An alternative approach towards Costing of denim jeans for...

105

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT 1 “An alternative approach towards Costing of denim jeans for Buying House / Export House” Graduation Project submitted in Partial Fulfilment of the requirements For the degree of Bachelor of Fashion Technology (Apparel Production) NATIONAL INSTITUTE OF FASHION TECHNOLOGY, MUMBAI Industry Mentor: Mr. Sanjay Achrekar (General Manager, Katmandu Apparel Pvt. Ltd., Mumbai) College Mentor: Mr. Ranjan K. Saha (Course Co-ordinator, Department of Fashion Technology, NIFT) Manish Singh Dhakad M/BFT/10/11 Semester: VIII

Transcript of An alternative approach towards Costing of denim jeans for...

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

1

“An alternative approach towards Costing of denim jeans for Buying House / Export House”

Graduation Project submitted in Partial Fulfilment of the requirements

For the degree of

Bachelor of Fashion Technology (Apparel Production)

NATIONAL INSTITUTE OF FASHION TECHNOLOGY, MUMBAI

Industry Mentor: Mr. Sanjay Achrekar (General Manager, Katmandu Apparel Pvt. Ltd., Mumbai)

College Mentor: Mr. Ranjan K. Saha (Course Co-ordinator, Department of Fashion Technology, NIFT)

Manish Singh Dhakad

M/BFT/10/11

Semester: VIII

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

2

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

3

PREFACE

The “Bachelor of Fashion Technology” programme is well structured and integrated course of NATIONAL INSTITUTE OF FASHION TECHNOLOGY. The main objective of B.F.Tech. Programme is to develop skill in student by supplement to the theoretical study of apparel mass-production. Textile internship helps to gain real life knowledge about the industrial environment and business practices. B.F.Tech. programme provides student with a fundamental knowledge of business and organizational functions and activities, as well as an exposure to strategic thinking of management. In every professional course, training is an important factor. Professors give us theoretical knowledge of various subjects in the college but we are practically exposed of such subjects when we get the training in the organization. It is only the training through which I come to know that what an industry is and how it works. I can learn about various departmental operations being performed in the industry, which would, in return, help us in the future when I will enter the practical field. During this whole training I got a lot of experience and came to know about the practices in real that how it differs from those of theoretical knowledge and the practically in the real life.

In today‟s globalized world, where cut-throat competition is prevailing in the market, theoretical knowledge is not sufficient. Beside this one need to have practical knowledge, which would help an individual in his/her carrier activities and it is true that “Experience is best teacher”.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

4

ACKNOWLEDGEMENT

With immense pleasure, I would like to present this report as a part of my Graduation Project on "Development of company specific costing model for buying house merchandising". It has been an enriching experience for me to undergo this project, which would not have possible without the goodwill and support of the people around. As a student of National Institute of Fashion Technology, Mumbai I would like to express my sincere thanks to all those who helped me during this period.

I feel my pleasure to extend my sincere thanks and gratitude to my college mentor Mr. Ranjan k. Saha, (Course-Co-ordinator, DFT, NIFT) & industry mentor Mr. Sanjay Achrekar, General Manager (KAPL-Mumbai) who genuinely played his role in right

from planning, project framework to guiding me through this project.

I would also like to thank Mr. Lokesh Gutta, Manager (Production & operation) of Katmandu Apparel Private Limited who gave me all the required information related to apparel production.

Not to forget, I am also thankful to Mr. Kiran Ramakant Temkar (Director) & Mrs. Manisha kiran Temkar (CEO) who was quite helpful in providing different facilities during the project period.

Mr. Mahesh Khopkar, Mr. Jude James, Mr. Sameer Gandhi, Mr. Gautam Kamble, Mr. Dharmesh Jain, Mrs. Tejal Pallan & Carmen Katke of KAPL also lend their helping hands in making me understand merchandising concepts & Costing parameters involved in the process.

I am also grateful to all the HODs and Miss. Vijeshri Kolbekar who led my way and I

am extremely thankful for the help and support of the staff and employees of

Katmandu Apparel Private Limited without which I could not make my project this

much successful.

Here comes the time to say my thanks to my institute NIFT which provided me

this golden opportunity. At last but not the least I‟d like to thank my seniors and

classmates who helped me directly or indirectly through their valuable suggestion.

However, I accept the sole responsibility for any possible error of omission

and would be extremely grateful to the readers of this project report if they bring such

mistakes to my notice.

MANISH SINGH DHAKAD

M/BFT/10/11

NIFT, MUMBAI

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

5

ABSTRACT

Sourcing operations in Garment Buying House are extremely complex due to

the intricacies of a global supply chain. Sourcing decisions should not be made

without an exhaustive analysis of cost structures of resources required for

production. FOB & Landed costs must be analysed for sourcing decisions, but they

must be complemented by information of the effects of supplier lead times and

consumer-retail interactions, which are critical to overall supply chain performance.

To do perfect garment costing, one must know about all these activities

thoroughly about their costs, procedures, advantages and risk factors. Also he must

know how to solve the problems when occurred and to take suitable alternate

decision immediately in time. We must be aware that there are always fluctuations in

the costs of raw materials and accessories, charges of knitting, processing, finishing,

sewing and packing, charges of transport and conveyance. Hence we must have

update knowledge about the latest prices and charges, latest procedures, methods

and quality systems, market prices and availability, transportation (road, sea, air) and

freight charges, etc.

An alternative approach towards Costing of denim jeans in a specific Buying

House has been developed in this study. The model looks at cost structures for the

entire supply chain from raw material sourcing to export of finished goods. The cost

model shows the accrual of costs throughout each processing step within the textile

and apparel industry. It also identifies costs related to international trade, including

transportation costs and other different types of cost.

The study examines the supply chain processes and costs for producing

denim jeans in Asian region of the world. Trade agreement duty provisions, world

cotton market price competitiveness, export tax rebates, and labour rates

significantly affect a countries‟ competitiveness in the textile and apparel industry.

The study helps identify the cost makeup of each process and the resources

consumed.

This model can assist companies to look outside their area of operation and

have an appreciation of costs related to upstream and/or downstream processes

within their supply chain. They can identify broad issues related to their strategic

partnerships with suppliers and customers and investigate these in more detail. By

combining supply chain costs, transportation time, and manufacturing

responsiveness, analyses can be performed to identify scenarios where

responsiveness is more critical than cost effectiveness. This study has found that a

responsive supply chain can outweigh a lower cost but less responsive supply chain

in certain sourcing environments.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

6

TABLE OF CONTENTS

1. INTRODUCTION ......................................................................................................................... 7

1.1. NEED OF THE PROJECT .............................................................................................................. 8

1.2. PROBLEM FORMULATION ........................................................................................................ 9

1.3. IDENTIFICATION OF TOPIC/DEVELOPMENT OF RESEARCH PROPOSAL ................................. 11

1.4. OBJECTIVE & SUB-OBJECTIVE OF THE PROJECT ..................................................................... 13

2. REVIEW OF LITERATURE ......................................................................................................... 14

2.1. COST, COSTING & COST ACCOUNTING .................................................................................. 15

2.2. CLASSIFICATION OF COST ON DIFFERENT BASIS .................................................................... 15

2.3. ESSENTIALS OF GOOD COSTING SYSTEM ............................................................................... 18

2.4. RESEARCH JOURNAL ABSTRACT .............................................................................................. 18

2.5. COST CALCULATION SOFTWARES AVAILABLE IN MARKET ..................................................... 20

2.6. COST COMPONENTS ANALYSIS .............................................................................................. 21

2.7. COST CALCULATIONS FORMULAS .......................................................................................... 22

2.8. DIFFERENT PRICES OF RAW MATERIAL & LABOUR IN MARKET ............................................. 23

3. METHODOLOGY ....................................................................................................................... 25

3.1. QUANTITATIVE RESEARCH ...................................................................................................... 26

3.2. QUALITATIVE RESEARCH ......................................................................................................... 27

3.3. DATA COLLECTION METHOD .................................................................................................. 27

3.4. REPRESENTATION OF DATA ANALYSIS .................................................................................... 28

3.5. STEPS OF METHODOLOGY ...................................................................................................... 29

3.6. WEEKLY TIME AND ACTION CALENDER .................................................................................. 31

4. DATA COLLECTION & ANALYSIS ............................................................................................. 32

5. RESULT & EXPECTED OUTCOME ............................................................................................ 98

6. LIMITATIONS & FUTURE SCOPE OF PROJECT ...................................................................... 100

7. CONCLUSION ......................................................................................................................... 102

8. BIBLIOGRAPHY....................................................................................................................... 104

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

7

CHAPTER-1

INTRODUCTION

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

8

1. INTRODUCTION:-

I conducted my Graduation Project at KATMANDU APPAREL PRIVATE LIMITED, MUMBAI from 20 January 2014 to 20 May 2014. During my course of project, I tried to understand the concepts of garment costing, starting from the concept sample to the bulk production. I tried to imply the knowledge I have gained through various Merchandising, Costing & production related subjects I have been taught at NIFT and from all the knowledge I have gained at our institute and here at KATMANDU APPAREL PVT. LTD.; I have tried to document it here with my best efforts.

1.1 NEED OF THE PROJECT:

The Indian textile and apparel industry is very large and diverse,

employing 35 million people and accounting for 27 per cent of the country's

exports. The apparel industry plays a pivotal role as a key driver of the

national economy and has grown to be the most significant contributor to the

country's economy over nearly three decades of its existence.

The industry recorded a remarkable growth in a protected market

environment; it faces a series of challenges notably in areas such as:

Price competitiveness.

Faster lead times.

High raw material base.

Full service offering.

Access to market. "A Cost is the value of economic resources used as

a result of producing or doing the things costed".

In order to achieve perfect garment costing, one must know about all

the activities including purchase of fabrics, sewing, packing, transport,

overheads, etc. & one must know about all these activities thoroughly about

their costs, procedures, advantages and risk factors. Also he must know how

to solve the problems when occurred and to take suitable alternate decision

immediately in time.

We must be aware that there are always fluctuations in the costs of raw

materials and accessories, charges of knitting, processing, finishing, sewing

and packing, charges of transport and conveyance. Hence we must have

update knowledge about the latest prices and charges, latest procedures,

methods and quality systems, market prices and availability, transportation

(road, sea, air) and freight charges, etc.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

9

We must remember that the quality depends on price; price depends

on quality. Each product will have different price according to its quality. We

do not manufacture only one quality of garments. Also we manufacture the

garments not only for one customer. While we do the garment costing, the

customer‟s price level, quality & quantity and payment terms, to be taken into

consideration.

1.2 PROBLEM FORMULATION:

1.2.1 INITIAL IDEA

Simplification of Costing of Denim Jeans during concept sample

development stage to generate value for research & development in

new technology by development of cost calculation system.

1.2.2 RESEARCH PROBLEM

During Costing process at the garment sampling stage, there

are certain variances that are not taken into consideration because of

its negligible effect during the production stage; there is a random

variation in costing from concept development stage to production

stage (usually a bit higher). The main problems here in Costing are

given below-

a. Standard operating procedures not followed b. No fix cost for value added service (embroidery, printing etc.) c. No check-points for cost components factors (stretch,

Shrinkage etc.) d. No Calculation of trims (sewing threads etc.) for optimizes

sourcing procedure. e. A department like sampling takes more time than the usual

because of absence of Research & Development.

