AN AIRLINE NETWORK DESIGN APPROACH CONSIDERING ENVIRONMENTAL AND

Airline Network Strategies Bruce Tecklenburg

Network, Fleet and Schedule

Strategic Planning

Module 5: 30 March 2015

Istanbul Technical University

Air Transportation Management

M.Sc. Program

2

Lecture Outline

Review: Evolving Network Strategies

Capacity Discipline and Profitability

Recent Capacity Strategies of Western airlines

Less Capacity Means Higher Yields and Load Factors

Global Network Expansion: Emerging Carriers

Rapid Growth of Competing Hubs

Airline Cooperation and Consolidation

Alliances and Code-sharing

Joint Ventures

Mergers and Acquisitions

2 20 de marzo de 2015

3

Review: Evolving Network Strategies

From linear – to hub construction – to hub-to-hub

flying

From national dominance – to a regional footprint –

to a global focus

Domestic networks supporting international growth

International expansion contributes to improved on board

revenue for the domestic operation

4

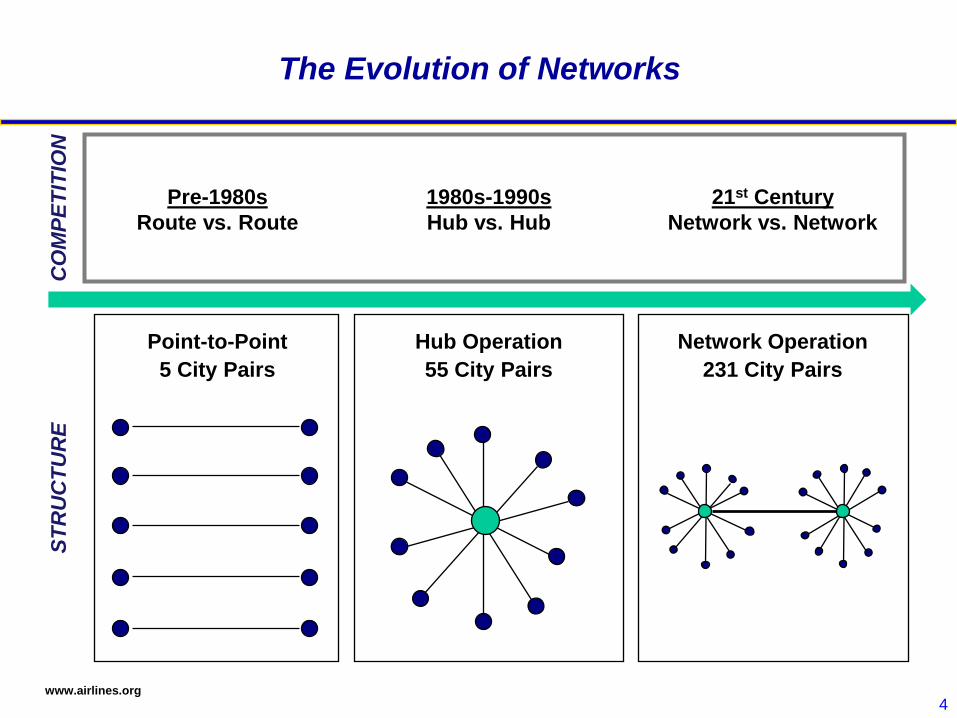

The Evolution of Networks

Hub Operation

55 City Pairs

Network Operation

231 City Pairs

Point-to-Point

5 City Pairs

Pre-1980s

Route vs. Route

1980s-1990s

Hub vs. Hub

21st Century

Network vs. Network

CO

MP

ET

ITIO

N

ST

RU

CT

UR

E

www.airlines.org

5

US- European Airline Network

Developments

Industry consolidation through mergers

Air France and KLM in 2004 [Air France-KLM]

Delta and Northwest in 2008 [Delta]

United and Continental in 2010 [United]

British Airways and Iberia in 2011 [Int’l Airlines Group]

American and US Airways in 2014 [American]

