Analysis of Cost Estimating Through Concurrent Engineering Environment Through Life Cycle Analysis

10

Analysis of cost estimating processes used within a concurrent engineering environment throughout a product life cycle Christopher Rush, Dr. Rajkumar Roy, Department of Enterprise Integration, SIMS, Cranfield University, Cranfield, Bedford, MK43 OAL, United Kingdom. Tel: 44 (0) 1254 765261. Email: [email protected] Tel: 44 (0) 1234 754073. Email: [email protected] Abstract Concurrent engineering environments affect the cost estimating and engineering capability of an organisation. Cost estimating tools become outdated and need changing in order to reflect the new environment. This is essential, since cost estimating is the start of the cost management process and influences the ‘go’, ‘no go’ decisions concerning a new product development. This paper examines both traditional and more recent developments in order to highlight their advantages and limitations. The analysis includes parametric estimating, feature based costing, artificial intelligence, and cost management techniques. This study was deemed necessary because recent investigations carried out by Cranfield University highlighted that many concurrent engineering companies are not making efficient, wide spread use of existing estimating and cost management tools. In order to promote more efficient use of the discussed estimating processes within the twenty first century, this paper highlights the work of a leading European aerospace manufacturer and their efforts to develop a more seamless estimating environment. Furthermore, a matrix is developed that illustrates particular concurrent engineering environments to which each technique is aptly suited. 1. Introduction Cost is perhaps the most influential factor in the outcome of a product or service within many of today’s industries. More often than not, reducing cost is essential for survival. To compete and qualify, companies are increasingly required to improve their quality, flexibility, product variety, and novelty while consistently maintaining or reducing their costs. In short, customers expect higher quality at an ever-decreasing cost. Not surprisingly, cost reduction initiatives are essential within today’s highly competitive market place. Concurrent engineering is one such initiative. Since cost has become such an important factor of success, project development needs to be carefully considered and planned. Recent research demonstrates that companies unable to provide detailed, meaningful cost estimates, at the early development phases, have a significant higher percentage of programs behind schedule with higher development costs, than those that can provide completed cost estimates [1]. Therefore, it is essential that the cost of a new project development be understood before it actually begins. It could mean the difference between success and failure. This article is divided into three broad sections. The first highlights the increasing need for effective cost estimating and cost management techniques within a concurrent engineering environment. Cost estimating being defined as the process of predicting the cost/outcome of an as yet undefined project, and cost management being defined as a technique for managing the development processes in order to achieve the estimate. The second section of the paper discusses several available estimating and cost management techniques, in order to provide a broad overview and to better understand where and when to use them within a project life cycle. Furthermore, it promotes awareness concerning the traditional and more state of the art techniques that have emerged over the last decade. The final section presents a snapshot view of several leading concurrent engineering companies, which demonstrates how estimating and cost management techniques are being utilised within industry. This study highlights a general lack of structure and order concerning the use of current estimating techniques within concurrent engineering environments. In an attempt to counter this problem a matrix is developed to assist the choice of applying an estimating technique at different stages of a product lifecycle. 2. The need for cost estimating/engineering Cost estimating helps companies with decision- making, cost management, and budgeting with respect to product development. It is a methodology used for predicting/forecasting the cost of a work activity or output

-

Upload

emdad-yusuf -

Category

Documents

-

view

52 -

download

4

description

Cost Estimating Through Concurrent Engineering Environment

Transcript of Analysis of Cost Estimating Through Concurrent Engineering Environment Through Life Cycle Analysis

Analysis of cost estimating processes used within a concurrent engineeringenvironment throughout a product life cycle

Christopher Rush, Dr. Rajkumar Roy,Department of Enterprise Integration, SIMS, Cranfield University, Cranfield, Bedford, MK43 OAL, United Kingdom.

Tel: 44 (0) 1254 765261. Email: [email protected]: 44 (0) 1234 754073. Email: [email protected]

AbstractConcurrent engineering environments affect the costestimating and engineering capability of an organisation.Cost estimating tools become outdated and need changingin order to reflect the new environment. This is essential,since cost estimating is the start of the cost managementprocess and influences the ‘go’, ‘no go’ decisionsconcerning a new product development. This paperexamines both traditional and more recent developmentsin order to highlight their advantages and limitations. Theanalysis includes parametric estimating, feature basedcosting, artificial intelligence, and cost managementtechniques. This study was deemed necessary becauserecent investigations carried out by Cranfield Universityhighlighted that many concurrent engineering companiesare not making efficient, wide spread use of existingestimating and cost management tools. In order topromote more efficient use of the discussed estimatingprocesses within the twenty first century, this paperhighlights the work of a leading European aerospacemanufacturer and their efforts to develop a more seamlessestimating environment. Furthermore, a matrix isdeveloped that illustrates particular concurrentengineering environments to which each technique isaptly suited.

1. Introduction

Cost is perhaps the most influential factor in theoutcome of a product or service within many of today’sindustries. More often than not, reducing cost is essentialfor survival. To compete and qualify, companies areincreasingly required to improve their quality, flexibility,product variety, and novelty while consistentlymaintaining or reducing their costs. In short, customersexpect higher quality at an ever-decreasing cost. Notsurprisingly, cost reduction initiatives are essential withintoday’s highly competitive market place. Concurrentengineering is one such initiative. Since cost has becomesuch an important factor of success, project developmentneeds to be carefully considered and planned. Recent

research demonstrates that companies unable to providedetailed, meaningful cost estimates, at the earlydevelopment phases, have a significant higher percentageof programs behind schedule with higher developmentcosts, than those that can provide completed costestimates [1]. Therefore, it is essential that the cost of anew project development be understood before it actuallybegins. It could mean the difference between success andfailure.

This article is divided into three broad sections. Thefirst highlights the increasing need for effective costestimating and cost management techniques within aconcurrent engineering environment. Cost estimatingbeing defined as the process of predicting thecost/outcome of an as yet undefined project, and costmanagement being defined as a technique for managingthe development processes in order to achieve theestimate.

