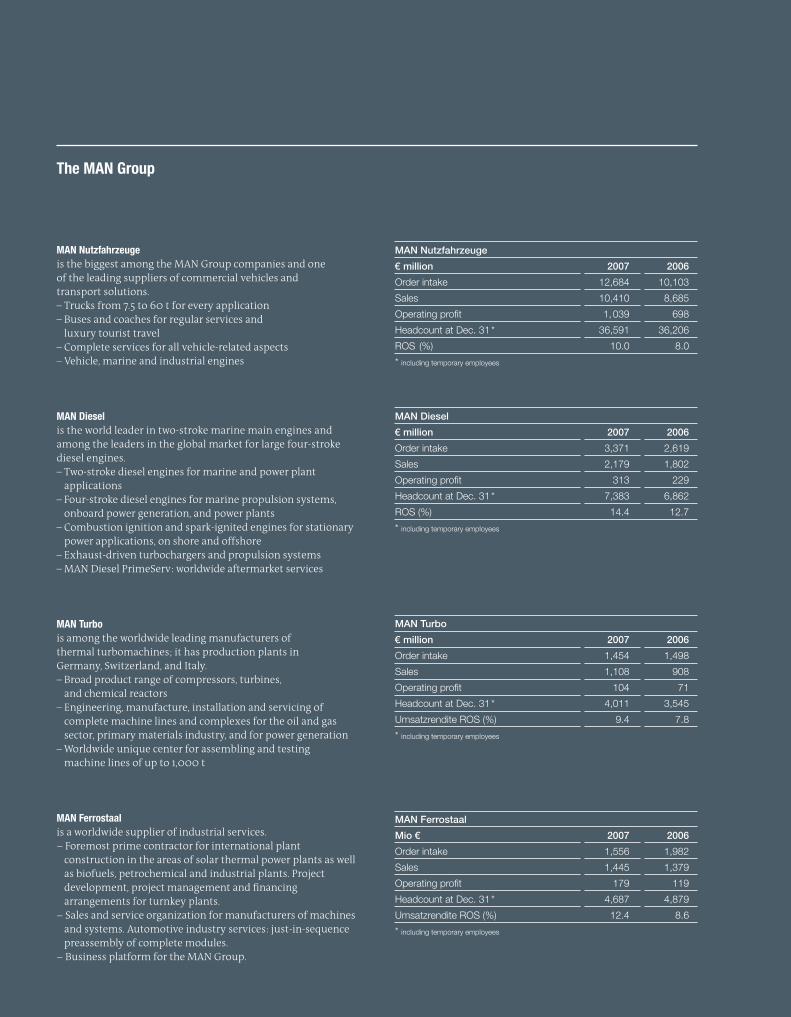

The MAn group

MAn nutzfahrzeugeis the biggest among the MAN Group companies and one of the leading suppliers of commercial vehicles andtransport solutions.– Trucks from 7.5 to 60 t for every application– Buses and coaches for regular services and luxury tourist travel– Complete services for all vehicle-related aspects– Vehicle, marine and industrial engines

MAn dieselis the world leader in two-stroke marine main engines and among the leaders in the global market for large four-stroke diesel engines.– Two-stroke diesel engines for marine and power plant applications– Four-stroke diesel engines for marine propulsion systems, onboard power generation, and power plants– Combustion ignition and spark-ignited engines for stationary power applications, on shore and offshore– Exhaust-driven turbochargers and propulsion systems– MAN Diesel PrimeServ: worldwide aftermarket services

MAn Turbois among the worldwide leading manufacturers ofthermal turbomachines; it has production plants inGermany, Switzerland, and Italy.– Broad product range of compressors, turbines, and chemical reactors– Engineering, manufacture, installation and servicing of complete machine lines and complexes for the oil and gas sector, primary materials industry, and for power generation– Worldwide unique center for assembling and testing machine lines of up to 1,000 t

MAn Ferrostaalis a worldwide supplier of industrial services.− Foremost prime contractor for international plant construction in the areas of solar thermal power plants as well as biofuels, petrochemical and industrial plants. Project development, project management and financing arrangements for turnkey plants.− Sales and service organization for manufacturers of machines and systems. Automotive industry services: just-in-sequence preassembly of complete modules.− Business platform for the MAN Group.

MAN Nutzfahrzeuge

€ million 2007 2006

Order intake 12,684 10,103

Sales 10,410 8,685

Operating profit 1, 039 698

Headcount at Dec. 31 * 36,591 36,206

ROS (%) 10.0 8.0

* including temporary employees

MAN Diesel

€ million 2007 2006

Order intake 3,371 2,619

Sales 2,179 1,802

Operating profit 313 229

Headcount at Dec. 31 * 7,383 6,862

ROS (%) 14.4 12.7

* including temporary employees

MAN Turbo

€ million 2007 2006

Order intake 1,454 1,498

Sales 1,108 908

Operating profit 104 71

Headcount at Dec. 31 * 4,011 3,545

Umsatzrendite ROS (%) 9.4 7.8

* including temporary employees

MAN Ferrostaal

Mio € 2007 2006

Order intake 1,556 1,982

Sales 1,445 1,379

Operating profit 179 119

Headcount at Dec. 31 * 4,687 4,879

Umsatzrendite ROS (%) 12.4 8.6

* including temporary employees

The MAn group The MAN Group is one of Europe’s foremost industrial players in the sector of Transport-Related Enginee- ring, with sales in 2007 of some €15.5 billion. As a supplier of trucks, buses, diesel engines, turbo machinery and industrial services, MAN employs a workforce of around 55,000 worldwide. The MAN business areas hold leading positions in their markets. MAN AG, Munich, is listed in the DAX (German Stock Index) which com- prises the thirty leading stock corporations in Germany.

Annual Report 2007MAN Ferrostaal AG

07 MANAGEMENT REPORT 82

“Simple action carried out logically is the surest way of reaching your goal.”Helmuth Karl Bernhard Graf von Moltke: Regulations. Moltke, Prussian Field Marshall, together with Otto von Bismarck, was one of the architects of the foundation of the German Empire in 1871.

8307 MANAGEMENT REPORT

Management Report

Global economic growth slowed slightly in 2007. At 5.2 percent it was below the level of the previ-ous year (5.4 percent). The primary factor affect-

ing this trend was the weakening economic situation in the USA. In 2007 the world’s largest economy grew by only 1.9 percent; in 2006 it was still growing by 3.3 per-cent. The economic situation within the eurozone on the other hand proved stable – at 2.5 percent, growth was only slightly below the value of the previous year (2.6 percent). This can be seen as a further indication of

the increasing independence of the European economic area from the USA.

The core growth regions remain those of Asia and Lat-in America as well as Central and Eastern Europe. The Chinese economy again showed particularly positive development: its gross national product increased by 11.5 percent in 2007. Apart from prospering emerging markets, more and more developing countries are ex-hibiting higher growth rates, especially in Africa.

Machinery and plant construction at record levelsFor our sector – the German engineering and plant con-struction industry – 2007 was one of the best years since the start of post-war reconstruction. According to the German Engineering Federation, VDMA, (2008) turnover in the sector totalled 193 billion euros (previous year: 167 billion euros), which represents a nominal increase of 16 percent. Exports increased by 12.3 percent.

And 2007 also marked another successful year for members of the VDMA's Large Industrial Plant Manu-facturer Group whose excellent figures exceeded those of the previous year. As a result, a record 31.3 billion eu-ros in orders were booked in the period from July 2006 through June 2007 (previous year: 26.3 billion euros). That represents a rise of 19 percent.

This positive development in the sector has been driven by several factors. The worldwide growth in electricity demand, for example, has translated into an increase in the demand for power plant construction. Here orders increased for the fourth time in as many years, attaining an international record level of 7.5 billion euros in 2007.

Interest in extending the value added chain continues to grow, particularly in emerging markets rich in natu-ral resources. The chemical industry plays a key role here. In 2007, international chemical plant construc-tion grew by 9 percent to 4.1 billion euros and ranked second overall in terms of incoming orders. The inter-est in plants for refining oil and natural gas was partic-ularly strong.

Economic environment

84

in % over the previous year 2005 2006 2007

World 4.9 5.4 5.2

Eurozone 1.4 2.6 2.5

USA 3.2 3.3 1.9*

China 10.2 10.7 11.5*

Source: International Monetary Fund (January 2008) * estimates

Further growthDevelopment of real gross national product

07 MANAGEMENT REPORT

85

At 3.8 billion euros, the construction of metallurgical plants and rolling mills ranked third among incoming orders. Driven by the continuing high demand for steel, the historical ten-year average was exceeded by about 50 percent. Along with China the most impor-tant markets were Brazil and Russia. In addition to positive effects from abroad, the demand on the Ger-man market stabilised. At 6.4 billion euros, this order

volume was 9 percent higher than it was during the previous year (5.9 billion euros). The top rank was also held here by the power plant business with 3 billion euros. The demand for alternative energies has also been accelerated by increases in the price of oil and gas. Orders of this type have also contributed noticeably to the good order results of 2007. Above average growth is expected here in the next several years.

Business development

In fiscal 2007 we continued the positive trend of the previous year and, with earnings before interest and taxes of 179 million euros achieved, the best re-

sult in the history of the company. Return on sales in-creased significantly to 12.4 percent (previous year: 8.6 percent) while sales rose slightly to 1,445 million euros (previous year: 1,379 million euros). At 1,556 million eu-ros, incoming orders remained below the unusually high level of the previous year (previous year: 1,982 million euros). Although that decline was not unex-pected, the total nevertheless exceeded current sales once again, raising orders on hand by another 3 per-cent versus the previous year to 2,415 million euros (previous year: 2,342 million euros).

Record operating profitIn the last fiscal year we increased the annual result by 50 percent over the previous year to 179 million euros (previous year: 119 million euros), thereby achieving the best result in the history of the company. This reflects above all the positive development of the in-vestments in methanol and ammonia plants. The re-sults in the service business also improved significant-ly. Moreover we see positive effects resulting from the steps we have taken toward corporate reorientation in which we took businesses that posted losses or weak results in recent years and realigned them, thereby significantly improving profitability in these areas.

Improved return indicatorsOur rate of return indicators also improved with enhanced results. The return on sales (ROS) increased to 12.4 percent compared to 8.6 percent in the previ-ous year. Return on sales and return on capital em-ployed (ROCE) are the most important indicators used to assess economic success in the MAN Group. In the calculation of capital employed, prepayments received have only been considered as non-interest bearing lia-bilities to the extent that they have already been uti-lised as part of order processing. On this basis, our company shows a return on equity of 36.9 percent compared to 31.2 percent in 2006. The positive devel-opment can also be seen in the cash flow: free cash flow, which was still negative last year, has increased to positive 257 million euros.

