ANALYSIS AND APPRAISAL OF MICROFINANCE SECTOR IN THE ...

123

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP) ANALYSIS AND APPRAISAL OF MICROFINANCE SECTOR IN THE PHILIPPINES August 2020

Transcript of ANALYSIS AND APPRAISAL OF MICROFINANCE SECTOR IN THE ...

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

ANALYSIS AND APPRAISAL OF MICROFINANCE SECTOR

IN THE PHILIPPINES

August 2020

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Authors

Aldo Cera: Etimos Foundation IARCDSP Team Leader

Alberto Contarini: Etimos Foundation IACRDSP Microfinance Expert

Emiterio F. Sanson Jr.: Etimos Foundation IARCDSP Field Support Manager

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Executive Summary

Philippine financial system is comprised of formal and informal sub systems. The formal system consists of banks and non-bank financial institutions (NBFIs) while the informal sub system is comprised of those that are not included in the published statistics of the Bangko Sentral ng Pilipinas-BSP (Central Bank of the Philippines) like credit and multi-purpose cooperatives and microfinance NGOs. Since these institutions perform functions that are similar with those performed by the other recognized financial institutions in the system, they are considered significant players under the Philippine financial system, especially in microfinance.

Lending to the poor in the agriculture sector remains a challenge to this day: the complexity of agriculture brought about by the risks associated with agricultural economic activities poses some challenges to microfinance. Low-income households face limited opportunity to acquire new technology and working capital for agricultural production. Lending to small farmers is risky and entails high transaction costs thus commercial banks are discouraged to lend to this sector. Traders and money lenders are often the only alternative source of financing and continue to lend to those excluded by the banking system.

Small farmer-borrowers are more concerned about accessibility and timeliness of loans releases particularly during the onset of the planting season that they are no longer conscious about the interest rate pegged on their loan. Aside from providing production inputs on credit, the

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

informal lenders also provide cash loan for emergencies, education, and even for special events live wedding of a member of the household.

The objective of this appraisal report is to present the most recent finding on the microfinance sector in Philippines and in Mindanao in particular. The report introduces the state of art of the Microfinance sector and highlights appropriate innovative solutions (main actors, microfinance products, technologies, intervention schemes) that could be adapted according to the local context and characteristics/needs of the IARCDSP project stakeholder (ARBOSs/FOs).

The primary data was collected through consultations with local stakeholders representatives : DAR Central Project Management Unit and Manila Liaison Office, Italian Embassy, potential local partners (Saving &Credit Cooperatives, Banks, Microfinance Institutions, Central Bank, DAR Regional/Provincial Project Management Units (R/PPMUs), and other public institutions engaged in microfinance operations like the representatives of the MMC (Mindanao Microfinance Council) and the Cooperative Development Authority.

Results of this report indicate Microfinance is dominating the industry of alternative lending in the Philippines that is usually backed up by the development of high-tech services operating both online and offline. BSP has acknowledge these developments but emphasizes the necessity of developing financial technologies for a better financial inclusion.

This process of funding in order to be accessible and efficient for small farmers need to be digital (i.e. to minimize transaction costs) and needs

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

to cover the whole value chain – from providers of inputs over farmers and collective farming organizations to distributers and sellers of agricultural products.

The best tool for digitalization of the funding process is an electronic wallet – application designed to serve as a storage of funds/value and execute transactions among all stakeholders in the process. Electronic wallet needs to be operated by trusted financial institution with good knowledge and understanding of agricultural business and should be able to start with minimum viable product functionality to support the process and add new functionalities gradually in order to support the whole agricultural funding process for small and individual farmers.

The electronic wallet should also be able to support non-traditional and innovative funding models that would better cater for risks involved in the agricultural production such as Islamic finance or similar micro equity funding instrument or microinsurance or community supported model (including micro saving and guarantee funds schemes).

The report results led out, particularly for BARMM areas and adhering to the concept of financial technology-driven operations and management, the importance to provide solutions which are Shari’ah-compliant as the key to accelerating financial inclusion in the Bangsamoro Autonomous Region in Muslim Mindanao (BARMM).

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

List of Acronyms

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

AAIIBP – Al-Amanah Islamic Investment Bank of the Philippines

ADB – Asian Development Bank

ARB – Agrarian Reform Beneficiary

ARC – Agrarian Reform Community

ARBO – Agrarian Reform Beneficiary Organization

BARMM – Bangsamoro Autonomous Region in Muslim Mindanao

BSP – Bangko Sentral ng Pilipinas

CDA – Cooperative Development Authority

CSF – Credit Surety Fund

CARD – Center for Agriculture and Rural Development

CGFC – Credit Guarantee Fund for Cooperatives

DAR – Department of Agrarian Reform

DA – Department of Agriculture

DBP – Development Bank of the Philippines

DOF – Department of Finance

DCP – Directed Credit Program

DTI – Department of Trade and Industry

EU – European Union

FPSDC – Federation of People’s Sustainable Development Cooperative

GFI – Government Financial Institution

IC – Insurance Commission

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

IFAD – International Fund for Agricultural Development

IGLF – Industrial Guaranty Loan Fund

IARCDSP – Italian Assistance to the Agrarian Reform Community Development Support Program

ITA – Italian Technical Assistance

LBP – Landbank of the Philippines

LGU – Local Government Unit

MFI – Microfinance Institution

MABS – Microenterprise Access to Banking Services

MCPI – Microfinance Council of the Philippines Incorporated

MSME – Micro small and medium enterprises

NBFI – Non Bank Financial Institution

PDAP – Philippine Development Assistance Program

PhilHealth – Philippine Health Insurance Corporation

ROSCA – Rotating Savings and Credit Association

RBAP – Rural Bankers Association of the Philippines

SEC – Securities and Exchange Commission

SBC – Small Business Corporation

TSKI – Taytay sa Kauswagan Incorporated

USAID – United States Assistance for International Development

UNDP – United Nations Development Program

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

SZOPAD – Special Zone of Peace and Development in Mindanao

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Table of Contents

Executive Summary……………………………………………………………. ………………………………2

List of Acronyms………………………………………………………………. ………………….............4

Table of Contents……………………………………………………………………………………………….5

I INTRODUCTION……………………………………………………………………………………… ……………7

II. OBJECTIVES OF THE APPRAISAL REPORT………………………………………….. ….9

III. STATE OF THE ART METHODOLOGY……………………………………………………… ….9

IV FINDINGS FROM THE APPRAISAL………………………………………………………….10

IV.1 The beginning and the development of the microfinance sector in the Philippines………………………………………………………………….. ……………………………….10

IV.2 Situation of the financial system in the Philippines…. …………………….14

IV.3 Providers of Microfinance Products and Services ………………………………17

IV.3.1 Wholesale Microfinance Institutions …………………………………………………18

IV.3.2 Microfinance Councils and Associations…………………………… ………….20

IV.3.3 Federation of Cooperatives…………………………………………………………………. .22

IV.3.4 Microfinance Technical Assistance

and Support Service Providers…………………………………………………………….. ………….23

IV.3.5 Donor support to the microfinance sector ……………………………………….25

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

IV.4 CURRENT SITUATION IN THE MICROFINANCE SECTOR IN MINDANAO………………………………………………………………………………………………………. 28

IV.4.1 Related DAR Programmes in the Agrarian Reform Communities of Mindanao……………………………………………………………………………………………………….. 33

