AMICUS CURIAE BRIEF OF THE AMERICAN INSURANCE ASSOCIATION, INSURANCE COUNCIL OF TEXAS ... · ·...

48

NO. 03-17-00081-CV IN THE THIRD COURT OF APPEALS PHI AIR MEDICAL, LLC, Appellant, v. TEXAS MUTUAL INSURANCE COMPANY, HARTFORD UNDERWRITERS INSURANCE COMPANY, TASB RISK MANAGEMENT FUND, TRANSPORTATION INSURANCE COMPANY, TRUCK INSURANCE EXCHANGE, TWIN CITY FIRE INSURANCE COMPANY, VALLEY FORGE INSURANCE COMPANY, ET AL., Appellees. AMICUS CURIAE BRIEF OF THE AMERICAN INSURANCE ASSOCIATION, INSURANCE COUNCIL OF TEXAS, AND PROPERTY CASUALTY INSURERS ASSOCIATION OF AMERICA GREENBERG TRAURIG, LLP Dale Wainwright State Bar No. 00000049 [email protected] Justin Bernstein State Bar No. 24105462 [email protected] 300 West 6th Street, Suite 2050 Austin, Texas 78701 Telephone: (512) 320-7200 Facsimile: (512) 320-7210 ACCEPTED 03-17-00081-CV 20573737 THIRD COURT OF APPEALS AUSTIN, TEXAS 11/7/2017 5:48 PM JEFFREY D. KYLE CLERK

Transcript of AMICUS CURIAE BRIEF OF THE AMERICAN INSURANCE ASSOCIATION, INSURANCE COUNCIL OF TEXAS ... · ·...

NO. 03-17-00081-CV

IN THE THIRD COURT OF APPEALS

PHI AIR MEDICAL, LLC,

Appellant,

v.

TEXAS MUTUAL INSURANCE COMPANY, HARTFORD UNDERWRITERS INSURANCE COMPANY, TASB RISK

MANAGEMENT FUND, TRANSPORTATION INSURANCE COMPANY, TRUCK INSURANCE EXCHANGE, TWIN CITY

FIRE INSURANCE COMPANY, VALLEY FORGE INSURANCE COMPANY, ET AL.,

Appellees.

AMICUS CURIAE BRIEF OF THE AMERICAN INSURANCE ASSOCIATION, INSURANCE COUNCIL OF TEXAS, AND PROPERTY CASUALTY INSURERS ASSOCIATION OF

AMERICA

GREENBERG TRAURIG, LLP

Dale Wainwright State Bar No. 00000049 [email protected] Justin Bernstein State Bar No. 24105462 [email protected] 300 West 6th Street, Suite 2050 Austin, Texas 78701 Telephone: (512) 320-7200 Facsimile: (512) 320-7210

ACCEPTED03-17-00081-CV

20573737THIRD COURT OF APPEALS

AUSTIN, TEXAS11/7/2017 5:48 PMJEFFREY D. KYLE

CLERK

-i-

TABLE OF CONTENTS

Page

INDEX OF AUTHORITIES .................................................................................... iii

IDENTITIES OF PARTIES AND COUNSEL ...................................................... vii

STATEMENT OF THE CASE .................................................................................. 1

ISSUES PRESENTED ............................................................................................... 1

STATEMENT OF FACTS ........................................................................................ 1

SUMMARY OF THE ARGUMENT ........................................................................ 1

ARGUMENT ............................................................................................................. 3

I. The Airline Deregulation Act Does Not Apply To Workers’ Compensation Regulation Of Air-Ambulance Fees. ....................................... 3

A. Federal preemption of a historic state police power requires expression of a clear and manifest purpose, which is not present here. ....................................................................................................... 4

B. Workers’ compensation regulation is a police power historically reserved for the states, without unnecessary and disruptive federal involvement. .............................................................................. 5

C. The purpose of the Airline Deregulation Act is to return airline ticket prices to a free-market system, not to preempt tort or insurance law. ........................................................................................ 6

D. Preemption would lead to absurd results that are inconsistent with Congress’s manifest purpose. ....................................................... 9

II. Even If The Airline Deregulation Act Applied To Workers’ Compensation Insurance, It Could Not Preempt Workers’ Compensation Regulation Because The McCarran-Ferguson Act Precludes Such Preemption. .......................................................................... 15

A. The MFA prevents application of generic preemption provisions to the business of insurance. .............................................. 15

-ii-

B. Workers’ compensation balance-billing and reimbursement regulations are “for the purpose of regulating the business of insurance.” ........................................................................................... 17

III. The Proper Reimbursement Rate Is 125% Of The Medicare Rate, Not Six Times The Proper Rate. ........................................................................... 23

A. Rule 134.203(d) sets air-ambulance reimbursement at 125% of the Medicare rate. ................................................................................ 23

B. If Rule 134.203(d) did not apply, 125% of the Medicare rate would more than satisfy the remaining requirements. ........................ 26

1. Achieving effective medical cost control. ................................ 27

2. Employing the methodology and values used by Medicare and Medicaid with minimal modifications when necessary. ........................................................................ 27

3. Applying adjustment factors taking into account economic indicators in health care. ........................................... 28

4. Being fair and reasonable. ......................................................... 28

5. Ensuring the quality of medical care. ....................................... 29

6. Not providing for payment in excess of the fee charged for similar treatment of an injured individual of an equivalent standard of living and paid. ..................................... 30

7. Taking into account the increased security of payment afforded by the TWCA. ............................................................ 31

PRAYER .................................................................................................................. 32

CERTIFICATE OF COMPLIANCE ....................................................................... 33

CERTIFICATE OF SERVICE ................................................................................ 34

APPENDIX ................................................................................................................ 1

-iii-

INDEX OF AUTHORITIES

Page(s)

Cases

Alessi v. Raybestos-Manhattan, Inc., 451 U.S. 504 (1981) .............................................................................................. 6

Altria Group, Inc. v. Good, 555 U.S. 70 (2008) ................................................................................................ 5

Am. Airlines, Inc. v. Wolens, 513 U.S. 219 (1995) ........................................................................................ 9, 10

Aranda v. Ins. Co. of N. Am., 748 S.W.2d 210 (Tex. 1988) .............................................................................. 17

Bryson v. City of DeRidder, 707 F. Supp. 245 (W.D. La. 1987) ....................................................................... 6

CTS Corp. v. Waldburger, 134 S. Ct. 2175 (2014) .......................................................................................... 4

De Canas v. Bica, 424 U.S. 351 (1976) .............................................................................................. 5

Eaglemed LLC v. Cox, No. 16-8064 (10th Cir. August 22, 2017) ........................................................... 20

Encompass Office Sols., Inc. v. Ingenix, Inc., 775 F. Supp. 2d 938 (E.D. Tex. 2011) .......................................................... 11, 12

Fredericksburg Care Co., L.P. v. Perez, 461 S.W.3d 513 (Tex. 2015) .............................................................................. 16

Group Life & Health Ins. Co. v. Royal Drug Co., 440 U.S. 205 (1979) ............................................................................................ 22

HK Partners, Inc. v. Power Computing Corp., 03-98-00124-CV, 1999 WL 332573 (Tex. App.—Austin May 27, 1999, no pet.) ...................................................................................................... 11

Hodges v. Delta Airlines, Inc., 44 F.3d 334 (5th Cir. 1995) .......................................................................... 4, 6, 8

Lawrence v. CDB Servs., Inc., 16 S.W.3d 35 (Tex. App.––Amarillo [7th Dist.] 2000, aff’d) .................. 2, 10, 22

-iv-

Liberty Mut. Ins. Co. v. Adcock, 412 S.W.3d 492 (Tex. 2013) .............................................................................. 13

Liberty Mut. Ins. Co. v. Whitehouse, 868 F. Supp. 425 (D.R.I. 1994) ............................................................................ 5

Medtronic, Inc. v. Lohr, 518 U.S. 470 (1996) .............................................................................................. 4

Mid-Town Surgical Ctr., LLP v. Blue Cross Blue Shield of Texas, Inc., 2012 WL 1252512 (S.D. Tex. Apr. 11, 2012) .................................................... 12

Moore v. Brunswick Bowling & Billiards Corp., 889 S.W.2d 246 (Tex. 1994) ................................................................................ 4

Mullinax v. Radian Guar. Inc., 199 F. Supp. 2d 311 (M.D.N.C. 2002) ............................................................... 16

