ALSTOM Switzerland Supplementary Insurance Plan Switzerland Supplementary Insurance Plan Rules, ......

34

ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition incorporating addendum no.1

Transcript of ALSTOM Switzerland Supplementary Insurance Plan Switzerland Supplementary Insurance Plan Rules, ......

ALSTOM Switzerland Supplementary Insurance Plan

Rules, 2010 editionincorporating addendum no.1

3ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

Contents

Paragraph Page

A General provisions

Name and purpose 1 5Definitions 2 5Membership 3 6Beginning and termination of insurance coverage 4 6Insured portion of salary 5 7Savings capital and savings credits 6 7

B Benefits provided by the Plan

Retirement benefitsPension/savings capital 7 8Pensioner’s child benefit 8 9

Benefits upon disabilityDisability pension 9 10Disabled person’s child benefit 10 11

Death benefitsSpouse’s pension, lump-sum payment 11 11Partner’s pension, lump-sum payment 12 12Orphans’ pension 13 13Death benefit 14 13

Additional benefitsVested benefit 15 14Payment of pensions 16 14Cost-of-living adjustment to benefits 17 15Overinsurance and reduction of benefits 18 15Promotion of home ownership 19 16

4 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

Contents

Paragraph Page

C Funding

Obligation to contribute 20 17Amount of contributions 21 17Personal payments 22 17Assets, financial equilibrium and segregated funds 23 20

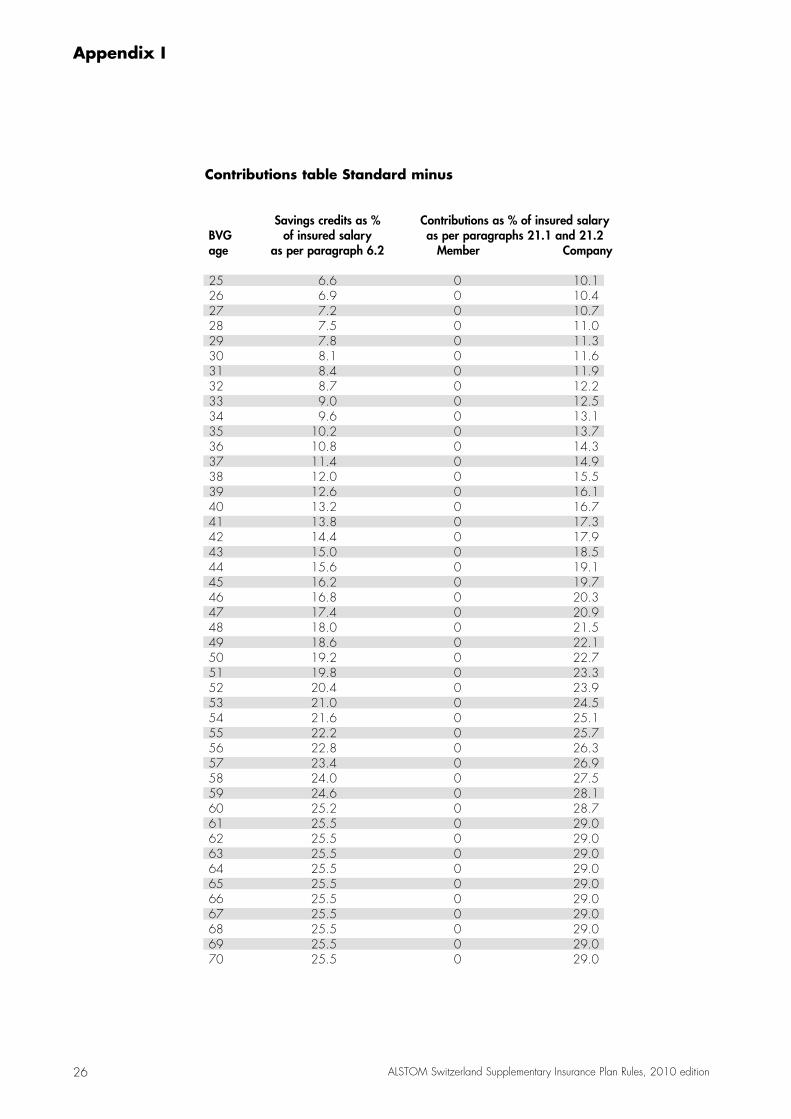

D Organisation and administration

Board of Trustees 24 20Administration of the Plan 25 21Information and disclosure obligation 26 21

E Concluding provisions

Legal recourse 27 22Loopholes in the Rules 28 22Partial or total liquidation 29 22Changes/entry into force 30 23

Appendix I: Contributions tables 24

Appendix II: Buy-in table 27

Appendix III: Buy-in plan for countering pensionreductions on early retirement 28

Addendum no. 1 29

Insured salary component 5 29Pension/savings capital 7 29

Alphabetical list of terms and concepts 30

5ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

A General provisions

1 Name and purpose

1.1 Under the name ALSTOM Switzerland Supplementary Insurance Plan, a foundation exists within the context of art. 80 ff of the Swiss Civil Code.

1.2 The purpose of the foundation (hereinafter, the “Plan”) is to provide against the economic consequences of old age, death or disability for the employees(and their dependents and survivors) of ALSTOM (Switzerland) Ltd as well as those of any economically or financially associated companies affiliated to the Plan via relevant contract.

2 Definitions

2.1 The pronouns “he”, “she” and the inflections thereof as they appear in theseSupplementary Insurance Plan Rules (the “Rules”) refer equally to persons of theother sex.

2.2 Within the scope of these Rules, the following definitions apply:

a) Foundation: The ALSTOM Switzerland Supplementary Insurance Plan in Baden(i.e. the “Plan”)

b) Company: ALSTOM (Switzerland) Ltd as well as all companies and institutionsaffiliated with the Plan

c) Members: All employees of the company who are insured in accordance withthese Rules

d) Age of retirement: Age at the time the member takes retirement

e) Statutory retirement age: First day of the month after completion of one’s 65th year of age

f) BVG: Federal Law on Occupational Retirement, Survivors’ and DisabilityBenefit Plans

g) BVG age: The age represented by the difference between the current calendaryear and the year of birth

h) Children entitled to a pension: Children up to the completed 18th year of age or, if they are still in formal schooling or have been declared to be at minimum 70% disabled, up to the completed 25th year of age. Foster children who are supported by the member are treated equally in this regard

i) Registered partnership: Members living in a registered partnership as per art. 2 of the Federal Law on Registered Partnerships of Same-Sex Couples of18 June 2004 (Partnership Law) are placed on a par with married membersin respect of the rights and obligations deriving from these Rules.To make for easier reading, these Rules refer to married members and tospouses. This is deemed to include persons living in a registered partnership

6 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

A General provisions

3 Membership

3.1 Membership in the Plan is mandatory for those employees whose incomeexceeds the income limit as per paragraph 5.1.

3.2 Not accepted as members are those employees:

a) who do not (or will foreseeably not continuously) work in Switzerland and are sufficiently insured abroad, provided that they apply for exemption fromjoining the Plan

b) who, upon entering into the employment relationship, have exceeded the statutory retirement age or

c) who have been declared to be at minimum 70% disabled

3.3 If pensioners are rehired as employees of the company, they must rejoin the Planas full-paying members; paragraphs 3.1 and 3.2 remain reserved.

3.4 Employees who, upon admittance to the Plan, are partially unfit to work will be insured only to the degree that corresponds to their ability to work.

3.5 Employees who leave the company may remain in the Plan for as long as they are not enrolled in a new employer’s pension scheme. It is then mandatoryfor contributions to be paid by direct debit. If contributions remain unpaid for 2 months, insurance coverage shall cease and the vested benefit will becomepayable.

The new employer must be in agreement with given individual’s remaining in thePlan. In all cases, specific agreements are to be reached with regard to thefuture structure of the insurance relationship.

4 Beginning and termination of insurance coverage

4.1 Membership commences when the conditions of paragraphs 3.1 and 5.1 aresatisfied, but not earlier than the BVG age of 25.