V RECENT DEVELOPMENTS AND INNOVATIONS IN MICROFINANCE 34

V.1 Mobile Banking……………………………………………………………………………………….. 34

V.2 Microfinance Housing …………………………………………………………………………….35

V.3 Microfinance in Agriculture…………………………………………………………………… 35

V.4 Business Development Services (BDS)………………………………………………. 35

V.5 Microinsurance………………………………………………………………………………………… 36

V.6 The Credit Surety Fund (CSF)………………………………………………………………. 38

V.7 The Islamic Finance……………………………………………………………………………… 39

VI.7.1 Distinguishing modes of Islamic Finance……………………………………. 40

VI.7.2 Islamic Finance actors in Philippines: Al Amanah Bank…………. 42

V ANALYSIS OF FINDINGS ON FINANCIAL SERVICES AND IARCDSP INTERVENTION OPPORTUNITIES…………………………………………………………….. 43

V.1 National Baseline Survey On Financial Inclusion………………………….. 43

V.2 Challenges for the microfinance sector ……………………………………………….47

V.3 Analysis of findings related to DAR-IARCDSP Microfinance Implementation……………………………………………………………………………………………….. 50

V.3.1 Weaknesses, Gaps and Challenges………………………………………………… 50

V.3.2 Demand and Supply……………………………………………………………………………. 53

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

VI CONCLUSION AND RECOMMENDATIONS……………………………………………. 54

VI.1 The Italian technical assistance (IARCDSP program)…………………… 54

VI.2 Recommendations related to the findings of this report……………… 56

VI.2.1 Recommendations that will require interventions in a wider scope from the concerned government agencies………………………………………………. 56

VI.2.2 Recommendations on pathways to be designed within the framework of the pilot projects implementation……………………………………. 62

VII. ANNEXES………………………………………………………………………………………………….64

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

I INTRODUCTION

The present appraisal report on microfinance in Philippines has been realized in the framework of the ITALIAN ASSISTANCE TO THE AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM - IARCDSP sponsored by the Italian government (Italian Agency for Development Cooperation -AICS).

The above initiative aims at reducing poverty in the rural areas of Mindanao, through the support at the Agrarian Reform implemented by the Government of the Philippines. In synthesis, the program will focus on supporting integrated development for the Agrarian Reform Beneficiaries in order to increase their incomes and quality of life. The Program is also in line with the on‐going peace process in Mindanao, in particular within the Autonomous Region in Muslim Mindanao (ARMM).

This working paper is the combination of perspectives from professionals working in the microfinance sector and research done on published microfinance industry reports, papers and articles and authors that are mentioned in the present documents. Valuable information and relevant data were also obtained from government institutions and agencies such as the Bangko Sentral ng Pilipinas (BSP), Department of Finance (DOF) and Insurance Commission, and from the private sector, the Mindanao Microfinance Council and the Microfinance

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Council of the Philippines Inc. (MCPI), the staunch supporters of the microfinance industry in the Philippines.

The present report has endeavoured to provide a clear insight into the state of affairs of the Microfinance industry in the Philippines starting from the development of the sector, to the regulatory framework, the actors and stakeholders, up to the challenges that the sector need to address in order to make real impact on the lives of the Poor Filipino households it is mandated to serve.

Lack of credit access is severe in low income and poor households in the country in general and in the Agricultural Reform Communities (ARCs) in particular. The low-income households are normally considered to have fewer opportunities to borrow from banks due to insufficient valuable assets for collateral security. These low-income households face limited opportunity to acquire new technology and working capital for agricultural production and thus tend to lag or fall behind. Providing access to financial capital in the ARCs through the Microfinance Scheme of the Italian Assistance to the Agrarian Reform Community Development Support Program (IARCDSP), being implemented by the Department of Agrarian Reform (DAR) is considered an important component of the government’s rural development strategy. Microfinance programmes have been gradually embedded in national strategies of many developing countries, including the Philippines as they are poverty-focused and aims to achieve livelihood sustainability in the long haul. The aim of the IARCDSP microfinance sub-component is to facilitate the access to financial services such as credit and microfinance products and services for the Agrarian Reform Beneficiary Organizations (ARBOs) who are usually disadvantaged in terms of access to conventional financial services from formal financial institutions.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Moreover, studies have shown that the growth of the microfinance sector, a good alternative source for rural credit, has been biased towards the urban areas. Majority of the MFIs are situated in the urban areas and have mostly been catering to the urban poor, who are engaged in retail or trading microenterprises. Considering that more than 50 percent of the poor reside in the rural areas, whose economic activities are mostly agriculture-based, the challenge is for microfinance institutions to meet the financial service needs of the rural, agriculture-based poor population .

Lending to the poor in the agriculture sector remains a challenge to this day. The complexity of agriculture brought about by the risks associated with agricultural economic activities poses some challenges to microfinance. While some MFIs have embarked on designing microfinance products for clients in the agriculture sector, evidence shows that the schemes were mostly saddled by high delinquencies after several cycles. The peculiarities of the agriculture sector make it difficult to design microfinance products that would fit all types of commodities in all localities. While market price fluctuations and systemic risks (e.g. climate change, pest and diseases) in agriculture are challenges beyond the microfinance sector, these are considered important factors on how the rural-agricultural based poor can be given continued access to financial services .

More recently, there is a growing interest on how microfinance can participate in value-chain financing. Given the importance of the input and the output market in ensuring profitability and sustainability of income from the agriculture sector, value-chain financing has long been recognized as an important concept in making agriculture profitable.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

However, value-chain financing in recent past have mostly been focused on small and medium-sized agri-based enterprises. If there were small farmers receiving credit from “value-chain financing”, this has mostly been provided through either input-suppliers or trader-lenders. Given these facts and considering that MFIs, especially those operating in the rural areas, are looking at effective means of helping their clients increase their incomes from their agriculture-based economic activities, the challenge is on how MFIs can participate in value-chain financing .

Very low margins impede the accumulation of capital to reinvest in next farming cycles. Therefore, a long-term oriented strategy to relief small farmers from their dependence from informal lenders is to improve their income generation and the selling price of their product. Valid solutions to sustain this strategy are to provide Business Development Services to assist ARBOs and farmers to enhance their business skills and market access, as well as to develop product processing facilities to increase the quality and value of agri-products. These solutions can be provided thru clustered or federated ARBOs to guarantee cost effectiveness and volumes.

The government launched and issued the National Strategy and the Regulatory Framework for Microinsurance in January 2010. These documents provide the pillars for the development of the microfinance sector in the Philippines and generally they call for increased private sector participation in the provision of credit solutions as well as risk protection to the low-income sector.

In this perspective Etimos Foundation will introduce innovative products and processes to be tested in some ARBOS identified among the beneficiaries of the IARCDSP.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

II. OBJECTIVES OF THE APPRAISAL REPORT

The present report have endeavoured to provide a clear insight into the state of affairs of the Microfinance industry in the Philippines starting from the development of the sector, to the regulatory framework, the actors and stakeholders, up to the challenges that the sector need to address in order to make real impact on the lives of the Poor Filipino households it is mandated to serve.

The scope of work also includes the analysis of many challenges and difficulties that faces the Agrarian Reform Beneficiary Organizations (ARBOs) in the Agrarian Reform Communities in order to identify gaps and weakness that have to be targeted during the project implementation.

III. STATE OF THE ART METHODOLOGY

This working paper is the combination of perspectives from professionals working in the microfinance sector and research done on published microfinance industry reports, papers and articles and authors that are mentioned in the present documents. Valuable information and relevant data were also obtained from government institutions and agencies such as the Bangko Sentral ng Pilipinas (BSP), Department of Finance (DOF) and Insurance Commission, and from the private sector, the Mindanao Microfinance Council and the Microfinance

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Council of the Philippines Inc. (MCPI), the staunch supporters of the microfinance industry in the Philippines

The study on which this working paper is based includes data, reports and other considerations drawing from the financial system and practical field experiences for analyzing and appraising the Microfinance situation in the Philippines in general and in Mindanao in particular.

The findings and recommendations presented in this working paper are the product of extensive consultations in the field through individual and group meetings with a variety of stakeholders, including the ARBOs, microfinance institutions (MFIs), microfinance clients, government officials, rural and microfinance banks, credit cooperatives, nongovernment organizations (NGOs), microfinance organizations (MCPI, Mindanao microfinance council) and some expert microfinance practitioners. In addition, relevant domestic and international studies, as noted and acknowledged herein, have helped in the realization of this working paper.