International vs. Domestic Network Growth

Short Haul Capacity Cuts and Shifts to Regional or LCC

franchises

Focus International Network Expansion and connectivity

6

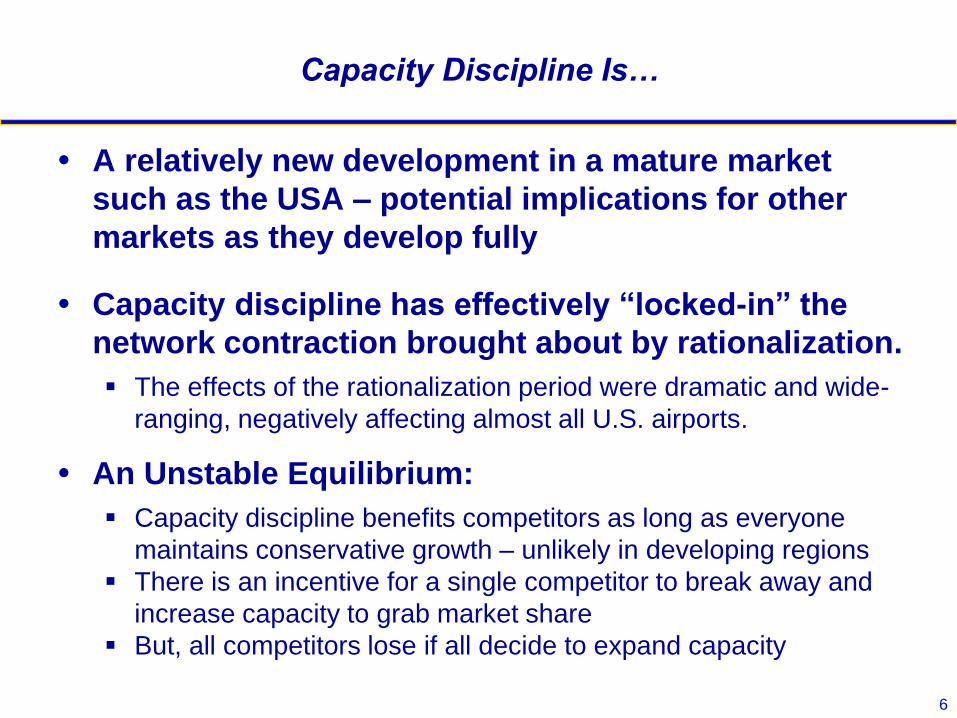

Capacity Discipline Is…

A relatively new development in a mature market

such as the USA – potential implications for other

markets as they develop fully

Capacity discipline has effectively “locked-in” the

network contraction brought about by rationalization.

The effects of the rationalization period were dramatic and wide-

ranging, negatively affecting almost all U.S. airports.

An Unstable Equilibrium:

Capacity discipline benefits competitors as long as everyone

maintains conservative growth – unlikely in developing regions

There is an incentive for a single competitor to break away and

increase capacity to grab market share

But, all competitors lose if all decide to expand capacity

7

Capacity Discipline Strategies

Airline capacity is a competitive weapon

Flight frequency is primary determinant of market share

Historically, market share strategies have led to excess capacity,

meaning lower load factors and lower yields

Recent “capacity discipline” in the industry

Mature U.S. market place with modest passenger growth

Perhaps the only strategy that can lead to both higher yields and

higher load factors

Short haul capacity reductions achieved with:

