altas FINAL(1)

22

BALANCE SHEET AS AT JUNE 30, 2010 2010 2010 ASSETS in 000 EQUITY AND LIABILITIES in 000 NON CURRENT ASSETS CAPITAL AND RESERVES 756,339 Authorised Capital - 100,000 Long term deposits 517 Long term loans 270 83,911 757,126 General reserves 375,500 CURRENT ASSETS Unappropriated profit 224,743 22,413 684,154 Stock-in-trade 531,597 Trade debts 100,396 Loans and advances 2,350 - leasehold land 173,786 Deposits and prepayments 5,928 NON CURRENT LIABILITIES Investments 26,224 Deferred liabilities 111,246 Accrued mark-up / interest 195CURRENT LIABILITIES Other receivables - Trade and other payables 368,911 Sales tax - net 31,050 Accrued mark-up / interest 1,245 Advance tax - net 6,792 Short term borrowing - secured 174,598 Cash and bank balances 29,869 Provision for taxation - net - 756,814 544,754 OTHER INFORMATIONS Depereciation charge 54,226,000 Common share outstanding 83,911,000 INVESTOR INFORMATION Earning Per Share 26.52 Market Price Per Share 185.13 Book Value Per Share 81.53 Cash flow per share 3 Property, plant and Investments - Available for 10,000,000 ordinary shares of 10 each Issued, subscribed and paid up capital 8,391,094 ordinary shares of 10 each Stores, spares and loose SURPLUS ON REVALUATION OF PROPERTY, PLANT AND EQUIPMENT 1,513,94 0 1,513,94 0

-

Upload

abeer-m-pirzada -

Category

Documents

-

view

217 -

download

0

Transcript of altas FINAL(1)

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 1/22

BALANCE SHEET

AS AT JUNE 30, 2010

2010 2010

ASSETS in 000 EQUITY AND LIABILITIES in 000

NON CURRENT ASSETS CAPITAL AND RESERVES

756,339 Authorised Capital

- 100,000Long term deposits 517

Long term loans 270 83,911757,126 General reserves 375,500

CURRENT ASSETS Unappropriated profit 224,743

22,413 684,154

Stock-in-trade 531,597

Trade debts 100,396

Loans and advances 2,350 - leasehold land 173,786

Deposits and prepayments 5,928 NON CURRENT LIABILITIESInvestments 26,224 Deferred liabilities 111,246

Accrued mark-up / interest 195CURRENT LIABILITIES

Other receivables - Trade and other payables 368,911

Sales tax - net 31,050 Accrued mark-up / interest 1,245

Advance tax - net 6,792 Short term borrowing - secured 174,598

Cash and bank balances 29,869 Provision for taxation - net -

756,814 544,754

OTHER INFORMATIONS

Depereciation charge 54,226,000

Common share outstanding 83,911,000

INVESTOR INFORMATION

Earning Per Share 26.52

Market Price Per Share 185.13

Book Value Per Share 81.53

Cash flow per share 3

Property, plant and

Investments - Available for 10,000,000 ordinary shares of 10eachIssued, subscribed and paid upcapital8,391,094 ordinary shares of 10each

