Al-Barrak

24

BUSINESS OPPORUNITIES IN SAUDI POWER SECTOR US-Saudi BUSINESS OPPORTUNITIES FORUM CHICAGO April 28-29, 2010 Ali Albarrak President &C E O Saudi Electricity Company

-

Upload

mohamad5357 -

Category

Documents

-

view

216 -

download

0

Transcript of Al-Barrak

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 1/24

BUSINESS OPPORUNITIES

IN SAUDI POWER SECTOR

US-SaudiBUSINESS OPPORTUNITIES FORUM

CHICAGO April 28-29, 2010

Ali Albarrak

President &C E O

Saudi Electricity Company

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 2/24

Electricity Industry in Saudi Arabia Starts as 100%private ownership and operation.

Late 70`S consolidated into four major power co

(SCECO).

The government involved as major shareholder .

Mid 2000 All operating entities merged in one company

Saudi Electricity Company (SEC).

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 3/24

Incorporated from 10 operating utilities in 2000.

Largest electric entity in the region in terms of capacity ,market capital and shareholder’s equity.

Owns 85% generation and 100% transmission ,distribution and retail .

Total assets over 50 billion US$.

Annual revenues 6 Billion US$ .

Annual growth 6%.

74% directly owned by the Government.

SAUDI ELECTRICITY COMPANY

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 4/24

Scope of Operations

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 5/24

High growth in demand ( 7- 8%).

Operate in a very supportive environment .

High credit rating (AA~ ).

Invest in productive assets.

Reliable and secured fuel supply.

government support.

SEC credit strength

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 6/24

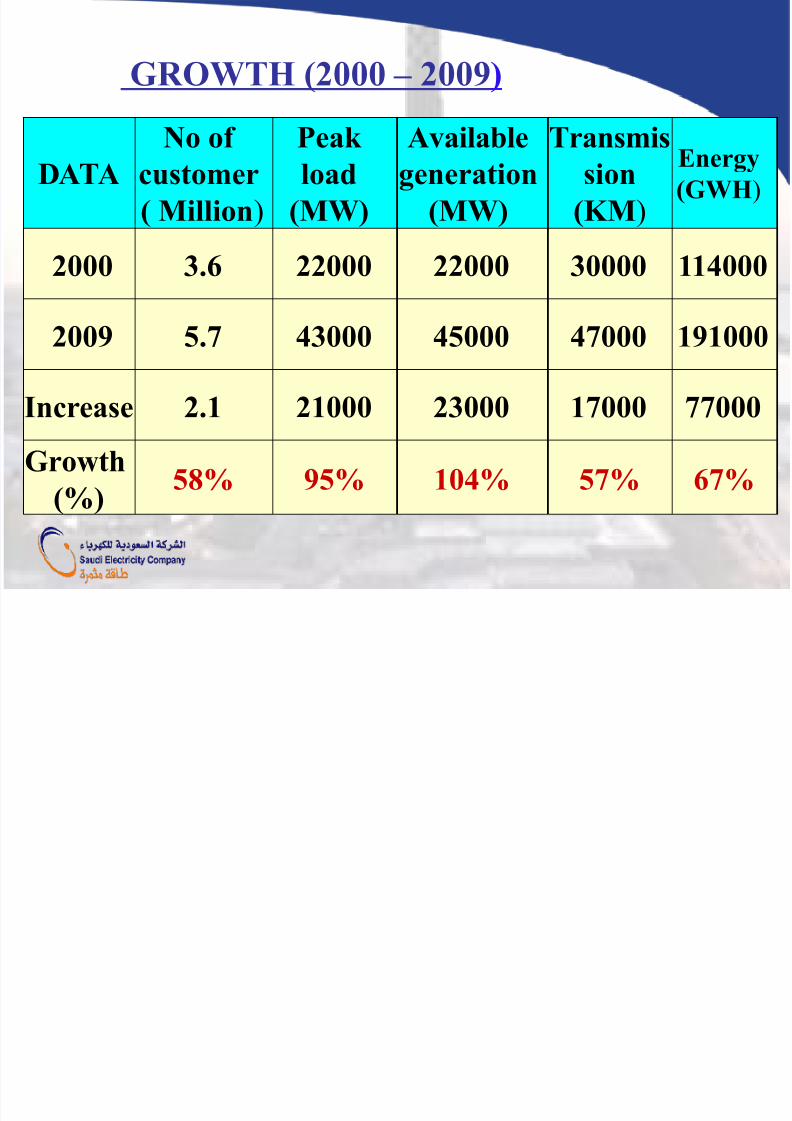

DATANo of

customer

( Million)