The remainder of this working paper elaborates the results in detail. Chapter IV discusses the situation of microfinance in the Philippines, including Mindanao, and recent developments and innovations.

Chapter V reports on the findings related to the DAR-IARCDSP microfinance implementation and finally Chapter VI outlines the conclusion and recommendations, including the strategies to be adapted in the implementation of the six (6) pilot projects under the IARCDSP.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

IV FINDINGS FROM THE APPRAISAL

IV.1 The beginning and the development of the microfinance sector in the Philippines

The Bangko Sentral ng Pilipinas (BSP) defines microfinance as the “provision of a broad range of financial services such as deposits, loans, payment services, money transfers and insurance products to the poor and low-income households and their microenterprises” . The financial service most commonly provided is microcredit which is typically issued and granted in the form of a specific business loan for microenterprise purposes. A key defining characteristic of a microfinance loan is the ability to secure credit without collateral. Microfinance loan providers in the Philippines often employ a group lending approach whereby each person within a small group is liable for any default by another group member. Other group lending-based methodologies being used in the Philippines include the ASA Model , whereby each group member is responsible only for his or her own loan.

The Philippines’ microfinance sector is credited by the Asian Development Bank as one of the oldest and most active in the world. While the roots of microfinance activity date back to the early 1900s through cooperatives, microfinance, as described today, surfaced in the 1980s and was codified into national law in 1997 with the signing of the Social Reform and Poverty Alleviation Act (R.A. 8425) and the establishment of both the National Anti-Poverty Commission and the National Strategy for Microfinance. The ultimate goal of the government’s National Strategy for Microfinance is to create a sustainable private microfinance market where the private sector drives market dynamics such as products and pricing and the government’s

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

role is limited to providing an environment which enables the market to thrive.

The low-income sector is perceived as a sector that do not have access to financial resources they need. With very low income, private formal financial institutions are reluctant to lend to the sector due to the perceived costs and risks associated with lending to the poor. Hence, from the 60s to the 80s, the government has mostly been providing financial services to the poor at subsidized interest rates.

Faced with this reality, the government implemented several credit programs targeted towards specific clientele groups. These credit programs were funded out of government resources and were implemented by government non-financial agencies, i.e. Department of Agriculture. For some credit programs, the government has tapped the private financial institutions to provide credit to the poor using government funds at subsidized interest rates. Perceived as government dole-outs, most of the credit programs suffered from very low repayment rates. This weakened the financial performance of several private financial institutions (rural banks in particular) which were used as conduits of cheap government funds. As a result, the flow of funds from most of the subsidized credit programs implemented during the period declined over time due mostly to high levels of default, disqualification of many borrowers and rural banks from program participation (due to massive default problems), the termination of major foreign-supported on-lending projects, and rediscounting restraints with the Bangko Sentral ng Pilipinas .

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

With the onset of financial reforms in the 80s, government terminated the implementation of subsidized credit programs in the agriculture sector. However, subsidized credit programs in the other sectors (industry, labor, science and technology) were continually implemented. In view of this, a strong lobby to bring back the implementation of subsidized credit programs was mounted resulting in the issuance of Cabinet Resolution No. 20 in 1986 which allowed the implementation of livelihood programs in all sectors, including agriculture. By the end of 1992, subsidized credit programs have once again mushroomed, undermining the government’s market-oriented credit and financial policy and the viability of the formal rural financial markets.

In view of this, the Social Pact on Credit was formed. This is an informal group comprised of representatives from various non-government organizations, people’s organizations, academe, concerned government agencies and government financial institutions. This informal group initiated discussions analysing the efficiency and the impact of the subsidized government Directed Credit Programs (DCPs) because the poor’s continued lack of access to credit despite the proliferation of government DCPs. These discussions led to the creation of the National Credit Council (NCC) under the Department of Finance (DOF) on 08 October 1999.

However, the development of the microfinance sector in the Philippines started to gain grounds only in the late 90s when the government realized the importance of providing viable, sustainable and realistic financial services to the poor. This bold move from the government was clearly mirrored in the National Strategy for Microfinance that was

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

launched in 1999 and issued by the National Credit Council under the Department of Finance as an offshoot of Executive Order No. 138, series of 1999. The National Strategy Framework is anchored on the following key policy principles:

I) Greater role of the private sector in the provision of financial services to the poor;

II) Establishment of an enabling environment that will facilitate increased participation of the

private sector in the provision of financial services to the poor;

III) Adoption of market-oriented financial and credit policies, and

IV) Non-participation of government non-financial agencies in the implementation of credit and guarantee program.

The adoption of the National Strategy led to the issuance and implementation of various policy measures that called for the non-participation of government in the delivery and implementation of subsidized credit programs and adoption of market-based credit and financial policies.

Realizing from past failures of government agencies in handling and managing credit delivery, the government veered away from directly intervening in the credit market. Several private financial institutions started to provide financial services to the poor. These are the rural banks and thrift banks, cooperatives engaged in savings and credit services and microfinance NGOs. Currently, a number of commercial banks like BPI, BDO, AlliedBank and UCPB, to name a few (mostly

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

engaged in wholesale microfinance operations) have also entered the market through the acquisition of smaller Thrift and rural banks and used these subsidiaries as vehicle to manage microfinance products and services.

The regulatory framework for microfinance developed by the National Credit Council recognizes the relevant regulatory authorities for each type of institution engaged in microfinance. Banks engaged in microfinance operations remain under the supervision of the Bangko Sentral ng Pilipinas. Cooperatives fall under the regulatory ambit of the Cooperative Development Authority (CDA) while microfinance NGOs, as non-deposit taking institutions are not subject to any prudential regulation. Microfinance NGOs, however, are required to register with and disclose to the Securities and Exchange Commission (SEC) that they are engaged in microfinance and related services.

The government have pursued market-oriented financial and credit policies that created incentives for greater private sector participation in the financial markets. It has then avoided costly, unsustainable and distorting credit subsidies.

The ensuing enabling policy and regulatory environment for MFIs ushered the growth and development of the Philippine Microfinance sector. From a few MFIs catering to a few thousands of clients in the early 90s, the microfinance sector has grown to several MFIs serving millions of clients starting in the middle of 2000.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Riding on the early success of microfinance lending activities, MFIs bonded themselves together and have organized both regional and national associations to provide technical support to members in terms of sharing knowledge, experience and information on the latest technology and developments in making MF operations more efficient and more responsive to MF clients’ needs. These associations also speak with one voice in advocating for relevant reforms to further develop the microfinance sector. Aside from the associations, several technical assistance and support service providers, some of which are funded internationally, also provide technical, and in some cases, financial support to MFIs. Most of these institutions cater to the MFI demand for training and capacity building services that would help them move towards greater outreach and efficiency .

The growth of the MF sector also welcomed innovations and developments. The advancement in technology as well as the popularity for mobile phones in the country led to the recognition of the huge potential of mobile banking particularly in the countryside. For instance in 2010, the MABS Program which was funded by the USAID pioneered some rural banks on innovative mobile phone banking in partnership with Globe Telecoms. Microfinance loan borrowers were able to transact loans and deposits through mobile phones. Other innovations in the sector include the development of additional products and services needed by microfinance clients. These are:

i) micro-agri loans to meet the funding requirement of farmers for farm inputs using the 60/40 formula ;

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

ii) microfinance housing to meet the housing improvement and repair needs of MF clients;

iii) microfinance that caters to the credit needs of clients in the rural areas;

iv) microloan product that finances water connection in some low-income households allowing them to have access to safe water supply;

v) partnership with PhilHealth in providing PhilHealth coverage to the MFI clients .

