AN EMERGING NORTH AMERICAN GOLD-SILVER...

31

AN EMERGING NORTH AMERICAN GOLD-SILVER PRODUCER OCTOBER2016

-

Upload

duongquynh -

Category

Documents

-

view

218 -

download

0

Transcript of AN EMERGING NORTH AMERICAN GOLD-SILVER...

AN EMERGING NORTH AMERICAN GOLD-SILVER PRODUCER

OCTOBER2016

www.rcgcorp.ca

Disclaimer

This presentation contains ‘forward-looking statements’ as defined or implied at common law and within the meaning of the Corporations Law. Such forward-looking statements may include, without limitation: (i) estimates of future gold, silver and copper sales; (ii) estimates of future cash costs; (iii) estimates of future capital expenditure; (iv) statements regarding the sensitivity of reserves to commodity prices; and (v) statements regarding future exploration results and the replacement of reserves.

Where the Company or any of its officers or directors or representatives expresses or implies an expectation or belief as to future events or results, such expectation or belief is expressed in good faith and the Company or its officers or representatives as the case may be believe to have a reasonable basis for implying such an expectation or belief. However, forward-looking statements are subject to risks, uncertainties and other factors, which could cause actual results to differ materially from future results expressed, projected or implied by such forward-looking statements. Such risks include, but are not limited to, gold, copper, silver and other metals price volatility, currency fluctuations, increased production costs and variances in ore grade or recovery rates from those assumed in mining plans, political and operational risks in the countries in which we operate, and governmental regulation and judicial outcomes.

The Company does not undertake any obligations to publicly release revisions to any ‘forward looking statement’, to reflect events or circumstances after the date of this release, or to reflect the occurrence of unanticipated events, except as may be required under applicable securities laws.

www.rcgcorp.ca

Introduction

3

Resource Capital Gold Corp. (TSXV: RCG) is an emerging precious metal (Au-Ag) developer and producer with a pipeline of late-stage exploration, development and producing assets in North America. • All projects located within prolific gold-silver regions • Targeting low CAPEX / OPEX processing routes with early cash flows

– First cash flows FY17 – Staged development to unlock value – First quartile cost profile

• Management team with proven success in mine development, operation and turnaround – Management and board ownership: 28.3%

• Substantial upside vs. base case NPVs and project NAVs • Recent restructure with balance sheet recapitalization

www.rcgcorp.ca

Project overview

4

Nova Scotia Gold Fields roll-up 90% ownership of fully permitted Dufferin Gold Mine with 300 t/d gravity flotation mill and all necessary infrastructure in place; PEA and resource estimate in progress; projected C$623 cash cost per Au ounce; restart to production within 90 days. • Staged buy-out for minimal upfront cash1 and at deep discount to project NPV • Acquisition of two additional past-producing high-grade gold mines with in-situ resources, 3rd mine under negotiation

Nevada Silver-Gold Project Investment right to control 80% of a Corcoran Canyon silver-gold project with a 33.3Moz Ag eq2 historical resource in place; cash cost US$5.97 per Ag eq. ounce; fast track to production; at current metal prices3 cumulative projected EBITDA of US$190M, NPV6 US$141M and IRR of 353%. • Low cost of entry for a drilled Ag-Au resource, US$2.6 million staged earn-in at an implied valuation of US$3.3m

1 Total acquisition cost US$9.5m payable over 5 years; plus 1% NSR (from year 5) 2 30.5Moz Ag + 37,100oz Au RCG is not treating this as a current mineral resource 3 US$17 Ag and US$1,200 Au

www.rcgcorp.ca

Leadership team

5

George Young Chairman and CEO: 35 years of experience acquiring, financing and developing mines in North and South America, both as a metallurgical engineer and as a lawyer. Has been instrumental in over US$600 million in financings for both major and junior mining companies in North America, and in over US$9 billion in financings for the utilities industry. Co-founder of MAG Silver Corp. and International Royalty Corp.

Dr. Mike Nelson Director: 40+ years as a mining engineer; currently Associate Professor and Chair of Mining Engineering, University of Utah. Worked for numerous resource companies including Rio Tinto Kennecott, EVRAZ North America, CODELCO El Teniente and BHP Billiton. Member, Society for Mining, Metallurgy and Exploration (US) and the Canadian Institute of Mining, Metallurgy and Petroleum; contributed to 16 books, including the SME Mining Engineering Handbook.

Gary Lewis Founder and major shareholder: 30 years in capital markets and business and strategy development. Has invested and/or operated resource projects or assets over the past ten years valued at more than US$350M, including the acquisition and ultimate sell-down or listing of high-value, multi-commodity resource projects in Australia, UK, SE Asia, Central Asia and the Americas.

www.rcgcorp.ca

Operations team

6

Michael Gross Mine operator with 45+ years of experience in mine operations, management, turnarounds, and team building. Mike is an expert in narrow-vein underground mining as well as open-pit mining. He has led major improvements at multiple mines, resulting in decreased costs, improved productivity, and higher earnings.

Dr. Clyde Smith Exploration and mining geologist with a career that spans over 50 years. Has discovered four ore deposits with contained total 2Moz Au, 40Moz Ag, 2.4B lbs Pb, 2.2B lbs Zn, and 200M lbs Cu. He has successfully guided projects through feasibility and development, and served as an officer and director on several successful companies.

David Smith 30 years in minerals exploration in the U.S., Canada, Mexico, Chile, and China on a wide range of ore deposits with particular emphasis on gold and precious metals. Core expertise encompasses the management of mineral projects from acquisition to initial mapping, drilling, resource modeling, and project development.

www.rcgcorp.ca

Nova Scotia Gold Roll-Up Strategy

7

• Acquired 4 historically producing gold projects • Over 500,000 ounces consolidated in high-

grade deposits with excellent upside • Dufferin Mine is a fully permitted, operational

gold mine - 90 days to resume operations

- Potential to produce >30,000 ounces per year

- PEA in progress with new resource estimate

• Dufferin planned to serve as central processing mill for surrounding deposits - Cash flow will allow expansion and development of

