ANK OF BOTSWANA Statutory... · Table 2.4 Trends in Income Inequality, 1985/86 ... BSE Botswana...

118

ANNUAL REPORT BANK OF BOTSWANA 2004

Transcript of ANK OF BOTSWANA Statutory... · Table 2.4 Trends in Income Inequality, 1985/86 ... BSE Botswana...

1

ANNUAL REPORT

BANK

OF

BOTSWANA

2004

blank page 2

3

4

BANK OF BOTSWANA ANNUAL REPORT 2004

5

BANK OF BOTSWANA ANNUAL REPORT 2004

BOARD MEMBERS

as at December 31, 2004

L. K. Mohohlo

Governor and Chairman of the Board

S. S. G. Tumelo

Board Member

G. K. Cunliffe

Board Member

J. SentshoBoard Member

B. MoeletsiBoard Member

U. CoreaBoard Member

6

BANK OF BOTSWANA ANNUAL REPORT 2004

CONTENTS – PART A

Statutory Report on the Operations and Financial

Statements of the Bank in 2004

Page

1. An Overview of the Bank 15

Objectives of the Bank 15

Functions of the Bank 15

Structure of the Bank 16

Strategies 17

2. Report on the Bank’s Operations 19

Introduction 19

External Relations 20

Management and Administration of the Bank 20

Monetary Policy Implementation 21

Reserve Management 21

Domestic Market Operations 21

Banking, Currency and Payment System Issues 21

Banking Supervision 22

Agency Role 22

Information Technology 22

Protective Services 23

3. Annual Financial Statements 25

7

BANK OF BOTSWANA ANNUAL REPORT 2004

CONTENTS – PART B

Page

1. The Botswana Economy in 2004 51

Output, Employment and Prices 51

Public Finance 57

Exchange Rates, Balance of Payments and International

Investment Position 60

Money and Capital Markets 64

2. Improved Productivity – The Key to Sustained Growth

and Higher Living Standards for All 73

Introduction 73

Productivity And Economic Growth 75

Issues in Measuring Productivity 83

Enhancing and Maintaining Productivity Growth:

