Analysis of ISA 330 and Mapping Document · Analysis of ISA 330 and Mapping Document ... controls...

30

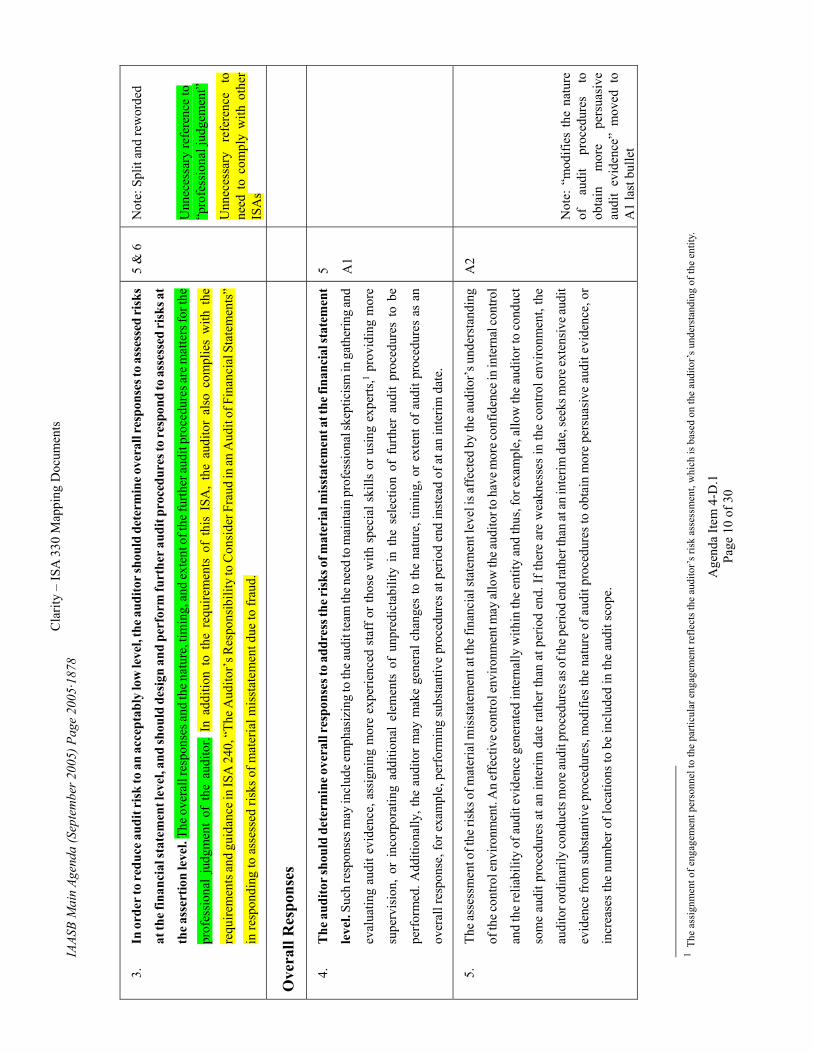

IAASB Main Agenda (September 2005) Page 2005·1869 Agenda Item 4-D.1 Prepared by: Michael Nugent (August 2005) Page 1 of 30 Analysis of ISA 330 and Mapping Document 1. Exhibit 1 sets out statements in ISA 330 that use the present tense to describe auditor actions, and the proposed treatment of whether the actions should be redrafted as a requirement, or redrafted to make clear that it is explanatory material. Paragraph references to extant ISA 330 and to the redrafted ISA 330 (shown in Agenda Item 4-D) are provided. 2. Exhibit 2 sets out extant ISA 330 and maps each of its paragraphs (which may have been reworded as necessary) to the redrafted ISA 330. The highlight material indicates sentences and paragraphs that are proposed to be deleted as part of the redrafting. An explanation of the proposed deletion and other comments are provided, where appropriate. Exhibit 1 Para Existing present tense statements Change to “shall” New para Rationale and comment 3 … the auditor also complies with the requirements and guidance in ISA 240, “The Auditor’s Responsibility to Consider Fraud in an Audit of Financial Statements” in responding to assessed risks of material misstatement due to fraud. No – Deleted as part of revised format 7 In designing further audit procedures, the auditor considers such matters as the following: • The significance of the risk. • The likelihood that a material misstatement will occur • The characteristics of the class of transactions, account balance, or disclosure involved. • The nature of the specific controls used by the entity and in particular whether they are manual or automated. • Whether the auditor expects to obtain audit evidence to determine if the entity’s controls are effective in preventing, or detecting and correcting, material misstatements. Yes No No Yes Yes Yes 6 – – 7(a)(i) 7(a) (ii) 7(a) (ii) These 2 dot points are very generic and are covered by new para 6. ) ) ) These considerations are ) essential in all cases to ) give effect to new para 7 ) ) ) 8 … the auditor needs to be satisfied that performing only substantive procedures for the relevant assertion would be effective in reducing the risk of material misstatement to an acceptably low level. … Irrespective of the approach selected, the auditor designs and performs substantive procedures for each material class of transactions, account balance, and disclosure as required by paragraph 49. No Yes – 18 & F/n 2 A restatement of the general principle of the ISA Repetition of existing “bold” requirement 9 … in addition to the matters referred to in paragraph 8 above, the auditor considers whether in the absence of controls it is possible to obtain sufficient appropriate audit evidence. No A5 Rephrased as a statement of fact, rather than appearing to impose an additional responsibility on SMSs

Transcript of Analysis of ISA 330 and Mapping Document · Analysis of ISA 330 and Mapping Document ... controls...

IAASB Main Agenda (September 2005) Page 2005·1869 Agenda Item

4-D.1

Prepared by: Michael Nugent (August 2005) Page 1 of 30

Analysis of ISA 330 and Mapping Document

1. Exhibit 1 sets out statements in ISA 330 that use the present tense to describe auditor actions, and the proposed treatment of whether the actions should be redrafted as a requirement, or redrafted to make clear that it is explanatory material. Paragraph references to extant ISA 330 and to the redrafted ISA 330 (shown in Agenda Item 4-D) are provided.

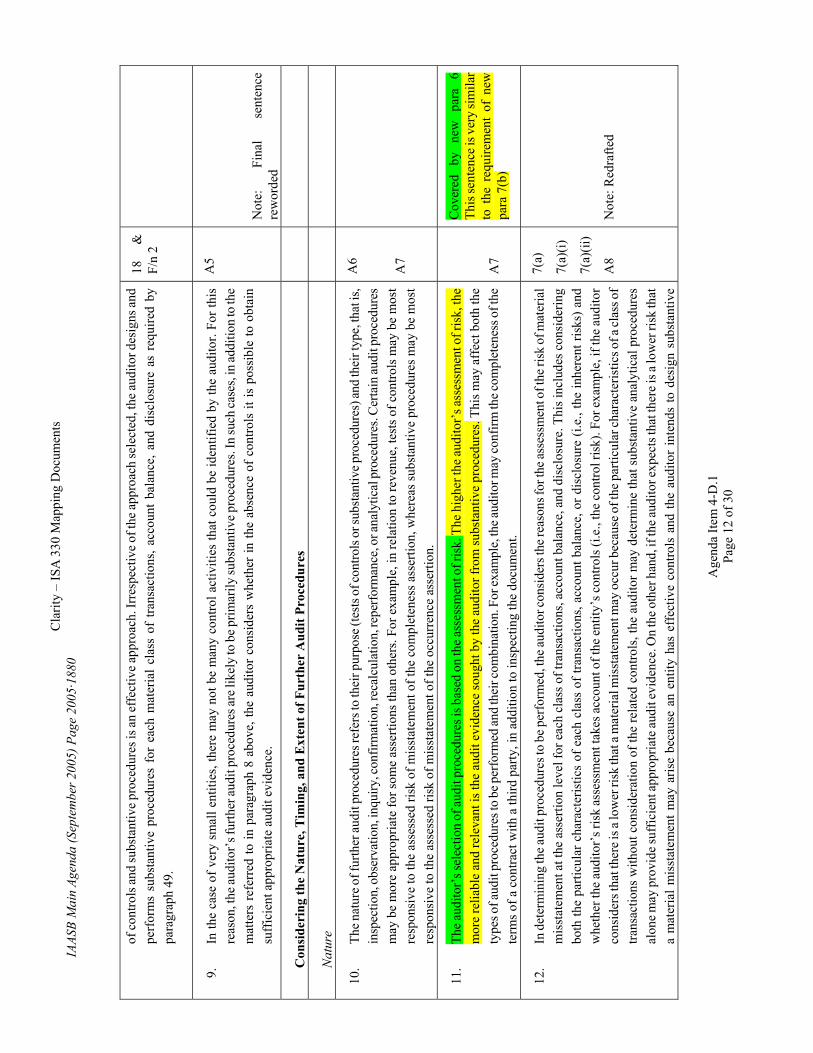

2. Exhibit 2 sets out extant ISA 330 and maps each of its paragraphs (which may have been reworded as necessary) to the redrafted ISA 330. The highlight material indicates sentences and paragraphs that are proposed to be deleted as part of the redrafting. An explanation of the proposed deletion and other comments are provided, where appropriate.

Exhibit 1

Para Existing present tense statements Change to

“shall”

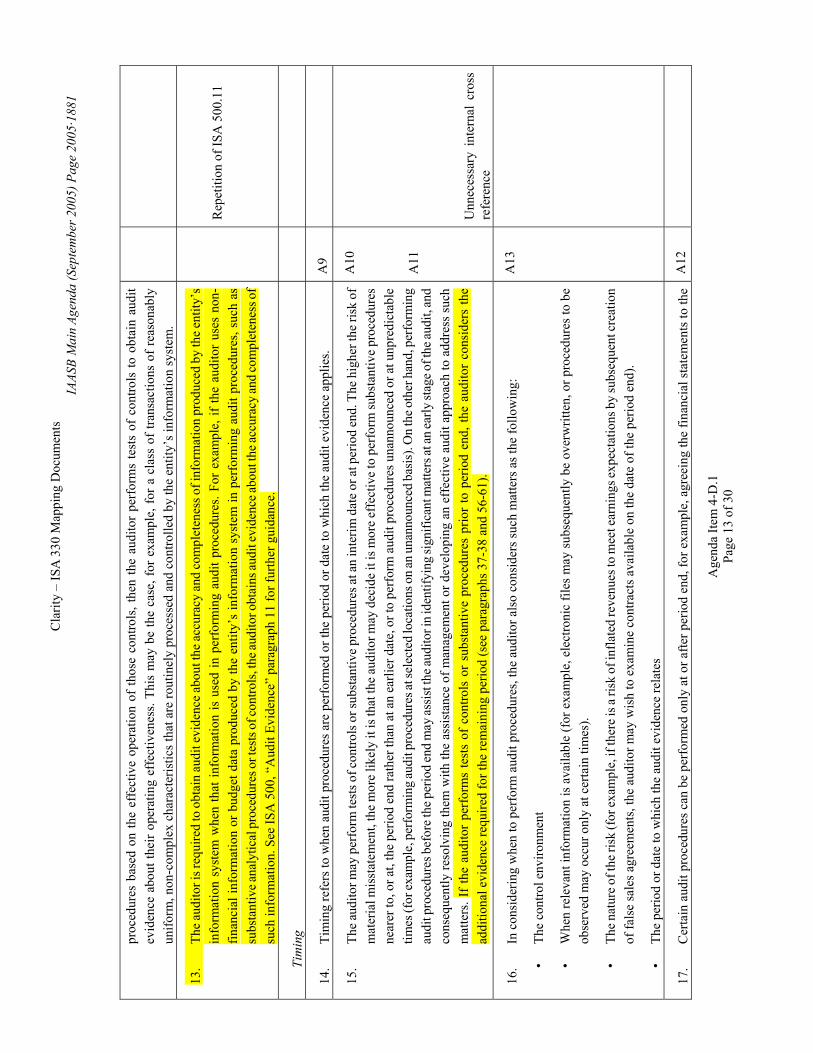

New para

Rationale and comment

3 … the auditor also complies with the requirements and guidance in ISA 240, “The Auditor’s Responsibility to Consider Fraud in an Audit of Financial Statements” in responding to assessed risks of material misstatement due to fraud.

