Annual Report 2004 - Assa Abloy · cards. The products are sold under well-known brand names such...

90

Security, safety and convenience Annual Report 2004

Transcript of Annual Report 2004 - Assa Abloy · cards. The products are sold under well-known brand names such...

Security, safety and convenience

Annual Report 2004

2004 in brief

Contents

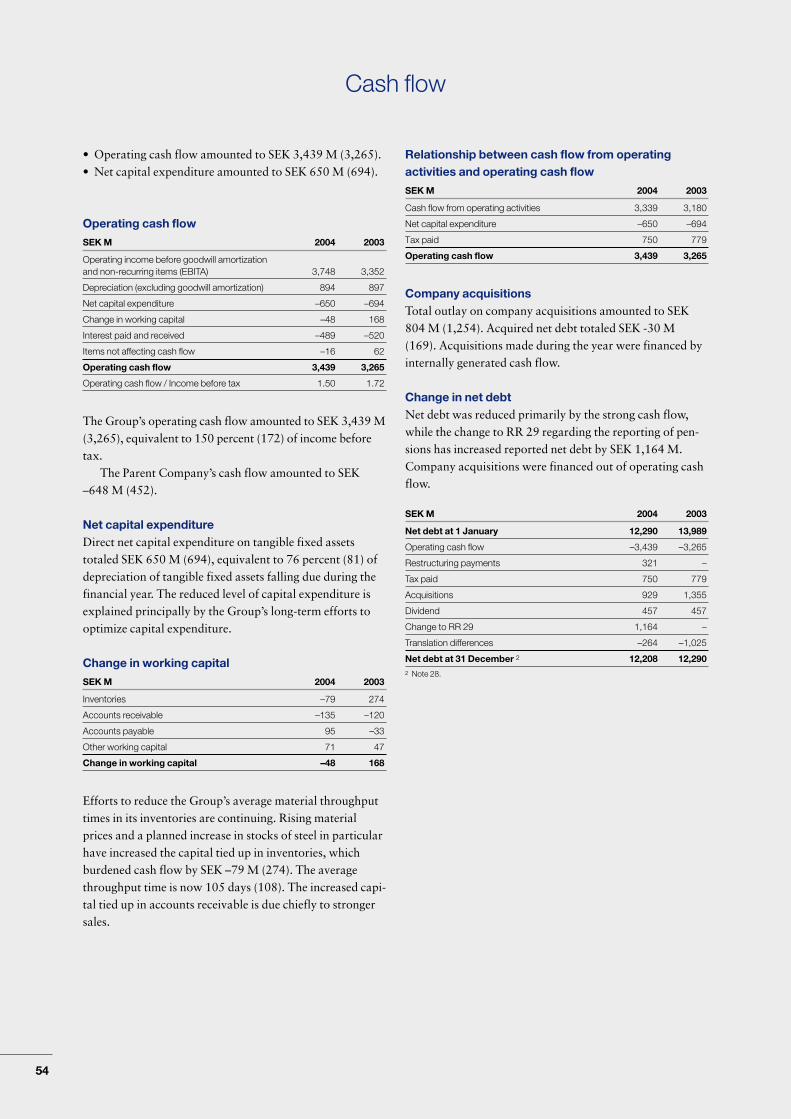

■ Sales increased to SEK 25,526 M (24,080) with organic growth of

5 percent. Exchange-rate effects had a negative impact of SEK 982 M.

■ Operating income before goodwill amortization (EBITA) amounted to

SEK 3,748 M (3,352) – an increase of 12 percent.

■ Earnings per share after tax and full conversion amounted to SEK 4.05

(3.31) – an increase of 22 percent.

■ Operating cash flow increased to SEK 3,439 M (3,265).

■ The two-year Leverage & Growth action program is progressing well,

with a long series of specific activities. Annual savings are expected to

reach SEK 450 M during the second half of 2005.

■ During 2004 ASSA ABLOY reviewed the Group’s strategies, which can

be summarized in three main themes: increasing growth in the current

core business, expanding into new markets and new segments, and

reducing the cost base.

Financials in brief . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

CEO’s statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Vision, Business Concept and strategy . . . . . . . . . . . . . . . 6

Leverage & Growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

The market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

ASSA ABLOY’s products . . . . . . . . . . . . . . . . . . . . . . . . 16

Sustainable development . . . . . . . . . . . . . . . . . . . . . . . . 20

Division EMEA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Division Americas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Division Asia Pacific . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Division Global Technologies . . . . . . . . . . . . . . . . . . . . . . 36

Report of the Board of Directors for 2004 . . . . . . . . . . . . . 42

Corporate governance . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Sales and earnings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

Income statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Results by division . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Financial position . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

Balance sheets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Cash flow . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

