Aker ASA Capital Markets Day 2013 · Aker Solutions ... low WACC › High revenue visibility ›...

54

Aker ASA Capital Markets Day 2013 14 November 2013

Transcript of Aker ASA Capital Markets Day 2013 · Aker Solutions ... low WACC › High revenue visibility ›...

Aker ASA Capital Markets Day 2013

14 November 2013

08:00 Registration

PART 1:

08:15 Aker 3Q13 results Øyvind Eriksen, CEO Trond Brandsrud, CFO

PART 2:

08:30 Status & strategic direction Øyvind Eriksen 09:00 Q&A

PART 3:

09:10 Investment perspectives on Aker’s energy portfolio:

Aker Solutions, Q&A Ed Ross, Investment Director Kvaerner, Q&A Michael Buffet, Investment Director Det norske, Q&A Trond Brandsrud

10:10 Break

PART 4:

10:30 Aker’s unlisted assets:

Aker BioMarine, Q&A Fredrik Nygaard, CFO, Aker BioMarine Fornebuporten, Q&A Torstein Storækre, Managing Director Converto, Q&A Frank O. Reite, Partner at Converto

PART 5:

11:40 Aker’s financial strategy Trond Brandsrud12:00 Q&A

Aker ASA Capital Markets Day 2013

Internet access:1. Log on to “ks-guest”2. Open your internet browser3. Register as new user and follow the instructions4. Write “ksa” in the field called “Secret”5. A username and password will be sent to your mobile

Proud ownership

Status and strategic directionØyvind Eriksen | President and CEO, Aker ASA

Development since CMD 2012

Capital Markets Day 2013 | Status & Strategic DirectionAker ASA

Objective Realisation

Active ownership

Dividend policy

Financial strength

Ocean Yield IPO, AKBM delisted

3.7% of NAV paid out, nominal increase

Upstream cash flow increased by over 80%

NAV growth 1. Aker Solutions execution challenges2. Kvaerner loss of contracts3. Det norske value unchanged4. AKBM value not fully reflected in NAV

2

Reveal underlying values

AKBM’s divestment of Epax

2

2013 YTD financial performance

Capital Markets Day 2013 | Status & Strategic Direction 3Aker ASA

22.9

21.8

(2.2)

(0.5)

(0.1)0.3

0.6

0.9

0.7 (0.9)

14

16

18

20

22

24

31.12.12 AKSO KVAER DETNOR AKBM OCY Funds Receiveddividend

Paid dividend 30.9.13

NOK billion

2008

Portfolio transformation over past 5 years

Capital Markets Day 2013 | Status & Strategic Direction 4Aker ASA

2013

3

Positioned in attractive industry segments

Capital Markets Day 2013 | Status & Strategic Direction 5Aker ASA

Oil and gas Maritime assetsSeafood and

Marine BioTech

Deepwater and subsea U.S. Jones Act Krill

A strong balance sheet

Capital Markets Day 2013 | Status & Strategic Direction 6Aker ASA

0

5

10

15

20

25

30

Gross assets Debt

Non-interest bearing liabilites ex. dividend

Interest bearing liabilities

Other assets

Receivables

Cash

Industrial holdings

BNOK 5 in cash

NOK 22 billionin unleveraged assets

BNOK

4

A liquid portfolio of investments

Capital Markets Day 2013 | Status & Strategic Direction 7Aker ASA

NOK 14 billion

A portfolio of both listed and unlisted assets

Capital Markets Day 2013 | Status & Strategic Direction 8Aker ASA

Unlisted

listed unlisted

5

0

100

200

300

400

500

600

700

800

900

2009 2010 2011 2012 2013

Aker Kvaerner Holding Ocean Yield Other

137191175

461

~850

Aker’s dividend income 2009 – 2013

Capital Markets Day 2013 | Status & Strategic Direction 9Aker ASA

Dividend income

2012 2013 2016 2020

Aker Solutions

Kvaerner

Det norske

Ocean Yield

Aker BioMarine

Havfisk

NOK million

Value contributors to Aker over past 5 years

Capital Markets Day 2013 | Status & Strategic Direction 10Aker ASA

18.5

22.2

5.0

3.21.0 (0.8) 0.3

0.6 (0.5)(1.8)

(3.3)

14

16

18

20

22

24

26

28

30

01.01.09 AKSO DETNOR OCY AKD Other Industrial Funds Admin andinterest

Write down andother

Paid dividend 31.10.13OtherInvestments(incl. Funds)

