Anatomy of a Shale Boom - University of Western … of a Shale Boom The Case of the Eagle Ford Shale...

30

Anatomy of a Shale Boom The Case of the Eagle Ford Shale Mark Agerton Rice University, Center for Energy Studies [email protected] 16th Feb 2016 5th Asian IAEE Conference Perth, Western Australia

Transcript of Anatomy of a Shale Boom - University of Western … of a Shale Boom The Case of the Eagle Ford Shale...

Anatomy of a Shale BoomThe Case of the Eagle Ford Shale

Mark Agerton

Rice University, Center for Energy [email protected] Feb 20165th Asian IAEE ConferencePerth, Western Australia

Enablers of US shale are unique

I Private ownership of mineral rights

I Low barriers to entry

I Robust services sector

Agerton (Rice Univ) Introduction 2 / 30

Private ownership of mineral rights

I Aligns interests of landowners & firms– Rents go directly to landowners– Decreases political resistance

I Purchasing leases requires– Costly searching– Many bilateral negotiations

I Versus ownership by crown

Agerton (Rice Univ) Introduction 3 / 30

Low barriers to entry in US shale

I Entire onshore upstream value chain is extremely competitive

I Common services purchased from third-party firms

I Smaller capex (not mega-projects)

Agerton (Rice Univ) Introduction 4 / 30

Why worry about dynamics?

I Papers on leasing ignore general equilibrium and dynamics:Brown, Fitzgerald, and Weber (2015), Brown et al. (2016), Ganglmair andShcherbakova (2016), Timmins and Vissing (2014), Vissing (2015), and Vissing andTimmins (2015)

I Need to understand agents’ outside options to predict negotiated prices

I Landowner’s outside option is waiting for the next firm

I This is a non-stationary, dynamic problem (fewer acres each period)

Agerton (Rice Univ) Introduction 5 / 30

Research question

I How does leasing-market evolve over time, accounting for– Equilibrium interactions of firms & landowners– Depletability of leases and resources– Forward looking agents

I How are rents distributed between E&P firms and landowners?

Agerton (Rice Univ) Introduction 6 / 30

What the model tells us

I When is it best to be a landowner or a firm?

I How well do landowners monetize their assets?

I Implications for taxing authorities?

Agerton (Rice Univ) Introduction 7 / 30

Eagle Ford Shale (≈ 33k km2)

Oil

Wet Gas

Dry Gas

Agerton (Rice Univ) Eagle Ford context 8 / 30

Competitive leasing market

Acreage share Firms

5–6.5% 22–4.99% 91–1.99% 13<1% 1365

Agerton (Rice Univ) Eagle Ford context 9 / 30

Leasing is rapid

0%

25%

50%

75%

100%

2000 2005 2010 2015

Sur

face

are

a le

ased

Oil

Wet Gas

Dry Gas

Agerton (Rice Univ) Eagle Ford context 10 / 30

Most surface area is leased

Agerton (Rice Univ) Eagle Ford context 11 / 30

Leasing precedes drilling

Oil Wet Gas Dry Gas

0

200

400

0

50

100

150

200

Leases (sq km)

Wells

'00 '05 '10 '15 '00 '05 '10 '15 '00 '05 '10 '15

Agerton (Rice Univ) Eagle Ford context 12 / 30

Key ideas in model

I Lease value derived from depletable resource

I Forward-looking agents

I Depletability =⇒ nonstationary world

I Decentralized lease-market– Costly random search– Many leases per firm– Bargaining

Agerton (Rice Univ) Model 13 / 30

Key assumptions

I Continuous time, complete information

I Finite and homogenous land

I Competitive firms

I And firms are “big” while landowners are “small”– Match arrival is random for landowners– But deterministic for firms– Use Acemoglu and Hawkins (2014) labor-search model

Agerton (Rice Univ) Model 14 / 30

Land and landowners

Total acres︷︸︸︷A =

Never sell (hold-outs)︷︸︸︷AN +

Sellers︷︸︸︷AS

Unleased acresu = A−A

can’t go below AN sou ∈ [AN ,A]

Probability match is with seller (vs non-seller)

σ ≡ u−AN

u

Agerton (Rice Univ) Model 15 / 30

Matching

Aggregate searching by firms

v =mass of firms︷︸︸︷

n ×looking for v acres︷︸︸︷

v

Aggregate matching functionM(u, v) = m uµ v1−µ

Market tightness, match-rates for firms and landowners

θ ≡ v

uq(θ) ≡ M(u, v)

vθq(θ) = M(u, v)

u

Individual firms’ acreage acquisitions:

A = v × σ × q(θ)