N.Y. State Conference of Blue Cross & Blue Shield Plans v. Travelers Ins. Co., 514 U.S. 645 (1995) .............................................................................................. 5

Neagle v. Nelson, 685 S.W.2d 11 (Tex. 1985) (Robertson, J., concurring) ...................................... 8

Ojo v. Farmers Group, Inc., 356 S.W.3d 421 (Tex. 2011) .............................................................................. 15

Paradissis v. Royal Indem. Co., 507 S.W.2d 526 (Tex. 1974) .............................................................................. 13

In re Poly-Am., L.P., 262 S.W.3d 337 (Tex. 2008) ........................................................................ 13, 21

Sabo v. Metro. Life Ins. Co., 137 F.3d 185 (3d Cir. 1998) ............................................................................... 16

SeaBright Ins. Co. v. Lopez, 465 S.W.3d 637 (Tex. 2015) .................................................................. 13, 14, 22

Sharp v. House of Lloyd, Inc., 815 S.W.2d 245 (Tex. 1991) ................................................................................ 9

State v. Richards, 301 S.W.2d 597 (Tex. 1957) ................................................................................ 6

Sw. Bell Tel. Co. v. DeLanney, 809 S.W.2d 493 (Tex. 1991) ................................................................................ 8

-v-

Tex. Workers ‘ Comp. Comm’n. v. Garcia, 893 S.W.2d 504 (Tex. 1995) ........................................................................ 14, 21

Texas Med. Ass’n v. Texas Workers Comp. Com’n, 137 S.W.3d 342 (Tex. App.—Austin 2004, no pet.) .......................................... 28

Texas Mut. Ins. Co. v. Ruttiger, 381 S.W.3d 430 (Tex. 2012) .............................................................................. 13

United States Dep’t of the Treasury v. Fabe, 508 U.S. 491 (1993) .......................................................................... 16, 17, 19, 20

United States v. Lopez, 514 U.S. 549 (1995) .............................................................................................. 6

Wisconsin Pub. Intervenor v. Mortier, 501 U.S. 597 (1991) .............................................................................................. 4

Wyeth v. Levine, 555 U.S. 555 (2009) .............................................................................................. 5

Statutes

15 U.S.C.A. § 1011 .................................................................................................. 15

15 U.S.C. § 1012(b) ................................................................................................. 16

49 U.S.C. § 41713(b) ................................................................................................. 7

Tex. Ins. Code § 2052.002 ....................................................................................... 19

Tex. Labor Code § 408.027(a) ................................................................................. 19

Tex. Labor Code § 408.027, Appx. G. .................................................................... 19

Tex. Labor Code § 408.027(c) ................................................................................. 19

Tex. Labor Code § 408.027(f) ................................................................................. 19

Tex. Labor Code § 413.011(a) ............................................................................. 3, 27

Tex. Labor Code § 413.011, Appx. J. .................................................... 19, 25, 26, 28

Tex. Labor Code § 413.011(b) ................................................................................. 28

Tex. Labor Code § 413.011(d) ................................................................................. 26

Other Authorities

28 Tex. Admin Code § 134.1(f), Appx. K, .............................................................. 26

28 Tex. Admin. Code § 134.203 .......................................................................... 2, 23

-vi-

28 Tex. Admin. Code § 134.203, Appx. H. ............................................................. 19

28 Tex. Admin. Code § 134.203(d) ....................................................... 23, 24, 26, 31

28 Tex. Admin. Code § 134.203(d)(1) .............................................................. 24, 25

28 Tex. Admin. Code § 134.203(d)(2) .................................................................... 24

28 Tex. Admin. Code § 134.203(d)(3) .............................................................. 24, 25

28 Tex. Admin. Code § 134.203(d), Appx. H. ........................................................ 23

28 Tex. Admin. Code § 134.203(f) ................................................................ 2, 24, 25

27 Tex. Reg. 12304 .................................................................................................. 30

27 Tex. Reg. 12312 .................................................................................................. 30

27 Tex. Reg. 12332 .................................................................................................. 29

27 Tex. Reg. 12344 .................................................................................................. 29

BALANCE BILLING, Black’s Law Dictionary (10th ed. 2014) ........................... 18

H.R. Rep. No. 95-1211 .............................................................................................. 7

Jenny Deam, Surprise bills in store for many Texas ER patients, HOUSTON CHRONICLE, February 22, 2017, available at http://www.houstonchronicle.com/business/medical/article/Surprise-bills-in-store-for-many-Texas-ER-patients-10952437.php?cmpid=premartcl ........................................................................ 12

NYU Stern School of Business, Margins by Sector (US), available at http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/margin.html ............................................................................................................ 28

Pub. L. No. 95-504, 92 Stat. 1705 ............................................................................. 7

Texas Workers’ Compensation and Employers’ Liability Insurance Policy—Part I, Sec. B, available athttp://www.tdi.texas.gov/wc/regulation/documents/Endform.pdf ............... 10, 22

-vii-

IDENTITIES OF PARTIES AND COUNSEL

Parties Counsel

Texas Mutual Insurance Company, et al.

Mary Barrow Nichols State Bar No. 01831600 Bryan W. Jones State Bar No. 24041208 TEXAS MUTUAL INSURANCE COMPANY

6210 Highway 290 East Austin, Texas 78723 Phone: (512) 224-7322 Facsimile: (512) 224-3214

Matthew Baumgartner State Bar No. 24062605 P. M. Schenkkan State Bar No. 17741500 GRAVES, DOUGHERTY, HEARON &MOODY

401 Congress Avenue, Suite 2200 Austin, Texas 78701 Phone: (512) 480-5603 Facsimile: (512) 480-9913

Attorneys for Texas Mutual Insurance Company

-viii-

James M. Loughlin State Bar No. 00795489 Dan Price State Bar No. 24041725 STONE LOUGHLIN & SWANSON, LLPP.O. Box 30111 Austin, Texas 78755 Phone: (512) 343-1300 Facsimile: (512) 343-1385

Attorney for Hartford Underwriters Insurance Company, TASB Risk Management Fund, Transportation Insurance Company, Truck Insurance Exchange, Twin City Fire Insurance Company, Valley Forge Insurance Company, and Zenith Insurance Company

PHI Air Medical, LLC Craig T. Enoch Amy Saberian Shelby O’Brien ENOCH KEVER PLLC 5918 W. Courtyard Drive, Suite 500 Austin, Texas 78730 Phone: (512) 615-1200 Facsimile: (512) 615-1198

Intervenor Texas Department of Insurance, Division of Workers’ Compensation

Lisa Bennett State Bar No. 24073910 Adrienne Butcher State Bar No. 24050363 OFFICE OF THE ATTORNEY GENERAL

P.O. Box 12548, Capitol Station Austin, Texas 78711-2548 Phone: (512) 463-1410 Facsimile: (512) 320-0167

-1-

STATEMENT OF THE CASE

The American Insurance Association, Insurance Council of Texas, and

Property Casualty Insurers Association of America (Amici Curiae) adopt and

incorporate by reference the Statement of the Case contained in Insurer Appellees’

Brief to the extent relevant to this amicus brief.

ISSUES PRESENTED

1. Does the Airline Deregulation Act preempt the Texas workers’ compensation system as applied to air ambulances?

2. Did the trial court correctly hold that the proper reimbursement rate for air ambulances under the Texas workers’ compensation system is 125% of Medicare’s reimbursement rate for air ambulances?

STATEMENT OF INTEREST

Amici Curiae have no direct financial interest in the outcome of this

litigation. No counsel for a party in this case authored this brief in whole or in part.

No person or entity―other than Amici Curiae, their members, or their

counsel―made monetary contributions specifically for the preparation or

submission of this brief.

The American Insurance Association (AIA), founded in 1866 as the National

Board of Fire Underwriters, is a leading national trade association representing

more than 320 major property and casualty insurance companies. AIA members

collectively underwrite more than $125 billion in direct property and casualty

premiums nationwide, including more than two-thirds of the workers’

-2-

compensation insurance market in this state, and range in size from small

companies to the largest insurers with global operations. These companies

underwrite virtually all lines of property and casualty insurance.

On issues of importance to the insurance industry and marketplace, AIA

advocates sound and progressive public policies on behalf of its members in

legislative and regulatory forums at the federal and state levels and submits amicus

curiae briefs in significant cases before federal and state courts, including this

Court. AIA members have a significant interest in preserving a healthy workers’

compensation insurance marketplace in this state, a cause furthered by the trial

court’s judgment.