4.2 Insurance coverage ceases at the time the employment relationship ends, pro -vided that no claims for retirement or disability benefits exist or if coverage is tocontinue within the context of paragraph 3.5. Insurance coverage against therisks of death and disability continues for 1 month subsequent to the end of theemployment relationship, provided that the departing individual has not alreadyentered into a new pension arrangement.

7ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

A General provisions

5 Insured portion of salary

5.1 Deemed to be the insured portion of salary is that part of a member’s income in excess of the income limit defined by the Board of Trustees. The companydecides what is considered to be income in this regard.

Remuneration for work done for companies that are not affiliated to the PensionFund cannot be counted towards the relevant annual salary.

5.2 The income limit and the maximum insured portion of salary are reviewed annually by the Board of Trustees, and adjusted as necessary.

5.3 If the salary of a member is reduced for reasons other than partial disability, with the agreement of the company the previous insured portion of salary mayremain unchanged, provided that contributions pursuant to paragraphs 21.1 and 21.2 continue to be paid as before.

5.4 If the income limit is increased without a corresponding rise in income, theinsured portion of the salary will be reduced. If, as a result of an increase in theincome limit, there is no longer any insured portion of salary, insurance coveragewill be suspended, whereas existing savings capital will continue to accrue inaccordance with paragraphs 6.3 and 6.4.

6 Savings capital and savings credits

6.1 A personal retirement account is administered for each member. The savings capital consists of:

a) the credited contributions plus interest

b) the accumulated savings credits plus interest

c) the savings credits for the current year

d) less withdrawals including the related interest

6.2 Annual savings credits are calculated on the basis of the insured salary and theage of the member in accordance with one of the contributions tables included inAppendix I.

6.3 The rate of interest is determined annually by the Board of Trustees. It may alsobe set to zero.

6.4 Provided the annual financial statements show a surplus and the financial situa-tion of the Supplementary Insurance Plan permits, every year at year-end theBoard of Trustees decides the amount of any interest bonus payable. This interestbonus ist credited to the retirement accounts as of 31 December of the relevantyear. Entitled to receive such bonus are employees who were members of thePlan on 31 December of the relevant year. Members who left during that yearhave no entitlement to any such interest bonus.

Calculation of the interest and interest bonus is based on:

a) the declared sum of savings capital in the Plan as at 1 January of the relevantyear

b) the time and amount of contributions credited during the relevant year

c) the time and amount of withdrawals made during the relevant year

8 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

B Benefits provided by the Plan

Retirement benefits

7 Pension/savings capital

7.1 Retirement (age 58 to 70)The entitlement to receive retirement benefits arises when employment ceases atthe age of retirement, as a general rule after completion of the member’s 63rdyear of age; members drawing a disability pension are entitled to receive retire-ment benefits upon reaching the statutory retirement age (65). At their expresswish, members may opt to take early retirement, however at the earliest uponcompletion of their 58th year of age1). Alternatively, in consultation with theemployer, they may reduce their rate of work and assert their right to receiveretirement benefits.

1) For members who already belonged to the ALSTOM Switzerland Pension Fund on 31 December2005, age 55 applies up until 2010.

Furthermore, the possibility exists to postpone retirement at latest until the mem-ber has completed his or her 70th year of age, provided the employer is inagreement.

Notice of retirement must be given at least 6 months in advance.

Retirement benefits may be drawn in the form of a capital payment or a pension.Married members requesting a payout of retirement capital must have the requestsigned by their spouse and notarised. Unmarried members must provide evi-dence of their unmarried status in the form of a recently issued official document(e.g. residency certificate). Upon withdrawal of the full sum of the savings capitalin the form of a capital payment, all of the member’s claims against the Planexpire.

Upon retirement, members also have the possibility to draw only a portion of their savings capital in the form of a capital payment. If a partial withdrawalof the savings capital is made in such a manner, the member’s retirement pen-sion and other insured benefits are reduced by the proportion such withdrawncapital represents in comparison to the total savings capital available.

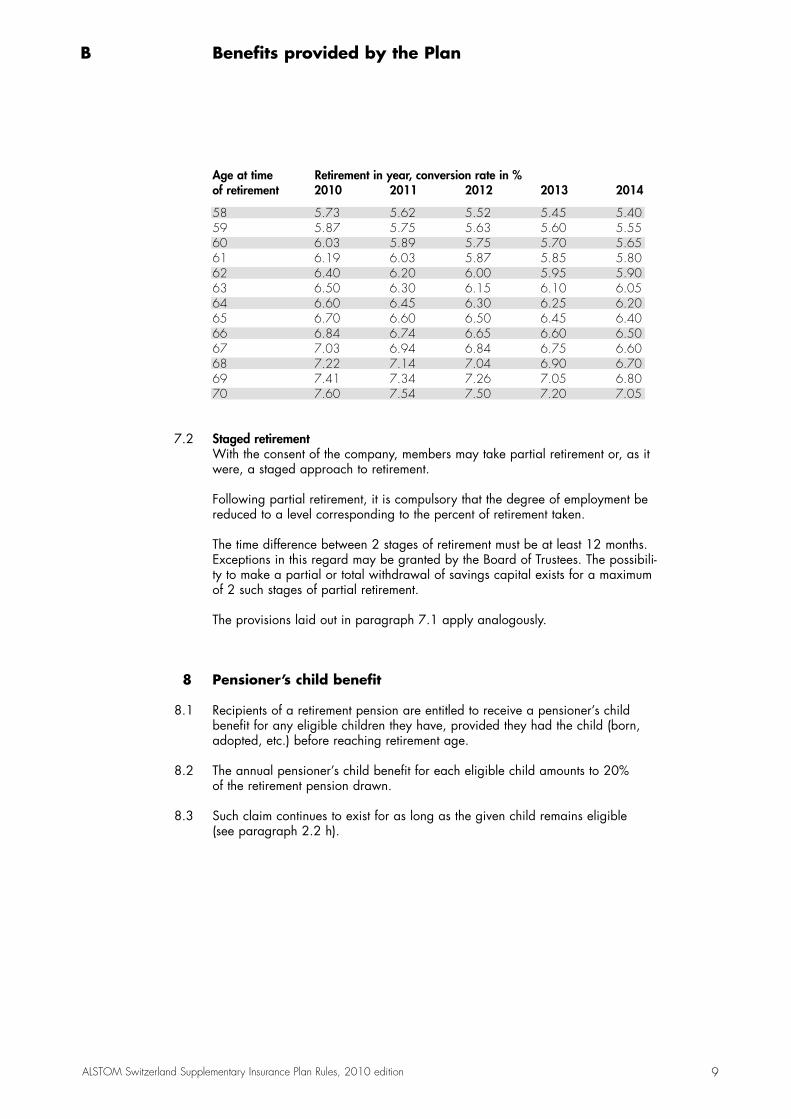

The retirement pension is calculated at the time of retirement on the basis of the available savings capital and the conversion rate. The conversion rate isdetermined by the Board of Trustees and can be seen in the following table. The Board of Trustees regularly checks that the conversion rates are up to date.These are interpolated to reflect the precise month of the member’s actual age at the time of retirement.

9ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

B Benefits provided by the Plan

Age at time Retirement in year, conversion rate in %of retirement 2010 2011 2012 2013 2014

58 5.73 5.62 5.52 5.45 5.4059 5.87 5.75 5.63 5.60 5.5560 6.03 5.89 5.75 5.70 5.6561 6.19 6.03 5.87 5.85 5.8062 6.40 6.20 6.00 5.95 5.9063 6.50 6.30 6.15 6.10 6.0564 6.60 6.45 6.30 6.25 6.2065 6.70 6.60 6.50 6.45 6.4066 6.84 6.74 6.65 6.60 6.5067 7.03 6.94 6.84 6.75 6.6068 7.22 7.14 7.04 6.90 6.7069 7.41 7.34 7.26 7.05 6.8070 7.60 7.54 7.50 7.20 7.05

7.2 Staged retirementWith the consent of the company, members may take partial retirement or, as itwere, a staged approach to retirement.

Following partial retirement, it is compulsory that the degree of employment bereduced to a level corresponding to the percent of retirement taken.