Significantly higher value added (MVA)MAN Value Added is the financial parameter that shows whether the MAN Ferrostaal Group has earned its capital costs and generated supplementary added value. In 2007 we raised our value added by 63 percent to 126 million euros (previous year: 77 million euros).

07 MANAGEMENT REPORT

Incoming orders below previous year’s levelIn fiscal year 2007 the incoming orders of the MAN Ferrostaal Group totalled 1,556 million euros, which was 21.5 percent below the very high level of the previ-ous year (1,982 million euros). The decline was expected and essentially resulted from an unusually high value in the previous year for a project in Trinidad valued at 1.5 billion US dollars. We are counterbalancing this through regional expansion of our business and by keeping the layout of our services flexible.

Incoming orders in the Services division totalled 707 million euros, which represents a 14 percent increase over 2006 (620 million euros). A substantial part of this development was from Ships. The orders generated here exceeded the value of the previous year by more than threefold. Automotive also continued to develop satisfactorily.

The largest share of orders in 2007 was generated out-side Germany (76 percent). The most important re-gions were Latin America with 39 percent, the MENA region with 15 percent and the EU (excluding Germa-ny) with 9 percent. Germany generated 24 percent of all new orders.

Orders on hand at a very high levelOrders on hand increased by 3 percent to 2,415 million euros (previous year: 2,342 million euros). This once

again surpassed the high level of the previous year. On December 31, 2007 the Projects division had a total of 1,443 million euros in orders on hand versus 1,321 mil-lion euros at the end of the previous year. A large share of these orders was in Petrochemical. The Services division had orders on hand totalling 972 million eu-ros versus 1,021 million euros in the previous year.

Increased salesThe sales of the MAN Ferrostaal Group developed sat-isfactorily and were, at 1,445 million euros, 5 percent above the value of the previous year (1,379 million euros). The contribution of Services to this positive development was particularly strong: net sales there were 751 million euros, which was 21 percent above the pervious year’s value (619 million euros). The highest rates of growth were posted by Equipment and Ships. The trend in Projects developed in the opposite direc-tion, where sales totalled 694 million euros and fell relative to 2006 (760 million euros). This effect was principally the result of Industrial Projects.

The largest share of sales in 2007 was also generated outside Germany (81 percent). The most important re-gions were Latin America with 38 percent, the MENA region with 14 percent and the EU (excluding Germa-ny) with 8 percent. Germany generated 19 percent of net sales.

86

New Order Sales

Rest of World 10%€158 mill. EU incl. Germany 34%

€523 mill.

MENA region 15%€241 mill.

Latin America 39%€609 mill.

CIS 2%€26 mill.

CIS 5%€70 mill.

Rest of World 16%€236 mill.

Latin America 38%€554 mill.

MENA region 14%€199 mill.

EU incl. Germany 27%€386 mill.

07 MANAGEMENT REPORT

87

Against the background of the considerable growth in the emerging countries of Latin America and Asia, the areas of energy and fuels are especially

significant. The International Energy Agency (IEA) esti-mates that worldwide energy consumption will increase by 75 percent by 2030. For this reason we plan to contin-ue our robust expansion in these areas.

Provided political conditions remain unchanged, the IEA projections assume only a proportional increase in biofuels and alternative electricity generation. Under this scenario, carbon dioxide emissions in the emerg-ing countries will more than double during the period from 2004 to 2030. This is why alternative sources of energy like biofuels and solar power are becoming increasingly significant.

Our business strategy-driven decision-making processes assume that legislation all over the world will focus even more on renewables in coming years in order to slow down the effects of climate change by reducing CO2 emissions.

For this reason we are placing ever more emphasis on sustainable forms of energy production, both in fuels and in the generation of electricity. Within the context of our strategic realignment, we have set milestones in 2007: with the newly established business divisions Solar and Biofuels, we are entering two new, future-ori-ented markets.

Significant business events

Worldwide energy consumption is rising. BTUs are British thermal units, 1 MMBTU = 1,000,000 BTUs = 1,055 MJ = 293.06 kWhSource: IEA, World Energy Fact Book 2007

If political conditions remain constant, carbon dioxide emissions will increase considerably.Source: IEA, World Energy Fact Book 2007

Trillions of BTUs

0

200

600

400

800

2004

447

2010

511

2015

559

2020

607

2025

654

2030

702

Non-OECD statesNon-OECD states OECD statesOECD states

Worldwide energy consumption by region, 2004 – 2030

Worldwide carbon dioxide emissions by region, 2003 – 2030

0

10

30

20

20152004

13 13

2010

14

17

2030

17

26

2025

16

24

2020

15

22

15

19

2003

1312

Billions of metric tonnes

07 MANAGEMENT REPORT

88

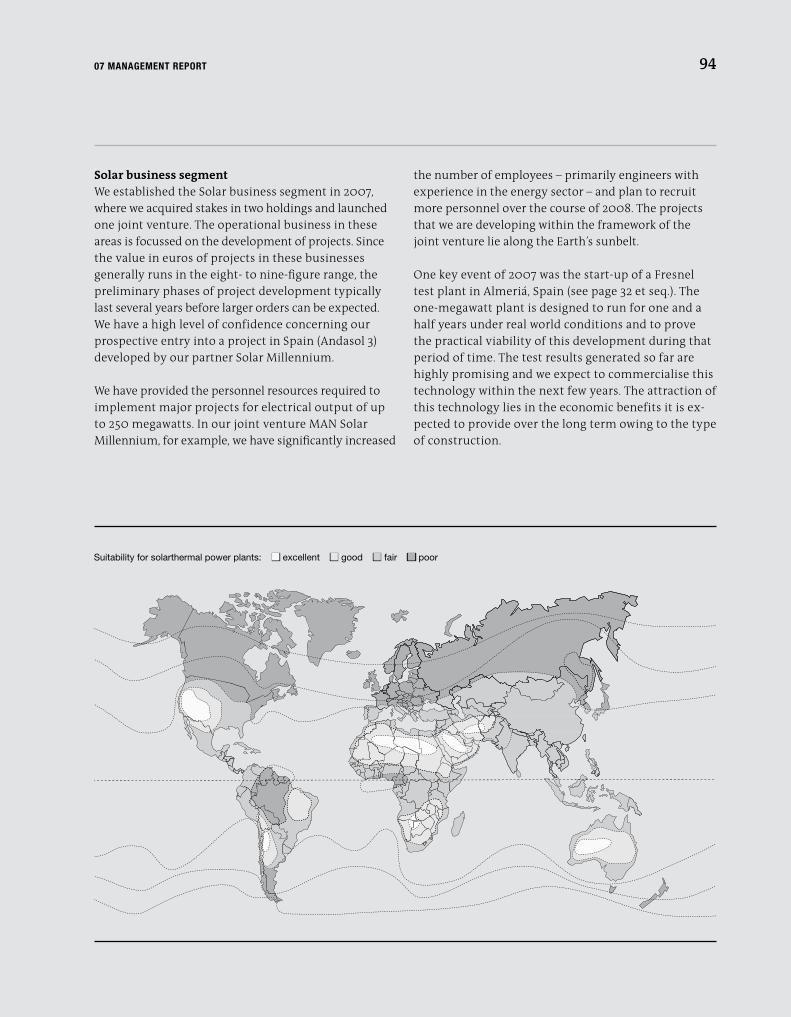

New business area for solarthermal plantsWe have added the business segment Solar to the Projects division (large-scale plant construction). Here in what is still a young market, we aim to position ourselves as a major market player. Our basic business approach here does not involve developing any of our own tech-nologies, but rather calls for us to work together with leading technology partners to realise joint projects. We succeeded in gaining three such partners over the course of the past year.

In a joint venture with Solar Millennium, we plan to build solarthermal power plants in the range of 20 to 250 megawatts. The 50-50 joint venture MAN Solar Millennium GmbH, which we established in May 2007, concentrates on the project development, financing and construction of solarthermal power plants. These plants are based on the proven parabolic trough tech-nology. Our long-term goal is to establish the company as the leading provider of solarthermal power plants in this size range. Together with its subsidiary Flagsol, our partner Solar Millennium, the technology leader in so-larthermal plants, has developed parabolic trough technology up to the point of marketability. The basis of this technology is already more than 20 years old. Solar Millennium developed Europe’s first commercial parabolic trough power plants in Spain. The first two of these 50-megawatt power plants are already under construction and construction of the third will com-mence in 2008. The joint venture has started preparing projects for the development and construction of solar power plants and has established subsidiaries in Dubai and the USA in order to serve the market in the Middle East directly. We expect to receive orders in 2008.

We acquired a 25 percent stake in a second technology provider in 2007, the Solar Power Group. This company recently developed a technology that will soon make it possible to generate electricity from solar energy at low cost. As this so-called Fresnel technology is able to work with flat mirrors, it is highly economical. Together with the Fraunhofer Institute and the DLR, we commis-sioned a test power plant of this type in Spain in 2007 (see page 32 et seq.). Its purpose is to prove the practi-cal application of the Fresnel technology under normal operating conditions. After successful conclusion of the tests, we intend to commercialise this technology.

In cooperation with the SOLITEM Group, we plan to build plants for solar cooling in the 1-20 megawatt power range. We have acquired a 20.1 percent share in this company. Plants of this type collect heat from smaller solarthermal parabolic troughs and use absorp-tion cooling machines to convert it directly into cool-ing. Markets for this technology are regions in which a high share of the electrical consumption is used to op-erate conventional air conditioning systems. In some countries in the Middle East, for example, that share can be as high as 80 percent. While the technology of these products is similar in many respects to that of the large parabolic troughs, the costs are lower due to the type of construction. The systems are also relative-ly lightweight. That makes residential rooftop applica-tions possible, which plays a major role in terms of the breadth of the potential market.

The markets in which we are focused in Solar are basi-cally Southern Europe, North Africa, the Middle East, the USA, Australia, South Africa and Chile. As we have already been well represented in most of these coun-tries for many years now, we see good prospects for near-term success.

