Alternative Investment Funds in Malta · 3rd pillar: Macroeconomic environment 21 5.8 4th pillar:...

26

Alternative Investment Funds in Malta www.kpmg.com.mt Fund Services

Transcript of Alternative Investment Funds in Malta · 3rd pillar: Macroeconomic environment 21 5.8 4th pillar:...

Alternative Investment Funds in Malta

www.kpmg.com.mt

Fund Services

Table of contentsWhy Malta? 2

Funds in Malta 6

Alternative Investment Funds 12

Taxation 30

Appendices 34

Appendix 1: Comparison between Investment Services jurisdictions 35

Appendix 2: Living in Malta 43

Key Contacts 46

Why Malta?Some Key data

• Malta became the smallest member state in the EU in May 2004, and joined the Euro Zone in 2008.

• GDP per capita is at 95% of the EU average, at €24,450 (June 2017).

• Malta was relatively unscathed during the years following the financial crisis of 2008, and stabilised by 2012.

• Malta has one of the highest figures of sunshine hours in Europe with an average of 3,000 per year.

• English widely spoken and written in Malta, and is the principal language for education and business.

Factors contributing to Malta’s competitive advantage

• Flexible legal and regulatory environment with a legislative framework in line with EU Directives. Malta is fundamentally a civil law jurisdiction, however business legislation is principally based upon English law principles

• Malta boasts a high level of education with graduates representing a cross-section of the various disciplines related to financial services. Specific training in financial services is offered at various post-secondary and tertiary education levels. The accounting profession is well-established on the island. Accountants are either university graduates or in possession of a certified accountant qualification (ACA/ACCA)

• A flexible and proactive regulator that is very approachable and business-minded and robust

• An ever-growing supply of high-quality office space for rent at cheaper prices than Western Europe

• Malta’s development as an international financial centre is reflected in the range of financial services available. Complementing the traditional retail functions, banks are increasingly offering private and investment banking,

project finance, syndicated loans, treasury, custody and depositary services. Malta also hosts a number of institutions specialising in trade-related products such as structured trade finance, factoring and forfeiting

• Major international accountancy firms, including the Big 4 firms, are present on the island. Legal firms tend to be local, though most form part of international legal networks. Many professionals in both areas pursue studies and training overseas

• Maltese standard time is one hour ahead of Greenwich Mean Time (GMT) and six hours ahead of US Eastern Standard Time (EST) so business runs smoothly with the international community

• International Financial Reporting Standards, as adopted by the EU, are entrenched in company legislation and applicable since 1997, so there are no local GAAP requirements to deal with

• A very competitive tax system approved by the EU and an extensive and growing double taxation treaty network

• No restrictions on the granting of work permits for EU and EEA nationals

Global Competitiveness Index 2017-2018 rankingsHow Malta scored

Global Competitiveness IndexRank (out of 140)

GCI 2016 - 2017 40 4.5GCI 2015 - 2016 48 4.4GCI 2014 - 2015 (out of 144) 47 4.4GCI 2013 - 2014 (out of 148) 41 4.5GCI 2012 - 2013 (out of 144) 47 4.4

Basic requirements (20.0%) 29 5.41st pillar: Institutions 38 4.52nd pillar: Infrastructure 42 4.83rd pillar: Macroeconomic environment 21 5.84th pillar: Health and primary education 11 6.6

Efficiency enhancers (50.0%) 37 4.65th pillar: Higher education and training 30 5.26th pillar: Goods market efficiency 29 4.97th pillar: Labor market efficiency 45 4.78th pillar: Financial market development 43 4.49th pillar: Technology readiness 22 5.910th pillar: Market size 119 2.7

Innovation and sophistication factors (30.0%) 34 4.211th pillar: Business sophistication 31 4.612th pillar: Innovation 38 3.6

Score(1 -7)

Overall, Malta has placed number 37 out of 137 countries in the 2017-2018 report. Malta remained in the top-tier category, that groups ‘innovation driven economies’. Malta has again scored highly in education, innovation, macroeconomic environment, business sophistication and technological readiness. It ranked 16th with regard to tax incentives encouraging investment.

(World Economic Forum’s Global Competitiveness Report 2017-2018, 137 countries reviewed)

The Global Competitiveness Report, compiled by the World Economic Forum’s centre for Global Competitiveness and Performance, provides an analysis of the strengths and weaknesses of countries, related to national competitiveness using the Global Competitiveness Index as themain methodology. Competitiveness is defined as “the set of institutions, policies, and factors that determine the level of productivity of a country” and is gauged on 12 pillars.

World Economic Forum

Joint 1st for the timely implementation of EU’s Internal Market Rules into national law