The Case of Botswana 90

Productivity, Sustained Growth and Higher Living Standards

for All 102

Conclusion 109

Appendix A: Data Sources and Growth Accounting

Methodology 111

8

BANK OF BOTSWANA ANNUAL REPORT 2004

FIGURE, CHARTS, AND TABLES

Figure Page

Figure 2.1: The Stages of Technological Progress 79

Charts

Chart 1.1 Growth in Real Gross Domestic Product 51

Chart 1.2 Economic Growth by Sector 51

Chart 1.3 Botswana Inflation 56

Chart 1.4 CPI Inflation by Tradeability 56

Chart 1.5 International Inflation 56

Chart 1.6 Nominal and Real Effective Exchange Rates and Relative Prices 61

Chart 1.7 NEER and Nominal Exchange Rate Indices Against

Selected Currencies 61

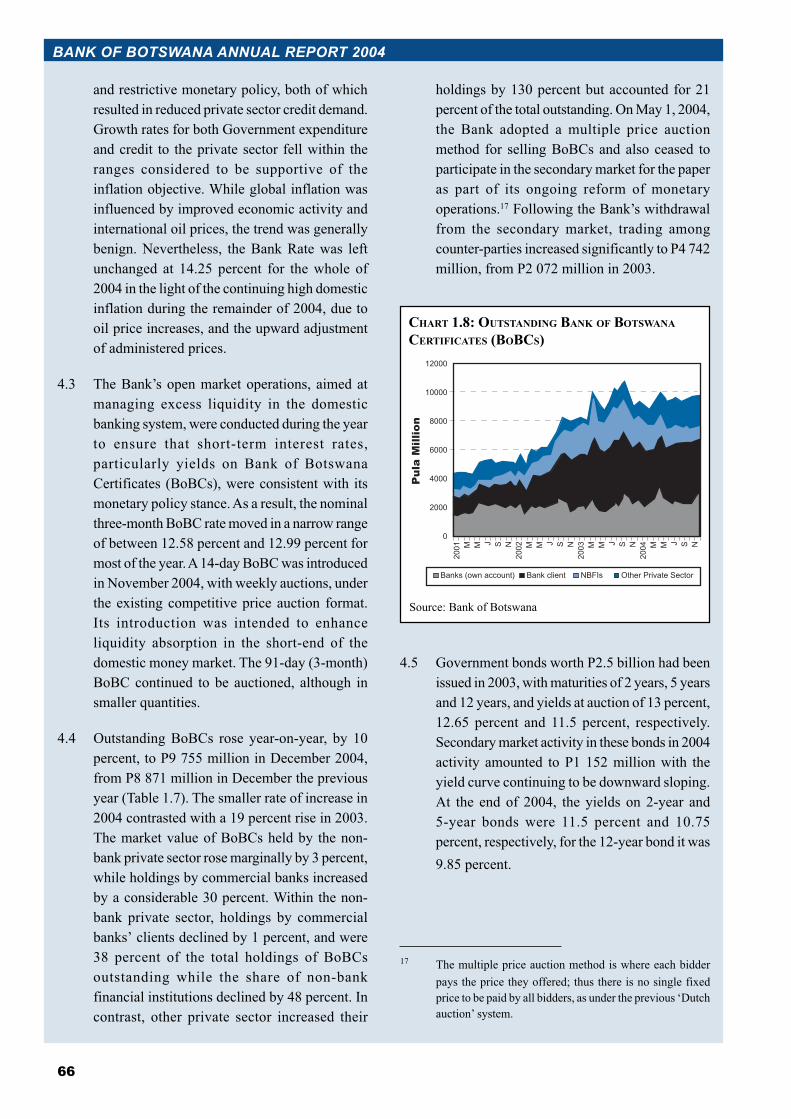

Chart 1.8 Outstanding Bank of Botswana Certificates (BoBCs) 66

Chart 1.9 Yield to Maturity on BoBCs and Government Bonds 67

Chart 1.10 Real Interest Rates: International Comparisons 68

Chart 1.11 Annual Growth Rates of Credit 68

Chart 2.1 Real GDP, Real GDP Less Mineral Rents, and Growth

Rates of GDP and GDP per Capita (3-Year Moving Averages) 84

Chart 2.2 Labour Force and Capital Stock 85

Chart 2.3 Real Recurrent Expenditure on Health and Education

and 3-Year Moving Average Growth Rates 86

Chart 2.4 Sectoral Share in GDP: 1974/75 87

Chart 2.5 Sectoral Share in GDP: 2002/03 87

Chart 2.6 Sectoral Share in GDP 87

Chart 2.7 Total Factor Productivity Growth 88

Tables

Table 1.1 The Government Budget: 2003/04 – 2005/06 (P million) 58

Table 1.2 Pula Exchange Rates Against Selected Currencies 60

9

BANK OF BOTSWANA ANNUAL REPORT 2004

Table 1.3 Balance of Payments: 2000–2004 (P million) 62

Table 1.4 Major Exports (P million) 62

Table 1.5 Levels of Foreign Investment in Botswana by Industry

(P million as at 31 December 2003) 65

Table 1.6 Levels of Foreign Investment in Botswana by Country

(P million as at 31 December 2003) 65

Table 1.7 Structure of Bank of Botswana Certificate Holdings 67

Table 1.8 Nominal Yields to Maturity on BoBCs and Government

Bonds (Percent) 67

Table 2.1 Percentage Shares of Factor Payments to Capital, Skilled

Labour and Unskilled Labour: 1985/86, 1992/93 and 1996/97 85

Table 2.2 Total Factor Productivity Growth, 1974/75 to 2004/05 90

Table 2.3 Sources of Real GDP Growth for Selected Countries and

Country Groupings 91

Table 2.4 Trends in Income Inequality, 1985/86 – 2002/03

(gini coefficient) 105

Table 2.5 Real Income Growth, 1993/94 – 2002/03 (percent) 105

Table 2.6 Poverty in Botswana (percent of population) 106

Table 2.7 Economically Active Population 1991 – 2001 (‘000) 107

Table 2.8 Unemployment by Settlement Type, 2002/03 (Percent) 107

Table A.1 Factor Inputs and Output: 1974/75 to 2004/05 (1993/94 prices) 112

Table A.2 Growth Competitiveness Index (GCI) Rankings for Selected

Countries: 2003 113

Table A.3 The Networked Readiness Index (NRI) Rankings for

Selected Countries: 2003–2004 114

Table A.4 Trade Competitiveness Rankings for Selected African

Countries: 1980–2001 115

Table A.5 Indicators of Ease or Difficulty of Doing Business

in Selected Countries: 2004 116

Page

10

BANK OF BOTSWANA ANNUAL REPORT 2004

ABBREVIATIONS USED IN THE REPORT

AGOA Africa Growth Opportunity Act

ATM Automated Teller Machine

BCI Business Competitiveness Index

BoBCs Bank of Botswana Certificates

BDC Botswana Development Corperation

BEDIA Botswana Export Development and Investment Agency

BIDPA Botswana Institute for Development and Policy Analysis

BMC Meat Commission

BNPC Botswana National Productivity Centre

BOTEC Botswana Technology Centre

BSB Botswana Savings Bank

BSE Botswana Stock Exchange

BURS Botswana Unified Revenue Services

CSO Central Statistics Office

CEDA Citizen Entrepreneurial Development Agency

DCEC Directorate on Corruption and Economic Crime

DPCF Debt Participation Capital Funding

ECH Electronic Clearing House

EFT Electronic Funds Transfer

FAP Financial Assistance Policy

FDI Foreign Direct Investment

FIAS Foreign Investment and Advisory Service

FTA Free Trade Area

GC Gini Coefficient

GCI Growth Competitiveness Index

GDP Gross Domestic Product

HIES Household Income and Expenditure Survey

ICT Information and Communications Technology

IFSC International Financial Services Centre

IIP International Investment Position

IMF International Monetary Fund

11

BANK OF BOTSWANA ANNUAL REPORT 2004

KBL Kgalagadi Breweries Limited

MDGs Millennium Development Goals

MEI Macroeconomic Environment Index

NDB National Development Bank

NEER Nominal Effective Exchange Rate

NPS National Payment System

NRI Network Readiness Index

NTBs Non-Tariff Barriers

OCC Olympia Capital Corporation Limited

OECD Organisation for Economic Cooperation and Development

OPEC Organisation of Petroleum Exporting Countries

PDSF Public Debt Service Fund

PMS Performance Management System

PMP Privatisation Master Plan

PRI Productive Resource Index

QPI Quality and Public Institutions Index

REER Real Effective Exchange Rate

REI Rigidity Employment Index

RIIC Rural Industries Innovation Centre

RTGS Real Time Gross Settlement

SADC Southern African Development Community

SDR Special Drawing Right

SSA Sub-Saharan Africa

VAT Value Added Tax

TFP Total Factor Productivity

TCI Trade Competitiveness Index

TEI Trade-Enabling Environment Index

TI Technology Index

UN United Nations

UNDP United Nations Development Programme

WEF World Economic Forum

BLANK PAGE 12 NOT NUMBERED

13

PART A

STATUTORY REPORT

ON THE OPERATIONS AND

FINANCIAL STATEMENTS OF

THE BANK, 2004

BANK OF BOTSWANA

14

HEADS OF DEPARTMENT

as at December 31, 2004

15

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

STATUTORY REPORT ON THE OPERATIONS OF THE

BANK IN 2004

1. AN OVERVIEW OF THE BANK

Objectives of the Bank

1.1. The primary objective of the Bank, as stated in the Mission Statement, is to promote

and maintain monetary stability. The Bank also ensures that the payments system

is efficient and that the banking system is sound. These functions of the Bank

support the broad national macroeconomic objectives, including the promotion of

sustainable economic diversification. The Bank’s main responsibilities, its

organisational structure and the framework for its activities are described below.

Functions of the Bank

1.2 As prescribed by the Bank of Botswana Act (CAP 55:01) the major responsibilities

of the Bank include the conduct of monetary policy; provision of banking services

to the Government, banks and selected public sector organisations; regulation and

supervision of banks and other financial institutions; issuance of currency;

implementation of exchange rate policy; management of foreign exchange reserves;

and provision of monetary and financial policy advice to the Government.

(a) Monetary Policy implementation is directed mainly at achieving the primary

responsibility of the Bank, which is the promotion and maintenance of monetary

stability. This requires the achievement of low and sustainable inflation, which

contributes to the promotion and maintenance of domestic and external

monetary and financial stability. This objective, together with fiscal, wage,

trade and exchange rate policies, fosters macroeconomic stability, which is a

crucial precondition for achieving sustained development, high rates of

employment and rising standards of living for Batswana.

(b) Central Banking and Payment System Services are mainly provided for the

Government, commercial banks and other selected institutions. The Bank also

operates a clearing system for the banking sector.

(c) Issuance of Currency (banknotes and coin) of high quality is an essential

ingredient of an efficient payments system as it fosters confidence in the legal

tender which, in turn, facilitates transactions and economic activity in general.

(d) Supervision of Banks and Other Financial Institutions is conducted in

accordance with the Banking Act (CAP 46:02) and other relevant statutes. The

purpose of prudential regulation and supervision is to ensure the safety, solvency

and efficient functioning of the banking system and the overall financial sector.

(e) Exchange Rate Policy is implemented on behalf of the Government in the

overall context of sound macroeconomic management. The objective of the

policy is to promote export competitiveness without compromising

macroeconomic stability. The Bank buys and sells foreign exchange at rates

determined in accordance with the exchange rate policy.

The Bank’s primary

objectives are to promote

monetary stability, ensure

an efficient payments

system and a sound

banking sector

Primary responsibilities

are prescribed by

legislation

16

BANK OF BOTSWANA ANNUAL REPORT 2004

(f) Official Foreign Exchange Reserves are managed by the Bank on behalf of the

Government. The Bank ensures their safety and return by diversifying the

investments within a framework of acceptable risks.

(g) Economic Analysis and Policy Advice are covered in periodic reports, published

research papers and statistical documents. Most of the materials are distributed

to other institutions and the public. The Bank is also represented on a number

of Government-led committees and task forces.

Structure of the Bank

1.3 The Bank of Botswana falls under the purview of the Minister of Finance and

Development Planning, who appoints members of the Board, except the ex-officio

Chairman (Governor of the Bank), who is appointed by His Excellency the President.

The Minister reports to Parliament on the Bank’s operations and financial performance.

The Board

1.4 Under the Bank of Botswana Act and the Bank’s Bye-Laws, overall responsibility

for the operations of the Bank is vested in the Board of the Bank. The Board is

responsible for ensuring that the principal objectives of the Bank, as set out in the

Act, are achieved. It also ensures that appropriate policies, management and

administrative systems as well as financial controls are in place at all times in

order for the Bank to achieve its objectives in an efficient and effective manner.

Accordingly, the Board has a direct role in the strategic planning of the Bank, and

in determining the broad policy framework. In this regard, the Board approves the

annual budget, monitors the financial and operational performance, reviews reports

of the external auditors and may call for any policy review.

1.5 The Board comprises nine members and is chaired by the Governor as required

under the Bank of Botswana Act. As at the end of 2004, six members were in place

and there were three vacancies. The Permanent Secretary of the Ministry of Finance

and Development Planning is an ex-officio member; the other members are drawn

from the public service (not more than two), the private sector and academia in

their individual capacities.

1.6 The Board is required to meet at least once each quarter, although typically it

meets more frequently. The Audit Committee of the Board is chaired by a non-

executive Board member, and its main responsibility is to ensure that accounting

policies, internal controls and financial practices are based on established rules

and regulations. The Governor submits a report, after approval by the Board, on

the operations and the audited financial statements of the Bank to the Minister of

Finance and Development Planning within three months of the end of the Bank’s

financial year.1

The Governor

1.7 In addition to chairing the Board, the Governor is the chief executive officer of the

Bank, and is responsible for the prompt and efficient implementation of the decisions

1 The Bank’s financial year coincides with the calendar year.

Minister of Finance

reports to Parliament on

the Bank’s operations

The Board has overall

responsibility over the

Bank’s operations

The nine-member Board

is required to meet at

least once each quarter

The Governor is the

Bank’s chief executive

officer, supported by the

Executive Committee

17

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

or resolutions of the Board. The Governor manages the Bank on a day-to-day

basis, and represents the institution in its relations with the Government, domestic

financial and other institutions as well as external organisations.

The Executive Committee

1.8 The Executive Committee, which is chaired by the Governor, comprises the Deputy

Governors and Heads of Department; it may include co-opted senior staff. Its

responsibility is to advise the Governor on the day-to-day management of the

Bank as well as the development of the Bank’s medium- and long-term plans.

Departments and Divisions

1.9 In order to carry out its functions and supporting activities, the Bank is organised

into Departments and Divisions. At the end of 2004, the Bank’s seven Departments

comprised Administration, Accounting, Banking, Banking Supervision, Financial

Markets, Information Technology and Research, while the three Divisions were

the Board Secretariat, Security and Internal Audit. The Heads of Department

report through the Deputy Governors to the Governor, as do the Heads of Security

and the Board Secretariat. The Internal Audit Division reports directly to the

Governor.