The second section of the paper discusses severalavailable estimating and cost management techniques, inorder to provide a broad overview and to betterunderstand where and when to use them within a projectlife cycle. Furthermore, it promotes awareness concerningthe traditional and more state of the art techniques thathave emerged over the last decade.

The final section presents a snapshot view of severalleading concurrent engineering companies, whichdemonstrates how estimating and cost managementtechniques are being utilised within industry. This studyhighlights a general lack of structure and order concerningthe use of current estimating techniques within concurrentengineering environments. In an attempt to counter thisproblem a matrix is developed to assist the choice ofapplying an estimating technique at different stages of aproduct lifecycle.

2. The need for cost estimating/engineering

Cost estimating helps companies with decision-making, cost management, and budgeting with respect toproduct development. It is a methodology used forpredicting/forecasting the cost of a work activity or output

C. Rush

Rush, C., and Roy, R. (2000). 'Analysis of cost estimating processes used within a concurrent engineering environment throughout a product life cycle.' 7th ISPE International Conference on Concurrent Engineering: Research and Applications, Lyon, France, July 17th - 20th, Technomic Inc., Pennsylvania USA, pp. 58-67.

[2]. It is the start of the cost management process. Costestimates during the early stages of product developmentare crucial. They influence the go, no go decisionconcerning a new development. If an estimate is too highit could mean the loss of business to a competitor. If theestimate is too low it could mean the company is unable toproduce the product and make a reasonable profit.

Many authors agree that 70-80% of a product cost iscommitted during the concept phase [2, 3, 4, 5]. Making awrong decision at this stage is extremely costly furtherdown the development process (see Figure 1). Productmodifications and process alterations are more expensivethe later they occur in the development cycle. Thus, costestimators need to approximate the true cost of producinga product, based on empirical data, with the purpose ofsatisfying both the customer and company.

Figure 1: Cost commitment curve

The difficulties of estimating at the conceptual designphase are well recognised [6, 7, 8, 9]. The major obstaclesestimators need to address are:• Working with a limited amount of available data

concerning the new development;• Accounting for step changes within technology over

the life span of a product development; a morepronounced problem within the aerospace industry;

• The requirements to show how cost estimates werederived including the assumptions and risks, and;

• The estimates need to be accurate.Therefore estimators/engineers need company-wide

co-operation and support, to assist them with theirdecision making. Concurrent engineering is an excellentinitiative to assist this process; however, it does present anew set of challenges as outlined below.

3. Cost estimating within a concurrentengineering environment

An optimised concurrent engineering environmentprovides an opportunity to substantially reduce the totalcost of a project. This is because, integrated product teams(IPTs) containing members of various skilled disciplines,enable a simultaneous contribution to an early productdevelopment and definition. Therefore, within a fullyintegrated product development (IPD) cycle,multidisciplinary teams working together increase thelikelihood of a reduced lifecycle cost by avoiding costlyalterations later in the design process. With this view inmind, concurrent engineering is a great step forward whencompared to an ‘over the wall mentality’, where eachdepartment works in ‘isolation’.

However, a concurrent engineering environmentpresents many new challenges to cost estimators whom, itcould be argued, are more used to predicting the cost of an‘over the wall’ environment. The impacts from adopting aconcurrent engineering philosophy are substantial andoften require significant changes to long-standing workingpractices. The whole culture begins to change. Existingcosting methods and systems soon become outdated andrequire updating to reflect the new environment. Thus,estimators find it extremely difficult to predict cost withinthis new environment with their existing tools. This is notall bad because it offers an opportunity to introduce newapproaches to old and possibly outdated workingpractices. This could cause difficulty for some, sinceadvances in technology and techniques have grownrapidly over the last decade. This period of change couldbe a daunting prospect unless practitioners have had theopportunity to follow recent trends and developments. Theremainder of this paper attempts to highlight and dispelsome of the mystique behind several state-of-the-art-estimating techniques, in order to make aware the choicesthat are currently available.

4. Cost estimating methods

4.1. Traditional cost estimating

In traditional costing there are two main estimates: a"first sight" estimate, which is done early in the cost stage,and a detailed estimate, done to calculate costs precisely.The former of these cost-estimating methods is largelybased around the experience of the estimator. Forexample it is not uncommon for a "first sight" projectestimate to be based upon a past similar project or purelyon experience in costing. However, to attain this level ofexperience takes years of apprenticeship and considerableoversight from senior estimators. Although useful for a

Scope forProductionCostReduction.

Production

70 -80%

Cost

Conceptphases

Cost committed

Cost incurred

Time

rough order of magnitude estimate, this type of estimatingis too subjective in today’s cost conscious culture andmore quantified and justified estimates are required [10,11].

For detailed estimates, cost is based upon the numberof operations, time per operation, labour cost, materialcost and overhead costs. Much of the information in adetailed estimate is based upon the internal synthetics(times or costs based upon expected rates of work for anyparticular task) of the company. To generate theseestimates, it is necessary to have an understanding of theproduct, the methods of manufacture/process andrelationships between processes. Detailed estimating goesthrough several iterations, since feedback from therelevant departments enables the estimates to be reviewedand improved. Thus, detailed estimating can be achievedonly when a product is well defined and understood.

Activity based costing (ABC) is a process formeasuring the cost of the activities of an organisation [12,13]. It is a quantitative technique used to measure the costand performance of activities e.g. inspection, productionprocesses and administration. Each activity within anorganisation is first identified and then an average cost isassociated. Once this is achieved it is then possible toestimate the amount of activity a product is likely to needand then associate the relative costs. This makes ABCappealing, since it combines estimates with hard data.This method follows similar processes to detailedestimating, and also requires a detailed understanding ofthe product definition. Thus, both detailed and ABCtechniques are not useful during the conceptual phase ofproject development. In order to estimate a project duringthis stage other approaches are required which arediscussed below.

