Alkim Alkali Kimya Anonim Şirketi and its...

61

(Convenience translation of the independent auditor’s report and consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya Anonim Şirketi and its Subsidiaries Consolidated financial statements as at December 31, 2015 together with the independent auditor’s report

Transcript of Alkim Alkali Kimya Anonim Şirketi and its...

(Convenience translation of the independent auditor’s report and consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya Anonim Şirketi and its Subsidiaries Consolidated financial statements as at December 31, 2015 together with the independent auditor’s report

Alkim Alkali Kimya Anonim Şirketi and its Subsidiaries Table Of Contents Page

Independent auditors report on the financial statements 1 - 2

Consolidated statement of financials position 3 - 4

Consolidated statement of profit or loss andother comprehensive income 5

Consolidated statement of changes in equity 6

Consolidated statement of cash flows 7

Summary of significant accounting policies and explanatory notes 8 – 59

(Convenience translation of a report and consolidated financial statements originally issued in Turkish) Independent auditors’ report on the consolidated financial statements To the Board of Directors of Alkim Alkali Kimya Anonim Şirketi Report on the Consolidated financial statements 1. We have audited the accompanying consolidated financial statetements of Alkim Alkali Kimya

Anonim Şirketi (the Company) and its Subsidiaries (together will be referred to as the ‘’Group’’) which comprise the consolidated statement of financial position as at December 31, 2015 and the consolidated statement of profit or loss and other comprehensive income, consolidated statement of changes in equity and consolidated statement of cash flows for the year then ended and a summary of significant accounting policies and explanatory notes.

Group Management's responsibility for the consolidated financial statements 2. Group’s management is responsible for the preparation and fair presentation of financial

statements in accordance with the Turkish Accounting Standards and for such internal controls as management determines is necessary to enable the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to error and/or fraud.

Independent auditors’ responsibility 3. Our responsibility is to express an opinion on these consolidated financial statements based on

our audit. Our audit was conducted in accordance with Standards on Auditing as issued by the Capital Markets Board of Turkey and Auditing Standards which are part of the Turkish Auditing Standards asissued by Public Oversight Accounting and Auditing Standards Authority of Turkey. Those standards require that ethical requirements are complied with and that the independent audit is planned and performed to obtain reasonable assurance whether the financial statements are free from material misstatement.

Independent audit involves performing independent audit procedures to obtain independent audit evidence about the amounts and disclosures in the financial statements. The independent audit procedures selected depend on our professional judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to error and/or fraud. In making those risk assessments, the Company’s internal control system is taken into consideration. Our purpose, however, is not to express an opinion on the effectiveness of internal control system, but to design independent audit procedures that are appropriate for the circumstances in order to identify the relation between the financial statements prepared by the Group and its internal control system. Our independent audit includes also evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Company’s management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained during our independent audit is sufficient and appropriate to provide a basis for our qualified audit opinion.

(2)

Basis for qualified opinion 4. As disclosed in Note 5 of the accompanying financial statements, as of December 31, 2014,

Alkim Kağıt Sanayi ve Ticaret A.Ş, a subsidiary of the Group, had trade and cheques receivables from a customer amounting to TL 30.780.137, of which significant amount were overdue. In 2014, due to the customer’s inability to make the payments on due dates, execution proceedings have been commenced for the overdue receivables amounting to TL 20.953.298 and a doubtful receivable provision had been booked in the financial statements for the related amount. As of December 31, 2014, the Group also had trade receivables amounting to TL 9.826.339 from the same customer. Since the Group had not booked doubtful receivable provision for the whole amount of the related receivables, our audit report dated March 2, 2015 on consolidated financial statements as at December 31, 2014 was qualified. Due to inability to collect above mentioned qualified trade receivables, the Group has booked doubtful receivable provision for these receivables in current year. Accordingly, the Group’s retained losses and the net profit as of December 31, 2015 has been realized less by TL7.861.071 (net of deferred tax).

Qualified opinion 5. In our opinion, except for the effects of the matter described in the “basis for qualified opinion”

section above, the consolidated financial statements present fairly, in all material respects, the financial position of Alkim Alkali Kimya Anonim Şirketi and its Subsidiaries as at 31 December 2015 and their financial performance and cash flows for the year then ended in accordance with the Turkish Accounting Standards.

Reports on independent auditor responsibilities arising from other regulatory requirements 6. Auditors’ report on Risk Management System and Committee prepared in accordance with

paragraph 4 of Article 398 of Turkish Commercial Code (“TCC”) 6102 is submitted to the Board of Directors of the Company on February 29, 2016.

7. In accordance with paragraph 4 of Article 402 of the TCC, no significant matter has come to our

attention that causes us to believe that the Company’s bookkeeping activities for the period 1 January – 31 December 2015 and financial statements are not in compliance with the code and provisions of the Company’s articles of association in relation to financial reporting.

8. In accordance with paragraph 4 of Article 402 of the TCC, the Board of Directors submitted to us the necessary explanations and provided required documents within the context of audit.

Güney Bağımsız Denetim ve Serbest Muhasebeci Mali Müşavirlik Anonim Şirketi A member firm of Ernst & Young Global Limited Cem Uçarlar, SMMM Partner February 29,2016 İstanbul, Türkiye

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Consolidated statement of financial position as of December 31, 2015 (Amounts expressed in Turkish Lira (“TL”) unless otherwise indicated.)

The accompanying notesform an integral part of these consolidated financial statements.

(3)

Current period Prior period Audited Audited

Notes December 31,

2015 December 31,

2014 Assets Current assets 162.259.654 124.211.504 Cash and cash equivalents 4 52.904.127 26.410.411 Trade receivables 40.083.686 42.217.230 - Due from related parties 29 275.137 56.676 - Trade receivables, third parties 5 39.808.549 42.160.554 Other receivables 3.248.638 785.066 - Other receivables, third parties 6 3.248.638 785.066 Inventories 7 53.191.029 42.438.747 Prepaid expenses 8 2.680.197 2.110.896 Current income tax assets 27 27.683 1.256.948 Other current assets 9 10.124.294 8.992.206 Non-current assets 118.529.627 123.059.047 Other receivables 321.334 222.207 - Other receivables, third parties 6 321.334 222.207 Financial İnvestments 10 14.313 14.313 Property, plant and equipment 11 109.647.626 118.908.026 Intangible assets 1.085.023 1.152.083 - Other intangible assets 12 1.085.023 1.152.083 Prepaid expenses 8 7.348.564 1.938.815 Deferred tax assets 27 38.711 808.442 Other non-current assets 74.056 15.161 Total assets 280.789.281 247.270.551

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Consolidated statement of financial position as of December 31, 2015 (Amounts expressed in Turkish Lira (“TL”) unless otherwise indicated.)

The accompanying notesform an integral part of these consolidated financial statements.

(4)

Current period Prior period Audited Audited

Notes December 31,

2015 December 31,

2014 Liabilities Current liabilities 53.393.791 43.131.720 Short-term financial liabilities 14 25.431.601 5.347.546 Current portion of long term financial liabilities 14 3.880.387 16.255.836 Other financial liabilities 15 - 2.020.319 Trade payables 19.953.683 15.589.818 - Trade payables, third parties 5 19.953.683 15.589.818 Liabilities for employee benefits 16 2.448.346 2.666.365 Other payables 954.571 94 - Other payables, third parties 29 954.571 94 Deferred income 17 601.921 701.682 Current income tax liabilities 27 24.359 406.908 Provisions 66.543 81.910 - Provisions for employee benefits 19 27.411 75.574 - Other provisions 39.132 6.336 Other current liabilities 32.380 61.242 Non-current liabilities 14.608.589 8.232.113 Long-term financial liabilities 14 9.240.552 3.475.001 Provisions 5.161.412 4.757.112 - Provisions for employee benefits 19 5.161.412 4.757.112 Deferred tax liability 27 206.625 - Total liabilities 68.002.380 51.363.833 Equity 212.786.901 195.906.718 Share capital 20 24.725.000 24.725.000 Adjustments to share capital 26.909.044 26.909.044 Restricted reserves 20.885.203 20.885.203 Accumulated other comprehensive income/(expense) not to be reclassified to profit or loss

(1.405.554) (1.082.680)

- Actuarial gain/(loss) arising from defined benefit plans (1.405.554) (1.082.680)

Retained earnings 91.974.422 86.845.800 Net profit for the period 30.545.452 20.519.441 Total equity attributable to equity holders of the parent 193.633.567 178.801.808 Non-controlling interests 19.153.334 17.104.910 Total equity and liabilities 280.789.281 247.270.551

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Consolidated statement of comprehensive income for the year then ended December 31, 2015 (Amounts expressed in Turkish lira (TL) unless otherwise indicated.)