ICT is a non-profit trade association representing the interests of over 500

property and casualty member insurers doing business in Texas, including

numerous members that write workers compensation insurance. ICT member

companies write over $819 million in workers compensation premium in Texas

and handle thousands of claims of injured workers under the Texas Workers

Compensation system, including claims made for transportation of injured workers

through an ambulance or air ambulance. Thus, ICT members have the same

interest as Texas Mutual and any other insurer licensed to write workers

compensation insurance in Texas that is subjected to claims from air ambulance

providers.

-3-

Property Casualty Insurers Association of America (PCI) promotes and

protects the viability of a competitive private insurance market for the benefit of

consumers and insurers. PCI is composed of nearly 1,000 member companies,

representing the broadest cross section of insurers of any national trade association.

PCI members write $216 billion in annual premium, 36 percent of the nation’s

property casualty insurance. Member companies write 43 percent of the U.S.

automobile insurance market, 29 percent of the homeowners market, 34 percent of

the commercial property and liability market and 36 percent of the private workers

compensation market. In Texas, PCI members write 32.6 percent of the property

casualty market including 33.7 percent of the personal lines insurance market and

32 percent of the commercial lines insurance market. PCI often files amicus briefs

in state and federal courts in cases that involve issues of interest to insurers and

their policyholders.

-1-

STATEMENT OF FACTS

The Amici Curiae adopt and incorporate by reference the Statement of Facts

in Insurer Appellees’ Brief to the extent relevant to this amicus brief.

SUMMARY OF THE ARGUMENT

PHI expanded and profited during the years it accepted reimbursement for

its air-ambulance services at the rate set by the Texas workers’ compensation

system. Now, PHI pushes for reimbursement at any rate PHI decides to charge for

emergency transport services for injured workers. To justify that, PHI argues that

(1) the workers’ compensation system as applied to air ambulances is preempted

by a federal statute enacted in 1978 to deregulate airline ticket prices, and, in the

alternative, (2) the workers’ compensation rules should be interpreted to set

reimbursement at a malleable “reasonable” rate PHI can press much higher than

the rate specified therein.

PHI argues that the Airline Deregulation Act preempts the reimbursement

rates set by the Texas Workers’ Compensation Act. However, the Airline

Deregulation Act does not preempt the Workers’ Compensation Act’s terms. The

Airline Deregulation Act’s purpose is to ensure that market forces generated by

buyers and sellers determine airline ticket prices. This has nothing to do with the

amount that insurers pay for emergency health care services for employees, which

is determined by insurance policies to which air ambulance companies are not

-2-

parties, by quantum meruit, and by tort law (either tort common law or a statutory

alternative to that common law, such as the workers’ compensation system).

Even if the Airline Deregulation Act applied, it could not preempt the

workers’ compensation system because the McCarran-Ferguson Act (MFA)

prevents a federal statute that does not specifically relate to the business of

insurance from preempting any state regulation enacted for the purpose of

regulating the business of insurance. The workers’ compensation regulations that

PHI seeks to preempt were enacted for the purpose of regulating the business of

insurance by mandating the content of insurance policies and regulating the

tripartite relationship amongst insurance companies, the insured employers, and the

employees who accept the benefits of coverage by workers’ compensation policies.

Lawrence v. CDB Servs., Inc., 16 S.W.3d 35, 41-42 (Tex. App.––Amarillo [7th

Dist.] 2000, aff’d).

PHI further argues that, if the workers’ compensation system is not

preempted, the rate specified in Rule 134.203 of the Texas Administrative Code

should be abandoned in favor of a “fair and reasonable fee” to be determined ad

hoc by courts. That interpretation conflicts with the language of the alternative rule

PHI invokes, Rule 134.203(f), which applies only “[f]or products and services for

which no relative unit or payment has been assigned by Medicare.” Rule

134.203(f) is inapplicable because Medicare does assign payments for air-

-3-

ambulance fees. Moreover, that interpretation violates the statutory requirement

that reimbursement rules be tied to Medicare when possible. Tex. Labor Code §

413.011(a). Even if the “fair and reasonable” standard applied, 125% of the

Medicare rate satisfies that standard because, in accordance with the applicable

statutory criteria, it: (1) achieves effective medical cost control; (2) employs the

methodology and values used by Medicare with minimal modifications when

necessary; (3) applies adjustment factors taking into account economic indicators

in health care; (4) is fair and reasonable; (5) ensures the quality of medical care; (6)

does not provide for payment of a fee in excess of the fee charged and paid for

similar treatment of an injured individual of an equivalent standard of living; and

(7) takes into account the increased security of payment afforded by the workers’

compensation system. Unlike the reasonable rate fixed by the workers’

compensation rules, PHI’s position would require ad hoc adjudication for each

provider after each change in circumstances.

ARGUMENT

I. The Airline Deregulation Act Does Not Apply To Workers’ Compensation Regulation Of Air-Ambulance Fees.

A federal statute only preempts a state’s historic police power, such as

workers’ compensation regulation, when such preemption is the clear and manifest

purpose of the statute. The Airline Deregulation Act’s purpose was to “dismantle

federal regulation” of airline prices by the Civil Aeronautics Board so that

-4-

bureaucratic regulations do not prevent market forces from determining airline

prices. Hodges v. Delta Airlines, Inc., 44 F.3d 334, 335 (5th Cir. 1995). While the

Airline Deregulation Act preempts state regulations that would thwart that purpose,

the Texas workers’ compensation system does not do so.

A. Federal preemption of a historic state police power requires expression of a clear and manifest purpose, which is not present here.

“When considering pre-emption, we start with the assumption that the

historic police powers of the States were not to be superseded by the Federal Act

unless that was the clear and manifest purpose of Congress.” Wisconsin Pub.

Intervenor v. Mortier, 501 U.S. 597, 605 (1991) (internal quotation marks

omitted); see also Moore v. Brunswick Bowling & Billiards Corp., 889 S.W.2d

246, 249 (Tex. 1994) (using this assumption to determine “whether such an

express preemption clause indeed preempts state law”). Therefore, “when the text

of a pre-emption clause is susceptible of more than one plausible reading, courts

ordinarily accept the reading that disfavors preemption.” CTS Corp. v.

Waldburger, 134 S. Ct. 2175, 2188 (2014) (internal quotation marks omitted).

The “purpose of Congress is the ultimate touchstone in every preemption

case,” and that purpose should be informed by the “structure and purpose of the

statute as a whole.” Medtronic, Inc. v. Lohr, 518 U.S. 470, 485-486 (1996)

(internal quotation marks omitted). In order to identify the purpose of Congress, it

-5-

is appropriate to “review the history of federal regulation” that allegedly preempts

state law. Wyeth v. Levine, 555 U.S. 555, 566 (2009).

“If a federal law contains an express pre-emption clause, it does not

immediately end the inquiry because the question of the substance and scope of

Congress’ displacement of state law still remains.” Altria Group, Inc. v. Good, 555

U.S. 70, 76 (2008). To determine the scope of preemption, courts must go beyond

“uncritical literalism . . . and look instead to the objectives of the . . . statute as a

guide to the scope of the state law that Congress understood would survive.” N.Y.

State Conference of Blue Cross & Blue Shield Plans v. Travelers Ins. Co., 514 U.S.

645, 656 (1995) (holding that ERISA’s broad “relate to” preemption language did

not reach the challenged state law because “Congress never envisioned ERISA pre-

emption as blocking state health care cost control”).

B. Workers’ compensation regulation is a police power historically reserved for the states, without unnecessary and disruptive federal involvement.

“States possess broad authority under their police powers to regulate the

employment relationship to protect workers within the State,” including through

“workmen’s compensation laws.” De Canas v. Bica, 424 U.S. 351, 356 (1976)

(superseded by a statute that did expressly preempt state law). “Workers’

compensation laws, which protect the economic well-being of a state’s citizens,

have long been considered valid exercises of a state’s police powers.” Liberty Mut.

-6-

Ins. Co. v. Whitehouse, 868 F. Supp. 425, 433 (D.R.I. 1994) (citing Alessi v.