Agerton (Rice Univ) Model 16 / 30

Nash Bargaining determines acreage price

Define

ψa : Marginal value of acresV u : Value of being unmatched

Acreage price

pa = arg maxpa

[pa − V u]τ [ψa − pa]1−τ

= τψa + (1− τ)V u

Match surplusS ≡ max {ψa − V u, 0}

Agerton (Rice Univ) Model 17 / 30

Landowner dynamics

Equation of motion for landowners’ value of being unmatched

V u =share of surplus︷ ︸︸ ︷−τS ×

match rate︷ ︸︸ ︷θq(θ) +

continuation︷︸︸︷ρV u

Agerton (Rice Univ) Model 18 / 30

Firm’s problem

Pick searching (v) and drilling (h) activity to

maxv,h

∫ T

0e−ρt

{ph− c(h)− κ(v)− paA

}dτ

subject to

A ≥ H Lease before drillA = vσq(θ) Lease-ratesH = h Drillingv ≥ 0 No resale of acresh ≥ 0 Irreversible drilling

Agerton (Rice Univ) Model 19 / 30

Equilibrium

Unique equilibrium given transversality conditions

A = ϕσβ (u/n)1−β Sβ

p = c′(H) + (−ψh)ψa = ρψa

ψh = ρψh

V u = (−τS)ϕσβ(S

u/n

)β+ ρV u

Where

ϕ = m1+β(

1−τκ

)ββ = 1− µ

1 + µ

Agerton (Rice Univ) Model 20 / 30

Cumulative drilling & leasing

0 5 10 15 20 250

20

40

60

A

H

Agerton (Rice Univ) Preliminary simulations 21 / 30

Equilibrium-searching

0 5 10 15 20 250

0.5

1

1.5

2

v

<

3

Agerton (Rice Univ) Preliminary simulations 22 / 30

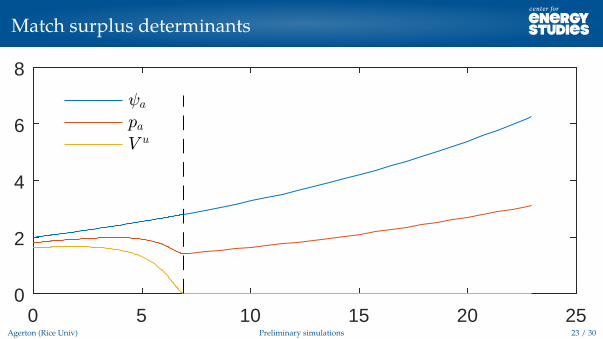

Match surplus determinants

0 5 10 15 20 250

2

4

6

8

Aa

pa

V u

Agerton (Rice Univ) Preliminary simulations 23 / 30

Real lease prices decline

0 5 10 15 20 250

0.5

1

1.5

2

e!;tAa

e!;tpa

e!;tV u

Agerton (Rice Univ) Preliminary simulations 24 / 30

Firm cash flow

0 5 10 15 20 250

10

20

30

Revenue

Extraction

Land

Search

Agerton (Rice Univ) Preliminary simulations 25 / 30

Model predictions

I Search frictions and landowners’ outside options play a meaningful role in limitingrate of leasing

I Landowners always get τ or higher share of Hotelling rents

I Landowners’ share (acreage price) decreases over time

I Scarcity only limits rate of price decrease... scarcity 6=⇒ price increase

I Leases are allocated optimally

Agerton (Rice Univ) Conclusion 26 / 30

Future directions for research

I Compare leasing allocation mechanisms in terms of1 ) Ability to match data2 ) Efficiency

I Modifications– Heterogeneity in firms’ productivity and landowners’ disutility of drilling– Principal–agent contracts– Directed search

Agerton (Rice Univ) Conclusion 27 / 30

References I

Acemoglu, Daron and William B Hawkins (2014). “Search with multi-worker firms”. In: TheoreticalEconomics 9.3.https://www.econtheory.org/ojs/index.php/te/article/viewFile/1061/11605/343,pp. 583–628.Brown, Jason P, Timothy Ryan Fitzgerald, and Jeremy Glenn Weber (2015). “Capturing rents fromnatural resource abundance: Private royalties from us onshore oil & gas production”. In: FederalReserve Bank of Kansas City Working Paper 15-04.Brown, Jason P et al. (2016). Regional Windfalls or Beverly Hillbillies? Local and Absentee Ownership ofOil and Gas Royalties. Working paper.Ganglmair, Bernhard and Anastasia Shcherbakova (2016). Information Spillovers in ContractNegotiations: Evidence from Oil and Gas Leases. The University of Texas at Dallas.Timmins, Christopher and Ashley Vissing (2014). Shale Gas Leases: Is bargaining efficient and what arethe implications for homeowners if it is not? Duke University.Vissing, Ashley (2015). One-to-Many Matching with Complementary Preferences: An Empirical Study ofNatural Gas Lease Quality and Market Power. Duke University.

Agerton (Rice Univ) References 29 / 30

References II

Vissing, Ashley and Christopher Timmins (2015). “Private Contracts as Regulation: A Study ofPrivate Lease Negotiations Using the Texas Natural Gas Industry”. In: Agricultural and ResourceEconomics Review 44.2, pp. 120–137.

Agerton (Rice Univ) References 30 / 30