Strategies

1.10 In pursuing its principal objectives of maintaining monetary stability as well as

ensuring the soundness and efficiency of the financial system, the Bank regularly

reviews and adapts its strategies to deal with the changing conditions prevailing in

the financial sector. The Bank’s activities are mainly in the following areas:

Monetary Operations, Reserve Requirements and the Bank Rate

1.11 Monetary stability is mainly reflected in low and stable inflation. Since inflation is

fundamentally influenced by monetary and credit factors, the Bank’s anti-inflation

strategy focuses on the control of banking system credit as an intermediate target.

However, controlling inflation in a small open economy such as Botswana’s, with

trading partners that have often experienced volatile inflation is a major challenge.

1.12 In implementing monetary policy, the Bank uses indirect policy instruments,

particularly open market operations and the Bank Rate. The Bank may also use

banking regulations and moral suasion to achieve monetary policy objectives.

However, the use of Bank of Botswana Certificates (BoBCs), in both the primary

and secondary markets, to control the liquidity of the financial system and influence

short-term interest rates, plays a prominent role in maintaining monetary stability.

1.13 In addition to the Secured Lending Facility (SLF), the Bank also uses Repurchase

Agreements (Repos) to manage short-term and overnight liquidity fluctuations in

the banking system.

1.14 The Bank incorporates data on fiscal and other policies of the Government in the

design of a monetary policy framework and its implementation strategy in order to

ensure macroeconomic stability. Therefore, whenever necessary, monetary policy

The Bank had seven

Departments and three

Divisions in 2004

Maintaining monetary

stability and a sound and

efficient financial system

are key objectives

18

BANK OF BOTSWANA ANNUAL REPORT 2004

may need to be restrictive in order to counteract expansionary fiscal and wage

policies that may erode monetary stability and, therefore, the nation’s prospects

for sustainable economic development. The broad framework of monetary policy

is presented to the public in the annual Monetary Policy Statement.

Banking Services to the Government and Commercial Banks

1.15 The Bank serves as the banker to the Government, commercial banks as well as

certain other institutions, and has provided a payment, clearing and settlement

system for the financial sector. In this regard, the Bank has promoted, coordinated

and successfully implemented a programme that enhances the efficiency and

security of the payments system. It is also a lender of last resort to the financial

institutions under its supervisory purview.

Implementing the Banking Act and Regulations

1.16 Through ongoing banking supervision and regulatory activities, the Bank seeks to

achieve a sound and stable financial system. Accordingly, the Bank ensures that

the mechanisms for sustaining the safety and soundness of licensed financial

institutions are appropriate and that the institutions are managed in a prudent and

safe manner. To that end, the Bank enforces prudential standards with respect to

capital adequacy, liquidity, asset quality and corporate governance of the banks.

1.17 In addition to its focus on the safety and soundness of licensed financial institutions,

the Bank is responsible for ensuring that banks maintain high professional standards

in their operations in order to provide efficient customer service in a transparent

manner. The Bank also has a surveillance responsibility with regard to breaches of

the Banking Act by the public, especially in the form of activities that involve

unauthorised deposit taking and use of banking names.

1.18 Under the provisions of the Banking Act, the Bank has specific responsibilities

relating to money laundering. Accordingly, banks are required to adhere to ‘know

your customer’ provisions when opening accounts, retain appropriate records, report

suspicious activities and cooperate fully with law enforcement agencies in an effort

to combat financial crimes and, in particular, money laundering.

1.19 The Bank is also responsible for the regulation and supervision of the International

Financial Services Centre (IFSC) entities as well as the administration of the

Collective Investment Undertakings (CIU) Act (CAP56:09).

1.20 The Bank monitors commercial bank compliance with primary reserve requirements

and ensures that clearing and settlement activities are conducted safely and

efficiently. As the volume and value of financial transactions managed by the

financial system increases, and Botswana’s linkages with international financial

markets expand, the Bank has to guard against systemic risks that may arise. It is

for this reason that the Bank continually collaborates with private sector institutions,

international organisations and the Government in introducing improvements to

the safety and efficiency of the payments system.

Supervision and

regulation of financial

institutions are

necessary for confidence

and stability

The Bank also has

responsibility for anti-

money laundering policy

and regulation of

international financial

services

19

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

Implementing Exchange Rate Policy

1.21 The Bank acts as the Government’s agent in implementing the exchange rate policy.

Under the Bank of Botswana Act, the President, on the recommendation of the

Minister of Finance and Development Planning, and after consultation with the

Bank, sets the framework for the determination of the external value of the Pula.

At present, the Pula is pegged to a basket of currencies comprising the South

African rand and the Special Drawing Right (SDR - the unit of account of the

International Monetary Fund). Based on the basket, the Bank calculates the

exchange rate for each business day, and quotes the buying and selling rates for

major international currencies to the banks. The Bank monitors the Pula exchange

rate developments regularly with a view to advising the Government on maintaining

export price competitiveness of domestically produced goods.

Managing Foreign Exchange Reserves

1.22 As Botswana’s foreign exchange reserves have continued to grow, the Bank has

subdivided the reserves into two portfolios to meet different objectives. A large

proportion of the reserves is invested in long-term assets (Pula Fund) with a view

to maximising long-term return, while the remainder comprises the Liquidity

Portfolio, which is invested in money market instruments and short-term bonds.

Advice on Economic Policy, Provision of Statistics and Public Education

1.23 In addition to its responsibilities of formulating and implementing monetary policy,

the Bank serves as economic and financial advisor to the Government on a wide

range of issues. These include exchange rate policy, financial sector development,

borrowing, taxation, industrial development and trade.

1.24 The Bank conducts annual briefings on economic trends and publishes economic

and financial statistics and a research bulletin. The Bank has also formulated and

is implementing a public education programme on banking and financial matters.

Meeting the Needs for Banknotes and Coin

1.25 The availability of a safe and convenient currency is essential for an efficient

payments system. For this reason, the Bank routinely ensures that there is an

adequate supply of high quality notes and coin in circulation by withdrawing soiled

and damaged currency and replacing it with new notes and coin. The Bank maintains

stringent standards in the design and production of both notes and coin to ensure

their acceptance as a medium of exchange and to deter counterfeiting and other

forms of debasement.

2. REPORT ON THE BANK’S OPERATIONS

Introduction

2.1 This section highlights key developments relating to the Bank’s functions during

2004.

Foreign exchange

reserves are managed to

meet specific objectives

The Bank serves as

advisor to Government

The Bank is the sole

supplier of notes and

coin

20

BANK OF BOTSWANA ANNUAL REPORT 2004

External Relations

2.2 The Bank continued to enjoy good relationships with regional and international

organisations in 2004, during which period it attended and participated in seminars,

workshops and conferences hosted by international institutions. Such conferences

and seminars included the SADC Committee of Central Bank Governors, the

Association of African Central Banks, the Bank for International Settlements, the

International Monetary Fund (IMF) and the World Bank. The Bank enjoyed

continued assistance from the IMF through long-term regional advisors, short-

term technical assistance and staff placements. As usual, the Bank held annual

economic briefings for a range of stakeholders, including the media, senior

Government officials, representatives of the private and parastatal sectors and

diplomats.

Management and Administration of the Bank

2.3 The Bank’s authorised establishment was unchanged at 559 positions, with 535

occupied positions and 22 vacancies at the end of the year. Of the occupied positions,

14 were held by staff members on various long-term training programmes at local,

regional and overseas universities. In addition, a large number of staff took part in

various short term training programmes during the year.

2.4 The Staff Health Clinic continued to provide primary health care and to assist in

the implementation of the HIV/AIDS in the Workplace programme, which focuses

on promoting awareness of the HIV/AIDS infection and associated dangers, and

developing a culture of tolerance and combating the stigma of HIV/AIDS. To this

end, both educational and promotional activities were carried out, including a

successful voluntary HIV/AIDS testing exercise for staff, conducted by Tebelopele

Voluntary Counselling and Testing Centre. The challenge for the Bank is to continue

to support those affected by HIV/AIDS in order for all to benefit from improved

quality of life, thereby sustaining a respectable level of productivity.

2.5 The Bank produced a number of publications during the year, including the 2003

Annual Report, the 2003 Banking Supervision Annual Report, the 2004 Monetary

Policy Statement (MPS) and its Mid-Year Review, the Research Bulletin and the

monthly Botswana Financial Statistics.

2.6 The Bank undertook numerous public relations activities and maintained close

relations with the media. It also undertook community service programmes through

the Donations Advisory Group; financial and ‘in-kind’ donations were made to a

number of deserving charities and non-governmental organisations. As part of its

Public Education Programme, the Bank participated in the Botswana Confederation

of Commerce Industry and Manpower and Botswana Annual Financial Trade Fairs

and various school career fairs. The Bank also produced a third booklet in the Tsa

Madi comic series and facilitated schools visits, radio broadcasts and TV magazine

programmes.

