Airo International Research Journal June, 2016 Volume VII ... · numerous people apply for home...

18

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714 1 | Page

Transcript of Airo International Research Journal June, 2016 Volume VII ... · numerous people apply for home...

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

1 | P a g e

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

2 | P a g e

COMPARATIVE STUDY OF HOUSING FINANCE OFFERED BY PUBLIC AND PRIVATE

SECTOR BANKS

Shivani Sharma

Abstract

This paper was an attempt to comparative analyzes the jousting finance offered by public and private

sector banks. Purchasing the house of your dreams is not an easy task. House loan means that you

buy a house on installments. Housing or shelter is the basic need of human being. This is accepted by

the civilized society. Housing is an enigma to the developing countries; it is simultaneously the

hardest problem to solve the social housing schemes. After 1990s all public sector banks were

struggling with NPA problem. The housing shortage is increasing day by day as a proportion to the

massive increase in population. Today, there are more than 350 housing finance companies

registered with the registrar of companies of these 29 have been approved by NHB for financial

assistance. The research examined the satisfaction level and problems faced by customers while

availing home loan. For this purpose we have taken four commercial banks in namely PNB, Central

Bank of India, HDFC Bank and ICICI Bank. It includes two public sector banks and two private

sector banks. In the research methodology a sample size of 100 respondents has been taken through

random sampling. For the study, researcher has collected both primary data as well as secondary

data. Finally the whole research was carried out in a systematic way to reach at exact result.

INTRODUCTION

Housing Finance is a broad topic, the concept

of which can vary across continents, regions

and countries, particularly in terms of the

areas it covers. Housing does not mean the

construction of a shelter only, a shelter to

protect way from the inclemency‟s of weather.

They channel human relationship and are an

integral part of the society. Attractive

packages and flexibilities in housing loan

Schemes. “Put simply, housing finance is what

allows for the production and consumption of

housing. It refers to the money we use to build

and maintain the nation‟s housing stock. But it

also refers to the money we need to pay for it,

in the form of rents, mortgage loans and

repayments.” Housing Finance brings

together complex and multi-sector issues that

are driven by constantly changing local

features, such as a country‟s legal environment

or culture, economic makeup, regulatory

environment, or political system.

The term “Housing Loans” or “Housing

Finance “means finance for buying or

modifying a property. Hence “Housing

Finance” maybe defined as the financial

resources for an individual or a group of

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

3 | P a g e

persons used facially for the purpose of

housing.

HOUSE LOAN-

Home loans are loans you have access to,

depending on whether you want to buy or

build a house and can also be used to repair or

extend an existing house. Home Loans are an

attractive and popular means of buying a

dream house for most people. In India, the

demand for home loans has increased

manifold in the last decade. Every day

numerous people apply for home loans to own

a perfect abode for themselves. The fact that

home loans come with added advantage (like

tax benefits) is the icing on the cake.

DIFFERENT TYPES OF HOME LOANS

IN INDIA-

Home purchase loans:

These are the basic home loans for the

purchase of new home.

Home improvement loans:

These loans are given for implementation

repair works & renovation in a home that has

already been purchased by the client.

Home construction loans:

These are available for the construction of

new home.

Home extension loans:

These are given for expanding or extending

an existing home for e.g.: addition of an

extra room etc.

Home conversion loan:

This is for those who have financed the

present home with home loan & wish to

purchase& move to another home for which

some extra funds are required through home

on version loan ,existing loan is transferred

to the new home including the extra amount

required eliminating the pre payment of the

previous loan.

Land Purchase loans:

This loan is available for the purchasing of

land for both construction and investment

purpose. Almost all leading banks offer this

loan like ICICI Bank (Land Loan), Axis

bank (Loan for Land Purchase).

Bridge loan:

These are designed for those people who

wish to sell the existing home & purchase

another one. The bridge loan help finance the

new home, until a buyer is found for the old

home.

Refinance Loans:

These loans help you to pay off the debt you

have incurred from private sources such as

relatives and friends, for the purchase of

your present home.

HOUSING FINANCE INSTITUTIONS IN

INDIA

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

4 | P a g e

At present housing finance market has a keen

competition, among the public sector housing

finance companies, private sector housing

companies and banks. Housing Finance is an

important element of housing policies

persuaded by‟ the Governments of developed

and developing countries of the world. In

India the flow of credit into the housing sector

comes from two sources that is formal and

informal sectors. According to Dr. Rangarajan

Committee Report in the year 1987, the formal

sector has been boom in the financial markets.