Cash flow analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

Changes in shareholders’ equity . . . . . . . . . . . . . . . . . . . 56

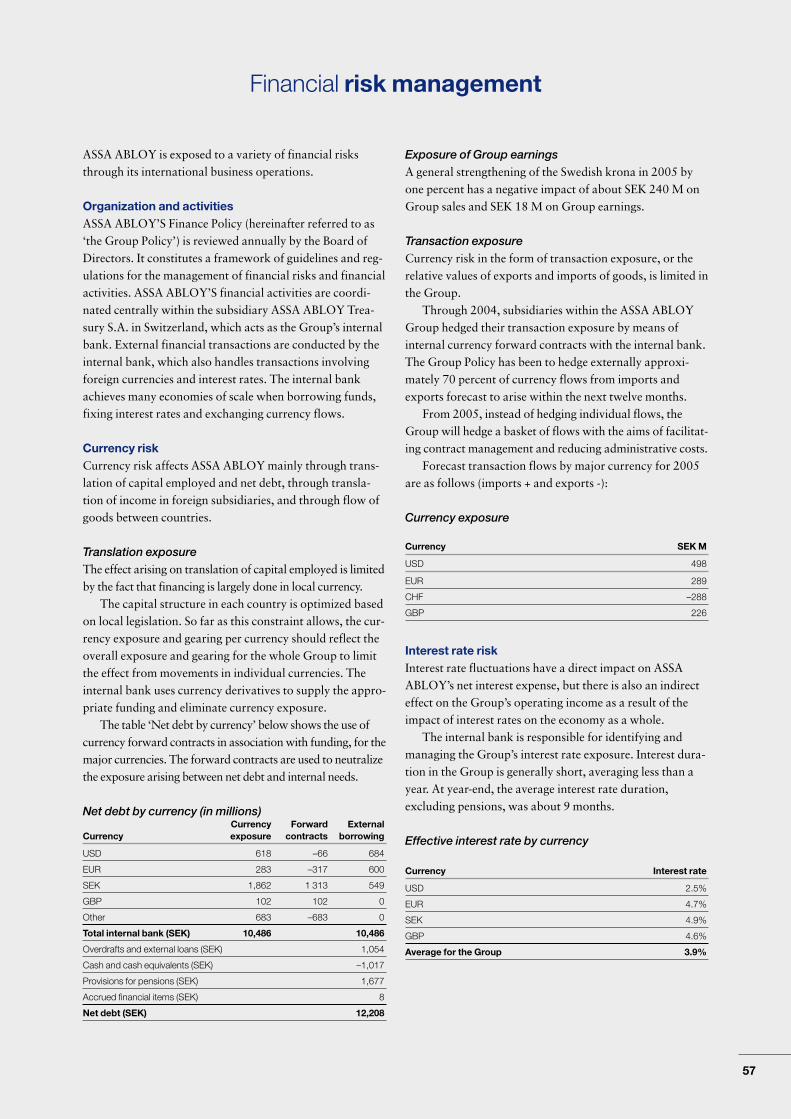

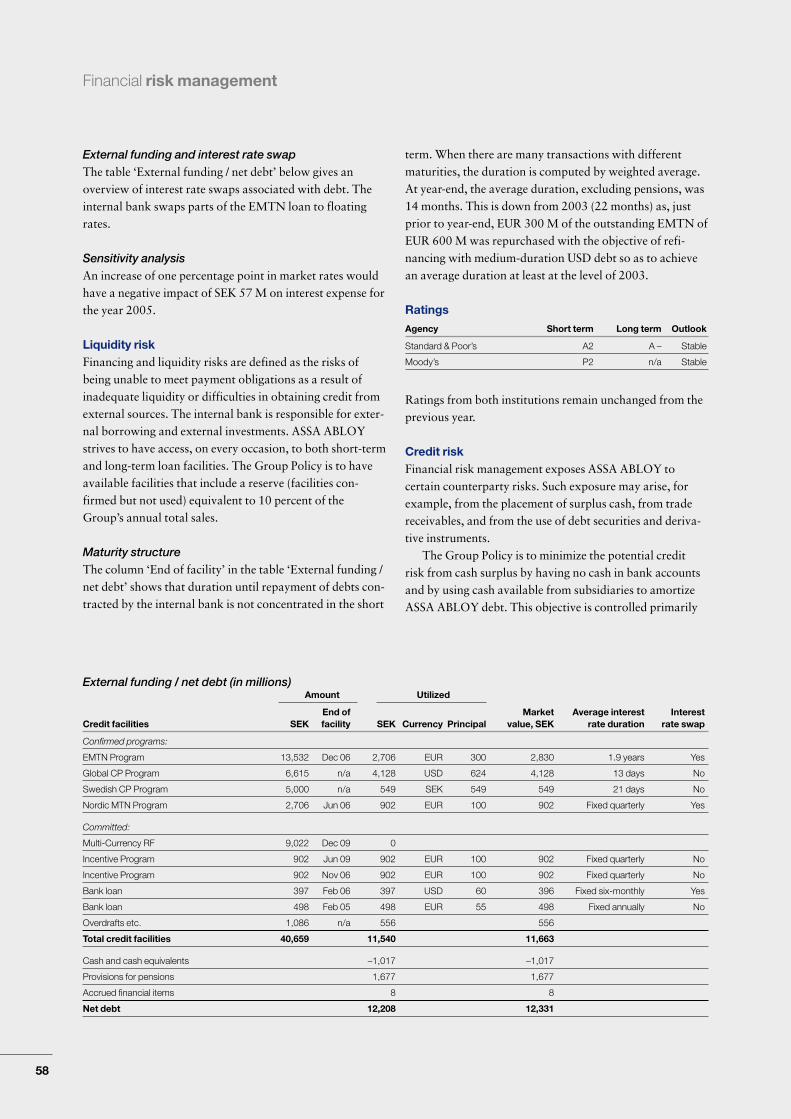

Financial risk management . . . . . . . . . . . . . . . . . . . . . . . 57

Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

Proposed disposition of earnings . . . . . . . . . . . . . . . . . . . 72

Audit report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

Comments on ‘Five years in summary’ . . . . . . . . . . . . . . 74

Five years in summary . . . . . . . . . . . . . . . . . . . . . . . . . . 75

Quarterly information . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

The ASSA ABLOY share . . . . . . . . . . . . . . . . . . . . . . . . . 78

Information for shareholders . . . . . . . . . . . . . . . . . . . . . . 81

Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

Executive Team . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

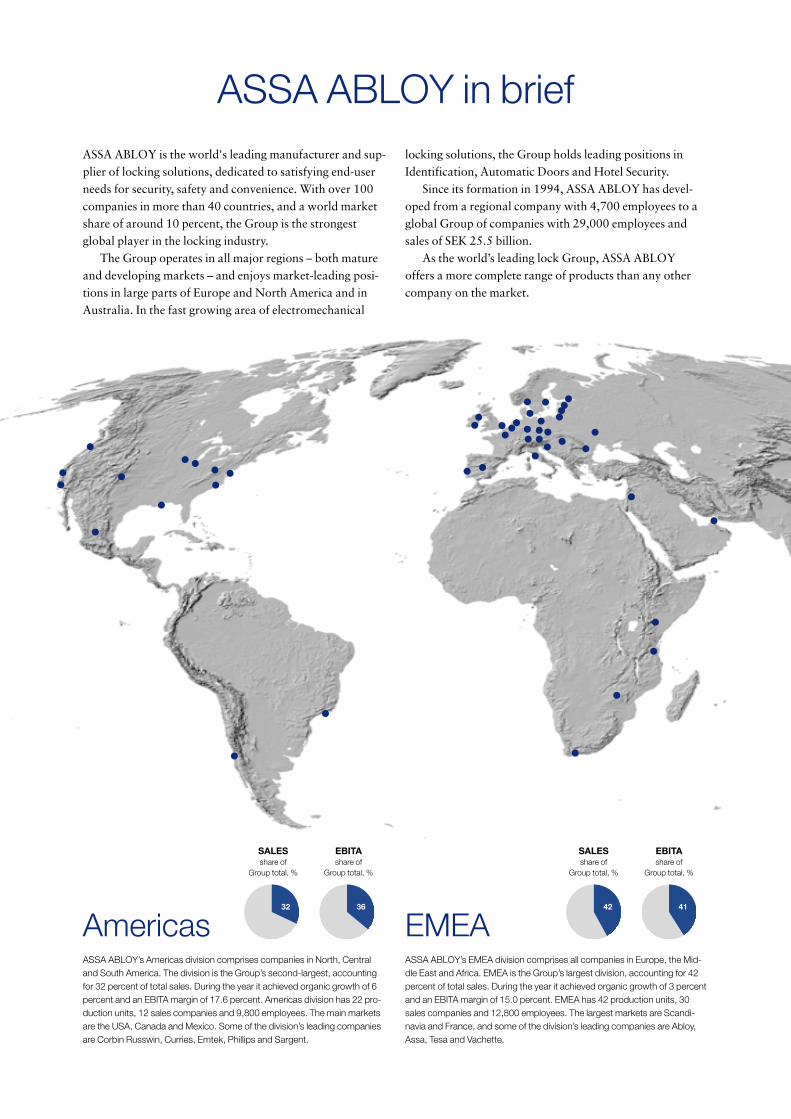

ASSA ABLOY in brief

AmericasASSA ABLOY’s Americas division comprises companies in North, Centraland South America. The division is the Group’s second-largest, accountingfor 32 percent of total sales. During the year it achieved organic growth of 6percent and an EBITA margin of 17.6 percent. Americas division has 22 pro-duction units, 12 sales companies and 9,800 employees. The main marketsare the USA, Canada and Mexico. Some of the division’s leading companiesare Corbin Russwin, Curries, Emtek, Phillips and Sargent.

EMEAASSA ABLOY’s EMEA division comprises all companies in Europe, the Mid-dle East and Africa. EMEA is the Group’s largest division, accounting for 42percent of total sales. During the year it achieved organic growth of 3 percentand an EBITA margin of 15.0 percent. EMEA has 42 production units, 30sales companies and 12,800 employees. The largest markets are Scandi-navia and France, and some of the division’s leading companies are Abloy,Assa, Tesa and Vachette.

ASSA ABLOY is the world's leading manufacturer and sup-plier of locking solutions, dedicated to satisfying end-userneeds for security, safety and convenience. With over 100companies in more than 40 countries, and a world marketshare of around 10 percent, the Group is the strongestglobal player in the locking industry.

The Group operates in all major regions – both matureand developing markets – and enjoys market-leading posi-tions in large parts of Europe and North America and inAustralia. In the fast growing area of electromechanical

locking solutions, the Group holds leading positions inIdentification, Automatic Doors and Hotel Security.

Since its formation in 1994, ASSA ABLOY has devel-oped from a regional company with 4,700 employees to aglobal Group of companies with 29,000 employees andsales of SEK 25.5 billion.

As the world’s leading lock Group, ASSA ABLOY offers a more complete range of products than any othercompany on the market.

32 36 42 41

SALESshare of

Group total, %

EBITAshare of

Group total, %

SALESshare of

Group total, %

EBITAshare of

Group total, %

0

6,500

13,000

19,500

26,000

040302010099989796950

1,000

2,000

3,000

4,000

Sales, SEK M EBITA, SEK M

SEK M SEK M

GROUP SALES AND EBITA

Asia PacificASSA ABLOY’s Asia Pacific division comprises companies in Australia, NewZealand, China and elsewhere in Asia. Asia Pacific accounts for 7 percent ofthe Group’s total sales and has 5 production units, 7 sales companies and3,600 employees. During the year it achieved organic growth of 7 percentand an EBITA margin of 15.1 percent. The division’s largest markets areAustralia, New Zealand and China. The largest companies in the divisionare Lockwood in Australia, Interlock in New Zealand and Guli in China.

7 7

SALESshare of

Group total, %

EBITAshare of

Group total, %

Global TechnologiesASSA ABLOY’s Global Technologies division is the Group’s worldwide organizationdedicated to high-technology products and services. The division accounts for19 percent of the Group’s sales and has 2,900 employees. During the year itachieved organic growth of 5 percent and an EBITA margin of 13.0 percent. GlobalTechnologies comprises three business areas:– The Identification Technology Group (ITG), which accounts for 42 percent ofGlobal Technologies’ sales. ITG’s products consist of various types of identificationtechnology for access control, Radio Frequency Identification (RFID) and smartcards. The products are sold under well-known brand names such as HID, Indala,Sokymat and ACG.– Automatic Doors, which accounts for 40 percent of Global Technologies’ sales.This business area consists of Besam, which is the world’s leading supplier ofautomatic door solutions.– ASSA ABLOY Hospitality, which accounts for 18 percent of Global Technolo-gies’ sales. This business area produces hotel locks and security systems and sellschiefly to hotels and cruise ships. Its two leading companies and brands are Ving-Card and Elsafe.

1619

SALESshare of

Group total, %

EBITAshare of

Group total, %

Edgar Velardo, Emtek, USA Kerstin Pipo, Ikon, Germany Camille Smith, Sargent, USA

Financials in brief2004 2003 Change, %

Sales, SEK M 25,526 24,080 6

of which: Organic growth 5

Acquired growth 5

Foreign exchange effects, SEK M –982 –4

Operating income before goodwill amortization (EBITA), SEK M 3,748 3,3522 12

Operating margin before goodwill amortization (EBITA), % 14.7 13.92

Income before tax, SEK M 2,294 1,9032 21

of which, Foreign exchange effects, SEK M –78 –4

Operating cash flow, SEK M 3,4393 3,265 5

Return on capital employed, % 11.8 9.62

Return on capital employed before goodwill amortization, % 16.0 13.32

Data per share (SEK/share) 2004 2003 Change, %

Earnings after tax and full conversion (EPS) 4.05 3.312 22

Earnings after tax and full conversion excluding goodwill 6.66 5.892 13

Cash earnings after tax and full conversion (CEPS) 9.06 8.612 5

Shareholders’ equity after full conversion 32.66 31.23 5

Dividend 2.601 1.25 108

Number of shares after full conversion (1,000s) 378,717 370,9351 Proposed dividend.2 Excluding non-recurring items.3 Excluding restructuring payments.

1

0

5,000

10,000

15,000

20,000

25,000

30,000

040302010099989796950

5

10

15

20

25

30

Capital employed, SEK M

Return on capital employed, %

Return on capital employedbefore goodwill amortization, %

SEK M %

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

04030201009998979695

Income before tax, SEK M

Operating cash flow, SEK M

SEK M

0

1

2

3

4

5

6

7

04030201009998979695

Earnings per share, SEK

Earnings per share excluding goodwill, SEK

SEK

CAPITAL EMPLOYED /RETURN ON CAPITAL EMPLOYED 4

INCOME BEFORE TAX /OPERATING CASH FLOW 4 EARNINGS PER SHARE 4

4 Data for 2001 and 2003 excludes non-recurring items.

How many keys do you have on your keyring? The factthat we nearly always carry keys and access cards aroundwith us demonstrates our daily need for security. And thefact that we have so many different keys on our keyringshows how fragmented the lock industry still is.

It is neither particularly secure nor convenient to carry afull keyring around. There is clearly a need for some inno-vative new solutions. And to be able to create and launchinnovative solutions calls not just for good ideas, but alsofor worldwide resources in development, marketing, logis-tics and manufacturing.

