Alia Ahmed Abdallah Ibrahim - repo.uofg.edu.sd

194

1 A Suggested EFL Programe for Islamic Economics Translation in Sudanese Institutes: A Case Study of Islamic Bank, Islamic Funds,(2016) Alia Ahmed Abdallah Ibrahim 2017

Transcript of Alia Ahmed Abdallah Ibrahim - repo.uofg.edu.sd

1

A Suggested EFL Programe for Islamic Economics Translation

in Sudanese Institutes:

A Case Study of Islamic Bank, Islamic Funds,(2016)

Alia Ahmed Abdallah Ibrahim

2017

2

A Suggested EFL Programe for Islamic Economics Translation

in Sudanese Institutes:

A Case Study of Islamic Bank, Islamic Funds,(2016)

Alia Ahmed Abdallah Ibrahim

B.A. Faculty of Education -in English Language- University of

Khartoum(1980)

M.A. Faculty of Education -in English Language- University of

Khartoum(1992)

A thesis

Submitted for the Degree of Doctor of Philosophy

in

Applied Linguistics

Department of Foreign Languages

Faculty of Education –Hasahisa

University of Gezira

February/2017

3

A Suggested EFL Programe for Islamic Economics Translation

in Sudanese Institutes:

A Case Study of Islamic Bank, Islamic Funds,(2016)

Alia Ahmed Abdallah Ibrahim

Supervision Committee

Name Position Signature

Dr. Hassan Ali Eissa Main supervisor ………………

Dr. Ahmed Gasm Alseed Co-supervisor

………………

February/2017

4

A Suggested EFL Programe for Islamic Economics Translation

in Sudanese Institutes:

A Case Study of Islamic Bank, Islamic Funds,(2016)

Alia Ahmed Abdallah Ibrahim

Examination Committee

Name Position Signature

Dr. Hassan Ali Eissa Chairperson

……………….

Dr. Ibrahim Mohamed Alfaki External Examiner

………….

Dr. Abdul Gadir Muhmmed Ali Internal Examiner

……………

Date of Examination: 2/2/2017

5

Dedication

To the soul of my mother and father who did everything possible to see their

education ambitions personified on us. To my son and daughters and their

father Dr. Bakri Mekki who contributed to this research through a hard task of

the computer work and correction and I hope this thesis will be an incentive

for my son and daughters to seek learning and contribute it to others.

6

Acknowledgement

First praise be to Allah for the completion of this thesis.

I would like to express my gratitude and appreciation to my Supervisor,

Dr. Hassan Ali Eissa, the former Head of the Department of Translation and

Arabasization (U of K), who inspires me with this academic programme, that I

choose it to be the translation of the Islamic economy. Also, I thank him for his

valuable directives and comments. My special thanks also go to my co-

superviser Dr. Ahmed Yousef Awad who made every possible effort to help

me with the methodology of this research. Also, I want to express my heartfelt

gratitude and appreciation to Dr. Muhammed Elfatih Hamid, the former Dean

of the Faculty of Law (UofK) and former legal advisor of the Islamic

Development Bank (Jeddah); who exerted Laudable efforts that I could

understand this complicated Islamic Economics Subject, for I am only a

graduate student of Languages with complete lack of economic knowledge.

On the other hand I extend thanks to Dr. Bashir Omer who supplied me with

notable references in Islamic economics from "The Islamic Research

Institute"(IRTI) of the Islamic Development Bank (Jeddah).

7

A Suggested EFL Programe for Islamic Economics Translation in

Sudanese Institutes:

A Case Study of Islamic Bank, Islamic Funds,(2016)

Alia Ahmed Abdallah Ibrahim

Abstract

The research is an attempt programme for the translation if Islamic economies to the

Sudanese universities and institutes. Present through details about the Islamic economic so,

students have to well acquainted and fatty understand the terms, the construction of

sentences and the mechanism of the subject itself, so they can translate precisely, accurately

and naturally. The Islamic economy and the feed lack will be supper. The methodology is

reflected in the great number and multi-texts taken from the great numbers of Islamic

economic terms and phrase. All these text and terms are being translated by those

professional translators as well as by researcher himself. So findings of this research is that,

notice that with such understanding of the subject itself, its terms phrase and how

explanation these terms and details works in their application and hence the translation

process is easier precise and natural. The researcher recommended that, I hope that Sudanese

universities and institutes adopt such programme within their courses of translation and the

researcher think that it‟s a new important subject to be added to the other domain for

translation.

8

:حبىت ىذراست بربح ترخت الاقتصبد الإسلاي في اىدبؼبث

(2016)دسحعش كخش حزى حلإعلا٤ش ،حقخد٣ن حؼشر٤ش،

ابراي ػبذالله ػبىيت احذ

يخص اىبحث

حلاهظقخد حلإعلا٢ ك٢ حـخؼخص حؼخذ ٣ؼذ زح حزلغ لخش مغ رشخؾ ظذس٣ظ طشؿش

حغدح٤ش، ك٤غ ٣ظؼشك حزخكغ ظلخف٤ حعؼش ػ٤وش ـحذ حؼذ٣ذس خدس حلاهظقخد حلإعلا٢ كظ٠

٣ظ هخذ حظشؿش حل حؼ٤ن قطلخص حظؼشف ػ٢ آ٤ش ر٤ش ز حـ حقطلخص

ض ك٢ حزى حلإعلا٤ش أ حقخد٣ن حؼشر٤ش حظ٢ طظؼخ ك٢ ػذ ططز٤و٤خ ػ٢ حسك ححهغ عحء خ

زح حـخ، رخظخ٢ ط حظشؿش طشؿش فل٤لش هز٤ؼ٤ش عغش. أخ حطش٣وش حظ٢ حطزؼخ حزخكغ ك٢

ـخ رلؼ ك٢ ػزخسس ػ أػذحد خثش ظػش رظع حؼ لغ قؿ طؾ حؼذ٣ذ أؿ

٢, حؼذ٣ذ حقطلخص حؼزخسحص حظؼوش رخلاهظقخد حلإعلا٢. طشؿش ز حلاهظقخد حلإعلا

حقؿ هز ظشؿ٤ ظخقق٤ هز حزخكغ لغ. رخظخ٢ كخ ظخثؾ زح حزلغ خ

لاكع حزخكغ أ حل حؼ٤ن زح حؼ ر حظلخف٤ حظؼوش رؤؿ حخظلش قطلخص

ؽشف حك٢ خ ٣ظؼن رزح حؼ، خسعش طشؿش حقؿ حخظلش ؼشكش آ٤ش حؼ ػزخسحص

لغ ػذ حظطز٤ن ك٢ حزى حلإعلا٤ش حقخد٣ن حؼشر٤ش ـذ أ ػ٤ش طشؿش زح حؼ ط عش

غ ك٢ فل٤لش هز٤ؼ٤ش ؿ٤ش قػش ـ ك٢ ـش حلأف الا خك٤ش حؼ٢. ٣ؤ حزخك

طف٤خط أ طو حـخؼخص حؼخذ حغدح٤ش حظ٢ طذسط خدس حظشؿش ربمخكش طشؿش حلاهظقخد

حلإعلا٢ ؼ ؿذ٣ذ م حسعخص حؼذ٣ذس ظشؿخص حؼذ٣ذس ك٢ حـخلاص حخظلش.