Peak load

(MW)

Availablegeneration

(MW)

Transmission

(KM)

Energy

(GWH)

2000 3.6 22000 22000 30000 114000

2009 5.7 43000 45000 47000 191000

Increase 2.1 21000 23000 17000 77000

Growth

(%)58% 95% 104% 57% 67%

)2009 – 2000GROWTH (

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 7/24

ACTIVITIES No of ProjectsCOST

( billion $)

GENERATION 174 17.3

TRANSMISSION 291 9.3

DISTRIBUTION 176 2.1

TOTALS 641 28.7

projects Under Execution

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 8/24

Load forecast (gwatts)68.4

65.3

62.6

59.957.4

54.952.5

50.1

46.944

41

38.1

35.2

32.5

30.5

28.227

24.423.7

10

16

22

28

34

40

46

52

58

64

70

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3

2 0 1 4

2 0 1 5

2 0 1 6

2 0 1 7

2 0 1 8

2 0 1 9

Series1

1.5

6.0%

2.6

7.8%

2.8

6.0%

2.7

4.5%

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 9/24

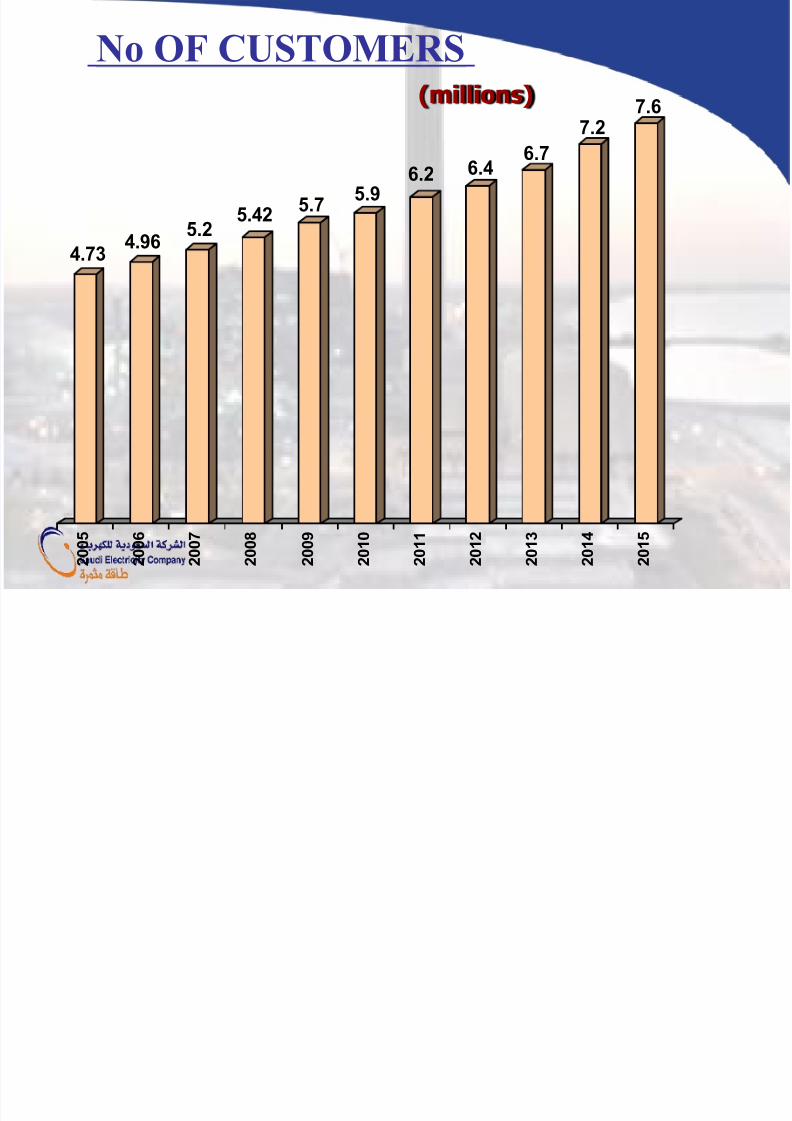

4.734.96

5.25.42

5.75.9

6.2 6.46.7

7.2

7.6

2 0

0 5

2 0

0 6

2 0

0 7

2 0

0 8

2 0

0 9

2 0

1 0

2 0

1 1

2 0

1 2

2 0

1 3

2 0

1 4

2 0

1 5

No OF CUSTOMERS(millions)

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 10/24

Generation Capacity

generation capacity installed should meet the expected7% increase in peak demand and a reserve margin.

90

74

59

41

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2006e 2007e 2008e 2009e 2010e 2011e 2012e 2013e 2014e 2015e 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e

SEC Installed & new capacity IWPP Installed capacity IPP Installed capacity SWCC Installed capacity Peak Load total capacity

Generation capacity (GW)

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 11/24

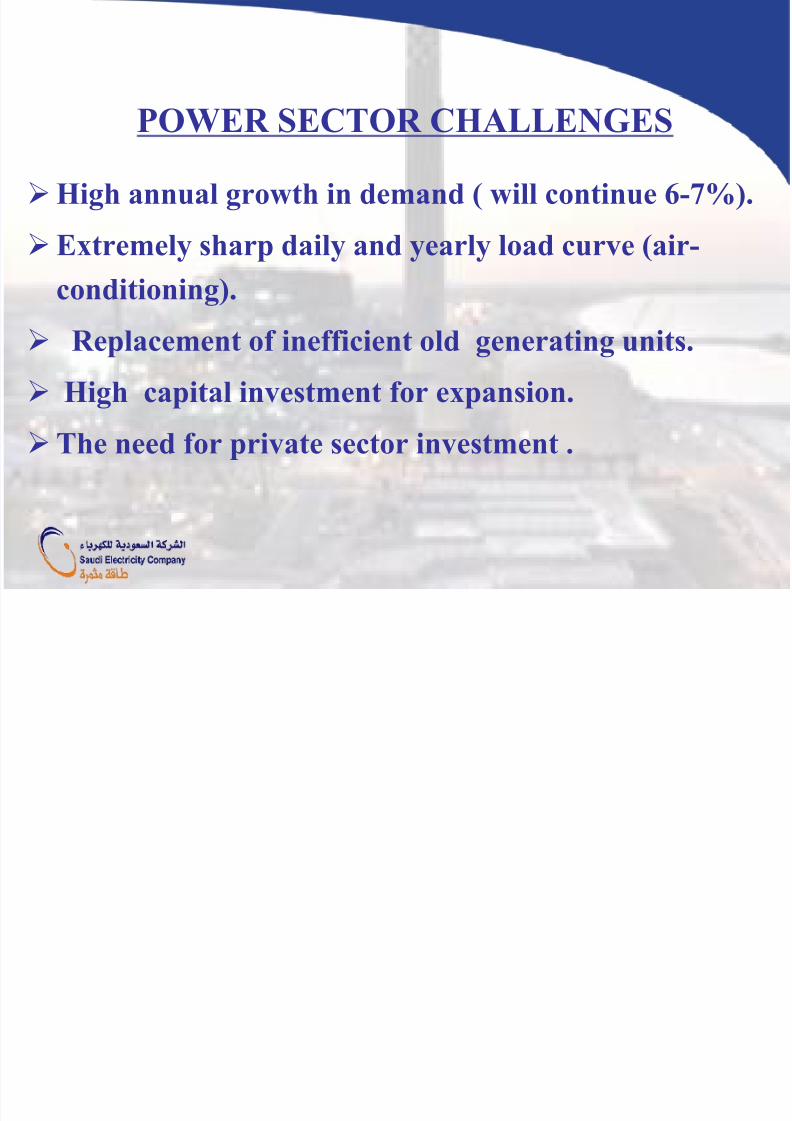

POWER SECTOR CHALLENGES

High annual growth in demand ( will continue 6-7%).

