AMAZON’S IMPACT ON AUSTRALIAN RETAILERScdn.vested.com.au/research/Amazon-Thematic.pdf · their...

16

CONTACT Address Vested Equities Level 11, 50 Cavill Ave Surfers Paradise QLD 4217 Phone & Fax Toll Free: 1300 980 849 Phone: + 61 7 5655 5333 Fax: + 61 7 5655 5341 Online Email: [email protected] Website: www.vested.com.au Vested Equities Research 20 APRIL 2017 THEMATIC INVESTING AMAZON’S IMPACT ON AUSTRALIAN RETAILERS

Transcript of AMAZON’S IMPACT ON AUSTRALIAN RETAILERScdn.vested.com.au/research/Amazon-Thematic.pdf · their...

CONTACT

Address

Vested EquitiesLevel 11, 50 Cavill AveSurfers ParadiseQLD 4217

Phone & Fax

Toll Free: 1300 980 849Phone: + 61 7 5655 5333 Fax: + 61 7 5655 5341

Online

Email: [email protected]

Website: www.vested.com.au

Vested EquitiesResearch

20 APRIL 2017

THEMATIC INVESTING

AMAZON’S IMPACT ON AUSTRALIAN RETAILERS

www.vested.com.au

2 Vested Research

We have fielded numerous questions about the

impact of Amazon’s imminent entry into the

Australian retail market. Given most Australian

investors will have some exposure to Australian

retailers in their portfolios (Wesfarmers,

Woolworths, Harvey Norman, JB Hi-Fi etc), we

deem it important to address the issue. In this

note we address Amazon’s impact on Australian

retailers and how investors could potentially

position their portfolios. The Amazon threat is

very real and, given the US experience (significant

job losses / earmarked store closures), we believe

some retailers are better placed than others. In

any case, we do expect redistribution of revenue

and margin pressure among the incumbents as

Amazon builds up scale, but there are also

mitigating factors which the incumbents can

utilise to buffer their businesses. Post this review,

we have maintained our key picks in the sector.

Who is Amazon? Amazon (or Amazon.com) is a US based

e-commerce company founded in 1994 by current CEO

Jeff Bezos. The Company sells a wide range of products

– beauty, electronics, jewellery, appliances, books, toys,

pet supplies etc - through its website directly to

consumers (Business-to-Consumer). Essentially, if the

product can fit in a small box and easily transported,

Amazon.com is likely to have it. Among its significant

product range, the website offers customised buyer

experience and value for money (low prices) – Amazon

prides itself on being an “obsessively” customer centric

company. The Company operates its own warehouses

and while Amazon.com sell its own products, it is also a

re-seller of other brands. That is, large and small retailers

can utilise Amazon.com as a distribution channel.

www.vested.com.au

3 Vested Research

Why is Amazon coming to Australia? Amazon already

makes between A$500-700m in revenue per annum

from Australian consumers, therefore it already has a

captured market in Australia. Additionally, Australia is

an attractive market given a high proportion of middle

class, concentrated population and increasing internet

penetration. However, it should also be highlighted that

from 1 July 2017 Australia will levy its 10% Goods and

Services Tax on online purchases made overseas.

Previously the A$1,000 personal consumption

exemption meant it was very attractive for consumers to

purchase from overseas website and not incur an

additional tax (GST). We wonder if the change in

legislation has fast tracked Amazon’s plans to protect its

existing revenue base in Australia and the maturing

penetration in its key global markets has meant it is

looking for new markets.

How will Amazon hurt the Australian retailers?

Amazon’s significant product range and focus on low

prices will likely impact the Australian retailers in three

main ways – increased competitive pricing, revenue

leakage in exposed categories and impact on margins

from negative operating leverage (high fixed costs). For

our analysis, we consider: food (WES/WOW),

clothes/accessories (PMV/MYR), electronics/bulky

goods (HVN/JBH) and auto accessories (SUL/BAP).

Unsurprisingly to most, the electronics category is the

most exposed and likely to be Amazon’s initial focus.