9

Table of Contents

Page Subject No

iii Dedication 1

iv Acknowledgements 2

v Abstract (English) 3

v Abstract (Arabic) 4

vi Table of Contents 5

CHAPTER ONE:INTRODUCTION

1 Background 1.0

1 What is Translation? 1.1

4 Problems of the Study 1.2

5 Objective of the Study 1.3

5 The Importance of the Research 1.4

6 Significance of the Study 1.5

7 Research Method 1.6

7 Limitation of the Study 1.7

7 Definition of Related Terms 1.8

CHAPTER TWO:LITERATURE REVIEW

10 Introduction 2.0

10 History of Islamic Economics 2.1

11 Early Islamic Economics 2.2

12 Economy in the Caliphate (Edit) 2.3

13 Agriculture in the Medieval Islamic World (Edit) 2.4

10

15 Ibn Khaladun 2.5

15 What is the Role of Religion on Economics?

2.6

18 Competitive Price Mechanism, Transparency and

Disclosures are Parts of The Market Function

2.7

20 Fundamentals of Islamic Economic Systems 2.8

26 Global English and the Role of Translation 2.9

27 Translation Activities 2.10

30 The Main Prohibitions and Business Ethics in Islamic

Economics

2.11

34 Avoiding Interest 2.12

40 Islamic Law of Contract and Business Transaction

2.13

40 MAL (Wealth), Usufruct and Ownership 2.14

42 Interpreting and Translating Techniques 2.15

45 General Framework of Contracts 2.16

47 Avoiding Riba 2.17

49 Trading in Islamic Commercial Law 2.18

52 Prices and Profit Margin 2.19

53 Loan and Debt in Islamic Commercial Law 2.20

58 Islamic Finance Products and Procedures 2.21

60 The Deposits Side of Islamic Banking 2.22

63 2 Islamic Investment Banking 2.23

67 STIANA'A (Order to Manufacture) 2.24

69 The Role of Translation Theory in Translator Training 2.25

70 Participatory Modes: Shirkah and its Variants 2.26

71 Legality, Forms and Definition of Partnership 2.27

72 Mudarabah 2.28

11

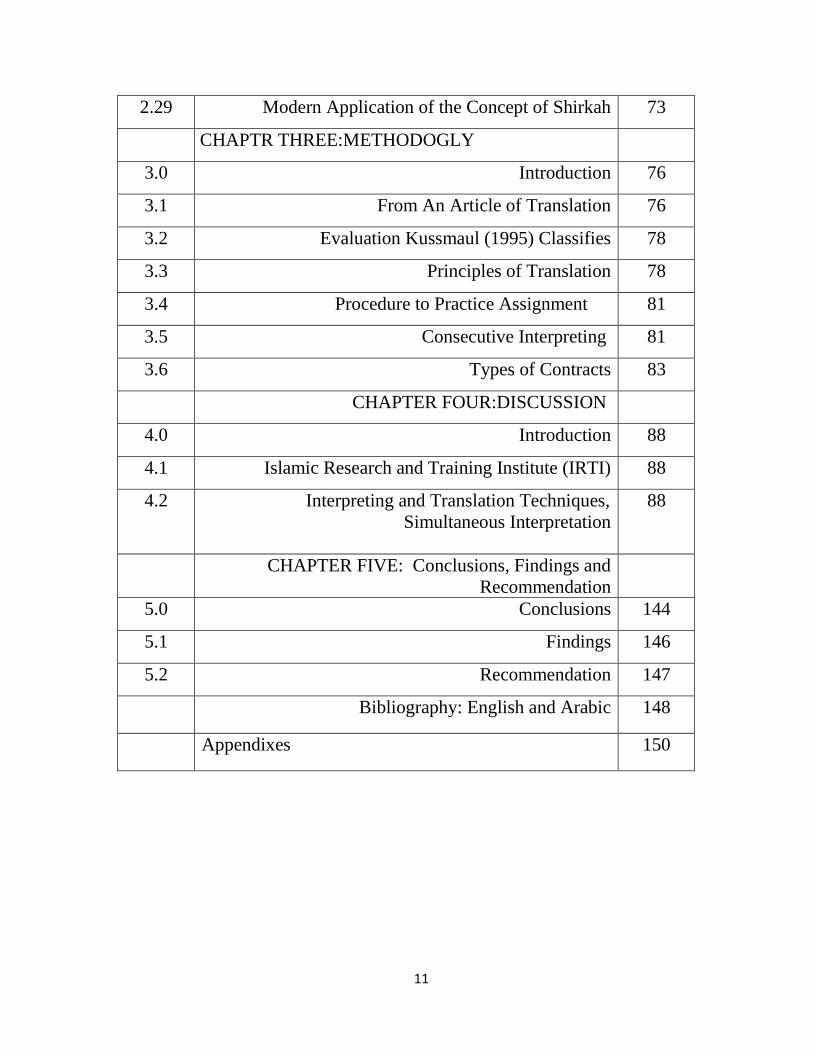

73 Modern Application of the Concept of Shirkah 2.29

CHAPTR THREE:METHODOGLY

76 Introduction 3.0

76 From An Article of Translation 3.1

78 Evaluation Kussmaul (1995) Classifies 3.2

78 Principles of Translation 3.3

81 Procedure to Practice Assignment 3.4

81 Consecutive Interpreting 3.5

83 Types of Contracts 3.6

CHAPTER FOUR:DISCUSSION

88 Introduction 4.0

88 Islamic Research and Training Institute (IRTI) 4.1

88 Interpreting and Translation Techniques,

Simultaneous Interpretation

4.2

CHAPTER FIVE: Conclusions, Findings and

Recommendation

144 Conclusions 5.0

146 Findings 5.1

147 Recommendation 5.2

148 Bibliography: English and Arabic

150 Appendixes

12

CHAPTER ONE

INTRODUCTION

1.0 Background

In this introduction, the researcher wants to reveal how the concept of studying

translation of Islamic economy with hope of attaining professional cadres in this field comes

into her mind. A friend had been graduated with languages from UofK, made the diploma in

(health translation) and there is a (legal translation). Both diplomas act as a license for any

person to work in these fields in England, provided that those graduates who attain these

diplomas are regarded as professional translators. The researcher notices the perpetual calls

for medical translation from the different hospitals and clinics, especially for those people

coming from the Gulf States. Definitely, this is a very serious field, the translator must be

well acquainted with the terminology and proper accurate medical background for such kind

of translation. So, this is what makes the attempt for the adaptation of such system and

applies it to the translation of Islamic economics.

1.1 What is Translation?

1.1.1 The Global Approach

The most remarkable translation theorists (Dellise, Newmark, Nida, Nord, Kussaul)

are in agreement to the following aspects concerning the main approaches to a translation

and interpretation of text.

- First, the comprehension and interpretation of texts with consideration to the textual,

referential, cohesion and naturalness levels. This competence embodies reading

comprehension and message interpretation i.e encoding and decoding.

- Secondly, re-wording is so essential. It is the application of different strategies for

(recoding) i.e the restitution process of the message and this happens by choosing the

right methods, techniques and procedures. There a translator may resort to transfer,

cultural or functional equivalent, synonymy, modulation, compensation, reduction

and expansion (see Newmark, P.,1995: A textbook of translation).

13

- Thirdly, those translation theorists focuses on the importance of the assessment of

the result comparing the translated text with the original text. It will be an accurate

revision of the output that will result in a final translation of higher quality.

1.1.2 Statistical System

In this research, there is a hard effort exerted to study and understand the essence

and the core of this different unique Islamic subject with its strong religious law of

prohibitions and permissions. The researcher is indebted to Dr. Mohmad Elfatih Hamid,

former Dean of the faculty of law (u of k) and the legal adviser to the president of the

Islamic Development Bank (IDB), who tries to explain and interpret most of these

complicated delails, senses and terminologies of these principles and fundamentals, their

procedures system applications and mainly their mechanism. So, this makes it possible to

present this attempt of reflecting a reasonable understanding of the Islamic finance. So,

unless one reaches this reasonable understanding of the various constituent subject matters

of Islamic economics such as Salam, murabaha, Mudarabah, Istisna'a, Istijrar, Takaful and

musharakah etc, their precise definitions ,terminologies, their mechanism; the process of

translation will be impossible.

There are attempts done for the adaptation of this diploma (DPSI) mode and

procedure to suit the Islamic economic translation, hoping to get the expected output;

and attaining professional cardre of Islamic economic translators.

The concentration on the understanding thoroughly of the main core and essence of

the research ie the subject itself with its peculiarities and uniqueness, it's various

subject matters, its prohibition and what is allowed, is so essencial.

There must be a concentration also on understanding thoroughly what is called a

peculiar unique (words, terms, phrases) connected with various subject matters of the

disciphine (Islamic economics).These constituents are such as Salam, Murabaha,

musharaka, Istisna, Mudarabah, Istijrar, Takaful etc . Each subject matter contains

definitions, terminologies, concepts and mainly its application on reality. The sense

of these subjects must be deeply understood. The researcher tried to define the

subject, its terms and phrases as well as exposing texts,for sight translation, and

written translation and how these texts work within the Islamic economic system.