Raybestos-Manhattan, Inc., 451 U.S. 504, 524 (1981)). Where the workers’

compensation system applies to emergency healthcare services like air ambulance

transportation, it also falls under the police power of the state to “provide for the

real needs of the people in their health.” See State v. Richards, 301 S.W.2d 597,

602 (Tex. 1957); Bryson v. City of DeRidder, 707 F. Supp. 245, 249 (W.D. La.

1987) (“operation of ambulance service is an exercise of a city’s governmental

function necessary to protect its citizens and . . . thus is within the general police

power”).

Moreover, air ambulance transport to the nearest hospital is a distinctly local

activity without a significant impact on interstate commerce. The United States

Supreme Court has warned that Congress’s laws should not be “extended so as to

embrace effects upon interstate commerce so indirect and remote that to embrace

them . . . would effectually obliterate the distinction between what is national and

what is local.” United States v. Lopez, 514 U.S. 549, 557 (1995).

C. The purpose of the Airline Deregulation Act is to return airline ticket prices to a free-market system, not to preempt tort or insurance law.

“Congress enacted the ADA to dismantle federal economic regulation” in

favor of “competitive market forces.” Hodges, 44 F.3d at 335. The economic

regulation it targeted was regulation under the Federal Aviation Act of airline

-7-

ticket prices, a regulatory system the Airline Deregulation Act sought to replace

with “an air transportation system which relies on competitive market forces.” See

Pub. L. No. 95-504, 92 Stat. 1705, Appx. A at 1. To achieve that purpose, the

Airline Deregulation Act preempts regulation that would prevent the market forces

generated by buyers and sellers from determining the “price” of airline services,

e.g., for tickets or cargo services. See 49 U.S.C.A. § 41713(b), Appx. B. Nothing in

the Airline Deregulation Act concerns payments that, even absent regulation,

would not be determined by deals between buyer and seller, such as payments

determined by tort law, quantum meruit, or insurance policies.

The Airline Deregulation Act’s focus on consumers setting prices for airline

services is apparent from the text of the Airline Deregulation Act and its

accompanying House Report. First, the Airline Deregulation Act was designed to

remove a rigid “formula for determining coach and first-class fares.” H.R. Rep.

No. 95-1211 at 9, Appx. C. Second, the Airline Deregulation Act refers to the

“traveling and shipping public.” Pub. L. No. 95-504, 92 Stat. 1705, Appx. A at 2.

Third, the Airline Deregulation Act promotes “a comprehensive and convenient

system of continuous scheduled airline service.” Id. In contrast, neither insurers

nor injured workers being rushed to the hospital negotiate over seating class, price-

shop for “travel” plans, or act as market forces that shape airlines to deliver

“convenient . . . continuous scheduled” service. Rather, insurers of employment-

-8-

related injuries pay amounts pre-determined by the workers’ compensation system.

“[T]he workers’ compensation system [is] . . . a statutory alternative to the

common law of torts.” Neagle v. Nelson, 685 S.W.2d 11, 13 (Tex. 1985)

(Robertson, J., concurring); see Sw. Bell Tel. Co. v. DeLanney, 809 S.W.2d 493,

495 n.2 (Tex. 1991) (distinguishing tort from contract liability). Courts recognize

“neither the ADA nor its legislative history indicates that Congress intended to

displace the application of state tort law.” Hodges, 44 F.3d at 338.

Preempting the workers’ compensation system would not serve the Airline

Deregulation Act’s intent to release market forces to determine ticket price; rather,

it would simply require courts to determine the obligation of insurers through tort

law and the obligation of workers through quantum meruit. Air ambulance services

result from emergency calls, not contracts formed through competitive market

forces. See Appellees’ Brief at 47 (citing Ins. Ex. 46 at 4, 199) (PHI’s expert

testifying that air ambulance service “doesn’t fit the free market”). Not only does

PHI not negotiate prices with insurers, but PHI negotiated no contract with

insurers, PHI Brief at 28, and air ambulance companies do not negotiate for

placement in workers’ compensation health insurance networks. Dr. Luke Expert

Report ¶ 45, Appx. D; Appellees’ Brief at 5 (citing Tr. v.1 at 37). The Airline

Deregulation Act’s deregulatory purpose “presupposes the vitality of contracts,”

and it is not “plausible that Congress meant to channel into federal court the

-9-

business of resolving” payment for airline services. See Am. Airlines, Inc. v.

Wolens, 513 U.S. 219, 230-231 (1995).

Therefore, it is far from clear and manifest that the Airline Deregulation Act

should preempt the Texas workers’ compensation system. In fact, the converse is

true. Congress’s clear indications in the Act’s text and legislative history establish

that Congress intended the Act to revive free market forces in setting airline ticket

prices, without any reference to state systems to provide for injured workers. PHI’s

position would conflict not only with the Airline Deregulation Act’s goals but also

its text, the House Report, and its treatment in case law.

D. Preemption would lead to absurd results that are inconsistent with Congress’s manifest purpose.

“Interpretations of statutes which would produce absurd results are to be

avoided.” Sharp v. House of Lloyd, Inc., 815 S.W.2d 245, 249 (Tex. 1991).

Preemption of reimbursement and balance-billing regulations would remove

insurers’ obligation to pay PHI and absurdly result in 100% of PHI’s fees falling

on injured workers.

1. If the Airline Deregulation Act preempted workers’ compensation regulations, PHI would have no basis to demand payment from workers’ compensation insurers.

Workers’ compensation insurers did not enter into agreements with air-

ambulance companies. PHI Brief at 28. Rather, insurers offered an insurance

policy created by the workers’ compensation system that establishes a “tripartite

-10-

contractual relationship in which the employer, the employee, and the workers’

compensation insurance carrier are parties.” Lawrence, 16 S.W.3d at 41. Insurers’

obligation under the standard policy is to pay “the benefits required of [employers]

by the workers compensation law.” Texas Workers’ Compensation and Employers’

Liability Insurance Policy—Part I, Sec. B, available at

http://www.tdi.texas.gov/wc/regulation/documents/Endform.pdf. (emphasis

added). Therefore, if the Airline Deregulation Act preempted workers’

compensation law, insurers would have no obligation under the policy to pay PHI.

To escape this result, PHI now argues that “the source of PHI’s complaint is the

mandatory reimbursement system” rather than the insurance policy. PHI Brief at

27. However, that leads to the same indefensible result because PHI also argues

“the ADA preempts the TWCA reimbursement system” and “all state laws related

to price.” PHI Brief at 19, 20.

Courts could not fill the void left by preemption by concocting an alternative

reimbursement system, implying a price term, or employing a quantum meruit

theory. First, a state-court concoction would, according to PHI’s own arguments,

be preempted because it would constitute “state-imposed regulation” rather than

“court enforcement of contract terms set by the parties themselves.” Wolens, 513

U.S. at 222 (1995) (emphasis added); see also PHI Brief at 20 (citing Wolens).

Second, courts will not imply a price when the parties have not already agreed on

-11-

enough of the other terms to allow the court to reasonably infer what the parties

intended. HK Partners, Inc. v. Power Computing Corp., 03-98-00124-CV, 1999

WL 332573, at *5 (Tex. App.—Austin May 27, 1999, no pet.). This rule applies

with even more force where, as here, PHI and the insurers have not even agreed to

enter into an agreement. Insurers might decide to pay certain air ambulance

companies nothing (choosing instead to deal with other companies or not cover air

ambulance services), insurers might insist that PHI offer the same price (100% of

the Medicare rate) that PHI agreed to in the one contract it did enter for services in

Texas, or insurers might negotiate the same rate they have been paying for years

(125% of the Medicare rate). Appellees’ Brief at 67 (citing Tr. v.2 at 465). In other

words, there is no reasonable way to infer the price to which the parties may have

agreed, notwithstanding the overriding problems with PHI’s approach that insurers

have not agreed and preempted regulations could not require insurers to pay PHI

anything.

Third, quantum meruit is an equitable remedy, so it would not apply under

PHI’s argument that its claims are “purely statutory.” PHI Brief at 27. Even if PHI

contradicted itself to argue for quantum meruit, that argument would fail as a basis

for seeking payment from insurers because a quantum meruit claim requires the

plaintiff to “show that the efforts were undertaken for the person to be charged and

not just that the efforts benefited that person.” Encompass Office Sols., Inc. v.

