All rights reserved | 1 Conditions for Service und Agency Permanent Establishments Summary of cases...

25

All rights reserved | 1 Conditions for Service und Agency Permanent Establishments Summary of cases discussed

-

Upload

joel-oliver -

Category

Documents

-

view

219 -

download

2

Transcript of All rights reserved | 1 Conditions for Service und Agency Permanent Establishments Summary of cases...

All rights reserved | 1

Conditions for

Service und Agency Permanent Establishments

Summary of cases discussed

All rights reserved | 2

Cases

Morgan Stanley, Supreme Court of India, 9 July 2007

Rolls Royce, Income Tax Appellate Tribunal Delhi Branch, 26 October 2006

by Bobby Parikh, BMR & Associates

Zimmer Ltd., Paris Administrative Court, 2 February 2007

by Jacques Sasseville, OECD

All rights reserved | 3T a x a n d R e g u l a t o r y

BMR Advisors

All rights reserved | 4

THE MORGAN STANLEY DECISION

All rights reserved | 5

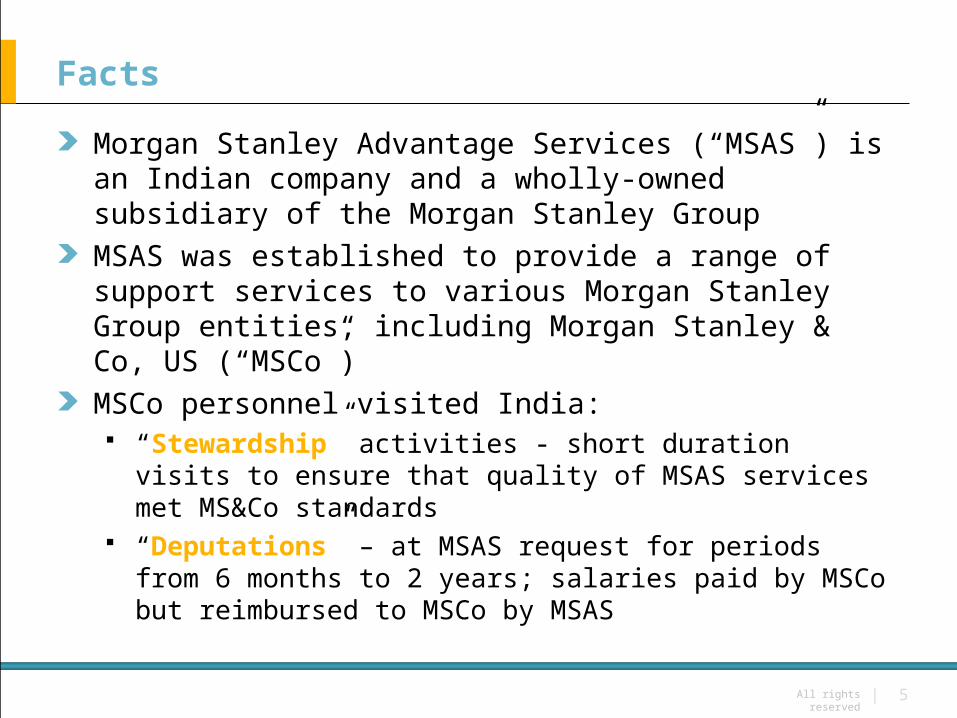

Facts

Morgan Stanley Advantage Services (“MSAS”) is an Indian company and a wholly-owned subsidiary of the Morgan Stanley Group

MSAS was established to provide a range of support services to various Morgan Stanley Group entities, including Morgan Stanley & Co, US (“MSCo”)

MSCo personnel visited India: “Stewardship” activities - short duration visits to ensure that

quality of MSAS services met MS&Co standards “Deputations” – at MSAS request for periods from 6 months to

2 years; salaries paid by MSCo but reimbursed to MSCo by MSAS

All rights reserved | 6

Application to the AAR

MSCo sought a ruling from the AAR on, inter-alia, the following matters:

Did MSCo have a Fixed Place PE in India – Article 5(1)

Whether MSAS could be regarded as constituting an Agency PE of MSCo in India – Article 5(4)

Whether MSCo would be regarded as having a Service PE in India on account of its Stewardship activities

Deputations

- Article 5(2)(l)

