ALPHA-OLEFINS - WORLD MARKETS, 2005-2015 - World Markets, 2005-2015... · ALPHA-OLEFINS - WORLD...

28

COLIN A. HOUSTON & ASSOCIATES, INC. Colin A. Houston & Associates, Inc. announces a new multiclient study ALPHA-OLEFINS - WORLD MARKETS, 2005-2015 Colin A. Houston & Associates, Inc. (CAHA) plans to undertake a new multiclient study of the global markets for alpha-olefins beginning in October 2006, with completion scheduled for April 2007. The results will be delivered electronically section by section on a monthly basis via an Internet database accessible via password. A printed version will be delivered following completion of the final sections. Since our last comprehensive global alpha-olefins study published in 2001, CAHA has carried out many projects involving alpha-olefins, including multiclient market studies for several LAO derivatives. In addition, CAHA follows alpha-olefin market developments on an ongoing basis for our monthly LAO newsletter. This will enable us to provide clients of the new study with access to a preliminary database of LAO consumption by end use by the end of October 2006. Thereafter, different chapters will be researched and updated sequentially, with new data posted each month. A final supply/demand balance and executive summary are scheduled for completion by the end of April 2007. Details of the new study and database service are explained on the following pages. Please contact either Marilyn Bradshaw, Vice President and Alpha-Olefins Project Leader or Joel Houston, President to discuss this valuable new program. CONTENTS Page Purpose of the Study 2 Electronic Version 4 Project Plan by Section 5 Tentative Print Version Table of Contents 10 Sample Tables 16 Qualifications & Personnel 25 How to Subscribe 28

Transcript of ALPHA-OLEFINS - WORLD MARKETS, 2005-2015 - World Markets, 2005-2015... · ALPHA-OLEFINS - WORLD...

COLIN A. HOUSTON & ASSOCIATES, INC.

Colin A. Houston & Associates, Inc. announces

a new multiclient study

ALPHA-OLEFINS - WORLD MARKETS, 2005-2015

Colin A. Houston & Associates, Inc. (CAHA) plans to undertake a new multiclientstudy of the global markets for alpha-olefins beginning in October 2006, with completionscheduled for April 2007. The results will be delivered electronically section by sectionon a monthly basis via an Internet database accessible via password. A printed versionwill be delivered following completion of the final sections.

Since our last comprehensive global alpha-olefins study published in 2001,CAHA has carried out many projects involving alpha-olefins, including multiclient marketstudies for several LAO derivatives. In addition, CAHA follows alpha-olefin marketdevelopments on an ongoing basis for our monthly LAO newsletter. This will enable usto provide clients of the new study with access to a preliminary database of LAOconsumption by end use by the end of October 2006. Thereafter, different chapters willbe researched and updated sequentially, with new data posted each month. A finalsupply/demand balance and executive summary are scheduled for completion by theend of April 2007.

Details of the new study and database service are explained on the followingpages. Please contact either Marilyn Bradshaw, Vice President and Alpha-OlefinsProject Leader or Joel Houston, President to discuss this valuable new program.

CONTENTS

Page

Purpose of the Study 2Electronic Version 4Project Plan by Section 5Tentative Print Version Table of Contents 10Sample Tables 16Qualifications & Personnel 25How to Subscribe 28

2 COLIN A. HOUSTON & ASSOCIATES, INC.

PURPOSE OF THE STUDY

The alpha-olefins market has faced an unusual number of challenges andinteresting developments in recent years, including a global recession occurring just aslarge new plants came on stream in 2002; skyrocketing raw material and energy coststhroughout 2003 and 2004; an unexpectedly strong recovery in demand, coupled withtight ethylene supplies, from late 2004 into 2005; hurricanes disrupting ethylene, alpha-olefin and derivative production along the U.S. Gulf coast in the second half of 2005;and the permanent closure of Ineos’ Pasadena, TX alpha-olefins plant, representingclose to 14 percent of global capacity, at the end of 2005.

Demand has continued to grow in the first half of 2006, although somewhat moreslowly than in 2005, but prospects for the full year and for 2007 are good. But foralpha-olefin producers, profitability depends on finding and winning the right mix ofcustomers while optimizing alpha-olefin production and disposition by chain length.

The purpose of CAHA’s new study is to provide LAO producers withcomprehensive data and analysis that will support the development of successfulalpha-olefin production, sales and marketing strategies.

The study is also designed to give LAO customers a better understanding of thecurrent and projected LAO market, especially the factors that affect LAO availability andpricing decisions.

ALPHA-OLEFIN SUPPLY

Three companies continue to dominate the global alpha-olefins market –CPChem, Ineos and Shell – producing a full range of alpha-olefins via ethyleneoligomerization Three others, with smaller capacities, – Idemitsu, Mitsubishi, andNizhnekamskneftekhim – utilize similar process technology. Sasol manufacturespentene-1, hexene-1 and octene-1 from coal-derived synthesis gas, and Q-Chemproduces hexene-1 via ethylene trimerization. In addition, there are over 30 producersof butene-1 from refinery streams.