-12-

Ingenix, Inc., 775 F. Supp. 2d 938, 966 (E.D. Tex. 2011). For example, the court in

Encompass dismissed a quantum meruit claim because the plaintiff’s healthcare

services were rendered to insureds rather than insurers. Id.; see also Mid-Town

Surgical Ctr., LLP v. Blue Cross Blue Shield of Texas, Inc., 2012 WL 1252512, at

*3 (S.D. Tex. Apr. 11, 2012) (dismissing a quantum meruit claim because “A must

have provided services to and for the benefit of B . . . [and] defendant is neither A

or B in the equation above—defendant is the third party insurer/administrator of

patients who received medical treatment”). Accordingly, PHI cannot use quantum

meruit to recover from insurers the alleged value of what it provided to insureds.

2. The consequences of preemption would be absurd.

Preemption would leave PHI without any basis in contract, statute, or

common law to recover from insurers, and without any bar on balance-billing

workers or express limitation on the amounts workers are charged. One-hundred

percent of PHI’s fees would then fall on injured workers, subjecting them to

surprises such as an unexpected $29,000 bill arriving when they should be focusing

on recovery rather than bankruptcy. See, e.g., Jenny Deam, Surprise bills in store

for many Texas ER patients, HOUSTON CHRONICLE, February 22, 2017, available at

http://www.houstonchronicle.com/business/medical/article/Surprise-bills-in-store-

for-many-Texas-ER-patients-10952437.php?cmpid=premartcl. This would lead not

-13-

only to personal hardships but to instability and degradation of the entire workers’

compensation system.

“In creating the Texas Workers’ Compensation Act, the Legislature

carefully balanced competing interests—of employees subject to the risk of injury,

employers, and insurance carriers—in an attempt to design a viable compensation

system, all within constitutional limitations.” In re Poly-Am., L.P., 262 S.W.3d

337, 352 (Tex. 2008). “The Act ultimately struck a bargain that allows employees

to receive a lower, but more certain, recovery than would have been possible under

the common law.” SeaBright Ins. Co. v. Lopez, 465 S.W.3d 637, 642 (Tex. 2015)

(internal quotation mark omitted). The Supreme Court of Texas has scrupulously

guarded this carefully balanced bargain, refusing to let legal theories outside the

TWCA “distort[] the balances struck in the Act.” See, e.g., Texas Mut. Ins. Co. v.

Ruttiger, 381 S.W.3d 430, 450–51 (Tex. 2012); Liberty Mut. Ins. Co. v. Adcock,

412 S.W.3d 492, 493 (Tex. 2013) (“the Act is a comprehensive statutory scheme,

and therefore precludes the application of claims and procedures not contained

within the Act”).

Employers, employees, and insurers all have the right to choose whether to

participate in the workers’ compensation system. Paradissis v. Royal Indem. Co.,

507 S.W.2d 526, 529 (Tex. 1974). Employees voluntarily participate to receive

more certain recovery, and employers and insurers voluntarily participate to avoid

-14-

higher, more variable tort judgments and the associated legal fees. See SeaBright,

465 S.W.3d at 642. PHI’s approach undermines the benefits supporting that

bargain. First, PHI argues that the protection against balance-billing workers is

preempted, PHI Brief at 20, which would remove employees’ certainty that they

will be compensated for the costs associated with their injury. Second, PHI argues

that it should be paid whatever it charges, and raised its charges 13 times in the

2010-2013 time period. Appellee’s Brief at 6 (citing PHI Ex. 12 at 20). Employers

and insurers would be deprived of the benefit of their bargain if subjected to fees

that rapidly change, exceed the maximums set by the workers’ compensation

system, and may need to be litigated through the tort system.

In addition, PHI’s theory could potentially spawn efforts by other medical

service providers to evade the reasonable rate limitations imposed by the workers’

compensation system. If PHI were able to trump the system’s fundamental

compensation tenets to recover nearly 600% of the regulated payments, other

providers would have a tremendous incentive to follow suit, with untenable results

for injured workers and employers alike.

Moreover, this unbalancing would run afoul of the Texas Constitution. The

“quid pro quo, which produces a more limited but more certain recovery, renders

the Act an adequate substitute for purposes of the open courts guarantee” of the

Texas Constitution. Tex. Workers’ Comp. Comm’n. v. Garcia, 893 S.W.2d 504,

-15-

521 (Tex. 1995). The open courts guarantee requires the careful calibration

inherent in the workers’ compensation system, not a hodgepodge and self-

interested preemption theory designed to justify fees that dramatically exceed

anything contemplated by the workers’ compensation system.

Even if some balance could be restored by state courts engrafting concocted

rates over piecemeal preemption, which as explained above would itself be

preempted state law under PHI’s logic, that engrafting would be unworkably

burdensome. Every time circumstances changed (for example, every time there

was a change in medical technology, the price of fuel, or competition in the

market), courts would have to recalculate the appropriate rate.

The absurd results that would flow from adopting PHI’s theory cannot be

Congress’s clear and manifest purpose for the airline deregulation statute.

II. Even If The Airline Deregulation Act Applied To Workers’ Compensation Insurance, It Could Not Preempt Workers’ Compensation Regulation Because The McCarran-Ferguson Act Precludes Such Preemption.

A. The MFA prevents application of generic preemption provisions to the business of insurance.

Based on its determination that state regulation of insurance is in the public

interest, 15 U.S.C.A. § 1011, Appx. E, the “declared policy of the MFA is to

ensure that state legislatures are able to regulate the business of insurance without

unintended federal interference.” Ojo v. Farmers Group, Inc., 356 S.W.3d 421,

-16-

430 (Tex. 2011); see also Sabo v. Metro. Life Ins. Co., 137 F.3d 185, 189 (3d Cir.

1998) (“The statute then takes the further step of proscribing unintended federal

interference [with] state insurance laws”); Mullinax v. Radian Guar. Inc., 199 F.

Supp. 2d 311, 317 (M.D.N.C. 2002) (“The Act was designed to protect against

unintended federal intrusion in the insurance industry.”). To prevent unintended

preemption by generic preemption provisions, the MFA provides:

No Act of Congress shall be construed to invalidate, impair, or supersede any law enacted by any State for the purpose of regulating the business of insurance …, unless such Act specifically relates to the business of insurance

15 U.S.C. § 1012(b), Appx. F (emphasis added). Congress mandated this rule of

construction knowing that, when its attention is focused on areas outside of

insurance, it cannot anticipate every creative application of its words to insurance

(such as application of an airline-deregulation statute to workers’ compensation

insurance). Even PHI “acknowledges that the ADA does not specifically relate to

the business of insurance.” PHI Brief at 31.

“[T]he test to determine whether laws are enacted for the purpose of

regulating the business of insurance is broad.” Fredericksburg Care Co., L.P. v.

Perez, 461 S.W.3d 513, 525 (Tex. 2015); United States Dep’t of the Treasury v.

Fabe, 508 U.S. 491, 501-505 (1993) (describing the “broad category of laws

enacted ‘for the purpose of regulating the business of insurance’”). One indicator

-17-

of the breadth of the term “business of insurance” is that it encompasses not only

laws that directly address insurance, but also those that “indirectly” manage the

business of insurance so long as such indirect effects were intentional. Fabe, 508

U.S. at 501-505. Another aspect of the breadth of this test is that it encompasses a

wide variety of regulation, including regulation of the relationship between

insurers and parties to the insurance contract, “the terms of an insurance contract,”

and the “performance of an insurance contract.” Id. at 501-503; Aranda v. Ins. Co.

of N. Am., 748 S.W.2d 210, 212 (Tex. 1988) (“The employee is thus a party to the

contract”) (overruled as to extra-contractual causes of action).

B. Workers’ compensation balance-billing and reimbursement regulations are “for the purpose of regulating the business of insurance.”

The Airline Deregulation Act cannot preempt regulations enacted for the

purpose of regulating the business of insurance. PHI argues that the Airline

Deregulation Act preempts state regulations regarding balance billing injured

employees that accept the benefits of workers’ compensation insurance and paying

for services on their behalf, but these regulations squarely aim at regulating the

business of insurance. Therefore, the McCarran-Ferguson Act prevents the Airline

Deregulation Act from preempting Texas’s balance billing and payment

regulations.