4.2. Parametric estimating

A widely used method for estimating product cost atthe early stages of development is known as parametricestimating (PE). To illustrate this concept more clearly thefollowing example will suffice. Typically, for aircraftdevelopment, mass relates to the cost of production. Thatis, as the weight of the aircraft increases, so does the costof producing it. What’s more, this particular relationshipis often described as linear, as illustrated in Figure 2below.

In this hypothetical example the points of the graphrepresent the relationship of cost to mass for differentaircraft. The line traversing the points represents a linearrelationship i.e. as the mass increases so does the cost.Using relatively simple algebra it is possible to derive aformula to determine a mathematical relationship for costto mass. For the above graph the equation, y = ax + b isused to describe the line of best fit between the points.With the relationship described it is then possible to use

the formula to predict the cost of a future aircraft based onits weight alone. Within the field of cost estimating thisrelationship is known as a cost estimating relationship(CER).

Figure 2: Simple linear equation

This is a rather simplistic illustration describing themain principals of parametric estimating. Nonetheless,variations of this approach are a widely used methodwithin industry to predict the cost of a product underdevelopment and throughout the life cycle. As CERsbecome more complex involving several variables, morecomplex mathematical equations are used to describe therelationships. When CERs become too complex formathematical equations to solve, cost algorithms aredeveloped [3].

4.2.1. Using parametric estimating

Parametric estimating can be used throughout theproduct life cycle. However, it is mainly used during theearly stages of development and for trade studies e.g.within design to cost (DTC) analyses (see Section 5.2).Both industry and Government accept the techniques.Many authors commend its usefulness [2, 3, 5, 6].

However, PE does have its downsides, for example,CERs are sometimes too simplistic to forecast costs.Furthermore, PE is primarily based on statisticalassumptions concerning the cost driver relationships tocost, and estimators should not completely rely uponstatistical analysis techniques. Hypotheses, common senseand engineering knowledge should come first, and thenthe relationship should be tested with statistical analysis.Most CER literature describes the process for estimatingquantitative issues but not qualitative/judgmental issues.Cranfield University is currently researching this area andearly work demonstrates the validity of this innovativeapproach [10, 11].

In summary parametric estimating is an excellentpredictor of cost when procedures are followed, data is

MASS vs. COST COST = 6.0422 + 1.1591 * MASS

Correlation: r = .97161

MASS C

OST

8

14

20

26

32

38

2 6 10 14 18 22 26 30

meaningful and accurate, and assumptions are clearlyidentified and carefully documented. A relatively newform of PE is that of feature based costing. This hasbecome popular due to the rise and sophistication of CADtools. The implications of FBC are discussed below.

4.3. Feature Based Costing

The growth of CADCAM technology and that of 3Dmodelling tools have largely influenced the developmentof feature based costing (FBC). Researchers areinvestigating the integration of design, process planningand manufacturing for cost engineering purposes using afeature based modelling approach [14, 15, 16, 17].

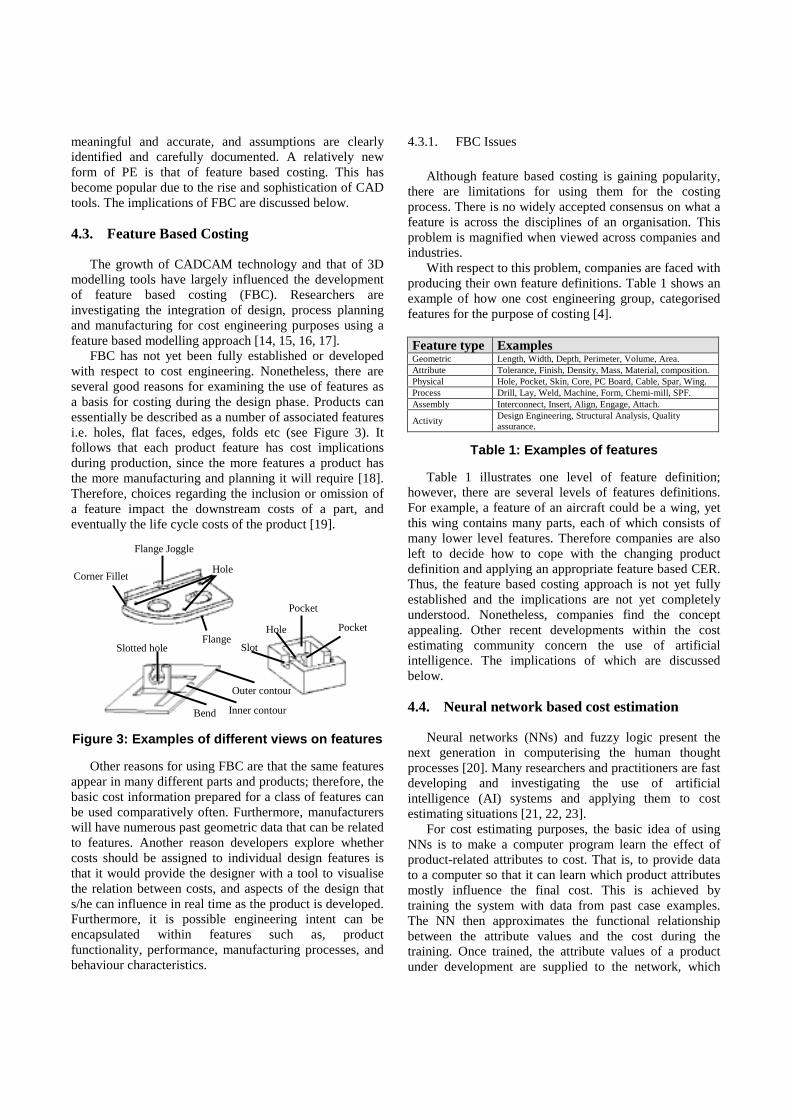

FBC has not yet been fully established or developedwith respect to cost engineering. Nonetheless, there areseveral good reasons for examining the use of features asa basis for costing during the design phase. Products canessentially be described as a number of associated featuresi.e. holes, flat faces, edges, folds etc (see Figure 3). Itfollows that each product feature has cost implicationsduring production, since the more features a product hasthe more manufacturing and planning it will require [18].Therefore, choices regarding the inclusion or omission ofa feature impact the downstream costs of a part, andeventually the life cycle costs of the product [19].

