Analysis of Credit Constraint and Financial Exclusion …economics.ca/2008/papers/0300.pdf · 1...

29

1 Draft: May 15, 2008 Analysis of Credit Constraint and Financial Exclusion With Canadian Microdata Jerry Buckland and Wayne Simpson 1 1 Buckland: International Development Studies Program, Menno Simons College, Winnipeg, MB R3C 0G2; Simpson: Department of Economics, University of Manitoba, Winnipeg MB R3T 5V5(corresponding author: contact at [email protected] or tel: (204)474-9274). We thank Wendy Pyper at Statistics Canada for discussions about the Survey of Financial Security but all errors, omissions and interpretations are our own.

-

Upload

nguyenthuy -

Category

Documents

-

view

227 -

download

1

Transcript of Analysis of Credit Constraint and Financial Exclusion …economics.ca/2008/papers/0300.pdf · 1...

1

Draft: May 15, 2008

Analysis of Credit Constraint and Financial Exclusion With Canadian Microdata

Jerry Buckland and Wayne Simpson1

1 Buckland: International Development Studies Program, Menno Simons College, Winnipeg, MB R3C 0G2; Simpson: Department of Economics, University of Manitoba, Winnipeg MB R3T 5V5(corresponding author: contact at [email protected] or tel: (204)474-9274). We thank Wendy Pyper at Statistics Canada for discussions about the Survey of Financial Security but all errors, omissions and interpretations are our own.

0

Abstract

Changes are occurring in the provision of consumer credit, including the

expansion of sub-prime and some fringe financial services (e.g., payday

lending). We link two existing literatures on credit constraint and

financial exclusion to assess the impact of these developments on the

financial circumstances of low and modest-income consumers. We

develop a model that identifies observable measures of credit constraint

and financial exclusion and relates them to consumer characteristics and

life cycle behaviour. We estimate this model using the two latest Surveys

of Financial Security for 1999 and 2005, which provide consistent

evidence of credit constraint and financial exclusion through time. We

find modest overlap among our measures of financial exclusion, which

include a zero bank balance, credit card refusal, and using a pawn shop.

Probit regression is used to investigate the factors influencing the

incidence of financial exclusion. The results are similar for 1999 and

2005 and indicate rising incidence of financial exclusion as income and

wealth fall, although the relationship is nonlinear such that incidence rises

much faster at very low levels of income and wealth. When we combine

the samples, we find statistically significant evidence of growth in the

incidence of each indicator of financial exclusion when other factors are

held constant. If financial exclusion is seen to be detrimental to poorer

groups in society, this may cause some concern in policy circles.

1

Analysis of Credit Constraint and Financial Exclusion With Canadian Microdata

1. Introduction

Changes are occurring in the provision of consumer credit. The expansion of

subprime lending, primarily in the U.S., is the most important current example, but not

the only one. In both the U.S. and Canada, for example, there has been a rapid expansion

in such fringe or alternative financial services as payday lending. As financial

institutions evolve, there is concern that a larger proportion of the population is being

excluded from mainstream financial services. This development may be important if

financial exclusion creates or exacerbates economic disadvantage. Moreover, financial

exclusion can have macroeconomic consequences, as the recent subprime mortgage crisis

in the U.S. attests.

The study of financial exclusion has a small but growing literature particularly in

the United States and the United Kingdom. The literature for Canada and Europe is

slimmer and there is little literature on financial exclusion per se for the global South

where a related literature has focused on micro credit and microfinance. Financial

exclusion is generally understood to be related with material poverty and/or social

exclusion, a type of deprivation that affects household functioning. This deprivation is

related to other forms of deprivation such as low levels of income and assets.

Financial exclusion is a relatively new concept arising from a variety of

interdisciplinary studies of a real world problem, people being unable to access

mainstream banking services. From an economic perspective, however, it is primarily a

microeconomic problem, i.e., how certain consumers operate within, and are affected by,

financial service markets. For that reason financial exclusion relates most closely to the

economic theory of consumer savings, and in particular, the credit or liquidity constraint

concept rooted in the life-cycle model of consumption. In this paper, we link two

existing literatures on credit constraint and financial exclusion and develop an empirical

model to assess their recent impact on Canadian consumers, particularly those with low

or modest incomes.

2

The remainder of our paper is constructed as follows. In the next section we

review the literature on financial exclusion and credit constraint and previous empirical

studies. We use this literature to develop our empirical model in section 3. Sections 4

and 5 then discuss our measures of financial exclusion and analyze their determinants.

2. Relevant Literature

Our literature review first discusses the concept of financial exclusion. It then

turns to theories of financial exclusion and the related literature on credit constrained

consumers.

2.1. Meanings of Financial Exclusion

Financial services provide consumers liquidity (e.g., cashing a cheque), payment

(e.g., bill payments, money wiring), savings (e.g., interest-bearing accounts, income tax

deductable programs like RRSPs) and credit (e.g., small loan, credit card, line of credit,

mortgage) services. Consumers who are without access to these services face multiple

constraints to enhancing their wellbeing. To be unbanked implies the consumer is without

access to any of these services from a mainstream bank typically referring to a bank,

credit union/caisse populaire or trust company. Instead, these consumers would rely on a

fringe bank –a cheque-casher, payday lender, pawnshop, etc. –and informal financial

service providers such as a small retailer, family member or friend. Here consumers

would pay higher direct fees or interest rates for virtually all of these services. Moreover,

building a credit relationship with a fringe bank will not facilitate accessing mainstream

bank credit.

There are two common indicators of financial exclusion: unbanked and

underbanked. Being unbanked simply means not having any type of mainstream bank

account. Being unbanked implies that the household relies on fringe and or informal

financial services for cheque-cashing, credit, savings and payment services. Underbanked

definitions vary and generally refer to either limited frequency of use of a bank account

or limited access to bank services. Underbanked may mean a person uses her/his bank

account only a few times a year, meaning that they rely on other financial service

providers at other times of the year. Alternatively being underbanked may be determined

3

by limited access to mainstream financial services. A household limited to only a current

account may not have access to adequate credit, savings, liquidity and payment services.

Operationalizing the unbanked concept is straight forward. The indicator is bank

account ownership and this is a question asked in national surveys in the US and UK, but

not so in Canada, as we shall see. With its less concrete definition, operationalizing the

underbanked concept is more complicated. One way would be to set a minimum

frequency of bank account use, a minimum set of bank account services (or if they rely

on fringe or informal financial services as a negative) or simply ask respondents if they

have adequate access to financial services through a mainstream bank.

2.2. Theories of Financial Exclusion

The literature related to financial exclusion comes from a number of theoretical

traditions and political ideologies and focuses on different units of analysis. Let us

examine some of the key theoretical approaches used to understand financial exclusion.

One perspective is that financial service markets are by-and-large functioning

well. Producers and consumers are participating in the market in a mutually beneficial

relationship. Competition is occurring both within and between mainstream and fringe

banks. The particular character of low-income consumers’ financial service needs is such

that fringe banks have a competitive advantage over mainstream banks. For instance,

payday lending is an innovation that provides consumers a new credit product in an

efficient way (Elliehausan and Lawrence, 2001). Payday lending provides a short-term

and small-sum loan to people who would otherwise not have enough credit or rely on a

pawnbroker, in which case they might loose their pawned item.

Instead of markets operating for the mutual advantage of producers and

consumers, the concept of bounded rationality from behavioural economics has been

applied to explain the apparently irrational behaviour of some credit consumers (Karlan

& Zinman, 2005). A payday loan of $250 for 12-days in Manitoba will cost on average

$63, implying an annual percentage rate of 771% (Buckland, et al., 2007). What reason

does a person have to pay so heavy a fee when she or he could pay an interest charge of

10% to 25% for a loan via a credit card or credit line? Since most payday loan consumers

are employed and have a bank account the answer is not immediately obvious.

4

Behavioural economics relaxes the assumption of consumer rationality and suggests that

consumers may behave in a way that ultimately hurts their interests.