NOK billion

6

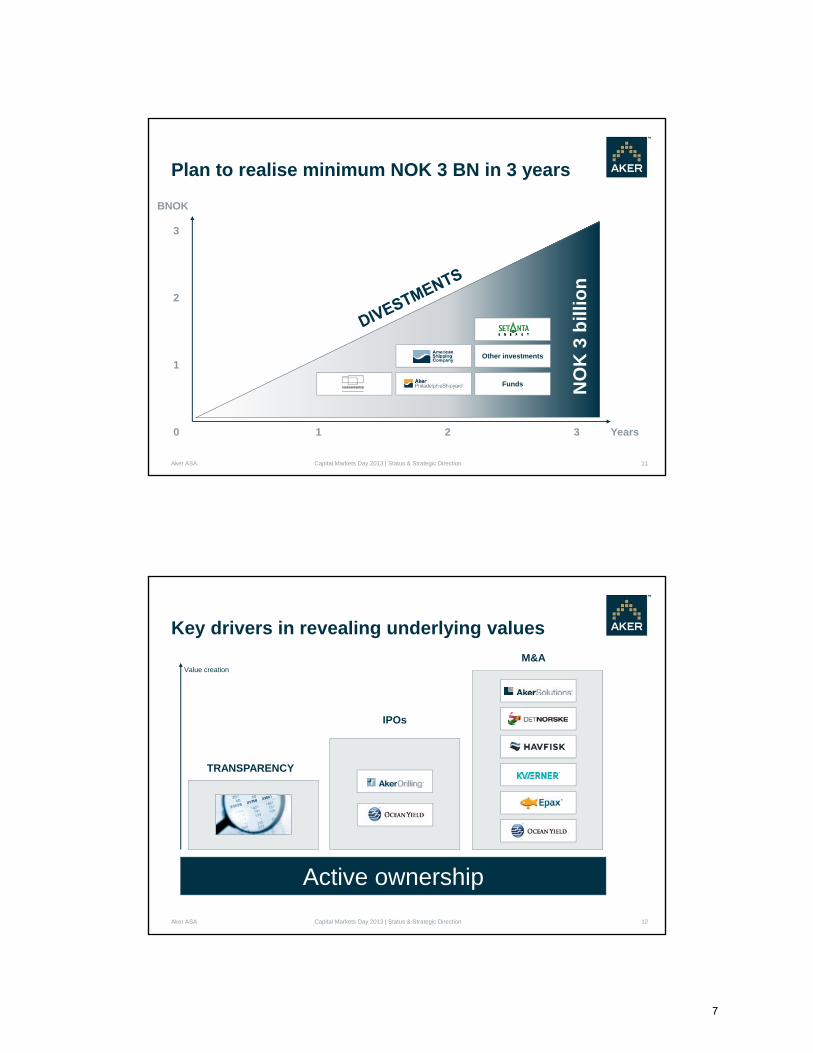

Plan to realise minimum NOK 3 BN in 3 years

Capital Markets Day 2013 | Status & Strategic Direction 11Aker ASA

Funds

Other investments

1 2 30 Years

BNOK

1

2

3

NO

K 3

bill

ion

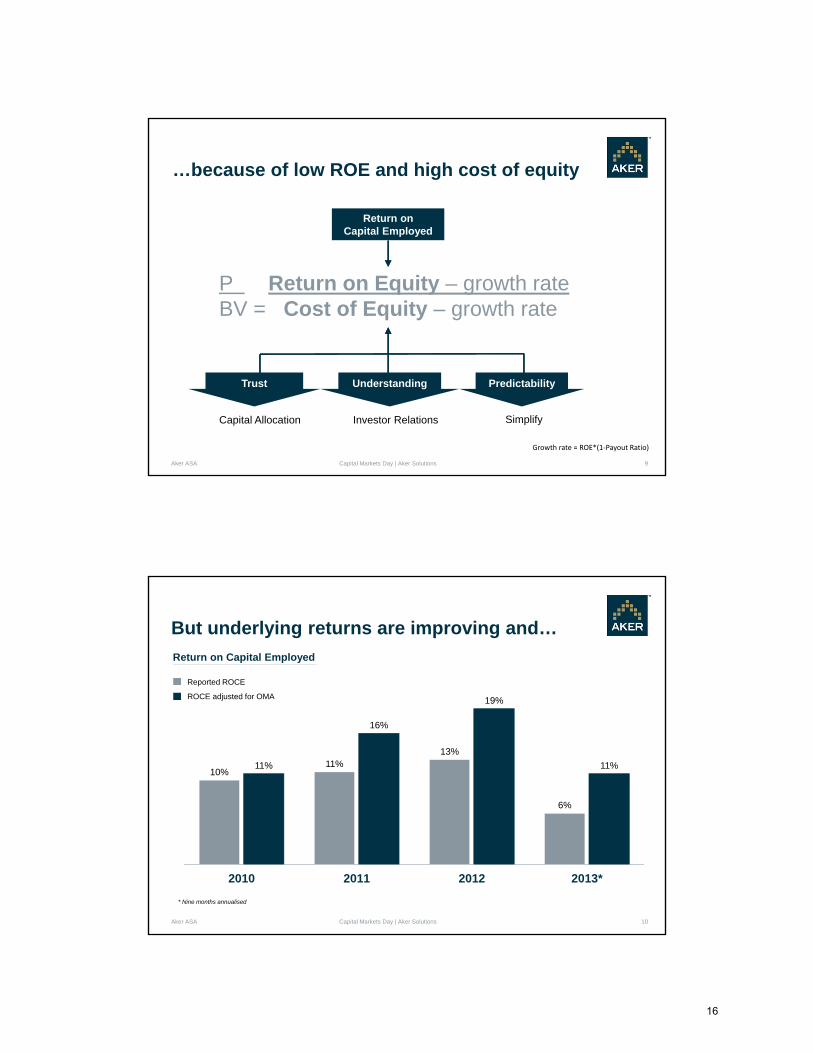

Key drivers in revealing underlying values

Capital Markets Day 2013 | Status & Strategic Direction 12Aker ASA

Active ownership

TRANSPARENCY

IPOs

M&AValue creation

7

How Aker operates

Board of Directors

Aker ASA Capital Markets Day 2013 | Status & Strategic Direction

OPERATING COMPANY

Aker’s Board representative(s)

DEFINE AND FOLLOW UP AKER’S VALUE CREATION PLAN

Investment DirectorFinance Committee Investment Team

Management

13

Industry Insights Analytical Capacity Feedback on Mgmt Proposals

Capital Discipline Cost control and operational improvements Focus on cost of equity IR strategy

Aker asa shareholder

Aker Solutions

Capital Markets Day 2013 | Status & Strategic DirectionAker ASA

Opportunities

Challenges

› Subsea factory - high systemintegration

› Strong presence on the NCS

› Execution challenges› Asset-intensive units

14

Ownership agenda› Subsea leadership

› High ROCE

› Promote operational excellence

› Streamline portfolio around growingoffshore regions and segments

Strong presence in growth regions

8

Opportunities

Challenges

Ownership agenda

Det norske

Capital Markets Day 2013 | Status & Strategic DirectionAker ASA

› Ownership stake in Johan Sverdrup› Building operatorship experience

15

› Financing requirements

› Young organisation whosecapabilities need to be enhanced

› Secure financing for Johan Sverdrup and participate without dilution

› Highgrade portfolio

› Grow through focused exploration

› Introduce annual dividend followingJohan Sverdrup production start

Opportunities

Challenges

Ownership agenda

Ocean Yield

Capital Markets Day 2013 | Status & Strategic DirectionAker ASA

› Cost-efficient operation, low WACC› High revenue visibility› Solid demand for ship leasing

› Portfolio insufficiently diversified› Risk of growing competition

16

› Maintain high dividend yield

› Grow and diversify portfolio through regular acquisitions

› Ensure optimal capital structure

9

Opportunities

Challenges

Ownership agenda

Aker BioMarine

Capital Markets Day 2013 | Status & Strategic DirectionAker ASA

› High margin business › Strong global growth in krill oil

17

› Legal disputes over patents› Risk of increased competition

› Expand krill oil production capacity

› Expand market for krill derivedproducts

› Generate upstream cash flow for Aker

› Gradually realise remainingpharmaceutical assets

Kvaerner

Capital Markets Day 2013 | Status & Strategic DirectionAker ASA 18

Ownership agenda

› Restructure and focus the business model

› Maintain operational excellence

› Focus on NCS and Concrete

› Optimise portfolio of quotas & trawlers

› Enhance profitability

› Generate upstream cash flow to Aker

Ownership agenda

Havfisk

10

Conclusion

Capital Markets Day 2013 | Status & Strategic DirectionAker ASA

Active and committed ownership

Prioritise resources to main portfolio value drivers

Focus on cost of equity and capital discipline

19

Actively pursue value-enhancing M&A opportunities

11

Proud ownership

Aker SolutionsEdward Ross | Investment Director, Aker ASA

Aker Solutions is the cornerstone of Aker ASA

2

431 700 741

1 053 1 082

2009 2010 2011 2012 2013

Aker Solutions’ dividend 2009 – 2013

% of Aker ASA gross asset value

23%

Aker ASA Capital Markets Day | Aker Solutions

(30.09.13)

NOK million

0

20

40

60

80

100

120

140

Aker Solutions has delivered a 30% average return p.a. , including dividend

NOK since April 2009

2010 2011 2012 2013

12

20

40

60

80

100

120

30. des. 2011 29. feb. 2012 30. apr. 2012 30. jun. 2012 31. aug. 2012 31. okt. 2012 31. des. 2012 28. feb. 2013 30. apr. 2013 30. jun. 2013 31. aug. 2013 31. okt. 2013

AKSO

FMC

NOV

CAM

Developments since Aker’s 2012 CMD

Record order intake for Subsea, but Engineering loses key contracts

Aker ASA Capital Markets Day | Aker Solutions 3

Challenges Disposal of MLS and start-up of Skandi Aker

Operational PortfolioBacklog

Placeholder Placeholder Placeholder

Share price development of AKSO and benchmarks (NOK, rebased to AKSO) – 1 Jan. 2012 to 8 Nov. 2013

20132012

Industrial conglomerate to subsea champion

Capital Markets Day | Aker Solutions 4Aker ASA

Future2002

Barriers to entry

Growth

Returns

Predictability

Lower

Higher

2010 Sale of P&C to JacobsReduce risk, exit Downstream EPC

2002 Merger of

2011 Sale of Marine Contractors to EzraReduce capital intensity

2011 Demerger of KvaernerReduce risk, exit EPC

Today 8 business areas

The future Subsea ChampionHigh growth and returns

2013 Sale of MLS to CargotecReduce Risk

13

7 055

Aker Solutions’positioning in industry trends

15 699

12 515

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013e 2014e 2015e 2016e 2017e 2018e