West Dufferin, Tangier, Forest Hill

• Eventual production target >120,000 ounces per year from four mines combined

Dufferin & West Dufferin

Tangier and Forest Hill

Regional

www.rcgcorp.ca

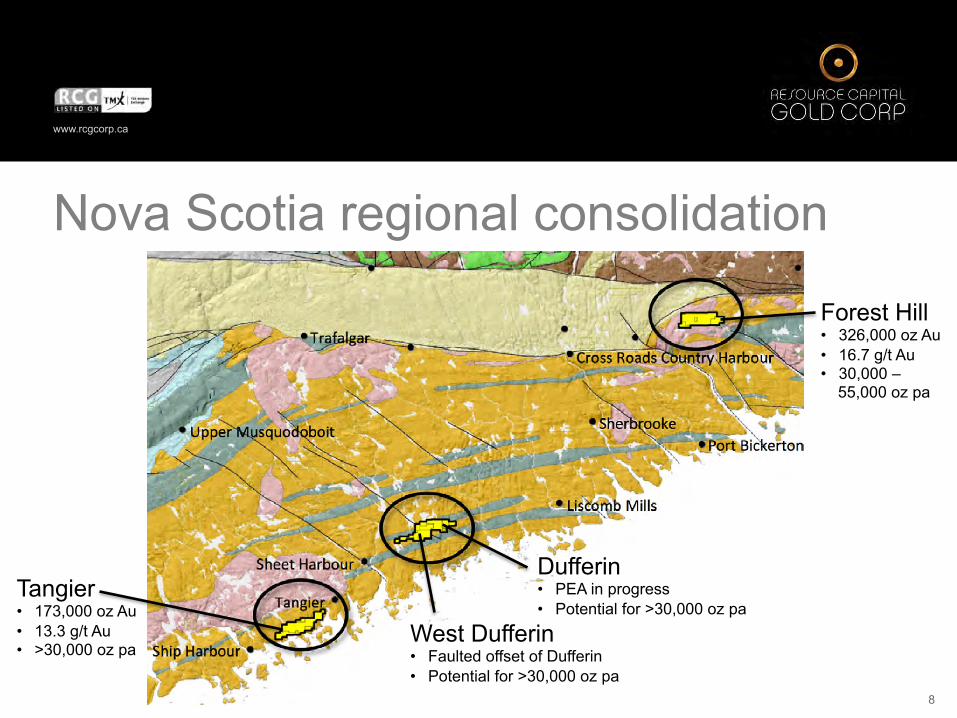

Nova Scotia regional consolidation

8

Forest Hill • 326,000 oz Au • 16.7 g/t Au • 30,000 –

55,000 oz pa

Dufferin • PEA in progress • Potential for >30,000 oz pa

West Dufferin • Faulted offset of Dufferin • Potential for >30,000 oz pa

Tangier • 173,000 oz Au • 13.3 g/t Au • >30,000 oz pa

www.rcgcorp.ca

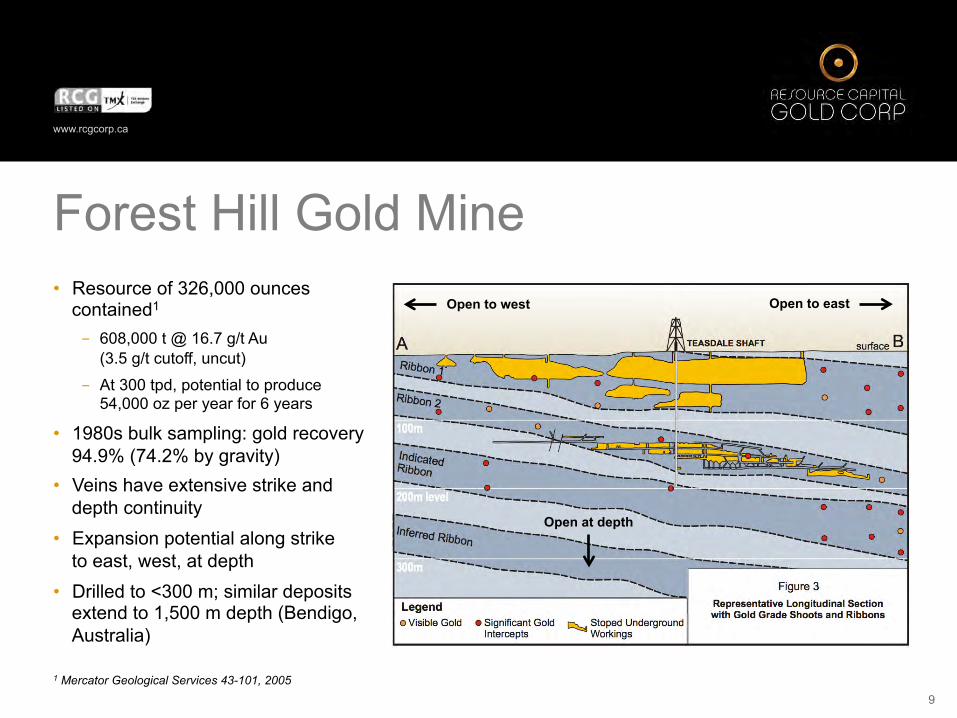

Forest Hill Gold Mine

9

• Resource of 326,000 ounces contained1

- 608,000 t @ 16.7 g/t Au (3.5 g/t cutoff, uncut)

- At 300 tpd, potential to produce 54,000 oz per year for 6 years

• 1980s bulk sampling: gold recovery 94.9% (74.2% by gravity)

• Veins have extensive strike and depth continuity

• Expansion potential along strike to east, west, at depth

• Drilled to <300 m; similar deposits extend to 1,500 m depth (Bendigo, Australia)

1 Mercator Geological Services 43-101, 2005

Open to east Open to west

Open at depth

www.rcgcorp.ca

Tangier Gold Mine

10

• Resource of 173,000 ounces contained1

- 405,000 t @ 13.3 g/t Au (3.5 g/t cutoff, uncut)

- At 225 tpd, potential to produce 32,000 oz per year for 6 years

• Historic production 29,000 oz @ 17.6 g/t Au

• 1,513-t bulk sample 1980s - 19.9 g/t Au

- 89% recovery by gravity

• 3,300 m underground development • Drill results up to 632 g/t Au • Excellent expansion potential along

strike and at depth 1 Mercator Geological Services 43-101, 2004

www.rcgcorp.ca

West Dufferin extension to the west

11

Dufferin Mine claims West Dufferin Mine claims

• Historical production of 41,000 oz from ore grading 11 g/t Au

• Faulted western extension of Dufferin deposit

• Mined only to 125m • Drilled to 400m

- 18 new saddle reef structures discovered

• Strike length over 1,500 meters - With Dufferin, offers

>3km potential

www.rcgcorp.ca

Tangier

Dufferin

Forest Hill

Dufferin gold mine, Nova Scotia

12

Unlocking value in a fully permitted underground gold mine

• 227 hectares (2.3 km2), 14 mineral claims all in good standing.