Extremely sharp daily and yearly load curve (air-

conditioning).

Replacement of inefficient old generating units.

High capital investment for expansion.

The need for private sector investment .

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 12/24

HOW TO MEET THE CHALLENGES ?

More investment in power generation,T&D .

Encourage the developers for more IPP.

Introduce the smart grid transmission system.

Promote energy conservation and load

management.

Invest in renewable energy.

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 13/24

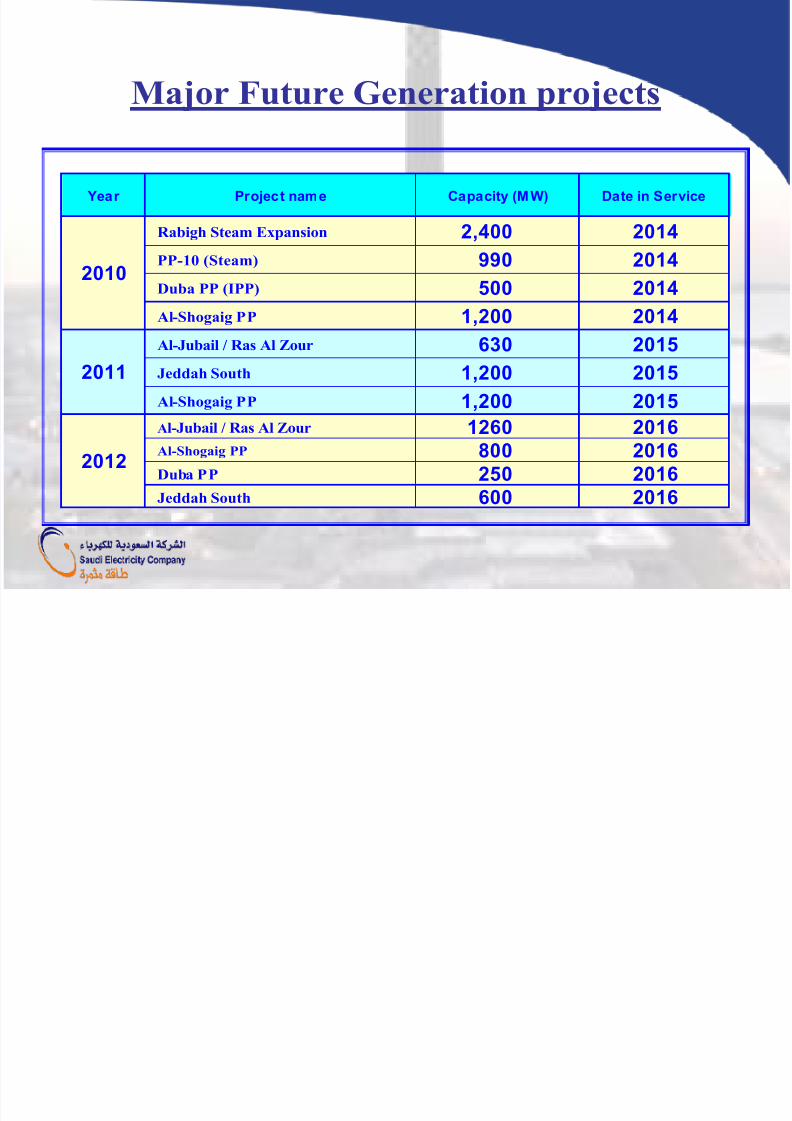

Year Project name Capacity (MW) Date in Service

Rabigh Steam Expansion 2,400 2014

PP-10 (Steam) 990 2014

Duba PP (IPP) 500 2014

Al-Shogaig PP 1,200 2014

Al-Jubail / Ras Al Zour 630 2015

Jeddah South 1,200 2015

Al-Shogaig PP 1,200 2015

Al-Jubail / Ras Al Zour 1260 2016Al-Shogaig PP 800 2016Duba PP 250 2016Jeddah South 600 2016

Major Future Generation projects

2010

2011

2012

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 14/24

Year Project Capacity (MW) Date in Service

Al-Jubail / Ras Al Zour 630 2017Al-Ogair / Salwa PP 630 2017Jeddah South 600 2016Al-Ogair / Salwa PP 1260 2017Jeddah South 600 2018Al-Ogair / Salwa PP 630 2018Al-Shogaig PP 400 2017Al-Ogair / Salwa PP 1,260 2019Al-Shogaig PP 400 2018

2016 Al-Jubail / Ras Al Zour 1,260 2020

total capacity: 25000 MW capital Cost : 50 Bln US$

Major Future Generation projects

2013

2014

2015

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 15/24

IPP PROGRAM IN SEC

SEC will Continue to encourage private investors

to invest in Future Generation projects .