Another literature, bridging the behavioural economics and the institutional theory

relates to financial literacy/capability (SEDI, 2004; Atkinson et al., 2007). This literature

posits that structural changes in Western economies increasingly place the responsibility

of financial planning from government and employers to the individual, citizen and

employee. The responsibility for retirement planning and insurance, in particular, are

increasingly placed with the individual. But do individuals understand their financial

service needs and the markets that serve them? Moreover, this literature asks a

behavioural economics question, do people apply their financial literacy to improve their

financial and social lives?

The final literature of interest is the institutional analysis literature. This literature

generally holds the consumer rationality assumption but places the consumer within a

dynamic institutional context. The literature often considers factors that affect either the

supply-side or the demand-side of the financial service market. For instance, an often

referred to supply-side factor is the liberalization of financial services which has led to,

among other things, mainstream banks to close marginally-profitable branches in low-

income neighbourhoods and pull out of the provision of small consumer loans. A

common demand-side factor is the stagnation of lower incomes and or the growing

income and wealth gaps. This has led to a large and growing number of households with

limited finances and limited accessibility to mainstream financial services.

2.3. Credit Constrained Consumers

A standard microeconomic approach to explain consumption and savings choices

is the life cycle model. At its simplest level, it posits perfectly functioning capital

markets within which the consumer will borrow and save over their lifetime to smooth

out consumption. The model implies that the individual or household consumes a higher

proportion (or in excess) of income in youth and old age and a smaller proportion (or in

deficit) of income in the middle years of life. The smoothing of consumption boosts long-

term well-being because the household is able to avoid periods of very low spending even

when its income is low. The life cycle model assumes that capital markets are

5

functioning perfectly so that lender and borrower have full information about each other,

and in particular, the lender is able to identify the riskiness of each borrower vis-à-vis

their likelihood of repaying the loan.

Some have argued on theoretical or empirical grounds, however, that consumers

sometimes lack sufficient access to credit and are credit or liquidity constrained. For

instance, Stiglitz and Weiss (1981) show how imperfect information between a principal

(lender) and agent (borrower) can act as an obstacle to perfectly functioning credit

markets. Imperfect information can lead the lender operating at an equilibrium interest

rate into adverse selection (selecting riskier borrowers) and can lead the borrower not to

repay her/his loan (moral hazard). According to the Stigltz-Weiss model, to avoid these

problems the lender will set an interest rate below the market equilibrium rate and ration

credit. Rationing of credit by lenders leads to excess demand, pushing some borrowers

into other credit markets such as fringe and informal credit providers. Dymski (2003,

2005) argues that the Stiglitz-Weiss model is consistent with the bifurcation of banking

service markets into mainstream and fringe banking observed in the US. The

consequence is that some consumers are both financially excluded and credit constrained.

Credit constraint is clearly related to financial exclusion. On the consumer side of

the equation, the underbanked have been defined as not having access to sufficient

financial services, particularly lacking access to credit. While an individual may have a

bank account, she/he may not have access to credit and therefore need to rely on fringe

and informal sources of credit. In this way credit constraint and financial exclusion

overlap. On the supply-side of the equation, the notion that banks keep interest rates

below the market rate and ration credit in order to reduce the adverse selection problem is

consistent with some recent changes in the banking sector that have been raised in the

financial exclusion literature. This literature raised the concern that banks have closed

inner-city branches reducing accessibility for low-income residents. In addition, this

literature has been concerned that, as mainstream banks have automated small lending in

the form of lines of credit and credit cards, many low-income people are no longer

eligible for credit. Thus there is considerable overlap between the credit constraint and

the financial exclusion concepts.

6

2.4. Empirical Studies of Financial Exclusion & Credit Constrained Consumers

Data on financial exclusion is most extensive in the US. For instance, Hogarth,

Anguelov & Lee (2005) use data from 5 iterations of the Survey of Consumer Finances

(Federal Reserve Board) (1989, 1992, 1995, 1998 & 2001) to examine the characteristics

of the unbanked and changes in financial exclusion over time. They found that the

unbanked proportion (households without a transactions account) of the sample dropped

from 14.6% in 1989 to 9.0% in 2001 (p.14). The proportion of unbanked rise with lower

income groups so that in 2001, 36.7% of households at the bottom decile are unbanked

(p.14). For 2001, using a logistic regression the results found that,

Banked households had higher income and net worth (measured in 2001 dollars); were less likely to spend all their money; more likely to be 2-person households; less likely to have children present; more likely to be married; had higher levels of education; were more likely to be white; more likely to be employed or retired; were older; were more likely to be home owners and vehicle owners; were more likely to use a medium or long-term planning horizon. All differences between the banked and unbanked groups were significant (Anguelov & Lee, 2005, p.18).

Evidence for the UK suggests that approximately 7% of households have no

current account and an additional 20% “on the margins of financial services” (such as no

access to mainstream bank credit) (FSA, 2000 cited in Devlin, 2005, p.78). Devlin used a

logistic model with several different independent variables of financial exclusion (current

account, savings account, contents insurance, life assurance & pension), drawing on a

questionnaire of almost 16,000 people. The results found that employment status,

household income and housing tenure showed “most consistent and marked influences on

financial exclusion” (p.96); marital status, age, and educational attainment were also

significant explanatory variables (p.96).

Evidence for Canada found that 3% all households and 8% low-income

households are unbanked but this is an underestimate of low-income households (The

Task Force Report on Future of Canadian Financial Services Sector, 1998; Ipsos-Reid

Corp., 2005). Using data from the 1999 Survey of Financial Security Buckland and Dong

(2008, forthcoming) concluded, “that financial exclusion is more concentrated among

7

low-income Canadians; low-income, low-level of assets and single-parent statuses are

correlated with being unbanked.”

Data on financial exclusion in Europe shows a considerable range. Northern

European countries have the highest levels of financial inclusion including Denmark

(99.1%), Netherlands (98.9%), Sweden (98.0%), and Finland (96.7%) (Carbo, Garderner

& Molyneux, 2007). Germany (96.5%) and France (96.3%) have very similar rates of

financial inclusion. Lower rates of financial inclusion are found in Southern Europe

including Portugal (81.6%), Greece (78.9%), Italy (70.4%) as well as Ireland (79.6%).

In regards to consumer credit constraint, Japelli (1990) noted that one-fifth of the

US population may be credit constrained and this would lead their consumption to be

very sensitive to current income. In examining consumer credit constraint in various

industrialized countries Jappeli and Pagano (1989) found that the credit constraint is

lower for the US and Sweden, moderate for the UK and Japan and higher for Italy, Spain

and Greece. More recently, Pozzi and Malengier (2007) estimate that, on average, across

17 OECD countries (including Canada) that 37% of people are ‘rule-of-thumb’

consumers such that their spending is directly tied to their current income.

3. An Empirical Model

Japelli (1990) provides a useful framework for the analysis of credit constraint

and, potentially, other aspects of financial exclusion at the level of the individual. Her

model of consumption over the life cycle defines credit constraint as a situation or

condition in which

0)1(* >−+−− iiii DrAYC [1]

where *iC is optimal consumption of household i along the life cycle path without credit

constraint, iY is current household income, iA is current wealth yielding rate of return r,

and iD is the amount of debt the individual is able to incur. Since *iC and iD are

unobservable, Japelli assumes that they can be approximated by observable cross-

sectional variables, iX , including income, wealth, debt, age, education and demographic

characteristics that include employment status, marital status, race, sex, family size, home

ownership, and region:

8

iii

iii

XD

XC

ηδ

εα

+′=

+′=*

[2]

so that condition [1] can be rewritten as

0)1( >+′≡−+′−+−−′iiiiiiii XXrAYX μβηεδα [3]

because iX contains both income iY and wealth iA and the return to wealth r is assumed

to be constant across individuals. This condition then forms the basis for a latent variable

model, such as a.logit or probit model, to explain the incidence of credit constraint among

households in microdata:

( )⎪⎩

⎪⎨⎧

<+′≥+′

=000)(1

ii

iii

XifnedunconstraiXifdconstrainecreditZ

μβμβ [4]

Jappeli argues that observables should be entered in nonlinear (e.g., quadratic and

interaction) forms on the assumption that expected optimal consumption can be

approximated by a quadratic function in a cross-section.