14

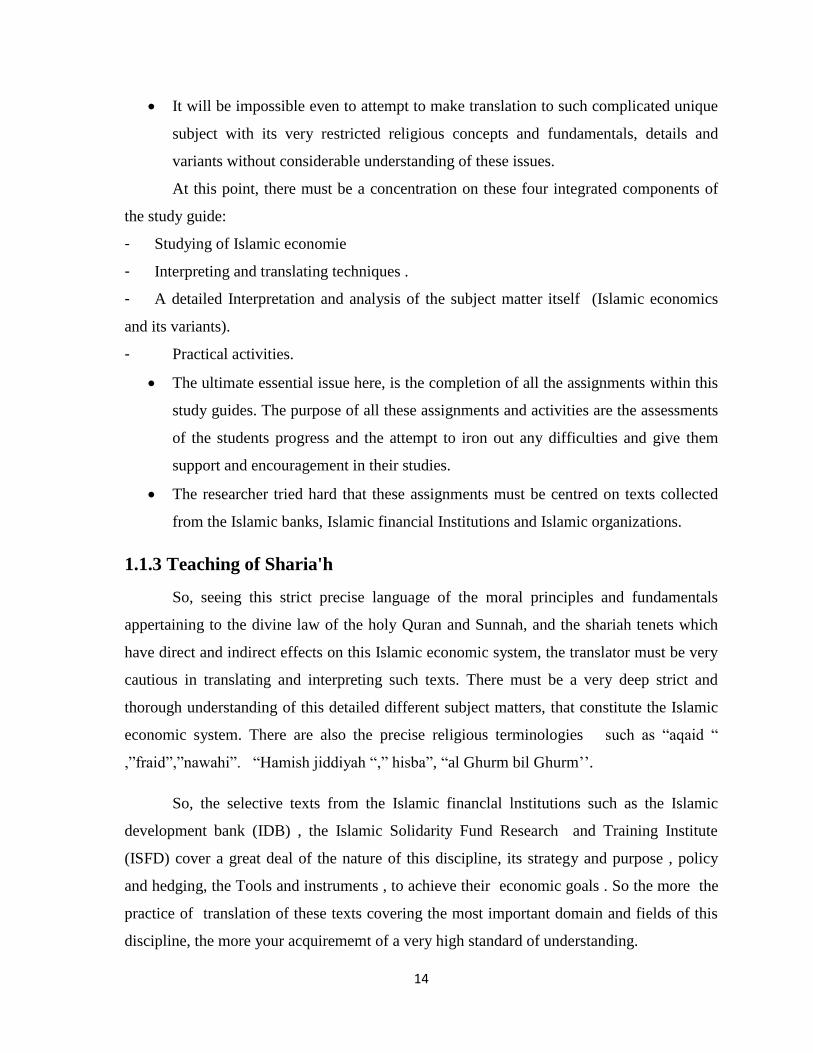

It will be impossible even to attempt to make translation to such complicated unique

subject with its very restricted religious concepts and fundamentals, details and

variants without considerable understanding of these issues.

At this point, there must be a concentration on these four integrated components of

the study guide:

- Studying of Islamic economie

- Interpreting and translating techniques .

- A detailed Interpretation and analysis of the subject matter itself (Islamic economics

and its variants).

- Practical activities.

The ultimate essential issue here, is the completion of all the assignments within this

study guides. The purpose of all these assignments and activities are the assessments

of the students progress and the attempt to iron out any difficulties and give them

support and encouragement in their studies.

The researcher tried hard that these assignments must be centred on texts collected

from the Islamic banks, Islamic financial Institutions and Islamic organizations.

1.1.3 Teaching of Sharia'h

So, seeing this strict precise language of the moral principles and fundamentals

appertaining to the divine law of the holy Quran and Sunnah, and the shariah tenets which

have direct and indirect effects on this Islamic economic system, the translator must be very

cautious in translating and interpreting such texts. There must be a very deep strict and

thorough understanding of this detailed different subject matters, that constitute the Islamic

economic system. There are also the precise religious terminologies such as “aqaid “

,”fraid”,”nawahi”. “Hamish jiddiyah “,” hisba”, “al Ghurm bil Ghurm‟‟.

So, the selective texts from the Islamic financlal lnstitutions such as the Islamic

development bank (IDB) , the Islamic Solidarity Fund Research and Training Institute

(ISFD) cover a great deal of the nature of this discipline, its strategy and purpose , policy

and hedging, the Tools and instruments , to achieve their economic goals . So the more the

practice of translation of these texts covering the most important domain and fields of this

discipline, the more your acquirememt of a very high standard of understanding.

15

The researcher is keen to present some texts that represent the core and essence of

the subject matters and topics. Some of these texts are translated by professional translators

of the Islamic banks. The texts are presented to show how such translation is achieved. So

students aquire knowledge concerning the theories and the methodologies in dealing with

this type of translation.

It is the important to understand thoroughly the terminologies concerning the

discipline whether they belong to the conventional economics or the Islamic economics

special subject matters such as mudarabah , murabaha, Istijrar , musawma, salam , takaful,

“Hamish Jiddiya” “ Bai Tawliyah “,”Bai al Inah.”

1.2 Problems of The Study

1. Translation is a challenging activity; there are difficulties arising during the

translation process. Languages have their own grammar structure, grammar rules and

different syntax.

2. During the translation process, some particular problems appear:

3. Problems of ambiguity: such problems originate from structural and lexical

differences between languages as well as multiword units such as idioms and

collocations.

4. There are the problems of grammar where many constructions of grammar and their

rules are not properly understood.

5. Problems of language: It includes terms and neologisms, slang which is difficult to

understand, proper names of people, organizations and places.

6. Problems of source text. These are illegible text, spell incorrectly.

7. Since languages differ from each other in many ways for example small words are

hard to translate and the meaning of common words depends on context.

8. Conveying the same meaning to the target languages is not an easy task for

translators; such as the translation of literature, poems and songs, so here translators

must be familiar with the two languages, and the translation is not matter of

translating words but of finding ones that rhyme well.

16

9. There is another problem which is lacking of vocabulary knowledge which leads to

the much use of dictionary for advanced text makes the process of translation very

boring.

10. The text problem is the encountering of complex grammar structure that must be

interpreted correctly.

1.3 Objective of the Study

In this thesis, the researcher has selected a wide range of topics that showed the

essence of the Islamic economic and Islamic finance. So, Islamic Economies subject is

loaded with the essential details concerning the various types of topics and the researcher

presented them in a simple clear language for a thorough and deep understanding and hence

the process of translation will be easier, accurate and precise. So this shows the target and

goal from the academic program of the Islamic economic translation in order to have

professional translator cadre within this domain.

1.4 The Importance of the Research

The most important issue about these texts is that, they deal with the different

Islamic economic topics, their precise definitions, concepts, how they work within the

market and financial reality. So translation and interpretation into Arabic and vise versa for

each text of these is so essential for practicing and acquiring both knowledge and translation

within this field.

The researcher describes this discipline as pecutiar or unique. The reference is to the

terminologies and concepts which often differ from the conventional economy. Such

phrases and terms are like “AL Ghnum bil Ghnum”,”Bai AlKali bil kali“, "Bai' al 'Inah",

"Bai' al Hasat" . The senses and implications of these terms and phrases must be shown.

The third step concerning this discipline as well as the activities related to the

interpretation, sight tranatalion and written translation from and into English and Arabic is

represented in the recommendations, that instead of the CDs mentioned before, groups of

students are called to perform conferences and meetings to discuss varous Islamic

economic topics. So students can practice interpretation and translation of these texts and

the feedback will be excellent.

17

1.5 Significance of the Study

Students in Sudanese universities and institutes lack background for the Islamic

economy subject as a whole; and also have linguistic difficulties, but with such research

study that covers many syntactic, semantic, lexical and many other aspects within these

multi-texts, will overcome such difficulties and problems. But the task is hard and complex

with numerous obstacles as Delisle put it (1981): “Translation is an arduous job that

mortifies you and put you in a state of despair at times, but also an enriching and

indispensable work, that demands honesty and modesty.”

At the same time, the whole translation process aims at the essence of the message

and its transparence faithful and accurate fixed background as Nida and Taber (1974) said:

“Translating consists of reproducing in the target language, the

nearest equivalent to the message in the source language in the first

place, in the semantic aspect and in the second place, in the stylistic

aspect.”

But surely, the quality of translation mainly depends on the quality of the translator.

So, translator knowledge, skills, training, cultural background, expertise and even mood are

needed. NewMark (1956) surmmerises the translator characteristics in the following:

1. Reading comprehension, and ability in a foreign language.

2. Knowledge of the subject.

3. Sensitivity to languages (both mother tongue and foreign language)

4. Competence to write the target language dexterously, clearly, economically and

resourcefully.

In addition, Mercedes Tricas (1995) mentions the six senses "making use of that

combination of intelligence, sensitivity and intuition." "this phenomenon works very well if

handled cautiously."

Delisle (1980) banishes the theorists who claim that linguistic competence is

condition to translate properly. Delisle states that reading comprehension ability, the

knowledge of the specialized subjects derived from specialized training and a wide cultural

background and the global vision of cross- cultural and inter lingual communication, are a

must to learn to handle the strategic and tactical tools for a good translating performance.

18

1.6 Research Method

The main goal of the study is to evaluate and analyze Islamic Econmic Translated

texts. The researcher follows the English law Diploma, its interpreting and translating

techniques, legal English and second language (Arabic) equivalent and practical activities

methods, that is also shown in Islamic Economic study, the theories of translation and their

application on the multi various texts.

1.7 Limitation of the Study

This study has been achieved mainly on texts and information from the Islamic

Banks, Islamic Financial Institutions, Arab Funds, Islamic Development Bank (IDB), The

Islamic Solidarity For Development (ISFD) and others.

1.8 Definition of Related Terms

The Islamic economics is distinguished with this essential and very curious

phenomenon which is personified in Arabic terms. Such terms are important and needful for

both Arabic –speaking as well as the non-Arabic speaking; due to their specific

environmental, cultural, religious and legal dimensions. So a translator who translates from

Arabic into English and vice versa must be well acquainted with all these dimensional

senses to reflect correct specific meanings in the target language.

Examples of such terms are: Mithaq 'Ahd or W'adah and 'Aqd.

Mithaq: - means a covenant; it is an earnest and firm determination on the part of the two

parties to fulfill their contractual obligations. The terms has more sanctity, it's used in the

holy Quran e.g. Mithaq are the treaties in the early Islamic era; also Mithaq is a contract of

marriage.