Figure 3: Examples of different views on features

Other reasons for using FBC are that the same featuresappear in many different parts and products; therefore, thebasic cost information prepared for a class of features canbe used comparatively often. Furthermore, manufacturerswill have numerous past geometric data that can be relatedto features. Another reason developers explore whethercosts should be assigned to individual design features isthat it would provide the designer with a tool to visualisethe relation between costs, and aspects of the design thats/he can influence in real time as the product is developed.Furthermore, it is possible engineering intent can beencapsulated within features such as, productfunctionality, performance, manufacturing processes, andbehaviour characteristics.

4.3.1. FBC Issues

Although feature based costing is gaining popularity,there are limitations for using them for the costingprocess. There is no widely accepted consensus on what afeature is across the disciplines of an organisation. Thisproblem is magnified when viewed across companies andindustries.

With respect to this problem, companies are faced withproducing their own feature definitions. Table 1 shows anexample of how one cost engineering group, categorisedfeatures for the purpose of costing [4].

Feature type ExamplesGeometric Length, Width, Depth, Perimeter, Volume, Area.Attribute Tolerance, Finish, Density, Mass, Material, composition.Physical Hole, Pocket, Skin, Core, PC Board, Cable, Spar, Wing.Process Drill, Lay, Weld, Machine, Form, Chemi-mill, SPF.Assembly Interconnect, Insert, Align, Engage, Attach.

Activity Design Engineering, Structural Analysis, Qualityassurance.

Table 1: Examples of features

Table 1 illustrates one level of feature definition;however, there are several levels of features definitions.For example, a feature of an aircraft could be a wing, yetthis wing contains many parts, each of which consists ofmany lower level features. Therefore companies are alsoleft to decide how to cope with the changing productdefinition and applying an appropriate feature based CER.Thus, the feature based costing approach is not yet fullyestablished and the implications are not yet completelyunderstood. Nonetheless, companies find the conceptappealing. Other recent developments within the costestimating community concern the use of artificialintelligence. The implications of which are discussedbelow.

4.4. Neural network based cost estimation

Neural networks (NNs) and fuzzy logic present thenext generation in computerising the human thoughtprocesses [20]. Many researchers and practitioners are fastdeveloping and investigating the use of artificialintelligence (AI) systems and applying them to costestimating situations [21, 22, 23].

For cost estimating purposes, the basic idea of usingNNs is to make a computer program learn the effect ofproduct-related attributes to cost. That is, to provide datato a computer so that it can learn which product attributesmostly influence the final cost. This is achieved bytraining the system with data from past case examples.The NN then approximates the functional relationshipbetween the attribute values and the cost during thetraining. Once trained, the attribute values of a productunder development are supplied to the network, which

Hole

Flange Joggle

Corner Fillet

PocketHole

SlotFlange

Slotted hole

Outer contour

Inner contourBend

applies the approximated function obtained from thetraining data and computes a prospective cost.

Recent work has demonstrated that neural networksproduce better-cost predictions than conventionalregression costing methods if a number of conditions areadhered to [21]. However, in cases where an appropriateCER can be identified, regression models have significantadvantages in terms of accuracy, variability, modelcreation and model examination [22].

4.4.1. Uses

The neural network does not decrease any of thedifficulties associated with preliminary activities whenusing statistical parametric methods, nor does it create anynew ones. The analyst is still left with a choice of costdrivers and must make a commitment to collectingspecific cost data before analysis can begin.

Models can be developed and used for estimating allstages of a product life cycle provided the data is availablefor training. A great advantage that a neural network hascompared to parametric costing is that it is able to detecthidden relationships among data. Therefore, the estimatordoes not need to provide or discern the assumptions of aproduct to cost relationship, which simplifies the processof developing the final equation [23].

4.4.2. Issues

Neural networks require a large case base in order tobe effective, which would not suit industries that producelimited product ranges. In addition, the case base needs tobe comprised of similar products, and new products needto be of a similar nature, in order for the cost estimate tobe effective. Thus, neural networks cannot cope easilywith novelty or innovation. With regression analysis onecan argue logically and audit trail the development of thecost estimate. This is because the analyst creates a CERequation that is based on common sense and logic. Whenconsidering neural networks, the resultant equation doesnot appear logical even if one were to extract it byexamining the weights, architecture, and nodal transferfunctions that were associated with the final trainedmodel. The artificial neural network truly becomes a“black box” CER. This is no good if customers require adetailed list of the reasons and assumptions behind thecost estimate. The black box CER also limits the use ofrisk analysis tools, which as discussed below, is a primebenefit of parametric estimating.

A final estimating technique to discuss is theanalogous method and more particularly that of case basedreasoning.

4.5. Case based reasoning

Analogy makes use of the similarity of products. Theimplicit assumption is that similar products have similarcosts. By comparing products and adjusting fordifferences it is possible to achieve a valid and useableestimate. The method requires the means of bothidentifying the similarity and differences of items. Thiscan be through the use of experience or databases ofhistorical products. A more modern approach to theanalogy method is case-based reasoning.

Case-Based Reasoning (CBR) can also be classed as aform of artificial intelligence since it can be used tomodel, store, and re-use historical data, and captureknowledge for problem-solving tasks. An importantfeature of CBR is the ability to learn from pastcases/situations. A CBR system stores and organises pastsituations, then chooses situations similar to the problemat hand and adapts a solution based on the previous cases.An overview of the CBR process is illustrated in Figure 4.

Figure 4: Case based reasoning process [24]

As with FBC, CBR relies on a feature descriptionbase. As previously explained this is not a straightforwardtask. Furthermore, CBR requires a number of past cases inorder to be effective. In a highly innovative company pastcases may not be available so will therefore reduce theeffectiveness of the CBR system. Companies that useanalogy estimates regularly may find CBR a more robustuseful method.

