Over $40 billion was invested within the oil and gas projects in Azerbaijan implemented by BP

TAX ADMINISTRATIONOF THE SLOVAK REPUBLIC

A N N U A L R E P O R T2 0 1 0

1

TABLE OF CONTENTS

FOREWORD 3

ORGANISATION IDENTIFICATION DATA 4Organisation of Tax Authorities 5

Tax Directorate of the Slovak Republic 5

Tax Office 6

Tax Office for Selected Taxpayers 6

Financial management 7

TAX ADMINISTRATION AND COLLECTION OF TAXES 8Taxpayer registration and records keeping 9

Number of filed and processed tax documents 10

Allocation of 2 % of tax 10

Transfers from operators of gambling facilities 10

Tax authorities decision making competence 11

State Aid granted in 2010 12

Services rendered to the public 12

TAX AUDIT 13Tools supporting the enhancement of tax audit 13

Risk Management Department tools used for supporting the performance of tax audit 14

Tax Authorities evaluation of submitted notifications on suspected tax crimes in 2010 14

TAX ARREARS ENFORCEMENT 15Main indicators set for enforcement of tax arrears 16

Methodological tools supporting enforcement of tax arrears 16

INTERNATIONAL COOPERATION 17Bilateral cooperation 18

Multilateral cooperation 18

PROJECT AND PROCESS MANAGEMENT 18UNITAS I. programme projects implemented at the Tax Authorities in 2010 18

Internal projects implemented at the Tax Authorities in 2010 18

Projects funded using the funds of the European Union in 2010 18

INFORMATION TECHNOLOGIES 19

INTERNAL AUDIT 20Results of audit activities 20

HUMAN RESOURCES MANAGEMENT 21Personnel overview of the Tax Administration of the Slovak Republic 21

Social policy 21

TAX ADMINISTRATION PERSONNEL TRAINING 22Adaptive training 22

Continuous training 23

Specialised training 23

National Project “Qualified employee of the Tax Administration – benefit for the whole society“ 23

Tax Administration of the Slovak Republic Annual Report - 2010

Tax Directorate of the Slovak Republic2

TAX A D M I N I S T R AT I O N O F T H E S LOVA K R E P U B L I C

A N N UA L R E P O R T2 0 1 0

Copyright © 2010

Tax Directorate of the Slovak Republic

Nová 13

975 04 Banská Bystrica

tel.: +421 48 439 31 11

fax: +421 48 413 49 89

www.drsr.sk

Copyright © 2011 illustrative photos & graphic design

www.euroart.sk

with which they have been directly linked. From the procedural standpoint, the

Extraordinary Audit Department has been transformed into a unit and functionally

assigned under the Section of Tax Audit and Tax Distrain where it in terms of contents

and description of its activities belongs and always should have belonged.

Given the very specific set of activities as well as demanding and frequently

changing legislation, it is crucial for the Tax Administration to have an adequate

number of qualified and technically skilled employees to ensure a proper fulfilment

of its tasks and duties. Therefore in 2010, the Tax Administration of the Slovak

Republic provided to its employees a systematic technical training and created

conditions for deepening and upgrading qualification. The training of employees

of the Tax Authorities was carried out based on the Framework Plan of Training of

Tax Authority Employees in 2010, which was elaborated into operational plans of

training. Thanks to support from the European Social Fund, our employees had the

opportunity to take part in training under the National Project „Qualified employee

of the Tax Administration - benefit for the whole society“.

In the following year, the Tax Administration of the Slovak Republic is awaiting one

of the biggest changes in its history. The reform of Tax and Customs Administration

with a subsequent unifi cation of the collection of taxes, customs duties and insurance

contributions is being gradually implemented in accordance with the UNITAS program

in its individual stages. The target of the reform is to build an effi cient and customer-

oriented Financial Administration which would be capable to take on tasks related to

unifi ed collection of taxes, customs duties and insurance contributions. In future, the

program UNITAS is expected to bring cost savings, better and more complex overview

of developments in public fi nances, reduction of tax and customs evasion as well

as reducing bureaucracy and substantially simplifying and clarifying the processes

associated with the tax and contribution duties. The program UNITAS will bring the

philosophy of client-oriented Financial Administration in relation to taxpayers, which

will be built on providing quality services and information.

Finally, I want to thank all employees of the Tax Administration of the Slovak

Republic for the work they delivered in 2010. Thanks to your expertise and full-

stretch work we have demonstrated that the Tax Administration of the Slovak

Republic is a vital and well functioning organism, which can achieve high goals and

so meet the expectations of the society.

I am pleased that we can continue all together in this effort. On this journey, I

wish us all enough energy and good decisions.

Miroslav Mikulčík

Director General

Miroslav Mikulčík

Director General

Tax Administration of the Slovak Republic Annual Report - 2010 3

FOREWORD

Dear Madam, Dear Sir,

You are just holding in your hands the

publication „Annual Report on Activities of Tax

Authorities of the Slovak Republic for 2010“. I would

like to briefl y comment – from my perspective –

everything what has happened in our organization

during 2010 but at the same time what we are

awaiting in the near future. I personally am very glad

to have the opportunity to be here and participate

actively in the Reform of the Tax Administration of

the Slovak Republic and I do invite you all to work

together on this diffi cult and long-term task. We

have a chance to build something new and „big“:

a Tax Administration which will serve the taxpayers

even more than ever before. We want our Tax Administration of the Slovak Republic to be

modern, digitized, effi cient and oriented to the needs of taxpayers.

The strategic objectives of the Tax Administration of the Slovak Republic for 2010

pointed out an ambition to further improve the performance of the Tax Administration

of the Slovak Republic, to increase the quality in all areas and to prepare it for the

upcoming period, where we await major structural and organizational changes. We

already launched some (mostly legislative) changes in the previous period and gradually

in 2010, we began the process to assume additional tasks relating in particular with the

strategic objectives in the area of unifying the collection of taxes, customs duties and

insurance contributions covered under the heading of the programme UNITAS.

Firstly, the Tax Directorate of the Slovak Republic passed in 2010 through a

fundamental organizational change, mainly due to streamlining its processes and

activities, and not least because of economies of top management directors. We have

looked at the original structure with new eyes and we adjust internal relations so that

the individual departments can communicate better among themselves to ensure a

better insight in the process of management and enhance the organisation of work.

The most substantial change aff ected the Section of Tax Administration. Its internal

processes have been divided into methodological and those related directly with

the performance of tax administration. A new Section of Methodology of Taxes has

been created, which is responsible for legislative and methodological management

of all components of the Tax Administration of the SR. Another major change was the

merger of Sections of General Administration and IT in one section named Section of

Economy and IT ensuring the streamlining of internal support processes of the Tax

Directorate of the Slovak Republic. The Section of International Relations has been

repealed and its activities have been divided into individual technical departments

Tax Directorate of the Slovak Republic4

ORGANISATION IDENTIFICATION DATA

Name: Tax Directorate of the Slovak Republic

Location: Nová ulica 13, 975 04 Banská Bystrica, Slovakia

Tel.: +421 48 43 93 111

Fax: +421 48 41 34 989

Webpage: www.drsr.sk

Resort: Ministry of Finance of the Slovak Republic

Statutory representative:

Ing. Miroslav Mikulčík

Director General

e-mail: [email protected]

phone: + 421 48 4393 902

Top management members:

Ing. Milan Sokol

Director of the Office of Director General

e - mail: [email protected]

phone: + 421 48 4393 903

Ing. Vasil Paňko

Deputy Director General for Administration of Taxes

e - mail: [email protected]

phone: + 421 48 4393 932

Ing. Igor Krnáč

Deputy Director General for Tax Audit and Tax Distraint

e - mail: [email protected]

phone: + 421 48 4393 801

Ing. Zdenka Klinková

Deputy Director General for Tax Methodology

e - mail: [email protected]

phone: + 421 48 4393 190

Ing. Martin Lejtrich

Deputy Director General for Economy and IT

e - mail: [email protected]

phone: + 421 48 4393 700

JUDr. Elena Rafaelisová

Director of Human Resources Management Office

e - mail: [email protected]

phone: + 421 48 4393 926

Ing. Anton Strašík, PhD.

Director of Internal Audit Department

e - mail: [email protected]

phone: + 421 48 4363 323

Mgr. Anna Jasovská

Director of Juridical and Legal Services Department

e - mail: [email protected]

phone: + 421 48 4393 732

Ing. Ivana Vilčeková

Director of Innovations Centre

e - mail: [email protected]

phone: + 421 48 4393 237

Mgr. Gabriela Dianová

Spokesperson

e - mail: [email protected]

phone: + 421 48 4393 905

5

Organisation of Tax Authorities

Tax authorities comprise the following:

Tax Directorate of the Slovak Republic and

Tax offices.

The Tax Directorate of the Slovak Republic (hereinafter as “TD SR”) was

established pursuant to Act No. 150/2001 Coll. on Tax Authorities amending the

Act No. 440/2000 Coll. on Financial Audit Administration.

In accordance with provisions of Tax Authorities Act, the TD SR has established

its regional offices which are currently eight in number and are located in capitals

of Higher Territorial Units (hereinafter as “HTU”), their objective being to ensure

that certain specific tax administration related activities are performed on regional

level.

To support the activities of tax offices, the Tax Office for Selected Taxpayers was

established in Bratislava pursuant to Act No. 150/2001 Coll. on Tax Administration

Authorities.

The scope and competences of the TD SR are defined by the above Act

No. 150/2001 Coll. on Tax Authorities which also governs the structure of Tax

Administration bodies, position and scope of Tax Directorate, tax offices and

Tax Administration bodies in matters related to taxes, including the penalties,

interest, tax and penalty increase in pursuance of special regulations, fees

chargeable according to special regulations being the State Budget direct revenue,

administration of court fees related to registration in respect thereof and settlement

according to special regulations, being equally the State Budget direct revenue,

state supervision in companies running the lotteries and other similar gambling

facilities, pursuant to special regulations.

Tax Directorate of the Slovak Republic - scope of activity

The Tax Directorate:

assumes responsibility for meeting tax regulations by each of its offi ces in a

uniform manner and makes suggestions for amendments in respect thereof,

defines internal organisational structure of tax offices,

proposes the changes of tax offices locations and their number,

elaborates the concept of Tax Administration development, including the

concept of tax bodies and municipal offices staff training,

submits notices on suspected tax crimes in connection with infringement

of special regulations to the authorities responsible for investigation and

prosecution in criminal proceedings,

establishes, maintains and operates the Tax Information System, keeps

the central register of all taxpayers, updates the database and provides

information pursuant to special regulations,

keeps taxpayers informed about their rights and obligations with respect

to tax related matters and about special regulations,

supervises the activities of local tax offi ces and takes appropriate measures to

provide for elimination of imperfections identifi ed from obtained fi ndings,

checks the compliance with rights and obligations of taxpayers and carries-

out statutory supervision in companies running the lotteries and other

similar gambling facilities subject to special regulations and to ensure this

it is granted the right of entering the premises operated by taxpayers or

operators of lotteries and other similar gambling facilities,

decides, as the authority on the nearest supervising level, in respect to the local tax

offi ces or municipalities, on matters addressed within the tax related proceedings,

decides on appeals in tax related matters against decisions taken by tax

offices and municipalities and investigates final decisions made by tax

offices and municipalities without initiation of appellate proceedings,

makes decisions on permissions relating to resumption of proceedings or

issues instructions to revert to such resumption, providing the authority

which has taken the decision is on the highest respective cognisance level,

being the authority on the nearest superior level in relation to tax offices,

the Tax Directorate makes decisions in administrative proceedings pursuant

to special regulations and to the extent specified therein,

provides for mutual international cooperation in tax related matters

pursuant to international treaties and on the basis of authorisation

provided by the Ministry of Finance of the SR (hereinafter as “MF SR”),

is entitled to carry out tax audits or repeated tax audits falling otherwise

under competence of tax offices.

Tax Administration of the Slovak Republic Annual Report - 2010

Tax Directorate of the Slovak Republic6

Tax Office - scope of activity includes the following

administering taxes pursuant to special regulations, predominantly

consisting of the following:

- keeping records and maintaining registers of taxpayers,

- keeping records and accounting for tax revenues,

identifying unregistered taxpayers,

enforcing tax arrears, including the enforcement of outstanding debt on

reversed taxes and contributions to funds as applied before 31st December

1992,

developing the tax audit methodology and tax audit plans,

directing the operations of tax office separate organisational units,

carrying out tax audit,

working out analyses pursuant to special regulations upon request from

the Tax Directorate,

decision making in tax proceedings according to special regulations,

decision making in administrative proceedings,

managing audits of administrative fees collection and enforcement of fees

settlement pursuant to special regulations, administering and keeping

the records on court fees with respect to their registration and settlement

according to special regulations,

keeping taxpayers informed about their rights and obligations in tax

related matters and about special regulations applied in this respect,

submitting notices on suspected tax crimes in connection with infringement

of special regulations to the authorities responsible for investigation and

prosecution in criminal proceedings, and reporting accordingly to the TD

SR,

carrying out statutory supervision of lotteries-operating companies and

other similar gambling facilities pursuant to special regulation,

establishing, maintaining, operating and updating the tax information

system database and providing information pursuant to special regulations,

carrying out the processing of recapitulative accounting statements

submitted by municipalities.

Tax offices are also provided with competence allowing their participation in

court proceedings and acting independently before courts within their scope of

operation.

Tax Office for Selected Taxpayers - scope of activity

The Tax Office for Selected Taxpayers administers the selected taxpayers

falling within the competence of Tax Offices of Bratislava I through VI, Tax Offices

in Malacky, Pezinok and Senec, providing these taxpayers belong to one of the

following categories:

banks and branches of foreign banks,

insurance companies and branches of foreign insurance companies,

reinsurance companies and branches thereof,

taxpayers with annual turnover exceeding 33,193,918.87 €.

With respect to other types of activities, the Tax Office for Selected Taxpayers

scope of activity is identical with that of ordinary tax office, except for statutory

supervision.

7

Financial managementIn respect of financial management, the TD SR is an institution fully funded

from the State Budget and its revenues and expenditures are linked to the State

Budget via the section operated by the MF SR.

Tax Administration of the Slovak Republic Annual Report - 2010

Tax Directorate of the Slovak Republic8

TAX ADMINISTRATION AND COLLECTION OF TAXES

Year 2010 has witnessed the continued direction of introducing qualitative

changes in the Tax Administration of the SR and the change of the whole system

of management and planning by application of new, modern procedures and

instruments of management.

The tax revenue figure achieved by the Tax Administration in 2010 from

collection of taxes reached 10,660 million €, a decrease of 964 million € compared

to the previous year figure (8.8 % decrease). In 2009 the Tax Administration of the

SR collected the taxes in the total amount of 11,624 million €. Against the year

2008 figure, this was a decrease by 1,133 million €. The overall tendency in the

collection of taxes in the Slovak Republic has in 2010 continued from 2009 when we

had witnessed a year-to-year decrease. The reason for this is the impact of global

economic crisis, not leaving out Slovakia.

Results

2008

Results

2009

Results

2010

Collection of taxes 12 756.5 11 623.7 10 659.6

- refund of excessive deductions of VAT -6 192.5 -5 282.5 -5 373.4

Gross tax revenues 6 563.9 6 341.2 5 286.2

- transfer of allotment taxes to revenues

of municipalities and HTU + transfer

of 2 % of tax revenues allocated for

community public services

-1 838.5 -1 791.5 -1 491.2

State Budget revenue 4 717.3 4 551.9 3 794.1

Rem.: discrepancies in totals (State Budget revenue) are due to rounding-up figures in million EUR

The Tax Administration of the SR collects taxes which represent revenues of the

State Budget, and also collects and administers taxes which are then transferred

into the budgets of municipalities and HTU, and allocates a portion of paid taxes for

purposes of community service.

Taxes collected by the Tax Administration of the SR, amounting to

10,660 million € were in 2010 decreased by:

VAT refunds (5,272 million €),

transfers from the yields of PIT into the budgets of municipalities and HTU

(1,328.5 million €),

transfers of motor vehicle tax paid (incl. the previous road tax) for HTU

(118.6 million €),

transfers of a portion of paid PIT and CIT for community services

(44.1 million €).

After deducting the above mentioned VAT refunds and transfers into the

budgets of municipalities and HTU, the Tax Administration of the SR transferred

into the State Budget tax revenues amounting to 3,794 million €.

Yearly interim VAT refunds (claims for returning the excessive deduction on VAT

paid) have increased by 90.9 million €; Yearly interim transfers of yields from PIT

into the budgets of municipalities and HTU have decreased by 282 million €; Yearly

interim transfers of motor vehicle tax paid (incl. the previous road tax) for HTU have

decreased by 7.2 million € and yearly interim transfers of a portion of paid PIT and

CIT for community services have decreased by 11 million €.

In 2010, all payments which are then transferred by the Tax Administration of

the SR to the budgets of municipalities and HTU and to taxpayers as VAT refunds,

represent 64 % of total volume of collected tax revenues – in 2009, this figure was

61 % and in 2008 63 %.

Collection of taxes – selected types of tax revenues in years 2008 – 2010:

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

in m

illio

ns

of

€

PIT - employees PIT -

- self-employed

CIT Withholding

tax

VAT

collection

2008 2009 2010

9

Tax revenues, transferred by the Tax Administration of the SR into the State

Budget amounting to 3,794 million €, represent a 48 % share on the total tax

revenues of the State Budget; in previous year, this share was 56.7 %.

Another type of State Budget revenues are non-tax revenues. In 2010, these

amounted to 254 million €, an annual interim decrease by 11.6 million €.

Compared to previous year, the volume of taxes collected by the Tax

Administration of the SR for the State Budget was lower by 757.9 million € (by 16.6 %).

The highest annual interim decrease was seen by the Corporate Income Tax (41 %)

– a decrease by 872 million €. This reflects the drop of production and activity of

taxpayers in times of economic crisis of 2009. The development of tax revenues in

2010 was to even higher degree than in 2009 influenced by the global crisis. CIT and

PIT from business activity reflects the production of 2009. That is because regarding

the income taxes, legislative changes and the impact of economic situation is

delayed by one year, while in regard of consumption taxes, the economic situation

has an immediate impact. The annual interim growth was seen for VAT – an increase

by ca 4 %. This condition is caused by the annual interim increase of actual tax

liabilities (1 %).

The highest shares of the Tax Administration on the State Budget have revenues

from VAT (59 %) and CIT (33 %). The rest of 8 % of the revenues is composed of

withholding tax, the share of SR on the PIT, residues from property taxes and fines

from tax audits.

As for the pursuance of plan for 2010 State Budget, the Tax Administration of

the SR achieved 100.57 % pursuance of budgeted revenues from taxes administered

by the Tax Administration. Lower yield that the planned figures were the yields from

direct taxes, above all CIT where the planned budget was pursued only up to 95.3 %

and PIT – 93.48 %. This low level of pursuance was caused by significant decrease

of the volume of tax settlement, and at the same time decrease of advance tax

payments.

More favourable development had VAT: the pursuance of budgeted revenues

for VAT administered by the Tax Administration of the SR achieved 103.47 %. Planned

revenues were over-passed also for withholding tax; the high level of pursuance in

this case was caused by the settlement of additionally assessed tax after the tax

audit at a large taxpayer.

Despite lower gross revenue from PIT, its State Budget revenues are higher

than the previous year – however, this is caused by a significant yearly interim

decrease of funds transferred from the yields of PIT into the budgets of HTU and

municipalities.

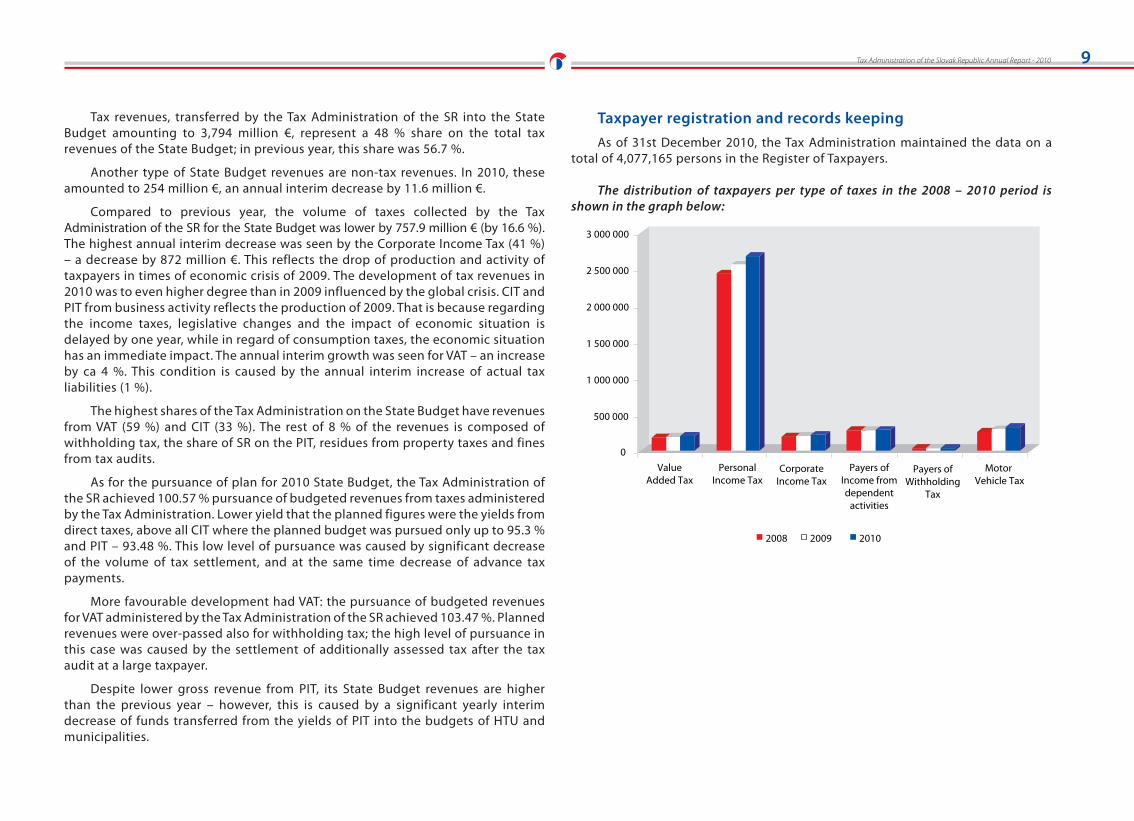

Taxpayer registration and records keeping

As of 31st December 2010, the Tax Administration maintained the data on a

total of 4,077,165 persons in the Register of Taxpayers.

The distribution of taxpayers per type of taxes in the 2008 – 2010 period is

shown in the graph below:

0

500 000

1 000 000

1 500 000

2 000 000

2 500 000

3 000 000

Value

Added Tax

Personal

Income Tax Corporate

Income Tax

Payers of

Income from

dependent

activities

Payers of

Withholding

Tax

Motor

Vehicle Tax

2008 2009 2010

Tax Administration of the Slovak Republic Annual Report - 2010

Tax Directorate of the Slovak Republic10

Number of filed and processed tax documents

In 2010, a total of 4,698,048 input tax documents were filed and processed at tax

offices. This number includes tax returns for PIT and CIT, VAT and motor vehicle tax.

Payers of income tax form dependent activities have to file reports on tax settlement,

and quarterly reviews of withheld and paid advanced taxes. As usually, even in 2010 the

taxpayers used the option of allocating a portion of the tax paid for special purposes.

All tax returns, tax reports, overviews and accounting reports were processed by the

tax information system. Compared to year 2009, the number of processed documents

is higher by 90,278. This increase is mostly caused by an increase in filed tax returns for

PIT and also CIT for the taxable period 2009, a repeated increase of filed VAT returns

and an increase of filed reviews of withheld and paid advanced taxes.

Allocation of 2 % of tax paid pursuant to provision under § 50

of Act No. 595/2003 Coll. on Income Tax as amended

The Tax Administration has been transferring the respective portion of tax

liability paid in favour of legitimate beneficiaries since 2002. Tax administrators

allocate 2% of the total tax liability paid by the taxpayer in favour of the beneficiaries

included for the respective year in the List of Beneficiaries, maintained by the

Notary Public Chamber of the Slovak Republic.

YearNumber of

benefi ciaries

Number of

individuals

who allo-

cated their

share from

tax paid

Number

of legal

entities who

allocated their

share from tax

paid

Sum

allocated by

indi viduals

(in thous. €)

Sum

allocated by

legal entities

(in thous. €)

Total amount

of allocated

funds from

tax paid in the

resp. year (in

thous. €)

2008 7 759 449 909 26 691 15 036 34 144 49 180

2009 9 098 503 253 30 078 17 684 37 496 55 180

2010 9 585 467 983 26 172 15 553 28 592 44 145

0

100 000

200 000

300 000

400 000

500 000

600 000

Number

of beneficiaries

Number

of individuals

who allocated

funds

Number

of businesses

who allocated

funds

Funds allocated

by individuals

(in th. €)

Funds allocated

by businesses

(in th. €)

Total sum

of funds allocated

to beneficiaries

(in th. €)

2008 2009 2010

In 2010, administrators of taxes have processed 494,155 declarations. If

compared to the previous year, the number of filed declarations fell by 39,176. The

amount of funds allocated to beneficiaries in 2010 achieved 44,145 thous. €.

Transfers from operators of gambling facilities

Considering the achieved amounts of bets and wins, as well as the amount of

taxes paid into the State Budget and municipalities, we can conclude that gambling

in Slovakia stagnates, with a slightly declining interest of the public.

Due to legalization of a new type of gambling game – poker type card games,

we saw an increase in registration of new operators, and thus a significant increase

in the number of active providers registered in the central register. The number of

operators in 2010 has increased as compared to 2009 by a total of 75 new operators

(an interim rise between year 2008 and 2009 amounted to a total of 44 operators),

and in the course of year 2010, there were as many as 315 active operators of

gambling facilities (in comparison with a total of 246 operators in 2009) on the

basis of granted and issued licences.

In previous year, the number of gaming and gambling facilities slightly

decreased, as there is a tendency to cumulate various types of gambling games

within one larger facility. While in 2008 there were 12,998 gaming premises, in 2009

there were 13,440 and in 2010 the games were offered at 13,064 different facilities.

The highest boom was seen in betting games (increase by 258), and in the new

11

type of poker card games (increase by 69). The number of gaming facilities fell in

year-to-year development, mostly in regard to the number of slot machines (as

compared to 2009, a decrease 3,717 down to total number of 17,373), as well as

decrease in the number of video-games terminals (from 8,353 terminals operated

in 2009 down to 7,423). Similarly, a decrease occurred in the number of operated

gaming electro-mechanical roulette and dice facilities (400 facilities less than in

previous year). The reason for these changes in the number of gambling premises

and facilities lies prevailingly in the change of tax burden (the rate and way) and

the determination of flat-rate fees according to the number of operated gambling

premises and facilities – a legislative change which was implemented as of

1st January 2010.

The achieved results of gambling expressed in the spent money, winnings,

proceeds, operators’ revenue, State Budget direct revenues, tax revenues of

municipalities and administrative fees respond to the development of abundance

of games, gaming and gambling facilities. In 2010, gamblers spent a total amount of

money exceeding 2,031 million €, i.e. a slight decrease by 39 million € if compared

to the year 2009. The total amount of winnings amounted to 1,521 million €, which

is an amount by 43 million € lower when compared to the year 2009; the operators’

revenue, i.e. their income was more than 510 million. The State Budget direct

revenue from levies imposed on lotteries and gambling operations amounted to

100.1 million € in 2010, by 11 million € less than in 2009.

Similarly, the tax revenues of municipalities in 2010 have decreased. In 2009,

funds of municipalities derived from gambling facilities amounted to almost 8.9

million €, in 2010 8.5 million €.

Other revenue was transferred into municipality budgets and the State Budged

by paying administrative fees. The State Budget direct revenue from administrative

fees amounted to 328 thousand € in 2010, and in 2009, the collected administrative

fees amounted to 539 thousand €. In 2010, funds of municipalities derived from

administrative fees amounted to a minimum of 26.1 million €, which is compared

to 2009, a decrease by 5.4 million €.

Tax authorities decision making competence

In 2010, the TD SR received a total of 4,633 appeals. The greatest share on these

appeals had the appeals against decisions on VAT with a total of 1,602 (35 %) and

against decisions on delinquency in administrative matters pursuant to provisions

under § 35 Act No. 511/1992 Coll. as amended (except electronic cash-registers),

the total number of which amounted to 1,217 (26 %).

The number of extraordinary remedies (review of a decision without appellate

procedure and retrial of proceedings) lodged in 2010 was the following:

427 submissions with request for review of a decision without appellate

procedure,

45 submissions with request for resumption of procedure, where such

resumption may be permitted or ordered by the appellate body.

With respect to jurisdiction related in administrative matters, the TD SR received

a total of 463 suits against decisions of body on a higher level of cognisance, out of

which 321 dealt with VAT (69 %).

Comparison of ordinary and extraordinary remedies and suits

0

1 000

2 000

3 000

4 000

5 000

6 000

Number

of appeals

received

Number

of appeals

addressed

Number

of filed

suits

Number

of requests

to examine

a decision

Number

of requests

to reopen

a case

2008 2009 2010

Tax Administration of the Slovak Republic Annual Report - 2010

Tax Directorate of the Slovak Republic12

State Aid granted in 2010

In 2010, a total of 13 taxpayers submitted their application with a request for

state aid in the form of tax relief, pursuant to provisions under § 35 and § 35a Act

No. 366/1999 Coll. on Income Taxes as amended and in accordance with § 52 Act No.

595/2003 Coll. on Income Taxes as amended, the providers of which are tax offices.

Two taxpayers have applied for tax relief pursuant to provisions under § 30a Act

No. 595/2003 Coll. on Income Taxes as amended (investment aid). Four taxpayers

have been granted state aid according to the Temporary Scheme to grant limited

aid in the Slovak Republic in the period of lasting financial and economic crisis

No. 222/2009 as in appendix No. 1, amounting to 7,748.30 €. The total amount of

state aid granted by the Tax Authorities in 2010 amounted to 8,896 million €.

Services rendered to the public

In 2010, the TD SR (including tax offices) received altogether 17,194 written

requests for information, out of which as many as 57 % concerning the income tax,

36 % concerning VAT, 5 % concerning local taxes and fees and 2 % concerning the

administration of taxes. In comparison with the previous year 2009, the number of

received enquiries submitted by the public increased by a total of 5,002 submissions.

VAT

36%

Local Fees

5%

Administration of taxes

2%

Income Tax

57%

Taxpayers were provided with information also in the form of specialized

information materials. Their contents reflected actual topics - mostly income tax

and value added tax, particularly in relation to the obligation to file tax returns and

pay taxes. Information materials were produced also in connection with the new

amended tax legislation. The public had access to such tailored information mostly

through the web-site of the Tax Directorate of the SR, as well as in the form of public

notice on tax offices’ information boards. Altogether 33 specialized information

materials were produced for the public in 2010. Each tax office organised at least

one consultation day related to filing income tax returns.

In the period just prior to the deadline for filing income tax returns, all kinds

of information related to these questions were provided to the public also in

cooperation with mass-media, mostly in the form of articles in daily press.

state aid granted by the Tax Authorities in 2010 amounted to 8,896 million €.

13

TAX AUDIT

The main indicators in the area of tax audit for the 2010 period were set as follows:

to ensure the compliance with the volume of findings from tax audit

(without the determination of tax liability with the use of aids) amounting

to 165 million €,

percentage of appeals against decisions by the end of tax audits and local

investigations focused on Electronic Cash Register (hereinafter only as “ECR”),

to carry out control actions,

to carry out at least 20,000 local investigations focused on ECR.

Compliance with the volume of fi ndings from tax audit for the entire tax

administration at 31st December 2010 has been in fi nancial terms 345,264 thousand €,

which represents compliance with planned fi gures at 209.3 %. The total fi ndings

exceeded the planed volume of controls by 109.3 %, in absolute terms by

180,264 thousand €.

During the period referred to herein tax auditors carried out as many as 18,400

tax audits. Of the total number of tax audits completed, the greatest share is assumed

by value added tax audits, with 11,442 audits, i.e. 62.2 % of the total number of tax

audits. Tax audits targeted on income tax of legal entities were performed in a total

of 2,350 audits, tax audits on income tax of individuals in 3,005 audits, tax audits of

income tax from dependent activity from employment accounted for 435 audits; road

tax and motor vehicle tax was subject to tax audits in 70 audits, 1,040 tax audits were

aimed at book-keeping, and the remaining 47 audits were of other types of tax.

Tax audits carried out by tax auditors comprised the following: 12 transfer

pricing audits accounting for the total findings of 2,735 thousand €, 92 network

audits with the total findings of 53,571 thousand €, and 628 EDP audits with total

findings amounting to 17,855 thousand € and 13 multilateral audits accounting for

the total findings of 8,131 thousand €.

In addition to regular tax audits, there were as many as 44,262 local investigations

carried out, on the basis of which the penalties were imposed amounting to

457 thousand €. Of the total number of local investigations, 20,805 were focused on

verifying the compliance with relevant provisions of MF SR Act No. 55/1994 Coll. on

Keeping Records on Sales with the Use of Electronic Cashing Register, as amended and

the Act No. 289/2008 Coll. on the Use of Electronic Cash Registers and on amendment

and supplements of Act of the Slovak National Council No. 511/1992 Coll. as amended.

The fi nes imposed following these local investigations amounted to 431 thousand €,

i.e. 94.3 % of the overall amount of penalties imposed in connection with local

investigations procedures. Of the total number of local investigations, 3,032 focused

on voluntary VAT registration and 396 focused on detecting illegal work.

As of 31st December 2010, within the tax audit activities at on one tax control

accounts for an average findings amounting to 30 thousand € and a single auditor

amounting to 347 thousand € which represents a considerable increase compared

with previous periods.

Tools supporting the enhancement of tax audit include the following

defining the strategy of tax audit,

designing the schedule and orientation of tax audit,

issuing the methodological guidelines and guidance, working aids and

standpoints supporting the performance of tax audit and spot findings,

operative methodological consultations and assistance in carrying out tax

audits and spot findings,

organising workshops and operating meetings with the view of information

exchange and addressing current problem issues,

introducing measures to prevent fraudulent action by organized groups,

coordination of tax audit performance and local investigations in

connection with taxpayers involved in carousel fraud,

cooperation with authorities carrying out investigation and prosecution in

criminal proceedings, and cooperation with customs offices,

updating of the databases used in the scope of the audit activities,

updating of technical support tools:

- ISK 1 – the software for selection of taxpayers for tax audit,

- ISK 2 – the software for electronic support of issuing tax audit related

documents,

- EDP audit – electronic audit using the software IDEA,

- Kontrolsoft – an electronic library used by tax auditors,

- SAR DPH – the system for risk analysis with respect to VAT, dividing the

taxpayers into groups,

- Application extension OIS - Customs database,

cooperation on international level in the area of tax audit (an active

participation in the OECD, FISCALIS, IOTA, OLAF working groups).

Tax Administration of the Slovak Republic Annual Report - 2010

Tax Directorate of the Slovak Republic14

Risk Management Department tools used for supporting the

performance of tax audit and meeting the plan of tax revenues

analytic information system (selection of high-risk taxpayers, ratio analyses,

forecasting, knowledge fund, criminal area, output reports range, etc.),

DATAMINING (DM1 model – with respect to tax audit potential finding,

DM2 model – taxpayers categorisation),

information from the Police Authorities,

unusual business operations and transactions,

defining risk factors within the Tax Administration of the SR competence

seen with taxpayers and resulting in a direct impact on taxpayers´

compliance with their tax liability,

identifying the high-risk business sectors and risk factors influencing the

classification of a business area as belonging among sectors with greater

amount of risk,

analysing the level of criminal consequences resulting from risk behaviour

of taxpayers not abiding by special regulations,

cooperation on international level (relevant representatives are the

members of multidisciplinary integrated groups of experts aimed at

elimination of economic criminality and suppression of delinquency),

cooperation on international level in the area of risk analysis (active

participation in the OECD, FISCALIS, IOTA, OLAF workgroups).

Tax Authorities evaluation of submitted notifications on

suspected tax crimes in 2010

Tax Administration of the SR announced in 2010 to the authorities carrying out

investigation and prosecution in criminal proceedings a total of 1,909 suspicions

of committing tax crime, in which it calculated the total loss of 186,132,052.71 €.

Number and development of notifications of tax crimes evaluated by the tax

authorities and the overall calculated total loss for the years 2009 and 2010

2009 2010Index

2010/2009

Number of submitted

notifi cations on tax crimes3 343 1 909 57.40 %

Overall calculated total loss

in €364 645 246.64 186 132 052.71 51.04 %

The development was affected negatively by a high and inefficient growth of

notifications which were closed by the authorities carrying out investigation and

prosecution in criminal proceedings even before the beginning of a prosecution

refusing to classify this act as a crime.

Share and development of taxes regarding the loss in notifications of tax cri-

mes sent by tax authorities for the specified periods (in %)

Period

Share of Legal

Entity Income

Tax (in %)

Share of VAT

(in %)

Share of

Personal Income

Tax (in %)

Share of

other taxes

(in %)

2009 19.34 73.09 4.77 2.80

2010 16.04 71.67 3.40 8.90

Number of Police Investigative Bodies (PIB) decisions in 2010

Period

Number of

received

resolutions

from PIB

Rejection -

§ 197 of the

Criminal

Procedure

Code (CPC)

Percentage

share

Beginning

of criminal

prosecu-

tion - § 199

of the CPC

Percentage

share

2010 820 538 65.61 282 34.39

15

TAX ARREARS ENFORCEMENT

Tax administrator (tax office) enforces tax arrears through its employees – tax

enforcement officers. Their main duty is to ensure that the recovery of tax arrears

is enforced while adhering to the principle of effectiveness of procedure, i.e. to

provide for maximum effect at minimum cost incurred in respect thereof.

Operation of a tax enforcement officer is not narrowly specialised to tax

enforcement proceedings but involves a great variety of steps associated with

securing property, submitting claims under separate proceedings (in bankruptcy,

reconstructing, dissolution, inheritance, distraining procedure, applying claims in

connection with lien set up by other lien creditors under enforcement of tax arrears

within international proceedings). This means that the requirements with respect

to educational background and skills of a tax enforcement officer in a variety of

areas of law and stringent adherence to rule of law are high, because reverting

to the original status in enforcement officer’s procedure is practically impossible.

Based on experience from other member countries of the European Union, in view

of effectiveness, it is indispensable that predominantly such tax arrears are enforced

that are the greatest in amount and when it comes to their duration in time, priority

should be given to the more recent ones over the older ones.

Enforcement of tax arrears is the duty of approximately 314 tax enforcement

officers in a total of 102 tax offices. According to tax office size, tax enforcement

officers are either members of tax audit and enforcement departments or operate

within separate departments of tax enforcement established within larger tax

offices. Performance of enforcement by using own employees has been considered

to be the most effective method of enforcement of tax arrears.

Following our experience and knowledge gained abroad we are familiar with the

fact that tax arrears are the indispensable accompanying eff ects of greater tax revenues

being collected. This phenomenon is quite common and is to be faced by each of the Tax

Administrations. Any further increase of tax arrears then greatly depends upon fl exibility

and sophistication of tax related legislation of a specifi c country. Tax arrears increase

as the phenomenon may currently be fully eliminated only under very exceptional

situations. Our legislation provides for legal instruments the use of which may have

some eff ect upon extent of tax arrears recorded, but very seldom to an extent expected.

These instruments within legislation of the Slovak Republic include the following:

enforcement of tax arrears in case there is a property which is enforceable

by enforcement procedure.

In other cases the procedure involves the following:

ceding tax claims within bankruptcy procedure pursuant to § 65b Act on

Administration of Taxes and Fees,

suggestion for deletion of the company from the Register of Companies

providing the relevant conditions of Commercial Code have been complied

with,

Tax Administration of the Slovak Republic Annual Report - 2010

submitting a petition for issuing a bankruptcy order with respect to a

taxpayer that is in delay with settlement of his/her tax liability pursuant to

§ 65c Act on Administration of Taxes and Fees, providing the conditions set

by special regulations have been met at the same time,

offsetting of a tax claim applicable by tax office towards the tax debtor in

case the debtor possesses concurrently an eligible claim receivable from

government organisation fully funded from the State Budget pursuant to

§ 63a Act on Administration of Taxes and Fees.

Tax Directorate of the Slovak Republic16

Main indicators set for enforcement of tax arrears

to accomplish the planned volume of enforceable tax arrears 135,700

thousand €,

to file at least 202 petitions for issuing a bankruptcy,

to promote a complex portfolio of tax enforcement methods and

procedures in particular organization of public sales of movable and

immovable property.

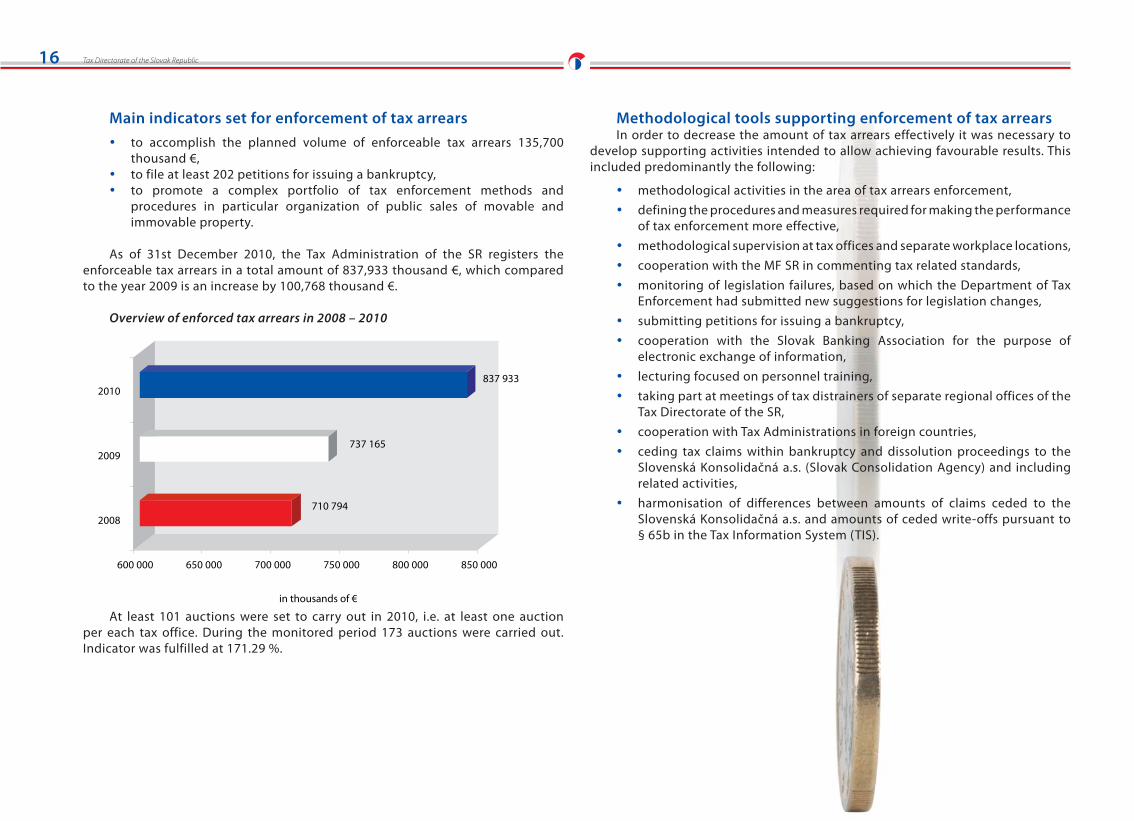

As of 31st December 2010, the Tax Administration of the SR registers the

enforceable tax arrears in a total amount of 837,933 thousand €, which compared

to the year 2009 is an increase by 100,768 thousand €.

Overview of enforced tax arrears in 2008 – 2010

710 794

737 165

837 933

600 000 650 000 700 000 750 000 800 000 850 000

in thousands of €

2008

2009

2010

At least 101 auctions were set to carry out in 2010, i.e. at least one auction

per each tax office. During the monitored period 173 auctions were carried out.

Indicator was fulfilled at 171.29 %.

Methodological tools supporting enforcement of tax arrearsIn order to decrease the amount of tax arrears effectively it was necessary to

develop supporting activities intended to allow achieving favourable results. This

included predominantly the following:

methodological activities in the area of tax arrears enforcement,

defining the procedures and measures required for making the performance

of tax enforcement more effective,

methodological supervision at tax offices and separate workplace locations,

cooperation with the MF SR in commenting tax related standards,

monitoring of legislation failures, based on which the Department of Tax

Enforcement had submitted new suggestions for legislation changes,

submitting petitions for issuing a bankruptcy,

cooperation with the Slovak Banking Association for the purpose of

electronic exchange of information,

lecturing focused on personnel training,

taking part at meetings of tax distrainers of separate regional offices of the

Tax Directorate of the SR,

cooperation with Tax Administrations in foreign countries,

ceding tax claims within bankruptcy and dissolution proceedings to the

Slovenská Konsolidačná a.s. (Slovak Consolidation Agency) and including

related activities,

harmonisation of differences between amounts of claims ceded to the

Slovenská Konsolidačná a.s. and amounts of ceded write-offs pursuant to

§ 65b in the Tax Information System (TIS).

17

INTERNATIONAL COOPERATION

In the area of international exchange of tax related information the number

of requests processed in 2010 amounted to 4,077. Of this number, a total of 308

requests referred to exchange of information in the area of direct taxes based on

bilateral agreements on avoidance of double taxation and on the Council Directive

No. 77/799/EEC on mutual assistance of respective bodies of member countries

in the area of direct taxes and insurance premium tax. Based on the Council

Enactment No. 1798/2003/EEC on administrative cooperation the number of

requests processed referring to VAT amounted to a total of 3,769 cases. In the area

of direct taxes there was an increase by 11 requests in 2010 compared to the year

2009; in the area of VAT there was an increase by 573 in the number of requests, i.e.

an increase by 17 %.

International exchange of information overview in 2008 – 2010

206

2 641

297

3 196

308

3 769

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

Nu

mb

er

of

req

ue

sts

2008 2009 2010

Direct taxes VAT

During the period from 2008 to 2010, the increase of financial effectiveness

resulting from international exchange of tax information was very significant;

however there has been a slight decrease in 2009. In 2010, there was again a

significant increase in financial efficiency by up to 274 % compared with 2009.

The financial effectiveness figure was determined from the value of additionally

imposed tax liability (or from the reduced amount of refunds of excessive VAT

deduction) and sanctions imposed following the information obtained through

the institute of international exchange of tax information. An overview of overall

financial effectiveness of information exchange is shown in the graph below:

Overall financial effectiveness of information exchange in 2008 - 2010

24 579 23 603

64 750

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

in t

ho

usa

nd

s o

f €

2008 2009 2010

An indirect, non quantifiable, yet the most significant effect of international

exchange of information is the preventive effect with respect thereof and support

of voluntary tax compliance.

During the last year, the employees of International Administrative Cooperation

Unit represented the Tax Administration of the SR in the Standing Committee for

Administrative Cooperation in the area of VAT (SCAC), in the Working Group for

Administrative Cooperation in the area of direct taxes (WG-ACDT), in Working Party

for Administrative Cooperation in the area of direct taxes (taxation of savings WP-

DT), in Project Group for the development of computer assisted country profiles for

administrative cooperation in direct taxation (FPG 58) and as well as in Recovery

Committee for International assistance for the recovery of claims.

During 2010, altogether 13 multilateral controls (MLC) were organised by

competent authorities of the EU member countries (Germany, Austria, Hungary,

Poland and Slovakia) and these were also participated by other EU member

countries. One of these MLCs was initiated by the Slovak Tax Administration. All the

MLCs refer to VAT frauds.

A pilot project of direct cross-border cooperation with the Czech Republic

in the field of direct taxation between directly selected tax offices of the SR and

financial offices of the CR has continued in 2010.

Tax Administration of the Slovak Republic Annual Report - 2010

Tax Directorate of the Slovak Republic18

Bilateral cooperation

Based on signed bilateral agreements the Slovak Tax Administration cooperates

with the Tax Administrations of the Czech Republic, Hungary, France, Austria and

Slovenia. The bilateral cooperation is realized in the form of working visits and

seminars, which are reciprocally organized on the territory of the SR and partner tax

administration and are aimed at improving the effectiveness of tax administrations,

exchange of experience and best working practices.

The Tax Directorate of the SR provides for the establishment of bilateral treaties

therefore it closely cooperates in this respect with the MF SR and participates in

arrangements leading to signing these treaties. It also addresses the tasks resulting

from these treaties and in connection with cooperation being developed in respect

thereof.

The closet cooperation has always been between the Tax Administrations in

Slovak Republic and Czech Republic. This is run on the basis of the bilateral Mutual

Cooperation Treaty signed in 2003. In 2009, Memorandum on Mutual Administrative

Cooperation between the Czech and the Slovak tax administrations, which should

assist the development of even closer cooperation between the countries in the

area of direct information exchange, has been signed.

Multilateral cooperation

Tax Administration of the SR carries out international cooperation on a

multilateral basis through meetings of Heads of V4 Tax Administrations + Austria

and Slovenia. In practical terms, the meetings on previously mentioned basis are

carried out under the work heading „V6 Meeting“. Two meetings were held in 2010.

The first V6 meeting targeted at issues related to enforcement of tax arrears and

fight against tax fraud was held in April in Austria. Another multilateral meeting of

representatives of V6 Tax Administrations took place in October in Portorož, Slovenia.

The most important international organisations with which the Tax

Administration of the SR closely cooperated in 2010 are as follows:

European Commission (EC)

EC Program: FISCALIS

Organisation for Economic Cooperation and Development (OECD)

Intra-European Organisation of Tax Authorities (IOTA)

Center of Inter-American Tax Administrations (CIAT)

PROJECT AND PROCESS MANAGEMENT

In 2010, the Tax Authorities of the SR implemented projects of the UNITAS I

program under the supervision of the MF SR and which are arising from the Concept

of Tax and Customs Administration Reform, with a View of Unifying the Collection

of Taxes, Customs Duties and Insurance Contributions.

The Tax Authorities implement internal projects as well and in 2010 they were

targeted on ensuring a higher level of international exchange of information.

The Tax Directorate of the SR ensures as well activities associated with the preparation

and implementation of projects fi nanced by the European Union. In 2010, the Tax

Administration of the SR focused on implementation of two projects of the Operational

Programme “Employment and Social Inclusion” using the funds of the European Social Fund.

UNITAS I programme projects implemented at the Tax Authorities in 2010

Standard tax system,

Administrative information system,

Tax Authorities of the SR reform,

UNITAS I programme projects security,

Ensuring continuity, availability and recovery of IT services,

Balanced Business Score Card,

Project management,

e-Learning,

Process model,

Further training and education.

Internal projects implemented at the Tax Authorities in 2010

Introduction of a new system of VAT refund in the SR,

International exchange of information forms,

The use of international exchange of information.

Projects funded using the funds of the European Union in 2010

Under the Operational “Programme Employment and Social Inclusion”,

implementation of two separate projects funded from the European Social Fund

continued in 2010, namely:

Qualified employee of the Tax Administration – benefit for the whole

society – project Slovakia,

Qualified employee of the Tax Administration – benefit for the whole

society – project Bratislava,

Project “Republic of Macedonia” - strengthening the administrative capacity

of Public Revenue Office.

19

INFORMATION TECHNOLOGIES

The Tax Information System serves in supporting the Tax Administration in the

Slovak Republic and is one of the most important information systems operated within

the Slovak Republic. Requirements laid on a modern and eff ective administration of

taxes in the SR have the direct infl uence upon the Tax Information System in the SR.

The target status is to establish the Tax Administration capable apart from addressing

the everyday tasks by processing the tax related agenda also of ensuring that the

communication with taxpayers is simpler and more eff ective. The fi nal objective is to

improve the effi ciency and eff ectiveness of the Tax Administration of the SR.

Tax Administration information technologies are implemented in accordance

with the principle of information support for the institution aimed in particular on

the following:

complying with objectives set up in the SR Government Program Declaration,

complying with international obligations assumed by the Slovak Republic,

Directives and Enactments approved by EC and under international treaties,

abiding by local legal regulations (acts, enactments, resolutions),

complying with the Tax Administration and MF SR strategic plans,

providing the professional as well as general public with access to

information and relevant legal regulations in accordance with the

Constitution of the Slovak Republic.

The Tax Administration of the SR basic objective in the IT area is to ensure that

TIS may be effectively used for complying with strategic and reform plans of the

SR Government, the MF SR, the Tax Directorate of the SR, legislation changes in

required time limits and with required quality.

The Tax Administration of the SR mirrored the effects of global economic crisis

in 2010 which caused that the solution of requirements were relegated to the

background and the Tax Administration focused primarily following tasks:

providing the clients with more complex and higher quality services by providing

a higher comfort of services via the internet portal of Tax Administration,

innovation of the Tax Information System so it could flexibly respond to

changes in legislation,

preparation for development of a new information system based on

modern technologies,

providing for further development in the area of Tax Information System

related complementary projects especially in the area of international

exchange of information and simplified access of tax administrators to

complex information about taxpayers, their discipline or about their risk in

relation to a proper and timely tax compliance.

Tax Information System innovation steps are being implemented under the

program of UNITAS, carried out under management of the MF SR, the objective of which

is to provide for the reform of the Tax Administration and the Customs Administration

with a view of unifying of taxes, custom duties, and health, social and pension insurance

related contributions to funds. Based on objectives and decisions made by the Tax

Administration of the SR and the Program Committee and Management Council at the

MF SR, following activities were accomplished in the course of year 2010:

Modification of the Tax Administration of the Slovak Republic

IT services management

Improving the provision of IT services continued in 2010 as part of UNITAS

programme by implementing the internal project of the Tax Directorate of the SR named:

„Change of management of Tax Administration IT services“. The project implementation

in 2010 followed up previous activities related to defi ning and describing the processes

aimed at everyday activities related to the support of provided IT services. After the

trial operation the Management Processes changes have been put into the production

operation with HP Open View Service Center software tool support.

Administrative information system

During 2010 working activity was launched regarding the Administrative

information system for Tax Administration and MF SR. However the project has

been terminated after the change of top management of MF SR.

Process model

The Process model of the Tax Administration, which is used to develop and

upgrade the Tax Information System, training of new employees of the Tax

Administration and processes optimization, has been updated during 2010.

Standard tax system

In 2010, development of a new Tax Administration Information System has

been launched. Following steps were undertaken in 2010:

- present state analysis,

- preparation of the future state process model, i.e. state arising from the

adopted legislation,

- proposal of alternatives implementation of the Standard tax system into

production operation.

Tax Administration of the Slovak Republic Annual Report - 2010

Tax Directorate of the Slovak Republic20

INTERNAL AUDIT

The main task of the internal audit of the TD of the SR is by pointing to

deficiencies in activities of employees of Tax Authorities to contribute complying

with general binding legal regulations, internal organisational and management

decrees on all management levels. A part of its audit related activities in individual

areas of interest is to monitor the compliance of internal organisational and

management decrees with general binding legal regulations and subsequent to

file suggestions for their amendment.

In 2010, internal audit related activities focused on the legality of the

procedures of Tax Authorities, on resource management of TD SR and management

of state property, on compliance with the measures adopted by the management

personnel of the Tax Authorities to remedy deficiencies and their causes identified

during the internal audit and on investigation of external and internal motion or

petition submitted.

Part of the internal audit system and content of activities of the Internal Audit

Department is the handling of submitted petitions, investigation of complaints,

announcements and suggestions.

Results of audit activities

During 2010, 79 audits were launched and carried out pursuant the Act on

Control in State Administration and the Act on Financial Control and Internal Audit

of which 73 audits were also accomplished during 2010. According to the aim of

individual audits following audits have been carried out:

24 audits aimed to check the legality of procedures of tax offices and

regional branches of the Tax Directorate of the SR,

21 audits aimed to check the measures adopted by the management

personnel to remedy deficiencies and their causes identified during the

internal audit,

34 investigations were carried out based on external and internal motion

or petition submitted.

In 2010, out of the total number of launched audits, 57 % were planned audits, 37 %

were unplanned audits and 6 % were of combined type (planned and unplanned

audit). In 2010, the audits completed by protocol, i.e. with a finding, accounted for

70 % (in 2009 accounted for 72,7 % and in 2008 accounted for 72,3 %). However, a

significant change occurred when comparing results of unplanned audits. Out of

32 launched and completed audits 84.4 % were completed by protocol, i.e. with a

finding (compared to 52.2 % in 2009). An important part of unplanned audits were

audits aimed to verify the procedures of Tax Authorities at administrating taxes of

taxpayers suspected of fictitious trading with non-ferrous metals and to verify the

procedures of Tax Authorities when refunding overpayments on unregistered bank

accounts and private accounts of Tax Administration employees.

In 2010, there were 111 submissions received – as per sources of submissions,

a total of 50 submissions were submitted by individuals, 11 submissions were

submitted by representatives of legal entities, 44 submissions were anonymous

and 6 submissions were submitted by authorities carrying out investigation

and prosecution in criminal proceedings. During 2010, three submissions were

submitted referring directly at a particular employee of the TD SR.

The submissions pointed out most frequently to the following: suspicions of

illegal activity of taxpayers in the areas of illegal employment, fictive employment

contracts, non-taxation of occasional income, non-use of ECR, tax evasion, issue of

fictive accounting documents, violations of the Act on Accountancy.

21

HUMAN RESOURCES MANAGEMENT

In the area of human resources management, the priority objectives in 2010

included mainly the following:

Personnel changes arising from organisational changes of Internal Audit

Department, Economy and IT Section, Tax Audit and Tax Enforcement Section,

the implementation of planned educational programs,

implementation of the Social Program,

monitoring and evaluation of the employee turnover rate,

realisation of selection procedures.

Personnel (structure and number) overview of the Tax

Administration of the Slovak Republic

The State Budget indicators that are of binding character include also the Tax

Administration number of employees limited to 5,761 persons in 2010, out of which

the civil servants with permanent employment status account for 5,359 persons

and employees with employment granted in the public interest account for 402.

The State Budget binding indicator of employees limit has been duly complied with.

Working positions representing main types of Tax Administration activities are

occupied by 77 % of employees, out of which the positions of tax auditor and tax

administrator account for 81 %.

Other

23%

Auditor

29%

Administrator

33%

Tax distrainer

6%

State supervision

3%

Registrant

5%Administrator

1%

Social policy

In 2010, the social policy was based on the relevant provisions of the Civil

Service Act, Act on Work Carried out in Public Interest, Labour Code and Collective

Agreement entered between the TD SR and the Labour Union of Public Servants of

the TD SR Committee.

An appropriate amount of emphasis with respect to social policy was laid

predominantly to provide for the best working conditions for personnel, and in the

areas of catering, training, health-care and recreational care.

Tax Administration of the Slovak Republic Annual Report - 2010

Tax Directorate of the Slovak Republic22

TAX ADMINISTRATION PERSONNEL TRAINING

The Civil Service Act defines that the employing office is organizing and

providing for technical preparation and systematic technical training of the civil

servants and creates conditions for training of civil servants by deepening and

improving of his/her qualification training. The Act defines this process as systematic

vocational training intended for civil servants and is aimed on continuous keep up

and improvement of required knowledge and skills needed for the performance of

civil servant’s related duties within the respective area of civil service sector. The

employing office provides for deepening of qualification of the civil servant in the

extent of minimally 5 working days a year.

In 2010, the Tax Directorate of the SR provided staff training mainly with the

object to enhance the qualifications of civil servants and also with respect to the

economic situation comprising the following:

adaptive training,

continuous training,

specialised training,

training within the National project.

Adaptive training

Adaptive training mediates in the adaptation period information and knowledge

needed to perform civil service activities. The newly recruited employees accepted

into permanent civil service were provided with innovative adaptive training in the

period from 1st January 2010 to 31st December 2010.

91 newly recruited employees participated on the introductory training in

electronic form under the UNITAS program - e-Learning project.

68 newly recruited employees participated on the APV TIS functional training

which was conducted in personal attendance form for administrators, state revenue

accountants, registrars and auditors. The newly recruited employees were trained

by Tax School internal lecturers.

23

Training delivered within the National Project “Qualified

employee of the Tax Administration – benefit for the whole society“

Employees of the Tax Administration of the SR with support from the European

Social Fund under the operational programme Employment and Social Inclusion

participated in 2010 within the National Project “Qualified employee of the Tax

Administration - benefit for the whole society” in following educational activities:

1. International accounting standards IAS/IFRS

2. Transfer Pricing

3. ECDL

4. Human Resources Management

5. Language training - English Language

6. Economics and law

6. Economics and law

Continuous training

Within the continuous training and in accordance with the Framework Plan

of Training of Tax Authority Employees in 2010, operational plans of training, as

well as with tasks taken by the top management decisions, the Tax Administration

organised in 2010 altogether 68 training sessions. These training sessions were

cumulatively attended by 3,812 employees.

Specialised training

In 2010, altogether 5,134 employees took part on specialised training which

was targeted at IT related training covering following issues: the use of legal system

on the internet, information security, electronic forms, electronic auction, analytical

information system, secured electronic signature, information system for tax

auditors, EDP audit and SAP training, training in the area of personal development,

under which a communication training was organized for 40 internal trainers.

Tax Administration of the Slovak Republic Annual Report - 2010

![winprotocoldoc.blob.core.windows.net… · Web view · 2016-06-22[MS-DRSR]: Directory Replication Service (DRS) Remote Protocol. Intellectual Property Rights Notice for Open Specifications](https://static.fdocuments.in/doc/165x107/5aa927fb7f8b9a81188c6c77/web-view2016-06-22ms-drsr-directory-replication-service-drs-remote-protocol.jpg)