ANNEXES - Universidade Nova de Lisboa · PDF fileField Lab in Entrepreneurial Innovative...

39

A Work Project, presented as part of the requirements for the Award of a Masters Degree in Management from the NOVA – School of Business and Economics. Field Lab in Entrepreneurial Innovative Ventures INTERNATIONALIZATION OF RESUL TO NAMIBIA ANNEXES Ânia Cárin Martins Ruivo Correia Student Number 600 A project carried out on the Management course, under the supervision of: Professor Filipe Castro Soeiro January 6 th , 2012

Transcript of ANNEXES - Universidade Nova de Lisboa · PDF fileField Lab in Entrepreneurial Innovative...

A Work Project, presented as part of the requirements for the Award of a Masters

Degree in Management from the NOVA – School of Business and Economics.

Field Lab in Entrepreneurial Innovative Ventures

INTERNATIONALIZATION OF RESUL TO NAMIBIA

ANNEXES

Ânia Cárin Martins Ruivo Correia

Student Number 600

A project carried out on the Management course, under the supervision of:

Professor Filipe Castro Soeiro

January 6th

, 2012

Internationalization of RESUL to Namibia Annexes

2 Ânia Cárin Correia

Glossary

AEP - Associação Empresarial de Portugal

AICEP - Agência para o Investimento e Comércio Externo de Portugal

Common Monetary Area

Members: Namibia, South Africa, Swaziland and Lesotho.

PACs: Production Associated Companies

RESUL: RESUL, Equipamentos de Energia SA

Southern African Customs Union (SACU)

Members: Namibia, South Africa, Botswana, Swaziland and Lesotho.

Southern African Development Community (SADC)

It is the largest trade and co-operation pact in Africa providing its members with

privileged access to each other, through transport infrastructure and customs-free

trading. Members: Angola, Botswana, Democratic Republic of the Congo, Lesotho,

Malawi, Mauritius, Mozambique, Namibia, Seychelles, South Africa, Swaziland,

Tanzania, Zambia and Zimbabwe.

Southern African Power Pool (SAPP)

Power pools are regional power markets formed by African countries aiming at joining

their natural resources and solving their energy deficit. Members of SAPP: generation,

transmission and distribution companies from Angola, Botswana, Congo, Lesotho,

Malawi, Mozambique, Namibia, South Africa, Swaziland, Tanzania, Zambia and

Zimbabwe.

Internationalization of RESUL to Namibia Annexes

3 Ânia Cárin Correia

Annexes

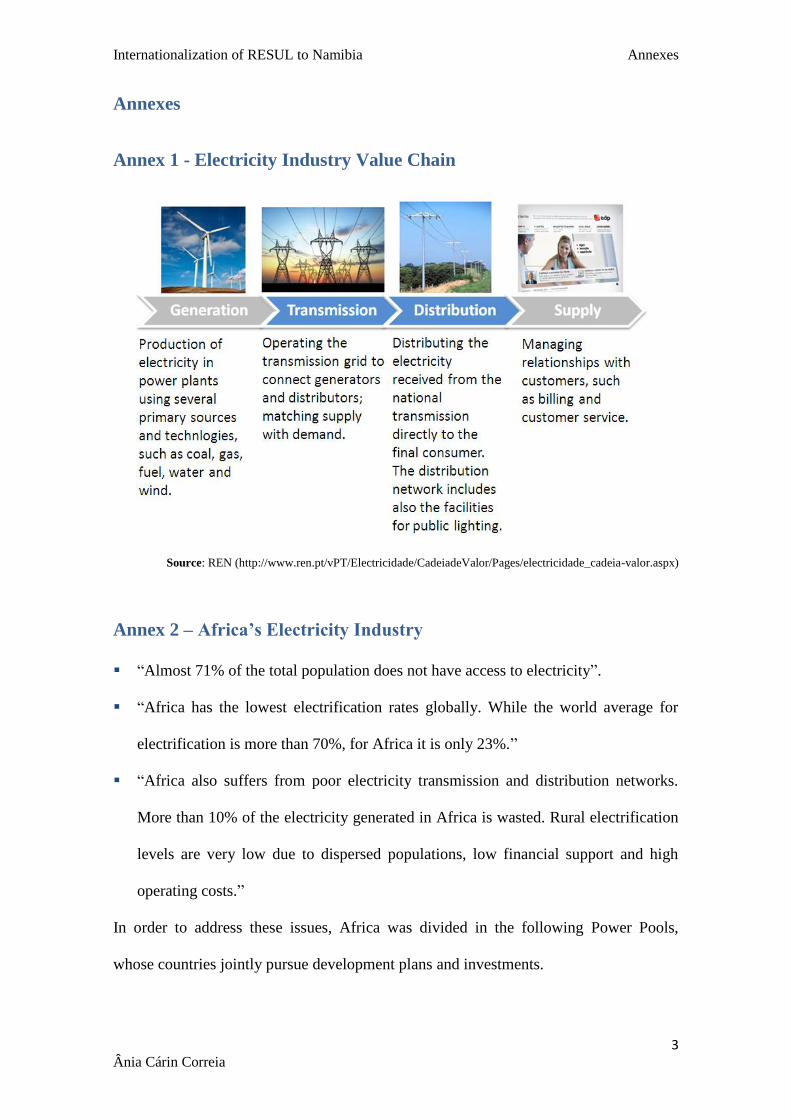

Annex 1 - Electricity Industry Value Chain

Source: REN (http://www.ren.pt/vPT/Electricidade/CadeiadeValor/Pages/electricidade_cadeia-valor.aspx)

Annex 2 – Africa’s Electricity Industry

“Almost 71% of the total population does not have access to electricity”.

“Africa has the lowest electrification rates globally. While the world average for

electrification is more than 70%, for Africa it is only 23%.”

“Africa also suffers from poor electricity transmission and distribution networks.

More than 10% of the electricity generated in Africa is wasted. Rural electrification

levels are very low due to dispersed populations, low financial support and high

operating costs.”

In order to address these issues, Africa was divided in the following Power Pools,

whose countries jointly pursue development plans and investments.

Internationalization of RESUL to Namibia Annexes

4 Ânia Cárin Correia

Power Pools in Africa

Source: GBI Research, “Power Market in Africa to 2020”

Annex 3 – Associated Companies and Subsidiaries

Source: RESUL and Conservatória do Registo Comercial

Annex 4 – Namibia

Total area: 824.269 sq km Source: CIA – World Factbook

Internationalization of RESUL to Namibia Annexes

5 Ânia Cárin Correia

The capital city, Windhoek (about 365,000 inhabitants), contains highly modern

facilities (internationally rated hotels, restaurants, conference amenities, cafes, etc.) and

public infrastructure par with the best in the world: well-maintained roads, first-rate

medical services, education and reliable municipal services.