All rights reserved | 7

AAR’s ruling

The AAR ruled that:

MSCo did not have a Fixed Place PE in India

MSAS could not be regarded as an agent of MSCo; consequently, MSCo did not have a agency PE in India

Stewardship and Deputation activities constitute the rendering of services by MSCo personnel in India; consequently, MSCo should be regarded as having a PE in India under Article 5(2)(l) and MSAS was the PE

This ruling was challenged before the Supreme Court

All rights reserved | 8

SC conclusions on Fixed Place PE

A functional and factual analysis of each of the activities undertaken in India must be conducted to determine whether or not a PE is constituted

That based on facts, the activities to be undertaken by MSAS in India are in the nature of back office operations

Accordingly, [although MSCo may be regarded as having a fixed place of business in India], it cannot be regarded as conducting its business through this fixed place since the activities are in the nature of back office operations

Functions performed by MSAS in India fall under preparatory and auxiliary activities, as per Article 5(3) of the DTAA and hence do not constitute a PE

No Fixed Place PE

All rights reserved | 9

SC conclusions on Agency PE

The PE in India had no authority to enter into or conclude contracts on behalf of MSCo

Contracts were entered into and concluded in the US

Implementation of those contracts, only to the extent of back office functions would be carried out in India

No Agency PE

All rights reserved | 10

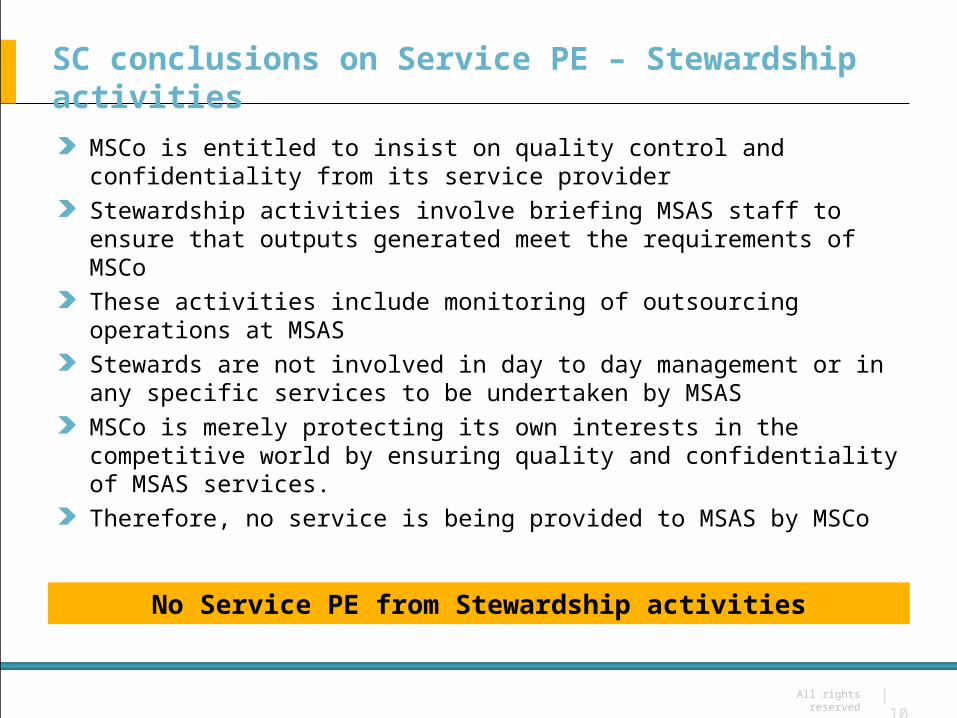

SC conclusions on Service PE – Stewardship activities

MSCo is entitled to insist on quality control and confidentiality from its service provider

Stewardship activities involve briefing MSAS staff to ensure that outputs generated meet the requirements of MSCo

These activities include monitoring of outsourcing operations at MSAS

Stewards are not involved in day to day management or in any specific services to be undertaken by MSAS

MSCo is merely protecting its own interests in the competitive world by ensuring quality and confidentiality of MSAS services.