17th for Soundest Banking Systems in the World

3rd for Inter-national bandwidth per user

22nd for Technological readiness

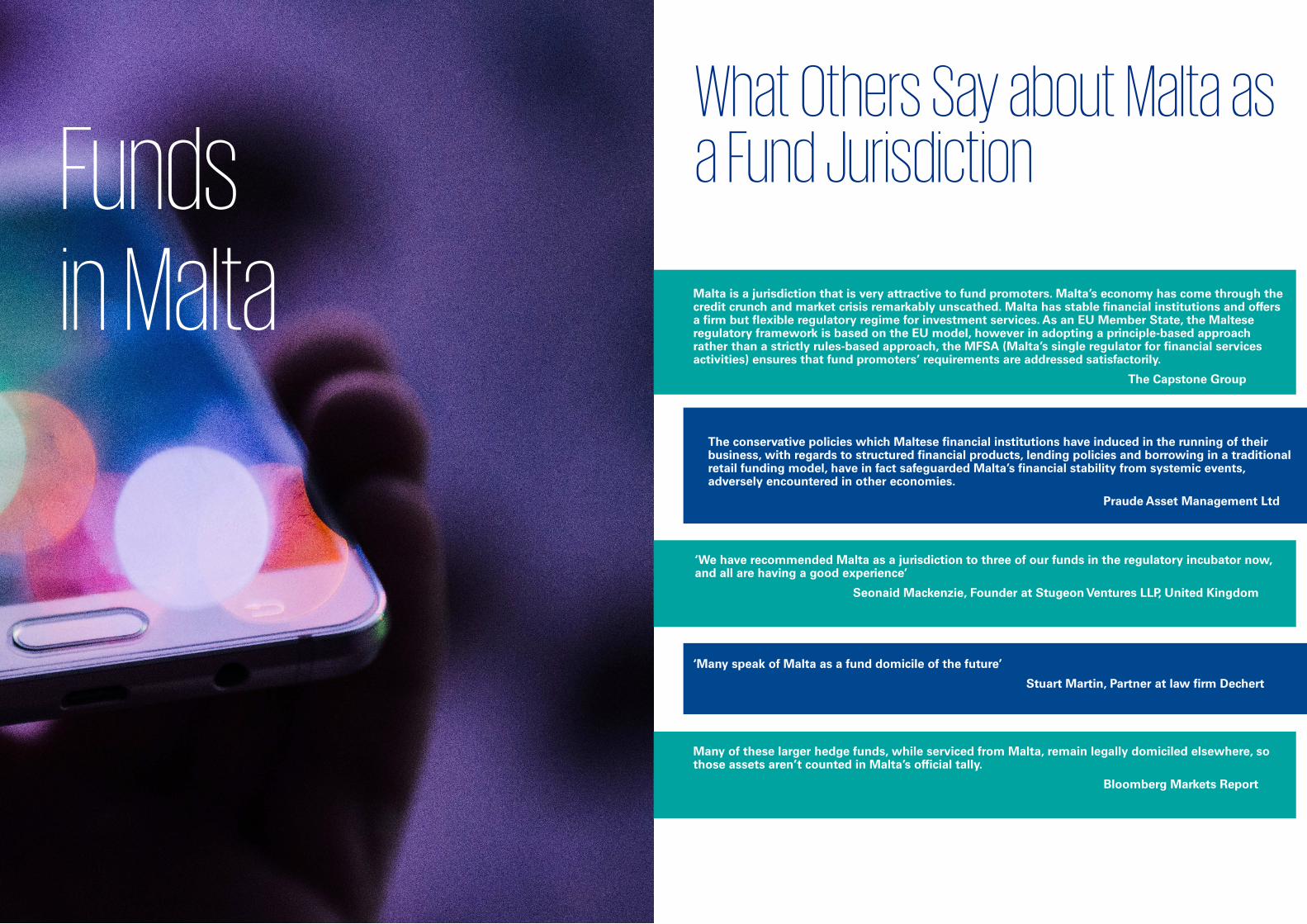

What Others Say about Malta as a Fund Jurisdiction

Malta is a jurisdiction that is very attractive to fund promoters. Malta’s economy has come through the credit crunch and market crisis remarkably unscathed. Malta has stable financial institutions and offers a firm but flexible regulatory regime for investment services. As an EU Member State, the Maltese regulatory framework is based on the EU model, however in adopting a principle-based approach rather than a strictly rules-based approach, the MFSA (Malta’s single regulator for financial services activities) ensures that fund promoters’ requirements are addressed satisfactorily.

The Capstone Group

The conservative policies which Maltese financial institutions have induced in the running of their business, with regards to structured financial products, lending policies and borrowing in a traditional retail funding model, have in fact safeguarded Malta’s financial stability from systemic events, adversely encountered in other economies.

Praude Asset Management Ltd

‘We have recommended Malta as a jurisdiction to three of our funds in the regulatory incubator now, and all are having a good experience’

Seonaid Mackenzie, Founder at Stugeon Ventures LLP, United Kingdom

‘Many speak of Malta as a fund domicile of the future’

Stuart Martin, Partner at law firm Dechert

Many of these larger hedge funds, while serviced from Malta, remain legally domiciled elsewhere, so those assets aren’t counted in Malta’s official tally.

Bloomberg Markets Report

Funds in Malta

The Malta Financial Services Authority (MFSA)

The Malta Financial Services Authority (MFSA) is the single regulator for financial services in Malta and regulates banking, insurance, pensions and investment services (securities) business. The MFSA adopts a firm but flexible approach to regulation.

• The licensing process is personalised

• Regulation is business-friendly and mindful of business needs

• Business oriented and efficient at transposing all potentially beneficial

discretionary clauses in EU Directives

• Supervision is risk based and minimally intrusive

• Several institutions in Malta choose to target “niche” segments of the market

• The MFSA is open to new business models

MFSA FOCUS

The reputation and suitability

of the applicant and all other

parties involved in the scheme

The experience and track

record of all parties involved in the scheme

The protection of investors and

the general public

The protection of Malta’s reputation

Promotion of competition and choice

• Regulatory Development Unit - co-ordinates the development of cross-sector policy initiatives and enables the MFSA to address market and regulatory developments as they arise

• Authorisation Unit - receives and processes all applications for authorisations to conduct regulated financial services in Malta

• Supervision Units - responsible for the post-licensing ongoing supervision of the regulated entities in their respective area

• Conduct Supervisory – responsible for conduct supervision of investment services license holders, insurance undertakings and intermediaries. As of 2018, the Conduct supervision function assumed the same responsibilities for credit and financial institutions.

• The Banking Supervision Unit - has continued to build upon the relationship of mutual trust with all key players in the financial sector following the transfer of the banking supervisory function from the Central Bank

• Insurance and Pensions Supervision Unit - conducts its regulatory and supervisory role to safeguard the safety and the soundness of the Maltese insurance sector. Through the supervisory process, action is taken to protect the interests of the industry as a whole, the interests of policyholders, and to minimize as far as possible consumer risks

The application and licensing processIt is normal practice for licence applications to be discussed with the MFSA before formal submission of the application documents. The supporting documents to be attached to the application include the following:

Comprehensive business profile, including a detailed business plan

Supporting board resolution

Financial Resources Statement

Audited accounts (where applicable)

Projected three-year financial statements

Auditor’s confirmation

Memorandum and Articles of Association

Auditors’ declaration to accept appointment

Auditor’s opinion on the Statement of Financial Resources

Individual questionnaires on key personnel of the company

Copy of representation agreements

Insurance policies (where applicable)

Personal questionnaire

Detailed shareholding structure

Evidence substantiating the competence of the proposed individuals

IT questionnaire (where applicable)

When considering whether to grant or refuse an Investment Services Licence, the MFSA must take account of:

• The degree of protection to the investors;

• The protection of the reputation of Malta, taking into consideration Malta’s international commitments

• The promotion of competition and choice

When considering whether to grant or refuse an Investment Services Licence, the MFSA must take account of:

• Integrity;• Competence; and• Solvency

As part of the licensing process,

the Applicant will be asked to identify an individual who will be designated as a Compliance

Officer once operations have commenced. Additionally the

Applicant must appoint a Money Laundering Reporting Officer as per Regulation 15 of the

Prevention of Money Laundering Regulations and Funding or

Terrorism Regulations (‘PMLFTR’) This person can be the same

as the Compliance Officer. The Applicant must formally propose these Officers to MFSA in which the MFSA will then confirm such

duties with the proposed.