2.7 On internal audit matters, 33 scheduled audits and three special audits were

completed based on risk-based auditing, and the reports were rated according to

the significance of the findings. The audits provide a means to continuously assess

internal controls and improve ways of communicating findings while ensuring

Voluntary HIV/AIDS

testing exercise for staff

conducted successfully

The Bank continued to

enjoy good relationships

with regional and

international

organisations

The Bank produced a

number of publications

during the year

Public initiatives were

sustained

21

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

that the Departments and Divisions achieve their objectives in the most efficient

manner.

Monetary Policy Implementation

2.8 The Monetary Policy Committee met six times in 2004 and there was no change in

interest rates, indicating maintenance of a tight policy stance. This stance was

necessitated by the desire to attain the inflation objective of 4 – 7 percent, as

announced in the 2004 Monetary Policy Statement, in a period during which there

were upside risks to inflation as a result of the devaluation of the Pula in February

2004, substantial government salary increases, upward adjustment of some

administered prices and rising international oil prices.

2.9 To enhance the capacity to undertake economic analysis in support of policy

formulation, the Bank continued to work on developing an inflation model for

Botswana, and considerable progress has been made with the assistance of an

IMF-sponsored technical assistance mission comprising staff of the Czech National

Bank. A near-term forecasting framework was finalised, while development of a

core model for medium-term forecasting was initiated towards the end of the year.

Work on a biannual business expectations survey progressed well with the first

report produced towards the end of 2004; going forward, this should provide timely

and substantive information on the real sector.

2.10 With respect to statistics, the implementation of the recommendations of the August

2003 IMF technical assistance mission on monetary statistics is continuing. A

follow-up mission was hosted during the year and laid the groundwork for

introducing an expanded depository corporations survey in 2005.

Reserve Management

2.11 The Management conducted a review of reserve management policies and

guidelines and these were approved by the Board in November 2004. The principles

underlying the Bank’s reserve management policies were reaffirmed, but some

adjustments were made to portfolio sizes and asset allocations.

Domestic Market Operations

2.12 In November 2004, the Bank introduced 14-day Bank of Botswana Certificates

(BoBCs) to increase the efficiency of monetary policy implementation. The 14-day

and 91-day BoBCs are auctioned on a weekly basis to market participants; the

supply of the 91-day paper was gradually reduced, as the market participants

accepted the new 14-day instrument, which is expected to play a progressively

more important role in the Bank’s monetary operations.

Banking, Currency and Payments System Issues

2.13 The National Clearance and Settlement System (NCSS) Regulations were finalised,

as a result of which the NCSS Act came into force on March 1, 2005. Agreement

was reached for the transfer of the electronic clearing house to the commercial

banks; this was necessitated by the NCSS Act, which requires the separation of

operational and supervisory responsibilities for clearing systems. Preparations

Restrictive monetary

policy stance maintained

The Bank introduced 14-

day Bank of Botswana

Certificates

The National Clearance

and Settlement System

(NCSS) Regulations

were finalised

The Bank continued to

work on developing an

inflation model for

Botswana

The implementation of

the recommendations

to improve monetary

statistics continued

Board approves reserve

management policies

and guidelines

22

BANK OF BOTSWANA ANNUAL REPORT 2004

continued for the implementation of the Real Time Gross Settlement (RTGS) system

project in 2005.

2.14 The Bank experienced a problem of dye-stained banknotes which were linked to

robberies during the year. A series of measures were taken to ensure that dye-

stained banknotes were removed from circulation.

2.15 Agreement has been reached on the transfer of the Letlole National Savings

Certificates (LNSCs) scheme to the Botswana Savings Bank (BSB) early in 2005.

2.16 New P100 notes with improved security features were introduced towards the end

of the year.

Banking Supervision

2.17 The financial condition of banks was assessed through regular bilateral and trilateral

meetings, on-site examinations, risk profiling and ‘early warning’ management

reports. There were no issues of supervisory concern with regard to banks’ capital,

profitability, liquidity and management.

2.18 Enterprise Banking Group (Pty) Limited was issued with a banking licence to

operate in the International Financial Services Centre (IFSC). Enterprise will provide

banking services to non-residents through its subsidiaries. As at December 31,

2004, there were three licensed offshore banks in the centre. Furthermore, nine

companies were issued with Exemption Certificates in accordance with IFSC rules.

Stanbic Investment Management Services (Pty) Limited (SIMS) was granted a

licence to manage unit trusts under the CIU Act.

2.19 The total number of licensed and operating bureaux de change as at December 31,

2004 was 34. On-site inspections were conducted on seven bureaux and, in general,

they were found to be operating satisfactorily with no major issues of prudential

concern. The new Bureaux de Change Regulations became effective during the

year.

Agency Role

2.20 As agent of the Government in terms of Section 43 of the Bank of Botswana Act,

the Bank hosted two annual review missions for Botswana’s sovereign credit rating

by the two international credit rating agencies (Standard and Poor’s and Moody’s

Investors Service). The credit ratings, first assigned to Botswana by both agencies

in 2001, were reconfirmed.

2.21 In addition, the Bank continued to act as agent for the Government in the

administration of the Government Bond Programme. Debt Participation Capital

Funding (DPCF) Limited, a special purpose investment company established in

March 2004 to purchase from the Government the Public Service Debt Fund (PDSF)

loan book, made 7 new listings.

Information Technology

2.22 The major IT project implemented during the year was the replacement of existing

Bankmaster core banking system with Globus. Implementation work started in

May 2004 and the system went live in February 2005. In addition, the SWIFT

The Bank experienced a

problem of dye-stained

banknotes

Enterprise Banking

Group (Pty) Limited was

issued with a banking

licence

The total number of

licensed and operating

bureaux de change as at

December 31, 2004 was

34.

The Bank hosted visits

by the international

credit rating agencies

Bankmaster core

banking system replaced

with Globus

23

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

system was successfully migrated to the SWIFTNet platform, which will be used

to support the RTGS implementation.

2.23 A revamped Bank website was launched in June 2004, providing a much broader

range of information about the Bank as well as economic and financial data. The

website carries a range of news items and is one of the Bank’s primary means of

communicating with its stakeholders.

2.24 Protection of the Bank’s network against viruses has been improved with the

installation of a new anti-virus software engine. Software for filtering and blocking

unwanted email messages, commonly referred to as junk mail or ‘spam’, was

acquired and installed on the Bank’s e-mail system. The Bank acquired and

configured an alternative firewall to enhance protection against hackers.

Protective Services

2.25 The banking system in general, and the Bank of Botswana in particular, continued

to experience attempted cheque frauds. Of particular concern to the Bank was the

discovery of high quality forged Government cheques which criminals were

attempting to use to withdraw large sums of money from Government accounts.

The suspects were arrested and the cases are currently before the courts.

In March 2004, a large number of counterfeit P100 banknotes were discovered.

Investigations established that the production and circulation of the counterfeits

was the work of a well organised group. After a vigorous public education drive,

the problem was brought under control.

A revamped Bank

website was launched

A large number of

counterfeit P100

banknotes were

discovered

A new anti-virus

software engine was

installed

The Bank continued to

experience attempted

cheque frauds

BLANK PAGE 24, NOT NUMBERED

25

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

ANNUAL FINANCIAL STATEMENTS

2004

BANK OF BOTSWANA

BLANK PAGE 26 NOT NUMBERED

27

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

CONTENTS

Page

Report of the Independent Auditors 28

Balance Sheet 29

Income Statement 30

Cash Flow Statement 31

Statement of Changes in Shareholder’s Funds 32-33

Accounting Policies 34-39

Notes to the Annual Financial Statements 40-47

The Annual Financial Statements set out on pages 29 to 47 were

approved by the Board on March 22, 2005 and signed by:

__________________ __________________

Linah K. Mohohlo Nozipho A. Mabe

Governor Director, Accounting Department

28

BANK OF BOTSWANA ANNUAL REPORT 2004

29 to 47

29

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

BALANCE SHEET

December 31, 2004

Notes 2004 2003ASSETS P’000 P’000

Property and Equipment 1 130 244 126 645

Foreign Exchange ReservesLiquidity Portfolio 2.1 3 727 352 3 910 508Pula Fund 2.2 20 013 213 19 245 850International Monetary Fund

Reserve Tranche 3.1 134 084 197 373Holdings of Special Drawing Rights 3.2 226 327 219 210Administered Funds 3.4 99 219 144 031