'Ahd or W'adah:- 'Ahd refers to a unilateral promise or undertaking. The terms also cover

a bilateral obligation. The Quran says “(But righteous) are those who fulfill the contracts,

which they have made”.

'Aqd (contract):- one concludes from the various definitions that 'Aqd in a specific sense,

is a combination of an offer (Ijab) and acceptance (Qabul), which gives rise to certain legal

consequences in relation to the subject matter, or as Abd Al-Rrazzag Al-Sanhuri defines

'Agd as "the concurrence of two wills to create an obligation or to shift it or to relinquish it".

19

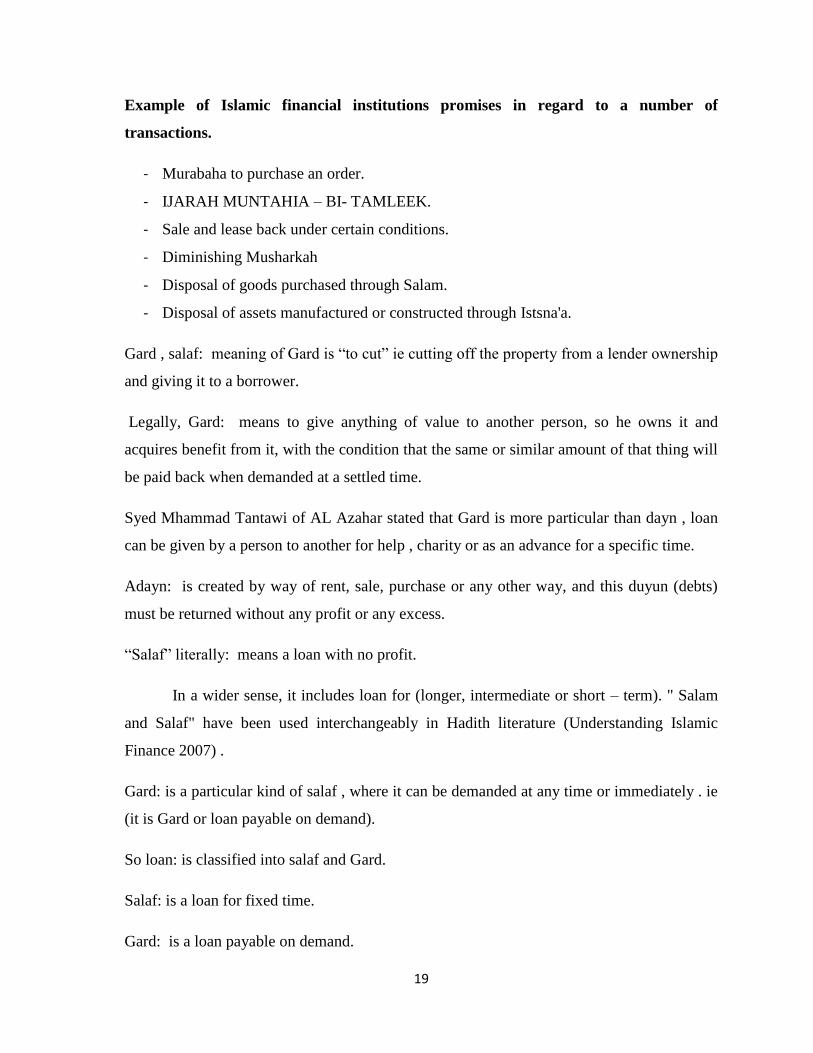

Example of Islamic financial institutions promises in regard to a number of

transactions.

- Murabaha to purchase an order.

- IJARAH MUNTAHIA – BI- TAMLEEK.

- Sale and lease back under certain conditions.

- Diminishing Musharkah

- Disposal of goods purchased through Salam.

- Disposal of assets manufactured or constructed through Istsna'a.

Gard , salaf: meaning of Gard is “to cut” ie cutting off the property from a lender ownership

and giving it to a borrower.

Legally, Gard: means to give anything of value to another person, so he owns it and

acquires benefit from it, with the condition that the same or similar amount of that thing will

be paid back when demanded at a settled time.

Syed Mhammad Tantawi of AL Azahar stated that Gard is more particular than dayn , loan

can be given by a person to another for help , charity or as an advance for a specific time.

Adayn: is created by way of rent, sale, purchase or any other way, and this duyun (debts)

must be returned without any profit or any excess.

“Salaf” literally: means a loan with no profit.

In a wider sense, it includes loan for (longer, intermediate or short – term). " Salam

and Salaf" have been used interchangeably in Hadith literature (Understanding Islamic

Finance 2007) .

Gard: is a particular kind of salaf , where it can be demanded at any time or immediately . ie

(it is Gard or loan payable on demand).

So loan: is classified into salaf and Gard.

Salaf: is a loan for fixed time.

Gard: is a loan payable on demand.

20

The word “A‟riyah” : is used for borrowing goods i.e. to give any commodity to

another for use and the borrower is liable for this commodity and he is bound to return this

same commodity to the lender.

The English word “Loan”: is the counterpart, of the word “Gard”; and “debt” that of dayn.

The banking system today works under these categories, by giving loans and

advances. In Murabaha operations, goods are sold by Islamic financing instuitions (IFIS) to

create duyun / debts, which must be returned with a marginal profit.

So the definition of “Gard” by Sunnah is a kind of loan advanced for the benefit of

the borrower and the creditor can ask for it at any time. By such ownership the borrower can

buy, sell or donate it. Salaf is used for a loan of fixed tenure, so it‟s like dayn and both kind

are the liabilities created due to credit transactions for fixed tenure. Loan may be of any

thing valuable, can be paid by a similar or a substitute thing immediately or on demand, in

the case of Gard and at stipulated time in the case of salaf and dayn.

21

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

In this section the knowledge of the foundation, principles, fundamentals, philosophy

and the main feature of the Islamic financial institutions (IFIs) will be consolidated. After

the completion of this section, the translation students in this programme, acquire a wide

understanding of the Islamic economics mechanism with its multi-financing systems and

institutions. The overlapping of economy and Islamic religion generates specialty and a

unique characteristic for such economy with its permissibility and prohibition to certain

factors; its crystallization to the purity and transparency of the ethical, morals and equitable

values that revolves around every step within this economics for the sake, benefits and

welfare of the individual, society and mankind in general.

Shedding light on interpreting and translation techniques will accustom students to

practice translation and prepare them for the examinations. On the other hand, one has also

the opportunity in this section to practice sight translation, interpretation and written

translation.

2.1 History of Islamic Economics

From Wikipedia, the free encyclopedia this is a sub-article of Islamic economic

jurisprudence and Muslim world Wikipedia.org/wiki/history–of Islamic– economic.

Between the 8th

and 12th

centuries, there are many advanced and developed concepts

and techniques of production, investment finance, economic, development, taxation,

property use such as Hawala, an early informal value transfer system, Islamic trusts such as

Waqf, system of contracts relied on the merchants, a widely spread currency, cheques,

promissory notes, bills of exchange (Mufawada), advanced agricultural techniques, capture

and use of slaves.

22

Specific Islamic concepts related to money, property taxation, charity as Zakat (the

taxing of certain goods such as harvest of which its explicitly defined, such as aid to the

needy; Gharar "the interdiction of chance – that is the presence of any uncertainty; in a

contract (which excludes not only insurance but also the lending of money without the

participation of risks) and Riba (charging interest or high interest on money lent). These

concepts, like others in islamic law and jurisprudence came from "the prescriptions,

anecdotes, examples word of the prophet ".

On the other hand, there are other sources such as al-urf (the custom), al-'aql (reason)

or al-ijma (consensus of the jurists) were employed. Islamic law has developed areas of law

that correspond to secular laws of contracts and torts. "Islamic economics" emerged in the

1940, as 2004 "Islamic banks" have been established in over 70 countries and interest has

been prohibited in Pakistan, Iran and Sudan.

2.2 Early Islamic Economics

The early prophet economic policy in early Islam is a ban on charging fees and rents;

and a ban on permanent buildings in medina market, only tents were allowed, this meant to

help poor traders.

2.2.1 Social Responsibility in Commerce

This issue is stressed in Islam. Usury is not allowed when Islamic bank and Islamic

economics were developed. Interest is prohibited and investors have to participate in risks.

All financing was equity financing (Musharaka) so, there is a social harmony purpose,

Shariah forbade any finance dealing in forbidden goods such as wine, pork, gambling. So

only ethical investing and moral purchasing are encouraged.

