Analyzing Transactions

40

Analyzing Transactions By Rachelle Agatha, CPA, MBA Slides by Rachelle Agatha, CPA, with excerpts from Warren, Reeve, Duchac

-

Upload

risa-caldwell -

Category

Documents

-

view

32 -

download

0

description

Analyzing Transactions. By Rachelle Agatha, CPA, MBA. Slides by Rachelle Agatha, CPA, with excerpts from Warren, Reeve, Duchac. 0. After studying this chapter, you should be able to:. - PowerPoint PPT Presentation

Transcript of Analyzing Transactions

Analyzing Transactions

By Rachelle Agatha, CPA, MBA

Slides by Rachelle Agatha, CPA, with excerpts from Warren, Reeve, Duchac

1. Describe the characteristics of an account and record transactions using a chart of accounts and journal.

2. Describe and illustrate the posting of journal entries to accounts.

3. Prepare an unadjusted trial balance and explain how it can be used to discover errors.

4. Discover and correct errors in recording transactions.

After studying this chapter, you should be able to:

Describe the characteristics of an account and record transactions using a

chart of accounts and journal.

Objective 1

Accounting systems are designed to show the

increases and decreases in each

financial statement line item as a separate

record. This record is called an account.

"T" Accounts

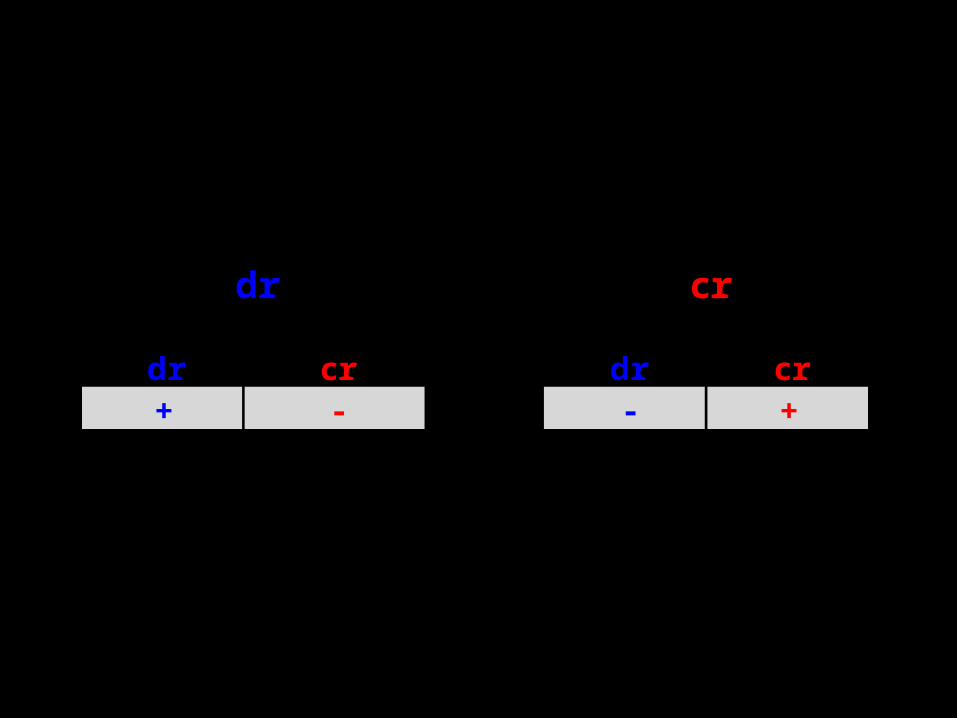

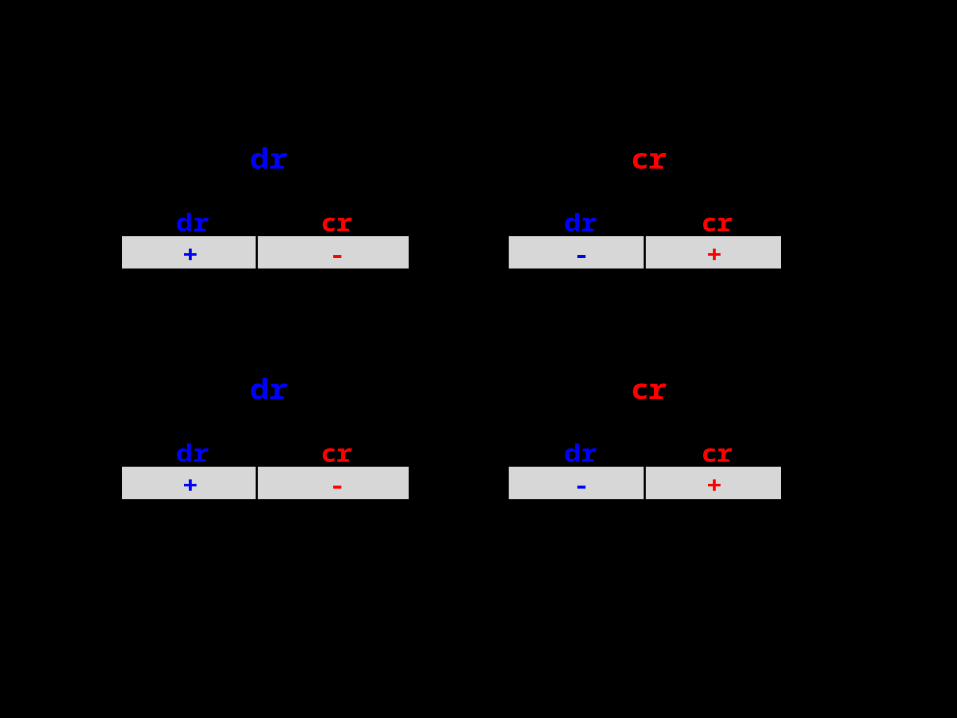

