AJ Kinghorn Shava Mining Enterprise - Fossil Fuel · 2014. 7. 22. · 27 June 2014 AJ Kinghorn...

39

South African Energy Update – Eskom: A Company in distress, South Africa: A Country in distress 27 June 2014 AJ Kinghorn Shava Mining Enterprise Tel: +27837011388 e-mail: [email protected] JCMV 9 1

Transcript of AJ Kinghorn Shava Mining Enterprise - Fossil Fuel · 2014. 7. 22. · 27 June 2014 AJ Kinghorn...

South African Energy Update – Eskom: A Company in distress, South Africa: A Country in distress

27 June 2014

AJ KinghornShava Mining Enterprise

Tel: +27837011388e-mail: [email protected]

JCMV 9

1

Coal’s Current Value Proposition

∗ The economic contribution of coal mining as follows: 19% of mineral exports by value, 7% of total merchandise exports, 21 % of liquid fuel production, and 91% of electricity generation capacity.

2 Source: Dick Kruger of the Chamber of Mines of SA, 10 March 2014 and DMR Public Mining Data

Coal’s Statistics 1

3 Source DMR Public Mining Data

Coal’s Labour and Fatalities

4 DMR Public Mining Data

Funding still an issue for miners, especially juniors

5

The Coal Road Map and the NPC (Vision)∗ Certain developments in 2011 have been very relevant for the coal industry in South Africa. The

electricity plan for the country to 2030 (the IRP2010) was recently promulgated in the absence of anymaster energy plan for the country. The National Climate Change response strategy green paper hasgiven a clear indication of government’s commitment to reduce carbon emissions from industry.Significantly, the National Planning Commission (NPC) expressed the following view on coal:

∗ “While most of South Africa’s energy comes from coal, it is striking that government has no integratedcoal policy. South Africa ranks fifth internationally as a coal producer and exporter, yet government hasno clear export strategy. There is also no integrated development of mining, rail and port infrastructureto facilitate either exports or anticipated increases in local production and consumption, withinacceptable environmental constraints.

∗ The private sector has initiated work on a Coal Road Map. Government needs to be an active partner”(NPC, 2011:18)

∗ It is thus important that South Africa maximises the value to society from the production and use of coalwhile at the same time minimising any negative impacts.

∗ Challenges include water, infrastructure, investment and institutional constraints. Infrastructure iscritical to the future of the coal sector - Transport infrastructure, particularly land-based transport, is akey determinant of the evolution of the coal sector. This is particularly important if the Mpumalanga,Waterberg and other coalfields are to be further exploited. The New Growth Path prioritises (amongother things) infrastructure development and increased mineral extraction and beneficiation within theoverarching goal of creating inclusive and high job rich growth (New Growth Path: Executive Summary2010).

6

Strategy is about making choices…

“Strategy means making clear-cut choices about how

to compete”~ Jack Welsch

7

Clem Sunter points to three potential courses for South Africa

none of the ducks in a rowall the ducks in a row

the failed state

To provide potential courses?

Energy Security – Post election State of the Nation address ∗ President Zuma promised to respond “decisively to the country’s energy

constraints in order to create a conducive environment for growth”.∗ “We will also need to identify innovative approaches to fast-track

procurement and delivery by government in the energy sector.”∗ To prepare the institutional capacity for such a change, government would

convert the National Nuclear and Energy Executive Coordinating Committeeinto the Energy Security Cabinet subcommittee.

∗ “There are also some urgent activities that we are engaging in, in the shortterm. Progress at Medupi power station construction site will be accelerated.Plans on the financing of the next large coal-fired power station, Coal 3, willbe speeded up so that the procurement process can commence.”

∗ But the President also gave his backing to the passing of the much-delayedIndependent System Market Operator Bill, which some view as key toopening up the electricity market to independent power producers.

9

Energy constraints more troublesome than platinum strike – Free Market Foundation FMF∗ South Africa’s economy was 13%, or R366-billion, smaller than it would have

been had energy supply been stable, and loadshedding and forced lowerenergy use by industry did not occur.

∗ The loss to the economy – which was estimated at the “lower end of thescale” – was a result of a failed energy policy, he noted, adding that: “Noenergy means no growth, and energy insecurity is actually an energycatastrophe.

∗ “We have a failed monopoly, but its not Eskom’s fault,” Louw said, explainingthat the parastatal had been a “victim” of government’s failure toimplement strategic policies aimed at introducing competition and dividingEskom’s assets.

∗ “We have a failed monopoly, but its not Eskom’s fault,” Louw said, explainingthat the parastatal had been a “victim” of government’s failure toimplement strategic policies aimed at introducing competition and dividingEskom’s assets.

10

Brazil - Rio de Janerio at night

11

Johannesburg, South Africa at night - sorry ...... Eskom apologises

12

∗ Speaking at a state-of-the-system update in Johannesburg on Tuesday, Public Enterprises Minister Malusi Gigaba said discussions were under way between the Department of Public Enterprises, the Department of Energy, the National Treasury and Eskom, but he indicated that announcements would only be made once solutions had been found and did not provide specific timeframes.

∗ Eskom had been granted yearly increases of 8% between April 1, 2013, and March 31, 2018, as opposed to the 16% sought, which translated into allowable revenue for the period of R862-billion, rather than the nearly R1.1-trillion requested – a R225-billion financial gap

∗ Gigaba stressed that government was aware of the disruptive economic consequences of South Africa’s power constraints, which led Eskom to issue two power emergencies in late February.

Eskom’s precarious financial position 1

Source: Creamer 26 Feb 201413

∗ Eskom has had to run its emergency reserves – 2426 MW of diesel powered open-cycle gas turbines (OCGTs) in the Western Cape – for extended periods. The R2-billion budgeted by Eskom for diesel fuel in the financial year ending 31 March 2014 has risen to R10-billion, resulting in a cash-flow crisis which the utility claims is affecting other necessary capital and operational expenditure.

Eskom’s precarious financial position 2

Source: Creamer 26 Feb 201414

∗ State-owned electricity utility Eskom will issue a tender soon for the procurement of an additional 500 MW of capacity from private generators, as part of a larger intervention to ensure supply security ahead of the introduction of new capacity from the Medupi, Kusile and Ingula projects

∗ The utility remained under major financial stress and would, thus, also need to consider the best way of funding the new capacity, while also ensuring the purchases were affordable. For this reason, volume and price caps could be included in the contracts.

∗ However, when compared with the cost of operating the open-cycle gas turbines (OCGT), Lennon was convinced that the National Energy Regulator of South Africa would view the additional IPP costs as having been “prudently incurred” – Eskom would then be entitled to use the Regulatory Clearing Account mechanism to recoup the expenses.

Eskom’s precarious financial position -Prudent expense?

Source: Creamer Feb and June 201415

∗ Eskom’s cents/kWh tariff has more than tripled from 20 c/kWh in 2003to >70c/kwh in 2014. (compared with an average price of 212 c/kwh forIndependent Power Producers (IPP) in 2013), and this price is expectedto double in the next five years. So, not only does South Africa face acoal cliff, but also has a cost cliff to contend with.

∗ It is important to note that most municipalities charge a 100% mark upwhich means that we are paying ~140c/kwh at home and at work inGauteng.

Eskom tariffs– the cost cliff 1

16

Eskom Wholesale electricity pricing system (WEPS) Note: this excludes the Municipality Margin (100%)

Source: 21314 Tariffbook (Eskom) 17

South Africa’s electricity prices rise to high end of China and India. NB: This not including a Carbon Tax

~R0.50/kWh

~R0.75/kWh

• China and India Prices by Frost and Sullivan

• RSA historic Price path Eskom• IRP Prices by DoEIRP TTT

Area of Industrial Prices China & India

Area of IRP 2010 Comparative Prices for South Africa

SA “energy gap”

Average Industrial Prices (2009 REAL)

Source: Subject concepts and issue outline, M Rossouw and R Baxter 2011

~R0.98/kWh

18

NERSA only granted Eskom an 8%

increase

The price that Eskom needs to stay in

business?

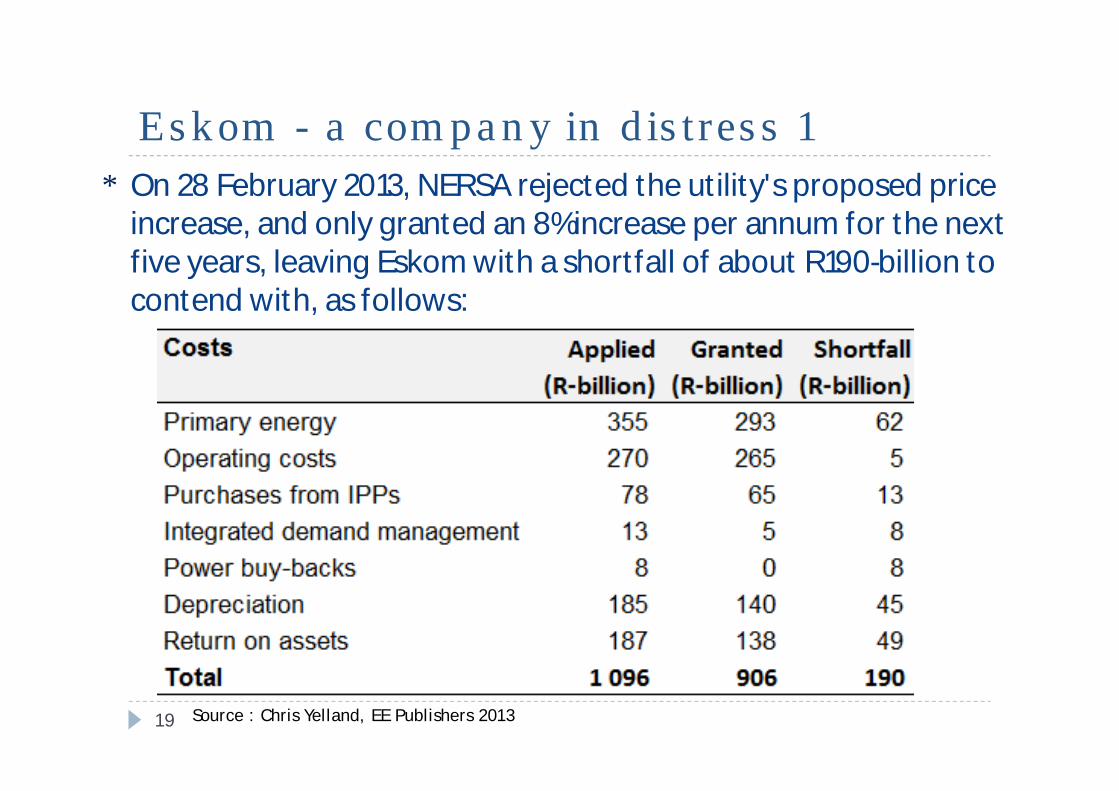

∗ On 28 February 2013, NERSA rejected the utility's proposed price increase, and only granted an 8% increase per annum for the next five years, leaving Eskom with a shortfall of about R190-billion to contend with, as follows:

Eskom - a company in distress 1

Source : Chris Yelland, EE Publishers 201319

∗ On 13 April 2014 the Sunday times quoted the Eskom spokesman Andrew Etzinger - “NERSA’s decision resulted in a R225 billion revenue shortfall for Eskom over the five years.”

∗ No breakdown of the R225 billion was provided.∗ We still have four more years to go to get to a final number. ∗ Eskom's only solution is to increase the price!

Eskom - a company in distress 2

Source : Sunday Times 201420

Minister of Public Enterprises

21

∗ The Honourable Lynne Brown promises swiftaction on Eskom sustainability and a newCEO.

∗ Eskom has stressed that interim CEO CollinMatjila has no aspiration to succeed BrianDames.

∗ On 09 June when she was interviewed on the702 talk show – She said all the “right things”.

∗ Will she be able to, or more importantly willshe be allowed to introduce corporategovernance and accountability?

Eskom Leadership – has the flame been extinguished?

22

Eskom Leadership - Controversy over acting Eskom CEO snowballs

23

∗ Mr Matjila is now in charge of Eskom, after the power utility’s board appointed him on April 1 to run the company until a new CEO had been employed. But the controversy surrounding Mr Matjila’s tenure at Kopano shows no sign of abating.

∗ ACTING Eskom CEO Collin Matjila had been asked to provide an explanation to the Congress of South African Trade Unions (Cosatu) over the suspicious flow of money to him and other employees of the trade union federation’s investment arm, Kopano ke Matla, but he left his post at the end of last month without doing so and without giving notice.

∗ When Mr Matjila was CEO of Kopano ke Matla, investment arm of the Congress of South African Trade Unions (Cosatu), the company was involved in all sorts of dubious shenanigans that resulted in an investigation by the regulator, the Financial Services Board (FSB). And Mr Matjila did not come out of it smelling good at all.

∗ The FSB report uncovered an “unusual and suspicious” payment of R1.33m to a company related to Mr Matjila called Summerlane. In addition, it found there had been all sorts of other shady dealings involving apparent fraud, corruption and money laundering in which both Kopano and Mr Matjila were implicated.

∗ Meanwhile, it has emerged that Mr Matjila was not the first choice for the interim CEO position, but the board opted for him after Public Enterprises Minister Malusi Gigaba rejected its preferred candidate. The board had wanted to bring in Eskom executive Steve Lennon, head of the renewable energy division, a month before Brian Dames’ departure, said several sources at Eskom and in the energy sector.

Source: Business Day, 9 Apr 2014

Clem Sunter points to three potential courses for South Africa

none of the ducks in a rowall the ducks in a row

the failed state

To provide potential courses?

THE DOMESTIC vs EXPORT DEBATE

25

Should coal be declared a strategic resource?

SA Coal Resources and Reserves

?

26

∗ It is too late for South Africa to prevent national debt reaching 44% of GDP within the next two years, finance director general Lungisa Fuzile said in early 2014.

∗ "We are too close to 2016," he said after a Treasury briefing to Parliament's finance committees, a day after Minister Pravin Gordhan tabled the 2014/15 budget.

∗ National debt had risen from a low of 27.3% of GDP in 2008/09 to 41.8% in 2012/13.

∗ Fitch estimated that general government debt had increased to 48% of GDP at end-2013, from 27% in 2008.

Too late to avert 44% debt – Treasury

27

∗ Widespread surprise, mixed with a good deal of concern, greeted news of Tina Joemat-Pettersson’s appointment as South Africa’s new Energy Minister – she replaces Dikobe Ben Martins, who himself only took up the position from Dipuo Peters following a Cabinet reshuffle in July last year.

∗ President Jacob Zuma moved Joemat-Pettersson from Agriculture, Forestry and Fisheries, where she had a relatively controversial tenure, having been found by the Public Protector to have behaved improperly in the management of a R800-million State fishery-vessels tender – a finding she is contesting.

∗ The final IEP will be published by March 2015, at the latest.

The energy minister

28

The coal cliff

29

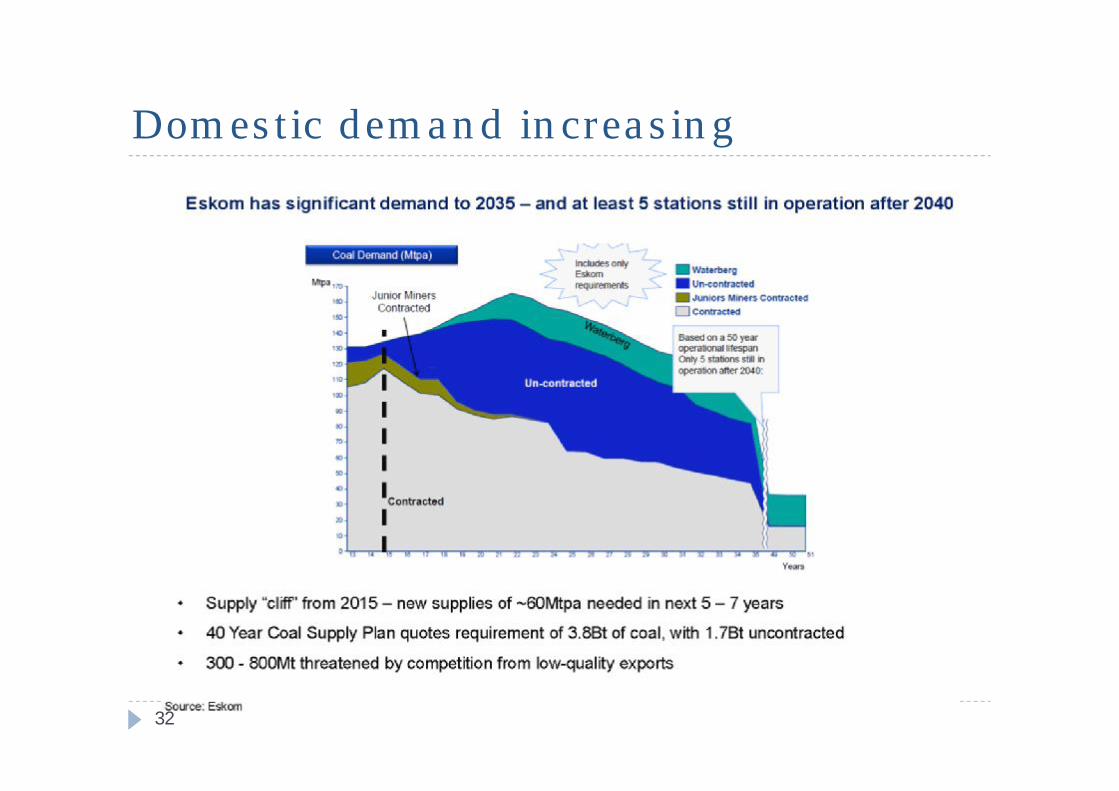

∗ South Africa is facing a dramatic power crisis, exacerbated largely by the looming coal cliff. The size of the coal cliff ranges from 60 – 120Mt and is expected to impact on the country between 2013 and 2019.

∗ This cliff refers to either an overhang (over supply of coal but no power station to use it) or underhang (under supply of coal with power station empty). Of the four billion tonnes of coal that Eskom needs over the next 40 years, two billion tonnes will have to come from new sources (coal mines).

∗ At this stage we are only considering the coal cliff from a volume perspective. However, if coal qualities are included as another parameter, the size of the cliff increases.

Immediate actions required 1

Source: SA Coal Roadmap 201330

Immediate actions required 2

Source: Cramer June 201431

∗ The Mining Charter requirement for 26% black economic-empowerment (BEE) shareholding and Eskom’s requirement that a portion of its coal be secured from black-controlled mining enterprises – mining enterprises that are 50% plus one share black- controlled means that there is an immediate need to start developing an emerging black junior coal mining sector in South Africa to help secure part of the coal needed by the power utility going forward.

∗ The South African Roadmap illustrates that a typical new mine supplying a power station with ten-million tons a year of coal would thus require an initial capital investment in the order of R10-billion to R15-billion. In other words, meeting Eskom’s projected requirement of 60-million tons a year of new coal will, therefore, require investment of between R60-billion and R90-billion for the construction of at least ten new mines.

Domestic demand increasing

32

Eskom’s Infrastructure Programme

Source: Eskom Mining Indaba 201333

∗ Eskom’s Medupi Power station was due to be commissioned in 2011.However, due to the delay in construction of Medupi, the first set ofMedupi boilers is only due to come on line late this year (2014) at a“guestimated” cost of nearly R200 billion (B) - against an original targetof R50 B. This particular cliff has had three negative impacts. Firstly,Eskom was not able to meet its supply requirements which has led to“load shedding” in the smelter sector. Secondly, there is an R8 B buy-back option which was rejected by NERSA. Thirdly, and most damaging,with demand significantly exceeding supply, Eskom is avoidinguncontrolled black-outs only by running its diesel-driven open-cycle gasturbines (OCGTs) flat-out at enormous cost, while simultaneouslyengaging in demand management and controlled load-shedding byexercising its interruptible contracts to large customers such as BHPBilliton, paying large energy-intensive industrial users such asferrochrome smelters to shut down, and urging consumers to switch offeverything possible.

Eskom capital expenditure – the cost cliff 1

34

∗ In August 2013, Trade and Industry Minister, Rob Davies, announcedcabinet approval of the building of a third coal-fired power station byEskom, although timelines, schedules and costs have yet to beapproved. This decision was taken based on Eskom spendingapproximately R240 B on the Medupi and Kusile power stations — thelion’s share of a R300 B budget to expand its generation capacity overten years. The construction of both stations has already been delayed bythree years (and counting). If the more accepted guestimate of a cost ofR400 B for the two power stations proves to be correct, where will theadditional R160 B needed for the completion of the two power stationsstation come from?

Eskom capital expenditure – the cost cliff 2

35

∗ It looks like Russia will be able to build an 8,000MW plant for less than Medupi which is4,800WM!!!

∗ Russia's Inter RAO might build the world's largest coal-fired power plant to sell electricityto China in a sign of strengthening bilateral economic and political ties. Chairman BorisKovalchuk told reporters the Russian power monopoly would examine the cost andtimetable required to build the 8-gigawatt plant, which would use coal from theErkovetskaya deposit in the Amur region in Russia's Far East. The announcement follows ahistoric $400 billion agreement to sell Russian natural gas to China for the next 30 years.Russia , a leading producer of oil and gas, wants to diversify its energy exports away fromits core European market. Inter RAO already supplies China with electricity. A subsidiary,East Energy Co, last year increased electricity exports to China by 33 percent to 3.5 billionkilowatt hours. Kovalchuk said that Inter RAO is looking for a loan from China to build theplant. Analysts have estimated it would cost about $12 billion to build. "If our Chinesepartners could make enough of the cheap money they have available, this would of courseimprove the economics of the project," Kovalchuk said. He said that State-owned ChinaHuaneng Group Corp , with which Inter RAO signed a cooperation deal last week, mightparticipate in the project. China regularly faces power shortages during peak consumptionperiods as a result of surging coal prices and coal supply bottlenecks as well astransmission constraints. "We want them to take part in it," Kovalchuk said, adding thatthe Chinese badly need electricity from Russia and want to build plants abroad to helpreduce air pollution.

Major Russian utility may supply China by building coal-fired power plant - R120 billion for an 8-gigawatt plant

36

∗ How long will Eskom continue being an albatross around the taxpayers’necks? When will the public, faced with ever increasing electricity costs,blackouts, and clear examples of management ineptitude, finally say‘enough is enough’? Clarity and transparency is urgently needed fromPublic Enterprises Minister Lynne Brown as to her strategy goingforward.

∗ With the government and its SOEs being so closely intertwined, it isdifficult to point fingers solely at either party.

The Albatross

37

Ten years to fix∗ Eskom CEO Brian Dames said South Africa was still feeling the

repercussions of the ANC government's decision not to build new plantswhen asked by the utility to do so in 1998. Construction of Medupi onlystarted in 2007 and has been plagued by delays related to design flawsand labour unrest.

∗ "It will take 10 years to fix the 1998 problem," said Dames.∗ Dames said the supply and demand relief measures had been identified

and were well known, but that key decisions were now needed toliberate the financial resources required for implementation.

∗ And after the 2008 debacle, the government realises it could pay aheavy price if it does not decide in time on the next phase of powerconstruction when Medupi and Kusile are complete.

∗ Where will the power come from in 2020?

38 March 2014

∗ Eskom’s credibility with operational time frames has been tested andfound wanting, and the way forward remains clouded in uncertainty,half-truths and indecision. Until government accepts accountability forEskom’s failure to provide the country with an adequate, and cost-effective, power supply, and long-term viable solutions are proposedand put into practice, South Africa will stagnate.

∗ Bad planning, a lack of transparency, poor management, unrealisticeconomic solutions and a lack of political will surrounding our nationalenergy planning can only serve to worsen the current power crisis,throwing Clem Sunter’s scenarios into stark relief.

Summary

39