The major housing financial institutions

meeting housing finance in India are as

follows:

(i) Scheduled Commercial Banks:

The Indian Mortgage Market has been

growing at around 18 percent in the fiscal year

2010-11 owing to enabling factors such as a

stable operating environment, buoyant

property prices etc. The share of Banks can be

attributed to extensive network and broad

customer base, access testable low-cost funds

and other regulatory mandates.

(a) Public sector banks: SBI, PNB, Bank of

Baroda, Dena Bank, Bank of India. Allahabad

Bank, OBC etc.

(b)Private sector banks: HDFC, ICICI Bank,

Axis Bank, IDBI, ING Vysya Bank etc.

(c)Foreign Banks: Standard Charted Bank,

City Bank, HSBC etc.

(ii) Housing Finance Companies:

Housing Finance Companies (specialized

institutions lending for housing) registered

with the National Housing Bank are a major

component of the mortgage lending

institutions in India. HFCs are regulated and

supervised by National Housing Bank under

the provisions of the National Housing Bank

Act, 1987 and the directions and guidelines

issued there under from time to time. The

regulatory measures include prudential norms,

transparent and standardized accounting and

disclosure policies, fair practice code, asset

liability management and other risk

management practices etc. DHFL, HDFC

GRUH, India bulls Housing Finance,

Sundaram BNP Paribas etc.

(iii) Insurance companies:

Insurance companies are another form of

housing financing institution, LIC Housing

finance is another major player in housing

sector in India with about 8% of market share.

Promoted by Life Insurance Corporation of

India, LICHFL has an extensive distribution

network with a strong brand presence. Other

insurance companies providing housing

finance is GIC Housing

Finance, New India assurance, National

Insurance, ICICI Lombard , TATA AIG, Bajaj

Allianz etc.

(iv) Micro Finance Institutions:

Microfinance Institutions or Non-

Governmental Organizations who are present

locally and have a bottom participative

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

5 | P a g e

approach are making various efforts to cater to

the housing finance needs of the low income

segments of the society. The MFIs work on

the model of SHGs linked with Banks. The

National Housing Bank has recognized the

penetration of Housing Micro Finance

Institutions as delivery mechanisms for

channelizing housing finance to the un-served

sections of society and accordingly developed

a suitable Housing Microfinance Programme

to cater to the needs of this section.

(v) Developmental Financial Institutions:

HUDCO, SIDBI, NA-BARD, Apex Housing

cooperative society, State Cooperative

agriculture and Rural Banks etc., Development

Finance Institutions (DFIs) have mainly

catered to the medium to long-term financing

requirements. Industrial Finance Corporation

of India (IFCI) was the first DFI which was

established to extend long-term finance to

industry. Industrial Investment Bank of India

(IIBI) Ltd, Export-Import Bank of India

(EXIM) and Tourism Finance Corporation of

India (TFCI) Ltd which provide long-term

finance to various sectors; and ii) refinance

institutions such as National Bank for

Agriculture and Rural Development

(NABARD), Small Industries Development

Bank of India (SIDBI) and National Housing

Bank (NHB) which pro-vide finance to

banking as well as non-banking financial

intermediaries.

For achieving the objectives, the researcher

has taken four commercial banks in namely

PNB, Central Bank of India, HDFC Bank and

ICICI Bank. It includes two public sector

banks and two private sector banks.

LITERATURE REVIEW

La cour Micheal (2006) examined the home

purchase mortgage product preferences of

LMI households. Objectives of his study were

to analysis the factors that determined their

choice of mortgage product. The role pricing

and product substitution play in this segment

of the market and to verify whether results

vary when loans are originated through

mortgage brokers. In this case regression

analysis has been used and results have shown

that high interest risk reduces loan value.

Singh and Sharma (2006), in their study on

Housing finance in India –LIC housing

finance limited examined the development of

housing finance in India. The study was based

on the case study of LIC Housing Finance

Limited. From time to time the government

introduces a number of loan schemes for the

development of housing finance system in

rural and urban areas. Half of the population

of India lives in slums and shabby shelters in

rural areas. As per the development of housing

finance the National Housing Policy (NHP),

was introduced in 1988 and the NHB was set

up in 1988 as an apex institution for housing

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

6 | P a g e

finance and a wholly-owned subsidiary of

RBI.

