ANALYSIS OF THE VALUE ADDED TAX (VAT) 2014 BILL, · PDF file16/05/2014 · 1...

21

1 ANALYSIS OF THE VALUE ADDED TAX (VAT) 2014 BILL, TAX ADMINISTRATION BILL 2014 AND INVESTMENT POLICY 1997 SUBMITTED BY DR. HONEST PROSPER NGOWI & MR. SILAS OLAN’G TO ACTION AID TANZANIA (AATZ) FOR TAX JUSTICE NETWORK -TANZANIA OCTOBER 2014

Transcript of ANALYSIS OF THE VALUE ADDED TAX (VAT) 2014 BILL, · PDF file16/05/2014 · 1...

1

ANALYSIS OF THE VALUE ADDED TAX (VAT) 2014 BILL, TAX ADMINISTRATION BILL 2014 AND

INVESTMENT POLICY 1997

SUBMITTED BY

DR. HONEST PROSPER NGOWI

&

MR. SILAS OLAN’G

TO

ACTION AID TANZANIA (AATZ) FOR TAX JUSTICE NETWORK -TANZANIA

OCTOBER 2014

2

1. Introduction and Background

This is a report on the study that analyzed the Value Added Tax (VAT) Bill of 2014, Tax

Administration Bill of 2014 and The Investment Policy 1997. The fundamental purpose of taxation

is to raise revenue effectively, through measures that suit each country’s circumstances and

administrative capacity. In fulfilling the revenue function, a well-designed tax system should be

efficient in minimizing the distortionary impact on resource allocation, and equitable in its impact

on different groups in society (Ndikumana, 2002).

The study has its background from the observation that recent studies (for example Curtis, Ngowi

and Attiya – 20121; Policy Forum: 20122,) indicate that due to tax incentives and exemptions,

Tanzania is being deprived of the badly-needed financial resources needed for financing public

expenditure of goods and services both in the development and recurrent budget. Studies reveal

that tax incentives and exemptions are not the main factors for attracting and retaining Foreign

Direct Investments (FDIs). Other factors that attract and retain investments include but are not

limited to enabling and friendly investments and business environment including adequate

quantity and quality of infrastructure (roads, railways, ports, airports); utilities (adequate, stable

and cheap electricity and water); less bureaucracy and corruption; high quality workforce; large

market; natural resources availability and efficiency among other factors. See TPSF (2013, 2012)3

for details.

There have been various proposals to the government to cut down tax exemptions so as to earn

the supposedly income from these areas and fund different development projects. With this

recognition that tax exemptions and incentives entail a large revenue loss, the government in

response submitted two bills: Value Added Tax (VAT) and Tax Administration (TAA) bills to be read

for second time in the November 2014 Parliamentary session. There is a need to analyze whether

these bills will introduce clarity and reduce tax incentives and streamline tax administration as it

was stipulated in the 2014/15 Budget Speech by the Minister for Finance. The study that informs

1 One Billion Dollar Question: How Can Tanzania Stop Loosing So Much Revenue

2 Tax Incentives in East Africa: A Race to the Bottom?

3 Business Leaders’ Perceptions on Business Environment in Tanzania

3

this report aimed at analyzing the VAT Bill of 2014 and the Tax Administration Bill 2014 in the

context of Investments Policy 1997.

2. Study Objective

The objective of the study was to analyze the VAT Bill 2014, Tax Administration Bill 2014 and the

Invetsment Policy 1997 in order to:

2.1. Determine whether it will serve to reduce tax incentives

2.2. Bring clarity on the criteria used to grant tax incentives

2.3. Identify whether incentives will be granted in a transparent manner

2.4. Identify whether the Bill limits powers of the Minister to grant incentives

2.5. Assess whether domestic stakeholders’ views on how best can the government

reduce exemptions have been taken into account in the bill.

2.6. To identify main areas of strength and weaknesses (missing information/gaps) in the

Bill in the context of revenue loss

2.7. To examining model VAT and TAA bills and other good practices from EAC, SADC, any

Commonwealth Country

2.8. To give specific recommendations for the Bills in the context of the study

3. Methodology

The report is mainly based on secondary data/desk review. Different documents containing data

and information on tax exemptions and incentives in Tanzania were reviewed in the context of the

study. The VAT and TAA Bills 2014, were the main document reviewed.

