Allocating Capital Gains to Distributable Net Income...

36

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. NOTE: If you are seeking CPE credit , you must listen via your computer — phone listening is no longer permitted. Allocating Capital Gains to Distributable Net Income in Estates and Trusts: Achieving Optimal Tax Treatment Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific WEDNESDAY, JULY 1, 2015 Presenting a live 110-minute webinar with interactive Q&A Andrew Whitehair, Principal/Director, Cohen & Company, Cleveland Diana S.C. Zeydel, Shareholder, Greenberg Traurig, Miami

Transcript of Allocating Capital Gains to Distributable Net Income...

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no

longer permitted.

Allocating Capital Gains to Distributable Net

Income in Estates and Trusts: Achieving

Optimal Tax Treatment

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, JULY 1, 2015

Presenting a live 110-minute webinar with interactive Q&A

Andrew Whitehair, Principal/Director, Cohen & Company, Cleveland

Diana S.C. Zeydel, Shareholder, Greenberg Traurig, Miami

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-320-7825 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address the

problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone

listening is no longer permitted.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you

will receive immediately following the program.

For additional information about CLE credit processing call us at 1-800-926-7926 ext.

35.

For CPE credits, attendees must participate until the end of the Q&A session and

respond to five prompts during the program plus a single verification code. In addition,

you must confirm your participation by completing and submitting an Attendance

Affirmation/Evaluation after the webinar and include the final verification code on the

Affirmation of Attendance portion of the form.

For additional information about CPE credit processing call us at 1-800-926-7926 ext.

35.

FOR LIVE EVENT ONLY

Allocating Capital Gains to Distributable Net Income in Estates and Trusts ACHIEVING OPTIMAL TAX TREATMENT

Andrew Whitehair, Director, Cohen & Company, Cleveland, OH Diana S.C. Zeydel, Shareholder, Greenberg Traurig, Miami, FL

Current Trust Income Tax Environment ATRA freezes income tax rates at 2012 levels and preserves Bush tax cuts except for the top bracket.

Changes to the top income tax brackets: ◦ 39.6% on ordinary income and short term capital gains

◦ 20% on long term capital gains and qualified dividend income

In 2015, the top income tax bracket is effective for trusts and estates with taxable income over $12,300.

5

Current Income Tax Environment ACA implements new 3.8% Net Investment Income Tax (NIIT) applicable to trusts and estates.

Applicable for trusts and estates with modified adjusted gross income in excess of $12,300 (in 2015).

NIIT applies to the lesser of: ◦ Undistributed net investment income, or

◦ Excess of modified adjusted gross income over the applicable threshold for the tax year (i.e. $12,300 in 2015)

6

Trust Capital Gains TOP MARGINAL FEDERAL RATE FOR LONG TERM CAPITAL GAINS

TOP MARGINAL FEDERAL RATE FOR SHORT TERM CAPITAL GAINS

* Above does not include the potential impact of state income taxes

7

2015 Federal Income Tax Rates and Brackets

Taxable income greater than < or = 2,500 2,500 5,900 9,050 12,300

Ordinary Rate 15% 25% 28% 33% 39.6%

Cap Gains/Qual. Divs 0% 15% 15% 15% 20%

NIIT Rate 0% 0% 0% 0% 3.8%

Trusts & Estates

Taxable income greater than < or = 9,225 9,225 37,450 90,750 189,300 411,500 413,200

Ordinary Rate 10% 15% 25% 28% 33% 35% 39.6%

Cap Gains/Qual. Divs 0% 0% 15% 15% 15% 15% 20%

NIIT Rate* 0% 0% 0% 0% 3.8% 3.8% 3.8%

*Applies for Single taxpayer if Modified Adjusted Gross Income is greater than $200,000

Individuals Filing Single

8

Fiduciary Income Taxation Distributable Net Income (“DNI”)

◦ Tax concept

◦ Taxable income of the trust with modifications: ◦ Capital gains generally excluded