B. Satish Kumar (2008), in his article on an

evaluation of the financial performance of

Indian private sector banks wrote Private

sector banks play an important role in

development of Indian economy. After

liberalization the banking industry underwent

major changes. The economic reforms totally

have changed the banking sector. RBI

permitted new banks to be started in the

private sector as per the recommendation of

Narsimha committee. The Indian banking

industry was dominated by public sector

banks. But now the situations have changed

new generation banks with used of technology

and professional management has gained a

reasonable position in the banking industry.

Kajal Choudhary and Monika Sharma

(June, 2011), in their study on Performance

of Indian Public Sector Banks and Private

Sector Banks: A Comparative Study,

mentioned that The economic reforms in India

started in early nineties, but their outcome is

visible now. Increased competition, new

information technologies and thereby

declining processing costs, the erosion of

product and geographic boundaries, and less

restrictive governmental regulations have all

played a major role for Public Sector Banks in

India to forcefully compete with Private and

Foreign Banks. This paper was an attempt to

analyze how efficiently Public and Private

sector banks have been managing and they

focuses on taking suitable & stringent

measures to get rid of NPA problem. They

also mentioned that bank staff involved in

sanctioning the advances should be trained

about the proper documentation and charge of

securities and motivated to take measures in

preventing advances turning into NPA. Public

banks must pay attention on their functioning

to compete private banks. Banks should be

well versed in proper selection of

borrower/project and in analyzing the financial

statement.

Dr. P.S. Ravindra (2013), in their study on

“Operational and Financial Performance

Evaluation of Housing” has evaluated the

operational performance of LIC Housing

finance Limited and HDFC. Top housing

finance companies such as HDFC, LIC

Housing Finance witnessed loan book growth

of 22-37 per cent during the year ended March

2012, thereby increasing their market share. It

was concluded that the success of the LICHFL

and HDFC in the housing finance industry is

in its marketing network. They have more

number of marketing personnel than the

regular office staff. Even though, these two

housing agencies are good in sanctioning loan

disbursal and delivery of service to the

customers, they have to modify and

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

7 | P a g e

differentiate their services from other financial

companies, which assure maximum benefit to

the customers.

Dr. Anand Kumar (2016), in his research on

“Growth and Impact of Housing Finance

on Indian Economy” concluded that the

housing sector contributes directly to overall

production activities of the economy like job

growth, tax revenue, wages, and the benefits

of shelter and wealth accumulation for

households. The housing sector is very

important for both local and national

economy. The results show that there is

significant great relationship between Housing

finance sector and employment.

Dr. Amit S. Nanwani (2016), in his research

on “A Comparative Study of Home Loans

Offered by Public and Private Sector Banks

in Nagpur District” concluded that both

public sector and private sector banks truly

deserve to be the leading banks in home loan

sector. Mostly people prefers public sector

banks for home loans, especially because they

believe that it is more secure bank and interest

rate is lower. It was found that private sector

banks are very popular among the customers

these days. The satisfaction level that

customer have with these banks is very high in

comparison to public sector banks. Customer

are associated with banks for many services

that they require on regular basis and people

tend to prefer banks which provide better

facilities and convenient banking. From the

overall analysis it can be said that the

satisfaction level in relation to the services

provided by private sector banks are very high

as compared to public sector banks.

OBJECTIVES OF THE STUDY

1. To study and compare the home loan

schemes offered by the Public Sector Banks

i.e. PNB,

Central Bank of India and Private Sector

Banks i.e. ICICI, HDFC.

2. To study marketing strategies of public &

private sector banks in housing Finance.

3. To study the customer‟s response regarding

the housing loans facility of the selected

banks.

SCOPE OF THE STUDY

The scope of the study involved getting

knowledge about the house loan schemes

offered by the Public Sector Banks & Private

Sector Banks and, also assess the problems of

the customers which they face at the time of

obtaining home loans & along with that

analyze the satisfaction level of the customers

while they deal with bank whether it is a

Private Bank or a Public Bank. The major part

of the study focused on making comparative

evaluation of the house loan schemes offered

by both private sector banks and public sector

banks. The scope of the study is limited to

Karnal, Kurukshetra, and Ambala.

