Analyst Presentation 4th Quarter 2014-15 - HDILhdil.in/.../Q4-Analyst-Presentation-F.Y.14-15.pdf ·...

30

Analyst Presentation 4 th Quarter 2014-15

Transcript of Analyst Presentation 4th Quarter 2014-15 - HDILhdil.in/.../Q4-Analyst-Presentation-F.Y.14-15.pdf ·...

Analyst Presentation 4th Quarter 2014-15

11111

• HDIL, promoted by Rakesh Kumar Wadhawan and Sarang Wadhawan

• Promoter Shareholding 36.16%

• FII & FPI Shareholding 49.02%

• Land Reserves of 243.99 Million Sq. Ft.

• Largest land bank owner in Mumbai Metropolitan Region

Company History

• HDIL Group has completed construction of 100 Mn. Sq. Ft. since inception in 1977

• More than 1.5 Lakhs homes delivered

• 23 Ongoing Projects

• 30.55 Million sq. ft. area under construction

• Possession handed in last 24 months of approx. 2500 residential units.

• Next 12-18 months we will hand over 4,500 residential units

Residential Portfolio

• Planet HDIL sale potential of 74 million sq. ft.

• Spread across 550 Acres

• India’s first smart city and affordable housing project

Future Plans - Iconic Project

Company Overview

as on March 31, 2015.

Project Mix

2

Residential

Commercial

Retail

•Ongoing Projects – 4,350,000•Planned Projects - 6,960,000

•Ongoing Projects – 264,456•Planned Projects - 16,727,821

•Ongoing Projects – 6,209,035 •Planned Projects - 47,175,000

•Ongoing Projects– 30,557,810•Planned Projects- 131,749,589

SRA

Ongoing Projects Segment wise Breakup & Saleable Area as on March 31, 2015.

Area in Million sq. ft

Residential Portfolio

3

BKC

Churchgate

Virar

Churc

hgate

to V

irar

(52 k

ms)

Bandra

to V

irar

(30 k

ms)

Suburb

an R

ail R

oute

Premier Exotica

Majestic Towers

Whispering Tower

Berkeley Square

Daulat Nagar

Residency Park

Planet HDIL

Meadows

Harmony

Ekta Nagar

Project Saleable Area (in Sq.ft.)

Metropolis 700,000

Residency Park - Phase II 600,000

Galaxy 175,000

Planet HDIL Phase I 15,882,810

Paradise City 5,000,000

Ekta Nagar 1,500,000

Majestic 1,300,000

Meadows - Phase I 1,000,000

Whispering Towers-Phase I 1,200,000

Whispering Towers-Phase II 800,000

Premier Exotica Phase II 800,000

Berkeley Square 900,000

Premier Exotica Phase I 700,000

30,557,810

Paradise City

Metropolis

Galaxy

as on March 31, 2015.

4

Project Update

Residency Park

5

March 31, 2015.December 31, 2014.

Possession commencing in Q1 FY 2015-16, Project fully sold

Metropolis

6

Possession commencing FY 2015-16, Project fully sold

Premier Exotica Phase I

7

March 31, 2015.December 31, 2014.

Premier Exotica Phase II

8

March 31, 2015.December 31, 2014.

Majestic Tower

9

Whispering Tower Phase I

10

Whispering Tower Phase II

11

Possession in next 12 months

Sr. No. Project Area (in sq. ft.) Sales Value (in Cr.)

1 Metropolis 7,00,000 560

2 Residency Park 6,00,000 210

3 Premier Exotica 7,00,000 630

4 Paradise City 50,00,000 1000

5 Galaxy 1,75,000 90

Total 71,75,000 2490

12

Sales to be recognized on project completion basis

TDR

Handing over 10,000 residential units

to Slum Rehabilitation Authority

7 Million Sq. Ft. TDR will be

generated in phase wise manner

2.5 Million Sq. Ft. TDR will be

generated in 1st phase for Sale

13Handed over 1700 Units to MCGM on April , 2015.

14

Iconic Project

Affordable Housing Project

‘Planet HDIL’ 550 Acre Township

Planet HDIL Location

Planet HDIL is proposed in Vasai-Virarbelt (Part of Thane district) Preferred residential destination, well connected with rail and road network

Mere 5Km away from Mumbai periphery

Thane is part of Mumbai Metropolitan Region and the fastest growing district in India.