2.2.2 Legal Institution (See also Shariah and Fiqh)

Hawala Agency: main article Hawala; it is the early informal value transfer system;

its origin came from the classical Islamic law and it is mentioned in Islamic jurisprudence

texts in the 8th

century. The development of agency has been influenced by Hawala later,

both in civil law and in common law. Example, that the aval in French law and the avallo in

Italian law; both words aval and avallo are derived from Hawala. Islamic law and the later

23

common law "had no difficulty in accepting agency as one of the institutions in the field of

contracts and of obligations in general"

2.2.3 Waqf Trust

Islamic Waqf: main article waqf was developed in the medieval Islamic world from

7th

to 9th

centuries, it is like the English trust law. The crusades introduce the trust law

during the 12th

centuries, those crusade may be influenced by the Waqf, and the Madrassah

foundations were establish, a great number of Bimaristan hospitals were established

throughout Islamic area. The Waqf trust institution funded the establishments of hospital and

all the staff and equipments of the hospital, the Waqf also funded medical schools.

2.2.4 Classical Muslim Commerce

Traders were known and supervised by officials of the city. Technology and industry

in Islamic civilization were highly developed; such distillation of water, perfume industry

and the industry of ceramics merchants relied on the system of contracts. They also sell on

commission. Wealthy investors give the merchants loans. There are joint investments by

money merchants, Muslim, jouish or Christian. There is also business partnership. In the

nine century, banks can draw checks from bank of Baghdad to be cashed in Morocco since

the 8th

century (the abbasid, khaliph Al Mansur, the idea of welfare and pension were

introduced in the form of Zakat (charity). The taxes included (Zakat and jizya) are collected

in the treasury of Islamic government for the needy.

2.3 Economy in the Caliphate (Edit)

In the medieval Arab agricultural revolution; a social change took place due to

allowance of attaining land by any individuals of any gender, ethnic or religious back

ground. They could buy, sell, mortgage and inherit land.

2.3.1 Trade (Edit)

Main article Islamic geography. In the Islamic golden age, there is afar reading

Muslim trade network. It extended from the Atlantic Ocean and Mediterranean in the west to

the Indian Ocean and South China Sea in the east. Arabic silver dirham coins were

circulated throughout the Afro-Eurasian land mass often in exchange for goods and slavers

24

so, due to these activities, the Islamic empire had (included the Rashidun, Umayad, Abbasid

and Fatimid (Caliphates).

2.4 Agriculture in the Medieval Islamic World (Edit)

Further information: Arab agricultural production during the period from 8th

century

to the 13th

century, many crops and plants were cultivated in Muslim trade routes. Many

changes took place such as farming techniques, changes in economy, population

distribution, agricultural production, urban growth, distribution of Labour force, and many

aspects of life in the Islamic world had been changed.According to Andrew Watson, in the

early Islamic empire there was a highest literacy rates in comparison with pre-modern

societies. Later due to the diffusion of paper from china which led to the flourishing of

books and written culture in Islamic society; and later the study and memorizing of the

Quran, flourishing commercial activities and the emergence of Maktaba and Madrasah

educational institutions, all these led to a better education and high literacy.

2.4.1 Islamic Capitalism (Edit) Main Article

Islamic number of concepts and techniques had been applied by early Islamic

commerce; such as bills of exchange, forms of partnerships (Mufawada) as limited

partnerships (Mudaraba), and also forms of capital (al-mal) capital accumulation (nama al-

mal), Cheques, promising notes, trust (see Waqf), transactional accounts, loans, ledgers and

assignments. There were independent organizational enterprises from the state in medieval

Islamic world. Agency institution was also introduced in the era. Europe had adopted these

concepts from the 13th

century onward.

A market economy was established in the Islamic world like merchant capitalism;

there were a considerable number of owner's monetary fund and precious metals. The Quran

prohibited (usury) but this did not prevent the development of capital, and the capitalist

(sahib-al-mal) from 9th

to 12th

the prominent figure at that period till the arrival of the ikta

(landowners). These two tends to hamper the industrial capitalism in the Islamic world. In

enterprise and business group controlled by entrepreneurs, they influenced the Islamic world

economy from the 11th

to the 13th

century. Each karimis merchant had wealth ranging from

at least (100,000 dinars' to 10 million dinars). They influenced politics through their

25

customers such as Emirs, Sultans, foreign merchants and common coinsurers. The Karimis

dominated the trade routes across the Mediterranean, the red sea and the Indian Ocean and

sub saharn Africa in the south where they braught gold from their miners. Karimis adopted

the use of agents, the financing of projects as a way of acquiring capital, and a banking

institution for loans and deposits.

2.4.2 Islamic Socialism Edit (main articles Islamic socialism and Bayt al-

mal)

The prophet Muhammad himself defended common ownership, he said according to

Ibn Abbas that "all Muslim are partners in three things, water, herbage and fire" in modern

days this can be interpreted as they are partners in water, food energy fuel, oil, and gas.

2.4.3 Industrial Development (Edit)

Muslim engineers in Islamic world had many innovations in the industrial field such

as tide mills, wind power and fossil fuels E.g. petroleum. There were industrial mills found

in every province by the 11th

century Muslim engineers used water turbine, dams as a source

of water power. Such advances changed many manual labours to be mechanized. Such

advances were later transferred to medieval Europe and lately laid the foundations for the

industrial revolution in 18th

century in Europe. The Muslim agricultural revolution led to the

generation of many industries, such as astronomical instruments, cerms, chemicals,

distillation technologies, clocks, glass, mechanical hydropower, etc

2.4.4 Further Information: Islamic (Edit) Economic Jurisprudence

To some degree, the early Muslim based their economics analyses on the Quran

(such as opposition to Riba, meaning usury or interest) and from Sunnah, the saying and

doings of Muhammad.

Al Ghazali (1058-1111) classified economics into the science related to religion in

commotion with metaphysic, ethics and psychology. Thinkers did not see that this

connection made Islamic economic thought to be static. Many scholars trace the history of

economics, though the Muslim world in the golden age ranging from the 8th

to the 13th

26

century and whose philosophy continued the work of the Greek and Hellenistic thinkers with

the rediscovery of Greek philosophy by the European through Arabic translation.

Aba Yusf (731-798). He is a student of the founder of the Hanafi Sunni School of

Islamic through, Abu Hanifah. Abu Yusif was chief jurists for Abbasid caliph Harun Al-

Rashid. He wrote for him the book of taxation. Abu Yusif favored the use of tax revenues

for socioeconomic infrastructure and had discussed many types of taxes as sale tax, death

taxes, and import tariffs. Another prominent thinker is Ibn Taymiyyah who made an

elaborated analysis of the market mechanism he discussed the welfare advantages and

disadvantages of market regulation and deregulation. Gazali suggests an early version of

price inelasticity of demand for certain goods .

2.5 Ibn Khaladun

Main articles: Ibn Khaladun and Muqaddimah see also sabiyyah.

Ibn Khaladun is the best known Islamic scholar who wrote about economics, he is

from Tunisia (1332 – 1406). In this book (kitab al-ibar) the history of the world, he

discussed (the social cohesion) and called it asabiyyah where he tells about the cause of

some civilization becoming great and others not. He also thought that many social forces

are cyclic, but also this pattern can be broken, his idea also about the benefits of the division

of labour; one of his concepts is that growth and development simulated both supply and

demand and the forces of supply and demand determine the prices of goods. He also

observed that the effect of macroeconomic force of population growth, human capital

development and technological developments on development. Ibn Khaldun noted that

population growth was a straight forward function of wealth; he also has his approach to

describe the sociological implications of tax choices, now it is part of economics. Ibn

Khaldun introduced also the labour theory of value which can be summarized as the value of

profit and acquired "capital" must include the value of labor by which it was obtained .

2.6 What is the Role of Religion on Economics?

Hence, one must differentiate between economics as a science and economics as a

system. An economic system should be seen as based on an ideology, while economics

27

science is seen as a science that deals with creation of wealth. The system includes these

three elements

a- Ownership of property, commodities and wealth.

b- Disposal of ownership.

c- Distribution of wealth among the people.

2.6.1 Difference Between Islamic Economic Principles and an Interest-

Based System

Islamic economic system can promote a balance between the social and the

economic aspects of human society, between the self and social, individual, family, society

and state interests.

1. Issues like income distribution and poverty alleviation which is the result of a balance

sustainable and equitable economics based on the socio-economic justice and fair play,

all these matters are among Islamic economic concern.

2. Such principles can achieve peace, happiness, welfare and prosperity for humanity.

3. At global level, sensible people call economists and policy makers to make an evolution

at inter and intra national levels which lead to a balanced sustainable and equitable

economics based on the socio-economic justice and fair play.

4. The late Yusuf Ali (translator of the holy Qur'an into English): "where as legitimate trade

and industry increase the prosperity and stability of men and nations, dependence over

usury would merely encourage a race of idler, cruel blood suckers and worthless fellows

who do not know their own good and therefore are akin to mad men" (translation of

verse 2:275).

2.6.2 Why Such Problems Occur In Free Market?

a. Due to unchecked creations of money.

b. A dependence on market forces with lack of ethical limits.

c. A stress on growth and profit per se with lack of any distribution aspect.

d. The state and regulators permit the pursuit of greed and unchecked profit.