Therefore, no service is being provided to MSAS by MSCo

No Service PE from Stewardship activities

All rights reserved | 11

SC conclusions on Service PE – Deputation activities

An MSCo employee deputed to MSAS does not become an employee of MSAS; the individual has a lien on his employment with MSCo As long as such a lien exists, MSCo retains control over the deputationist’s terms and employmentMSCo deputes personnel on MSAS’ request from time to time for durations which could extend up to 2 yearsSuch deputationists would be experienced in banking and finance and upon deputation, would lend their experience to MSAS in India

Service PE results from Deputations; MSAS is the PE

All rights reserved | 12

THE ROLLS ROYCE DECISION

All rights reserved | 13

Facts

Rolls Royce Plc (“RRPlc”) supplied equipment and spares to customers in India

RRPlc established Rolls Royce India Limited (“RRIndia”) as its wholly-owned subsidiary in the UK; RRIndia established an office in India

The India office employed a number of individuals – some deputed from the UK and others employed locally. UK individuals were employees of RRPlc prior to their deputation to India

RRIndia was required to provide a range of services to RRPlc; for these services, it was to be reimbursed on a cost plus an agreed mark up

All rights reserved | 14

Tax office findings

In audit, the Revenue authorities held that:

RRPlc was conducting sales and marketing activities in India through RRIndia

RRIndia constituted a PE of RRPlc in India

RRPlc did not maintain books of account in relation to its Indian operations; accordingly, profits attributable to the Indian PE would need to be estimated

75% of the profits arising from Indian sales should be taxable in India

All rights reserved | 15

Commissioner (Appeals) conclusions

In appeal, the Commissioner (Appeals) held that:

RRPlc had a Fixed Place PE in India – Article 5(1), 5(2)(c), 5(2)(f)

RRPlc had a Agency PE in India – Article 5(4)(c)

75% of the profits attributable to Indian sales should be taxed in India

All rights reserved | 16

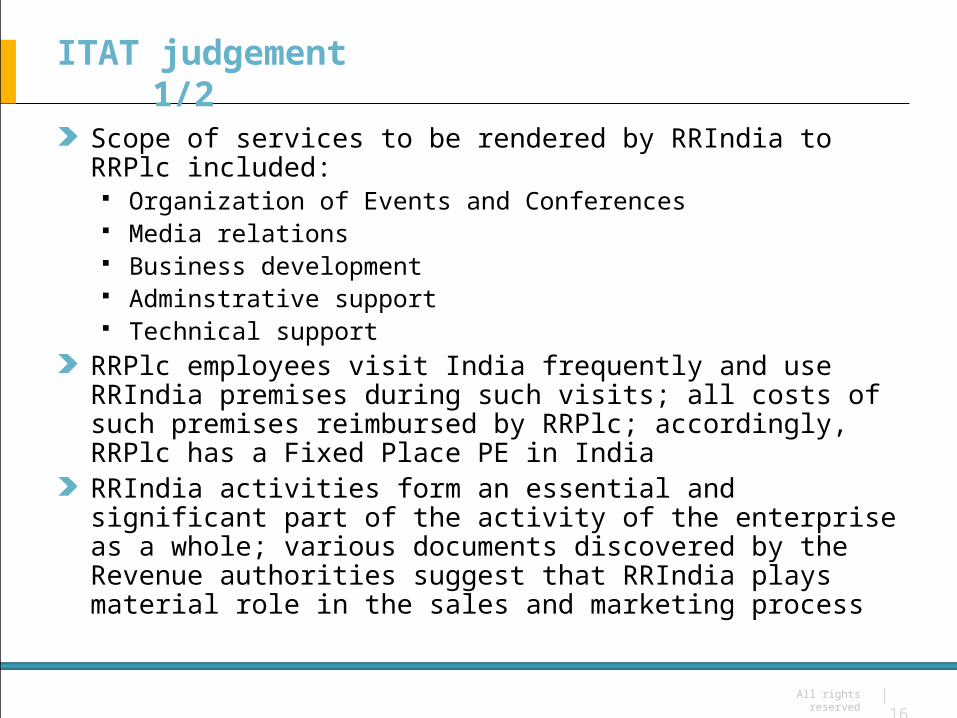

ITAT judgement 1/2

Scope of services to be rendered by RRIndia to RRPlc included: Organization of Events and Conferences Media relations Business development Adminstrative support Technical support