The application and licensing process

Phase OnePreparatory

Phase TwoLicence

Application

Phase ThreePost Licensing

& Pre Commencement

of Business

• Initial meeting with the MFSA Authorisation Unit

• Communication of the applicant’s intended activities to the regulator

• Preliminary indication by the regulator to move to the second stage

• Submission of documents in draft form to the MFSA Authorisation Unit

• Fit and proper tests carried out by MFSA on the applicant

• MFSA feedback on documents

• Provision of replies to MFSA queries by applicant

• Completion of review of the application and all documents to the satisfaction of the MFSA

• MFSA will issue its ‘in principle’ approval subject to licence conditions

• Applicant to finalize all outstanding matters and submit full applicant in final format

• Registration of company establishing the institution requesting a licence

• Issue of official licence

• Applicant to satisfy all post licensing matters prior to formal commencement of business

• Ongoing supervision by the Securities & Markets Supervision Unit

AlternativeInvestment Funds

AIFMD

An AIF is a non-retail collective investment scheme licensable in terms of the Investment Services Act, 1994, following the transposition of the Alternative Investment Fund Managers Directive (“AIFMD”) into Maltese law in July 2013.

AIFMD lays down the rules for the authorisation, ongoing operation and transparency of fund managers that manage and/or market Alternative Investment Funds (AIFs) in the European Union.

Fund operations are indirectly impacted by AIFMDw provisions such as requirements for leverage limits, fund risk profiles and portfolio liquidity.

Examples of AIFs include hedge funds, private equity funds, real estate funds and venture capital funds.

Units or shares of AIFs may be marketed in other Member States or EEA States by means of the passporting procedure provided in the applicable rules as transposed from AIFMD.

A third party Fund manager which can be unregulated or supervised. Quick licenses gained from this process, usually with 10 days.

Alternative Investment Funds

AIF

Impact

E.g.

Feature

Alternative Investment Funds (AIFs)

NAIF

ProfessionalInvestorFunds

AlternativeInvestment

Funds

When the Professional

Investor Fund (PIF) has a total of Assets Under

Management which exceed EUR 100M (including leverage)

the Scheme would need to

be registered as an Alternative

Investment Fund.

In the case of a PIF which does not

employ leverage and whereby

investors may not redeem their shares for the first 5 years of operation of the fund, the threshold to apply for an AIF

license is set atEUR 500M.

An AIF has very similar

characteristics to the PIF except

that it has stricter regulatory

requirements.

The Maltese regulatory

framework includes provisions which allow alternative

investment funds to register under the PIF regime

and to eventually apply for licensing

under the AIF, following growth

in their AUM, thus providing additional

flexibility to such funds.

Professional Investor Funds vs Alternative Investment Funds

IncorporatedCell Company

LimitedPartnership

ContractualFund

SICAV or INVCO

Unit Trust

AIFs

AIF Structure

AIF’s Targeted Investors

1. Professional Investors

MIFID defines a professional investor as

a ‘client who possesses the experience,

knowledge and expertise to make its own

investment decisions and properly assess

the risks that it incurs’ and who meets the

following criteria:

• Entities which are required to be

authorised or regulated to operate in

the financial markets

• Large undertakings

• National and regional governments,

Central Banks, international and

supranational institutions

• Other institutional investors whose

main activity is to invest in financial

instruments

The Investment Services Rules applicable

to Alternative Investment Funds specify

that AIFs targeted to professional investors

must abide by investment objectives,

policies and restrictions outlined in its

Offering Document.

Otherwise, no investment, borrowing or

leverage restrictions apply except for cases

whereby there is investment through

Trading Companies and Special Purpose

Vehicles.

In the case of a conversion of a PIF into

an AIF, the AIF may continue to target

the same categories of investors as a

PIF; namely, Experienced, Qualifying and

Extraordinary Investors. In this case, the

AIF would be subject to the same ongoing

compliance regulations as those imposed

on a PIF targeted to such investors, in

addition to the requirements in relation to

AIFs.

In all cases, the AIF must comply with

the investment objectives, policies

and restrictions outlined in its Offering

Document.

2. Qualifying Investors

• Minimum investment threshold is

EUR 100,000 or currency equivalent

• No investment, borrowing or leverage

restrictions

• Supplementary conditions in case of

investment through trading companies

or Special Purpose Vehicles

Internally Managed AIFs

Externally Managed AIFs

• The governing body of the AIF shall be composed of one or more directors independent from the AIFM and the depositary

• An AIF is obliged to appoint a Depositary, an Auditor, a Compliance Officer and a Money Laundering Reporting Officer.

• The AIF may be self-managed or externally managed. In the case of a self-managed AIF, an Investment Committee must be appointed.

• The appointment of a fund administrator or investment advisor is on a voluntary basis, or may be performed by the AIFM (if applicable).

Money Laundering Reporting Officer

(MLRO)

ComplianceOfficer

Scheme

Directors

Individuals and/or Corporate

InvestmentCommittee

Risk ManagementFunction

InvestmentAdvisor

Auditor Depositary

Administrator

AlternativeInvestment

Fund ManagerPrime Broker

The Management of AIFsManagement of an AIF

An AIF may be self-managed or managed externally by another entity

The main activities to be undertaken in the management of AIFs are portfolio management and risk management. However, the manager of an AIF may also undertake ancillary activities such as administration, marketing and activities related to the assets of the AIF e.g. activities related to fiduciary duties, facilities management and advice to undertakings on capital structure

The AIF shall be subject to investment objectives, policies and restrictions outlined in its Offering Document. The AIFM shall take all reasonable steps to comply with the investment policies and restrictions of the AIF. Self-managed AIF

Discretionary management activities vested in the Investment Committee, made up of no less that 3 members, under the responsibility of the Board of Directors.

Majority of Investment Committee meetings, at least quarterly, must be physically held in Malta

Must have at least one independent director and one Malta resident director

Initial capital requirement of EUR 300,000

Required to comply with all requirements for AIFMs under the AIFMD (and Maltese law) and be authorised as such

(Reference in the following pages to AIFM also shall be construed to refer also to self-managed AIFs)

Externally managed AIF

If manager is established in Malta, it must be in possession of a Category 2 Investment Services Licence and must also be licensed as an Alternative Investment Fund Manager (AIFM).