The poor, particularly the rural poor are vulnerable to risks such as illness, physical injury, accident or death, basic business risks, loss of property, and loss of job. MFIs realised the need to assist their microfinance clients with financial products that will help them manage these risks and/or provide financial relief when contingent events occur, hence the birth of microinsurance.

To realize the provision of microinsurance, the government through the Department of Finance (DOF)-National Credit Council (NCC) and Insurance Commission (IC) have developed the National Strategy and the Regulatory Framework for Microinsurance by calling on and enjoining the private insurance service providers to provide risk protection to the low-income sector.

Considering that most of the poor households are in the rural areas, there is also a need to design and innovate for the right MF product design for clients engaged in agricultural activities.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

As businesses of MF clients grow as years pass by, bigger amount of working capital is required which more often than not are beyond what MFIs can afford to lend due to limitation in the MFIs policy guidelines as well as in compliance with the Bangko Sentral ng Pilipinas’ Rules and Regulations (BSP Circular No. 272, 39 January 2001). The need for higher working capital, therefore, has to be addressed by formal financial institutions such as Rural and Thrift Banks.

Cooperatives engaged in savings and credit operations comprise a sizable number of MFIs. Latest figures (as of December 2018 from the CDA) show that there are 3,180 credit cooperatives and 14,885 multi-purpose cooperatives, about 80 percent of which are engaged in savings and credit operations. These cooperatives are significant players in microfinance. However, at present, these cooperatives are not regulated and supervised as it should be desired. According to Ms. Ma. Piedad Geron, an Industry Analyst who wrote the Microfinance Industry Report of 2010, the CDA seemed to have focused mainly on its developmental functions rather than on its regulatory functions. In part because the CDA Charter is ambiguous and does not grant the CDA the necessary authority to regulate cooperatives. The thrusts of the CDA need to be refocused and its policy and regulatory functions need to be enhanced so that it can help strengthen cooperatives in the areas of governance, management and operations, among others.

To sustain the development and growth of the Philippine microfinance sector, it is important that challenges such as those highlighted below

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

are looked into and addressed properly so that appropriate measures are instituted and adopted by the concerned stakeholders .

rationalization and optimization of government credit programs;

development of a credit delivery system that incorporates capability upgrading and institutional strengthening mechanisms;

encouraging greater private sector participation in the delivery of credit;

defining and rationalizing the role of guarantee programs and guarantee agencies.

IV.2 Situation of the financial system in the Philippines

Philippine financial system is comprised of formal and informal sub systems. The formal system consists of banks and non-bank financial institutions (NBFIs) while the informal sub system is comprised of those that are not included in the published statistics of the Bangko Sentral ng Pilipinas (Central Bank of the Philippines).

Banks are financial institutions regulated and supervised by the Bangko Sentral ng Pilipinas. They are categorized into universal and commercial banks, thrift banks, and rural and cooperative banks and are classified according to the amount of capitalization required and the type of services allowed. Universal Banks have the highest capital requirement. Together with commercial banks, they are authorized to

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

provide a wide range of financial services such as underwriting of investment houses and investments in equities of non-allied undertakings. Universal banks usually operate in cities and major urban areas. Thrift banks, on the other hand, are mostly engaged in providing short-term working capital and long-term financing to businesses. Meanwhile rural and cooperative banks have relatively lower capital requirements and are limited to only provide savings and credit services. They operate mostly in the rural and poor areas and provide the much needed financial services to rural communities such as farmers, fisher folks and micro and small enterprises.

At present, rural and cooperative banks are engaged in the provision of microfinance services (savings, loans, payment and money transfer for the low-income sector). The Bangko Sentral classifies these banks into two categories: microfinance banks are those whose total loan portfolios are 100 percent microfinance while microfinance-oriented banks are those that have at least 50 percent of microfinance loans in their gross loan portfolio.

Non-bank financial institutions (NBFIs), on the other hand, are entities that are engaged in financial services but may or may not have quasi-banking functions. These include the investment houses, financing companies, investment companies, securities dealers/brokers, fund managers, lending investors, pension funds, pawnshops, credit card companies, venture capital corporations and non-stock savings and loan associations.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

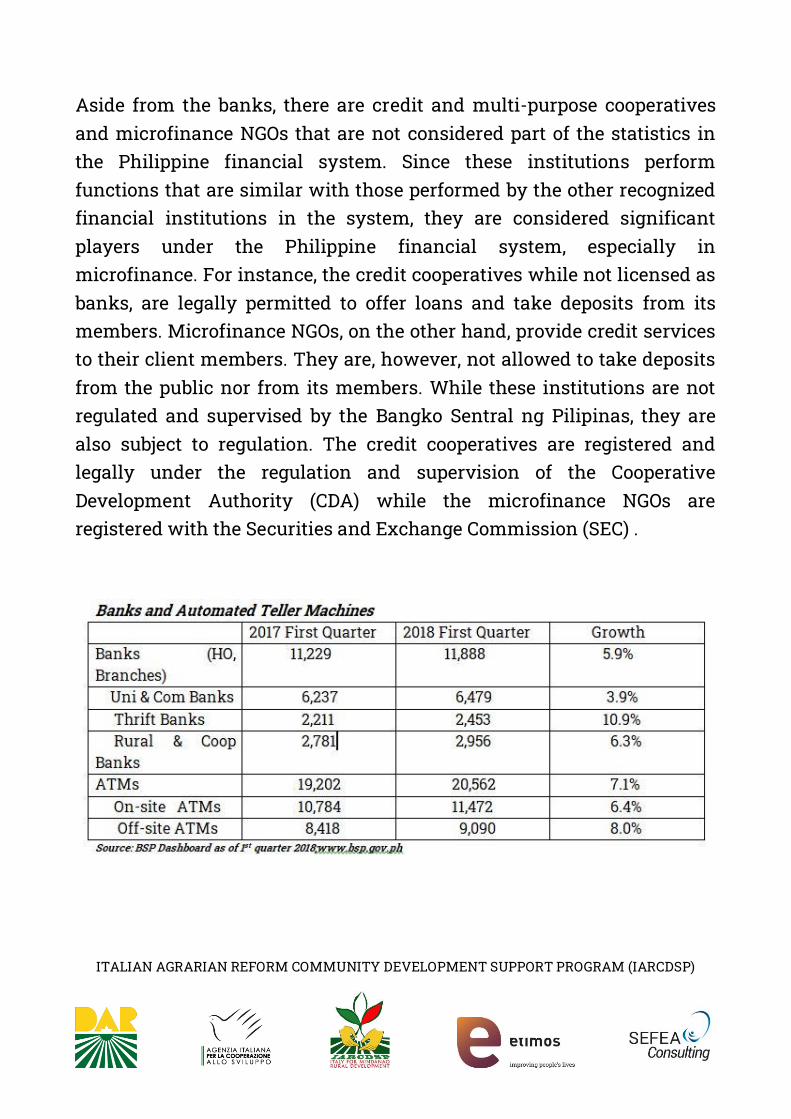

Aside from the banks, there are credit and multi-purpose cooperatives and microfinance NGOs that are not considered part of the statistics in the Philippine financial system. Since these institutions perform functions that are similar with those performed by the other recognized financial institutions in the system, they are considered significant players under the Philippine financial system, especially in microfinance. For instance, the credit cooperatives while not licensed as banks, are legally permitted to offer loans and take deposits from its members. Microfinance NGOs, on the other hand, provide credit services to their client members. They are, however, not allowed to take deposits from the public nor from its members. While these institutions are not regulated and supervised by the Bangko Sentral ng Pilipinas, they are also subject to regulation. The credit cooperatives are registered and legally under the regulation and supervision of the Cooperative Development Authority (CDA) while the microfinance NGOs are registered with the Securities and Exchange Commission (SEC) .

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

The informal finance system is composed of money lenders, trader lenders, input suppliers, and savings clubs and associations. These are entities providing credit services that are not registered with any authorized registering agency or entity.