4. Study Findings

4

4.1. VAT Bill

In what follows, the findings of the study are presented based on the stated objectives. The

specific findings are preceded by a brief description of the VAT Bill 2014.

4.1.1. A Brief Description of the VAT Bill 2014

The Value Added Tax (VAT) Bill 2014 is a Special Bill Supplement No. 3 of 12th May, 2014 . It was

gazzeted in the Gazette of the United Republic of Tanzania No. 20 Vol. 95 dated 16th May, 2014.

The bill contains eight (8) parts as detailed in appendix one of this report. It is a bill for an Act to

make elite legal framework for the imposition and collection of, administration and management

of the value added tax, to repeal the Value Added Tax Act, Cap. 147 and to provide for other

related matters.

4.1.2. Specific Study Findings

In what follows, the specific study findings based on the objective of the study are presented.

4.1.2.1. Possibility of the Bill to Reduce Tax Incentives

Introduction to Tax Incentives

Tax incentives are among investment incentives in general and for Foreign Direct Investments

(FDIs) in particular. They are the benefits offered by governments to investors so as to attract

investments and retain those already in a country. Tax incentives include tax reductions to attract

investors in a specific location or sectors. Such incentives include tax holydays, investment

allowances and tax credits, timing differences, general tax reductions and non-income tax –based

incentives.

5

Tax incentives in Tanzania are granted to various kinds of investors. These include those investing

in the Export Processing Zones (EPZs) and Special Economic Zones (SEZs) as well as those holding

Tanzania Investment Centre (TIC) certificate of incentives.

Issues around Tax Incentive

The granting of tax incentives is seen as ineffective and a loss of revenue for the Treasury and

expensive distortions that reduce the true value of output. At times the generosity question arises

from the school of thought that sees tax incentives to be too generous compared to benefits from

the same.

Tax Incentives in the Bill

The word ‘incentive’ does not appear in the Bill. Instead, tax exemption does. Tax exemption is

provided for in PART II of the Bill which is on imposition of value added tax as shown in what

follows.