07 MANAGEMENT REPORT

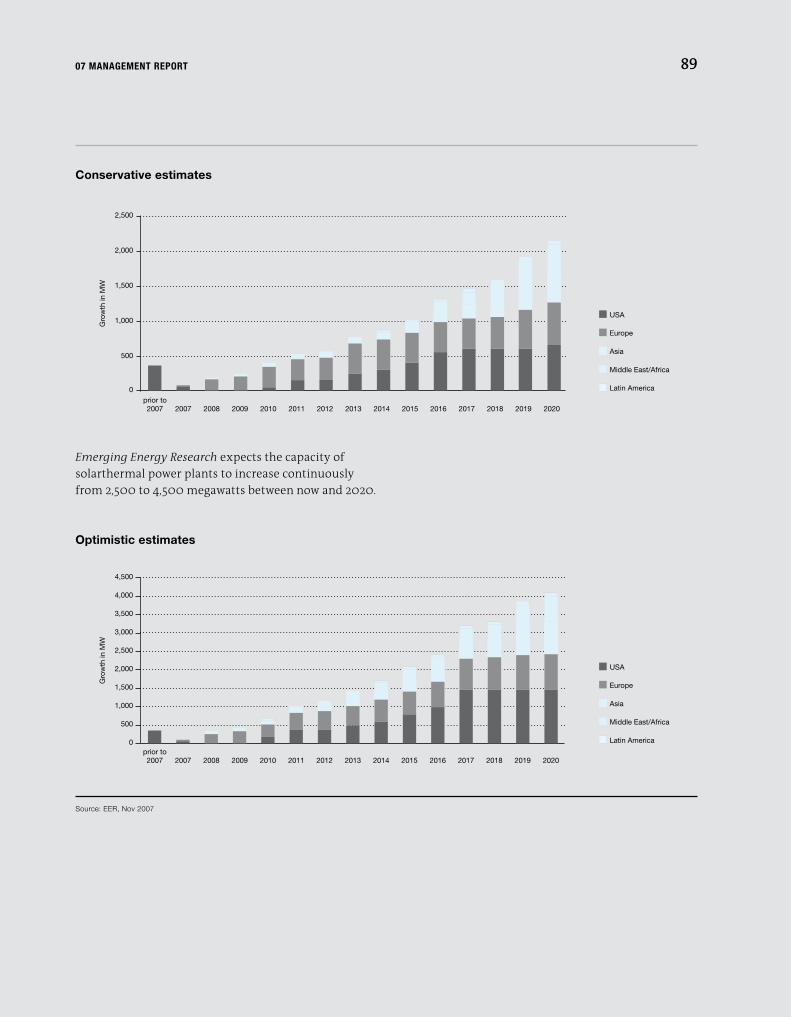

Emerging Energy Research expects the capacity of solarthermal power plants to increase continuously from 2,500 to 4,500 megawatts between now and 2020.

prior to2007 2007 2008 201820172015201420132009 2010 2011 2012 2016 2019 2020

89

0

500

1,000

1,500

2,000

2,500

Gro

wth

in M

W

Europe

Asia

Middle East/Africa

Latin America

USA

Source: EER, Nov 2007

prior to2007 2007 2008 201820172015201420132009 2010 2011 2012 2016 2019 2020

4,500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Gro

wth

in M

W

Europe

Asia

Middle East/Africa

Latin America

USA

Optimistic estimates

Conservative estimates

07 MANAGEMENT REPORT

90

Millions of tonnes of oil equivalent

1 tonne of oil equivalent = 11.63 kWhSource: IEA World Energy Outlook 2006

0

0.5

2.5

1.0

1.5

2.0

20012000 2003 2004 20052002

New business area for biofuel plantsIn 2007 we established a second new business segment in the renewable energies sector: Biofuels. The global market for biofuels is developing very rapidly at the moment. We have managed to achieve initial successes in this area: in Poland and the Netherlands we are cur-rently acting as general contractor in the construction of two turnkey bio-diesel plants with annual capacities of 100,000 and 200,000 tonnes respectively.

In future we will concentrate on sugar-based raw mate-rials, especially sugarcane, that do not compete with the food chain. We assume that demand for this fuel will grow significantly in the coming years: bioetha-nol’s high octane rating translates into low CO and NOx emissions in passenger vehicle engines. CO2 emissions are also reduced considerably, as the plants absorb about the same amount of CO2 while they grow as the amount released by engines in the combustion proc-ess. Mandatory blending such as in Brazil (22 percent) is expected in future.

Since the price of petroleum has risen considerably, we expect today’s generally regional structure of bioetha-nol production to become globalised. Production and consumption are diverging and the distance between them is growing. Focussing on Latin America and South East Asia in particular, we are concentrating on coun-tries that have the necessary climatic, economic and political conditions to produce biofuels economically. In 2007 we began work on initial projects; we expect to book orders in 2008.

As soon as the relevant technologies become available, we plan to expand our spectrum to second-generation biofuels. Biofuel plants will then no longer convert only agricultural products based on sugar, starch or oil, but rather entire plants that can be processed further into biofuels by means of synthetic processes. This will raise yield severalfold and protect land necessary for farming. Raw materials such as straw and scrap wood, which have no other use and do not compete with food production, can then be used extensively.

France

Germany Italy

Rest of Europe

USA

Others

Worldwide production of bio-diesel

07 MANAGEMENT REPORT

Industrial Projects business segment formedWe have merged the traditional business units Power, Metallurgy and Oil & Gas into Industrial Projects. This combining of skills and resources increases flexibility in the project management and engineering of major projects by making it easier for employees to switch from one project to another. Free exchange as a func-tion of workload enables us to optimise the processes used in preparing quotations and carrying out projects and to combine capacities around lucrative projects.

KOCH de Portugal taken overWe have also strengthened the Industrial Projects busi-ness segment through the takeover of the Lisbon-based plant construction company KOcH de Portugal. The company specialises in the management and execu-tion of large-scale industrial projects and focuses in particular on the construction of power plants. This acquisition helps us further strengthen Industrial Projects. KOCH de Portugal’s list of plant construction references includes a number of major clients, and it has established a clear corporate profile as an EPC con-tractor with strong expertise in project execution. Along with the turnkey construction of plants, KOCH de Portugal also provides project development services and is using its project execution competence to sup-port Industrial Projects with a series of orders.

Steel trade incorporated in joint ventureIn 2007 we incorporated our steel trade activities with a total turnover of about 1.1 billion euros into a joint venture with ccc Steel GmbH & co. KG of Hamburg, Germany. The new company has been in operation un-der the name coutinho & Ferrostaal GmbH & co. KG since January 1, 2008. MPc Münchmeyer Petersen & co., Grupo Villacero and MAN Ferrostaal each hold a one-third share (33.33 percent) of the new company. In addi-tion, we achieved a profit of 7 million euros.

The steel trade activities of CCC Steel and MAN Ferrostaal complement each other: there is little overlap, our busi-ness philosophies are very similar and we see very good chances for us to grow together. With a turnover of 2.1 billion euros, the joint venture is one of the world’s lead-ing independently operated steel trading companies. The new joint venture has a workforce of 320 employees in 34 countries at 56 locations worldwide, trading a total vol-ume of nearly five million tonnes of steel products. The main locations are Hamburg, Houston and Essen.

91

Millions of tonnes of oil equivalent

1 tonne of oil equivalent = 11.63 kWh Source: IEA World Energy Outlook 2006

0

4

8

12

16

20

2000 2001 2002 2003 2004 2005

Worldwide production of bioethanol

India

OthersUSA

Brazil

China

EU

07 MANAGEMENT REPORT

92

International organisation focusedIn China, having opened the MAN House in Beijing, we have also established MAN Ferrostaal co. Ltd. in Beijing. The new company’s primary activity will be in the ma-chine business. On the one hand we aim to use the company to market equipment from foreign manufac-turers, especially German ones, in China and to provide the associated after-sales service. At the same time, we plan to use the company to provide Chinese machines for the worldwide sales organisation of our Equipment business segment.

As in previous years, we have continued to sharpen our profile through the divestment of marginal activities. Within the MAN Group we sold off various activities to sister companies, including 25 percent plus one share of MAN Ltd. in London, in which we previously held a 75 percent stake. In view of the fact that this company is almost exclusively concerned with providing service for turbomachinery, MAN Turbo has taken over this share. The same principle applies to the bus assembly operations that we built up in Mexico in past years, and on the basis of which we established a sales and service organisation in that country: we have transferred this business to MAN Nutzfahrzeuge.

We sold 66 percent of the Luxembourg-based company Eurotecnica Melamine S.A., a licensee for the produc-tion of melamine, to our partner in Trinidad, clico Energy Ltd. The remaining 34 percent share ensures our company’s continued access to this technology. With Eurotecnica we are currently erecting a melamine plant in Trinidad. We sold the steel construction operation DSD Venezuela to Pirson Steel construction AG, Switzer-land, and construzioni cimolai Armando S.p.A., Italy; at the end of 2007 we also sold our remaining 49 percent share in the DSD Steel Group. We retain access to the services of this former business segment without hav-ing to carry any risk of our own.

07 MANAGEMENT REPORT

93

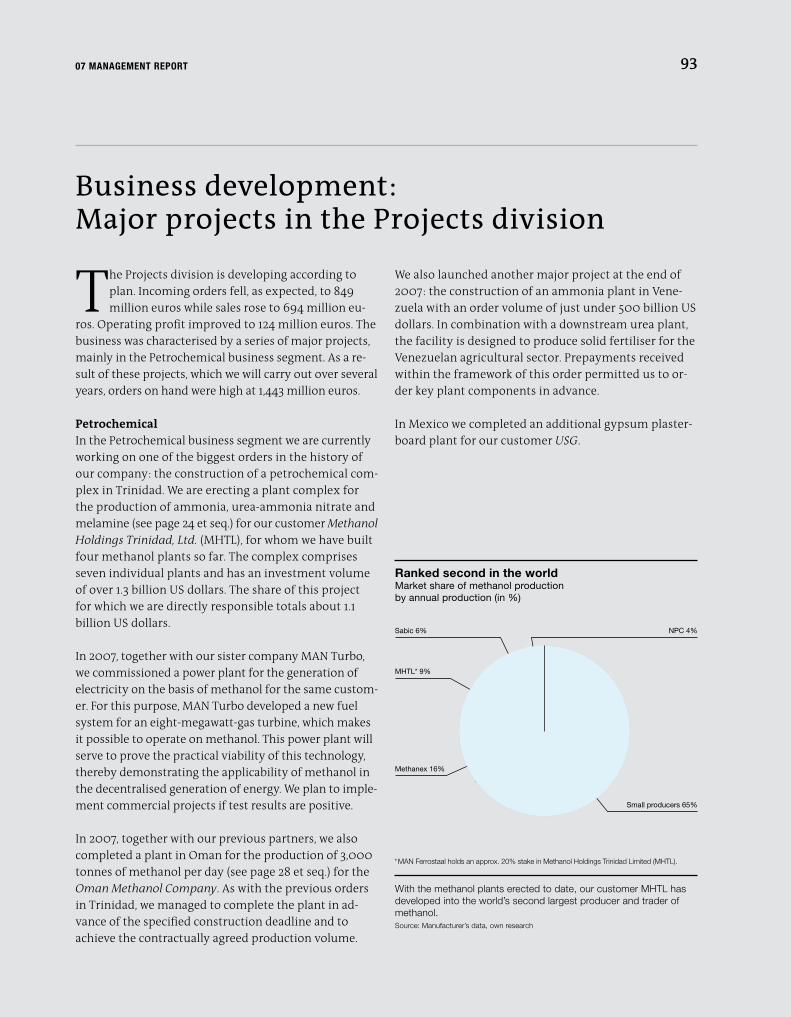

Business development: Major projects in the Projects division

The Projects division is developing according to plan. Incoming orders fell, as expected, to 849 million euros while sales rose to 694 million eu-

ros. Operating profit improved to 124 million euros. The business was characterised by a series of major projects, mainly in the Petrochemical business segment. As a re-sult of these projects, which we will carry out over several years, orders on hand were high at 1,443 million euros.