Source: PwC - Namibia 2010 and beyond

Namibia’s Regions

Source: PwC - Namibia 2010 and beyond

Internationalization of RESUL to Namibia Annexes

6 Ânia Cárin Correia

Annex 5 - ENFORCING CONTRACTS - Doing Business (Namibia)

DB 2012 RANK 40 | DB 2011 RANK 41 | CHANGE IN RANK 1

(TOTAL: 183 Economies – 1 is the best rank, 183 the worst)

The ranking is the simple average of the percentile rankings on the indicators described

below (procedures, time and cost).

Enforcing Contracts Indicators Measure:

“Procedures to enforce a contract through the courts (number): any interaction

between the parties in a commercial dispute, or between them and the judge or the court

officer; steps to file and serve the case; steps for trial and judgement; steps to enforce

the judgement.”

“Time required completing procedures (calendar days): time to file and serve the

case; time for trial and obtaining judgement; time to enforce the judgement.”

“Cost required to complete procedures (% of claim): no bribes; average attorney

fees; court costs, including expert fees; enforcement costs.”

Ranking of Namibia and comparator economies on the ease of enforcing contracts:

Internationalization of RESUL to Namibia Annexes

7 Ânia Cárin Correia

Procedures, time and cost for resolving a commercial lawsuit (enforcing a contract)

Source: http://doingbusiness.org/data/exploreeconomies/namibia#enforcing-contracts

Annex 6 - Custom Tariffs for a sample of RESUL’s products

Product Code Tariff

85369010

85371099

39219090

85369010

85354000

85399010

0%

39269097 10% of the FOB value

85043300 1,3% of the FOB value

85444995 1,95% of the FOB value

Source: Market Access Database

(http://madb.europa.eu/mkaccdb2/datasetPreviewFormATpubli.htm?datacat_id=AT&from=publi)

Internationalization of RESUL to Namibia Annexes

8 Ânia Cárin Correia

Annex 7 - TRADING ACROSS BORDERS - Doing Business (Namibia)

DB 2012 RANK 142 | DB 2011 RANK 142 | CHANGE IN RANK 0

(TOTAL: 183 Economies – 1 is the best rank, 183 the worst)

“Excessive document requirements, burdensome customs procedures, inefficient port

operations and inadequate infrastructure all lead to extra costs and delays for exporters

and importers, stifling trade potential.”

The ranking is the simple average of the percentile rankings on the indicators described

below (documents, time and cost).

Trading Across Borders Indicators Measure:

*Assumption: standard container of goods - dry-cargo, 20-foot full container load.

“Documents required to export and Import (number): bank documents; customs

clearance documents; port and terminal handling documents; transport documents.”

“Time required to export and import (days): obtaining all the documents; inland

transport and handling [to the largest business city]; customs clearance and inspections;

port and terminal handling; does not include ocean transport time.”

“Cost required to export and import (US§ per container): all documentation; inland

transport and handling [to the largest business city]; customs clearance and inspections;

port and terminal handling; official costs only, no bribes.”

Documents, Time and Cost

Internationalization of RESUL to Namibia Annexes

9 Ânia Cárin Correia

Ranking of Namibia and comparator economies on the ease of trading across borders

Procedures and documents relevant for this internationalization Plan

Source: http://doingbusiness.org/data/exploreeconomies/namibia#trading-across-borders

Internationalization of RESUL to Namibia Annexes

10 Ânia Cárin Correia

Annex 8 - Corruption Perception Index, 2011 [0.0: Most corrupt; 10.0:

Least corrupt]

Source: www.transparency.org (last update: December the 1st, 2011)

Annex 9 – Macroeconomic Indicators

2008 2009 2010 2011a 2012

a 2016

a

GDP (US$ millions)2 8,959.9 9,397.2 12,238.8 - - -

Real GDP Growth (%)1 4.3 -0.7 4.8 3.6 4.2 4.3

Inflation Rate1 10.4 8.8 4.5 5.0 5.6 4.5

a) Projections; 1Source: IMF – “World Economic Outlook “(September 2011); 2 Source: Euromonitor -

“Namibia: country profile” (18 November 2011)

Namibia’s Export countries (2008): 1st South Africa (31.8%), 2

nd UK (15.5%), 3

rd

Angola (8.6%)… 17th

Portugal (0.6%), etc. (AICEP, 2011)

Namibia’s Import countries (2008): 1st South Africa (67.8%), 2

nd UK (8%), 3

rd India

(3.5%)… 41th

Portugal (0.1%), etc. (AICEP, 2011). According to INE – Instituto

Nacional de Estatística, there were 63 portuguese companies exporting to Namibia in

2010.

Internationalization of RESUL to Namibia Annexes

11 Ânia Cárin Correia

Annex 10 – Exchange Rate Analysis

Date Exchange rate % Change ZAR/€ Dez-06 9,3 Dez-07 10,0 7,85% Dez-08 12,9 29,23% Dez-09 10,7 -17,60% Dez-10 8,9 -16,91% Nov-11 11,4 28,14% Min 8,9 30,71% ---> Total Cumulative Change

Max 12,9 Source: http://www.x-rates.com/

Internationalization of RESUL to Namibia Annexes

12 Ânia Cárin Correia

Annex 11 - Namibia’s Transport Infrastructure

Infrastructure Investment Projects for the 2011/12 and 2012/13 fiscal years comprise

road construction and upgrading (NAD1.9bn = €17M) and railway construction and

upgrades (NAD0.7bn = €64M). Other key project being implemented regards the

expansion of container handling capacity at the Walvis Bay Port.

Internationalization of RESUL to Namibia Annexes

13 Ânia Cárin Correia

Rankings from the World Economic Forum’s 2011-12 Global Competitiveness Report,

[scores: 0.0: least competitive – 7.0: most competitive]

Quality of overall Namibian Infrastructure: scored 5.3

2nd

ranked in Sub-Saharan Africa (after Mauritus); at 58th out of 142 countries

Road Network: 64,189 km (5,477 km paved, 58,712 km unpaved)

- Road’s quality scored 5.4 (top-ranked in Africa)

Main Ports: Walvis Bay (principal) and Lüderitz

- Port infrastructure scored 5.5 (top-ranked in Africa)

Airports: 129 (21 with paved runways, 108 with unpaved runways);

2 international (Windhoek and Walvis Bay)

- Air transport infrastructure scored 5.0 (59th

worldwide)

Rail Network: 2,615km of narrow gauge

- Scored: 4.0 (top-ranked in Africa)

Extensive and generally well-maintained roads link the majority of towns and

communities, as well as the country with Angola, Zambia, Zimbabwe, Botswana and

South Africa. The Walvis Bay Port positions Namibia as a western gateway to SADC and it

is considered one of Africa’s most efficient, with no single lost of cargo during the last 15

years of operation, characterized also by low crime and low congestion. There are daily

international flights between Namibia and Frankfurt, as well as direct air links to Luanda

(Angola); Cape Town and Johannesburg (South Africa); Maun (Botswana), etc.