ASSA ABLOY is the only truly global player in ourindustry. In the past ten years we have acquired many of thelock industry’s strongest companies and built a lock Groupthat is world-leading in both size and vigor. But the factthat you are still carrying all those keys around on yourring shows that, despite our success, we have yet to achieveour biggest victories. We have restructured a whole indus-try and are now ready to take the next step, which is tochange our industry – to change how companies, institu-tions and private individuals relate to security and to locks.

Our task now is to exploit our size, our market positionand our worldwide presence to become the leader both instrength of innovation and in cost management. That, inessence, is what we are saying in the new strategy andvision that we defined and presented during 2004.

2004 was, above all, a good business year for ASSAABLOY. We are back to good organic growth of 5 percent.The Group’s operating margin has improved markedly andwe are continuing to deliver strong cash flow. During theyear work under our Leverage & Growth action programcontinued. We set out to solve a number of specific struc-tural issues, turn round a handful of underperforming com-panies and work towards a long-term improvement in ourorganic growth. As a result of our restructuring measuresefficiency has improved. We have sold two companies, andwe are now expecting profitability from the companies that

CEO’s statement

A clear strategyfor better security

2

were not performing to the required level before. Duringthe year we also worked hard to develop our marketing andsales operations and we are continuing with that.

A refined business strategyIn 2004 we decided to take the next step in developing ourindustry. We have therefore clarified and simplified our busi-ness strategies, which we have condensed into three mainthemes. The first theme is to increase growth in our corebusiness by strengthening cooperation with architects, doormanufacturers, suppliers of security systems and distributorsall over the world. In short, to become even better at what weare already good at. The second theme is concerned withexpanding in markets and in segments with higher growth.This covers three principal markets: the consumer market,where customers actively choose their own security solu-tions; the market for electronic access-control; and the fast-growing Chinese market, where we need to increase ourpresence. The third theme is to try to gain more benefit fromour advantages of scale and thereby radically lower ourcosts. This requires greater specialization of our factories,better utilization of production capacity in low-cost coun-tries, and continuing coordination of our purchasing.

People make the company We are now investing more resources – both centrally andin the divisions – to develop the expertise that our employ-ees possess. We are therefore launching a comprehensiveskills development program in Human Resources, while incommunications we are working to strengthen our com-pany culture and our common values. In just ten years wehave built a remarkable Group – and we must now invest infurther development of our own employees, with the over-all purpose of achieving our business goals and our Vision.

Our future is directed towards developing and sellingsecurity solutions – solutions that reduce the number ofkeys on our keyrings and that, above all, improve the security of everything that is important in our lives.

Stockholm, February 2005

Bo Dankis

President and CEO

3

Secure access – safe andconvenient for teachers and students

4

Colleges and universities Many college and

university sites have a mixture of open and closed areas, in

which students, teachers and other staff must all feel safe.

An electronic card system allows everyone to be securely

identified and given authorized access to the places they

need to go.

With their high data storage capacity, fast data transfer

and ability to use encryption and biometric information,

cards can also be used to log on to computer networks and

to make payments, for example in university cafeterias.

And it is quick and easy to invalidate lost cards or restore

security after a break-in.

5

Over the last ten years ASSA ABLOY has built a world-leading lock Group and changed the structure of the lockingindustry. This has been achieved through acquisitions andthrough improving the performance of the acquired compa-nies. The Group was formed in 1994 when Securitas andWärtsilä merged their lock businesses. Over the last ten yearsASSA ABLOY has increased its sales from SEK 3 billion toSEK 25.5 billion. At the same time the number of companieshas increased to more than 100, with operations in over 40countries.

In the light of the Group's rapid development – withacquisitions that have led to involvement in new markets andtechnologies – ASSA ABLOY has carried out a full, fact-based review of the Group’s strategies for existing and poten-tial markets, and of expected future developments. The workhas resulted in a refined business strategy whose goal is tofurther strengthen the Group’s position by driving organicgrowth and improving efficiency. ASSA ABLOY’s new busi-ness strategy is more precise than before, and the Group’sVision and Business Concept have been updated in line withthe strategy.

Vision“ASSA ABLOY will be the most successful and innovativecompany in our markets by placing locks at the heart ofsecurity and providing safe and secure solutions that givetrue added value to our customers. Our solutions makepeople around the world feel safer and more secure, creatingmore freedom in their lives.”

Business Concept“ASSA ABLOY provides safe and secure solutions that arewell-designed, convenient and cost-efficient. Throughcustomer relevance and innovation, our solutions createsuperior value for businesses and for people at work, athome and at leisure.”

Financial objectivesThe primary financial objective for the ASSA ABLOY Groupis that return on capital employed should exceed 20 percent.During the acquisition phase of the Group’s strategy, sub-stantial amounts of goodwill have been added, which havereduced return on capital employed. The goal is to achievethe secondary financial objectives detailed below and on thenext page by 2008 at the latest.

Vision, Business Concept and Strategy

Placing locks at the heart of every security solution

6

ORGANIC GROWTH: • About 5% a year over a business cycle

MARGIN IMPROVED TO 16–17%• Stand-alone improvements• Leverage Group synergies

STRONG CASH FLOW:• The long-term positive trend in operating cash flow should be maintained

CAPITAL RATIONALIZATION:• Inventory reductions• Maintained capital expenditure level

FINANCIAL OBJECTIVES

20%Return

on capitalemployed

Secondary financial objectives:• Sales should, on average, grow organically at about 5

percent a year over a business cycle.• The EBITA margin should be improved to 16–17 per-

cent. This should be achieved mainly by exploiting syner-gies within the Group.

• The long-term positive trend in ASSA ABLOY’s opera-ting cash flow should be maintained.

• Capital employed should be maintained at the presentabsolute level in spite of organic growth. Measures tomake production more specialized will reduce capitaltied up in inventory. Given the potential to increase uti-lization of current production capacity, capital expendi-ture can be maintained at today’s level – below currentdepreciation.

StrategyFor a number of years ASSA ABLOY has followed a strat-egy model based on three phases of development:1. Global platform. Build a worldwide presence and add

new areas of expertise.2. Leverage synergies and develop the Group’s strength.3. Customer value. Accelerate organic growth by creating

value for customers.ASSA ABLOY has accomplished the main objectives in thethe first phase and created a global platform, althoughthere are still areas of expertise that can be added. As

regards exploiting the Group’s size and advantages of scale,a major step towards correcting some structural imperfec-tions was taken last year with the launch of the Leverage &Growth action program.

The locking industry todayThe world of locks and locking solutions is changing. Newplayers are entering the arena, both from emerging marketsand from other industries. The rapid development of newtechnologies is impacting all parts of the industry. ASSAABLOY’s present competitors are improving their prod-ucts, their quality and their sales strategies. The way peoplebuy locks is changing and so are the various channelsthrough which ASSA ABLOY’s products are distributed. Inseveral market segments there are trends towards providingholistic safety and security solutions rather than offeringindividual products. Customers are similarly shifting focusfrom traditional products to a comprehensive notion ofsafety and security.

At the same time customers’ preferences are polarizing.While some are willing to pay a higher price for well-known, innovative brand names, others are satisfied withfinding a low-price alternative that will meet basic securityrequirements. ASSA ABLOY is now well positioned tomeet these market changes.

A refined business strategyASSA ABLOY’s new strategies aim to realize the Group’sVision, fulfill the Group’s Business Concept and achieve theGroup’s financial objectives. The refined strategy is basedon three overriding themes subdivided into seven mainactivities, as detailed overleaf:

7

Americas division’s new manufacturing plant in Guadalajara, Mexico.

Theme 1. Grow our core business1. Lead the specification markets

Architects and security consultants play an important role in choosing security solutions for new construction. ASSAABLOY’s goal is to strengthen the Group’s resources and ability to market high-security solutions in the specificationsegment.

2. Develop channels to market

A clear majority of ASSA ABLOY’s sales goes through frag-mented local distribution. The Group’s goal is to developexisting and new channels and to influence end-users ofASSA ABLOY’s products more effectively.

3. Develop the door and window OEM markets

In many geographical markets ASSA ABLOY has a lowmarket share of the important door and window OEMmarkets. The Group’s goal is to improve ASSA ABLOY’sability to adapt to large customers’ specific requirements.

Theme 2. Expand into new markets and segments4. Capture and develop consumer opportunities

Customers are demanding security solutions, but the con-sumer market is currently fragmented. ASSA ABLOY’s goalis to increase the Group’s presence in the consumer segmentthrough all channels and to offer integrated solutions thatmeet customers’ needs for safety and security.

5. Grow electromechanical door solutions

The electromechanical door solutions segment is showingrapid growth. ASSA ABLOY’s goal is to increase marketshares and lower costs by developing Standards, adaptingwireless and similar technologies for use with locks, andleveraging the Group’s worldwide strength. Efforts willalso be made to use sales channels such as electric installersto reach a larger market.

6. Develop the Asian potential

Asia in general and China in particular provide a potentialmarket for growth. ASSA ABLOY’s goal is to develop theGroup’s presence on domestic Asian markets and to benefitfrom low-cost manufacturing.

Theme 3. Radically reduce our break-even cost7. Capture purchasing and production synergies and adopt

Lean methods

Because of its many acquisitions, the Group has a complexand fragmented production capacity. ASSA ABLOY’s goalis to use the Group’s size to realize purchasing synergies, to benefit from economies of scale in production, and toadopt Lean methods to achieve even more cost-efficientproduction throughout the Group. Some production willbe moved to low-cost countries.