This framework is limited by its maintained hypotheses regarding the critical

unobservable elements in [2] and, as such, provides only a guide to the list of observable

characteristics that should explain credit constraint and other forms of financial

exclusion. Other studies have been less explicit but have used similar empirical

frameworks to explain other aspects of financial exclusion. Devlin’s (2005) study of

financial exclusion in the U.K., for example, uses income, proxies for wealth (such as

housing tenure), age, education and demographic characteristics that include employment

status, marital status, ethnicity, sex, household size, and region in a logit regression

model to explain financial exclusion for five types of accounts: current account, savings

account, household insurance, life insurance, and a private pension. Thus, his

specification corresponds quite closely to Japelli’s and is used to address other aspects of

financial exclusion, including the unbanked.

Two studies of the unbanked by Hogarth et al. (2003 and 2005) adopt a similar

approach to explaining whether individuals have an account at a financial institution.

Hogarth et al. (2005, p. 9) summarizes: “Income, net worth, employment status,

education, age, region, race/ethnicity, gender and marital status are predictors of account

9

ownership.” Their paper combines data from the Surveys of Consumer Finance for 1989,

1992, 1995, 1998, and 2001 to assess the impact of these factors and, holding these

factors constant, whether the incidence of being unbanked fell with time. They find that

the probability of being unbanked fell, particularly between 1995 and 1998, a period of

rapid economic growth in the U.S.

Finally, Buckland and Dong (2008) use a probit model and the 1999 Survey of

Financial Security to explain financial exclusion on three dimensions: no account, no

credit card, and use of a pawnshop. Their model includes income, wealth, education,

employment status (sources of income), family type, home ownership, region, and

whether households have a budget or help from friends or relatives in a financial crisis.

They find that low income and wealth, larger families, single parenthood, low education

and the absence of a friend or relative to turn to in a financial crisis all increase the

probability of financial exclusion across the three dimensions.

Another potential limitation of Japelli’s approach is its reliance on the rational

theory of individual consumption. The rapid change in financial services in the last

twenty years make institutional theory a potentially important literature to examine

financial exclusion, but it is difficult to operationalize this theoretical approach. In

particular, we would require a dataset that would include both supply-side and demand-

side factors, but most datasets, including the Survey of Financial Security we use here,

are household surveys which are limited to the demand side. For example, there is no

data on the address of respondents to permit us to include supply-side factors such as

proximity to bank branch. Inclusion of detailed geographical information might be

considered for future surveys on financial security.

4. Indicators of Financial Exclusion

Our analysis suggests three indicators of financial exclusion which we can

attempt to measure directly with microdata provided by the Surveys of Financial

Exclusion (SFS) for 1999 and 2005 (Statistics Canada, 1999 and 2005). These indicators

are:

(1) Absence of a bank account to capture the “unbanked” sector of the economy, as in

Hogarth et al (2005) or Devlin (2005)

10

(2) Absence of access to a credit card to capture those who are “credit constrained,” as in

Japelli (1990)

(3) Reliance on alternatives to traditional financial institutions, including pawnshops and,

more recently, payday lenders.

In this section we look at these indicators, assess measurement issues, and examine the

degree to which these measures are interrelated within the Canadian population.

The SFS does not ask respondents whether they or a member of their family have

an account at a bank or other financial institution, which would be the best indicator of

the unbanked. Rather, it asks the respondent to report any non-zero deposit balance in

financial institutions. As a result, those who happen to have one or more bank accounts

with a zero balance and those who do not have a bank account are mixed and there is no

way to separate them in the SFS for 1999 and 2005. In addition, negative bank balances

are reported in the 2005 SFS but not in the 1999 SFS. Since negative bank balances are

evidence of possession of a bank account with overdraft privileges, those with a negative

bank balance are clearly not unbanked. In the 1999 SFS, however, negative bank

balances were assigned to “other loans from financial institutions” so that a family with a

bank account in overdraft might report a zero bank balance and a positive value for

“other loans from financial institutions.” To complicate matters further, the publicly

released data combines “other loans from financial institutions” with “other money

owed” into a variable called “other debts,” which does not allow us to check directly for

the presence of “other loans from financial institutions.” Our strategy, therefore, is to

check for “other debts,” but this will identify the unbanked only if the presence of “other

money owed” is consistent with the presence of a bank account.

The SFS does ask respondents whether the respondent or anyone in his/her family

has a credit card and, if not, whether it is because they were refused a credit card. This

should provide a clear measure of credit constraint along the lines used by Jappelli but

only with respect to credit cards and not other forms of lending from financial

institutions.

In recent years, alternative sources of credit outside the traditional financial sector

have developed fairly rapidly. In particular, payday lenders have experienced dramatic

growth in Canada, providing short-term loans between paychecks at high effective

11

interest rates. The 2005 SFS recognizes this development by asking whether the

respondent or a member of his/her family unit has borrowed money from a payday lender

in the last three years. There is no comparable measure in the 1999 SFS. Both surveys

record whether any member of the respondent’s family sold any possession to a pawn

broker in the previous calendar year. And both surveys, in conjunction with the questions

on pawn shop and payday loan use, also recorded whether an asset was sold or used to

pay a debt in the previous calendar year. We look at these measures as indicators of

reliance on alternatives to mainstream financial institutions.

Descriptive means for these indicators of financial exclusion are provided in

Table 1. First, our attempt to identify those families without an account at a financial

institution includes two indicators. The first indicator of the unbanked population is a

zero account balance, which would include account holders with a negative balance in

1999. The second includes those with a zero bank balance and no other debts, which

excludes those with a negative bank balance in 1999 but also excludes those with no bank

balance but other unspecified forms of debt. Both these indicators suggest that the

proportion of families without an account at a financial institution is growing between

1999 and 2005. The proportion of the population with a zero account balance has grown

from 12.07 to 13% and the proportion of the population with a zero account balance and

no other debts has grown from 9.13 to 10.3%.

Other indicators show little or mixed evidence of growth in financial exclusion.

The proportion of families that have been refused a credit card has declined slightly from

3.76 to 3.32%. The proportion of families using a pawn shop has increased slightly from

2.24 to 2.66% and the proportion of families using a pawn shop or an asset to pay a debt

has also increased slightly from 6.89 to 7.06%.

The other substantial evidence of financial exclusion is the rapid growth in the

proportion of families using payday lenders. This proportion reached 2.65% in 2005,

approaching the same level as the use of pawn shops.1 Indeed, the rapid growth in this

1 The SFS’s question in reference to payday lending refers to the respondent’s previous three years, while the question in reference to use of a pawn shop refers only to the previous year. A recent survey from the Financial Consumer Agency of Canada (FCAC, 2005) suggests that 57% of those using payday lenders in 2005 were using the lenders at least once a year. If the remaining 43% are distributed uniformly over three years, the FCAC results imply that 71% of payday loan consumers would have used a payday loan service

12

area explains the absence of any comparable statistic in the 1999 SFS. Some evidence of

the rapid growth of this financial alternative is provided in Table 2 for three major

Canadian cities using yellow page and business directories for 1999 and 2005. It shows

that payday lending outlets have increased by 149% during this period.

To what extent do these indicators overlap? To assess this, we present Tables 3

and 4. In Table 3 we consider the joint incidence of our various indicators of financial

exclusion. It shows, for example, that among those respondents with a zero bank

balance, 8.3% were refused a credit card in 1999 and 8.8% in 2005. Using our alternative

definition of the unbanked, a zero bank balance and no other debt, the proportion of

respondents who were refused a credit card has also risen from 7.6% to 8.3%. For those

who were refused a credit card, 33.3% had a zero account balance in 1999, rising to

38.1% in 2005. Thus, the measures of the unbanked and the credit constrained overlap to

some extent and there is modest evidence that the overlap is increasing over time.

Similarly, if we look at those who used a pawnshop in the previous year, 37.6% had a

zero bank balance in 1999 and 21.9% were refused a credit card. In 2005, these figures

had risen to 43.5% and 26.9%.