Informal finance remains a valuable and significant source of funds among the low-income and marginalized sector. Among small farmers, for instance, majority still rely on informal credit sources such as traders, private money lenders, and relatives/friends for their working capital needs.

IV.3 Providers of Microfinance Products and Services

As the government veered away from directly intervening in the credit market, several private financial institutions started to provide financial services to the poor. There are:

Non-Government Organizations (NGOs)

Registered as non-stock, non-profit organizations, these are entities whose initial main objective is to provide developmental services to specific clientele in various geographical locations. As they provide developmental support services, a number of them realized and recognized that most of their target clientele are unable to engage in livelihood or entrepreneurial activities due to the lack of access to financial service.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

As a result, a number of these NGOs started to pioneer the provision of financial services to the poor through the use of the Grameen technology.

Cooperatives

Cooperatives engaged in the provision of savings and credit services are one of the low-income sector’s earliest sources of credit resources. Community-based and open-type cooperatives are registered institutions that can only provide services and transact with their members who usually belong to the lower middle-income sector and those living below the poverty line. While considered to be lending to the poor, most of these cooperatives use the member’s share capital as basis in determining the amount of the member’s loan.

Banks

Prior to the issuance of the National Strategy for Microfinance, most of the banks were reluctant to lend to the poor due to the perceived risks and transaction costs associated with lending to this sector. Their experience with government subsidized directed credit programs in lending to this sector have also contributed to this indifference. With the adoption of the market-based credit policies and the termination of the participation of government non-financial agencies, i.e. DA in the implementation of credit programs, an increasing number of private financial institutions (rural banks in particular) have ventured into microfinance. In 2001, the Bangko Sentral issued several circulars recognizing non-collateralized cash-flow based lending. Also, the moratorium on establishing bank branches was lifted for those banks

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

that will engage in microfinance operations. These regulatory policies coupled with some technical assistance encouraged an increasing number of rural banks to engage in microfinance operations.

Performance Standards for Microfinance Operations in the Philippines

As provided for in the regulatory framework and to ensure greater transparency in microfinance operations, the NCC in collaboration with concerned regulatory authorities and private sector representatives, developed the performance standards for microfinance operations in 2004. The Performance Standards focus on the following key areas of microfinance operations: Portfolio quality (40 percent), Efficiency (30 percent), Sustainability (15 percent) and Outreach (15 percent), otherwise known as the PESO standards.

Various stakeholders use the Performance Standards for varying purposes. For instance, in addition to the existing regulatory tools, the benchmarks are being used by the different regulators in assessing the financial institutions with microfinance operations that are under their supervision. Private and government wholesale financial institutions also use these standards, as complement to their existing guidelines, for evaluating the credit worthiness of a microfinance retail institution.

The managers of MFIs, on the other hand, use the indicators and standards to identify weak areas of operations that need specific or immediate management attention.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Domestic and international private investors use these standards as guideposts to decide whether to invest in a certain MFI. Donor agencies, for their part, are guided by these standards to more appropriately identify the type or area of assistance that is needed by a specific MFI.

Key government financial institutions such as the People’s Credit and Finance Corporation (PCFC), Land Bank of the Philippines (LBP) and the Development Bank of the Philippines (DBP) have adopted the various PESO indicators in evaluating and assessing the performance of retail microfinance institutions. Some wholesale commercial banks (e.g. Bank of the Philippine Islands, United Coconut Planters Bank) have also adopted the PESO in assessing and evaluating MFIs that would like to access their wholesale funds.

IV.3.1 Wholesale Microfinance Institutions

Lending funds of private retail financial institutions are sourced either from deposits in the case of banks and cooperatives, or external borrowings and donor funds. With the development of the microfinance sector in the Philippines and an increasing need for donor funds in transition economies, MFIs in the Philippines resort to either deposit mobilization (in the case of banks and cooperatives) and external borrowings as source of loanable funds. Government financial institutions (GFIs), which includes People’s Credit and Finance Corporation (PCFC), the Land Bank of the Philippines (LBP), the Development Bank of the Philippines (DBP) and the Small Business Corporation (SBC) are considered one of the important sources of external funds for MFIs. Credit policy reforms implemented by the government have limited the involvement of GFIs to the provision of wholesale funds for retail microfinance institutions.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Aside from GFIs that are allowed and mandated to provide wholesale lending funds at market rates, an increasing number of commercial banks are now engaged in providing wholesale lending funds to the microfinance sector (e.g. Bank of the Philippine Islands, Allied Bank, United Coconut Planters Bank and BDO) .

People’s Credit and Finance Corporation (PCFC)

PCFC is a government-owned and controlled corporation (GOCC) registered with the Securities and Exchange Commission authorized to operate as a financing company. It is tasked to provide microfinance services to poor households in the Philippines and to act as the lead government entity specifically tasked to mobilize financial resources from both local and international funding sources for microfinance.

As a wholesaler of microfinance funds, PCFC provides lending funds to its conduits comprised of cooperatives, rural and thrift banks, and non-government organizations – collectively called microfinance institutions (MFIs). PCFC provides MFIs any of the following :

• Investment Credit Facility – revolving wholesale credit to MFIs to support their relending activities to end-clients

• Institutional Credit Facility – for strengthening the MFIs capability to implement, manage and viably operate a microfinance project

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

• Capacity building – conduct of training, dialogues and conferences, assistance in setting up MIS and internal control systems

Land Bank of the Philippines (LBP)

The LBP is a government financial institution that was created under the Agrarian Reform Law in 1963. It was specifically created to provide financing support to agrarian reform beneficiaries. Today, it has evolved into a full-service commercial bank. However, it continues to fulfil its social mandate of promoting countryside development while remaining financially viable.

As one of the GFIs mandated by law to provide support to the microfinance sector, the LBP has provided guarantees to the loans obtained by PCFC from International Funders such as the ADB and the World Bank .

Development Bank of the Philippines (DBP)

The DBP was established by an act of congress in 1949 to provide banking services to SMEs. In support to the microfinance sector, DBP launched its Financing Program for Microfinance Enterprises (FPME) in 2001 where it allocated PhP500 Million pesos from its Window III facility for wholesale lending to retail MFIs .

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Small Business Corporation (SBC)

The SBC is the result of a merger between the Small Business Guarantee and Finance Corporation (SBGFC) and the Guarantee Fund for SMEs (GFSME) under Executive Order No. 98 in November 2001. The corporation is mandated to offer a range of financial services for small and medium enterprises engaged in manufacturing, processing, agribusiness (except crop level production) and services (except trading). These financial services include among other things, guarantee, direct and indirect lending, financial leasing, secondary mortgage, venture capital operations and the issuance of debt instruments for compliance with the mandatory allocation provision .

IV.3.2 Microfinance Councils and Associations

Microfinance Council of the Philippines (MCPI)

MCPI started in 1996 as a tactical coalition of NGOs engaged in microfinance – an offshoot of the USAID-funded Developing Standards for Microfinance Project. The coalition was initially comprised of 69 institutions and represented by the key stakeholders in microfinance in the Philippines. Aside from developing standards for microfinance, the coalition also conducted advocacy to key policymakers and concerned government agencies for the establishment of an appropriate policy environment for the growth and development of the microfinance sector.

The Microfinance Council of the Philippines, Inc. (MCPI) evolved out of a USAID-funded project entitled “Developing Standards for Microfinance Project” (DSMP) that started in mid-1996 and continued until the end of

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

1999. The MFIs that were part of the DSMP decided to form an association or network and the resulting organization, MCPI, was registered with the Securities and Exchange Commission (SEC) as a non-stock corporation in June 1999.

In 2004, MCPI merged with the Philippine Network for Helping the Hardcore Poor (PHILNET), a microfinance association focused on Grameen replicators in the Philippines. Since then, MCPI has grown to comprise 59 institutions, including 46 practitioners, 2 regional councils and 11 support institutions. It is estimated that MCPI members account for at least 75 percent of the total active outreach of the microfinance sector in the Philippines.