Fewer departures, particularly at smaller airports

Smaller aircraft, with more 70-100 seat large regional jets

Shift of wide-body aircraft from short to long haul routes

8

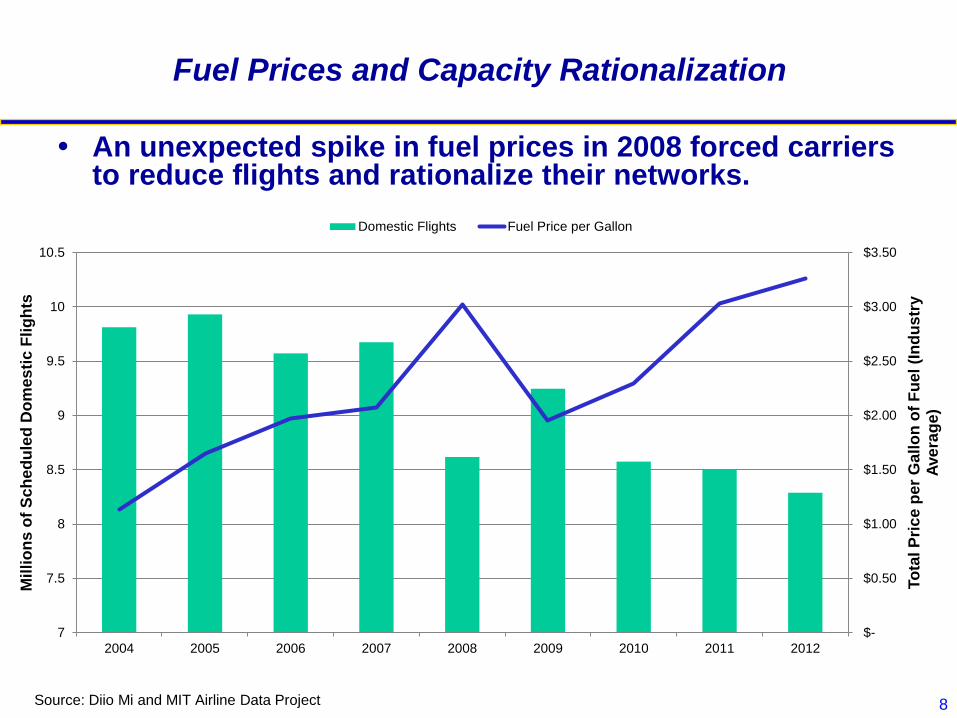

Fuel Prices and Capacity Rationalization

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

7

7.5

8

8.5

9

9.5

10

10.5

2004 2005 2006 2007 2008 2009 2010 2011 2012

To

tal P

ric

e p

er

Ga

llo

n o

f F

ue

l (I

nd

us

try

Ave

rag

e)

Mil

lio

ns o

f S

ch

ed

ule

d D

om

es

tic F

lig

hts

Domestic Flights Fuel Price per Gallon

An unexpected spike in fuel prices in 2008 forced carriers to reduce flights and rationalize their networks.

Source: Diio Mi and MIT Airline Data Project

9

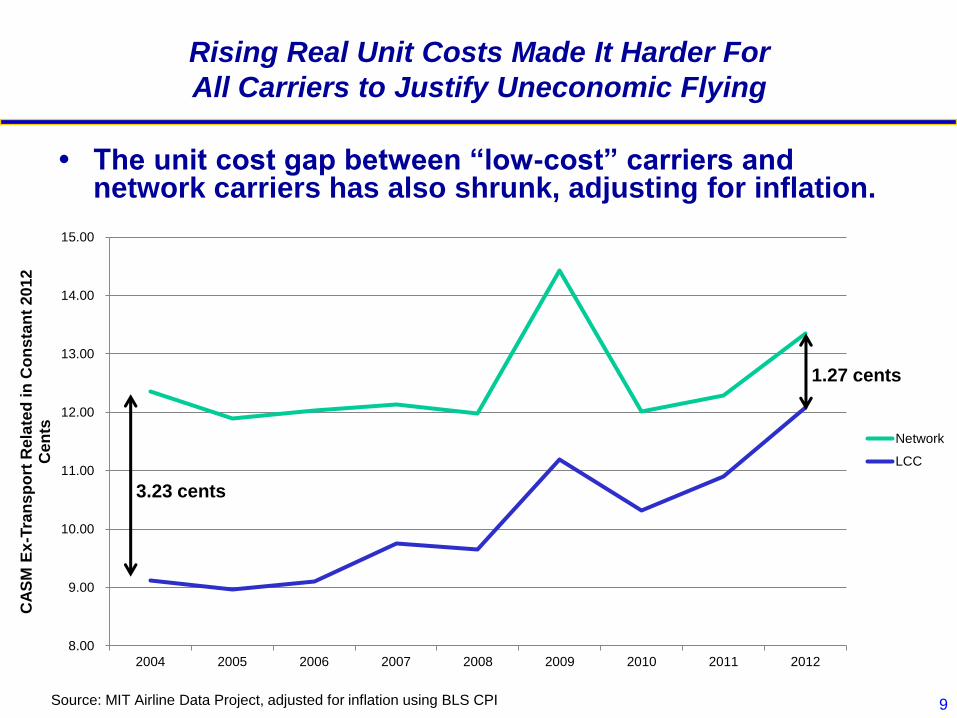

Rising Real Unit Costs Made It Harder For

All Carriers to Justify Uneconomic Flying

The unit cost gap between “low-cost” carriers and network carriers has also shrunk, adjusting for inflation.