The accompanying notesform an integral part of these consolidated financial statements.

(5)

Current Period Prior Period Audited Audited January 1 - January 1 -

Notes December 31,

2015 December 31,

2014 Revenue (net) 21 262.136.444 246.182.611 Cost of sales (-) 21 (195.531.590) (178.593.881) Gross profit 66.604.854 67.588.730 General administrative expenses (-) 22 (13.174.262) (12.592.434) Marketing, selling and distribution expenses (-) 22 (19.294.692) (18.948.543) Research and development expenses (-) 22 (83.728) (144.599) Other operating income 24 12.622.906 8.577.593 Other operating expenses (-) 24 (14.860.558) (22.647.453) Operating profit 31.814.520 21.833.294 Income from investment activities 25 9.424.880 3.412.730 Operating profit before financial income/(expense ) 41.239.400 25.246.024 Financial income 26 3.587.963 4.749.915 Financial expense (-) 26 (8.207.747) (7.836.650) Profit before tax 36.619.616 22.159.289 Tax expense (4.025.740) (3.017.351) - Taxes on income (-) 27 (2.968.665) (5.023.619) - Deferred tax income/(expense) 27 (1.057.075) 2.006.268 Net income from continued operations 32.593.876 19.141.938 Other comprehensive income Actuarial gain/(loss) arising from defined benefit plans (403.593) (65.060) Tax effect of other comprehensive income / (loss) not to be reclassified

to profit or loss 80.719 13.014 - Deferred tax income 27 80.719 13.014 Other comprehensive income (322.874) (52.046)

Total comprehensive income 32.271.002 19.089.892

Distribution of income for the period: Non-controlling interests 2.048.424 (1.377.503) Attributable to equity holders of the parent 30.545.452 20.519.441

Distribution of total comprehensive income Non-controlling interests 2.048.424 (1.377.503) Attributable to equity holders of the parent 30.222.578 20.467.395 Earnings per share Attributable to equity holders of the parent (in TL)) 28 1,2354 0,8299

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Statement of changes in shareholders’ equity for the year ended December 31, 2015 (Amounts expressed in Turkish lira (TL) unless otherwise indicated.

The accompanying notesform an integral part of these consolidated financial statements.

(6)

Other accumulated comprehensive income

/ (loss) not to be reclassified to profit or

loss Retained Earnings

Share capital

Adjustment to share

capital Restricted

reserves

Actuarial gain/(loss) arising

from defined benefit plans

Retained earnings

Net profit for

the period

Equity holders

of the parent

Non-

controlling interests Total equity

1 January 2014 24.725.000 26.909.044 20.885.203 (1.030.634) 81.123.596 16.556.238 169.168.447 19.908.020 189.076.467 Transfers - - - - 16.556.238 (16.556.238) - - - Dividends paid - - - - (10.834.034) - (10.834.034) (1.425.607) (12.259.641) Total comprehensive income - - - (52.046) - 20.519.441 20.467.395 (1.377.503) 19.089.892 December 31, 2014 24.725.000 26.909.044 20.885.203 (1.082.680) 86.845.800 20.519.441 178.801.808 17.104.910 195.906.718

Other accumulated comprehensive

income / (loss) not to be reclassified to

profit or loss Retained Earnings

Share capital

Adjustment to share

capital Restricted

reserves

Actuarial gain/(loss) arising

from defined benefit plans

Retained earnings

Net profit for

the period

Equity holders

of the parent

Non-

controlling interests Total equity

1 January 2015 24.725.000 26.909.044 20.885.203 (1.082.680) 86.845.800 20.519.441 178.801.808 17.104.910 195.906.718 Transfers - - - - 20.519.441 (20.519.441) - - - Dividends paid - - - - (15.390.819) - (15.390.819) - (15.390.819) Total comprehensive income - - - (322.874) - 30.545.452 30.222.578 2.048.424 32.271.002 December 31, 2015 24.725.000 26.909.044 20.885.203 (1.405.554) 91.974.422 30.545.452 193.633.567 19.153.334 212.786.901

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Consolidated statement of cash flows for the year ended December 31, 2015 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

The accompanying notesform an integral part of these consolidated financial statements.

(7)

Current period Prior period Notes Audited Audited January 1 - January 1 -

December 31,

2015 December 31,

2014 A. Cash flows from operating activities 26.403.168 39.155.985 Profit/(loss) before taxation 36.619.616 22.159.289 Adjustment for reconciliation of profit/(loss) before

taxation - Adjustment for depreciation and amortisation expense 15.942.836 15.424.788 - Adjustment for provisions 996.524 21.972.180 - Adjustment for unrealized foreign currency translation

differences (71.621) 131.900 - Adjustment for interest income and expense 247.668 422.648 - Adjustment for gains on sales of property, plant and

equipment

25 (8.763.196) (2.469.593) Changes in working capital - Adjustment for increase/decrease in inventories (10.752.282) (11.969.641) - Adjustment for increase/decrease in trade receivables 2.078.042 4.771.129 - Adjustment for increase/decrease in other receivables

related with operations (9.537.426) (3.176.499) - Adjustment for increase/decrease in trade payables 5.338.406 (914.693) - Adjustment for increase/decrease in other payables

related with operations (2.382.326) 129.028 Cash flows from operating activities - Tax payments/returns (2.317.256) (6.254.124) - Other cash inflow/outflow 19 (995.817) (1.070.427) B. Cash flows from investing activities 2.787.740 366.555 Interest received 25 639.920 941.102 Cash inflows from the sale of property, plant and equipment

and intangible assets

11, 12 9.939.894 6.407.326 Cash outflows from the purchase of property, plant and

equipment and intangible assets

11, 12 (7.792.074) (6.981.873) C. Cash flows from financing activities (2.717.617) (44.639.508) Cash inflows/(outflows) from financial liabilities 13.364.650 (31.137.305) Dividends paid 20 (15.390.819) (12.259.641) Interest paid (691.448) (1.242.562) Net increase/decrease in cash and cash equivalents 26.473.291 (5.116.968) E. Cash and cash equivalents at beginning of period 26.410.411 31.527.379 Cash and cash equivalents at end of period 52.883.702 26.410.411

Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(8)