In Table 4 we present pearson correlation coefficients to summarize the overlap

among our set of indicators. All correlations are significant at the 5% level and generally

indicate a positive but modest degree of correlation among the categories. For example,

in 1999 the correlation coefficient of a zero bank balance is about 0.11 with a credit card

refusal or pawn shop dealing; in 2005 this correlation coefficient rose to 0.13. The

correlation of a refused credit card with use of a pawnshop is about 0.16 in 1999, rising to

0.20 in 2005. For 2005 only, since there are no comparable figures for 1999, the

correlation of payday borrowing is 0.06 with a zero account balance, 0.12 with a refused

credit card, and 0.19 with use of a pawnshop.

One concern with these results is that the combination of a zero account balance

and no other debts is negatively correlated with all other indicators, including the

indicator of a zero account balance alone. If the absence of “other debts” provided us

with a better indicator of those without an account at a financial institution (the

in the past year. This implies that about 1.9% of families used a payday lender in 2004 compared to the 2.7% of families using a pawn shop.

13

unbanked), these negative correlations seem unlikely. Thus, we drop this indicator from

our subsequent analysis and focus on a zero account balance as an indicator of the

unbanked.

5. Analysis of the Determinants of Financial Exclusion

Much of the concern regarding financial exclusion has been its effect in

exacerbating income disparities. We have seen in developing our model in section 3 how

income and wealth can play an important role in identifying credit constraint and

financial exclusion. In this section, we first look at these links before turning to more

general analysis. Figure 1 provides smoothed or nonparametric estimates of the simple

relationship between family after-tax income and three indicators of financial exclusion

from the 1999 and 2005 SFS. After some experimentation, we limited our graph to

incomes between zero and $100,000, since negative incomes and very large incomes

tended to obscure the pattern of greatest interest for low and moderate income Canadians.

Figure 1 illustrates that financial exclusion rises as income falls, with the sharpest

increase for zero account balance, our indicator of the unbanked. The incidence

relationship with income is similar for credit card refusal and pawnshop use. The

relationship is nonlinear, as Japelli (1990) suggested. For 2005, we include the

relationship between income and using a payday lender. It is interesting that this

relationship is weaker and does not increase sharply (toward higher incidence) for

incomes under $30,000. This may occur because use of a payday lender requires a

paycheck at the time the loan is taken, such that these users are more likely to be

employed than those covered under the other measures of financial exclusion.

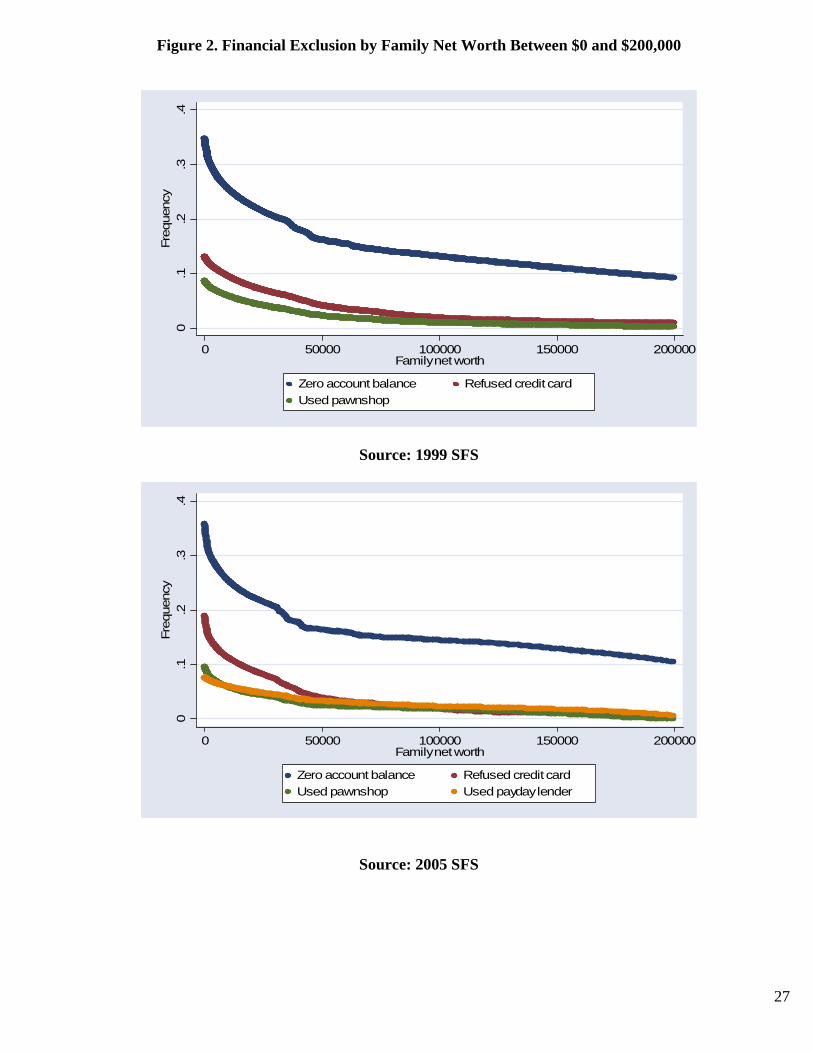

Figure 2 looks at the relationships between the indicators of financial exclusion

and wealth.2 The results are very similar. Financial exclusion rises as wealth falls in a

nonlinear fashion, with the sharpest increases below $50,000 for those with a zero bank

account, followed by credit card refusal and pawnshop use. The pattern of incidence and

payday lending use in 2005 is very similar to pawnshop use.

2 Wealth is defined as total assets, including pension benefits evaluated on a going concern basis, minus total debt. For further discussion of wealth measurement in the SFS see the documentation at: http://www.statcan.ca/english/Dli/Data/Ftp/sfs/1999/sfs1999.htm and http://www.statcan.ca/english/Dli/Data/Ftp/sfs/2005/sfs2005.htm

14

We have identified a number of other factors in section 3 that likely affect the

incidence of financial exclusion, including debt, age, education and such demographic

characteristics as employment status, marital status, race, sex, family size, home

ownership, and region. Two questions arise here. First, to what extent do these factors

affect the incidence of our indicators of financial exclusion? Second, does the inclusion

of these factors affect our conclusions from the simple relationships in Figures 1 and 2

about the effect of income and wealth on these indicators? In order to address these

questions, we turn to probit estimates of the incidence of financial exclusion.

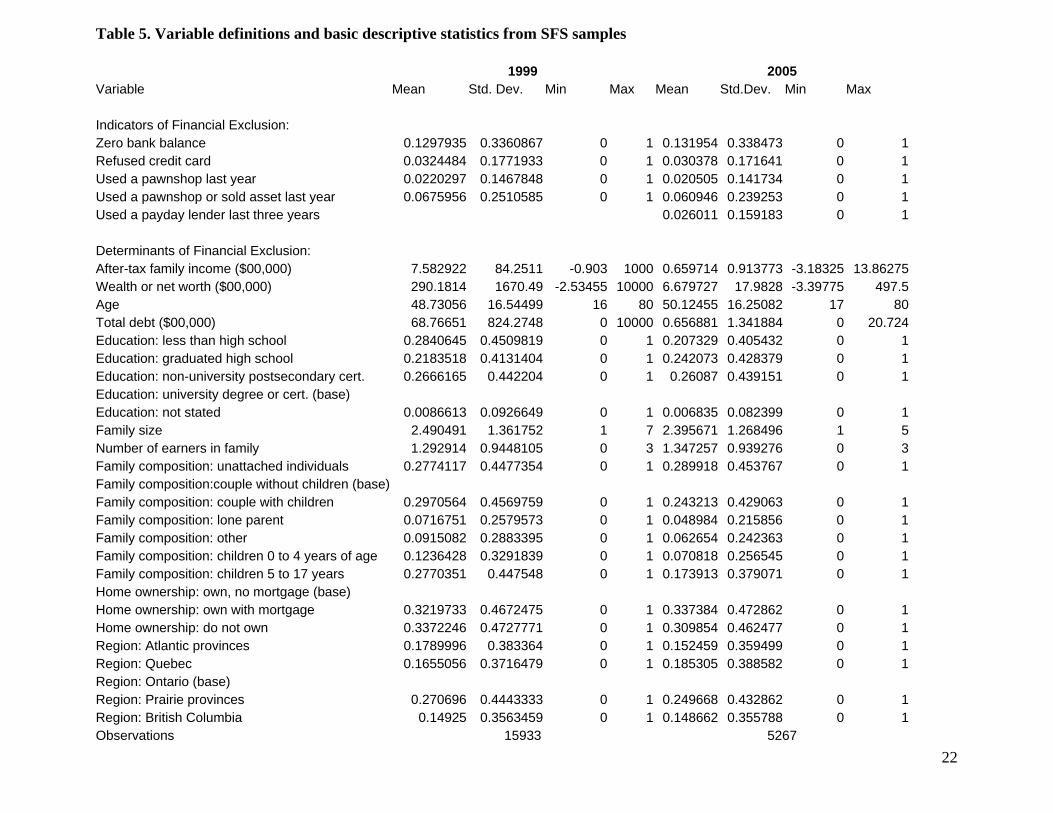

Table 5 provides brief definitions of the variables used in our probit analysis and