JUSTIFICATION OF THE STUDY

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

8 | P a g e

Literature revealed that not much research

work has been done in the area of housing

finance provided by various types of bank

from the customer‟s point of view, So the

study has been undertaken in some of the

cities to know about the satisfaction level and

problems of the customers in availing housing

finance along with that the different schemes

offered by the public and private banks. The

approach of the study was to get a deep insight

into the industry through a study which would

include all the details about the housing

finance, how many customers are aware of

housing finance schemes offered, how they get

informed about these, how they perceived it as

an effect of the offered schemes on the

satisfaction level of the bank customers. So,

two Public sector banks i.e. Punjab National

Bank & Central Bank of India and two Private

sector banks i.e. ICICI Bank & HDFC Banks

have been selected so that a comparative

analysis can be undertaken.

RESEARCH METHODOLOGY

For the study I have collected both primary

data as well as secondary data. The primary

data has been collected through the responses

of the customers through structured

questionnaires to check the satisfaction level

of customers about the home loan schemes

and their providers. In secondary data, the

annual reports of RBI, commercial banks and

broachers of these banks, articles published in

magazines, journals and newspapers have

been studied.

Sources of Data Collection-Primary data

source as well as Secondary data source.

Sample Size

The research was conducted on the sample of

100 respondents. Professionals, Bank

employees & other category people i.e. people

seeking home loans were selected for the

survey.

Sample Area

Karnal, Kurukshetra & Ambala

SAMPLING TECHNIQUE

The selection of the respondents was done on

the basis of convenience sampling.

RESEARCH TOOLS

Tools of analysis:-Analytical techniques have

been used to obtain findings and arrange

information in a logical sequence from the

data collected. After tabulation of the data,

researcher used the following quantitative

techniques:

PERCENTAGE ANALYSIS-

The data that is obtained from the

questionnaire is analyzed through percentage

Analysis.

The results are shown on the percentage basis.

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

9 | P a g e

GRAPHS- Graphical representations are used to show the

results in simple form.