Total Foreign Exchange Reserves 24 200 195 23 716 972

Government of Botswana Bonds 4 108 229 111 723

Advances to Banks 5 11 900 –

Other Assets 6 42 513 53 983

TOTAL ASSETS 24 493 081 24 009 323

LIABILITIES

Notes and Coin in Circulation 7 910 858 817 995Bank of Botswana Certificates 8 9 649 272 8 739 346Deposits 9 1 684 555 1 599 776Allocation of Special Drawing Rights (IMF) 3.3 28 584 28 379Liabilities to Government (IMF Reserve Tranche) 10 134 084 197 373Dividend to Government 11 97 025 188 750Other Liabilities 12 26 370 26 774

Total Liabilities 12 530 748 11 598 393

SHAREHOLDER’S FUNDS

Paid-up Capital 13 25 000 25 000Government Investment Account

Pula Fund and Liquidity Portfolio 8 936 740 9 680 966Currency Revaluation Reserve 129 893 153 138Market Revaluation Reserve 1 270 700 951 826General Reserve 14 1 600 000 1 600 000

Total Shareholder’s Funds 11 962 333 12 410 930

TOTAL LIABILITIES AND SHAREHOLDER’S FUNDS 24 493 081 24 009 323

FOREIGN EXCHANGE RESERVES IN US DOLLARS1 5 660 426 5 338 690

FOREIGN EXCHANGE RESERVES IN SDR2 3 700 210 3 642 927

Note: Bid (2003-mid) rates of exchange used at year-end

1 Pula/United States dollar 0.2339 0.2251

2 Pula/SDR 0.1529 0.1536

30

BANK OF BOTSWANA ANNUAL REPORT 2004

INCOME STATEMENT

Year ended December 31, 2004

Notes 2004 2003

P’000 P’000

INCOME

Interest – Foreign exchange reserves 634 184 719 686

Interest – Debt Participation Capital Funding Limited Loan 23 19 989 –

Interest – Government of Botswana Bonds 10 996 8 626

Net market gains on disposal of securities 439 742 21 284

Dividends 171 156 151 715

Commissions 4 625 5 159

Unrealised currency revaluation gains – Liquidity Portfolio 15 6 872 9 758

Other income 9 263 5 704

1 296 827 921 932

EXPENSES

Interest 16 1 174 385 1 237 173

Administration costs 164 868 131 751

Realised currency revaluation losses 15 341 837 1 778 989

Depreciation 11 604 11 488

Unrealised market revaluation losses – Liquidity Portfolio 8 844 20 459

1 701 538 3 179 860

NET LOSS FOR THE YEAR (404 711) (2 257 928)

TRANSFER FROM CURRENCY REVALUATIONRESERVE

15 338 065 1 766 708

NET LOSS BEFORE TRANSFER FROM GOVERNMENTINVESTMENT ACCOUNT (66 646) (491 220)

TRANSFER FROM GOVERNMENT INVESTMENTACCOUNT 454 746 1 246 220

NET INCOME AVAILABLE FOR DISTRIBUTION 388 100 755 000

APPROPRIATIONS

DIVIDEND TO GOVERNMENT FROM PULA FUND (388 100) (755 000)

31

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

CASH FLOW STATEMENT

Year ended December 31, 2004

Notes 2004 2003

OPERATING ACTIVITIES

P’000 P’000

Cash generated by operations 18 871 845 1 063 542

INVESTING ACTIVITIES

(Net foreign investments purchased)/Net proceeds from

disposal of foreign investments (81 584) 4 210 781

Loan to Debt Participation Capital Funding Limited (800 000) –

Loan Repayment by Debt Participation Capital Funding

Limited 800 000 –

Purchase of Government of Botswana Bonds – (101 903)

Proceeds from disposal of property and equipment 404 215

Purchase of property and equipment 1 (16 107) (11 628)

NET CASH (USED IN)/FRO M INVESTING

ACTIVITIES (97 287) 4 097 465

FINANCING ACTIVITIES

Dividend to Government 11 (479 825) (823 475)

Government Withdrawals (387 596) (4 396 452)

NET CASH USED IN FINANCING ACTIVITIES (867 421) (5 219 927)

NET INCREASE IN CURRENCY IN CIRCULATION (92 863) (58 920)

CURRENCY IN CIRCULATION AT THE BEGINNING OF

THE YEAR (817 995) (759 075)

CURRENCY IN CIRCULATION AT THE END OF THE YEAR (910 858) (817 995)

32

BANK OF BOTSWANA ANNUAL REPORT 2004

STATEMENT OF CHANGES IN SHAREHOLDER’S FUNDS

Year ended December 31, 2004

Paid-up

Share

Capital

Currency

Revaluation

Reserve

Market

Revaluation

Reserve

General

Reserve

P’000 P’000 P’000 P’000

Balance at January 1, 2003 25 000 2 449 842 – 1 600 000

Unrealised currency losses for the year – (1 767 738) – –

Unrealised market gains for the year – – 1 573 082 –

Transfers to/(from) Government Investment Account:

Unrealised market gains for the year – – (621 256) –

Unrealised currency losses for the year – 1 237 742 – –

Government withdrawals – – – –

Net (losses)/gains not recognised in the

Income Statement for the year – (529 996) 951 826 –

Net loss for the year – – – –

Transfer from Currency Revaluation Reserve – (1 766 708) – –

Dividend to Government from Pula Fund – – – –

Transfers to/(from) the Income Statement for the year:

Deficit of Government Pula Fund income over Pula

Fund Dividend – – – –

To cover residual deficit – – – –

Balance at December 31, 2003 as previously

stated 25 000 153 138 951 826 1 600 000

Prior year adjustments resulting from changes in

accounting policies – (7 975) (28 667) –

Balance at December 31, 2003 as restated 25 000 145 163 923 159 1 600 000

Transfer to Income Statement of currency gains realised

on repayment of loan by the IMF’s Poverty Reduction

& Growth Facility (PRGF) Administered Fund – (17 229) – –

Unrealised currency gains for the year – 373 309 – –

Net unrealised market gains for the year – – 427 730 –

Transfers to/(from) Government Investment Account:

Unrealised market gains for the year – – (80 189) –

Unrealised currency gains for the year – (33 285) – –

Government withdrawals – – – –

Net gains/(losses) not recognised in the Income

Statement for the year – 322 795 347 541 –

Net loss for the year before realised currency gains on

the IMF’s PRGF Administered Fund loan repayment – – – –

Currency gains realised on loan repayment by the IMF’s

PRGF Administered Fund – – – –

Transfer from Currency Revaluation Reserve – (338 065) – –

Dividend to Government from Pula Fund – – – –

Transfers to/(from) the Income Statement for the year:

Deficit of Government Pula Fund Income over Pula

Fund Dividend – – – –

To cover residual deficit – – – –

Balance at December 31, 2004 25 000 129 893 1 270 700 1 600 000

1. The Government Investment Account, which represents the Government’s share of the Pula Fund and the Liquidity Portfolio, was

established on January 1, 1997.

2. The dividend to the Government of P388 100 000 for the year was made from the Government’s capital investment in the Pula Fund.

33

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

Government

Investment Account

Accumulated

Profit Total

P’000 P’000 P’000

15 940 124 – 20 014 966 Balance at January 1, 2003

– – (1 767 738) Unrealised currency losses for the year

– – 1 573 082 Unrealised market gains for the year

Transfers to/(from) Government Investment Account:

621 256 – – Unrealised market gains for the year

(1 237 742) – – Unrealised currency losses for the year

(4 396 452) – (4 396 452) Government withdrawals

(5 012 938) – (4 591 108)

Net (losses)/gains not recognised in the

Income Statement for the year

– (2 257 928) (2 257 928) Net loss for the year

– 1 766 708 – Transfer from Currency Revaluation Reserve

– (755 000) (755 000) Dividend to Government from Pula Fund

Transfers to/(from) the Income Statement for the year:

(494 888) 494 888 –

Deficit of Government Pula Fund income over Pula

Fund Dividend

(751 332) 751 332 – To cover residual deficit

9 680 966 – 12 410 930

Balance at December 31, 2003 as previously

stated

(15 358) – (52 000)

Prior year adjustments resulting from changes in

accounting policies

9 665 608 – 12 358 930 Balance at December 31, 2003 as restated

– – (17 229)

Transfer to Income Statement of currency gains realised

on repayment of loan by the IMF’s Poverty Reduction

& Growth Facility (PRGF) Administered Fund

– – 373 309 Unrealised currency gains for the year

– – 427 730 Net unrealised market gains for the year

Transfers to/(from) Government Investment Account:

80 189 – – Unrealised market gains for the year

33 285 – – Unrealised currency gains for the year

(387 596) – (387 596) Government withdrawals

(274 122) – 396 214

Net gains/(losses) not recognised in the Income

Statement for the year

– (421 940) (421 940)

Net loss for the year before realised currency gains on the

IMF’s PRGF Administered Fund loan repayment

– 17 229 17 229

Currency gains realised on loan repayment by the IMF’s

PRGF Administered Fund

– 338 065 – Transfer from Currency Revaluation Reserve

– (388 100) (388 100) Dividend to Government from Pula Fund

Transfers to/(from) the Income Statement for the year:

(94 210) 94 210 –

Deficit of Government Pula Fund Income over Pula

Fund Dividend

(360 536) 360 536 – To cover residual deficit

8 936 740 – 11 962 333 Balance at December 31, 2004

34

BANK OF BOTSWANA ANNUAL REPORT 2004

ACCOUNTING POLICIES

December 31, 2004

BASIS OF PRESENTATION OF FINANCIAL STATEMENTS

The financial statements are prepared on the historical cost basis as modified to include the revaluation of

investments in domestic and foreign assets, liabilities, and the result of the activities of the Pula Fund. The

financial statements comply with International Financial Reporting Standards.