◦ Short term capital gain dividends from mutual funds included

◦ Net tax-exempt interest included

◦ Limit for beneficiary’s taxable income

◦ Determines character of income

◦ Income distribution deduction

Fiduciary accounting income (“FAI”) ◦ Determined by the governing instrument and applicable local law

◦ Not a tax concept but important in determining income tax treatment

◦ IRC Sec. 643(b)

9

Example 1 – Fiduciary Income Taxation ◦ “A Trust” is required to distribute all income to B, during her life, with the

remainder to children. The governing instrument is silent regarding the treatment of capital gains, but the governing state has adopted the 1997 UPAIA. The trustee invests for total return with a 70/30 allocation between equities and fixed income. In 2014, the trust has $50,000 of dividend income ($30,000 qualified) and $50,000 of realized long-term capital gain income from the sale or exchange of assets.

◦ FAI = $50,000

◦ Income distribution deduction = $50,000

◦ Trust taxable income = $49,700 ($50,000 - $300 exemption)

10

Planning opportunity example Using same facts as Example #1 plus B’s income as follows:

◦ Social security income: $25,000

◦ Interest income: $750

◦ Qualified dividend Income: $5,000

◦ Capital gain distributions: $5,000

◦ IRA distribution: $15,000

What is the benefit of tax rate arbitrage?

11

Planning opportunity example (cont) Net tax savings of distributing capital gains: $2,885

What options does the trustee have to pass out capital gains to the beneficiary?

CG not in DNI CG in DNI

Beneficiary B 13,575 21,075

Trust A 10,385 -

Total Tax: 23,960 21,075

* 2014 income tax brackets & rates

Federal Tax

12

Capital Gains and DNI IRC Sec. 643 excludes capital gains from DNI to the extent such gains are allocated to corpus.

Sec. 404 of the 1997 UPAIA allocates money or property received from the sale, exchange, or liquidation of an asset to principal.

1997 UPAIA reflects the concept of “total return investing.”

2004 final Sec. 643 regulations intended to provide additional tax guidance in wake of the revised UPAIA.

13

Final Regulations Final regulations under Regs. Sec. 1.643(a)-3 discuss when capital gains are includible in DNI:

Gains from the sale or exchange of capital assets are included in distributable net income to the extent they are, pursuant to the terms of the governing instrument and applicable local law, or pursuant to a reasonable and impartial exercise of discretion by the fiduciary (in accordance with a power granted to the fiduciary by applicable local law or by the governing instrument if not prohibited by applicable local law)— (1) Allocated to income (but if income under the state statute is defined as, or consists of, a unitrust amount, a discretionary power to allocate gains to income must also be exercised consistently and the amount so allocated may not be greater than the excess of the unitrust amount over the amount of distributable net income determined without regard to this subparagraph Regs. Sec. 1.643(a)-3(b); (2) Allocated to corpus but treated consistently by the fiduciary on the trust's books, records, and tax returns as part of a distribution to a beneficiary; or (3) Allocated to corpus but actually distributed to the beneficiary or utilized by the fiduciary in determining the amount that is distributed or required to be distributed to a beneficiary.

14

Regulations – Exception 1 Capital gains actually allocated to income per the governing instrument or a reasonable and impartial exercise of discretion by the fiduciary.

Under this exception, capital gains are allocated to fiduciary accounting income and thus included in DNI.

Several different scenarios to which this exception applies: ◦ Trust agreement allocates gains to income

◦ Power of adjustment

◦ Unitrust provision

◦ Discretionary power to allocate gains to income

15

Capital Gains Allocated to Income Regs. Sec. 1.643(b)-1 – “…an allocation to income of all or a part of the gains from the sale or exchange of trust assets will generally be respected if the allocation is made either pursuant to the terms of the governing instrument and applicable local law, or pursuant to a reasonable and impartial exercise of a discretionary power granted to the fiduciary by applicable local law or by the governing instrument, if not prohibited by applicable local law.”

16

Exception 1 – Trust agreement allocates capital gains to income

Governing instrument calls for capital gains to be included in income and this provision is not prohibited by local law.