-18-

1. Balance billing.

PHI argues that the Airline Deregulation Act preempts state “balance-billing

prohibitions.” PHI Brief at 20. Balance billing is defined as a “healthcare

provider’s practice of requiring a patient or other responsible party to pay any

charges remaining after insurance.” BALANCE BILLING, Black’s Law

Dictionary (10th ed. 2014) (emphasis added). The concept of balance billing is

meaningful only in the context of the insurance business, and air ambulance

companies have used the threat of balance billing injured workers to coerce

payment from insurers. Appellees’ Brief at 48 (citing Tr. v.1 at 33). The

prohibition against balance billing is also a necessary part of the “grand bargain” of

workers’ compensation, wherein injured workers give up the right to sue their

employers (the insureds) in exchange for swift and certain indemnity compensation

and medical treatment, underwritten by insurers. Therefore, balance-billing

regulation affects “the performance of an insurance contract” and the relationship

between workers’ compensation insurers and injured employees that enter into the

tripartite contractual relationship to receive the benefits of the workers’

compensation insurance.

2. Workers’ compensation insurance reimbursement system.

PHI argues that the Airline Deregulation Act preempts “the TWCA

reimbursement system.” PHI Brief at 20. Yet, the TWCA reimbursement system is

-19-

integral to, and directly regulates, the business of insurance. The reimbursement

system is, essentially, an integrated system employing a balance-billing prohibition

in coordination with the following four parts. First, the TWCA provides that a

“healthcare provider shall submit a claim for payment to the insurance carrier” and

that “any payment made by an insurance carrier under this section shall be in

accordance with the fee guidelines authorized under” Section 413.011. Tex. Labor

Code §§ 408.027(a), (f), Appx. G. This regulates the performance of an insurance

contract, and there “can be no doubt that the actual performance of an insurance

contract falls within the ‘business of insurance.’” Fabe, 508 U.S. at 503. Second,

Section 413.011 authorizes the Commissioner of Workers’ Compensation to

“adopt health care reimbursement policies” that do not violate the “Insurance

Code.” Tex. Labor Code §§ 413.011(a), (c), Appx. J. Third, the Commissioner

promulgated guidelines that tie the maximum allowable reimbursement from

insurance companies to certain benchmarks, such as Medicare fee schedules. See

28 Tex. Admin. Code § 134.203(d), Appx. H. Fourth, the Commissioner

prescribes “a uniform policy for workers’ compensation insurance” provided by

private insurance companies. Tex. Ins. Code § 2052.002, Appx. I. This uniform

policy obligates insurers to pay “the benefits required . . . by the workers

compensation law.” Texas Workers’ Compensation and Employers’ Liability Insurance

Policy—Part I, Sec. B, available at http://www.tdi.texas.gov/wc/regulation/documents/Endform.pdf.

-20-

Texas’s authorization of private companies to write workers’ compensation

insurance distinguishes cases about its workers’ compensation system from cases

in states in which the government has supplanted the private marketplace. For

example, in Eaglemed LLC v. Cox, No. 16-8064 (10th Cir. August 22, 2017) the

court explained that Wyoming is not one of the “states [that] have structured their

workers’ compensation programs to operate through private insurance companies.”

Id. at 21. Unlike in Texas, in Wyoming even if one assumes the compensation

system can have the effect of insurance, there is no business of insurance to

regulate because the state government collects, manages, and pays out workers’

compensation funds. Eaglemed is further distinguished because that court based its

decision in part on finding that “[n]either Amicus nor Defendants . . . presented a

single textual reason to support the argument that” the Airline Deregulation Act

did not apply to air ambulances, whereas Amici and Insurers in this case plainly

present multiple, fundamental textual reasons to rebut the unintended degradation

of the workers’ compensation system. Supra at Section I.C.

All of these components regulate “the terms of an insurance contract,” the

performance of an insurance contract, or the relationship between insurers and

insureds (for example because they determine insurers’ obligations to pay for

services for their insureds). Fabe, 508 U.S. at 502.

-21-

3. Integrated system.

Each of the challenged regulations serves the purpose of regulating the

business of insurance. However, even if one assumes that some of the balance

billing and reimbursement regulations, when viewed in isolation, were not clearly

intended to regulate the business of insurance, they would need to be analyzed for

their function within the larger integrated system for regulating insurance.

The workers’ compensation system “carefully balanced competing interests”

so that each component works in conjunction with, and provides the “quid pro

quo” for, the other components. See In re Poly-Am., L.P., 262 S.W.3d at 352; Tex.

Workers’ Comp. Comm’n. v. Garcia, 893 S.W.2d 504, 521 (Tex. 1995). Therefore,

the correct question is not whether a particular regulation viewed in isolation

regulates the business of insurance, but rather whether a regulation was included in

the workers’ compensation system to further the purpose of regulating the business

of insurance.

The proper question thus rebuts PHI’s arguments that the balance billing and

reimbursement regulations do not serve the purpose of spreading risk or form “an

integral part of the policy relationship between the insurer and the insured.” PHI

Brief at 31-34. The balance-billing prohibition furthers the purpose of the workers’

compensation system by shielding injured workers from the risk of unexpected

bills, as part of the bargain through which insured employers furnish indemnity

-22-

benefits and medical treatment outside of the court’s tort system. See SeaBright

Ins. Co., 465 S.W.3d at 642 (explaining that the TWCA struck a bargain in which

employees receive “more certain recovery” and employers are spared “uncertain,

possibly high damage awards under the common law”). This prohibition furthers

the purpose of the workers’ compensation system by transferring the risk of

unexpected bills and tort claims from workers and employers to insurers. The

reimbursement regulations are an integral part of the workers’ compensation

system. They form the backbone of a “framework for a tripartite contractual

relationship in which the employer, the employee, and the workers’ compensation

insurance carriers are parties.” Lawrence, 16 S.W.3d at 41.

PHI’s citation to Royal Drug Co. is inapposite. PHI Brief at 34 (citing

Group Life & Health Ins. Co. v. Royal Drug Co., 440 U.S. 205, 214 (1979)). Royal

Drug considered whether the MFA precludes antitrust regulation of an insurance

company’s contracts with pharmacies for reduced prices. The court held that it

does not, stating that the pharmacy contracts are not the business of insurance

because they “are separate contractual arrangements” and do not spread risk. Id.

216, 213-214. As explained above, the regulations that PHI challenges spread risk.

They also regulate agreements between parties to an insurance agreement because

the regulations determine the content of the workers’ compensation policies and

are directly incorporated into those policies. See Texas Workers’ Compensation

-23-

and Employers’ Liability Insurance Policy—Part I, Sec. B, available at

http://www.tdi.texas.gov/wc/regulation/documents/Endform.pdf.

4. Conclusion.

The McCarran-Ferguson Act prevents the Airline Deregulation Act from

preempting state regulations enacted for the purpose of regulating the business of

insurance. The regulations PHI challenges govern the business of insurance by

allocating risk among insurers, employers, and the workers covered by the

insurance policies, as contemplated by the grand bargain justifying the workers’

compensation system. The regulations necessarily regulate the business of

insurance because they address the terms of insurance contracts and the

performance of insurance policies.