1.2.3 OBJECTIVE OF RESEARCH

To develop an alternative approach towards costing of denim

jeans with extrapolation of existing methods which will try to reduce

cost & generate value for investment for Research & Development in

new technical machinery.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

10

1.2.4 APPROCH ADOPTION TO METHODOLOGY

INITIAL IDEA

BACKGROUND STUDY

REFINEMENT OF IDEA & PROBLEM FORMULATION

REVIEW OF LITERATURE

DESIGN & DEVELOPMENT

OF METHODOLOGY

DATA COLLECTION &

ANALYSIS

EXPECTED OUTCOME

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

11

1.3 IDENTIFICATION OF TOPIC / DEVELOPMENT OF RESEARCH PROPOSAL:

Project Title: An alternative approach towards Costing of denim

jeans for Buying House Merchandising.

Company Name: Katmandu Apparel Private Limited, Mumbai

Student Name: Manish Singh Dhakad (M/BFT/10/11)

Industry Mentor: Sanjay Archrekar, General Manager,

Kathmandu Apparel Private Limited, Mumbai

College Mentor: Ranjan Kumar Saha, Course-Coordinator

Department of Fashion Technology,

National Institute Of Fashion Technology

Project Idea: Simplification of Costing of Denim Jeans during

concept sample development stage to generate

value for research & development in new

technology by development of cost calculation

system.

Problem Statement: • During costing process at the garment sampling

stage, there are certain variables that are not &

taken into consideration because of its negligible

effect during the production stage, hence there is a

random deviation in the costing from sampling

stage to production stage.

• This project will help the company to find various

dependent variables in garment costing to

minimize the deviation in costing & to find

accuracy in costing at Research & development

stage by involving those variables which are not

there in past researches and previously developed

application/software.

Objective: To develop an alternative approach towards

costing of denim jeans with extrapolation of

existing methods which will try to reduce cost &

generate value for investment for Research &

Development in new technical machinery.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

12

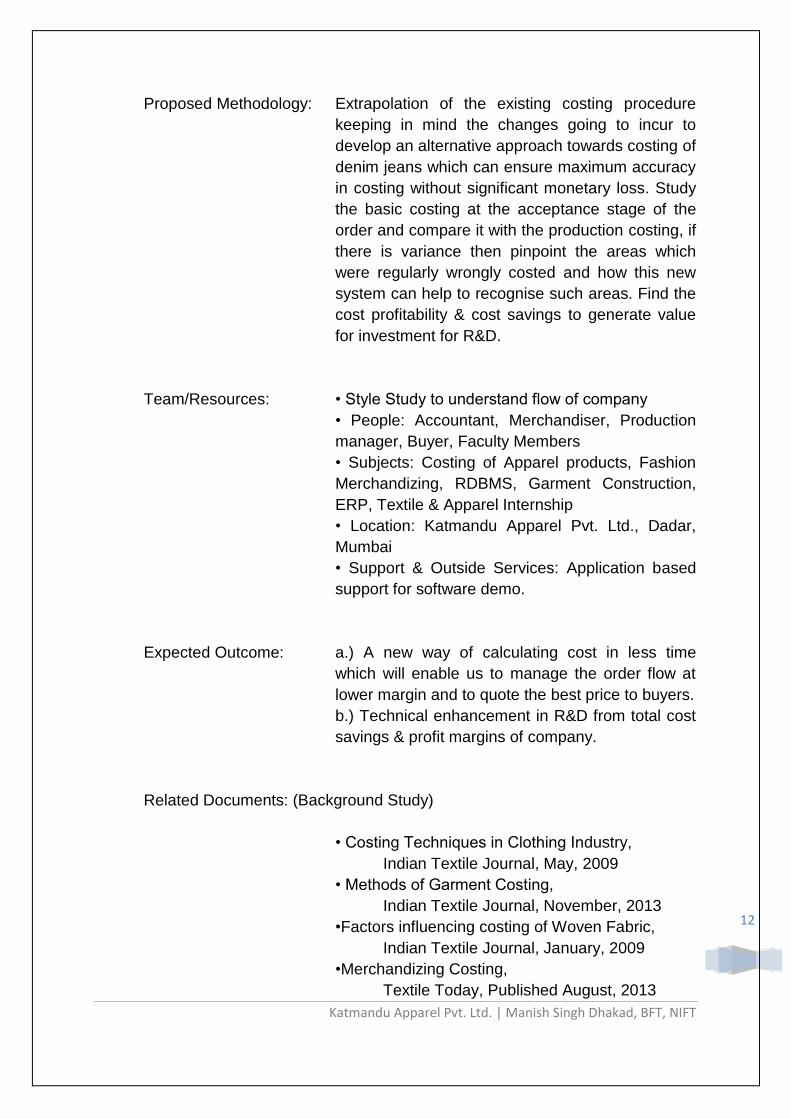

Proposed Methodology: Extrapolation of the existing costing procedure

keeping in mind the changes going to incur to

develop an alternative approach towards costing of

denim jeans which can ensure maximum accuracy

in costing without significant monetary loss. Study

the basic costing at the acceptance stage of the

order and compare it with the production costing, if

there is variance then pinpoint the areas which

were regularly wrongly costed and how this new

system can help to recognise such areas. Find the

cost profitability & cost savings to generate value

for investment for R&D.

Team/Resources: • Style Study to understand flow of company

• People: Accountant, Merchandiser, Production

manager, Buyer, Faculty Members

• Subjects: Costing of Apparel products, Fashion

Merchandizing, RDBMS, Garment Construction,

ERP, Textile & Apparel Internship

• Location: Katmandu Apparel Pvt. Ltd., Dadar,

Mumbai

• Support & Outside Services: Application based

support for software demo.

Expected Outcome: a.) A new way of calculating cost in less time

which will enable us to manage the order flow at

lower margin and to quote the best price to buyers.

b.) Technical enhancement in R&D from total cost

savings & profit margins of company.

Related Documents: (Background Study)

• Costing Techniques in Clothing Industry,

Indian Textile Journal, May, 2009

• Methods of Garment Costing,

Indian Textile Journal, November, 2013

•Factors influencing costing of Woven Fabric,

Indian Textile Journal, January, 2009

•Merchandizing Costing,

Textile Today, Published August, 2013

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

13

1.4 OBJECTIVE OF THE PROJECT:

The objectives of graduation project is firstly to gain practical exposure and

secondly application of knowledge on real life projects and/or assignments.

This graduation project is aimed towards blending the class room principles

with industry application. This project also helps students to learn and improve

their interpersonal communication skills with colleagues, peer group and workers.

The main Objective of this Graduation Project is -

“To develop an alternative approach towards costing of denim jeans

with extrapolation of existing methods which will try to reduce cost &

generate value for investment for Research & Development in new

technology & machinery.”

1.4.1 SUB-OBJECTIVE OF THE PROJECT

Sub-objectives of the project will be all the secondary objectives which

are required for achieving Primary or main objective of the research.

To find dependent and independent factors of costing which are not there in past researches & previously developed applications.

To minimize the deviation in costing from concept development stage to production stage for accuracy in Costing.

To find Cost profitability in implementing new software, this will also reduce lead time, labour & Cost.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

14

CHAPTER-2

REVIEW OF LITERATURE

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

15

2. REVIEW OF LITERATURE:-

A review of literature may be a self-contained unit -- an end in itself -- or a preface to and rationale for engaging in primary research. A review is a required part of research proposals and generally, the purpose of a review is to analyze critically a segment of a published body of knowledge through summary, classification, and comparison of prior research studies, reviews of literature, and theoretical articles or Journals.

2.1 COST, COSTING & COST ACCOUNTING:

Cost can be defined as the expenditure incurred on or attributable to a

given thing. Cost is the amount of resources used for something which must be measured in terms of money.

Costing is the techniques and processes of ascertaining costs. The techniques to be followed for the analysis of expenses and the processes of different products or services differ from industry to industry. The main object of costing is the analysis of financial records, so as to subdivide expenditure and to allocate it carefully to selected cost centres, and hence to build up a total cost for the departments, processes or jobs or contracts of the undertaking.

Cost Accounting primarily deals with collection, analysis of relevant of cost data for interpretation and presentation for various problems of management. It is defined as, „the establishment of budgets, standard costs and actual costs of operations, processes, activities or products and the analysis of variances, profitability or the social use of funds‟.

(Source: Managerial and Cost Accounting_2009

Larry M. Walther, Christopher J. Skousen, Free book by Bookboon.com)

2.2 CLASSIFICATION OF COST ON DIFFERENT BASIS

2.2.1 On the Basis of Time: a. Historical Costs: These costs are ascertained after they are

incurred. Such costs are available only when the production of a particular thing has already been done.

b. Pre-determined Costs: These costs are calculated before they are incurred on the basis of a specification of all factors affecting cost. Such costs may be:

(i) Estimated costs: Costs are estimated before goods

are produced; these are naturally less accurate than

standards.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

16

(ii) Standard costs: This is a particular concept and

technique. This method involves:

2.2.2 On the basis of Nature of Elements:

There are three broad elements of costs which can be illustrated

by the following chart:

2.2.3 On the basis of Association with the Product:

a. Product Costs: Product costs are those which are traceable to the product and included in inventory values. In a manufacturing concern it comprises the cost of direct materials, direct labour and manufacturing overheads.

b. Period Costs: Period costs are incurred on the basis of time such as rent, salaries, etc., include many selling and administrative costs essential to keep the business running. Though they are necessary to generate revenue, they are not associated with production; therefore, they cannot be assigned to a product.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

17

2.2.4 On the basis of Functionality:

A company performs a number of functions. Functional costs

may be classified as follows:

a. Manufacturing/production Costs: It is the cost of operating the manufacturing division of an undertaking.

b. Administration Costs: They are indirect and covers all expenditure incurred in formulating the policy, directing the organisation and controlling the operation of a concern, which is not related to research, development, production, distribution or selling functions.

c. Selling and Distribution Cost: Selling cost is the cost of seeking to create and stimulate demand e.g. advertisements, market research etc. Distribution cost is the expenditure incurred which begins with making the package produced available for dispatch and ends with making the reconditioned packages available for re-use e.g. warehousing, cartage etc.

d. Research and Development Costs: They include the cost of discovering new ideas, process and products by experiment and implementing such results on a commercial basis.

e. Pre-production Cost: When a new factory is started or when a new product is introduced, certain expenses are incurred. There are trial runs. Such costs are termed as pre-production costs and treated as deferred revenue expenditure.

2.2.5 On the basis of behaviour:

Costs can also be classified according to their behaviour.

a. Fixed Costs b. Variable Costs c. Semi-variable Costs

(Source: Study material: Executive programme

Cost and Management Accounting (Module-1, Paper-2)

The Institute of Company Secretaries of India

In Pursuit of Professional Excellence, Statutory body under an Act of Parliament

ICSI House, 22, Institutional Area, Lodi Road, New Delhi- 110003

Class notes (Sem-VI) : Costing of Apparel Products

By- Rengini Chandramohan (Associate Professor))

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

18

2.3 ESSENTIALS OF GOOD COSTING SYSTEM:

For availing of maximum benefits, a good costing system should

possess the following characteristics.