Illustrated by Example 4 of the regulations: ◦ The facts are the same as in Example 1, except that pursuant to the terms of

the governing instrument (in a provision not prohibited by applicable local law), capital gains realized by Trust are allocated to income. Because the capital gains are allocated to income pursuant to the terms of the governing instrument, the $10,000 capital gain is included in Trust's distributable net income for the taxable year.

17

Exception 1 “Power of adjustment” under UPAIA

Capital gain allocated to income pursuant to “power of adjustment” allowed under UPAIA section 104.

◦ Power of adjustment available when:

◦ fiduciary invests and manages the trust as a prudent investor

◦ terms of the trust describe the amount that may or must be distributed by referring to the trust’s income, and

◦ the trustee exercises the power to adjust impartially based on what is fair and reasonable to all beneficiaries.

◦ No guidance in the tax code as IRS declined to include examples of including capital gains in DNI pursuant to a power of adjustment (preamble to TD 9102).

◦ Consistency needed?

18

Exception 1 – Unitrust Provision Not addressed by UPAIA but provided for under state law.

FAI calculated as a percentage of the trust’s assets as of the beginning of the year or averaged over several years.

Consistent with total return investing and administratively simple.

IRS addresses taxable treatment of unitrusts in examples 11-14 of the final regulations.

19

Exception 1 – Unitrust Provision Taxable treatment of unitrust election depends upon whether an ordering rule is in effect either via state law or the governing instrument.

If the applicable state statute provided for the order from which the unitrust should first be considered paid, then the ordering rule will determine taxable treatment.

For example, state statute provides that this unitrust amount shall be considered paid first from ordinary and tax-exempt income, then from net short-term capital gain, then from net long-term capital gain and finally from return of principal. Trust's governing instrument provides that A is to receive each year income as defined under state statute. Trustee makes the unitrust election under state statute. At the beginning of the taxable year, Trust assets are valued at $500,000. During the year, Trust receives $5,000 of dividend income and realizes $80,000 of net long-term gain from the sale of capital assets. Trustee distributes to A $20,000 (4% of $500,000) in satisfaction of A's right to income. Net long-term capital gain in the amount of $15,000 is allocated to income pursuant to the ordering rule of the state statute and is included in distributable net income for the taxable year. (Regs. Sec. 1.643(a)-3(e) Example 11)

20

Exception 1 – Unitrust Provision What if the state statute and governing instrument both do not contain an ordering rule for the character of the unitrust amount but rather gives the trustee the discretion to determine the character?

Examples 12 and 13 of the final regulations discuss this scenario and allow capital gain to be distributed to the beneficiary provided the trustee follows this treatment consistently in future years.

As seen in Example 11, the unitrust amount is the upper limit for the amount of capital gain that can be distributed thus potentially resulting in incomplete income shifting.

Preamble to T.D. 9102 clearly indicates that “in implementing a different method for determining income under a state statute, the trustee may establish a pattern for including or not including capital gains in DNI.”

21

Language in the trust explicitly allows the trustee to decide whether capital gains should be trust income or principal.

To be included in DNI, the fiduciary’s exercise of the power must be both reasonable and impartial.

Does the trustee’s power need to be exercised consistently?

Discretionary power under state law.

Exception 1 – Trust agreement grants fiduciary a discretionary power to allocate capital gain to income

22

Exception 2 Allocated to corpus but consistently treated as part of a distribution

Discretionary principal distributions can be included in DNI under this exception.

Example 1 of the Final Regulations addresses this scenario: ◦ Under the terms of Trust's governing instrument, all income is to be paid to A for

life. Trustee is given discretionary powers to invade principal for A's benefit and to deem discretionary distributions to be made from capital gains realized during the year. During Trust's first taxable year, Trust has $5,000 of dividend income and $10,000 of capital gain from the sale of securities. Pursuant to the terms of the governing instrument and applicable local law, Trustee allocates the $10,000 capital gain to principal. During the year, Trustee distributes to A $5,000, representing A's right to trust income. In addition, Trustee distributes to A $12,000, pursuant to the discretionary power to distribute principal. Trustee does not exercise the discretionary power to deem the discretionary distributions of principal as being paid from capital gains realized during the year. Therefore, the capital gains realized during the year are not included in distributable net income and the $10,000 of capital gain is taxed to the trust. In future years, Trustee must treat all discretionary distributions as not being made from any realized capital gains.