• Preliminary Economic Assessment (PEA) and 43-101 resource calculation in progress with additional sample data4

– High-grade drill intercepts up to 339 g/t Au • Cash cost: C$623 per Au ounce • Staged acquisition at deep discount to NPV • Technical team with deep expertise in turning

around and improving underground mining operations

• Close analogue to high-grade 25Moz Au Bendigo goldfields (Victoria, Australia)

4 Underground sampling of the mine faces and drill core to date are in the range 27 to 370 g/t Au

www.rcgcorp.ca

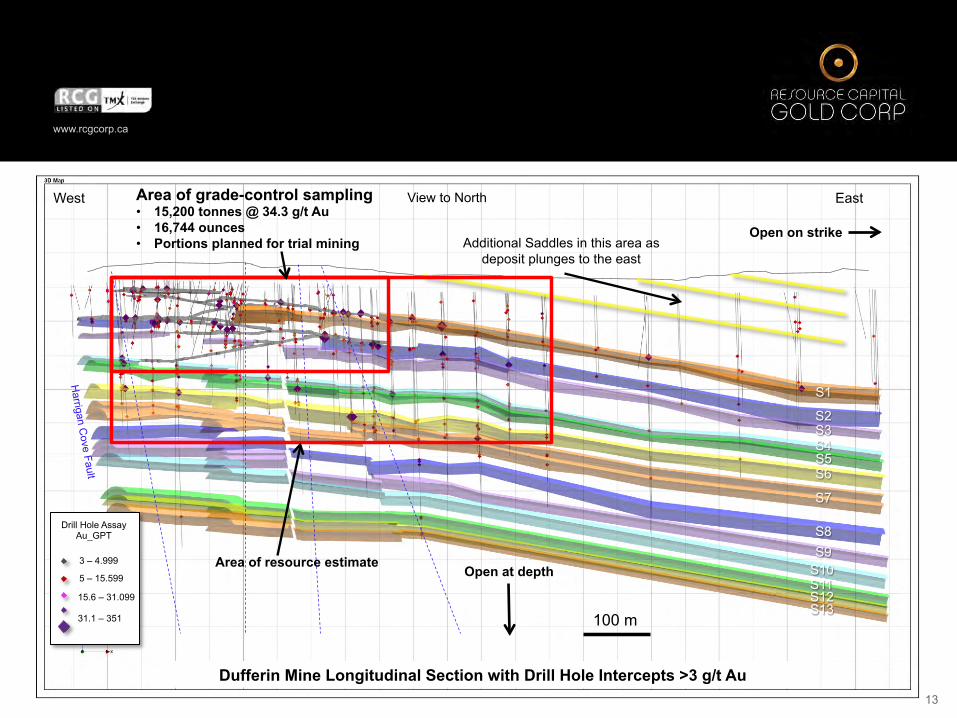

S1

S2 S3 S4 S5 S6

S7

S8 S9

S10 S11 S12 S13

3 – 4.999

Drill Hole Assay Au_GPT

5 – 15.599

15.6 – 31.099

31.1 – 351 100 m

View to North West East

Harrigan C

ove Fault

Open at depth

Open on strike Additional Saddles in this area as

deposit plunges to the east

Area of resource estimate

Dufferin Mine Longitudinal Section with Drill Hole Intercepts >3 g/t Au 13

Area of grade-control sampling • 15,200 tonnes @ 34.3 g/t Au • 16,744 ounces • Portions planned for trial mining

www.rcgcorp.ca

Mine development + resource potential

14

18+ saddle reef veins showing good continuity

Saddle Reef Vein Deposit

Anticline Fold Nose

D

Dufferin Mine Gold Quartz Vein

20-100 meters

7 OU3 (FWB) / APP (TSX.V)

Potential continuity in depth and toward east open structure

Drill program defined for significant resource expansion • 1.4km strike; drilled only to 400m depth • Deposit open along strike and at depth

www.rcgcorp.ca

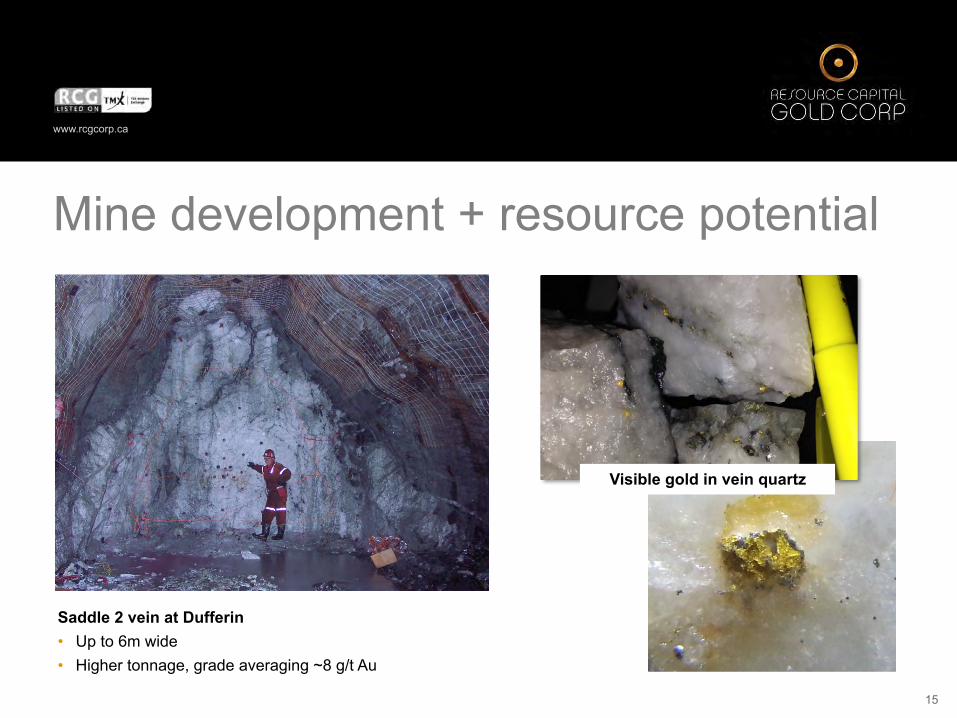

Mine development + resource potential

15

Saddle 2 vein at Dufferin • Up to 6m wide • Higher tonnage, grade averaging ~8 g/t Au

