Akuntansi Biaya - Mercu Buana UniversitySim+... · Modul ke:02 Fakultas Program ... Break-even and...

17

Modul ke: Fakultas Program Studi Akuntansi Biaya Cost Behavior Analysis Suryadharma Sim, SE, M. Ak 02 Ekonomi dan Bisnis S1 Manajemen

Transcript of Akuntansi Biaya - Mercu Buana UniversitySim+... · Modul ke:02 Fakultas Program ... Break-even and...

Modul ke:

Fakultas

Program Studi

Akuntansi Biaya Cost Behavior Analysis

Suryadharma Sim, SE, M. Ak

02 Ekonomi dan

Bisnis

S1 Manajemen

Cost Behavior Analysis

Classifying Costs

Success in planning and controlling cost depends on a thorough

understanding of the relationship between the incurrence of cost

and business activity. Careful study and analysis of the effect of

business activities on costs generally will result in the

classification of each type of expenditure as a fixed, variable, or

semi variable cost.

Cost Behavior Analysis

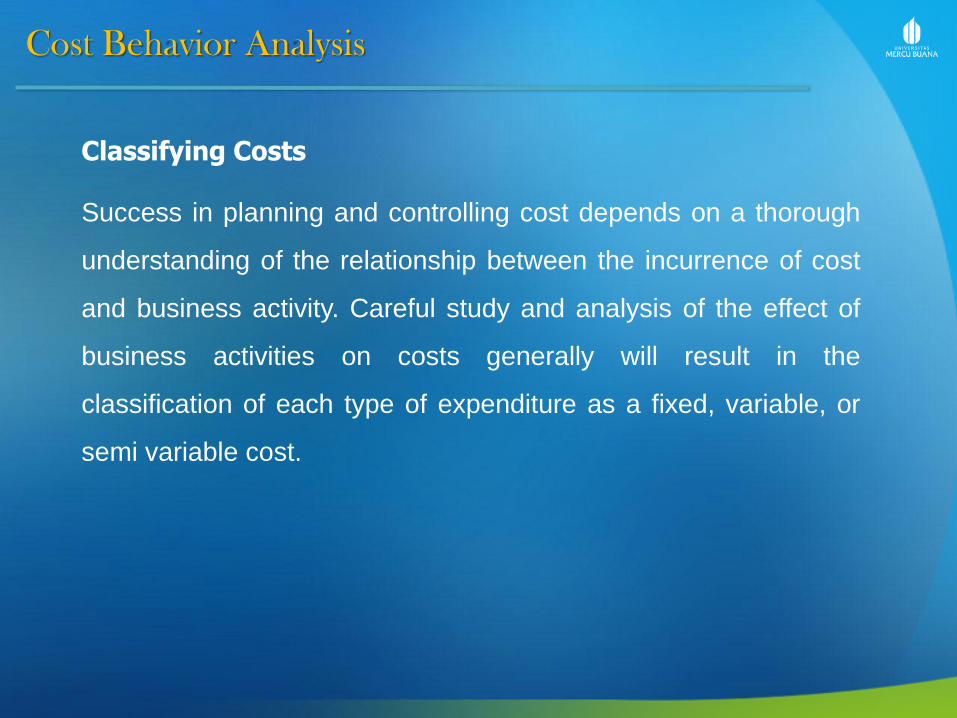

Fixed Cost

A fixed cost is defined as one that does not change in total as business activity

increases or decreases. Although some kinds of costs have the appearance of being

fixed, all costs are variable in the long run. If all business activity decreases to zero

and there is no prospect for an increase, a firm will liquidate and avoid all costs. If

activity is expected to increase beyond the capacity of current facilities, fixed costs

must be increased to handle the expected increase in volume. For example, factory

overhead includes items such as supervision, depreciation, rent, property insurance,

and property taxes-all generally considered fixed costs. If management expects

demand for the company’s products to increase beyond present capacity, it may

acquire additional plant, equipment, indirect labor, and possibly supervisors to

produce the level of output necessary to meet demand. Such additions increase the

level of expenditure for each of these items of factory overhead.

Cost Behavior Analysis

Total Fixed Cost $30,000 $30,000 $30,000

÷ Units Produced 5,000 10,000 15,000

Fixed Cost per Unit $6.00 $3.00 $2.00

Fixed costs are those which do not change with the level of activity

within the relevant range. These costs will incur even if no units are

produced. For example rent expense, straight-line depreciation

expense, etc.

Fixed cost per unit decreases with increase in production. Following

example explains this fact:

Cost Behavior Analysis

Cost Behavior Analysis

Variable Cost

A variable cost is defined as one that increases in total proportionately with an

increase in activity and decreases proportionately with a decrease in activity.

Variable costs include the cost of direct materials, direct labor, some supplies,

some indirect labor, small tools, rework, and normal spoilage. Variable costs

usually can be directly identified with the activity that causes the cost.

In practice, the relationship between a business activity and the related

variable cost usually is treated as if it were linear; that is, total variable cost is

assumed to increase by a constant amount for each unit increase in activity.