III. The Proper Reimbursement Rate Is 125% Of The Medicare Rate, Not Six Times The Proper Rate.

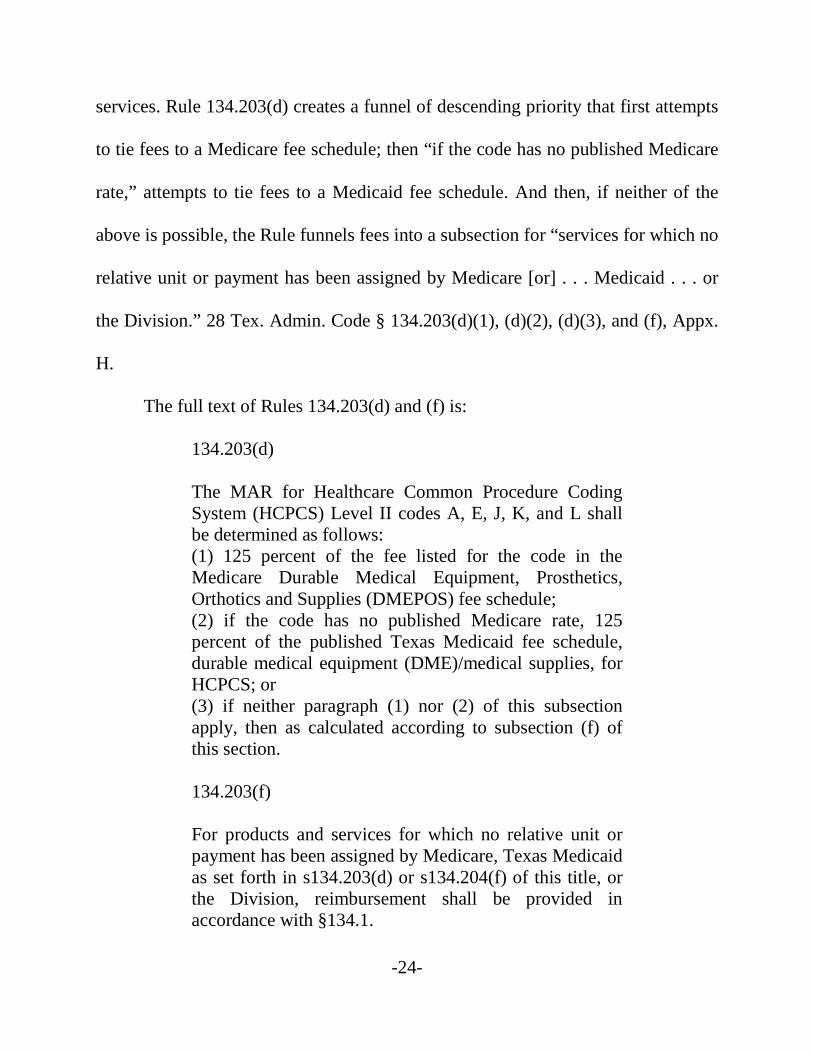

A. Rule 134.203(d) sets air-ambulance reimbursement at 125% of the Medicare rate.

Insurers paid 125% of the Medicare rate when they received PHI’s claims.

They did so because everyone in the system—insurers, providers, and the

Division—had for years applied Rule 134.203. Rule 134.203(d) sets the maximum

allowable reimbursement (the “MAR”) for Healthcare Common Procedure Coding

System (“HCPCS”) Level II codes A, E, J, K, and L services. 28 Tex. Admin.

Code § 134.203(d), Appx. H. Air-ambulance services are HCPCS Level II code A

-24-

services. Rule 134.203(d) creates a funnel of descending priority that first attempts

to tie fees to a Medicare fee schedule; then “if the code has no published Medicare

rate,” attempts to tie fees to a Medicaid fee schedule. And then, if neither of the

above is possible, the Rule funnels fees into a subsection for “services for which no

relative unit or payment has been assigned by Medicare [or] . . . Medicaid . . . or

the Division.” 28 Tex. Admin. Code § 134.203(d)(1), (d)(2), (d)(3), and (f), Appx.

H.

The full text of Rules 134.203(d) and (f) is:

134.203(d)

The MAR for Healthcare Common Procedure Coding System (HCPCS) Level II codes A, E, J, K, and L shall be determined as follows: (1) 125 percent of the fee listed for the code in the Medicare Durable Medical Equipment, Prosthetics, Orthotics and Supplies (DMEPOS) fee schedule; (2) if the code has no published Medicare rate, 125 percent of the published Texas Medicaid fee schedule, durable medical equipment (DME)/medical supplies, for HCPCS; or (3) if neither paragraph (1) nor (2) of this subsection apply, then as calculated according to subsection (f) of this section.

134.203(f)

For products and services for which no relative unit or payment has been assigned by Medicare, Texas Medicaid as set forth in s134.203(d) or s134.204(f) of this title, or the Division, reimbursement shall be provided in accordance with §134.1.

-25-

This funnel of descending priorities is based on the Labor Code’s

requirement that reimbursement rules start with Medicare and Medicaid and only

apply “minimal modifications to those reimbursement methodologies as

necessary.” Tex. Labor Code § 413.011(a), Appx. J. However, a drafting error

unsettles the priority order and would leave air-ambulance fees in limbo if

misinterpreted.

The drafting error is that Rule 134.203(d)(1) refers to a specific Medicare

fee schedule under the assumption that it covers all of the Level II codes addressed,

when in fact air-ambulance fees are listed on a separate Medicare fee schedule. See

Ambulance Fee Schedule Public Use Files, available at

https://www.cms.gov/Medicare/Medicare-Fee-for-Service-

Payment/AmbulanceFeeSchedule/afspuf.html (last visited November 7, 2017). If

subsection (d)(1) did not encompass all relevant Medicare schedules, that would

cause a malfunction in the next step, (d)(2), which is only supposed to apply “if the

code has no published Medicare rate.” Such an interpretation would also mean that

no rules set air ambulance fees. See PHI Brief at 50 (PHI “found no reference to air

ambulance services anywhere else in the Division’s fee guidelines”). PHI argues

that Rule 134.203(d)(3) applies and therefore subjects air ambulance fees to

subsection 134.203(f). PHI Brief at 49. However, that is not possible because

subsection (f) is “[f]or products and services for which no relative unit or payments

-26-

has been assigned by Medicare,” and, as explained above, air-ambulance fees do

have payments assigned by Medicare. These rules could not have been designed to

leave air ambulance fees in limbo when there is a Medicare fee they could be tied

to, not only because of the chaos that would cause, but also because of the Labor

Code’s directive to link fees to Medicare whenever possible.

B. If Rule 134.203(d) did not apply, 125% of the Medicare rate would more than satisfy the remaining requirements.

But even if Rule 134.203(d) did not apply to air-ambulance reimbursement,

such reimbursement would be governed by the overarching factors for all

reimbursement policies. Those factors are set out in Rule 134.1(f), Appx. K, which

requires fair and reasonable reimbursement consistent with the criteria of Section

413.011 of the Texas Labor Code, Appx. J. Section 413.011 provides that

reimbursement should: (1) achieve effective medical cost control (subsection d);

(2) employ the methodology and values used by Medicare and Medicaid with

minimal modifications when necessary (subsection a); (3) apply adjustment factors

taking into account economic indicators in health care (subsection b); (4) be fair

and reasonable (subsection d); (5) ensure the quality of medical care (subsection

d); (6) not provide for payment of a fee in excess of the fee charged for similar

treatment of an injured individual of an equivalent standard of living and paid

(subsection d) (emphasis added); and (7) take into account the increased security of

payment afforded by the TWCA (subsection d).

-27-

Both the Administrative Law Judge (“ALJ”) and PHI strayed from these

criteria, whereas Appellees presented competent and uncontroverted evidence that

125% of the Medicare fee meets each criterion. See, e.g., Dr. Luke Expert Report.

The trial court properly reversed the ALJ’s ruling.

1. Achieving effective medical cost control.

PHI argues that its fees should be set at their “full billed charges.” PHI Brief

at 60. Allowing air ambulances to set their own reimbursement rates (something no

other medical-service providers are entitled to do) is not “effective medical cost

control;” it is a blank check. Similarly, the methodology the ALJ used—setting

PHI’s reimbursement rate at the average rate for all of its transports in the

preceding years—will reward PHI for relentlessly ratcheting up its rates and

number of helicopters. Decision and Order at 25.

2. Employing the methodology and values used by Medicare and Medicaid with minimal modifications when necessary.

Section 413.011(a) mandates the use of Medicare and Medicare

methodology and values to determine reimbursement. PHI ignores this criterion.

The ALJ only gave it cursory attention by first deciding the appropriate fee was the

average historical fee and then describing that historical fee using the percentage of

the Medicare fee that it happened to constitute (149% in this case). Decision and

Order at 25. But the fee determination must “begin” with the Medicare fee and

-28-

rationally, if necessary, “adjust that formula.” Texas Med. Ass’n v. Texas Workers

Comp. Com’n, 137 S.W.3d 342, 348 (Tex. App.—Austin 2004, no pet.)

In contrast, Appellees’ expert report properly started with the Medicare fee

and applied adjustment factors when necessary. Dr. Luke Expert Report ¶¶ 39-44

(describing “payment adjustment factors” that Dr. Luke used to adjust the

Medicare rates).

3. Applying adjustment factors taking into account economic indicators in health care.

Section 413.011 mandates use of “payment adjustment factors taking into

account economic indicators in health care.” Tex. Labor Code § 413.011(b). PHI

omits any mention of this indicator. Appellees’ expert created adjustment factors

outside of Medicare and Medicaid guidance based on key economic indicators in

health care, such as inflation in provider costs and new technology employed by air

ambulances. Appellees’ Brief at 65 (citing Tr. v.1 at 174-186); CR:579 (citing Ins.

Ex. 50 at Figure 8 and pp. 11-14).