In 2006 the market is adjusting to last December’s closure of Ineos’ 505,000 ton/yearLAO plant in Pasadena, TX, and anticipating the start-up of SABIC’s new 150,000 ton/yearplant in Saudi Arabia. Also this year, Dow may disclose further details of its plans for anoctene-1 plant that will be based on a different process that utilizes butadiene feedstock.Looking further ahead, Sasol will double its octene-1 capacity with a 100,000 ton/year plantdue on stream in 2007, and CPChem plans to start up a 350,000 ton/year full range LAOplant in 2008 as a joint venture with Qatar Petroleum. CAHA’s new study will analyze theimpact of this new capacity, detailing potential production versus forecast demand by chain

3 COLIN A. HOUSTON & ASSOCIATES, INC.

length annually through 2010, with a projection to 2015.

Alpha-olefin technology is available for license from UOP, Axens and DuPont, andSABIC has not ruled out licensing its proprietary process once its own plant is operatingsuccessfully. New plants are on the drawing board in China, India and Iran. CAHA’s newstudy will discuss the advantages and disadvantages of each available technology, andassess the individual prospects for potential new alpha-olefin producers.

ALPHA-OLEFIN DEMAND

After booming from 1999-2001, alpha-olefin demand growth slowed considerably in2002-2003 during the global economic downturn, but began to rebound in late 2004, andwas especially strong in 2005. Polyolefin comomoners continue to account for well over 50percent of alpha-olefin consumption, and global growth is expected to be quite strongthrough 2010, with HDPE averaging around 4-5 percent/year and LLDPE 6-7 percent/year.Demand has been strong enough to keep both hexene-1 and octene-1 tight in 2006.

Since an unexpected surge in decene-1 demand in 2004, the polyalphaolefin market

12has been constrained by insufficient supplies of decene-1. PAO based on C alpha-olefinhas been available for years, but is gaining new momentum, with new products being

12 14introduced, including a C -C blend from Ineos. The lubricant market continues toembrace Group III base oils, but a potentially greater threat to PAO – GTL base oil – is onthe horizon.

12 18For some of the C to C alpha-olefins, demand is being dampened by high pricesneeded to cover increased raw material costs. In the detergent alcohol market, oleo-basedmaterials are growing more rapidly than ethylene-based alcohols. And a significant portionof alkyldimethylamine production has been switched from alpha-olefin feedstocks to oleo

16-18feedstocks. Demand for C alpha-olefins for alkenyl succinic anhydride and for oilfielddrilling fluids has been strong, but these markets are not immune to rising costs either.

CAHA’s new study will carefully examine each end use for alpha-olefins and all thecurrent and future factors affecting them in order to provide comprehensive quantitativedata and qualitative analysis.

CAHA has extensive files, data, contacts, knowledge and expertise on alpha-olefinswhich provide a unique foundation for this study. New research will be accomplishedthrough an initial literature search, taking advantage of online databases and resources,followed by telephone, e-mail and personal interviews with alpha-olefin producers and usersin each region of the world.

The next few pages describe the electronic version of the study, and its proposeddelivery schedule. Following that is a traditional table of contents for the print version, andsample tables of the data that will be available in both formats.

4 COLIN A. HOUSTON & ASSOCIATES, INC.

ELECTRONIC VERSION

CAHA will set up an electronic database organized by individual sectors of the alpha-olefins market, as outlined below. The database will initially contain the most recentinformation that CAHA has available in-house. Over a seven-month period, CAHA willconduct research to obtain current data and insights for each of the sections, and willupdate the sections according to the schedule shown below.

CAHA has up-to-date information on producers and capacities, and certain end usesas of July 2006. Information which is not up-to-date will require review prior to posting on-line. The entire preliminary database will be available to subscribers by the end of October2006, provided that sufficient subscribers have been obtained by mid-October.

From October 2006 through April 2007 CAHA will conduct research to update eachsection according to the schedule shown below. The study is scheduled to be completedand a final supply/demand balance and executive summary delivered by the end of April2007. The electronic version of the study will be delivered through an Internet databaseaccessible by password. Passwords will be assigned when the study commences.

The first schedule below lists the sections of the study in the traditional order of amulticlient study showing the delivery dates for each section. The second schedule showsthe sections that will be delivered chronologically by month.

In the Project Plan by Section, specific dates listed for each section, e.g., December2006, indicate when complete new information will be available to clients. There will beregular updates thereafter.

5 COLIN A. HOUSTON & ASSOCIATES, INC.

PROJECT PLAN BY SECTION

Chapter Description Completion Dates

I. PRODUCERS AND CAPACITIES

CAPACITY DATABASE

Plant locations and capacities by chain length for 2005 to 2010,

with forecasts to 2015, based on announced new capacity

Regional and global capacity totals

October 2006

Monthly updates

PRODUCER PROFILES

In-depth profiles: corporate overview, process technology,

products, product quality, integration, captive use, merchant sales,

strategic issues

March 2007

II. PRODUCTION

Production by chain length for each producer for 2005 & 2006

Regional and global production by chain length for 2005 through

2010, and 2015.