Stores, spares and loose

SURPLUS ON REVALUATION OFPROPERTY, PLANT AND EQUIPMENT

1,513,94

0

1,513,940

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 2/22

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 3/22

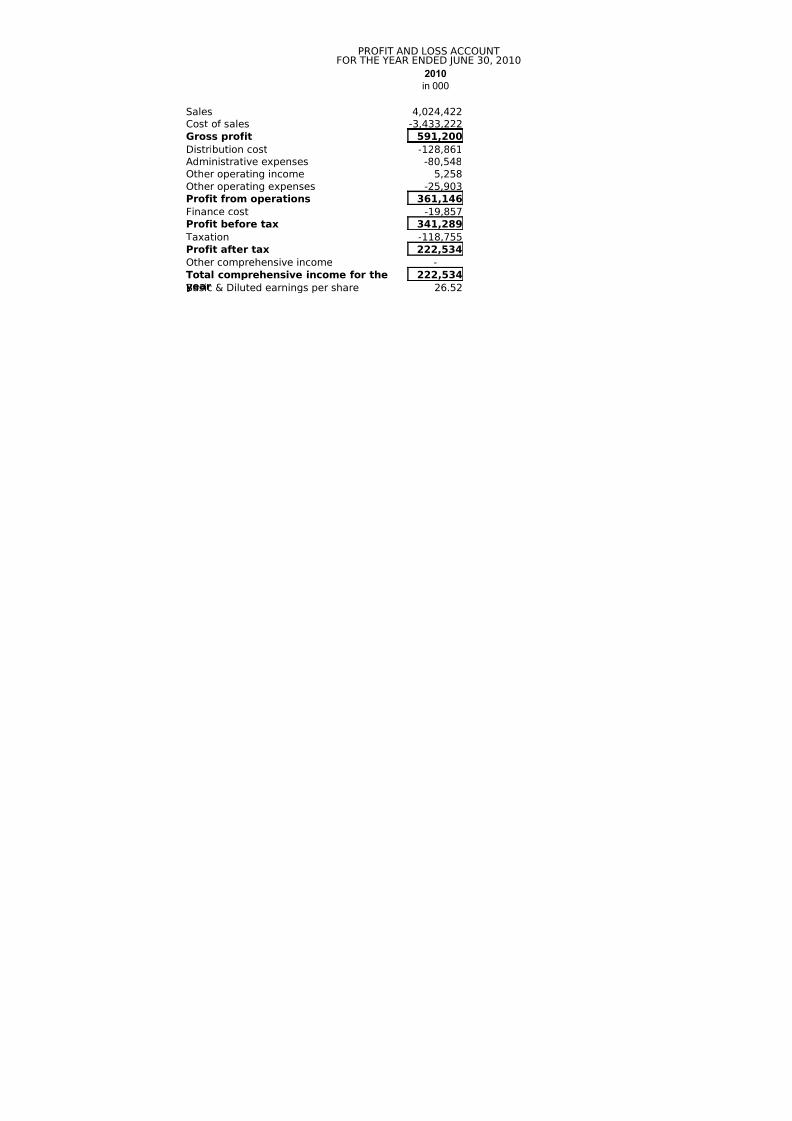

PROFIT AND LOSS ACCOUNTFOR THE YEAR ENDED JUNE 30, 2010

2010

in 000

Sales 4,024,422

Cost of sales -3,433,222Gross profit 591,200

Distribution cost -128,861

Administrative expenses -80,548

Other operating income 5,258

Other operating expenses -25,903

Profit from operations 361,146

Finance cost -19,857

Profit before tax 341,289

Taxation -118,755

Profit after tax 222,534Other comprehensive income -

222,534

Basic & Diluted earnings per share 26.52

Total comprehensive income for theyear

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 4/22

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 5/22

CASH FLOW STATEMENTFOR THE YEAR ENDED JUNE 30, 2010

2010

in 000

CASH FLOWS FROM OPERATING ACTIVITIES 190,487CASH FLOWS FROM INVESTING ACTIVITIES 406,363

Fixed capital expenditure -177,831

Investments acquired -210,700

2,867

Proceeds from disposal of investments 194,227

Cash used in investing activities -191,437

Net cash flow before financing activities -950

FINANCING ACTIVITIES

Increase / (decrease) in short term borrowing 70,982