1. Organization and Nature of Operations Alkim Alkali Kimya A.Ş (the “Company”) was established in 1948 as Alkali Madencilik Limited Şirketi. Since October 1963, the Company has continued its operations as Alkim Alkali Kimya A.Ş. The nature of the operation of the Company is the mining of ores and the production and distribution of all kinds of chemical materials in domestic and foreign markets as disclosed in the articles of association. The nature of the businesses of the Subsidiaries is as follows: Subsidiaries Country Nature of business - Alkim Kağıt Sanayi ve Ticaret A.Ş. (“Alkim Kağıt”) Turkey Production and Sales of paper products - Alkim Sigorta Aracılık Hizmetleri Ltd. Şti. (“Alkim Sigorta”) Turkey Insurance The Company and its subsidiaries (“the Group”) are registered in Turkey. The Company and its subsidiary Alkim Kağıt, are publicly quoted companies and 33,01% (December 31, 2014 – 33,01%) of the Company’s shares, 20,00% (December 31, 2014 - 20,00%) of Alkim Kağıt shares are quoted on the Stock Exchange Istanbul (“SEI”). As of December 31, 2015 average number of employees of the “Group” is 319 (December 31,2014 was 321). The address of the registered office is as follows: Gümüşsuyu Mahallesi İnönü Caddesi No: 13 34437 Taksim - İstanbul Approval of consolidated financial statements Consolidated financial statements are approved for issue by board of directors on February 29, 2016. Statutory financial statements that form the basis of these consolidated financial statements are subject to the approval of General Assembly.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(9)

2. Basis of preparation of consolidated financial statements 2.1 Basis of preparation The consolidated financial statements of the Group have been prepared in accordance with the Turkish Accounting Standards/Turkish Financial Reporting Standards, (“TAS/TFRS”) and interpretations as adopted in line with international standards by the Public Oversight Accounting and Auditing Standards Authority of Turkey (“POA”) TAS/TFRS are updated in harmony with the changes and updates in International Financial and Accounting Standards. (“IFRS”) With the decision taken on March 17, 2005, the CMB announced that, effective from January 1, 2005, the application of inflation accounting is no longer required for companies operating in Turkey. The Group has prepared its consolidated financial statements in accordance with this decision under the historical cost convention. All items with significant amounts and nature, even with similar characteristics, are presented separately in the financial statements. Insignificant amounts are grouped and presented by means of items having similar substance and function. When the nature of transactions and events necessitate offsetting, presentation of these transactions and events over their net amounts or recognition of the assets after deducting the related impairment are not considered as a violation of the rule of non-offsetting. As a result of the transactions in the normal course of business are presented as net provided that if the nature of the transaction or the event qualify for offsetting. The consolidated financial statements are prepared based on the historical cost convention in Turkish Lira (“TL”) which is the Company’s and its subsidiaries’ functional and presentation currency 2.2 The new standards, amendments and interpretations The accounting policies adopted in preparation of the consolidated financial statements as at December 31, 2015 are consistent with those of the previous financial year, except for the adoption of new and amended TFRS and TFRIC interpretations effective as of January 1, 2015. The effects of these standards and interpretations onthe Group’s financial position and performance have been disclosed in the related paragraphs. i) The new standards, amendments and interpretations which are effective as at January 1,

2015 are as follows: TAS 19 Defined Benefit Plans: Employee Contributions (Amendment) TAS 19 requires an entity to consider contributions from employees or third parties when accounting for defined benefit plans. The amendments clarify that, if the amount of the contributions is independent of the number of years of service, an entity is permitted to recognise such contributions as a reduction in the service cost in the period in which the service is rendered, instead of allocating the contributions to the periods of service. The amendment did not have an impact on the consolidated financial statements of the Group. Annual Improvements to TAS/TFRSs In September 2014, POA issued the below amendments to the standards in relation to “Annual Improvements - 2010–2012 Cycle” and “Annual Improvements - 2011–2013 Cycle.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(10)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

Annual Improvements - 2010–2012 Cycle TFRS 2 Share-based Payment: Definitions relating to performance and service conditions which are vesting conditions are clarified. The amendment is effective prospectively. TFRS 3 Business Combinations The amendment clarifies that all contingent consideration arrangements classified as liabilities (or assets) arising from a business combination should be subsequently measured at fair value through profit or loss whether or not they fall within the scope of TAS 39 (or TFRS 9, as applicable). The amendment is effective for business combinations prospectively. TFRS 8 Operating Segments The changes are as follows: i) An entity must disclose the judgements made by management in applying the aggregation criteria in TFRS 8, including a brief description of operating segments that have been aggregated and the economic characteristics (e.g., sales and gross margins) used to assess whether the segments are ‘similar’. ii) The reconciliation of segment assets to total assets is only required to be disclosed if the reconciliation is reported to the chief operating decision maker. The amendments are effective retrospectively. TAS 16 Property, Plant and Equipment and TAS 38 Intangible Assets The amendment to TAS 16.35(a) and TAS 38.80(a) clarifies that revaluation can be performed, as follows: i) Adjust the gross carrying amount of the asset to market value or ii) determine the market value of the carrying amount and adjust the gross carrying amount proportionately so that the resulting carrying amount equals the market value. The amendment is effective retrospectively. TAS 24 Related Party Disclosures The amendment clarifies that a management entity – an entity that provides key management personnel services – is a related party subject to the related party disclosures. . In addition, an entity that uses a management entity is required to disclose the expenses incurred for management services. The amendment is effective retrospectively. Annual Improvements – 2011–2013 Cycle TFRS 3 Business Combinations The amendment clarifies that: i) Joint arrangements are outside the scope of TFRS 3, not just joint ventures ii) The scope exception applies only to the accounting in the financial statements of the joint arrangement itself. The amendment is effective prospectively. TFRS 13 Fair Value Measurement The portfolio exception in TFRS 13 can be applied to financial assets, financial liabilities and other contracts within the scope of TAS 39 (or TFRS 9, as applicable). The amendment is effective prospectively.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(11)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

TAS 40 Investment Property The amendment clarifies the interrelationship of TFRS 3 and TAS 40 indetermining whether the transaction is the purchase of an asset or business combination. The amendment is effective prospectively. The amendments did not have a significant impact on the consolidated financial statements of the Group. ii) Standards issued but not yet effective and not early adopted Standards, interpretations and amendments to existing standards that are issued but not yet effective up to the date of issuance of the consolidated financial statements are as follows. The Group will make the necessary changes if not indicated otherwise, which will be affecting the consolidated financial statements and disclosures, when the new standards and interpretations become effective. TFRS 9 Financial Instruments – Classification and measurement As amended in December 2012 and February 2015, the new standard is effective for annual periods beginning on or after January 1, 2018, with early adoption permitted. Phase 1 of this new TFRS 9 introduces new requirements for classifying and measuring financial instruments. The amendments made to TFRS 9 will mainly affect the classification and measurement of financial assets and measurement of fair value option (FVO) liabilities and requires that the change in fair value of a FVO financial liability attributable to credit risk is presented under other comprehensive income. The Group will quantify the effect in conjunction with the other phases, when the final standard including all phases is adopted by POA. TFRS 11 Acquisition of an Interest in a Joint Operation (Amendment) TFRS 11 is amended to provide guidance on the accounting for acquisitions of interests in joint operations in which the activity constitutes a business. This amendment requires the acquirer of an interest in a joint operation in which the activity constitutes a business, as defined in TFRS 3 Business Combinations, to apply all of the principles on business combinations accounting in TFRS 3 and other TFRSs except for those principles that conflict with the guidance in this TFRS. In addition, the acquirer shall disclose the information required by TFRS 3 and other TFRSs for business combinations. These amendments are to be applied prospectively for annual periods beginning on or after January 1, 2016. Earlier application is permitted. The amendments will not have an impact on the financial position or performance of the Group. TAS 16 and TAS 38 - Clarification of Acceptable Methods of Depreciation and Amortisation (Amendments to TAS 16 and TAS 38) The amendments to TAS 16 and TAS 38, have prohibited the use of revenue-based depreciation for property, plant and equipment and significantly limiting the use of revenue-based amortisation for intangible assets. The amendments are effective prospectively for annual periods beginning on or after January 1, 2016. Earlier application is permitted. The amendments will not have an impact on the financial position or performance of the Group.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(12)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