Costing system adopted in any organization should be suitable to its nature and size of the business and its information needs.

A costing system should be such that it is economical and the benefits derived from the same should be more than the cost of operating of the same.

Costing system should be simple to operate and understand. Unnecessary complications should be avoided.

Costing system should ensure proper system of accounting for material, labour and overheads and there should be proper classification made at the time of recording of the transaction itself.

Before designing a costing system, need and objectives of the system should be identified.

The costing system should ensure that the final aim of ascertaining of cost as accurately possible should be achieved.

(Source: Intermediate (Group-II, Paper-8) Cost and Accounting management

The institute of Cost Accountants of India,

12, Sudder Street, KOLKATA- 700016)

2.4 RESEARCH JOURNALS ABSTRACT

Costing is a very complex procedure, with set patterns and guidelines

followed by the industry, and it is difficult to find out costs for every processes

there are some inbuilt costs while costing, elaborate Saroj Bala and Tripti

Gupta.

About 65 - 70% cost of the garment is the cost of the fabric and hence,

it is very crucial to get the right cost of the fabric from fabric manufacturers

and suppliers. Garment manufacturers struggle to get the best possible cost

of the fabric. It would be interesting to know the important points to consider

for getting a comprehensive understanding of costing. Costing seems to be a

complex exercise as it depends on a number of variables.

What are the costs to consider…?

i) Direct cost: Cost of raw material -- 66%. Cost of size and chemicals -

4%. Production cost comprising of running the machine, maintenance, power

fuel, humidification and other utilities -- 8 % and worker wages and salaries --

8% losses incurred due to shrinkage, wastage, grading, and also selling

commissions.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

19

ii) Indirect cost: Interest on investment, loan, working capital,

depreciation, etc. Above 7%, overheads and administrative expenses like

travelling, telephone, couriers, legal issues, taxes comprising of 7%.

iii) Profit: 10 - 20% depending on the order size. In some companies, 70% of the fabric cost will comprise of direct cost, but in corporate selling only 40% cost of the fabric is direct cost and 60% is overheads.

What are the factors which affect the cost …?

Type of raw material

Amount of raw material or GSM of the fabric

Sizing and Chemicals Cost

Production cost or cost of weaving process

Mill-made or power loom made

Wastage and shrinkage

Dyeing costs

Length & Width of fabric

Shade %

Class of dye and quality

Colour

Weight of the fabric

Finishing cost

Shrinkage and wastage

Export terms & Conditions

(Source: Ms Saroj Bala, Associate Professor & Mrs Tripti Gupta, Assistant Professor

Pearl Academy of Fashion, New Delhi

Factors influencing costing of Woven Fabric

Indian Textile Journal, January, 2009)

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

20

2.5 COST CALCULATION SOFTWARES AVAILABLE IN MARKET

MerchanNet 6.08 (Cost: $599.00USD)

Software for garment, clothing, apparel, leather, footwear, bags,

luggage, socks, hats, necktie manufacturer, export trading company and

factory in soft line products.

CostingNet 4.38 (Cost: $249.00USD)

CostingNet is used to create a detail product costing sheet. Best for

factory or manufacturer in industry like garment, clothing, apparel, toys, home

textiles, giftware, premium goods, household product, footwear, bags,

luggage, plastic products, electrical & electronics, travel and sporting goods.

SampleNet 4.28 (Cost: $249.00USD)

SampleNet is used to manage all the sample development activity for

your merchandising department. It generates sample orders with YY, trim

parts and size spec., sample invoices, customs invoice, sample history report

and sample status report in different grouping.

(Source: www.softmenu.org

www.ibuyer.hk)

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

21

2.6 COST COMPONENTS ANALYSIS

Direct Material:

Fabric Shell (Consumption, Rate, Unit of measurement, Quantity)

Fabric lining (Consumption, Rate, Unit of measurement, Quantity)

Fabric Pocketing (Consumption, Rate, Unit of measurement, Quantity)

Trims & accessories

(Consumption, Rate, Unit of measurement, Quantity)

All sewing trims are taken into consideration like Buttons,

Zipper, Label, Rivet, Velcro, Twill tape, Studs, Hanger, and

Polybags etc. except packaging trims like Carton boxes & stick

tapes.

Direct Labour: (Average manufacturing cost is taken from factory)

Cut, Make (Rate, UOM, Quantity)

Packaging charges (Rate, UOM, Quantity)

Direct expenses: (Average manufacturing cost is taken from factory)

Washing (Rate, UOM, Quantity)

Heat Seal (Rate, UOM, Quantity)

Print (Rate, UOM, Quantity)

Embroidery (Rate, UOM, Quantity)

Profit margin are added as per Buyer`s requirement of Quality,

Quantity & Lead-time.

(Source: Basic Cost sheet and Quotation sheet,

Katmandu Apparel Private Limited)

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

22

2.7 COST CALCULATIONS FORMULAS

Warp Cost (cost per yard) = [{ } ]

Weft Cost (cost per yard) = [{ } ]

Warp weight =

Weft weight =

Fabric cost = [warp weight × warp yarn cost × weft weight × weft

yarn cost]

Cutting labour cost =

Finishing labour cost =

Cost per minute =

CM cost = SAM of garment x minute cost of labour / line efficiency

Efficiency for styles =

Labor cost (salary paid) = SMV x Labour cost per minute

CM = cutting cost + sewing cost + finishing cost

(Source: www.ocs.com (Online Clothing Study)

Class notes-NIFT (Sem-VI-B.F.Tech.) : Costing of Apparel Products

By- Rengini Chandramohan (Associate Professor))

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

23

2.8 DIFFERENT PRICES OF RAW MATERIAL, LABOUR & OTHER

SERVICES IN MARKET

Cotton seed price: 2.52 Yuan per ton (china)

Seed cotton price: 8.93 Yuan per ton (china)

Cotton Price:

S.No. Month US Cents per pound

1 July 2013 92.62

2 Jun 2013 93.08

3 August 2013 92.71

4 September 2013 90.09

5 October 2013 89.35

6 November 2013 84.65

7 December 2013 87.49

8 Jan 2013 87.21 *Cotton with seed = 3 × cotton without seed

Labour cost in different manufacturing countries by ILO in USD

per hour:

Asian competitors:

S.No. Country USD per hour

1. Bangladesh 0.22

2. Cambodia 0.33

3. Pakistan 0.37

4. Vietnam 0.38

5. Srilanka 0.43

6. Indonesia 0.44

7. India 0.51

8. Remote inland area China

0.55 - 0.80

9. Other costal & core area China

0.86 - 0.94

10. Prime costal area China 1.08

11. Malaysia 1.18

12. Thailand 1.29-1.36

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

24

US region supplier:

S.No. Country USD per hour

1. Mexico 2.54

2. Honduras 1.72 - 1.82

3. Dominican Republic 1.55 - 1.95

4. Haiti 0.49 - 0.55

5. US 14.10

African region supplier:

S.No. Country USD per hour

1. Turkey 2.44

2. Morocco 2.24

3. Russia 1.97

4. Tunisia 1.68

5. Bulgaria 1.53

6. Jordan 1.01

7. Egypt 0.83

Energy rates:

S.No. Country USD per kilo watt hour

1. China 0.1000

2. Colombia 0.1070

3. Guatemala 0.1600

4. India 0.1120

5. US 0.0630

6. Vietnam 0.0550 *Water rates, steam, other cost can also be added.

Duty Rates:

S.No. Country Duty % Rebate %

1. China 16.5 15

2. Colombia 16.5 0

3. Guatemala 0 0

4. India 16.5 0

5. US 0 0

6. Vietnam 16.5 0

(Source: International Labour Organisation, ILO)

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

25

CHAPTER-3

METHODOLOGY

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

26

3. DESIGN AND DEVELOPMENT OF METHODOLOGY

3.1 Quantitative Research

3.1.1 Descriptive and interpretive approaches to qualitative research

(Whatisthecurrentsituation?)

Descriptive research seeks to describe the current status of an

identified variable or phenomenon. The researcher does not usually

begin with an hypothesis, but is likely to develop one after collecting

data. Analysis and synthesis of the data provide the test of the

hypothesis. Systematic collection of information requires careful

selection of the units studied and measurement of each variable in

order to demonstrate validity.

3.1.2 Correlation analysis approach

(Whatisthe Possible cause?)

Correlational research attempts to determine the extent of a

relationship between two or more variables using statistical

data. Relationships between and among a number of facts are sought

and interpreted to recognize trends and patterns in data, but it does not

go so far in its analysis to establish cause and effect for them. Data,

relationships, and distributions of variables are observed only.

Variables are not manipulated; they are only identified and are studied

as they occur in a natural setting.

*Sometimes correlational research is considered a type of descriptive

research, and not as its own type of research, as no variables are

manipulated in the study.

3.1.3Causal-Comparative/Quasi-Experimental

(Whatwasthecause?)

Causal-comparative/quasi-experimental research attempts to

establish cause-effect relationships among the variables. These types

of design are very similar to true experiments, but with some key

differences. An independent variable is identified but not manipulated

by the experimenter, and effects of the independent variable on the

dependent variable are measured. The researcher does not randomly

assign groups and must use ones that are naturally formed or pre-

existing groups. Identified control groups exposed to the treatment

variable are studied and compared to groups who are not.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

27

3.2 Qualitative Research

3.2.1 Historical (Whatwasthesituation?)

Descriptionofpastevents,problems,issues,facts

Datagathered from written or oral descriptions of past events,

artifacts, etc.

Describeswhatwasinanattempttoreconstructthepast involves

much interpretationofeventsanditsinfluenceonthepresent

3.2.2 Grounded Theory (What is grounded theory?)

Grounded theory is probably applied less often in business

research than is either phenomenology or ethnography.

Grounded theory represents an inductive investigation in which the

researcher poses questions about information provided by

respondents or taken from historical records. The researcher asks the

questions to him or herself and repeatedly questions the responses to

derive deeper explanations. Grounded theory is particularly applicable

in highly dynamic situations involving rapid and significant change.

3.2.3 Ethnography (what is self-Observation?)

Ethnography represents ways of studying cultures through

methods that involve becoming highly active within that culture.

Participant Observation involved in ethnography approach means the

researcher becomes immersed within the culture that he or she is

studying and draw data from his or her observation.

(Source: http://www.weber.edu, http://www.bcps.org/ and

CHAPTER 7 QUALITATIVE RESEARCH TOOLS_ http://www.cengage.com/)

3.3 Data collection method:

3.3.1 Primary Data: Extrapolation of Past records, Company Cost

sheets, ERP Software Database, Different Directories of fabric, Trims & other

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

28

Costs. Demonstrations of different cost effective software, Sourcing

Department Records. Analysis of existing system.

3.3.2 Secondary Data: Available researches on costing, Textile

Journals and Books available in Resource Center, Related Internet websites

and previously developed application available on web. Class room Study

Material & Internship reports.