4. Being fair and reasonable.

PHI achieved an average profit margin of 9.15% from 2010 to 2013, while

accepting the same rate from insurers that it now claims is unreasonable.

Appellees’ Brief at 6 (citing Tr. v.2 at 284, 330). For comparison, the average

profit margin in the general insurance industry is approximately 4.3%. See NYU

Stern School of Business, Margins by Sector (US), available at

-29-

http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/margin.html. In

addition, PHI negotiated a 100%-of-Medicare rate in the one service contract it

entered in Texas. Appellees’ Brief at 67 (citing Tr. v.2 at 465). These facts

demonstrate that the status quo rate is reasonable.

5. Ensuring the quality of medical care.

During years that air-ambulance companies accepted 125% of the Medicare

fee for workers’ compensation patients and received less than that for the majority

of its patients, the number of air ambulances in Texas increased substantially, from

61 to 86. Appellees’ Brief at 4 (citing Ins. Ex. 189 at 27 and Ins. Ex. 120 at 11).

PHI was part of that increase. Appellees’ Brief at 66 (citing Ins. Ex. 29, Tr. v.1 at

232, and CR:83). Therefore, there is no need to speculate about whether 125% of

the Medicare fee is sufficient to ensure access to health care; the air ambulance

companies have shown by their expansion that it is. This fact is supported by

Appellees’ economic analysis, which showed that 125% of the Medicare fee more

than covers all of PHI’s variable costs for an additional flight, and therefore the

rational air-ambulance company would continue providing service to workers at

the 125% rate. Appellees’ Brief at 66 (citing 27 Tex. Reg. 12,332,344 and Tr. v.1

at 217-218).

-30-

6. Not providing for payment in excess of the fee charged for similar treatment of an injured individual of an equivalent standard of living and paid.

The “Commission has recognized that Medicare recipients have a similar

standard of living as the general working population, and therefore injured

employees. Medicare is an appropriate point of reference for workers’

compensation fees.” 27 Tex. Reg. 12304, 12312, Appx. L. Twenty-nine percent of

payments to PHI are from Medicare. PHI Brief at 57. PHI’s average charges from

2010 to 2013 ranged from 360% to 590% of the Medicare rate. Appellees’ Brief at

74 (citing Ins. Ex. 155 at 1). Therefore, in demanding reimbursement for charges

that are many times higher than Medicare payments, PHI demands payment well in

excess of the fee for equivalent populations. Moreover, by focusing on the amount

it charges, PHI ignores this criterion’s requirement that the fees used as

equivalents be not only charged but “paid.” This significantly inflates PHI’s claims

within the workers’ compensation system because “PHI, like other air ambulance

providers, incurs exceptionally high levels of ‘bad debt.’” PHI Brief at 3. PHI’s

position is counter to this criterion by permitting air ambulance companies to

charge more in the workers’ compensation system to make up for lower Medicare

payments and charges it fails to collect from others. PHI Brief at 59.

-31-

In contrast, Appellees’ methodology, which determined that appropriate fees

are 125% or less of Medicare fees, provides for similar payment for equivalent

populations.

7. Taking into account the increased security of payment afforded by the TWCA.

Compensation from the workers’ compensation system is more certain than

compensation for the majority of PHI’s patients, yet rather than accept the

workers’ compensation rate, which takes into account this increased security, PHI

demands more profit from the workers’ compensation system. “125% of Medicare

is actually equal to or higher than the amount paid by or on behalf of 72% of PHI’s

patients.” CR:83. However, these other patients present a risk of non-payment. PHI

contends that its patients without insurance comprise 17% of its patients and paid

$0 from 2010-2013. PHI Brief at 57. Medicare requires patients to cover a

substantial copay, which they cannot always afford. On the other hand, when air-

ambulance companies transport workers covered by workers’ compensation

insurance, those companies are guaranteed payment. This increased security of

payment weighs against insurers paying substantially more than Medicare.

All of these factors support reimbursement at 125% or less of the Medicare

rate. PHI lists these statutory factors but quickly abandons them in favor of the

subjective factors it considers when deciding how much to charge. As the

foregoing analysis of the statutory factors confirms, Rule 134.203(d) has

-32-

appropriately established a rate for air ambulance services—125% of the Medicare

rate.

PRAYER

For these reasons, Amici Curiae respectfully request that the Court affirm

the trial court’s grant of summary judgment in favor of Appellees.

Respectfully submitted,

GREENBERG TRAURIG, LLP

By: /s/ Dale Wainwright Dale Wainwright State Bar No. 00000049 [email protected] Justin Bernstein State Bar No. 24105462 [email protected] 300 West 6th Street, Suite 2050Austin, TX 78701 Telephone: (512) 320-7200 Facsimile: (512) 320-7210

Counsel for Amicus Curiae American Insurance Association, Insurance Council of Texas, and Property Casualty Insurers Association of America

-33-

CERTIFICATE OF COMPLIANCE

This brief complies with the length limitations of TEX. R. APP. P. 9.4(i)(3)

because this brief consists of 7,067 words, excluding the parts of the brief

exempted by TEX. R. APP. P. 9.4(i)(1).

/s/ Dale Wainwright Dale Wainwright

-34-

CERTIFICATE OF SERVICE

I hereby certify that a true and correct copy of the foregoing was

electronically filed with the Court and that counsel of record, who are deemed to

have consented to electronic service, are being served on this 7th day of November

2017 via the court’s CM/ECF System.

Mary Barrow Nichols State Bar No. 01831600 [email protected] Bryan W. Jones State Bar No. 24041208 [email protected] TEXAS MUTUAL INSURANCE COMPANY

6210 Highway 290 East Austin, Texas 78723-1098 Phone: (512) 224-7322 Facsimile: (512) 224-3214

Matthew Baumgartner State Bar No. 24062605 [email protected] P. M. Schenkkan State Bar No. 17741500 [email protected] GRAVES, DOUGHERTY, HEARON &MOODY

401 Congress Avenue, Suite 2200 Austin, Texas 78701 Phone: (512) 480-5603 Facsimile: (512) 480-9913

Counsel for Appellee Texas Mutual Insurance Company

Craig T. Enoch State Bar No. 00000026 [email protected] Amy Saberian State Bar No. 24041842 [email protected] Shelby O’Brien State Bar No. 24037203 [email protected] ENOCH KEVER PLLC

5918 W. Courtyard Drive, Suite 500 Austin, Texas 78730 Phone: (512) 615-1200 Facsimile: (512) 615-1198

Counsel for Appellant PHI Air Medical, LLC

-35-

James M. Loughlin State Bar No. 17741500 [email protected] STONE LOUGHLIN & SWANSON, LLP P.O. Box 30111 Austin, Texas 78755 Phone: (512) 343-1300 Facsimile: (512) 343-1385

Counsel for Hartford Underwriters Insurance Company, TASB Risk Management Fund, Transportation Insurance Company, Truck Insurance Exchange, Twin City Fire Insurance Company, Valley Forge Insurance Company, and Zenith Insurance Company

Adrienne Butcher State Bar No. 24050363 [email protected] OF THE ATTORNEY GENERAL OF

TEXAS

P.O. Box 12548, Capitol Station Austin, Texas 78711 Phone: (512) 463-1410 Facsimile: (512) 320-0167

Counsel for Intervenor Texas Department of Insurance, Division of Workers’ Compensation

/s/ Dale Wainwright Dale Wainwright

-1-

APPENDIX

Tab A PL 95–504, 92 Stat 1705

Tab B 49 U.S.C.A § 41713, Preemption of authority over prices, routes, and service

Tab C H.R. REP. 95-1211 (1978)

Tab D Dr. Luke Expert Report, Insurers’ Exhibit 46

Tab E 15 U.S.C.A § 1011, Declaration of policy

Tab F 15 U.S.C.A. § 1012, Regulation by State law

Tab G Tex. Labor Code § 408.027, Payment of Health Care Provider

Tab H 28 Tex. Admin. Code § 134.203, Medical Fee Guideline for Professional Services

Tab I Tex. Ins. Code § 2052.002, Standard Policy Forms and Uniform Policy; Exceptions

Tab J Tex. Labor Code § 413.011. Reimbursement Policies and Guidelines

Tab K 28 Tex. Admin. Code § 134.1, Medical Reimbursement

Tab L 28 Tex. Admin. Code § 134.202, Medical Fee Guidelines