What is the likely response from the Australian

retailers? In our view the Australian retailers are likely

to combat Amazon at the pricing level (in the hope to

retain and even grow volumes), increased focused on

customer experiences/value add services (give

customers reasons to come in-store), increased

investment on online capabilities and perhaps adapt

their business model (that is, we wonder if an aggressive

store roll-out strategy is the best growth option going

forward?)

www.vested.com.au

4 Vested Research

Who is best placed among Australian retailers?

Vertically integrated players (Premier Investment

Group), low cost producers and larger focus on bulky

goods, in our view.

Global consumer trends...

lessons for retailers?

A recent global survey conducted by McKinsey & Company

provides interesting insights into the changing behaviour

of consumers. These insights are also relevant for the

domestic market but also provide some insights to how

incumbent retailers could approach the Amazon threat.

The Company conducted a global survey of over 22,000

consumers from around the world (26 countries) to better

understand changing consumer buying behaviour, as

relevant for retailers and packaged-goods companies.

The key findings from the survey were: (1) the new

consumer proactively searches for savings; (2) the new

consumer is loyal to particular brands but price does come

into consideration; (3) the new consumer is unlikely to

return to a particular brand once they trade down; (4) the

new consumer will splurge on certain categories; (5) the

new consumer will shop across channels.

The main message from this survey is the desire for “value

for money”. The global financial crisis has forced

consumers to become more frugal; exposed structurally

challenged industries (and therefore jobs); and reshaped

others to become more efficient (mostly through the

adoption of technology). In our view, the implications from

the key findings of McKinsey & Company’s survey are

already being played out in the retail industry. Key points

for consideration:

Competition has significantly increased since the GFC,

as retailers are competing for a more money conscience

consumer. That is, “sales” or “mark downs” is now an all

year around phenomena. Price comparison across

www.vested.com.au

5 Vested Research

channels (and geographical boundaries) has meant that

consumers are more switched on to being charged

premium prices for overseas brands. The once very

strong Australian dollar meant overseas websites

offered much better value for the same product than in

Australian stores. However, even the decline of the

Australia dollar has not deterred consumers from

websites like Amazon to purchase certain items. This

has meant price deflation across many categories is now

a norm. We believe incumbents in Australia will likely

need to match Amazon on price (or increase the value

proposition) to compete effectively.

Consumers have considerably shifted their spending

towards online (some just pure online plays) – both for

getting the best deals but also convenience. Companies

must have a credible online presence and offering to

compete in the world of the new consumer.

“Generic” retailers no longer work. That is retailers must

have a very clear value proposition and know exactly

who their target consumer is. This also means investing

significant amount of resources (e.g. have established

analytical and revenue analysis teams) to understand

the attributes and behaviour of their target consumer.

Brands matter but at reasonable price. The survey

indicates consumers are not necessarily shy of paying

up, but they need to see value. If the price is not justified,

then as the survey indicates, once consumers trade

down (or to an alternative) companies will find it difficult

to bring them back.

Who is Amazon?

Amazon (or Amazon.com) is a US based e-commerce

company founded in 1994 by current CEO Jeff Bezos. The

www.vested.com.au

6 Vested Research

Company sells a wide range of products – beauty,

electronics, jewellery, appliances, books, toys, pet supplies

etc - through its website directly to consumer (Business-to-

Consumer…B2C). Essentially, if the product can fit in a

small box and easily transported, Amazon.com can sell it.

Among its significant product range, the website offers

customised buyer experience and value for money (low

prices). The Company operates its own warehouses and

while Amazon.com sell its own products, it is also a re-

seller of other brands. That is, large and small retailers can

utilise Amazon.com as a distribution channel.