23

Exception 2 Allocated to corpus but consistently treated as part of a distribution

Example 2 of the regulations is exactly the same as Example 1 except that the Trustee decides to treat discretionary principal distribution as first being made from any realized capital gains.

Trustee is bound by their initial decision in all subsequent tax years.

Some state statutes provide this discretion.

Do legislative changes allow a trustee to adopt a new consistent practice?

24

Exception 2 Allocated to corpus but consistently treated as part of a distribution

Exception 2 does not provide a trustee with much flexibility, or does it?

Example 3 seems to give a trustee a substantial amount of flexibility: ◦ The facts are the same as in Example 1, except that Trustee intends to follow

a regular practice of treating discretionary distributions of principal as being paid from any net capital gains realized by Trust during the year from the sale of certain specified assets or a particular class of investments. This treatment of capital gains is a reasonable exercise of Trustee's discretion.

Practical implications of Example 3. ◦ Definitions of specified assets or particular class

◦ Election deadline

25

Exception 3 – Allocated to corpus but actually distributed

Capital gains allocated to principal but actually distributed or used by the fiduciary in determining the amount that is distributed or required to be distributed to a beneficiary may be included in DNI.

Remaining examples in the regulations pertain to various scenarios illustrating exception 3.

◦ Trust termination

◦ Age attainment provisions

◦ Distributions based on capital gains

◦ Distributions of sales proceeds

26

Exception 3 – Trust termination Example 7 - Under the terms of Trust's governing instrument, all income is to be paid to A during the Trust's term. When A reaches 35, Trust is to terminate and all the principal is to be distributed to A. Because all the assets of the trust, including all capital gains, will be actually distributed to the beneficiary at the termination of Trust, all capital gains realized in the year of termination are included in distributable net income. See Regs. Sec. 1.641(b)-3 for the determination of the year of final termination and the taxability of capital gains realized after the terminating event and before final distribution.

In trust’s final year, capital gains will be included in DNI and pass out to the beneficiary.

27

Exception 3 – Age attainment Example 9 - The facts are the same as Example 7, except Trustee is directed to distribute one-half of the principal to A when A reaches 35 and the balance to A when A reaches 45. Trust assets consist entirely of stock in corporation M with a fair market value of $1,000,000 and an adjusted basis of $300,000. When A reaches 35, Trustee sells one-half of the stock and distributes the sales proceeds to A. All the sales proceeds, including all the capital gain attributable to that sale, are actually distributed to A and therefore all the capital gain is included in distributable net income.

Distribution must be required by terms of governing instrument upon happening of a specified event. (Rev. Rul. 68-392)

Impact of sufficient cash on hand?

28

Exception 3 – Distributions based on capital gains

Example 5 – The facts are the same as in Example 1, except that Trustee decides that discretionary distributions will be made only to the extent Trust has realized capital gains during the year and thus the discretionary distribution to A is $10,000, rather than $12,000. Because Trustee will use the amount of any realized capital gain to determine the amount of the discretionary distribution to the beneficiary, the $10,000 capital gain is included in Trust's distributable net income for the taxable year.

How common is this?

Is consistency required?

Capital loss netting under Regs. Sec. 1.643(a)-3(d).

29

Exception 3 – Distributions based on sales proceeds

Example 6 – Trust's assets consist of Blackacre and other property. Under the terms of Trust's governing instrument, Trustee is directed to hold Blackacre for ten years and then sell it and distribute all the sales proceeds to A. Because Trustee uses the amount of the sales proceeds that includes any realized capital gain to determine the amount required to be distributed to A, any capital gain realized from the sale of Blackacre is included in Trust's distributable net income for the taxable year.

30

Grantor Trust Status Under IRC Sec. 671, when a grantor or another person is treated as the owner of any portion of a trust, then all income, deductions, and credits including capital gains attributable to the grantor portion of the trust are taxed to the grantor.