Section four has described the main estimatingtechniques and their related issues and promotes a broadunderstanding of both traditional and state-of-the-arttechniques. The next section describes and highlights themain techniques available for managing and reducingcosts in order to achieve the target of an early estimate.

Store

NewCase

NewCase

Problem

PreviousCases

RetrievedCase(s)

AdaptedSolution

TestedCase

Retrieve

ReuseRevise

SuggestedSolution

ConfirmedSolution

KnowledgeBase

Similarity

AdaptationVerification

Learning

5. Cost management and cost reduction

5.1. Value analysis and value engineering

Although similar to each other these techniques servedifferent purposes. Value analysis (VA) is concerned withthe analysis of a product with respect to reducingproduct/process costs. Typically, VA is a technique usedon existing items/products in light of new processes,materials or assembly methods being available. Valueengineering (VE) on the other hand is an approach thatrigorously examines the relationship between a productfunction and cost and can be used during the conceptstage. VE identifies the functions that are beneficial to thecustomer so that the value of a product is not justperceived as a low cost product, but rather one thatsatisfies the customer. This technique was used widelywithin the aerospace industry up until the 1970’s.However, with the introduction of tighter defence budgets,a more stringent technique was required for ensuring costtargets were achieved and design to cost was introduced.

5.2. Design to cost

The objective with design to cost (DTC) is to make thedesign converge to an acceptable cost, rather than to letthe cost converge to design. DTC activities, during theconceptual and early design stages, are one of determiningthe trade-offs between cost and performance for each ofthe concept alternatives. DTC can produce massivesavings on product cost before production begins.

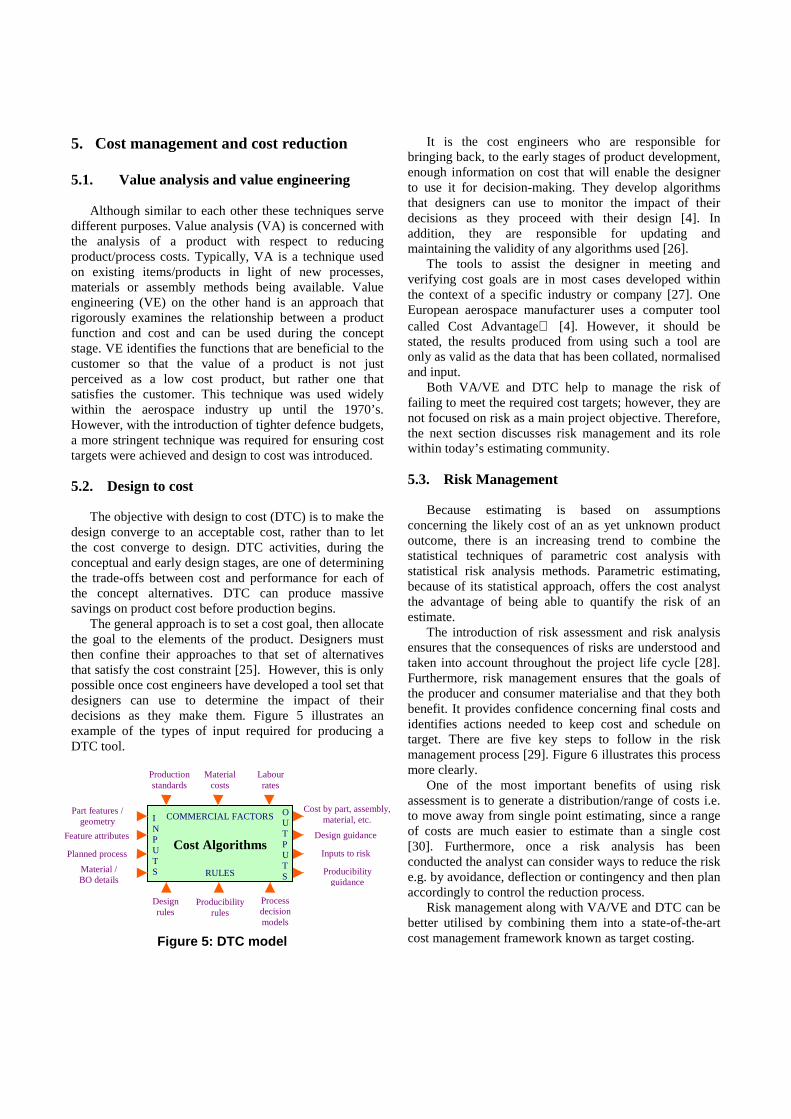

The general approach is to set a cost goal, then allocatethe goal to the elements of the product. Designers mustthen confine their approaches to that set of alternativesthat satisfy the cost constraint [25]. However, this is onlypossible once cost engineers have developed a tool set thatdesigners can use to determine the impact of theirdecisions as they make them. Figure 5 illustrates anexample of the types of input required for producing aDTC tool.

It is the cost engineers who are responsible forbringing back, to the early stages of product development,enough information on cost that will enable the designerto use it for decision-making. They develop algorithmsthat designers can use to monitor the impact of theirdecisions as they proceed with their design [4]. Inaddition, they are responsible for updating andmaintaining the validity of any algorithms used [26].

The tools to assist the designer in meeting andverifying cost goals are in most cases developed withinthe context of a specific industry or company [27]. OneEuropean aerospace manufacturer uses a computer toolcalled Cost Advantage [4]. However, it should bestated, the results produced from using such a tool areonly as valid as the data that has been collated, normalisedand input.

Both VA/VE and DTC help to manage the risk offailing to meet the required cost targets; however, they arenot focused on risk as a main project objective. Therefore,the next section discusses risk management and its rolewithin today’s estimating community.

5.3. Risk Management

Because estimating is based on assumptionsconcerning the likely cost of an as yet unknown productoutcome, there is an increasing trend to combine thestatistical techniques of parametric cost analysis withstatistical risk analysis methods. Parametric estimating,because of its statistical approach, offers the cost analystthe advantage of being able to quantify the risk of anestimate.