Vasai-Virar is sanctioned as Satellite city by Govt. of India.

Project is well connected through road and railways

Project is adjoining to Proposed railway station “HDIL City” connected to Mumbai with 4 dedicated tracks.

1KM away from NH-8, connecting to Mumbai

BKC

Churchgate

Virar

Churc

hgate

to V

irar

(52 k

ms)

Bandra

to V

irar

(30

km

s)

Planet HDIL Suburb

an R

ail R

oute

India’s Largest Smart Affordable City

Bandra

Attached to proposed railway station “HDIL City”

1KM from NH-8, Connecting to Mumbai to Ahmedabad

Land Area: 550 Acres Non-Agricultural Land

Suburban Station 2KM Away

Planet HDIL- Regional Setting

HDIL Industrial Park, Home to 150 Industries

Proposed Freight Corridor connecting JNPT under DMIC.

Railway Track

Commitment towards

Environment Protection,

Education and Health

Care Facility

Plot Area-

2,48,76,761 Sq. Ft

Construction Area consisting Residential,

Commercial, Infrastructure-

5,49,71,909 Sq. Ft.

Saleable Area-

7,41,71,577 Sq. Ft.

Proposed Project Cost-

Rs. 11,000 Cr

Future Revenue Generated-

Rs 35,000-40,000 Cr

Residential Population Estimated-

3,36,050

Employment Generation Estimated-

35,000

Development will take place in 8-10 phases

Time Line-

10-12 Years

Open Green Space 15% of plot area

Economic Indicators of Project

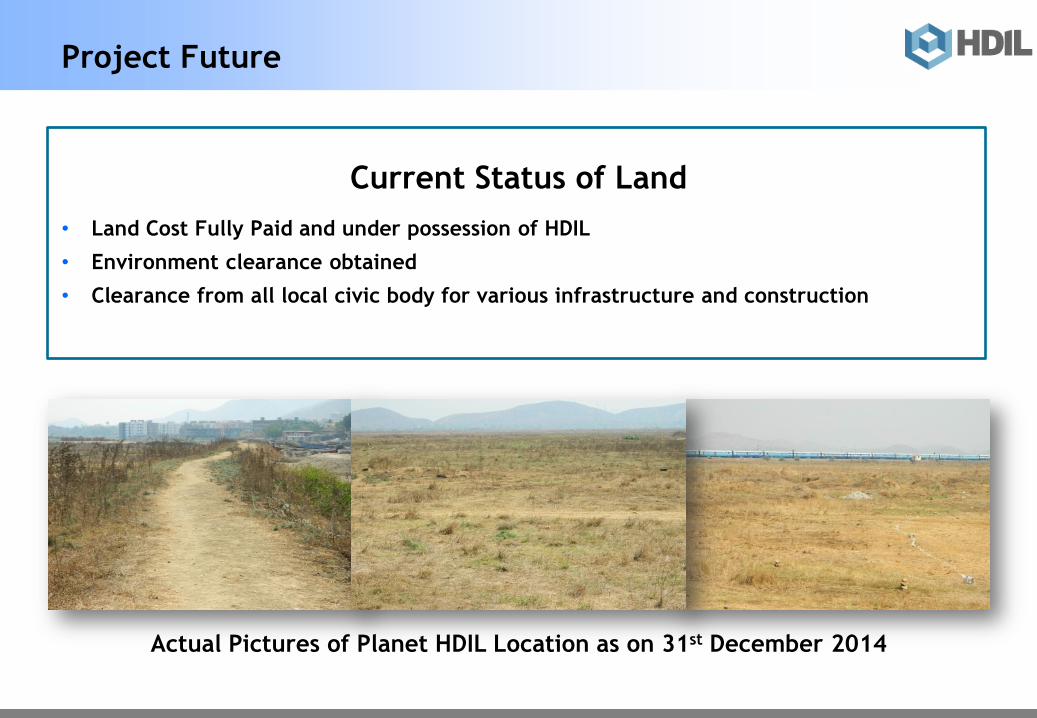

Project Future

Current Status of Land

• Land Cost Fully Paid and under possession of HDIL

• Environment clearance obtained

• Clearance from all local civic body for various infrastructure and construction

Actual Pictures of Planet HDIL Location as on 31st December 2014

Financials

20

Key Development: 4th Quarter 2014-15

• HDIL FY15 net profit at Rs. 218.65 crore, up 23.14%

• For the year FY15, consolidated turnover remains at Rs.