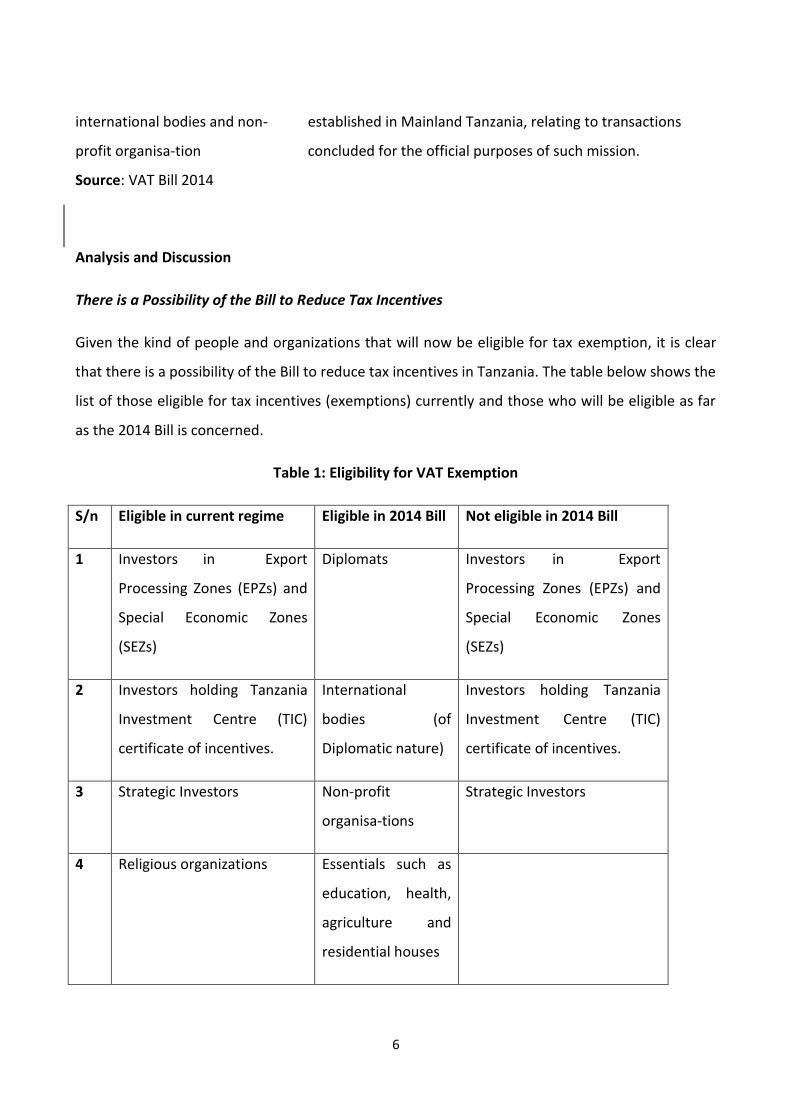

Box 1: (a) Imposition and Exemptions of VAT

Imposition of value added tax 3. Value added tax shall be imposed and payable on taxable

supplies or taxable imports.

Person liable to pay value added

tax

4. The following persons shall be liable to pay value added

tax-

(a) in the case of a taxable import, the importer;

(b) in the case of a taxable supply that is made in Mainland

Tanzania, the supplier; and

(c) in the case of a taxable supply of imported services, the

purchaser.

Exemptions and rates to be

specified by law

6.-(1) Except as otherwise provided under this Act-

(a) a supply, class of supplies, import, or class of import

shall not be exempt or zero-rated; and

(b) a person or class of persons shall not be exempted from

paying value added tax imposed under this Act.

Refund to diplomats, (c) a diplomatic or consular mission of a foreign country

6

international bodies and non-

profit organisa-tion

established in Mainland Tanzania, relating to transactions

concluded for the official purposes of such mission.

Source: VAT Bill 2014

Analysis and Discussion

There is a Possibility of the Bill to Reduce Tax Incentives

Given the kind of people and organizations that will now be eligible for tax exemption, it is clear

that there is a possibility of the Bill to reduce tax incentives in Tanzania. The table below shows the

list of those eligible for tax incentives (exemptions) currently and those who will be eligible as far

as the 2014 Bill is concerned.

Table 1: Eligibility for VAT Exemption

S/n Eligible in current regime Eligible in 2014 Bill Not eligible in 2014 Bill

1 Investors in Export

Processing Zones (EPZs) and

Special Economic Zones

(SEZs)

Diplomats Investors in Export

Processing Zones (EPZs) and

Special Economic Zones

(SEZs)

2 Investors holding Tanzania

Investment Centre (TIC)

certificate of incentives.

International

bodies (of

Diplomatic nature)

Investors holding Tanzania

Investment Centre (TIC)

certificate of incentives.

3 Strategic Investors Non-profit

organisa-tions

Strategic Investors

4 Religious organizations Essentials such as

education, health,

agriculture and

residential houses

7

5 A supply, class of supplies,

import, or class of imports

A person or class of persons

Importers of taxable imports

Supplier of taxable supplies in

Tanzania

Purchaser of imported

services

Source: Various including VAT Bill 2014

Discussion

From the table above it is seen that the number and categories of those eligible for tax exemption

in the old regime (the regime before the 2014 VAT Bill) are much more than those eligible under

the 2014 VAT Bill. According to the VAT Bill 2014, investors with TIC certificate of incentives,

investors in EPZs and SEZ as well as those with strategic investors’ status will no longer enjoy VAT

exemption. Therefore the Bill has reduced tax incentives.

4.1.3. Criteria To Be Used To Grant Tax Incentives in the Bill

Part II of the Bill (imposition of value added tax) outlines those eligible for tax exemptions as

shown above. Criteria used for a diplomatic or consular mission of a foreign country established in

Mainland Tanzania include , “transactions concluded for the official purposes of such mission”. For

such exemptions for essentials such as education, health and agriculture, there are no

coditions/criteria specified for granting such exemptions. This may pose as an avenue through

which revenues from VAT may be lost due to lack of specific criteria.