April 2007

III. CONSUMPTION SUMMARY

Consumption by end use and by chain length

and by region for 2005 through 2010 and 2015April 2007

IV. POLYOLEFINS

POLYOLEFIN PRODUCER DATABASE

Plant locations, capacities, product and catalyst technology,

products and comonomer types used by region for 2006 and

announced new capacity through 2015

November 2006

Monthly updates

CONSUMPTION

Comonomer consumption by polyolefin type, by chain length and

by region for 2005 through 2010 and 2015

March 2007

V. DETERGENT ALCOHOLS

ALCOHOL PRODUCER DATABASE

Plant locations, capacities, products, feedstocks, process

technology, products by region for 2006 and announced new

capacity through 2015

October 2006

Monthly updates

CONSUMPTION

Alpha-olefin consumption by product and by chain length and by

region for 2005 through 2010 and 2015

October 2006

6 COLIN A. HOUSTON & ASSOCIATES, INC.

Project Plan by Section (continued)

Chapter Description Completion Dates

VII. LINEAR ALKYLBENZENE

LAB PRODUCER DATABASE

Plant locations, capacities, feedstocks, process technology by

region for 2005 through 2010 and 2015

October 2006

Monthly updates

CONSUMPTION

Alpha-olefin consumption by chain length and by region for 2005

through 2010 and 2015

October 2006

VIII. ALKYLDIMETHYLAMINE

ADA PRODUCER DATABASE

Producers, plant locations, capacities, feedstocks, captive/

merchant use by region for 2005 through 2010 and 2015

January 2007

Monthly updates

CONSUMPTION

Alpha-olefin consumption by chain length and by region for 2005

through 2010 and 2015

January 2007

IX. ALPHA-OLEFIN SULFONATE

AOS PRODUCER DATABASE

Producers, plant locations, capacities by region for 2005 through

2010 and 2015

November 2006

Monthly updates

CONSUMPTION

Alpha-olefin consumption by chain length and by region for 2005

through 2010 and 2015

November 2006

X. PLASTICIZER ALCOHOLS

PLASTICIZER ALCOHOL PRODUCER DATABASE

Linear plasticizer alcohol producers, plant locations, capacities,

product types by region for 2005 though 2010 and 2015

December 2006

Monthly updates

CONSUMPTION

Alpha-olefin consumption by chain length and by region for 2005

through 2010 and 2015

December 2006

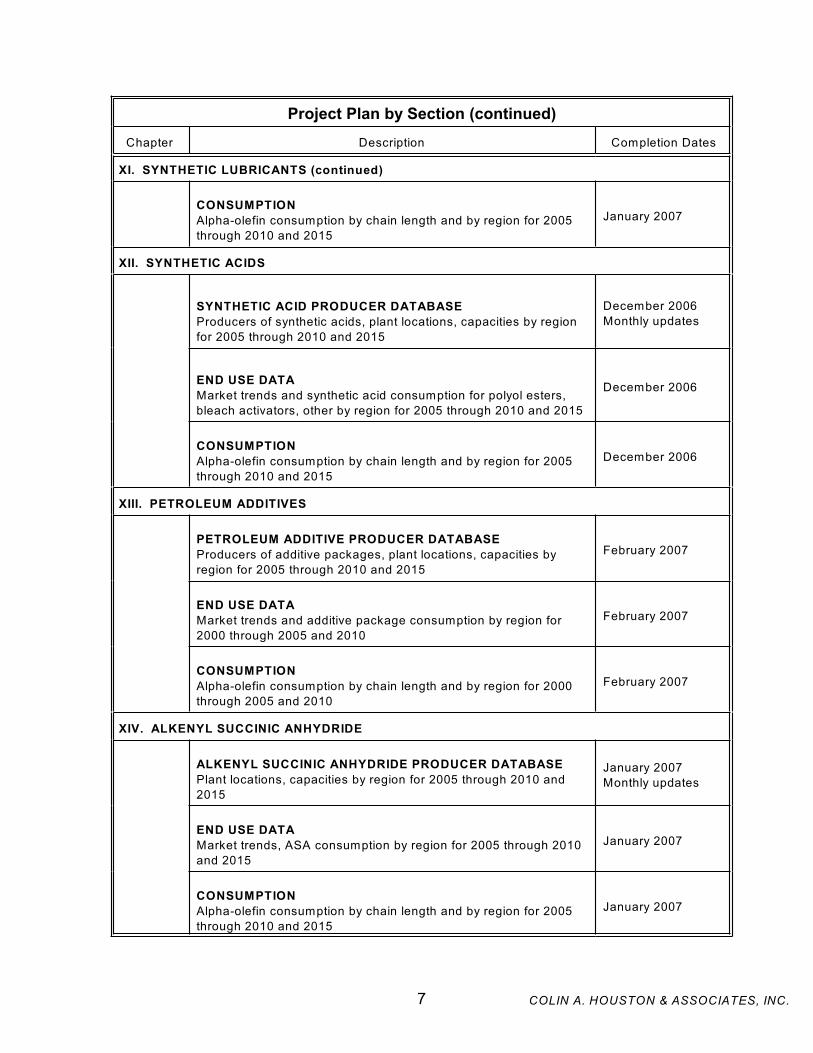

XI. SYNTHETIC LUBRICANTS

POLYALPHAOLEFIN PRODUCER DATABASE

Polyalphaolefin producers, plant locations, capacities, integration

by region for 2005 through 2010 and 2015 based on current

announcements

January 2007

Monthly updates

7 COLIN A. HOUSTON & ASSOCIATES, INC.

Project Plan by Section (continued)