Sources:

PwC Namibia. 2010. “Namibia 2010 and beyond”

PwC Namibia. 2008. “A business and Investment Guide for Namibia”

AfDB, OECD, UNDP, UNECA. June 2011. “African Economic Outlook 2011 – Namibia”

CIA – World factbook

U.S. Commercial Service. “Doing Business in Namibia: 2011 Country Commercial Guide for U.S. Companies”,

www.buyusainfo.net

ISI Emerging Markets, Sept. 2011.“Dun & Bradstreet Country Report, Namibia”

Internationalization of RESUL to Namibia Annexes

14 Ânia Cárin Correia

Annex 12 – Namibia’s Power Market

Namibian Electricity Supply Industry Structure

Source: ECB "Annual Report 2010"

GENERATION and power IMPORTS

Installed Capacity

Power Station Plant Type Capacity [MW]

Ruacana Hydro 249

Van Eck Coal 120

Paratus Diesel 24

Anixas Diesel 22

Total 415

In 2012, Ruacana’s capacity will be increased by 92MW. However, the installed

capacity is not enough to meet Namibia’s power demand which leads the country to

import the deficit, mainly from Zimbabwe (Zesa) and South Africa (Eskom). The

remaining is imported from Zambia (Zesco) and Mozambique (EDM). The recently

Internationalization of RESUL to Namibia Annexes

15 Ânia Cárin Correia

constructed Caprivi Link (transmission infrastructure) connects Namibia with Zambia,

Zimbabwe and the Eastern members of SAPP, opening alternatives for electricity

imports, thus decreasing Namibia’s dependence on power imports from South Africa,

whose rapid economic growth is boosting power needs and putting export ability at risk.

Sources:

Namibia Trade Directory. “Electricity - Meeting Changing Needs - Namibia’s Electricity Supply Sector”,

www.namibiatradedirectory.com

U.S. Commercial Service. “Doing Business in Namibia: 2011 Country Commercial Guide for U.S. Companies”,

www.buyusainfo.net

Power Supply Outlook (July 2009 -June 2010)

Source: Nampower’s Annual Report, 2010

In order to address the gap between supply and demand of electricity in Namibia, the

country also plans to continue increasing its installed capacity.

Internationalization of RESUL to Namibia Annexes

16 Ânia Cárin Correia

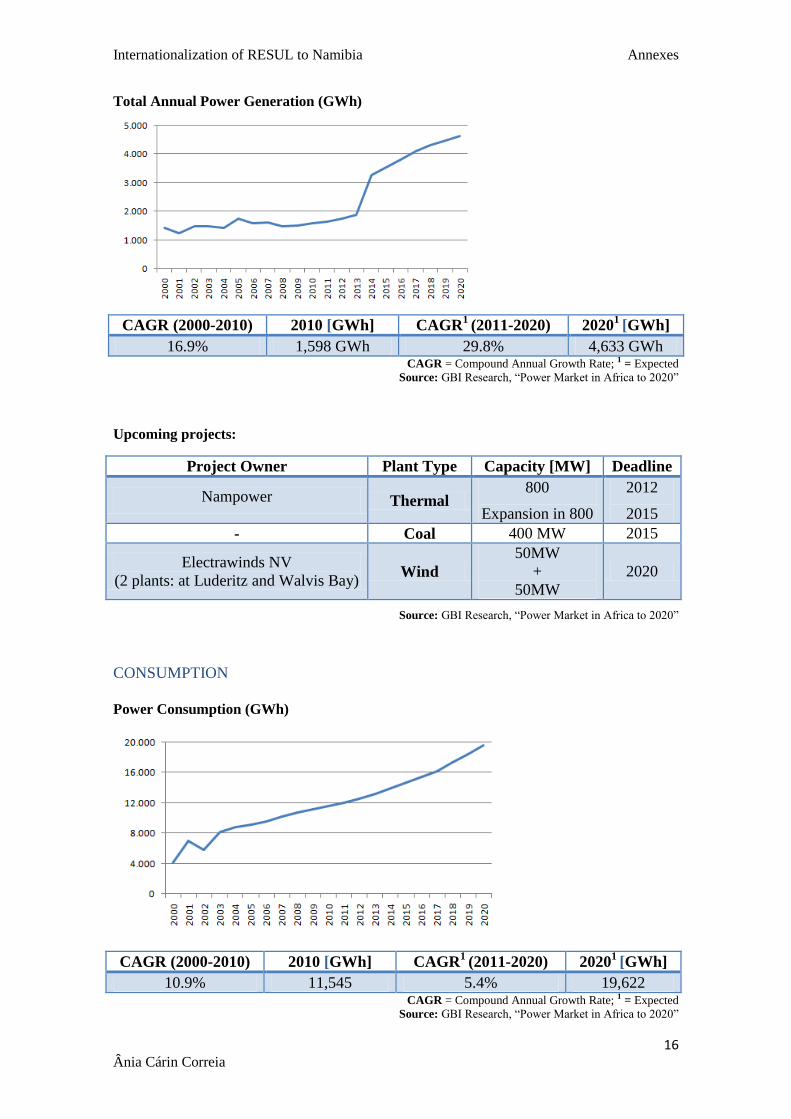

Total Annual Power Generation (GWh)

CAGR (2000-2010) 2010 [GWh] CAGR1

(2011-2020) 20201

[GWh]

16.9% 1,598 GWh 29.8% 4,633 GWh CAGR = Compound Annual Growth Rate; 1 = Expected

Source: GBI Research, “Power Market in Africa to 2020”

Upcoming projects:

Project Owner Plant Type Capacity [MW] Deadline

Nampower Thermal 800

Expansion in 800

2012

2015

- Coal 400 MW 2015

Electrawinds NV

(2 plants: at Luderitz and Walvis Bay) Wind

50MW

+

50MW

2020

Source: GBI Research, “Power Market in Africa to 2020”

CONSUMPTION

Power Consumption (GWh)

CAGR (2000-2010) 2010 [GWh] CAGR1

(2011-2020) 20201

[GWh]

10.9% 11,545 5.4% 19,622 CAGR = Compound Annual Growth Rate; 1 = Expected

Source: GBI Research, “Power Market in Africa to 2020”

Internationalization of RESUL to Namibia Annexes

17 Ânia Cárin Correia

TRANSMISSION

Transmission Lines in Namibia (Km)

Source: GBI Research, “Power Market in Africa to 2020”