Dividend paid -69,055Net cash generated / (used) from financing activities 1,927

Increase/(decrease) / in cash & cash equivalent 977

28,892

Cash and cash equivalent as at June 30 29,869

Proceeds from disposal of property, plant and

Cash and cash equivalent as at the beginning of the

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 6/22

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 7/22

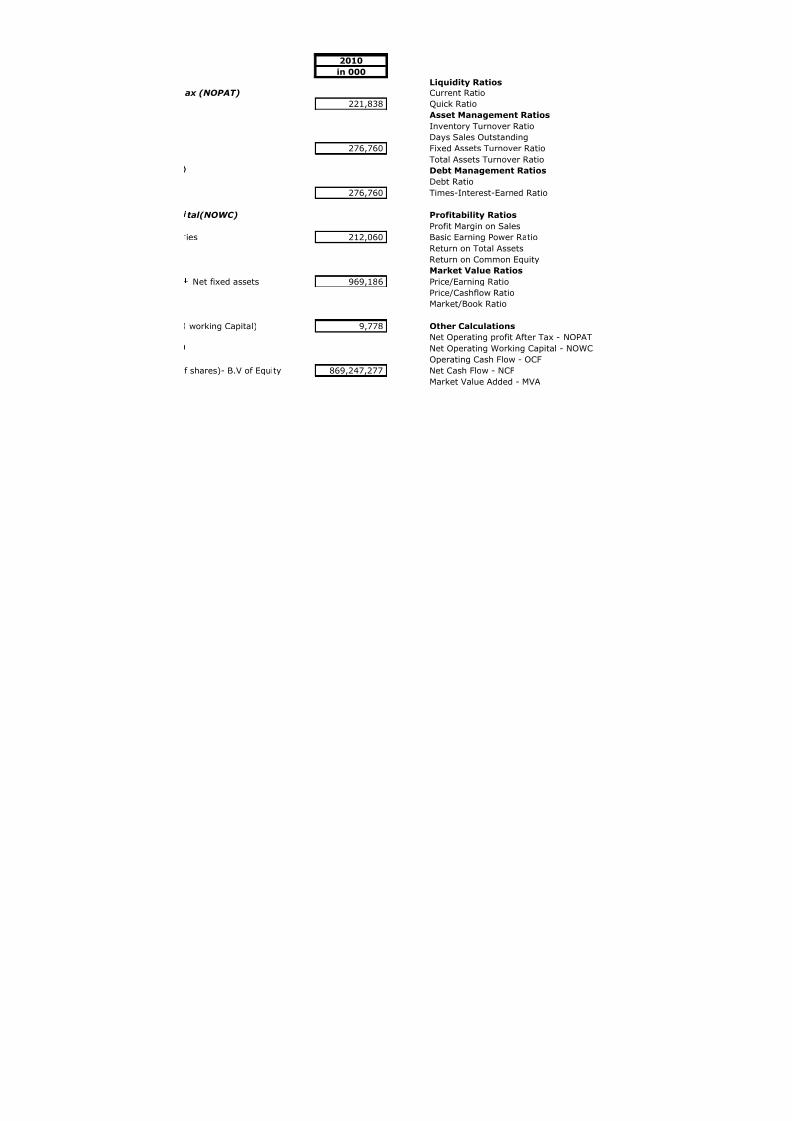

2010

in "000"

Liquidity Ratios

Current Ratio:

Current Assets 756,814

Current Liabilities 544,7541.39

Quick Ratio:

Current Assets - Inventories 225,217

Current Liabilities 544,754

0.41

Asset Management Ratio

Inventory Turn over Ratio:

Sales 4,024,422

inventories 531,597

7.57Days Sales Outstanding:

Account Receivable 100,396

Annual sales/365 11025.81

9.11

Fixed Assets Turn over Ratio:

Sales 4,024,422

Net fixed assets 757,126

5.32

Total Assets Turn over Ratio:

Sales 4,024,422

Total Assets 1,513,940

2.66

Debt Management Ratio

Debt Ratio:

Total Debt 100,396

Total Assets 1,513,940

6.6%

Time Interest Earned Ratio:

EBIT 341,289

Interest Charges 19,857

17.19

DU Pont Equation

Net Income 222,534

Equity 684,154

0.33

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 8/22

2010

in "000"

Profitability Ratios

Profitability Margin on Sales: Net operating profit after t

Net income 222,534 NOPAT = EBIT ( 1 - tax)