No – Deleted as part of revised format

7 In designing further audit procedures, the auditor considers such matters as the following:

• The significance of the risk.

• The likelihood that a material misstatement will occur

• The characteristics of the class of transactions, account balance, or disclosure involved.

• The nature of the specific controls used by the entity and in particular whether they are manual or automated.

• Whether the auditor expects to obtain audit evidence to determine if the entity’s controls are effective in preventing, or detecting and correcting, material misstatements.

Yes

No

No

Yes

Yes

Yes

6

– – 7(a)(i)

7(a) (ii)

7(a) (ii)

These 2 dot points are very generic and are covered by new para 6.

) ) ) These considerations are ) essential in all cases to ) give effect to new para 7 ) ) )

8 … the auditor needs to be satisfied that performing only substantive procedures for the relevant assertion would be effective in reducing the risk of material misstatement to an acceptably low level. … Irrespective of the approach selected, the auditor designs and performs substantive procedures for each material class of transactions, account balance, and disclosure as required by paragraph 49.

No

Yes

–

18 & F/n 2

A restatement of the general principle of the ISA

Repetition of existing “bold” requirement

9 … in addition to the matters referred to in paragraph 8 above, the auditor considers whether in the absence of controls it is possible to obtain sufficient appropriate audit evidence.

No A5 Rephrased as a statement of fact, rather than appearing to impose an additional responsibility on SMSs

Clarity – ISA 330 Mapping Documents IAASB Main Agenda (September 2005) Page 2005·1870

Agenda Item 4-D.1 Page 2 of 30

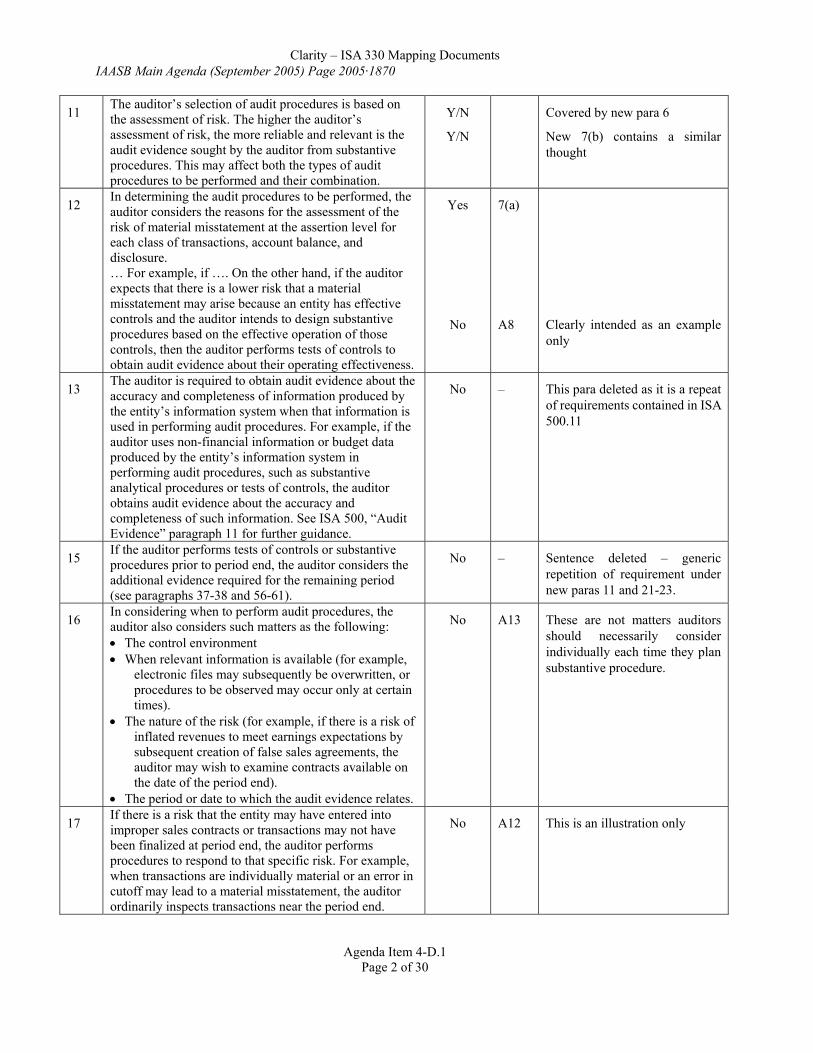

11 The auditor’s selection of audit procedures is based on the assessment of risk. The higher the auditor’s assessment of risk, the more reliable and relevant is the audit evidence sought by the auditor from substantive procedures. This may affect both the types of audit procedures to be performed and their combination.

Y/N

Y/N

Covered by new para 6

New 7(b) contains a similar thought

12 In determining the audit procedures to be performed, the auditor considers the reasons for the assessment of the risk of material misstatement at the assertion level for each class of transactions, account balance, and disclosure. … For example, if …. On the other hand, if the auditor expects that there is a lower risk that a material misstatement may arise because an entity has effective controls and the auditor intends to design substantive procedures based on the effective operation of those controls, then the auditor performs tests of controls to obtain audit evidence about their operating effectiveness.

Yes

No

7(a)

A8

Clearly intended as an example only

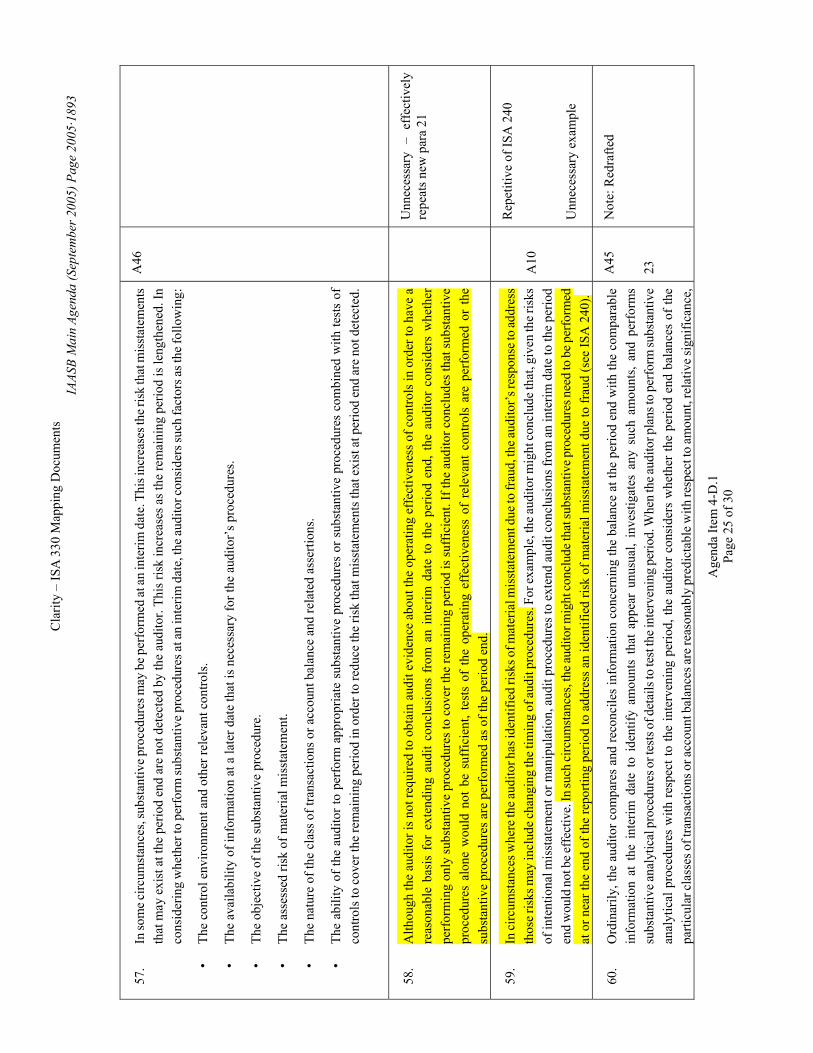

13 The auditor is required to obtain audit evidence about the accuracy and completeness of information produced by the entity’s information system when that information is used in performing audit procedures. For example, if the auditor uses non-financial information or budget data produced by the entity’s information system in performing audit procedures, such as substantive analytical procedures or tests of controls, the auditor obtains audit evidence about the accuracy and completeness of such information. See ISA 500, “Audit Evidence” paragraph 11 for further guidance.

No – This para deleted as it is a repeat of requirements contained in ISA 500.11

15 If the auditor performs tests of controls or substantive procedures prior to period end, the auditor considers the additional evidence required for the remaining period (see paragraphs 37-38 and 56-61).

No – Sentence deleted – generic repetition of requirement under new paras 11 and 21-23.

16 In considering when to perform audit procedures, the auditor also considers such matters as the following: • The control environment • When relevant information is available (for example,

electronic files may subsequently be overwritten, or procedures to be observed may occur only at certain times).

• The nature of the risk (for example, if there is a risk of inflated revenues to meet earnings expectations by subsequent creation of false sales agreements, the auditor may wish to examine contracts available on the date of the period end).

• The period or date to which the audit evidence relates.