RRPlc employees visit India frequently and use RRIndia premises during such visits; all costs of such premises reimbursed by RRPlc; accordingly, RRPlc has a Fixed Place PE in IndiaRRIndia activities form an essential and significant part of the activity of the enterprise as a whole; various documents discovered by the Revenue authorities suggest that RRIndia plays material role in the sales and marketing process

All rights reserved | 17

ITAT judgement 2/2

RRIndia employees are functionally responsible to RRPlc

Based on facts, RRIndia activities could not be regarded as being preparatory or auxiliary in nature

RRIndia habitually secures orders in India for RRPlc; this is supported by a number of documents discovered by the Revenue authorities; RRIndia is a dependent agent of RRPlc and constitutes an agency PE for RRPlc

35% of the profits attributable to India sales should be taxable in India

All rights reserved | 18C h a l l e g e U s

BMR Advisors

All rights reserved | 19Morgan Stanley - Supreme CourtFriday Morning Meeting - Morgan Stanley

Agency Permanent Establishment: Zimmer

Jacques Sasseville

Head, Tax Treaty Unit

OECD

24-25 January 2008

Mumbai

All rights reserved | 20

Facts

Zimmer SAS (French resident company) and Zimmer Ltd (UK resident company) are parts of the same multinational group

Zimmer SAS is the distributor in France of the products of Zimmer Ltd

In 1995, the distributorship arrangement is replaced by a contract of “commissionnaire”

All rights reserved | 21

Facts

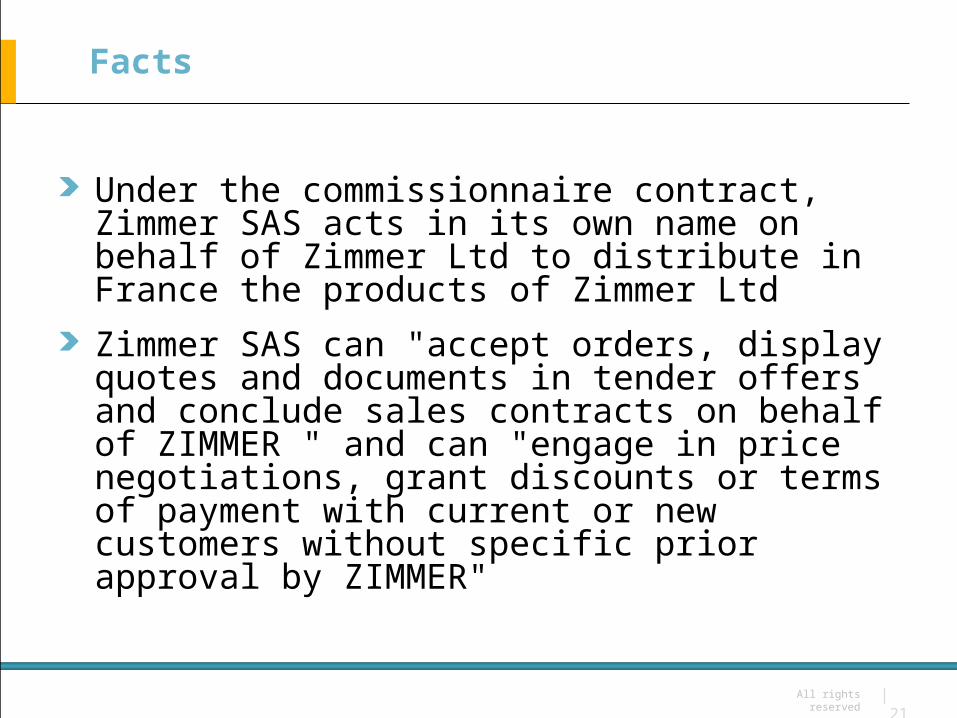

Under the commissionnaire contract, Zimmer SAS acts in its own name on behalf of Zimmer Ltd to distribute in France the products of Zimmer Ltd

Zimmer SAS can "accept orders, display quotes and documents in tender offers and conclude sales contracts on behalf of ZIMMER " and can "engage in price negotiations, grant discounts or terms of payment with current or new customers without specific prior approval by ZIMMER"