Vision, Business Concept and Strategy

8

BUSINESS STRATEGY

7. Capture purchasing and production synergies and adopt Lean methods

Radically reduce our break-even cost

3. Develop the door and window OEM markets

1. Lead the specification markets

2. Develop channels to market

Grow our core business

4. Capture and develop consumer opportunities

5. Grow electromechanical door solutions

6. Develop the Asian potential

Expand into new markets and segments

Inno

vatio

n

Customer relevance

Cost efficiency

9

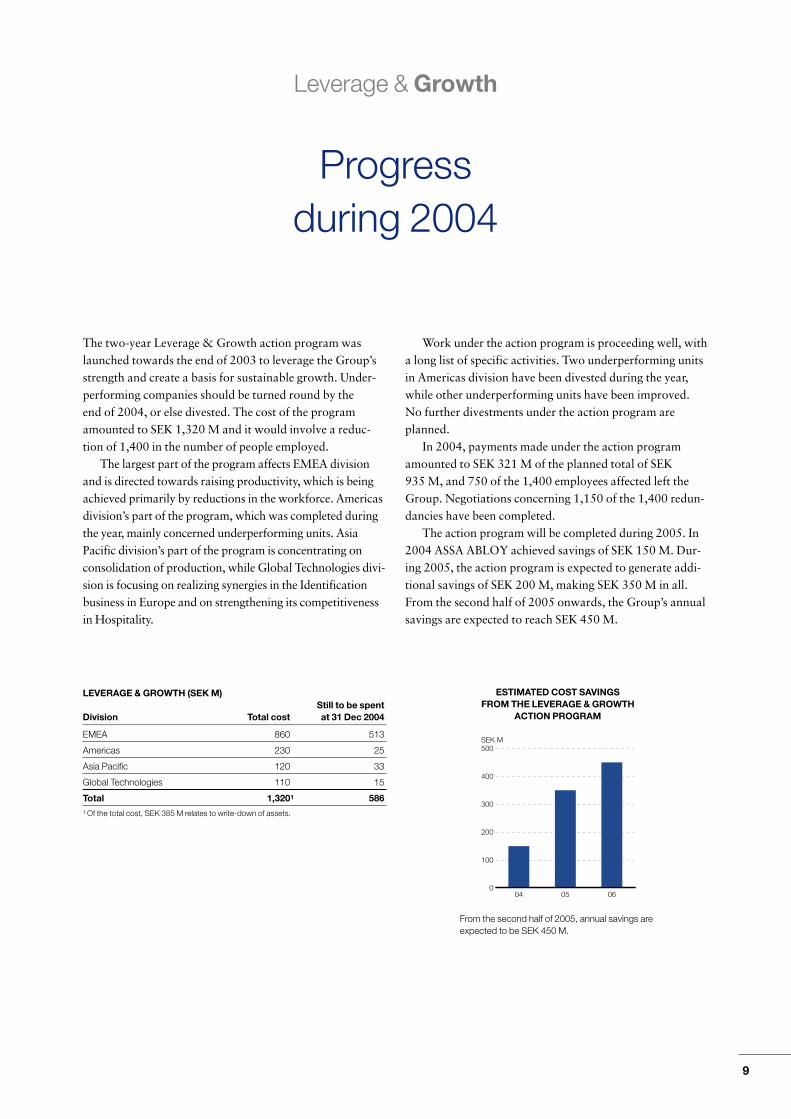

The two-year Leverage & Growth action program waslaunched towards the end of 2003 to leverage the Group’sstrength and create a basis for sustainable growth. Under-performing companies should be turned round by the end of 2004, or else divested. The cost of the programamounted to SEK 1,320 M and it would involve a reduc-tion of 1,400 in the number of people employed.

The largest part of the program affects EMEA divisionand is directed towards raising productivity, which is beingachieved primarily by reductions in the workforce. Americasdivision’s part of the program, which was completed duringthe year, mainly concerned underperforming units. AsiaPacific division’s part of the program is concentrating onconsolidation of production, while Global Technologies divi-sion is focusing on realizing synergies in the Identificationbusiness in Europe and on strengthening its competitivenessin Hospitality.

Work under the action program is proceeding well, witha long list of specific activities. Two underperforming unitsin Americas division have been divested during the year,while other underperforming units have been improved.No further divestments under the action program areplanned.

In 2004, payments made under the action programamounted to SEK 321 M of the planned total of SEK935 M, and 750 of the 1,400 employees affected left theGroup. Negotiations concerning 1,150 of the 1,400 redun-dancies have been completed.

The action program will be completed during 2005. In2004 ASSA ABLOY achieved savings of SEK 150 M. Dur-ing 2005, the action program is expected to generate addi-tional savings of SEK 200 M, making SEK 350 M in all.From the second half of 2005 onwards, the Group’s annualsavings are expected to reach SEK 450 M.

Leverage & Growth

LEVERAGE & GROWTH (SEK M)Still to be spent

Division Total cost at 31 Dec 2004

EMEA 860 513

Americas 230 25

Asia Pacific 120 33

Global Technologies 110 15

Total 1,3201 5861 Of the total cost, SEK 385 M relates to write-down of assets.

0

100

200

300

400

500

060504

SEK M

ESTIMATED COST SAVINGSFROM THE LEVERAGE & GROWTH

ACTION PROGRAM

From the second half of 2005, annual savings areexpected to be SEK 450 M.

Progressduring 2004

Besam doors – efficient entrancesfor millions of people all over theworld

10

Shopping centers and offices 50 million

people a day pass through our doors in stores, shopping

centers, hospitals and office buildings. Automatic doors

provide convenience for everyone, including parents with

baby carriages and people in wheelchairs.

Shops must seem welcoming but must deter shoplifting.

Offices must admit staff and visitors while protecting com-

mercial data worth far more than any security system. In

fire or emergency, rapid escape is vital. The balance of secu-

rity, safety and access control can best be met by sophisti-

cated systems incorporating locks, door controls and per-

sonal identification.

11

Today ASSA ABLOY is the world’s leading lock Group. As theGroup has grown, its product range too has expanded to includea number of product groups, in addition to locks, that are crucialto security. Hence when assessing ASSA ABLOY’s market it hasbecome relevant not just to consider the lock market but to widenthe perspective to the security market in general.

ASSA ABLOY estimates the total security market at around200 billion Euro. The market can be divided into two sections,Security Services and Electronic Security Products, andMechanical Security Products.

Security Services and Electronic Security ProductsElectronic Security Products include electronic cylinders, auto-matic doors and products for access control, which form partof ASSA ABLOY’s product portfolio. The annual growth in the market for Electronic Security Products in which ASSAABLOY is mainly active is around 10 percent.

The development of Security Services and Electronic Secu-rity Products is driven mainly by the general trend towards

higher security. Increased threats in the world around us, in theform of crime, violence and terrorism, create insecurity, whichin turn increases security awareness. This drives the develop-ment of more advanced security solutions and upgrades ofexisting lock solutions to obtain increased protection.

However, this section also contains product groups whereASSA ABLOY has no manufacturing. These include, for ex-ample, fire protection, X-ray scanners and CCTV surveillancecameras, and also Security Services, which mainly compriseguards and surveillance.

Mechanical Security ProductsAs well as locks themselves, Mechanical Security Products alsoinclude products such as handles, strikes, hinges, door closers,exit devices and door and window fittings.

The development of Mechanical Security Products is drivenmainly by new construction, which means that this section ofthe market is expected to grow at about the same rate as GDP.However, a substantial aftermarket creates stability and makes

The market

The security market – two worlds in one

12

0

20

40

60

80

100

120EUR billion

Security guards

Other

Logical authorization control

Automatic doors

Access control

Surveillance cameras (CCTV)

Fire alarms

X-ray inspection systems

Intrusion protection

Other IT security

Alarm centers

Interior hardware

The main product areas where ASSA ABLOY is active are shown in boldface.

Door and window hardware

Locks, exit hardware and door closers

Doors and windows

SECURITY SERVICES AND ELECTRONIC SECURITY PRODUCTS

MECHANICAL SECURITY PRODUCTS

The product groups that ASSA ABLOY manufactures today mean that the Group is active in about 15 percent of the total security market. ASSAABLOY’s market can therefore be estimated at around 30 billion Euro, which in turn gives the Group a market share of around 10 percent. Threequarters of this business is in Mechanical Security Products and the remaining one quarter in Electronic Security Products. ASSA ABLOY’sgrowth target is based on the expected growth in these two markets.

the market less sensitive to changes in the economic climate, asdoes the fact that ASSA ABLOY’s operations are geographi-cally distributed over a large number of countries with differenteconomic cycles.

Distribution channels for security productsA characteristic of today’s security market is that security prod-uct manufacturers such as ASSA ABLOY are usually isolatedfrom end-users behind at least one layer of distributors.

Locksmiths and similar firms are among the most impor-tant distributors of Mechanical Security Products, but otherplayers have a significant role too. Many manufacturers ofdoors and windows integrate lock cases and other securityitems into their products before delivery to customers. Whole-salers of building materials and locks play important parts indelivering the solutions specified by manufacturers for differentconstruction projects. Retailers such building material super-markets and ironmongers serve the consumer market. In thecase of Electronic Security Products, products flow from manu-facturers to end-users mainly via security installers and special-ized distributors. But the products are also sold through inte-grators who often offer turnkey solutions for the installation ofperimeter security, access control and IT security.

TrendsOne of the most obvious trends in the security market is theincreased demand for electronic products. Another clear trendis increased technical standardization, which makes it easier tointegrate the different components of security solutions withone another. This means that, to remain competitive, manufac-turers will be forced to specialize and focus on specific productsegments.

Distribution is changing too. A number of door and win-dow manufacturers, DIY chains and other players are gainingstrength by consolidation. The role of some locksmiths is mov-ing towards increased use of electronics; conversely, IT integra-tors are starting to offer physical security solutions to an evergreater extent.

Another clear trend is that manufacturers in low-cost coun-tries in Asia and elsewhere are increasing their market shares inthe low-price segments of the western world. In some Europeancountries this type of import has increased by nearly 50 percenta year over the last five years. A change can also be seen in thedemand for different levels of security solution. In the past the greatest potential was in the middle segment, but now cus-tomers increasingly choose either a high-security solution or alow-priced alternative.