+22%

10 460

5 723

8 3196 295

5 2333 7673 272

1 294

19 184

9 588

6 1854 145

Subsea Market size by product group

Sources: Quest, Rystad, Pareto, Morgan Stanley, AKSO

MUSD

Engineering12- 15%

Drilling Technology8-10% ~ 12-17 UDW units year

MMO3-5%

Umbilicals and Process 10% +Industry

growth rates2012-2017

Subsea production umbilicals installed

Subsea manifoldsTree control packagesSubsea trees & control pods

Outlook for Aker Solutions’ business areas

Platforms/FPSO Subsea Drill Tech

ProductsSUB, PRS, UMB

Cost PlusEngineering

Lump sumIntegration &Maintenance

Target ROCE: 18%-22%Growth: 15%+

Target ROCE: 15%-20%Growth: 8%-10%

The FutureSubsea Factory

AKSO Exposure Growth and Return Outlook8 Barriers to entry

4

6

4

7

8

9

7

Aker ASA Capital Markets Day | Aker Solutions 6

7

7

14

How to ensure that AKSO captures value

Capital Markets Day | Aker Solutions 7Aker ASA

Focus investments

on businesses with high growth and high barriers to entry

Focus investments

on businesses with high growth and high barriers to entry

Cost control

especially SG&A and group purchasing

Cost control

especially SG&A and group purchasing

Upgrade financial control function

to improve information collectionand analysis

Upgrade financial control function

to improve information collectionand analysis

9.6x8.8x

8.3x7.9x 7.6x 7.5x 7.3x 7.0x

SUB UMB ENG MMO PRS DRT OMA WIS

8

Aker Solutions trades at a discount to peers…

SUB: FMC Technologies and Cameron. UMB: Oceaneering, Technip. ENG: Wood Group, WorleyParsons, Petrofac, Amec. DRT: National Oilwell Varco. MMO: Wood Group, Amec, Petrofac. WIS: Schlumberger, Baker Hughes, Weatherford, Halliburton. OMA: Helix, PRS: CB&I, KBR, Fluor, Jacobs Eng.Consensus analyst 2014 EBITDA by business area applied. Source: Bloomberg, research reports.

EV/EBITDA 2014 Peer group trading multiples by business area (consensus)

~30% discount to peer

group

Peer group multiples

suggest NOK ~130-135

~40-50% upside from

current share price

Aker ASA Capital Markets Day | Aker Solutions

15

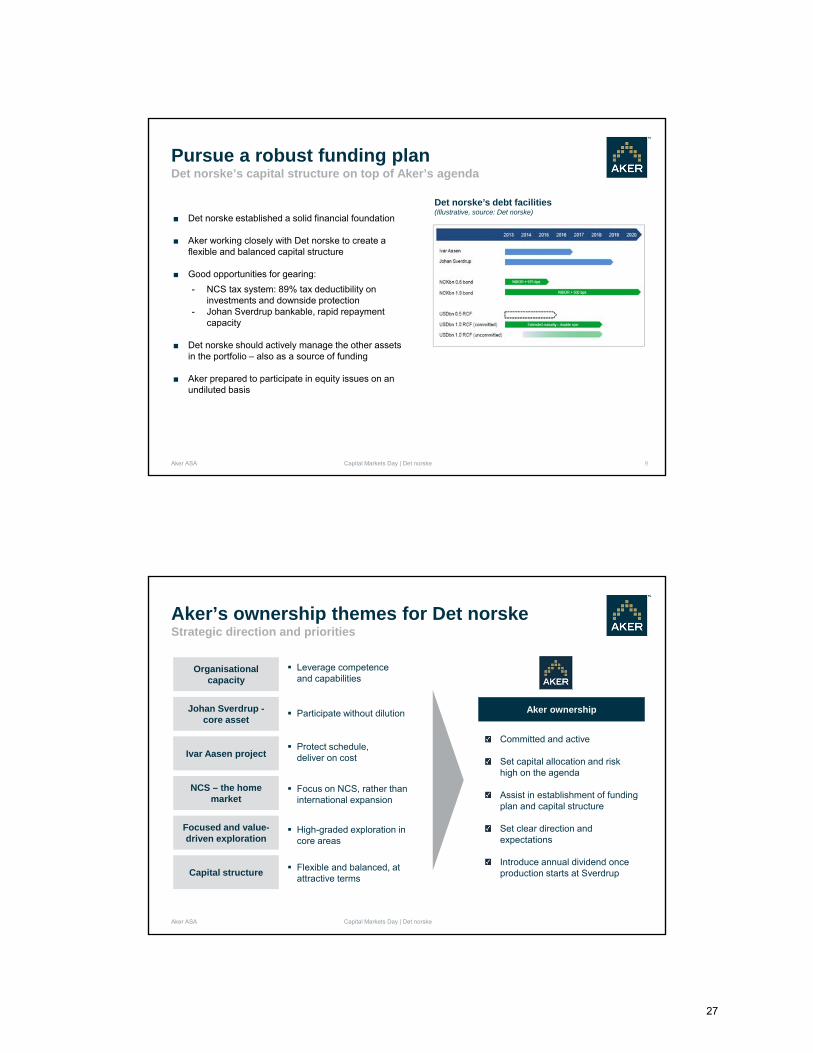

…because of low ROE and high cost of equity

9

P Return on Equity – growth rateBV = Cost of Equity – growth rate

Return onCapital Employed

Capital Allocation Investor Relations Simplify

PredictabilityTrust Understanding

Aker ASA Capital Markets Day | Aker Solutions

Growth rate = ROE*(1‐Payout Ratio)

But underlying returns are improving and…

10

10%11%

13%

6%

11%

16%

19%

11%

2010 2011 2012 2013*

* Nine months annualised

Return on Capital Employed

Aker ASA Capital Markets Day | Aker Solutions

Reported ROCE

ROCE adjusted for OMA

16

…higher capital discipline will increase returns

11

The cost of equity should be the referencepoint for all capital allocation decisions

Mgmt Incentive Structures based on ROCE and Total Return to Shareholders

Cost ofEquity

Capex

DivestInvest

ShareholderReturn

Aker ASA Capital Markets Day | Aker Solutions

Engineering, Subsea etc. and MMO

Lower earnings volatility will reduce cost of equity and help build trust in the market

12

2010 2011 2012 20132009

Brazil Trees

Drilling Technologies

Rig Building Shut down / spun offH6

Rigs

Offshore EPC spun out into Kvaerner , last legacy project Ecofisk Zulu

Onshore EPC spun out into Kvaerner

EcofiskZulu

Longview

Vessel Ownership: slated for disposal AOFS

Aker ASA Capital Markets Day | Aker Solutions

Mooring and Loading SystemsBarriers toentry

Growth

Returns

Lower

Higher

17

Conclusion

13

Aker Solutions is well positioned in attractive markets

But needs to focus on:

› Operational improvement

› Capital discipline

› Improving predictability

› Building trust and understanding in the

financial markets

Aker ASA Capital Markets Day | Aker Solutions

18

Proud ownership

KvaernerMichael Buffet | Investment Director, Aker ASA

4

8

12

16

20

jul. 11 okt. 11 jan. 12 apr. 12 jul. 12 okt. 12 jan. 13 apr. 13 jul. 13Kvaerner

OSEBX

Brent Spot

2013 was a difficult year for Kvaerner

Capital Markets Day | Kvaerner 2

CMD 2012

CMD 2013

Analysts' average target price

Business model challenged

Market turned bearish since last CMD› Share price NOK 16 to NOK 10› Target price NOK 19 to NOK 12› Target margins 6-7% to 4-5%

Significant risks perceived› Not winning new projects› Execution of new projects under

– New partnerships– Tighter contractual terms

› Legacy projects

Aker ASA

Listing

normalised

Share price NOK

19

Market opportunities

Attractive EPC markets...