Sales 4,024,422

% 5.5% Net Cash Flow (NCF)Basic Earning Power Ratio:

EBIT 361,146 Net income + Depreciation

Total Assets 1,513,940

% 23.9% Operating Cash Flow (OCF)

Return on Total Assets:

Net income 222,534 NOPAT+ depreciation

Total Assets 756,814

% 29.4% Net operating working cap

Return on Common Equity:

Net income 222,534 Current assets-Current Laibilit

Common Equity 83,911% 265.2% Operating Capital (OC)

Market Value Ratios

Price Earning Ratio: Net operating working capital

Price Per Share 185.13

Earnings Per Share 26.52 Free Cash Flow (FCF)

(Times) 6.98

Price/Cash flow Ratio: NOPAT- ( Change in operating

Price Per Share 185.13

Cash flow per share 3.30 Market Value Added (MVA)

56.13

Market Book Ratio: ( Market price per share* # o

Market Price Per Share 185.13

Book Value Per Share 81.53

(Times) 2.27

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 9/22

2010

in 000

Liquidity Ratios

ax (NOPAT) Current Ratio

221,838 Quick Ratio

Asset Management Ratios

Inventory Turnover RatioDays Sales Outstanding

276,760 Fixed Assets Turnover Ratio

Total Assets Turnover Ratio

Debt Management Ratios

Debt Ratio

276,760 Times-Interest-Earned Ratio

tal(NOWC) Profitability Ratios

Profit Margin on Sales

ies 212,060 Basic Earning Power Ratio

Return on Total AssetsReturn on Common Equity

Market Value Ratios

Net fixed assets 969,186 Price/Earning Ratio

Price/Cashflow Ratio

Market/Book Ratio

working Capital) 9,778 Other Calculations

Net Operating profit After Tax - NOPAT

Net Operating Working Capital - NOWC

Operating Cash Flow - OCF

f shares)- B.V of Equity 869,247,277 Net Cash Flow - NCF

Market Value Added - MVA

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 10/22

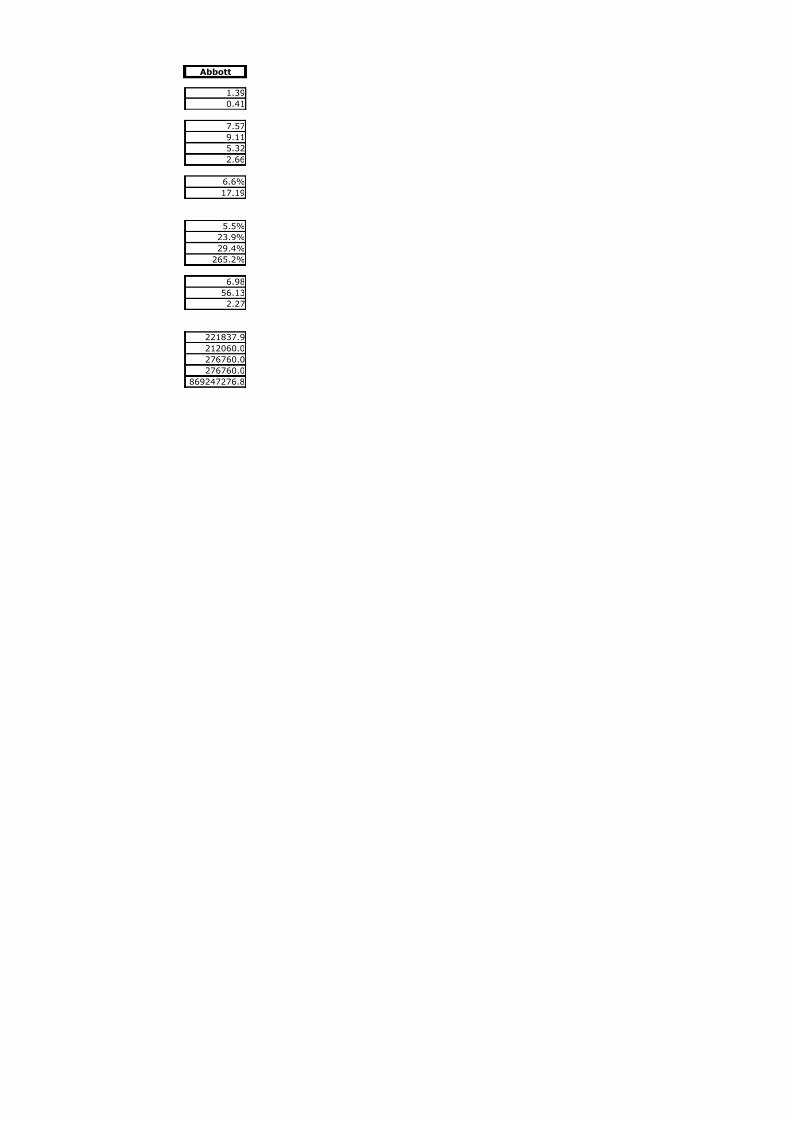

Abbott

1.39

0.41

7.579.11

5.32

2.66

6.6%

17.19

5.5%

23.9%

29.4%265.2%

6.98

56.13

2.27

221837.9

212060.0

276760.0

276760.0

869247276.8

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 11/22

Part I Dividend Growth Model

=

Po 185.13

working

2006 2007 2008 2009

total dividend distributed 11290000 15669000 36046000 51671000

total number of shares 52874000 60805000 69926000 69926000