Visible gold in vein quartz

www.rcgcorp.ca

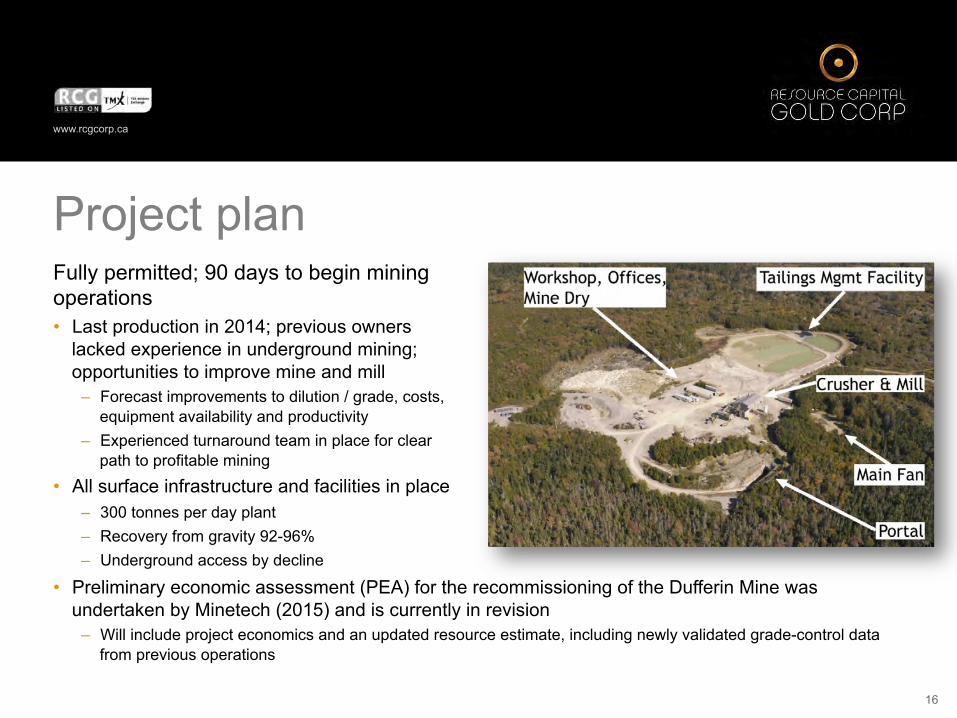

Project plan

16

Fully permitted; 90 days to begin mining operations • Last production in 2014; previous owners

lacked experience in underground mining; opportunities to improve mine and mill

– Forecast improvements to dilution / grade, costs, equipment availability and productivity

– Experienced turnaround team in place for clear path to profitable mining

• All surface infrastructure and facilities in place – 300 tonnes per day plant – Recovery from gravity 92-96% – Underground access by decline

• Preliminary economic assessment (PEA) for the recommissioning of the Dufferin Mine was undertaken by Minetech (2015) and is currently in revision

– Will include project economics and an updated resource estimate, including newly validated grade-control data from previous operations

Infrastructure and Facilities

www.rcgcorp.ca

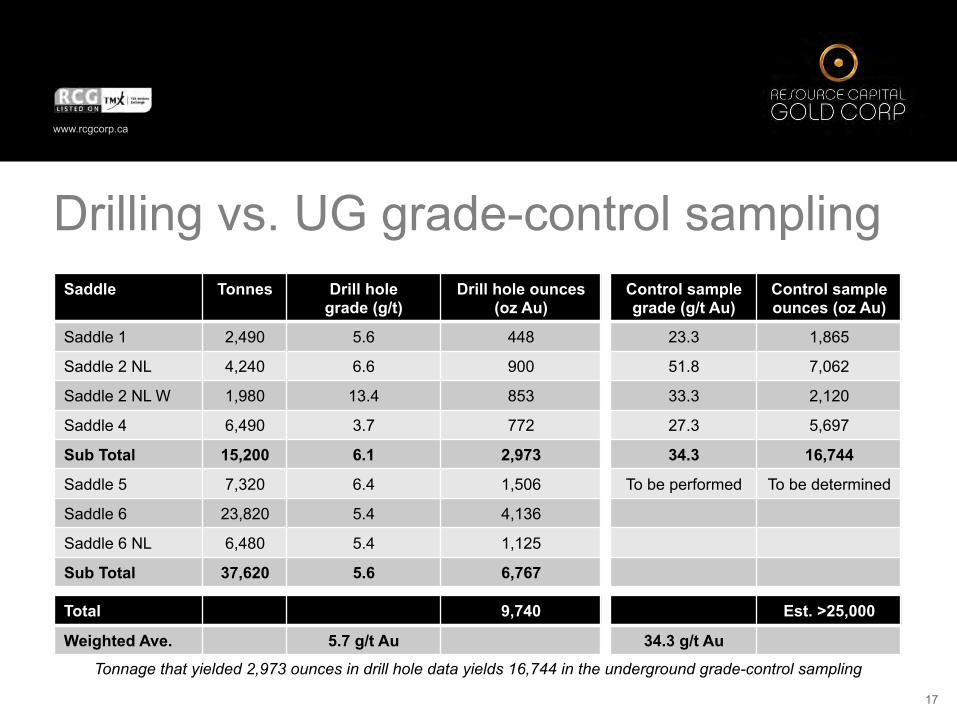

Drilling vs. UG grade-control sampling

17

Saddle Tonnes Drill hole grade (g/t)

Drill hole ounces (oz Au)

Saddle 1 2,490 5.6 448

Saddle 2 NL 4,240 6.6 900

Saddle 2 NL W 1,980 13.4 853

Saddle 4 6,490 3.7 772

Sub Total 15,200 6.1 2,973

Saddle 5 7,320 6.4 1,506

Saddle 6 23,820 5.4 4,136

Saddle 6 NL 6,480 5.4 1,125

Sub Total 37,620 5.6 6,767

Control sample grade (g/t Au)

Control sample ounces (oz Au)