As a major industry player, MCPI serves as the voice of the microfinance community in advocating for policies that will promote a more inclusive, gender responsive, and client-friendly environment for microfinance. MCPI also promotes consciousness on the social value of a holistic approach to poverty eradication.

MCPI works closely with the Bangko Sentral ng Pilipinas on matters relating to the regulation of microfinance institutions, particularly banks and NGOs. MCPI also spearheaded the formulation of a Code of Practice for MFIs, initiated the drafting of the Standard Chart of Accounts for NGOs and promoted the MF Performance Standards for all types of institutions.

Currently, MCPI’s advocacy agenda is focused on tax issues, client protection and social performance.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Mindanao Microfinance Council Inc. (MMCI)

In the 1990s, the microfinance industry landscape in Mindanao was changing and confronted with challenges such as escalating competition among microfinance practitioners; an unprecedented demand for quality and value on the part of clients; and growing pressure from government regulation. Microfinance practitioners in Mindanao agreed to work together and establish an organization that will support the common interests of microfinance institutions in Mindanao; become their voice in the microfinance industry; and promote growth of and cooperation among MFIs to achieve desired results of poverty alleviation efforts of the Mindanao microfinance industry.

The Mindanao Microfinance Council (MMC) was formally registered with the Philippine Securities and Exchange Commission on March 25, 2004 and its first officers were elected and sworn in on March 30, 2004 during the 2004 Mindanao Microfinance Summit in Davao City.

True to its mission “to strengthen member institutions in delivering effective financial and capability development services to the poor and to develop them into effective catalysts of economic and social development of Mindanao”, MMC regularly provides training and education, and technical assistance to its member organizations in

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Western, Northern, Eastern, and Southern Mindanao. It also organizes conferences and meeting of MFIs and does research on and dissemination of best practices in the industry.

Rural Bankers Association of the Philippines (RBAP)

The RBAP is an organization comprised of rural bank owners and operating officers. The organization was formed to support and enable its members to offer quality banking services, comply with regulatory requirements and promote the welfare of the communities. RBAP provides various training programs on corporate governance, risk management, financial management, credit and fund management and other relevant areas that will help rural banks improve their operation.

In 1998, RBAP received a technical assistance from the USAID to implement the Microenterprise Access to Banking Services (MABS) Program. The program is an initiative to encourage the Philippine rural

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

banking industry to provide microenterprises access to microfinance services. In this regard, the MABS Program provides technical assistance and training to rural banks in the area of microfinance operations. Trained banks in turn offer microfinance loan and deposit services specifically tailored to microenterprise clients .

IV.3.3 Federation of Cooperatives

As of December 2018, there are 18,065 operating cooperatives, 2,596 are involved in credit and 637 are in agrarian reform. It would also be noted that 853 out of total coops are in Region 12 while no data of operations was reported for BARMM (ARMM).

Based on CDA definition, a cooperative is a duly registered association of persons with a common bond of interest, who have voluntarily joined together to achieve a lawful common social or economic end, making equitable to contribution to the capital required and accepting a fair share of the risks and benefits of the undertaking in accordance with universally accepted cooperative principle.

Based on CDA categories, there are different kinds of cooperatives. In general, these are: (1) Credit cooperative, which promotes thrift and savings among its members and creates funds in order to grant loans for productivity; (2) Consumer cooperative, the primary purpose of which is to procure and distribute commodities to member and non-members; (3) Producers cooperative, which undertakes joint production whether

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

agricultural or industrial; (4) Service cooperative, which engages in medical, and dental care, hospitalization, transportation, insurance, housing, labor, electric light and power, communication and other services; and (5) Multi- purpose cooperative, which combines two or more of the business activities of these different types of cooperatives. In terms of membership, cooperatives are classified as: (a) Primary, wherein the members are natural persons of legal age; (2) Secondary, the members of which are primaries; and (3) Tertiary, the member of which are secondaries upward to one or more apex organizations. Cooperatives whose members are cooperatives are called federations or unions

Under the Cooperative Code and based on international cooperative principles, primary cooperatives are enjoined to form or join cooperative federations. Cooperative federations are organized to provide assistance to its member cooperatives in the areas of education, business and advocacy. At present, there are a number of cooperative federations formed and organized in various parts of the country. The following are the big cooperative federations whose primary cooperative members are mostly engaged in microfinance operations.

National Confederation of Cooperatives

The National Confederation of Cooperatives (NATCCO) is a national federation of cooperatives that provides continuous capacity building services to its members in the following areas: good governance, financial management, accounting and bookkeeping, human resource management, and management information system. It also provides ancillary services such as the federation’s liquidity fund.38 NATCCO is also engaged in advocacy work related to the establishment of an appropriate regulatory environment for cooperatives. The federation also

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

participates in various legislative hearings on proposed bills involving cooperatives.

In 2006, NATCCO launched the Microfinance Innovations in Cooperatives (MICOOP) Project. The MICOOP Project seeks to help cooperatives in providing microfinance services to individuals who are engaged or wish to engage in microenterprises but have no access to financial services. The MICOOP Project provides capacity building assistance in the following areas: i) financial intermediation (savings and credit) operations and ii) microfinance operations. The MICOOP Project also provides assistance in improving the total savings and credit operations of the participating cooperative. NATCCO implements various models and schemes in helping its member-cooperatives become sustainable and viable microfinance providers.

As of June 2008, the MICOOP has established 59 branches strategically located all over the country and has garnered a total outreach of 79,550. Thirty-two of the branches operate according to the Build, Operate, Adopt, Transfer (BOAT) partnership arrangement while six branches have opted for the 50/50 investment partnership .

IV.3.4 Microfinance Technical Assistance and Support Service Providers

As MFIs expand their operations and as new institutions enter the microfinance market, demand for training and capacity building on microfinance increase.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

The following are institutions that provide these services.

PinoyME Foundation

PinoyMe Foundation is a private sector, multi-stakeholder, social consortium and movement whose main objective is to bring multiple sectors together to widen access of the poor to financial services. It aims to contribute to reducing poverty by providing five million poor people with financial and nonfinancial services and mobilizing PhP 5 billion in new capital for microfinance by 2021. It aims to achieve its goal through capacity building, resource mobilization, business development services, and knowledge management. The PinoyMe consortium consists of different institutions from the academe, MFIs, corporations, foundations, and NGOs .

MICRA Philippines

MICRA Philippines is a consulting and advisory firm that provides technical inputs and support to various stakeholders in the microfinance sector. As an independent resource center, MICRA is committed to promoting innovations, transparency, improved outreach to the poor and ever improving performance in the microfinance sector through the following services: i) training and technical assistance; and ii) research and innovations. MICRA provides these services on a fee-for-service basis .

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Oikocredit

Oikocredit is an international organization that provide support to the microfinance sector in the Philippines. It is a cooperative financial institution that finances and invests in microfinance institutions, cooperatives and small and medium- sized enterprises in developing countries, aimed at social impact. Oikocredit started to support projects in the Philippines in 1983 and has since approved loans amounting to PhP3.07 billion (€52.65 million). It has 44 active partners in the Philippines at present (17 in Luzon, 13 in the Visayas, and 14 in Mindanao) benefiting over 2.9 million economically active poor Filipinos, the majority of whom are women. At present, Oikocredit Southeast Asia offers the following types of products to its partner MFIs: loans, credit line, equity investment, and technical assistance .

Oikocredit is also one of the Pioneers that launched the first Social Performance Management (SPM) Peer Learning Community in collaboration with MCPI and Grameen Foundation.