4.1.4. Transparency in Granting Incentives

The Bill is Silent of Transparency Measures

8

As stated above, the Bill outlines those who will be eligible for exemption. However, it does not

indicate how transparent the process and its outcomes will be. In the 2014/15 budget speech, the

Minister stated there would be high level of transparency in granting exemptions. Among the

transparency measures stated in the budget is public announcement (through the Ministry’s

website and newspaper for example) of all those enjoying exemptions on quarterly basis. The Bill

is silent on such transparency measures.

4.1.5. Limitation of the Powers of the Minister to Grant Incentives

The Bill Provides for the Limitation

The Bill, under “Objects and Reason” provides for among other things, limitation of the power of

the Minister to grant incentives. It states that “… the Bill seeks to do away with powers of the

Minister to grant exemptions on payment of value added tax”. This is in line with what was stated

by the Minister in the 2014/15 budget speech. Part II of the Bill, inter alia, “proposes to remove

powers of the Minister to grant tax exemption”.

4.1.6. Incorporation in the Bill of Domestic Stakeholders’ Views on Best Ways of Reducing

Exemptions

Generally, the Bill has incorporated most of domestic stakeholders’ views on reducing

exemption. Such views have included but not necessarily limited to reducing or removing

unproductive tax exemptions. This has been done as partly shown in table one above. It has

also incorporated the views against tax competition within the region that can lead to the race

to the bottom. It has also incorporated views of exempting VAT on essentials such as food,

education, agriculture and residential houses. It has also incorporated the views of reducing

the power of the Minister in granting exemptions.

However, it has not incorporated the views of making the exemption process and results

transparent by way of putting in the public space the names of those who have enjoyed

exemptions.

9

Box 2: Selected Recommendations From Curtis, Ngowi and Attiya (2002)4 on Tax Incentives

The government should address tax revenue losses with a sense of urgency and take greater

steps to increase revenue collections. Most importantly, it should:

• Undertake a review, to be made public, of all tax incentives with a view to reducing or

removing many of them. The aim should be to remove most of the incentives granted

to the mining sector and reduce or remove many of those granted in the EPZs. What tax

incentives remain should be linked to performance requirements for sectors, such as

employment creation and technology transfer.

• Provide annually, during the budget process, a publicly available tax expenditure analysis,

showing the cost to the government of the various tax incentives and the

beneficiaries.

4.1.7. Main areas of strength in the Bill in the Context of Increasing Revenue

Among the areas of strength in the Bill in the context of increasing revenue include limitation

of exemptions mainly to diplomatic missions, international organizations and essentials such as

food, health, education, agriculture and residential houses. Another strength in that context is

removal of VAT exemptions to investors who have been enjoying it so far. However it would be

more meaningful to use part of revenues gained from removing exemptions to improve other

business environment components. These include but are not limited to infrastructure, power

(electricity), corruption, skills levels etc.

4.1.8. Main areas of Weaknesses in the Bill in the Context of Revenue Loss

The Bill has some areas of weakness in the context of revenue loss. Among other things, it

provides for deferral payment of taxes as shown below.

Box 3: Deferral of value added tax on imported capital goods

11.-(1) A registered person may, in the form and manner prescribed, apply to the Commissioner

4 One Billion Dollar Question: How Can Tanzania Stop Loosing So Much Tax Revenue

10

General for approval to defer payment of value added tax on imported capital goods.

(2) The Commissioner General shall approve an application under this section if satisfied that-

(a) the person is carrying on an economic activity;

(b) the person makes taxable supplies;

(c) the person keeps proper records and files value added tax returns and complies with

obligations under other tax law;

(d) the person has provided a bank guarantee required under subsection (4); and

(e) there are no reasons to refuse the application in accordance with subsection (3)

(3) The Commissioner General shall refuse an application under this section if the applicant or a

person connected to the applicant:

(a) has an outstanding liability or an outstanding return under any tax law; or

(b) has been convicted in a court of law in the United Republic or elsewhere for an offence of

evading payment of tax, custom duty or an offence relating to violation of trade laws or

regulations.