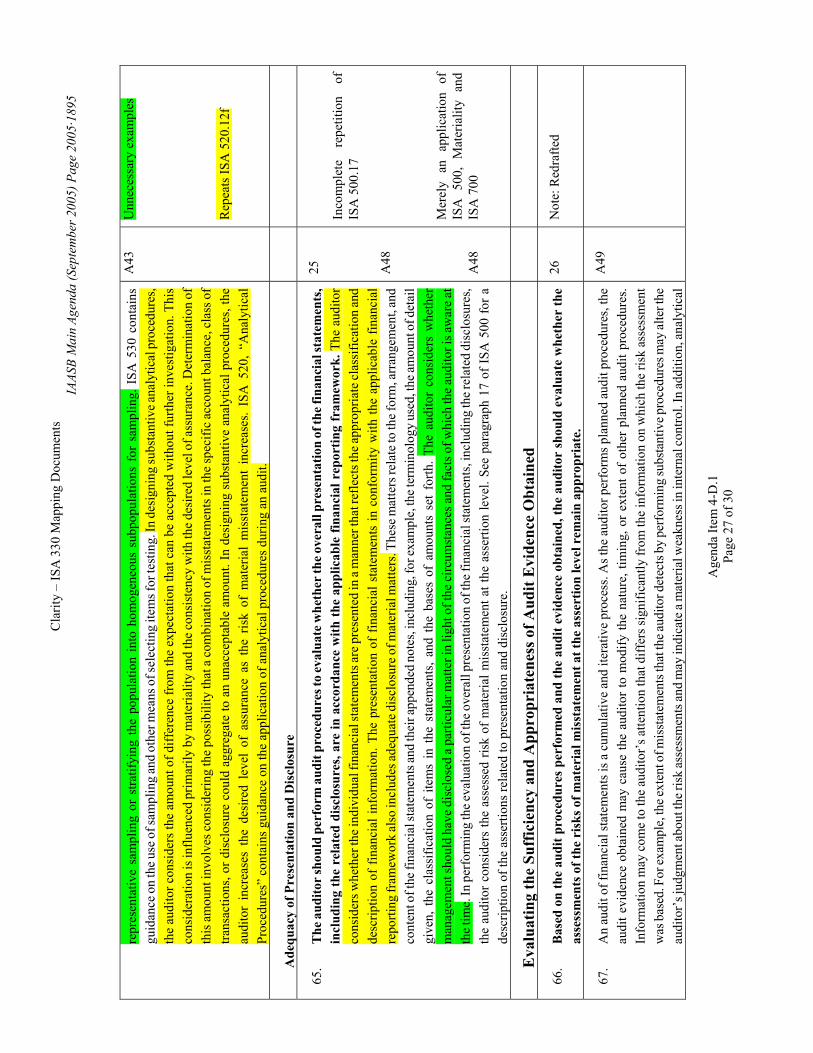

No A13 These are not matters auditors should necessarily consider individually each time they plan substantive procedure.

17 If there is a risk that the entity may have entered into improper sales contracts or transactions may not have been finalized at period end, the auditor performs procedures to respond to that specific risk. For example, when transactions are individually material or an error in cutoff may lead to a material misstatement, the auditor ordinarily inspects transactions near the period end.

No A12 This is an illustration only

Clarity – ISA 330 Mapping Documents IAASB Main Agenda (September 2005) Page 2005·1871

Agenda Item 4-D.1 Page 3 of 30

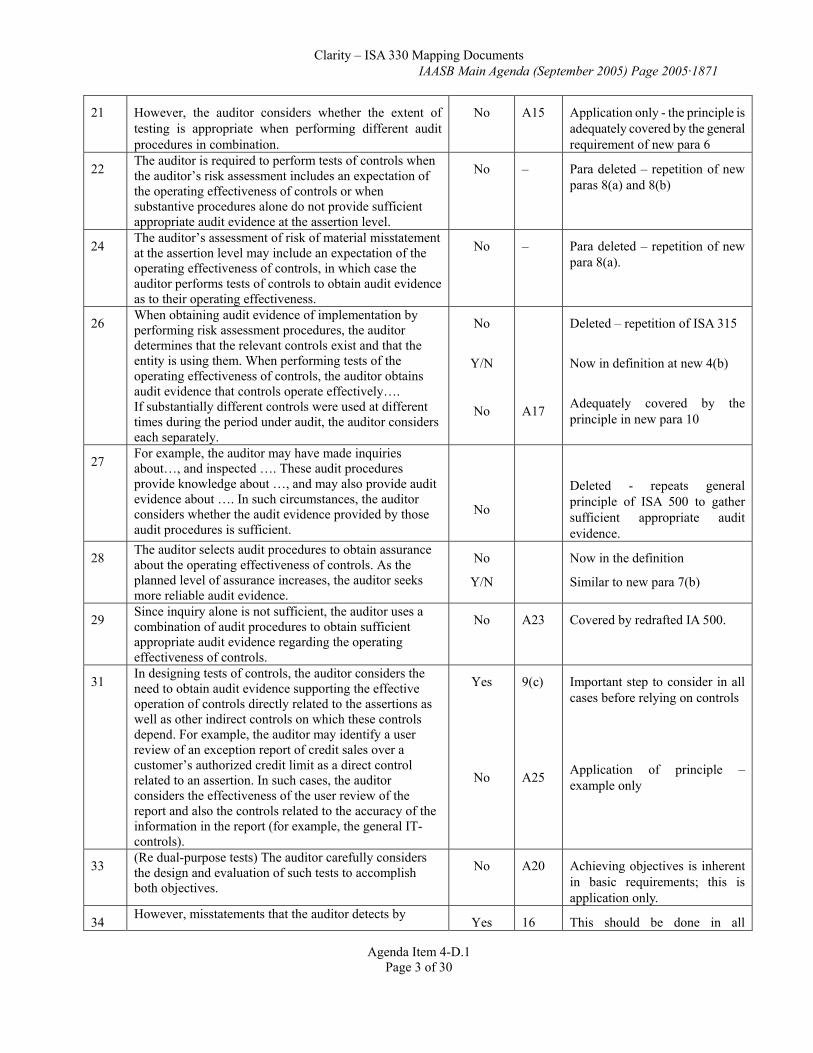

21 However, the auditor considers whether the extent of testing is appropriate when performing different audit procedures in combination.

No A15 Application only - the principle is adequately covered by the general requirement of new para 6

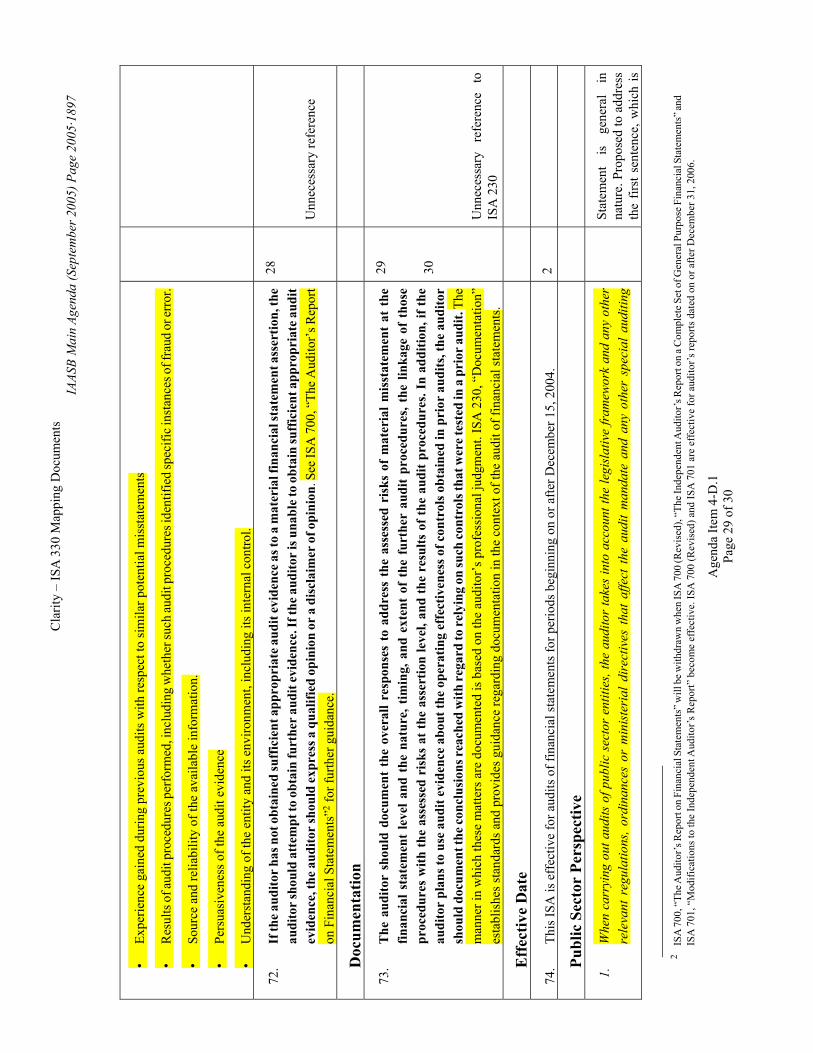

22 The auditor is required to perform tests of controls when the auditor’s risk assessment includes an expectation of the operating effectiveness of controls or when substantive procedures alone do not provide sufficient appropriate audit evidence at the assertion level.

No – Para deleted – repetition of new paras 8(a) and 8(b)

24 The auditor’s assessment of risk of material misstatement at the assertion level may include an expectation of the operating effectiveness of controls, in which case the auditor performs tests of controls to obtain audit evidence as to their operating effectiveness.

No – Para deleted – repetition of new para 8(a).

26 When obtaining audit evidence of implementation by performing risk assessment procedures, the auditor determines that the relevant controls exist and that the entity is using them. When performing tests of the operating effectiveness of controls, the auditor obtains audit evidence that controls operate effectively…. If substantially different controls were used at different times during the period under audit, the auditor considers each separately.

No

Y/N

No

A17

Deleted – repetition of ISA 315

Now in definition at new 4(b)

Adequately covered by the principle in new para 10

27 For example, the auditor may have made inquiries about…, and inspected …. These audit procedures provide knowledge about …, and may also provide audit evidence about …. In such circumstances, the auditor considers whether the audit evidence provided by those audit procedures is sufficient.

No

Deleted - repeats general principle of ISA 500 to gather sufficient appropriate audit evidence.

28 The auditor selects audit procedures to obtain assurance about the operating effectiveness of controls. As the planned level of assurance increases, the auditor seeks more reliable audit evidence.

No

Y/N

Now in the definition

Similar to new para 7(b)

29 Since inquiry alone is not sufficient, the auditor uses a combination of audit procedures to obtain sufficient appropriate audit evidence regarding the operating effectiveness of controls.

No A23 Covered by redrafted IA 500.

31 In designing tests of controls, the auditor considers the need to obtain audit evidence supporting the effective operation of controls directly related to the assertions as well as other indirect controls on which these controls depend. For example, the auditor may identify a user review of an exception report of credit sales over a customer’s authorized credit limit as a direct control related to an assertion. In such cases, the auditor considers the effectiveness of the user review of the report and also the controls related to the accuracy of the information in the report (for example, the general IT-controls).

Yes

No

9(c)

A25

Important step to consider in all cases before relying on controls

Application of principle – example only

33 (Re dual-purpose tests) The auditor carefully considers the design and evaluation of such tests to accomplish both objectives.

No A20

Achieving objectives is inherent in basic requirements; this is application only.

34 However, misstatements that the auditor detects by Yes 16 This should be done in all

Clarity – ISA 330 Mapping Documents IAASB Main Agenda (September 2005) Page 2005·1872

Agenda Item 4-D.1 Page 4 of 30

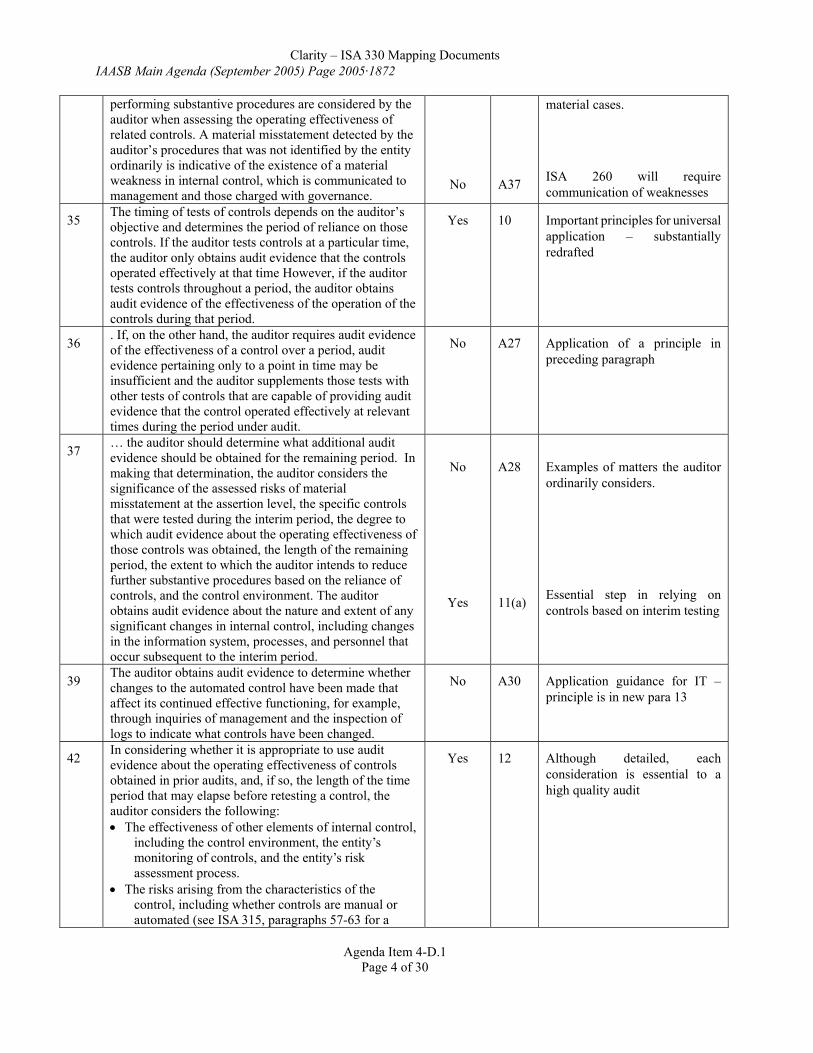

performing substantive procedures are considered by the auditor when assessing the operating effectiveness of related controls. A material misstatement detected by the auditor’s procedures that was not identified by the entity ordinarily is indicative of the existence of a material weakness in internal control, which is communicated to management and those charged with governance.

No

A37

material cases.

ISA 260 will require communication of weaknesses

35 The timing of tests of controls depends on the auditor’s objective and determines the period of reliance on those controls. If the auditor tests controls at a particular time, the auditor only obtains audit evidence that the controls operated effectively at that time However, if the auditor tests controls throughout a period, the auditor obtains audit evidence of the effectiveness of the operation of the controls during that period.

Yes 10 Important principles for universal application – substantially redrafted

36 . If, on the other hand, the auditor requires audit evidence of the effectiveness of a control over a period, audit evidence pertaining only to a point in time may be insufficient and the auditor supplements those tests with other tests of controls that are capable of providing audit evidence that the control operated effectively at relevant times during the period under audit.

No A27 Application of a principle in preceding paragraph

37 … the auditor should determine what additional audit evidence should be obtained for the remaining period. In making that determination, the auditor considers the significance of the assessed risks of material misstatement at the assertion level, the specific controls that were tested during the interim period, the degree to which audit evidence about the operating effectiveness of those controls was obtained, the length of the remaining period, the extent to which the auditor intends to reduce further substantive procedures based on the reliance of controls, and the control environment. The auditor obtains audit evidence about the nature and extent of any significant changes in internal control, including changes in the information system, processes, and personnel that occur subsequent to the interim period.

No

Yes

A28

11(a)

Examples of matters the auditor ordinarily considers.

Essential step in relying on controls based on interim testing

39 The auditor obtains audit evidence to determine whether changes to the automated control have been made that affect its continued effective functioning, for example, through inquiries of management and the inspection of logs to indicate what controls have been changed.

No A30 Application guidance for IT – principle is in new para 13

42 In considering whether it is appropriate to use audit evidence about the operating effectiveness of controls obtained in prior audits, and, if so, the length of the time period that may elapse before retesting a control, the auditor considers the following: • The effectiveness of other elements of internal control,

including the control environment, the entity’s monitoring of controls, and the entity’s risk assessment process.

• The risks arising from the characteristics of the control, including whether controls are manual or automated (see ISA 315, paragraphs 57-63 for a

Yes 12 Although detailed, each consideration is essential to a high quality audit

Clarity – ISA 330 Mapping Documents IAASB Main Agenda (September 2005) Page 2005·1873

Agenda Item 4-D.1 Page 5 of 30

discussion of specific risks arising from manual and automated elements of a control).

• The effectiveness of general IT-controls. • The effectiveness of the control and its application by

the entity, including the nature and extent of deviations in the application of the control from tests of operating effectiveness noted in prior audits.

• Whether the lack of a change in a particular control poses a risk due to changing circumstances.

• The risk of material misstatement and the extent of reliance on the control.

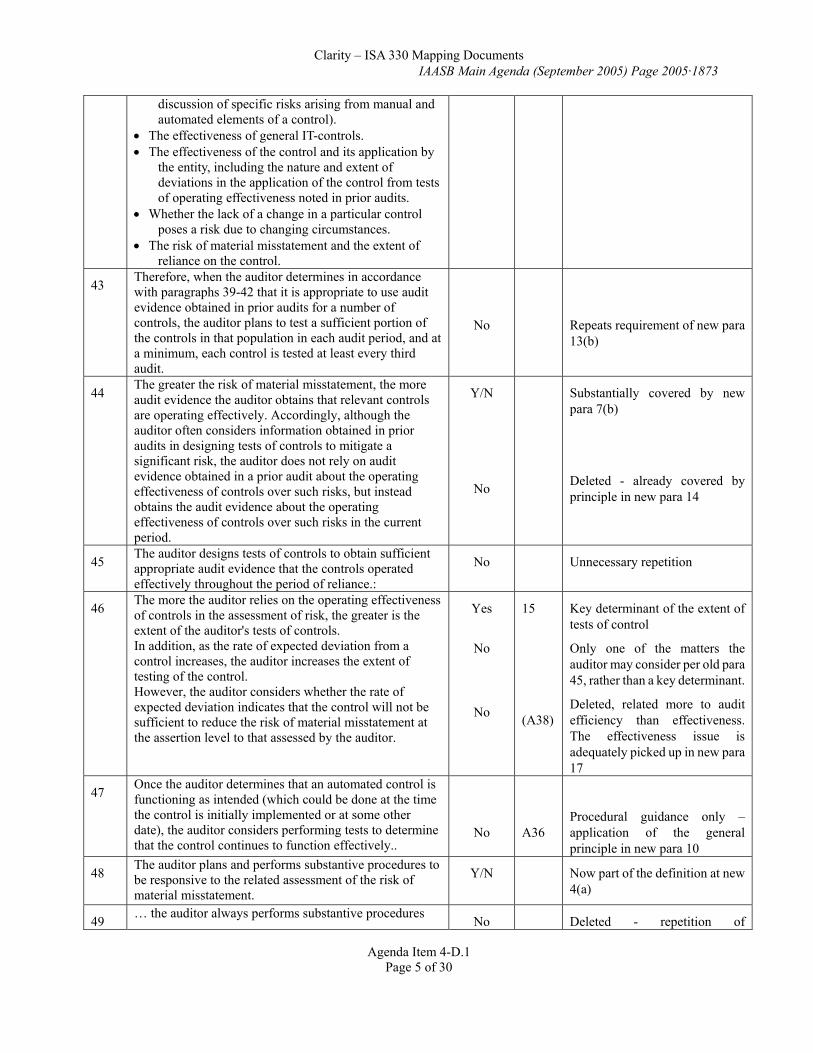

43 Therefore, when the auditor determines in accordance with paragraphs 39-42 that it is appropriate to use audit evidence obtained in prior audits for a number of controls, the auditor plans to test a sufficient portion of the controls in that population in each audit period, and at a minimum, each control is tested at least every third audit.

No

Repeats requirement of new para 13(b)

44 The greater the risk of material misstatement, the more audit evidence the auditor obtains that relevant controls are operating effectively. Accordingly, although the auditor often considers information obtained in prior audits in designing tests of controls to mitigate a significant risk, the auditor does not rely on audit evidence obtained in a prior audit about the operating effectiveness of controls over such risks, but instead obtains the audit evidence about the operating effectiveness of controls over such risks in the current period.

Y/N

No

Substantially covered by new para 7(b)

Deleted - already covered by principle in new para 14

45 The auditor designs tests of controls to obtain sufficient appropriate audit evidence that the controls operated effectively throughout the period of reliance.:

No Unnecessary repetition

46 The more the auditor relies on the operating effectiveness of controls in the assessment of risk, the greater is the extent of the auditor's tests of controls. In addition, as the rate of expected deviation from a control increases, the auditor increases the extent of testing of the control. However, the auditor considers whether the rate of expected deviation indicates that the control will not be sufficient to reduce the risk of material misstatement at the assertion level to that assessed by the auditor.

Yes

No

No

15

(A38)

Key determinant of the extent of tests of control

Only one of the matters the auditor may consider per old para 45, rather than a key determinant.

Deleted, related more to audit efficiency than effectiveness. The effectiveness issue is adequately picked up in new para 17

47 Once the auditor determines that an automated control is functioning as intended (which could be done at the time the control is initially implemented or at some other date), the auditor considers performing tests to determine that the control continues to function effectively..

No

A36

Procedural guidance only – application of the general principle in new para 10

48 The auditor plans and performs substantive procedures to be responsive to the related assessment of the risk of material misstatement.

Y/N

Now part of the definition at new 4(a)

49 … the auditor always performs substantive procedures No Deleted - repetition of

Clarity – ISA 330 Mapping Documents IAASB Main Agenda (September 2005) Page 2005·1874

Agenda Item 4-D.1 Page 6 of 30

for each material class of transactions, account balance, and disclosure.