Transmission Infrastructure Map

Source: http://www.nampower.com.na/Pages/downloads.asp

Internationalization of RESUL to Namibia Annexes

18 Ânia Cárin Correia

DISTRIBUTION

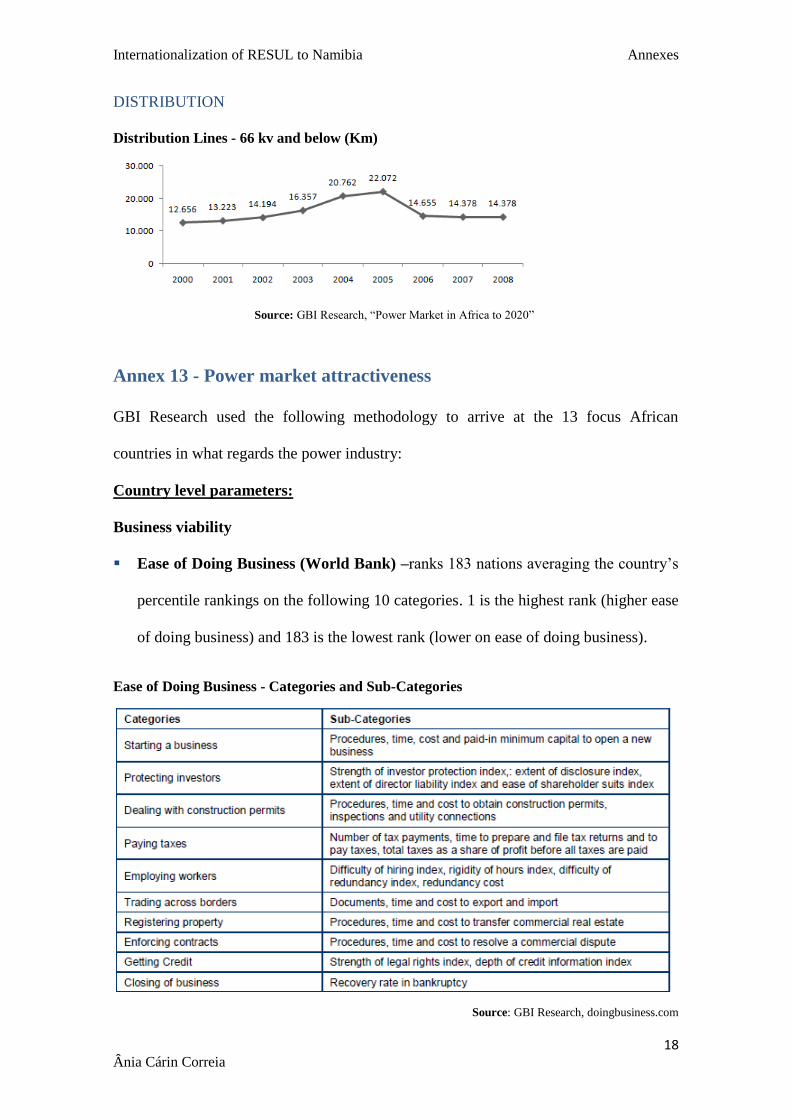

Distribution Lines - 66 kv and below (Km)

Source: GBI Research, “Power Market in Africa to 2020”

Annex 13 - Power market attractiveness

GBI Research used the following methodology to arrive at the 13 focus African

countries in what regards the power industry:

Country level parameters:

Business viability

Ease of Doing Business (World Bank) –ranks 183 nations averaging the country’s

percentile rankings on the following 10 categories. 1 is the highest rank (higher ease

of doing business) and 183 is the lowest rank (lower on ease of doing business).

Ease of Doing Business - Categories and Sub-Categories

Source: GBI Research, doingbusiness.com

Internationalization of RESUL to Namibia Annexes

19 Ânia Cárin Correia

Operational Risk (Economic Intelligence Unit – EIU) – evaluates 150 markets for

operational risks on a scale 0-100. The overall score is an aggregate of the score for

following 10 categories of risk. 1 is the highest rank (lowest operational risk) and

150 is the lowest rank (highest operational risk).

Risk Categories for Business

Source: GBI Research, Economic Intelligence Unit (EIU)

Industry Specific parameters (power industry growth drivers):

Annual power generation in the country

Electrification ratio =

Consumption Growth rate

Weighing the parameters appropriately, GDI arrived at the following winning countries:

Top Countries in Africa, Country Attractiveness Analysis

Source: GBI Research, “Power Market in Africa to 2020”

Internationalization of RESUL to Namibia Annexes

20 Ânia Cárin Correia

Annex 14 – Competitor Assessment

Competitor: KEY ATTRIBUTES VALUED BY THE TARGET

Product

diversification

Cost

&

Price

Innovation Service +

Technical

Assistance +

follow up

Physical

presence in

the market /

Proximity

Co

ncl

usi

on

RESUL Multi-category

(+)

Low Medium

(leading

brands)

High Locally

(Agent)

SICAME Few categories High

(source:

RESUL)

High (R&D) High Nearby

(South

Africa)

2

CAHORS INT Multi-category High (e) High (R&D) Low. With 1

commercial

manager for

15 African

markets I

suppose it is

not able to

give such

attentive

service and

follow-up

Far away

(France) 3

Siemens

Southern

Africa

Mono-category High (e) High (R&D) High Nearby

(South

Africa)

3

EBM Few categories Low

(source:

RESUL)

Medium

(leading

brands)

N/A Nearby

(South

Africa)

1

ADC ENERGY Multi-category Medium (e) Medium High Nearby

(South

Africa),

already

doing

business

with

NORED

2

ARB Multi-category Low Medium Medium Nearby

(South

Africa)

1

Schneider

Electric

Few categories

(source:

RESUL)

High (e) High (R&D) Low

(distributors) Locally

(distributors) 3

ACTOM

Electrical

Products

Few categories High (e) High (R&D) Medium Nearby

(South

Africa)

3

Powertech

Transformers

Mono-category High (e) High (R&D) High Nearby

(South

Africa)

3

Legend: (e) Our Perception according to RESUL’s experience with the same or similar companies in other markets

1 – Strong Threat; 2 – Medium Threat; 3 – Low Threat

Internationalization of RESUL to Namibia Annexes

21 Ânia Cárin Correia

SICAME (France, subsidiary in South Africa)

Vision “Sicame, under the guidance of the EDF (the French utility), has gained a

reputation for the originality of its products connected with advanced

techniques for the electrical power supply.”

Products Wide range of accessories (connectors, cable joints, surge arresters, LV ABC

accessories, etc.) and installation tools.

Service “After-sale service (repairs under guarantee, spare parts, routine maintenance,

collection and delivery of equipment); Training (presentations on client’s site)

and technical assistance (recommendations for the use of their products,

assistance in preparation of specifications and choosing products according to

application requirements).”