Source: VAT Bill 2014

Discussion

It is seen in the content of the box above that there is no time period limitation for deferral

payment in the Bill. This may provide for a loophole of businesses deferring from paying taxes for

a long period of time thereby exposing such revenues to risks of being lost. It would add more

value and reduce possibilities of revenue loss if the Bill stipulated the length and number of times

VAT payment may be deferred.

4.1.9. Conclusions and Recommendations

The Bill is basically good in the context of increasing government revenues from VAT. It

proposes removal of the VAT exemptions hitherto granted to investors such as those with TIC

certificate of incentives, investors in EPZs and SEZ as well as strategic investors. It has proposes

the removal of the power of the Minister to grant exemptions and has incorporated some

11

views of stakeholders on reducing incentives/exemptions. However, the Bill is silent on a few

recommendations from the stakeholders as outlined in this paper. It also lacks provisions for

transparency in granting exemptions.

4.2 Tax Administration Bill 2014

4.2.1 A Brief Description of the Tax Administration Bill 2014

Any tax administration system aims to enhance tax revenue collection, improve service to tax

payer, reduce compliance burden, reduce administration cost, facilitate trade and investment and

improve integrity of the tax authority. It is however, worth noting that tax rates and terms are set

in the respective tax laws and not the Tax Administration law. The administration of tax laws,

however, may lower or increase cost of compliance (convenience) to tax payer or cost of

collection (efficiency) to the government.

Published in the Gazette of the United Republic of Tanzania No. 20 Vol. 95 dated 16th May, 2014,

Tax Administration Bill (2014) aims to creating modern, effective, fair and transparent tax

administration in Tanzania by simplifying, unifying, and harmonizing tax procedures from various

tax laws with a view to promoting voluntary tax compliance, fair tax governance and increasing tax

revenue .The harmonization and consolidations is anticipated to enhance TRA’s potential for

enhanced tax revenue collection. The bill also introduces currency point system to insulate the

value of tax revenue against inflationary effects (the time value).

If enacted, this will be the first single piece of legislation for the administration of various tax laws

that fall under the current remit of the Tanzania Revenue Authority (TRA). Currently, Tax

administration is performed under several provisions dispersed in 12 different tax laws (Table 1).

This complicates the administration, may add cost of compliance and confusion to the tax payers,

especially those whose operations are integrated and therefore fall under different tax law.

12

4.2.1 Specific Finding

4.2.1.1 Effect on Tax Revenue

Convenience of Payment and ease of collection

While it is difficult to predict the extent to which the bill is likely to guarantee increased tax

revenues as this will depend on the administrative capacity, by and large the bill contains

provisions that if effectively enforced; government revenue is likely to increase. These

include: options for method of payment -physical payment at any tax office, bank and mobile

phone (Section 56.-(1)). These measures are likely to minimize collection cost, lower

compliance cost for the tax payer, hence increased revenue contribution. However, the

convenience of the taxpayer is somehow eroded by the subsequent sub section (2) which

requires the tax payer to notify the tax office where the taxpayer is registered of the

payment. In the era of ICT revolution, a tax payer would expect the Tax authority to have this

information in the TRA information.

Tax Liability Assessment

Section 46.-(1) provides for self-assessment to determine primary liability file a tax returns.

Adoption of Self-Assessment is an acknowledgement of the universal reality that no single

tax administration that has or will ever have sufficient resources to determine the correct tax

liability of every tax payer. While this may be convenient to the tax payer, it may reward

dishonest tax payers, a phenomenon that is not unusual in Tanzania. Further, the bill seems

to suggest that self-assessment is applied universally (without targeting specific category of

tax payers). While this may be convenient to the tax payers, it may fail revenue generation

test. It would be useful for TRA to provide an assessment of efficacy of the Self-Assessment

system since its introduction in 2004. Under this system, the role of tax administration is to

assist tax payer to understand their rights and obligation as a basic principle of ensuring

voluntary compliance.

To complicate the matter, Section 46 (2), empowers no person other than the Commissioner

General to adjust any assessment. There two emerging concerns about this provision:

13

- This provision may create ambiguity in its implementation as it refers to the

Commissioner General as the only person with powers to adjust assessments thus, may

contradict the provisions of section 16.-(1) regarding the powers of the Commissioner

General to delegate.