Grameen Foundation

Grameen Foundation (GF) is a global foundation that helps the world’s poorest, especially women, improve their lives through access to microfinance and technology. In the Philippines, GF has provided support to some of the largest and most progressive MFIs since 2003. These MFIs are now considered the leaders in the Philippine MF sector. Realizing that smaller MFIs, are mostly found in the areas where most of the poor resides, GF started in 2009 to work with more MFIs and other stakeholders to bring the benefits of microfinance and technology to the rural areas where most of the three million poor and still unserved families reside.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

At present, GF provides assistance to the MFIs through a combination of catalytic capital, systems, automation, and social performance metrics. Grameen Foundation also works with other microfinance intermediaries to build a better infrastructure for collective action and encourage greater accountability, efficiency and transparency across the sector. Aside from providing access to capital (either through advisory services to assist MFIs in accessing commercial capital or direct lending capital) and help MFIs to automate and manage business information, GF also works with MCPI and Oikocredit in creating a peer learning community where local MFIs can develop a robust SPM strategy, implement a concrete SPM initiative, and share the critical lessons of implementation with each other .

Federation of People’s Sustainable Development Cooperative (FPSDC)

FPSDC is an organization comprised of non-government organizations, cooperatives and people’s organizations. FPSDC started from the Central Loan Fund (CLF) under the Philippine Development Assistance Program (PDAP) and has metamorphosed into a network of PDAP’s affiliate organizations that provide both financial and non-financial assistance to its member-organizations. At present, FPSDC has a credit facility and a social investment facility for its members. The former provides credit funds to its member organizations while the latter is designed to provide alternative investment opportunities to organizations to earn better returns for their money and at the same time support development initiatives of the disadvantaged communities. Aside from these, FPSDC also provides institutional support to beef up the capability of its members and partners to deliver financial and non-financial products and services, and to implement community enterprises to their respective clientele .

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

SEEDFINANCE Corporation

Founded in 2002, SEEDFINANCE Corporation is a nongovernmental organization that provides savings and loans products, as well as technical and implementation assistance, to poor and low-income individuals and small businesses in the Philippines. On 30 April 2007, SEEDFINANCE Corporation was registered as a financing company that will continue the work of CARE-USA (Cooperative for Assistance and Relief Everywhere-USA) and SEAD, Inc. (Sustainable Economic Activity Development, Inc.–Philippines). Both institutions were initially involved in providing microfinance services to the poor and low-income households through a network of partner organizations. As of April 2010, SEEDFINANCE and its 70 partner organizations work with approximately 1.2 million clients across the Philippines .

Other service providers

Other service providers in the Philippines are the following: Asian Institute of Management (AIM), Center for Development Management, Punla sa Tao Foundation, and the CARD Mutually Reinforcing Institutions Development Institute (CMDI). All of these institutions have various training modules on the different aspects of microfinance operations. CMDI, for its part, provides training in the following areas: microfinance management, social performance management, micro-insurance, basic financial management training, internal auditing and financial controls, training of trainers on micro-enterprise management, various lending methodologies, leadership and governance.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

At present, there are also various universities that are offering management courses, e.g., the Ateneo de Manila University and De la Salle University. In Ateneo, for instance, they are offering some courses that are focused on management of microfinance operations.

Aside from the foregoing there are other international development organization such as PlaNet Finance that has recently set-up local offices in the country. Likewise, international microfinance rating agencies such as Planet Rating and MicroFinanza Rating have also set up offices in the country indicating support and recognition of the robust and vibrant microfinance sector in the Philippines .

IV.3.5 Donor support to the microfinance sector

Foreign donors continue to support the development of the Philippine microfinance sector. Technical and funding assistance were and still are provided by the United States Agency for International Development (USAID), the United Nations Development Programme (UNDP), the Asian Development Bank (ADB), and the European Union (EU) and International Fund for Agriculture Development (IFAD).

United States Agency for International Development (USAID)

USAID has provided a three-pronged support to microfinance development in the Philippines. The first is the implementation of the Credit Policy Improvement Program (CPIP), a technical assistance to the National Credit Council (NCC) under the Department of Finance. CPIP provided technical assistance to the government (DOF-NCC in particular)

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

in establishing a policy and regulatory environment that encouraged the private sector to participate in the provision of microfinance services. CPIP was implemented from November 1996 to February 2006. This assistance resulted in the adoption of key policy reforms that provided commercialization impetus to the sector.

In addition to the policy level support, USAID also provided assistance to rural banks through the Microenterprise Access to Banking Services (MABS) Project. The MABS program is an initiative that supports the Philippine rural banking industry to significantly expand microenterprise access to bank-microfinance services. Specifically, the program provides technical assistance and training in various areas of microfinance operations to partner rural banks. Partner rural banks offer microfinance loans and deposit services specially tailored to microenterprise clients. Since its inception in 1998, the MABS Program has helped more than 230 rural banks and branches in the Philippines.

Aside from rural banks, USAID also provided assistance to cooperatives engaged in savings and credit operations through the Credit Union Enhancement and Strengthening (CUES) Program (ended in 2018). The main objective of CUES was to identify and transform credit cooperatives into safe and sound institutions. Aside from enjoining partner-cooperatives to adopt the model credit union approach in their operations, CUES also implemented a microfinance component (the Savings and Credit with Education -SCWE- component). Under the SCWE, women in the rural areas are organized into village centers and are provided microfinance services through the partner- cooperatives. Upon project completion, the partner-cooperatives had organized the

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Model Cooperative Network (MCN), which continued to provide similar technical assistance to its members.

Asian Development Bank (ADB)

In 2006, the ADB provided a US$150 million Microfinance Development Program loan to the Philippine government. The assistance focused on the following: strengthening the regulatory and supervisory capacities of concerned institutions for a sound microfinance sector; building the capacities of MFIs to provide cost-efficient microfinance services to the poor; and improving financial literacy and increasing consumer protection for the poor. Accompanying the program loan is a technical assistance and two grants that assisted concerned government agencies in implementing the needed reforms. The technical assistance focused on the following areas: i) development of consumer protection and business development services guidebook for MFIs; ii) development and implementation of training modules for various types of MFIs on the use of the PESO (Profitability, Efficiency, Sustainability and Outreach) performance standards; iii) development of the National Microfinance Literacy Program Framework and conduct of relevant training courses; and iv) provision of technical assistance to the National Credit Council (NCC) and the National Anti-Poverty Commission (NAPC) in implementing the relevant reforms to strengthen the regulatory environment for the microfinance sector.

United Nations Development Programme (UNDP)

In 1998, the Philippines became one of the recipients of the “Microfinance Support Project” (MSP) under UNDP’s Global MicroStart

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

Programme. The MSP assists partner MFIs to have efficient and sustainable microfinance operations using the ASA methodology. The MSP ended in 2001.

International Fund for Agricultural Development (IFAD)

Apart from financing projects related to agricultural development, IFAD also founded in 2011 a program for microfinance in the Philippines—the Rural Micro-Enterprise Promotion Program (RUMEPP). The program ended in 2018 and was focused in two main components: micro-credit and support component and the microenterprise promotion and development component. The first component provided loan funds and capacity building assistance to MFIs. Loan funds are provided at market rates through the Small Business Corporation (SBC) while capacity building includes training, systems development, and provision of institutional loans and matching grants to enable MFIs to open new microfinance windows in the program target areas. The second component provided efficient, cost-effective and demand-responsive business development services to rural micro-enterprises.

European Union (EU)

The EU provided assistance to specific area-based development programs. In addition to the development components of the programs, the EU also provided capacity building funds for partner-MFIs in the project area. For some projects, microfinance loanable funds were deposited as trust funds in and administered by the PCFC. The funds are then provided to their partner MFIs at market rates using the eligibility

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

and creditworthiness criteria of the wholesale lending institution. The partner-MFIs then lend to the program participants in the area.