3.4 Representation of data analysis:

3.4.1 Brainstorming:

Brainstorming works by focusing on a problem, and then

deliberately coming up with as many solutions as possible and by pushing the

ideas as far as possible. One of the reasons it is so effective is that the

brainstormers not only come up with new ideas in a session, but also spark off

from associations with other people's ideas by developing and refining them.

No criticism Welcome unusual ideas Quantity Wanted Combine and improve ideas

3.4.2 Check-sheet (Defect concentration diagram)

A check sheet is a structured, prepared form for collecting and

analyzing data. This is a generic tool that can be adapted for a wide variety of

purposes.

3.4.3 Histogram:

A graphical representation, similar to a bar chart in structure,

that organizes a group of data points into user-specified ranges. The

histogram condenses a data series into an easily interpreted visual by taking

many data points and grouping them into logical ranges or bins.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

29

3.5 Steps of methodology:

To develop an alternative approach towards costing of denim jeans

with extrapolation of existing methods which will try to reduce cost & generate

value for investment for Research & Development in new technical

machinery.

3.5.1 To find dependent and independent factors of costing which are not there in past researches & previously developed applications.

Study the Company flow process & Job of Costing merchant.

Study the Cost related Journals and Researches for finding

variables.

Brain-storming for developing check-sheet of Material & Labour

requirement.

Collection of Check-sheet data of any concept sample for

correction & Improvisation.

Differentiate dependent & independent factors for each entity.

Find advantages & disadvantages of including different

dependent & independent variables.

3.5.2 To minimize the deviation in costing from concept development stage to production stage for accuracy in Costing.

Study of detailed Costing process & Cost components for

effective Sourcing procedures.

Study of all Costing formulas in detail for accuracy in Costing.

Development of cost-sheet formats & other cost absorption

formats in detail.

Customization of thread calculator as per the company product

type for effective thread consumption calculation.

Collect data for costing of samples & costs which are followed

by the company during concept sampling stage including

wastages & profit margins to develop cost sheet for a particular

season.

Compare cost and find variance & total cost savings.

Develop charts for the total trends followed in fabric prices.

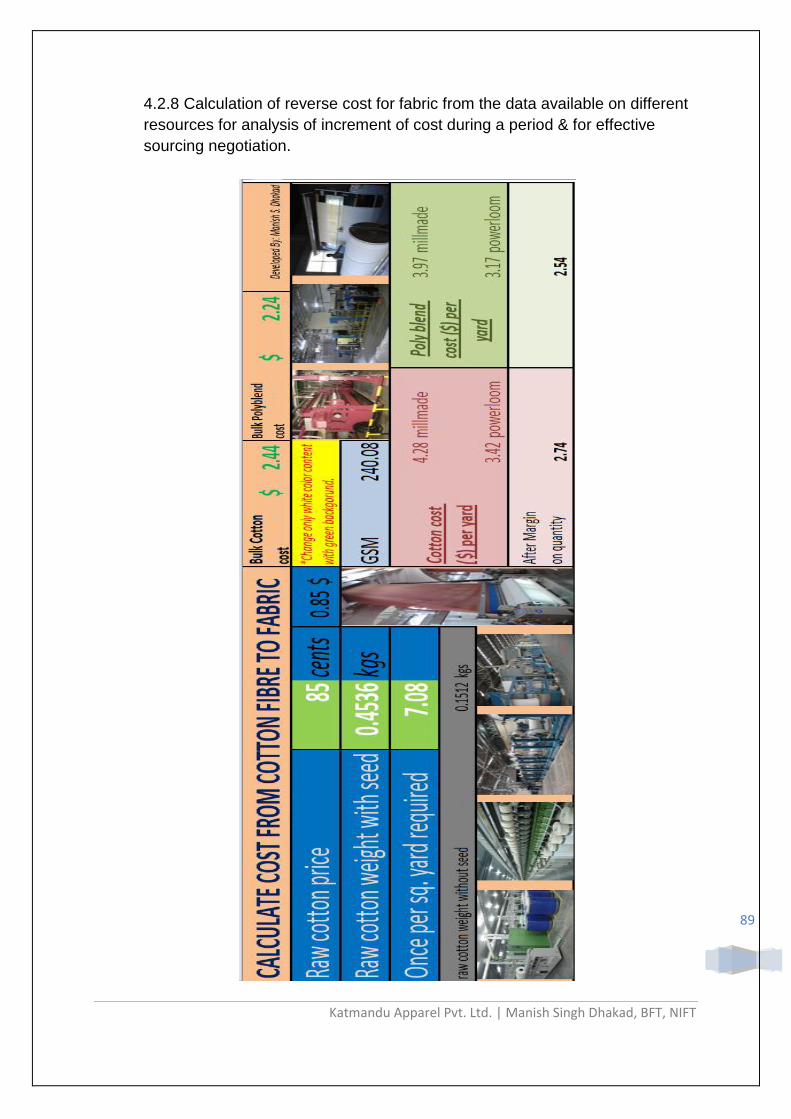

Calculation of reverse cost for fabric from the data available on

different resources for analysis of increment of cost during a

period & for effective sourcing negotiation.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

30

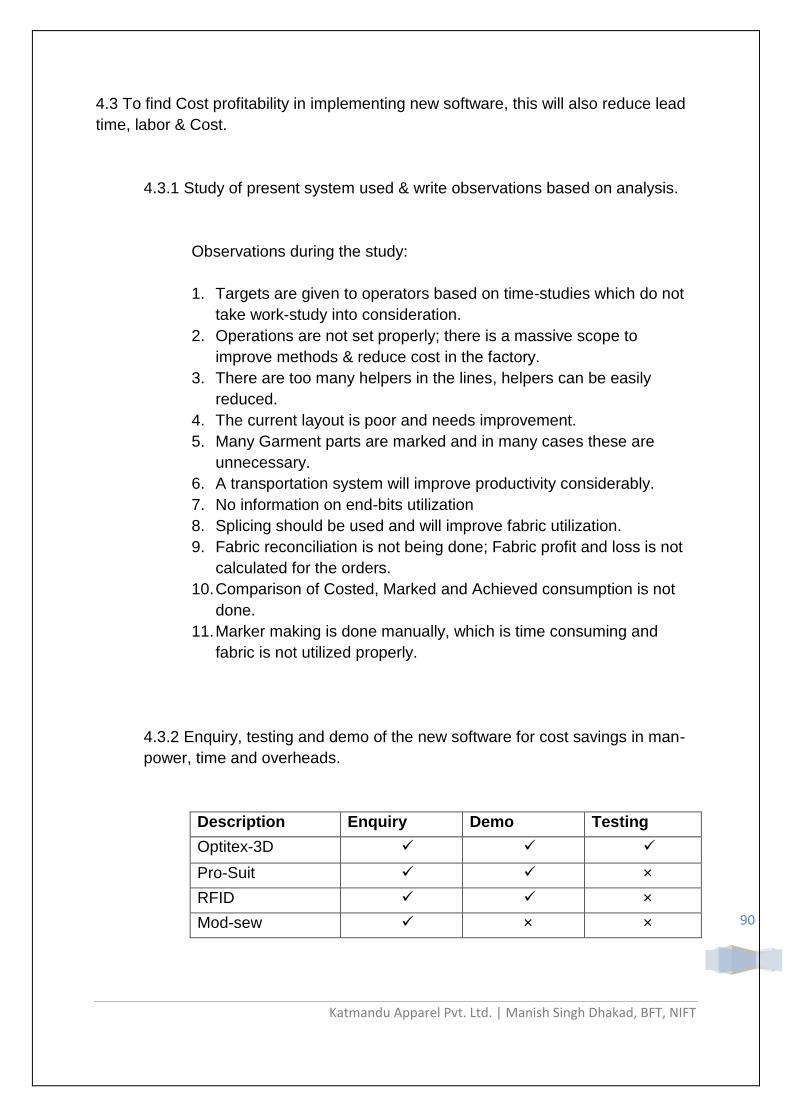

3.5.3 To find Cost profitability in implementing new software, this will also reduce lead time, labour & Cost.

Study of present software used & find advantages &

disadvantages of the system.

Enquiry, testing and demo of the new software for cost savings

in man-power, time and overheads.

Comparison of cost profitability in implementing new system.

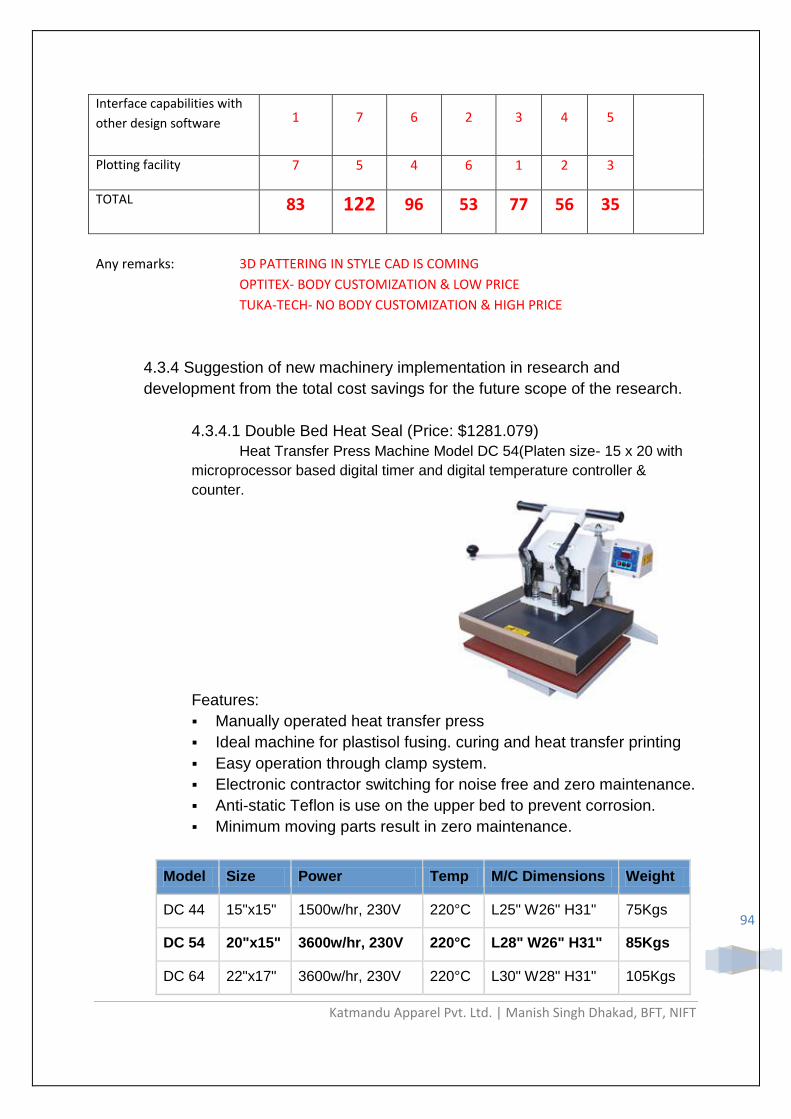

Suggestion of new machinery implementation in research and

development from the total cost savings for the future scope of

the research.