8.00

9.00

10.00

11.00

12.00

13.00

14.00

15.00

2004 2005 2006 2007 2008 2009 2010 2011 2012

CA

SM

Ex

-Tra

nsp

ort

Rela

ted

in

Co

ns

tan

t 2

01

2

Cen

ts

Network

LCC

Source: MIT Airline Data Project, adjusted for inflation using BLS CPI

3.23 cents

1.27 cents

11

Global Network Expansion:

Emerging Global Carriers

Continued rapid growth of these airlines will affect

global traffic flows

Emirates (Dubai), Etihad (Abu Dhabi), Qatar (Doha) and Turkish

(Istanbul) building large hubs that depend on connecting traffic

Future success is highly dependent on negotiating new bilateral

rights to further expand their hub networks

Implications for airports

Emerging carriers looking for new spoke cities to feed their

connecting global hubs with 6th freedom international traffic

Operations involve long-haul, wide-body (and A380) aircraft and

full-service products (premium classes, lounges)

Competition among airports to attract these new services – at

BOS, Turkish started in May 2014 and Emirates in March 2014

12

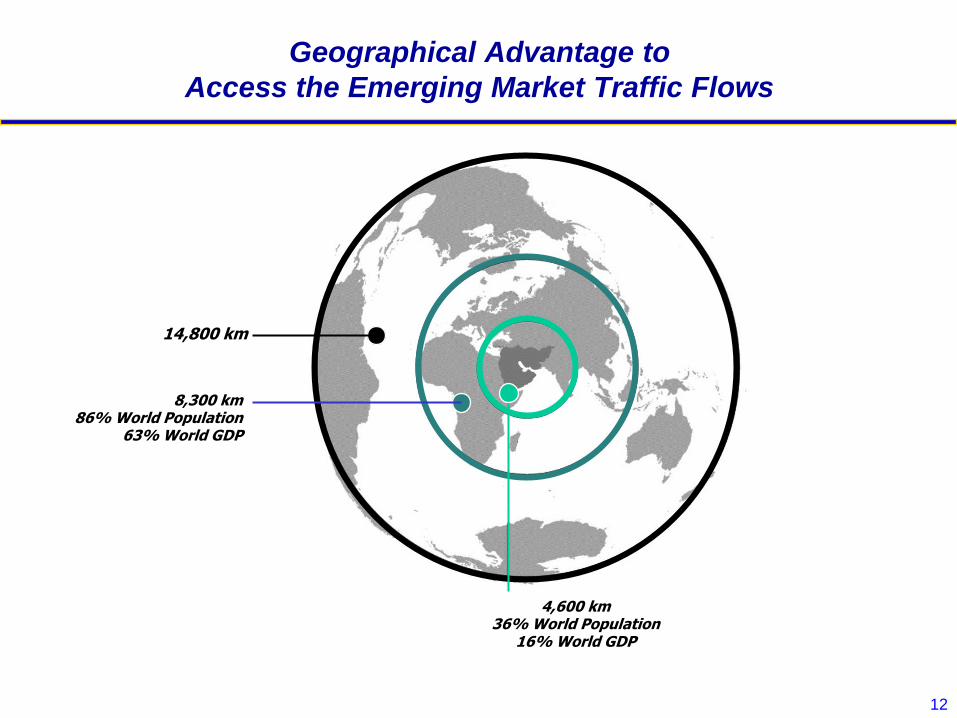

Geographical Advantage to

Access the Emerging Market Traffic Flows

14,800 km

8,300 km 86% World Population

63% World GDP