Aside from these, the EU has also provided funding to improve financial inclusion and build social impact towards food security in Southeast Asia. The Philippines is one of the countries in the region that was given financial assistance. The program aims to build the capacity of MFIs and their networks to increase financial inclusiveness in rural areas in order to help farm households improve their food security. The program is being implemented in partnership with the Microfinance Council of the Philippines, Inc. (MCPI). It has the following components: i) strengthening MCPI’s capacity to serve its members & stakeholders; ii) strengthening MFI operations through customized on-site coaching and mentoring of MFI staff using the social performance management (SPM) approach; iii) providing support for the development and testing of new or improved financial services for farm households; and iv) training rural households on their rights and responsibilities as microfinance clients.

International NGOs and Foundations.

Aside from the Official Development Assistance (ODA) provided by foreign donors through the government, a number of international NGOs also provided assistance to the Philippine microfinance sector. Assistance is usually coursed directly to MFIs or network of MFIs (e.g., MCPI, cooperative federations, and regional microfinance councils). These include, among others, the following: Interchurch Organisation for Development Cooperation (ICCO), CORDAID, Small Enterprise Education and Promotion Network (SEEP), ECLOF, and Oikocredit.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

IV.4 CURRENT SITUATION IN THE MICROFINANCE SECTOR IN MINDANAO

In spite of the goals achieved in the microfinance sector, the current situation in Mindanao as well in all the country shows that there is still a long way to go towards financial inclusion, which can be estimated in terms of the following: (a) access – supply and availability of different microfinance products and services; (b) usage – use of different financial products and services; (c) quality –experience of the consumer, measured in terms of attitudes and opinions towards those currently available products (d) welfare – impact of a financial product or service on the lives of consumers, including changes in consumption, business activity and wellness.

The on-going policy of the Republic of Philippines aims to address the sources of grievance of previously conflict-affected communities and prioritise its interventions to accelerate barangay-focused rehabilitation and development. Along with the peace process, the government’s approach to eradication of poverty is focused on “creating ten million jobs by supporting the development of three million entrepreneurs and on developing at least two (2) million hectares of new lands for agribusiness”. Under this strategy, the government set to make “super region” Mindanao as the country’s main agro-fishery export zone”. With regards to micro-finance, one of the main challenges is that formal financial providers cannot reach those who have effective demand for outside financing in the target area due to established stringent banking requirements. The Return on Investment (ROI) pursued by enterprising individual borrowers are thus reduced as they are forced to avail of loans

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

from the unregistered sources, mostly traders and money lenders, who usually charge much higher interest rates than the formal sources.

In addition, empirical evidence shows that microfinance services thrive in areas with relatively better infrastructure, and that there is “a severe lack of microfinance services in areas with poor physical infrastructure since this means unacceptably high risks and transaction costs”.

In Mindanao, the large commercial farms (pineapple, cavendish bananas, rubber and palm oil plantations) have access to loans from both government and private commercial banks. Large agribusiness companies that operate commercial farms, particularly cavendish bananas have entered into contract-growing schemes with farmers to grow this crop. The Davao Region and parts of Bukidnon Province is the dominant producers of cavendish bananas in the country. These firms are highly capitalized and can use their internal funds to finance commercial operations. Even farms that have shifted and diversified into livestock and poultry were also able to borrow from private and government banks. The large demand for chicken and pork particularly in urban and commercial areas has made livestock and poultry business a profitable venture for commercial growers. Government and Private commercial banks have lent and are still lending to these borrowers without having to depend on government credit funds. However, Smallholder agriculture engaged in rice and corn production could not have access to funding from private commercial and government banks. The main sources of formal loans are the Land Bank of the Philippines (LBP) and rural banks. The credit programs of the Land Bank of the Philippines currently supporting agriculture are mainly for primary production of rice and corn. However, in reality, most of the small farmer borrowers continue to depend on informal lenders mainly traders,

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

money lenders and even relatives for their production financing. Also, the traditional banks have failed to innovate and develop credit products nor have simplified their lending procedures that would allow small farmers access to their loan facilities.

Access to loans is more visible among large agribusiness corporations who have the 5Cs – Capital, Character, Collateral, Capability and Conditions which makes for a good risk management on the part of the formal lenders. While small farmers on the other hand are limited to informal lenders. Lending to small farmers is risky and entails high transaction costs thus commercial banks are discouraged to lend to this sector. Traders and money lenders are the only alternative source of financing and continue to lend to those excluded by the banking system. Small farmer-borrowers are more concerned about accessibility and timeliness of loans releases particularly during the onset of the planting season that they are no longer conscious about the interest rate pegged on their loan. Informal credit also offer products that are specifically designed to meet the needs of small farmer-borrowers. Aside from providing production inputs on credit, the informal lenders also provide cash loan for emergencies, education, and even for special events live wedding of a member of the household.

The collection of data to draw a clear picture of the microfinance situation in Mindano resulted quite difficult. Etimos F. met representatives of the Mindanao Microfinance Council but no significant data can be extracted from their office because members have not submitted statistics and financial statements since 2015.

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

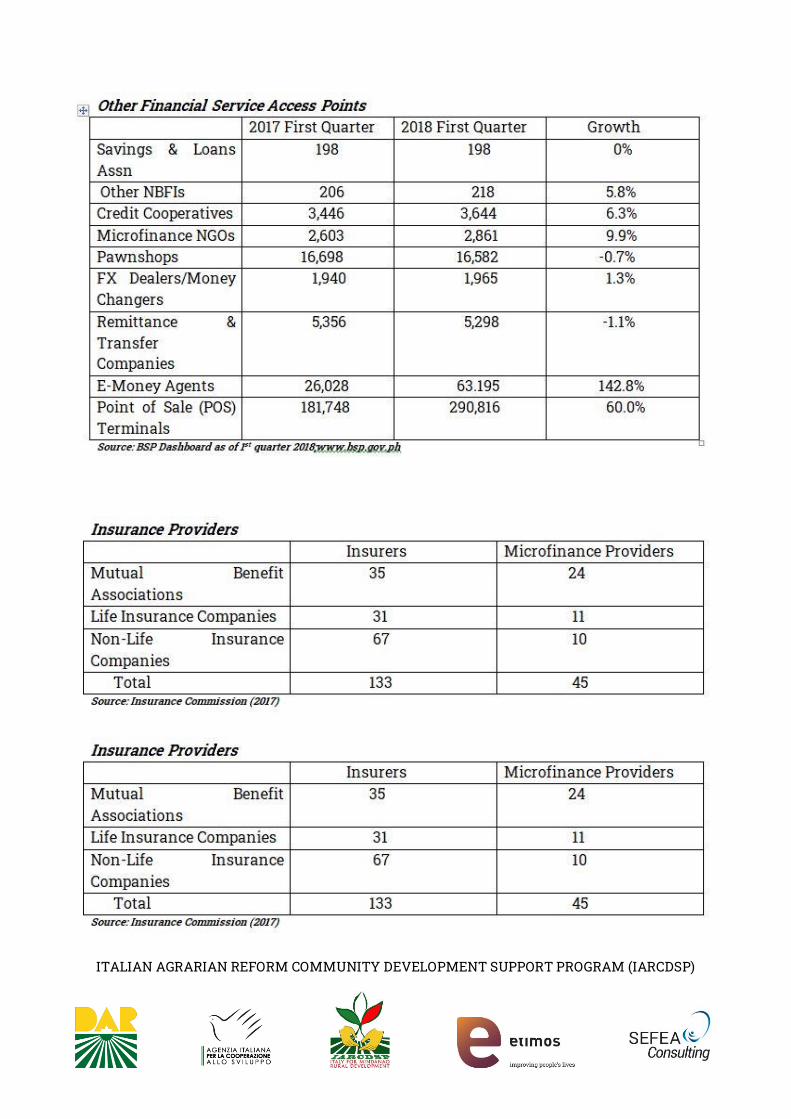

The data available are mainly coming from formal sector according to the following tables:

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

ITALIAN AGRARIAN REFORM COMMUNITY DEVELOPMENT SUPPORT PROGRAM (IARCDSP)

The major provider of Microfinance services in IARCDSP covered areas are reported in the following table: