an analysis of extreme el niño insurance in Protecting a...

16

TECHNICAL NOTE 5 An Analysis of Extreme El Niño Insurance in Protecting a Financial Institution’s Portfolio 5 Insurance for Climate Change Adaptation Project

Transcript of an analysis of extreme el niño insurance in Protecting a...

Technical noTe 5

an analysis of extreme el niño insurance in Protecting a Financial institution’s Portfolio

5

Insurance for C l imate Change Adaptat ion Pro ject

2

Technical noTe 5an analysis of extreme el niño insurance for Protecting a Financial institution’s PortfolioDeutsche Gesellschaft für internationale Zusammenarbeit (GiZ) Gmbh

insurance for climate change adaptation Project Main advisor Alberto Aquino [email protected] Jr. Los Manzanos 119, San Isidro http://seguros.riesgoycambioclimatico.org/

author GlobalAgRisk

Translation Damian HagerDesign and layout Renzo Rabanal Photographs GIZ photo archives, Diario El Tiempo, PiuraPrinting Giacomotti Comunicación Gráfica S.A.C. Calle Huiracocha 1291. Of 302, Jesús María First edition, Lima (Peru), August 2012 Legal deposit in the Biblioteca Nacional del Perú (National Library of Peru) No. 2012-09426

Cooperación Alemana al Desarrollo – Agencia de la GIZ en el PerúAv. Prolongación Arenales 801, MirafloresTotal or partial reproduction of this work is allowed, provided the source is cited.

Dia

rio

El

tiEm

po, P

iUra

3

an analysis of extreme el niño insurance in Protecting a Financial institution’s Portfolio

Executive summary

The purpose of this paper is to present the portfolio benefits of Extreme El Niño In-

surance for a financial institution and describe risk assessment results, a quantitative

model of a financial institution’s exposure to the El Niño Phenomenon, and the prod-

uct’s expected benefits. Specifically, insurance payments can contribute to maintaining

a satisfactory capital ratio by compensating capital losses due to increased provisions

and bad loans. The high cost of undercapitalization will, inevitably, translate into lost

opportunities of cost effective loans (Van den Heuval, 2006); thus an insured financial

institution should expect greater income than those that do not opt for this type of

insurance coverage.

The results of the model suggest it would be possible to obtain substantial portfolio protec-

tion by purchasing a relatively small amount of insurance, for example, a sum insured

equivalent to 1% - 4% of the credit portfolio value. Since the insurance protects a financial

institution’s ability to extend loans after an extreme El Niño event the model also indicated

that the product increases, on average, the final capital position at the end of a 15 year

period. More importantly, the insurance greatly reduces the volatility of the bank’s equity.

In addition to the quantitative effects of the model, insurance coverage can produce

other qualitative benefits, namely

1. Heightened reputation of the financial institution of the financial institution as an

innovative, socially committed company and market leader.

2. Increased international visibility among socially conscious investors and donors.

3. Improved risk profile for credit rating agencies and debt and capital investors.

4. Reduced net regulatory burden since insurance is formally recognized as a risk

management device.

5. Strategic market positioning after an extrem El Niño event which facilitates growth

in market share.

Based on the results of the model and these other potential benefits, let’s assume

that a financial institution chooses to insure partially its risk at an amount equivalent

4

to roughly 0.8% of its credit portfolio. The premium paid for this risk transfer is about

0.5 basis points of the credit portfolio, and thus it will reduce capital volatility related to

an extreme El Niño by nearly 22%.

Background

The El Niño Phenomenon causes catastrophic flooding in northern Peru. This climatic

event is associated with an increase in Pacific sea surface temperatures off the coast

of Peru (Lagos et al., 2008). Warm air from the west collides with cold air cascading

down from the Andes in the east, thereby setting off severe rainfall (McPhaden, 2003).

During the 1982–83 and 1997–98 extreme events, January to May precipitation levels

were nearly 40 times above. The volume of water in the Piura River was also 40 times

the norm during those events(Skees and Murphy, 2009). As a result of the extreme

weather, bridges washed away, roads were destroyed, fields flooded, assets were lost,

communities were isolated, and food prices, and diseases increased. An extreme El

Niño creates problems for financial intermediaries and limits access to credit. For

instance, the 1997–98 El Niño event caused credit payment problems that lasted for

years (Trivelli, 2006). Afterwards, some financial intermediaries reacted by drastically

reducing access to credit for sectors they considered highly vulnerable to the phenom-

enon, such as agriculture. Moreover, interest rates rose close to 3% in northern Peru

on account of the hightened risk of nonpayment associated with the El Niño (Skees and

Barnett, 2006).

Extreme El Niño Insurance is a type of index insurance which provides pays out on the

basis of objective measurements of the severity of a disaster and it is widely used in

places where traditional insurance does not meet all the needs of the target market.

Its payments are based upon the increase in Pacific sea surface temperatures (SST),

which is the standard means climatologists gauge the severity of an El Niño event. The

temperature readings accurately predict catastrophic flooding in northern Peru (Khalil

et al., 2007), and because of that predictive ability, insurance can be paid even before

disaster onset of the disaster. The contract the financial institution is evaluating em-

ploys November-December SST readings and pays out in January, the reason being

that previous event reports indicate that catastrophic floods occur in February.

Thus, the index insurance plan benefits are: 1) advanced payout for more robust disas-

ter management, 2) coverage against business interruptions and higher costs that

would not typically be included in traditional insurance plans, and 3) lower insurance

costs since adverse selection and moral hazard related to traditional insurance are

substantially reduced in index insurance.

5

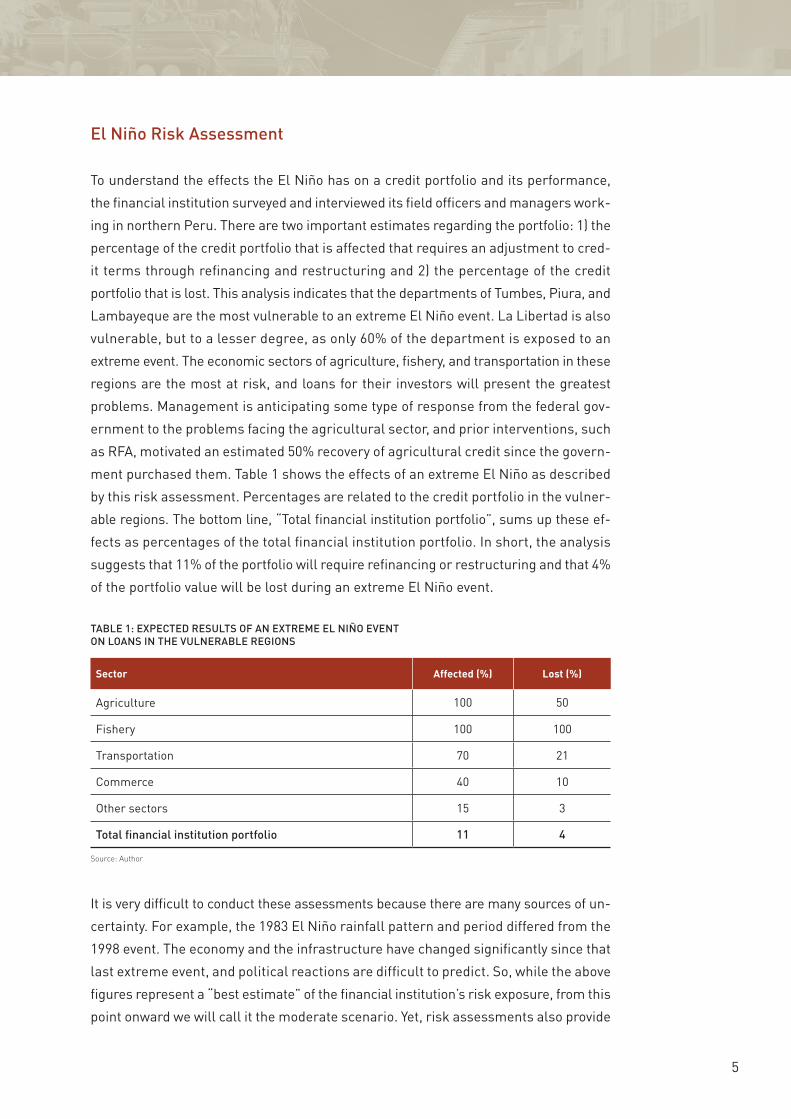

El Niño Risk Assessment

To understand the effects the El Niño has on a credit portfolio and its performance,

the financial institution surveyed and interviewed its field officers and managers work-

ing in northern Peru. There are two important estimates regarding the portfolio: 1) the

percentage of the credit portfolio that is affected that requires an adjustment to cred-

it terms through refinancing and restructuring and 2) the percentage of the credit

portfolio that is lost. This analysis indicates that the departments of Tumbes, Piura, and

Lambayeque are the most vulnerable to an extreme El Niño event. La Libertad is also

vulnerable, but to a lesser degree, as only 60% of the department is exposed to an

extreme event. The economic sectors of agriculture, fishery, and transportation in these

regions are the most at risk, and loans for their investors will present the greatest

problems. Management is anticipating some type of response from the federal gov-

ernment to the problems facing the agricultural sector, and prior interventions, such

as RFA, motivated an estimated 50% recovery of agricultural credit since the govern-

ment purchased them. Table 1 shows the effects of an extreme El Niño as described

by this risk assessment. Percentages are related to the credit portfolio in the vulner-

able regions. The bottom line, “Total financial institution portfolio”, sums up these ef-

fects as percentages of the total financial institution portfolio. In short, the analysis

suggests that 11% of the portfolio will require refinancing or restructuring and that 4%

of the portfolio value will be lost during an extreme El Niño event.

It is very difficult to conduct these assessments because there are many sources of un-

certainty. For example, the 1983 El Niño rainfall pattern and period differed from the

1998 event. The economy and the infrastructure have changed significantly since that

last extreme event, and political reactions are difficult to predict. So, while the above

figures represent a “best estimate” of the financial institution’s risk exposure, from this

point onward we will call it the moderate scenario. Yet, risk assessments also provide

TABlE 1: ExPECTEd REsulTs of AN ExTREmE El NIño EvENT oN loANs IN ThE vulNERABlE REgIoNs

Sector affected (%) lost (%)

Agriculture 100 50

Fishery 100 100

Transportation 70 21

Commerce 40 10

Other sectors 15 3

Total financial institution portfolio 11 4

Source: Author

6

optimistic and pessimistic scenarios. In terms of the former, an extreme El Niño affects

La Libertad to a lesser extent and creates fewer portfolio losses in the transportation,

commerce, and “other” sectors, thereby resulting in an affected portfolio of 9.5% and

losses of 2.7%. Under a pessimistic scenario, an extreme El Niño has a greater affect

in La Libertad and heightens the problems and/or losses in the agriculture, transpor-

tation, and commerce sectors, resulting in an affected portfolio of 14.5% and losses of

6%. If the government was not to intervene through the purchase of agricultural credits

after an extreme event, then portfolio losses under the moderate scenario would also

be as high as 6%. Table 2 summarizes the three scenarios in terms of the financial in-

stitution’s total portfolio.

Benefits of the insurance for an El Niño event

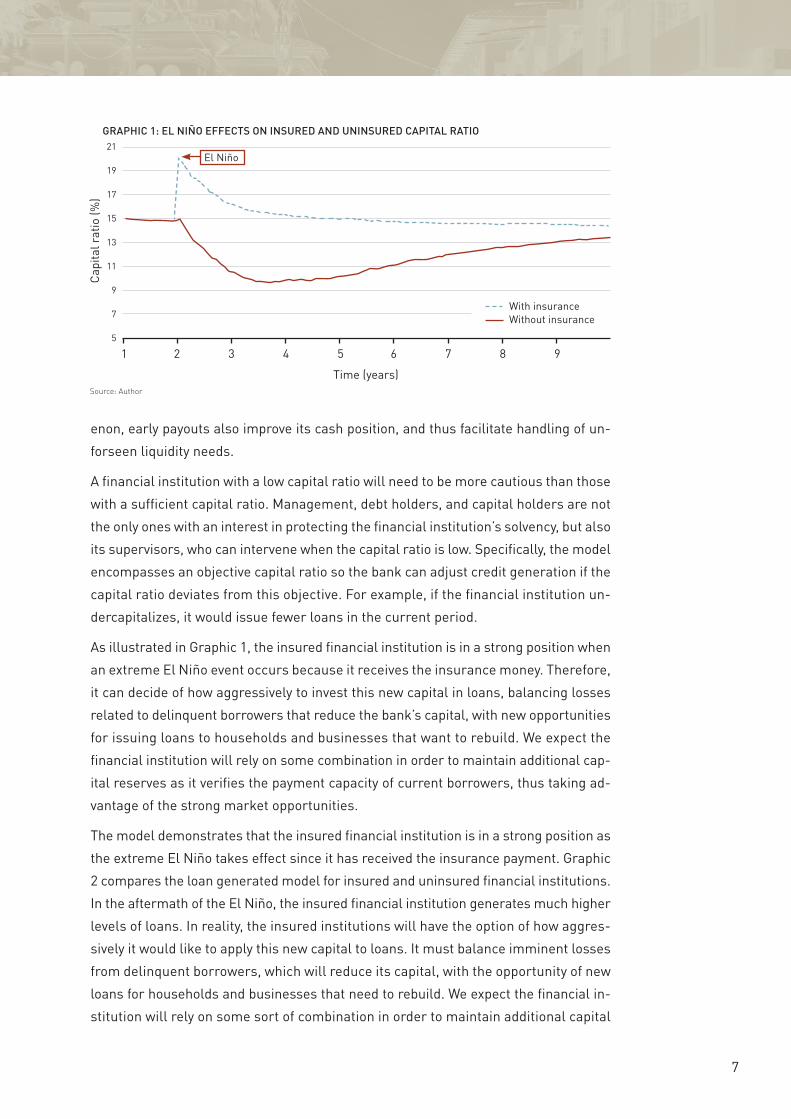

The greatest risk the El Niño poses for a financial institution is asset loss through late

loan payments, a situation that could destroy the bank’s capital. Undercapitalization dis-

rupts normal income generating opportunities since bank originates fewer new loans

when it reduces leverage. Bad loans also reduce gross income from interest, thereby

decelerating recovery due to a reduction in earnings flows. Graphic 1 was generated

from a banking model using a moderate scenario. The solid line shows the effect of

an extreme El Niño event has on the capital ratio during the second year of the model.

El Niño Insurance protects the bank’s capital, and it will be paid just before a strong

event. The insurance money will be entered into the balance sheet as new capital since

it increases the financial institution’s assets without associated liabilities. Hence, it in-

creases the capital ratio,by the dotted line in Graphic 1, where the insured amount is

4% of the portfolio value. Bear in mind that the financial institution’s insured capital ratio

will fall after the El Niño event for two reasons: 1) the portfolio insurance does not di-

rectly deal with problems related to borrowers’ failure to make loan payments, thus the

portfolio value will continue to fall, and 2) we anticipate that the financial institution

will want to offer loans aggressively after the catastrophic event in order to cover a grow-

ing demand from its good customers in the region who need to rebuild. While a financial

institution is not very vulnerable to liquidity risks due to an extreme El Niño phenom-

TABlE 2: summARy of ExTREmE El NIño EffECTs oN ThE PoRTfolIo IN ThE ThREE sCENARIos

Sector affected (%) lost (%)

Optimistic 9,5 2,7

Moderate 11,0 4,0

Pessimistic 14,5 6,0

Source: Author

7

enon, early payouts also improve its cash position, and thus facilitate handling of un-

forseen liquidity needs.

A financial institution with a low capital ratio will need to be more cautious than those

with a sufficient capital ratio. Management, debt holders, and capital holders are not

the only ones with an interest in protecting the financial institution’s solvency, but also

its supervisors, who can intervene when the capital ratio is low. Specifically, the model

encompasses an objective capital ratio so the bank can adjust credit generation if the

capital ratio deviates from this objective. For example, if the financial institution un-

dercapitalizes, it would issue fewer loans in the current period.

As illustrated in Graphic 1, the insured financial institution is in a strong position when

an extreme El Niño event occurs because it receives the insurance money. Therefore,

it can decide of how aggressively to invest this new capital in loans, balancing losses

related to delinquent borrowers that reduce the bank’s capital, with new opportunities

for issuing loans to households and businesses that want to rebuild. We expect the

financial institution will rely on some combination in order to maintain additional cap-

ital reserves as it verifies the payment capacity of current borrowers, thus taking ad-

vantage of the strong market opportunities.

The model demonstrates that the insured financial institution is in a strong position as

the extreme El Niño takes effect since it has received the insurance payment. Graphic

2 compares the loan generated model for insured and uninsured financial institutions.