= +dr cr dr cr dr cr+ - - + - +

TermsNormal Balance dr cr dr crDebit - + + -Credit

dr cr+ -

drDRAWING

ASSETdr cr

LIABILITYcr

EQUITY

crREVENUE

drEXPENSE

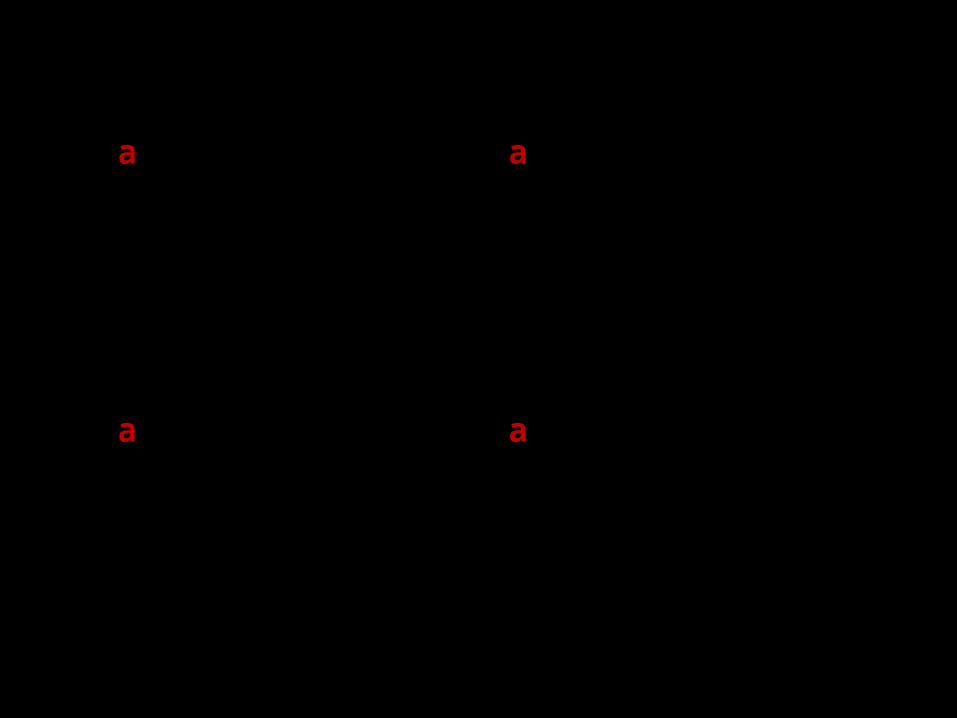

dr cr a 500 b 300+ - c 300

500$ 300$

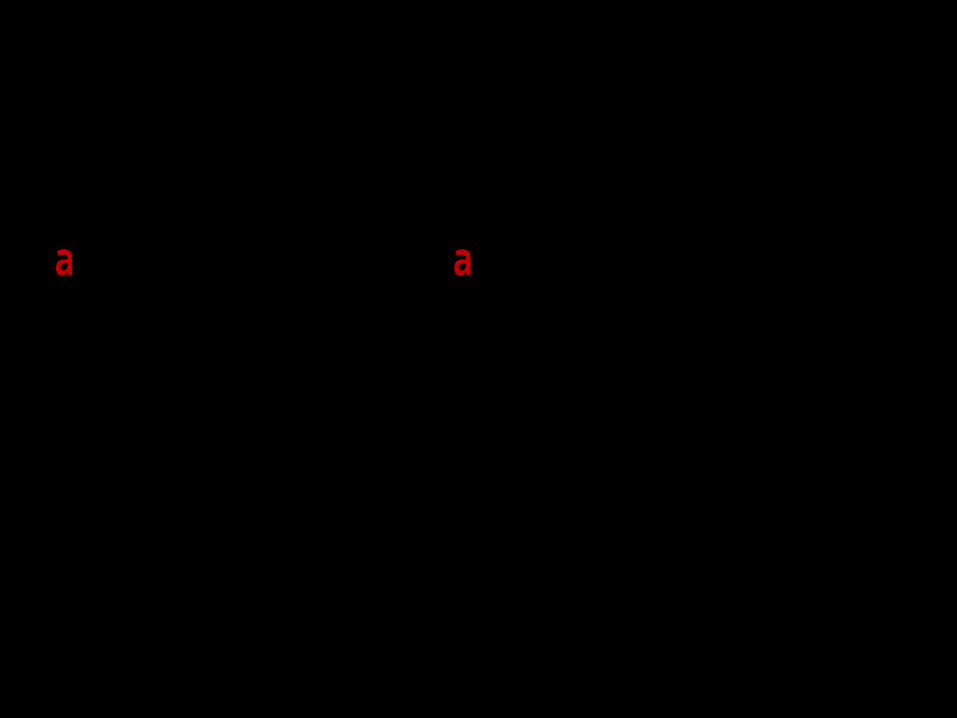

dr cr b 300- + c 300

-$

dr cr a 500- +

500$

SUPPLIES

crEQUITY SMITH, CAPITAL

LIABILITY

CASH

crA/P

drASSET

LEDGER - A group of accounts for a business entity

2-1

CHART OF ACCOUNTS - A

list of the accounts in a

ledger.

2-1

Assets are resources owned by the business entity.

• Cash• Supplies• Prepaid expenses• Buildings

2-1

Liabilities are debts owed to outsiders (creditors).