Markets The Group has 45 subsidiaries worldwide.

Target/market

presence

Supplier of Nampower.

Capabilities Designs, manufactures and sells.

production facility in South Africa since 1990.

Value

Proposition

High quality products directed at system efficiency; solutions tailored to client

needs due to the synergy with the whole Sicame Group; high product and

service quality and focus on customer satisfaction. Through direct

competition with Sicame in other markets, RESUL classifies its products as

expensive, which makes it difficult for Sicame to compete with largest

competitors from South Africa such as EBM (Eberhardt Martin).

Source: http://www.sicame.co.za/Home.aspx

GROUPE CAHORS (France) - subsidiary Cahors International (France), markets all

Group’s products everywhere in the world.

Key figures 17 subsidiaries worldwide (8 in France and 9 abroad), 1700 employees, €213M

turnover (2009), 6% of turnover invested in R&D.

Products Accessories (ABC, MV/LV connections, cable termination, etc.), switchboards,

metering boxes, MV/LV electrical transformers and equipments for street

lighting (boxes and cubicles for the protection of standard or specific equipment;

and custom made equipment).

Capabilities R&D, production (France, Morocco, Spain, China, Uruguay, and Tunisia) and

high investment in staff training (created its own training institute).

Value

Proposition

Innovation, quality, reliable and cost-saving technical solutions, solutions

adapted to customer specifications.

Distribution Commercial manager responsible for: South Africa, Angola, Botswana, Egypt,

Eritrea, Ethiopia, Kenya, Malawi, Mozambique, Namibia, Nigeria, Uganda,

Tanzania, Zambia, Zimbabwe

Source: http://www.groupe-cahors.com/le-groupe-cahors/legroupe/filiales/francaises/article/cahors-international

Internationalization of RESUL to Namibia Annexes

22 Ânia Cárin Correia

Siemens Southern Africa (South Africa)

Vision “Creating long term value for our shareholders and customers, while acting

responsibly and in the spirit of excellence and innovation.”

Key figures 3,000 employees in the Southern African Region and 88,000 employees

worldwide. In 2010 the energy sector (wider than the electricity sector) provided

it with total revenues of €25.5 billion and €3.6 billion of profit.

Markets The Group is established in over 190 countries and this subsidiary is focused on

countries in the Southern Africa.

Products Transformers and switchgear.

Capabilities Global engineering and manufacturing capabilities for MV and LV switchgear

(global investment of 7% of sales in R&D; 47,000 researchers and developers

worldwide – more than 10% of total employees).

Value

Proposition

Innovation, unique assortment of products tailored to the regional conditions and

requirements, 75% of products and services sold have been developed in the last

5 years; cost-effective, turnkey end-to-end solutions and customer focus.

Target /

Market

Presence

Business unit Power Transmission and Distribution (PTD) equipped sub-stations

in Namibia.

Source:

http://www.siemens.com/entry/za/en/

http://www.saeec.org.za/members/siemens-southern-africa

Eberhardt-Martin cc (EBM) - South Africa

Products Wide range of fittings (E.g.: connectors for underground cables, Aerial Bundle

Conductors, etc.), tools, surge arrestors and switchgear.

Value

Proposition

Innovative and cost effective products (EBM’s range of products and

representation of several leading European and American Manufacturers - WH

Salsbury, Joslyn, Hastings, Klauke, etc.

Target /

Market

Presence

Supplies the Southern Africa.

Source: http://www.ebm.co.za/our_company.htm

Internationalization of RESUL to Namibia Annexes

23 Ânia Cárin Correia

ADC ENERGY (South Africa)

Products Switchgear, Circuit Breakers, Surge Arresters, Mini-subs, Bulk Metering

Units, Transformers and cable accessories (LV, MV, HV Cable Accessories;

Heat Shrink; Cold Shrink; Cold Applied Connectors - Lugs, Ferrulles,

Connectors, Torque Shear Connectors; etc.)

Capabilities Manufacturing.

Value

Proposition

The company states that it provides only the best quality and tested products, it

is customer oriented, has strong technical expertise and customer service,

works close to customers in order to better satisfy their needs, keeps up with

technology and provides training to customers for them to make the best use of

their equipments.

Target /

Market

Presence

It targets utilities, municipalities, distributors, wholesalers and contractors.

ADC has already completed a contract with NORED Namibia, Exhibited at the

African Utility Week in 2011 and provided training to NORED Namibia in

2010.

Source: http://www.adcenergy.co.za/

ARB (South Africa) – Electrical Wholesalers

Size 15 branches in South Africa.

Markets Over 5 000 customers throughout South and sub-Saharan Africa (probably

resellers).

Products Stocks all products necessary to complete any electrical project (produced in

South Africa or imported): Aluminum conductors, Aerial Bundle Conductor,

Transformers & Mini-subs, Voltage Regulators, Insulators, Low voltage aerial

bundle accessories, House connection accessories (Passive bases, ready

boards), Surge Arrestors, Compression fittings, Circuit Breakers, Distribution

Boards, Earthing Materials, Light Fittings and Lamps, Switchgear, Tools, etc.

Value

Proposition

Competitive pricing and product variety.