CHANGES IN ACCOUNTING POLICIES

In terms of International Accounting Standard No. 39 ‘Financial Instruments: Recognition and Measurement’,

investments held at year end are required to be valued at bid market prices and liabilities held, at offer/ask

market prices. In accordance with this standard, resultant market values were translated using the bid rates of

exchange, for assets held, and the offer/ask exchange rates for liabilities held. Up until December 31, 2003, all

investments and liabilities were valued at middle market prices, and the resultant market values were translated

to Pula using the middle rates of exchange at the balance sheet date, as required in terms of International

Accounting Standard No. 21 ‘Effects of Changes in Foreign Exchange Rates’. The effect on the Currency

Revaluation Reserve, the Market Revaluation Reserve and the Government Investment Account as at December

31, 2003 as a result of the changes in accounting policies referred to above is as follows:

The cumulative impact of the changes in accounting policies on the income statement as at December 31, 2003

of P413 000 was adjusted during the current year.

The bid rates of exchange for the Pula/United States dollar and the Pula/SDR as at December 31, 2003 were

0.2254 and 0.1538, respectively.

P’000

Currency Revaluation Reserve:

Increase in Pula Fund unrealised currency losses (10 652)

Increase in International Monetary Fund (IMF) reserves

unrealised currency losses (1 239)

(11 891)

Transfer to Government Investment Account 3 916

Net decrease at December 31, 2003 (7 975)

Market Revaluation Reserve:

Decrease in unrealised market gains (40 109)

Transfer to Government Investment Account 11 442

Net decrease at December 31, 2003 (28 667)

Government Investment Account:

Transfer to Currency Revaluation Reserve (3 916)

Transfer to Market Revaluation Reserve (11 442)

Decrease at December 31, 2003 (15 358)

35

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

ACCOUNTING POLICIES (continued)

FINANCIAL INSTRUMENTS

General

Financial instruments carried on the balance sheet include all assets and liabilities, including derivative

instruments, but exclude property and equipment, and notes and coin in circulation.

Short-term Investments (Liquidity Portfolio)

The Bank has designated the Liquidity Portfolio as a fund in which money market instruments and bonds are

invested to facilitate payments for regular transactions.

Securities invested in this portfolio are initially recognised at cost and are subsequently remeasured at market

value based on bid prices. All related realised and unrealised gains and losses are taken to the income statement.

All purchases and sales of investment securities in the portfolio are recognised at trade date, which is the date

the Bank commits to purchase or sell the investments. All other purchases and sales are recognised as derivative

forward transactions until settlement.

Long-term Investments (Pula Fund)

This is a long-term fund intended to maximise returns and is invested in foreign financial instruments with a

long-term duration. These investments, which may be sold in response to needs for liquidity, changes in interest

rates, exchange rates, etc. are classified as available-for-sale. These securities are initially recognised at cost

(which includes transaction costs) and are subsequently remeasured at market value, based on bid prices.

Unrealised gains and losses arising from changes in the market value of the instruments classified as available-

for-sale are recognised in the Currency Revaluation Reserve or the Market Revaluation Reserve as may be

appropriate. When these instruments are disposed of or impaired, the related accumulated market value

adjustments are included in the income statement as gains and losses from investment securities.

All purchases and sales of investment securities in the fund are recognised at trade date, which is the date that

the Bank commits to purchase or sell the investments. All other purchases and sales are recognised as derivative

forward transactions until settlement.

Derivative Instruments

Derivative financial instruments are recognised in the balance sheet at cost (including transaction costs) and are

subsequently remeasured at market value, based on bid prices for assets held or liabilities to be issued, and ask/

offer prices for assets to be acquired or liabilities held. The treatment of market value movements in derivative

instruments depends on whether they are designated as part of the Pula Fund or the Liquidity Portfolio.

FOREIGN CURRENCY ACTIVITIES

During the year ended December 31, 2004, transactions denominated in foreign currencies were translated to

Pula using the middle rates of exchange at the transaction date. With effect from December 31, 2004, transactions

denominated in foreign currencies will be translated using bid and offer rates of exchange, as described in the

Changes in Accounting Policies note above.

36

BANK OF BOTSWANA ANNUAL REPORT 2004

All monetary assets and liabilities denominated in foreign currencies are translated to Pula using the bid and

offer rates of exchange, respectively, at the close of the financial year. All exchange gains/losses realised on

disposal of instruments and unrealised exchange gains/losses on the short-term investments are taken to the

income statement. However, all those gains and losses relating to disposals whose proceeds are reinvested in

foreign assets, and unrealised gains/losses on short-term investments, are appropriated to the Currency

Revaluation Reserve.

BANK OF BOTSWANA CERTIFICATES

As one of its tools for maintaining monetary stability in the economy, the Bank of Botswana issues its own

paper, Bank of Botswana Certificates (BoBCs), to absorb excess liquidity in the market and thereby to influence

the rate of monetary growth, and also interest rates. BoBCs are issued at a discount to counterparties.

The Bank’s liability in respect of BoBCs is stated at market value, based on offer prices, with movements in

matured and unmatured discount recognised in the income statement.

GOVERNMENT OF BOTSWANA BONDS

The Bank acquired Government of Botswana Bonds for purposes of facilitating orderly trading in the local

bond market. The bonds, which may be sold in response to needs to intervene in the market, are classified as

available-for-sale securities.

The bonds are initially recognised at cost and are subsequently remeasured at market value, based on bid prices.

All unrealised gains and losses arising from changes in the market value are recognised in the Market Revaluation

Reserve. When these instruments are disposed of or impaired, the related accumulated market value adjustments

are included in the income statement as gains and losses from Government of Botswana Bonds.

All regular purchases and sales of bonds are recognised at trade date, which is the date that the Bank commits

itself to purchase or sell the bonds.

SECURED LENDING FACILITY

Under the Secured Lending Facility (SLF), the Bank provides emergency and intermittent funding to solvent

financial institutions, intended to bridge overnight liquidity shortages. The advances are secured by Government

of Botswana Bonds and Bank of Botswana Certificates (BoBCs), valued at market prices on the date of the

transaction. The Bank has the right to call for additional collateral, should the value of the security decline

during the tenure of the facility. Interest earned on the advances is credited to the income statement while

advances outstanding as at the balance sheet date are recorded under the heading ‘Advances to Banks’.

REPURCHASE AND REVERSE REPURCHASE AGREEMENTS

This facility is one of the mechanisms designed to deal with short-term liquidity fluctuations in the domestic

money market. It is available to solvent institutions licensed and supervised by the Bank.

Securities purchased under agreement to resell (Repurchase Agreement) are recorded as funds receivable under

the heading ‘Advances to Banks’.

ACCOUNTING POLICIES (continued)

37

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

Only high quality, marketable and freely transferable paper with a minimum amount of risk is acceptable as

security at the discretion of the Bank. Government and Government guaranteed securities of any maturity and

other eligible paper with a remaining life of 184 days or less are also acceptable as security.

Securities sold under agreement to repurchase (Reverse Repurchase Agreement) are disclosed as deposits

received.

The term of the repurchase agreement and reverse repurchase agreement varies from overnight to one month,

depending on the liquidity conditions in the domestic market.

Interest earned by the Bank on repurchase agreements is credited to the income statement while interest paid by

the Bank on reverse repurchase agreements is charged to the income statement.

ASSETS, LIABILITIES AND PROVISIONS RECOGNITION

Assets

Assets are recognised when the Bank obtains control of a resource as a result of past events, and from which

future economic benefits are expected to flow to the Bank.

Contingent Assets

The Bank discloses a contingent asset arising from past events where, it is highly likely that economic benefits

will flow from it, but this will only be confirmed by the occurrence or non-occurrence of one or more uncertain

future events outside the control of the Bank.