• Accounts payable

• Notes payable• Wages payable

2-1

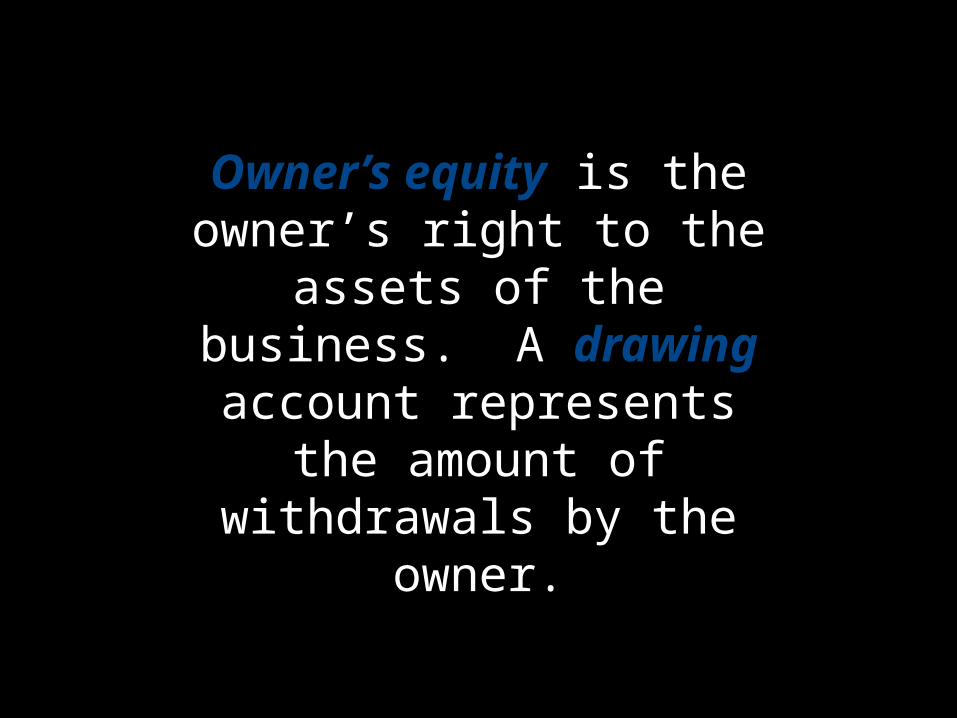

Owner’s equity is the owner’s right to the

assets of the business. A drawing account

represents the amount of withdrawals by the

owner.

2-1

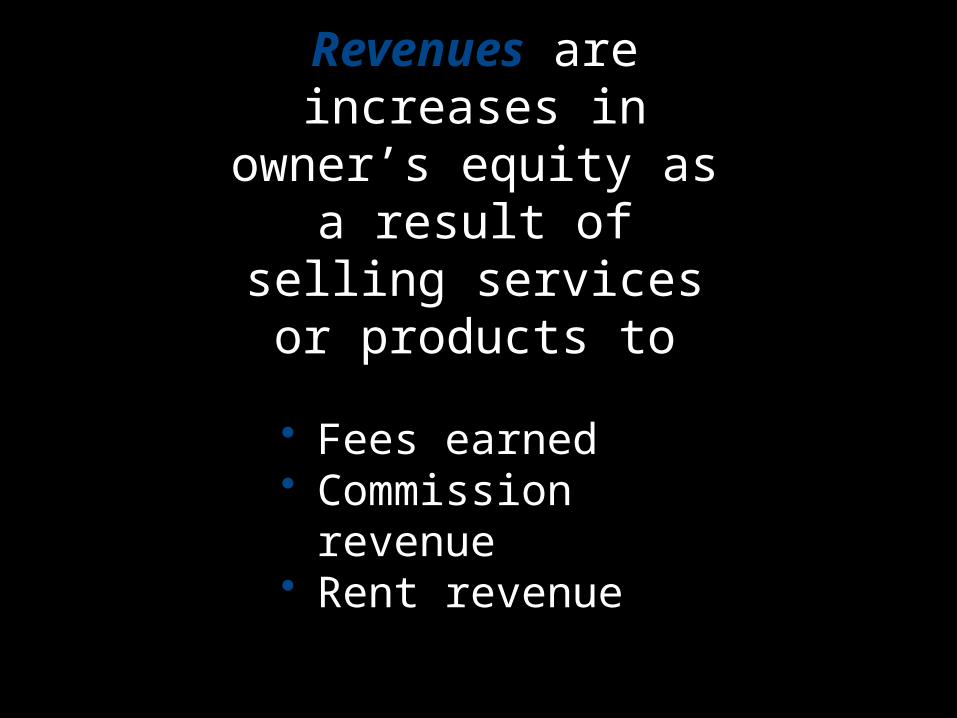

Revenues are increases in owner’s equity as a result of selling services or

products to customers.

• Fees earned• Commission

revenue• Rent revenue

2-1

The using up of assets or consuming services

in the process of generating revenues results in expenses.

• Wages expense• Rent expense• Miscellaneous

expense

2-1

Every transaction affects at least two

accounts.