28

2.6.3 Islamic Principles

So, Islamic principles of economics lay down checks for all these factors. They are

ethical and moral principles focus on clarity, just, fair treatment and care for the right of the

others.

2.6.4 Compare and Contrast Between the Islamic Economics and The Free

Market System

2.6.4. 1 Islamic Economic Comprises

a. Market mechanism.

b. Private property and enterprise.

c. Self-interest and competitions.

2.6.4.2 Parts of the Islamic Economics Market Mechanism are When

Goods are Produced

They either consumed or invested.

2.6.4.3 For Further Production, the Goods Can Be For

a. Sale.

b. Purchase (trading).

c. Leasing.

2.6.4.4 These Processes Can Be Carried Out By

a. Individuals.

b. Partnership firms.

c. Corporations.

2.6.4.5 Such Transactions are Undertaken Properly According to

a. Islamic jurisprudence contracts.

b. Subcontracts with detailed rules.

2.6.4.6 Socio-Economics and Distributive Justice are

29

a. Fundamental feature of Islamic economics.

b. The system encourages social welfare based on mutual help and character building. e.g.

2.6.4.7 The Islamic System of Zakat System

a. It is a religious obligation for every Muslim.

b. When one's wealth exceeds his need at a non progressive rate.

c. Generally, 2.5% of net wealth or 5 to 10 % in the case of agricultural produce above a

minimum limit.

d. The have-nots and the needy are the people entitled to zakat money.

e. This will be according to tenets of the holy Qur'an (verse 9:60).

2.7 Competitive Price Mechanism, Transparency and Disclosures are

Parts of The Market Function

i. Individuals have the right of ownership and freedom of enterprise and can gain and lose

under this frame work.

ii. Commercial interest, excessive uncertainty, gambling and all other games of chance are

prohibited by Islamic economics system, mainly the prohibition of Riba (interest).

iii. The main principles governing trade exchange must be carried out under certain rules :

2.7.1 Various Transactions Contracts Form A Fundamental Principles in

Islamic Economics

a. Transaction contracts are classified as commutative and non commutative (U good -e-

MU'awadha and U good ghair MU'awadha).

b. The validity of profit and return existed only in the case of (U good -e- MU'awadha)

such as the contract of sale and leasing.

c. No return can be taken in the case of gifts, guarantees and loans.

d. Shari'ah considers such activities as gratuitous and benevolent acts.

e. In the case of loans, it is a timely help for the needy, the debtor is charged only with the

exact amount of the loan or the debt.

f. The debtor has to repay the debt unless the creditor gives relaxation or the debtor

declared insolvency.

30

g. In The Hereafter the debt remains intact unless the creditor waives the amount of debt

even in the case of insolvency.

2.7.2 Regulating Trade and Business

Gordon Brown, the chancellor of the UKexchange said "it was mainly through

peaceful trade, the faith of Islam arrived in different countries". So, an interaction between

Muslim and non-Muslim communities, social cohesion among different societies can be

achieved through the trade that is based on ethical values, some standard of justice and fairly

play. Due to the above complications of the Islamic finance, economists, policy makers and

regulators must concentrate into two aspects:-

a. The role of the government must not concentrate only in conducting the different

businesses but mostly focusing in the proper and smooth functioning of market forces

with the utmost accountability and transparency so that vested interest cannot be

manipulated through malpractices as happen in the bitter experience of capitalism

leaving many human beings in at most poverty.

b. The second aspect is concerned with money, banking and finance, financial instruments,

institutions and the markets.

All financial transactions and instruments in Islamic finance should be represented by

genuine assets and business transactions are carried out according to the rules and norms

based on fair play, transparency and justice.

2.7.3 Other Fundamental Principle of Islamic Finance is That

i. All financial assets should be based on real assets (not necessarily gold and silver).

ii. On the other hand, there is the best standard for the value of the time factor in business

transaction, and that is through the pricing of goods and their usufructs.

iii. So, with such supply and demand of money, management of savings, investment and

financial assets should be conducted according to these principles which result in

sustainable and equitable growth and development leading to the happiness of mankind.

31

2.7.4 Funds Owners Must Share The Risk and The Return with Users of

the Funds

i. All parties to contract have to undertake liabilities for entitlement to profit under the

nature of the transactions.

ii. Parties will be charged differently during the various business activities according to

trading, leasing or Shirkah(partnership) principles.

iii. These parties have both risk and reward during the different stages of the transactions

process.

iv. The risk shall be there; it can be mitigated but not eliminated if the profit from such

transaction has to be legitimized.

[

2.8 Fundamentals of Islamic Economic Systems

Fundamental of the Islamic world view with its direct and indirect effect on business

of Islamic financial institutions and markets.

2.8.1 Shariah is A Code of Law or Divine Injunctions that Regulates

Human Being Conduct In Both their Individual and Collective Lives

a. All business and financial contracts in Islamic finance framework must conform with

shariah rules and its objectives.

2.8.2 Here are Some Specific Branches of These Injunctions

a. "Aqaida" or matters of belief and worship.

b. "Akhlaq", or matters for disciplining one's self.

c. "ahkam", or socio economic and legal system.

d. "Fraidh", or obligations

e. "Nawahi",or prohibition. So Islamic economics is controlled with these disciplines.

2.8.3 Sources of Shariah Tenets

The main source of the divine law is the revelation. The Holy Qur'an and Sunnah of

the Holy prophet (PbUh). So absolute belief of the revelation as the source of tenets and

information requires complete submission to Shari'ah rules.

32

2.8.4 Other Sources of Shari'ah Tenets

a. Ijma'a (consensus)

b. Ijtihad (the mental effort of juristic expertise to find solutions to emerging problems.

c. (Giyas)(analogy)

d. Ijma'a of the companions of the holy prophet is important source for the derivation of

laws.

e. Urf (prevalent practice) is one of the tools in the hand of Islamic jurists to deal with

shari'h position of the different contracts activities.

f. So, jurists, sharia'h scholar, shari'ah boards of Islamic banks and their institution are

needed to deal with solutions and issue edicts concerning various activities on the

basis of the above Shari'ah sources.

g. Shari'ah rules are divided into dos (order to undertake any act).

h. And don‟t (prohibition from some acts).

2.8.5 Shari'ah Objectives (Maqasid): Primary Objectives to Preserve and

Protect

1. Religion (the worship of Allah (S.W.T)).

2. Life (the sanscity of life protected by the law of Qias).

3. Progeny family unit (protection of family and married institution)

4. Property (sanctity of wealth).

5. Intellect.

6. Honour.

2.8.6 Secondary Objectives of Shari'ah

1. The establishment of justice and equity in society.

2. The promotion of social security, mutual help and solidarity, particularly to the poor and

the needy in meeting their basic needs.

3. The maintenance of peace and security.

4. The promotion of cooperative in matter of goodness and prohibition of evil deeds and

actions.

33

5. The promotion of supreme universal moral values and all actions necessary for the

preservation and authority of nature.

2.8.7 Studying Quran and Sunnah, Some Basic Socio-Economic Right of

Human Beings are Deduced

1. The right of safety.

2. The right to be informed.

3. The right to choose.

4. The right to be heard.

5. The right to satisfaction of basic needs.

6. The right to redress.

7. The right to education.

8. The right to healthy environment

2.8.8 For Achieving The Above Mentioned Goals, The Islamic Economics

Structure Should Be Clarified

a. Islamic economics approach is that, the creation and growth are means to satisfy human

needs as well as to support society.

b. Islamic encourages Muslims to seek the Hereafter by what they earn and not to forget

their worldly share during life.

c. The Shariah shows the directions towards a social order of justice, well being, security

and knowledge, and gives equal chance to all for earning a livelihood leading to

equitable distribution of income and wealth.

d. But when there is undue monopolistic and unjust pricing during the production and

distribution practices, ALHisba(the institution of the ombudsman) should be prevailed as

a social regulatory body to check these imbalances to achieve the Shariah goals of

justice and equitable distribution of wealth within different segment, sectors and

individuals among societies.

2.8.9 The Economic System Comprises

The main elements

1. Ownership of commodities and wealth.

34

2. Transfer of the ownership.

3. Distribution of wealth among people.

4. Among the thoughts used in economic analysis are the determinants of the level of

income and employment, money and banking, fiscal and money polices, national

income accounting, economic growth, demand and supply of money and stability.

5. Other details may comprise expenditure, saving-investment relationship, the saving-

income relationship. Consumption and investment functions. The potential level of

output, employment, and labour force and profit as aggregate variables.

6. All these determinants correspond to the main Islamic values and tenets.

7. While the absolute prohibition of interest(Riba), promotion of other various business

activities and trading, the existence of profit sharing, and the application of (Zakat)

and prevention of a wasteful consumption(Israf) with an overseeing role of the state,

form the key features of the macro-economics in the ideal Islamic economy.

2.8.10 Ownership and Property Right

i. Islamic economics is based on socio-economic justice.

ii. All resource in the world belongs to the creator; human beings act as vicegerent of God,

the holy Qur'an says "and give them from the mal of Allah he gave you". (04:33) and

spend from what He put you in charge of.( 57:7).

iii. Thus, Islam has put the limits and the means by which individual, groups, the public and

the state can possess propriety.