The conditions for authorisation

If established outside Malta the manager must be licensed as an AIFM and situated in another EU Member State.

AIF must have at least one director acting independently from the manager and the depositary

EUR 125,000 as initial capital requirement to set up AIFM in Malta Conditions for authorisation of a fund management company in Malta The MFSA must be satisfied that the AIFM will continue to meet its legal obligations

The AIFM has sufficient capital and own funds

The AIFM’s business is carried out by persons of experience and good repute

The qualifying shareholders are suitable and can ensure sound and prudent management

The AIFM’s head office is located in Malta, and adequately staffed to carry out the duties as required.

AIFMs are required to appoint a risk management function that is functionally and hierarchically separate from the portfolio management function and the two functions must also be separate from other operational functions.

AIFMs must satisfy their competent authorities that persons proposed to exercise duties in relation to the portfolio and risk management functions are fit and proper to occupy their role.

The AIFM is responsible for both the portfolio and risk management functions and must always retain effective management of the fund. As a result, it may only delegate one of the two functions, in all cases retaining responsibility for the proper performance of such functions.

These functions may only be delegated to undertakings authorised or registered for the purpose of asset management and subject to adequate supervision and should not be delegated to a depositary or any entities which may be in conflict with the interests of the AIF or AIFM.

AIFMs are also required to establish, implement and apply a conflicts of interest policy, remuneration policy and appropriate procedures for the proper and independent valuation of the assets of each AIF under management. The valuation function must be separate from the portfolio management function.

The valuation procedure of the respective underlying assets of the AIF needs to be spelt out in the Offering Documents. The MFSA expects the AIFM to gain an independent valuation for the purpose of valuing unlisted securities or other assets which are not dealt in regulated market and where prices are not readily available.

In such cases, the valuer will need to satisfy the following criteria:

• Be an independent person from the AIF, its offiicals, or any service providers to the AIF;

• Be of good standing with recognised and relevant qualifications and an authorised member of a recognised professional body in the jurisdiction of the assets;

• Be appointed by the AIFM

The valuation function may also be performed by the AIFM when it is with respect to securities other than those referred to above, provided that the valuation task is functionally independent from the portfolio management and the remuneration policy and other measures ensure that conflicts of interest are mitigated and that undue influence upon employees is prevented.

The Remuneration policy must cover senior management, portfolio management functions and functions with an impact on the risk profile; and which discourages risk taking that is inconsistent with the AIF’s risk profile.

AIFMs must comply with transparency requirements with regards to the financial position of the AIFs under management and information to be provided to investors of the AIFs under management and to the MFSA.

Requirements imposed on AIFMs and self-managed AIFs Requirements imposed on AIFMs and self-managed AIFs Depository requirement

A single independent depositary is required to be appointed for each AIF under management to be responsible for safekeeping, cash monitoring and oversight duties

The depositary must adhere to a strict liability regime which dictates that a loss by a depositary or its delegate of a financial instrument held in custody will give rise to an obligation to replace the instrument or pay compensation to the AIF without undue delay

AIFs established in Malta are required to appoint depositaries established in Malta that are in possession of a Category 4a licence in terms of the Investment Services Act (ISA)

Entities established in Malta in possession of a Category 4b license in terms of the ISA may be appointed as depositary to AIFs which have no redemption rights exercisable during the period of 5 years from the date of the initial investments and which, in accordance with their core investment policy, generally do not invest in assets that must be held in custody and to third country AIFs managed by a Maltese or EU AIFM, which are marketed in the EU/EEA

AIFMs and Prime Brokers are prohibited from acting as depositaries. The prohibition is lifted from Prime Brokers if measures have been taken to functionally and hierarchically separate the two functions and where no potential conflicts of interest arise

De Minimis AIFMs

AIFMs managing portfolios of AIFs, the AUM of which is less than EUR 100 million

or

AIFMs managing portfolios of AIFs, the AUM of which is less than EUR 500 million where the AIFs are unleveraged and have no redemption rights exercisable during a period of 5 years following the date of initial investment in each AIF

If the above conditions are met, an entity wishing to set up in Malta must apply for a de minimis Category 2 Investment Services Licence

PIFs managed by de minimis AIFMs are not subject to the same requirements as for AIFs.

When the conditions above cease to apply, the de minimis AIFM must apply for a full AIFM licence

Requirements imposed on AIFMs and self-managed AIFs De Minimis AIFMs

Requirements

• Requirements much less onerous than those applicable for a full AIFM

• Must have an established place of business in Malta

• Must be independent from the Custodian of the AIF

• Shall implement and maintain adequate risk management policies depending on the nature, scale and complexity of AIFs managed

• When choosing to delegate any functions, there is only the request of notification to MFSA and ensuring that such delegation does not bring about undue operational risk

• Initial capital requirement of EUR 125,000

• Reporting requirements towards MFSA as regards:

• Investment strategies of the AIFs under management

• Main instruments in which the AIFs under management are trading

• Principal exposures and most important concentrations of the AIFs under management

PassportingThe AIFMD confers an EU-wide marketing passport to the AIFM to market AIFs that it manages to professional investors across the EU.

An AIFM licence also confers an EU-wide management passport to the AIFM that permits the management of AIFs based in any EU Member State, either directly or through a branch. The host country competent authorities cannot impose any additional requirements on the AIFM in respect of the areas covered by the Directive.

AIFMs that fall under the de minimis regime cannot benefit from an EU-wide management or marketing passport, however small AIFMs have an opt-in procedure to apply for a full AIFM licence, which would make passporting possible.

