“ANALYSIS OF THE EFFECT OF INFLATION RATE, INTEREST...

116

“ANALYSIS OF THE EFFECT OF INFLATION RATE, INTEREST RATE AND EXCHANGE RATE ON STOCK RETURN OF CONSUMER GOODS AND PROPERTY AND REAL ESTATE SECTOR IN INDONESIA STOCK EXCHANGE (IDX) 2006-2010” Submitted by: Ariningtyas Widyasnia Agustina Student ID:107081101584 INTERNATIONAL UNDERGRADUATE PROGRAM MANAGEMENT DEPARTMENT FACULTY OF ECONOMICS AND BUSINESS UIN SYARIF HIDAYATULLAH JAKARTA 2011

Transcript of “ANALYSIS OF THE EFFECT OF INFLATION RATE, INTEREST...

“ANALYSIS OF THE EFFECT OF INFLATION RATE, INTEREST

RATE AND EXCHANGE RATE ON STOCK RETURN OF CONSUMER

GOODS AND PROPERTY AND REAL ESTATE SECTOR IN

INDONESIA STOCK EXCHANGE (IDX) 2006-2010”

Submitted by:

Ariningtyas Widyasnia Agustina

Student ID:107081101584

INTERNATIONAL UNDERGRADUATE PROGRAM

MANAGEMENT DEPARTMENT

FACULTY OF ECONOMICS AND BUSINESS

UIN SYARIF HIDAYATULLAH JAKARTA

2011

i

ACKNOWLEDGEMENT

My greatest gratitude to Allah SWT, the Grandest and Almighty, the Most

Gracious and the Most Merciful, for giving me the chance and ability to complete this

thesis,and for all the miracles He has granted to my life. May the talent You have

bestowed upon me will not got to waste. My greatest ggratitude to Prophet

Muhammad SAW for the teachings and love he has spread to all the creatures in this

whole universe. May we all always under his guidance.

First and foremost, I would like to thank to my thesis supervisors; Prof. Dr.

Ahmad Rodhoni, MM and Mr. Tirmidzi Taridi,MBA for their help, time, contribution

and effort in providing guidance and constructive suggestion to perform this study,

and for the understanding and support they had given.

I would also like to thank to the head of International Program, Faculty of

Economics and Business, UIN Syarif Hidayatullah Jakarta, Mr. Arief Mufraini, Lc.

M.Si, and his deputies Mr. Ahmad Dumiyati. Also, thanks to Kak Sugih, for his

patients in accomodating all of my administrative needs. Thank you.

This thesis will never be completed without the continous support and prays

from my friends, collagues, and people around me. Thank you for the people in my

current internship place, Bank Indonesia, the place where this thesis born. I would

also like to thank to my bestfriends in International Program Batch 4; Sukria, Andrea

Ardilla, Wike Vidya, Pramayassya, Fitra, Weldan, Muhammad Kharisma and all,

whose name can’t be mentioned one by one. Individually, thank you to Aprima Arta

for his continous support and understanding during my hardest time in making this

thesis.

Last, but not least, I dedicated this thesis to the greatest gift God has given to

my life, my family. My father, H. Sumarno, for his support and increadible patient,

you are the soul of our life. My mother, Hj. Sri Irawati, for her unlimited guidance

that always keeping me on the right track. My brother, Rifki Hidayat Rahkumulyo,

and my sister, Arindani Tri Ramadhani, for made my life so blessed and colorful

everyday. Thank you.

Ariningtyas W. Agustina

Jakarta, March 20 2011

ii

ABSTRAK

Penelitian ini bertujuan untuk menganalisis pengaruh suku bunga, inflasi, dan

nilai tukar terhadap tingkat pengembalian saham pada sektor properti dan real estate

serta sektor industry barang konsumsi periode 2006-2010. Penelitian ini

menggunakan model regresi linear berganda. Berdasarkan hasil penelitian, secara

parsial suku bunga berpengaruh signifikan negatif terhadap tingkat pengembalian

saham property dan real estate dan tingkat pengembalian saham barang konsumsi

.Inflasi tidak berpengaruh terhadap tingkat pengembalian saham property dan real

estate serta saham barang konsumsi. Nilai tukar berpengaruh signifikan negatif

terhadap tingkat pengembalian saham property dan real estate serta saham barang

konsumsi. Hasil penelitian juga menunjukkan bahwa suku bunga, inflasi, dan nilai

tukar berpengaruh lebih besar terhadap tingkat pengembalian saham property dan real

estate daripada saham barang konsumsi.

Kata Kunci: tingkat pengembalian saham, suku bunga, inflasi, nilai tukar.

iii

ABSTRACT

This research shows the effect of inflation rate, interest rate, and exchange

rate on stock return of property and real estate and consumer goods sector in period

2006-2010. A multiple regression model is applied to test the significance of

influence between the independent variable and the dependent variable. Based on the

result, partially interest rate has a negative effect to stock return of property and real

estate sector and consumer goods sector. Inflation has no effect to stock return of

property and real estate and consumer goods sector, while exchange rate has negative

effect to stock return of property and real estate sector. The result shows that the

inflation rate, exchange rate, and interest rate have a bigger effect on stock return of

property and real estate sector than consumer goods sector.

Keywords: stock return, interest rate, inflation, exchange rate.

iv

LIST OF CONTENTS

CHAPTER 1: INTRODUCTION __________________________________________ 1

A. Background ________________________________________________________ 1

B. Problem Formulation ________________________________________________ 6

C. Research Objectives _________________________________________________ 8

D. Usefullness of the Research ___________________________________________ 8

CHAPTER 2: LITERATURE REVIEW ____________________________________ 13

A. Fundamental of Capital Market _______________________________________ 13

1. History of Indonesian Capital Market _________________________________ 13

2. Capital Market Definition __________________________________________ 14

3. Capital Market Instrument __________________________________________ 15

B. Investment ________________________________________________________ 16

C. Stock Rate of Return ________________________________________________ 19

D. Risks ____________________________________________________________ 21

E. Inflation __________________________________________________________ 23

1. Relationship between inflation rate and stock return ______________________ 27

F. Interest Rate _______________________________________________________ 26

2.6.1 Relationship between interest rate and stock return ____________________ 27

2.6.2 SBI (Sertifikat Bank Indonesia) Rate _______________________________ 28

G. Exchange Rate ____________________________________________________ 30

H. Previous Researches ________________________________________________ 31

I. Research Framework and Hypotheses __________________________________ 37

v

CHAPTER 3: RESEARCH METHODOLOGY ______________________________ 40

A. Data Collection ____________________________________________________ 40

1. Unit of Analysis and Research Sampling _______________________________ 40

2. Types of Data ____________________________________________________ 41

B. Research Models ___________________________________________________ 41

3.3 Operational Variable _______________________________________________ 42

3.3.1 Stock’s Rate of Return __________________________________________ 42

3.3.2 Inflation Rate __________________________________________________ 43

3.3.2 Exchange Rate _________________________________________________ 44

3.3.2 Interest Rate ___________________________________________________ 45

3.4 Data Analysis Technique ____________________________________________ 45

3.4.1 Normality Test _________________________________________________ 46

3.4.1.1 Jarque-Bera Test of Normality _________________________________ 47

3.4.2 Classical Assumption Test _______________________________________ 48

3.4.2.1 Heteroscedastic Test _________________________________________ 50

3.4.2.2 Autocorrelation Test _________________________________________ 53

3.4.2.3 Multi-Collinearity Test _______________________________________ 54

3.4.3 Hypothesis Test ________________________________________________ 55

3.4.3.1 T Test ____________________________________________________ 55

3.4.3.2 F Test ____________________________________________________ 55

3.4.3.3 R Square (R2) Test __________________________________________ 56

3.4.4.4 Adjusted R Squared Test _____________________________________ 56

3.5 Research Design __________________________________________________ 57

CHAPTER 4: RESEARCH FINDINGS AND ANALYSIS _____________________ 58

4.1 Brief Introduction _________________________________________________ 58

vi

4.2 Descriptive Statistic ________________________________________________ 59

4.3 Normality Test ____________________________________________________ 60

4.4 Classical Assumption Test ___________________________________________ 62

4.4.1 Heteroscedasticity Test __________________________________________ 62

4.4.2 Auto-Correlation Test ___________________________________________ 64

4.4.3 Multi-Collinearity Test __________________________________________ 65

4.5 Multiple Linear Regression Model ____________________________________ 66

4.6 Hypothesis Testing ________________________________________________ 67

4.6.1 T-Test _______________________________________________________ 67

4.6.2 f Test ________________________________________________________ 81

4.6.3 R-Squared (R2) ________________________________________________ 81

4.6.4 Adjusted R-Squared ____________________________________________ 82

4.7 The comparison between macroeconomic factors’ influences towards the

stock’s return on consumer goods and property and real estate sector _________ 83