dividend per share 0.21 0.26 0.52 0.74

Year sales difference growth in sales net profit

2006 1209033000 41323000

2007 1585648000 376615000 31.15% 87510000

2008 2628820000 1043172000 65.79% 106797000

2009 3156807000 527987000 20.08% 177678000

2010 4024422000 867615000 27.48% 222534000

Average Growth (g) 36.13%

Year EPS difference growth in EPS

2006 7.82

2007 14.39 6.57 84.02%

2008 15.27 0.88 6.12%

2009 25.41 10.14 66.40%

2010 26.52 1.11 4.37%

Average Growth 40.23%

I have selected the growth with repsect to sales

Overall Po with respect to average growth and dividend as per 2010.

Ks= 36.73%

The corporate Value Model

Do(1+g)/K

s-g

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 12/22

Part II FCF/(1+WACC)

164729173.47

working for free cash flow

EBIT NOPAT Current Assets Current Liabilities Ne

2003 818000000 531700000

2004 1080000000 702000000

2005 1366000000 887900000

2006 1440000000 936000000

2007 1744197000 1133728050 3129129000 881681000

2008 544822000 354134300 3421308000 1346771000

Dividend Yield Capital G

Part III 0.61%

Working

1.12

Total Return (Ks) = Dividend yield+Capital gain yield

0.72%+10.57%

36.73%

Vcompany

Dividend Yield = D1/P

0Capital Gain Yie

D1 = D0 (1+g)1 P1 = P0 (1+g)

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 13/22

WACC Book Value WACC Market Value

0 + 36.73188255498390% 0 +

WACC= 36.73% WACC= 36.73%

working Book Value Working Market Value

2010

Kd Kd

Kp Kp

Ks 36.73% Ks

% age of total

long term debt Wd 0 0.00% long term debt Wd

commmon stock Wc 83911000 100.00% Common Stock (market Value) W1

total 83911000

W1

No of Shares 8

Po

market value of Wc

WACC = wdk

d(1-T) + w

pk

p+ w

ck

sWACC = w

dk

d(1-T) + w

pk

p+ w

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 14/22

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 15/22

Cost 50,000,000

Shipping 1,000,000

Installation 3,000,000

Total cost 54,000,000

Life (Years) 10

Market Value 1,000,000

Annual sales 50,000

Price / Unit 2,000

Cost / Unit 1,200

NOWC 29.4%

Tax 39%

WACC 36.73%

Growth / Year 40.23%

0 1

Units sold 50,000

Unit price 2,000

Unit cost (1,200)

sales 100,000,000

costs (60,000,000)