4,600 km 36% World Population

16% World GDP

13

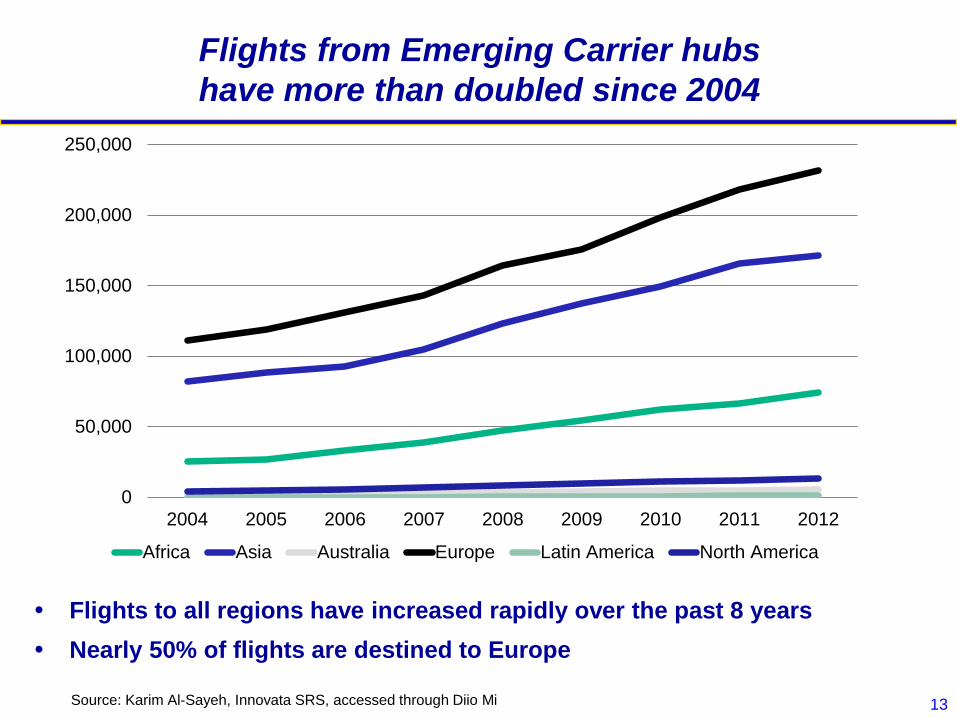

Flights from Emerging Carrier hubs

have more than doubled since 2004

Flights to all regions have increased rapidly over the past 8 years

Nearly 50% of flights are destined to Europe

0

50,000

100,000

150,000

200,000

250,000

2004 2005 2006 2007 2008 2009 2010 2011 2012

Africa Asia Australia Europe Latin America North America

Source: Karim Al-Sayeh, Innovata SRS, accessed through Diio Mi

14

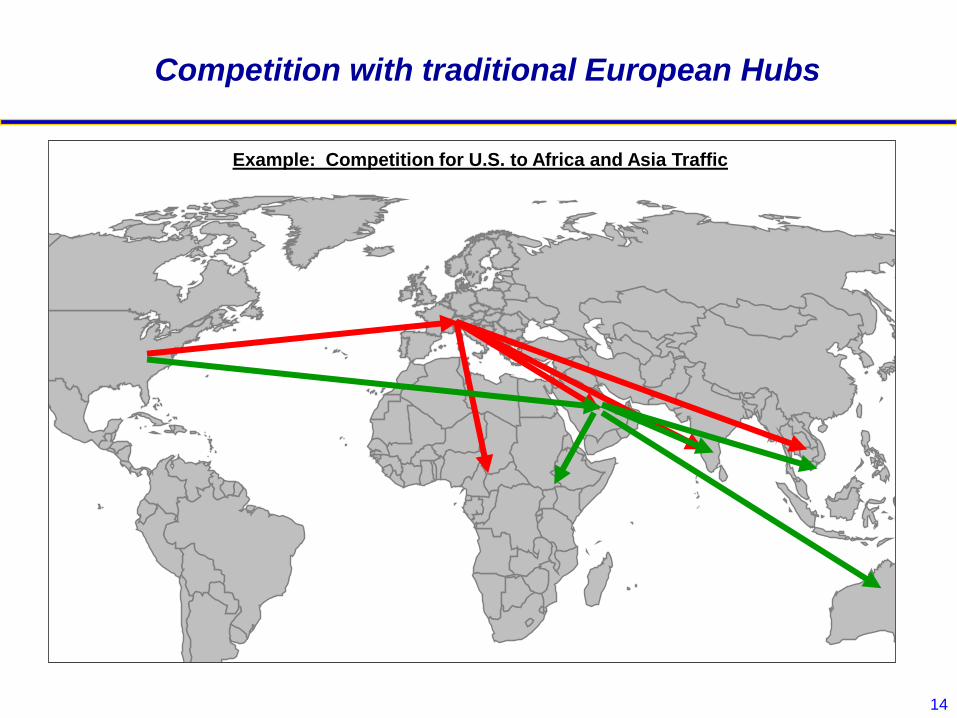

Competition with traditional European Hubs

Example: Competition for U.S. to Africa and Asia Traffic

15

What are the implications of the forecasted

fleet growth for the emerging carriers?

How will they attract 100 million new passengers?

Is it reasonable to assume that they can maintain 10% growth

rates through the end of the decade?

Can their home airports accommodate the influx of wide-body

aircraft?

What effect will the emerging carriers have on global

air transportation?

How will their growth further affect legacy carriers around the

world?

Will the growth of new LCCs and the revamping of legacy carriers

affect them?

Can all four emerging carriers coexist?