basic descriptive statistics. We would note with some concern that the range of incomes

and wealth is much wider in the larger 1999 sample as compared to the 2005 SFS sample.

We expect that this is the major reason for the much larger mean income and wealth

figures in Table 5. This result dictates some caution in comparing results from the two

samples.

Table 6 provides the probit estimates for 1999. Family income and wealth and

their squared terms are consistently significant at the 5% level, implying the nonlinear,

inverted-U shaped relationship with the incidence of financial exclusion implied by

Figures 1 and 2, i.e. as income falls, financial exclusion incidence rises at an increasing

rate. Age and its squared term are also significant for zero bank balance and credit card

refusal, reflecting a rise in the incidence of financial exclusion early in the life cycle.

Debt is also significant for zero bank balance and credit card refusal, but higher debt

reduces the likelihood of refusal of a credit card and increases the likelihood of a zero

bank balance, suggesting that different mechanisms are at play. It seems likely, for

example, that credit card refusal plays a role in limiting debt accumulation for families,

such that the causal effect is from credit card refusal to debt rather than as implied here.

Education matters and a lower education is associated with a greater incidence of

financial exclusion for all indicators. Larger families with fewer earners are significantly

more likely to have a zero bank balance and to use a pawnshop, while lone parents and

families with children 5-17 are more likely to be refused credit. Home ownership,

particular mortgage-free, is associated with a lower incidence of financial exclusion.

15

Note that, in our estimates, we have already allowed for the wealth effect of home

ownership, implying some other aspect of behavior may also be at work here.

The comparable estimates for 2005 are shown in Table 7. The patterns are very

similar to those found for 1999, reinforcing those results, but are generally weaker as

would be expected from a smaller sample. With encouragement from the similarity of

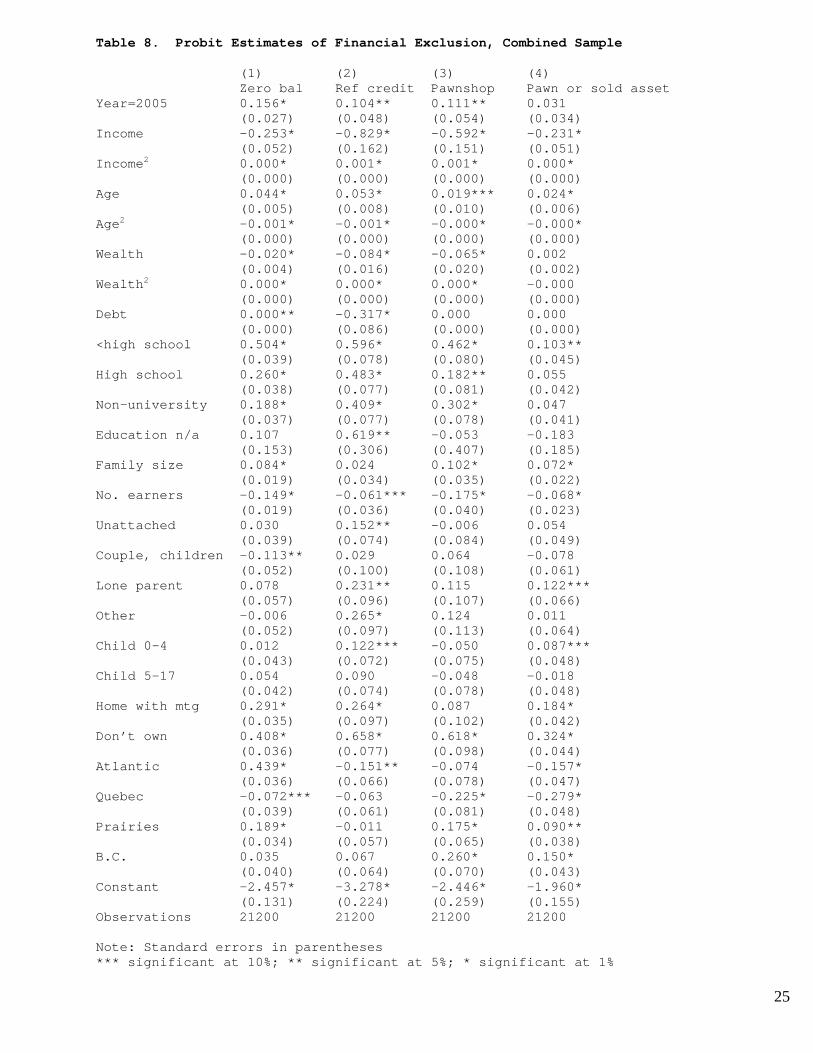

the results for 1999 and 2005, we adopt the approach of Hogarth et al. (2005, Table 3)

and combine our SFS samples for 1999 and 2005 to examine the trend over time. In

particular, we add a dummy to our specification to see if, holding the effects of other

factors constant, we can detect a time trend in our results. The results are presented in

Table 8. The coefficient on our time dummy (Year=2005) is positive and significant for

all three measures of financial exclusion: having a zero bank balance, having been

refused a credit card, and having used a pawnshop. At the mean incidence for each

indicator, they imply an increase in the probability of that indicator of 3.5% (for having a

zero bank balance), 0.8% (for being refused a credit card) and 0.7% (for using a pawn

shop), other factors in our analysis held constant.3 We are, of course, unable to assess the

trend for use of a payday lender, since that information was not collected in 1999.

6. Conclusions

From the theoretical perspective, the results of this research demonstrate an

important relationship between credit constraint and concepts of the unbanked or

underbanked. This relationship is very useful because while the unbanked concept has

identified a troublesome contemporary problem, the credit constraint has a deep

connection in economic theory. Thus, the credit constraint literature may usefully inform

the study of financial exclusion. While the unbanked concept is generally understood as a

person without a bank account, the underbanked concept is less well developed and may

mean being without some services and/or without convenient access. If underbanked

implies limited services and, in particular, limited credit access, then there is a direct link

to the credit constraint literature. What the financial exclusion concept usefully articulates

3 That is, the probability of a zero bank balance would be predicted to rise from 13% (the mean in Table 1 for 1999) to 16.5% in 2005, the probability of a credit card refusal would be predicted to rise from 3.2% to 4%, and the probability of using a pawn shop would be predicted to rise from 2.2% to 2.9% for families with the same characteristics.

16

is the there are important financial services in addition to credit that constrain individuals.

Lacking access to effective ‘liquidity’ services (especially timely cheque-cashing),

savings vehicles (including asset-building) and financial advice can also act as obstacles

to personal financial development. We conclude that future work on financial exclusion

might usefully address this theoretical relationship.

Our empirical analysis uses the 1999 and 2005 Surveys of Financial Security

produced by Statistics Canada. The surveys are closely comparable except that one

potentially important measure of financial exclusion, the use of a payday lender, is not

captured in 1999, reflecting the rapid recent growth in this financial alternative. We find

evidence of modest overlap among our measures of financial exclusion, particularly

having a zero bank balance, being refused a credit card and having used a pawn shop.