NOWC (29,400,000) (11,827,620)Depreciation (5,400,000)

EBIT 22,772,380

Tax @ 39% (8,881,228)

NOPAT 13,891,152

NOCF 19,291,152

Salvage

Capital G / L

Tax on salvageNet CF -

Terminal CF (83,400,000) 19,291,152

Incremental CF (64,108,848)

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 16/22

NPV 115,799,302

IRR 55%

MIRR 47%

n the basis of these values of NPV and IRR the pr

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 17/22

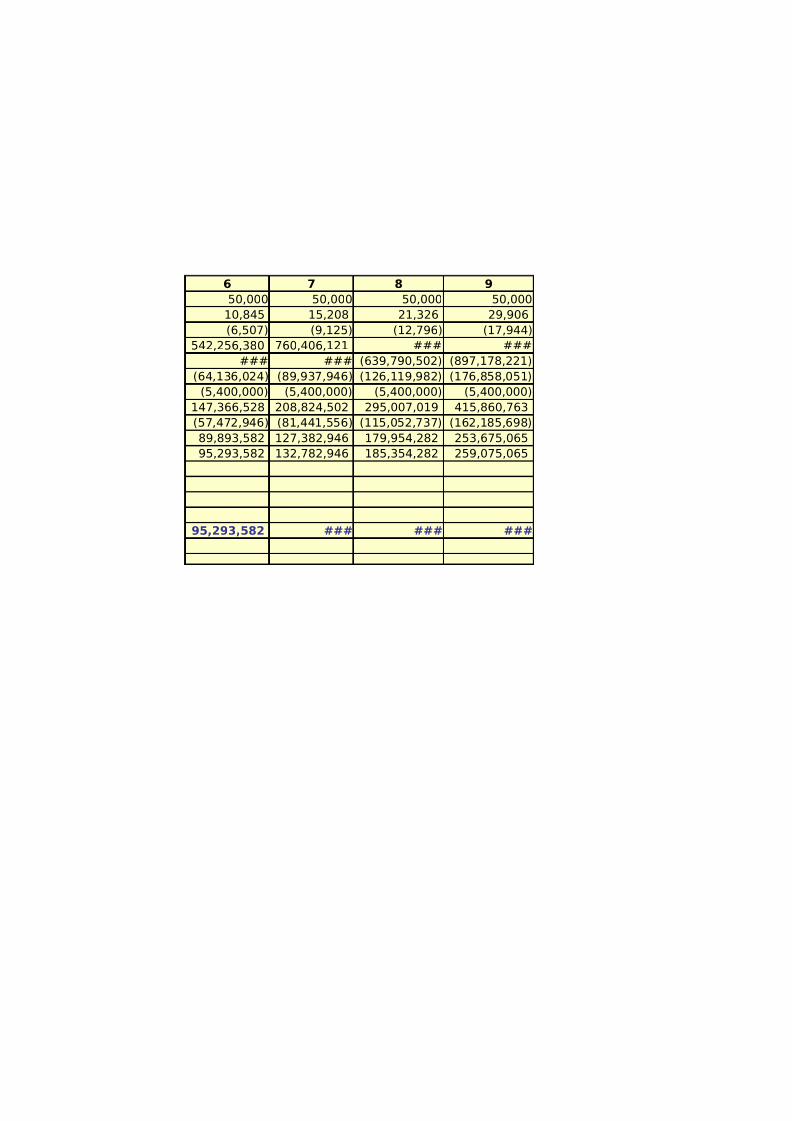

5,400,000

(straight line)

2 3 4 5

50,000 50,000 50,000 50,000

2,805 3,933 5,515 7,734

(1,683) (2,360) (3,309) (4,640)