PetrochemicalIn the Petrochemical business segment we are currently working on one of the biggest orders in the history of our company: the construction of a petrochemical com-plex in Trinidad. We are erecting a plant complex for the production of ammonia, urea-ammonia nitrate and melamine (see page 24 et seq.) for our customer Methanol Holdings Trinidad, Ltd. (MHTL), for whom we have built four methanol plants so far. The complex comprises seven individual plants and has an investment volume of over 1.3 billion US dollars. The share of this project for which we are directly responsible totals about 1.1 billion US dollars.

In 2007, together with our sister company MAN Turbo, we commissioned a power plant for the generation of electricity on the basis of methanol for the same custom-er. For this purpose, MAN Turbo developed a new fuel system for an eight-megawatt-gas turbine, which makes it possible to operate on methanol. This power plant will serve to prove the practical viability of this technology, thereby demonstrating the applicability of methanol in the decentralised generation of energy. We plan to imple-ment commercial projects if test results are positive.

In 2007, together with our previous partners, we also completed a plant in Oman for the production of 3,000 tonnes of methanol per day (see page 28 et seq.) for the Oman Methanol company. As with the previous orders in Trinidad, we managed to complete the plant in ad-vance of the specified construction deadline and to achieve the contractually agreed production volume.

We also launched another major project at the end of 2007: the construction of an ammonia plant in Vene-zuela with an order volume of just under 500 billion US dollars. In combination with a downstream urea plant, the facility is designed to produce solid fertiliser for the Venezuelan agricultural sector. Prepayments received within the framework of this order permitted us to or-der key plant components in advance.

In Mexico we completed an additional gypsum plaster-board plant for our customer USG.

NPC 4%

Small producers 65%

Sabic 6%

MHTL* 9%

Methanex 16%

Ranked second in the worldMarket share of methanol production by annual production (in %)

With the methanol plants erected to date, our customer MHTL has developed into the world’s second largest producer and trader of methanol.Source: Manufacturer’s data, own research

* MAN Ferrostaal holds an approx. 20% stake in Methanol Holdings Trinidad Limited (MHTL).

07 MANAGEMENT REPORT

Suitability for solarthermal power plants: ■ excellent ■ good ■ fair ■ poor

94

Solar business segmentWe established the Solar business segment in 2007, where we acquired stakes in two holdings and launched one joint venture. The operational business in these areas is focussed on the development of projects. Since the value in euros of projects in these businesses generally runs in the eight- to nine-figure range, the preliminary phases of project development typically last several years before larger orders can be expected. We have a high level of confidence concerning our prospective entry into a project in Spain (Andasol 3) developed by our partner Solar Millennium.

We have provided the personnel resources required to implement major projects for electrical output of up to 250 megawatts. In our joint venture MAN Solar Millennium, for example, we have significantly increased

the number of employees – primarily engineers with experience in the energy sector – and plan to recruit more personnel over the course of 2008. The projects that we are developing within the framework of the joint venture lie along the Earth’s sunbelt.

One key event of 2007 was the start-up of a Fresnel test plant in Almeriá, Spain (see page 32 et seq.). The one-megawatt plant is designed to run for one and a half years under real world conditions and to prove the practical viability of this development during that period of time. The test results generated so far are highly promising and we expect to commercialise this technology within the next few years. The attraction of this technology lies in the economic benefits it is ex-pected to provide over the long term owing to the type of construction.

07 MANAGEMENT REPORT

95

Biofuels business segmentThe Biofuels business segment is being systematically equipped to become a focus of strategic competence. Current activities are focussed on first-generation bio-fuels. In future, the focus will be on second-generation technologies.

With the strategic reorientation in this global market, MAN Ferrostaal is focussing on industrial agricultural countries in Latin America and South East Asia charac-terised by sustainability and competitive raw materials for biofuels. The business segment is being strengthened by highly qualified employees who bring not only many years of industry experience, but also technological ex-pertise. We managed to recruit Dr. Stefan Reimelt, for example, a recognised expert in this area who has joined our Executive Board.

As general contractor for the Polish Lotos Group, we erected a turnkey bio-diesel plant. Construction began in early 2007 and start-up was May 2008. The plant is designed for a capacity of 100,000 tonnes per annum. We are erecting another bio-diesel plant with a capacity of 200,000 tonnes for J&S Bio Energy B.V. in the Nether-lands. This plant is scheduled to go into operation in 2009. The investment volume of the two plants totals just under 70 million euros. In bio-diesel production we hold a worldwide licence from Ölmühle Leer connemann GmbH (a subsidiary of the US ADM Group) for the application of what is referred to as the CD process (continuous deglycerolisation), which is being used in the two plants in Poland and the Netherlands.

Although the market for bio-diesel is currently undergo-ing consolidation, we aim to maintain our commitment in this sector. As with bio-ethanol, worldwide growth is expected to continue in this market, which is becoming increasingly internationalised and dominated by ever larger market players. Our work focuses on Eastern and Western Europe.

Industrial ProjectsIn Industrial Projects we completed a number of large-scale plants in 2007. The largest of these projects in-volved a power plant in Venezuela that we expanded from an output of 320 to 500 megawatts (see page 36 et seq.) for an order valued at 170 million euros. This

project is extremely important to our customer, the en-ergy provider ENELVEN, because the increase in output is being achieved without additional fuel consumption. This power plant expansion is part of a major infra-structural initiative by the Venezuelan government de-signed to expand the country’s electrical supply net-work. A number of other power plant projects are cur-rently in the development phase. In a consortium with ABB Lummus we added a new production line to a crude oil conditioning plant in Libya owned and operated by Veba Oil, facilitating the connection of 20 new sources of oil. Our role in this project covered procurement, construction, assembly and start-up. In a consortium with Siemens VAI and Paul Wurth, we completed the construction of a blast furnace in Brazil for Arcelor Mittal cST. Our scope of delivery comprised media supply, burdening, the electrical systems and the dedusting unit. On behalf of the consortium we also assumed re-sponsibility for financing the import element of the project as well as for the financial processing and con-cluded these within the framework of the completion.

Most of the larger orders we received in 2007 were in the sectors of oil and gas. In Algeria, within the frame-work of upgrading a gas liquefaction unit of the Algeri-an oil company SONATRAcH, we are assuming responsi-bility for the replacement of heat exchangers and steam condenser. The order is being handled by a range of in-ternational suppliers. For ENI Oil, one of the biggest oil producers in Libya, we are building a water treatment works. The plant separates oil from the water that is pumped into oil deposits to improve yields. In Libya we are also modernising a fire extinguisher system for a tank farm owned by Veba Oil. We are currently building the gas system for an integrated steel works owned by ThyssenKrupp cSA in Brazil. Our services cover project management, engineering, supply, assembly and start-up. For this order we are assuming responsibility for process management and for the use of about one mil-lion cubic metres of blast furnace and converter gas needed each hour, some of which is used in the furnace and some of which is converted to electricity.

Along with these projects we also worked on a number of other large orders that will extend over the course of several years. One of the countries that remained an important partner was Iran: we assumed responsibility

07 MANAGEMENT REPORT

96

for the procurement of the process-specific equipment for a petrochemical plant that will produce basic chemi-cal feedstock for the production of polyurethane foams. The order for the initial phase of the project, which had a volume of 54 million euros, has been completed. A fol-low-up order for the second phase of the project valued at 78 million euros is now in progress. For phases nine and ten of the project for the development of the South Pars gas field, we are handling components and equip-ment valued at 150 million euros. We also supply plant components for the petrochemical industry – for an ethylene cracker within the Olefin 13 petrochemical complex in Ilam, for example. Valued at about 200 mil-lion euros, this order runs until 2011. Another project involves the expansion of an existing 520-megawatt power plant to 830 megawatts. That order has a volume of 70 million euros and will be completed in the second

quarter of 2008. In the expansion of an aluminium smelter, we are assuming responsibility for a scope of delivery valued at nearly 140 million euros that covers engineering, procurement, supply, construction and as-sembly as well as the installation and start-up of all plant components. The expansion is scheduled for com-pletion in 2008. In the expansion of a cement factory, we are supplying machinery and components such as crushers, conveyor systems, furnaces and filling units. This order is also scheduled for completion in 2008. Under contract for the government of Mauritania we are conducting a study of strategic importance in which we are analysing the economic feasibility of developing a new ore mine estimated to hold some 650 million tonnes of iron ore.

Services: stable, growing business

In 2007 the key indicators of our Services division showed continued improvement. Incoming orders rose to 707 million euros while sales rose to 751 mil-

lion euros. At the end of 2007, orders on hand totalled 972 million euros, which was slightly below the previous year’s level. The Automotive and Equipment Solutions business units formed the sustainably profitable core of our business once again in 2007. Along with the success-ful implementation of our offset programme in the Republic of South Africa, the sale of the commercial vehicle activities in Mexico improved our result.

AutomotiveThe Automotive business segment is dominated by solid business: the assembly of individual parts into complete modules, which we deliver to automotive manufacturers’ assembly lines on a just-in-sequence basis, follows the cyclical pattern of the models. Our business is essentially influenced by the customers’ acceptance of the vehicle models we supply modules to and by the utilisation of the manufacturing capacity of the relevant factories. As demand for several Ford vehicle models was particularly

high, we were able to utilise our full capacity in the asso-ciated factories.

For the first time, we assumed responsibility for the as-sembly of complete cockpits for major customers. This module is of interest to us not only for its high number of components, but also because it reflects the overall complexity of the car: all vehicle functions are controlled from the cockpit. We successfully integrated orders for the assembly of complete doors into our process compe-tence. We were able to start filling a follow-up order for our customer GM Europe at our operation in Rüsselshe-im. We also commenced delivery of a wide range of addi-tional services at the GM location in Bochum.