2-1

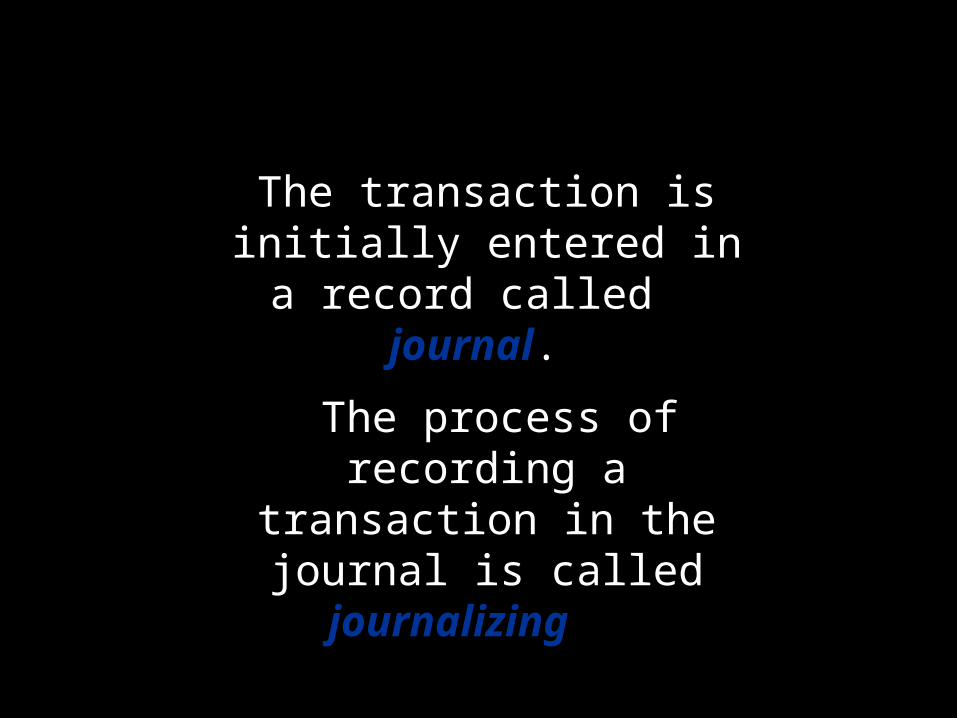

The transaction is initially entered in a record called

a journal.

The process of recording a transaction in the

journal is called journalizing.

2-1

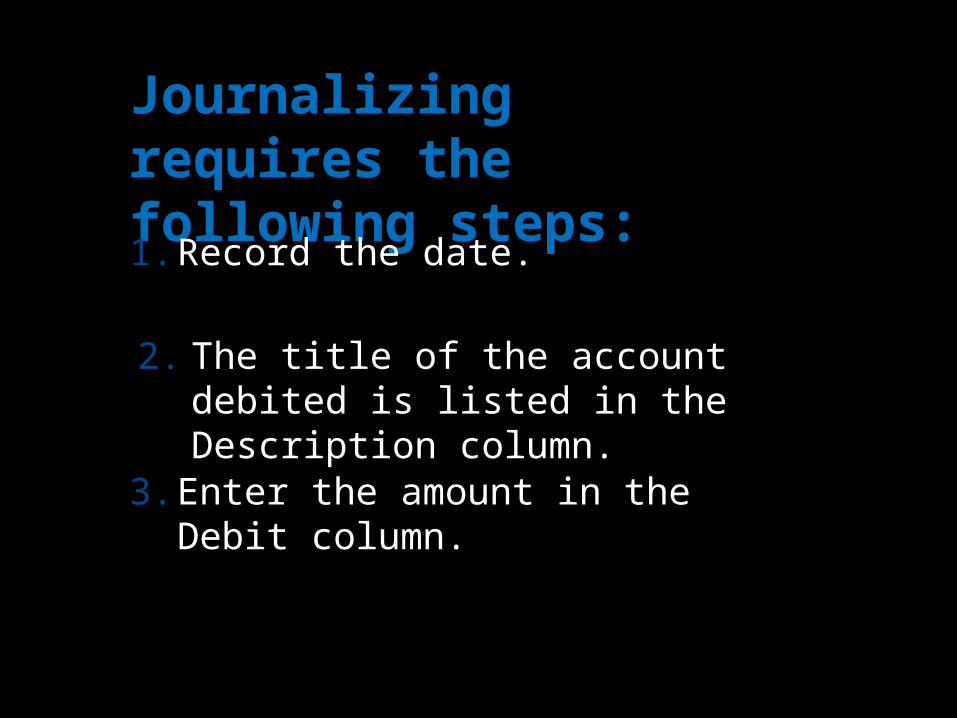

Journalizing requires the following steps:

1. Record the date.

(Continued)

2-1

2. The title of the account debited is listed in the Description column.

3. Enter the amount in the Debit column.

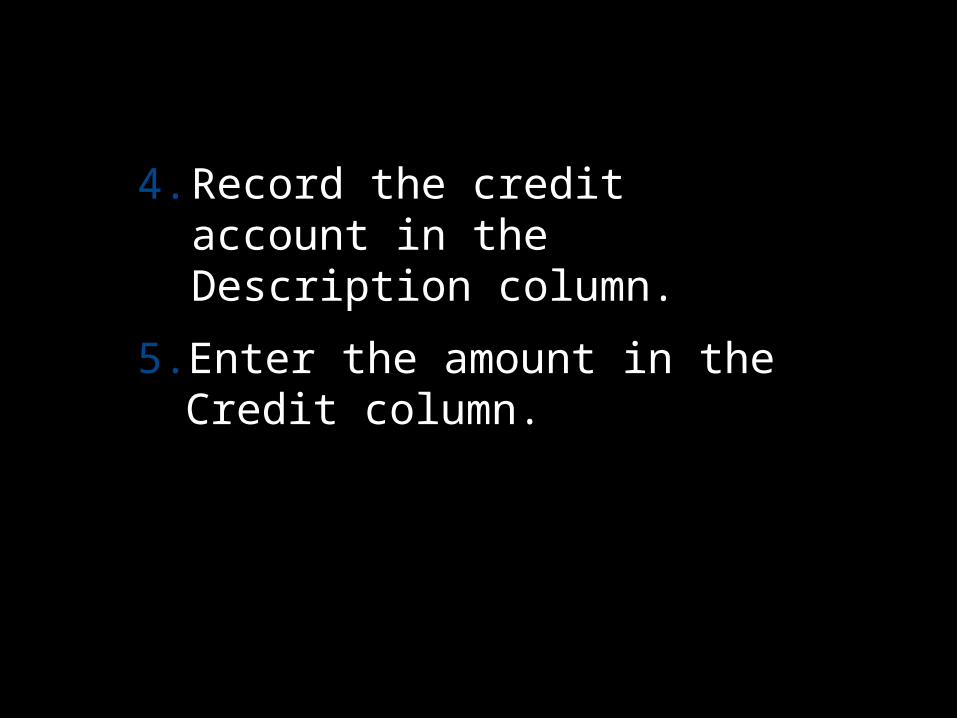

4. Record the credit account in the Description column.

5. Enter the amount in the Credit column.

2-1

2-1Page 1

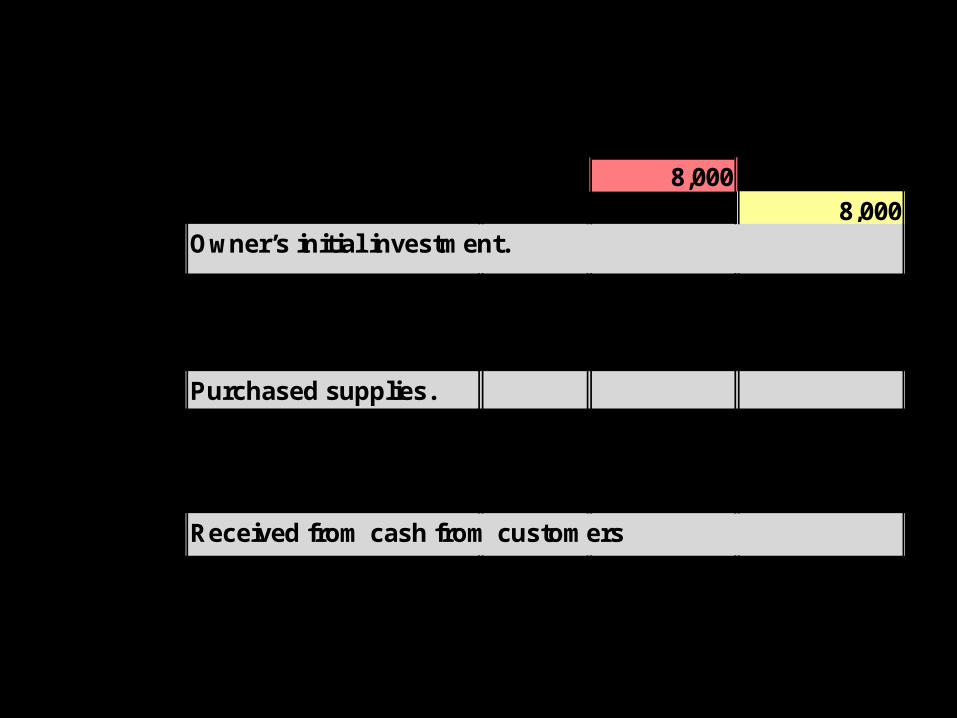

DATE DESCRIPTION DEBIT CREDIT

09/01/08 Cash 8,000 S. Morgan, Capital 8,000

09/15/08 Supplies 200 Cash 200Purchased supplies.

09/21/08 Cash 500 Fees Earned 500

JOURNALPOST.RE

F.