CHAPTER 5: CONCLUSION AND IMPLICATIONS ________________________ 84

5.1 Conclusion ______________________________________________________ 84

5.2 Implication of Study _______________________________________________ 85

5.2.1 For the Investor ________________________________________________ 85

5.2.1 For the Researcher ______________________________________________ 85

5.3 Limitation _______________________________________________________ 86

REFERENCES

APPENDIX I

APPENDIX I

vii

LIST OF FIGURES

2.1 Indonesia Interest Rate _____________________________________________ 29

2.2 Research Model ___________________________________________________ 39

3.1 Research Framework _______________________________________________ 57

4.1 Histogram Residual, Consumer Goods Sector ___________________________ 61

4.2 Histogram Residual, Property and Real Estate Sector _____________________ 61

4.3 Graph of Ex. Rate & Stock Return Movement 1 __________________________ 69

4.4 Graph of Inflation Rate & Stock Return Movement 1 _____________________ 71

4.5 Graph of SBI Rate & Stock Return Movement 1 _________________________ 73

4.6 Graph of Exchange Rate & Stock Return Movement 2 ____________________ 76

4.7 Graph of Inflation Rate & Stock Return Movement 2 _____________________ 78

4.8 Graph of SBI Rate & Stock Return Movement 2 _________________________ 80

viii

LIST OF TABLES

2.1 Indonesia Interest Rate _____________________________________________ 29

2.2 Research Model ___________________________________________________ 39

1.3 Research Objectives ________________________________________________ 8

1.4 Research Benefits __________________________________________________ 8

1.4 Research Benefits __________________________________________________ 8

4. Descriptive Statistics ________________________________________________ 59

4.2 Heteroscedasticity Test for Property and Real Estate Sector ________________ 63

4.3 Auto-Correlation Test for Consumer Goods Sector _______________________ 63

4.4 Auto-Correlation Test for Property and Real Estate Sector _________________ 64

4.5 Multi-Collinearity Test _____________________________________________ 65

4.6 Multi-Collinearity Test _____________________________________________ 65

4.7 Multi-Collinearity Test _____________________________________________ 67

4.8 Output Multiple Linear Regression Property and Real Estate Sector _________ 74

4.9 Comparison of Coefficient Regression _________________________________ 83

ix

LIST OF FORMULAS

2.1 Simple Returns ___________________________________________________ 19

2.2 Continously Compounded Return _____________________________________ 20

2.3 Consumer Price Index ______________________________________________ 24

2.4 Wholeseller Price Index _____________________________________________ 24

2.5 Inflation Rate _____________________________________________________ 25

2.6 Relationship between nominal and interest rate __________________________ 27

2.7 Capital Price Index Model ___________________________________________ 35

2.8 Multi Index Model _________________________________________________ 36

3.1 Model 1 _________________________________________________________ 41

3.2 Model 2 _________________________________________________________ 41

3.3 Continously Compounded Method ____________________________________ 42

3.4 Inflation Rate _____________________________________________________ 43

3.5 Change in Inflation Rate ____________________________________________ 43

3.6 Change in Exchange Rate ___________________________________________ 44

3.7 Change in Interest Rate _____________________________________________ 45

3.8 Jarque-Bera Test of Normality _______________________________________ 47

3.9 Zero Mean Value of Disturbance _____________________________________ 48

3.10 Homoscedasticity or equal variance of ui ______________________________ 49

3.11 No autocorrelation between the disturbances ___________________________ 49

x

3.12 Zero covariance between ui and Xi ____________________________________ 49

3.13 Regression Model ________________________________________________ 51

3.14 Auxiliary Regression Model ________________________________________ 51

3.15 Chi Square Distribution ____________________________________________ 52

3.16 R-Squared Test __________________________________________________ 56

xi

“In the name of Allah, the Most Gracious, the Most Merciful....

All praise be to God alone, the Lord of all the world, the All-Merciful, the Ever Mercy-giving,

and the Master of the Day of Judgement.

You alone we worship, and You alone we ask for help.

Guide us on the right path,

The path of whom You have blessed, not of those who incur You anger, nor of those who go

astray.......”

(QS Al-Fathihah : 1-7)