TAS 16 Property, Plant and Equipment and TAS 41 Agriculture (Amendment) – Bearer Plants TAS 16 is amended to provide guidance that bearer plants, such as grape vines, rubber trees and oil palms should be accounted for in the same way as property, plant and equipment in TAS 16. Once a bearer plant is mature, apart from bearing produce, its biological transformation is no longer significant in generating future economic benefits. The only significant future economic benefits it generates come from the agricultural produce that it creates. Because their operation is similar to that of manufacturing, either the cost model or revaluation model should be applied. The produce growing on bearer plants will remain within the scope of TAS 41, measured at fair value less costs to sell. Entities are required to apply the amendments for annual periods beginning on or after January 1, 2016. Earlier application is permitted. The amendment is not applicable for the Group and will not have an impact on the financial position or performance of the Group. TAS 27 Equity Method in Separate Financial Statements (Amendments to TAS 27) In April 2015, Public Oversight Accounting and Auditing Standards Authority (POA) of Turkey issued an amendment to TAS 27 to restore the option to use the equity method to account for investments in subsidiaries and associates in an entity’s separate financial statements. Therefore, an entity must account for these investments either: • At cost • In accordance with TFRS 9, Or • Using the equity method defined in TAS 28 The entity must apply the same accounting for each category of investments. The amendment is effective for annual periods beginning on or after January 1, 2016. The amendments must be applied retrospectively. Early application is permitted and must be disclosed. The amendment is not applicable for the Group and will not have an impact on the financial position or performance ofthe Group. TFRS 10 and TAS 28: Sale or Contribution of Assets between an Investor and its Associate or Joint Venture (Amendments) In February 2015, amendments issued to TFRS 10 and TAS 28, to address the acknowledged inconsistency between the requirements in TFRS 10 and TAS 28 in dealing with the loss of control of a subsidiary that is contributed to an associate or a joint venture, to clarify that an investor recognises a full gain or loss on the sale or contribution of assets that constitute a business, as defined in TFRS 3, between an investor and its associate or joint venture. The gain or loss resulting from the re-measurement at fair value of an investment retained in a former subsidiary should be recognised only to the extent of unrelated investors’ interests in that former subsidiary. An entity shall apply those amendments prospectively to transactions occurring in annual periods beginning on or after January 1, 2016. Earlier application is permitted. The amendment is not applicable for the Group and will not have an impact on the financial position or performance of the Group. TFRS 10, TFRS 12 and TAS 28: Investment Entities: Applying the Consolidation Exception (Amendments to TFRS 10 and TAS 28) In February 2015, amendments issued to TFRS 10, TFRS 12 and TAS 28, to address the issues that have arisen in applying the investment entities exception under TFRS 10 Consolidated Financial Statements. The amendments are applicable for annual periods beginning on or after January 1, 2016. Earlier application is permitted. The amendment is not applicable for the Group and will not have an impact on the financial position or performance of the Group.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(13)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

TAS 1: Disclosure Initiative (Amendments to TAS 1) In February 2015, amendments issued to TAS 1. Those amendments include narrow-focus improvements in the following five areas: Materiality, Disaggregation and subtotals, Notes structure, Disclosure of accounting policies, Presentation of items of other comprehensive income (OCI) arising from equity accounted investments. The amendments are applicable for annual periods beginning on or afterJanuary 1, 2016. Earlier application is permitted. These amendments are not expected have significant impact on the notes to the consolidated financial statements of the Group. Annual Improvements to TFRSs - 2012-2014 Cycle In February 2015, POA issued, Annual Improvements to TFRSs 2012-2014 Cycle. The document sets out five amendments to four standards, excluding those standards that are consequentially amended, and the related Basis for Conclusions. The standards affected and the subjects of the amendments are: - TFRS 5 Non-current Assets Held for Sale and Discontinued Operations – clarifies that changes in

methods of disposal (through sale or distribution to owners) would not be considered a new plan of disposal, rather it is a continuation of the original plan

- TFRS 7 Financial Instruments: Disclosures – clarifies that i) the assessment of servicing contracts that includes a fee for the continuing involvement of financial assets in accordance with TFRS 7; ii) the offsetting disclosure requirements do not apply to condensed interim financial statements, unless such disclosures provide a significant update to the information reported in the most recent annual report

- TAS 19 Employee Benefits – clarifies that market depth of high quality corporate bonds is assessed based on the currency in which the obligation is denominated, rather than the country where the obligation is located

- TAS 34 Interim Financial Reporting –clarifies that the required interim disclosures must either be in the interim financial statements or incorporated by cross-reference between the interim financial statements and wherever they are included within the interim financial report

The amendments are effective for annual periods beginning on or after January 1, 2016, with earlier application permitted.The Group is in the process of assessing the impact of the amendments on financial position or performance of the the Group. The new standards, amendments and interpretations that are issued by the International Accounting Standards Board (IASB) but not issued by Public Oversight Authority (POA) The following standards, interpretations and amendments to existing IFRS standards are issued by the IASB but not yet effective up to the date of issuance of the financial statements. However, these standards, interpretations and amendments to existing IFRS standards are not yet adapted/issued by the POA, thus they do not constitute part of TFRS. The Group will make the necessary changes to its consolidated financial statements after the new standards and interpretations are issued and become effective under TFRS.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(14)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

Annual Improvements – 2010–2012 Cycle TFRS 13 Fair Value Measurement As clarified in the Basis for Conclusions short-term receivables and payables with no stated interest rates can be held at invoice amounts when the effect of discounting is immaterial. The amendment is effective immediately. Annual Improvements – 2011–2013 Cycle IFRS 15 Revenue from Contracts with Customers In May 2014, the IASB issued IFRS 15 Revenue from Contracts with Customers. The new five-step model in the standard provides the recognition and measurement requirements of revenue. The standard applies to revenue from contracts with customers and provides a model for the sale of some non-financial assets that are not an output of the entity’s ordinary activities (e.g., the sale of property, plant and equipment or intangibles). IFRS 15 original effective date was January 1, 2017. However, in September 2015, IASB decided to defer the effective date to reporting periods beginning on or after January 1, 2018, with early adoption permitted. Entities will transition to the new standard following either a full retrospective approach or a modified retrospective approach. The modified retrospective approach would allow the standard to be applied beginning with the current period, with no restatement of the comparative periods, but additional disclosures are required. The Group is in the process of assessing the impact of the standard on financial position or performance of the Group. IFRS 9 Financial Instruments - Final standard (2014) In July 2014 the IASB published the final version of IFRS 9 Financial Instruments. The final version of IFRS 9 brings together the classification and measurement, impairment and hedge accounting phases of the IASB’s project to replace TAS 39 Financial Instruments: Recognition and Measurement. IFRS 9 is built on a logical, single classification and measurement approach for financial assets that reflects the business model in which they are managed and their cash flow characteristics. Built upon this is a forward-looking expected credit loss model that will result in more timely recognition of loan losses and is a single model that is applicable to all financial instruments subject to impairment accounting. In addition, IFRS 9 addresses the so-called ‘own credit’ issue, whereby banks and others book gains through profit or loss as a result of the value of their own debt falling due to a decrease in credit worthiness when they have elected to measure that debt at fair value. The Standard also includes an improved hedge accounting model to better link the economics of risk management with its accounting treatment. IFRS 9 is effective for annual periods beginning on or after January 1, 2018. However, the Standard is available for early application. In addition, the own credit changes can be early applied in isolation without otherwise changing the accounting for financial instruments. The Group is in the process of assessing the impact of the standard on financial position or performance of the Group.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(15)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