The time difference between 2 stages of retirement must be at least 12 months.Exceptions in this regard may be granted by the Board of Trustees. The possibili-ty to make a partial or total withdrawal of savings capital exists for a maximumof 2 such stages of partial retirement.

The provisions laid out in paragraph 7.1 apply analogously.

8 Pensioner’s child benefit

8.1 Recipients of a retirement pension are entitled to receive a pensioner’s child benefit for any eligible children they have, provided they had the child (born,adopted, etc.) before reaching retirement age.

8.2 The annual pensioner’s child benefit for each eligible child amounts to 20% of the retirement pension drawn.

8.3 Such claim continues to exist for as long as the given child remains eligible (see paragraph 2.2 h).

10 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

B Benefits provided by the Plan

Benefits upon disability

9 Disability pension

9.1 Within the scope of legal provisions, members are entitled to a disability pensionif they become at least 40% disabled as defined by the Federal DisabilityInsurance (IV) and provided they are insured under the Plan at the onset of theincapacity for work that led to their disability.

Provided that the member has already registered with the IV, the Board ofTrustees may, on the basis of a certificate from a doctor of its choice, decide topay a disability pension prior to the member’s receiving IV insurance benefits.These benefits are treated as an advance payment and must be repaid to thePension Fund if the IV does not grant a pension entitlement.

9.2 For members who are working abroad on behalf of the company and are notcovered by Swiss Federal Disability Insurance, the Board of Trustees may, on thebasis of a certificate issued by a recognised authority, decide to pay a disabilitypension without requiring a formal IV decree.

9.3 The right to receive disability benefits arises at the same time as the right to an IVpension. However, pension payments are deferred for as long as the member isreceiving a salary or salary replacement benefits (especially compensating healthor accident insurance benefits).

Entitlement to a disability pension ceases with the end of the disability or uponthe member’s death, at latest however at statutory retirement age.

9.4 The amount of disability pension to which the member is entitled is determinedby the IV disability scale as follows:

Degree of disability Pension level

a) At least 70% disabled Full pensionb) At least 60% disabled Three-quarter pensionc) At least 50% disabled Half pensiond) At least 40% disabled Quarter pension

The Board of Trustees may take into account changes in the degree of disabilitythat are not, or not immediately, recognised by the IV. It may also order a medical examination by a doctor of its choice. The entitlement to a pensionmay be changed on the basis of such examination. In the event that a recipientof a disability pension refuses to undergo medical examination, the Board ofTrustees may declare the pension entitlements forfeit.

9.5 The annual full disability pension amounts to 65% of the insured salary. Oncepayment of the disability pension commences, the member’s savings capital continues to accrue via savings credits that are based on the most recent insuredsalary and calculated in accordance with the Standard contributions table shownin Appendix I, together with interest and interest bonuses, until the statutoryretirement age has been reached. This savings capital then serves as the basisfor determining the retirement benefits.

9.6 In the case of partial disability, the member’s savings capital available at theonset of the disability is divided up in a manner that reflects the pension levelreceived. The portion of savings capital corresponding to the member’s per -centage capacity to work continues to accrue in the same manner as for fully able-bodied members.

11ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

B Benefits provided by the Plan

10 Disabled person’s child benefit

10.1 Recipients of a disability pension are entitled to receive a disabled person’s childbenefit for any eligible children they have.

10.2 The annual disabled person’s child benefit for each eligible child amounts to 20% of the disability pension paid out.

10.3 Such claim continues to exist for as long as the given child remains eligible (see paragraph 2.2 h).

Death benefits

11 Spouse’s pension, lump-sum payment

11.1 The surviving spouse of a member or of a pensioner is entitled to a spouse’s pension if he or she must financially support one or more eligible children or has completed the 40th year of age. If a spouse who is not yet 40 draws an IV disability pension, then the Board of Trustees may also grant that individuala spouse’s pension.

11.2 Surviving spouses who fulfil none of the conditions laid down in paragraph 11.1 are entitled to a single lump-sum payment equal to 5 times the annual amount ofthe spouse’s pension.

11.3 Entitlement to a spouse’s pension commences upon cessation of a deceasedmember’s retirement or disability pension payments or, as the case may be,when salary payments cease. Entitlement expires at the end of the month of death or upon remarriage, provided the spouse has at that time not yet completed his or her 60th year of age. If the spouse’s pension ceases owing to remarriage, the spouse is entitled to a lump-sum settlement equal to 3 times the annual amount of the spouse’s pension.

11.4 Upon the death of the member prior to the statutory retirement age, the spouse’s pension amounts to 39% of the insured salary and is payable until the memberwould have reached the statutory retirement age. Afterwards, it amounts to 60%of the implied retirement pension. At that time, the surviving spouse may opt toreceive instead of such pension a single lump-sum payment equal to 60% of thedeceased member’s implied savings capital.

Used in determining this theoretical retirement pension is the deceased member’snet savings capital (savings capital minus the deceased member’s personal buy-ins into the foundation) that would have accrued on the basis of his/her mostrecent insured salary, with savings credits accumulating in accordance with theStandard contributions table shown in Appendix I, together with interest and interest bonuses, until the deceased member would have reached the statutoryretirement age.

Upon the death of a pensioner, the spouse’s pension amounts to 60% of the mostrecent retirement pension of the deceased individual.

12 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

B Benefits provided by the Plan

11.5 The rules governing spouse’s pensions also apply to divorced spouses, providedthe former marriage lasted at least 10 years. Benefits paid by the Fund do notexceed the BVG statutory minimum. They are also limited to the amount by whichthe maintenance/alimony payment established in the divorce decree exceeds thebenefits payable by AHV and any foreign social security insurance.

11.6 At the time of retirement or, as it were, of drawing the retirement pension, members have the option to increase the prospective spouse’s pension. As a consequence, the retirement pension will be reduced for the pensioner’s lifetime in accordance with the technical principles applied by the Plan. The increased spouse’s pension may not be higher than the reduced retirement pension. This reduction pertains to the retirement pension only; the pensioner’schild be nefit remains unchanged. The reduction will remain in force even if the spouse predeceases the pensioner.

12 Partner’s pension, lump-sum payment

12.1 If an unmarried member dies, the following persons are entitled to a partner’spension:

a) the unmarried partner of an unmarried, legally unrelated member, providedthe partner is 40 or older and cohabitated continuously with the member forat least 5 years prior to the member’s death

b) the unmarried partner of an unmarried member, provided the surviving part-ner must support children (up to the age of 25) that the couple had together

c) individuals who have been supported to large extent by the deceased memberand who are at least 40 years of age. A prerequisite for any claim in thisregard is that such support lasted for a minimum of 5 years and was reportedto the Plan by means of the appropriate form prior to the member’s death. Atmaximum, benefits paid in this regard by the Plan correspond to the amountof support no longer provided

Partners of unmarried pensioners are only entitled to receive a partner’s pensionif the partnership was already entered into prior to the pensioner’s 60th year ofage.

12.2 A maximum of one partner’s pension may be paid out. If more than one personfulfils the criteria set out in paragraph 12.1, the partner’s pension may be splitbetween them. Any such person must have been identified by the deceasedmember as a partner. If this is not the case, the Board of Trustees shall decide.

12.3 Application must be made at latest within 3 months of the member’s death. Thebeginning, end and size of the pension are determined by the same criteria asset out in paragraph 11. If the criteria under paragraph 12.1 are not fulfilled,there is no entitlement to a settlement pursuant to paragraph 11.2.

The partner’s pension will be reduced by any spouse’s or partner’s pensions thatare currently being paid.

13ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

B Benefits provided by the Plan

13 Orphans’ pension

13.1 Upon the death of a member or pensioner, his or her eligible children are entitled to draw an orphan’s pension.

13.2 The annual orphan’s pension for each eligible child amounts to 20% of theinsured full disability pension or, as the case may be, 20% of the retirement pension that was paid. The orphan’s pension is doubled for orphans bereaved of both parents.

13.3 Entitlement to an orphan’s pension commences upon the cessation of retirementor disability pension payments or, as the case may be, when salary paymentscease. Entitlement continues for as long as the given child remains eligible toreceive such pension (see paragraph 2.2 h).

14 Death benefit

14.1 A capital sum is payable upon the death of a member. Entitled to receive payment of such are the member’s survivors, irrespective of right of inheritance,in the following amount and order of precedence:

a) in the full amount: the member’s spouse, and their children under the age of 25, failing them

b) in the full amount: partners or persons who were supported to a substantialdegree by the deceased member prior to his or her death (as per paragraph12.1), failing them

c) in the full amount: other children or parents of the deceased, failing them

d) in half the amount: the other legal heirs of the deceased member, excludingthe state

14.2 By written instruction addressed to the Plan, members may stipulate which persons among the eligible group are entitled to receive the death benefit, and in which proportions. If no such instructions are given, the death benefit will fundamentally be distributed in equal portions among the eligible group. The Board of Trustees may opt for an alternative regulation in this regard.

14.3 If death occurs prior to retirement, the death benefit is equal to the deceasedmember’s accrued net savings capital (savings capital minus the deceased member’s personal buy-ins into the Pension Fund) reduced by the costs of fundingthe survivors’ benefits, but at least 100% of the insured salary. Subsequent to retirement, the death benefit is equal to twice the annual retirement pension,reduced by the retirement pension payments received.

14 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

B Benefits provided by the Plan

Additional provisions

15 Vested benefit

15.1 Insurance coverage ceases upon termination of the employment relationship, provided no claim exists for Plan benefits under these Rules. If savings capitalhas accrued, the member is entitled to receive the relevant vested benefit.

15.2 The amount of the vested benefit is calculated in accordance with the definedcontribution principle. It is equal to the member’s available savings capital plusthe capital available from the buy-in plan.

15.3 The death and disability benefits insured at the time employment ceases remaininsured without change until such time as the individual begins a new pensionarrangement, but at most for the period of 1 month. If the Plan becomes obligat-ed to pay benefits after the vested benefit has already been paid out and norepayment of the latter amount has been made, the individual’s savings capitalwill be reduced by a corresponding amount.

15.4 The vested benefit is transferred to the occupational benefits plan of the indi -vidual’s new employer.

In the absence of such a fund, the member may opt to transfer the vested benefitto a specially designated vested benefit account or use it to purchase a vestedbenefit insurance policy. Should the individual fail to provide appropriate notifi-cation, the vested benefit will be automatically remitted to the BVG SuppletoryInstitution 6 months after his or her departure.

15.5 Departing members may request cash payment of the vested benefit if:

a) they are leaving Switzerland and the Principality of Liechtenstein permanently or

b) they become self-employed and are no longer subject to mandatory occupational insurance or

c) the vested benefit is less than the member’s annual contribution

For married members, cash payment of the vested benefit is permitted only withthe spouse’s written consent. The signature of the latter must be notarised.Unmarried members must provide evidence of their unmarried status in the formof a recently issued official document (e.g. residency certificate).

15.6 Furthermore, the Federal Law on Vested Pension Benefits, as well asSwitzerland’s bilateral agreements with the European Union, shall apply in this regard.

15.7 For the duration of an underfunding, the calculation of exit benefits pursuant toart. 17 FZG is based on the interest rate determined by the Board of Trustees forthe savings capital rather than on the BVG minimum rate.

15ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

B Benefits provided by the Plan

16 Payment of pensions

16.1 Pensions are paid in advance in monthly instalments. The full pension is paid out for the month in which entitlement ceases. Upon the death of a recipient of a retirement or disability pension, entitlement to payment of the related pensionceases only 2 months after the month of death.

16.2 If, at the time of drawing a pension, the annual pension or the sum of annualpensions is less than 10% of the minimum AHV pension, a lump-sum capital settlement calculated according to actuarial rules will be paid out in place ofsuch pension(s).

17 Cost-of-living adjustment to benefits

17.1 The Board of Trustees decides on an annual basis whether and to what extentpensions can be increased within the realm of financial possibilities of the Plan.To this purpose, the assets of the Plan are deployed in a manner favourable to members and pensioners (see paragraph 23.4 a).

18 Overinsurance and reduction of benefits

18.1 If the survivors’ or disability benefits payable by the Plan, aggregated with thebenefits of a different occupational benefits plan, the AHV/IV, accident or military insurance or foreign social security schemes, result in a pension incomethat exceeds 90% of the presumed lost income, the pensions to be paid out by the Plan may be reduced until such limit is no longer exceeded. The sameprovision shall likewise apply to the insurance schemes for which the companyhas paid at least one half of the premium.

The additional earned income, or income that could reasonably be earned, byrecipients of disability benefits may be taken into account in this regard. In deter-mining the income that could reasonably be earned, the income that a personcould be expected to earn as an able-bodied person (“able-bodied income”) andthe income they could be expected to earn as a disabled person (“disabled per-son’s income”), and the residual earning capacity of the recipient of the benefitsas per the IV Decision will always be taken as a basis.

The retirement benefits shall be reduced only if they coincide with benefits paid under accident and/or military insurance. In such an instance, the reduced retirement benefits will correspond at minimum to the given member’s total contributions at the time he or she became disabled. Lump-sum settlements or, as the case may be, capital payments are converted into actuarially equivalentpensions.

16 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

B Benefits provided by the Plan

18.2 Persons entitled to benefits in the event of death or disability are required to surrender to the Plan their claims against any liable third party, up to the amountof the Plan’s benefit obligations vis-à-vis such entitled persons.

18.3 The Plan may reduce its benefits by a corresponding degree if AHV/IV or theaccident or military insurers reduce, withdraw or refuse the payment of benefitsbecause the beneficiary has caused his or her death or disability through grossnegligence or refuses to undergo rehabilitation measures.

19 Promotion of home ownership

19.1 Within the scope of the relevant legal provisions, members may use their savingscapital to purchase residential property.

19.2 The Board of Trustees adopts the necessary implementing provisions in thisregard.

17ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

C Funding

20 Obligation to contribute

20.1 The obligation to make contributions commences upon acceptance into the Planand continues until the member’s retirement, departure from the Plan or death.

20.2 For those members who are disabled, the obligation to contribute is reduced inaccordance with the relevant breakdown (as per paragraph 9.4).

20.3 Members’ contributions are deducted by the company from their salary, sick pay or compensatory salary, and transferred to the Plan in monthly instalmentstogether with the company’s contributions.

21 Amount of contributions

21.1 Members have 3 contributions tables from which to choose: Standard, Standardplus and Standard minus. Members may choose each year the contributionstable according to which they wish to contribute in the following year, for effectas of 1 January. The Standard contributions table applies if the Plan has notreceived written notification of the member’s choice. Once a decision has beentaken, it shall continue to apply until changed by the member.

21.2 The company pays a contribution according to the contributions table shown in Appendix I. This contribution is composed of the age-dependent savings credits, as well as a contribution of 3.5% of the member’s insured salary for the risks of death and disability and also for other expenses.