Target /

Market

Presence

No evidence of presence in Namibia but corporate objective of geographic

expansion into sub-Saharan Africa

Source: http://www.arbhold.co.za/

Internationalization of RESUL to Namibia Annexes

24 Ânia Cárin Correia

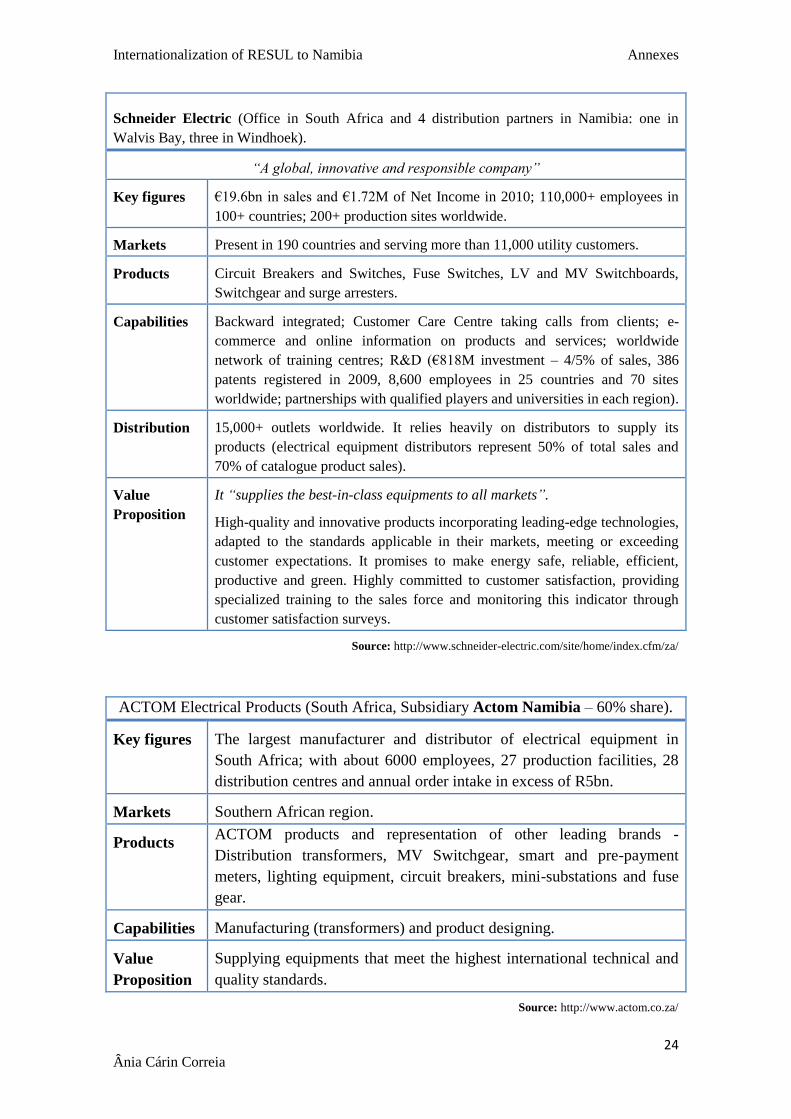

Schneider Electric (Office in South Africa and 4 distribution partners in Namibia: one in

Walvis Bay, three in Windhoek).

“A global, innovative and responsible company”

Key figures €19.6bn in sales and €1.72M of Net Income in 2010; 110,000+ employees in

100+ countries; 200+ production sites worldwide.

Markets Present in 190 countries and serving more than 11,000 utility customers.

Products Circuit Breakers and Switches, Fuse Switches, LV and MV Switchboards,

Switchgear and surge arresters.

Capabilities Backward integrated; Customer Care Centre taking calls from clients; e-

commerce and online information on products and services; worldwide

network of training centres; R&D (€818M investment – 4/5% of sales, 386

patents registered in 2009, 8,600 employees in 25 countries and 70 sites

worldwide; partnerships with qualified players and universities in each region).

Distribution 15,000+ outlets worldwide. It relies heavily on distributors to supply its

products (electrical equipment distributors represent 50% of total sales and

70% of catalogue product sales).

Value

Proposition

It “supplies the best-in-class equipments to all markets”.

High-quality and innovative products incorporating leading-edge technologies,

adapted to the standards applicable in their markets, meeting or exceeding

customer expectations. It promises to make energy safe, reliable, efficient,

productive and green. Highly committed to customer satisfaction, providing

specialized training to the sales force and monitoring this indicator through

customer satisfaction surveys.

Source: http://www.schneider-electric.com/site/home/index.cfm/za/

ACTOM Electrical Products (South Africa, Subsidiary Actom Namibia – 60% share).

Key figures The largest manufacturer and distributor of electrical equipment in

South Africa; with about 6000 employees, 27 production facilities, 28

distribution centres and annual order intake in excess of R5bn.

Markets Southern African region.

Products ACTOM products and representation of other leading brands -

Distribution transformers, MV Switchgear, smart and pre-payment

meters, lighting equipment, circuit breakers, mini-substations and fuse

gear.

Capabilities Manufacturing (transformers) and product designing.

Value

Proposition

Supplying equipments that meet the highest international technical and

quality standards.

Source: http://www.actom.co.za/

Internationalization of RESUL to Namibia Annexes

25 Ânia Cárin Correia

Powertech Transformers, the largest and most sophisticated distribution transformer

manufacturer in the Southern Africa, 80% owned by Power Technologies (Pty) Ltd, (known as

Powertech).

Vision “To be the preferred supplier of power and distribution transformers and

related services for our targeted markets”.

Products Distribution transformers from 16kVA to 20MVA and miniature substations.

Capabilities R&D and production.

Transformers supplied in Africa are produced at the Powertech Transformers’s

world class plants in Pretoria West, Cape Town and Johannesburg, South

Africa; the first being the largest and most sophisticated transformer

production facility in the Southern Africa and one of the biggest in the world.

Value

Proposition

Products tailor-made to customer requirements, leading-edge technology,

installation, customer centric (first finding out what client’s need and then

make efforts to achieve it), and updating customers on new products and

market trends.

Source: http://www.pttransformers.co.za/

Annex 15 – RESUL’s financial position

Balance sheet, 2010

EQUITY 5,193,417

Non Current Liabilities 1,064,580

Non Current Assets 1,875,920

Current Liabilities 8,544,896

Current Assets 12,926,974

LIABILITIES 9,609,476

ASSETS 14,802,894

TOTAL EQUITY +

LIABILITIES 14,802,893

Source: Sabi - Iberian Balance Sheet Analysis System, 2011

Ratio Analysis:

CURRENT RATIO (liquidity) = Total current Assets / Total current Liabilities =

1,875,920 / 8,544,896 = 1.5

SOLVENCY RATIO = (Net Income + Depreciation) / Non Current Liabilities =

(746,155 + 118,261) / 1,064,580 = 0.8

Internationalization of RESUL to Namibia Annexes

26 Ânia Cárin Correia

Annex 16 – Business Model Analysis

Source: Model used in the course of Internationalization & Implementation Analysis

Annex 17 – REDs

Business Structure

Source: ECB (Detailed RED Model)

Internationalization of RESUL to Namibia Annexes

27 Ânia Cárin Correia

Company Structure

Source: ECB (Detailed RED Model)

NORED (1st RED to be established) received a 25 year distribution and supply licence,

starting in 2003.

Regions: Omusati, Oshana, Ohangwena, Oshikoto, Caprivi, Kavango and

part of Kunene.

Head Office: Ondangwa.

Regional Offices: Katima Mulilo, Rundu, Ondangwa, Ongwediva, Divundu,

Nkurenkuru, Omuthiya, Eenhana, Helao Nafidi and Outapi.

Board of Directors: Mr. E.I. Negonga Independent Director (MRLG & H)

RC Electricity Company

Mr. B.W. Mwaningange Independent Director

Mr. S. Kayone

LA Electricity Company

Mr. L.S. Negonga

Ms. H. T. Udjombala Independent Director

NamPower

Mrs. B.R. Hans

Mr. W. Jetschko Independent Director

Internationalization of RESUL to Namibia Annexes

28 Ânia Cárin Correia

Shareholding:

Source: http://www.nampower.com.na/pages/nored.asp

Erongo RED (2nd

RED to be established) received a distribution licence for 25 years

and a supply licence for 5 years, starting in 2005.