The Investment Services Act (Marketing of AIFs) Regulations set out the conditions to be met for the:

• marketing of units or shares of European AIFs by a Maltese AIFM in Malta

• marketing of units or shares of European AIFs by a Maltese AIFM in an EU or EEA Member State other than Malta

• marketing of units or shares of European AIFs by a European AIFM in Malta

• marketing of AIFs by AIFMs to retail investors in Malta

The Investment Services Act (Alternative Investment Fund Manager) (Passport) Regulations set out the conditions to be met for:

• the freedom of establishment of Maltese AIFMs; namely, for the:

• direct management of a European AIF

• establishment of a branch in another Member State (MS) or EEA State

• the freedom of establishment for European AIFMs; namely, for the:

• direct management of a European AIF

• establishment of a branch in Malta

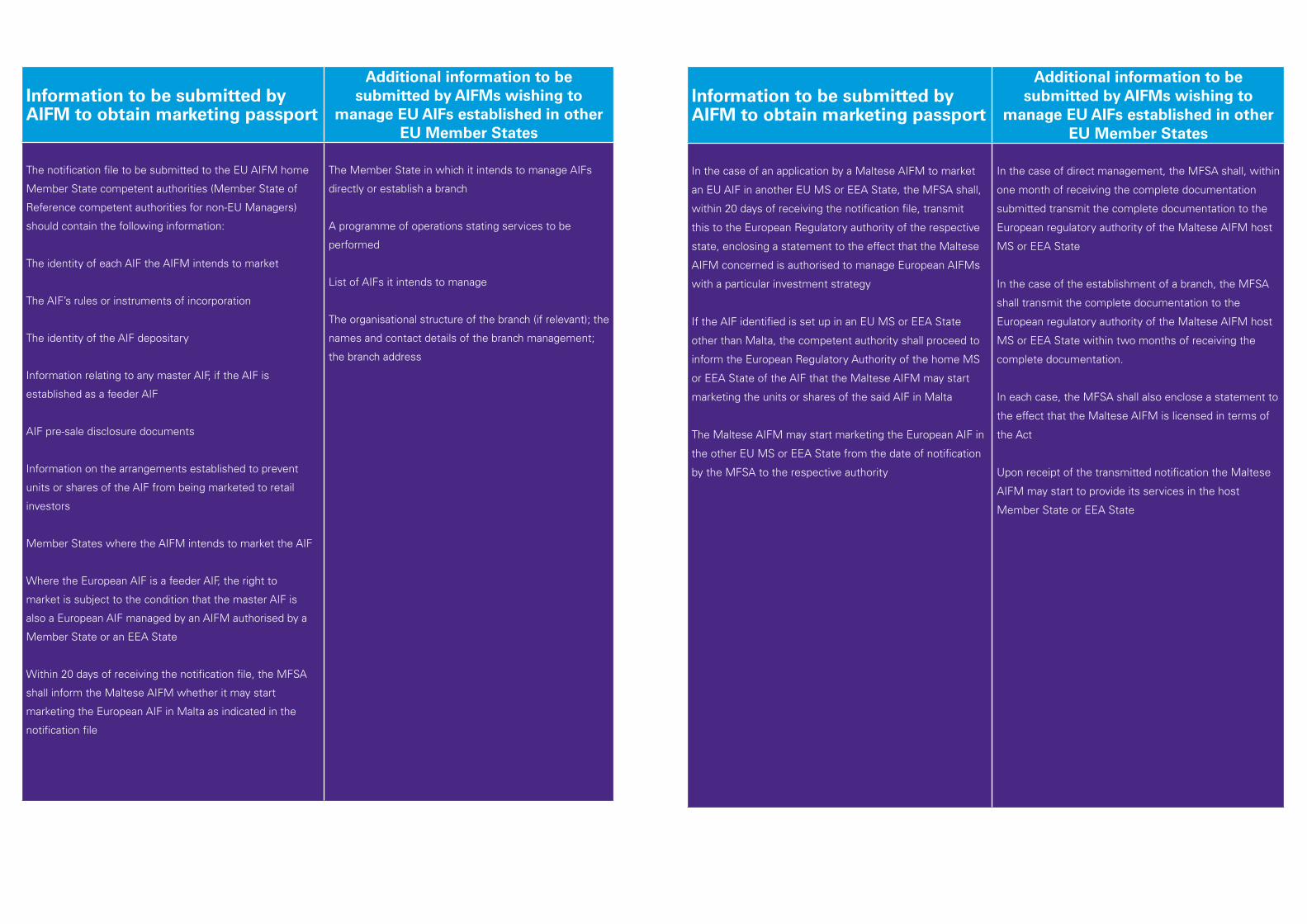

Information to be submitted by AIFM to obtain marketing passport

Additional information to be submitted by AIFMs wishing to

manage EU AIFs established in other EU Member States

The notification file to be submitted to the EU AIFM home

Member State competent authorities (Member State of

Reference competent authorities for non-EU Managers)

should contain the following information:

The identity of each AIF the AIFM intends to market

The AIF’s rules or instruments of incorporation

The identity of the AIF depositary

Information relating to any master AIF, if the AIF is

established as a feeder AIF

AIF pre-sale disclosure documents

Information on the arrangements established to prevent

units or shares of the AIF from being marketed to retail

investors

Member States where the AIFM intends to market the AIF

Where the European AIF is a feeder AIF, the right to

market is subject to the condition that the master AIF is

also a European AIF managed by an AIFM authorised by a

Member State or an EEA State

Within 20 days of receiving the notification file, the MFSA

shall inform the Maltese AIFM whether it may start

marketing the European AIF in Malta as indicated in the

notification file

The Member State in which it intends to manage AIFs

directly or establish a branch

A programme of operations stating services to be

performed

List of AIFs it intends to manage

The organisational structure of the branch (if relevant); the

names and contact details of the branch management;

the branch address

Information to be submitted by AIFM to obtain marketing passport

Additional information to be submitted by AIFMs wishing to

manage EU AIFs established in other EU Member States

In the case of an application by a Maltese AIFM to market

an EU AIF in another EU MS or EEA State, the MFSA shall,

within 20 days of receiving the notification file, transmit

this to the European Regulatory authority of the respective

state, enclosing a statement to the effect that the Maltese

AIFM concerned is authorised to manage European AIFMs

with a particular investment strategy

If the AIF identified is set up in an EU MS or EEA State

other than Malta, the competent authority shall proceed to

inform the European Regulatory Authority of the home MS

or EEA State of the AIF that the Maltese AIFM may start

marketing the units or shares of the said AIF in Malta

The Maltese AIFM may start marketing the European AIF in

the other EU MS or EEA State from the date of notification

by the MFSA to the respective authority

In the case of direct management, the MFSA shall, within

one month of receiving the complete documentation

submitted transmit the complete documentation to the

European regulatory authority of the Maltese AIFM host

MS or EEA State

In the case of the establishment of a branch, the MFSA

shall transmit the complete documentation to the

European regulatory authority of the Maltese AIFM host

MS or EEA State within two months of receiving the

complete documentation.