22 Personal payments

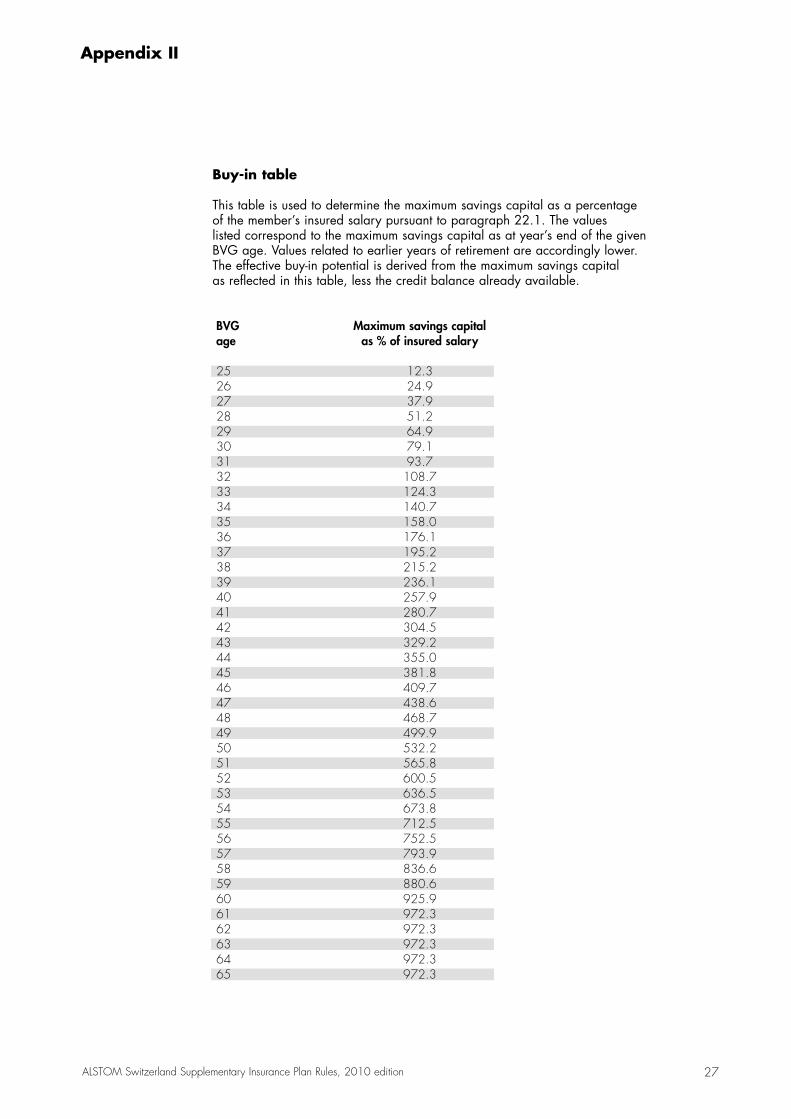

22.1 Within the scope of the relevant legal provisions, members may at any timemake payments into the Pension Fund in order to increase their retirement benefits. The Pension Fund shall determine the related buy-in limit by applying re cognised principles (see buy-in table in Appendix II).

Any vested assets or pillar 3a assets are deducted from the buy-in limits shown inAppendix II. For members who move to Switzerland from abroad and who havenever been in a Swiss pension scheme, the restrictions set out in art. 60b BVV 2also apply.

If death occurs prior to retirement, the sum of the deceased member’s personalbuy-ins into the Pension Fund plus interest will be paid to the beneficiaries pursuant to paragraphs 14.1 and 14.2 in addition to the death benefit pursuantto paragraph 14.3.

18 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

C Funding

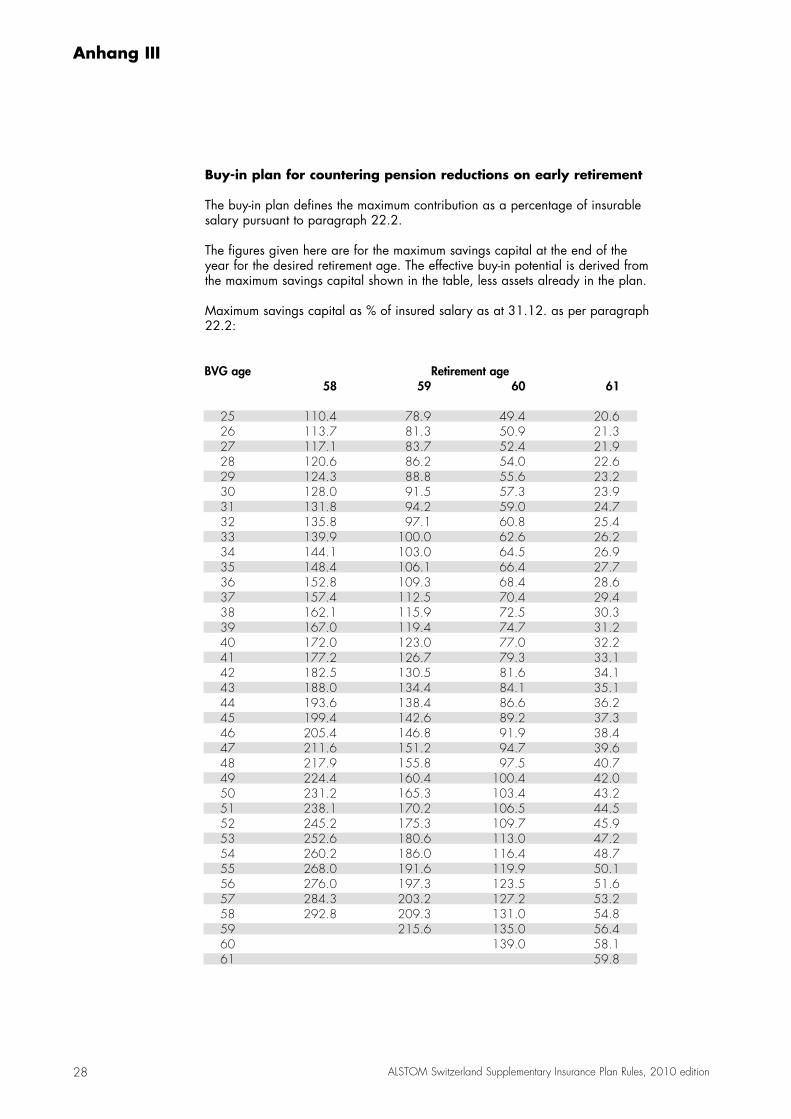

22.2 The member can make up the reduction in benefits resulting from early retirement by paying deposits into an interest-bearing buy-in plan account inaccordance with Appendix III.

Interest on this account will be determined analogously to paragraph 6.3.

Deposits to the buy-in plan account are only possible if:

a) the member has transferred all vested benefits from earlier pension schemesinto the Plan

b) the member has bought in the full benefits of the Basic plan (Appendix II)

c) the member is at least 25 years of age and the maximum amount specified inthe table in Appendix III has not yet been reached

d) all withdrawals for home ownership have first been paid back

The capital accrued in the buy-in plan is payable on retirement, and can bedrawn either as a lump-sum payment or as a pension in accordance with thetechnical principles of the Plan.

If the member has made buy-ins for early retirement but does not take early retirement, the balance of the buy-ins is forfeited to the pension scheme if the retirement benefit would be more than 5% higher than that of a member who has made no buy-ins for early retirement.

When withdrawals are made for home ownership or to pay divorce-relatedbenefits, capital from the buy-in plan is used first.

22.3 If a buy-in is made, the resulting benefits may not be withdrawn from the Plan inthe form of capital for a period of 3 years. If early withdrawals have been madein connection with the promotion of home ownership, voluntary buy-ins may bemade only once such withdrawals have been repaid. Exempted from this limita-tion are buy-ins made in the case of divorce.

19ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

C Funding

23 Assets, financial equilibrium and segregated funds

23.1 The Plan’s assets are to be prudently invested. The Board of Trustees determinesthe investment strategy. The composition of the invested assets must comply with relevant legal provisions. Sufficient liquid assets must be maintained to coverthe ongoing outlays of the Plan.

23.2 The Board of Trustees appoints annually an accredited occupational benefitsexpert to conduct an actuarial audit of the Plan on the principles of the funded-system method for a closed pension fund.

23.3 If the actuarial balance sheet reveals an underfunding which threatens the securityof benefits payable under these Rules, the Board of Trustees shall implement anymeasures it deems necessary. In particular, and as long as the legal provisionsare complied with, the Board of Trustees may take the following steps:

n Remedial contributions may be levied as a percentage of insured salary. Thecompany’s remedial contributions must be at least as high as the members’contributions. Remedial contributions may in principle be levied until theunderfunding is corrected. The Board of Trustees shall determine the size ofthe contributions and the dates on which they begin and end.

n Future or, if necessary, acquired insurance benefits may be reduced as appropriate.

n Early withdrawals to repay mortgage loans may be refused during a period of underfunding. The Board of Trustees shall decide when this restriction isimposed and when it is lifted.

n The company can put funds into a separate employer contribution reserveaccount with usage restrictions.