30 – 40 % of Future generation will be IPP(BOO).

SEC partnership will be 10%-50% in the equity.

Long term power purchase agreements (20years)

With reasonable return on investment .

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 16/24

WHY IPP?

Providing Financial Option for Highly Capital

Intensive Generation Projects .

Helping To Re-Direct Available Funds To T&D

(Monopoly Activities)

Reallocation Expenditure From CAPEX To OPEX.

Avoiding Mismatch Between Medium TermFinancing and Long Life PP Projects.

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 17/24

SUCCESSFUL IPP ROJECTS

Two IPP Projects in process:

1. Rabigh Power Plant (closed financialyJuly last yea)• 1200 MW / HFO

• IPCOD APRIL 2012

• Investment US$ 2.4 billions

2. Riyadh Power Plant 11 (financial close next month)• 1800 MW / GAS

•

IPCOD APRIL 2013• INVESTMENT US 1.5 billions.

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 18/24

18

IPP FUTURE OPPORTUNITIES

NAME OF IPP

PROJECT

CAPACITY

(GW)

PRIVATE

SECTOR SHARE %

PROJECT

COMPLETION

QURAYYAH 2 80 2014

DHEBA 1.6 80 2015

SHUQAIQ 1.6 80 2015

ALOGAIR 2.4 80 2016

JEDDAH

SOUTH2.4 80 2017

RAS ALZOUR 2.4 80 2019

(INVESTMENTS OF $20B) TO BUILD 12 GW

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 19/24

2018SAUDI NATIONAL GRID by

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 20/24

Year Project Length KM Date in Serv ice

HAIL-ALJOUF-380KV 300 2014

ASIR_NAJRAN 380KV 400 2014GAISOUMAH -ALFADLI 380 KV 250 2014

BISHA_DAWASIR 380KV 500 2015

5th 380 KV LINE TO CENTRAK 400 2015

MADINAH-HAIL 360 2015

RIYADH-JEDDAH DC line 800 2016TABUK-TABARGAL 600 2016WEAST _SAUTH 2ND LINE 500 2016

Future 380KV transmission lines projects

2010

2011

2012

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 21/24

Year Project Circuit Length KM

Tabuk-Tabarjal 300Umluj-Wadjh 250South-West 2nd line 500Jouf-Tabarjal 150

2015 Al-grayat- Tabarjal 200

2016 Madinah-Tabuk DCLine 800

total capital cost 24 billion $.

Future 380KV transmission line

2013

2014

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 22/24

BUSINESS OPPORTUNITIES

Material and Equipment supply.

As an EPC contractor .

Local manufacturing .Participate in IPP projects .

Opportunity in consultation and

engineering.

Invest in future energy retail.

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 23/24

The growth of electrical energy demand in SaudiArabia will continue 6-7%.

Power projects needs 80-90 billion US$ as capitalinvestments for the next 10 years .

Private investors have the opportunity to take 30-40% of the generation projects as a BOO projects.

US companies have the opportunity to take part

both in EPC and IPP.There are oportunities in Consultation ,

Engineering and Services in power sector.

Conclusion

7/29/2019 Al-Barrak

http://slidepdf.com/reader/full/al-barrak 24/24

![BESPOKE MANUFACTURE & INDUSTRIAL PROTOTYPES · gold. Bespoke natural wood Wall lamp Design : Nacho Timón [2017] AL BARRAK LUXURY VILLA QATAR [2016] Design : Minimal Custom Studio.](https://static.fdocuments.in/doc/165x107/6034235af417a72a4e0a3d0a/bespoke-manufacture-industrial-gold-bespoke-natural-wood-wall-lamp-design.jpg)