In each case, the MFSA shall also enclose a statement to

the effect that the Maltese AIFM is licensed in terms of

the Act

Upon receipt of the transmitted notification the Maltese

AIFM may start to provide its services in the host

Member State or EEA State

Specific RequirementsFinancial Resource Requirement

Investment services providers are subject to Capital Adequacy rules on own funds, large exposures, and risk weightings as set out in the EU Capital Requirements Directive.

The components and amount of the Capital Resources Requirements varies according to the category of Licence Holder, the risks to which it is exposed and in certain cases the fixed overhead requirement.

In all cases, the Capital Resources Requirement may not be less then the Initial Capital Requirement applicable to each category, as outlined in the following table:

Licence CategoryMinimum Initial Capital Net Tangible Assets (€)

Category 1A €50,000Category 1B - with PII* €20,000

Category 1B - without PII* €50,000

Category 2 €125,000Category 3 €730,000Category 4a €730,000Category 4b €125,000

* PII – Professional Insurance Indemnity Cover

Supplementary Licence Conditions

The AIF shall obtain the written consent of the MFSA before admitting a General Partner. The request shall be accompanied by a Personal Questionnaire completed by the person proposed or by the Directors and Qualifying Shareholders of the proposed General Partner (in the case of a body corporate). If the corporate General Partner is regulated in a recognised jurisdiction, the request for consent shall include details of the regulatory status of the General Partner.

General Partners shall be persons falling within these categories:

• a company licensed under the Investment Services Act, 1994, for the provision of fund management services

• a company falling within the exemptions applicable to overseas fund managers

• any other entity of sufficient standing and repute as approved by the MFSA

• any other individual who satisfies the fit and proper test

The AIF, or the AIFM or Administrator on behalf of the AIF is required to disclose to potential investors, the identity of the beneficial owners of the General Partner(s) upon request

Supplementary conditions for AIFs established as Limited Partnerships

A special purpose vehicle is:

• set up by the Scheme as part of its investment strategy for the purpose of achieving its investment objectives

• owned or controlled via majority shareholding of the voting shares either directly or indirectly by the Scheme

• having the majority of its directors in common with the Scheme which it set up

SPVs must be established in Malta or in a jurisdiction which is not an FATF Blacklisted country

The AIF shall –through its Directors or General Partner(s) –at all times maintain the majority directorship of any SPV

The AIF shall –through its Directors or General Partner(s) –at all times maintain the majority directorship of any SPV

The AIF shall retain at its Registered Office, a copy of its

written agreements with investors who have committed to invest in

the AIF. Such agreements shall be

available for inspection by MFSA officials during compliance visits. The AIF’s Offering Memorandum

is to include specific risk warnings in relation to the drawdown of

committed funds.Any request on committed funds

shall be effected pro-rata amongst all relevant investors of the AIF. The AIF shall only make a fresh

call for further commitments once all the outstanding commitments from existing investors have been

requested.

If the AIF is set up as a SICAV, units in the scheme

may be issued at a discount to an existing member who has entered into a written

commitment with the SICAV to subscribe for additional shares provided that this is permissible by the scheme’s Memorandum & Articles and

the nature of the discount is disclosed in the Offering

Document.

The value of shares issued at a discount must not be below

the net asset value of the initial shares in the SICAV subscribed

to by that same member.

Reporting Frequency

Licence Category Assets Under Management

Frequency of Reporting

De minimis AIFM Less than €100M AnnualLess than €100M unleveraged with five year lock-up period

Annual

Other AIFM Greater than €100M and less than €1Bn Half-yearly

Greater than €1Bn QuarterlySpecific AIF Reporting

AIF’s greater than €500M

Quarterly

Unleveraged AIF investing in non-listed companies and issuers in order to acquire control

Annual

AIF Reporting Frequency

TaxationTaxationA fund will be treated as a prescribed fund if:

• it is formed in accordance with the laws of Malta;• it declares that the value of its assets situated in Malta amount to at least 85% of the value of the total assets;• it has been so classified by the Maltese Commissioner for Revenue by means of a notice in writing.

A fund which does not satisfy these requirements is classified as non-prescribed.

A fund which invests in cryptocurrencies and distributed ledger technologies is treated the same as any other fund for tax purposes.

Taxation of Funds

Investment income (other than bank interest income)

Bank interest income Income from Immovable Property situated in Malta

Other income of fund

Prescribed Fund 10% finalwithholding tax

15% final withholding tax

15% flat final withholding tax on gross rental income or 35% on net rental income; The transfer of Maltese real estate is generally taxable at 8% on the value of the property transferred

Exempt from tax in Malta

Non-Prescribed fund Exempt from tax in Malta

Exempt from tax in Malta

15% flat final withholding tax on gross rental income or 35% on net rental income; The transfer of Maltese real estate is generally taxable at 8% on the value of the property transferred

Exempt from tax in Malta

Taxation of Funds

• Fund managers and advisors incorporated and tax resident in Malta are subject to Malta’s general system of taxation, subject to tax in Malta on world-wide income, including chargeable capital gains at the standard corporate tax rate of 35%, subject to relief by ordinary credit method for foreign tax suffered.

• A fundamental pillar of Malta’s general tax system is the full imputation system which includes a tax refund system. This system completely eliminates the economic double taxation of company profits whereby shareholders, wherever resident, in receipt of dividends, are entitled to a tax credit equal to the tax borne by the distributing company on the profits out of which the dividends are paid. Since the tax rate of 35% applicable to companies is the highest tax rate in Malta, shareholders do not suffer any additional tax on the receipt of dividends.

• In addition, upon a dividend distribution of taxed profits, the shareholders of a company registered in Malta (i.e. a company resident in Malta or a non-resident company with a branch in Malta) are eligible to claim a partial tax refund of the Malta tax charge of the distributing company, with the exclusion of tax suffered by the distributing company on income derived directly or indirectly from Maltese immovable property. The applicable tax refund for shareholders of fund managers and advisors is generally 6/7ths of the 35% tax, resulting in an effective rate of tax on distributed taxable profits of a maximum of 5%.

• The tax refund system, which has been formally approved by the EU Commission and Code of Conduct group, extends to both resident and non-resident shareholders, and applies to all taxed profits derived from local and foreign sources, with the exclusion of profits derived directly or indirectly from immovable property situated in Malta.

• Tax consolidation rules which were recently introduced in Malta grant the option for group of companies to be treated as a tax group upon complying with certain requirements. This tax grouping enables a cash flow benefit when compared to the current operation of the partial shareholder tax refund mentioned above in that the 35% tax need not be paid and then partially reclaimed; instead the tax group is taxed at the effective tax rate.