23.3 1,865

51.8 7,062

33.3 2,120

27.3 5,697

34.3 16,744

To be performed To be determined

Total 9,740

Weighted Ave. 5.7 g/t Au

Est. >25,000

34.3 g/t Au

Tonnage that yielded 2,973 ounces in drill hole data yields 16,744 in the underground grade-control sampling

www.rcgcorp.ca

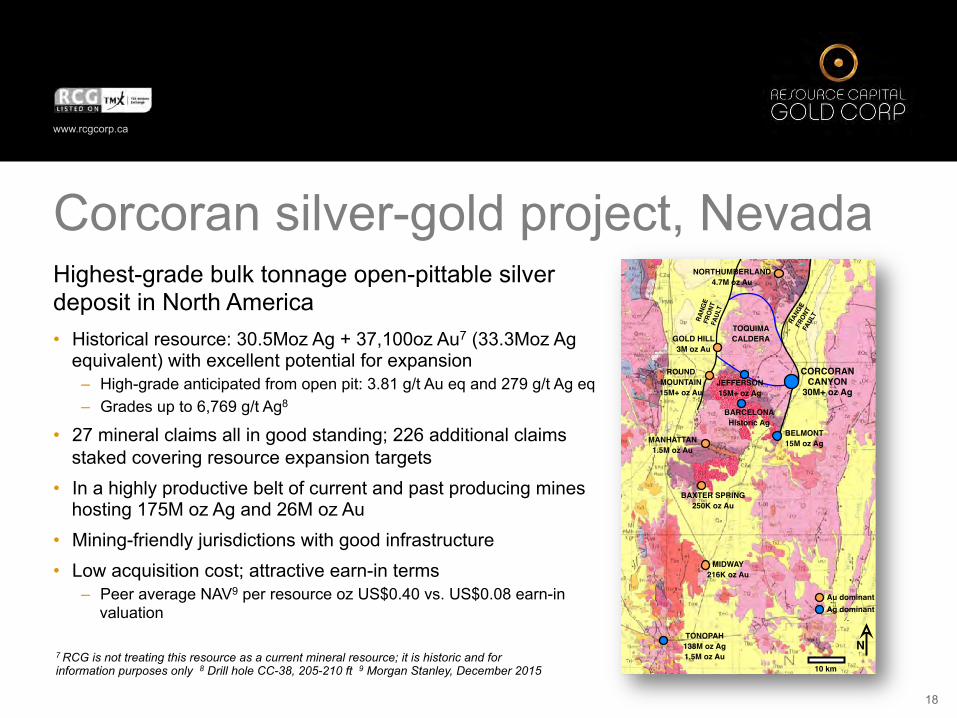

Corcoran silver-gold project, Nevada

18

Highest-grade bulk tonnage open-pittable silver deposit in North America • Historical resource: 30.5Moz Ag + 37,100oz Au7 (33.3Moz Ag

equivalent) with excellent potential for expansion – High-grade anticipated from open pit: 3.81 g/t Au eq and 279 g/t Ag eq – Grades up to 6,769 g/t Ag8

• 27 mineral claims all in good standing; 226 additional claims staked covering resource expansion targets

• In a highly productive belt of current and past producing mines hosting 175M oz Ag and 26M oz Au

• Mining-friendly jurisdictions with good infrastructure • Low acquisition cost; attractive earn-in terms

– Peer average NAV9 per resource oz US$0.40 vs. US$0.08 earn-in valuation

Highly Productive Mineral Belt

3"

• In a belt of mines, resources, and advanced projects that host over 168M oz Ag, 26M oz Au

• Same deposit type as nearby Tonopah • Historic 138M oz Ag, 1.5M oz Au

• 20 km from and similar mineralization to Round Mountain • Barrick-Kinross, 15M oz Au

• On same productive caldera margin as Gold Hill • Barrick-Kinross, 3M oz Au

• Within 30 km of Northumberland • Newmont, 4.7M oz Au

CORCORAN!CANYON!

30M+ oz Ag

NORTHUMBERLAND!4.7M oz Au

GOLD HILL!3M oz Au

ROUND!MOUNTAIN!15M+ oz Au

MANHATTAN!1.5M oz Au

MIDWAY!216K oz Au

TONOPAH!138M oz Ag!1.5M oz Au

TOQUIMA!CALDERA

RANG

E!FR

ONT!

FAUL

T

RANG

E!FR

ONT!

FAUL

T

10 km

N

BELMONT!15M oz Ag

JEFFERSON!15M+ oz Ag

BARCELONA!Historic Ag

BAXTER SPRING!250K oz Au

Au dominantAg dominant

7 RCG is not treating this resource as a current mineral resource; it is historic and for information purposes only 8 Drill hole CC-38, 205-210 ft 9 Morgan Stanley, December 2015

www.rcgcorp.ca

Resource can be expanded and optimised with further drilling and study work

High-grade resource expansion targets

19

• Mineralization open along strike to NE and SW with multiple high-quality expansion targets

• Immediate expansion potential surrounding historical resource

• Lateral expansion targets relatively more Au-rich

• Depth expansion potential for Tonopah bonanza grade mineralization, initial intercepts already drilled

1 km

N

RANGE-FRONT!FAULT

SILVER REEF !HISTORIC!

Ag-Au RESOURCE

CORCORAN!ALTERATION!

SYSTEM

SILVER REEF!EXPANSION POTENTIAL

WEST!TARGET

DRILL HOLE CC44!24 m @ 0.63 g/t Au!

0 - 24 m

DRILL HOLE CC42!15 m @ 0.89 g/t Au!

2 - 17 m

DRILL HOLE CC15!23 m @ 2.15 g/t Au!

35 - 58 m

TRAIL !CANYON !CALDERA!MARGIN

MASTER!FAULT

PEDIMENT!TARGET

INTRUSIONS!TARGET

R/S

M/NL

J

CB

FH

www.rcgcorp.ca

Highest-grade bulk tonnage open-pittable silver deposit in North America

20

• Outcropping Silver Reef deposit • Low strip ratio • Heap leach vs. milling scenario

being evaluated

www.rcgcorp.ca

Project plan

21

Feasibility study, construction and commissioning on a fast track • Upgrade resource to 43-101 standards with 2,000m drilling • Complete Feasibility Study including metallurgical testwork and environmental studies • Mine construction and commissioning

– Estimated pre-production CAPEX

– US$11m (heap leach scenario)

– US$50M (milling scenario)

– Forecast rate of production: 2,150 tpd

– 5-year initial mine life

• Use cash flows to expand resource

www.rcgcorp.ca

Project financial model

22

Preliminary financial modelling, heap-leach scenario10

10 Highlands Geoscience LLC, Seattle, Washington, USA. Projected economic model is for illustration purposes only; it is based on historical resource and numerous assumptions, and not on a preliminary economic assessment.