Requirement at new para 18.

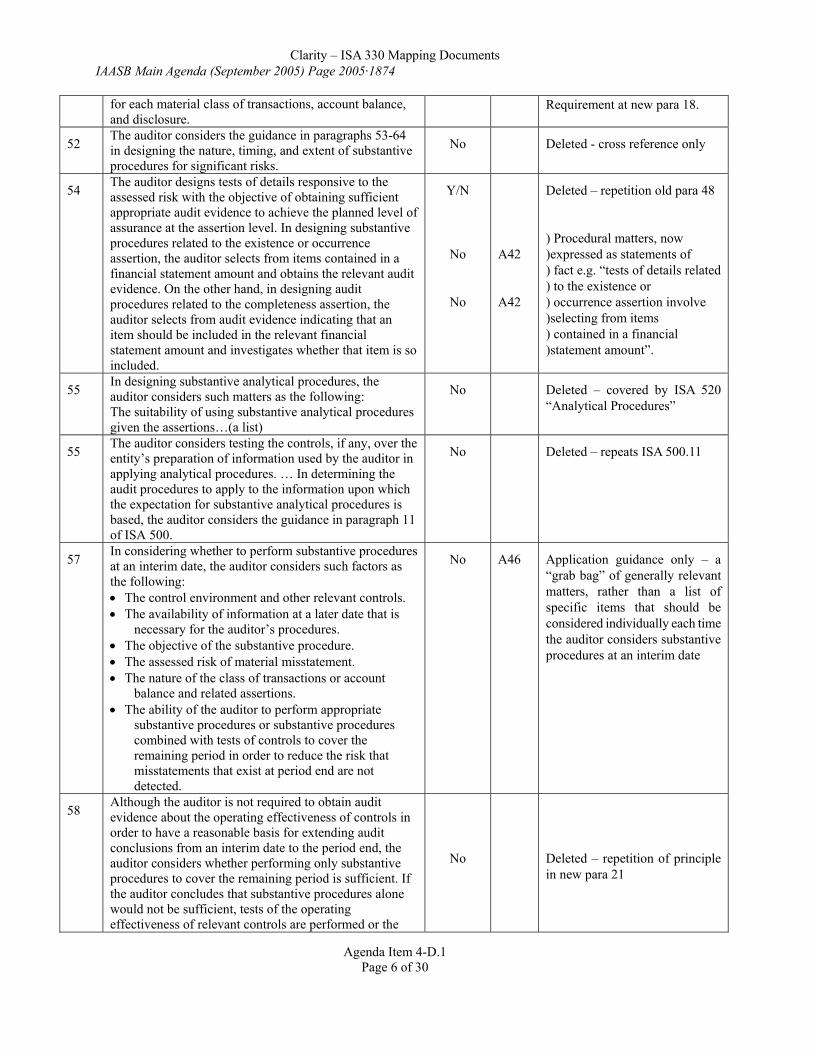

52 The auditor considers the guidance in paragraphs 53-64 in designing the nature, timing, and extent of substantive procedures for significant risks.

No Deleted - cross reference only

54 The auditor designs tests of details responsive to the assessed risk with the objective of obtaining sufficient appropriate audit evidence to achieve the planned level of assurance at the assertion level. In designing substantive procedures related to the existence or occurrence assertion, the auditor selects from items contained in a financial statement amount and obtains the relevant audit evidence. On the other hand, in designing audit procedures related to the completeness assertion, the auditor selects from audit evidence indicating that an item should be included in the relevant financial statement amount and investigates whether that item is so included.

Y/N

No

No

A42

A42

Deleted – repetition old para 48

) Procedural matters, now )expressed as statements of ) fact e.g. “tests of details related) to the existence or ) occurrence assertion involve )selecting from items ) contained in a financial )statement amount”.

55 In designing substantive analytical procedures, the auditor considers such matters as the following: The suitability of using substantive analytical procedures given the assertions…(a list)

No Deleted – covered by ISA 520 “Analytical Procedures”

55 The auditor considers testing the controls, if any, over the entity’s preparation of information used by the auditor in applying analytical procedures. … In determining the audit procedures to apply to the information upon which the expectation for substantive analytical procedures is based, the auditor considers the guidance in paragraph 11 of ISA 500.

No Deleted – repeats ISA 500.11

57 In considering whether to perform substantive procedures at an interim date, the auditor considers such factors as the following: • The control environment and other relevant controls. • The availability of information at a later date that is

necessary for the auditor’s procedures. • The objective of the substantive procedure. • The assessed risk of material misstatement. • The nature of the class of transactions or account

balance and related assertions. • The ability of the auditor to perform appropriate

substantive procedures or substantive procedures combined with tests of controls to cover the remaining period in order to reduce the risk that misstatements that exist at period end are not detected.

No A46 Application guidance only – a “grab bag” of generally relevant matters, rather than a list of specific items that should be considered individually each time the auditor considers substantive procedures at an interim date

58 Although the auditor is not required to obtain audit evidence about the operating effectiveness of controls in order to have a reasonable basis for extending audit conclusions from an interim date to the period end, the auditor considers whether performing only substantive procedures to cover the remaining period is sufficient. If the auditor concludes that substantive procedures alone would not be sufficient, tests of the operating effectiveness of relevant controls are performed or the

No

Deleted – repetition of principle in new para 21

Clarity – ISA 330 Mapping Documents IAASB Main Agenda (September 2005) Page 2005·1875

Agenda Item 4-D.1 Page 7 of 30

substantive procedures are performed as of the period end.

60 When the auditor plans to perform substantive analytical procedures with respect to the intervening period, the auditor considers whether the period end balances of the particular classes of transactions or account balances are reasonably predictable with respect to amount, relative significance, and composition. The auditor considers whether the entity’s procedures for analyzing and adjusting such classes of transactions or account balances at interim dates and for establishing proper accounting cutoffs are appropriate. In addition, the auditor considers whether the information system relevant to financial reporting will provide information concerning the balances at the period end and the transactions in the remaining period that is sufficient to permit investigation of: significant unusual transactions or entries (including those at or near period end); other causes of significant fluctuations, or expected fluctuations that did not occur; and changes in the composition of the classes of transactions or account balances.

) ) ) ) Yes ) ) ) ) ) ) ) ) ) ) ) ) )

) ) ) ) 23 ) ) ) ) ) ) ) ) ) ) ) ) )

) ) ) ) Statement of the ) principles to be applied ) whenever substantive ) analytical procedures are ) used with respect to ) an intervening period ) ) ) ) ) ) ) )

62 As required by paragraph 23 of ISA 500, if the auditor plans to use audit evidence obtained from the performance of substantive procedures in a prior audit, the auditor performs audit procedures during the current period to establish the continuing relevance of the audit evidence.

Yes

24

Statement of the general principle to be applied whenever evidence is used from substantive procedures in a prior audit

64 In designing tests of details, the extent of testing is ordinarily thought of in terms of the sample size, which is affected by the risk of material misstatement. However, the auditor also considers other matters, including whether it is more effective to use other selective means of testing, such as … In designing substantive analytical procedures, the auditor increases the desired level of assurance as the risk of material misstatement increases.

No

No

A43

Intended as an example of other matters that may be relevant.

Deleted – repeats ISA 520.12f

65 The auditor considers whether the individual financial statements are presented in a manner that reflects the appropriate classification and description of financial information. … The auditor considers whether management should have disclosed a particular matter in light of the circumstances and facts of which the auditor is aware at the time. In performing the evaluation of the overall presentation of the financial statements, including the related disclosures, the auditor considers the assessed risk of material misstatement at the assertion level. See paragraph 17 of ISA 500 for a description of the assertions related to presentation and disclosure.

No

No

No

A48

Deleted - already in ISA 500

Deleted: application of 500, Materiality and ISA 700

Now stated as an explanation, that “Evaluating presentation and disclosure relates to the assessed risk of material misstatement at the assertion level …”

68 … When such deviations are detected during the performance of tests of controls, the auditor makes specific inquiries to understand these matters and their potential consequences, for example, by inquiring about the timing of personnel changes in key internal control

Yes

17

) ) Both these matters are ) essential follow up if tests ) of controls are to be

Clarity – ISA 330 Mapping Documents IAASB Main Agenda (September 2005) Page 2005·1876

Agenda Item 4-D.1 Page 8 of 30

functions. The auditor determines whether the tests of controls performed provide an appropriate basis for reliance on the controls, whether additional tests of controls are necessary, or whether the potential risks of misstatement need to be addressed using substantive procedures.

Yes 17 ) effective ) )

69 The auditor cannot assume that an instance of fraud or error is an isolated occurrence, and therefore considers how the detection of a misstatement affects the assessed risks of material misstatement. Before the conclusion of the audit, the auditor evaluates whether audit risk has been reduced to an acceptably low level and whether the nature, timing, and extent of the audit procedures may need to be reconsidered.

No

No

Y

A50

26/7

Repeats ISA 240

Repeats old para 70

Redrafted - Necessary to ensure other steps in the audit process have achieved the objective of reducing risk to an acceptable level.

70 In developing an opinion, the auditor considers all relevant audit evidence, regardless of whether it appears to corroborate or to contradict the assertions in the financial statements.

No Moved to ISA 500

Cla

rity

– IS

A 3

30 M

appi

ng D

ocum

ents

IA

ASB

Mai

n Ag

enda

(Sep

tem

ber 2

005)

Pag

e 20

05·1

877

Prep

ared

by:

Mic

hael

Nug

ent (

Aug

ust 2

005)

Pa

ge 9

of 3

0

Map

ping

Doc

umen

t

Exhi

bit 2

Ori

gina

l ISA

330

N

ew

Par

Ref

Com

men

t on

prop

osed

del

etio

n of

hi

ghlig

hted

mat

eria

l an

d ot

her

note

s In

trod

uctio

n

1.

The

purp

ose

of th

is In

tern

atio

nal S

tand

ard

on A

uditi

ng (I

SA) i

s to

esta

blis

h st

anda

rds a

nd p

rovi

de g

uida

nce

on d

eter

min

ing

over

all

resp

onse

s an

d de

sign

ing

and

perf

orm

ing

furth

er a

udit

proc

edur

es t

o re

spon

d to

the

ass

esse

d ris

ks o

f m

ater

ial

mis

stat

emen

t at t

he fi

nanc

ial s

tate

men

t and

ass

ertio

n le

vels

in a

fina

ncia

l sta

tem

ent a

udit.

The

aud

itor’

s und

erst

andi

ng o

f the

entit

y an

d its

envi

ronm

ent,

incl

udin

g its

inte

rnal

cont

rol,

and

asse

ssm

ent o

f the

risk

s of m

ater

ial m

isst

atem

ent a

re d

escr

ibed

in

ISA

315

, “U

nder

stan

ding

the

Entit

y an

d Its

Env

ironm

ent a

nd A

sses

sing

the

Ris

ks o

f Mat

eria

l Mis

stat

emen

t.”

Pu

rpos

e re

stat

ed

in

new

pa

ra 1

Not

ne

cess

ary

in

new

fo

rmat

2.

The

follo

win

g is

an

over

view

of t

he re

quire

men

ts o

f thi

s sta

ndar

d:

• O

vera

ll re

spon

ses.

This

sect

ion

requ

ires t

he au

dito

r to

dete

rmin

e ove

rall

resp

onse

s to

addr

ess r

isks o

f mat

eria

l miss

tate

men

t at

the

finan

cial

stat

emen

t lev

el a

nd p

rovi

des g

uida

nce

on th

e na

ture

of t

hose

resp

onse

s.

• Au

dit p

roce

dure

s res

pons

ive t

o ri

sks o

f mat

eria

l mis

stat

emen

t at t

he a

sser

tion

leve

l. Th

is se

ctio

n re

quire

s the

audi

tor t

o de

sign

and

perf

orm

furth

er au

dit p

roce

dure

s, in

clud

ing

test

s of t

he o

pera

ting

effe

ctiv

enes

s of c

ontro

ls, w

hen

rele

vant

or r

equi

red,

and

subs

tant

ive

proc

edur

es, w

hose

nat

ure,

tim

ing,

and

ext

ent a

re re

spon

sive

to th

e as

sess

ed ri

sks o

f mat

eria

l mis

stat

emen

t at t

he

asse

rtion

leve

l. In

addi

tion,

this

sect

ion

incl

udes

mat

ters

the a

udito

r con

side

rs in

det

erm

inin

g th

e nat

ure,

tim

ing,

and

exte

nt o

f

such

aud

it pr

oced

ures

.

• Ev

alua

ting

the s

uffic

ienc

y and

app

ropr

iate

ness

of a

udit

evid

ence

obt

aine

d. T

his s

ectio

n re

quire

s the

audi

tor t

o ev

alua

te w

heth

er

the

risk

asse

ssm

ent r

emai

ns a

ppro

pria

te a

nd to

con

clud

e w

heth

er su

ffic

ient

app

ropr

iate

aud

it ev

iden

ce h

as b

een

obta

ined

.

• D

ocum

enta

tion.

Thi

s sec

tion

esta

blis

hes r

elat

ed d

ocum

enta

tion

requ

irem

ents

.

O

verv

iew

not

inc

lude

d in

ne

w fo

rmat

Cla

rity

– IS

A 3

30 M

appi

ng D

ocum

ents

IA

ASB

Mai

n Ag

enda

(Sep

tem

ber 2

005)

Pag

e 20

05·1

878

Age

nda

Item

4-D

.1

Page

10

of 3

0

3.

In o

rder

to re

duce

aud

it ri

sk to

an

acce

ptab

ly lo

w le

vel,

the a

udito

r sho

uld

dete

rmin

e ove

rall

resp

onse

s to

asse

ssed

risk

s

at th

e fin

anci

al st

atem

ent l

evel

, and

shou

ld d

esig

n an

d pe

rfor

m fu

rthe

r aud

it pr

oced

ures

to re

spon

d to

ass

esse

d ri

sks a

t

the a

sser

tion

leve

l. Th

e ove

rall

resp

onse

s and

the n

atur

e, ti

min

g, an

d ex

tent

of t

he fu

rther

audi

t pro

cedu

res a

re m

atte

rs fo

r the

prof

essi

onal

jud

gmen

t of

the

aud

itor.

In a

dditi

on t

o th

e re

quire

men

ts o

f th

is I

SA,

the

audi

tor

also

com

plie

s w

ith t

he

requ

irem

ents

and

guid

ance

in IS

A 2

40, “

The A

udito

r’s R

espo

nsib

ility

to C

onsi

der F

raud

in an

Aud

it of

Fin

anci

al S

tate

men

ts”

in re

spon

ding

to a

sses

sed

risks

of m

ater

ial m

isst

atem

ent d

ue to

frau

d.

5 &

6

Not

e: S

plit

and

rew

orde

d U

nnec

essa

ry re

fere

nce

to

“pro

fess

iona

l jud

gem

ent”

Unn

eces

sary

re

fere

nce

to

need

to

com

ply

with

oth

er

ISA

s

Ove

rall

Res

pons

es

4.

The

aud

itor s

houl

d de

term

ine o

vera

ll re

spon

ses t

o ad

dres

s the

risk

s of m

ater

ial m

issta

tem

ent a

t the

fina

ncia

l sta

tem

ent

leve

l. Su

ch re

spon

ses m

ay in

clud

e em

phas

izin

g to

the a

udit

team

the n

eed

to m

aint

ain

prof

essio

nal s

kept

icism

in g

athe

ring

and

eval

uatin

g au

dit e

vide

nce,

ass

igni

ng m

ore

expe

rienc

ed s

taff

or t

hose

with

spe

cial

ski

lls o

r usi

ng e

xper

ts,1 p

rovi

ding

mor

e

supe

rvis

ion,

or

inco

rpor

atin

g ad

ditio

nal

elem

ents

of

unpr

edic

tabi

lity

in t

he s

elec

tion

of f

urth

er a

udit

proc

edur

es t

o be

perf

orm

ed. A

dditi

onal

ly, t

he a

udito

r may

mak

e ge

nera

l cha

nges

to th

e na

ture

, tim

ing,

or e

xten

t of a

udit

proc

edur

es a

s an

over

all r

espo

nse,

for e

xam

ple,

per

form

ing

subs

tant

ive

proc

edur

es a

t per

iod

end

inst

ead

of a

t an

inte

rim d

ate.

5 A1

5.

The a

sses

smen

t of t

he ri

sks o

f mat

eria

l mis

stat

emen

t at t

he fi

nanc

ial s

tate

men

t lev

el is

affe

cted

by

the a

udito

r’s u

nder

stan

ding

of th

e con

trol e

nviro

nmen

t. A

n ef

fect

ive c

ontro

l env

ironm

ent m

ay al

low

the a

udito

r to

have

mor

e con

fiden

ce in

inte

rnal

cont

rol

and

the

relia

bilit

y of

aud

it ev

iden

ce g

ener

ated

inte

rnal

ly w

ithin

the

entit

y an

d th

us, f

or e

xam

ple,

allo

w th

e au

dito

r to

cond

uct

som

e au

dit p

roce

dure

s at

an

inte

rim d

ate

rath

er th

an a

t per

iod

end.

If th

ere

are

wea

knes

ses

in th

e co

ntro

l env

ironm

ent,

the

audi

tor o

rdin

arily

cond

ucts

mor

e aud

it pr

oced

ures

as o

f the

per

iod

end

rath

er th

an at

an in

terim

dat

e, se

eks m

ore e

xten

sive a

udit

evid

ence

from

subs

tant

ive

proc

edur

es, m

odifi

es th

e na

ture

of a

udit

proc

edur

es to

obt

ain

mor

e pe

rsua

sive

aud

it ev

iden

ce, o

r

incr

ease

s the

num

ber o

f loc

atio

ns to

be

incl

uded

in th

e au

dit s

cope

.

A2

Not

e: “

mod

ifies

the

nat

ure

of

audi

t pr

oced

ures

to

ob

tain

m

ore

pers

uasi

ve

audi

t ev

iden

ce”

mov

ed t

o A

1 la

st b

ulle

t

1 The

ass

ignm

ent o

f eng

agem

ent p

erso

nnel

to th

e pa

rticu

lar e

ngag

emen

t ref

lect

s the

aud

itor’s

risk

ass

essm

ent,

whi

ch is

bas

ed o

n th

e au

dito

r’s u

nder

stan

ding

of t

he e

ntity

.

Cla

rity

– IS

A 3

30 M

appi

ng D

ocum

ents

IA

ASB

Mai

n Ag

enda

(Sep

tem

ber 2

005)

Pag

e 20

05·1

879

Age

nda

Item

4-D

.1

Page

11

of 3

0

6.

Such

con

side

ratio

ns, t

here

fore

, hav

e a

sign

ifica

nt b

earin

g on

the

audi

tor’

s ge

nera

l app

roac

h, fo

r exa

mpl

e, a

n em

phas

is o

n

subs

tant

ive

proc

edur

es (s

ubst

antiv

e ap

proa

ch),

or a

n ap

proa

ch th

at u

ses

test

s of

con

trols

as

wel

l as

subs

tant

ive

proc

edur

es

(com

bine

d ap

proa

ch).

A3

Aud

it Pr

oced

ures

Res

pons

ive

to R

isks

of M

ater

ial M

isst

atem

ent a

t the

Ass

ertio

n L

evel

7.

The

aud

itor s

houl

d de

sign

and

per

form

furt

her a

udit

proc

edur

es w

hose

nat

ure,

tim

ing,

and

exte

nt a

re re

spon

sive t

o th

e as

sess

ed ri

sks o

f mat

eria

l mis

stat

emen

t at t

he a

sser

tion

leve

l. Th

e pur

pose

is to

pro

vide

a cl

ear l

inka

ge b

etw

een

the n

atur

e,

timin

g, an

d ex

tent

of t

he au

dito

r’s f

urth

er au

dit p

roce

dure

s and

the r

isk

asse

ssm

ent.

In d

esig

ning

furth

er au

dit p

roce

dure

s, th

e au

dito

r con

side

rs su

ch m

atte

rs a

s the

follo

win

g:

6

Not

e: In

new

par

a 6

“bas

ed

on”

adde

d

Rep

lace

d by

le

ad-in

w

ordi

ng fr

om o

ld p

ara

12

• Th

e si

gnifi

canc

e of

the

risk.

• Th

e lik

elih

ood

that

a m

ater

ial m

isst

atem

ent w

ill o

ccur

.

• Th

e ch

arac

teris

tics o

f the

cla

ss o

f tra

nsac

tions

, acc

ount

bal

ance

, or d

iscl

osur

e in

volv

ed.

• Th

e na

ture

of t

he sp

ecifi

c co

ntro

ls u

sed

by th

e en

tity

and

in p

artic

ular

whe

ther

they

are

man

ual o

r aut

omat

ed.

• W

heth

er th

e au

dito

r ex

pect

s to

obt

ain

audi

t evi

denc

e to

det

erm

ine

if th

e en

tity’

s co

ntro

ls a

re e

ffec

tive

in p

reve

ntin

g, o

r de

tect

ing

and

corr

ectin

g, m

ater

ial m

isst

atem

ents

.

The

natu

re o

f the

aud

it pr

oced

ures

is o

f mos

t im

porta

nce

in re

spon

ding

to th

e as

sess

ed ri

sks.

7(a)

(i)

7(a)

(ii)

7(a)

(ii)

7(b)

Thes

e 2

dot p

oint

s ar

e ve

ry

gene

ric a

nd a

re c

over

ed b

y ne

w p

ara

6

8.

The

audi

tor’

s as

sess

men

t of t

he id

entif

ied

risks

at t

he a

sser

tion

leve

l pro

vide

s a

basi

s fo

r con

side

ring

the

appr

opria

te a

udit

appr

oach

for

des

igni

ng a

nd p

erfo

rmin

g fu

rther

aud

it pr

oced

ures

. In

som

e ca

ses,

the

audi

tor

may

det

erm

ine

that

onl

y by

pe

rfor

min

g te

sts o

f con

trols

may

the

audi

tor a

chie

ve a

n ef

fect

ive

resp

onse

to th

e as

sess

ed ri

sk o

f mat

eria

l mis

stat

emen

t for

a

parti

cula

r ass

ertio

n. In

oth

er c

ases

, the

aud

itor m

ay d

eter

min

e th

at p

erfo

rmin

g on

ly su

bsta

ntiv

e pr

oced

ures

is a

ppro

pria

te fo

r sp

ecifi

c as

serti

ons a

nd, t

here

fore

, the

aud

itor e

xclu

des t

he e

ffec

t of c

ontro

ls fr

om th

e re

leva

nt ri

sk a

sses

smen

t. Th

is m

ay b

e be

caus

e the

audi

tor’

s ris

k as

sess

men

t pro

cedu

res h

ave n

ot id

entif

ied

any

effe

ctiv

e con

trols

rele

vant

to th

e ass

ertio

n, o

r bec

ause

te

stin

g th

e ope

ratin

g ef

fect

iven

ess o

f con

trols

wou

ld b

e ine

ffic

ient

. How

ever

, the

audi

tor n

eeds

to b

e sat

isfie

d th

at p

erfo

rmin

g on

ly su

bsta

ntiv

e pr

oced

ures

for t

he re

leva

nt a

sser

tion

wou

ld b

e ef

fect

ive

in re

duci

ng th

e ris

k of

mat

eria

l mis

stat

emen

t to

an

acce

ptab

ly lo

w le

vel.

Ofte

n th

e aud

itor m

ay d

eter

min

e tha

t a co

mbi

ned

appr

oach

usin

g bo

th te

sts o

f the

ope

ratin

g ef

fect

iven

ess

A4

A re

stat

emen

t of t

he g

ener

al

prin

cipl

e of

the

ISA

and

th

eref

ore

not

a se

para

te

requ

irem

ent

Cla

rity

– IS

A 3

30 M

appi

ng D

ocum

ents

IA

ASB

Mai

n Ag

enda

(Sep

tem

ber 2

005)

Pag

e 20

05·1

880

Age

nda

Item

4-D

.1

Page

12

of 3

0

of co

ntro

ls an

d su

bsta

ntiv

e pro

cedu

res i

s an

effe

ctiv

e app

roac

h. Ir

resp

ectiv

e of t

he ap

proa

ch se

lect

ed, t

he au

dito

r des

igns

and

perf

orm

s su

bsta

ntiv

e pr

oced

ures

for

eac

h m

ater

ial c

lass

of

trans

actio

ns, a

ccou

nt b

alan

ce, a

nd d

iscl

osur

e as

req

uire

d by

pa

ragr

aph

49.

18

&

F/n

2

9.

In th

e ca

se o

f ver

y sm

all e

ntiti

es, t

here

may

not

be

man

y co

ntro

l act

iviti

es th

at c

ould

be

iden

tifie

d by

the

audi

tor.

For t

his

reas

on, t

he au

dito

r’s f

urth

er au

dit p

roce

dure

s are

like

ly to

be p

rimar

ily su

bsta

ntiv

e pro

cedu

res.

In su

ch ca

ses,

in ad

ditio

n to

the

mat

ters

ref

erre

d to

in p

arag

raph

8 a

bove

, the

aud

itor c

onsi

ders

whe

ther

in th

e ab

senc

e of

con

trols

it is

pos

sibl

e to

obt

ain

suff

icie

nt a

ppro

pria

te a

udit

evid

ence

.

A5

Not

e:

Fina

l se

nten

ce

rew

orde

d

Con

side

ring

the

Nat

ure,

Tim

ing,

and

Ext

ent o

f Fur

ther

Aud

it Pr

oced

ures

Nat

ure

10.

The n

atur

e of f

urth

er au

dit p

roce

dure

s ref

ers t

o th

eir p

urpo

se (t

ests

of c

ontro

ls or

subs

tant

ive p

roce

dure

s) an

d th

eir t

ype,

that

is,

insp

ectio

n, o

bser

vatio

n, in

quiry

, con

firm

atio

n, re

calc

ulat

ion,

repe

rform

ance

, or a

naly

tical

pro

cedu

res.

Cer

tain

audi

t pro

cedu

res

may

be

mor

e ap

prop

riate

for s

ome

asse

rtion

s tha

n ot

hers

. For

exa

mpl

e, in

rela

tion

to re

venu

e, te

sts o

f con

trols

may

be

mos

t re

spon

sive

to th

e as

sess

ed ri

sk o

f mis

stat

emen

t of t

he c

ompl

eten

ess a

sser

tion,

whe

reas

subs

tant

ive

proc

edur

es m

ay b

e m

ost

resp

onsi

ve to

the

asse

ssed

risk

of m

isst

atem

ent o

f the

occ

urre

nce

asse

rtion

.

A6

A7

11.

The a

udito

r’s s

elec

tion

of au

dit p

roce

dure

s is b

ased

on

the a

sses

smen

t of r

isk.

The

hig

her t

he au

dito

r’s a

sses

smen

t of r

isk,

the

mor

e re

liabl

e an

d re

leva

nt is

the

audi

t evi

denc

e so

ught

by

the

audi

tor f

rom

subs

tant

ive

proc

edur

es. T

his m

ay a

ffec

t bot

h th

e ty

pes o

f aud

it pr

oced

ures

to b

e per

form

ed an

d th

eir c

ombi

natio

n. F

or ex

ampl

e, th

e aud

itor m

ay co

nfirm

the c

ompl

eten

ess o

f the

te

rms o

f a c

ontra

ct w

ith a

third

par

ty, i

n ad

ditio

n to

insp

ectin

g th

e do

cum

ent.

A7

Cov

ered

by

ne

w

para

6

This

sent

ence

is v

ery

simila

r to

the

req

uire

men

t of

new

pa

ra 7

(b)

12.

In d

eter

min

ing

the a

udit

proc

edur

es to

be p

erfo

rmed

, the

audi

tor c

onsid

ers t

he re

ason

s for

the a

sses

smen

t of t

he ri

sk o

f mat

eria

l m

isst

atem

ent a

t the

ass

ertio

n le

vel f

or e

ach

clas

s of t

rans

actio

ns, a

ccou

nt b

alan

ce, a

nd d

iscl

osur

e. T

his i

nclu

des c

onsi

derin

g bo

th th

e pa

rticu

lar c

hara

cter

istic

s of

eac

h cl

ass

of tr

ansa

ctio

ns, a

ccou

nt b

alan

ce, o

r dis

clos

ure

(i.e.

, the

inhe

rent

risk

s) a

nd

whe

ther

the

audi

tor’

s ris

k as

sess

men

t tak

es a

ccou

nt o

f the

ent

ity’s

con

trols

(i.e

., th

e co

ntro

l ris

k). F

or e

xam

ple,

if th

e au

dito

r co

nsid

ers t

hat t

here

is a

low

er ri

sk th

at a

mat

eria

l mis

stat

emen

t may

occ

ur b

ecau

se o

f the

par

ticul

ar ch

arac

teris

tics o

f a cl

ass o

f tra

nsac

tions

with

out c

onsi

dera

tion

of th

e re

late

d co

ntro

ls, t

he a

udito

r may

det

erm

ine

that

sub

stan

tive

anal

ytic

al p

roce

dure

s al

one m

ay p

rovi

de su

ffic

ient

appr

opria

te au

dit e

vide

nce.

On

the o

ther

han

d, if

the a

udito

r exp

ects

that

ther

e is a

low

er ri

sk th

at

a m

ater

ial m

isst

atem

ent m

ay a

rise

beca

use

an e

ntity

has

eff

ectiv

e co

ntro

ls a

nd th

e au

dito

r in

tend

s to

des

ign

subs

tant

ive

7(a)

7(a)

(i)

7(a)

(ii)

A8

Not

e: R

edra

fted

Cla

rity

– IS

A 3

30 M

appi

ng D

ocum

ents

IA

ASB

Mai

n Ag

enda

(Sep

tem

ber 2

005)

Pag

e 20

05·1

881

Age

nda

Item

4-D

.1

Page

13

of 3

0

proc

edur

es b

ased

on

the

effe

ctiv

e op

erat

ion

of th

ose

cont

rols

, the

n th

e au

dito

r pe

rfor

ms

test

s of

con

trols

to o

btai

n au

dit

evid

ence

abo

ut th

eir o

pera

ting

effe

ctiv

enes

s. Th

is m

ay b

e th

e ca

se, f

or e

xam

ple,

for a

cla

ss o

f tra

nsac

tions

of r

easo

nabl

y un

iform

, non

-com

plex

cha

ract

eris

tics t

hat a

re ro

utin

ely

proc

esse

d an

d co

ntro

lled

by th

e en

tity’

s inf

orm

atio

n sy

stem

.

13.

The a

udito

r is r

equi

red

to o

btai

n au

dit e

vide

nce a

bout

the a

ccur

acy

and

com

plet

enes

s of i

nfor

mat

ion

prod

uced

by

the e

ntity

’s

info

rmat

ion

syst

em w

hen

that

info

rmat

ion

is u

sed

in p

erfo

rmin

g au

dit p

roce

dure

s. Fo

r ex

ampl

e, if

the

audi

tor

uses

non

-fin

anci

al in

form

atio

n or

bud

get d

ata

prod

uced

by

the

entit

y’s

info

rmat

ion

syst

em in

per

form

ing

audi

t pro

cedu

res,

such

as

subs

tant

ive a

naly

tical

pro

cedu

res o

r tes

ts of

cont

rols,

the a

udito

r obt

ains

audi

t evi

denc

e abo

ut th

e acc

urac

y an

d co

mpl

eten

ess o

f su

ch in

form

atio

n. S

ee IS

A 5

00, “

Aud

it Ev

iden

ce”

para

grap

h 11

for f

urth

er g

uida

nce.

R

epet

ition

of I

SA 5

00.1

1

Tim

ing

14.

Tim

ing

refe

rs to

whe

n au

dit p

roce

dure

s are

per

form

ed o

r the

per

iod

or d

ate

to w

hich

the

audi

t evi

denc

e ap

plie

s. A

9

15.

The

audi

tor m

ay p

erfo

rm te

sts o

f con

trols

or s

ubst

antiv

e pro

cedu

res a

t an

inte

rim d

ate

or a

t per

iod

end.

The

hig

her t

he ri

sk o

f m

ater

ial m

isst

atem

ent,

the

mor

e lik

ely

it is

that

the

audi

tor m

ay d

ecid

e it

is m

ore

effe

ctiv

e to

per

form

subs

tant

ive

proc

edur

es

near

er to

, or a

t, th

e pe

riod

end

rath

er th

an a

t an

earli

er d

ate,

or t

o pe

rfor

m a

udit

proc

edur

es u

nann

ounc

ed o

r at u

npre

dict

able

tim

es (f

or ex

ampl

e, p

erfo

rmin

g au

dit p

roce

dure

s at s

elec

ted

loca

tions

on

an u

nann

ounc

ed b

asis)

. On

the o

ther

han

d, p

erfo

rmin

g au

dit p

roce

dure

s bef

ore t

he p

erio

d en

d m

ay as

sist t

he au

dito

r in

iden

tifyi

ng si

gnifi

cant

mat

ters

at an

early

stag

e of t

he au

dit,

and

cons

eque

ntly

reso

lvin

g th

em w

ith th

e as

sist

ance

of m

anag

emen

t or d

evel

opin

g an

eff

ectiv

e au

dit a

ppro

ach

to a

ddre

ss su

ch

mat

ters

. If

the

audi

tor

perf

orm

s te

sts

of c

ontro

ls o

r su

bsta

ntiv

e pr

oced

ures

prio

r to

per

iod

end,

the

audi

tor

cons

ider

s th

e ad

ditio

nal e

vide

nce

requ

ired

for t

he re

mai

ning

per

iod

(see

par

agra

phs 3

7-38

and

56-

61).

A10

A11

Unn

eces

sary

int

erna

l cr

oss

refe

renc

e

16.

In c

onsi

derin

g w

hen

to p

erfo

rm a

udit

proc

edur

es, t

he a

udito

r als

o co

nsid

ers s

uch

mat

ters

as t

he fo

llow

ing:

• Th

e co

ntro

l env

ironm

ent

• W

hen

rele

vant

info

rmat

ion

is a

vaila

ble

(for

exa

mpl

e, e

lect

roni

c fil

es m

ay s

ubse

quen

tly b

e ov

erw

ritte

n, o

r pro

cedu

res t

o be

ob

serv

ed m

ay o

ccur

onl

y at

cer

tain

tim

es).

• Th

e nat

ure o

f the

risk

(for

exam

ple,

if th

ere i

s a ri

sk o

f inf

late

d re

venu

es to

mee

t ear

ning

s exp

ecta

tions

by

subs

eque

nt cr

eatio

n of

fals

e sa

les a

gree

men

ts, t

he a

udito

r may

wis

h to

exa

min

e co

ntra

cts a

vaila

ble

on th

e da

te o

f the

per

iod

end)

.

• Th

e pe

riod

or d

ate

to w

hich

the

audi

t evi

denc

e re

late

s

A13

17.

Cer

tain

aud

it pr

oced

ures

can

be

perf

orm

ed o

nly

at o

r afte

r per

iod

end,

for e

xam

ple,

agr

eein

g th

e fin

anci

al st

atem

ents

to th

e A

12

Cla

rity

– IS

A 3

30 M

appi

ng D

ocum

ents

IA

ASB

Mai

n Ag

enda

(Sep

tem

ber 2

005)

Pag

e 20

05·1

882

Age

nda

Item

4-D

.1

Page

14

of 3

0

acco

untin

g re

cord

s and

exam

inin

g ad

just

men

ts m

ade d

urin

g th

e cou

rse o

f pre

parin

g th

e fin

anci

al st

atem

ents

. If t

here

is a

risk

that

the

entit

y m

ay h

ave

ente

red

into

impr

oper

sale

s con

tract

s or t

rans

actio

ns m

ay n

ot h

ave

been

fina

lized

at p

erio

d en

d, th

e au

dito

r per

form

s pro

cedu

res t

o re

spon

d to

that

spec

ific

risk.

For

exa

mpl

e, w

hen

trans

actio

ns a

re in

divi

dual

ly m

ater

ial o

r an

erro

r in

cuto

ff m

ay le

ad to

a m

ater

ial m

isst

atem

ent,

the

audi

tor o

rdin

arily

insp

ects

tran

sact

ions

nea

r the

per

iod

end.

Unn

eces

sary

exa

mpl

e

Exte

nt

18.

Exte

nt in

clud

es th

e qu

antit

y of

a s

peci

fic a

udit

proc

edur

e to

be

perf

orm

ed, f

or e

xam

ple,

a s

ampl

e si

ze o

r th

e nu

mbe

r of

ob

serv

atio

ns o

f a

cont

rol a

ctiv

ity. T

he e

xten

t of

an a

udit

proc

edur

e is

det

erm

ined

by

the

judg

men

t of

the

audi

tor

afte

r co

nsid

erin

g th

e mat

eria

lity,

the a

sses

sed

risk,

and

the d

egre

e of a

ssur

ance

the a

udito

r pla

ns to

obt

ain.

In p

artic

ular

, the

audi

tor

ordi

naril

y in

crea

ses

the

exte

nt o

f aud

it pr

oced

ures

as

the

risk

of m

ater

ial m

isst

atem

ent i

ncre

ases

. How

ever

, inc

reas

ing

the

exte

nt o

f an

audi

t pro

cedu

re is

effe

ctiv

e onl

y if

the a

udit

proc

edur

e its

elf i

s rel

evan

t to

the s

peci

fic ri

sk; t

here

fore

, the

nat

ure o

f th

e au

dit p

roce

dure

is th

e m

ost i

mpo

rtant

con

side

ratio

n.

A14

A15

7 (b

)

19.

The

use

of c

ompu

ter-

assi

sted

aud

it te

chni

ques

(CA

ATs

) may

ena

ble

mor

e ex

tens

ive

test

ing

of e

lect

roni

c tra

nsac

tions

and

ac

coun

t file

s. Su

ch te

chni

ques

can

be

used

to s

elec

t sam

ple

trans

actio

ns fr

om k

ey e

lect

roni

c fil

es, t

o so

rt tra

nsac

tions

with

sp

ecifi

c ch

arac

teris

tics,

or to

test

an

entir

e po

pula

tion

inst

ead

of a

sam

ple.

A16

20.

Val

id c

oncl

usio

ns m

ay o

rdin

arily

be

draw

n us

ing

sam

plin

g ap

proa

ches

. How

ever

, if t

he q

uant

ity o

f sel

ectio

ns m

ade

from

a

popu

latio

n is

too

smal

l, th

e sa

mpl

ing

appr

oach

sel

ecte

d is

not

app

ropr

iate

to

achi

eve

the

spec

ific

audi

t ob

ject

ive,

or

if ex

cept

ions

are n

ot ap

prop

riate

ly fo

llow

ed u

p, th

ere w

ill b

e an

unac

cept

able

risk

that

the a

udito

r’s co

nclu

sion

base

d on

a sa

mpl

e m

ay b

e di

ffer

ent f

rom

the

conc

lusi

on re

ache

d if

the

entir

e po

pula

tion

was

sub

ject

ed to

the

sam

e au

dit p

roce

dure

. ISA

530

, “A

udit

Sam

plin

g an

d O

ther

Mea

ns o

f Tes

ting”

con

tain

s gui

danc

e on

the

use

of sa

mpl

ing.

U

nnec

essa

ry r

epet

ition

of

conc

epts

from

ISA

530

21.

This

stan

dard

rega

rds t

he u

se o

f diff

eren

t aud

it pr

oced

ures

in c

ombi

natio

n as

an

aspe

ct o

f the

nat

ure

of te

stin

g as

dis

cuss

ed

abov

e. H

owev

er, t

he au

dito

r con

side

rs w

heth

er th

e ext

ent o

f tes

ting

is ap

prop

riate

whe

n pe

rfor

min

g di

ffer

ent a

udit

proc

edur

es

in c

ombi

natio

n.

A15

N

ote:

R

edra

fted

as

2nd

sent

ence

of A

15

Tes

ts o

f Con

trol

s

22.

The a

udito

r is r

equi

red

to p

erfo

rm te

sts o

f con

trols

whe

n th

e aud

itor’

s ris

k as

sess

men

t inc

lude

s an

expe

ctat

ion

of th

e ope

ratin

g ef

fect

iven

ess

of c

ontro

ls o

r whe

n su

bsta

ntiv

e pr

oced

ures

alo

ne d

o no

t pro

vide

suf

ficie

nt a

ppro

pria

te a

udit

evid

ence

at t

he

asse

rtion

leve

l.

R

epea

ts n

ew p

ara

8(a)

R

epea

ts n

ew p

ara

8(b)

23.

Whe

n th

e au

dito

r’s

asse

ssm

ent o

f ris

ks o

f mat

eria

l mis

stat

emen

t at t

he a

sser

tion

leve

l inc

lude

s an

exp

ecta

tion

that

8(

a)

Not

e:

Rew

orde

d –

in

Cla

rity

– IS

A 3

30 M

appi

ng D

ocum

ents

IA

ASB

Mai

n Ag

enda

(Sep

tem

ber 2

005)

Pag

e 20

05·1

883

Age

nda

Item

4-D

.1

Page

15

of 3

0

cont

rols

are

ope

ratin

g ef

fect

ivel

y, th

e au

dito

r sh

ould

per

form

test

s of c

ontr

ols t

o ob

tain

suff

icie

nt a

ppro

pria

te a

udit

evid

ence

that

the c

ontr

ols w

ere o

pera

ting

effe

ctiv

ely

at re

leva

nt ti

mes

dur

ing

the p

erio

d un

der a

udit.

See

par

agra

phs 3

9-44

bel

ow fo

r dis

cuss

ion

of u

sing

aud

it ev

iden

ce a

bout

the

oper

atin

g ef

fect

iven

ess o

f con

trols

obt

aine

d in

prio

r aud

its.

parti

cula

r re

fere

nce

to

timin

g de

lete

d (p

icke

d up

in

new

par

a 10

)

Unn

eces

sary

int

erna

l cr

oss

refe

renc

e

24.

The

audi

tor’

s ass

essm

ent o

f ris

k of

mat

eria

l mis

stat

emen

t at t

he a

sser

tion

leve

l may

incl

ude

an e

xpec

tatio

n of

the

oper

atin

g ef

fect

iven

ess

of c

ontro

ls, i

n w

hich

cas

e th

e au

dito

r per

form

s te

sts

of c

ontro

ls to

obt

ain

audi

t evi

denc

e as

to th

eir o

pera

ting

effe

ctiv

enes

s. Te

sts

of th

e op

erat

ing

effe

ctiv

enes

s of

con

trols

are

per

form

ed o

nly

on th

ose

cont

rols

that

the

audi

tor

has

dete

rmin

ed ar

e sui

tabl

y de

sign

ed to

pre

vent

, or d

etec

t and

corr

ect,

a mat

eria

l miss

tate

men

t in

an as

serti

on. P

arag

raph

s 104

-106

of

ISA

315

dis

cuss

the

iden

tific

atio

n of

con

trols

at t

he a

sser

tion

leve

l lik

ely

to p

reve

nt, o

r de

tect

and

cor

rect

, a m

ater

ial

mis

stat

emen

t in

a cl

ass o

f tra

nsac

tions