Reasons for investment in technological upgradation.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

31

MO

NTH

(W

eek)

TOP

IC1

st2

nd

3rd

4th

1st

2n

d3

rd4

th1

st2

nd

3rd

4th

1st

2n

d3

rd4

th

1D

evel

op

men

t o

f C

on

cep

t fo

r G

P

2Id

enti

fica

tio

n o

f To

pic

3D

evel

op

men

t o

f R

esea

rch

Pro

po

sal

4St

ud

y o

f co

mp

any

flo

w p

roce

ss

5Li

tera

ture

Stu

dy

6B

ackg

rou

nd

Stu

dy

7D

esig

n &

Dev

elo

pm

ent

of

Met

ho

do

logy

8Jo

b o

f C

ost

ing

mer

chan

t

9St

ud

y al

l co

stin

g fo

rmu

la in

det

ail f

or

accu

racy

in c

ost

ing

10

Un

der

stan

d t

he

Co

stin

g p

roce

ss &

co

st c

om

po

nen

ts

11

Dev

elo

p f

orm

ats

of

form

s an

d c

hec

k-sh

eet

12

Dev

elo

p f

orm

at f

or

Co

st-s

hee

t

13

Mid

term

Rev

iew

& A

nal

ysis

of

feed

bac

k

14

Exec

uti

on

an

d F

ield

Wo

rk

15

Dat

a C

olle

ctio

n a

nd

An

alys

is

16

Dev

elo

p n

ew c

ost

sh

eet

for

con

cep

t sa

mp

les

17

Stu

dy

of

con

cep

t d

evel

op

men

t sa

mp

le f

or

cost

ing

18

Fin

d a

ll d

epen

den

t an

d in

dep

end

ent

vari

able

s

19

Dif

fere

nti

ate

dep

end

ent

and

ind

epen

den

t fa

cto

rs

20

Dat

a co

llect

ion

of

styl

es f

or

chec

k-sh

eet

dir

ecto

ry

21

Fin

d t

he

mar

gin

var

ian

ce b

etw

een

qu

ota

tio

n o

f d

iffe

ren

t st

yles

22

Fin

d a

dva

nta

ges

and

dis

adva

nta

ges

of

incl

ud

ing

dep

end

ent

and

ind

epen

den

t va

riab

les

23

Fin

d t

ota

l co

st s

avin

gs a

nd

mar

gin

incr

emen

ts d

uri

ng

the

per

iod

24

Test

ing

and

dem

o o

f th

e n

ew s

oft

war

e fo

r co

st s

avin

gs in

man

-po

wer

, tim

e an

d o

verh

ead

s

25

Co

mp

aris

on

of

new

ap

plic

atio

n im

ple

men

tati

on

26

Enq

uir

y o

f n

ew m

ach

iner

y im

ple

men

tati

on

in r

esea

rch

an

d d

evel

op

men

t

27

The

futu

re s

cop

e o

f th

e re

sear

ch

28

Rep

ort

Wri

tin

g

WEE

KLY

TIM

E A

ND

AC

TIO

N C

ALE

ND

ER

S.N

o.

JAN

UA

RY

FEB

RU

AR

YM

AR

CH

AP

RIL

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

32

CHAPTER-4

DATA COLLECTION &

ANALYSIS

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

33

4.1 To find dependent and independent factors of costing which are not there

in past researches/Journals/Literature & previously developed applications.

4.1.1 Study the Company flow process & Job of Costing merchant.

a) Company flow process of Katmandu Apparel Pvt. Ltd.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

34

b) Job of Costing Merchant:

Develop standard costs.

Determine the cost of purchased or manufactured products/services.

Analyze the variance between costs and standard costs.

Interact with Production Control to ensure Bills of Materials (BOM) are accurate and up to date. Review and audit BOM‟s to ensure they reflect the latest manufacturing practices.

Analyze actual labor, material, and overhead cost against standard/Budget.

Work with the finance department to implement and apply cost accounting policies and procedures.

Support Controller‟s efforts for implementing and maintaining internal controls for operations, sales, engineering, and finance.

Development of new labor and overhead rates, budget, and forecasts.

(Manufacturing Cost Analyst Job Description, http://www.lewmar.com

Main Duties of Cost Analyst, http://www.jobwings.com)

4.1.2 Study the Cost related Journals and Researches for finding variables.

(

(Source: Factors influencing costing of Woven Fabric,

Indian Textile Journal, January, 2009)

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

35

4.1.3 Brain-storming for developing check-sheet of Material & Labor

requirement.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

36

4.1.4 Collection of Check-sheet data of any concept sample for correction &

Improvisation.

Co

st_i

dSM

_23_

01SM

_23_

02SM

_23_

03SM

_23_

04SM

_23_

05

Pro

du

ct p

acka

ge n

o.

8264

4

Styl

e n

o.

KA

G_8

2644

Re

fere

nce

no

.C

F14_

8264

4

Co

lle

ctio

nSk

inn

y Je

ans

Seas

on

Fall

201

4

Pro

du

ct G

rou

pD

en

im J

ean

s

Bra

nd

JCP

Cat

ego

ryC

hil

dre

ns

Mat

eri

alW

ear

Bu

yer

De

nim

Fact

ory

Jess

ica

Mar

ple

Pro

du

ct D

esc

rip

tio

nK

AG

Fab

ric

sup

pli

er

AZG

(DC

M)-

Skin

ny

Jean

s

Ass

ign

ed

IBO

Ind

ia

Co

stin

g Fo

rSu

pp

lie

r

Size

sR

egu

lar

Fin

ish

De

stru

ctiv

e, r

inse

, Ro

ck

was

hD

est

ruct

ive

, rin

se, R

ock

De

sign

er

Sgil

l 19

Styl

e li

ne

Bo

tto

m W

ear

Co

stin

g re

mar

kD

eve

lop

me

nt

Stag

e

Cu

rre

ncy

fo

r co

stin

gU

SD-I

NR

Han

dle

d b

yM

anis

h D

hak

ad

UO

Mp

er

Gar

me

nt

Trad

e t

erm

FOB

STYL

E D

ETA

ILS

BR

EAKD

OW

N

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

37

Cost_id

Fabric For Shell_1 Shell_2 Pocketing

Mill Reference_id KAG-13-391 KAG-13-1091 poly-cotton

Buyer Reference_id

Supplier

Fabric Type Denim Denim Pocketing

Composition Cotton, Ramie, Poly, Spandex Cotton, Ramie, Poly, Spandex Poly, Cotton

Sourcing type Yarn dyed yarn dyed Solid

UOM yds yds yds

Quantity

Quality grade

Weave Twill Twill Twill

Color Blue Blue White

Style

Yarn type Ring-spun Ring-spun Ring-spun

Loom

Country of origin China China China

Count 28x28

GSM 120

Payment terms

Shrinkage 4.5 to 8.5 4.5 to 8.5 4.5 to 8.5

Wastage

Size & chemical

Finishing

Cuttable width 57 55 57

Finished width 58/59 56/57 58/59

Dyeing type Indigo Indigo

Lead time 120 Days 120 Days 120 Days

Extra % 3-5 % 3-5 % 3-5 %

Consumption per marker

Number of garments in marker 18 18

Average consumption

SM_23_01

MATERIAL COST BREAKDOWN

Cost_id

Trim_id TS_82644_1 TS_82644_2 TS_82644_3 TS_82644_4 TS_82644_5 TS_82644_6 TS_82644_7 TP_82644_1

Trim type Stitching Stitching Stitching Stitching Stitching Stitching Stitching Packaging

Trim Description AZ Metal logo Shank-27L-6-16

Category Buttons Buttons Zipper Thread Thread Elastic Buttons

Sub-catergory Shank Rivet Metal Sewing Decorative Adjustable 4 hole Plastic

Size 27L 14L 3 120-60 Tkt 40 Tkt 3/4 inches 24 L

UOM Piece Piece Piece Meter Meter Inche Piece

Price terms

Consumption

Quantity

Extra % 5 5 5 10 10 5 5

Wastage 3 3 3 3 3 3 3

Brand Arizona Arizona YKK Coats Coats Slotted Clear Plastic

Material Metal Metal Metal Cotton Cotton Spandex Plastic

Supplier

Remark/Code JAZ-086AT JAZ-083 #3 Color Contrast Slotted 4 hole

Destruction Wash GY22 GY22 Antique Copper C8601 C3950 DTM Clear

Rinse Wash GY22 GY22 Antique Copper C2336 C3950 DTM Clear

Rock Wash GY22 GY22 Antique Copper A&E#45957 Tan#3 C3950 DTM Clear

TRIMS COST BREAKDOWN

SM_23_01

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

38

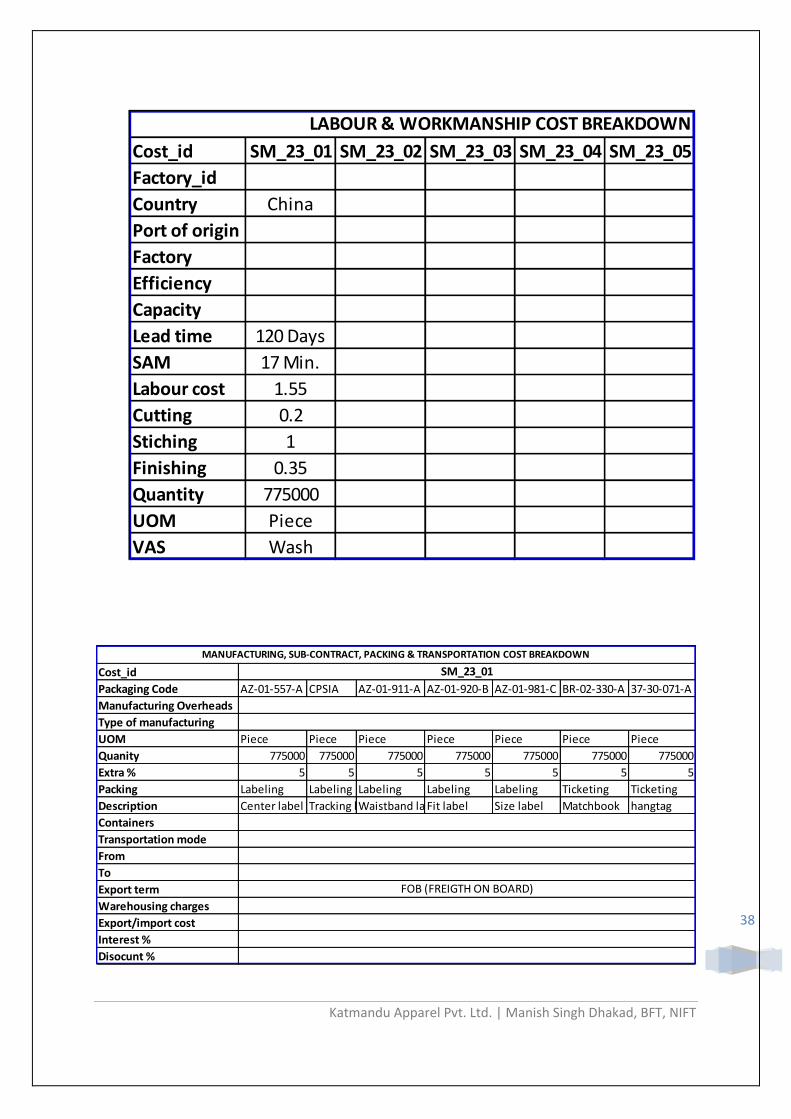

Cost_id

Packaging Code AZ-01-557-A CPSIA AZ-01-911-A AZ-01-920-B AZ-01-981-C BR-02-330-A 37-30-071-A

Manufacturing Overheads

Type of manufacturing

UOM Piece Piece Piece Piece Piece Piece Piece

Quanity 775000 775000 775000 775000 775000 775000 775000

Extra % 5 5 5 5 5 5 5

Packing Labeling Labeling Labeling Labeling Labeling Ticketing Ticketing

Description Center label Tracking labelWaistband labelFit label Size label Matchbook hangtag

Containers

Transportation mode

From

To

Export term

Warehousing charges

Export/import cost

Interest %

Disocunt %

MANUFACTURING, SUB-CONTRACT, PACKING & TRANSPORTATION COST BREAKDOWN

FOB (FREIGTH ON BOARD)

SM_23_01

Cost_id SM_23_01 SM_23_02 SM_23_03 SM_23_04 SM_23_05

Factory_id

Country China

Port of origin

Factory

Efficiency

Capacity

Lead time 120 Days

SAM 17 Min.