Region: Erongo

Size: 47.959 customers (22.075 in Walvis Bay, 14.723 in Swakopmund,

3.183 in the remaining towns, 7.095 clients of pre-paid electricity and

253 in rural areas).

Head Office: Walvis Bay

Board of

Directors:

Walvis Bay: 2 seats (vacant)

Swakopmund: Mr. W. Rencs and Mr. C. B. N. Botha

Nampower: Mr. I Tjombonde

Henties Bay: Mr. P. F. Hamman

Omaruru: Mr. W. Lita

Arandis TC, Karibib and Usakos Municipalities, Uis VC and

Erongo RC: Mr t. Kaimbi

Shareholders: Municipality of Walvis Bay: 49.87%

Municipality of Swakopmund: 28.49%

Nampower: 10.14%

Municipality of Henties Bay: 4.63%

Municipality of Omaruru: 1.84%

TC of Arandis: 1.66%

Municipality of Karibib: 1.44%

Municipality of Usakos: 1.26%

VC of Uis village: 0.35%

Erongo RC: 0.32%

Source: http://erongored.com/, http://www.nampower.com.na/pages/erongo.asp

Internationalization of RESUL to Namibia Annexes

29 Ânia Cárin Correia

CENORED - Central-North Electricity Distribution Company (Pty) Ltd (3rd RED to be

established) received a 10 years Distribution-and Supply Licence, starting in 2005.

Region: Otjozondjupa and part of Kunene

Size: 40.000 customers over an area of about 120.000 sq Km.

Head Office: Otjiwarongo

Board of Directors: NamPower: Ms Foibe Louise Jacobs (Chairperson),Mr

Horst Dieter Mutschler, Mr Siegfried Schneider, (Mr

Simson Haulofu)

Tsumeb: Mr Oscar Norich,(Dr Ndapandula Jacobs)

Grootfontein: Mr Dirk Hugo,(Mr JJ Oxurub)

Small S/H: Mr Joseph Abel /Urib, (Mr Jhosua E Shilungu)

Otjiwarongo: Mr Manfred /Uxamb, (Mr Burgert A

Liebenberg)

11 Shareholders: Nampower: 50,2%

4 Municipalities: Otjiwarongo, Grootfontein, Outjo and

Tsumeb

2 RCs: Otjozondjupa and Kunene

2 TCs: Khorixas and Okakarara

2 VCs: Otavi and Kamanjab

Sources: http://www.cenored.com.na/, http://www.nampower.com.na/pages/cenored.asp,

http://www.afdevinfo.com/htmlreports/org/org_68416.html

Central RED – will be established in the future.

Shareholders: Nampower: 14%

Windhoek, Witvlei, Gobabis, Okahandja, Ojozondjupa

Region, Khomas Region and Omaheke.

Source: ECB

Southern RED (SORED) – will be established in the future.

Shareholders: Nampower: 37.1%, nominating 2 out of 7 Directors

Stampriet, Mariental, Keetmanshoop, Karasburg, Luderitz,

Rehoboth, Hardap Region, Karas Region, Omaheke Region,

Aranos, Aroah, Berseba, Bethanie, Gibeon, Goohas, Kalkrand,

Koes, Leonardville, Maltahoehe and Tses.

Source: ECB

Legend:

RC – Regional Council

TC – Town Council

LA – Local Authority

VC – Village Council

Internationalization of RESUL to Namibia Annexes

30 Ânia Cárin Correia

Annex 18 - RESUL’s PORTFOLIO – Categories with Product

examples (Source: catalogue)

Overhead Bare Lines Accessories

HV and MV Accessories for Underground Cables

Aerial Bundle Conductors (ABC cables) Accessories

Underground Networks Accessories

String Accessories

Bronze and Aluminium Connectors for Substations

Internationalization of RESUL to Namibia Annexes

31 Ânia Cárin Correia

Terminals, Splices and Tap-Off Connectors

Generators, Transformers and Regulators

Metering

Protection and Disconnection

Band and Buckles

Tools

Internationalization of RESUL to Namibia Annexes

32 Ânia Cárin Correia

Earthing Equipments

Iron Fittings LV and MV

Safety

Switchboards, Distribution Cabinets and Components

Surge and Lightning Arresters

Public Lighting (luminaires and accessories)