In the aftermath of the El Niño, the insured financial institution generates much higher

levels of loans. In reality, the insured institutions will have the option of how aggres-

sively it would like to apply this new capital to loans. It must balance imminent losses

from delinquent borrowers, which will reduce its capital, with the opportunity of new

loans for households and businesses that need to rebuild. We expect the financial in-

stitution will rely on some sort of combination in order to maintain additional capital

1 2 3 4 5 6 7 8 9

Time (years)

Capi

tal r

atio

(%)

21

19

17

15

13

11

9

7

5

With insuranceWithout insurance

Source: Author

gRAPhIC 1: El NIño EffECTs oN INsuREd ANd uNINsuREd CAPITAl RATIo

El Niño

8

reserves as it determines the repayment capacity of its current borrowers, whereby it

takes advantage of the strong market opportunities. One financial benefit of the insur-

ance not shown in this model is that after an extreme event, the stronger financial in-

termediaries have the potential to gain more of the market share from the weaker.

Results comparison over a 15 year time period

The above example describes how an extreme El Niño event can affect a financial in-

stitution. The following analysis compares a range of possible results in order to deter-

mine whether the bank will be in a better or worse position due to the purchase of the

insurance. We use a 15 year time period because it offers a clearer image of how the

insurance helps protect the bank’s long term stability

We use the Monte Carlo simulation for this analysis, in which the same test is repeated

when a result is uncertain (for example, if and when the El Niño event will occur) and

the possible results are summarized. Thus, a Monte Carlo simulation is like throwing

dice over and over again, while documenting the results. The result of interest in this

method is the financial institution’s capital at the end of a 15 year period.

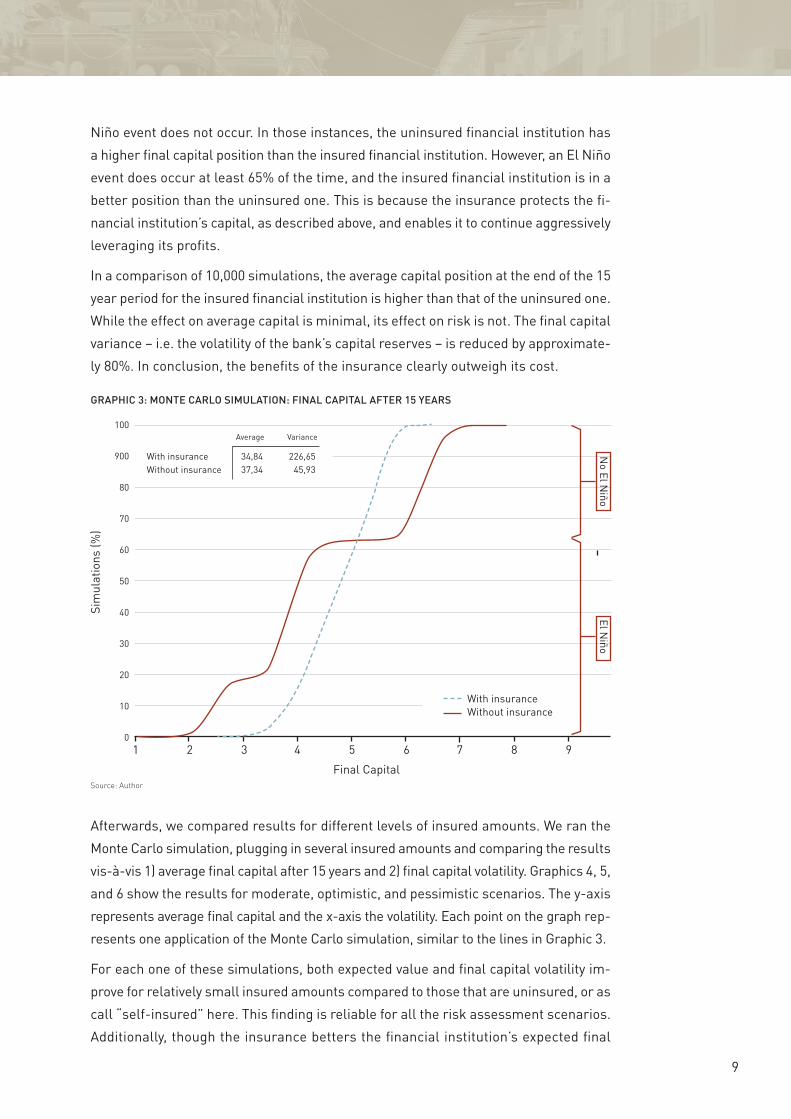

Graphic 3 features the results for a moderate scenario. The insured amount is equal

to 4% of the credit portfolio value, the price of the insurance in this model is 7% of the

insured amount each year, and the number of simulations is 10,000. The graph is laid

out so that the simulations with lower final capital are on the left and those with high-

er are on the right. Approximately 35% of the time during the 15 year period, an El