Major differences between marketsThere are substantial differences between markets. Americansspend more than twice as much on exit devices as Europeans.Conversely, northern Europeans spend three to four times morethan Americans on high-security locks for their homes. Auto-matic doors are also significantly more common in Europe than

13

Intruder alarms

Distributors

Primarily commercial end-users

Integrators.dealers,installers

WholesalersDoor/

window OEM

CCTV Accesscontrol

Locksmiths Distributors Retail

Buildingcontractors

Commercial and residential end-users

Locks Exit hardware

Door/window hardware

ELECTRONIC SECURITY PRODUCTS

Manufacturing

MECHANICAL SECURITY PRODUCTS Manufacturing

Route to market

Route to market

the USA. Electromechanical products are now far more widelyused in the commercial segment than in private homes. In thelong term these differences are likely to disappear. Assumingthat all security and safety solutions could be used equallywidely in Europe and in the USA, a rough estimation indicatesthat the total value of the market could be doubled. Informingand developing the market to reduce the international differ-ences in these market segments is a major challenge for ASSAABLOY.

Americas divisionIn the USA the commercial segment, including schools, hospi-tals and companies, is ASSA ABLOY’s most important market.Interest in security has risen significantly. Product developmentis carried out in close collaboration with insurance companies,police and fire services, customer organizations and other lead-ers of opinion.

In general the residential segment in the USA has lower lockStandards than in Europe. Instead, alarms play a major role insecurity awareness. However, the media are giving more andmore coverage to the fact that better locks are a proactive measure while alarms are a reactive measure when damage has already been done. The residential segment is growing also as a result of rising housing construction.

South AmericaMuch of South America is a fragmented market and there arefew established security Standards. However, the region has amajor need for security solutions and is a future growth market.

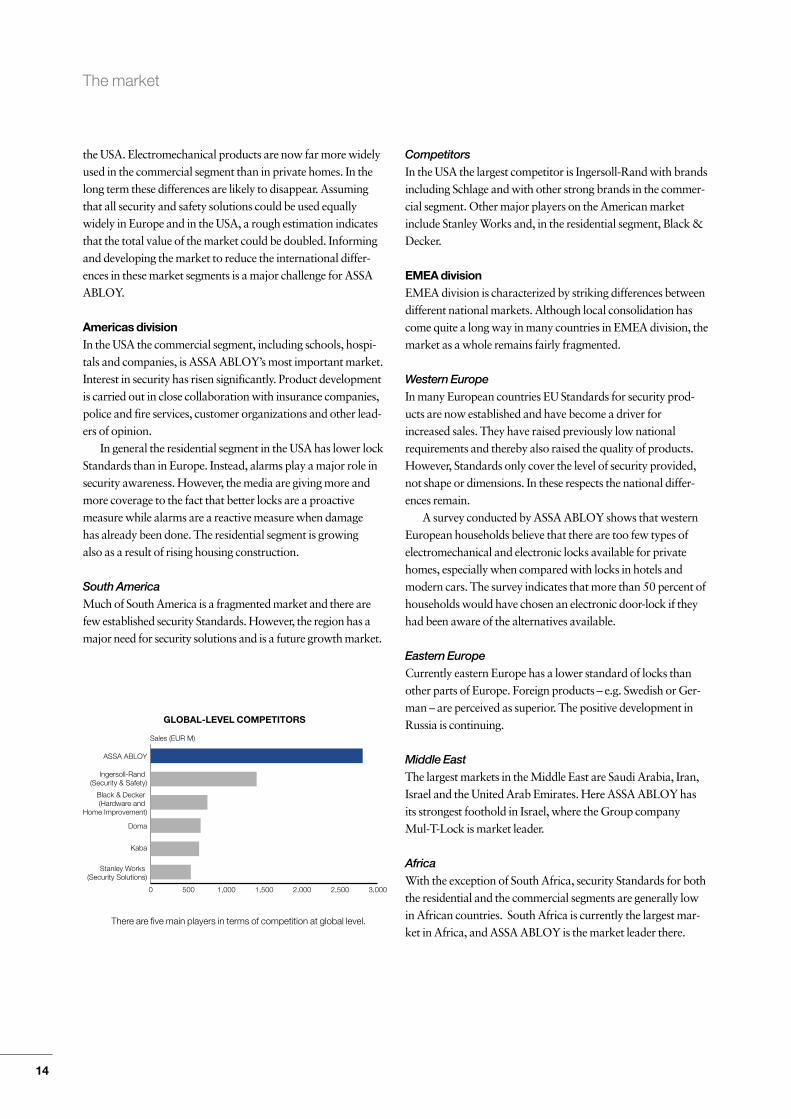

CompetitorsIn the USA the largest competitor is Ingersoll-Rand with brandsincluding Schlage and with other strong brands in the commer-cial segment. Other major players on the American marketinclude Stanley Works and, in the residential segment, Black &Decker.

EMEA divisionEMEA division is characterized by striking differences betweendifferent national markets. Although local consolidation hascome quite a long way in many countries in EMEA division, themarket as a whole remains fairly fragmented.

Western EuropeIn many European countries EU Standards for security prod-ucts are now established and have become a driver forincreased sales. They have raised previously low nationalrequirements and thereby also raised the quality of products.However, Standards only cover the level of security provided,not shape or dimensions. In these respects the national differ-ences remain.

A survey conducted by ASSA ABLOY shows that westernEuropean households believe that there are too few types ofelectromechanical and electronic locks available for privatehomes, especially when compared with locks in hotels andmodern cars. The survey indicates that more than 50 percent ofhouseholds would have chosen an electronic door-lock if theyhad been aware of the alternatives available.

Eastern EuropeCurrently eastern Europe has a lower standard of locks thanother parts of Europe. Foreign products – e.g. Swedish or Ger-man – are perceived as superior. The positive development inRussia is continuing.

Middle EastThe largest markets in the Middle East are Saudi Arabia, Iran,Israel and the United Arab Emirates. Here ASSA ABLOY hasits strongest foothold in Israel, where the Group company Mul-T-Lock is market leader.

AfricaWith the exception of South Africa, security Standards for boththe residential and the commercial segments are generally lowin African countries. South Africa is currently the largest mar-ket in Africa, and ASSA ABLOY is the market leader there.

The market

14

0 500 1,000 1,500 2,000 2,500 3,000

Stanley Works (Security Solutions)

Kaba

Doma

Black & Decker (Hardware and

Home Improvement)

Ingersoll-Rand (Security & Safety)

ASSA ABLOY

Sales (EUR M)

GLOBAL-LEVEL COMPETITORS

There are five main players in terms of competition at global level.

The market

CompetitorsThe largest competitor in the EMEA division is the Swiss com-pany Kaba, which focuses primarily on high-security solutions.

Other major players include Dorma and Abus in Germany,Sécuridev in France and Evva in Austria.

Asia Pacific divisionAustralia and New ZealandThe lock markets in Australia and New Zealand are relativelyconsolidated. ASSA ABLOY’s companies, headed by Lock-wood in Australia and Interlock in New Zealand, are the clearmarket leaders. Growth remains healthy in both residential andcommercial segments.

ChinaChina is the fastest-growing market in Asia, with a majormovement of population from country to town. Today themarket is undeveloped in terms of security Standards and pro-duces an abundance of low-quality products that are mostlyexported. ASSA ABLOY has established its own manufactur-ing plants in China and now faces a major challenge in educat-ing and developing the distribution chain towards productsoffering higher security.

Rest of AsiaIn other parts of Asia, ASSA ABLOY is represented by salesoffices. During the year ASSA ABLOY acquired BEST Met-aline, one of the largest players on the Korean market. Japanand India are other important markets with potential forexpansion.

CompetitorsIn Australia and New Zealand competition comes largely fromimports from low-cost countries, as well as some global compe-tition. In China the lock market is still very fragmented, andeven the largest companies have low market shares. Tri-Circle,whose business is strongly focused on padlocks, is the largestlock manufacturer in China. More than half of Tri-Circle’s salesare exports. In Japan the market leader is Miwa.

Global Technologies divisionIdentification Technology Group (ITG)Because the technological differences between markets aresmall, cards and card readers for both smart cards – based onradio-frequency identification (RFID) – and traditional con-tact-based methods of access control form a worldwide product segment. Demand for products of this type continuesto increase and growth was strong in 2004. The marketremains fairly fragmented and the strongest competition comesfrom the global players and from security integrators such asTyco, Honeywell and GE Infrastructure.

Automatic DoorsThere are a great many local differences between different partsof the world in what they ask of automatic door solutions.Nonetheless, the requirements of the largest customer segments– airports, hospitals, hotels, restaurants and stores – are so simi-lar everywhere that the product segment is best marketed glob-ally. The market is growing and margins improving, especiallyin Europe but also in the USA where competition is fiercest.Consolidation is ongoing, and the strongest competitors, inaddition to the global players Dorma and Stanley Works,include Agta Record from Switzerland, Boon Edam from theNetherlands and Horton Automatics in the USA.

ASSA ABLOY HospitalityThe primary target group for ASSA ABLOY Hospitalityincludes large international hotel and restaurant chains, whichmakes it desirable to organize this business on a global basis.Continuing low demand in the travel industry accounts for thepresent weakness of the hospitality market. Terrorism, politicaldisturbances and natural catastrophes can all be viewed ascauses. At the same time there are contrary trends, for exampleprice pressure in the aviation industry which is likely to lead tomore traveling in the future. The largest competitors are Onityand Saflok.

15

ASSA ABLOY has a world-leading position not just insales, but also in the form of a strong and highly variedrange of products. The development of ASSA ABLOY’sproducts starts from the differing needs of customers. Acontinuous flow of innovative new products is the singlemost important source of organic growth. Focused productdevelopment is thus a critical success factor.

ASSA ABLOY works all the time to develop its productsin ways that will satisfy the end-user’s requirements forsecurity, safety, convenience and design. To meet these cus-tomer requirements more comprehensively, the Groupfocuses on developing total security solutions. Together

with a complete mechanical or electromechanical product,these total solutions include installation and after-salesservice as well.

Design growing in importanceDesign is becoming an ever more important factor in sellingASSA ABLOY’s products. Customers appreciate beinggiven greater choice regarding shape, color and finish, andthis adds value to the product. During the year the Grouphas launched a number of products where design hasplayed a major role in the development process. Sales ofthese ‘designed’ products are rising faster than sales of

ASSA ABLOY’s products

Increased demand for total security solutions

16

Brighthandle – Design is becoming more important for lock products.

standard products. A good example of a designed productis Brighthandle.