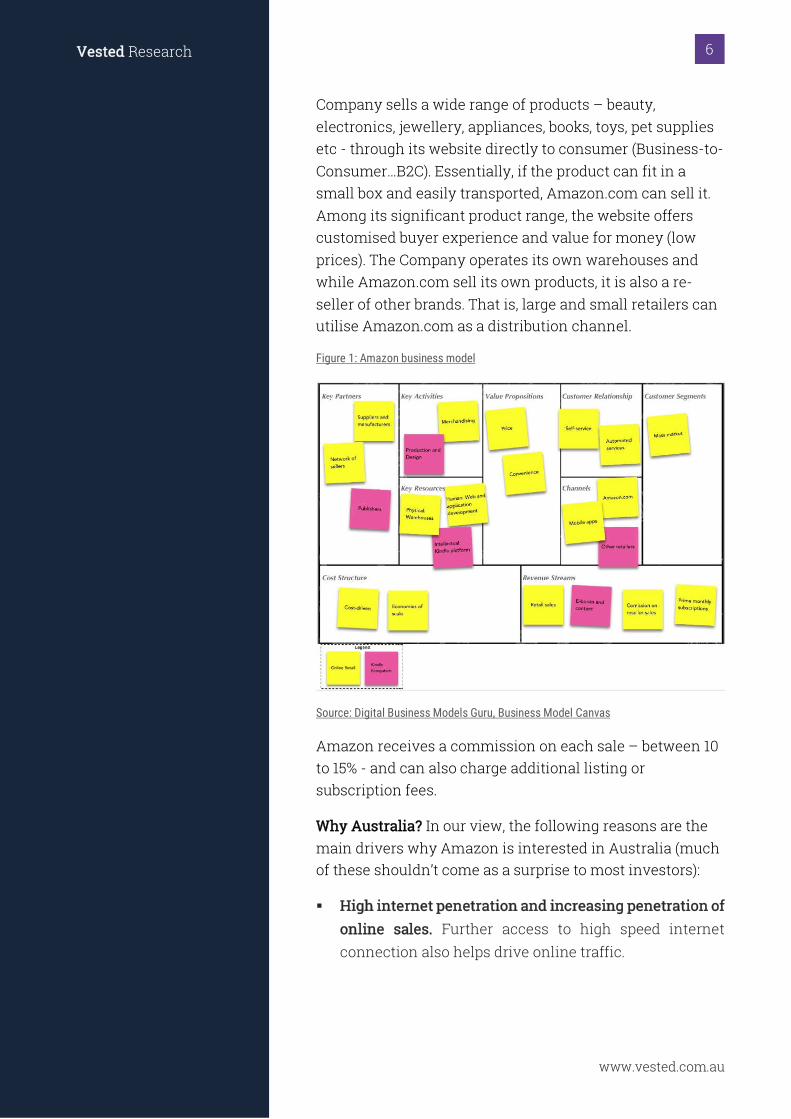

Figure 1: Amazon business model

Source: Digital Business Models Guru, Business Model Canvas

Amazon receives a commission on each sale – between 10

to 15% - and can also charge additional listing or

subscription fees.

Why Australia? In our view, the following reasons are the

main drivers why Amazon is interested in Australia (much

of these shouldn’t come as a surprise to most investors):

High internet penetration and increasing penetration of

online sales. Further access to high speed internet

connection also helps drive online traffic.

www.vested.com.au

7 Vested Research

High disposable income. Relative to other parts of the

world, Australia has a healthy middle class and

disposable incomes remain attractive.

Population is concentrated around key coastal cities.

This helps companies which require distribution

channels to move their products. Hence Amazon can get

maximum leverage from fewer distribution warehouses.

Amazon already derives revenue from Australia.

Australian consumers are already warm to online

shopping and Amazon already has a following in the

local market. It has been reported, Amazon already

makes between A$500-700m in revenue per annum

from Australian consumers.

Australians are already shopping on Amazon.com. It is

worth reminding investors, Amazon already makes

between A$500-700m in revenue per annum from

Australian consumers. A recent survey conducted by

Neilson of ~1,500 Australians, indicated 27% of respondents

were aware of Amazon Prime (online video streaming

service) and 38% of respondents were aware of Amazon.