EquipmentThe Equipment business segment also has a very stable structure based on our partnerships with customers and suppliers built up over the course of many years. We are the sales and service partner for manufactur-ers of capital goods, primarily printing, plastics processing and packaging machinery, machine tools

07 MANAGEMENT REPORT

97

and individual machines as well as conveyor systems and pipelines.

Our most important supply partners in 2007 included MAN Roland, Ryobi and Achenbach. In many countries, we represent our sister companies MAN Diesel and MAN Turbo. Our range of supply also includes more and more products from India and China. Our custom-ers are primarily based in the regions of South America, Asia-Pacific, Africa and Eastern Europe. In 2007 we seized the opportunity to expand our distribution net-work further and to develop new regions such as the Middle East and the CIS.

In printing machinery we already rank among the world’s leading independent suppliers. The market for packaging machinery is a strategic growth market of global signifi-cance, especially in emerging countries. We have expand-ed our worldwide operations in this area accordingly by representing established manufacturers. We were able to hand over two system lines for food production to cus-tomers in Africa; in China we delivered five rolling mills for aluminium foil.

We were able to build up our position through the vertical expansion of our service portfolio for our target groups.

In Mexico, after the successful expansion of a manufac-turing facility for buses as well as the associated service network, we transferred the activity to our sister compa-ny MAN Nutzfahrzeuge within the framework of an asset deal. We continue to provide support to major customers of strategic importance to our Mexican subsidiary. In 2007 we took orders to supply a total of more than 400 passenger coaches for urban rail systems in Hungary and Bulgaria.

We supplied pipe and piping accessories to the process industry and its suppliers in 2007 in Germany, Europe, Asia and the Middle East. One of the largest of these projects was for an order valued at 33 million euros to supply a 46-kilometre-long pipeline for LUOc, the local subsidiary of Lukoil in Uzbekistan. The key factor in signing this order was the fact that we represent suppli-ers from Western Europe with a good reputation in East-ern Europe. The Pearl GTL Project involves a petrochemi-cal complex in Qatar where natural gas will be used to

produce 140,000 barrels per day of liquid hydrocarbons including naphtha, GTL fuels, paraffin, kerosene and lu-bricants as well as 120,000 barrels per day of condensate, liquefied petroleum gas and ethane. For this project we are supplying the complete piping for the world’s largest air separation plant. In Germany we further expanded our service business in which we provide procurement, storage and just-in-time delivery for our customers.

GovernmentalIn the Governmental business segment we achieved sub-stantial successes in 2007: we considerably reduced the offset obligations in South Africa that we had incurred through the sale of three submarines from the HDW ship-yard in Kiel, Germany. This makes us the first company that has provided offset goods and services in South Afri-ca valued at three billion euros. Our close collaboration with the South African ministries led to a strategic part-nership with the Department of Trade and Industry. This represents a basic prerequisite for future use of our offset expertise as a service provided for third parties.

One milestone in connection with this was the handover of a production facility for oil platforms in Saldanha Bay, Western Cape (see page 40 et seq.). Moreover we deliv-ered ahead of schedule and under budget. In the course the limelight of the official opening ceremonies hosted by the acting President of South Africa, our project partner Grinaker negotiated supply agreements totalling 450 million US dollars. The key factor in the high offset value of this project is the creation of a large number of jobs. Together with a second platform dockyard in Cape Town, the realisation of which we are currently following, some 12,000 jobs are being created directly at the dock-yards and in their surroundings.

Two other offset projects that we started in 2007 are also having a very positive effect on the South African job market: the cleanup of a tea plantation in Limpopo province and the modernisation of a ship lifting and refitting station for sailing yachts in the harbour of Saldanha Bay. The latter project is creating additional capacity for about 400 sailing yachts per year and per-mits the South African yacht industry to expand its business significantly. This is also yet another example of how to safeguard existing jobs and create new em-ployment in South Africa.

07 MANAGEMENT REPORT

98

ShipsIn the Ships business segment we completed a phase of strategic further development. Having initially taken over the commercial operations relative to the construction of cargo ships and tankers, in 2007 we concentrated on the construction of anchor handling tugs. With the handover of the most powerful ocean tug built in Eu-rope, we managed to improve our position in offshore services even further. This segment is of interest to us as we have good know-how and contacts with the custom-ers in the oil and gas industry. We anticipate a substantial increase in demand in this sector in coming years trig-gered by dwindling production volumes in easily accessi-ble regions. The development of oil and gas reserves on modern offshore platforms will become more and more important as a result. This requires technical equipment such as powerful tugs in ocean-going applications.

We delivered three tugs in 2007, one of which has a bol-lard pull of 100 tonnes and two with a bollard pull of more than 200 tonnes, Taurus and Janus, as well as two safety chemical oil tankers (SCOTs) No. 9 and 10, Wappen von Dresden and Wappen von Nürnberg, from a series of twelve ships in all. Five more tugs are currently under construction: two with a bollard pull of 100 and 280 tonnes, respectively, and one with 220 tonnes, plus the last two SCOT tankers. Further evidence of our focus on the offshore area can be seen in the receipt of orders for two platform supply vessels. When these ships reach the market in 2009 and 2010, they will be among the most modern of their kind. As these special ships serve only a very small segment, transparency is relatively high for us and market development is predictable.

Workforce

Year 2007 2006 Difference

Employees including temporary employees 4,687 4,879 – 192

Projects 1,176 1,296 – 120

Services 3,145 3,238 – 93

Headquarters 366 345 21

Headcount 4,175 4,290 – 115

Germany 2,229 2,271 – 42

Abroad 1,946 2,019 – 73

Temporary employees 512 589 – 77

Germany 419 444 – 25

Abroad 93 145 – 52

Employees including temporary employees 4,687 4,879 – 192

Germany 2,648 2,715 – 67

Abroad 2,039 2,164 – 125

Labour cost in € million 216 203 13

Labour cost per employee in € 51,715 47,418 4,297

Trainees (not included in the headcount) 56 62 – 6

07 MANAGEMENT REPORT

99

Our business success relies on the commitment and experience of our 4,175 employees. Every day they apply their broad wealth of experi-

ence in the development of large-scale plant projects and in the operation of an extensive distribution net-work, giving customers, investors and business partners new reasons to choose MAN Ferrostaal. Numerous in-ternational deployments, an open corporate culture, and professional personnel support and employee de-velopment are the factors which form the foundation of their skills.

The size of the MAN Ferrostaal workforce diminished only slightly versus the previous year. As of year-end, the company employed 4,175 persons worldwide (previ-ous year: 4,290). The number of employees hence fell by 115 (3 percent) compared with the previous year.

In Projects the number of employees fell by 9 percent to 1,176 (previous year: 1,296). As a result of our focus on the strategic business sectors of “Energy and Fuels”, the operations of Metallwerk Elisenhütte GmbH Nassau were sold off (144 employees) in 2007. Moreover the op-erations of DSD Venezuela, such as the construction of boilers, have been outsourced (72 employees). Our competence in the execution of major plant projects – especially in power plant construction – has been strengthened through the acquisition of the Portu-guese company KOCH de Portugal (KdP). These 131 new employees were successfully integrated in 2007.

The number of employees in Services remained essen-tially unchanged. As of year-end 2007, a total of 3,145 persons were employed (previous year: 3,238). In addi-tion, the Automotive business segment employs approxi- mately 500 contractors at various European locations in order to be able to react flexibly to the customers’ changing process requirements.

As was already the case in the previous year, workforce statistics do not reflect the employees from the steel trade business of MAN Ferrostaal. Within the context of the fusion of the steel trade business of MAN Ferrostaal with the operations of CCC Steel GmbH & Co. KG in Ham-burg, around 150 former MAN Ferrostaal employees have been transferred to Coutinho & Ferrostaal GmbH & Co. KG, which was established on January 1, 2008.

Personnel support and employee developmentAs project developers and project managers, qualified employees are our most important resource. For this reason, MAN Ferrostaal goes to great lengths to train and develop its current employees according to their potential and leanings. We certify our employees in Germany and abroad within the framework of an inter-nationally recognised project management qualification, for example. Moreover employees can choose from a wide range of accredited further education offerings.

Within the framework of our trainee programme, we are able to attract exceptionally well-trained university graduates to our company. Along with the interesting assignments at MAN Ferrostaal, the variety we offer and the international character of our company are the key factors behind the numerous job applications we receive. The specifically tailored professional training programmes we offer represent a further focal point of our employee recruitment.

07 MANAGEMENT REPORT

100

Risk management

The responsible handling of opportunities and risks is of crucial importance in the large-scale plant business as well as in the service business.

The identification of opportunities and risks, their appropriate assessment, and the early incorporation of the results of those assessments in the decision-making process are key to the success of our company. For this reason, risk management is a management task. For operational purposes, risk management is handled by a service unit of the same name.

Our risk policy is an expression of our efforts to secure lasting growth and improve the value of our company. We accept orders only when we deem the associated risks to be acceptable and manageable.

The normative framework of our risk management sys-tem is established by MAN Group guidelines – especial-ly the MAN Risk Management Handbook. Adequate management and control systems tailored to the spe-cific concerns of our company are used to apply the rules governing the identification, assessment and con-trol of significant risks throughout the company.

Risk reporting – incorporation of the international networkAs an internationally oriented project developer and project manager, MAN Ferrostaal is active in a large number of markets. The opportunities and risks that must be weighed against each other by the employees of our company are no less varied.

Owing to the country-specific nature of many risks, these are initially assessed by the relevant national and international business units. As a uniform tool, risks are recorded in a standardised risk catalogue every three months and analysed with regard to the prospective amount of damage they may cause and their probabili-ty of occurring. In parallel, central units assess the ap-propriateness of the measures being applied and of those planned.

This ensures that possible risks are reported early on to the Executive Board, the Supervisory Board and MAN AG from a variety of sources.

Thinking of the future soonerMAN Ferrostaal has established a so-called Risk Board as a central control and management body for risk management systems. Its members are experts from operating areas and services departments. The Risk Board submits qualified opportunity and risk assess-ments along with recommendations for further action to the Executive Board at regular intervals.

Internal Audit critically examines our company’s risk management instruments and constructively contrib-utes to continuous improvement in the functionality and efficiency of the tools used. MAN AG Audit performs checks on the basis of random samples – at construction sites, for example – in order to verify the practical im-plementation of the measures used. Moreover there is ad hoc reporting to and by the risk coordinator if the risk situation changes significantly between regularly scheduled reporting dates.

Opportunity and risk fields – at a glanceNumerous opportunities and risks can have an impact on the business development of our company. Some of these are presented below.