APPENDIX I

Consumer Goods Return

Date

Consumer

Goods Index

Price

Consumer

Goods Return

12/30/2005 280.928

1/31/2006 288.583 0.026884331

2/28/2006 292.458 0.013338327

3/31/2006 293.905 0.004935519

4/28/2006 328.354 0.110835709

5/31/2006 294.929 -0.107357645

6/30/2006 299.316 0.014765222

7/31/2006 313.201 0.045345285

8/31/2006 331.074 0.055496758

9/29/2006 343.543 0.03697037

10/31/2006 349.721 0.017823408

11/24/2006 347.347 -0.006811413

12/29/2006 392.458 0.122105245

1/31/2007 390.251 -0.005639403

2/28/2007 385.22 -0.012975522

3/30/2007 385.827 0.001574483

4/30/2007 391.795 0.015349661

5/31/2007 411.99 0.050260333

6/29/2007 324.964 -0.23728467

7/31/2007 453.843 0.334036916

8/31/2007 415.462 -0.088360169

9/28/2007 421.425 0.014250672

10/31/2007 429.804 0.019687465

11/30/2007 426.853 -0.006889599

12/28/2007 436.039 0.021291997

1/31/2008 438.132 0.004788546

2/29/2008 430.084 -0.018539696

3/31/2008 405.011 -0.060066311

4/30/2008 394.385 -0.026586638

5/30/2008 414.54 0.049841882

6/30/2008 398.285 -0.040001642

7/31/2008 390.81 -0.018946321

8/29/2008 396.007 0.013210379

9/29/2008 381.36 -0.037688077

10/31/2008 321.919 -0.16944385

11/28/2008 320.9 -0.003170413

12/30/2008 326.843 0.018350385

1/30/2009 337.847 0.033113197

2/27/2009 346.155 0.024293521

3/31/2009 351.269 0.01466566

4/30/2009 381.322 0.082091851

5/29/2009 433.732 0.128782669

6/30/2009 495.732 0.133608626

7/31/2009 591.202 0.176122294

8/31/2009 559.178 -0.055689904

9/30/2009 597.628 0.066500639

10/30/2009 575.396 -0.037909987

11/30/2009 625.728 0.083857272

12/30/2009 671.305 0.070307807

1/29/2010 699.783 0.041546708

2/26/2010 717.932 0.02560457

3/31/2010 738.141 0.027760006

4/30/2010 821.588 0.10710419

5/31/2010 889.807 0.079765532

6/30/2010 959.04 0.074928199

7/30/2010 1,001.30 0.043122649

8/31/2010 1,005.91 0.004595432

9/30/2010 1,176.56 0.15670104

10/29/2010 1,179.98 0.00290171

11/30/2010 1,070.01 -0.097826604

12/30/2010 1,094.65 0.022765686

Property and Real Estate Return

Date

Property and

Real Estate

Index Price

Property and

Real Estate

Return

12/29/2005 64.12

1/31/2006 70.484 0.094629406

2/28/2006 71.33 0.011931263

3/31/2006 79.331 0.106311977

4/28/2006 88.956 0.114512893

5/31/2006 81.352 -0.089356447

6/30/2006 77.433 -0.049372372

7/31/2006 77.942 0.006551914

8/31/2006 78.985 0.013293001

9/29/2006 83.775 0.058876673

10/31/2006 90.316 0.075179998

10/24/2006 90.467 0.001670511

12/29/2006 122.918 0.306532323

1/31/2007 123.101 0.00148769

2/28/2007 136.185 0.101009099

3/30/2007 143.243 0.050528233

4/30/2007 168.687 0.163502438

5/31/2007 201.037 0.175444044

6/29/2007 211.718 0.05176623

7/31/2007 247.47 0.156034162

8/31/2007 225.648 -0.0923131

9/28/2007 242.834 0.073401819

10/31/2007 247.309 0.018260485

11/30/2007 232.089 -0.063517648

12/28/2007 251.816 0.081577743

1/31/2008 229.563 -0.09252116

2/29/2008 229.517 -0.000200401

3/31/2008 195.603 -0.159890006

4/30/2008 177.721 -0.09587219

5/30/2008 184.272 0.036198022

6/30/2008 168.528 -0.089311019

7/31/2008 174.699 0.035962585

8/29/2008 164.414 -0.060676856

9/29/2008 142.421 -0.143600177

10/31/2008 101.346 -0.340247055

11/28/2008 105.632 0.041420951

12/30/2008 103.489 -0.020496029

1/30/2009 96.026 -0.074846339

2/27/2009 96.558 0.005524876

3/31/2009 99.742 0.032442988

4/30/2009 112.318 0.118747282

5/29/2009 130.986 0.153756313

6/30/2009 144.787 0.10017325

7/31/2009 159.975 0.099753856

8/31/2009 157.959 -0.012682047

9/30/2009 162.285 0.027018543

10/30/2009 153.985 -0.052498854

11/30/2009 143.635 -0.069579836

12/30/2009 146.8 0.021795757

1/29/2010 153.491 0.044570817

2/26/2010 150.231 -0.021467824

3/31/2010 166.378 0.102088199

4/30/2010 182.123 0.090419975

5/31/2010 154.504 -0.164462297

6/30/2010 163.384 0.055883272

7/30/2010 168.259 0.029401201

8/31/2010 170.904 0.015597536

9/30/2010 192.768 0.120385398

10/29/2010 202.413 0.048822771

11/30/2010 203.223 0.003993734

12/30/2010 203.097 -0.000620201

Data of Exchange Rate

Year Month Sell Buy Mid Change

2005 December 9879 9781 9830

2006 January 9442 9348 9395 -0.0443

February 9276 9184 9230 -0.0176

March 9120 9030 9075 -0.0168

April 8819 8731 8775 -0.0331

May 9266 9174 9220 0.05071

June 9347 9253 9300 0.00868

July 9115 9025 9070 -0.0247

August 9146 9054 9100 0.00331

September 9281 9189 9235 0.01484

October 9156 9064 9110 -0.0135

November 9211 9119 9165 0.00604

December 9065 8975 9020 -0.0158

2007 January 9135 9045 9090 0.00776

February 9206 9114 9160 0.0077

March 9164 9072 9118 -0.0046

April 9128 9038 9083 -0.0038

May 8872 8784 8828 -0.0281

June 9099 9009 9054 0.0256

July 9232 9140 9186 0.01458

August 9457 9363 9410 0.02438

September 9183 9091 9137 -0.029

October 9149 9057 9103 -0.0037

November 9423 9329 9376 0.02999

December 9466 9372 9419 0.00459

2008 January 9337 9245 9291 -0.0136

February 9096 9006 9051 -0.0258

March 9263 9171 9217 0.01834

April 9280 9188 9234 0.00184

May 9365 9271 9318 0.0091

June 9271 9179 9225 -0.01

July 9164 9072 9118 -0.0116

August 9199 9107 9153 0.00384

September 9425 9331 9378 0.02458

October 11050 10940 10995 0.17242

November 12212 12090 12151 0.10514

December 11005 10895 10950 -0.0988

2009 January 11412 11298 11355 0.03699

February 12040 11920 11980 0.05504

March 11633 11517 11575 -0.0338

April 10767 10659 10713 -0.0745

May 10392 10288 10340 -0.0348

June 10276 10174 10225 -0.0111

July 9970 9870 9920 -0.0298

August 10110 10010 10060 0.01411

September 9729 9633 9681 -0.0377

October 9593 9497 9545 -0.014

November 9527 9433 9480 -0.0068

December 9447 9353 9400 -0.0084

2010 January 9412 9318 9365 -0.0037

February 9382 9288 9335 -0.0032

March 9161 9069 9115 -0.0236

April 9057 8967 9012 -0.0113

May 9226 9134 9180 0.01864

June 9128 9038 9083 -0.0106

July 8997 8907 8952 -0.0144

August 9086 8996 9041 0.00994

September 8969 8879 8924 -0.0129

October 8973 8883 8928 0.00045

November 9058 8968 9013 0.00952

December 9036 8946 8991 -0.0024

Data of SBI Rate

Year Month

SBI

Rate Change

2005 December 0.1275

2006 January 0.1275 0

February 0.1274 -0.0008

March 0.1273 -0.0008

April 0.1274 0.00079

May 0.125 -0.0188

June 0.125 0

July 0.1225 -0.02

August 0.1175 -0.0408

September 0.1125 -0.0426

October 0.1075 -0.0444

November 0.1025 -0.0465

December 0.0975 -0.0488

2007 January 0.095 -0.0256

February 0.0925 -0.0263

March 0.09 -0.027

April 0.09 0

May 0.0875 -0.0278

June 0.085 -0.0286

July 0.0825 -0.0294

August 0.0825 0

September 0.0825 0

October 0.0825 0

November 0.0825 0

December 0.08 -0.0303

2008 January 0.08 0

February 0.0793 -0.0088

March 0.0796 0.00378

April 0.0799 0.00377

May 0.0831 0.04005

June 0.0873 0.05054

July 0.0923 0.05727

August 0.0928 0.00542

September 0.0971 0.04634

October 0.1098 0.13079

November 0.1124 0.02368

December 0.1083 -0.0365

2009 January 0.0977 -0.0979

February 0.0874 -0.1054

March 0.0821 -0.0606

April 0.0764 -0.0694

May 0.0725 -0.051

June 0.0695 -0.0414

July 0.0671 -0.0345

August 0.0658 -0.0194

September 0.0648 -0.0152

October 0.0649 0.00154

November 0.0647 -0.0031

December 0.0646 -0.0015

2010 January 0.0645 -0.0015

February 0.0641 -0.0062

March 0.0632 -0.014

April 0.0625 -0.0111

May 0.0637 0.0192

June 0.0629 -0.0126

July 0.067 0.06518

August 0.067 0

September 0.0645 -0.0373

October 0.0645 0

November 0.065 0.00775

December 0.063 -0.0308

Data of Inflation Rate

Year Month Inflation Change in Inflation

2005 December -0.04

2006 January 1.36 -35

February 0.58 -0.573529412

March 0.03 -0.948275862

April 0.05 0.666666667

May 0.37 6.4

June 0.45 0.216216216

July 0.45 0

August 0.33 -0.266666667

September 0.38 0.151515152

October 0.86 1.263157895

November 0.34 -0.604651163

December 1.21 2.558823529

2007 January 1.04 -0.140495868

February 0.62 -0.403846154

March 0.24 -0.612903226

April -0.16 -1.666666667

May 0.10 -1.625

June 0.23 1.3

July 0.72 2.130434783

August 0.75 0.041666667

September 0.80 0.066666667

October 0.79 -0.0125

November 0.18 -0.772151899

December 1.10 5.111111111

2008 January 1.77 0.609090909

February 0.65 -0.632768362

March 0.95 0.461538462

April 0.57 -0.4

May 1.41 1.473684211

June 2.46 0.744680851

July 1.37 -0.443089431

August 0.51 -0.627737226

September 0.97 0.901960784

October 0.45 -0.536082474

November 0.12 -0.733333333

December -0.04 -1.333333333

2009 January -0.07 0.75

February 0.21 -4

March 0.22 0.047619048

April -0.31 -2.409090909

May 0.04 -1.129032258

June 0.11 1.75

July 0.45 3.090909091

August 0.56 0.244444444

September 1.05 0.875

October 0.19 -0.819047619

November -0.03 -1.157894737

December 0.33 -12

2010 January 0.84 1.545454545

February 0.30 -0.642857143

March -0.14 -1.466666667

April 0.15 -2.071428571

May 0.29 0.933333333

June 0.97 2.344827586

July 1.57 0.618556701

August 0.76 -0.515923567

September 0.44 -0.421052632

October 0.06 -0.863636364

November 0.60 9

December 0.92 0.533333333

APPENDIX II

EVIEWS 5 OUTPUT (Consumer Goods Sector)

MULTIPLE REGRESSION

Dependent Variable: Y

Method: Least Squares

Date: 02/07/11 Time: 16:04

Sample: 2006M01 2010M12

Included observations: 60

Variable Coefficient Std. Error t-Statistic Prob.

C 0.016385 0.008014 2.044428 0.0456

X1 -0.693450 0.226342 -3.063726 0.0034

X2 3.36E-05 0.001505 0.022330 0.9823

X3 -0.483347 0.223922 -2.158550 0.0352

R-squared 0.286679 Mean dependent var 0.022268

Adjusted R-squared 0.248466 S.D. dependent var 0.067858

S.E. of regression 0.058827 Akaike info criterion -2.764084

Sum squared resid 0.193796 Schwarz criterion -2.624461

Log likelihood 86.92251 F-statistic 7.502025

Durbin-Watson stat 2.016865 Prob(F-statistic) 0.000263

AUTO CORRELATION TEST

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 0.150862 Probability 0.860328

Obs*R-squared 0.333385 Probability 0.846460

White Heteroskedasticity Test:

F-statistic 1.985143 Probability 0.084204

Obs*R-squared 11.00974 Probability 0.088076

DESCRIPTIVE STATISTICS

Y C X1 X2 X3

Mean 0.022268 1.000000 -0.000831 -0.483316 -0.011012

Median 0.003819 1.000000 -0.003781 -0.076498 -0.007476

Maximum 0.193360 1.000000 0.172425 9.000000 0.130793

Minimum -0.169444 1.000000 -0.098840 -35.00000 -0.105425

Std. Dev. 0.067858 0.000000 0.037145 5.192304 0.036939

Skewness 0.352901 NA 1.717417 -5.028711 0.705108

Kurtosis 3.747713 NA 10.70772 34.36123 6.116995

Jarque-Bera 2.643079 NA 178.0175 2711.697 29.26092

Probability 0.266724 NA 0.000000 0.000000 0.000000

Sum 1.336056 60.00000 -0.049875 -28.99897 -0.660716

Sum Sq.