Modular platformsMany of ASSA ABLOY’s products, and especially mechani-cal locks, contain similar components. This creates a power-ful opportunity to exploit economies of scale among theGroup’s many companies. Product development and pro-duction are focused on a number of efficient modular plat-forms which can then be used by all companies. Likewise,many different ASSA ABLOY companies can utilize compo-nents produced in a single plant. ASSA ABLOY also worksconstantly to coordinate its purchasing and to limit thenumber of suppliers to the Group so as to improve its procurement performance.

New electromechanical productsASSA ABLOY’s fastest growing product segment is electro-mechanical products for doors and windows. The develop-ment of improved technologies has opened up new opportu-nities to incorporate better components in tailored solutions.These new electromechanical components provide greaterconvenience, for example by automating doors and locks.

17

Mechanicalproducts, 53%

Electromechanical products, 27%

Security doors, 20%

ASSA ABLOY’s SALES BY PRODUCT GROUP

Simpler use with electronic authentication. The iClass card combines RFID and a smart card.

Mechanical productsMechanical locks and accessories continue to form the coreof the ASSA ABLOY product range, accounting for overhalf the Group’s worldwide sales. Mechanical locks pro-vide the two primary functions of any security device: iden-tification (the key) and mechanical strength (the lock).

There is a clear trend towards higher levels of security.In many developing countries, rising standards of livingmean that more people feel the need for greater security.Simpler locks are being replaced by modern high-securitylocks. In developed markets there is a similar demand forthe peace of mind that higher security provides. TheGroup’s huge installed base of locks in these markets cre-ates a solid foundation for new installations and upgrades –and the products are continually being improved.

Modularization of the various product components isan important part of the development of new mechanicallock products. The Evolution series of lock cases from theSwedish company Assa AB is an example of modulariza-tion. The modular series of lock cases makes it possibleto provide new functions in the products, while the com-pany can continue to utilize and improve existing lockcomponents. In comparison with the company’s previousseries of lock cases, Evolution provides a better range ofproducts with 60 percent fewer components.

Another advantage of using modular platforms whendeveloping products is that ASSA ABLOY achieves economiesof scale in its purchase of materials. This also reduces the capi-tal tied up in materials and makes it possible to automate theproduction process more fully. Modular platforms also meanthat improvements and updates are applied to the whole prod-uct range and that new requirements from customers canquickly be incorporated in the products.

Electromechanical productsThe market for electromechanical door systems is growingfaster than the traditional mechanical lock market. ASSAABLOY has developed a communication Standard thatlinks together the various components around the door andalso makes the individual components more intelligent.This makes it simpler to install doors and door frames,which opens up new channels to the market. Anotheradvantage of ASSA ABLOY’s new communication Stan-dard is that it gives customers a greater ability to check thattheir electromechanical doors are working as intended.

A growing trend in electromechanical lock products isto incorporate of an identification unit (reader) directly inthe lock.

ASSA ABLOY’s products

18

The new Evolution series of locks – an example of modular product development put into practice.

ASSA ABLOY’s products

Security doorsOn the American market, ASSA ABLOY is also a majormanufacturer of security doors. During the year the Ameri-cas division launched a new range of electromechanicaldoors and door frames with a pre-installed cable harnessand contacts ready to connect up the lock unit. Such pre-wiring of the doors and door frames simplifies installation,and doors and frames can easily be upgraded and fittedwith electromechanical locks later. This is the Americasdivision’s first step towards the ‘intelligent door’, with com-ponents that are connected to the existing wiring and canintercommunicate via the Hi-O communication Standard.

Shared TechnologiesThe growing use of electronics in doors, and the need tointegrate doors into access control systems, for example,places new demands on lock and door products. In 2004 acentral unit, Shared Technologies, was created to takeresponsibility for the standardization of electronics inASSA ABLOY’s Group-wide platforms.

The goal is that standardization should result in lowerdevelopment costs and shorter development times for new products. ASSA ABLOY aims to make the Group’sproducts easier than competitive products to use and to

integrate in new or existing security systems. For this rea-son interfaces are open and designed to permit simple inte-gration into other systems.

To enable ASSA ABLOY to develop the right platformsfor future products, local customers are involved in theprocess of definition and development. This allows theGroup to undertake generation-planning of its productsand to foresee when the market will be ready for newsecurity solutions.

CoreStreetIn 2004 ASSA ABLOY intensified its cooperation with theAmerican company CoreStreet, which is aimed at develop-ing a new system of secure identification in electromechani-cal locks. Using both fixed and wireless communicationlinks, the new system makes it possible to provide centraladministration of access control to control points without afixed connection, such as freight containers, trucks and thecockpit doors of aircraft.

The system is based on CoreStreet’s CRT technology(CoreStreet Real Time™), which makes it possible to con-trol both authentication and authorization securely, using avery small data format.

19

Hi-O – Highly Intelligent Operation – the platform for intelligentcommunication between the various components of the doorenvironment.

Doors pre-wired for electronic locking can be installed morecheaply and simply.

ASSA ABLOY’s work towards sustainable development isfounded on the four Cornerstones of Vision, Realism, Ethicsand Courage laid down when the Group was formed in 1994.The primary strategy for achieving sustainable development isconstantly to integrate all measures concerned into the Group’sday-to-day work.

ASSA ABLOY has identified the areas where such measuresare desirable, relevant and advantageous for the Group. Themain areas are environmental responsibility, business ethicsand social responsibility. Within these primary classifications alarge number of issues have to be addressed.

A comprehensive analysis of the Group’s risks and opportuni-ties in the field of sustainable development was initiated in 2002,together with an audit of the current position. The analysis, cover-ing all the main elements of the value-chain, was completed in2003 and showed that the industry as a whole – as well as ASSAABLOY specifically – belongs to a medium-risk rather than ahigh-risk segment. ASSA ABLOY has defined the issues that needto be addressed and analyzed how important they are to sustain-able development and what opportunities ASSA ABLOY has toinfluence each individual link in the value-chain.

For example, ASSA ABLOY’s most important raw materialsare metals. Mining and extraction operations often carry risks of major environmental damage and also problems in defendingthe human rights of workers. However, ASSA ABLOY has littleability to influence the mining industry. This is partly becausetrading in metals takes place on commodity exchanges where the

producer is often unknown, and partly because ASSA ABLOY is asmall player on this market and a long way down the value-chain.

The use of lock products is, in a broad view, uncontrover-sial, but there remains much for the Group to do. ASSAABLOY concentrates on taking action in areas where theGroup’s impact is greatest.

Risks and opportunitiesASSA ABLOY has identified risks in the following areas:• Risks related to operations in, and suppliers from, countries

of low production costs. These include environmental, ethi-cal and social issues.

• Problems of business ethics, such as bribery and conflictsof interest, arise in many markets where ASSA ABLOY isactive. ASSA ABLOY has therefore established a zero-tolerance policy regarding bribes, for example.

• Environmental problems of historical origin arising in pro-duction operations. Many plants now forming part of theGroup have occupied the same site for a long time, in somecases more than a century. Instances of soil pollution requir-ing clean-up are arising. ASSA ABLOY is already undertak-ing remedial measures, and is investigating where there arerisks of environmental damage. The costs of these cleaningoperations are relatively small.

• There are still production operations today that give rise to envi-ronmental impact – for example, the use of organic solvents.

Sustainable development

Improved documentation and supervision

20

Courage

Vision

EthicsRealism

Collaboration

People make the difference

Vision• The world leader in safe and secure

lock solutions.• Leading in size and thought.

Realism• Develop the core business.• Know your business.

Ethics• High ethical standards.• Trust and respect other people.

Courage• Lead and embrace change.• Innovate.

The list of potential risk could be extended, especially at a timewhen some business operations are being moved to low-costcountries. However, there are many opportunities too, whichcontribute to the economic argument for ASSA ABLOY tointensify its involvement in sustainable development.

Directives and organization

ASSA ABLOY has produced a number of directives that applyto the whole Group. These are documented and in many casestranslated into several languages. The documents are availableto everyone on the website www.assaabloy.com.

Ultimately it is the Board of Directors that takes responsi-bility for these directives, and ASSA ABLOY’s President andCEO reports to the Board on relevant activities. The CEO alsohas operational responsibility and heads the control groupdealing with such issues. There is an executive with primaryresponsibility for sustainable development in the Parent Com-pany and at least one person with similar responsibility in eachdivision. In each subsidiary, the Managing Director and/or theHuman Resources Director is responsible for ethical and socialissues and the Environmental Director for environmentalissues.

Management systems

Group Management has decided that ASSA ABLOY shouldimplement certifiable environmental management systemsmeeting ISO 14001 in all Group production plants that gener-ate significant environmental impact.

A Code of Conduct has been produced detailing the valuesand guidelines that apply in ASSA ABLOY.

All Group companies should ensure that the guidelinesare followed locally. An overriding system for managing andfollowing up sustainability issues is in course of preparationin the Parent Company.

To ensure that the Group’s suppliers act correctly, a specialquestionnaire has been put to many of them since 2002. Thequestionnaire currently covers quality and environmentalissues and is being expanded to include human rights andworking conditions. The Code of Conduct provides furtherrules of behavior for suppliers.

Ethics and social responsibility

ASSA ABLOY adopted its Code of Conduct in October 2004.The Code is based on a series of internationally accepted con-ventions ratified in most countries. It can naturally not replacelocal laws, which in many cases are more specific, but itexpresses the values and guidelines that should apply within theGroup.ASSA ABLOY is a Group active throughout the world,and major cultural differences inevitably exist between employ-ees in different countries. It is nevertheless valuable from theGroup point of view that employees should share the same val-ues on many issues.An action that constitutes acceptablebehavior in one part of the world may create problems for otheremployees within the Group. Our Code of Conduct covers thefollowing subjects, among others:

• Business ethics– Fair competition and antitrust legislation

– Bribery– Records and reports– Government investigations– Conflict of interest• Workers’ rights, human rights, consumer interests and com-

munity outreach– Child labor– Forced or bonded labor– Freedom of association and collective bargaining– Working hours, overtime and overtime compensation– Discrimination, harassment, equal opportunities, gender

balance and diversity– Employee privacy– Alcohol and/or drug abuse– Human rights under special circumstances– Consumer interests– Community outreach

• Environment, health & safety issues– Environment– Health & safety

Responsibility for the environment

ASSA ABLOY has carried out an analysis of all links in the value-chain and identified the most significant environmental impacts.The analysis revealed major differences between companies inthe impact they have on the environment.Thus manufacturingcompanies have greater impact than those that just sell products.From the Group point of view it is important to concentrate com-mon efforts on production in the first instance.A survey is also inhand to assess historical environmental impacts on soil andground water at all plants with a relevant risk pattern.Thisshould be complete before 2007.