› North Sea› Arctic

...served by core activities› Topsides / jackets (North Sea)› Concrete (Arctic)

Kvaerner has a stable base to leverage from

Capital Markets Day | Kvaerner 3Aker ASA

Financials

Higher predictability

Historically high backlog

NOK 2.66 in dividends, 8% annual return

Backlog BNOKEBITDA MNOK

0

5

10

15

20

25

30

35

3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q130

50

100

150

200

250

300

3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Backlog Consensus

Kvaerner creates value for clients

Capital Markets Day | Kvaerner 4

Unique track record

High value for money› Efficient delivery cycle with limited risk

World class assets & partners› Local yards that can offer high value services› Cost competitive partners in EU and China› Collaboration with AKSO Engineering

Arctic enabler› Year-round operations in icy waters (Concrete)

Aker ASA

Still a proven alternative to low cost yards

20

And offers upside potential for investors

Capital Markets Day | Kvaerner 5

Exposure to attractive market› High entry barriers› Competition not proven yet

High return on investment› High yield, predictable dividend: a priority

Arctic upside potential

Aker ASA

Significant upside potential

Restructuring the business to unlock value

Capital Markets Day | Kvaerner 6

Focus

Increaseflexibility

Internalimprovements

Partnerships

Divest non core assets

Stop no-margin projects

Cost: meet client needs› low-cost overseas

partnerships› productivity in Norway

Activity: offer whatcompetitors can't› EPC services› Alternatives to EPC

What to do...

Own productivity

Structural, not marginal

Close collaboration withclients

Aker ASA

Enablers...

21

How Aker supports value creation in Kvaerner

Capital Markets Day | Kvaerner 7Aker ASA

Market

Company

Stakeholders

Expectations

Operations

Decision-making

Partnerships

Clients

› Focus on value creation drivers

› Monitor execution closely, through relevant KPIs

› Control sizeable M&A and investment activities

› Ensure risks are assessed and mitigated

› Use Aker's access to clients to convey key messages

22

Proud ownership

Det norske oljeselskapTrond Brandsrud | CFO Aker ASA

Det norske – a key industrial holding for Aker

Capital Markets Day | Det norske 2Aker ASA

Det norske is a significant part of Aker’s NAV… …and will be an important upstream cash contributor once Johan Sverdrup is in production

Det norske production profile % of Aker ASA gross asset value

21%

2013 2020

Illustrative based on Wood Mackenzie

2013 2020

23

Merger with Det norske

Det norske has been a first-rate investment

Capital Markets Day | Det norske 3Aker ASA

Share price

TimeDec 2009

Dec 2011

Nov 2013

Sverdrup discovery

Today

Market capNOK 12 bn

Value generation to Aker ASA in the period of NOK 2.5 bn

Dec 2007

AKX IPO

Johan Sverdrup is Det norske’s main assetRobust economics and significant funding potential

3 588

3 581

2 419

2 299

1 659

1 572

1 145

927

923

Statfjord

Ekofisk

Johan Sverdrup

Oseberg

Gullfaks

Troll

Snorre

Heidrun

Valhall

Draugen

26

23

21

Subsea

Fixed platforms

Floaters

Johan Sverdrup

Capital Markets Day | Det norske 4Aker ASA

■ Large volumes at low cost, robust economics

■ Well appraised, low subsurface risk

■ Bankable, with significant funding potential

■ Source of dividend once onstream

Norway’s biggest oil fields Development costs on the NCS

Cost benchmarks Include 20 assets PDO approved between2011 and 2013 on the NCS, Johan Sverdrup illustrative

Johan Sverdrup resource estimate indicatecombined range from Statoil/Lundin 2011-2012

?

?

Million barrels of oil Capex / boe – arithmetic average

24

The Ivar Aasen projectAn opportunity to grow into a fully integrated E&P company on the NCS

5

■ License partners: - Det norske 35% - operator- Statoil 50%- Bayerngas 15%

■ Resources 148 mboe (115 mbbl oil). CapexNOK 27.4 bn (nominal)

■ Will be unitised with PL457 by July 2014

Discovery PDO submission

TargetFirst oil

End 20162008 20122010

Appraisal HanzPhase 2

2019

Ivar Aasen - key facts

Hanz

Ivar AasenEdvard Grieg

A coordinated development with Edvard Grieg

■ Building competence as an operator

■ Positions the company for attractive acreageawards in future licensing rounds

■ Project execution according to plan, but tooearly to conclude that main risks are reduced

Capital Markets Day | Det norskeAker ASA

Project milestones

Aker ASA’s view

Aker continues to view NCS as attractiveDet norske should focus on its home market

6

Exploration potential

19 billion barrels of oil equivalentsundiscovered

43% of resources on NCS produced

Recent success in Barents Sea with play openers Wisting/Gotha

Source: NPD

Opportunities in APA and ordinary rounds

Opening Barents Sea South East

Expected opening of Lofoten/ Vesterålen, although area closed for next four years

Stable framework and fiscal regime, although recent tax change was unexpected

Cash back on exploration costs and incentives such as APA rounds

5,3 4,96,0

1,90,6

Undiscovered resourcesBillion boe

Exploration potential Access to acreage Stable framework

Aker ASA Capital Markets Day | Det norske

25

Focused and value-driven explorationDet norske entering a new phase with focus on capital allocation

7Aker ASA

Det norske is built on exploration success… …and should continue to explore, based on a focused and value-driven strategy.

Capital Markets Day | Det norske

Discovered:2010On-stream: 2012

Discovered: 2009On-stream: 2013

Discovered: 2008On-stream: 2016

Discovered: 2011On-stream: 2018

Atla 2012

Jette 2013

Ivar Aasen 2016

Johan Sverdrup 2018

103 94 87 98 95

4844

2732 33

146133

113122 122

Bank 1 Bank 2 Bank 3 Bank 4 Averageof 15banks

Det norske trades at a discount to NAVAker see significant upside in Det norske’s share price