MarketOwing to the company’s international orientation, MAN Ferrostaal is subject to a wide range of complex market risks. This situation has considerable advantages, however: thanks to this international character and to phase-delayed business cycles, we are in a position to compensate for international risks. This results in constant business development.

Rising raw material prices harbour risks. However, they also present us with great potential: we reap greater benefits from increasing investments and infrastruc-ture projects undertaken by booming industry sectors, such as the oil and gas industry. Similarly we profit

07 MANAGEMENT REPORT

101

from sustained growth in the demand for plants used to produce alternative energies.

Risks can also stem from the price policy of individual competitors. In order to circumvent a ruinous competi-tive environment, MAN Ferrostaal is focused on a proven business model. This does not principally rely on parti-cipation in tenders, but rather promotes the develop-ment of our own projects and supports highly attractive projects with equity. This enables us to achieve substan-tial margins. The Services division uses a very similar approach: here we counter the price risk by offering in-teresting overall concepts that often include financing or counter-trades. In this way, we are developing a par-ticularly friendly and collegial relationship with our customers in this area, too.

Political risksMany of our strategic target markets are situated in the world’s growth regions. Such regions are not infrequent-ly marked by political instability. Built up over the course of several decades, our market knowledge com-bines with our constantly expanding local presence to offer us profound insights into regions that might ap-pear precarious to others. On this basis, actual local conditions become assessable within the framework of a risk assessment. Moreover, changes that occur can be anticipated ahead of time.

Execution risksAs a general contractor, we confront various contract and order risks, particularly in the Projects division. Sources of uncertainty include contract formulation, commercial execution and, above all, technical risks. Failure to manage these aspects adequately can cause delays during the realisation and start-up of plants, leading in turn to added costs.

We use a series of tools to manage these risks effective-ly and efficiently. A computer-aided project controlling system specifically tailored to meet our needs, for ex-ample, ensures process quality throughout the course of project and order execution.

Moreover, we work only with trusted partners who possess tried-and-tested methods and technologies. Subcontractors are regularly put through stringent quality and credit assessments.

Financial risksWe achieve over 80 percent of our turnover from inter-national business and are therefore exposed to non-neg-ligible levels of currency and financing risk. Where in-voicing in euros cannot be negotiated or procurement in foreign currency cannot be avoided, we apply active financial management to minimise the resulting risks. As a matter of standard practice, we monitor the world’s currency markets, perform credit checks, cooperate with renowned banks, carry credit insurance, and make use of intelligent financing concepts.

Personnel risksAs project developers and managers of large-scale plant projects, our primary function is not that of an engi-neering or installation firm, but rather that of a think tank. Our most important resource is our workforce. Against this background, we also monitor personnel risks, in particular those risks that may result from em-ployee turnover and inadequate qualification. Apart from continuous advanced training and success-orient-ed remuneration for our employees, we place special emphasis on the proper staffing of our project teams. Numerous instruments, such as a well-structured succession planning are used, as in the recruiting of university graduates.

07 MANAGEMENT REPORT

102

Quality management

As project managers with global operations on the market for energy and fuels and as opera-tors of a worldwide network, our challenge is to

meet the highest standards of quality in our goods and services. We guarantee the reliability of our products and services. In order to maintain these distinctive characteristics, we have implemented a modern quality management system and are certified according to the international standard DIN EN ISO 9001:2000.

Available for use by all employees – for the customer's benefitThe quality management system, which is applicable across the entire Group, represents an integral part of our daily work. All necessary regulations are presented here in transparent form. At the same time, documents and checklists for core processes are stored together in a central database as an aid to all employees. The quali-ty management system provides our employees with a major tool for controlling workflows and avoiding mis-takes. Early recognition of errors pays dividends, be-cause the later an error is discovered, the more it costs to correct it.

Sophisticated systemOur quality management system distinguishes between managerial, core and support processes. Managerial processes are used to direct and manage our company. Here, the strategy, planning and targets for the business operation are set out and monitored. In so doing, we pay particular attention to staff qualifications and risk management. Core processes comprise the actual, value-creating business activity of MAN Ferrostaal. They con-sist of a system of clearly defined working steps – rang-ing from the formulation of the project idea, through the execution of the project, to final after-sales services. Besides project management, contractual and financial management count as some of the most important core processes at MAN Ferrostaal. Support processes com-prise all activities that guarantee the smooth running of core and managerial processes. Our comprehensive quality management system mirrors the performance of our products and services: economical, technologi-

cally advanced, consistent implementation carried out rapidly and with high product quality.

Lived quality cultureThe planning, implementation, monitoring and im-provement of our quality management system are initi-ated and controlled by the Quality Management service unit – because we take our responsibility seriously. In ad-dition to this, process owners with cross-departmental functions are responsible for key sub-processes within the company. Each and every employee is responsible for complying with our quality standards. Our system not only enables us to maintain our high standards, but also fosters our employees’ creativity, personal responsibility, motivation and qualification. Because quality manage-ment cannot be applied successfully without a motivat-ed and responsible workforce.

Continuous improvementAll of our company’s processes and procedures are con-stantly examined within the framework of a continu-ous improvement process. In order to raise our level of quality, we continuously implement improvement po-tentials identified during regular internal and external audits. We consider ongoing employee training as an essential task.

In this way we ensure that products and services “made by MAN Ferrostaal” will also continue to maintain the world’s highest quality standards in future.

07 MANAGEMENT REPORT

103

Outlook

Our goal is to establish MAN Ferrostaal as the lead-

ing developer and manager of major industrial

plant projects for the energy and fuels industry.

We are well positioned to achieve this objective. Our inte-

grated plant and services business combines with our

strong international presence to form a highly stable busi-

ness. This permits us to limit our exposure to regional eco-

nomic risks while realising opportunities for growth in

countries with expanding economies at the same time.

Moreover, our worldwide orientation in the machinery

business is developing into an ever-stronger basis for our

plant building business. Our own local presence in their

country is often a key factor in our partners’ decision to

place their order with us. This point clearly distinguishes

us from our competitors.

Our business model presents another important competi-

tive advantage: we have no technologies and products of

our own. What might appear to be a weakness at first

glance is actually a tremendous advantage for us: under no

obligation to sell only our own products, we are free to se-

lect the best technologies and products according to the

customer’s preference. Our technology independence also

offers us a high level of flexibility. As a company with no

fixed product structure, it is far easier for us to take advan-

tage of emerging market opportunities.

Our business model places a high value on project devel-

opment. We do not ignore tenders, but we focus nonethe-

less on developing projects ourselves, before we imple-

ment them. In that case the competition is no longer the

benchmark, but rather the project is judged on its own

economic merits. This improves our position. It also im-

proves our customers’ position at the same time, as we tai-

lor the entire project to their needs: starting from the

business model and financing, to technologies and com-

ponents, right through to the final realisation of the

project. We also often help our customers market their

products, and in certain cases we invest capital resources

in a major project. The banks that provide financing see

this as a very solid and attractive business model.

Against this background, a large number of development

opportunities arise for us. The newly formed Solar and Bio-

fuels business segments are good examples. These are two

relatively new markets in which the players are still in the

process of coalescing. As a general contractor for plant

construction with strong technology partners, we are well

positioned here. Many governments want to reduce their

CO2 emissions and are looking for ways to place their en-

ergy and fuel supply system on an increasingly ecological-

ly sound basis. At the same time producers are discovering

that oil and gas are valuable raw materials that are too pre-

cious to burn. Broad independence from specific suppliers

also plays a key role in this context. Renewable energies

are a logical solution for these problems. Many investors

are still looking for the right partners to implement these

projects. We are now in the process of establishing our-

selves as the right partner for these markets. As success

here hinges on establishing a lead position in the market

early, we are forming alliances with companies that have

developed technologies or whose progress in project de-

velopment in this area is already well advanced.

Our traditional businesses also offer good opportunities

for growth. Petrochemical and Industrial Projects serve sec-

tors currently undergoing strong expansion. We are partic-

ipating in this growth, both in basic chemicals and in

fuels as well as in the power plant segment. In the service

business, we see the strongest opportunities for growth in

Automotive and Ships: as an independent service provider

for automobile manufacturers, we can take advantage of

the continuing trend toward outsourcing, and our Ships

business segment is well positioned to serve the growing

offshore oil market. Our strong presence outside of Germany

is based on the sales organisation in our Equipment busi-

ness segment, which we plan to continue expanding in

future. It is an ideal starting point from which to intensify

our international plant construction business. Close ties

with our customers in Governmental form a foundation

that can later serve to facilitate the realisation of major

projects.

Overall we anticipate continued positive development in

fiscal year 2008.

07 MANAGEMENT REPORT

104

Key indicators of the subsidiaries in Germany and abroad

Consolidated companies of the MAN Ferrostaal Group

As at December 31, 2007

MAN Ferrostaal Aktiengesellschaft – Essen, Germany - * 1,915 768 723

DSD Asset Management GmbH – Essen, Germany(formerly: MAN Ferrostaal Air Technology GmbH – Essen) 100 300 1 -

MAN Ferrostaal Industrieanlagen GmbH – Geisenheim, Germany 100 272 82 152

MAN Ferrostaal Automotive GmbH – Essen, Germany ** 100 115 146 1,514

SGI Saarländische Gesellschaft für Industriebeteiligungen GmbH – Essen, Germany 100 97 - -

MAN Ferrostaal Industrial Projects GmbH – Essen, Germany 100 71 18 84

MAN Ferrostaal Piping Supply GmbH – Essen, Germany ** 100 44 149 97

DSD de Venezuela, C.A. – Caracas, Venezuela 100 51 31 27

SLS Services GmbH – Saarlouis, Germany 100 39 - 70

DSD Construcciones y Montajes S.A. – Santiago de Chile, Chile 100 34 54 120

MAN Ferrostaal Air Technology GmbH – Saarlouis, Germany 100 28 23 60

MAN Ferrostaal do Brasil Comércio e Indústria Ltda. – São Paulo, Brazil 100 28 10 79

MAN Ferrostaal Methanol International Ltd. – St. Kitts 100 23 - -

Ferrostaal Metals Holding GmbH – Munich, Germany 100 23 - -

SIRIUS Grundstücksgesellschaft mbH & Co. KG – Essen, Germany 100 22 - -

KOCH de Portugal Lda. – Lisbon. Portugal 100 21 20 131

MAN Ferrostaal México S.A. de C.V. – Mexico City, Mexico 100 20 38 88

New Providence Corp. – Panama/Panama 100 19 - -

DSD Grundstücksverwaltungsgesellschaft mbH & Co. KG – Essen, Germany 100 18 - -

MAN Ferrostaal Bausystem GmbH – Bad Honnef, Germany 100 14 37 39

MAN Ferrostaal Procurement Services – Hooge Zwaluwe, Netherlands 100 13 8 8

FERROMARINE Africa (Pty.) Ltd. – Cape Town, South Africa 85 13 - -

Gesellschaft für Vermögensverwaltung mbH – Essen, Germany 100 11 - -

MAN Ferrostaal Australia Pty. Ltd. – Alexandria, Australia 100 9 28 62

MAN Ferrostaal Chile S.A.C. – Santiago de Chile, Chile 100 8 7 64

Fritz Werner Industrieausrüstungen GmbH – Geisenheim, Germany 100 7 2 28

MAN Ferrostaal (Thailand) Co. Ltd. – Bangkok, Thailand 100 7 9 88

Ferrostaal Piping Supply N.V. – Antwerp-Berchem, Belgium 100 7 - -

P.T. MAN Ferrostaal Equipment Solutions – Jakarta, Indonesia 100 6 8 127

MAN Ferrostaal Equipment Solutions (Pty.) Ltd. – Johannesburg, South Africa 100 5 9 46

MAN FS Venezuela – Caracas, Venezuela 100 5 4 31

Printing Products (Pty.) Ltd. – Cape Town, South Africa 100 5 10 41

* Shares held by MAN Ferrostaal Beteiligungs GmbH, Munich.