2.8.11 The Means to Possess Goods

1. Work.

2. Inheritance.

3. Purchasing.

4. Obtaining property for sustenance.

5. Properties granted as gifts, granting of possession of anything to the people by the state.

6. As mentioned before, there are limits set in terms of the quality of the wealth and the

means of acquiring it, but not in terms of the quantity of wealth, because the latter resists

human being strife to work diligently.

35

2.8.12 Legal Means of Ownership and Transfer Through Different Kind of

Contracts are Set By Islam to Facilitate the Acquisition of Property and

Wealth

i. There are general rules for these contracts submitted to the allowed limits.

ii. The rules permit man to use the resources by consuming them, benefiting from them or

exchanging them via various contracts such as sale, loans, lease or gift. Other rules are

concerned with investment of wealth and property.

2.8.13 Distribution

There is also the distribution through partnership, trade joint venture, loans, as well

as other transfer means such as grants, Zakat and the control of waste (Israf). So, Islamic

economy links between the market functions of production and growth, and the institution

functions of policy and control.

2.8.14 Factors of Production

i. Qur'anic injunctions set basis for the distribution of wealth and income.

ii. All factors of production have share in this distribution and prevention of any kind of

exploitation to take place in this process.

iii. The fact that, capital has to bear the loss if any, represents a distinctive feature in Islamic

system.

iv. Islam also keeps a part of the produce wealth as Zakat for the needy ones who cannot

contribute to the production due to social, economic or physical handicap.

2.8.15 Factors of Production in Islamic Economy

1. Capital: comprises means of production that are consumed or altered in during the

process of production. In Islamic economics the compensation for the capital is profit.

Profit is the residual revenue of a business but it comes with responsibility or liability.

2. Land: Here, the means of production used in the process are not changed in corpus or

original form. The compensation here is rental; e.g. land, machinery and plant, owner of

houses, vehicles, and machines. All these can be rent or leased.

36

3. Labour: is human exertion, physical or mental effort, organization and planning are also

included. The compensation here is wages:

a. An entrepreneur who rent land, machinery and labour and uses his own (money capital)

he has to pay wages and rentals for utilizing all these factors of production.

b. The entrepreneur gains profit from his capital only if there is residual after paying the

entire rental and wages and other expenses.

c. If the money capital is taken as a loan, the loan shall be repaid without any addition or

reduction of the amount whether there is profit or a loss.

d. In case there is a provider of the whole or part of the money capital and he wants a profit

as a result of such business, and the business suffers a loss, the provider has to accept the

shortfall of the whole amount.

e. So an entrepreneur or a capital provider is not entitled to a profit just by being a capital

owner.

f. All participants in a business must share similar liabilities and rights according to the

nature of the business and agreements terms.

g. On the other hand, management, responsibility and liability are considered also as

factors of production.

h. For example, a group of people get together as business partners or group of financers

who pursue business of their choice, or hired a manger to do the job.

i. On the other hand, a profit can be a reward for taking the responsibility to coordinate and

get the work done according to contracts terms.

j. In Islam there must be balance dealing between individual freedom and the welfare of

society.

k. The balance of market mechanism concerning demand and supply of goods is necessary

to achieve economic justice for the welfare of society and adequate allocation of

resources.

l. So for efficient functioning of the banking and finance sectors, there must be a good

overseeing role on the part of governments and regulators to make sure that market

forces and stakeholders not exploit each other and hence, fairness, justice and healthy

monetary system will be achieved.

37

m. Government and regulators must devise and adopt fiscal and monetary policies in their

respective ambits in such a way that the rate of return emerging from real sector business

in the economies becomes the benchmark and an effective signal for the allocation of

funds to various sectors.

n. The state also must achieve the stability in the value of money. This vitally important for

both the growth of the economy as well as for the achievement of social justice and

economic welfare. The holy Quran says:"and give full measure and weight with justice",

(6:152).

2.9 Global English and the Role of Translation

In the last two decades, language has been affected by the trend of globalization.

According to international status, one notices that English occupies an unchallenged and

most dominant language. The factors that determine power in language and society may be

shown as follows:

1- Access to resources such as economic, political, material etc.

2- The language role in international decision making.

3- The ability to cope with global technical developments including the information

and communication technology and taking the lead in mediating information

technology and other tools such e-mail service and world-wide-web.

On the other hand, there is the important role of English in international politics and

diplomacy in resolving international conflicts and it‟s effect in the world economy. Now, the

big question for the specialist, is whether the translation from or into English can play a role

in this rapid advances in communication technology. Globalization and the Role of

Translation Research conducted in English/Arabic translation leads to the fact that the need

for translation is on the rise. [Al-Salman (2002, P.99)]. There is also the transfer of

technology where the language of the “sending” countries differs from that of the „receiving‟

ones; and when 60% of the technical documentation of the world is written in English; so,

the need for translation from English to other languages and vice versa is necessary.

In ( U S ) “from 1980 – 1990”, the number of Spanish speakers grew by 50% and the

number of speakers of Chinese grew by 98% ( op cit, p.2). With such statistics of speakers

38

of other languages, this indicates that English will be probably not the only medium of

communication between the people of the world. So, this fact implies that translation is the

way out; Wall raff (2000) says ”we monolingual English speakers may never be able to

communicate fluently with every one everywhere – we may well need help from something

other than English”. In other words, translation is the solution – there is a frequent and on-

going of translations of English terms and expressions into the local languages of other

speakers language. Statistics reflect the leadership of the English language in the publishing

industry, so it has more chances to be translated; because writers in English reach large

audience and hence their topics can be translated to other languages. So, global English

boosts the process of translation. We find that the English-speaking world is keen to learn

about the latest world development such as advances in the scientific, technological,

economic and cultural fields in the industrial countries; such countries as China, Japan,

Germany and France do not speak the English language. Wiersema (2003) reports that

“Because of the current trend of globalization, the translator no longer

has the absolute need to always find a translation of a term in the target

language if this could make the target – language text loses credibility.

These translations contribute to a better and more correct understanding

of the source culture”.

The role of translation in the Arab world and specifically in Jordon is well

known. All B.A degree in the department of English include translation in their curriculum,

as well there is the MA degree in their universities. Language experts in Jordon believe that

the English language will not lose its power dramatically, because all pharmaceutical leaflets

of medicine and drugs have an Arabic translation of the product‟s scientific and commercial

name, indications, side-effects, precautions, dose, etc., …. On the other hands, all

appliances, electronics they have an Arabic version concerning the operation manuals. So,

the translation role is there whether the source language is English or any other language.

(Al-Salman).

2.10 Translation Activities

2.10.1 Activity

1. Interpreting and translation technique:

39

a. Before interpreting any assignment you should be sure that you are competent to do it,

so asking about the people participating in a conference or a meeting for example, it is

important to know about their region, dialect and accent finding out about the

assignment and researching any specialized vocabulary is essential move.

b. The awareness of the meaning of a word can change from one country to another

especially in Arabic country.

2. Interpreting and translation techniques:

As an interpreter you must be aware of the register importance. Register is the

appropriate language for given context.

2.10.2Register is Classified into

1. Tenor

2. Field

3. Mode

4. Tenor is the choice of the language according to the relationship created between people

participation in language exchange. The choice of language changes according to age,

social status, familiarity and may be gender of the speaker, also the mood and the

emotions can affect the choice of the language.

5. The second aspect of register is the FILD.

6. Field is the right choice of word for the situation. Such definition can refer to jargon or

terminology or in legal context, it can point out to every long sentence with many

clauses and elaborate mode of expressing ideas.

7. The third aspect of register is mode; Mode is concerned with the means of

communication the translator used. e.g. (speech, writing, non-verbal).

2.10.3 Written Translation

Before the act of translation, some stages have to be taken.

1- Scan the text.

2- One has to be aware of factors such as:

40

I. To whom the text is written.

II. Who wrote the text?

III. The purpose of the text.

3- Determine difficult, ambiguous terms.

4- Identify any difficulties concerning grammatical constructions e.g. (passive

constructions, very long or convoluted sentences).

5- Key words or phrases can be highlighted.

6- Each paragraph should be read to "decode" the meaning.

7- Translate, or "encode" the meaning in the target language.

8- For checking the transferred meaning, style and register correctly, the original and the

translated texts should be read side by side.

9- So by following these steps one hope to achieve a state where the translation stands

independently in every aspect.

You have been asked to make a written translation of this next text deduced from

sources of Shariah tenets "section. Use the above guide lines to help you prepare your

translation.

I. The text: Shariah can be divided into dos (orders to undertake any act) and don't

(prohibition from some acts), which can further be divided into the rituals (matters of

worship) that are considered as rights of ALLAH (SWT) and the matters for disciplining

human life, that constitute the rights of human beings. While the former acts (rituals or

matters of relating to belief and worship in the form of Fradh or obligation) have to be

accomplished strictly according to Shariah tenets.