LV Heat-Shrinkable Products

Internationalization of RESUL to Namibia Annexes

33 Ânia Cárin Correia

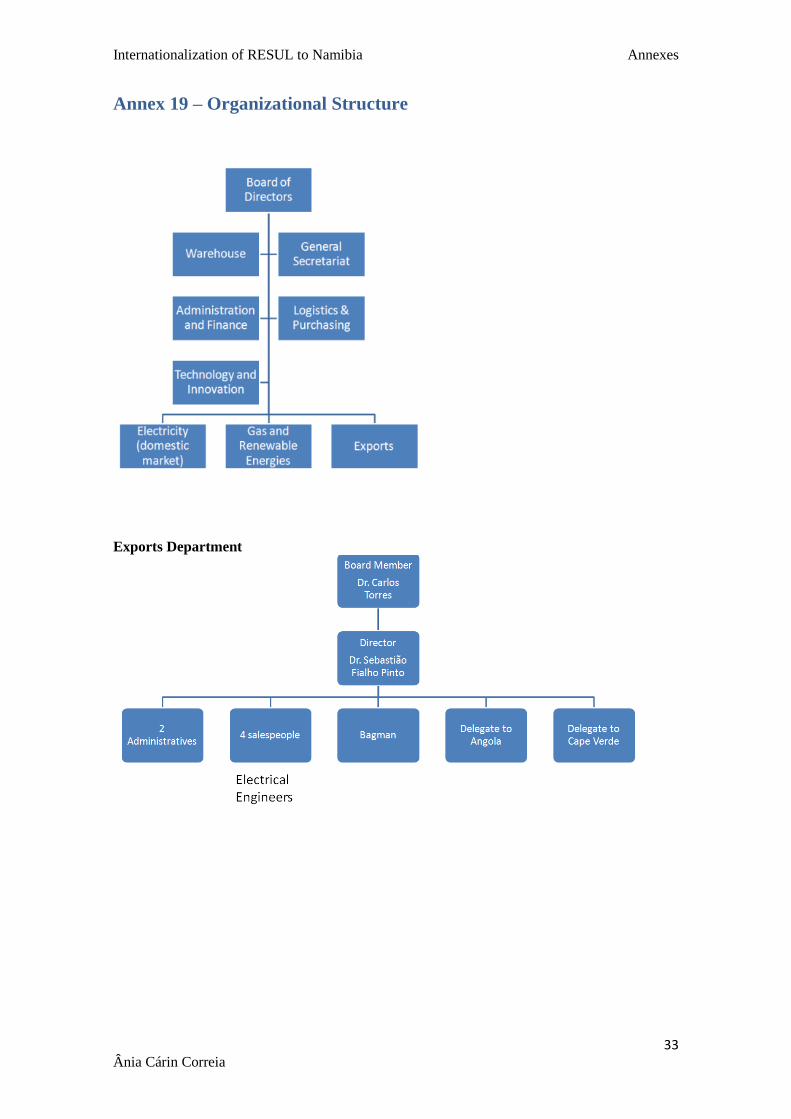

Annex 19 – Organizational Structure

Exports Department

Internationalization of RESUL to Namibia Annexes

34 Ânia Cárin Correia

Annex 20 - SWOT

Strengths Weaknesses

S1: Well-diversified Portfolio

S2: Cost Advantage

S3: Highly qualified and motivated sales

engineers with experience dealing with

African markets

S4: Proximity: Delegation in Angola;

Assembling unit in Mozambique; 2 future

assembly units in Angola and

Mozambique (SADC members)

S5: Good quality-price ratio

S6: Quick customer response

W1: Not being a Namibian company

W2: Lack of local presence, business

contacts within the industry and

knowledge

W3: Lack of cultural affinity like with the

PALOP

W4: Lack of installation capabilities

Opportunities Threats

O1: Small electrification ratio: 34% and

Namibia’s planned investments in

distribution network expansion and

upgrade RESUL’s portfolio matches

the products with immediate need or

potential in Namibia.

O2: Market needs present similarities

with other African countries where

RESUL operates

O3: Potential clients value the price over

the latest innovations

T1: High internal rivalry and price

competition triggered by clients with high

power and price sensitivity

T2: Corruption and importance of

lobbying power

T3: Expected Fierce competition from

South African competitors (benefiting

from low trade barriers, geographical and

cultural proximity)

T4: Culture: Importance of presence and

relationships

T5: Tender preferences given to local

companies

Annex 21 – The RED’s buying process

Purchasing orders up to N$75k [€6.8k] can be handled by the business units, provided

they are approved by the Manager of Financial Administration, who must document

proofs that effort has been made to guarantee a competitive price and satisfactory

quality (e.g.: by obtaining 3 quotations in writing).

Procurement for supplies with total cost in excess of N$75k [€6.8k] is always done

through the tender system. The Head of the Business Unit procuring the goods (Wires

Internationalization of RESUL to Namibia Annexes

35 Ânia Cárin Correia

Business) prepares the tender documentation and sends the application to the Secretary

of the Tender Committee stating the need for the supplies in question. Then the

Secretary of the Tender Committee advertises the tender (stating opening and closing

date, cost of participation, product specifications and delivery requirements, details of

tender collection, etc.).

On the defined date and time, the sealed bids ought to be opened by the Secretary of the

Tender Committee, in the presence of the tender participants attending to the opening

(names of tender participants and prices submitted should be announced), tenders

should be numbered and details registered in a schedule. A copy of the schedule with

details of tender bids and supporting documentation is sent to the Business Unit

requiring the products for evaluation and comparison. The first phase of the assessment

consists of verifying the accuracy of tender prices and ability to meet the technical

specifications and the conditions defined in the tender documents. The second phase

places the remaining tender participants in order of merit, having in consideration:

“efficiency and compatibility of the equipment; operating cost where applicable,

availability of after-sales service and spare parts and financial resources” available to

the tender participant. Subsequently, the Business Unit shall prepare a detailed report

with the assessment and comparison of tenders, mentioning the specific reasons for the

awarding of the contract or refusal of all tenders. The Manager of Financial

Administration should communicate the outcome to the Tender Committee, for its

approval.

The tender should be awarded within the period specified for validity of tender,

followed by the emission of detailed ordering letters or purchase orders signed by the

Manager of Financial Administration.

Internationalization of RESUL to Namibia Annexes

36 Ânia Cárin Correia

Decision Making Unit

USER: installers and engineers responsible for the electrification projects.

BUYER: the Head of the Business Unit procuring the goods (Wires Business) and staff

from its purchasing department.

ANALYSER (examines and evaluates information and alternatives): The Business unit

requiring the products, the Manager Financial Administration, Tender Committee

and/or Board as is appropriate.

INFLUENCER (supply information for the evaluation of alternatives and sets product

specifications): External consultants hired to evaluate tenders, those in technical

departments, engineers, quality control, etc.

GATEKEEPER (controls information to be reviewed by others): Secretary of the

Tender Committee and the assistants of the important decision makers.

DECIDER: The award of a contract shall be made by majority vote of the Tender

Committee subject to ratification by the Board as is appropriate.

Source: http://erongored.com/

Internationalization of RESUL to Namibia Annexes

37 Ânia Cárin Correia

Annex 22 - Head Offices of the REDs and the country capital (where the

technical seminars will take place)

Time distances by car

Source: http://maps.google.com/

Internationalization of RESUL to Namibia Annexes

38 Ânia Cárin Correia

Annex 23 – Implementation Costs

Internationalization of RESUL to Namibia Annexes

39 Ânia Cárin Correia

Annex 24 - MINUTE

Before Entering the market Dependency of

Activities

Activity 1: Accommodation of Eng. Mesquita e Carmo in

Angola (5 months before)

Activity 2: Fine tune Strategic Approach to Namibia

(5 months before)

Activity 3: Extend Brands Representation Agreements to

include Namibia (4 months before)

Activity 4: Contact AICEP (4 months before)

Activity 5: Site Assessment Due Diligence (4 months before)

Activity 6: Contract CCIPN’s services (4 months before)

Activity 7: 1st visit to Namibia - approaching the agent (2

months before)

Activity 2

Activity 8: Signing contract with the Agent (1 month before) Activity 2 and 7

Activity 9: Agent’s visit to Portugal (1 month before) Activity 8

After Entering the market Dependency of

Activities

Activity 10: Visits of Eng. Mesquita e Carmo to Namibia (1st

month onwards: 3 visits /year)

Activity 2

Activity 11: Visits to Potential Clients – Agent (1st month

onwards)

Activity 2 and 8

Activity 12: Get the products included in the potential clients’

supplier list (when applicable) (during the 7 first months)

Activity 11

Activity 13: Tender Participations (2nd

month onwards) Activity 8 and 11

Activity 14: 1st participation in the Ongwediva Annual Trade

Fair (3 months after)

Activity 15: 1st participation in the Power & Electricity World

Africa (10 months after)

Activity 16: Providing the 1st Technical Seminar in Windhoek

(18 months after)