** Total assets, turnover and workforce including operationally administered subsidiaries.

Capital share

%

Total assets€ mill.

Sales

€ mill.

Employees

Dec 31

07 MANAGEMENT REPORT

105

Consolidated companies of the MAN Ferrostaal Group

As at December 31, 2007

MAN Ferrostaal Malaysia Sdn. Bhd. – Shah Alam, Malaysia 100 4 3 69

MAN Ferrostaal Incorporated – Delaware, USA 100 4 2 7

MAN Ferrostaal de Colombia Ltda. – Bogotá, Colombia 100 4 4 32

MAN Ferrostaal Equipamentos e Soluções Ltda. – São Paulo, Brazil 100 4 10 100

Eisenbau Essen GmbH – Essen, Germany 100 3 11 -

SAGEXPORT S.A. – Levallois Perret, France 100 3 - -

Seibert Immo SARL – Sarralbe, France 100 2 - -

MAN Ferrostaal Diesel Power GmbH – Essen, Germany 100 2 - 2

FME Grundstücksgesellschaft mbH & Co. KG – Essen, Germany 100 2 - -

PT MAN Ferrostaal Indonesia – Jakarta, Indonesia 100 2 5 150

MAN Ferrostaal Singapore Pte. Ltd. – Singapore, Singapore 100 2 2 19

MAN FS Argentina – Buenos Aires, Argentina 100 2 2 28

DSD Construcciones y Montajes S.A. de C.V. – Mexico City, Mexico 100 1 - 40

MAN Ferrostaal NZ Ltd. – Auckland, New Zealand 100 1 2 5

MAN Ferrostaal Philippines Inc. – Parsig City, Philippines 100 1 2 39

Verkehrsentwicklungsgesellschaft Südosteuropa GmbH – Vienna, Austria 99 1 5 -

MAN Ferrostaal Versicherungsvermittlung GmbH – Essen, Germany 100 - - 5

Capital share

%

Total assets€ mill.

Sales

€ mill.

Employees

Dec 31

As at December 31, 2007 Capital share, in %

Consolidated Energy Ltd. – Port of Spain, Trinidad and Tobago 45.45

OMAN Methanol Company L.L.C. – Sohar, Oman 20

Eurotecnica Melamine S.A. – Luxembourg, Luxembourg 34

Eurotecnica Contractors & Engineers S.p.A. – Milan, Italy 34

MAN Ltd. – London, Great Britain 50

SCG SILS Centre Gliwice Sp.z.o.o. – Gliwice, Poland 50

FerroVAZ Gesellsch. für Export, Import und Engineering mbH – Essen, Germany 50

MAN Solar Millennium GmbH – Essen, Germany 50

Coutinho & Ferrostaal GmbH & Co. KG – Hamburg, Germany (formerly CCC Steel GmbH & Co. KG) 33.33

INVESTMENTS REPORTED ACCORDING TO THE EQUITY METHOD

07 MANAGEMENT REPORT

08 FINANCIAl APPENDIx 106

“The first thing one learns in the banking business is respect for the figure zero.”Carl Fürstenberg, A banker at the Berlin-based Handels-Gesellschaft whose financing concepts played a major role in the expansion of heavy industry along the Ruhr during the first decades of the twentieth century. Within the framework of the Treaty of Rapallo (1922), he was the first western banker to enter into major loan relations with the Soviet Union.

10708 FINANCIAl APPENDIx

Financial Appendix

108

The summarized subgroup financial statement of MAN Ferrostaal Aktiengesellschaft for the fiscal year from January 1 to December 31, 2007, comprising the income statement, the balance sheet and the cash flow statement has been derived from the consolidated fi-nancial statements of MAN Ferrostaal Aktiengesellschaft for the fiscal year from January 1 to December 31, 2007. KPMG Deutsche Treuhand-Gesellschaft Aktiengesellschaft audited the consolidated financial statements of MAN Ferrostaal Aktiengesellschaft for the fiscal year from January 1 to December 31, 2007 and it certified these statements without qualification on February 12, 2008.

08 FINANCIAl APPENDIx

109

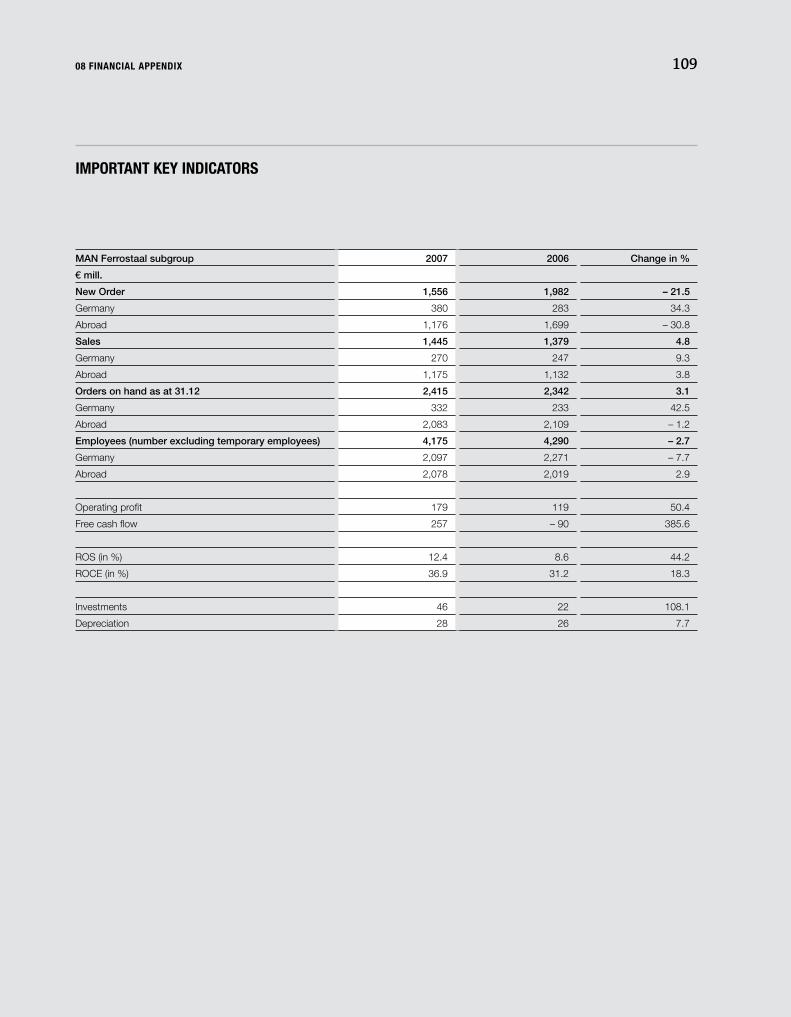

MAN Ferrostaal subgroup 2007 2006 Change in %

€ mill.