Liabilities and Provisions

The Bank recognises liabilities (including provisions) when:

(i) it has a present legal obligation resulting from past events;

(ii) it is probable that an outflow of resources embodying economic benefits will be required to settle this

obligation; and

(iii) a reliable estimate of the amount of the obligation can be made.

Derecognition of Assets and Liabilities

The Bank derecognises a financial asset when it loses control over the contractual rights that comprise the asset

and transfers substantially all the risks and benefits associated with the asset. This arises when the rights are

realised, expire or are surrendered. A financial liability is derecognised when it is legally discharged.

INCOME AND EXPENSE RECOGNITION

Interest income and expense and dividend income are recognised in the income statement on an accrual basis.

ACCOUNTING POLICIES (continued)

38

BANK OF BOTSWANA ANNUAL REPORT 2004

OFFSETTING FINANCIAL INSTRUMENTS

The Bank offsets financial assets and liabilities and reports the net balance in the balance sheet where:

(i) there is a legally enforceable right to set off;

(ii) there is an intention to settle on a net basis or to realise the asset and settle the liability simultaneously;

(iii) the maturity date for the financial assets and liability is the same; and

(iv) the financial asset and liability is denominated in the same currency.

In view of the fact that the Bank values its foreign exchange investments on a portfolio basis, assets and

liabilities within each portfolio have been set off.

GENERAL RESERVE

Under Section 7(1) of the Bank of Botswana Act, (CAP 55:01), the Bank of Botswana is required to establish

and maintain a General Reserve sufficient to ensure the sustainability of future operations of the Bank. The

Bank may transfer to the General Reserve funds from other reserves, which it maintains, for the purposes of

maintaining the required level of the General Reserve.

CURRENCY REVALUATION RESERVE

Any changes in the valuation, in terms of Pula, of the Bank’s assets and liabilities in holdings of Special

Drawing Rights and foreign currencies as a result of any change in the values of exchange rates of Special

Drawing Rights or foreign currencies are transferred to the Currency Revaluation Reserve.

The proportion directly attributable to the Government Investment Account is transferred to such investment

account.

MARKET REVALUATION RESERVE

Any changes in the value of the Bank’s long-term investments held in foreign currencies as a result of any

change in the market values of such investments are transferred to the Market Revaluation Reserve.

The proportion directly attributable to the Government Investment Account is transferred to such investment

account.

PROPERTY AND EQUIPMENT AND DEPRECIATION

Property and equipment are stated at cost less related accumulated depreciation.

No depreciation is provided on land. All other property and equipment are depreciated on a straight line basis

at the following annual rates:-

Percent

Buildings 2.50

Furniture, fixtures and equipment 20–50

Computer hardware 33.33

Computer software 100.00

Motor vehicles – Commercial 25.00

– Bullion Truck 5.00

ACCOUNTING POLICIES (continued)

39

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

RETIREMENT BENEFITS

Pension benefits are provided for employees through the Bank of Botswana Defined Contribution Staff Pension

Fund, which is governed in terms of the Pension and Provident Funds Act (CAP 27:03). Contributions are at

the rate of 21.5 percent of pensionable emoluments of which pensionable employees of the Bank pay 4 percent.

Other than the contributions made, the Bank has no further commitments or obligations to this Fund.

FINANCE LEASES

The Bank classifies leases of land, property and equipment where it assumes substantially all the benefits and

risks of ownership as finance leases. Finance leases are capitalised at the estimated net present value of the

underlying lease payments. The Bank allocates each lease payment between the liability and finance charges to

achieve a constant periodic rate of interest on the finance balances outstanding for each period. The interest

element of the finance charges is charged to the income statement over the lease period. The land, property and

equipment acquired under finance leases are depreciated over the useful lives of the assets, on the basis consistent

with similar property and equipment.

ACCOUNTING POLICIES (continued)

40

BANK OF BOTSWANA ANNUAL REPORT 2004

NOTES TO THE ANNUAL FINANCIAL STATEMENTS

December 31, 2004

1. PROPERTY AND EQUIPMENT Free-

hold

Land

Lease-

hold

Land Buildings

Capital

Works in

Progress

Other

Assets Total

P’000 P’000 P’000 P’000 P’000 P’000

Cost or Valuation

Balance at the beginning of the year 607 3 486 129 556 1 347 64 873 199 869

Additions – – – 5 499 10 608 16 107

Disposals – – (1 128) – (7 249) (8 377)

Transfers – – 261 (261) – –

Balance at the end of the year 607 3 486 128 689 6 585 68 232 207 599

Accumulated Depreciation

Balance at the beginning of the year – – 27 789 – 45 435 73 224

Charge for the year – – 3 231 – 8 373 11 604

Disposals – – (331) – (7 142) (7 473)

Balance at the end of the year – – 30 689 – 46 666 77 355

Net book value at December 31, 2004 607 3 486 98 000 6 585 21 566 130 244

Net book value at December 31, 2003 607 3 486 101 767 1 347 19 438 126 645

2. FOREIGN EXCHANGE RESERVES 2004 2003

P’000 P’000

2.1 Liquidity Portfolio

Bonds 2 059 241 1 166 785

Amounts due from Pula Fund 417 235 782 254

Net Payables – (720)

Cash and Cash Equivalents 1 250 876 1 962 189

3 727 352 3 910 508

2.2 Pula Fund

Equities 8 445 392 8 356 889

Bonds 11 068 919 10 008 682

Amounts due to Liquidity Portfolio (417 235) (782 254)

Net Payables (70 566) (42 466)

Cash and Cash Equivalents 986 703 1 704 999

20 013 213 19 245 850

41

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)

Pula Fund Balance Sheet 2004 2003

P’000 P’000

Capital Employed

Government 8 892 951 9 506 781Bank of Botswana 11 120 262 9 739 069

20 013 213 19 245 850

Employment of Capital

Investments 20 013 213 19 245 850

Investments expressed in US dollars (‘000) 4 681 091 4 332 241

Investments expressed in SDR (‘000) 3 060 020 2 956 163

Pula Fund Income Statement

Income

Interest and dividends 665 291 685 904Realised market gains 446 027 –Sundry income 19 49

1 111 337 685 953

Expenses

Realised currency revaluation losses (356 836) (1 177 036)Net realised market losses – (11 878)Administration charges (60 211) (53 668)

(417 047) (1 242 582)

Net Income/(Loss) for the year 694 290 (556 629)

Transfer from Currency Revaluation Reserve 356 836 1 177 036

Net income before transfer from Government InvestmentAccount 1 051 126 620 407

Transfer from Government Investment Account 94 210 494 888

Net income available for distribution 1 145 336 1 115 295

Appropriations

Dividend to Government (388 100) (755 000)

Bank of Botswana’s share of net income 757 236 360 295

42

BANK OF BOTSWANA ANNUAL REPORT 2004

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)

2004 2003

P’000 P’000

3. INTERNATIONAL MONETARY FUND (IMF)

3.1 Reserve Tranche

This asset represents the difference between Botswana’sQuota in the IMF and IMF Holdings of Pula. Botswana’sQuota is its membership subscription, of which at least 25percent was paid for in foreign currencies and the balancein Pula. The holdings of Pula by the IMF, which initiallywere equal to 75 percent of the quota, have changed fromtime to time as a result of the use of Pula by the IMF in itslendings to member countries.

Quota (SDR 63 000 000) 412 034 410 156Less IMF Holdings of Pula (277 950) (212 783)

Reserve Position in IMF 134 084 197 373

The IMF Holdings of Pula are represented by a Non-Interest Bearing Note of P165 324 035 (2003 – P165 324035) issued by the Government of Botswana in favour ofthe IMF, maintenance of value currency adjustments andthe amount in current account held at the Bank (includedin other deposits in Note 9).

3.2 Holdings of Special Drawing Rights 226 327 219 210

The balance on the account represents the value ofSpecial Drawing Rights allocated and purchased lessutilisation to date.

3.3 Allocation of Special Drawing Rights (IMF)

This is the liability of the Bank to the IMF in respect ofthe allocation of SDRs to Botswana. 28 584 28 379

3.4 Administered Funds

(i) Poverty Reduction & Growth Facility (PRGF) Trust – 45 275

The amount representing the equivalent ofSDR6 893 680 (and interest accrued thereon) lent onJuly 1, 1993 to the Poverty Reduction & GrowthFacility (formerly Enhanced Structural AdjustmentFacility Trust), a fund administered in trust by theIMF, which was repaid in March 2004.