• Furthermore, such companies have the option to avail of a Notional Interest Deduction (NID), a deemed interest deduction against their chargeable income, calculated at approximately 7% of risk capital in the company, where risk capital includes share capital, share premium, reserves, interest free loans and other items shown as equity in the financial statements. Depending on the amount of risk capital of the company and the chargeable income for the year, the effective tax rate of the company may be reduced to as low as 3.5%.

Taxation of Fund Managers and advisors

• Participation Exemption: Dividends and gains derived from qualifying participations are fully exempt from tax.

• Capital Gains: The transfer of shares in a resident company by a non-resident is exempt from tax, provided there are no interests in immovable property.

• Stamp duty: No transfer taxes like stamp duty on share transfers by non-residents involving international business companies.

• Capital taxes: Malta has no net worth net or similar taxes on capital.

• Withholding Taxes: Malta does not impose any withholding taxes on interest, royalties, dividends and proceeds from liquidation.

• Double taxation agreements (DTAs): Successive Maltese governments have sought to conclude DTAs with important trading partners, as well as with emerging countries. The 78-strong treaty network is expected to grow further in the coming years.

• Malta is compliant with international tax standards:

• Malta is a member of the OECD Base Erosion and Profit Shifting (BEPS) Inclusive Framework and is fully co-operative in the international initiative against tax evasion. Malta fully applies EU law and all OECD initiatives on combatting tax evasion, including the directives on mutual assistance between tax authorities, automatic exchange of information, beneficial ownership register, as well as the exchange of tax rulings and advance pricing arrangements in the transfer pricing field.

• Malta was also an early adopter of the Common Reporting Standard and Country-by-Country reporting obligations.

• Malta is effectively implementing the requirements of the OECD BEPS standards into its tax system through the transposition of the EU tax directives (various anti-tax avoidance measures have been transposed into Maltese tax law through the Anti-Tax Avoidance Directive and mandatory disclosure rules for tax intermediaries and tax payers, in addition to the above measures), as well as through the adoption of international instruments, including the Multilateral Instrument to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting.

Other Tax matters

• Malta has a value added tax (VAT) system modelled on the EU VAT Directive.

• The standard rate in Malta is 18%.

• Supplies by funds are exempt without credit. This means that any VAT charged to the fund by other service providers (such as auditors and lawyers) will be a sunk cost to the fund.

• Funds may be required to be registered for VAT in Malta if they procure services from outside Malta which are subject to VAT.

• The supply of services consisting of the management of collective investment is exempt without credit, provided that these services are limited to those acts that are specific to and essential to the core activity of the scheme. This is interpreted as including administration of the fund and services related to investment selection whether provided by a fund manager, administrator or a third party service provider.

• No VAT is charged on the supplies made by a fund manager or fund administrator if the services are specific to and essential to the core activity of the fund.

Value Added Tax

• Malta operates an attractive expatriate taxation regime. Individuals who are resident but not domiciled in Malta are subject to tax on Maltese source income (employment income for work carried out in Malta) and capital gains, and foreign source income, only to the extent that the latter income is received or remitted to Malta.

• In order to attract top professionals, Malta introduced a Highly Qualified Persons scheme which allows eligible persons, namely resident non-domiciled individuals occupying eligible offices in the financial services sector, including employment with funds and fund management companies, to apply a reduced 15% income tax rate to their salary for an eligibility period, provided that such income, excluding the value of any fringe benefits, amounts to at least €84,991 for 2019, as adjusted annually for inflation.

• Furthermore, no tax would be charged on qualifying income exceeding €5,000,000 earned during the eligibility period.

• Eligible offices in the financial services sector include positions such as Chief Executive Officer, Chief Operations Officer, Chief Financial Officer, Chief Risk Officer, Chief Investment Officer, Portfolio Manager, Senior Trader, Head of Marketing, Head of Investor Relations.

• A number of conditions must be satisfied in order to be eligible for the flat tax rate, which include amongst others that the income must arise from a qualifying contract of employment; the person must not be domiciled in Malta; the person must have health insurance in respect of all risks for himself/herself and the members of his/her family; and the person may not have received any other benefit or arrangement in terms of business incentive laws.

• Alternatively, expatriates employed within the fund sector may benefit from 10-year exemption on the taxation of certain fringe benefits, including relocation expenses, accommodation expenses and a monthly subvention of €600 per month.

Expatriates

Appendices Appendix 1:

Comparison between Fund Jurisdictions

Comparison of Malta with other Fund

Jurisdictions

Comparing Malta with other jurisdictions -

Taxation

Applicable Taxes at Fund level

Malta:

• Exempt from Income and capital gains for non- prescribed funds

• No withholding tax on Distributions made to foreign investors

Stamp Duty Applicability: No stamp duty payable on the transfer of securities by/to a fund licensed under the Malta Financial Services Act

Ireland:

• Income and capital gains – Exempt

• Distributions made to non- resident or exempt Irish resident investors – No withholding tax

• No net asset tax

Stamp Duty Applicability: duty payable on issue / transfer / redemption / repurchase of fund units or on transfer of non-Irish stocks / marketable securities

Luxembourg:

• Income and capital gains – Exempt

• Distributions made to investors – No withholding tax

• Annual subscription tax between 0.01% and 0.05% of Net Asset Value and a fixed fee on capital duty of €1,250

Stamp Duty Applicability: No stamp duty or capital duty

Double taxation treaties

78

73

83

Number of international administrators

Number of custodians

Number of law firms

Malta

26 16640 +

Number of audit firms

Ireland Luxembourg

26 16640 +

13 9320 +

70 5971

35 9181

Comparing Malta with other jurisdictions -

Regulation

Malta:

Different Fund types available: SICAV, INVCO, Unit Trust, Contractual Fund, Limited Partnership, Incorporated Cell Company, Private Funds

Types of regulated Funds:• UCITS Funds • Professional Investor Funds (PIFs)• Alternative Investment Funds (AIFs)• Notified AIFs

• Retail AIFs

Re- domiciliation Possibility: Possible

Funds exempt from regulation: Private CISs - whose number of participants is 15 or less and the scheme is private and does not qualify as a PIF

Exempt CISs - As scheme where the participants carry on a business not related to investment services but enter in the scheme for business purposes

A scheme established for a company’s (former) employees and their dependants in instruments issued by the same company / approved by the authority

A commercial scheme in respect of which profits, income and the contribution of the participants are pooled or a scheme which operates according to the principle of risk spreading

Ireland:

Different Fund types available: Unit Trust, Investment Limited Partnership, Investment Company, Common Contractual Fund, ICAV

Types of regulated Funds:Authorized investment funds in Ireland are established as either UCITS or AIFs

UCITS Funds•Exchange Traded Funds (ETFs)•Money Market Funds (MMFs)

Alternative Investment Funds•Qualifying Investor AIF (QIAIF)•Retail Investor AIF (RIAIF)

• Retail AIFs

Re- domiciliation Possibility: Possible

Funds exempt from regulation: Yes. This may happen in the case of funds relating to certain investors which are exempt.