IFRS 16 Leases In January 2016, the IASB has published a new standard, IFRS 16 'Leases'. The new standard brings most leases on-balance sheet for lessees under a single model, eliminating the distinction between operating and finance leases. Lessor accounting however remains largely unchanged and the distinction between operating and finance leases is retained. IFRS 16 supersedes TAS 17 'Leases' and related interpretations and is effective for periods beginning on or after January 1, 2019, with earlier adoption permitted if IFRS 15 'Revenue from Contracts with Customers' has also been applied.The Group is in the process of assessing the impact of the standard on financial position or performance of the Group. IAS 12 Income Taxes: Recognition of Deferred Tax Assets for Unrealised Losses (Amendments) In January 2016, the IASB issued amendments to TAS 12 Income Taxes. The amendments clarify how to account for deferred tax assets related to debt instruments measured at fair value. The amendments clarify the requirements on recognition of deferred tax assets for unrealised losses, to address diversity in practice. These amendments are to be retrospectively applied for annual periods beginning on or after January 1, 2017 with earlier application permitted. However, on initial application of the amendment, the change in the opening equity of the earliest comparative period may be recognised in opening retained earnings (or in another component of equity, as appropriate), without allocating the change between opening retained earnings and other components of equity. If theGroup applies this relief, it shall disclose that fact. The amendment are not applicable for the Group and will not have an impact on the financial position or performance of the Group. TAS 7 'Statement of Cash Flows (Amendments) In January 2016, the IASB issued amendments to TAS 7 'Statement of Cash Flows'. The amendments are intended to clarify TAS 7 to improve information provided to users of financial statements about an entity's financing activities. The improvements to disclosures require companies to provide information about changes in their financing liabilities. These amendments are to be applied for annual periods beginning on or after January 1, 2017 with earlier application permitted. When the Group first applies those amendments, it is not required to provide comparative information for preceding periods. The amendment are not applicable for the Group and will not have an impact on the financial position or performance of the Group. 2.3 Basis of consolidation The consolidated financial statements include the accounts of the parent company, Alkim Alkali Kimya A.Ş. and its Subsidiaries. The financial statements of the companies included in the consolidation have been prepared as of the date of the consolidated financial statements in conformity with Turkey Financial Reporting Standards and applying uniform accounting policies and presentations. Subsidiaries Subsidiaries are companies which Alkim Alkali Kimya A.Ş. owns, directly or over other subsidiaries, in terms of capital and management relations, 50% or over 50% of the shares, voting power or the majority in management or electing the majority of the management.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(16)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

The table below sets out all Subsidiaries included in the scope of consolidation and shows their shareholding structure: Subsidiaries Direct shares

owned by parent company

(%)

Indirect shares owned by

parent company (%)

Non controlling

interest (%)

Alkim Kağıt (*) 79,93 - 20,07 Alkim Sigorta 50,00 39,96 10,04

(*) According to the decision of Board of Directors dated March 26,2015, the Company has applied to the

CMB for the sale of a part of shares or whole shares of its subsidiary Alkim Kağıt. Sale of the related shares has not been realised yet as of the date of these consolidated financial statements.

Offsetting All items with significant amounts and nature, even with similar characteristics, are presented separately in the financial statements. Insignificant amounts are grouped and presented by means of items having similar substance and functionWhen the nature of transactions and events necessitate offsetting, presentation of these transactions and events over their net amounts or recognition of the assets after deducting the related impairment are not considered as a violation of the rule of non-offsetting. As a result of the transactions in the normal course of business, revenue other than sales described in “Revenue Recognition” are presented as net provided that if the nature of the transaction or the event qualify for offsetting.

2.4 Summary of significant accounting policies Significant accounting policies applied in the preparation of these consolidated financial statements are summarized below: Revenue recognition Revenues are recognised on an accrual basis at the time deliveries are made, services are given and significant risks and rewards are transferred to the buyer, the amount of revenue can be measured reliably and it is probable that the economic benefits associated with the transaction will flow to the Group at the fair value of considerations received or receivable. Net sales represent the invoiced value of goods shipped less sales returns, sales discounts and commissions (Note 21). Rent income is recognised on an accrual basis, interest income is recognised on an accrual basis with effective yield method calculation. Dividend income is recognised when the right to receive dividend is possessed. Inventories Inventories are valued at the lower of cost or net realisable value. Net realisable value is the estimated selling price in the ordinary course of business, less the costs of completion and selling expenses. The cost components of inventories include materials, conversion costs and other costs that are necessary to bring the inventories to their present location and condition. The cost of inventories is determined on the process costing method and Group values its inventories based on weighted average cost (Note 7).

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(17)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

The Group fulfills the raw material need of the production facility located in Çayırhan/Ankara by using solution mining technique for processing sodium sulfate reserves (glaubert and thenardite layers). The Group accounts for related reserves in two ways. The first one is reserves in underground production panels that are in the process of industrial production, second one is reserves available in underground production panels which are not extracted and not used in production as of balance sheet date. The Company is recording the first form of mineral stocks by makingproven and probable reserve calculation related with underground reserve amount and extracted sodium sulfate amount from panels. The Company uses proven and probable mine reserve calculation and books only extracted part of reserves. Property, plant, equipment and related depreciation Property, plant and equipment acquired before January 1, 2005 are carried at cost in purchasing power of TL as at December 31, 2004; less accumulated depreciation and impairment losses. Property, plant and equipment acquired after January 1, 2005 are carried at cost less accumulated depreciation and impairment losses. Property, plant and equipment are capitalized and depreciated when they are fully commissioned and in a physical state to meet their designated production capacity. Depreciation is provided using the straight-line method based on the estimated useful lives of the assets (Note 11). Land is not depreciated as it is deemed to have an indefinite life. Residual values of property plant and equipment are considered to be immaterial. The estimated useful lives for property, plant and equipment are as follows: Yıl Land improvements 2 - 20 Buildings 8 - 50 Machinery and equipment 4 - 30 Motor vehicles 4 - 15 Furniture and fixtures 3 - 20 Property, plant and equipment are reviewed for impairment losses whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the carrying amount of the asset exceeds its recoverable amount. Gain or losses on disposals of property, plant and equipment with respect to their restated net book values are included in the related income and expense accounts (Note 11). Repair and maintenance expenditures are charged to the comprehensive income as they are incurred. Repair and maintenance expenditures are capitalised if they result in an enlargement or substantial improvement of the respective assets and depreciated over remaining useful life of related asset.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(18)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

Intangible assets Intangible assets comprise of computer software programme and development costs. The acquired before January 1, 2005 are carried at cost in the purchasing power of TL as at December 31, 2004; less accumulated amortisation and impairment losses; those acquired after January 1, 2005 are carried at cost less accumulated amortization and impairment losses, which are amortised using the straight-line method over three to ten years following the acquisition date in either case. In case of impairment, the carrying amount of an intangible asset is written down to its recoverable amount (Note 12). Development costs Research costs are charged to statement of comprehensive income when incurred. Development costs (or the improvement phase of an intergroup project) are recognised as intangible assets when the following criteria are met: - it is technically feasible to complete the intangible asset so that it will be available for sale or for

use, - completion of intangible assets , there is an intention to use or sell, - it can be demonstrated how the intangible asset will generate probable future economic benefits, - management intends to complete the intangible asset, use or sell it, - adequate technical, financial and other resources to complete the development or sell the

intangible asset are available, and - the expenditure attributable to the intangible asset during its development can be reliably

measured. Other development expenditures that do not meet these criteria are recognized as an expense as incurred. Development costs previously recognized as an expense are not recognized as an asset in a subsequent period. Development costs are amortised in five years following capitalization (Note 12). Impairment of assets Except for deferred tax assets each class of assets are reviewed for impairment losses at each balance sheet date whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognized for the amount by which the carrying amount of the asset or any cash generating unit of that asset exceeds its recoverable amount which is the higher of an asset’s net selling price and value in use. Impairment losses are accounted for in the statement of income. Impairment loss on assets can be reversed, to the extent of previously recorded impairment losses, in cases where increases in the recoverable value of the asset can be associated with events that occur subsequent to the period when the impairment loss was recorded. Borrowings and borrowing cost If the maturity of the borrowings is less than 12 months, these borrowings are classified in current liabilities and if more than 12 months, classified in non-current liabilities (Note 14). Borrowings are stated at amortised cost using the effective yield method. Any proceeds and the redemption value are recognized in the consolidated statement of income as borrowing cost over the period of the borrowings.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(19)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