Labour cost 1.55

Cutting 0.2

Stiching 1

Finishing 0.35

Quantity 775000

UOM Piece

VAS Wash

LABOUR & WORKMANSHIP COST BREAKDOWN

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

39

Co

st_i

dSM

_23_

01SM

_23_

02SM

_23_

03SM

_23_

04SM

_23_

05SM

_23_

06SM

_23_

07

Lead

tim

e

Bu

ild

ing

ren

t

sala

ry o

f st

aff

Bil

ls

Uti

liti

es

Tran

spo

rtai

on

Exp

en

ses

Ad

min

istr

ativ

e

Emp

loye

e w

elf

are

Stat

ion

ary

& p

rin

tin

g

Pan

try

Ho

use

ke

ep

ing

Ove

rtim

e

Sale

s &

Dis

trib

uti

on

Pro

fit

%

R &

D

Secu

rity

& h

elp

ers

Trai

nin

g &

Re

cru

itm

en

t

Re

pai

r &

Re

pla

cem

en

t

De

pre

ciat

ion

Ne

wsp

ape

r &

Mag

azin

es

Aft

er

sale

s e

xpe

nse

s

Ban

k Ex

pe

nse

s

Oth

ers

AD

MIN

ISTR

ATI

VE,

SA

LES

& D

ISTR

IBU

TIO

N, P

RO

FIT

& O

THER

CO

ST B

REA

KD

OW

N

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

40

4.1.5 Differentiate dependent & independent factors for each entity.

STYLE DETAILS BREAKDOWN

S.No. Entity Dependent/Independent

1 Cost_id

2 Product package no.

3 Style no.

4 Reference no.

5 Collection

6 Season

7 Product Group

8 Brand

9 Category

10 Material Dependent

11 Buyer Dependent

12 Factory Dependent

13 Product Description

14 Fabric supplier

15 Assigned IBO

16 Costing For

17 Sizes

18 Finish Dependent

19 Wash Dependent

20 Designer

21 Style line

22 Costing remark

23 Currency for costing

24 Handled by

25 UOM

26 Trade term Dependent

MATERIAL COST BREAKDOWN

S.No. Entity Dependent/Independent

1 Cost_id

2 Fabric For

3 Mill Reference_id

4 Buyer Reference_id

5 Supplier

6 Fabric Type Dependent

7 Composition Dependent

8 Sourcing type

9 UOM

10 Quantity Dependent

11 Quality grade Dependent

12 Weave Dependent

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

41

13 Color Dependent

14 Style

15 Yarn type Dependent

16 Loom Dependent

17 Country of origin Dependent

18 Count Dependent

19 GSM Dependent

20 Payment terms Dependent

21 Shrinkage Dependent

22 Wastage Dependent

23 Size & chemical Dependent

24 Finishing Dependent

25 Cuttable width Dependent

26 Finished width Dependent

27 Dyeing type Dependent

28 Lead time Dependent

29 Extra %

30 Consumption per marker

31 Number of garments in marker

32 Average consumption Dependent

TRIMS COST BREAKDOWN

S.No. Entity Dependent/Independent

1 Cost_id

2 Trim_id

3 Trim type Dependent

4 Trim Description

5 Category Dependent

6 Sub-catergory Dependent

7 Size Dependent

8 UOM

9 Price terms Dependent

10 Consumption Dependent

11 Quantity Dependent

12 Wastage

13 Brand Dependent

14 Material Dependent

15 Supplier

16 Remark/Code

17 Destruction Wash Dependent

18 Rinse Wash Dependent

19 Rock Wash Dependent

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

42

LABOUR & WORKMANSHIP COST BREAKDOWN

S.No. Entity Dependent/Independent

1 Cost_id

2 Factory_id

3 Country Dependent

4 Port of origin Dependent

5 Factory Dependent

6 Efficiency Dependent

7 Capacity

8 Lead time Dependent

9 SAM Dependent

10 Labour cost Dependent

11 Cutting Dependent

12 Stitching Dependent

13 Finishing Dependent

14 Quantity Dependent

15 UOM

16 VAS Dependent

MANUFACTURING, SUB-CONTRACT, PACKING & TRANSPORTATION COST BREAKDOWN

S.No. Entity Dependent/Independent

1 Cost_id

2 Packaging Code

3 Manufacturing

4 Overheads

5 Type of manufacturing Dependent

6 UOM

7 Quanity Dependent

8 Packing Dependent

9 Description

10 Containers Dependent

11 Transportation mode From/To

Dependent

12 Export term Dependent

13 Warehousing charges

14 Interest % Dependent

15 Export/import cost

16 Disocunt % Dependent

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

43

ADMINISTRATIVE, SALES & DISTRIBUTION, PROFIT & OTHER COST BREAKDOWN

S.No. Entity Dependent/Independent

1 Cost_id

2 Lead time

3 Building rent

4 salary of staff Bills

5 Utilities

6 Transportation Expenses

Dependent

7 Administrative Dependent

8 Employee welfare

9 Stationary & printing

10 Pantry

11 House keeping

12 Overtime

13 Sales & Distribution

14 Profit %

15 R & D

16 Security & helpers

17 Training & Recruitment

18 Repair & Replacement

19 Depreciation

20 Newspaper & Magazines

21 After sales expenses

22 Bank Expenses

23 Others

4.1.6 Find advantages & disadvantages of including different

dependent & independent variables in Cost Accounting.

Advantages Disadvantages

Dependent variables are directly related to the cost of the entity, as it is directly linked to value added service. Independent variable helps us to understand & create linkage to develop directory & also for reference purpose.

Dependent variables must be analyzed time to time as; cost may differ from time to time. Independent variables are not directly related to cost; hence they can be used for referring material type etc. Not for cost of material directly.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

44

4.2 To minimize the deviation in costing from concept development stage to

production stage for accuracy in Costing.

4.2.1 Study of detailed Costing process & Cost components for

effective Sourcing procedures.

Material cost is a major cost component of garment

manufacturing costs and a correct cost calculation method will give one

a better projection of garment cost for a style, explains Vishnu Pareek.

To do perfect garment costing, one must know about all these

activities thoroughly about their costs, procedures, advantages and risk

factors. Also he must know how to solve the problems when they occur

and to take suitable alternate decision immediately in time.

There are always fluctuations in the costs of raw materials and

accessories, charges of knitting, processing, finishing, sewing and

packing, charges of transport and conveyance. Hence knowledge

update is required about the latest prices and charges, latest

procedures, methods and quality systems, market prices and

availability, transportation (road, sea, air) and freight charges, etc.

Different Costing methods include:

Job Costing

Batch Costing

Contract or Terminal Costing

Single or Output Costing

Process Costing

Operation Costing

Operating Costing

Departmental Costing

Multiple Costing

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

45

4.2.2 Study of all Costing formulas in detail for accuracy in Costing.

Fabric Cost Breakdown: (No transportation cost involved)

1). Warp Cost (cost per yard) = [{ } ]

(1Maund ≈ 37 Kilograms)

(1 Oz. = 28.350 grams)

(Denim⟶ 7-10 oz. & Non-denim⟶ 4-6 oz.)

2). Weft Cost (cost per yard) = [{ } ]

(1 meter = 1.094 yards = 39.3701 inches)

(Fabric width 59" = 1.4986 meters)

3). Wastage = 7 %

4). Miscellaneous = (weaving + Electricity + Maintenance etc.)

5). Fabric weight = [warp weight + weft weight]

6). Weaving Cost per Yard = Warp cost + Weft cost +

Wastage + Miscellaneous

7). Warp weight =

8). Total ends = Fabric width X Ends per inch X Shrinkage %

(Raw Cotton yarn shrinkage = 8 - 10 %)

9). Weft weight

=

10). Fabric cost = [warp weight × warp yarn cost × weft

weight × weft yarn cost]

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

46

Price of fabric depends upon:

a) Raw material cost

b) Weaving cost

c) Processing cost

d) Yarn dyeing cost

e) Packaging cost

f) Grey checking cost

g) Excise & other duties

h) Machine & Land depreciation

i) Manpower cost (Indirect labour)

j) Power & Water cost

k) Profit

For ascertaining turns per inch:

For weft (medium) yarn = √ × 3.25

For warp (medium) yarn = √ × 3.75

GSM ∝ Ends per inch/Picks per inch/Construction ∝

GSM ∝ Cost (for same type of fabric)

Sizing cost ∝

Weight of warp per sq. meter of fabric in grams (A)

=

Weight of weft per sq. meter of fabric in grams (B)

=

GSM = Weight of weft yarn (A) + Weight of warp yarn (B)

GSM = *

+

(Ounce/Sq. yard) = (GSM/33.91)

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

47

General specification of denim jeans:

GSM = 200 - 400

Yarn density (Tex) = 60 - 100

Density or Count = 10 – 6

GSM = *

+ ×[ ]

1 Tex = weight of 1000 meter thread in grams.

Tkt. = (

)

(Rs.30) (Rs. 30) (Rs. 10per meter.)

Ginning ⟶ Roving ⟶ Yarn ⟶ weaving

(Rs. 1.5 kg) (1 kg.)