Avoid the DNI issue altogether.

Trust can be partial grantor trust.

31

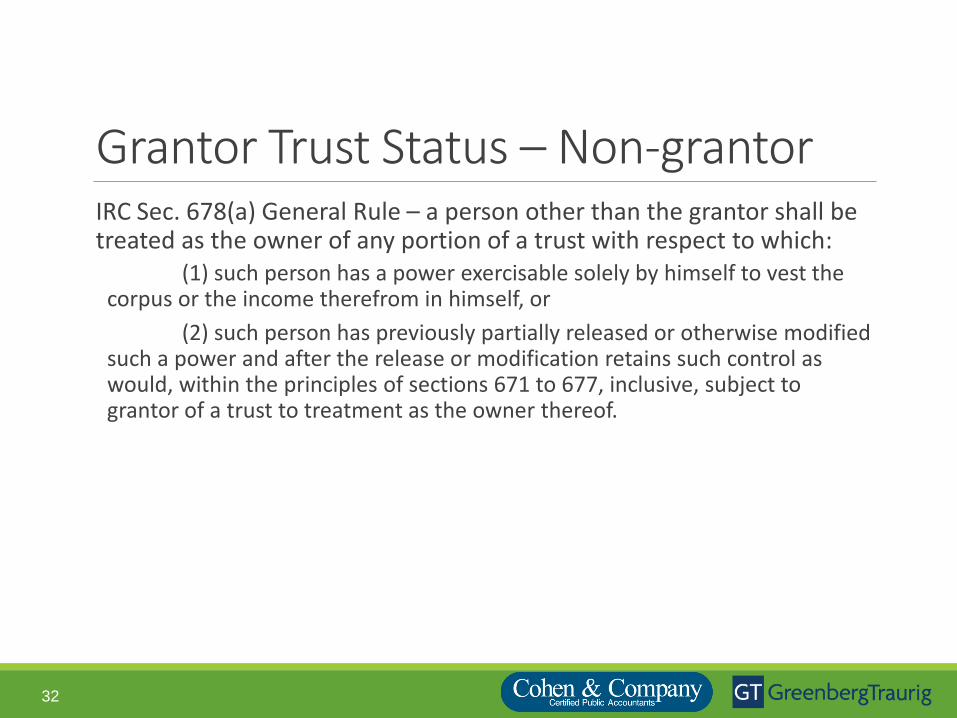

Grantor Trust Status – Non-grantor IRC Sec. 678(a) General Rule – a person other than the grantor shall be treated as the owner of any portion of a trust with respect to which:

(1) such person has a power exercisable solely by himself to vest the corpus or the income therefrom in himself, or

(2) such person has previously partially released or otherwise modified such a power and after the release or modification retains such control as would, within the principles of sections 671 to 677, inclusive, subject to grantor of a trust to treatment as the owner thereof.

32

IRC Sec. 678 applicability Age attainment provisions

“Crummey” trusts

“5 and 5” power

Beneficiary defective trusts

33

Other ideas In-kind distributions

◦ Distribute out capital gain property and have beneficiary sell.

◦ Careful of triggering gain if in satisfaction of mandatory income distribution. (Regs. Sec. 1.661(a)-2(f))

◦ “Actually” distributed?

Pass-through entities ◦ Non-liquidating distributions allocated to income

◦ “Gains from the sale or exchange of capital assets allocated to corpus”

◦ Crisp v. United States

34

Non-Tax & Other Considerations Estate & GST tax planning

State & local taxation

Asset protection

Spendthrift protection

35

Contact Information ANDREW WHITEHAIR,

CPA/PFS, AEP®

Director, Family Wealth

Cohen & Company

1350 Euclid Ave., Suite 800

Cleveland, OH 44115

(216) 774-1121

DIANA S.C. ZEYDEL

National Chair, Trusts & Estates Department

Greenberg Traurig, P.A.

333 S.E. 2nd Avenue

Miami, FL 33131

(305) 579-0575

36