Another goal is to eliminate all use of chlorinated solventsand hexavalent chromium.

In 2004 ASSA ABLOY listed all its planned environmentalmeasures in an Environmental and Stakeholder Integrity Pro-gram together with time schedules for carrying out all Group-wide and local projects. In addition, ASSA ABLOY intends toimplement relevant parts of the EU’s directives on Waste Elec-trical and Electronic Equipment (WEEE) and the Restriction ofHazardous Substances (RoHS) in electrical and electronicequipment within firm time frames.

External auditing

Since March 2004 ASSA ABLOY has been included in theFTSE4Good series of indexes, which judges companies ontheir work on environmental and social issues with a view toencouraging socially responsible investment. Rating institutesand unit trusts also actively follow ASSA ABLOY’s progress insustainable development.

Ongoing developments

ASSA ABLOY continually monitors the evolution of the lawsand conventions governing issues in the field of sustainabledevelopment. However, probably the most important factor isthe common platform of values concerning such issues that isbeing built up in the Group.

21

karin

Placerad bild

Yale – keeping safe what we valuemost, for more than a century

22

Safe houses Many of our customers today are look-

ing for secure protection for their homes and holiday

houses. As the world’s leading lock Group, ASSA ABLOY

can offer customers everything from individual products to

convenient integrated solutions for their home security.

ASSA ABLOY’s goal is clear: by placing its locks at the

heart of every security solution, the Group can provide

solutions that will make people around the world feel safer

and more secure and able to live their lives more freely.

23

IntroductionThe EMEA division comprises companies in Europe, theMiddle East and Africa. EMEA is the Group’s largest divi-sion and accounts for 42 percent of total sales. During theyear the division achieved an organic growth of 3 percentand an EBITA margin of 15.0 percent. The EMEA divisionhas 42 production units, 30 sales companies and 12,800employees. The division is organized into eleven geographi-cal market regions, each with its own management groupwhich is responsible for the region’s marketing strategy,finances and business development. EMEA’s divisional man-agement is based in Stockholm, Sweden. ASSA ABLOY’slargest markets in the division are Scandinavia and France,and the leading companies are Abloy, Assa, Tesa andVachette.

A strongly diversified marketThe EMEA division companies operate in a strongly diver-sified market with significant local differences. Differenttraditions in the markets of northern Europe, southern

Europe, the Middle East and Africa, reinforced by differentBuilding Standards and different climates, mean that thereare many different needs to be met. ASSA ABLOY’sstrength is that its companies have excellent knowledge ofcustomers’ requirements in each local market, which winsthem high levels of repeat business and provides a strongbasis for their operations. ASSA ABLOY also has stronglinks with distributors and good knowledge of local lockStandards. The aftermarket accounts for a significant frac-tion of the division’s sales, which means that local brandsserve an important function.

No clear boundary between the residential and commercial segmentsIn Europe there is no clearly defined boundary betweenproducts for the residential segment and products for thecommercial segment. Many products currently sell to cus-tomers in both segments. An interior door lock for an officewill serve equally well in a home. In this respect the Europeanmarket contrasts with, for example, the American market.

Division EMEA

Focus on the Leverage & Growth program

24

The division operates in a strongly diversified marketwith significant local differences.

Many and varied companies with good knowledge oftheir own markets’ requirements.

No clearly defined boundary between the residentialand commercial segments.

CHARACTERISTICS OF THE EMEA DIVISION

Bo Dankis, President and CEO of ASSA ABLOY and head of EMEA division.

Report on the year2004 saw good demand for ASSA ABLOY’s products.Growth was strongest in the residential segment in Scandi-navia and the Benelux countries. There was also gooddemand in the Do-It-Yourself segment, but growth in thecommercial segment was rather lower this year. The weakUS dollar and rising material prices had a negative effect onsome of the division’s regions during the year. However,ASSA ABLOY was able to compensate for the higher mat-erial prices by means of higher prices for its own products.

ScandinaviaIn Scandinavia, the residential segment made strongadvances in 2004 after a weak 2003. Intensified marketingand increased discussion in the media about how best toprotect the home contributed to rising sales. Developmentin the commercial market was less strong, but increasedfocus on higher security meant that sales still showed somegrowth. There was also growing demand from door andwindow manufacturers for ASSA ABLOY’s products. Toshorten lead-times in delivering to customers, the Grouphas expanded its assembly capacity in Denmark while mov-ing component manufacture to Sweden.

FinlandIn Finland, growth took off in the latter part of 2004 andthe business also improved its margins. Abloy invested inthe aftermarket, which gave stability to its operations.Abloy also increased its export share, especially in the high-security segment, thanks in past to the launch of the newAbloy PROTEC lock cylinder.

25

0

100

200

300

400

Q4Q3Q2Q1Q4Q3Q2Q10

25

50

75

100

Sales, EUR M

EBITA, EUR M

2003 2004

EUR M EUR M

SALES / EBITA

0

200

400

600

800

1,000

1,200

Q4Q3Q2Q1Q4Q3Q2Q10

5

10

15

20

25

30

Capital employed, EUR M

Return on capital employed, %Return on capital employed before goodwill amortization, %

2003 2004

EUR M %

CAPITAL EMPLOYED /RETURN ON CAPITAL EMPLOYED

0

10

20

30

40

50

60

70

Q4Q3Q2Q1Q4Q3Q2Q1

EBITA, EUR MCash flow, EUR M

2003 2004

EUR M

EBITA / CASH FLOW

Division EMEA, Key figures

2004 2003 2004 2003Income statement SEK M SEK M EUR M EUR M

Sales, external 10,747 9,858 1,179 1,081

Sales, internal 284 318 31 35

Sales 11,031 10,176 1,210 1,116

Organic growth 3% –1% 3% –1%

Operating income beforegoodwill amortization (EBITA)1 1,650 1,359 181 149

Operating margin beforegoodwill amortization (EBITA)1 15.0% 13.4% 15.0% 13.4%

Goodwill amortization –358 –338 –39 –37

Operating income (EBIT)1 1,292 1,021 142 112

Operating margin (EBIT)1 11.7% 10.1% 11.7% 10.1%

Capital employed

Capital employed 9,204 8,519 1,020 939

– of which goodwill 4,748 4,728 526 521

Return on capital employed 1 13.5% 10.6% 13.5% 10.6%

Return on capital employedbefore goodwill amortization1 17.2% 14.2% 17.2% 14.2%

Cash flow

Operating income beforegoodwill amortization (EBITA)1 1,650 1,359 181 149

Depreciation (excluding goodwill amortization) 500 505 55 55

Net capital expenditure –340 –357 –37 –39

Change in working capital 16 66 2 7

Cash flow 2 1,826 1,573 201 172

Average number of employees 12,774 12,481 12,774 12,4811 Excluding non-recurring items.2 Excluding restructuring payments.

FranceFrance achieved good growth during the year. Residentialnew construction increased. Electromechanical solutionsare beginning to take market share from the traditionalmechanical lock market.

Germany and SwitzerlandThe German and Swiss markets are showing signs of newgrowth after several years of weakness. As part of theLeverage & Growth program, ASSA ABLOY carried out a major reorganization in Germany during the year. Thenumber of units was reduced from seven to two. The re-organization has improved ASSA ABLOY’s positioning on the market.

United KingdomMost of the Group’s business in the United Kingdom lies inrelatively simple lock products – a segment with many play-ers and price pressure. This business lost some market shareduring the year, and some production was moved to coun-tries with lower production costs, resulting in redundanciesin Britain. The Group also reorganized the companies serv-ing the residential segment and invested resources in moreefficient product development. ASSA ABLOY’s business inthe high-security segment showed good development in2004.

ItalyASSA ABLOY’s companies in Italy showed weak sales andpoor profitability. The profitability of export sales – tradi-tionally important – was hurt by worsening exchange rates.The Italian operations have embarked on a major reorgani-zation involving specialization of units and the movementof some production to low-cost countries. New investmentshave been made, and the Group acquired Corbin in Italy at the start of the year. ASSA ABLOY is working towards

specific goals designed to build up its organization in Italyso as to achieve a critical mass.

BeneluxIn Benelux, integration between companies acquired earlieris progressing well, and synergies between the companies arebecoming apparent. To strengthen ASSA ABLOY’s customeroffering on the market and specifically to boost its position inthe OEM segment for door and window manufacturers,Nemef in the Netherlands was acquired during 2004.

SpainSales on the Spanish market rose in 2004 despite reducedexports. As part of ASSA ABLOY’s strategy to get closer tothe customer, the companies developed specially tailoredsecurity solutions. ASSA ABLOY consolidated its produc-tion companies and sales companies in Spain in 2004 andalso focused on initiatives in the specification segment.

Eastern EuropeASSA ABLOY’s companies in eastern Europe showedstrong growth during the year. The Group is investing inmanufacturing units in the low-cost countries of easternEurope such as Romania and the Czech Republic, both forproduction itself and for the development of new products.Ongoing investment in skills development has resulted inASSA ABLOY now having some 70 locally employedgraduate engineers in Romania. The availability of a well-qualified workforce and high levels of efficiency mean thatthe east European plants have good future expansioncapacity.

Middle EastAfter two years of reduced demand, Mul-T-Lock hasincreased its market shares on the Israeli market and haslaunched a number of new products.