If the financial underpinnings of the Pension Fund are put at risk by exceptional circumstances such as war, epidemics, loss of assets, etc., the Board of Trusteesmay as a precautionary measure reduce acquired, current and future benefits.

23.4 a) The Plan maintains a segregated fund for the benefit of members and pensioners.

Credited to this fund are:n revenue surpluses on the portion of the assets reserved for membersn revenue surpluses on the portion of the assets reserved for pensionersn risk profits on the insurance of pensioners

Debited to this fund are:n interest bonus paymentsn pension increases (capitalised)n risk losses on the insurance of pensioners

b) The Plan also maintains a risk fluctuation fund; credited or, as it were, debitedto this fund are profits/losses on the risk insurance of members.

20 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

D Organisation and administration

24 Board of Trustees

24.1 The Board of Trustees is the sole official body of the Plan. It is composed of 3 to5 trustees who, except as provided under paragraph 24.2, are appointed byALSTOM (Switzerland) Ltd. All employees of the companies affiliated with thePlan are capable of being elected to the Board of Trustees, provided the givencandidate is interested in matters related to occupational benefits, possesses abasic knowledge in such matters, and has a command of the German language.

24.2 The entire body of members elects from its midst one individual to represent them on the Board of Trustees. The Board of Trustees enacts rules on how repre-sentatives of Plan members are to be elected to the Board.

24.3 The term of office of trustees is 4 years, and re-election is possible. If an employee representative leaves the company, the company shall decide whetherhis or her term of office is to end. In the case of such a premature departure, a by-election is to be held. The newly elected trustee then completes his or herpredecessor’s term of office.

The employee representatives may remain on the Board of Trustees beyond theirretirement until their term of office expires.

24.4 The Chairman of the Board of Trustees is appointed by ALSTOM (Switzerland)Ltd. In all other respects, the Board of Trustees constitutes itself.

24.5 The Board of Trustees is responsible for the administration of the Plan in compliance with these Rules. It may delegate particular tasks to commissions,administrative bodies and committees, and enacts the directives and regulationsthat are necessary to do so. The Board of Trustees makes rulings in all matters pertaining to the Plan in keeping with the requirements of law and the provisionsof these Rules. It appoints the auditors and the accredited occupational benefitsexperts.

24.6 A quorum is constituted when all, or all but one, members of the Board ofTrustees are present. Resolutions are adopted by a simple majority of votes. In the case of a voting deadlock, the Chairman’s vote shall count double. The Board of Trustees enacts rules on how voting via circular letter is to beaccomplished.

24.7 The members of the Board of Trustees, as well as the persons acting on itsbehalf, are obligated to maintain secrecy with regard to the personal circum-stances of Plan members, as well as the business matters of the Plan and thecompany, which may come to their knowledge in the exercise of their duties.

21ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

D Organisation and administration

25 Administration of the Plan

25.1 The Board of Trustees appoints the general management of the Plan.

25.2 The Plan bears the costs of its administration. Such costs are shown in the annualfinancial statements of the Plan.

26 Information and disclosure obligation

26.1 The annual financial statements of the Plan are made available to all membersand pensioners.

By means of an insurance certificate, members are informed each year about theinsured benefits and the balance of their savings capital.

On request, personal data will be disclosed to the member by the Plan.

26.2 Members or, as the case may be, their survivors are required to provide at any time truthful information on circumstances relevant to their insurance and to submit the documents necessary to substantiate any claims for benefits.

26.3 The Board of Trustees reserves the right to cease payment of benefits, or to demand repayment of benefits paid out wrongly, if a member or a pensionerfails to comply with the obligation to provide relevant information.

26.4 The Plan may levy charges for special expenses. The Board of Trustees regulatesthe details in this regard.

22 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

E Concluding provisions

27 Legal recourse

27.1 Any disputes arising from the application or interpretation of these Rules, or with regard to issues that are not specifically covered by these Rules, are tobe presented to the Board of Trustees for amicable settlement.

27.2 If no amicable settlement can be achieved, legal recourse may be sought inkeeping with the provisions of BVG.

27.3 The original German text is legally binding.

28 Loopholes in the Rules

28.1 In the case of situations not explicitly foreseen by the provisions of these Rules,the Board of Trustees is authorised to enact an appropriate rule that correspondsto the spirit and purpose of the Plan.

29 Partial or total liquidation

29.1 Upon the partial or total liquidation of the Plan, each departing member has aright to a portion of the freely available assets in keeping with the relevant legalprovisions. Said assets may be transferred individually or, in the case of a groupmove by members to the same employer, collectively to a new occupational benefits scheme.

29.2 Actuarial deficits may be deducted from the payment of vested benefits.

29.3 The Board of Trustees enacts the necessary implementing provisions in thisregard.

23ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

E Concluding provisions

30 Changes/entry into force

30.1 Within the scope of the relevant legal provisions and the purpose of the Plan, the Board of Trustees may amend these Rules at any time. Entitlements alreadyacquired by beneficiaries are not affected by a subsequent amendment of theseRules.

If, however, a retirement pension or disability pension is supplanted through payment of a death benefit, then the version of the Rules valid at that time shallapply with regard to such death benefit.

At the time a disability or spouse’s pension converts into a retirement pension orfull spouse’s pension, determination of the new benefits is made in accordancewith the version of these Rules valid at that time.

Disability pensions that have commenced prior to 1 January 2007 will not beaffected by the new breakdown reflected in paragraph 9.4.

The following arrangements apply in the event of a change in the degree of disability:

Pension entitlement Increase in Reduction in Applicable acquired degree of disability degree of disability Rules

Before 01.01.2005 Before 01.01.2007 Rules 2003, para. 9.4Before 01.01.2005 As of 01.01.2007 Rules 2007, para. 9.4Before 01.01.2005 As of 01.01.2005 Rules 2003, para. 9.4Between 01.01.2005 Before 01.01.2007 Before 01.01.2007 Rules 2003, para. 9.4and 31.12.2006Between 01.01.2005 As of 01.01.2007 As of 01.01.2007 Rules 2007, para. 9.4and 31.12.2006

30.2 These Rules enter into force on 1 January 2010 and replace the version dated 1 January 2007, including the Appendices.