(ii) Poverty Reduction & Growth Facility/Heavily IndebtedPoor Countries (PRGF/HIPC) Trust 99 219 98 756

The amount represents SDR 15 065 760 (and interestaccrued thereon) lent on August 31, 2002, to thePoverty Reduction & Growth Facility/HeavilyIndebted Poor Countries Trust Fund, a fundadministered in trust by the IMF.

99 219 144 031

43

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)

2004 2003

P’000 P’000

4. GOVERNMENT OF BOTSWANA BONDS

(i) Purchased on May 26, 2003, maturing on June 1,

2005, bearing interest at the rate of 10.75 percent,

receivable semi-annually in arrears:

Market value 19 935 20 125

Interest accrued 179 179

20 114 20 304

(ii) Purchased on March 31, 2003, maturing on March 1,

2008, bearing interest at the rate of 10.25 percent,

receivable semi-annually in arrears:

Market value 85 166 88 471

Interest accrued 2 949 2 948

88 115 91 419

108 229 111 723

5. ADVANCES TO BANKS

Secured Lending Facility 11 900 –

6. OTHER ASSETS

Staff Loans and Advances 37 743 30 022

Uncleared Effects – 16 496

Prepayments 1 059 2 244

Other 3 711 5 221

42 513 53 983

7. NOTES AND COIN IN CIRCULATION

Notes 854 062 766 382

Coin 56 796 51 613

910 858 817 995

Notes and coin in circulation held by the Bank as cash in

hand at the end of the financial year have been netted off

against the liability for notes and coin in circulation t o

reflect the net liability to the public.

8. BANK OF BOTSWANA CERTIFICATES

Face Value 9 755 220 8 870 460

Unmatured Discount (105 948) (131 114)

Market Value 9 649 272 8 739 346

Bank of Botswana Certificates are issued at various short-

term maturity dates and discount rates.

44

BANK OF BOTSWANA ANNUAL REPORT 2004

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)

2004

P’000

2003

P’000

9. DEPOSITS

Government 481 230 848 503Bankers 350 977 520 347Other 852 348 230 926

1 684 555 1 599 776

These represent current accounts lodged by Government,commercial banks, parastatal bodies and others, which arerepayable on demand and are interest free.

The Government balance includes P2 043 479 (2003 –P2 139 258) in respect of the Letlole National SavingsCertificate Scheme, which was launched by the Bank onbehalf of the Government in 1999 as a means ofencouraging savings.

This is analysed as follows:

Issues of National Savings Certificates 5 551 4 769Redemptions (3 517) (2 623)

Net issues 2 034 2 146Amounts awaiting collection from/ (by) agents 9 (7)

Amount due to Government on behalf of the Scheme 2 043 2 139

10. LIABILITIES TO GOVERNMENT (IMF RESERVE

TRANCHE) 134 084 197 373

This balance represents the Bank’s liability to theGovernment in respect of the Reserve Tranche positionin the IMF (Note 3.1)

11. DIVIDEND TO GOVERNMENT

Balance due at the beginning of the year 188 750 257 225Dividend to Government from Pula Fund 388 100 755 000Paid during the year (479 825) (823 475)

Balance due at the end of the year 97 025 188 750

The final instalment of the pre-set dividend ofP97 025 000 unpaid at December 31, 2004 was providedfor in accordance with Section 6 of the Bank of BotswanaAct (CAP 55:01), which requires that all profits of theBank be distributed to the shareholder, the Government.

12. OTHER LIABILITIES

Accounts payable 1 076 1 875Other creditors and accruals 25 294 24 899

26 370 26 774

45

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)

2004

P’000

2003

P’000

13. CAPITAL

Authorised and paid-up capital 25 000 25 000

The paid-up capital is the amount subscribed by theGovernment in accordance with Section 5 of the Bank ofBotswana Act (CAP 55:01).

14. GENERAL RESERVE 1 600 000 1 600 000

In the opinion of the Board, the General Reserve, takentogether with other reserves which the Bank maintains, issufficient to ensure the sustainability of future operationsof the Bank.

15. CURRENCY REVALUATION (LOSSES)/GAINS

TAKEN TO INCOME STATEMENT

Total realised losses (341 837) (1 778 989)Unrealised gains – Liquidity Portfolio 6 872 9 758

Total taken to income statement (334 965) (1 769 231)

Appropriated to Currency Revaluation Reserve:

Realised and reinvested in foreign assets 344 937 1 776 466Unrealised – Liquidity Portfolio (6 872) (9 758)

338 065 1 766 708

Net credited/(charged) to income statement 3 100 (2 523)

16. INTEREST EXPENSE

Bank of Botswana Certificates (BoBCs) 1 123 103 1 182 199Debswana Tax Holding Account 38 703 39 161Reverse Repurchase Agreements 12 359 15 624National Savings Certificates 220 189

1 174 385 1 237 173

17. CASH FLOW STATEMENT

This has been prepared under International AccountingStandard No. 7 – Cash Flow Statements (Revised 1992).The definition of cash in the Standard is not whollyappropriate to the Bank. Due to its role in the creationand withdrawal of currency in circulation, the Bank has nocash balances on its balance sheet (also see Note 7).However, it has the ability to create cash when needed.

46

BANK OF BOTSWANA ANNUAL REPORT 2004

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)

2004 2003

P’000 P’000

18. CASH GENERATED BY OPERATIONS

Net loss for the year (404 711) (2 257 928)Adjustments for:

Unrealised exchange losses 338 065 1 766 708Depreciation of property and equipment 11 604 11 391Loss on disposal of property and equipment 500 15

Operating cash flows before movements in working capital (54 542) (479 814)

Increase in Deposits – banks and other 452 052 174 735(Decrease)/Increase in Deposits – Government (367 273) 244 277Increase in Bank of Botswana Certificates 909 926 1 075 889(Increase)/Decrease in other assets (497) 1 720(Decrease)/Increase in other liabilities (67 821) 46 735

Cash generated by operations 871 845 1 063 542

19. CAPITAL COMMITMENTS

Approved and contracted for 6 451 1 609Approved but not contracted for 31 958 38 631

38 409 40 240

These capital commitments will be funded from internalresources.

20. GOVERNMENT OF BOTSWANA BOND AGENCY

In accordance with Sections 45 and 46 of the Bank of Botswana Act (CAP 55:01), the Bank acts asagent of the Government for the issuance and management of the Government Bonds. Ananalysis of the three bonds issued is provided below:

GOVERNMENT OF BOTSWANA BONDS ISSUED AS AT DECEMBER 31, 2004 (P’000)

Bond Detail BW 001 BW 002 BW 003

Date of Issue May 26, 2003 March 31 and

December 1, 2003

May 6 and

November 3, 2003

Total

Since Inception

Date of Maturity June 1, 2005 March 1, 2008 October 31, 2015

Interest Rate (per annum) 10.75 percent 10.25 percent 10.25 percent

Nominal Value 750 000 850 000 900 000 2 500 000

Net Discount (30 401) (21 029) (32 571) (84 001)

Net Proceeds 719 599 828 971 867 429 2 415 999

Interest Paid 120 938 112 750 117 875 351 563

Interest Accrued 6 719 29 042 15 375 51 136

Net proceeds realised from the issue of the bonds were invested in the Government InvestmentAccount.

47

PART A: STATUTORY REPORT ON THE OPERATIONS AND FINANCIAL STATEMENTS OF THE BANK, 2004

Interest is payable on all bonds on a semi-annual basis in arrears. Total cumulative interest payments of

P351 563 000 made to December 31, 2004 (2003 – P91 563 000) were funded from the Government’s

current account maintained with the Bank.

21. COMPARATIVES

Where necessary, comparative figures have been restated to conform with changes in presentation in the

current year. The adjustments required as a result of the changes in accounting policies are reflected in

the Statement of Accounting Policies and the Statement of Changes in Shareholder’s Funds.

22. RISK MANAGEMENT POLICIES IN RESPECT OF FINANCIAL INSTRUMENTS

The risk management policies of the Bank regarding financial instruments are dealt with in regular

reviews of the Bank’s reserve management policies. The main risk areas are market, currency, credit

and interest rates. The Bank invests in investment grade currencies (AA/Aa2) and above. Interest rate

risk is managed by using modified duration, while credit risk is controlled by dealing with the best

quality institutions or counterparties, as determined by international rating agencies.

23. RELATED PARTY TRANSACTIONS

The Bank provides several services to its shareholder, the Government, and to other Government-owned

institutions. The main services during the year to December 31, 2004 were:

(i) provision of banking services, including holding of the principal accounts of the Government;

(ii) management of the Notes and Coin issue, including printing and minting of notes and coin,

respectively; and

(iii) being the Government’s agent in issuing of bonds.

The aggregate balances in Government and other public sector accounts are disclosed in Notes 9 to 11.

No charge is made to the Government for provision of these services, except for commissions charged on