140,230,000 196,644,529 275,754,623 386,690,708

(84,138,000) (117,986,717) ### ###

(16,585,872) (23,258,368) (32,615,209) (45,736,308)(5,400,000) (5,400,000) (5,400,000) (5,400,000)

34,106,128 49,999,444 72,286,640 103,539,976

(13,301,390) (19,499,783) (28,191,790) (40,380,591)

20,804,738 30,499,661 44,094,851 63,159,385

26,204,738 35,899,661 49,494,851 68,559,385

-

26,204,738 35,899,661 49,494,851 68,559,385

(37,904,110)

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 18/22

ject should be accepted as NPV is positive and the IRR is also

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 19/22

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 20/22

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 21/22

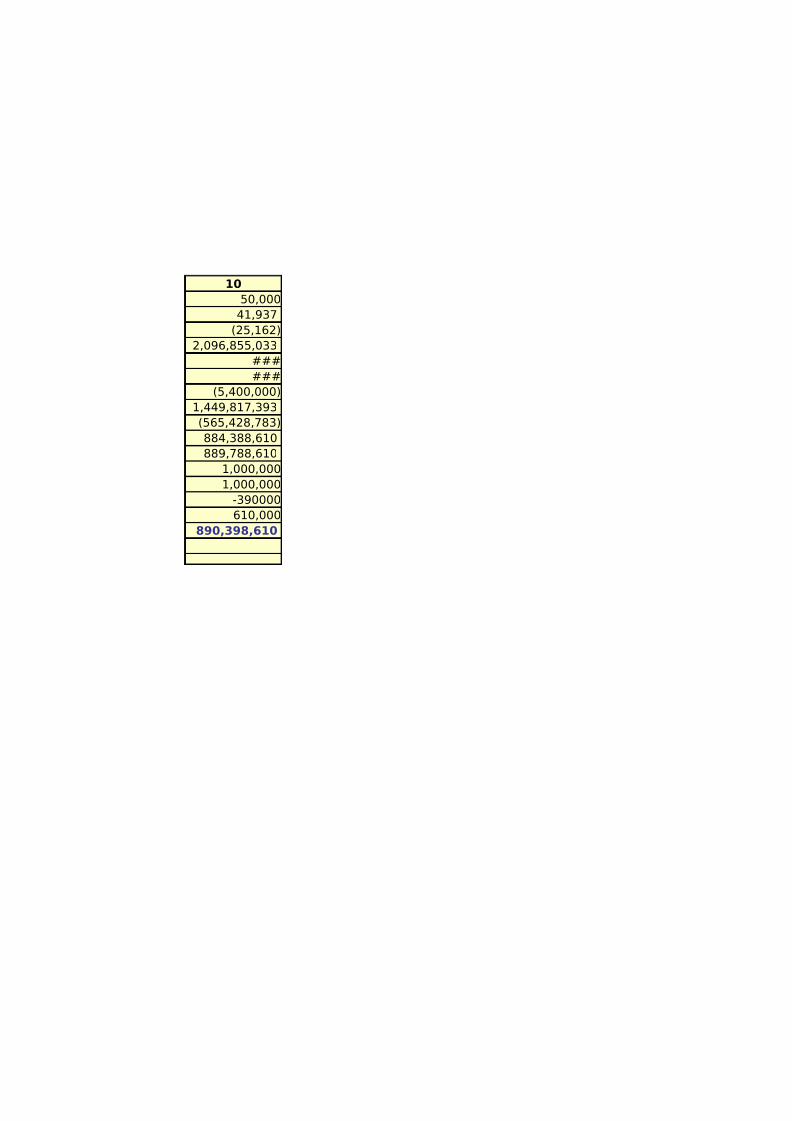

10

50,000

41,937

(25,162)

2,096,855,033

###

###(5,400,000)

1,449,817,393

(565,428,783)

884,388,610

889,788,610

1,000,000

1,000,000

-390000610,000

890,398,610

8/8/2019 altas FINAL(1)

http://slidepdf.com/reader/full/altas-final1 22/22