1083.12 crore representing an increase of 13.58%

• During the quarter, the company booked the turnover from

retail property Harmony located in Mumbai suburb Goregoan

• For the quarter ended March 2015, new residential sales

crossed Rs 400 crore, representing 100% growth on YoY basis

• Customer collection during the quarter stands at approx. Rs.

425 crore

• Consolidated EBITDA for the quarter ended on 31st March 2015

stands at 35.86% as against 27.25% in Q4FY14

• Consolidated Net debt for the year ended March 2015 remains

at Rs. 2942 crore, a decline of 10.41% as compare to Rs. 3284

in the previous year

• During the current quarter, the company has handed over

approx. 1700 apartments of SRA project located in Kurla to

the Government of Maharashtra

• Around 2 million sq. ft TDR generation is expected which will

boost operating cash flow in next 12-15 months

• TDR generated approx 0.2 million during current quarter21

Consolidated Debt Analysis

22

70% of debt has a floating cost, with decrease in interest rates the overall repayment also decrease

Gross Debt 3231.30

Lease Rental Discounting 75.00

Cash & cash equivalents 214.14

Net Debt 2942.16

All Figure in INR Crore.

•HDIL has reduced its debt by INR 793.71 Cr

from its peak level, an overall decline of

19.71% in last Six Quarters

•Net debt as on March 31, 2015 is INR

2942.16 Cr

•Lease rental discounting is on account of

rental income of approx 10 Cr every year.

•Cash and cash equivalents includes cash on

hand of Rs 189.14 Cr and balance in liquid

instruments

Consolidated Financial Ratios Y-o-Y

23

PAT

EPS Finance Cost

EBIDTA

All Figure in INR Crore.

Financial Ratio

24

Note:

* Company follows project completion method of accounting and hence quarter turnover cannot be compared

** Includes other income of 44 Cr, from sale of HDIL Leisures Private Limited Business in March 2014 Quarter

*** PAT for March 2014 include Rs. 35.63 Cr. On account of revision of income tax provision

Particulars

Consolidated Stand alone Consolidated

Quarter Ended Year Ended Year Ended

31-Mar-15 31-Dec-14 Growth % 31-Mar-15 31-Mar-14 Growth % 31-Mar-15 31-Mar-14 Growth % 31-Mar-15 31-Mar-14 Growth %

Turnover (Net) 156.45 350.83 -55.41% 156.45 208.92* -25.11% 1,005.25 770.79 30.42% 1,022.48 872.27 17.22%

Other Income 6.23 8.65 -27.98% 6.23 50.34** -87.62% 85.68 169.65 -49.50% 60.65 81.38 -25.47%

Total Income 162.68 359.48 -54.75% 162.68 259.26 -37.25% 1,090.93 940.44 16.00% 1,083.13 953.65 13.58%

PBT&E 45.94 86.71 -47.02% 45.94 79.38 -42.13% 307.53 255.52 20.35% 297.80 189.06 57.52%

PBT % to income 28.24% 24.12% 28.24% 30.62% 28.19% 27.17% 27.49% 19.82%

EBIDTA 58.34 98.31 -40.66% 58.34 129.07 -54.80% 372.76 365.63 1.95% 369.37 380.27 -2.87%

EBIDTA % to

income35.86% 27.35% 35.86% 49.78% 34.17% 38.88% 34.10% 39.88%

PAT 31.88 67.30 -52.63% 31.88 113.52*** -71.92% 226.33 244.85 -7.56% 218.65 177.57 23.14%

PAT % to income 19.60% 18.72% 19.60% 43.79% 20.75% 26.04% 20.19% 18.62%

Net worth 10,804.68 10,775.17 0.27% 10,804.68 10,775.17 0.27% 10,655.05 10,425.21 2.20% 10,804.68 10,559.05 2.33%

Debt 3,231.30 3,339.36 -3.24% 3,231.30 3,508.52 -7.90% 2,206.46 2,441.80 -9.64% 3,231.30 3,508.42 -7.90%

Debt Equity ratio 0.30 0.31 0.31 0.33 0.21 0.23 0.30 0.33

EPS -Basic 0.71 1.76 0.71 2.71 5.49 5.81 5.20 4.21

- Diluted 0.71 1.76 0.71 2.71 5.49 5.81 5.20 4.21

Inventories 13,078.97 12,903.10 1.36% 13,078.97 12,467.85 4.90% 10,905.36 10,596.54 2.91% 13,078.97 12,467.85 4.90%

All Figure in INR Crore.

