Analytics, Big Data and The Cloud II Conference - Kiribatu Labs

19

Learn how insurers predict risk and how you can apply it to your predictive analytics project Pawel Brzeminski, Founder & CEO [email protected] May 15, 2013 Analytics, Big Data, and The Cloud II Edmonton

-

Upload

pawel-brzeminski -

Category

Technology

-

view

581 -

download

0

Transcript of Analytics, Big Data and The Cloud II Conference - Kiribatu Labs

Learn how insurers predict risk and how you can apply it to your predictive analytics project

Pawel Brzeminski, Founder & CEO [email protected]

May 15, 2013 Analytics, Big Data, and The Cloud II

Edmonton

The Company KIRIBATULABSDiscovering Knowledge Assets

Kiribatu is a predictive analytics company, founded in 2009 / 6 employees We serve the Canadian financial sector, predominantly Property & Casualty insurance

Predic1ve analy1cs, huh? KIRIBATULABSDiscovering Knowledge Assets

Goal-driven ANALYSIS of a large data set to PREDICT human behavior

If speed was important to you… KIRIBATULABSDiscovering Knowledge Assets

YOUR insurance premium is calculated by methods designed 40-50 years ago

VS.

Risk assessment in Insurance KIRIBATULABSDiscovering Knowledge Assets

A vast majority of Canadian insurers (May 2013) still use outdated premium rating formulas created in 1960-1970s Only a handful of Canadian insurance companies are sophisticated predictive analytics users Leaders are decimating their competition

Where to start? KIRIBATULABSDiscovering Knowledge Assets

Source: By Phil McElhinney from London (Jeremy Wariner) (http://creativecommons.org/licenses/by-sa/2.0)

How to identify an opportunity for a predictive analytics project?

Ques1ons to ask while star1ng KIRIBATULABSDiscovering Knowledge Assets

Data is already collected (or can be easily acquired) Transactional data, customer data, sensor-generated data, usage data, etc.

There is a clear objective to predict something Future price, failure rate, customer risk, customer profitability, customer retention, etc.

Well-defined functional settings are a great place to start We focused on a Risk Sharing Pool (RSP) problem optimization

Typically the SMEs (Subject Matter Experts) are making decisions based on their experience and “gut feeling” Senior underwriters in our case

Significant ROI is expected Investment in analytics can be small but usually it is not trivial

Example KIRIBATULABSDiscovering Knowledge Assets

Risk Sharing Pool is a construct used by Canadian insurers to optimize their risk assessment Insurers put their highest risks (primary driver and a vehicle) in the pool to avoid paying for the claims But they forfeit the premium

Insurers retain the risks they deem profitable on their book of business They can collect the premium and make a profit

Challenge KIRIBATULABSDiscovering Knowledge Assets

Can we effectively predict future claims on policies? The model would need to predict claims that will occur up to 12 months in advance

Introducing Underwri1ng Score KIRIBATULABSDiscovering Knowledge Assets

The predictive model generates an Underwriting (UW) Score The UW Score is a number between 1 to 1000

High UW Score = high profitability = low risk Low UW Score = low profitability = high risk

Highly accurate predictor of future claims on a policy UW Score will be used to assess which risks are placed in the pool and which risks are not placed in the pool