The introduction of risk assessment and risk analysisensures that the consequences of risks are understood andtaken into account throughout the project life cycle [28].Furthermore, risk management ensures that the goals ofthe producer and consumer materialise and that they bothbenefit. It provides confidence concerning final costs andidentifies actions needed to keep cost and schedule ontarget. There are five key steps to follow in the riskmanagement process [29]. Figure 6 illustrates this processmore clearly.

One of the most important benefits of using riskassessment is to generate a distribution/range of costs i.e.to move away from single point estimating, since a rangeof costs are much easier to estimate than a single cost[30]. Furthermore, once a risk analysis has beenconducted the analyst can consider ways to reduce the riske.g. by avoidance, deflection or contingency and then planaccordingly to control the reduction process.

Risk management along with VA/VE and DTC can bebetter utilised by combining them into a state-of-the-artcost management framework known as target costing.

COMMERCIAL FACTORS

Cost Algorithms

RULES

OUTPUTS

INPUTS

Planned process

Part features /geometry

Feature attributes

Material /BO details

Designrules

Producibilityrules

Processdecisionmodels

Inputs to risk

Cost by part, assembly,material, etc.

Design guidance

Producibilityguidance

Productionstandards

Materialcosts

Labourrates

Figure 5: DTC model

5.4. Target costing

Target costing (TC) is a cost management concept thatis well suited for use within a concurrent engineeringenvironment. It has mostly been used within theautomotive industry as a means of strategically managingcost. TC provides a framework that places costmanagement issues into the forefront from the earlyphases of product development and can be usedthroughout all phases of a product life cycle. However, itis mostly practised during the design and developmentstages where most of the decisions that impact life cyclecost are made [31]. TC is a framework in whichestimating becomes an integrated element. It combines theconcepts from existing cost management and costestimating/engineering tools e.g. VA/VE, DTC, riskmanagement, and bases its philosophy on the logic andbenefits of activity based costing.

5.3.1. Unresolved TC Issues

TC is not suited to all industries. It is best used on newproducts, which characterise small incrementaldevelopment changes from past similar products. Theconcept falls down when addressing the cost estimation ofinnovative products. Chiefly because, the process requiresa breakdown of how the components of a product willeffect the functionality of an, as yet, undefined product,and furthermore, what the cost of each product feature orcomponent will cost in relation to whole product. This isnot possible unless some sort of system has beendeveloped that has the capability of producing a detailedproduct definition/breakdown during these early stages.Therefore, it is not as yet, widely used for companies thatdevelop highly innovative products.

This concludes the discussion concerning availabletools for estimating within a concurrent environment.Both the advantages and limitations of current and futureestimating techniques have been summarised. Theremainder of the paper discusses how industry uses the

above techniques and also provides a matrix to assist withthe planning and application of a particular techniquethroughout the product life cycle.

6. State-of-the-art-practices

Seven high technology concurrent-engineeringcompanies were interviewed as part of recent work carriedout by Cranfield University [32]. The analysis wasconducted within three main areas: the use of CER's,general costing, and the types of computing tools adopted.

Only a few of the companies had developed CERs forthe manufacturing processes. These were either developedusing computer tools or using the experience of highlyskilled cost engineers. There seemed to be a lack offormal validation procedures for the CER’s and no type ofdocumentation seemed to be in place. There was generallyno formal approach for costing the conceptual or detaildesign stage. Companies that did attempt these estimatesseemed to rely mostly on expert knowledge with regardsto past data, which is fraught with subjectivity. Non of thecompanies had CERs to predict their design activities.

For general costing analysis there was a tendency forcompanies to use a computer-based tool at the detailedmanufacturing cost estimation level. The results producedfrom these analyses seemed to be fairly accurate. Mostcompanies could validate this through feedback fromproduction. Overall it was found cost benefit analysis wasnot being conducted. However, the companies did reviewtheir costing processes regularly, although there were nocosting standards used as guidelines for this process.

A variety of costing software was used for both highlevel and detailed costing, and there was a mix of the levelof integration with other business systems. Examples ofthe tools used included KAPES, PRICE (H), TIMSET andspecifically developed in-house systems.

6.1 The challenges faced by Europeanmanufacturing industry

The snapshot view highlighted that the application ofCERs within industry was not widely practised, and thosethat did use them did so badly. Companies could greatlyenhance CER effectiveness and use by examining theirprocedures and methodologies for creating them. Theapplication of CER’s for the design process was one noteven considered by the above companies. This was one ofthe underlying reasons that Cranfield University devised amethodology to take account of both the quantitative andqualitative issues of designing, and developed a CERmethodology for costing the design process [10, 11].

IdentifyRisks

AssessRisks

AnalyseRisks

ReduceRisks

ControlRisksFeedback

Figure 6: Risk Management Process

The use of features, artificial intelligence and casebased reasoning techniques were not used within any ofthe companies visited. And as mentioned earlier, few ofthem had adjusted their costing practices after theadoption of IPT or concurrent engineering practices. Fewcompanies had completed a benefits analysis on thecosting function.

In summary, there appeared to be a general lack ofplanning and order to the estimating process. In view ofcost becoming an ever-increasing concern cost estimatingand management needs a better focus. Companiesconsidering the adoption of a concurrent engineeringphilosophy should use the opportunity to re-examinecurrent practises and evaluate the possibility of adoptingsome of the more recent developments within the field ofcost estimating and engineering. Benchmarking theleaders can also assist this process.

6.2. Benchmark the leaders

In cost estimating and cost engineering the USA leadsthe way in both practice and development [3, 33]. InEurope the European Space Agency (ESA) activelypromotes the sharing of estimating best practices [34].