- The section could be improved by inserting a subsection that provides for delegation of

such powers of the commissioner to a tax officer.

- It may contrast provisions of Section 48 (6) which apparently, empowers the Board or

Tribunal under the Tax Revenue Appeals Act to make adjustments. The section states

“The Commissioner General shall not adjust an assessment that has been adjusted or

reduced pursuant to a decision of the Board or Tribunal under the Tax Revenue Appeals

Act or an order of the court of competent jurisdiction.

Sanctions

The bill also contains fairly strong and comprehensive sanctions for non-compliance (Section

75- 92), if enforced in a cost effective way should minimize defaults hence, positive effect on

revenue revenues on one hand. However, on the other hand, it may be very costly to pursue

these sanctions which may undermine the revenue gains. It would require effective tax payer

education and support to ensure high levels of voluntary compliance.

Tax Refund

Section 73.-(6) suggests establishment of a separate Bank Account with sufficient funds for

the purposes of tax refunds. This may be a good idea to address the current challenges

especially in the VAT refund for mining companies leading to offsetting payments against tax

liabilities under a particular tax law. The bill is however, silent about the following key

questions:

i. How will the account be prudently managed to avoid possible mismanagement.

14

ii. From which source the account will be financed, to who and how the refunds will be

accounted transparently.

iii. What would be the basis/criteria for determining the sufficiency of the fund as the

term sufficient is relative. There is a need for the law to provide details of how such

account will be managed to avoid the likes of The BOT-EPA scandal.

iv. Mindful of the fact that VAT refund constituted the largest proportion of tax refund,

to what extent the fund is still relevant in the context of the proposed removal of

VAT exemptions in the VAT Bill?

4.2.1.2 Transparency and Accountability

Links to Investment Policy (Accounting for Tax Expenditure)

It is worth noting from the outset that strengthening domestic resource mobilization is not just a

question of raising revenues. Tax can also be used as important instrument for enhanced

accountability of state to its citizens. It is also about designing a tax system that promotes

inclusiveness, encourages good governance, matches society’s views on appropriate income and

wealth inequalities and promotes social justice.

Tanzania offers a range of fiscal incentives to attract investment in commercial and social ventures

with the aim to contribute to social and economic transformation of the country. These include:

investment tax credit, investment allowances, accelerated depreciation (100%), reduced tax rates,

tax holidays and indirect tax exoneration. While these exemptions are largely found in a specific

tax laws, it argued that some of these may have entered the tax law after they were granted under

different laws e.g. investment law.

- The bill is silent about many aspects of the tax incentives that are critically important for

revenue transparency, accountability and fairness. The administrative discretion in the

management of tax incentives significantly increase the risk of corruption and rent seeking.

15

- As part of tax administration, the bill could make provisions for identification, quantification

and publicizing the revenue cost of preferential tax treatments (tax exemptions) which are a

key element of fiscal transparency.

Generating such information will enhance cost-benefit analysis of tax exemptions and regular

impact evaluation of investment policies and project which is a potentially powerful tool in

avoiding and scaling back tax preferences that do not generate social benefit. It is also an effective

tool for rationalization of tax incentives across sectors.

Powers of the Commissioner

The bill contains a number of provisions that exert discretionary and or unchallenged powers to

the Commissioner General. Without effective checks and balances (which is the case) may create

loopholes for abuse.

Powers of the Commissioner General to Issue Practice Notice

9.-(1) The Commissioner General may, issue practice notes with a view to ensuring consistency in

the administration of tax laws and to provide guidance to persons affected by such laws.

The bill does not prescribe circumstances that may lead to issuance of a practice note and

therefore, may excessively empower the commissioner to use his/her discretionary powers to

issues a practice note for the purposes that may undermine enforcement of other provisions of

the applicable laws. It would be useful to provide broader description of such circumstance/

environment

The ruling Powers of Commissioner General

11.-(1) The Commissioner General may, on application in writing by a person, issue a private ruling

or a class ruling setting out position on the application of a tax law to an arrangement proposed or

entered into. This is a very important and positive provision in the context of related party

arrangements that do not conform to Arm’s Length transactions. However, to protect the integrity

of the Authority, the capacity of TRA in terms of deeper understanding of circumstances of

transaction or relations to stand legal challenges from powerful Trans National Corporations need

to be significantly enhanced.

16

11-(6) A person shall not challenge a private or class ruling, unless the challenge is in respect of a

tax decision made with respect to an arrangement which is the subject of a ruling.

There may be some ambiguity in translation of this provision and provisions of § 11.(1) in terms of

what the difference between application of a tax law and a tax decision especially for a common

person.

11- (7) The Commissioner General may, by notice published in the Gazette, impose fees to be

payable for an application and issuance of a private or class ruling.

Despite the fact that the imposed fees will be published in the Gazette, the absence of

predetermined criteria and procedures for setting such fees may create a dangerous loopholes for

the commissioner to impose prohibitive fees to discourage tax payers pursue their rights in this

perspective or to protect access to the ruling. This may seriously impose injustices especially for

small enterprises and individuals who cannot afford the fees.

Section 36 (2) requires the Commissioner General to publish a list of persons or class of persons

who are excluded from the requirement of the use of electronic fiscal device or the use of fiscal

receipt or invoice, the law should already provide for the classification to avoid potential

administrative lacuna and opacity in the compilation of the list. As such, the Income tax (Electronic

Fiscal Devise regulation, 2012 already provides such categorization which includes:

i. Persons who are not VAT registered with a threshold of TZS. 14 million

ii. Traders trading in the region’s prime areas identified on the basis of rent payable

iii. Traders dealing with selected business sectors

Section 35.- (5)(a) The Commissioner General may, by notice in writing-relieve a person from the

obligation to maintain documents or the time for which the documents are to be retained;

Administratively this is appropriate; however, without farther qualifying the circumstances under

which the commissioner may issues the relief may create a loophole for discretional and arbitrary

decision that is prone to abuse. `

Conflict of Interest

17

18. (4)-Where an expert is engaged and it is discovered that his engagement may result into a

conflict of interest, the Authority may terminate the engagement of such expert upon discovery of

such conflict of interest.

For effectiveness of this provision, the term “may” is rightfully applied due to the environment of

“uncertainty” about existence of effective conflict of interest. However, in a situation where it is

established that an expert knew about the conflict of interest at the point of engagement BUT

deliberately failed to disclose such interest, then it is recommended that the term “shall” be used

instead to strengthen powers of enforcement.

Subsections 5-6 empowers any person to inform the Authority of potential conflict interest and

expected actions from the Tax Authority, however, it is silent about what should happen when

allegation is proved to be true. A new subsection could be introduced to provide further

qualifications.

Fairness

The bill contains provisions that ensure fairness e.g. Section 73 (3) compels the Commissioner

General to pay interest on the on tax refunds. The bill further clarifies that the interest will be

calculated using “statutory rate”, however, it does not clarify what it means (it is not defined in

the bill)! Further, the time set for repayment of interest from the date decision is made vis-à-vis

the time tax was paid in excess especially where excess payment arises from TRA’s action. This

does not create an incentive for TRA to expedite timely decision on tax decisions that may attract

interest.

4.3 Investment Incentives in the Policy

Following economic reforms in the 1980-90’s, Tanzania pursued policy and legal reforms; the

passage of Investment Policy 1996, Investment Act 1997, establishment of Investment Centre

among others. Investment incentives are provided for in part 4.2, page 35 of the policy. Among

the issues of interest with regard to loosing government revenues include provisions for tax

incentives which are provided for in part 4.2.1. of the policy as shown below.

18

i) Fiscal incentives include the following:

a. Investment allowances on capital expenditure

b. Infrastructure allowances on infrastructure expenditure

c. Preferential tax rates for withholding tax on dividends, royalties and interest

d. Preferential tax rates on personal income tax

e. Preferential rates on indirect taxes

f. Double deductions on approved/specified costs and expenses

4.3.1 Discussion in Relation to the VAT Bill of 2014

The fiscal incentives listed above, so long as they involve VAT will be removed by the Bill. However,

so long as they are not related to VAT, the Bill is silent on them because it focuses solely on VAT.

4.3.1.1 Potential Revenue Loss Issues in the Policy

The following issues in the policy are among the issues that can potentially lead to revenue loss for

the government through fiscal incentives.

i. The policy states that Tanzania’s tax system shall be competitive compared to similar

economies

Discussion

Having tax system that is ‘competitive compared to similar economies’ is against the

recommendations given in several studies including the one on “Tax Incentives in Tanzania:

A Race to the Bottom?” by Policy Forum (2012) and on “One Billion Dollar Question: How

Can Tanzania Stop Loosing So Much Tax Revenue” by Curtis, Ngowi and Attiya (2012). It

was recommended in the publications among other things that Tanzania should not involve

itself in tax competition within East Africa. This is because it is likely to lead to the race to

the bottom problem of losing tax revenues. Therefore, the VAT Bill may reduce tax

19

revenues lost through exemption but revenue may still be lost through other ‘competitive

tax system’ than VAT.

ii. The policy states that the government will provide tax incentives in order to improve

investment productivity

Discussion

The kind of tax incentives that has been removed by the VAT Bill 2014 are the VAT

exemptions. Other tax incentives granted to investors are not dealt with in the VAT Bill.

iii. The policy states that the government will make taxes affordable and provide investment

allowances that allow investors to contribute to tax revenue

Discussion

The VAT Bill has only removed tax exemptions for investors and does not deal with other

types of taxes. Therefore, revenue loss that may be reduced is only that related to VAT

exemption. Other taxes and investment allowances are not dealt with in the VAT Bill.

The policy states further that the simplified tax incentive will be provided and maintained

on a schedule in the investment code. These include

- Corporate tax: Shall be low, affordable and competitive enough to assure profits

and thus stimulate investments

- Cooperative society taxes: Incentives will be extended to investing cooperative

societies

- Investment allowances on capital expenditure: These are applied to the assessed

statutory income, subject to account being taken of the goals of the investment

policy.

- Re-investment allowances on capital expenditure: These are provided to cover

capital expenditure for re-investment and rehabilitation purposes

- Withhoding tax on dividends, royalties and interest payable on foreign loans

20

- Personal income tax

- Sole proprietors: Tax rate shall be low, affordable and competitive in order to

encourage registration of sole proprietors and partnerships

- Indirect taxes: Import duties and sales/excise taxes are payable on imported

investment goods at a competitive rate and subject to periodic review; export

duties/subsidies and taxes are to be charged/offered at a zero rate

- Infrastructure allowance: Allowance for infrastructure expenditure

- Double taxation avoidance agreements

- Accelerated depreciation allowance

- Specified sectoral tax incentives

- Expatriate inducement: Tax concessions to expatriate employees

Discussion and Analysis

The policy clearly gives a lot of tax incentives. However, it does not have anything to

do with VAT. This is because the policy was drafted in 1996 while the VAT Act was

introduced after the policy in 1997 and came into operation on 1st July 1998. It is not

strange therefore that the policy does not contain anything on VAT in general or VAT

exemption in particular

The opposite is the case in the VAT Bill 2014 where there has been substantial reduction of tax

incentives but only those related to VAT exemptions. Therefore, whereas the VAT Bill 2014 stands

to reduce revenue loss that would take place through VAT exemptions, the policy still provides a

number of tax incentives. Since the policy is under review, it is recommended that when it is out it

should be analyzed with the view of determining the extent to which it still offers incentives and

whether it is in line with the VAT Bill 2014 which by then is likely to be a law.

21

References

Curtis, M., Ngowi, H. P and Attiya, W (2012). One Billion Dollar Question: How Can Tanzania

Stop Loosing So Much Tax Revenue

Policy Forum (2012) Tax Incentives in East Africa: A Race to the Bottom?

TPSF (2013). Business Leaders’ Perceptions on Business Environment in Tanzania

VAT Bill 2014

Tax Administration Act 2014

United Republic of Tanzania – URT – (1996). National Investment Promotion Policy

OECD Investment Policy Review: Tanzania 2013