(If order >15,000-20,000 meter then Dyeing Cost lowers by Rs.1-2/-)

Price in China market:

S.No. Process Cost (USD per pound)

1 Washing fiber $ 2.75 per pound

2 Twist $ 3 per pound

3 Carding $ 2.75 per pound

4 Worsted single ply $19 per pound

Average textile processing cost:

S.No. Process Cost Percentage

1 Carding cost $ 1.373 per pound

19-20 %

2 Filling Spinning room cost

$ 1.26 per pound 18 %

3 Warping room cost

$ 0.92 per pound 13 %

4 Spooling cost $0.558 per pound 8 %

5 Warping $ 0.183 per pound

2.5 %

6 Drawing cost $ 0.239 per pound

3.5 %

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

48

7 Web drafting $ 0.501 per pound

7 %

8 Weaving $ 1.267 per pound

7.5 %

9 Finishing $ 0.639 per pound

Different types of wastes:

S.No. Item Percentage

1 Invisible loss 1.5 %

2 Sweepings 1.5 %

3 Usable waste 3-4 %

4 Card Sliver 0.5 %

5 Draw frame sliver 0.6 %

6 Speed frame 0.5 %

7 Ring frame 1.0 %

8 Roving end 0.4 %

9 Open end sliver 0.3 %

10 Combing 1 - 1.5 %

11 Waste overall 3-4 % (seeds)

12 Trash 15 % (depending upon geographical location)

13 Doff conditioning 1-1.5 %

14 Poly Spandex 6-12 % (weaving performance 100-130 %)

15 Warping & Weaving waste 2-3 %

16 Waste shrinkage 1-1.5 %

17 Value loss 7 % in running cotton

18 3 % in running polyester

Dyeing cost:

Vat Dyes > Reactive Dyes

Finishing Cost:

Flame retardency - 15Rs./meter

Anti-static - 5Rs./meter

Anti-satin - 10Rs./meter

Anti-wrinkle - 5Rs./meter

If added in jigger (softners) - 10Rs./Kg.

Stentering - 20Rs./Kg.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

49

Shrinkage/Wastage:

Cambric / Cotton - 5%

Poly blends - 4.5% - 5%

COST OF FABRIC = COST OF GREY FABRIC+DYEING

CHARGES+FINISHINGING CHARGES+SHRINKAGE/WASTAGE

Weaving costs:

Mill made loom cost ≈ 125 % Power loom cost

Twill weave = 12 paisa / pick / inch / sq. meter

Satin weave = 12 paisa / pick / inch / sq. meter

P.V. Suiting = 14.2 paisa / pick / inch / sq. meter

For 1000 meter dobby = 17 paisa / pick / inch / sq. meter

For 1000 meter Jacquard = 20 paisa / pick / inch / sq. meter

For 2400 hook Jacquard = 17 paisa / pick / inch / sq. meter

Double beam fabric = 40 paisa / pick / inch / sq. meter

Rs. 35 per Kg. (approx.) includes steam, power or wages.

Raw material cost per meter for 150 cm fabric width

= [2.3 x Ozs. per sq. yard + 8.4]±4%

RMC (Ring per meter) = RMC OE per meter x [1+Oz. per sq. yard/100]

iNDEX = [ ] x 0.27

UHML=Upper half mean limit

Str.=Strength in grams per tex using HVI mode.

Fabric cost consideration:

a.) Take accurate fabric consumption based upon new marker

ratio and take testing commitment for width, shrinkage & defect

percentage.

b.) Take 2-7% buffer margin on material cost estimation.

c.) Take consumption of pocket lining, shell etc. & all other

different fabric used.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

50

Labour cost breakdown:

Efficiency for styles =

Cutting labour cost =

Finishing labour cost =

Cost per minute =

Labor cost (salary paid) = SMV x Labour cost per minute

CM = cutting cost + sewing cost + finishing cost

CM cost = SAM of garment x minute cost of labour / line efficiency

For accuracy:

Labour cost per minute =

CMT charges will include stitching, cutting, finishing, packing,

embellishment, value added services, trims.

Factory overhead over direct labour wages =

Labour rate variance = (standard rate - actual rate) x actual hour

worked

Cutting SAM = Spreading, Marking, Cutting, Re-layering, Re-

cutting, Sorting, Bundling.

Stitching SAM = m/c time + material handling with allowances +

Bundle time

Total m/c time = [{(A+17B+C) x D} + {(A+17B+C) x D} E

= (1+E %) x {(A+17B+C) x D}

Finishing SAM: Pressing & finishing SAM will be calculated as

per operations.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

51

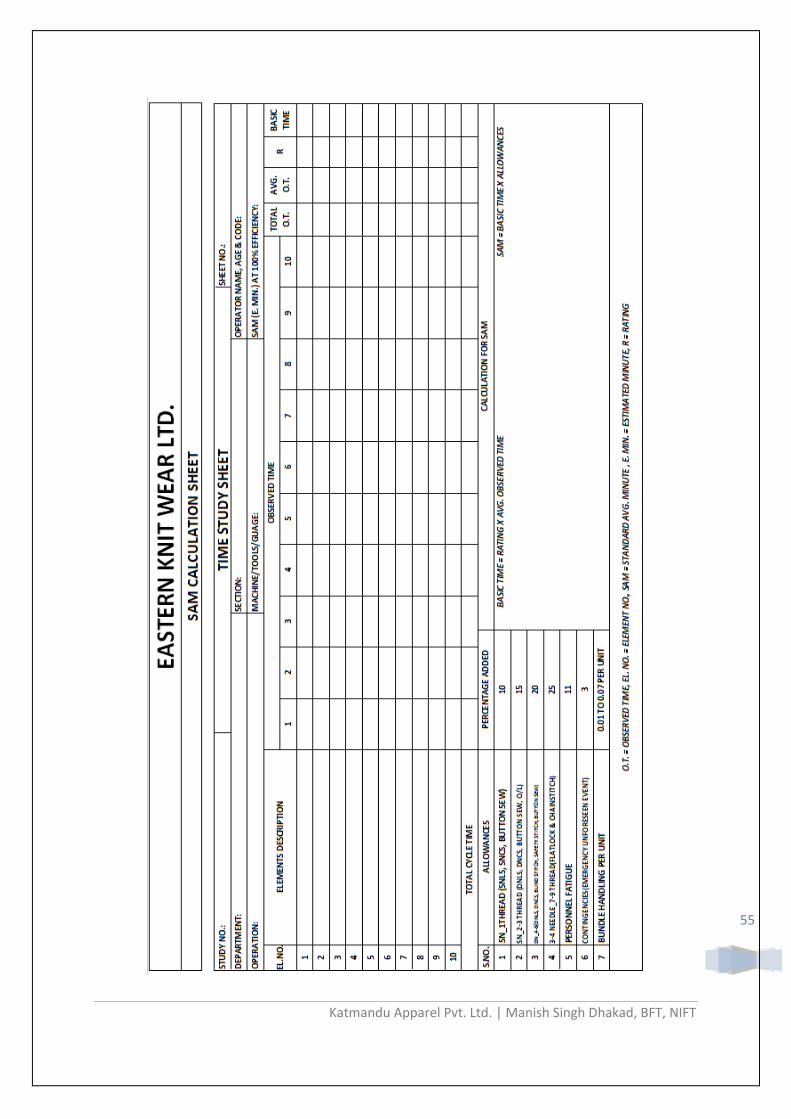

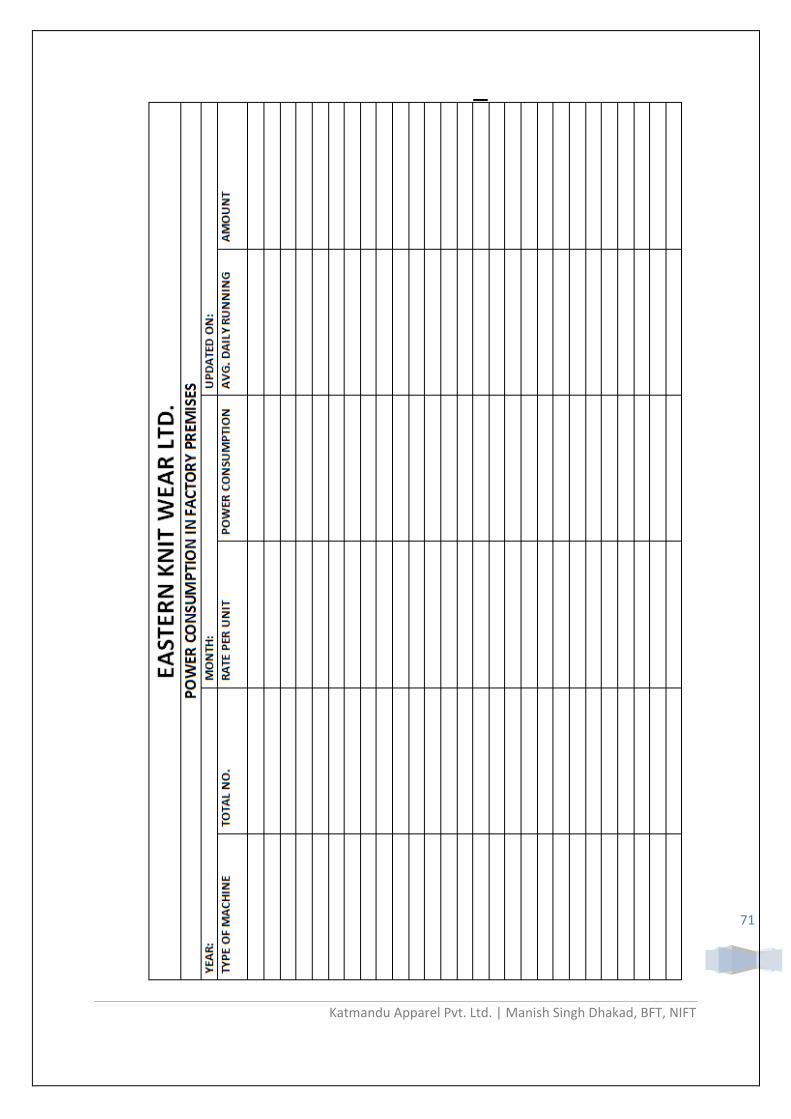

4.2.3 Development of cost-sheet formats & other cost absorption

formats in detail.

For Pre-production Costing formats:

Factory expenses sheet

Administrative expenses sheet

Selling & Distribution expenses sheet

Time-study sheet

Data-base sheet

Cost-Sheet format

For Post-production Costing formats:

Sewing Section sheet

Cutting Section sheet

Finishing & Packaging Section sheet

Power consumption in Cutting section

Power consumption in Sewing section

Power consumption in finishing & packing section

Depreciation Sheet

Insurance Premium sheet

Consumable goods sheet

Vehicles sheet

Mechanic`s purchase form

Total electricity consumption sheet

Indirect Labour expenses

Power consumption sheet

Cost-sheet format

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

52

EASTERN KNIT WEAR LTD.