Cost Behavior Analysis

Total Variable Cost $10,000 $20,000 $30,000

÷ Units Produced 5,000 10,000 15,000

Variable Cost per Unit $2.00 $2.00 $2.00

Variable costs change in direct proportion to the level of

production. This means that total variable cost increase when

more units are produced and decreases when less units are

produced. Although variable in total, these costs are constant

per unit. For example explains this fact:

Cost Behavior Analysis

Cost Behavior Analysis

Semivariable Cost

A semivariable cost is defined as one that displays both fixed and variable

characteristics. Examples include the cost of electricity, water, gas, fuel oil,

coal, some supplies, maintenance, some indirect labor, employee group-term

life insurance, pension cost, payroll taxes, and travel and entertainment.

Mixed costs or semi-variable costs have properties of both fixed and variable

costs due to presence of both variable and fixed components in them. An

example of mixed cost is telephone expense because it usually consists of a

fixed component such as line rent and fixed subscription charges as well as

variable cost charged per minute cost. Another example of mixed cost is

delivery cost which has a fixed component of depreciation cost of trucks and a

variable component of fuel expense.

Cost Behavior Analysis

Separating Fixed and Variable Costs

To plan, analyze, control, measure, or evaluate costs at different levels of activity, fixed and

variable costs must be separated. Those costs that are entirely fixed or entirely variable

within the range of activity anticipated must be identified, and the fixed and variable

components of semivariable costs must be estimated. As discussed in later chapter, the

separation of fixed and variable costs is necessary for the following purposes:

1. Predetermined factory overhead rate computation and variance analysis.

2. Flexible budget preparation and variance analysis.

3. Direct costing and contribution margin analysis.

4. Break-even and cost-volume-profit analysis.

5. Differential and comparative cost analysis.

6. Short-run profit maximization and cost minimization analysis.

7. Capital budgeting analysis.

8. Marketing profitability analysis by territories, products, and customers.

Cost Behavior Analysis

In practice, managerial judgment often is used to classify costs as fixed or variable.

In such cases, classification is based on the personal experience of management.

Although such an approach is expedient, it often results in unreliable estimates of

cost. The behavior of a particular type of cost is not always readily apparent from

casual observation. Furthermore, managers often attempt to simplify the process

by classifying each cost as either entirely fixed or entirely variable, thereby ignoring

the fact that some costs are semivariable. Generally, more reliable classifications

and cost estimates are obtained by using one of the following computational

methods, all of which are illustrated in this section: (1) the high and low points

method, (2) the scattergraph method, or (3) the method of least squares. These

methods are used not only to estimates the fixed and variable components of

semivariable costs, but also to determine whether a cost is entirely fixed or entirely

variable within the relevant the relevant range of activity.

Cost Behavior Analysis

y = a + bx

High and Low Points Method In the high and low points method, the fixed and variable elements of a

cost are computed from two data points. The data points (periods)

selected from the historical data are the periods of highest and lowest

activity.

Although easy to understand, high low method is relatively unreliable.

This is because it only takes two extreme activity levels (i.e. labor hours,

machine hours, etc.) from a set of actual data of various activity levels

and their corresponding total cost figures. These figures are then used to

calculate the approximate variable cost per unit (b) and total fixed cost

(a) to obtain a cost volume formula:

Cost Behavior Analysis

Variable Cost per Unit = y2 − y1

x2 − x1

High-Low Method Formulas

Variable Cost per Unit

Variable cost per unit (b) is calculated using the following formula:

Where,

y2 is the total cost at highest level of activity;

y1 is the total cost at lowest level of activity;

x2 are the number of units/labor hours etc. at highest level of activity; and

x1 are the number of units/labor hours etc. at lowest level of activity

The variable cost per unit is equal to the slope of the cost volume line (i.e. change in total

cost ÷ change in number of units produced).

Total Fixed Cost = y2 − bx2 = y1 − bx1

Total Fixed Cost

Total fixed cost (a) is calculated by subtracting total variable cost from total cost, thus:

Cost Behavior Analysis

Scatter Graph Method

Scatter graph method is a graphical technique of separating fixed and

variable components of mixed cost by plotting activity level along x-axis and

corresponding total cost (mixed cost) along y-axis. A regression line is then

drawn on the graph by visual inspection. The line thus drawn is used to

estimate the total fixed cost and variable cost per unit. The point where the

line intercepts y-axis is the estimated fixed cost and the slope of the line is the

average variable cost per unit. Since the visual inspection does not involve

any mathematical testing therefore this method should be applied with great

care.

Cost Behavior Analysis

Method of Least-Squares

A mixed cost can be split into variable and mixed components by a statistical

technique called simple linear regression analysis. This technique mathematically

calculates the y-intercept and the slope of a straight line that ideally fits through a set

of points on a graph. In least-squares method, the ideal fitting of the regression line is

achieved by minimizing the sum of squares of the distances between the line and all

the points on the graph.

Formulas

In cost behavior analysis, the cost volume formula "y = a + bx", is equivalent to

regression line. Its y-intercept (a) and slope (b) represent the total fixed cost and

variable cost per unit respectively, can be calculated by solved following simultaneous

linear equations of least-squares regression analysis:

Cost Behavior Analysis

By solving the above equations for total fixed cost (a) and

variable cost per unit (b), we obtain:

Terima Kasih Suryadharma Sim, SE, M. Ak