All rights reserved | 22

The issue

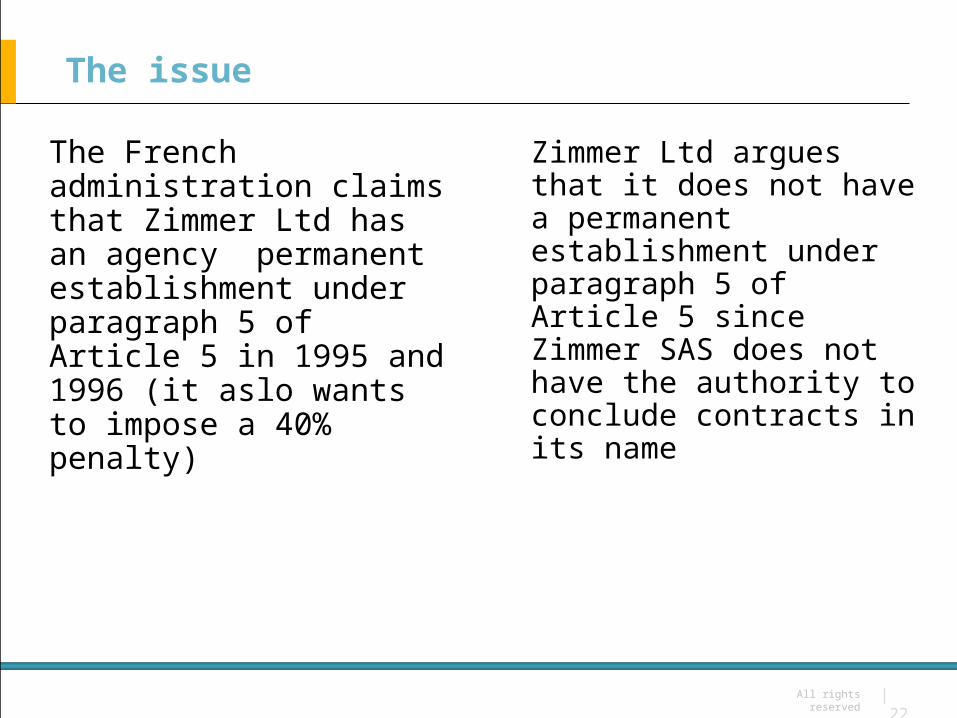

The French administration claims that Zimmer Ltd has an agency permanent establishment under paragraph 5 of Article 5 in 1995 and 1996 (it aslo wants to impose a 40% penalty)

Zimmer Ltd argues that it does not have a permanent establishment under paragraph 5 of Article 5 since Zimmer SAS does not have the authority to conclude contracts in its name

All rights reserved | 23

Decision (which is under Appeal)

There is an agency permanent establishment

“it results therefore from the terms of the contract itself that Zimmer SAS had the power to bind ZIMMER LIMITED; that the circumstance whereby Zimmer SAS, owing to its status as commission agent, acted in its own name and could not therefore effectively conclude contracts in the name of its principal is without effect on the power of that company to bind its principal in commercial transactions pertaining to the said principal’s own activities, by virtue of the principle set out above”

All rights reserved | 24

Decision

“Zimmer SAS, as we have just said, had the authority to bind Zimmer Ltd”

“according to Articles 2.1 and 5.4 of the commission agency contract Zimmer SAS was subject to the instructions of Zimmer Ltd,

or under its control, […] the risks stemming from the execution of products sales

contracts were borne by Zimmer Ltd […] Zimmer SAS acted solely on behalf of ZIMMER

LIMITED

[…] Zimmer SAS cannot therefore be deemed to have an ‘independent status’”

All rights reserved | 25

Conclusions of the Court expert

“Zimmer SAS acts “in the name of” its principal since the term should not be taken literally but merely means that Zimmer SAS can bind Zimmer Ltd for activities specific to that company.”“This is the interpretation of the OECD Committee on Fiscal Affairs with regard to the provisions of the OECD Model Tax Conventions […] The OECD Committee on Fiscal Affairs has made a specific statement on this issue, in its commentary on subsequent conventions: “the phrase ‘authority to conclude contracts in the name of the enterprise’ does not confine the application of the paragraph to an agent who enters into contracts literally in the name of the enterprise; the paragraph applies equally to an agent who concludes contracts which are binding on the enterprise even if those contracts are not actually in the name of the enterprise” (§32.1 of Commentary on Article 5).