Dev. 0.271681 0.000000 0.081406 1590.641 0.080504

Observations 60 60 60 60 60

MULTI-COLLINEARITY TEST

Dependent Variable: X1

Method: Least Squares

Date: 02/07/11 Time: 16:09

Sample: 2006M01 2010M12

Included observations: 60

Variable Coefficient Std. Error t-Statistic Prob.

C 0.003920 0.004661 0.841008 0.4039

X2 0.001321 0.000863 1.530626 0.1314

X3 0.373475 0.121341 3.077900 0.0032

R-squared 0.170209 Mean dependent var -0.000831

Adjusted R-squared 0.141094 S.D. dependent var 0.037145

S.E. of regression 0.034425 Akaike info criterion -3.851354

Sum squared resid 0.067550 Schwarz criterion -3.746637

Log likelihood 118.5406 F-statistic 5.846004

Durbin-Watson stat 1.836991 Prob(F-statistic) 0.004905

Dependent Variable: X2

Method: Least Squares

Date: 02/07/11 Time: 16:09

Sample: 2006M01 2010M12

Included observations: 60

Variable Coefficient Std. Error t-Statistic Prob.

C -0.601305 0.700757 -0.858079 0.3944

X1 29.87945 19.52107 1.530626 0.1314

X3 -12.97014 19.63019 -0.660724 0.5115

R-squared 0.039652 Mean dependent var -0.483316

Adjusted R-squared 0.005956 S.D. dependent var 5.192304

S.E. of regression 5.176819 Akaike info criterion 6.174965

Sum squared resid 1527.569 Schwarz criterion 6.279683

Log likelihood -182.2490 F-statistic 1.176746

Durbin-Watson stat 1.268507 Prob(F-statistic) 0.315656

Dependent Variable: X3

Method: Least Squares

Date: 02/07/11 Time: 16:09

Sample: 2006M01 2010M12

Included observations: 60

Variable Coefficient Std. Error t-Statistic Prob.

C -0.010978 0.004512 -2.432994 0.0181

X1 0.381592 0.123978 3.077900 0.0032

X2 -0.000586 0.000887 -0.660724 0.5115

R-squared 0.142669 Mean dependent var -0.011012

Adjusted R-squared 0.112587 S.D. dependent var 0.036939

S.E. of regression 0.034797 Akaike info criterion -3.829852

Sum squared resid 0.069018 Schwarz criterion -3.725135

Log likelihood 117.8956 F-statistic 4.742714

Durbin-Watson stat 0.862207 Prob(F-statistic) 0.012437

0

1

2

3

4

5

6

7

8

9

-0.10 -0.05 -0.00 0.05 0.10 0.15

Series: Residuals

Sample 2006M01 2010M12

Observations 60

Mean -4.97e-18

Median -0.005805

Maximum 0.145997

Minimum -0.105790

Std. Dev. 0.057312

Skewness 0.487487

Kurtosis 2.684504

Jarque-Bera 2.625284

Probability 0.269108

EVIEWS 5 OUTPUT (Property and Real Estate Sector)

MULTIPLE REGRESSION

Dependent Variable: Y

Method: Least Squares

Date: 02/07/11 Time: 10:59

Sample: 2006M01 2010M12

Included observations: 60

Variable Coefficient Std. Error t-Statistic Prob.

C 0.008209 0.011062 0.742136 0.4611

X1 -1.065215 0.312405 -3.409723 0.0012

X2 -0.000461 0.002077 -0.221818 0.8253

X3 -0.898840 0.309064 -2.908261 0.0052

R-squared 0.369993 Mean dependent var 0.019215

Adjusted R-squared 0.336243 S.D. dependent var 0.099661

S.E. of regression 0.081195 Akaike info criterion -2.119578

Sum squared resid 0.369190 Schwarz criterion -1.979955

Log likelihood 67.58735 F-statistic 10.96265

Durbin-Watson stat 1.908693 Prob(F-statistic) 0.000009

AUTO CORRELATION TEST

Breusch-Godfrey Serial Correlation LM Test:

F-statistic 0.587759 Probability 0.559086

Obs*R-squared 1.278303 Probability 0.527740

Test Equation:

Dependent Variable: RESID

Method: Least Squares

Date: 02/07/11 Time: 10:57

Presample missing value lagged residuals set to zero.

Variable Coefficient Std. Error t-Statistic Prob.

C 0.000104 0.011158 0.009328 0.9926

X1 0.009653 0.322981 0.029888 0.9763

X2 -0.000342 0.002124 -0.161050 0.8727

X3 0.030717 0.315445 0.097378 0.9228

RESID(-1) 0.039112 0.138929 0.281525 0.7794

RESID(-2) 0.141898 0.137328 1.033283 0.3061

R-squared 0.021305 Mean dependent var 6.94E-19

Adjusted R-squared -0.069315 S.D. dependent var 0.079104

S.E. of regression 0.081800 Akaike info criterion -2.074447

Sum squared resid 0.361324 Schwarz criterion -1.865012

Log likelihood 68.23341 F-statistic 0.235103

Durbin-Watson stat 2.037779 Prob(F-statistic) 0.945374

White Heteroskedasticity Test:

F-statistic 0.538939 Probability 0.776195

Obs*R-squared 3.450216 Probability 0.750581

MULTI-COLLINEARITY TEST

Dependent Variable: X1

Method: Least Squares

Date: 02/07/11 Time: 11:01

Sample: 2006M01 2010M12

Included observations: 60

Variable Coefficient Std. Error t-Statistic Prob.

C 0.003920 0.004661 0.841008 0.4039

X2 0.001321 0.000863 1.530626 0.1314

X3 0.373475 0.121341 3.077900 0.0032

R-squared 0.170209 Mean dependent var -0.000831

Adjusted R-squared 0.141094 S.D. dependent var 0.037145

S.E. of regression 0.034425 Akaike info criterion -3.851354

Sum squared resid 0.067550 Schwarz criterion -3.746637

Log likelihood 118.5406 F-statistic 5.846004

Durbin-Watson stat 1.836991 Prob(F-statistic) 0.004905

Dependent Variable: X2

Method: Least Squares

Date: 02/07/11 Time: 11:02

Sample: 2006M01 2010M12

Included observations: 60

Variable Coefficient Std. Error t-Statistic Prob.

C -0.601305 0.700757 -0.858079 0.3944

X1 29.87945 19.52107 1.530626 0.1314

X3 -12.97014 19.63019 -0.660724 0.5115

R-squared 0.039652 Mean dependent var -0.483316

Adjusted R-squared 0.005956 S.D. dependent var 5.192304

S.E. of regression 5.176819 Akaike info criterion 6.174965

Sum squared resid 1527.569 Schwarz criterion 6.279683

Log likelihood -182.2490 F-statistic 1.176746

Durbin-Watson stat 1.268507 Prob(F-statistic) 0.315656

Dependent Variable: X3

Method: Least Squares

Date: 02/07/11 Time: 11:02

Sample: 2006M01 2010M12

Included observations: 60

Variable Coefficient Std. Error t-Statistic Prob.