One leading European aerospace manufacturer iscurrently examining the feasibility of developing aseamless cost-estimating environment. Their earlydevelopment plans and intentions are to adopt a featurebased costing approach [4]. The company embraced thephilosophy of an IPD approach and has demonstrated astrong commitment towards concurrent engineering. Theyhave invested extensively into digital product assembly

methods and information management systems, which areused to discharge information in line with their concurrentengineering process development. The emergence of thenew IPD processes rendered their existing parametricestimating algorithms out of date, particularly for thedesign process. They seized this opportunity to embraceand integrate new estimating processes.

They recognised the potential of providing non-specialist cost estimators (design engineers) with acomputer tool to inform them about the costs incurredwith particular design approaches; in real time. Thiscapability would empower non-cost specialists to makedecisions related to cost improvements as they designedthe product. This potential was realised due to the adventof 3D CAD modelling systems, which store information,related to features throughout the product hierarchy.

The idea of the process is to capture features from theCAD modelling tools, which can then be integrated to adesign for manufacture (DFM) expert system that canprice the cost of a design in real time. The DFM toolunder evaluation is called cost advantage. It can acceptpart geometry directly from feature based modelling toolssuch as Pro-E and Unigraphics. It can be populated withdesign and manufacturing knowledge in the form ofproducibility algorithms so that it can evaluate a designbased on the features, materials, and manufacturability.This then empowers the designer to make decisionsrelated to cost as s/he worked.

Figure 7 illustrates a high level concept of thecompanies intent to integrate their cost modellingcapabilities using a feature based approach throughout theconcurrent engineering phases.

A B C D E F G

(LEVEL 3)

IPD PROCESS

PARAMETRIC COSTESTIMATION

(LEVEL 2)

(LEVEL 1)

COST DATABASE

PRODUCT FEATURES / COST DRIVERSPRODUCT FEATURES / COST DRIVERS

Support to otherCost/Business systems

DETAILED COSTESTIMATION

Project Concept In Service

Figure 7: Integrated cost modelling

Companies wishing to use this approach would need acomplete set of computerised tools that interface witheach other. An obvious drawback for companies that maywant to follow such an approach is the requirement for acomprehensive suit of expensive computerised tools.However, as computing power increases these toolsbecome available and accessible for other industries touse. This development work may provide futureestimators with an almost seamless system that can beused throughout the product lifecycle.

7. Matrix

Table 2 summarises where and when each of thetechniques and processes discussed in this paper are bestused throughout a product lifecycle.

The matrix shows that as a product moves throughdevelopment the estimating processes need to change. Thetable suggests hard breaks between where one techniqueshould be used against another. However, it should beborne in mind that parametric estimating (PE), neuralnetworks (NN), and case based reasoning (CBR) could beused during later project phases, whereas ABC anddetailed cost estimating cannot be used during the earlierproduct phases. Target costing (TC) is shown as usefulthroughout the product lifecycle, however, this is onlypossible when other estimating techniques and tools areintegrated into the TC framework. Neural networks arenot deemed suitable in the concept phase of innovativeproducts since the estimates they produce are of a ‘blackbox’ nature. That is, they do not provide a facility todemonstrate the assumptions and reasoning behind thefinal estimate.

8. Summary and Conclusions

This paper describes how cost is an increasinglyimportant factor of success within industry. And how costestimating and cost management is essential to thesurvival of leading companies. Several state-of-the-art-

techniques and processes, used to facilitate costestimating, have been discussed with particular referenceto their applicability within a concurrent engineeringenvironment. This provided a broad overview of thestrengths and weaknesses of each method. A snapshotview of several leading concurrent engineering companieswas provided, which demonstrated the general lack offormal, organised processes to the estimating function.One leading European aerospace company was discussedwith particular reference to their efforts at utilising andadvancing the cost estimating process. And finally amatrix was provided that details where each of thediscussed estimating processes should be used throughoutthe product life cycle.

In conclusion, there are a wide variety of emergingtechniques available that companies can utilise to improvetheir cost estimating and management processes. Artificialintelligence will play an increasingly important rolewithin the estimating communities. Because cost hasbecome such an influential factor cost estimators andengineers should be aware of these technologies so thatthey can utilise them to improve their cost managementprocesses. Although only a snapshot view of severalcompanies was conducted a general observation was thelack of formal, disciplined approaches to the estimatingprocess. Companies that want to continue succeeding andwinning contracts will need to become more efficient andproficient at estimating their new developments. In aworld of rapid change, increasing competition both localand global, the winners will be those that can confidentlypredict and successfully manage the cost of theirdevelopments. The tools are available lets start usingthem!

Acknowledgements

The authors would like to thank Geoff Tuer for hisinput and guidance to the work of this paper. This workhas been performed within the research project ‘Theintegration of quantitative and qualitative knowledge forcost modelling’. BAE SYSTEMS and EPSRC(Engineering and Physical Sciences Research Council) arejoint sponsors. The work is jointly developed andsupervised by BAE SYSTEMS and Cranfield University.

References

[1] HOULT D. P., MEADOR, C. L., DEYST, J., DENNIS, M.Cost Awareness in Design: The Role of DataCommonality, SAE Technical Paper, Number 960008,1996.

[2] STEWART, R., WYSKIDSA, R., JOHANNES, J., CostEstimator's Reference Manual, 2nd ed., WileyInterscience, 1995.

Table 2: Estimating process matrix

[3] DEPARTMENT OF DEFENCE. Parametric EstimatingHandbook, 2nd Ed., DoD, http://www.ispa-cost.org/PEIWeb/cover.htm, (1999).

[4] TAYLOR, I. M. Cost engineering-a feature basedapproach. In: 85th Meeting of the AGARD Structures andMaterial Panel, Aalborg, Denmark, October 13-14, 14:1-9,1997.

[5] MILEHAM, R. A., CURRIE, C. G., MILES, A. W.,BRADFORD, D. T. A Parametric Approach to CostEstimating at the Conceptual Stage of Design. Journal ofEngineering Design, 4(2): 117-125, 1993.

[6] PUGH, P. Working Top-Down: Cost Estimating BeforeDevelopment Begins. Journal of Aerospace Engineering,Part G, Vol. 206, pp. 143-151, 1992.