8Aker ASA

Target price

140 130 110 120 117

Equity analyst NAV – NOK / share

Source: DETNOR equity analyst reports

…in line with the rest of the small cap E&Ps

1,2

0,9

0,8

0,7 0,7 0,7

0,6

0,4

0,3 0,3

1

En

dev

ao

ur

Ihta

ca

Lu

nd

in

Far

oe

En

qu

est

Ste

rlin

g

Pre

mie

r

Det

no

rske

Ex

cit

e

No

rec

o

Price / NAV – Public North Sea exposed E&Ps

Average

J.Sverdrup OtherExploration

Share price

Capital Markets Day | Det norske

Det norske is trading at a discount to NAV…

Source: Credit Suisse

Net debt

26

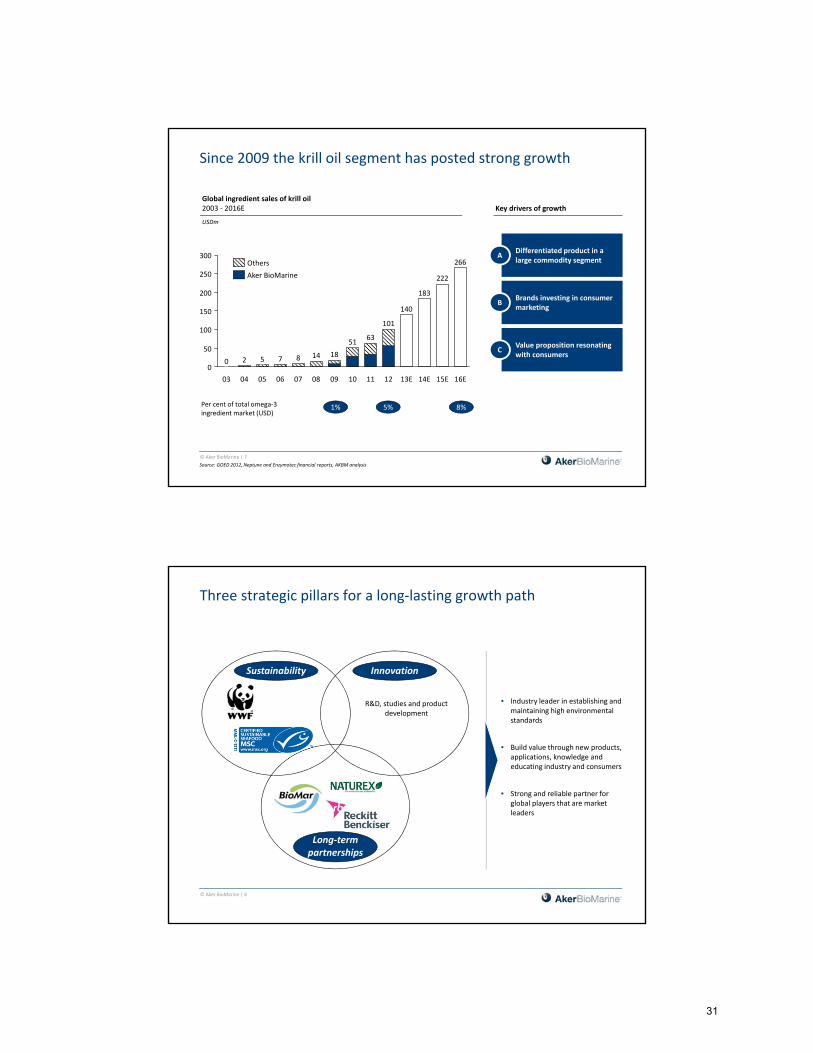

Pursue a robust funding plan Det norske’s capital structure on top of Aker’s agenda

9Aker ASA

■ Det norske established a solid financial foundation

■ Aker working closely with Det norske to create a flexible and balanced capital structure

■ Good opportunities for gearing:

- NCS tax system: 89% tax deductibility on investments and downside protection

- Johan Sverdrup bankable, rapid repayment capacity

■ Det norske should actively manage the other assets in the portfolio – also as a source of funding

■ Aker prepared to participate in equity issues on an undiluted basis

Capital Markets Day | Det norske

Det norske’s debt facilities(Illustrative, source: Det norske)

Aker’s ownership themes for Det norskeStrategic direction and priorities

10Aker ASA

Aker ownership

Committed and active

Set capital allocation and risk high on the agenda

Assist in establishment of fundingplan and capital structure

Set clear direction and expectations

Introduce annual dividend onceproduction starts at Sverdrup

Johan Sverdrup -core asset

Ivar Aasen project

NCS – the home market

Capital structure

Organisationalcapacity

Focused and value-driven exploration

Leverage competenceand capabilities

Participate without dilution

Protect schedule, deliver on cost

Focus on NCS, rather thaninternational expansion

High-graded exploration in core areas

Flexible and balanced, at attractive terms

Capital Markets Day | Det norske

27

Proud • Determined • Diverse • Sustainable

Aker BioMarineFredrik Nygaard | CFO, Aker BioMarine Proud • Determined • Diverse • Sustainable

© Aker BioMarine | 2

The Aker BioMarine Group comprises the core krill business and three pharmaceutical ventures

* Lindsay Goldberg is a NYC‐based PE company with >USD 10 billion under management

Opportunistic pharmaceutical ventures NutraCore krill business

AKBM

50% 50%100% Trygg PharmaGroup

• Supplements• Intermediates• API

Aker ASA

100%

• Separate team pursuing pharmaopportunities based on krill

• Indirect ownership in a specialisedpharmacompany that develops products with abuse deterrent features and benefits

• Submitted NDA for its lead drug candidate, which targets the market for patients with hypertriglyceridemia in the U.S.

Lindsay Goldberg

28

© Aker BioMarine | 3

Aker BioMarine develops and sells krill‐based products

Dietary supplement

High value feed ingredient

• Documented as a more efficient form of omega‐3

• Naturally free from pollution and heavy metals

• Product traceability

• Documented growth, health and quality performance benefits

• High quality feed ingredient for aquaculture and specialty pet diets

• Integrated marine biotechnology company focused on krill‐based products

• Headquartered in Oslo with operations in the Antarctica, Uruguay and Spain

• Two modern krill factory trawlers and a transport vessel

• MSC1) certified and sustainable harvesting operations

1) Marine Stewardship Council – leading, global non‐profit certification organization responsible for eco‐labeling of sustainable marine products

© Aker BioMarine | 4

Small company with integrated global product supply chain

Sales offices

Production facilities

Onboard processing and quality control

Eco‐Harvesting™ Storage and transport to shore

Superba™ Krill oil extraction and encapsulation

R&D, Sale and distribution

Logistics and research facilities

New onshore production facility in Houston on stream in 2014

New onshore production facility in Houston on stream in 2014

29

© Aker BioMarine | 5

From “Rebuilding” in 2008 to “Cash flow generation” in 2014…

• Fully invested to produce up to 2 000 MT Superba™1

• New krill product launches and applications

• Optimise assets and reduce costs

• Opportunistic approach towards krill pharmathrough Aker BioPharma

Profitablegrowth

21 Break‐evenEBITDA

3 4

2008/09

Cash flow generation and

dividends

2011‐ 2013

5

2010 2014/15 ‐

1) Onshore production capacity of up to 2,000 MT annually once Houston factory is completed2) Excluding krill pharma e.g share of Trygg Pharma Group and Aker BioPharma earnings from 2013

EBITDA performance2

2008 – 2014E, USD million

‐27

‐21

36

11

2013F 2014E2012

~25

2011201020092008

Strategic and financials ambitions2008 ‐ 2015

USDm

© Aker BioMarine | 6

…driven by two key performance drivers

0

50

177

232

363

2011201020092008 2013F

~515

2012

Average prices1)USD/KGMT

Volume

1) Blend of bulk oil and capsules

2013F2012201120102009

2013F

10,539

~13,000

20122011

10,092

2010

10,830

2009

7,066

2009 2010 2012 2013F2011

Average pricesUSD/MTMT

Volume

30

© Aker BioMarine | 7

Since 2009 the krill oil segment has posted strong growth

87520

266

222

183

140

0

50

100

150

200

250

300

18

08

14

0706050403 16E15E14E13E12

101

11

63

10

51

09

1% 5% 8%Per cent of total omega‐3 ingredient market (USD)

Key drivers of growth

• Differentiated product in a large commodity segment

A

• Brands investing in consumer marketing

B

• Value proposition resonating with consumers

C

Global ingredient sales of krill oil2003 ‐ 2016E

Source: GOED 2012, Neptune and Enzymotec financial reports, AKBM analysis

USDm

Aker BioMarine

Others

© Aker BioMarine | 8

Three strategic pillars for a long‐lasting growth path

Sustainability Innovation

Long‐termpartnerships

• Industry leader in establishing and maintaining high environmental standards

• Build value through new products, applications, knowledge and educating industry and consumers

• Strong and reliable partner for global players that are market leaders

R&D, studies and product development

31

© Aker BioMarine | 9

EBITDA

Superba gross profit

Qrill & raw material value

Fixed costs

Onshore costs

Offshore costs

Illustration of AKBM business drivers and profit model

• Optimise vessel operations, offshore logistics and warehouses

• “Be smart” regarding SG&A and R&D related costs, but global expansion comes at a price

• Qrill™ and raw material production dependent on krill fisheries

• Focus on vessel “up time” and sustainable harvesting

• Pursue global market growth opportunities

• Reduce COGS with new factory

• New product launches

ILLUSTRATIVE

1) Excluding krill pharma i.e. Aker BioPharma

Substantial upside if we deliver on our plan…Profit model and key priorities

USDm

45‐50

70‐75

~25

3 year target…

EBITDA Krill(USDM)

100 Normalised krill harvesting of 150,000 MT

Superba™ sales doubled without material price erosion

Average Qrill™ prices +25% from mix of new products

Further reduce Superba™ production costs

“Be smart” on costs

Does not include…

• Krill powder and krill‐based gummy products, still in early stages

© Aker BioMarine | 10

Key takeaways

Market leader within krill‐based products and well positioned in growing global market for omega‐3 products

Fully invested to produce and sell up to 2 000 MT Superba™ Krill Oil once Houston plant completed mid‐2014