Borrowing costs directly attributable to the acquisition, construction or production of an asset that necessarily takes a substantial period of time to get ready for its intended use or sale are capitalized as part of the cost of the respective assets. All other borrowing costs are expensed in the period they occur. Borrowing costs consist of interest and other costs that an entity incurs in connection with the borrowing of funds. Financial assets Loans and receivables constitute non-derivative financial instruments, which are not quoted in active markets and have fixed or scheduled payments. Loans and receivables arise, without held-for-sale intention, from the Group’s supply of goods, service or direct fund to any debtor. They are classified as current assets when they have a maturity less than 12 months, and non-current assets when they have a maturity more than 12 months as of balance sheet date. Loans and receivables are recognized initially at their fair value plus transaction costs directly attributable to the acquisition or issue of the financial asset. These loans and receivables are included in trade receivables and other receivables in the balance sheet. Loans are recorded at the proceeds received, net of any transaction costs incurred. In subsequent periods, loans are stated at amortised cost using the effective yield method. Recognition and derecognition of financial assets and liabilities Group recognizes a financial asset or financial liability in its balance sheet when only when it becomes a party to the contractual provisions of the instrument. Group derecognizes a financial asset or a portion of it only when the control on rights under the contract is discharged. Group derecognizes a financial liability when the obligation under the liability is discharged or cancelled or expires. All regular way financial asset purchase and sales are recognized at the date of the transaction, the date the Group committed to purchase or sell. The mentioned purchases or sales are ones which require the delivery of the financial assets within the time interval identified with the established practices and regulations in the market. Foreign currency transactions and balances Transactions in foreign currencies during the year have been translated at the exchange rates prevailing at the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies have been translated into TL at the exchange rates prevailing at the balance sheet dates. Foreign exchange gains or losses arising from the settlement of such transactions and from the translation of monetary assets and liabilities are recognized in the consolidated statements of income. Earnings per share Earnings per share indicated in the consolidated statements of comprehensive income are determined by dividing consolidated net income for the year by the weighted average number of shares that have been outstanding during the year concerned (Note 28).

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(20)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

In Turkey, companies can increase their share capital by making a pro-rata distribution of shares ("bonus shares") to existing shareholders from retained earnings and revaluation surplus. For the purpose of earnings per share computations, the weighted average number of shares outstanding during the year has been adjusted in respect of bonus shares issues without a corresponding change in resources, by giving them retroactive effect for the year in which they were issued and for each earlier year. In case of dividend distribution, earnings per share is calculated by dividing net income by the number of shares, rather than dividing by weighted average number of shares outstanding. Events after the balance sheet date Subsequent events, announcements related to net profit or even declared after other selective financial information has been publicly announced; include all events that take place between the balance sheet date and the date when balance sheet was authorized for issue (Note 32). In case the events require a correction subsequent to the balance sheet date, the Group makes the necessary corrections to the consolidated financial statements. Moreover, the events that occur subsequent to the balance sheet date and not require a correction to be made are disclosed in accompanying notes, when they may affect decision of making of users of financial statements. Provisions, contingent assets and contingent liabilities Provisions are recognized when the Group has a present legal or constructive obligation as a result of past events; it is more likely than not that an outflow of resources will be required to settle the obligation; and the amount has been reliably estimated. In cases where the time value of money is material, provisions are determined at the present value of expenses required to be made to settle the liability. The rate used to discount provisions to their present values is determined taking into account the interest rate in the related markets and the risk associated with the liability. This discount rate does not consider risks associated with future cash flow estimates. Possible assets or obligations that arise from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the Group are treated as contingent assets or liabilities. The Group does not recognise contingent assets and liabilities (Note 18). Accounting policies, changes in accounting estimates and errors Significant changes in accounting policies and errors are applied on a retrospective basis and reflected upon previous periods’ consolidated financial statements. Changes in accounting estimates involving single periods are reflected upon the current period when the change occurs; changes involving future periods are reflected both upon the current period when the change occurs and the future period, on a prospective basis.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(21)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

Leases Leases of property, plant and equipment are classified regarding the belonging of all the risks and rewards of ownership to lessor or lessee. According to this principle, leases of property, plant and equipment where the Group has substantially all the risks and rewards of ownership are classified as finance leases (Note 14). Leases of property, plant and equipment excluding finance leases are classified as operating leases. Payments for assets leased out under operating leases are reflected to statement of income as expense on a straight-line basis over the lease term even if the installments are not fixed. Rental income is also recognised on a straight-line basis over the lease term and reflected to statement of income as income; uncommitted to period of collections. Related Parties Parties are considered related to the Company if; (a) A person or a close member of that person's family is related to a reporting entity if that person:

(i) has control or joint control over the reporting entity; (ii) has significant influence over the reporting entity; or (iii) is a member of the key management personnel of the reporting entity or of a parent of the

reporting entity.

(b) parent, subsidiary and fellow subsidiary is related to the others. (i) The entity and the company are members of the same group. (ii) One entity is an associate or joint venture of the other entity (or an associate or joint

venture of a member of a group of which the other entity is a member). (iii) Both entities are joint ventures of the same third party. (iv) One entity is a joint venture of a third entity and the other entity is an associate of the third

entity. (v) The entity is a post-employment benefit plan for the benefit of employees of either the

reporting entity or an entity related to the reporting entity. If the reporting entity is itself such a plan, the sponsoring employers are also related to the reporting entity.

(vi) The entity is controlled or jointly controlled by a person identified in (a). (vii) A person identified in (a)(i) has significant influence over the entity or is a member of the

key management personnel of the entity (or of a parent of the entity). A related party transaction is a transfer of resources, services or obligations between related parties, regardless of whether a price is charged (Note 29). Segment reporting Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision maker. The chief operating decision-maker, who is responsible for allocating resources and assessing the performance of the operating segments, has been identified as the steering committee that makes strategic decisions. As the Group is engaged in two major business segments, namely mining and paper production, the financial information regarding business segments are reported in Note 3.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(22)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