[7] I.L., CROZIER, P. AND GUENOV, M. [M.D.].Concurrent conceptual design and cost estimating.Transactions of 13th International Cost EngineeringCongress, London 9-12 October, 1994.

[8] MEISL, C. Techniques for Cost Estimating in EarlyProgram Phases. Engineering Costs and ProductionEconomics, 14: 95-106, 1988.

[9] WESTPHAL, R., SCHOLZ, D. A Method for PredictingDirect Operating Costs During Aircraft System Design.Cost Engineering, Vol. 39, (No. 6): pp. 35 – 39, 1997.

[10] ROY R., BENDALL D., TAYLOR J.P., JONES P.,MADARIAGA A. P., CROSSLAND J., HAMEL J.,TAYLOR I. M. Development of Airframe EngineeringCERs for Military Aerostructures. Second WorldManufacturing Congress (WMC'99), Durham (UK), 27-30th Sep., 1999.

[11] ROY R., BENDALL D., TAYLOR J.P., JONES P.,MADARIAGA A. P., CROSSLAND J., HAMEL J.,TAYLOR I. M. Identifying and Capturing the QualitativeCost Drivers within a Concurrent EngineeringEnvironment. Advances in Concurrent Engineering,Chawdhry, P.K., Ghodous, P., Vandorpe, D. (Eds),Technomic Publishing Co. Inc., Pennsylvania (USA), pp.39-50, 1999.

[12] DEAN, EDWIN B. Activity Based Cost from thePerspective of Competitive Advantage. NASA,http://mijuno.larc.nasa.gov/dfc/abc.html

[13] COKINS, GARY. ABC Can Spell a Simpler, CoherentView of Costs. Computing Canada, Sep 1, 1998.

[14] WIERDA, L. S. Linking design, process planning and costinformation by feature-based modelling, Journal ofEngineering Design, 2 (1), pp. 3-19, 1991.

[15] BRONSVOORT, W. F., JANSEN, F. W. Multi-viewfeature modelling for design and assembly. In: Advancesin Feature Based Manufacturing, Ch.14, pp. 315-329,1994.

[16] CATANIA, G. Form-features for mechanical design andmanufacturing. Journal of Engineering Design, 2 (1), pp.21-43, 1991.

[17] OU-YANG, C. AND LIN, T. S. Developing an IntegratedFramework for Feature Based Early Manufacturing CostEstimation. The International Journal of AdvancedManufacturing Technology, 13, pp. 618-629, 1997.

[18] BRIMSON, J. A. Feature costing: Beyond ABC. Journalof Cost Management, pp. 6-12, 1998.

[19] KEKRE, S., STARLING, S., THERANI, M. Featurebased cost estimation in design

http://barney.sbe.csuhayward.edu/sstarling/starling/working2.htm (accessed 22nd February, 1999).

[20] VILLARREAL, J. A., LEA, R. N., SAVELY, R. T. Fuzzylogic and neural network technologies. In: 30th AerospaceSciences Meeting and Exhibit, Houston, TX, January 6-9,1992.

[21] BODE, J. (1998). Neural networks for cost estimation.American Association of Cost Engineers, 40(1), 25-30.

[22] SMITH, A. E., MASON, A. K. Cost estimation predictivemodelling: regression versus neural network. EngineeringEconomist, 42 (2), pp. 137-162, 1997.

[23] HORNIK, K., STINCHCOMBE, M., WHITE, H.Multilayer feed-forward networks are universalapproximators. Neural Networks. Vol. 2, pp. 359-366,Cited in: Smith, A. E., Mason, A. K. (1997). Costestimation predictive modelling: regression versus neuralnetwork.. Engineering Economist, 42 (2), pp. 137-162,1989.

[24] AAMODT, A., PLAZA, E. Case base reasoning:Foundational Issues, methodological variations, andsystem approaches. Artificial IntelligenceCommunications, IOS Press, Vol. 7: 1, pp. 39-59, 1994.

[25] MICHAEL, J., WOOD, W. Design to cost. WileyInterscience, 1989.

[26] SIVALOGANATHAN, S., JEBB, A., EVBUOMWAN, N.F. O. Design for cost within the taxonomy of designfunction deployment. In: 2nd International Conference onConcurrent Engineering and Electronic DesignAutomation, Bournemouth, UK, pp.14-19, April 7-8, 1994.

[27] HEINMULLER, B., DILTS, D. M. Automated design-to-cost: Application in the aerospace industry. In: AnnualMeeting of the Decision-Science-Institute, San Diego, CA,Vol. 1-3, ch.569, pp.1227-1229, November 22-25 1997.

[28] EDMONDS, R. J. A case study illustrating the riskassessment and risk analysis process at the bid phase of aproject. British Aerospace Defence Limited, Dynamicsdivision, Ch. 2.

[29] TURNER, R: J. The handbook of project-basedmanagement. McGraw-Hill International (UK) Limited,1993.

[30] FORSBERG, S., KELVESJÖ, S., ROY, R., RUSH, C.Risk analysis of parametric cost estimates within aconcurrent engineering environment. Proceedings, 7th

International Conference on Concurrent Engineering,University Lyon 1, France, July 17-20th, 2000.

[31] HORVATH, P., NIEMAND, S., WOLBOLD, M. TargetCosting a State of the Art Review. CAM I ResearchProject, Niemand, University of Stuttgart, 1993.

[32] ROY R., BENDALL D., TAYLOR J. P., JONES P.,MADARIAGA A. P., CROSSLAND J., HAMEL J.,TAYLOR I. Development of Airframe engineering CERsfor military aerostructures. MSc group project, CranfieldUniversity, UK, 1999.

[33] HERNER, A. E. Joint Strike Fighter ManufactureDemonstrator, RTO Workshop on Virtual Manufacture,Aalborg, Denmark, October, 1997.

[34] NOVARA, M. AND WNUK, G. An ESA approach tolinked cost-engineering databases: Preparing for theFuture. Vol. 7, no. 1, March, 1997.