Chapter Description Completion Dates

XI. SYNTHETIC LUBRICANTS (continued)

CONSUMPTION

Alpha-olefin consumption by chain length and by region for 2005

through 2010 and 2015

January 2007

XII. SYNTHETIC ACIDS

SYNTHETIC ACID PRODUCER DATABASE

Producers of synthetic acids, plant locations, capacities by region

for 2005 through 2010 and 2015

December 2006

Monthly updates

END USE DATA

Market trends and synthetic acid consumption for polyol esters,

bleach activators, other by region for 2005 through 2010 and 2015

December 2006

CONSUMPTION

Alpha-olefin consumption by chain length and by region for 2005

through 2010 and 2015

December 2006

XIII. PETROLEUM ADDITIVES

PETROLEUM ADDITIVE PRODUCER DATABASE

Producers of additive packages, plant locations, capacities by

region for 2005 through 2010 and 2015

February 2007

END USE DATA

Market trends and additive package consumption by region for

2000 through 2005 and 2010

February 2007

CONSUMPTION

Alpha-olefin consumption by chain length and by region for 2000

through 2005 and 2010

February 2007

XIV. ALKENYL SUCCINIC ANHYDRIDE

ALKENYL SUCCINIC ANHYDRIDE PRODUCER DATABASE

Plant locations, capacities by region for 2005 through 2010 and

2015

January 2007

Monthly updates

END USE DATA

Market trends, ASA consumption by region for 2005 through 2010

and 2015

January 2007

CONSUMPTION

Alpha-olefin consumption by chain length and by region for 2005

through 2010 and 2015

January 2007

8 COLIN A. HOUSTON & ASSOCIATES, INC.

Project Plan by Section (continued)

Chapter Description Completion Dates

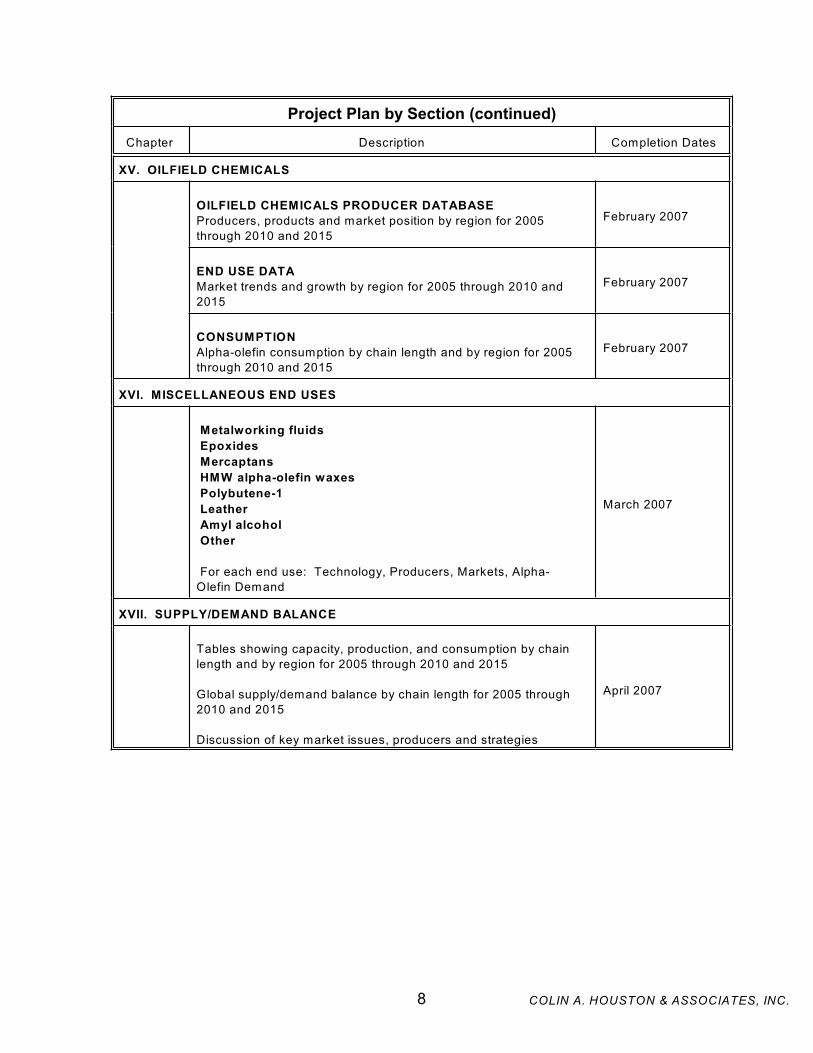

XV. OILFIELD CHEMICALS

OILFIELD CHEMICALS PRODUCER DATABASE

Producers, products and market position by region for 2005

through 2010 and 2015

February 2007

END USE DATA

Market trends and growth by region for 2005 through 2010 and

2015

February 2007

CONSUMPTION

Alpha-olefin consumption by chain length and by region for 2005

through 2010 and 2015

February 2007

XVI. MISCELLANEOUS END USES

Metalworking fluids

Epoxides

Mercaptans

HMW alpha-olefin waxes

Polybutene-1

Leather

Amyl alcohol

Other

For each end use: Technology, Producers, Markets, Alpha-

Olefin Demand

March 2007

XVII. SUPPLY/DEMAND BALANCE

Tables showing capacity, production, and consumption by chain

length and by region for 2005 through 2010 and 2015

Global supply/demand balance by chain length for 2005 through

2010 and 2015

Discussion of key market issues, producers and strategies

April 2007

9 COLIN A. HOUSTON & ASSOCIATES, INC.

PROJECT PLAN BY MONTH

2006

October Complete Preliminary Database Posted

Alpha-olefin Capacity Database

Detergent Alcohols

Linear Alkylbenzene

November Polyolefin Capacity Database

Alpha-olefin Sulfonates

December Synthetic Acids

Plasticizer Alcohols

2007

January Alkyldimethylamines

Alkenyl Succinic Anhydride

Synthetic Lubricants

February Petroleum Additives

Oilfield Chemicals

March Polyolefin Comonomers

Miscellaneous End Uses

Alpha-Olefin Producer Profiles

April Alpha-olefin Supply/Demand Balance

Executive Summary

10 COLIN A. HOUSTON & ASSOCIATES, INC.

TENTATIVE PRINT VERSION TABLE OF CONTENTS

I. REGIONAL ALPHA-OLEFIN MARKETSWorld Overview

CapacityProductionConsumption

Regions: North America, Latin America, West Europe, Asia, OtherFor each region:

CapacityProducersProduction by chain lengthConsumption by chain lengthPricing

II. PRODUCERSRefinery Stream Butene-1

Producers, Plant Locations and Capacities

6Producers (C +): Chevron Phillips, Godrej, Idemitsu, Ineos, Mitsubishi,Nizhnekamskneftekhim, SABIC, Sasol, Shell

For each producer:Plant Locations and Capacities

Recent and Future ExpansionsProduction Technology and EconomicsProduction by Chain LengthIntegration

Feedstock SituationCaptive vs Merchant Use

Alpha-Olefin Technology Available for LicenseAxensDuPontUOP

Potential ProducersDowRelianceNPC (Iran)Others

III. END USE MARKETS FOR ALPHA-OLEFINSWorld Summary

By End UseBy Chain Length

11 COLIN A. HOUSTON & ASSOCIATES, INC.

IV. POLYOLEFIN COMONOMERSPolyolefin Technology

Process and Catalyst SummaryTechnologies available for license

HDPEHMWHDPEUHMWHDPELLDPEVLDPE/PlastomersPolyolefin ElastomersPolypropylene Multipolymers

Polyolefin Producers and Capacities by RegionRegions: North America, Latin America, West Europe, Asia, OtherFor each producer: Ownership, integration, plant/product details

For each plant:LocationProcess/CatalystCapacity and planned expansionsComonomer type(s) used

Polyolefin Markets by RegionRegions: North America, Latin America, West Europe, Asia, OtherFor each region:

LLDPEAlpha-olefin Consumption by Type/Chain Length

HDPEAlpha-olefin Consumption by Type/Chain Length

VLDPE/PlastomersAlpha-olefin Consumption by Type/Chain Length

Polyolefin ElastomersAlpha-olefin Consumption by Type/Chain Length

Polypropylene MultipolymersAlpha-olefin Consumption by Type/Chain Length

V. SURFACTANTS AND INTERMEDIATESDetergent Alcohols

Sources and TechnologiesMarkets

Regions: North America, Latin America, West Europe, Asia, OtherFor each region:

Producers and Capacities

12 COLIN A. HOUSTON & ASSOCIATES, INC.

ProductionAlpha-Olefin Demand by Chain Length

Linear AlkylbenzeneSources and TechnologiesMarkets

Regions: North America, Latin America, West Europe, Asia, OtherFor each region:

Producers and CapacitiesProductionAlpha-Olefin Demand by Chain Length

AlkyldimethylaminesSources and TechnologiesMarkets

Regions: North America, Latin America, West Europe, Asia,Other

For each region:Producers and CapacitiesProductionAlpha-Olefin Demand by Chain Length

Alpha-olefin SulfonatesSources and TechnologiesMarkets

Regions: North America, Latin America, West Europe, Asia,Other

For each region:Producers and CapacitiesProductionAlpha-Olefin Demand

VI. PLASTICIZER ALCOHOLSPlasticizer Alcohols

TechnologyProducts

2-EthylhexanolIso AlcoholsLinear Alcohols

PlasticizersEnvironmental & Health IssuesLinear Plasticizer Alcohol Markets

Regions: North America, Latin America, West Europe, Asia, OtherFor each region:

Producers and CapacitiesProductionAlpha-Olefin Demand

13 COLIN A. HOUSTON & ASSOCIATES, INC.

VII. SYNTHETIC LUBRICANTSTechnology

Raw MaterialsPolyalphaolefinsUnconventional/Group III Base OilsNeopolyol EstersDibasic Acid EstersOther

Finished LubricantsAutomotive LubricantsIndustrial LubricantsAircraft Lubricants

World Lubricant MarketProducersConsumption by Market Segment and by Region

Polyalphaolefin Markets by RegionRegions: North America, Latin America, West Europe, Asia, OtherTypes: Low viscosity PAO and High viscosity PAOFor each region:

Review of Major Lubricant MarketsSynthetic Lubricant Consumption by TypePolyalphaolefin Producers and Capacities by TypePolyalphaolefin Production and Consumption by TypeAlpha-Olefin Demand by Chain Length for Polyalphaolefin Manufacture by Type

VIII. SYNTHETIC ACIDSTechnologyEnd Uses

Polyol EstersBleach ActivatorsOther

5 7 9Alpha-Olefin Derivatives (C , C , C ) vs.Fatty Acids from Other SourcesMarkets

Regions: North America, Latin America, West Europe, Asia, OtherFor each region:

Producers and CapacitiesProductionConsumptionAlpha-Olefin Demand by Chain Length

IX. PETROLEUM ADDITIVESTechnology

Lube Oil PerformanceAdditives

14 COLIN A. HOUSTON & ASSOCIATES, INC.

Types and FunctionMarkets

Regions: North America, Latin America, West Europe, Asia, OtherFor each region:

Petroleum Additive Producers/ProductsAlpha-Olefin Demand by Chain Length

X. ALKENYL SUCCINIC ANHYDRIDETechnologyMarkets

Regions: North America, Latin America, West Europe, Asia, OtherFor each region:

ProducersProductionConsumption

PaperOther

Alpha-Olefin Demand by Chain Length

XI. OILFIELD CHEMICALSIntroduction

Oil IndustryOilfield Chemical Companies

TechnologyDrilling FluidsEnhanced Oil RecoveryDrag Reducers

MarketsRegions: North America, Latin America, West Europe, Asia, OtherFor each region:

ProducersUtilizationAlpha-Olefin Demand by Chain Length

XII. MISCELLANEOUS END USESEnd uses:

Metalworking FluidsEpoxidesMercaptansHigh Molecular Weight Alpha-Olefin WaxesPolybutene-1LeatherAmyl AlcoholMiscellaneous Other

For each end use:Technology

15 COLIN A. HOUSTON & ASSOCIATES, INC.

ProducersMarketsAlpha-Olefin Demand by Chain Length

XIII. APPENDIXList of AbbreviationsList of Contacts

16 COLIN A. HOUSTON & ASSOCIATES, INC.

SAMPLE TABLES

Sample Table 1

W ORLD - ALPHA-OLEFIN PRODUCTION BY REGION, 2005-2015

(thousand tons)

Region 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

North America

W est Europe

Asia

Other Regions

TOTAL

Sample Table 2

W ORLD - ALPHA-OLEFIN PRODUCTION BY CHAIN LENGTH, 2005-2015

(thousand tons)

Chain Length 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

4C

6C

8C

10C

12C

14C

16C

18C

20+C

TOTAL

17 COLIN A. HOUSTON & ASSOCIATES, INC.

Sample Table 3

W ORLD - ALPHA-OLEFIN CONSUMPTION IN ALL APPLICATIONS, 2005-2015

(thousand tons)

2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

POLYOLEFIN COMONOMERS

HDPE

LLDPE

VLDPE/Plastomers

Elastomers

Polypropylene Multipolymers

Subtotal

SURFACTANTS AND INTERMEDIATES

Detergent Alcohols

Linear Alkylbenzene

Alkyldimethylamines

Alpha-olefin Sulfonates

Subtotal

Plasticizer Alcohols

Synthetic Lubricants

Synthetic Acids

Petroleum Additives

Alkenyl Succinic Anhydride

Oilfield Chemicals

Miscellaneous End Uses

GRAND TOTAL

18 COLIN A. HOUSTON & ASSOCIATES, INC.

Sample Table 4

NIZHNEKAMSKNEFTEKHIM - ALPHA-OLEFIN

PRODUCTION BY CHAIN LENGTH, 2005

(thousand tons)

Carbon

Chain Length Production

Percent of Total

Production

4C

6C

8C

10C

12C

14C

16C

18C

20+C

TOTAL

Sample Table 5

SABIC - ALPHA-OLEFIN CAPACITY BY CHAIN LENGTH, 2006

(thousand tons)

Carbon

Chain Length Capacity

Percent of Total

Capacity

4C

6C

8C

10C

12-18C

20+C

TOTAL

19 COLIN A. HOUSTON & ASSOCIATES, INC.

Sample Table 6

W ORLD TOTAL - ALPHA-OLEFIN END USE CONSUMPTION BY CHAIN LENGTH, 2008

(thousand tons)

4 6 8 10 12 14 16 18 20+End Use C C C C C C C C C TOTAL

POLYOLEFIN COMONOMERS

HDPE

LLDPE

VLDPE/Plastomers

Elastomers

Polypropylene Multipolymers

Subtotal

SURFACTANTS AND INTERMEDIATES

Detergent Alcohols

Linear Alkylbenzene

Alkyldimethylamines

Alpha-olefin Sulfonates

Subtotal

Plasticizer Alcohols

Synthetic Lubricants

Synthetic Acids

Petroleum Additives

Alkenyl Succinic Anhydride

Oilfield Chemicals

Miscellaneous End Uses

GRAND TOTAL

20 COLIN A. HOUSTON & ASSOCIATES, INC.

Sample Table 7

W ORLD - ALPHA-OLEFIN DEMAND FOR HDPE PRODUCTION BY REGION, 2005-2015

(thousand tons)

2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

North America

Latin America

W est Europe

Asia

Other Regions

TOTAL

Sample Table 8

LATIN AMERICA - ALPHA-OLEFIN DEMAND FOR LLDPE

PRODUCTION BY CHAIN LENGTH, 2005-2015

(thousand tons)

Chain

Length 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

4 C

6 C

8 C

TOTAL

21 COLIN A. HOUSTON & ASSOCIATES, INC.

Sample Table 9

W ORLD - ALKYLDIMETHYLAMINE PRODUCTION BY SOURCE, 2005-2015

(thousand tons)

Process 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

from olefin

from alcohol

from acid

TOTAL

Sample Table 10

ASIA - AOS PRODUCTION BY CHAIN LENGTH, 2005-2015

(thousand tons)

Chain

Length 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

14C

16C

18C

TOTAL

Sample Table 11

W EST EUROPE - ALPHA-OLEFIN DEMAND FOR POLYALPHAOLEFIN

PRODUCTION BY CHAIN LENGTH, 2005-2015

(thousand tons)