1 2 3 4 5 6 7 8 9Time (years)

CPor

tfolio

gro

wth

(%)

1,20

1,00

0,80

0,60

0,40

0,20

0,00

-0,20

-0,40

-0,60

With insuranceWithout insurance

Source: Author

gRAPhIC 2: PoRTfolIo gRowTh

9

Niño event does not occur. In those instances, the uninsured financial institution has

a higher final capital position than the insured financial institution. However, an El Niño

event does occur at least 65% of the time, and the insured financial institution is in a

better position than the uninsured one. This is because the insurance protects the fi-

nancial institution’s capital, as described above, and enables it to continue aggressively

leveraging its profits.

In a comparison of 10,000 simulations, the average capital position at the end of the 15

year period for the insured financial institution is higher than that of the uninsured one.

While the effect on average capital is minimal, its effect on risk is not. The final capital

variance – i.e. the volatility of the bank’s capital reserves – is reduced by approximate-

ly 80%. In conclusion, the benefits of the insurance clearly outweigh its cost.

Afterwards, we compared results for different levels of insured amounts. We ran the

Monte Carlo simulation, plugging in several insured amounts and comparing the results

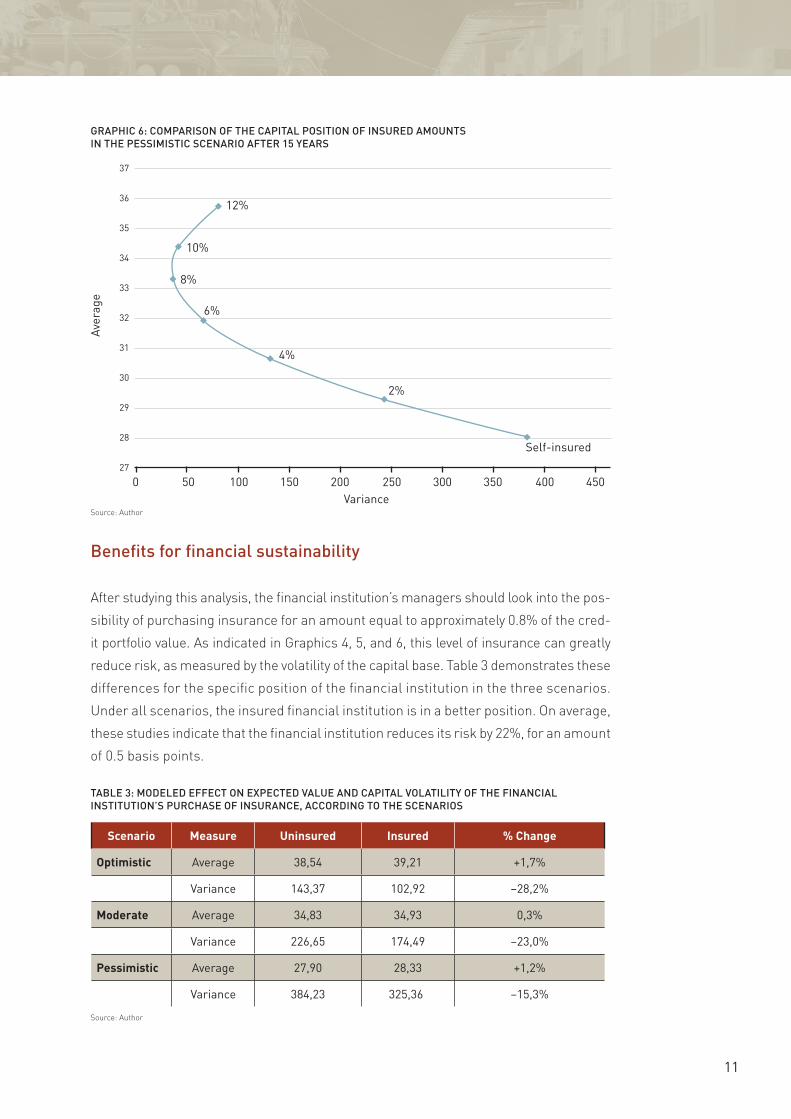

vis-à-vis 1) average final capital after 15 years and 2) final capital volatility. Graphics 4, 5,

and 6 show the results for moderate, optimistic, and pessimistic scenarios. The y-axis

represents average final capital and the x-axis the volatility. Each point on the graph rep-

resents one application of the Monte Carlo simulation, similar to the lines in Graphic 3.