DATA ANALYSIS AND INTERPRETATION

SCHEMES OFFERED BY PNB, CNTRAL BANK OF INDIA, HDFC and ICICI BANK-

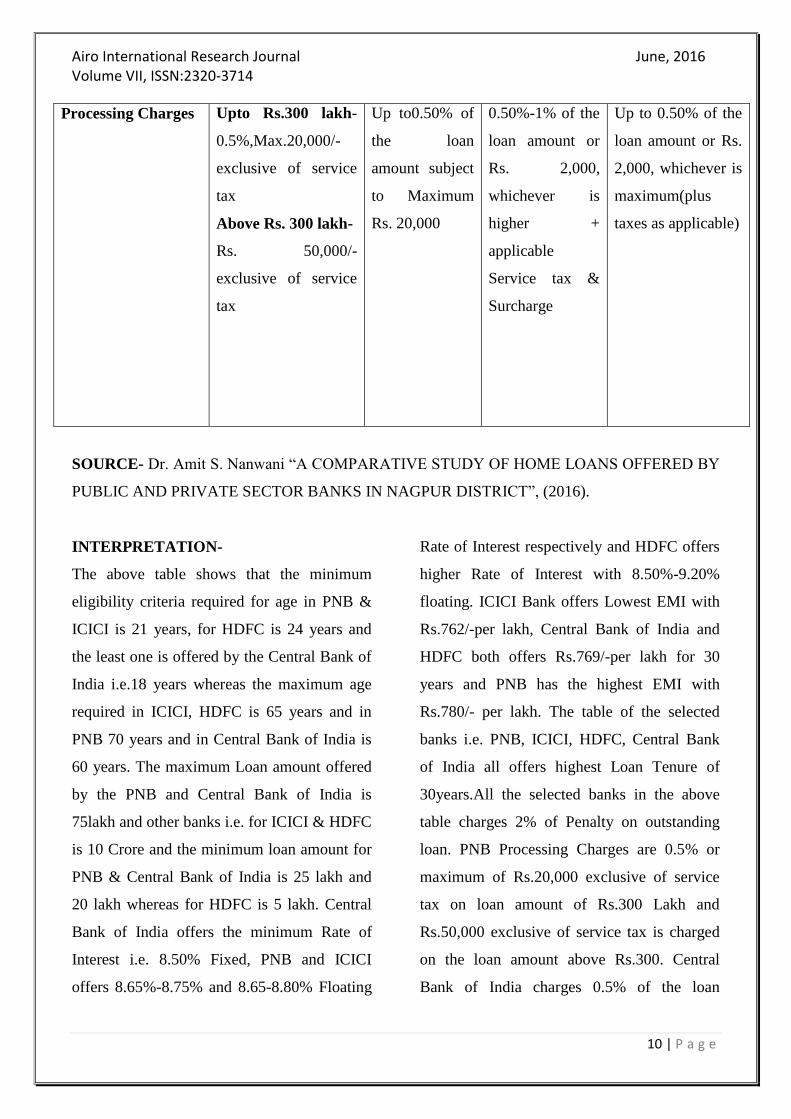

TABLE - CRITERIA FOR AVAILING HOME LOAN FACILITY BY SELECTED BANKS

BASIS PNB CENTRAL

BANK OF

INDIA

ICICI HDFC

Eligibility Min. Age-21years

Max. Age-70 years

(65yr for

professional)

Min. Age-

18years

Max. Age-60

years

Min. Age-

21years

Max. Age-

65years (60

years for

salaried)

Min. Age- 24 years

Max. Age-65years

(60years for

salaried)

Maximum Loan

Amount

25 lakh-75 Lakh 20 Lakh-75

Lakh

Up to 10crore 5 Lakh-10Crore

Rate of Interest 8.65%-8.75%

Floating

8.50% Fixed 8.65%-8.80%

Floating

8.5%-9.20%

Floating

Lowest EMI Rs. 780/- per lakh Rs. 769/- per

lakh for 30

years

Rs.762/- per lakh Rs.769/- per lakh

for 30 years

Loan Tenure 30 Years or 70 years

of age, whichever is

earlier

30 Years 30 Years 1 Year to 30 Years

Penalty 2%for outstanding

loan amount

2% 2% 2% for outstanding

loan amount

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

10 | P a g e

Processing Charges Upto Rs.300 lakh-

0.5%,Max.20,000/-

exclusive of service

tax

Above Rs. 300 lakh-

Rs. 50,000/-

exclusive of service

tax

Up to0.50% of

the loan

amount subject

to Maximum

Rs. 20,000

0.50%-1% of the

loan amount or

Rs. 2,000,

whichever is

higher +

applicable

Service tax &

Surcharge

Up to 0.50% of the

loan amount or Rs.

2,000, whichever is

maximum(plus

taxes as applicable)

SOURCE- Dr. Amit S. Nanwani “A COMPARATIVE STUDY OF HOME LOANS OFFERED BY

PUBLIC AND PRIVATE SECTOR BANKS IN NAGPUR DISTRICT”, (2016).

INTERPRETATION-

The above table shows that the minimum

eligibility criteria required for age in PNB &

ICICI is 21 years, for HDFC is 24 years and

the least one is offered by the Central Bank of

India i.e.18 years whereas the maximum age

required in ICICI, HDFC is 65 years and in

PNB 70 years and in Central Bank of India is

60 years. The maximum Loan amount offered

by the PNB and Central Bank of India is

75lakh and other banks i.e. for ICICI & HDFC

is 10 Crore and the minimum loan amount for

PNB & Central Bank of India is 25 lakh and

20 lakh whereas for HDFC is 5 lakh. Central

Bank of India offers the minimum Rate of

Interest i.e. 8.50% Fixed, PNB and ICICI

offers 8.65%-8.75% and 8.65-8.80% Floating

Rate of Interest respectively and HDFC offers

higher Rate of Interest with 8.50%-9.20%

floating. ICICI Bank offers Lowest EMI with

Rs.762/-per lakh, Central Bank of India and

HDFC both offers Rs.769/-per lakh for 30

years and PNB has the highest EMI with

Rs.780/- per lakh. The table of the selected

banks i.e. PNB, ICICI, HDFC, Central Bank

of India all offers highest Loan Tenure of

30years.All the selected banks in the above

table charges 2% of Penalty on outstanding

loan. PNB Processing Charges are 0.5% or

maximum of Rs.20,000 exclusive of service

tax on loan amount of Rs.300 Lakh and

Rs.50,000 exclusive of service tax is charged

on the loan amount above Rs.300. Central

Bank of India charges 0.5% of the loan

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

11 | P a g e

amount or maximum of Rs.20,000. The

Processing Charges of ICICI and HDFC are

0.5% - 1%of the loan amount or Rs.2,000

whichever is highest and additional service tax

and surcharge is applicable.