Division EMEA

26

Mechanical products, 69%

Electromechanical products, 18%

Security doors, 13%

DIVISION EMEASALES BY PRODUCT GROUP

Perti Lempiäinen, Abloy, Finland.

Division EMEA

AfricaThe African market is highly fragmented and ASSAABLOY’s operations in the region are concentrated prima-rily on South Africa, where the Group has held a strongposition for many years. However, low-price imports had anegative impact on the business in 2004.

Ongoing initiativesThe EMEA division works continually to develop its distri-bution and product offerings to customers and to makethem more efficient. One prioritized area has been to focuson specific customer segments. Thus the companies work-ing in the car-lock segment were brought together duringthe year. FAB in the Czech Republic, which supplies locksto the Volkswagen Group, and C.E. Marshall in England,which supplies locks to the Ford Group, have formed ajoint Car Lock Group. Cooperation between the companieswill enable ASSA ABLOY to offer the automotive industrya more attractive product package.

A similar initiative in cooperation has been undertakenby the EMEA companies that supply security solutions toairports. Through exchange of expertise between the com-panies, ASSA ABLOY can now offer security solutions toairports in all its markets worldwide.

Greater cooperation with the OEM segmentDuring the year the EMEA division has advanced its stand-ing with OEM door and window manufacturers, which are important channels for ASSA ABLOY’s products. Col-laboration with the OEM segment will affect generation-planning for the division’s products and may also influenceprojects spanning several customer segments and countries.

Competence Centers for specificationIn the security industry it is becoming increasingly impor-tant to become involved in the building process at an earlystage when a new housing development, factory or officecomplex is to be built. By specifying a total security solu-tion covering security, safety, convenience and design,ASSA ABLOY stands a good chance of going on to supplysecurity solutions to the building. Today’s large office andfactory buildings have highly complex security require-ments, and helping the architects to specify appropriatesecurity solutions gives ASSA ABLOY an advantage later inthe sales process. To train salesmen to specify new buildingprojects, special Competence Centers have been set up inNorway and Spain.

The importance of exploiting production synergiesThere is great potential for coordinating production in theASSA ABLOY Group. In the long term, production will beconcentrated in fewer plants, and a proportion of produc-tion will be moved to low-cost countries. Plants will manu-facture fewer different products but larger volumes of indi-vidual products. Faster delivery times and ready availabilityof products are also important to ASSA ABLOY’s sales.Installers therefore remain important both as partners andas customers.

Leverage & Growth to be completed during 2005The Leverage & Growth action program will come to anend in the course of 2005 as the reorganization of ASSAABLOY’s companies in the United Kingdom, Germany,Spain and Italy is completed.

27

Exploit production synergies in the division through on-going specialization.

Continue to develop ASSA ABLOY’s product offerings tospecific customer segments.

Develop cooperation across geographical boundaries forlarge customers and projects.

KEY PRIORITIES

Christine Phoko, ASSA ABLOY South Africa.

The Americas division comprises companies in North,Central and South America. Americas is ASSA ABLOY’ssecond-largest division and accounts for 32 percent of totalsales. During the year the division had an organic growth of6 percent and an EBITA margin of 17.6 percent. The divi-sion is subdivided into product and channel focused groupsin the USA and into geographical regions elsewhere. Itshead office is in New Haven, Connecticut, USA. Americasdivision has 22 production units, 12 sales companies andabout 9,800 employees. Among the major companies in thedivision are Corbin Russwin, Curries, Emtek, Phillips and Sargent.

Report on the yearThe economic climate in the division’s markets was gener-ally more favorable in 2004 than in 2003, resulting in goodgrowth in both non-residential and residential segments.The Door Group and the Residential Group reportedimproved sales during the year, and the Door Group hascontinued to develop positively despite higher material

costs. The Architectural Hardware Group has alsoimproved its margins through continuing focus on imple-menting Lean operations. The division’s EBITA margin roseby 110 basis points during the year as a consequence ofcontinuous improvement efforts, the Leverage & Growthaction program and better market conditions. Significantincreases in material prices, primarily due to the global steelmarket situation, had some negative effect, but the divisionwas able to offset the impact through operational efficien-cies and price increases to the market.

Clear distinction between market segmentsThe North American market differs from the Europeanmarket in having a clear distinction between productsintended for the non-residential segment and productsintended for the residential segment. The commercial seg-ment accounts for a very large percentage of the division’ssales. Due to the segment and channel distinctions, only afew of the division’s products are suitable for both officeand home applications.

Division Americas

Growing with increased margins

28

A clear majority of the division’s sales comes from thenon-residential segment.

There is a significant differentiation between products andchannels for the institutional and commercial segment andproducts for the residential segment.

Doors and door frames are major components of solu-tions offered to the non-residential segment in the USA.

CHARACTERISTICS OF THE AMERICAS DIVISION

Thanasis Molokotos, Executive Vice President of ASSA ABLOY and head of Americas division.

The non-residential segmentThe non-residential segment consists primarily of publicbuildings, offices, schools and hospitals. Security and safetyStandards for these environments are much more demand-ing than for typical residential applications; consequently,product functionality, quality and prices are all significantlyhigher. Growth in the commercial segment recovered thisyear after being weak for a number of years.

Products sold to the non-residential segment includedoors and door frames from the Door Group; door fittings,handles, locks etc. from the Architectural Hardware Groupand the Electromechanical Group; and high-security prod-ucts from the High Security and Aftermarket Group.

Emtek continues the positive trendIn the residential segment, Emtek continued to show stronggrowth and rising margins. The company, based in Califor-nia, focuses on high-end residential products.

Actions under the Leverage & Growth programThe division’s operations have been rationalized by thedivestment of its two companies specializing in the deten-tion segment – Folger Adam Security and Trussbilt. Theirproducts did not fit ASSA ABLOY’s core business, and thecompanies were underperforming on sales and margins.Other companies included under the Leverage & Growthaction program have improved their sales and margins.

29

0

50

100

150

200

250

300

Q4Q3Q2Q1Q4Q3Q2Q10

10

20

30

40

50

60

2003 2004

Sales, USD M

USD M USD M

EBITA, USD M

SALES / EBITA

0

250

500

750

1,000

1,250

Q4Q3Q2Q1Q4Q3Q2Q10

10

20

30

40

50

2003 2004

Capital employed, USD M

Return on capital employed, %Return on capital employed before goodwill amortization, %

USD M %

CAPITAL EMPLOYED /RETURN ON CAPITAL EMPLOYED

0

10

20

30

40

50

60

70

Q4Q3Q2Q1Q4Q3Q2Q1

2003 2004

EBITA, USD MCash flow, USD M

USD M

EBITA / CASH FLOW

Division Americas, Key figures

2004 2003 2004 2003Income statement SEK M SEK M USD M USD M

Sales, external 8,242 8,625 1,125 1,069

Sales, internal 28 32 4 4

Sales 8,270 8,657 1,129 1,073

Organic growth 6% –2% 6% –2%

Operating income beforegoodwill amortization (EBITA)1 1,452 1,428 198 176

Operating margin beforegoodwill amortization (EBITA)1 17.6% 16.5% 17.6% 16.5%

Goodwill amortization –314 –331 –43 –41

Operating income (EBIT)1 1,138 1,097 155 135

Operating margin (EBIT)1 13.8% 12.6% 13.8% 12.6%

Capital employed

Capital employed 7,049 7,528 1,066 1,046

– of which goodwill 4,332 5,010 655 696

Return on capital employed 1 14.6% 12.4% 14.6% 12.4%

Return on capital employedbefore goodwill amortization 1 18.7% 16.2% 18.7% 16.2%

Cash flow

Operating income beforegoodwill amortization (EBITA)1 1,452 1,428 198 176

Depreciation (excluding goodwillamortization) 227 250 31 31

Net capital expenditure –195 –212 –27 –26

Change in working capital –72 61 –10 8

Cash flow2 1,412 1,527 192 189

Average number of employees 9,767 10,091 9,767 10,0911 Excluding non-recurring items.2 Excluding restructuring payments.

MexicoContinued efforts have been made by ASSA ABLOY’s com-panies in Mexico to improve the division’s market position.Implementation of Lean manufacturing principles, cross-learning with other companies and participation in Groupprocurement practices have helped to improve overall per-formance.

Tesa Mexico has built a new plant in Guadalajara,which started production in September 2004. The plant has significantly increased manufacturing capacity and efficiency. Production was previously split among eight different buildings but has now been concentrated in onebuilding laid out for one-piece-flow Lean operations.

The plant supplies products to both the domestic and export markets. Among its exports are Yale-brandedproducts for the US residential market and products andcomponents for other Group companies in the USA, wherestrategically beneficial.

CanadaASSA ABLOY’s Canadian operations have achievedgrowth during the year despite low non-residential growthin the marketplace. All but one, Fleming Door, are sales and service companies. The sales companies have been neg-atively impacted by the weak US dollar.

South AmericaASSA ABLOY’s companies in South America have grownwith increased margins during 2004. The Brazilian market,which accounts for a relatively small percentage of the divi-sion’s sales, has undergone significant improvements. LaFonte has been restructured, with a new management, new organization, cost reductions and more efficientadministrative functions. Its success is also due in part tosubstantial collaboration with many companies across theAmericas division. By working together on the develop-ment of new products, the companies offer more attractivesecurity solutions on their own local markets.

Ongoing initiativesSpecification skills increasingly importantThe division is expanding its knowledge of the various cus-tomer categories. Different types of buildings require differ-ent solutions. The development of specification skills is animportant initiative in the Americas division. Modernsafety and security Standards are complex, and new build-ing regulations constantly appear. Helping architects tosolve their safety and security requirements during thedesign and planning phases of a building project can oftenlead on directly to good sales.

Division Americas

30

Mechanical products, 51%

Electromechanical products, 9%

Securitydoors, 40%

DIVISION AMERICASSALES BY PRODUCT GROUP

Joaquim Chaves, La Fonte, Brazil.

Division Americas

Education of ASSA ABLOY’s distributorsDistributors are an essential part of the Americas division’smarketing strategy. Educational support to ASSA ABLOY’sdistributors as well as end-users will help bring the impor-tance of integrated solutions to the forefront.