II. We identified the following points for attention:

a. A paragraph with very two long sentences.

b. The syntax (order), of these two long sentences is loaded with a peculiar terminology

that needed definitions between brackets, there are also about four passive constructions

with only one active sentence within the Para.

c. Astonishing use for the use of the familiar verb (Do); as the verb here is converted into

noun with the change of the spelling of the (Dos) which is usually does:

41

1. There are the terminology with a deep Islamic religious connotation that cannot be

changed such as ALLAH (SWT) and the word (Fraidh).

2. Islamic economics texts are loaded with such terms of Islamic religious connotations.

Such terms present us with two problems: decoding what is meant exactly by these

terms and encoding- raises the question – is there an equivalent to such terms in the

L2? If not – would an explanation in the L2 do?. After paying attention to such points

translate your text and send it to your teacher or tutor for assessment.

2.10.4 Interpreting and Translation Techniques:

a. Creating your term bank.

b. Definition of term bank.

It is a glossary, dictionary that is created and developed by you. It reflects the meaning

and translation of specialist terms.

2.10.5 Information's Sources for your Dictionary:

1. For your quest to achieve such task, your experience, contacts with agent, language

tutors, specialist book-shops, libraries and the internet will be needed.

2. Examination: the time is very short to look up a word term in a dictionary; so your term

bank will be of great help to you; provided that your method of classification is

alphabetic or thematic. You must be absolutely sure of the meanings and the information

concerning your chosen words, terms and phrases. Find Arabic equivalent for the

following economic words and phrases.

2.11 The Main Prohibitions and Business Ethics in Islamic Economics

The prohibitions, being discussed here include Riba which is commonly known as

“interest” in conventional commercial terminology; also Maisir Gimar (gambling) and

Gharar; the latter means the excessive uncertainty about the subject matter and/or the price

in exchanges, as well as the chapter discusses the norms and ethics of business and finance

in Islamic framework. Shariah has identified some elements that should be avoided in

commerce or business transaction:

42

2.11.1 Prohibition of Riba

a. The word “Riba” means prohibited gain.

b. The Holy Qur‟an explains that all income and earnings, salaries and wages,

remuneration and profits, usury and interest, rent and hire, etc; can be categorized either

as:

I. Profit from trade and business along with liability which is permitted or

II. Return on cash or a converted form of cash without bearing liability in terms of the

result of deployed cash or capital is prohibited.

So Riba includes "any increase over or above the principal amount payable in a

contract obligation, not covered by a corresponding increase in labour, commodity, risk or

expertise." (Understanding Islamic finance).

2.11.2 All Real Sector Business Transactions Comprise

1- Sale, purchase which may be in cash or credit.

2- Loaning.

3- Leasing.

In Bai‟, or sale, the commodity is transferred to the buyer when the sale is executed. It

doesn‟t make any difference if the payment of the price is on the spot or deferred. The

payment for the ownership of this commodity can be on – the – spot or credit payment with

a profit margin for the seller. Bai‟ salam: it is a kind of forward sale, the goods will be

delivered in a future time, both parties must give and take ownership at a definite time and

on agreed terms, irrespective of the rises and falls of prices at the delivery time. If the

transaction is of (Hiba) or a gift, there will be no pay for the ownership of the assets.

2.11.3 A Loan In Islamic Finance

A loan is a temporary transfer of ownership of goods and assets without any

payment. The debtor is liable to pay back the same assets to the creditor.Riba in (loan or

debts) involves payment of interest during the transfer which is prohibited.

43

Ijarah is a different transaction, the lessor still has the ownership of the leased asset

against the payment of rent. But, on the other hand, he is liable for expenses relating to

ownership and loss of the asset, if any. In Islamic finance renting money is prohibited. In

Islamic finance, capital is a factor of production as in conventional economic system, but

with a different view that one cannot derive any profit from money unless one uses it in an

exchange for commodities or services in valid contracts of sale or lease taking into account

the liability of the risk of loss.

2.11.4 Prohibition of Gharar

Gharar represent the second major prohibition in Islamic economics.

Definition of Gharar:

Gharar comprises the elements of ambiguity, uncertainty about the end consequence

of a contract and nature and/or quality and specification of the subject matter of the contract,

the rights and obligations of the parties and the ambiguity of the possession and/or sending

of the item of exchange. That is to say the whole thing relate to the uncertainty of the basic

elements of any agreement, subject matter, consideration and liabilities.

Example: the sale of an escaped animal or a contract in which the price is indefinite.

Example of Gharar in the terms and essence of a contract:

a- Two sale in one

b- Down payment (Arbun) sale.

c- Suspended (Mu‟llaq) sale.

Example of Gharar in the object of contract:

a- Ignorance about the species.

b- Ignorance about attributes.

c- Ignorance about the quantity and also about the time of payment in deferred sale.

d- Contracting on a nonexistent object.

44

2.11.5 Prohibition of Maisir / Qumar (Games of Chance)

According to jurists, “Qumar” is an important kind of the “Maisir” Maisir means

wishing to obtain valuable thing easily and without paying any compensation (I‟wad) for it,

without working for it one obtain things only by game of chance and without undertaking

any liability against it. Qumar also means having money, benefit or usufruct at the cost of

others by merely game of chance. Injunction of Islam generally prohibits gambling,

wagering and swearing. Lotteries and prize bond schemes that have been launched

sometimes by financial institutions and banks are prohibited by Islam. Why?

Although the investors‟ money may remain safe, but the prizes are result of the

interests accumulated from the capital. There is also the element of chance that few people

may become millionaires at the cost of others, and without undertaking any liability or doing

any kind of work. So this process is repugnant to the tenets of Shari‟ah, it involves both Riba

and Maisir.

But generally since the purchaser knows what he is purchasing and the vendor is

aware of what he is selling and knows what its prices as well as the property for sale is

available for inspection, therefore there is no element of chance and hence the whole process

comply with, Shari‟ah tenets, in spite of the fact that there the element of publication to

attract customers. Islamic financing institutions and banks must forbid launching

conventional lotteries or prize bond schemes. Both are repugnant to the tenets of the

shariah because of their involvement to both riba and maisir.

- All Islamic financial transactions must comply with certain ethical standards such as

trustworthiness in business transactions and generosity in bargaining. In business

transactions, acts such as false swearing, lying and hiding facts in any bargaining must

be avoided.

- Important pillars of business ethics in Islamic shariah comprise fair dealing that

involves honesty, straight forwardness, free consent and negation of misstatement,

misrepresentation and exaggerated description of products.

45

2.11.6 Free Marketing and Fair Pricing

The Jeddah-based “Council of the Islamic Figh Academy” of the OIC in its fifth

session stated that:

1. Islamic banks should conform with shariah rules concerning trades and other business

(O66

you who believe! Consume not each other‟s property in vanities, unless there is

trade based on mutual acceptance).

2. Trader has freedom in the percentage of profit in his transactions.

3. Generally this left to the merchants, the business environment and the nature of the

merchant and of the goods. Merchants should be aware of the ethics recommended by

shariah such as moderation, contentment and leniency.

4. Shariah forbids all illicit acts features and benefits that are detrimental to the well –

being of society and individual.

5. Government must not interfere in fixing prices unless there are clear pitfalls noticed

in the market and the prices due to artificial factors. So, here the government

intervenes to get rid of these factors, their causes, the excessive price increases and

fraud.

2.12 Avoiding Interest

In Islamic banks, credit transactions, taking or giving any loan or enter into contracts

with intention of any increase over the principal of loans or debts is forbidden. While buying

/ selling goods in the form of cash payment and credit with the intention of earning profit is

allowed.

2.12.1 Avoidance of Interest

Lending on interest is alien to Islamic banks and financial institutions. In any case of

debts concerning trade or Ijarah transactions, there must not be any charge over or above the

principal of the debt. debtor are not allowed to charge any costs of funds or rent on money in

short, medium, or long term loans, over draft guarantees, financing against bill, receivable or

other instrument or sell their debt instruments.

46

2.12.2 Alternative Financing Principles

Avoiding interests as a basis in Islamic finance, a number of techniques and tools are

used by Islamic banks to do their business. Such tools as the principle of participation and

sharing found in musharaka, mudarabah, and the deferred trade principles applicable in

credit and forward sales (muaj'jal and salam); there is also a combination of techniques such

as shirkah and ijarah, murabaha, and salam and istisna'a. Here are the major forms of Islamic

finance that shed lights on the above discussion concerning the philosophy of Islamic

banking.

1. Mudarabah is a form of partnership, where one party provides the capital and the

other party provides entrepreneurial skills. Any loss is borne by the financier but in

case of profit, it will be shared by the partners according to a pre agreed ratio.

2. Musharakah is another arrangement that may take the form of a permanent equity

investment. It is a partnership in a certain project with a fixed duration or a

diminishing partnership (the banks share is repaid overtime by the company that

borrowed the funds).