Unique operational set‐up, Antarctic experience and high initial investments create competitive advantage

Strong balance sheet and focus on cash generation from 2014 and onwards

Potential for krill oil business to attract fish oil industry’s attention as segment grows

Key risks relate to intellectual property disputes, upholding operational excellence in harsh environments and

ability to differentiate in the market through R&D and innovation

Additional upside potential through Trygg Pharma Group and Aker BioPharma pharmaceutical ventures

Strong outlook for krill business, with some uncertainties given industry is still in its infancy

32

Fornebuporten HoldingTorstein Storækre | Managing Director, FPH

Overview

› Part of Aker’s Financial Investments portfolio

› Office developments:

› Fornebuporten (Oslo)› Aberdeen International Business Park

› Residential developments:

› Fornebuporten Bolig

› Fornebuporten is a developer, not a long-term holder of real estate

› Fornebuporten will opportunistically dispose assets prior to or upon building completion

› Meets Aker’s ROE requirements

Fornebuporten offices

Aker ASA Capital Markets Day | Fornebuporten 2

33

Aker ASA

Overview – Group structure

▪ Fornebuporten – 67,000 SQM

▪ Widerøeveien 5 – 10,000 SQM

▪ JV with Profier

▪ Planned for 46,600 SQM

▪ 15,750 SQM commenced

Fornebuporten Holding AS

AIBPFornebuporten Offices Fornebuporten Residential

▪ Planned for 100,000 SQM

Capital Markets Day | Fornebuporten 3

Fornebuporten

Aker ASA

Location

4

34

Aker ASA

Fornebuporten

Fornebuporten Commercial development

Aker ASA

› Currently ~ 67,000 SQM under development

› Construction on track with forecast completion:

› Building B in June 2015 › Building A in June 2016

› 2/3 of area let out at competitive market prices:

› Aker Solutions (12-year lease) › Kværner (12-year lease)› NorgesGruppen, incl. two shops (20-year lease)› Eurest (Compass Group)

› Advanced discussions with other tenants

› Project cost in line with budget (NOK 2.5 billion all-in)

› External bank financing secured

› WØV 5 building rent ~ NOK 14 million

Capital Markets Day | Fornebuporten 6

35

Market development Commercial

Rent

› Oslo market remains strong and rental prices are increasing

› Current market prices in the Lysaker / Fornebuporten area at NOK 2,200 -2,500 per SQM

Investment market

› Strong appetite for real estate leading to lower yield

› Fornebu yield in vicinity of 6%Source: Akershus Eiendom

Office rents 1986-2013

Aker ASA Capital Markets Day | Fornebuporten 7

Fornebuporten Commercial

Time

Regulation and planning

Marketing and sales

Construction

Aker Divestment[1]

(partly or fully)

Acquisition of land

2011 2015 2016

Building B

complete

Building A

complete

2012 2013 2014

Aker Solutions

Kværner

NorgesGruppen

Eurest

Operating

Fornebuporten’s value chain Non-Fornebuporten value chain Progress [1] Divestment with repayment of investment and profit

Aker ASA Capital Markets Day | Fornebuporten 8

36

Market development Residential

Source: Akershus Eiendom

Residential

Fornebuporten Residential

Aker ASA

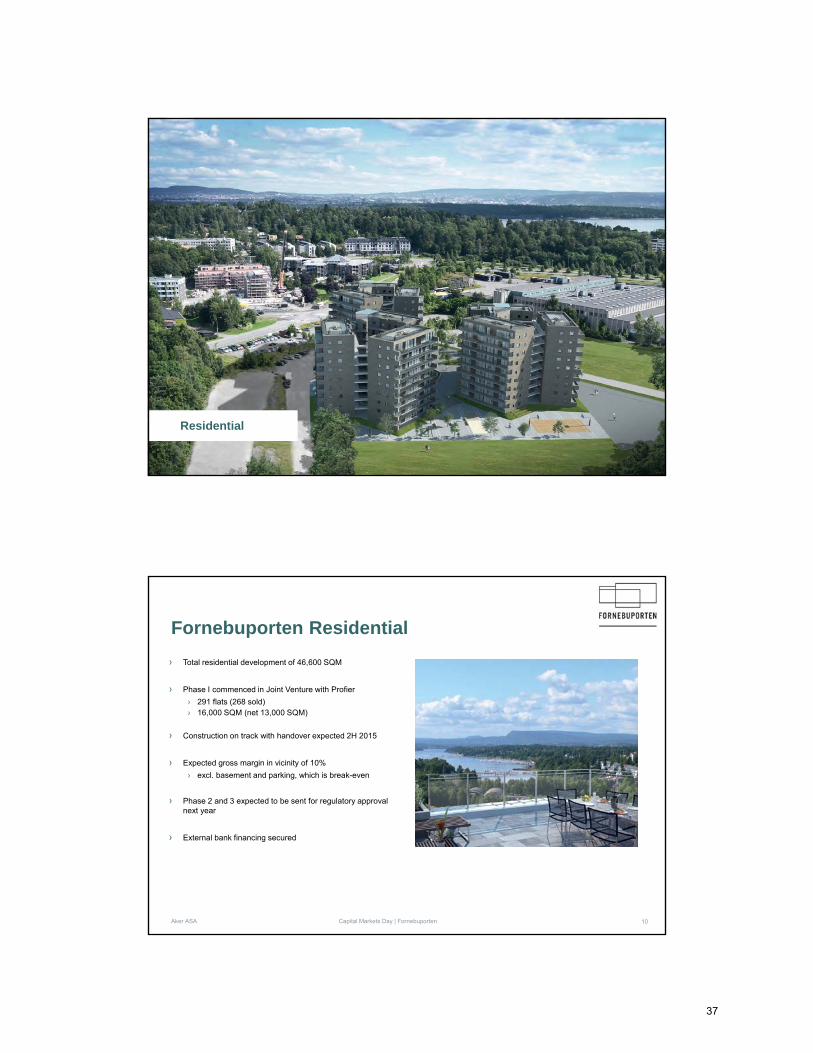

› Total residential development of 46,600 SQM

› Phase I commenced in Joint Venture with Profier

› 291 flats (268 sold)› 16,000 SQM (net 13,000 SQM)

› Construction on track with handover expected 2H 2015

› Expected gross margin in vicinity of 10%

› excl. basement and parking, which is break-even

› Phase 2 and 3 expected to be sent for regulatory approval next year

› External bank financing secured

Capital Markets Day | Fornebuporten 10

37

Market development Residential

› Residential market currently sluggish

› Prices modestly down

› Few new projects commenced

› Long term fundamentals remains strong› Urbanisation› Favourable demographics › Good economic outlook› Low interest rates

Larger Oslo area new build housing starts vs. population growth 1925-2011

New build housing starts

Demographic development

Source: Aftenposten

Aker ASA Capital Markets Day | Fornebuporten 11

Fornebuporten Residential

Time

Regulation and planning

Marketing and sales

Construction

Acquisition of land

2011 2015 2016

Handover

2012 2013 2014

268 of 291 flats sold

Fornebuporten’s value chain Progress

Aker ASA Capital Markets Day | Fornebuporten 12

38

Future drivers

Aker ASA

› Metroline from Oslo to Fornebu a political priority

› Government plans part private funding of the metroline through release of building concessions

› Size of undeveloped land at Fornebuporten similar to that of existing development

› 10,000 SQM already approved by regulatory authorities, subject to metroline in place

Footprint larger than current office development

MM

Nasjonalteatret FornebuportenVækerøSkøyenMajorstuen Lysaker

12min

Capital Markets Day | Fornebuporten 13

Future drivers

Aker ASA

Aberdeen International Business Park

39

Premier location next to airport

Aker ASA Capital Markets Day | Fornebuporten 15

Aberdeen International Business Park

Aker ASA

› Land acquired 1Q 2013 for ~GBP 17 million (incl. infrastructure)

› Three buildings (30,000 SQM) under construction

› The current building concession is 46,000 SQM › Planned development 100,000 SQM

› Advanced discussions with tenants for lease

› Development of CAT A[1] (not CAT B[2])› Forecast cost GBP 65M million for CAT A

[1] A category A fit out includes e.g. entrance hall, staircases, suspended ceilings and the extension of the Mechanical and electrical above the ceilings.