Owner’s initial investment.

Received from cash from customers

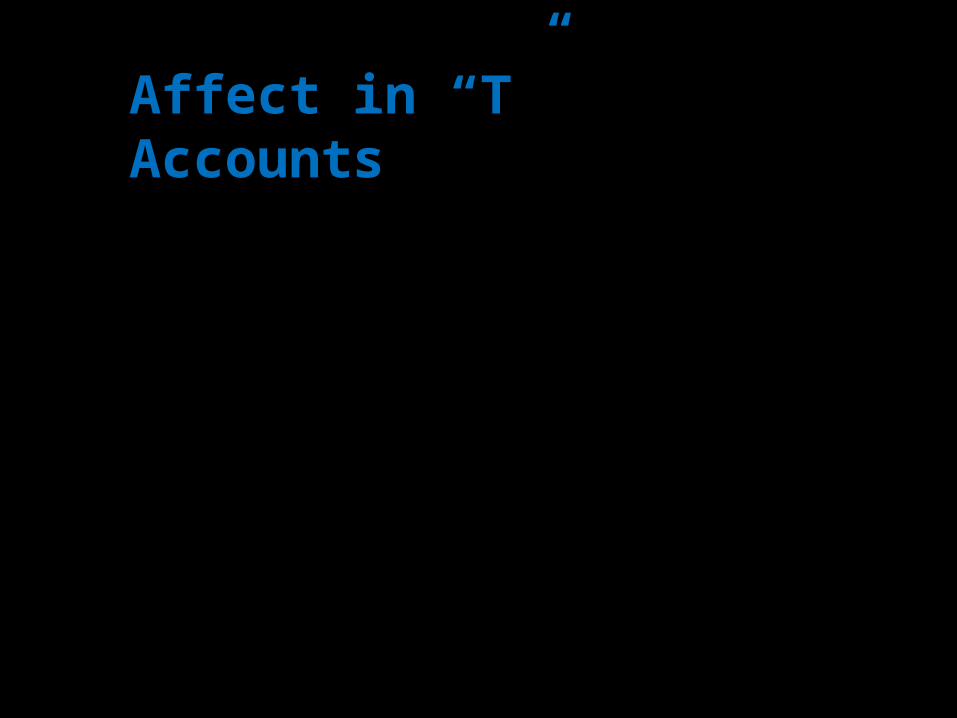

2-1Affect in “T” Accounts

8,000 8,000

8,000$ 8,000$

CASH S. Morgan Capital

2-1

dr cr dr cr+ - - +

dr cr- +

BALANCE SHEET

crLIABILITY

crEQUITY

drASSET

2-1

dr cr dr cr+ - - +

INCOME STATEMENT

dr crEXPENSE REVENUE

2-1

dr cr dr cr+ - - +

dr cr dr cr+ - - +

crINVESTMENT

drEXPENSE

EQUITY / CAPITAL

dr crDRAWING REVENUE

Where Revenue > Expense .

Net Income 2-1

and Credits >Debits

Net Income Increases Owner’s Equity.