Preliminary financial modelling, milling scenario10

Production and Costs! Unit! Base Case!

Tonnes per day ore! tpd" 2,150"

Silver recovery! %" 80.0"

Gold recovery! %" 90.0"

Recovered silver-equivalent! ounces" 26,874,888"

Cash cost per silver-equivalent ounce recovered! US$" 5.64"

Pre-production investment! US$" 51,500,000"

Production and Costs! Unit! Base Case!

Tonnes per day ore! tpd" 2,150"

Silver recovery! %" 50.0"

Gold recovery! %" 75.0"

Recovered silver-equivalent! ounces" 17,307,368"

Cash cost per silver-equivalent ounce recovered! US$" 5.90"

Pre-production investment! US$" 11,000,000"

Earnings and Metrics! Cum. EBITDA! NPV66! IRR!

$15 Ag, $1,100 Au! US$157.4m" US$115.1m" 292%"

$17 Ag, $1,200 Au! US$190.1m" US$141.1m" 353%"

$20 Ag, $1,500 Au! US$243.2m" US$183.3m" 451%"

Earnings and Metrics! Cum. EBITDA! NPV66! IRR!

$15 Ag, $1,100 Au! US$251.7m" US$151.9m" 96%"

$17 Ag, $1,200 Au! US$302.8m" US$192.6m" 117%"

$20 Ag, $1,500 Au! US$384.4m" US$257.6m" 150%"

www.rcgcorp.ca

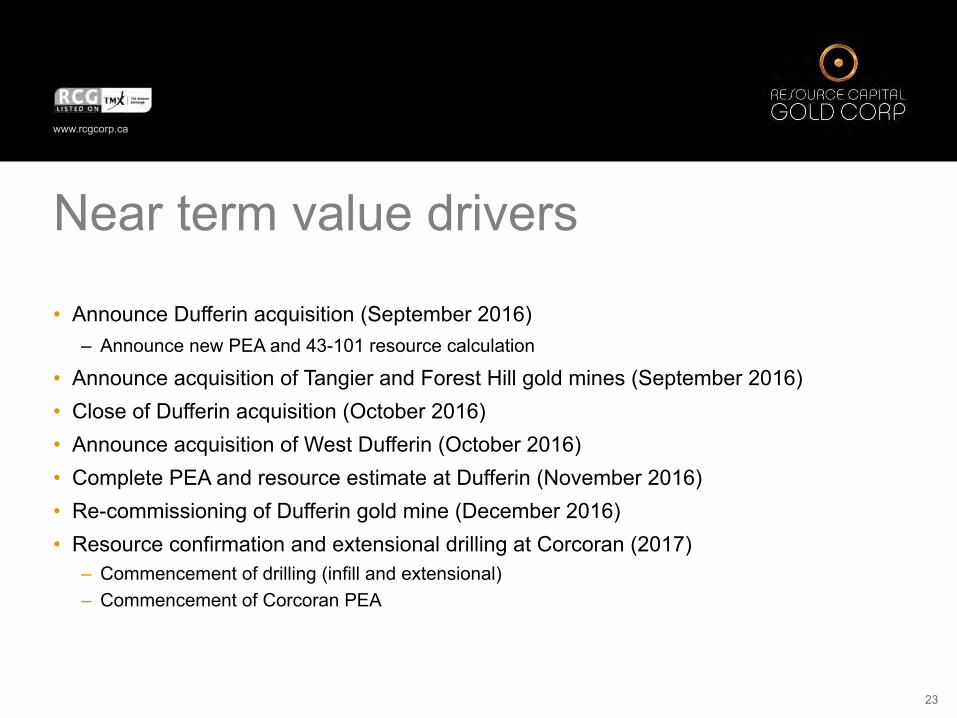

Near term value drivers

23

• Announce Dufferin acquisition (September 2016) – Announce new PEA and 43-101 resource calculation

• Announce acquisition of Tangier and Forest Hill gold mines (September 2016) • Close of Dufferin acquisition (October 2016) • Announce acquisition of West Dufferin (October 2016) • Complete PEA and resource estimate at Dufferin (November 2016) • Re-commissioning of Dufferin gold mine (December 2016) • Resource confirmation and extensional drilling at Corcoran (2017)

– Commencement of drilling (infill and extensional) – Commencement of Corcoran PEA

www.rcgcorp.ca

Summary

24

• Launched revitalized business plan targeting low CAPEX, late-stage exploration, development and producing precious metal assets in North America. – Acquired fully permitted, operational Nova Scotia gold mine with all necessary personnel,

facilities and infrastructure in place to restart operations within 90 days from transaction close. – Regional roll-up of historic gold mines in Nova Scotia with c. 600,000 high-grade ounces gold

resources – Acquired investment right to control 80% of Nevada-based silver-gold project with 33Moz Ag-

equivalent historical resource in situ.

• Restored balance sheet and capital base. • Management team with proven success in developing, operating and turning-

around mines. • Presents a sound case for revaluation of share price:

– Current market cap c. C$11.6M – Combined project NPV +US$350M

www.rcgcorp.ca

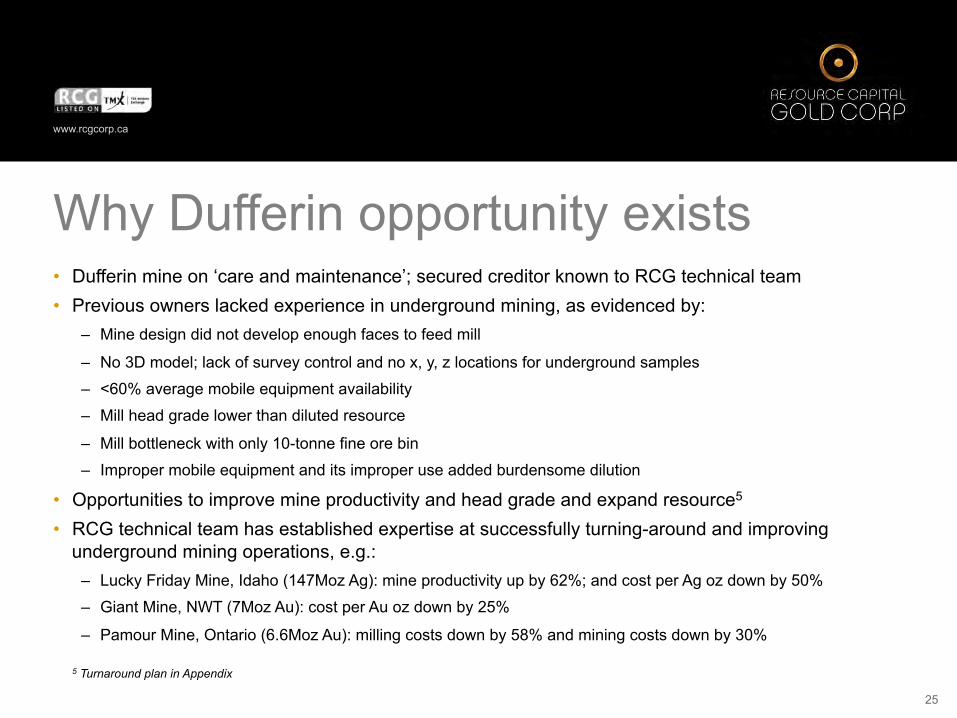

Why Dufferin opportunity exists

25

• Dufferin mine on ‘care and maintenance’; secured creditor known to RCG technical team • Previous owners lacked experience in underground mining, as evidenced by:

– Mine design did not develop enough faces to feed mill

– No 3D model; lack of survey control and no x, y, z locations for underground samples

– <60% average mobile equipment availability

– Mill head grade lower than diluted resource

– Mill bottleneck with only 10-tonne fine ore bin

– Improper mobile equipment and its improper use added burdensome dilution

• Opportunities to improve mine productivity and head grade and expand resource5

• RCG technical team has established expertise at successfully turning-around and improving underground mining operations, e.g.:

– Lucky Friday Mine, Idaho (147Moz Ag): mine productivity up by 62%; and cost per Ag oz down by 50%

– Giant Mine, NWT (7Moz Au): cost per Au oz down by 25%

– Pamour Mine, Ontario (6.6Moz Au): milling costs down by 58% and mining costs down by 30%

5 Turnaround plan in Appendix

www.rcgcorp.ca

Dufferin turnaround plan

26

1. Mine design did not develop enough faces to feed mill • Complete 3 months of development prior to resuming mining • Drive access ramp in waste so that ore in saddle legs will not be sterilized until end of mine life and

more saddle can be developed at the same time • Develop long-hole stopes on saddle legs and re-using where long holing is not practical • Always keep development far enough ahead of mining to provide sufficient faces to maintain

production are always available • Implement stringent grade control protocols

2. No 3D model: lack of survey control, no x, y, z locations for underground samples • Purchase 3D modeling software • Hire geologist with excellent modeling skills • Implement strict sampling protocols that pinpoint sample locations • Build 3D model to support effective and efficient mine planning

www.rcgcorp.ca

Dufferin turnaround plan

27

3. <60% average mobile equipment availability • Acquire new or rebuilt equipment to resume mining • Contract with equipment vendor for equipment maintenance which will be tied to availability • Enforce preventative maintenance schedules • Include road grader to improve tire wear and reduce rolling resistance in mine haulage for lower

operating costs 4. Mill head grade lower than diluted resource • Implement strict grade control protocols • Focus on mining best grade from every face • Having enough faces available delivers sufficient tonnage and grade for profitable milling operations 5. Mill bottleneck with only 10-tonne fine ore bin • Construct a 1,000 tonne fine ore bin to eliminate mill bottlenecks and reduce operating time for the

crushing plant, which in turn reduces operating costs • Cover screening plant and winterize the entire mill facility

www.rcgcorp.ca

Technical Team - Consultants Terrence Byberg Mine operations executive with over 42 years of experience worldwide in numerous mines. He specializes in turning around troubled mining operations, gained through hands-on mine operations from shift boss to President of Silver Eagle Mines.

Allen Cockle Retired VP, Technical Services of Newmont Mining Corporation and a practicing consultant with over 40 years of experience in exploration geology, geological engineering, and mining engineering. His specialty is the valuation of mining projects at various stages of development as they advance from exploration to pre-feasibility, feasibility, and production.

Randy Powell Over 35 years of varied mineral processing and operations management experience including 16 years as Project Manager, Process Superintendent, and Mill Superintendent at Cortez Gold Mines, Barrick Gold’s and Nevada’s largest gold producer. Has extensive processing experience in gold metallurgy (CIL, CIC and heap leaching), hydrometallurgy, and pyro-metallurgy.