C -0.010978 0.004512 -2.432994 0.0181

X1 0.381592 0.123978 3.077900 0.0032

X2 -0.000586 0.000887 -0.660724 0.5115

R-squared 0.142669 Mean dependent var -0.011012

Adjusted R-squared 0.112587 S.D. dependent var 0.036939

S.E. of regression 0.034797 Akaike info criterion -3.829852

Sum squared resid 0.069018 Schwarz criterion -3.725135

Log likelihood 117.8956 F-statistic 4.742714

Durbin-Watson stat 0.862207 Prob(F-statistic) 0.012437

Descriptive Statistics

Y X1 X2 X3

Mean 0.019215 -0.000831 -0.483316 -0.011012

Median 0.024407 -0.003781 -0.076498 -0.007476

Maximum 0.306532 0.172425 9.000000 0.130793

Minimum -0.340247 -0.098840 -35.00000 -0.105425

Std. Dev. 0.099661 0.037145 5.192304 0.036939

Skewness -0.521612 1.717417 -5.028711 0.705108

Kurtosis 5.198717 10.70772 34.36123 6.116995

Jarque-Bera 14.80669 178.0175 2711.697 29.26092

Probability 0.000609 0.000000 0.000000 0.000000

Sum 1.152927 -0.049875 -28.99897 -0.660716

Sum Sq. Dev. 0.586010 0.081406 1590.641 0.080504

Observations 60 60 60 60

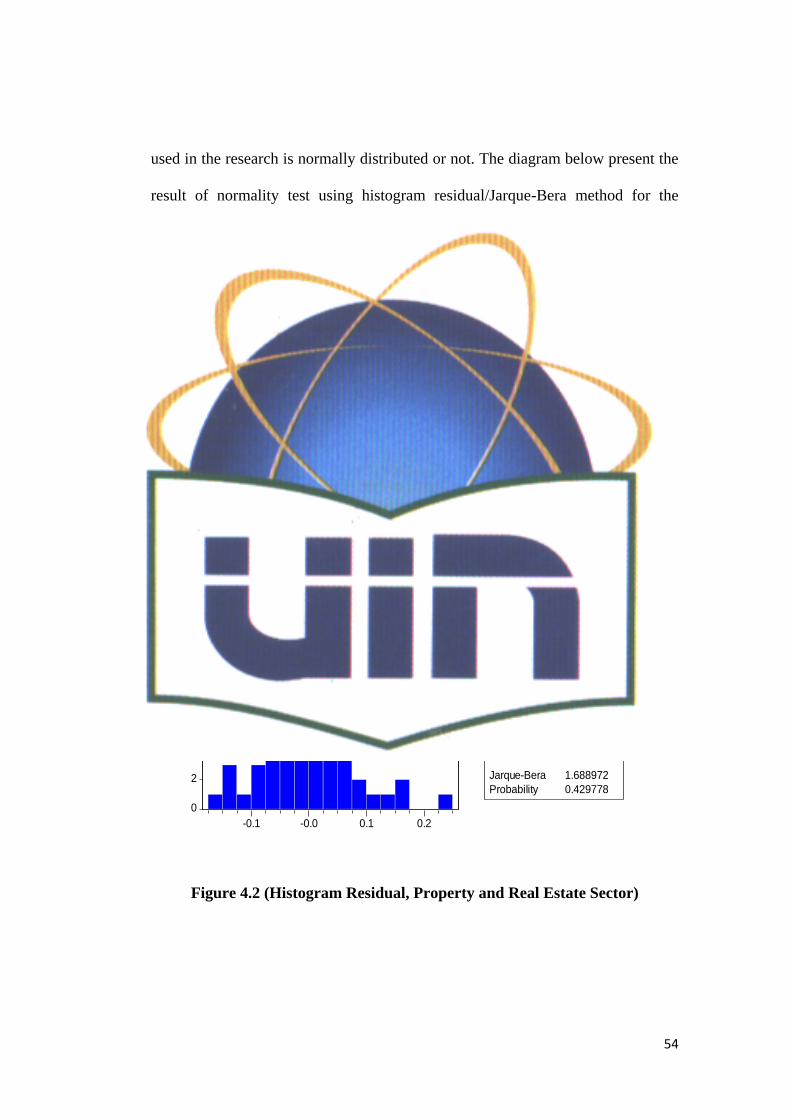

Normality Test

0

2

4

6

8

10

12

14

-0.1 -0.0 0.1 0.2

Series: Residuals

Sample 2006M01 2010M12

Observations 60

Mean 6.94e-19

Median 0.001880

Maximum 0.238803

Minimum -0.167392

Std. Dev. 0.079104

Skewness 0.363828

Kurtosis 3.382237

Jarque-Bera 1.688972

Probability 0.429778

1

CHAPTER 1

INTRODUCTION

A. Background

Investment is the commitment of money or capital to the purchase of

financial instruments or other assets so as to gain profitable returns in the form of

interest, income (dividends), or appreciation (capital gains) of the value of the

instrument (Sullivan,2003). It is related to saving or deferring consumption.

Investment is involved in many areas of the economy, such as business

management and finance no matter for households, firms, or governments.

Investment comes with the risk of the loss of the principal sum. The investment

that has not been thoroughly analyzed can be highly risky with respect to the

investment owner because the possibility of losing money is not within the

owner's control. The fundamental principle of investment‟s risk is the more risks

possible, the higher return we receive. The level of risk, especially in Indonesian

Capital Market is mainly affected by economics and political factors. Therefore,

to make an investment decision, investors need to be carefully analyzing the

investment‟s instrument they are most likely to choose. This analysis aims to

minimize the risk of the investment.

According to Bodi, Kane, and Marcus (2007, p.112) in their books “Investment”,

there are two types of risks that commonly faced by the investor when investing

2

their money; systematic and unsystematic risk. Interest rates, recession and wars

all represent sources of systematic risk because they affect the entire market and

cannot be avoided through diversification. While unsystematic risk is company or

industry specific risk that is inherent in each investment. Systematic risk can be

mitigated only by being hedged, while unsystematic risk can be reduced through

appropriate diversification.

Analyses of the financial markets are broadly divided between two schools of

thought; fundamental and technical analysis (Graham, et al: 1999). Fundamental

analysis is a method of evaluating the intrinsic value of a company, and hence the

share price, by researching and examining the corporate financial statements, the

business itself, industry outlook and so on. Conventional wisdom dictates that the

price of a stock that is trading for less than its intrinsic value should rise and the

price of a stock that is trading for higher than its intrinsic value should fall

(Chong, 2006). On the other hand, Technical analysis is a method of evaluating

future price of a stock based on statistical analysis of past behaviors of the stock.

Behaviors of stock include trading volume, moving averages, price trends and

other types of charts. Technical analysis assumes that the price chart frequently

anticipates news and other fundamental events before they become public

knowledge. It is used by market analysts to identify the beginning of an uptrend,

entry point, beginning of a downtrend and the exit point.

After the financial crisis hit Indonesia in 1998, the macroeconomic condition of

this country becomes unstable. The interest rate rose substantially and makes

3

investor prefers investing in the form of deposit rather than in stock market.

Inflation also rose and thus makes the exchange rate of Indonesian Rupiah to US

dollar dropped. On the article publish by daily news agency Reuters1, this

condition is likely to be happened again in 2008. This crisis is the effect resulted

from subprime mortgage case in US in 2007. The immediate cause or trigger of

the crisis was the Fed policy to decrease the interest rate which peaked in

approximately 2005–2006 (Lahart, 2007). Already-rising default rates on

"subprime" and adjustable rate mortgages (ARM) began to increase quickly

thereafter. As banks began to increasingly give out more loans to potential home

owners, the housing price also began to rise. In the optimistic terms the banks

would encourage the home owners to take on considerably high loans in the belief

they would be able to pay it back more quickly overlooking the interest rates.

Once the interest rates began to rise in mid 2007 the housing price started to drop

significantly in 2006 leading into 2007. In many states like California refinancing

became more difficult. As a result the number of foreclosed homes began to rise

as well.

The Global Financial Crisis brings a negative impact of other countries, and

Indonesia is one that is affected also. Based on the report publish by Bank

Indonesia, during this crisis, the exchange rates of Indonesian Rupiah to US dollar

1 Three top economists agree 2009 worst financial crisis since great depression;

risks increase if right steps are not taken. (February 29, 2009). Reuters.

Retrieved 2010-09-30, from Business Wire News database.

4

decline significantly to Rp 12,000/ US$. On October 9-10 2008, many stocks in

Jakarta Stock Exchange are being suspended because of market‟s overreaction. It

seems like the Financial Global Crisis will harm the economic conditions of a

country, as well as its stock market.

The unstable macroeconomic conditions could affect the stock price in a stock

market. According to Bodi, Kane, and Marcus (2007 P.226) in their books

“Investment” the macroeconomic factors that affect the stock price are; interest

rate, inflation, and exchange rate. The stock price that is influenced by the cyclical

factors such as stock on property and real estate industries will be affected more

than the stock price on the other industries that is not influenced by cyclical

factors, such as consumption goods industries.

The interest rate influences the choice of investment choosed by investor. The

raise of interest rate makes investor tend to invest their money in the form of

deposit, rather than in stock market which has higher risk. The higher rate of

interest will bring a negative significant effect to the property and real estate

sector because it depends on the mortgage. In contradictory, if the interest rates

fell, and the mortgage also fell, the willingness of investor to buy property is

raised. This happens in United States when the Fed decreases their interest rate

and triggers the people to buy houses with lower mortgage. This condition makes

the performance of property and real estate sector increase, because the amount of

houses sold are also increased. However, when the Fed increases back the interest

rate, it will leads to the failure of payment from the creditor, and this condition

5

makes the performance of the property and real estate sector declining.

Fundamentally, the decreasing performance of a company will lead to the

decreasing of its stock price in the stock market.

Inflation, as an unpredictable macroeconomic indicator also influences the

performance of the stock in the market. Inflation is the raise of overall goods and

services in an economy over period of time (Mankiw, 2007). The raise of overall

goods and services will create the declining demand of secondary and tertiary

product, such as property and real estate, because the people will try to fulfill their

basic needs first. This makes the stock price on property and real estate sector will

be more affected than the stock price on consumption goods, theoretically.

The exchange rate of Indonesian Rupiah to US Dollar depreciated when the crisis

occurred. This condition caused a huge damage to major industries in Indonesia,

especially for those who finance their company by borrowing fund from foreign

country. They have to pay more for their debt and this will make the performance

of their company weaken and thus make their stock prices decrease. Exchange

rate also influences the foreign investor‟s decision to invest their money in

Indonesian stock market. Foreign investors are allowed to invest their money in

certain limitation. When the exchange rates change, foreign investor must rethink

their decision to invest carefully and this will influence the stock price as a whole.

As the condition described above, this research try to examine the macroeconomic

factors, especially interest rate, inflation, and exchange rate, that will influence the

stock performance, both for stock which influenced much by cyclical factors, and

6

stock which less influenced by cyclical factors. This research aims to help investor

to make the best decision regarding the choice of stocks when the economic

condition is unstable.

B. Problem Formulation

A country‟s capital market plays a significant role in determining the

growth of that particular country. There are many research conducted in various

countries, using various types of data to prove that theory, which later will be

explored on the next part of this research. But so far the result of this study is still

inconclusive. Every market is different and dynamic and that makes some

researches resulted in the opposite way of theory. The choice of method analysis

also influences the result of the research. Therefore, the writer desires to prove the

negative effect of macroeconomic factors, such as interest rate, inflation, and

exchange rate to the stock return in Indonesia‟s capital market.

This research chooses the property and real estate sector and consumer goods

sector as the object of research. The reason behind this choice is because both

sectors differ in terms of the level of cyclical factors‟ influence. Consumer goods

are become the sample of this research because this sector are less likely to be

influenced by cyclical factors so it can be a good comparator to the property and

real estate sector, which is considerably more influenced by cyclical factors.

Based on the two factors, we will see how macroeconomics variables affect the

performance of the stock on consumption goods sector and property and real

estate sectors.

7

Based on the consideration above, this research aims to answer these following

questions:

1. How the interest rate, inflation, and exchange rate are influences the

performance of a stock on consumption goods and property and real estate

sector in Indonesia stock exchange?

2. How much the influence of interest rate, inflation, and exchange rate

affected the performance of stock on consumption goods and property and

real estate sector in Indonesia stock exchange?

C. Research Objectives

The objectives of this research are:

1. To identify the influence of interest rate, inflation, and exchange rate to the

performance of stock on consumption goods sector and property and real

estate sector in Indonesia stock exchange.

2. To determine the extent to which interest rate, inflation and exchange rate

influence the performance of stock on consumption goods sector and

property and real estate sector in Indonesia stock exchange.

D. Usefullness of the Research

In general, this research is expected to provide the significant contribution to

investors especially the individual investors to have new insights regarding the

8

perfect time to invest in the capital market given a current macroeconomic

circumstances. This eventually will help investor in obtaining their investments‟ risks

manageable, which eventually will help in the improvement of the social economics

circumstances. Specifically, the benefits of research is diveded into three scope of

areas, which are:

1. For the Author

As for the author, this research is expected to enrich the author‟s

knowledge about investment in capital market, as well as macroeconomic

knowledges. This reserach is also expected to become a medium to

implement lessons learned during the author‟s study in the university.

2. For the Investor

As for the investor, this research attempts to help investor in increasing

their knowledge about macroeconomic condition before they choose to

invest in the capital market. By examining the condition, investors could

forecast their return in capital market. Thus, this is expected to help

investor minimize the risk of their investmrnt.

3. For academic purposes

This research aims to add the literature study for investor who wishes to

know the influence of macroeconomic factors, such as interest rate,

inflation, and exchange rate to the rate of return in consumption good

stocks and property and real estate stock. This study can be used as a

consideration before selecting the most appropriate stock for investor.

Also, This research aims to add understanding for other researcher who

wishes to do research in the same field of study.

9

CHAPTER 2

LITERATURE REVIEW

A. Fundamental of Capital Market

1. History of Indonesian Capital Market

The capital market in Indonesia has actually existed long before the

Independence of Indonesia. The first stock exchange in Indonesia was established

on 1912 in Batavia during the Dutch colonial era. At that time, the exchange was

established for the interest of the Dutch East Indies (VOC).

During that era, the capital market grew gradually, and even became inactive for a

period of time due to various conditions, such as the World War I and II, power

transition from the Dutch government to Indonesian government, etc.

Indonesian government reactivated its capital market in 1977, and it grew rapidly

ever since, along with the support of incentives and regulations issued by the

government.

The milestone of Indonesian capital market occurred in 2007, where Surabaya

Stock Exchange merged with Jakarta Stock Exchange and thus change the name

to become Indonesia Stock Exchange (IDX). This merger is expected to boost the

performance of Indonesian capital market in the future2.

2 www.bapepam.go.id

10

2. Capital Market Definition

The Capital Market is a market for several long-term investment

instruments which can be traded, whether in the form of debt or self-own capital

(equity) (Darmadji and Hendy, 2001). Capital market enables corporations to

issue the security in the form of certificate of indebtedness (bond) or the

certificate of ownership (stock). Through the existence of capital market, this

would be possible for the parties who has surplus of fund (lender) to move their

fund to another parties who are deficit in fund (borrower). The parties who have

the surplus of fund can invest their money to the parties who are deficit with the

expectation to get the return, while the issuer (in this case the corporate) can

utilize the fund for its interest to make its business growth without depending on

the operational activity of the corporate.

Capital market has many advantages which can be categorized as economic

advantage and financial advantage. On the economic side, capital market is

expected to boost economic activity because capital market is becoming a funding

alternative for the corporations so that the corporations can operate in the higher

scale which eventually can increase its revenue and prosperity of the society.

While in the financial side, capital market is expected to become the source of

financing (long term) for the corporations and enable investor to diversify its

investment.

3. Capital Market Instrument

Stock exchange instrument consist of promissory notes that can be traded

through the stock exchange. Capital market instruments which currently traded at

11

Indonesia Stock Exchange (IDX) are classified into three types; stocks, bonds, and

rights3.

a) Stock

The capital stock of a business entity represents the original capital paid

into or invested in the business by its founders. Stock typically takes the

form of shares of either common stock or preferred stock. As a unit of

ownership, common stock typically carries voting rights that can be

exercised in corporate decisions. They include the right to receive dividend

payments typically from earnings, if authorized by the board of directors

and the power to sell the stock (liquidity rights) and realize capital gains

on public trading markets or in private transactions. On the other hand,

preferred stock differs from common stock in that it typically does not

carry voting rights but is legally entitled to receive a certain level of

dividend payments before any dividends can be issued to other

shareholders.

b) Rights

Rights are the right given to the old shareholder to buy new additional

shares issued by a particular company.

3 www.idx.co.id

12

c) Bond

Bond is a debt security, in which the authorized issuer owes the holders a

debt and, depending on the terms of the bonds, is obliged to pay interest

(the coupon) and/or repay the principal at later date, termed maturity. A

bond is a formal contract to repay borrowed money with interest at fixed

intervals.

B. Investment

Investment is putting money into something with the hope of profit. More

specifically, investment is the commitment of money or capital to the purchase of

financial instruments or other assets so as to gain profitable returns in the form of

interest, income (dividends), or capital gain appreciation of the value of the

instrument (Sullivan, 2003). It is related to saving or deferring consumption.

Investment is involved in many areas of the economy, such as business

management and finance no matter for households, firms, or governments. An

investment involves the choice by an individual or an organization, such as a

pension fund, after some analysis or thought, to place or lend money in a vehicle,

instrument or asset, such as property, commodity, stock, bond, financial

derivatives (e.g. futures or options), or the foreign asset denominated in foreign

currency, that has certain level of risk and provides the possibility of generating

returns over a period of time (Graham et al., 1991).

Investor usually assesses their risk before making an investment decision. They

assess the expected profitability return they will earn from the investment. In the

practice, not all of the expected returns in the future match the prediction of the

13

investor. There are many factors that make investment‟s return somehow

unpredictable. Because of these factors, investor needs to make a comprehensive

analysis before they make an investment decision to minimize the risks. The

analysis could be a fundamental analysis or technical analysis.

Generally, there are two different styles and types of investors that exist in the

stock market; investors use the stock market to build their investment portfolio so

that they can see a long term profit that takes place over a long period of time, and

investor who just using the stock market to make money quickly for a short period

of time, which is called a "trader". The first type of investor has a short term

orientation while the second type has a long term orientation.

Investor in capital market must analyze the factors that could influence the change

of stock price. Stock prices definitely change over the course of time. Some can

increase rapidly and make investors a fortune, whereas others can lose a lot of

value quickly and bankrupt investors. Stock prices change because of the

economics of market forces, and the supply and demand for the stock (Coleman,

2006). This is all based on personal perception. If people think that a company

will do better in the future, this will raise the demand and price of the stock, and if

they think a company will do worse, this will lower the demand and price of the

stock.

The change of stock price is influenced by many factors. Some studies have

concluded that company fundamentals such as earning and valuation multiple are

major factors that affect stock prices. Other indicated that inflation, economic

conditions, investor behavior, the behavior of the market and liquidity, are the

14

most influencing factors of stock prices (Bodie, 2007). News or information also

affects the change in stock price. Positive news about a company can increase

buying interest in the market while a negative press release can ruin the prospect

of a stock. Nevertheless, investor could not only rely on the news when

attempting to predict stock price. It is the overall performance of the company

that matters more than news. It is always wise to take a wait and watch policy in a

volatile market or when there is mixed reaction about a particular stock.

In capital market, there is term named „market efficiency concept‟ which

mentions the degree to which stock prices reflect all available and relevant

information. In 1900, Louis Bachelier made an important contribution to the

formalism of classical economics with a theory that says trading strategies based

only on observed price changes cannot succeed. Markets are moved by news and

since, by definition, news cannot be predicted (or it would not be news), price

movement cannot be anticipated. Consequently, price data are not linked and price

series follow a geometric Brownian random walk, whereby market prices are log-

normal distributed, i.e. the differences of the logarithms of prices are Gaussian

distributed.

There are three categories of market efficiency concept (Elton, et al: 2007)

1. Weak Form Efficiency: In this form of market efficiency, no investor can

earn excess returns by developing trading rules based solely on historical

price or return information.

15

2. Semi-Strong Form Efficiency: In this form of market efficiency, no

investor can earn excess returns from using trading rules based on any

publicly available information.

3. Strong Form Efficiency: In this form of efficiency, no investor can earn

excess returns using any information whether publicly available or not.

As every casual follower of financial news knows, stock prices rise and fall in

response to earnings and revenues (Yee, 2001). Positive information regarding

expected Earnings per Share (EPS) will boost the stock price and vice versa.

C. Stock Rate of Return

Capital Market Theory explains the behavior of investor in making an

investment decision. Investor will consider two most important factors when

making an investment decision; risk and return. A stock‟s rate of return is gained

from the dividend paid annually or capital gain or margin from the purchase-sell

activity.

Chris Brooks (2002 p.154) in his book, Introductory of Econometrics for Finance

explain two methods in calculating return gained from capital gain margin; simple

return and continuously compounded returns. The formula of each method is as

follows:

Simple returns:

(2.1)

16

Continuously compounded return

(2.2)

Where,

Rt = Simple returns on t period

rt = Continuously compounded returns on t period

Pt = Stock Price on t period

Pt-1 = Stock Price on t-1 period

Investor will make an investment decision to buy a particular stock if a stock‟s

rate of return forecasted to be increased in the future. In this condition, investor

will gained more return than they‟re required rate of return. When a stock‟s return

is predicted to up, it will increase the demand from investor to that particular stock

and automatically increase the stock price. On the other hand, when a stock‟s

return is predicted to decrease, it will also decrease the demand from investor to

that particular stock and resulted in the decrease of stock price as well. Investor

will tend to sell the stocks which not meet their required rate of return. Here we

can see a linear correlation between a stock‟s rate of return and stock‟s price.

D. Risks

Despite considering a stock‟s return, investor who wishes to invest their

money on capital market must also define the risk of the stock. In one definition,

"risks" are simply future issues that can be avoided or mitigated, rather than

17

present problems that must be immediately addressed (Hubbard, 2009). While

others said that risk is the uncertainty about rate of return in the future (Bodie et

al: 2007). Risks that faced by investors are strongly related to the fluctuation of

stock price. According to Yan Yee Chong (2006, p. 75) in his books Investment

Risk Management, risks are classified into several types:

a. Business Risk

Business risk is the potential for loss of value through competition,

mismanagement, and financial insolvency. There are a number of

industries that are predisposed to higher levels of business risk (airlines,

railroads, steel, etc).

b. Credit and Country Risk

Credit risk is the risk that firm unable to deal with its obligations, and

therefore the asset will become unprofitable. Country risk refers to the risk

that a country will change the rules under which its financial system

operates in some way that affects that country‟s native financial instrument

and assets; country risk is also known as political risk.

c. Interest

The raise of interest rate will decrease the demand of stocks investment

because people will prefer to invest in the form of deposits. This resulted

in the decreasing of stock price.

d. Market Risk

Market risk is risk associated with daily fluctuations in stock price. Market

risk is also referred to as volatility; assets with high volatility (market risk)

18

are likely to fluctuate greatly in stock price, whereas assets with low

volatility are more immune to fast, large price changes. Volatility is

important in the stock world for a variety of reasons. The more volatile a

stock, the more potential for profit there may exist (which is why some

investors focus on identifying growth stocks, which have the capability for

explosive growth), but at the same time, there is also the possibility of

dramatic loss. The less volatile the investment, the less on average the

return will be to that investment.

e. Liquidity Risk

The final type of risk associated with stock market transactions is liquidity

risk. Liquidity risk refers to risk that the stock will not be able to be traded

fast enough to avoid or loss or capitalize on a potential profit. Liquidity

risk can be avoided by making sure the daily volume of share trading is

above a certain level.

Generally, risk is calculated by the deviation of the actual return from the required

rate of return (expected return) as a result of success/failure of an investment. Risk

of a stock can be measured by its variance or standard deviation. With the risk of

uncertainty, investors not only need to calculate the return of a stock but also the

risks associated with it.

There are two types of risks that commonly faced by the investor when investing

their money; systematic and unsystematic risk. Interest rates, recession and wars

all represent sources of systematic risk because they affect the entire market and

cannot be avoided through diversification. While unsystematic risk is company or

19

industry specific risk that is inherent in each investment. Systematic risk can be

mitigated only by being hedged, while the amount of unsystematic risk can be

reduced through appropriate diversification.

E. Inflation

In economics, inflation is a rise in the general level of prices of goods and

services in an economy over a period of time (Blanchard, 2000). The rise of

general prices of goods and services does not merely caused inflation if it is only

happen in a moment of time. Therefore, inflation is at least measured by monthly

basis. If in one month the rise of general price of goods and services are

continuously, a country can be claimed to have an increase in inflation rate.

Inflation rate is the percentage change in the price index from the preceding

period (Mankiw, 2007). Another longer period to measure inflation is by yearly,

or quarter-yearly basis. Still According to Mankiw in his books, Theory of

Macroeconomic, there are several macroeconomic indicators that can be used to

measure an inflation rate within a period;

a. Consumer Price Index (CPI)

The consumer price index is a measure of the overall costs of the goods

and services brought by a typical consumer. Inflation rate can be measured

by applying the following formula:

(2.3)

b. Wholesale Price Index

20

If consumer price index measure inflation rate from the perspective of the

consumers, wholesale price index measure inflation rate from the

perspective of the producers. Wholesale price index measures the cost of a

basket of goods and services. Inflation rate can be measured by applying

the following formula:

(2.4)

c. GDP Deflator

Two previously discussed indicators have some limitation in measuring

inflation rate. Both indicators only measure some goods and services in

some cities, and it does not reflect the overall goods and services produced

and consumed within a country. Therefore, economist uses GDP deflator

to measure inflation rate more precisely. GDP Deflator is the ratio of

nominal GDP to real GDP. Because nominal GDP is current output valued

at current prices and real GDP is current output valued at base-year prices,

GDP deflator reflects the current level of prices relatives to the level of

prices in the base year. Interest rate calculation using GDP deflator can be

measured as follows:

21

(2.5)

Theoretically, inflation has a negative relationship with the stock return. This

phenomenon is caused by:

a. Cost-push inflation

When the cost of production increases, a company‟s ability to fulfill the

demand from the customer is decrease. This will cause an aggregate

supply. Aggregate supply is the total volume of goods and services

produced by an economy at a given price level. When there is a decrease

in the aggregate supply of goods and services stemming from an increase

in the cost of production, cost-push inflation occurred. Cost-push inflation

basically means that prices have been “pushed up” by increases in costs of

any of the four factors of production (labor, capital, land or

entrepreneurship) when companies are already running at full production

capacity. With higher production costs and productivity maximized,

companies cannot maintain profit margins by producing the same amounts

of goods and services. As a result, the increased costs are passed on to

consumers, causing a rise in the general price level (inflation).

b. Demand-pull inflation

Demand-pull inflation occurs when there is an increase in aggregate

demand, categorized by the four sections of the macroeconomic:

households, businesses, governments and foreign buyers. When these four

22

sectors concurrently want to purchase more output than the economy can

produce, they compete to purchase limited amounts of goods and services.