Where Revenue < Expense..

Net Loss (Deficit) 2-1

Credits < Debits

Net Loss Decreases Owner’s Equity.

2-1Page 1

DATE DESCRIPTION DEBIT CREDIT

09/25/08 Accounts Receivable 15,000 Fees Earned 15,000

POST.REF.

Fees Earned for services rendered

JOURNAL

2-1

a 15,000 a 15,000

15,000$ 15,000$

A/R FEES EARNED

2-1

Page 1

DATE DESCRIPTION DEBIT CREDIT

09/21/08 Wages Expense 2,500Utilities Expense 800Rent Expense 3,500 Cash 6,800

JOURNALPOST.RE

F.

Paid for expenses

a 2,500 a 800

2,500$ 800$

a 3,500 a 6,800

3,500$ 6,800$

RENT EXP

UTILITIES

CASH

WAGES EXP

Page 1

DATE DESCRIPTION DEBIT CREDIT

09/30/08 S.Morgan, Drawing 1,000 Cash 1,000

JOURNALPOST.REF

.

Withdrawl by Morgan

a 1,000 a 1,000

1,000$ 1,000$

MORGAN DRAWING CASH

Balance sheet accounts:Asset Debit CreditLiability Credit DebitOwner’s Equity:

Capital Credit DebitDrawing Debit Credit

Income statement accounts:Revenue Credit DebitExpense Debit Credit

Increase(Normal

Bal.)

Decrease

Describe and illustrate the

posting of journal entries to the

accounts.

Objective 2

2-2

POSTING is the process of transferring the debits and credits

from the journal entries to the accounts

2-2

2-2Page 1

DATE DESCRIPTION DEBIT CREDIT

09/01/08 Cash 8,000 S. Morgan, Capital 8,000

POST.

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

09/01/08 1 8,000

POST.

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

09/01/08 8,000

BALANCE

BALANCE

ACCOUNT S. Morgan, Capital ACCOUNT NO. 31

JOURNALPOST.REF

.

Owner’s initial investment.

ACCOUNT Cash ACCOUNT NO. 10

Prepare an unadjusted trial

balance and explain how it can

be used to discover errors.

2-3

Objective 3

TRIAL BALANCE is prepared to show the equality of debits and

credits in the ledger . It is prepared as of a date in

time.

2-3

2-2DEBIT CREDIT

Cash 12,000$ Supplies 1,300 Prepaid insurance 900 Inventory 16,000 Equipment 182,865 Acc. Depreciation 47,335 Accounts payable 15,000 Wages payable 4,500 Notes Payable 25,000 J . Terrier Capital, J anuary 1, 2008 75,000 J . Terrier Drawing 15,000 Fees Earned 153,750 Wages 20,775 Rent 48,000 Depreciation 10,800 Supplies 9,375 Utilities 1,065 Insurance 1,800 Miscellaneous 705

320,585$ 320,585$

San Diego Designer Puppy Store and CoutureAdjusted Trial Balance

December 31, 2008

Discover and correct errors in

recording transactions.

2-4

Objective 4

A transposition error occurs when the order of

the digits is changed mistakenly, such as writing

$542 as $452 or $524. (usually divisible by 9)

In a slide, the entire number is mistakenly

moved one or more spaces to the right or the left, such

as writing $542.00 as $54.20.

2-4

2-2

Posting errors occur when posting from the journal to the ledger. Such as taking $1,200 from journal and entering it as $1,120 in

Ledger.

![Chapter 02 Analyzing and Recording Transactions · Chapter 02 Analyzing and Recording Transactions True / False Questions [Question] 1. Accounting records are also referred to as](https://static.fdocuments.in/doc/165x107/5f442472b82a1f335b1be308/chapter-02-analyzing-and-recording-transactions-chapter-02-analyzing-and-recording.jpg)

![Chapter 02 Analyzing and Recording Transactions...Chapter 02 – Analyzing and Recording Transactions 2-1 Chapter 02 Analyzing and Recording Transactions True / False Questions [Question]](https://static.fdocuments.in/doc/165x107/5ea240e72b04b75f702106a5/chapter-02-analyzing-and-recording-transactions-chapter-02-a-analyzing-and.jpg)