Consolidated Balance Sheet

25

Particulars31st March, 2015 31st December, 2014 31st March, 2014

(Audited) (Unaudited) (Audited)

I. EQUITY AND LIABILITIES

(1) Shareholders' Funds

Share Capital 4,190,039,860 4,190,039,860 4,190,039,860

Reserves and Surplus 103,856,772,143 108,046,812,003 103,561,746,982 107,751,786,842 101,400,471,700 105,590,511,560

Share application money pending allotment - - -

(2) Minority Interest 73,672,691 73,553,176 73,821,394

(3) Non-Current Liabilities

Long-term borrowings 10,616,671,060 10,787,726,768 11,271,184,637

Deferred tax liabilities (Net) 189,358,704 185,741,639 189,309,365

Long term provisions 16,722,995 10,822,752,759 13,848,486 10,987,316,893 13,674,831 11,474,168,833

(4) Current Liabilities

Short-term borrowings 16,457,319,243 16,342,694,217 16,432,932,858

Trade payables 4,464,317,035 4,400,872,382 4,408,538,410

Other current liabilities 34,169,315,588 32,516,403,528 29,449,416,582

Short-term provisions 2,148,837,620 57,239,789,486 2,019,702,198 55,279,672,325 1,440,042,655 51,730,930,505

Total 176,183,026,939 174,092,329,236 168,869,432,292

II.ASSETS

(1) Non-current assets

Fixed assets

(i) Tangible assets 1,199,384,767 1,202,643,798 2,207,427,918

(ii) Intangible assets 926,732 1,076,436 9,915,961

(iii) Capital work-in-progress - 1,200,311,499 6,506,392 1,210,226,626 69,099,550 2,286,443,429

Goodwill on consolidation - 17,870,729 71,482,914

Non-current investments 1,596,503,096 1,047,188,813 500,725,787

Long term loans and advances 728,277,925 728,305,415 857,336,295

(2) Current assets

Current investments 79,485,202 79,485,202 147,148,414

Inventories 130,789,665,668 129,031,042,007 124,678,503,229

Trade receivables 3,041,733,047 3,534,044,202 3,813,955,394

Cash and bank balances 1,891,446,976 1,968,747,066 2,267,065,655

Short-term loans and advances 36,855,603,526 172,657,934,419 36,475,419,176 171,088,737,653 34,246,771,175 165,153,443,867

Total 176,183,026,939 174,092,329,236 168,869,432,292

P&L Consolidated

26

Particulars

Quarter ended

31st March, 2015

Quarter ended

31st December, 2014

Quarter ended

31st March, 2014

Year ended

31st March, 2015

Year ended

31st March, 2014

(Audited) (Unaudited) (Audited) (Audited) (Audited)

Revenue:

Revenue from operations 1,564,475,903 3,508,300,778 2,089,263,677 10,224,754,579 8,722,654,507

Other Income 62,327,977 86,476,297 503,462,577 606,466,288 813,786,514

Total Revenue 1,626,803,880 3,594,777,075 2,592,726,254 10,831,220,867 9,536,441,021

Expenses :

Cost of material consumed 1,957,973,012 2,184,961,161 1,597,436,320 7,748,110,835 6,141,119,666

Changes in inventories of finished goods, work in

progress and stock in trade (2,348,810,268) (1,103,632,972) (1,983,823,572) (6,705,520,873) (7,616,428,237)

Employee benefits expense 100,124,503 114,299,811 97,817,517 411,940,797 401,388,130

Finance costs 1,212,611,256 1,308,899,983 1,693,647,352 5,534,449,193 7,072,930,265

Depreciation and amortisation expense 46,888,905 30,852,516 199,193,422 153,194,532 785,746,516

Other expenses 198,637,213 192,252,625 194,622,345 711,063,390 861,052,817

Total Expenses 1,167,424,621 2,727,633,124 1,798,893,384 7,853,237,874 7,645,809,157

Profit before tax 459,379,259 867,143,951 793,832,870 2,977,982,992 1,890,631,864

Tax expense:

Current tax 136,830,917 197,052,144 (356,341,410) 791,696,257 90,571,887

Deferred tax 3,617,064 (2,774,380) 13,295,438 (71,158) 23,168,429

140,447,981 194,277,764 (343,045,972) 791,625,099 113,740,316

Profit after tax 318,931,278 672,866,187 1,136,878,842 2,186,357,893 1,776,891,548

Less : Minority Interest 119,518 (179,731) 1,712,845 (155,359) 1,240,883

Add : Share of profit of Associates - - 37,584 - -

Profit for the year 318,811,760 673,045,918 1,135,203,581 2,186,513,252 1,775,650,665

Earnings per equity share of ` 10/-

(1) Basic 0.71 1.76 2.71 5.20 4.21

(2) Diluted 0.71 1.76 2.71 5.20 4.21

Cash flow Consolidated

27

ParticularQuarter ended

31st March, 2015

(Audited)

Cash flow from operating activities

Net profit before tax 459,379,259

Adjustments for :

Depreciation and amortisation expense 46,888,905

Interest expenses 1,212,611,256

Interest received (37,665,510)

Dividend received -

Loss/(profit) on sale of investments -

Loss by fire -

Loss on sale of fixed assets - 1,221,834,651

Operating profit before working capital changes 1,681,213,910

Movements in working capital :

Decrease / (Increase) in inventory (1,758,623,661)

Decrease / (Increase) in trade receivable 492,311,155

Decrease / (Increase) in other receivables (380,156,860)

(Decrease) / Increase in trade and other payables2,743,901,867

Net movement in working capital 1,097,432,501

Cash generated from operations 2,778,646,411

Less : Direct taxes paid (net of refunds) 8,166,140

Net cash from operating activities 2,770,480,271

Cash flows from investing activities

(Increase) / Decrease in capital work in progress6,506,392

(Increase) / Decrease in investments (net) (596,692,998)

Interest received 37,665,510

Dividend received -

Purchase of fixed assets (383,577)

Consideration received on diposal of subsidiary-

Sale of fixed assets -

Net cash from investing activities (552,904,673)

Cash flows from financing activities

Proceeds from borrowings 436,070,907

Repayment of borrowings (1,516,701,589)

Expenses on increase in authorised share capital(1,633,750)

Interest paid (1,212,611,256)

Net cash used in financing activities (2,294,875,688)

Net increase in cash and cash equivalents (A + B + C) (77,300,090)

Cash and cash equivalents at the beginning of the year 1,968,747,066

Less : Delink of subsidiary -

Cash and cash equivalents at the end of the year 1,891,446,976

Components of cash and cash equivalents as at

Quarter ended

31st March, 2015

Cash on hand 47,521,420

With banks - on current account 229,336,761

- on escrow account 2,770,670

- on deposit account * 1,611,818,125

1,891,446,976

Disclaimer

28282828

This investor presentation has been prepared by Housing Development and Infrastructure Ltd (“HDIL”). and does notconstitute a prospectus or placement memorandum or an offer to acquire any securities. This presentation or any otherdocumentation or information (or any part thereof) delivered or supplied should not be deemed to constitute an offer.

No representation or warranty, express or implied is made as to, and no reliance should be placed on, the fairness,accuracy, completeness or correctness of such information or opinions contained herein. The information contained in thispresentation is only current as of its date. Certain statements made in this presentation may not be based on historicalinformation or facts and may be “forward looking statements”, including those relating to the general business plans andstrategy of HDIL, its future financial condition and growth prospects, future developments in its industry and itscompetitive and regulatory environment, and statements which contain words or phrases such as ‘will’, ‘expected to’,‘horizons of growth’, ‘strong growth prospects’, etc., or similar expressions or variations of such expressions. Theseforward-looking statements involve a number of risks, uncertainties and other factors that could cause actual results,opportunities and growth potential to differ materially from those suggested by the forward-looking statements. Theserisks and uncertainties include, but are not limited to risks with respect to its real estate business, SEZ business and itsinfrastructure business.

HDIL may alter, modify or otherwise change in any manner the content of this presentation, without obligation to notifyany person of such revision or changes. This presentation cannot be copied and disseminated in any manner.

No person is authorized to give any information or to make any representation not contained in and not consistent withthis presentation and, if given or made, such information or representation must not be relied upon as having beenauthorized by or on behalf of HDIL. This presentation is strictly confidential.

29

For further information please log on to http://www.hdil.in/ or contact:

Mr. Shriram TotalaTel: +91 (22) 67888000Email: [email protected]/[email protected]

Thank You