28

www.rcgcorp.ca

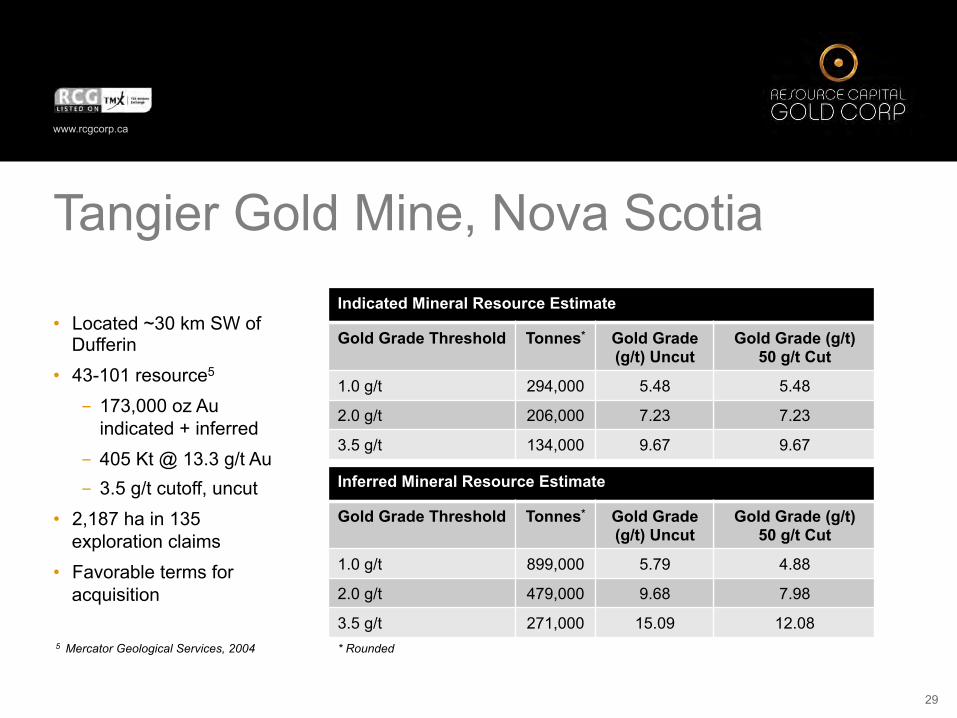

Tangier Gold Mine, Nova Scotia

29

• Located ~30 km SW of Dufferin

• 43-101 resource5

- 173,000 oz Au indicated + inferred

- 405 Kt @ 13.3 g/t Au - 3.5 g/t cutoff, uncut

• 2,187 ha in 135 exploration claims

• Favorable terms for acquisition

5 Mercator Geological Services, 2004

Indicated Mineral Resource Estimate

Gold Grade Threshold Tonnes* Gold Grade (g/t) Uncut

Gold Grade (g/t) 50 g/t Cut

1.0 g/t 294,000 5.48 5.48

2.0 g/t 206,000 7.23 7.23

3.5 g/t 134,000 9.67 9.67

Inferred Mineral Resource Estimate

Gold Grade Threshold Tonnes* Gold Grade (g/t) Uncut

Gold Grade (g/t) 50 g/t Cut

1.0 g/t 899,000 5.79 4.88

2.0 g/t 479,000 9.68 7.98

3.5 g/t 271,000 15.09 12.08 * Rounded

www.rcgcorp.ca

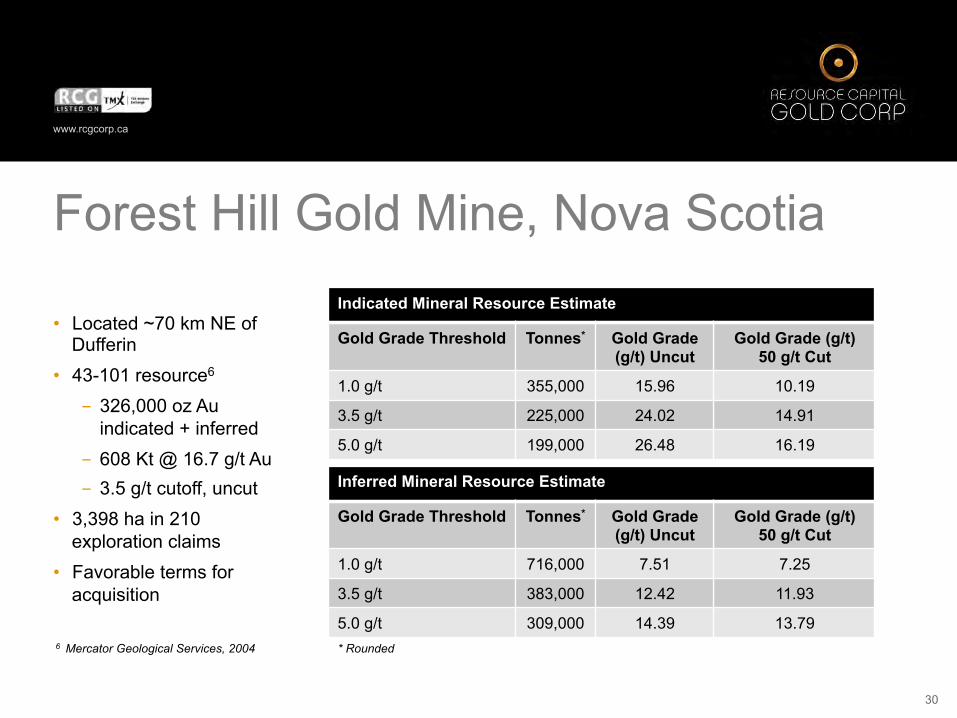

Forest Hill Gold Mine, Nova Scotia

30

• Located ~70 km NE of Dufferin

• 43-101 resource6

- 326,000 oz Au indicated + inferred

- 608 Kt @ 16.7 g/t Au - 3.5 g/t cutoff, uncut

• 3,398 ha in 210 exploration claims

• Favorable terms for acquisition

6 Mercator Geological Services, 2004

Indicated Mineral Resource Estimate

Gold Grade Threshold Tonnes* Gold Grade (g/t) Uncut

Gold Grade (g/t) 50 g/t Cut

1.0 g/t 355,000 15.96 10.19

3.5 g/t 225,000 24.02 14.91

5.0 g/t 199,000 26.48 16.19

Inferred Mineral Resource Estimate

Gold Grade Threshold Tonnes* Gold Grade (g/t) Uncut

Gold Grade (g/t) 50 g/t Cut

1.0 g/t 716,000 7.51 7.25

3.5 g/t 383,000 12.42 11.93

5.0 g/t 309,000 14.39 13.79 * Rounded

www.rcgcorp.ca

Contact Information RESOURCE CAPITAL GOLD CORP. 666 Burrard Street #500 Vancouver, BC V6C 3P6 Canada

T 1-604 642 6114 E [email protected] W rcgcorp.ca

DISCLAIMER This presentation contains ‘forward-looking statements’ as defined or implied at common law and within the meaning of the Corporations Law. Such forward-looking statements may include, without limitation: (i) estimates of future gold, silver and copper sales; (ii) estimates of future cash costs; (iii) estimates of future capital expenditure; (iv) statements regarding the sensitivity of reserves to commodity prices; and (v) statements regarding future exploration results and the replacement of reserves.

Where the Company or any of its officers or directors or representatives expresses or implies an expectation or belief as to future events or results, such expectation or belief is expressed in good faith and the Company or its officers or representatives as the case may be believe to have a reasonable basis for implying such an expectation or belief. However, forward-looking statements are subject to risks, uncertainties and other factors, which could cause actual results to differ materially from future results expressed, projected or implied by such forward-looking statements. Such risks include, but are not limited to, gold, copper, silver and other metals price volatility, currency fluctuations, increased production costs and variances in ore grade or recovery rates from those assumed in mining plans, political and operational risks in the countries in which we operate, and governmental regulation and judicial outcomes.

The Company does not undertake any obligations to publicly release revisions to any ‘forward looking statement’, to reflect events or circumstances after the date of this release, or to reflect the occurrence of unanticipated events, except as may be required under applicable securities laws.

31