[2] A Category B fit out includes e.g. suspended ceiling upgrades, special area fit out (auditoria, kitchens, restaurants, gym, meeting rooms, canteen etc.), reception desk etc.

Capital Markets Day | Fornebuporten 16

40

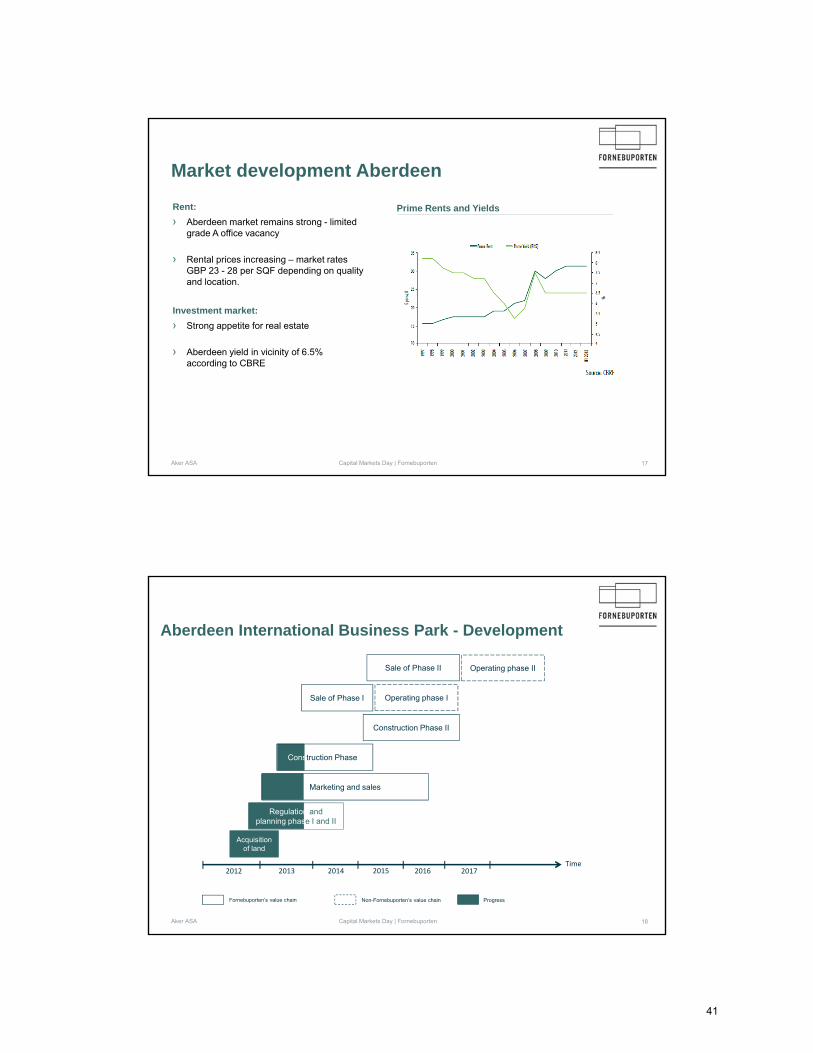

Market development Aberdeen

Source: Akershus Eiendom

Rent:

› Aberdeen market remains strong - limited grade A office vacancy

› Rental prices increasing – market rates GBP 23 - 28 per SQF depending on quality and location.

Investment market:

› Strong appetite for real estate

› Aberdeen yield in vicinity of 6.5% according to CBRE

Prime Rents and Yields

Aker ASA Capital Markets Day | Fornebuporten 17

Regulation and planning phase I and II

Aberdeen International Business Park - Development

Time

Marketing and sales

Construction Phase I

Acquisition of land

2012 2016 20172013 2014 2015

Construction Phase II

Sale of Phase I

Sale of Phase II

Fornebuporten’s value chain Non-Fornebuporten’s value chain Progress

Operating phase I

Operating phase II

Aker ASA Capital Markets Day | Fornebuporten 18

41

-1 200

-800

-400

-

400

Aker ASA

Aker’s receivable to Fornebuporten

September 2011 September 2012 2014

Dividend

Repayment of loan to Aker

September 2013

Capital Markets Day | Fornebuporten 19

Summary & timeline

Aker ASA

› Fornebuporten and Aberdeen projects on track and de-risked

› Favorable market development both in Oslo and Aberdeen

› Potential upside through additional building concession at Fornebuporten

› Reduction in Aker’s receivable expected in 2014

› Fornebuporten is a developer, not a long-term holder of real estate and will opportunistically dispose its assets either through a forward sale or upon building completion

Capital Markets Day | Fornebuporten 20

42

Proud ownership

Converto Capital FundFrank O. Reite | Managing Partner, Converto Capital

About Converto Capital Fund

Owned 99.8% by Aker

Closed-end investment fund

established in 2009

7-year investment horizon

Originally 11 portfolio companies within

seafood, oil service and U.S. Jones Act

(Bond)

Selected realisations (per 3Q13)

2

NOK 1.3bn realised (cost 0.8bn)

Key facts

Current portfolio (per 3Q13)

Value of investments (% of total fund value)

Total fund value ~ NOK 1.8bn

27%

29%

44%

Tight oil production forecasts and current fleet indicate significant upside potential in U.S. Jones Act market

U.S. Shale Crude Production Forecast

Tight oil production doubled in less than two years

Significant future increases predicted

Total recoverable reserves estimated to be as much as

120 billion bbls

U.S. imports of crude trending down

Existing pipeline and rail infrastructure not able to meet

transportation needs

Fleet utilisation currently at 100%

25% of fleet used to transport crude

Ageing of the fleet; newbuild capacity constrained

Substantial fuel savings on new product tankers

Jones Act Fleet

4

0

1 000

2 000

3 000

4 000

5 000

0

5 000

10 000

15 000

20 000

25 000

2000 2005 2012

2000 to 2012 36%

1,0

00

bb

ls/ d

ay

1,0

00

bb

ls

AKPS - Well positioned in promising Jones Act market

2009

2013

Empty order book beyond OSG vessels

Insignificant equity value

Closing down yard considered

Government support of USD 42 million secured

New orders of more than USD 1.4 billion and backlog

secured until mid-2018

Partnership with Crowley

New contract with Matson

5

Converto’s view Long term visibility and steady cash flow

through fully-funded newbuilding program

Upside through Crowley partnership

AMSC - Exciting upside in profit sharing agreement

Legal dispute with OSG

Difficult financial situation

No short/medium term outlook for profit sharing

Low market value

OSG settlement agreement negotiated

Balance sheet restructured

Prolonged bareboat charter agreements

Strong outlook going forward

6

Converto’s view Predictable cash flow through bareboat hire

and upside through profit sharing

agreement

OSG Chapter 11 situation monitored

closely and related risk considered low

2009

2013

Ocean Harvest - Focus on preserving quota values

7

Converto’s view Case remains highly challenging

Focus on preserving quota values in one of

the world’s few remaining open ITQ quota

regimes

2009

2013

Weak historical profitability

High external debt and need for

refinancing

Need for asset upgrade

Challenging biological situation

Continued weak profitability and operational

challenges

Divestment of Faroe Island business and subsequent

debt reduction

New business plan

Country risk

NWS - Potential profitability uplift if capacity adjusted

8

Converto’s view Unique raw material access

Significant overcapacity

2009

2013

Integrated processing and harvesting

company lacking focus

Focus on bulk products

High fixed costs

Inflated balance sheet values and

inefficient capital allocation

Focused processing and sales company

Significant asset divestments

Fixed-cost savings realised

New sales & marketing-focused organisation

New branded value-added products in Scandinavian

market

Bokn - 3-way split unlocked substantial value potential

2009

2013

Value of investment not clear

Passive ownership

Conglomerate lacking focus

9

Converto’s view Entrenched position in the strong NCS

market

Attractive acquisition candidates

Delisting from OSE

Three-way split to unlock value Stream – Supplier of products, solutions and services