Chain

Length 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

8 C

10 C

12 C

TOTAL

22 COLIN A. HOUSTON & ASSOCIATES, INC.

Sample Table 12

5 7 9NORTH AMERICA - CONSUMPTION OF LINEAR C , C , AND C ACID

FROM ALL SOURCES BY END USE, 2005-2015

(thousand tons)

End Use 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

Synthetic Lubricants

NOBS Production

Other

TOTAL

Sample Table 13

ASIA - ALPHA-OLEFIN DEMAND FOR PETROLEUM ADDITIVE

PRODUCTION BY CHAIN LENGTH, 2005-2015

(thousand tons)

Chain

Length 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

12 C

14C

16C

18 C

20+ C

TOTAL

23 COLIN A. HOUSTON & ASSOCIATES, INC.

Sample Table 14

W EST EUROPE - PRODUCTION OF ALPHA-OLEFIN DERIVED ASA

BY CHAIN LENGTH, 2005-2015

(thousand tons)

Chain Length 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

8C

16C

18C

20+C

TOTAL

Sample Table 15

NORTH AMERICA - INTERNAL AND ALPHA-OLEFIN DEMAND FOR

OILFIELD USES BY CHAIN LENGTH, 2005-2015

(thousand tons)

Chain Length 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

6C

8C

10C

14C

16C

18C

20+C

TOTAL

24 COLIN A. HOUSTON & ASSOCIATES, INC.

Sample Table 16

W ORLD - ALPHA-OLEFIN DEMAND FOR MISCELLANEOUS END USES, 2005-2015

(thousand tons)

End Use 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

Metalworking

Epoxides

Mercaptans

HMW W axes

Polybutene-1

Leather

Amyl Alcohol

Misc. Other

TOTAL

Sample Table 17

ASIA - ALPHA-OLEFIN DEMAND FOR METALW ORKING FLUIDS

AND ADDITIVES BY CHAIN LENGTH, 2005-2015

(thousand tons)

Chain Length 2005 2006 2007 2008 2009 2010 2015

AAGR %

2005-2015

10C

12C

14C

16C

18C

TOTAL

25 COLIN A. HOUSTON & ASSOCIATES, INC.

QUALIFICATIONS AND PERSONNEL

Colin A. Houston & Associates, Inc. was founded in 1971 to provide consulting services tothe chemical industry worldwide. The primary area of expertise was and continues to besurfactants: raw materials, intermediates, major surfactants, and the surfactant-consumingindustries. Other areas of activity include: a variety of industry studies on such topics asoilfield chemicals, detergent builders, ingredients for personal care products, and bleachingagents; engineering studies such as a worldwide study of glycerine evaporation plants withrecommendations for improved efficiency; a world study of the state of the art in spray-drying detergents; contracts with the U.S. Government to develop industry effluentguidelines; and business strategy and acquisition studies.

The reputation thus earned by CAHA for comprehensive, high quality techno-economic andmarket analyses has led to a variety of engineering, marketing, and strategic planningstudies for individual clients in North America, Latin America, West Europe, Asia, the MiddleEast and Africa.

CAHA has been studying alpha-olefin markets for most of its 35 year history. In 1980,CAHA was commissioned to undertake a major proprietary study of North American andWest European alpha-olefin markets. In 1988, CAHA published its first world multiclientstudy on alpha-olefins. A second comprehensive study was completed in 1994, and a thirdmulticlient study in 2001. CAHA also published a multiclient study of global markets forpolyolefin comonomers in 1999. In addition, since 1989 CAHA has published a monthlyalpha-olefin newsletter covering pricing and market developments for alpha-olefins and forpolyolefins and other end uses for alpha-olefins.

The project team approach utilized by CAHA includes a core of senior and technicalprofessionals augmented by expert consultant associates. The following synopses presentthe staff and consultants who will carried out the study, Alpha-Olefins - World Markets,

2005-2015.

Marilyn L. Bradshaw, Vice President,was the project leader for ALPHA-OLEFINS - WORLD MARKETS, 2000-2010 AND

ALPHA-OLEFIN MARKET INTELLIGENCE DATABASE. She is also the author andeditor of CAHA’s monthly alpha-olefin newsletter, and provides consultation to clientson alpha-olefins. Ms. Bradshaw was also the project leader for POLYOLEFINCOMONOMERS - WORLD MARKETS, 1995-2005 and ALPHA-OLEFINS - WORLDMARKETS, 1990-2002. Other recent multiclient studies she has directed includeU.S. I&I CLEANING PRODUCTS - SURFACTANT SUPPLIERS AND CUSTOMERS,and INDUSTRIAL APPLICATIONS OF SURFACTANTS - NORTH AMERICANFORECAST TO 2010. Since joining CAHA in 1980, she has also been the projectleader for numerous proprietary projects. Ms. Bradshaw has a B.A. from FinchCollege and an economics and management certificate from Manhattanville College.

26 COLIN A. HOUSTON & ASSOCIATES, INC.

Joel H. Houston, President,

authored the Detergent Alcohols section of ALPHA-OLEFINS - WORLD MARKETS,

2000-2010 AND ALPHA-OLEFIN MARKET INTELLIGENCE DATABASE. In addition,

Mr. Houston was the project leader for numerous multiclient studies including HIGHER

ALCOHOLS - FORECAST TO 2020, SURFACTANTS FOR EMERGING MARKETS IN

ASIA/PACIFIC, 1996-2010, OPPORTUNITIES IN PERFORMANCE SURFACTANTS IN

THE U.S., SURFACTANTS FOR CONSUMER PRODUCTS - NORTH AMERICAN

FORECAST TO 2008, and DETERGENT ALKYLATES - WORLD MARKETS, 1992-

2005. He has guided CAHA's research in oleochemicals since 1980, and in detergents

since 1987. Mr. Houston has extensive experience in projects for consumer products,

has presented papers at CMRA, ECMRA and CSMA meetings, and is the editor of

CAHA's global detergent newsletters, AGGLOMERATIONS, LAB MARKET REPORT

and SURFACTANT DEVELOPMENT NEWSLETTER. He is a member of CDMA, AOCS

and ASTM.