The Board of TrusteesALSTOM Switzerland Supplementary Insurance Plan

Baden, 27 August 2009

24 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

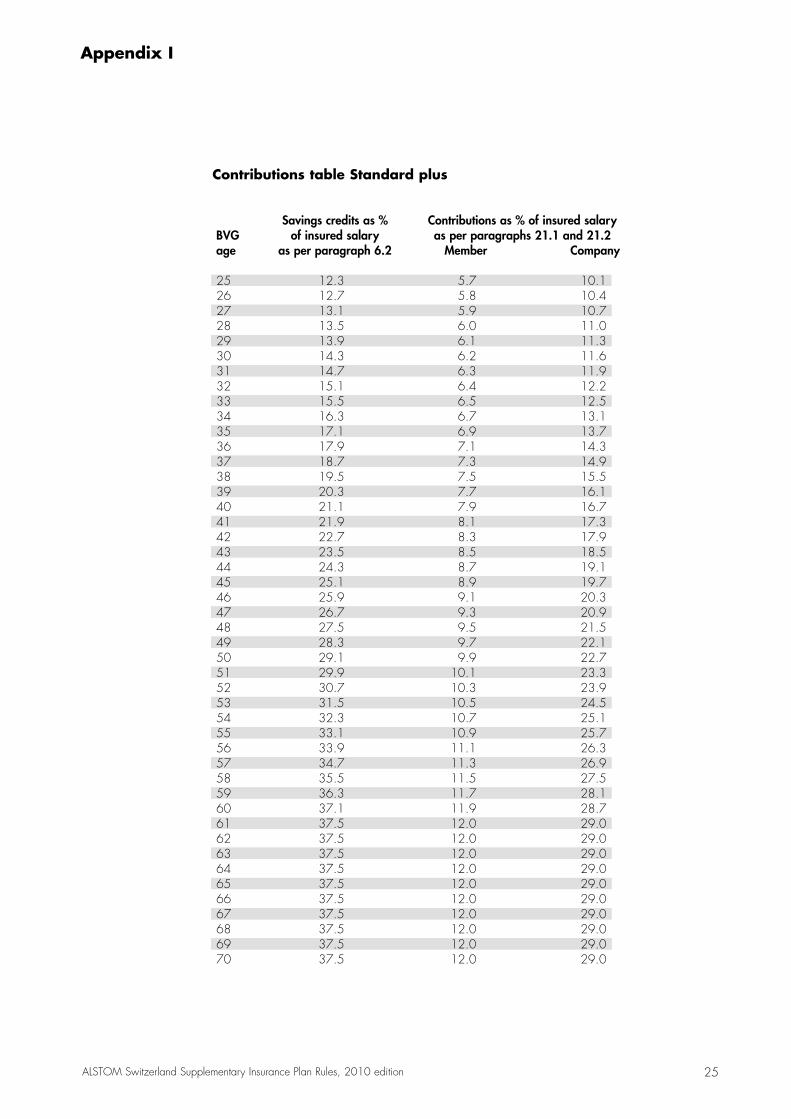

Appendix I

Contributions table Standard

Savings credits as % Contributions as % of insured salaryBVG of insured salary as per paragraphs 21.1 and 21.2age as per paragraph 6.2 Member Company

25 8.8 2.2 10.126 9.2 2.3 10.427 9.6 2.4 10.728 10.0 2.5 11.029 10.4 2.6 11.330 10.8 2.7 11.631 11.2 2.8 11.932 11.6 2.9 12.233 12.0 3.0 12.534 12.8 3.2 13.135 13.6 3.4 13.736 14.4 3.6 14.337 15.2 3.8 14.938 16.0 4.0 15.539 16.8 4.2 16.140 17.6 4.4 16.741 18.4 4.6 17.342 19.2 4.8 17.943 20.0 5.0 18.544 20.8 5.2 19.145 21.6 5.4 19.746 22.4 5.6 20.347 23.2 5.8 20.948 24.0 6.0 21.549 24.8 6.2 22.150 25.6 6.4 22.751 26.4 6.6 23.352 27.2 6.8 23.953 28.0 7.0 24.554 28.8 7.2 25.155 29.6 7.4 25.756 30.4 7.6 26.357 31.2 7.8 26.958 32.0 8.0 27.559 32.8 8.2 28.160 33.6 8.4 28.761 34.0 8.5 29.062 34.0 8.5 29.063 34.0 8.5 29.064 34.0 8.5 29.065 34.0 8.5 29.066 34.0 8.5 29.067 34.0 8.5 29.068 34.0 8.5 29.069 34.0 8.5 29.070 34.0 8.5 29.0

25ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

Appendix I

Contributions table Standard plus

Savings credits as % Contributions as % of insured salaryBVG of insured salary as per paragraphs 21.1 and 21.2age as per paragraph 6.2 Member Company

25 12.3 5.7 10.126 12.7 5.8 10.427 13.1 5.9 10.728 13.5 6.0 11.029 13.9 6.1 11.330 14.3 6.2 11.631 14.7 6.3 11.932 15.1 6.4 12.233 15.5 6.5 12.534 16.3 6.7 13.135 17.1 6.9 13.736 17.9 7.1 14.337 18.7 7.3 14.938 19.5 7.5 15.539 20.3 7.7 16.140 21.1 7.9 16.741 21.9 8.1 17.342 22.7 8.3 17.943 23.5 8.5 18.544 24.3 8.7 19.145 25.1 8.9 19.746 25.9 9.1 20.347 26.7 9.3 20.948 27.5 9.5 21.549 28.3 9.7 22.150 29.1 9.9 22.751 29.9 10.1 23.352 30.7 10.3 23.953 31.5 10.5 24.554 32.3 10.7 25.155 33.1 10.9 25.756 33.9 11.1 26.357 34.7 11.3 26.958 35.5 11.5 27.559 36.3 11.7 28.160 37.1 11.9 28.761 37.5 12.0 29.062 37.5 12.0 29.063 37.5 12.0 29.064 37.5 12.0 29.065 37.5 12.0 29.066 37.5 12.0 29.067 37.5 12.0 29.068 37.5 12.0 29.069 37.5 12.0 29.070 37.5 12.0 29.0

26 ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

Appendix I

Contributions table Standard minus

Savings credits as % Contributions as % of insured salaryBVG of insured salary as per paragraphs 21.1 and 21.2age as per paragraph 6.2 Member Company

25 6.6 0 10.126 6.9 0 10.427 7.2 0 10.728 7.5 0 11.029 7.8 0 11.330 8.1 0 11.631 8.4 0 11.932 8.7 0 12.233 9.0 0 12.534 9.6 0 13.135 10.2 0 13.736 10.8 0 14.337 11.4 0 14.938 12.0 0 15.539 12.6 0 16.140 13.2 0 16.741 13.8 0 17.342 14.4 0 17.943 15.0 0 18.544 15.6 0 19.145 16.2 0 19.746 16.8 0 20.347 17.4 0 20.948 18.0 0 21.549 18.6 0 22.150 19.2 0 22.751 19.8 0 23.352 20.4 0 23.953 21.0 0 24.554 21.6 0 25.155 22.2 0 25.756 22.8 0 26.357 23.4 0 26.958 24.0 0 27.559 24.6 0 28.160 25.2 0 28.761 25.5 0 29.062 25.5 0 29.063 25.5 0 29.064 25.5 0 29.065 25.5 0 29.066 25.5 0 29.067 25.5 0 29.068 25.5 0 29.069 25.5 0 29.070 25.5 0 29.0

27ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

Appendix II

Buy-in table

This table is used to determine the maximum savings capital as a percentage of the member’s insured salary pursuant to paragraph 22.1. The values listed correspond to the maximum savings capital as at year’s end of the givenBVG age. Values related to earlier years of retirement are accordingly lower. The effective buy-in potential is derived from the maximum savings capital as reflected in this table, less the credit balance already available.

BVG Maximum savings capital age as % of insured salary

25 12.326 24.927 37.928 51.229 64.930 79.131 93.732 108.733 124.334 140.735 158.036 176.137 195.238 215.239 236.140 257.941 280.742 304.543 329.244 355.045 381.846 409.747 438.648 468.749 499.950 532.251 565.852 600.553 636.554 673.855 712.556 752.557 793.958 836.659 880.660 925.961 972.362 972.363 972.364 972.365 972.3

28

Anhang III

Buy-in plan for countering pension reductions on early retirement

The buy-in plan defines the maximum contribution as a percentage of insurablesalary pursuant to paragraph 22.2.

The figures given here are for the maximum savings capital at the end of theyear for the desired retirement age. The effective buy-in potential is derived fromthe maximum savings capital shown in the table, less assets already in the plan.

Maximum savings capital as % of insured salary as at 31.12. as per paragraph22.2:

BVG age Retirement age58 59 60 61

25 110.4 78.9 49.4 20.626 113.7 81.3 50.9 21.327 117.1 83.7 52.4 21.928 120.6 86.2 54.0 22.629 124.3 88.8 55.6 23.230 128.0 91.5 57.3 23.931 131.8 94.2 59.0 24.732 135.8 97.1 60.8 25.433 139.9 100.0 62.6 26.234 144.1 103.0 64.5 26.935 148.4 106.1 66.4 27.736 152.8 109.3 68.4 28.637 157.4 112.5 70.4 29.438 162.1 115.9 72.5 30.339 167.0 119.4 74.7 31.240 172.0 123.0 77.0 32.241 177.2 126.7 79.3 33.142 182.5 130.5 81.6 34.143 188.0 134.4 84.1 35.144 193.6 138.4 86.6 36.245 199.4 142.6 89.2 37.346 205.4 146.8 91.9 38.447 211.6 151.2 94.7 39.648 217.9 155.8 97.5 40.749 224.4 160.4 100.4 42.050 231.2 165.3 103.4 43.251 238.1 170.2 106.5 44.552 245.2 175.3 109.7 45.953 252.6 180.6 113.0 47.254 260.2 186.0 116.4 48.755 268.0 191.6 119.9 50.156 276.0 197.3 123.5 51.657 284.3 203.2 127.2 53.258 292.8 209.3 131.0 54.859 215.6 135.0 56.460 139.0 58.161 59.8

ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

29

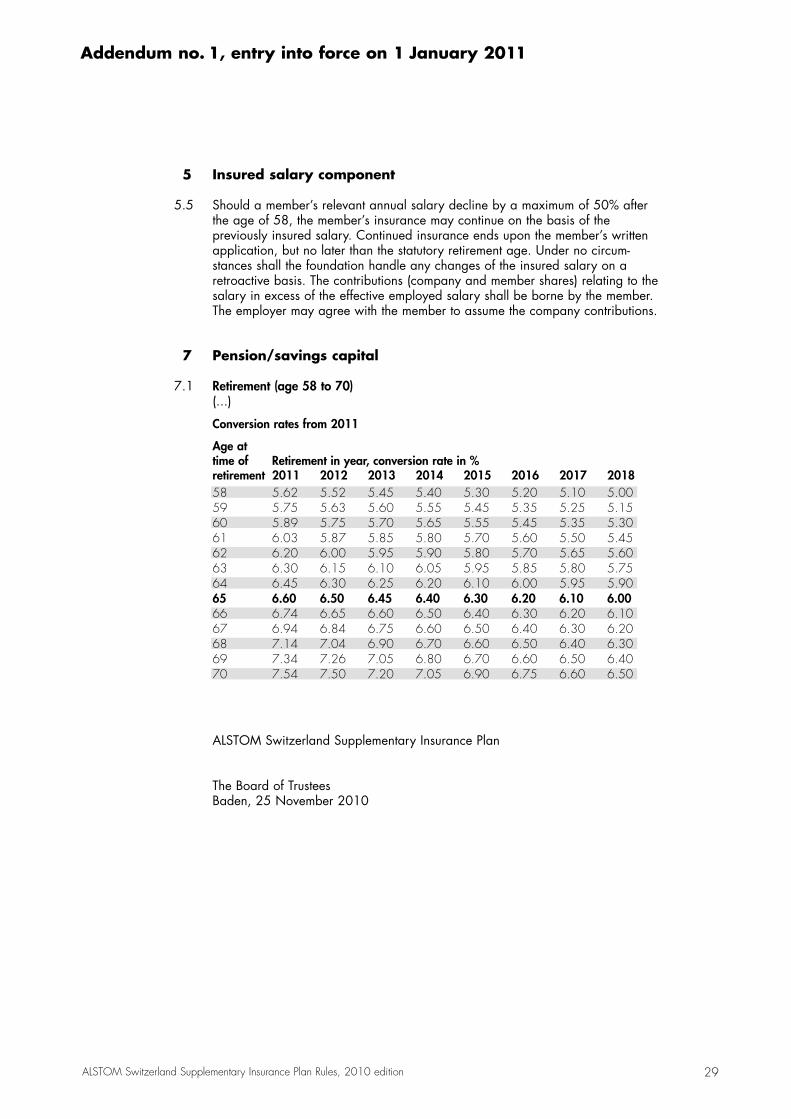

Addendum no. 1, entry into force on 1 January 2011

5 Insured salary component

5.5 Should a member’s relevant annual salary decline by a maximum of 50% afterthe age of 58, the member’s insurance may continue on the basis of the previously insured salary. Continued insurance ends upon the member’s writtenapplication, but no later than the statutory retirement age. Under no circum -stances shall the foundation handle any changes of the insured salary on a retroactive basis. The contributions (company and member shares) relating to thesalary in excess of the effective employed salary shall be borne by the member.The employer may agree with the member to assume the company contributions.

7 Pension/savings capital

7.1 Retirement (age 58 to 70)(...)

Conversion rates from 2011

Age at time of Retirement in year, conversion rate in %retirement 2011 2012 2013 2014 2015 2016 2017 201858 5.62 5.52 5.45 5.40 5.30 5.20 5.10 5.0059 5.75 5.63 5.60 5.55 5.45 5.35 5.25 5.1560 5.89 5.75 5.70 5.65 5.55 5.45 5.35 5.3061 6.03 5.87 5.85 5.80 5.70 5.60 5.50 5.4562 6.20 6.00 5.95 5.90 5.80 5.70 5.65 5.6063 6.30 6.15 6.10 6.05 5.95 5.85 5.80 5.7564 6.45 6.30 6.25 6.20 6.10 6.00 5.95 5.9065 6.60 6.50 6.45 6.40 6.30 6.20 6.10 6.0066 6.74 6.65 6.60 6.50 6.40 6.30 6.20 6.1067 6.94 6.84 6.75 6.60 6.50 6.40 6.30 6.2068 7.14 7.04 6.90 6.70 6.60 6.50 6.40 6.3069 7.34 7.26 7.05 6.80 6.70 6.60 6.50 6.4070 7.54 7.50 7.20 7.05 6.90 6.75 6.60 6.50

ALSTOM Switzerland Supplementary Insurance Plan

The Board of TrusteesBaden, 25 November 2010

ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

30

Alphabetical list of terms and concepts

ParagraphA

administration of the Plan 25age definition 2.2 d, 2.2 e, 2.2 gamount of contributions 21application/interpretation of the Rules 27.1, 27.2, 28assets 23

B

beginning of insurance coverage 4.1beneficiaries 12.1, 14.1Board of Trustees 24BVG 2.2 fBVG age 2.2 g, Appendix I, Appendix II

C

capital withdrawal 7.1cash payment of vested benefit 15.5, 15.6changes to the Rules 30company contributions 21.2, Appendix Icontribution tables Appendix Iconversion rate 7.1, Addendum no. 1cost-of-living adjustment to benefits 17

D

death benefit 14definitions 2departures 4.2, 15disability pension 9disabled person’s child benefit 10disclosure obligation 26disputes 27.1divorce 11.5divorced spouses 11.5

E

early retirement 7.1external membership 3.5

F

financial equilibrium 23follow-up insurance coverage 15.3fund for the benefit of members 23.4fund for the benefit of pensioners 23.4

ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

31

Alphabetical list of terms and concepts

ParagraphG

general management of the Plan 25.1

I

income limit 5.1, 5.2, 5.4information and disclosure obligation 26insured portion of salary 5, Addendum no. 1interest 6.1, 6.3, 6.4interest bonus 6.4

L

legal recourse 27loopholes in the Rules 28lump-sum payment 11, 12

M

members 2.2 c, 3members’ contributions 21.1, Appendix Imembership in the Plan 3, 4.1

N

notice of retirement 7.1

O

obligation to contribute 20orphan’s pension 13overinsurance 18

P

partial disability 5.3, 9.6, 20.2partial liquidation 29partial withdrawal of capital 7.1partner’s pension 12payment of pensions 16pension 7.1, 7.2, 22.1, 22.2

Addendum no. 1pensioner’s child benefit 8postponed retirement 7.1promotion of home ownership 19

ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

32

Alphabetical list of terms and concepts

ParagraphR

reduction of benefits (overinsurance) 18registered partnership 2.2.iretirement age 2.2 d, 7.1retirement benefits 7, 8retirement capital 7.1risk fluctuation fund 23.4risk premium 21.2

S

savings capital 6, 7.1, 9.5, 9.6, 11.4, 14.3,15.1–3, 19.1, Appendix II,Addendum no. 1

savings credits 6, 9.5, 21.1, 21.2,Appendix I

spouse’s pension 11staged retirement 7.2statutory retirement age 2.2 e, 7.1, 9.3, 9.5, 11.4

T

termination of insurance coverage 4.2total liquidation 29

U

underfunded status 23.3, 29.2

V

vested benefit 15voluntary contributions/buy-ins 6.1, 22.1, 22.2, Appendix II

ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition

ALSTOM Switzerland Supplementary Insurance Plan, c/o Avadis Vorsorge AG, Bruggerstrasse 61a, Postfach, 5401 Baden T 058 585 54 91, F 058 585 29 00, [email protected], www.alstomvorsorge.ch