We use probit regression to investigate the factors influencing the incidence of these

measures of financial exclusion for Canadian families. The results are similar for 1999

and 2005 and indicate rising incidence of financial exclusion as income and wealth fall,

although the relationship is nonlinear such that incidence rises much faster at very low

levels of income and wealth. Pawnshop lending appears to have a weaker relationship

with income and wealth looking only at the 2005 sample. Finally, when we combine the

samples, we find statistically significant evidence of growth in the incidence of each

indicator of financial exclusion when other factors are held constant. If financial

exclusion is seen to be detrimental to poorer groups in society, this may cause some in

policy circles.

Another conclusion from this research is that an examination of financial

exclusion and credit constraint at the national level is limited by the available microdata.

At this point, the Survey of Financial Security appears to us to provide the most useful

data to analyze these issues (Pyper, 2008). To examine financial exclusion and credit

constraint more effectively, more precise questions about banking and credit need to be

added to a regularly implemented national survey. Questions of particular relevance

would include those about the use of access to, and use of, banking services: accounts

and type, credit instruments and type, types of savings, and forms of financial advice.

These questions would ideally encompass all types of banking services from mainstream

through fringe to informal financial services.

17

References

Atkinson, Adele, Stephen McKay, Sharon Collard, and Elaine Kempson. 2007. Levels of Financial Capability in the UK. Public Money & Management 27, no. 1.

Buckland, J., Carter, T., Simpson, W., Friesen, A., & Osborne, J. (2007). Serving or exploiting people facing a short-term credit crunch: A study of consumer aspects of payday lending in Manitoba. Winnipeg, Canada: Public Utilities Board Hearing to Cap Payday Loan Fees.

Buckland, Jerry and Xiao-Yuan Dong. 2008. Banking on the Margin in Canada. Economic Development Quarterly, forthcoming.

Carbo, Santiago, Edward Gardener, and Philip Molyneux. 2007. Financial Exclusion in Europe. Public Money & Management 27, no. 1: 21.

Devlin, James F. 2005. A Detailed Study of Financial Exclusion in the UK. Journal of Consumer Policy 28: 75-108.

Dymski, Gary A. 2003. Banking on transformation: Financing development, overcoming poverty. In Seminario basil em desenvolvimento. Sacramento: University of California Center in Sacramento.

Dymski, Gary A. 2005. Financial Globalization, Social Exclusion and Financial Crisis. International Review of Applied Economics 19, no. 4 (10) : 439-457.

Elliehausen, Gregory, and Edward C. Lawrence. Payday Advance Credit in America: An

Analysis of Customer Demand. Washington, D.C.: Credit Research Center, Georgetown University, 2001.

Hogarth, Jeanne M., Christoslav E. Anguelov, and Jinhook Lee. 2005. Who Has a Bank

Account? Exploring Changes Over Time, 1989-2001. Journal of Family and Economic Issues 26, no. 1: 7.

Holt, Richard P. F., and Steven Pressman. 2001. A new guide to post keynesian economics. London: Routledge.

Ipsos-Reid Corporation. 2005. Public Experience with Financial Services and Awareness of FCAC. Ottawa: Financial Consumer Agency of Canada.

Jappelli, Tullio. 1990. Who Is Credit Constrained in the U.S. Economy? The Quarterly Journal of Economics 105, no. 1.

18

Jappelli, Tullio, Marco Pagano. 1989. Consumption and Capital Market Imperfections:

An International Comparison. The American Economic Review 79, no. 5.

Karlan, Dean S., Jonathan Zinman. 2005. Observing Unobservables: Identifying Information Assymetries with a Consumer Credit Field Experiment. New York: Federal Reserve Bank of New York.

MacKay, Harold. 1998. Task Force Report on Future of Canadian Financial Services Sector (MacKay Report). Ottawa: Department of Finance, Canada.

Pozzi, Lorenzo, Griet Malengier. 2007. Certainty Equivalences and the Excess Sensitivity

of Private Consumption. Journal of Money, Credit and Banking 39, no. 7.

Pyper, Wendy. 2008. Personal Communication.

Social and Enterprise Development Innovations (SEDI). 2004. Financial Capability and Poverty: Discussion Paper. Ottawa: Policy Research Initiative.

Stiglitz, Joseph, Andrew Weiss. 1981. Credit Rationing in Markets with Imperfect Information. The American Economic Review 71, no. 3. Statistics Canada (1999). 1999 Survey of Financial Security, Income Statistics Division.

Ottawa, Canada. Documentation can be found at: http://www.statcan.ca/english/Dli/Data/Ftp/sfs/1999/sfs1999.htm

Statistics Canada (2005). 2005 Survey of Financial Security, Income Statistics Division. Ottawa, Canada. Documentation can be found at: http://www.statcan.ca/english/Dli/Data/Ftp/sfs/2005/sfs2005.htm

19

Table 1. Descriptive Statistics for Indicators of Financial Exclusion Variable 1999 (unwtd) 1999 (wtd) 2005 (unwtd) 2005 (wtd) Zero account balance

2,068 (12.98 %)

1,475,004 (12.07 %)

695 (13.20 %)

1,935,195 (13.00 %)

Zero balance and no other debts

1,540 (9.67 %)

1,115,375 (9.13 %)

542 (10.29 %)

1,374,809 (10.30 %)

No credit card

3,369 (21.14 %)

2,665,960 (21.82 %)

869 (16.50 %)

2,377,218 (17.81 %)

Refused credit card

517 (3.24%)

459,569 (3.76 %)

160 (3.04 %)

443,142 (3.32 %)

Used pawn shop last year

351 (2.20 %)

273,692 (2.24 %)

108 (2.05 %)

355,048 (2.66 %)

Used pawn shop or asset to pay debt

1,077 (6.76 %)

841,898 (6.89 %)

321 (6.09 %)

942,345 (7.06 %)

Used payday lender within three years

n a n a 137 (2.60 %)

353,713 (2.65 %)

Observations

15,933 12,215,618 5,267 13,347,657

Source: Authors’ calculations from the 1999 and 2005 Surveys of Financial Security public files Notes: Those who have been refused a credit card do not have other credit cards. Table 2. Payday Loan Outlet Numbers, 1999 & 2005* 1999 2005 Toronto** 41 96 Vancouver*** 24 38 Winnipeg 6 43 Total 71 177 Outlet Increase 1999-2005 106 Percent Change 1999-2005 149%

*Data collected by Daniel Liadsky (in Toronto) for both Toronto and Vancouver and Jennifer Braun (in Winnipeg) for Winnipeg and is taken from yellow page and business directories for 1999 and 2005. **Toronto data are for pre-amalgamation municipalities, previously known as Metropolitan Toronto. ***Vancouver data are for Vancouver proper and exclude surrounding municipalities such as Burnaby and Surrey.

20

Table 3. Overlap of Financial Indicators

Variable 1999

0 acct bal 0 bal,oth debt

Ref cr card Pawn shop

Pawn or asset

Payday lender

Zero account balance

2,068 (100%)

1,540 (74.5%)

172 (8.3%)

132 (6.4%)

277 (13.4%)

n.a.

Zero balance, no other debts

1,540 (100%)

1,540 (100 %)

117 (7.6%)

78 (5.1%)

161 (10.5%)

n.a.

Refused credit card

172 (33.3%)

117 (22.6 %)

517 (100%)

77 (14.9%)

122 (23.6%)

n.a.

Used pawn shop in last yr

132 (37.6%)

78 (22.2%)

77 (21.9 %)

351 (100%)

351 (100%)

n.a.

Used pawn shop or asset to pay debt

277 (25.7%)

161 (15.0%)

122 (11.3%)

351 (32.6%)

1,077 (100%)

n.a.

Used payday lender in 3 yrs

n a n a n.a. n.a. n.a. n.a.

2005

Zero account balance

695 (100%)

542 (78.0%)

61 (8.8%)

47 (6.8%)

90 (13.0%)

34 (4.9%).

Zero balance, no other debts

542 (100%)

542 (100 %)

45 (8.3%)

31 (5.7%)

59 (10.9%)

18 (3.3%).