Align – Production- and safety critical equipment

Naxys – Subsea technology

Naxys successfully divested to GE in 2012

Remaining portfolio has significant underlying value

[1]

[1]

10

Main Activity Consideration

U.S. Jones Act shipyard

Owner of ten U.S. Jones Act product tankers

Supplier to the oil and gas industry

Seafood harvesting in Argentina

Supplier to the oil and gas industry

Processing and sales of seafood

Solid order backlog in an attractive market

Upside through profit sharing agreement

Attractive acquisition candidate

Challenging situation in Argentina

Eureka Pumps the main value driver

Unique raw material access

[1] Owned through Bokn Invest. CCF holds 39.9% in Bokn Invest, which in turn holds >95% in Stream /Align

Proud ownership

Financial OverviewTrond Brandsrud | CFO, Aker ASA

Overview

Aker’s Financial Investments

2

-

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

10 000

CashBNOK 4.8

ReceivablesBNOK 1.7

Equity inv. 0.1

FundsBNOK 2.5

Largest assets

Converto 1814OAM 375Norron 314

Fornebu 993Setanta 302Navigator 120

Aker ASA Capital Markets Day 2013 | Financial Overview

MNOK The value of Aker’s financial investments

has grown over the past year, for the right reasons:

› Underlying values have increased › Cash holding has increased

No new investments made

The roadmap remains the same:

1. Focus2. Develop3. Exit/realise

924342265

500-

199

3Q13 3Q12

Other 0.3

Financial Investment portfolio, current (3Q13) composition

NAV value (MNOK)

Aker's financial objectives

Capital Markets Day 2013 | Financial Overview 3Aker ASA 3

Returns

Balance Sheet

Secure competitive total returns to shareholders, year on year

Maintain a solid balance sheet, protecting the company from adverse portfolio changes and market effects

Cash

Keep a solid cash buffer to have financial flexibility for: opportunities downward market trends

DividendsSustain increasing dividends, without funding from divestments or new debt as of 2018

CAPACITY

LIQUIDITY

SOLIDITY

4

Aker ASA Capital Markets Day 2013 | Financial Overview

Aker’s liquidity sources and uses

DIVIDENDS RECEIVED

FINANCE INCOME

DIVESTMENTS –FINANCIAL INV.

DIVESTMENTS / M&A – IND. HOLDINGS

DIVIDEND PAYMENTS

FINANCE COSTS

OPERATINGCOSTS

INVESTMENTS –IND. HOLDINGS

RE

CC

UR

ING

NO

N-R

EC

CU

RIN

G

DEBT REPAYMENTNEW DEBT

Sources

Financial portfolio divestments

Capital Markets Day 2013 | Financial Overview 5Aker ASA

Realise NOK 3 billion in values in three years through gradual disposal of non-core assets

Financial Investments portfolio holds significant upside potential

Realised ~NOK 400 million (repayment of AKPS receiv-able, Converto sale of Naxysand Aker sale of MING shares)

Achieved substantial value growth in unrealisedassets

Continue gradual disposals,waiting for the right timing/value

What we said What we have done • What we will do

Sources

Industrial holdings

Capital Markets Day 2013 | Financial Overview 6Aker ASA

Three sources:

1. Ordinary dividends

› Now: AKSO, Kvaerner, Ocean Yield

› Future: AKBM, Havfisk, Det norske

2. Extraordinary dividends from M&A activity at portfolio company level

› E.g. AKBM’s sale of Epax unit

3. Sale of shares

› Optionality in terms of share holdings

Sources

Aker’s debt profile

Capital Markets Day 2013 | Financial Overview 7Aker ASA

Financial Covenants Limit Status per

30.09.2013i Total debt/equity2 < 80% 42%

ii Group loans to NAV < 50% 10 %or Group loans/loan guarantees < NOK 10 bn NOK 2.1 bn

Average debt maturity close to 5.1 years

MNOK

AKER07

0

200

400

600

800

1000

1200

1400

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Bank debtBond

AKER06

AKER05

AKER08

BANK DEBT

AKER11

AKER10

AKER09

AKER07

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

Cash

Interest-bearing receivables

Debt

Net interest bearing receivables NOK 1.0 billion

MNOK

Net interest bearing items Debt overview & financial covenants

2 Covenant applies to Aker ASA (parent only). Reference is made to loan agreements for details.

1 Aker ASA has exercised call option on AKER06. The bond issue will be repaid with settlement date 28 November 2013, at 104% of par value

1

Sources

Aker’s debt strategy

Capital Markets Day 2013 | Financial OverviewAker ASA 8

Long-term funding profile – efficient yield curve

Minimum cash > debt and loan guarantees due next 3 years

Flexibility to optimise timing of refinancing and capture market opportunities

Regular and open dialogue with bond and bank markets

Equity ratio (based on NAV) to reflect risk profile of portfolio; normally 80% or above

Gearing capacity: financial covenants with significant headroom

Invest only equity in Industrial Holdings. Portfolio companies to be financed independently from Aker

100

150

200

250

300

350

400

450

500

550

600

1 2 3 4 5 6 7 8 9 10

2011

2012

2013

Aker’s indicative yield curve development

Ind

ica

tive

sp

rea

ds

IllustrativeIllustrative

Key guidelines

Uses

Investments and dividends

Capital Markets Day 2013 | Financial Overview 9Aker ASA 9

Det norske will require additional equity to develop Johan Sverdrup

No other Industrial Holding companies require additional funding according to current business plans. However, potential to increase current exposure through share purchases

Dividend policy: 2-4% of NAV

Current cash and cash sources are sufficient to uphold dividend policy and increase investments in Industrial Holdings

Conclusion

Capital Markets Day 2013 | Financial Overview 10Aker ASA

Solid balance sheet and strong equity position

Financial flexibility through significant cash holding and other sources of liquidity

Sustainable and increasing dividend with competitive yield

Continue divestments and focus portfolio

Leverage Aker’s position in debt market to further reduce cost of capital

▪ This Document includes and is based, inter alia, on forward-looking information and statements that are subject to risks and uncertainties that could cause actual results to differ. These statements and this Document are based on current expectations, estimates and projections about global economic conditions, the economic conditions of the regions and industries that are major markets for Aker ASA and Aker ASA’s (including subsidiaries and affiliates) lines of business. These expectations, estimates and projections are generally identifiable by statements containing words such as ”expects”, ”believes”, ”estimates” or similar expressions. Important factors that could cause actual results to differ materially from those expectations include, among others, economic and market conditions in the geographic areas and industries that are or will be major markets for Aker's businesses, oil prices, market acceptance of new products and services, changes in governmental regulations, interest rates, fluctuations in currency exchange rates and such other factors as may be discussed from time to time in the Document. Although Aker ASA believes that its expectations and the Document are based upon reasonable assumptions, it can give no assurance that those expectations will be achieved or that the actual results will be as set out in the Document. Aker ASA is making no representation or warranty, expressed or implied, as to the accuracy, reliability or completeness of the Document, and neither Aker ASA nor any of its directors, officers or employees will have any liability to you or any other persons resulting from your use.

▪ The Aker group consists of many legally independent entities, constituting their own separate identities. Aker is used as the common brand or trade mark for most of this entities. In this document we may sometimes use ”Aker", "Group, "we" or "us" when we refer to Aker companies in general or where no useful purpose is served by identifying any particular Aker company.

Disclaimer

Capital Markets DayAker ASA

53