For each one of these simulations, both expected value and final capital volatility im-

prove for relatively small insured amounts compared to those that are uninsured, or as

call “self-insured” here. This finding is reliable for all the risk assessment scenarios.

Additionally, though the insurance betters the financial institution’s expected final

1 2 3 4 5 6 7 8 9

Final Capital

Sim

ulat

ions

(%)

100

900

80

70

60

50

40

30

20

10

0

With insuranceWithout insurance

Source: Author

gRAPhIC 3: moNTE CARlo sImulATIoN: fINAl CAPITAl AfTER 15 yEARs

With insuranceWithout insurance

34,84 226,6537,34 45,93

Average Variance

El Niño

No El N

iño

10

capital position, the sound risk reduction benefits of acquiring even a small amount of

insurance are extremely evident.

0 50 100 150 200 250

8%

6%

4%

2%

Self-insured

Variance

Aver

age

41

40

39

38

7

36

35

34

Source: Author

gRAPhIC 4: ComPARIsoN of ThE fINAl CAPITAl PosITIoN of INsuREd AmouNTs IN ThE modERATE sCENARIo AfTER 15 yEARs

0 20 40 60 80 100 120 140 160

6%

4%

2%

Self-insured

Variance

Aver

age

43,0

42,5

42,0

41,5

41,0

40,5

40,0

39,5

39,0

38,5

38,0

Source: Author

gRAPhIC 5: ComPARIsoN of ThE CAPITAl PosITIoN of INsuREd AmouNTs IN ThE oPTImIsTIC sCENARIo AfTER 15 yEARs

11

Benefits for financial sustainability

After studying this analysis, the financial institution’s managers should look into the pos-

sibility of purchasing insurance for an amount equal to approximately 0.8% of the cred-

it portfolio value. As indicated in Graphics 4, 5, and 6, this level of insurance can greatly

reduce risk, as measured by the volatility of the capital base. Table 3 demonstrates these

differences for the specific position of the financial institution in the three scenarios.

Under all scenarios, the insured financial institution is in a better position. On average,

these studies indicate that the financial institution reduces its risk by 22%, for an amount

of 0.5 basis points.

0 50 100 150 200 250 300 350 400 450

12%

10%

8%

6%

4%

2%

Self-insured

Variance

Aver

age

37

36

35

34

33

32

31

30

29

28

27

Source: Author

gRAPhIC 6: ComPARIsoN of ThE CAPITAl PosITIoN of INsuREd AmouNTs IN ThE PEssImIsTIC sCENARIo AfTER 15 yEARs

TABlE 3: modElEd EffECT oN ExPECTEd vAluE ANd CAPITAl volATIlITy of ThE fINANCIAl INsTITuTIoN’s PuRChAsE of INsuRANCE, ACCoRdINg To ThE sCENARIos

Scenario Measure Uninsured insured % change

optimistic Average 38,54 39,21 +1,7%

Variance 143,37 102,92 –28,2%

Moderate Average 34,83 34,93 0,3%

Variance 226,65 174,49 –23,0%

Pessimistic Average 27,90 28,33 +1,2%

Variance 384,23 325,36 –15,3%

Source: Author

12

social and qualitative benefits

Insurance has several benefits additional to those presented in the previous model.

1

2

3

4

heightened reputation as an innovative, socially committed company and market leader

The financial institution is already known as a rapidly growing, effec-

tive, and socially committed financial intermediary. This reputation should

improve when it becomes the first to insure itself against a major

banking risk in Peru. The financial institution’s marketing strategies

will highlight this innovation and the increased resiliency.

increased international visibility among socially conscious investors and donors

The financial institution plans to use the protection offered by the insur-

ance to increase its outreach to underserved households and business-

es. Furthermore, if there were an extreme El Niño event, it would expect

to allocate its payments to the most affected regions where it operates

where the demand for credit for recovery and reconstruction will be

greatest. The opportunities for extending the benefits of the insurance

to borrowers in a more formal manner through the financial services it

offered may also be a significant step for the financial institution.

improved risk profile of credit rating agencies and debt and capital investors

Although it is not clear if the insurance will improve the financial insti-

tution’s explicit rating, it certainly will improve its risk profile, a factor

which can also be important to current and potential investors.