Refused credit card

61 (38.1%)

45 (28.1%)

160 (100%)

29 (18.1%)

34 (21.3%)

21 (13.1%)

Used pawn shop in last yr

47 (43.5%)

31 (28.7%)

29 (26.9 %)

108 (100%)

108 (100%)

25 (23.2%).

Used pawn shop or asset to pay debt

90 (28.0%)

59 (18.4%)

34 (10.6%)

108 (33.6%)

321 (100%)

37 (11.5%).

Used payday lender in 3 yrs

34 (24.8%)

18 (13.1%)

21 (15.3%)

25 (18.3%)

37 (27.0%)

137 (100%)

Source: Author’s calculations from the 1999 and 2005 Surveys of Financial Security public files Notes: Those who have been refused a credit card do not have other credit cards.

21

Table 4. Pearson correlation coefficients for indicators of financial exclusion 1999 | Bal=0 Bal=D=0 CCref Pawn Pawn+ ------------------------------------------------------------------------------- Balance=0 1.0000 Bal=Debt=0 -0.0921 1.0000 CC refused 0.1106 -0.0598 1.0000 Pawnshop 0.1100 -0.0729 0.1583 1.0000 Pawn or asset 0.1021 -0.1320 0.1228 0.5574 1.0000 Source: Survey of Financial Security public file, 1999 (obs=15933) 2005 | Bal=0 Bal=D=0 CCref Pawn Pawn+ Payday -------------------------------------------------------------------------------------------- Balance=0 1.0000 Bal=Debt=0 -0.0909 1.0000 CC refused 0.1304 -0.0565 1.0000 Pawnshop 0.1296 -0.0656 0.2008 1.0000 Pawn or asset 0.1117 -0.1037 0.1121 0.5679 1.0000 Payday loan 0.0561 -0.1133 0.1170 0.1868 0.1429 1.0000 Source: Survey of Financial Security public file, 2005 (obs=5267) Notes: All coefficients are statistically significant at the 5% level Legend: Balance=0 (Bal=0) Zero account balance Bal=Debt=0 (Bal=D=0) Zero balance and no other debts CC refused (CCref) Refused credit card Pawnshop (Pawn) Used pawn shop last year Pawn or asset (Pawn+) Used pawn shop or asset to pay debt Payday loan (Payday) Used payday lender within three years

22

Table 5. Variable definitions and basic descriptive statistics from SFS samples 1999 2005 Variable Mean Std. Dev. Min Max Mean Std.Dev. Min Max Indicators of Financial Exclusion: Zero bank balance 0.1297935 0.3360867 0 1 0.131954 0.338473 0 1Refused credit card 0.0324484 0.1771933 0 1 0.030378 0.171641 0 1Used a pawnshop last year 0.0220297 0.1467848 0 1 0.020505 0.141734 0 1Used a pawnshop or sold asset last year 0.0675956 0.2510585 0 1 0.060946 0.239253 0 1Used a payday lender last three years 0.026011 0.159183 0 1 Determinants of Financial Exclusion: After-tax family income ($00,000) 7.582922 84.2511 -0.903 1000 0.659714 0.913773 -3.18325 13.86275Wealth or net worth ($00,000) 290.1814 1670.49 -2.53455 10000 6.679727 17.9828 -3.39775 497.5Age 48.73056 16.54499 16 80 50.12455 16.25082 17 80Total debt ($00,000) 68.76651 824.2748 0 10000 0.656881 1.341884 0 20.724Education: less than high school 0.2840645 0.4509819 0 1 0.207329 0.405432 0 1Education: graduated high school 0.2183518 0.4131404 0 1 0.242073 0.428379 0 1Education: non-university postsecondary cert. 0.2666165 0.442204 0 1 0.26087 0.439151 0 1Education: university degree or cert. (base) Education: not stated 0.0086613 0.0926649 0 1 0.006835 0.082399 0 1Family size 2.490491 1.361752 1 7 2.395671 1.268496 1 5Number of earners in family 1.292914 0.9448105 0 3 1.347257 0.939276 0 3Family composition: unattached individuals 0.2774117 0.4477354 0 1 0.289918 0.453767 0 1Family composition:couple without children (base) Family composition: couple with children 0.2970564 0.4569759 0 1 0.243213 0.429063 0 1Family composition: lone parent 0.0716751 0.2579573 0 1 0.048984 0.215856 0 1Family composition: other 0.0915082 0.2883395 0 1 0.062654 0.242363 0 1Family composition: children 0 to 4 years of age 0.1236428 0.3291839 0 1 0.070818 0.256545 0 1Family composition: children 5 to 17 years 0.2770351 0.447548 0 1 0.173913 0.379071 0 1Home ownership: own, no mortgage (base) Home ownership: own with mortgage 0.3219733 0.4672475 0 1 0.337384 0.472862 0 1Home ownership: do not own 0.3372246 0.4727771 0 1 0.309854 0.462477 0 1Region: Atlantic provinces 0.1789996 0.383364 0 1 0.152459 0.359499 0 1Region: Quebec 0.1655056 0.3716479 0 1 0.185305 0.388582 0 1Region: Ontario (base) Region: Prairie provinces 0.270696 0.4443333 0 1 0.249668 0.432862 0 1Region: British Columbia 0.14925 0.3563459 0 1 0.148662 0.355788 0 1Observations 15933 5267

23

Table 6. Probit Estimates of Financial Exclusion, 1999 (1) (2) (3) (4) Zero bal Ref credit Pawnshop Pawn or sold asset Income -0.359* -0.896* -0.509* -0.335* (0.074) (0.194) (0.183) (0.073) Income2 0.000* 0.001* 0.001* 0.000* (0.000) (0.000) (0.000) (0.000) Wealth -0.039* -0.063* -0.054** 0.012** (0.007) (0.018) (0.023) (0.005) Wealth2 0.000* 0.000* 0.000** -0.000** (0.000) (0.000) (0.000) (0.000) Age 0.046* 0.044* 0.008 0.019* (0.006) (0.009) (0.011) (0.007) Age2 -0.001* -0.001* -0.000** -0.000* (0.000) (0.000) (0.000) (0.000) Debt 0.000** -0.433* 0.000 0.000 (0.000) (0.114) (0.000) (0.000) <high sch 0.462* 0.581* 0.592* 0.153* (0.046) (0.089) (0.098) (0.052) High sch 0.247* 0.488* 0.312* 0.054 (0.046) (0.089) (0.099) (0.050) Non-univ 0.156* 0.407* 0.423* 0.062 (0.044) (0.089) (0.097) (0.048) Ed n/a 0.221 0.483 -0.268 (0.167) (0.363) (0.214) Family size 0.088* 0.012 0.119* 0.068** (0.024) (0.042) (0.044) (0.028) No.earners -0.149* -0.025 -0.139* -0.044 (0.023) (0.041) (0.046) (0.027) Unattached 0.013 0.205** 0.076 0.068 (0.046) (0.087) (0.099) (0.057) Couple, ch -0.068 0.039 0.086 -0.060 (0.061) (0.113) (0.124) (0.071) Lone parent 0.103 0.218** 0.165 0.126*** (0.065) (0.111) (0.124) (0.075) Other 0.020 0.314* 0.057 0.032 (0.062) (0.113) (0.136) (0.075) Chld 0-4 -0.030 0.135 -0.034 0.094*** (0.050) (0.084) (0.089) (0.056) Chld 5-17 0.044 0.172*** -0.048 -0.010 (0.052) (0.091) (0.099) (0.060) Home mtg 0.291* 0.369* 0.070 0.240* (0.041) (0.112) (0.119) (0.050) Don’t own 0.407* 0.710* 0.663* 0.390* (0.042) (0.088) (0.115) (0.053) Atlantic 0.429* -0.160** -0.105 -0.126** (0.042) (0.075) (0.090) (0.055) Quebec -0.080*** -0.042 -0.252* -0.244* (0.046) (0.070) (0.095) (0.057) Prairies 0.187* -0.007 0.196* 0.162* (0.039) (0.065) (0.073) (0.045) B.C. 0.063 0.064 0.251* 0.221* (0.047) (0.073) (0.081) (0.050) Constant -2.424* -3.195* -2.502* -1.961* (0.153) (0.256) (0.299) (0.180) Observations 15933 15933 15795 15933 Note: Standard errors in parentheses *** significant at 10%; ** significant at 5%; * significant at 1%