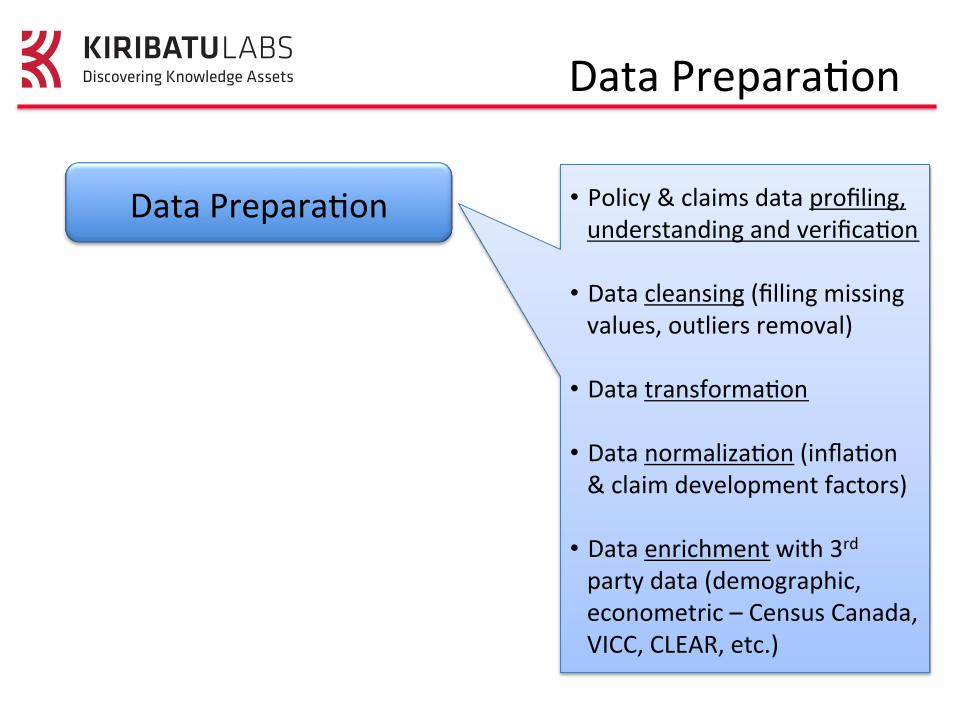

Data Prepara1on

Ra1ng Factor Analysis

Model Development

Gain Assessment

KIRIBATULABSDiscovering Knowledge Assets 4 Key Modeling Steps

Data Prepara1on • Policy & claims data profiling, understanding and verifica1on

• Data cleansing (filling missing values, outliers removal)

• Data transforma1on

• Data normaliza1on (infla1on & claim development factors)

• Data enrichment with 3rd party data (demographic, econometric – Census Canada, VICC, CLEAR, etc.)

Data Prepara1on KIRIBATULABSDiscovering Knowledge Assets

Ra1ng Factor Analysis KIRIBATULABSDiscovering Knowledge Assets

• Sta1s1cal analysis of each data element for its propensity to claim

• Ra1ng factors with high correla1ons are included in the final predic1ve model(s)

• OYen, new powerful ra1ng factors are discovered in this step (very useful for Underwri1ng)

Ra1ng Factor Analysis

Data Prepara1on

Model Development KIRIBATULABSDiscovering Knowledge Assets

• Algorithm selec1on (gene1c algorithms, neural networks, logis1c regression, SVM)

• Time-‐wise training and tes1ng data set split

• Model parameteriza1on, genera1on and evalua1on

Data Prepara1on

Ra1ng Factor Analysis

Model Development

• Calcula1on of UW Scores on test data set

• Retrospec1ve underwri1ng gain assessment on historical data sets

Data Prepara1on

Ra1ng Factor Analysis

Model Development

Gain Assessment

KIRIBATULABSDiscovering Knowledge Assets RSP Gain Assessment

Results KIRIBATULABSDiscovering Knowledge Assets

Source: “Improving P&C Insurance Risk Management and Policy Pricing with Predictive Analytics”, Pawel Brzeminski, September 2011, http://www.kiribatulabs.com/resources.php.

UW Score = 1000 – Risk Score

4 Key Challenges KIRIBATULABSDiscovering Knowledge Assets

Extremely low correlations / Data set imbalance 98% of policy transactions do not have any claims, 2% have claims

Bad, bad data Drivers driving 200,000 km per year (that's driving over 500 km per day for 365 days a year)

Over-fitting Certain features do not generalize very well in a time-wise data split

Data sparcity Motor Vehicle Abstract (MVA) data that contains convictions, suspensions and reinstatement is not always available

5 Key Breakthroughs KIRIBATULABSDiscovering Knowledge Assets

Policy transactions collapsed into single vectors Individual risk assessment for each vehicle on policy

Instance sampling and weighting Dealing with dataset imbalance and bad data

Custom model quality metric Aggregation of the highest claims in the top 5% of all transactions really moved the needle

Risk Assessment per insurance coverage Different data elements are important for each coverage, for instance liability coverage and comprehensive coverage are completely different products behave very differently

Prediction of Profitability Include written premiums in 2nd level model

Homework KIRIBATULABSDiscovering Knowledge Assets

Where can I apply predictive analytics in my business?

Questions? Always happy to have a coffee

Pawel Brzeminski, Founder & CEO [email protected]

780-232-2634

http://ca.linkedin.com/pub/pawel-brzeminski/0/523/555

@pawelwb