H. James Bigalow, Senior Research Associate,

authored several sections of ALPHA-OLEFINS - WORLD MARKETS, 2000-2010 AND

ALPHA-OLEFIN MARKET INTELLIGENCE DATABASE. In addition he has contributed

to numerous multiclient studies including HIGHER ALCOHOLS - FORECAST TO 2020,

SURFACTANTS FOR CONSUMER PRODUCTS - NORTH AMERICAN FORECAST TO

2010, INDUSTRIAL APPLICATIONS OF SURFACTANTS - NORTH AMERICAN

FORECAST TO 2010, SURFACTANTS FOR EMERGING MARKETS IN ASIA/PACIFIC,

1995-2010 and DETERGENT ALKYLATES - WORLD MARKETS, 1995-2010. Mr.

Bigalow has also worked on proprietary detergent and surfactant studies. Mr. Bigalow

has over 20 years experience as a senior marketing research executive in the chemical

industry. He has conducted successful business analysis projects which have included

financial evaluations of businesses and acquisition candidates, identifying current and

future markets for new and existing products, and product development and usage.

Additional experience has included economic and sales forecasting, strategic planning,

proprietary market research projects, benchmarking, and product safety. He is a

member of the CDMA, the Society of Competitive Intelligence Professionals (SCIP), ACS

and the Chemical Marketing and Economics Division of the ACS. Mr. Bigalow holds an

M.S. Industrial Administration, Krannert School of Management, Purdue University and a

B.S. degree in Chemistry, Denison University.

Mack Hunt, Senior Research Consultantauthored the Synthetic Lubricants, Petroleum Additives and Metalworking Fluidssections of ALPHA-OLEFINS - WORLD MARKETS, 2000-2010 AND ALPHA-OLEFIN

MARKET INTELLIGENCE DATABASE. He has over 35 years of experience in thecreation, synthesis, development, manufacture and management of fuel andlubricating oil additives. Mr. Hunt is an internationally know expert in motor oildetergents and has authored or co-authored 53 U.S. patents and many foreignpatents. He authored U.S. GASOLINE DETERGENT ADDITIVES, 1997-2004 andthe U.S. portion of GASOLINE DETERGENT ADDITIVES - UNITED STATES ANDWEST EUROPE II, 1992-2002 as well as the Petroleum Additives section of ALPHA-OLEFINS - WORLD MARKETS, 1990-2002. He also conducted a globalpolyisobutylene market study and proprietary studies of market prospects forgasoline detergent additives. He holds an A.B. Chemistry, Math and Biology,

27 COLIN A. HOUSTON & ASSOCIATES, INC.

Nebraska Wesleyan University and an M.S. Organic Chemistry, University ofNebraska.

Pete LaChappelle, Senior Research Associatehas worked with CAHA on several proprietary reports. Mr. LaChappelle has hada long and distinguished career in the Lubricants, Metalworking Fluids andLubricant Chemical industry. He has also directed sales efforts in the coatingsand synthetic lubricant markets. He has a B.S. degree in Biology - Chemistryfrom Holy Cross College.

John Rapko, Senior Research Associateauthored the Higher Alcohols Technology section of HIGHER ALCOHOLS -FORECAST TO 2020 report and has also assisted on numerous proprietary reports.Dr. Rapko has over 32 years of professional experience in various positions. In hisprofessional career he has directed the work of professional chemists and chemicalengineers at all degree levels in the areas of process development, chemistry,engineering and assessment of technologies related to the manufacture of detergentalkylate, detergent builders, zeolites, dehydrogenation catalysts, antimicrobials,amines, amino acids, chlorophenols, alkylphenols and alkylphenol ethoxylates,methyl ester sulfonates, phosphonates, bleaches and bleach ingredients, bleachacribators, polymeric sequestrants and deflocculants, phosphorus chemicals,synthesis of C labeled materials for environmental assessment, waste minimization14

and remediation including incineration and processes for sulfuric acid recovery,construction and operation of bench scale evaluation and pilot units, projecteconomies and start-up of commercial scale units. He holds a Ph.D. and B.S. inChemistry (ACS Certified) from St. Louis University.

Joseph Polak, Research Associateauthors portions of our bimonthly LAB Market Newsletter. He has also contributed to a

proprietary study of the LAB markets in Asia and the Middle East. He holds a B.S.degree in Chemistry from Fordham University.

28 COLIN A. HOUSTON & ASSOCIATES, INC.

HOW TO SUBSCRIBE

To subscribe to the study please complete and sign the detachable contract and mailto the address below. On receipt, we will countersign it and return a photocopy to you foryour files along with our invoice for the first one-third payment.

Colin A. Houston & Associates, Inc.20 Milltown Road, Suite 206

Brewster, NY 10509 USATelephone No.: (845) 279-7891

Fax No.: (845) 279-7751E-Mail: [email protected]

http://www.colin-houston.com