New Order 1,556 1,982 – 21.5

Germany 380 283 34.3

Abroad 1,176 1,699 – 30.8

Sales 1,445 1,379 4.8

Germany 270 247 9.3

Abroad 1,175 1,132 3.8

Orders on hand as at 31.12 2,415 2,342 3.1

Germany 332 233 42.5

Abroad 2,083 2,109 – 1.2

Employees (number excluding temporary employees) 4,175 4,290 – 2.7

Germany 2,097 2,271 – 7.7

Abroad 2,078 2,019 2.9

Operating profit 179 119 50.4

Free cash flow 257 – 90 385.6

ROS (in %) 12.4 8.6 44.2

ROCE (in %) 36.9 31.2 18.3

Investments 46 22 108.1

Depreciation 28 26 7.7

IMPORTANT KEY INDICATORS

08 FINANCIAl APPENDIx

110

€ mill. Notes 2007 2006

Net sales [1] 1,445 1,379

Cost of sales – 1,179 – 1,126

Gross margin 266 253

Other operating income [2] 236 179

Selling expenses – 129 – 121

General administrative expenses – 83 – 88

Other operating expenses [3] – 172 – 141

Results of participations shown in the balance sheet

according to the equity method [4] 61 31

Results from financial investments [4] - 6

EBIT 179 119

Interest earned 9 21

Interest expenses – 15 – 59

EBT (earnings before taxes) 173 81

Taxes – 32 – 111

Net result of discontinued operations [5] 15 15

Net income after taxes 156 – 15

Of which minority assets - 7

Of which shares of MAN shareholders 156 – 22

INCOME STATEMENTFISCAL YEAR 2007

08 FINANCIAl APPENDIx

111

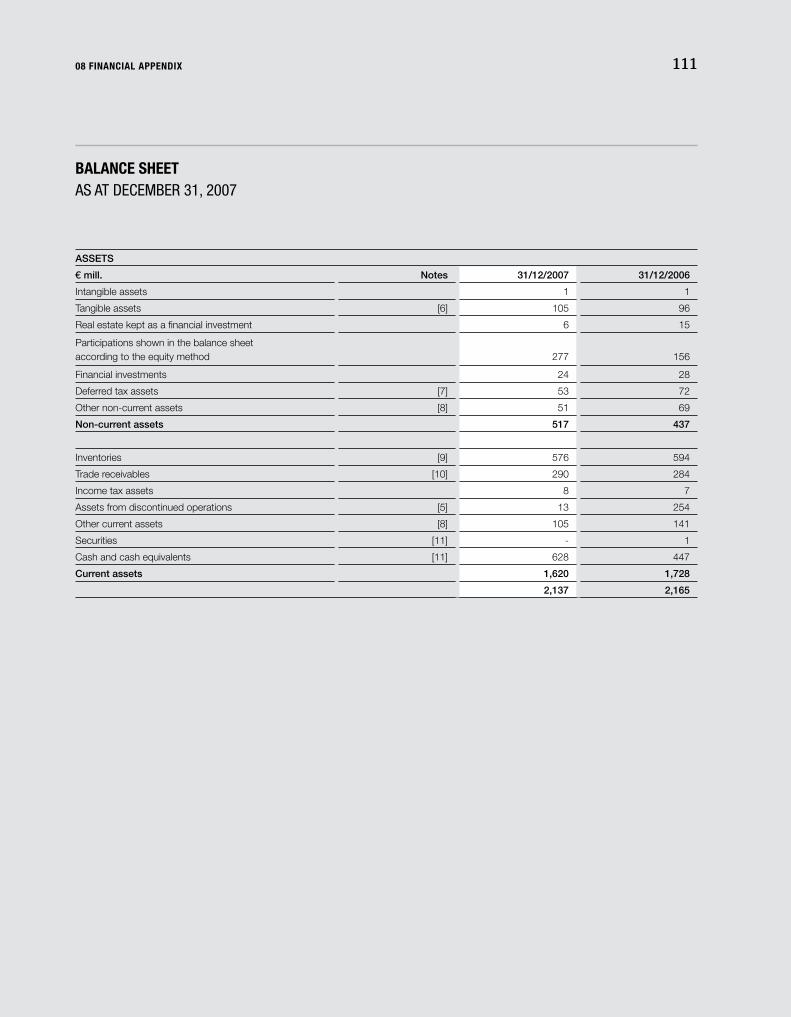

ASSETS

€ mill. Notes 31/12/2007 31/12/2006

Intangible assets 1 1

Tangible assets [6] 105 96

Real estate kept as a financial investment 6 15

Participations shown in the balance sheet according to the equity method 277 156

Financial investments 24 28

Deferred tax assets [7] 53 72

Other non-current assets [8] 51 69

Non-current assets 517 437

Inventories [9] 576 594

Trade receivables [10] 290 284

Income tax assets 8 7

Assets from discontinued operations [5] 13 254

Other current assets [8] 105 141

Securities [11] - 1

Cash and cash equivalents [11] 628 447

Current assets 1,620 1,728

2,137 2,165

BAlANCE SHEET AS AT DECEMBER 31, 2007

08 FINANCIAl APPENDIx

112

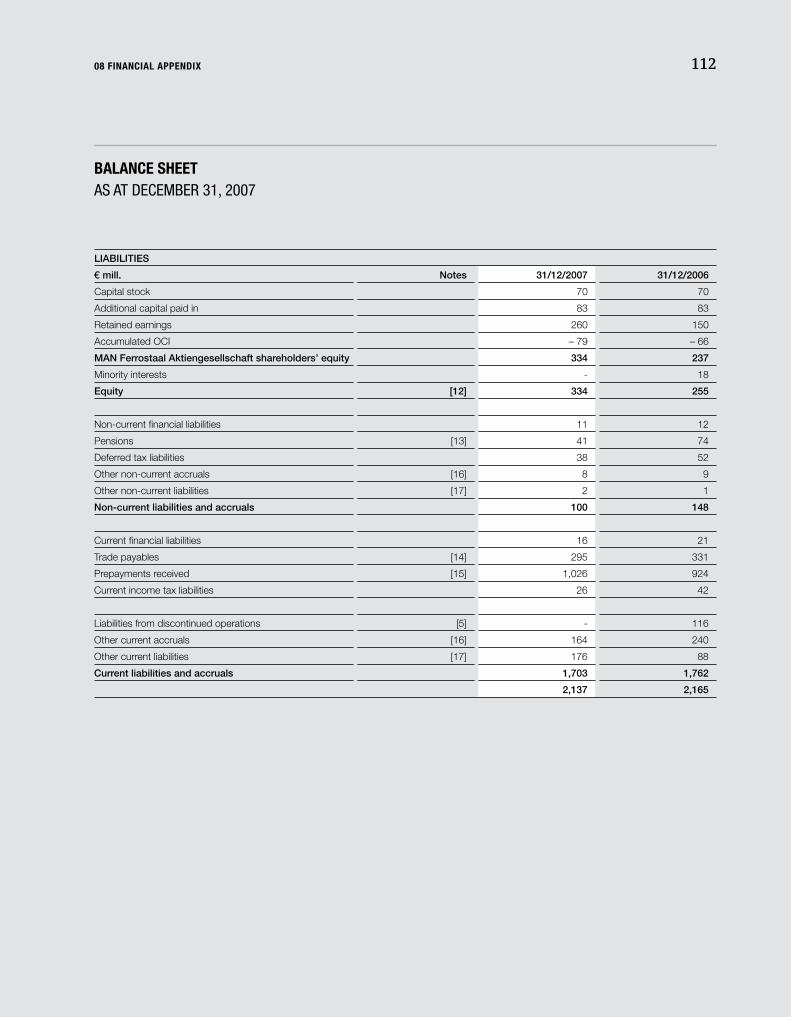

BAlANCE SHEETAS AT DECEMBER 31, 2007

LIABILITIES

€ mill. Notes 31/12/2007 31/12/2006

Capital stock 70 70

Additional capital paid in 83 83

Retained earnings 260 150

Accumulated OCI – 79 – 66

MAN Ferrostaal Aktiengesellschaft shareholders’ equity 334 237

Minority interests - 18

Equity [12] 334 255

Non-current financial liabilities 11 12

Pensions [13] 41 74

Deferred tax liabilities 38 52

Other non-current accruals [16] 8 9

Other non-current liabilities [17] 2 1

Non-current liabilities and accruals 100 148

Current financial liabilities 16 21

Trade payables [14] 295 331

Prepayments received [15] 1,026 924

Current income tax liabilities 26 42

Liabilities from discontinued operations [5] - 116

Other current accruals [16] 164 240

Other current liabilities [17] 176 88

Current liabilities and accruals 1,703 1,762

2,137 2,165

08 FINANCIAl APPENDIx

113

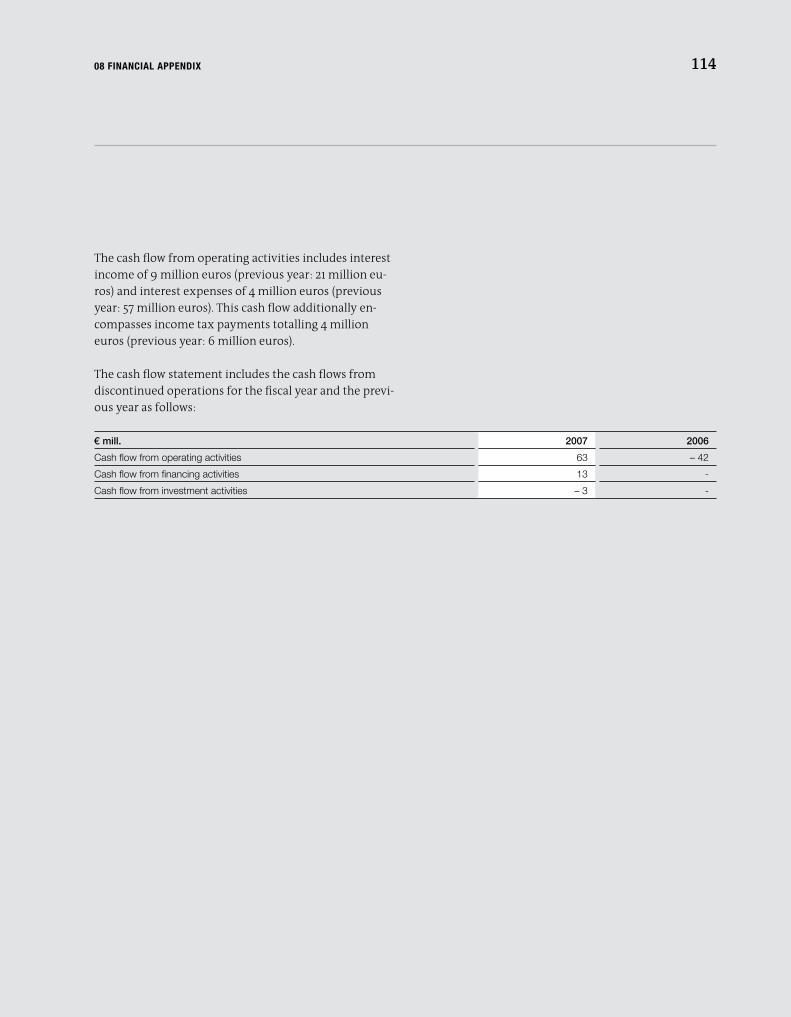

€ mill. 2007 2006

EBT (earnings before taxes) 173 81

Current income taxes – 39 – 57

Depreciation and loss in value of non-current assets 28 26

Changes in pensions – 3 5

Undistributed results from associated affiliates – 63 – 30

Cash earnings discontinued operations 6 15

Cash earnings 102 40

Changes in working capital 125 – 50

Changes in other accruals – 68 – 53

Changes in other assets 43 – 66

Changes in other liabilities 75 – 1

Elimination of the fixed-asset disposal result – 13 -

Other changes in working capital – 4 36

Cash flow from operating activities 260 – 94

Investments – 45 – 22

Income from fixed-asset disposals 23 22

Disposal of discontinued operations 22 4

Cash flow from the investment activity of discontinued operations – 3 -

Cash flow from investment activities – 3 4

Free cash flow from operating and investment activities 257 – 90

Distribution – 31 50

Capital increase 3 -

Disposal (+) and purchase (–) of securities - 170

Cash flow from the financing activities of discontinued operations 13 -

Changes in intra-group financing – 3 18

Social endowment of pension funds – 14 -

Cash flow from financing activities – 32 238

Changes in cash and cash equivalents affecting payments 225 148

Cash and cash equivalents at the start of the fiscal year 447 373

Cash and cash equivalents of discontinued operations at the start of the fiscal year 3 -

Consolidation and parity-rated changes to cash and cash equivalents – 47 – 71

Cash and cash equivalents from discontinued operations revealed in the balance sheet - – 3

Cash and cash equivalents at the end of the fiscal year 628 447

Composition of net liquid assets as at 31/12

Cash and cash equivalents 628 447

Securities - 1

Financial liabilities – 27 – 33

Net liquid assets as at 31/12 601 415

CASH FlOW STATEMENT 2007

08 FINANCIAl APPENDIx

114