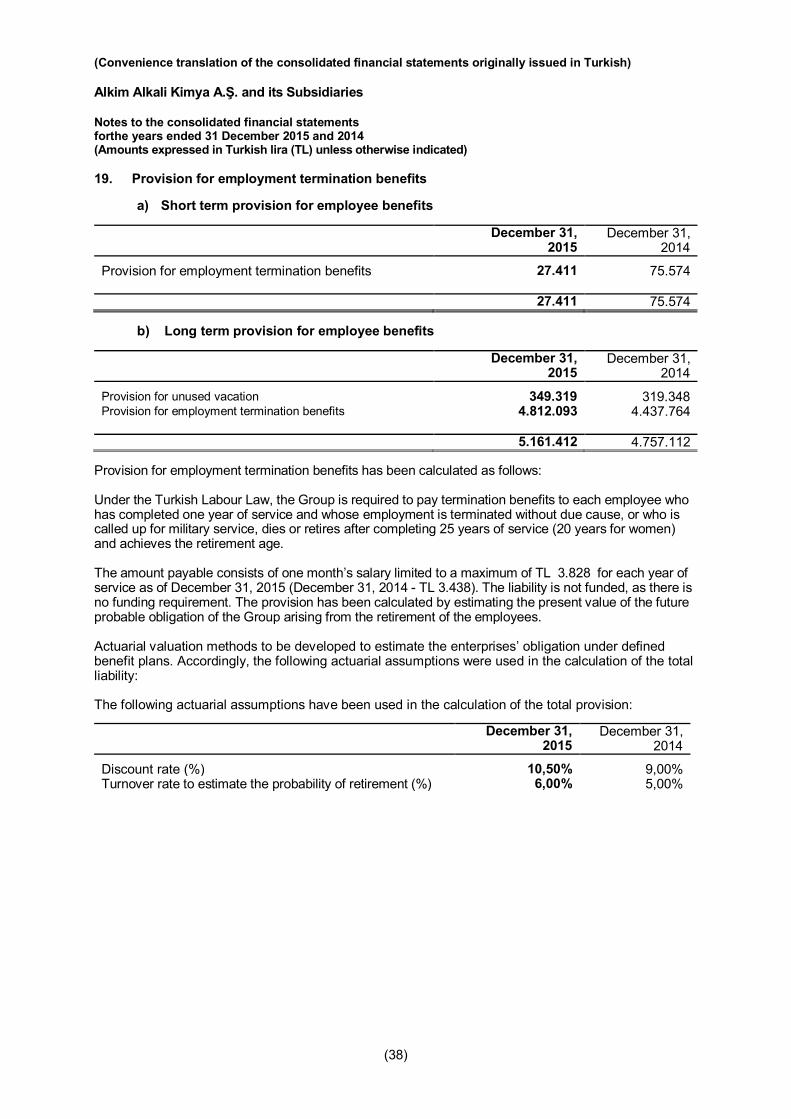

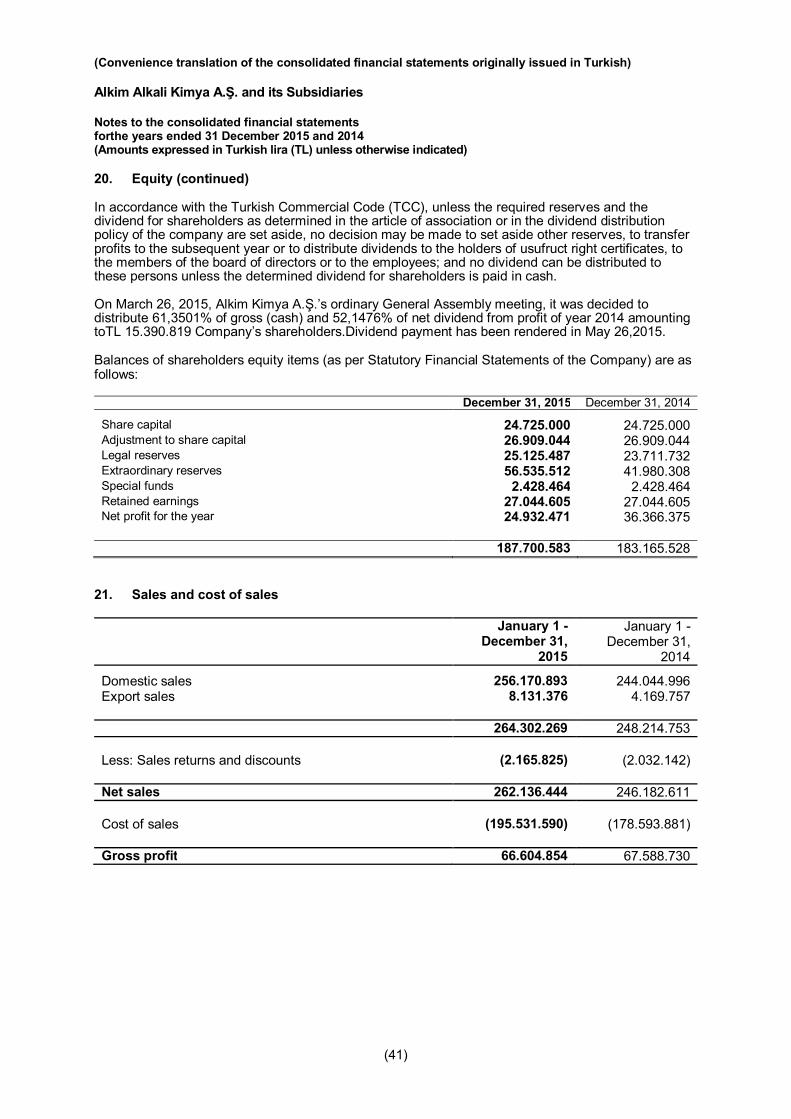

Taxation on income Taxation on income includes current income tax liability and deferred income taxes. Current income tax liability includes the taxes payable calculated on the taxable portion of period income with tax rates enacted on the balance sheet date and the correction adjustments related to prior period tax liabilities (Note 27). Deferred tax assets and liabilities are provided, using the liability method, for all temporary differences arising between the tax bases of assets and liabilities and their carrying values for financial reporting purposes with the enacted tax rates as of the balance sheet date (Note 27). Deferred tax assets or liabilities are reflected to the financial statements to the extent that they will provide an increase or decrease in the taxes payable for the future periods where the temporary differences will reverse. Deferred tax liabilities are recognised for all taxable temporary differences, where deferred income tax assets resulting from deductible temporary differences are recognised to the extent that it is probable that future taxable profit will be available against which the deductible temporary difference can be utilised. To the extent that deferred tax assets will not be utilised, the related amounts have been deducted accordingly. Deferred tax assets and deferred tax liabilities related to income taxes levied by the same taxation authority are offset accordingly, at individual entity level. Consequently, the net deferred tax positions of the parent company and the individual subsidiaries and joint venture are not offset in the consolidated financial statements (Note 27). Employee benefits/provision for employment termination benefits a) Defined benefit plans: In accordance with existing social legislation in Turkey, the Group is required to make lump-sum termination indemnities to each employee who has completed over one year of service with the Group and whose employment is terminated due to retirement or for reasons other than resignation or misconduct. In the financial statements, the Group has recognized a liability using the “Projected Unit Credit Method” based upon factors derived using the Group’s experience of personnel terminating and being eligible to receive benefits, discounted by using the current market yield at the balance sheet date on government bonds (Note 19). All actuarial gains and losses are recognized in the comprehensive income statement. b) Defined contribution plans: The Group pays contributions to the Social Security Institution on a mandatory basis. The Group has no further payment obligations once the contributions have been paid. The contributions are recognized as an employee benefit expense when they are due.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(23)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

Statement of cash flows In the statement of cash flows, cash flows are classified into three categories as operating, investing and financing activities. Cash flows from operating activities are those resulting from the Group’s operating activities. Cash flows from investing activities indicate cash inflows and outflows resulting from fixed asset and financial investments. Cash flows from financing activities indicate the resources used in financing activities and the repayment of these resources. For the purposes of the cash flow statement, cash and cash equivalents comprise of cash in hand accounts, bank deposits, mutual funds and loans originated by the Group by providing money directly to a bank under reverse repurchase agreements with a predetermined sale price at fixed future dates of less than or equal to three months. Trade receivables and impairment of receivables Trade receivables that are created by the Group by way of providing goods or services directly to a debtor are carried at amortised cost, using the effective interest rate method, less the unearned financial income. Short duration receivables with no stated interest rate are measured at original invoice amount unless the effect of imputing interest is significant. A credit risk provision for trade receivables is established if there is objective evidence that the Group will not be able to collect all amounts due. The amount of the provision is the difference between the carrying amount and the recoverable amount, being the present value of all cash flows, including amounts recoverable from guarantees and collateral, discounted based on the original effective interest rate of the originated receivables at inception. If the amount of the impairment subsequently decreases due to an event occurring after the write-down, the release of the provision is credited to other income in the consolidated statements of income (Note 24). Trade receivables from certain customers that are assigned to a factor by the Company, are followed as long and short term trade receivables in the accompanying balance sheet and commission paid to factoring company as a result of the mentioned transaction. Payable to factoring company is followed as long and short term other financial liabilities in the balance sheet (Note 5 and 15). Trade payables Trade payables are initially recognized at fair value and subsequently measured at amortised cost using the effective interest method (Note 5). Share capital and dividends Share capital is classified as capital and dividends distributed from common stocks are deducted at the period of the declaration from the retained earnings. 2.5 Significant accounting estimates and decisions Preparation of consolidated financial statements requires disclosure of reported assets and liabilities, contingent assets and liabilities as at balance sheet date and utilisation of estimates and assumptions that can effect income and expense balances of the reporting period. Estimations and assumptions can differ from actual results in spite of these estimations and assumptions are based on Group management’s best knowledge. Significant accounting estimates are as follows:

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(24)

2. Basis of presentation of consolidated financial statements and accounting policies (continued)

a) Income taxes There are many transactions and calculations for which the ultimate tax determination is uncertain during the ordinary course of business and significant judgment is required in determining the provision for income taxes. The Group recognises tax liabilities for anticipated tax issues based on estimates of whether additional taxes will be due and recognises tax assets for the carry forward tax losses and unused investment tax credits to the extent that the realisation of the related tax benefit through the future taxable profits is probable (Note 27). Where the final tax outcome of these matters is different from the amounts that were initially recorded, such differences will impact the income tax and deferred tax provisions in the period in which such determination is made. b) Provision for employment termination benefits: To calculate the employee benefit provision actuarial assumptions relating to turnover ratio, discount rate and salary increase are used. Calculation details are given in Employee benefits disclosure (Note 19). c) Economic useful lives: Tangible assets, and intangible assets, have been depreciated and amortised by using estimated useful lives. Estimated useful lives determined by management have been disclosed in Note 2.4 d) Provisions for doubtful receivables Provisions for doubtful receivables reflect the amounts remaining as of the balance sheet date but believed to compensate the future losses which can be resulting from the risk of not being able to collect the receivables within the context of the current economical conditions(Note 5). e) Allowance for decrease in value of inventories While the decrease in value of inventories is computed just for the goods, the periods of holding the goods in inventory and their physical situation is considered by taking the technical staff’s opinion into account. The inventories accepted as inactive goods may also be subject to regenerating. The recognition of decrease in value of inventories is conducted through taking the losses resulting from regeneration process into account. (Note 7) f) Legal reserves The group management evaluates the liabilities which can emerge by losing a case or a possibility of losing within the advisory of experts and Group’s legal counsel. Group management decides on the amount for legal reserves by basing it on the best estimates(Note 24). 2.6 Comparable information and adjusting the previous dated financial statements So as to ensure the detection of the financial situation and performance trends, the group’s finacial statements concerning the current period are drafted through the comparison with the previous period. For providing the compliance with the presentation of current period’s financial statements, the comparable information would be re-classified if needed. The classifications made over the Group’s financial statements of profit or loss for the year ending on 31 December 2014 are as follows: The revenue from power sale amounting to TL 507.102 which is shown in proceeds accounts group are disclosed under the other incomes account group.

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(25)

3. Segment reporting The Group’s primary reporting format is business segments. A business segment is a group of assets and operations engaged in providing products or services that are subject to risk and return that are different from those of other business segments. The Group is organised mainly into three main business segments. - Chemical products: Production and sales of Sodium Sulphate and derivatives - Paper: Production and sales of paper products - Other operations segment Other operations of the Group mainly comprise insurance which is not significant enough to qualify as an individual reportable segment in accordance with Turkish Financial Reporting Standards. Since the operations of the Group out of Turkey is not significant enough to be reportable in the basis of consolidated financial statements and monetary seasonality, the reportings based on the geographical segments have not been disclosed in the consolidated financial statements. Segment assets consist primarily of property, plant and equipment, intangible assets, inventories, receivables and operating cash. They exclude deferred income tax assets. Segment liabilities comprise operating liabilities. They exclude items such as bank borrowings, taxation on income and deferred income tax liabilities. Capital expenditure comprises additions to property, plant and equipment and intangible assets. The segment results for the year ended January 1 - December 31, 2015 are as follows:

Chemical products Paper Other Total

Total gross segment sales 113.270.805 150.437.558 405.665 264.114.028 Inter-segment sales - (5.970) (1.971.614) (1.977.584) Net sales 113.270.805 150.431.588 (1.565.949) 262.136.444 Operating profit/(loss) segment result 25.045.892 6.685.383 83.245 31.814.520 Income from investment activities 646.833 8.776.708 1.339 9.424.880 Financial income 1.549.060 1.732.815 306.088 3.587.963 Financial expense (1.833.227) (6.153.718) (220.802) (8.207.747) Profit before taxes on income/(expense) 25.408.558 11.041.188 169.870 36.619.616 Taxes on income/(expense) (3.037.335) (988.405) - (4.025.740) Net profit/(loss) for the year 22.371.223 10.052.783 169.870 32.593.876

The segment results for the year ended January 1 - December 31, 2014 are as follows:

Chemical products Paper Other Total Total gross segment sales 121.534.386 126.098.205 403.879 248.036.470 Inter-segment sales (6.241) (83.632) (1.763.986) (1.853.859) Net sales 121.528.145 126.014.573 (1.360.107) 246.182.611 Operating profit segment result 30.498.484 (8.758.452) 93.262 21.833.294 Income from investment activities 992.379 2.419.363 988 3.412.730 Financial income 3.516.628 1.188.906 44.382 4.749.916 Financial expense (3.932.031) (3.866.409) (38.210) (7.836.650) Profit before taxes on income 31.075.460 (9.016.592) 100.422 22.159.290 Taxes on expense (5.080.819) 2.063.468 - (3.017.351) Net profit for the year 25.994.641 (6.953.124) 100.422 19.141.939

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(26)

3. Segment reporting (continued) The segment assets and liabilities at December 31, 2015 and capital expenditure for the year then ended are as follows: Chemical

Products Paper Other Total Assets 132.992.416 147.226.602 531.552 280.750.570 Deferred income tax assets (Note 27) 38.711 - - 38.711 133.031.127 147.226.602 531.552 280.789.281 Liabilities 12.724.021 14.865.192 1.629.645 29.218.858 Bank borrowings and financial liabilities 5.402.334 33.150.206 - 38.552.540 Provision for income taxes (Note 27) 24.359 - - 24.359 Deferred income tax liabilities (Note 27) - 206.625 - 206.625 18.150.714 48.222.023 1.629.645 68.002.382 Capital expenditures 7.287.031 505.043 7.792.074 The segment assets and liabilities at December 31, 2014 and capital expenditure for the year then ended are as follows: Chemical

Products Paper Other Total Assets 131.328.285 114.745.689 388.135 246.462.109 Deferred income tax assets (Note 27) 173.171 635.271 - 808.442 131.501.456 115.380.960 388.135 247.270.551 Liabilities 11.485.738 12.925.263 1.467.540 25.878.541 Bank borrowings and financial liabilities 12.053.819 13.024.564 - 25.078.383 Provision for income taxes (Note 27) 406.908 - - 406.908 Deferred income tax liabilities (Note 27) - - - - 23.946.465 25.949.827 1.467.540 51.363.832 Capital expenditures 6.256.889 724.983 - 6.981.872 4. Cash and cash equivalents December 31,

2015 December 31,

2014 Cash 43.149 55.137 Banks 52.827.087 25.654.725 - TL denominated time deposits 6.388.169 6.400.000 - TL denominated demand deposits 792.468 314.463 - Foreign currency denominated time deposits 44.642.036 18.260.470 - Foreign currency denominated demand deposits 1.004.414 679.792 Other 33.891 700.549 52.904.127 26.410.411

Negative: interest accrual on time deposits (20.425) -

Total cash and cash equivalentsas the basis of cash flow 52.883.702 26.410.411

(Convenience translation of the consolidated financial statements originally issued in Turkish) Alkim Alkali Kimya A.Ş. and its Subsidiaries Notes to the consolidated financial statements forthe years ended 31 December 2015 and 2014 (Amounts expressed in Turkish lira (TL) unless otherwise indicated)

(27)