Further, 75% of the respondents said that they were

interested in Amazon Australia and 56% are likely to

purchase from this site.

Electronic goods appear to be the most likely impacted

category from Amazon’s move into Australia. According to

the survey, products which are most likely to be bought on

Amazon’s Australia site are: electronics (67%), books (61%),

clothes (59%), shoes (42%), music (36%), videos (32%),

packaged groceries (18%), fresh vegetables (9%) and fresh

meat (7%).

When is Amazon likely to open in Australia? We have done

some snooping around (e.g. industry experts, consultants

carrying out potential impact studies) to gauge an entry

date, but at present any date appears to be speculative

(most investors would have heard by now how Amazon is

“hiring hundreds of people”). In our view, it is safe to

www.vested.com.au

8 Vested Research

assume at the earliest it will be December 2017 (the all-

important Christmas shopping period), however it is more

likely to be sometime in 2018.

How will Amazon hurt

Australian retailers?

Amazon’s significant product range and focus on low

prices will likely impact the Australian retailers in three

main ways – increased competitive pricing, revenue

leakage in exposed categories and impact on margins from

negative operating leverage (high fixed costs). For our

analysis, we consider: food (WES / WOW),

clothes/accessories (PMV / MYR), electronics/bulky goods

(HVN / JBH) and auto accessories (SUL / BAP).

What is consensus presently forecasting? While there are

many moving parts to these numbers (acquisition impacts,

non-discretionary business mix, one-offs etc), what we

want to highlight as a key takeaway is that neither margins

or revenue is expected to fall off the cliff – particularly for

the stocks we cover or are positive on. HVN is the only

stock for which consensus expects revenue to go

backwards in FY19e, by which time Amazon is likely to be

in advanced stages of cementing its Australian operations.

Figure 2: Consensus estimates for selected retailers

Source: Bloomberg, BTIG

Category specific comments and our rating of exposure to

the Amazon threat (High / Medium / Low):

Current EBIT Margin EPS Growth Revenue Growth

Select Australian Retailers Price FY17E FY18E FY19E FY17E FY18E FY19E FY17E FY18E FY19E

JB HI-FI LTD 25.05 5.4% 5.2% 5.3% 22.5% 10.4% 6.7% 41.4% 21.3% 4.8%

HARVEY NORMAN HOLDINGS LTD 4.36 17.7% 18.3% 19.0% 18.0% 3.2% 1.7% 76.4% 2.8% -1.2%

MYER HOLDINGS LTD 1.19 3.6% 3.9% 4.1% 3.4% 11.0% 5.9% 17.1% 0.9% 1.1%

PREMIER INVESTMENTS LTD 14.20 12.5% 13.2% 14.0% 8.4% 13.8% 13.9% 6.1% 8.7% 9.2%

SUPER RETAIL GROUP LTD 9.92 8.3% 8.7% 9.0% 21.9% 13.5% 11.2% 0.9% 6.3% 6.1%

BAPCOR LTD 5.39 9.5% 9.7% 10.2% 36.9% 26.2% 13.4% 56.2% 34.7% 4.5%

WOOLWORTHS LTD 26.47 4.2% 4.5% 4.7% -45.3% 10.6% 6.9% -1.5% 2.4% 3.2%

WESFARMERS LTD 45.14 6.5% 6.3% 6.3% 30.4% 0.8% 4.9% 5.1% 4.0% 4.3%

www.vested.com.au

9 Vested Research

Electronics, books & media (HIGH). These categories are

typically Amazon’s go to segments when entering most

markets. In this regard, JB Hi-Fi and other electronics

retailers are most exposed. Harvey Norman also has a

substantial electronics’ offering. We expect price

competition to increase within this category, as

consumers will likely shop for value and compare price

discrepancies across channels.

Bulky goods (LOW). In our view, the least exposed to the

Amazon threat is the bulky goods category. Not only are

these much harder to transport, they also require

significant distribution channels. Also, given the price

point for these products tend to be higher relative to

other categories, in our view, consumers generally want

to ‘look and feel’ before purchasing. With its recent

acquisition of The Good Guys, JB Hi-Fi is well placed.

Discount Department Stores (DDS) (MEDIUM). We think

the impact to DDS will be mixed and will come down to

value proposition. We note most DDS have moved to

everyday low price business model (such as Target, Big

W and Kmart) and, in our view, are not over-earning. We

see companies such as Myer (MYR) at greater risk –

especially in the cosmetics category (which is a higher

margin) – who don’t own all their brands but act more

like a brick and mortar ‘marketplace’. Myer introduced

Myer Exclusive Brands (MEB) for this very reason,

however we note at its 1H17 results, MEB sales were

down 11.6%. Further, the Company has struggled to get its

online offering right and remains less than 5% of group

revenue.

Consumer staples – food (LOW). In our view, this

category is less exposed to the Amazon threat. It is our

understanding that Amazon will look to offer packaged

groceries and eventually move into the fresh segment.

However, the survey conducted by Neilson indicated

that there was less enthusiasm from consumers to

purchase these products from the Amazon Australia

www.vested.com.au

10 Vested Research

website – packaged groceries (18% of respondent said

likely to buy online), fresh vegetables (9% of

respondents) and fresh meat (7% of respondents).

Further, we note the major supermarkets have a strong

loyalty and fuel card programs, which provided some

buffer.

Auto-parts (MEDIUM). We are not totally convinced that

all auto-part retailers (including aftermarket parts &

accessories) are equally exposed to this threat. In the

case of Bapcor, which derives a large part of its business

from trade sales (that is selling parts to mechanics) the

ability to talk to an expert on specific parts over the

phone and then have them delivered within hours is a

highly complex distribution model. Further, the costs of

these parts are a straight pass-through to the client,

hence the cost of the part is a not a major consideration

in the purchasing decision.

How will Australian retailers

respond to Amazon?

Amazon’s significant product range and focus on low

prices will likely impact the Australian retailers in three

main ways – increased competitive pricing, revenue

leakage in exposed categories and impact on margins from

negative operating leverage (high fixed costs). We discuss

each below.

Increase / improve respective online offering. Online retail

penetration remains very low in Australia relative to other

key markets. Australia has penetration of less than 4%,

which is much lower than 14% for the U.K. and 12% in

China. Within our coverage, JB Hi-Fi’s online penetration is

actually equivalent to the national average.

Figure 3: Online retail penetration for key regions (%)

www.vested.com.au

11 Vested Research

Source: BTIG, Bloomberg

Adapting business model for the new world. Many

retailers supplement organic growth (like-for-like sales)

with a store roll-out strategy. In our view, the Amazon

threat should provide management teams of incumbents

to re-evaluate indiscriminate “land-grab” strategy. As we

are now finding in the US, household names such as

Macy’s is looking to shed 10,000 jobs and close hundreds of

stores as consumer shift online. We expect local retailers to

take a proactive approach to store network rationalisation,

rather than a (forced) reactive one.

Strong sourcing capabilities. In our view the better placed

retailers already have strong product sourcing teams in

place.

Who is best placed among

Australian retailers?

In our view, companies which are vertically integrated

players (Premier Investment Group), low cost producers

and more focus on bulky goods (The Good Guys) should be

well placed to weather an increased competitive

environment. However, we note they will not be completely

immune.

Vertically integrated. That is, companies who manufacture

and market their own brands are better placed to withstand

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Sep-07 Nov-08 Jan-10 Mar-11 May-12 Jul-13 Sep-14 Nov-15 Jan-17

Australia U.K. China South Korea

www.vested.com.au

12 Vested Research

increased competition, such as Premier Investment Group

(PMV). PMV’s management pointed out that they believe

they are well placed relative to peers for the imminent

entry of Amazon to the domestic market. They noted that

PMV designs, sources and supplies all its own brands.

Therefore, it will all come down to its brand power. Further,

PMV has a growing global exposure (away from Australia)

which should also provide it with some buffer. PMV already

competes with Amazon, given the Company’s strong

online sales growth in Smiggle in the UK where Amazon

has a strong market position. PMV sells its strong market

brands of Smiggle and Peter Alexander via its distribution

channels (and not eBay or Amazon), which should provide

buffer to the Company.

Strong loyalty program / value added services. Incumbents

must consider strong loyalty programs and increased

value-add services to attract (or even keep) consumers. As

noted above, we highlight as an example the strong loyalty

/ fuel discount program the major supermarkets

(Wesfarmers) operate.

www.vested.com.au

13 Vested Research

PE-multiples charts for key

retailers – is the Amazon

effect in the price?

Figure 5: JBH PE-multiple vs long-term average

Figure 6: HVN PE-multiple vs long-term average

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

Apr-07 Jul-08 Oct-09 Jan-11 Apr-12 Jul-13 Oct-14 Jan-16 Apr-17

JBH PE-Multiple LT Avg

5.0x

10.0x

15.0x

20.0x

25.0x

Apr-07 Jul-08 Oct-09 Jan-11 Apr-12 Jul-13 Oct-14 Jan-16 Apr-17

HVN PE-Multiple LT Avg

www.vested.com.au

14 Vested Research

Figure 7: PMV PE-multiple vs long-term average

Figure 8: MYR PE-multiple vs long-term average

Source: Bloomberg, BTIG

Figure 9: SUL PE-multiple vs long-term average

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

Apr-07 Jul-08 Oct-09 Jan-11 Apr-12 Jul-13 Oct-14 Jan-16 Apr-17

PMV PE-Multiple LT Avg

6.0x

7.0x

8.0x

9.0x

10.0x

11.0x

12.0x

13.0x

14.0x

15.0x

16.0x

Oct-09 Jan-11 Apr-12 Jul-13 Oct-14 Jan-16 Apr-17

MYR PE-Multiple LT Avg

5.0x

7.0x

9.0x

11.0x

13.0x

15.0x

17.0x

19.0x

Apr-07 Jul-08 Oct-09 Jan-11 Apr-12 Jul-13 Oct-14 Jan-16 Apr-17

SUL PE-Multiple LT Avg

www.vested.com.au

15 Vested Research

Figure 10: BAP PE-multiple vs long-term average

Figure 11: WES PE-multiple vs long-term average

Figure 12: WOW PE-multiple vs long-term average

Source: Bloomberg, BTIG

12.0x

14.0x

16.0x

18.0x

20.0x

22.0x

24.0x

26.0x

28.0x

Jun-14 May-15 Apr-16 Mar-17

BAP PE-Multiple LT Avg

5.0x

10.0x

15.0x

20.0x

25.0x

Apr-07 Jul-08 Oct-09 Jan-11 Apr-12 Jul-13 Oct-14 Jan-16 Apr-17

WES PE-Multiple LT Avg

12.0x

14.0x

16.0x

18.0x

20.0x

22.0x

24.0x

26.0x

Apr-07 Jul-08 Oct-09 Jan-11 Apr-12 Jul-13 Oct-14 Jan-16 Apr-17

WOW PE-Multiple LT Avg

www.vested.com.au

Contact Us:Office: Level 11, 50 Cavill Avenue, Surfers Paradise, QLD 4217

Email: [email protected]: 1300 980 849

Vested Equities Pty Ltd holds an Australian Financial Services License 478987. All advice (if any) is general advice only. Your personal circumstances and financial

objectives have not been taken into consideration. Accordingly you should consider if the advice is right for you. Past performance is not a reliable indicator of future

performance. Please be aware that all investment and trading activity is subject to both profit & loss and may not be suitable for you. All advice and education content is of the nature of general information only and must not in any way be construed

or relied upon as legal, financial or personal advice. No consideration has been given or will be given to the individual investment objectives, financial situation or needs of any particular person. The decision to invest or trade and the method selected is a personal decision and involves an inherent level of risk, and you must undertake

your own investigations and obtain your own advice regarding the suitability of this product for your circumstances.