EXPENSES INCURRED IN FACTORY

S.NO. ITEMS PER MONTH PER MONTH ON DENIM JEANS

TAKA USD TAKA USD

1 LESS: CLOSING STOCK

2 Freight & Forwarding

3 Freight inward

4 Electricity Bills

5 Fuel (Diesel & petrol) & Coal

6 Consumables stores

7 Annual maintenance contract

8 Books & Periodicals

9 Conveyance

10 Courier charges

11 Recruitment & Training

12 Insurance premium

13 Staff welfare

14 Miscellaneous expenses

15 Postage & telegram

16 Printing & stationary

17 Rent & Taxes

18 Repair & maintenance (m/c)

19 Repair & maintenance (Vehicles)

20 Repair & maintenance (plant)

21 Telephone & VC

22 Travelling

23 Water charges

24 Depreciation

25 Indirect labor (Managers)

26 Power

27 Waste/normal loss of material

28 Waste for foremen

29 Oil

30 Gases

31 Steam

32 Canteen & recreation

33 Drawing & Office expenses

34 Workers Compensation

35 Research expenses R&D

36 Health & Safety (facilities)

37 Security & House keeping

38 Store supervision expenses

39 Expenses of service department

40 ADD: OPENING WIP

TOTAL

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

53

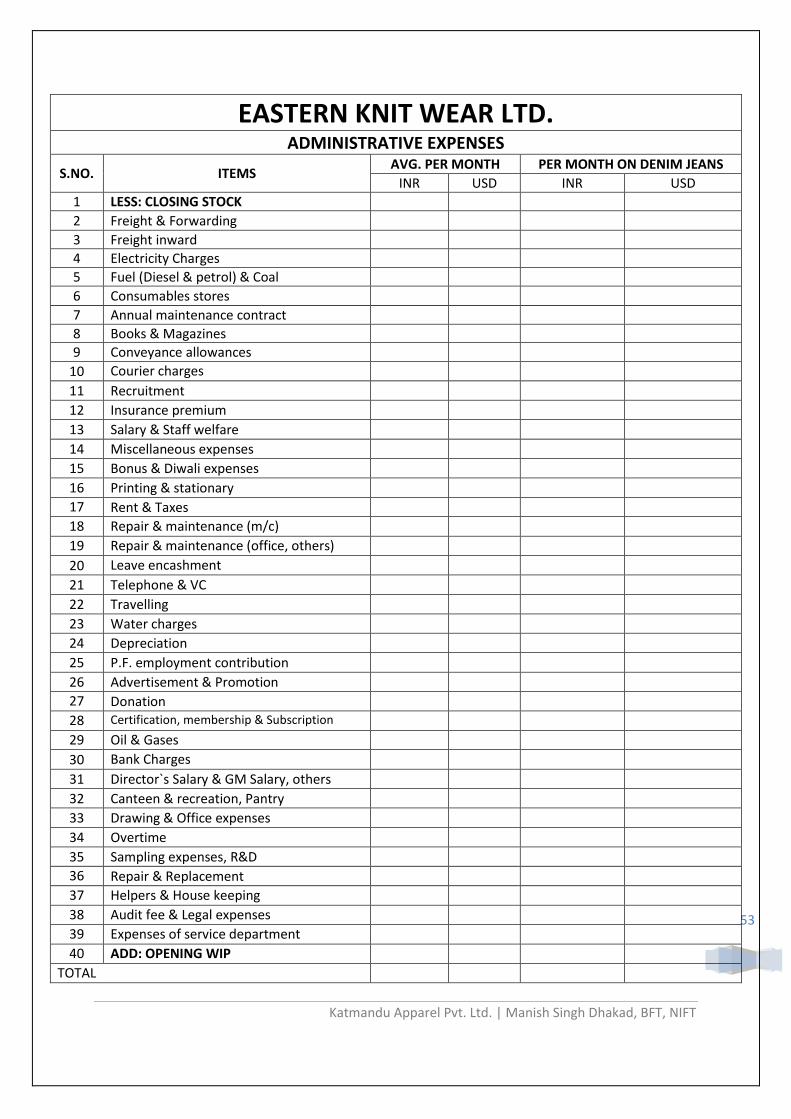

EASTERN KNIT WEAR LTD.

ADMINISTRATIVE EXPENSES

S.NO. ITEMS AVG. PER MONTH PER MONTH ON DENIM JEANS

INR USD INR USD

1 LESS: CLOSING STOCK

2 Freight & Forwarding

3 Freight inward

4 Electricity Charges

5 Fuel (Diesel & petrol) & Coal

6 Consumables stores

7 Annual maintenance contract

8 Books & Magazines

9 Conveyance allowances

10 Courier charges

11 Recruitment

12 Insurance premium

13 Salary & Staff welfare

14 Miscellaneous expenses

15 Bonus & Diwali expenses

16 Printing & stationary

17 Rent & Taxes

18 Repair & maintenance (m/c)

19 Repair & maintenance (office, others)

20 Leave encashment

21 Telephone & VC

22 Travelling

23 Water charges

24 Depreciation

25 P.F. employment contribution

26 Advertisement & Promotion

27 Donation

28 Certification, membership & Subscription

29 Oil & Gases

30 Bank Charges

31 Director`s Salary & GM Salary, others

32 Canteen & recreation, Pantry

33 Drawing & Office expenses

34 Overtime

35 Sampling expenses, R&D

36 Repair & Replacement

37 Helpers & House keeping

38 Audit fee & Legal expenses

39 Expenses of service department

40 ADD: OPENING WIP

TOTAL

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

54

EASTERN KNIT WEAR LTD.

SALES & DISTRIBUTION EXPENSES

S.NO. ITEMS AVG. PER MONTH PER MONTH ON DENIM JEANS

INR USD INR USD

1 LESS: CLOSING STOCK

2 Courier charges

3 EGCC Report

4 Export promotion Council

5 Freight charges

6 Laboratory charges

7 Sales & Promotion

8 Ware housing charges

9 Audit & Quality checking

10 Sales tax

11 Foreign tours

12 Insurance

13 Catalogues

14 Samples

15 Folders

16 Royalties

17 Market research

18 Demonstration expenses

19 Cost of sales

20 Profit

21

22 ADD: OPENING WIP

TOTAL

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

55

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

56

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

57

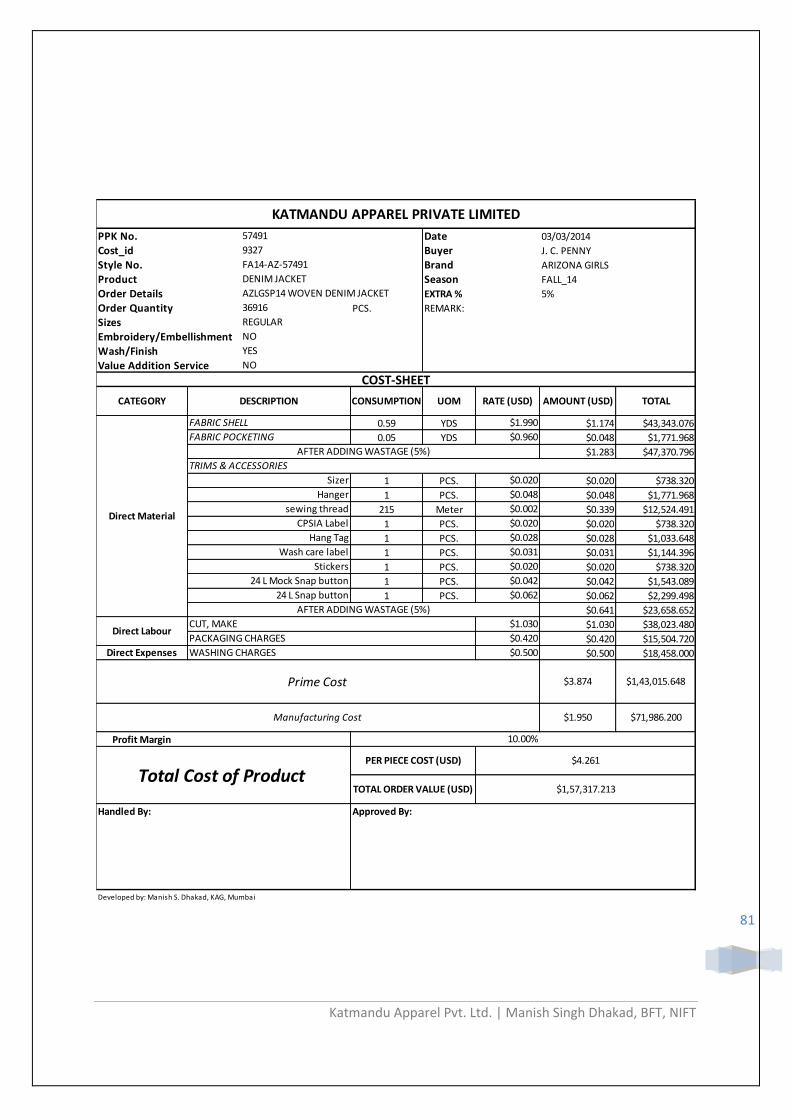

KATMANDU APPAREL GROUP

PPK No.

Date

Cost_id

Buyer

Style No.

Brand

Product

Season

Order Details Remark:

Order Quantity

Sizes

Embroidery/Embellishment

Wash/Finish

Value Addition Service

PRE-PRODUCTION COST-SHEET

DESCRIPTION QUANTITY UOM UNIT PRICE AMOUNT

Direct Material

Direct Labour

Direct Expenses

Prime Cost

Indirect material

Indirect Labour

Indirect Expenses

Manufacturing Cost

Administrative Expenses

Sales & marketing Expenses

Profit Margin

Total Cost of Product

Handled By:

Approved By:

Developed by: Manish S. Dhakad, KAG, Mumbai

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

58

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

59

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

60

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

61

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

62

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

63

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

64

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

65

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

66

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

67

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

68

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

69

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

70

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

71

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

72

Date

Buyer

Brand

Season

Remark:

QUANTITY AMOUNT

Direct Material

Direct Labour

Direct Expenses

Indirect material

Indirect Labour

Indirect Expenses

Profit Margin

Developed by: Manish S. Dhakad, KAG, Mumbai

Value Addition Service

Order Details

Order Quantity

Sizes

Embroidery/Embellishment

Wash/Finish

Total Cost of Product

Manufacturing Cost

Administrative Expenses

COST-SHEET

ADD: WASTAGE

FINISHING & PACKING

KATMANDU APPAREL GROUP

PPK No.

Cost_id

Style No.

Product

FABRIC

PRINT/EMBROIDERY/WASH/DYEING

TRIMS & ACCESSORIES

CUTTING

SEWING

Prime Cost

DESCRIPTION UOM UNIT PRICE

Sales & marketing Expenses

Handled By: Approved By:

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

73

4.2.4 Customization of thread calculator as per the company product

type for effective thread consumption calculation.

Katmandu Apparel Pvt. Ltd. | Manish Singh Dhakad, BFT, NIFT

74

4.2.5 Collect data for costing of samples & costs which are followed by the

company during concept sampling stage including wastages & profit margins

to develop cost sheet for a particular season.

Date 06/03/2014

Buyer J. C. PENNY

Brand ARIZONA BOYS

Season FALL_14

EXTRA % 5%

PCS. REMARK:

0.80 YDS $2.008 $44,192.064

0.23 YDS $0.207 $4,555.656

$2.326 $51,185.106

135 Meter $0.213 $4,688.364

1 PCS. $0.020 $440.160

1 PCS. $0.050 $1,100.400

1 PCS. $0.036 $792.288

1 PCS. $0.025 $550.200

5 PCS. $0.220 $4,841.760

2 PCS. $0.035 $764.118

0.95 YDS $0.054 $1,191.733

1 PCS. $0.051 $1,122.408

1 PCS. $0.262 $5,766.096