1. Relationship between inflation and stock return

Inflation influences the purchasing power of the individuals in some

extend. Brealey and Meyer (2000) exposes that inflation has a negative

inlfluences to the stock performance in capital market. When inflation rate

increase, the price of overall goods and services increase as well. Thus will make

individuals loose their ability to invest in capital market. They prefer to fulfill

their basic needs first before making an investment. The capital matket will suffer

because of this condition. The price of overall stocks in the capital market will

decrease and thus make the return of the stock decrease as well.

F. Interest Rate

According to Mankiw (2007, p. 297), an interest rate is the rate at which

interest is paid by a borrower for the use of money that they borrow from a lender.

It is consist of two types, real and nominal interest rate. In finance and economics

nominal interest rate or nominal rate of interest refers to the rate of interest before

adjustment for inflation (in contrast with the real interest rate); or, for interest

rates "as stated" without adjustment for the full effect of compounding (also

referred to as the nominal annual rate). An interest rate is called nominal if the

frequency of compounding (e.g. a month) is not identical to the basic time unit

(normally a year). The "real interest rate" is approximately the nominal interest

23

rate minus the inflation rate. It is the rate of interest an investor expects to receive

after subtracting inflation.

The relationship between real and nominal interest rates can be described in the

equation (Brealey and Meyer, 2000)

( )( ) ( )

(2.6)

Where r is the real interest rate, i is the inflation rate, and R is the nominal interest

rate.

1. Relationship between interest rate and stock return

Interest rate are important variables in for macroeconomic to understand

because they link the economy of the present and the economy of the future

through their effects on saving and investment (Mankiw, 2007 p.369). Keynes

reanalyzed about the effect of interest rate on investment decision. The increase of

interest rate could increase the exchange rate, but this can make the price of stock

decrease. Keynes also stated the negative relationship between interest rate and

stock price. This happen because if the interest rate increases, people tend to

invest their money in the form of deposit, and thus make investment in capital

market weakened.

The relationship between interest rate and investment decision also explained by

Fisher in his Theory of Investment(1930). Through the IS and LM curve, if the

24

interest rate increase, the cost of investment will increase and thus make

company‟s profit decrease. A decrease in profit will make a dividend for the

stockholder decrease too, which affected the stock price to be decreasing as well.

2. SBI (Bank Indonesia Certificate) Rate

In the past two centuries, interest rates have been variously set either by

national governments or central banks. In Indonesia, the interest rate is set by the

Central Bank of Indonesia, namely BI rate. The SBI Rate is announced by the

Board of Governors of Bank Indonesia in each monthly Board of Governors

Meeting. It is implemented in the Bank Indonesia monetary operations conducted

by means of liquidity management on the money market through SBI Rate to

achieve the monetary policy operational target.

The monetary policy operational target is reflected in movement in the Interbank

Overnight (O/N) Rate. It is then expected that bank deposit rates will track the

movement in interbank rates, with bank lending rates following suit.

While other factors in the economy are also taken into account, Bank Indonesia

will normally raise the BI Rate if future inflation is forecasted ahead of the

established inflation target. Conversely, Bank Indonesia will lower the BI Rate if

future inflation is predicted below the inflation target.

The benchmark interest rate in Indonesia was last reported at 6.50 percent. In

Indonesia the interest rate decisions are taken by The Central Bank of Republic of

Indonesia. The official interest rate is the Discount rate. This is the rate at which

25

central banks lend or discount eligible paper for deposit money banks, typically

shown on an end-of-period basis. From 2005 until 2010, Indonesia's average

interest rate was 8.76 percent reaching an historical high of 12.75 percent in

December of 2005 and a record low of 6.50 percent in August of 2009. The graph

below represents the interest rate in Indonesia from December 2005 to August

2009.

Figure 2.1 (Indonesia Interest Rate)

G. Exchange Rate

According to Jeff Madura (2007, p.78), exchange rate between two

countries specifies how much one currency is worth in terms of the other. It is the

value of a foreign nation‟s currency in terms of the home nation‟s currency.

According to traditional approach, exchange rates lead stock prices. This approach

states that stock price is expected to lead exchange rate with a negative correlation

26

since a decrease in stock prices reduces domestic wealth, which leads to lower

domestic money demand and interest rates (Aydemir and Demirhan, 2009). Also,

the decrease in domestic stock prices leads foreign investors to lower demand for

domestic assets and domestic currency. These shifts in demand and supply of

currencies cause capital outflows and the depreciation of domestic currency. On

the other hand, when stock prices rise, foreign investors become willing to invest

in a country‟s equity securities. Thus, they will get benefit from international

diversification. This situation will lead to capital inflows and a currency

appreciation (Granger et al. 2000;Pan et al. 2007).

Exchange rates can affect stock prices not only for multinational and export

oriented firms but also for domestic firms. For a multinational company, changes

in exchange rates will result in both an immediate change in value of its foreign

operations and a continuing change in the profitability of its foreign operations

reflected in successive income statements. Therefore, the changes in economic

value of firm‟s foreign operations may influence stock prices. Domestic firms can

also be influenced by changes in exchange rates since they may import a part of

their inputs and export their outputs. For example, a devaluation of its currency

makes imported inputs more expensive and exported outputs cheaper for a firm.

Thus, devaluation will make positive effect for export firms (Aggarwal, 1981) and

increase the income of these firms, consequently, boosting the average level of

stock prices (Wu, 2000).

1. Relationship between exchang rate and stock return

27

Stock return will get effected by the fluctuation of exchange rate in a

country (Wu, 2000). When the exchange rate fluctuates, foreign investor

will get atrratcted to invest their money in capital market. Thus will make

the price of stock corrected.

H. Previous Research

In 2004, Maysami, et al. made a research about relationship between

selected macroeconomic variables and the Singapore Stock Market Index (STI),

as well as with various Singapore Exchange Sector Indices-the finance index, the

property index, and the hotel index. This research used VCEM model proposed by

Johansen(1990) which allows for testing cointegration in a whole system of

equations in one stop, without requiring a specific variable to be normalized. The

research‟s data is the monthly time-series which is obtained from the

PublicAccess Time-Series system, an online service by the Singapore Department

of Statistics. And the SES All-S Equities indicies figures are obtained from the

Singapore Statistics published by the Singapore Department of Statistics. The

study concludes that the Singapore‟s stock market and the property index form

cointegrating relationship with changes in the short and long-term interest rates,

industrial production, price levels, exchange rate and money supply

(macroeconomics variables).

Gay (2008) conducted a research about effect of macroeconomic variables on

stock market return for four emerging economies: Brazil, Russia, India and China.

The Box-Jenkins ARIMA model used to describe the relationship will use the

28

moving-averages at the one-month MA(1), three-month MA(3), six-month

MA(6), and twelve-month MA(12) for the lagged dependent of stock market price

and the two intervening variables of exchange rate and oil price. Available

monthly data for stock market price index, exchange rate, and oil price between

1999:03 to 2006:06 for Brazil, Russia, India, and China from the Organization for

Economic Cooperation and Development (OECD) is used in this study, which

will provide 90 observations per variable for each BRIC for a total of 1,080

observations. This study concludes that no significant relationship was found

between respective exchange rate and oil price (Macroeconomic variables) on the

stock market index prices of either BRIC country, this may be due to the influence

other domestic and international macroeconomic factors on stock market returns,

warranting further research. Also, there was no significant relationship found

between present and past stock market returns, suggesting the markets of Brazil,

Russia, India, and China exhibit the weak-form of market efficiency.

Wan Mahmood (2009) from Universiti Teknologi Mara Trengganu, Malaysia,

examine the dynamics relationship between stock prices and economic variables

in six Asian-Pacific selected countries of Malaysia, Korea, Thailand, Hong Kong,

Japan, and Australia. The monthly data on stock price indices, foreign exchange

rates, consumer price index and industrial production index that spans from

January 1993 to December 2002 are used. This study performed two cointegration

tests of Engle and Granger (1987) and Johansen and Juselius as his method. The

results indicate the existing of a long run equilibrium relationship between and

among variables in only four countries, i.e., Japan, Korea, Hong Kong and

29

Australia. As for short run relationship, all countries except for Hong Kong and

Thailand show some interactions. The Hong Kong shows relationship only

between exchange rate and stock price while the Thailand reports significant

interaction only between output and stock prices. An accurate estimation of these