Luxembourg:

Different Fund types available: Investment Company (SICAV), Common Fund (FCP)

Types of regulated Funds:UCITS Funds•Specialized Investment Funds•Part II UCIs•SICARs

Re- domiciliation Possibility: Possible

Funds exempt from regulation: No

Comparing Malta with other jurisdictions -

Set up Fees

Malta:

Notary fees: N/A

Regulatory fees: Collective Investment schemes:Application Fee: Scheme - €2,000 + an additional fee (€1,000 per sub-fund)Supervisory Fee: Scheme - €2,000 p.a. + an additional fee (€600) per sub- fund p.a.

Professional Investor Funds (PIFs): In principal approval - €600Scheme: €1,500 Additional Sub-funds: €1,000

Supervisory Fee: €1,500 per scheme €500 per sub-Fund

Stock Exchange fees: Admission fee for the listing of the CIS: €1,200Annual admission fees: Annual fee: €1,200First 5 sub- funds: Application fee: €1,200 (per sub-fund)6th – 10th sub- fund: Annual fee: €1,000 (per sub-fund)11th – 15th sub- fund: Annual fee: €730 (per sub fund)

Thereafter Annual fee: €500 (per sub fund)

Ireland:

Notary fees: N/A

Regulatory fees: €5,000 -

Stock Exchange fees: Administration fee €300Formal Notice fee €550Closed ended funds: Initial fee: EU €1,000Non-EU €1,000

Subsequent fee: EU €500, Non-EU €500

Annual Fees: Up to 5 sub- funds: EU: €1,900, Non-EU: €1980 (per sub- fund)6 - 10 sub-funds: EU €1,150, Non-EU €1,200 (per sub-fund)Over 11 sub-funds EU: 760, Non-EU : 800 (per sub-fund)

Ireland:

Notary fees: For a fund organized under a corporate form, the notary fee is €2,500 – €5,000

Regulatory fees: Initial Fee: €2,650 - €5,000Annual Fee: €2,650 - €5,000

Stock Exchange fees: Fees for EU CIS Approval fee €1250Listing fee €1250

Maintenance fees 1st line: €1,8752nd line: €1,2503rd line: €875Subsequent lines:€500

Fees for Non EU CIS

Approval fee €2500Listing fee €2500

Maintenance fees1st line: €2,5002nd line: €1,8753rd line: €1250Subsequent lines:€625

Appendix 2:

Living in Malta

Health Care

Safety

Transport

Based on the British National Health Service model, the system in Malta is further boosted by a strong element of private health care for those who choose to go down this route. The overall quality of care is of the highest order and foreign residents draw comfort from the fact that all health care workers are very fluent in English, ensuring that communication between provider and patient is very straightforward.

Malta is one of the safest countries worldwide, having been recently ranked as the seventh safest small country globally. It is a country where one’s children can still go off with their friends for a day at the beach without any undue concerns on the part of their guardians. Violent, random crime is a rarity, leading to noticeably diminished levels of tension.

Domestically the country is served by an extensive road network, covering all parts of the island, with a regular ferry service to the neighbouring island of Gozo. Most Maltese are private car owners although a reliable public transport service consisting of buses and taxis means that car ownership is not strictly necessary. Indeed, most foreign residents staying in Malta for relatively short periods make use of the public transport option. Internationally, regular, daily flights to important European and Middle-Eastern hubs as well as fast ferry services to mainland Europe mean that one is never more than a few hours away from one’s destination. Cargo services, both inbound and outbound, are catered for by an extensive network of both air and sea routes which connect the island to the rest of the world via its airport and the Malta Freeport, which is the third largest in the Mediterranean, handling in excess of 3 million units per annum.

The Maltese Climate

Cultural and social life

Education

• The Maltese islands benefit from 3,000 hours of sunshine during the year.

• Annual rainfall is quite low, with an average of 700mm of rain annually

The Maltese islands enjoy a pleasant, temperate climate, characterised by long, dry summers, with cooling sea breezes, followed by short, wet winters. Temperatures rarely dip below 5 degrees centigrade in winter, while summer peak temperatures hover around the low thirties. Snow is unheard of and outdoor activities are possible throughout the year.

Albeit a tiny country, Malta’s location at the centre of the Mediterranean has endowed it with a rich cultural heritage one would normally expect to find in much larger, more historically dominant states. The various empires and cultures which colonised the island all left their mark, resulting in a vibrant, eclectic mix just waiting to be discovered by visitors. Enhanced by the country’s compact size and the mild climate, opportunities for leisure activities are varied and numerous. From scuba diving, rock climbing and various other outdoor sports for the more adventurous, to a wide range of cultural activities such as concerts, theatre productions and outdoor festivals spread throughout the calendar, there is little time for one to get bored in this small, but vibrant island state.

Malta has a well-established educational system, based on the UK model, a reflection of the many years spent as part of the British Empire. Nowadays, one finds a mixture of state and private schools, providing qualifications up to post-graduate level, all fully recognised on an international level. International students fit in seamlessly into a system geared to meeting their needs.

Follow KPMG in Malta:

© 2020 KPMG, a Maltese civil partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.The KPMG name, logo and ‘cutting through complexity’ are registered trademarks or trademarks of KPMG International Cooperative (KPMG International).

Alex AzzopardiDirector Risk Consulting Advisory Services+356 2563 [email protected]

Kristina Mifsud BonniciManager Risk Consulting Advisory Services+356 2563 [email protected]

Juanita BrockdorffPartner Tax Services+356 2563 [email protected]

Noel MizziPartner Audit Services+356 2563 [email protected]

Lisa Zarb MizziDirector Tax Services+356 2563 [email protected]