CUSTOMER RESPONSE TOWARDS HOUSE LOAN FACILITY OF SELECTED BANKS

TABLE- bank preference

Bank Segments Frequency Percent

Public Sector Banks 60 60.0

Private Sector Banks 40 40.0

Total 100 100.0

SOURCE- Survey Result

Bank Segments

Interpretation: Table depicts that out of the

total respondent‟s i.e.100, 60% of the people

have their account in Public Sector Banks and

the remaining 40% of the people are having

their account in Private Sector Banks.

Public

Sector

Banks, 60

Private

Sector

Bnaks, 40

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

12 | P a g e

Table: accounts of respondents in banks

Account Holding Bank Frequency Percentage

ICICI Bank 19 19.0

HDFC Bank 18 18.0

PNB 31 31.0

Central Bank of India 9 9.0

SBI 14 14.0

Syndicate Bank 2 2.0

Corporation Bank 2 2.0

IDBI 1 1.0

Axis 1 1.0

BOB 2 2.0

Bank of India 1 1.0

Total 100 100.0

SOURCE- Survey Result

Account Holding Bank

Interpretation: The Table depicts that out of

the total respondents i.e. 100, 31 are having

their accounts in PNB, following by ICICI

Bank & HDFC Bank with 19% and 18%

respectively. SBI is holding the accounts of

14% of the respondents and the rest of them

are having their account in Syndicate bank,

19 18

31

914

2 2 1 1 2 105

101520253035

Account Holding Bank Frequency

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

13 | P a g e

Corporate Bank, IDBI, AXIS, BOB and Bank of India.

Table: Duration taken by your bank to sanction a home loan

Duration taken for

Sanctioning of Home Loan

Frequency Percentage

0-1 Month 29 29.0

0-2 Months 26 26.0

0-3 Months 29 29.0

More than 3 Months 16 16.0

Total 100 100.0

SOURCE- Survey Result

Duration taken for Sanctioning of Home Loan

Interpretation: Table graph depicts that most of the bank takes one to three months in sanctioning

the loan and only 16% are among those who take more than three months in sanctioning of Home

Loan.

Table: Politeness of Bank Employees towards their customers-

This table shows us the mean and standard deviation value of the banks.

05

1015202530

0-1 Month 0-2 Months

0-3 Months

More than 3 Months

DU

RA

TIO

N T

AK

EN

FREQUENCY

Duration taken for sanctioning of Home Loan

Frequency

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

14 | P a g e

Group Statistics

N Mean Std.

Deviation

Minimum Maximum

Public Sector Banks 100 1.5500 .50000 1.00 2.00

.

Private Sector Banks 100 1.1800 .38612 1.00 2.00

IN PUBLIC SECTOR BANKS-

Politeness of Bank

Employees

Frequency Percentage

Yes 45 45.0

No 55 55.0

Total 100 100.0

SOURCE- Survey Result

Politeness of Employees of Public Sector Bank

IN PRIVATE SECTOR BANKS-

Politeness of Bank

Employees

Frequency Percentage

Yes 82 82.0

0 10 20 30 40 50 60

Yes

No

45

55

Frequency

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

15 | P a g e

No 18

18.0

Total 100 100.0

SOURCE- Survey Result

Politeness of Employees of Private Sector Bank

Interpretation-Table 13.1 conveys that 45%

respondents say that employees of Public

Sector Banks are Polite to them and 55% say

they are not polite to them. Table 13.2

conveys that 82% respondents say the

employees of the Private Sector Banks are

polite and 18% say they are not.

CONCLUSION

In nutshell, we can conclude that both public

sector and private sector banks truly deserve to

be the leading banks in home loan sector. The

services offered by them are very competitive.

Mostly people prefers public sector banks (i.e.

most have select PNB as per my study) for

home loans, especially because they believe

that is more secure bank, interest rate is lower

and because of having low processing

charges. On the other hand the private sector

banks are coming daily in our country and the

preference of younger population is changing

because of services & facilities provided by

them. Private sector banks are very fast and

lots of time they make things easy for

borrower and also bends some rules for home

loans but on the other hand public sector

banks rules are very strict and stringent. The

documents needed for home loan by private

sector banks are also less as compared to

0 20 40 60 80 100

Yes

No

82

18

Frequency

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

16 | P a g e

public sector banks. It was found that private

sector banks are very popular among the

customers these days. The satisfaction level

that customer have with these banks is very

high in comparison to public sector banks.

Customer are associated with banks for many

services that they require on regular basis and

people tend to prefer banks which provide

better facilities and convenient banking. From

the overall analysis it can be said that the

satisfaction level in relation to the services

provided by private sector banks are very high

as compared to public sector banks. Different

banks offer same product but their services

differentiate and the bank has gone for in this

direction. The customer can choose these

schemes which he feels is good for him and

have the capacity to repay it on that specified

time period.

SUGGESTIONS-

Banks should use easy / simple

procedure for the sanctioning of home

loans to the customers.

The banks need to improve on the

customer satisfaction level due to stiff

competition among the banks.

Banks employees who deal with

customers should have complete

knowledge about the home loans.

More personal attention should be

given to the customers and working

efficiency should be increased.

The bank should improve their

customer service. The services

provided by banks need to be

automated.

The loan passing process should be

quicker by public sector bank like a

private sector bank.

Rate of interest should be competitive

and free accident insurance cover for

home loan customers should be

provided.

Many booklets and attractive

advertisement should be provided to

the customer for awareness about

different housing loan schemes of

public sector banks like private sector

banks.

LIMITATIONS OF THE STUDY-

This research study was time bound

and only certain criteria were taken up

for study.

The survey has been conducted in

Haryana i.e. (Karnal, Ambala &

Kurukshetra) region only. It may not

reflect the public opinion at large and it

was not good enough for perfectly

knowing about the housing loan

schemes of Public &Private Sector

Banks.

Some of the respondents might have

been biased in their responses as it

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

17 | P a g e

depends on their experience gained by

them during processing of such loans

and the results of the study may not be

the same for all the cities & at all

places.

The sample size has not been that

much large (54) which may reflect the

broader picture.

Due to limitation of time and broad

sector of Housing Finance Sector, the

Banks & sample are selected as per the

convenience of the researcher and the

preference is given to only top banks in

the banking industry.

References:

Books

Banking Theory and Practice, P.k.

Srivastav, Himalaya Publishing

House.

Indian Institute of Banking &Finance

(IIBF), Home Loan Counseling

(„Know Your Banking‟ Series),

Taxmann Publications Pvt.LTD. New

Delhi, 2007.

Research papers and Articles

Kajal Chaudhary and Monika Sharma,

“Performance of Indian Public

Sector Banks and Private Sector

Banks”, International Journal of

Innovation, Management and

Technology (2011).

Dr. Shiv Kumar Garg and Dr.

Gajendra Kumar, “Housing Finance

in India : A Comparative Study of

Public and Private Sector Banks”,

Journal of Commerce and Trade

(2014).

D.D. Naik, “You and Your Housing

Co-operative”New Delhi: The

National Co-operative Housing

Federation Ltd. (1976).

G.Gopikuttan, “Housing Boom in

Kerala – Causes and

Consequences”, Ph.D. thesis, Centre

for Development Studies,

Thiruvananthapuram (1988).

Dr. Anand Kumar, “Growth and

Impact of Housing Finance on

Indian Economy”, International

Journal of Research in Management,

Science and Technology (2016).

Dr. P.S. Ravindra, D. P., “Operational

and Financial Performance

Evaluation of Housing Finance

Companies in India” (A Case Study

of LIC Housing Finance Limited and

HDFC). International Journal of

Management and Social Sciences

Research (2013).

Singh, F., and Sharma, R., “Housing

Finance in India – A case study of

LIC housing finance limited”, The

IUP Journal of Financial Economics

(2006)

Airo International Research Journal June, 2016 Volume VII, ISSN:2320-3714

18 | P a g e

Dr. Amit S. Nanwani “A

COMPARATIVE STUDY OF

HOME LOANS OFFERED BY

PUBLIC AND PRIVATE SECTOR

BANKS IN NAGPUR DISTRICT”,

international journal of progresses in

engineering, management, science and

humanities (2016).

R.C.Dangwal, “Housing Finance in

India: Myth and Reality”, eds. G.S

Batra and R.C Dangwal, New Studies

in Commerce and Business, (New

Delhi: Deep and Deep Publications,

1999).

Samkutty George, “Prospects for a

Suitable Housing Finance Scheme

for Kerala”, Ph.D. thesis, University

of Kerala, (2002).

Dr. P.S. Ravindra, “Operational and

Financial Performance Evaluation of

Housing Finance Companies in

India (A Case Study of LIC Housing

Finance Limited and HDFC)”,

International Journal of Management

and Social Sciences Research (2013).

La CourMicheal, “The Home

Purchase Mortgage Preferences of

Lowand-Moderate Income

Households”, Forthcoming in Real

Estate Economics (2006).