Potential for reduced regulator burden of the financial institution because insurance is a formally recognized as a risk management tool

The banking sector provides important services to the economy that can

facilitate growth. Bank failure can generate shocks in credit generation

13

5 Strategically market positioning after an extreme el niño event can open doors to the financial institution for an in-creased market share

After a severe El Niño event, borrowers will have a growing need for

credit to recover and to rebuild, but many banks will not be in a good

position to extend them loans because they will have experienced huge

losses. Bankers that were in business during the 1998 El Niño reported

that strong banks were able to take over entire groups of weakened

banks in the aftermath. Since the insurance will improve the financial

institution’s position after a severe El Niño event vis-à-vis uninsured

banks, it will be able to capture a greater market share in that period.

that lead to economic losses. Therefore, one policy objective is to avoid

shocks in the credit market, thereby reducing bank failure. Policymak-

ers expect to satisfy this objective with minimal social cost related to

a reduction in credit access.

Capital requirements are an important risk management mechanism

that can act as a buffer against losses from a variety of risks. Banking law

dealing with portfolio risk management that solely uses capital reserves

is limited in the following ways: 1) Basel requirements are not sensitive

to the systemic risks that Peruvian banks face, 2) they implicitly limit ac-

cess to credit and raise interest rates, 3) they fail to promote portfolio risk

reduction, through diversification, 4) they fail to encourage loans in re-

gions where systemic risks can be transferred, and 5) they perpetuate

credit shocks since banks have to reduce investment after losing capital.

Insuring against significant systemic risks can be a viable complement

to capital reserves that improve prudent regulatory efficiency and ef-

fectiveness by addressing these limitations of capital requirements.

The best use of insurance will probably be for unsettling systemic risks

that can generate substantial portfolio losses, such as disasters. Insur-

ing against natural disasters is usually more important for development

banks in the country since their portfolios tend to be more concentrated

in geographic area and economic sectors. El Niño Insurance is an ex-

cellent example and creates an opportunity for the Peruvian banking

regulatory agency to set a precedent that will reward strategies which

tend to reduce risks among banks in developing countries and that

tackle limitations in the current international banking standards.

14

References

Boucher, S; Carter, M, and C. Guirkinger. “Risk Rationing and Wealth Effects in Credit

Markets: Theory and Implications for Agricultural Development” in American Journal of Agricultural Economics 90 (2008): 409-23.

Khalil, A.F., H.H. Kwon, U. Lall, M.J. Miranda, J.R. Skees. “El Niño-Southern Oscilla-

tion-based Index Insurance for Floods: Statistical Risk Analyses and Application to

Peru.” Water Resources Research 43 (2007): W10416.

McPhaden, M. J. “El Niño and La Niña: Causes and Global Consequences”. Encyclo-pedia of Global Environmental Change, Volume 1: The Earth System: Physical and Chemical Dimensions of Global Environmental Change. MacCracken, M. M., Perry, J. S.

(Eds.) & Munn, T. (Editor-in-Chief), Wily: Hoboken, NJ, 2003.

Skees, J.R. and B. J. Barnett. “Enhancing Microfinance Using Index-Based Risk-Trans-

fer Products.” Agricultural Finance Review 66 (2006): 235-250.

Skees, J.R. and A. G. Murhpy. “ENSO Business Interruption Index Insurance for Cata-

strophic Flooding in Piura, Peru.” GlobalAgRisk, Inc.

Trivelli, C. “Rural Finance and Insurance on the North Coast of Peru.” Summary Report

2005/06. Instituto de Estudios Peruanos, Lima, September 2006.

Van den Heuvel, S. “The Bank Capital Channel of Monetary Policy.” 2006 Meeting Papers

512, Society for Economic Dynamics (2006).

15

Dia

rio

El

tiEm

po, P

iUra

Risk is out there, get insured.

The Insurance for Climate Change Adaptation Project is part of the International Climate Initiative (ICI) of the German Federal Ministry for the Environment, Nature Conservation and Nuclear Safety (BMU).