24

Table 7. Probit Estimates of Financial Exclusion, 2005 (1) (2) (3) (4) (5) Zero bal Ref credit Pawnshop Pawn or Payday sold asset Income -0.247* -0.557 -0.961* -0.242** 0.325 (0.089) (0.342) (0.361) (0.100) (0.510) Income2 0.020*** 0.084** 0.079 0.015 -0.411 (0.011) (0.040) (0.068) (0.013) (0.349) Wealth -0.016* -0.226* -0.100*** -0.001 -0.033 (0.005) (0.056) (0.060) (0.008) (0.035) Wealth2 0.000** 0.000* -0.001 -0.000 -0.000 (0.000) (0.000) (0.004) (0.000) (0.002) Age 0.045* 0.083* 0.054* 0.042* -0.018 (0.010) (0.017) (0.021) (0.012) (0.017) Age2 -0.001* -0.001* -0.001* -0.001* 0.000 (0.000) (0.000) (0.000) (0.000) (0.000) Debt 0.050** -0.198 0.054 0.045*** 0.038 (0.023) (0.140) (0.060) (0.024) (0.046) <high sch 0.545* 0.620* 0.135 -0.072 0.371** (0.077) (0.163) (0.153) (0.097) (0.145) High sch 0.249* 0.449* -0.112 0.063 0.246*** (0.071) (0.157) (0.148) (0.081) (0.128) Non-univ 0.228* 0.389** 0.049 0.021 0.267** (0.070) (0.158) (0.142) (0.081) (0.127) Ed n/a -0.429 0.757 0.771 0.197 1.336* (0.492) (0.664) (0.569) (0.369) (0.410) Family size 0.084** -0.068 0.049 0.070 0.155** (0.042) (0.085) (0.090) (0.050) (0.067) No.earners -0.130* -0.183** -0.325* -0.129* 0.099 (0.040) (0.082) (0.089) (0.048) (0.076) Unattached 0.064 -0.157 -0.284 0.012 0.141 (0.082) (0.164) (0.182) (0.102) (0.158) Couple, ch -0.225*** 0.183 0.066 -0.074 -0.114 (0.126) (0.270) (0.293) (0.151) (0.203) Lone parent -0.035 0.412*** 0.096 0.162 0.014 (0.145) (0.250) (0.283) (0.171) (0.236) Other -0.004 0.096 0.307 0.028 0.191 (0.105) (0.209) (0.210) (0.129) (0.171) Chld 0-4 0.136 0.120 -0.208 0.034 0.054 (0.102) (0.177) (0.196) (0.121) (0.151) Chld 5-17 0.056 -0.215 -0.170 -0.060 0.080 (0.090) (0.172) (0.185) (0.106) (0.138) Home mtg 0.199* 0.015 0.106 0.027 0.106 (0.072) (0.215) (0.220) (0.090) (0.164) Don’t own 0.294* 0.413** 0.483** 0.210** 0.611* (0.071) (0.171) (0.204) (0.091) (0.169) Atlantic 0.438* -0.119 0.097 -0.208** -0.273*** (0.072) (0.143) (0.162) (0.094) (0.151) Quebec -0.055 -0.141 -0.114 -0.357* -0.580* (0.075) (0.129) (0.159) (0.093) (0.160) Prairies 0.203* -0.071 0.121 -0.114 0.035 (0.066) (0.124) (0.142) (0.078) (0.111) B.C. -0.027 0.079 0.306** -0.060 0.215*** (0.079) (0.135) (0.146) (0.087) (0.115) Constant -2.339* -3.124* -2.271* -2.096* -2.276* (0.264) (0.489) (0.560) (0.325) (0.465) Obs 5267 5267 5267 5267 5267 Note: Standard errors in parentheses *** significant at 10%; ** significant at 5%; * significant at 1%

25

Table 8. Probit Estimates of Financial Exclusion, Combined Sample (1) (2) (3) (4) Zero bal Ref credit Pawnshop Pawn or sold asset Year=2005 0.156* 0.104** 0.111** 0.031 (0.027) (0.048) (0.054) (0.034) Income -0.253* -0.829* -0.592* -0.231* (0.052) (0.162) (0.151) (0.051) Income2 0.000* 0.001* 0.001* 0.000* (0.000) (0.000) (0.000) (0.000) Age 0.044* 0.053* 0.019*** 0.024* (0.005) (0.008) (0.010) (0.006) Age2 -0.001* -0.001* -0.000* -0.000* (0.000) (0.000) (0.000) (0.000) Wealth -0.020* -0.084* -0.065* 0.002 (0.004) (0.016) (0.020) (0.002) Wealth2 0.000* 0.000* 0.000* -0.000 (0.000) (0.000) (0.000) (0.000) Debt 0.000** -0.317* 0.000 0.000 (0.000) (0.086) (0.000) (0.000) <high school 0.504* 0.596* 0.462* 0.103** (0.039) (0.078) (0.080) (0.045) High school 0.260* 0.483* 0.182** 0.055 (0.038) (0.077) (0.081) (0.042) Non-university 0.188* 0.409* 0.302* 0.047 (0.037) (0.077) (0.078) (0.041) Education n/a 0.107 0.619** -0.053 -0.183 (0.153) (0.306) (0.407) (0.185) Family size 0.084* 0.024 0.102* 0.072* (0.019) (0.034) (0.035) (0.022) No. earners -0.149* -0.061*** -0.175* -0.068* (0.019) (0.036) (0.040) (0.023) Unattached 0.030 0.152** -0.006 0.054 (0.039) (0.074) (0.084) (0.049) Couple, children -0.113** 0.029 0.064 -0.078 (0.052) (0.100) (0.108) (0.061) Lone parent 0.078 0.231** 0.115 0.122*** (0.057) (0.096) (0.107) (0.066) Other -0.006 0.265* 0.124 0.011 (0.052) (0.097) (0.113) (0.064) Child 0-4 0.012 0.122*** -0.050 0.087*** (0.043) (0.072) (0.075) (0.048) Child 5-17 0.054 0.090 -0.048 -0.018 (0.042) (0.074) (0.078) (0.048) Home with mtg 0.291* 0.264* 0.087 0.184* (0.035) (0.097) (0.102) (0.042) Don’t own 0.408* 0.658* 0.618* 0.324* (0.036) (0.077) (0.098) (0.044) Atlantic 0.439* -0.151** -0.074 -0.157* (0.036) (0.066) (0.078) (0.047) Quebec -0.072*** -0.063 -0.225* -0.279* (0.039) (0.061) (0.081) (0.048) Prairies 0.189* -0.011 0.175* 0.090** (0.034) (0.057) (0.065) (0.038) B.C. 0.035 0.067 0.260* 0.150* (0.040) (0.064) (0.070) (0.043) Constant -2.457* -3.278* -2.446* -1.960* (0.131) (0.224) (0.259) (0.155) Observations 21200 21200 21200 21200 Note: Standard errors in parentheses *** significant at 10%; ** significant at 5%; * significant at 1%

26

Figure 1. Financial Exclusion by Family After-Tax Income Between $0 and $100,000

0.1

.2.3

Freq

uenc

y

0 20000 40000 60000 80000 100000After-tax household income

Zero account balance Refused credit cardUsed pawnshop

Source: 1999 SFS

0.1

.2.3

.4Fr

eque

ncy

0 20000 40000 60000 80000 100000After-tax household income

Zero account balance Refused credit cardUsed pawnshop Used payday lender

Source: 2005 SFS

27

Figure 2. Financial Exclusion by Family Net Worth Between $0 and $200,000

0.1

.2.3

.4Fr

eque

ncy

0 50000 100000 150000 200000Family net worth

Zero account balance Refused credit cardUsed pawnshop

Source: 1999 SFS

0.1

.2.3

.4Fr

eque

ncy

0 50000 100000 150000 200000Family net worth

Zero account balance Refused credit cardUsed pawnshop Used payday lender

Source: 2005 SFS