16

Airline Cooperation and Consolidation

Regulatory hurdles block the type of cross-border

consolidation that has occurred in other industries.

International flight operations still regulated by bilateral

agreements

Limits on foreign ownership of airlines in many countries

Influence of political and union forces against such consolidation

Anti-trust laws can constrain mergers and cooperation even

within same country

Many forms of cooperation possible:

Code-sharing agreements between two airlines

Membership in global airline alliances

Joint ventures to share both revenues and costs

Mergers and acquisitions

17

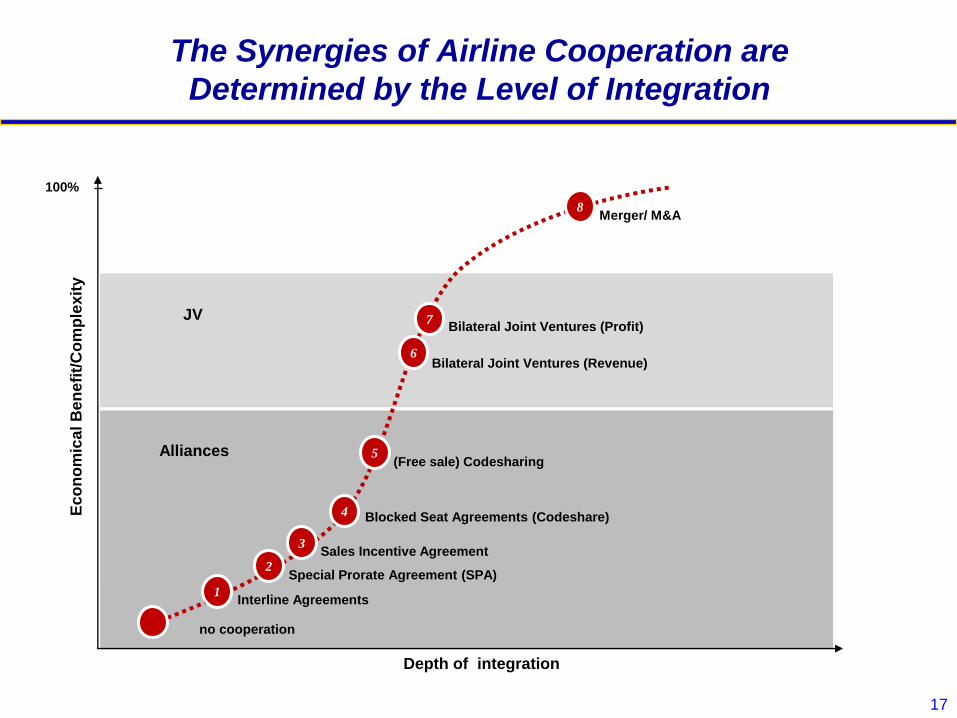

The Synergies of Airline Cooperation are

Determined by the Level of Integration E

co

no

mic

al B

en

efi

t/C

om

ple

xit

y

Special Prorate Agreement (SPA)

(Free sale) Codesharing

Merger/ M&A

Depth of integration

100%

no cooperation

Interline Agreements

Sales Incentive Agreement

Blocked Seat Agreements (Codeshare)

1

2

3

4

5

6

8

Alliances

JV

Bilateral Joint Ventures (Revenue)

Bilateral Joint Ventures (Profit) 7

18

Code-Sharing

Under a “code-share” arrangement, partner airline

places its own code on an alliance flight:

Partner markets and sells its own tickets for the flight

Flight is actually operated by another alliance airline

Flight is listed twice (or more) in airline schedules and computer

reservations systems (CRS)

Code sharing increases consumers’ perceptions of

network coverage in CRS displays:

EXAMPLE:

TK 012 JFK-IST

also listed as US* 5003 JFK-IST

19

Airline Alliances and Network Coverage

“Strategic alliances” between two airlines take the

economic logic of hub networks one step further:

Partner airlines can expand their network coverage without

increasing their own flights and operating costs

Leads to further consolidation of loads, as two or more airlines

now contribute passengers to a single “alliance flight”

Marketing power of larger networks is reinforced--more

destinations, seamless connections, frequent flyer benefits

Additional cost savings are possible in alliance airlines due to

combined flights, airport check-in and club operations, integrated

purchasing and information systems

20

Hubs

Airline I

Hubs

Airline II

Network

Airline II

Network

Airline I

Aircraft

Airline IAircraft

Airline II

Aircraft

Airline II

& Airline I

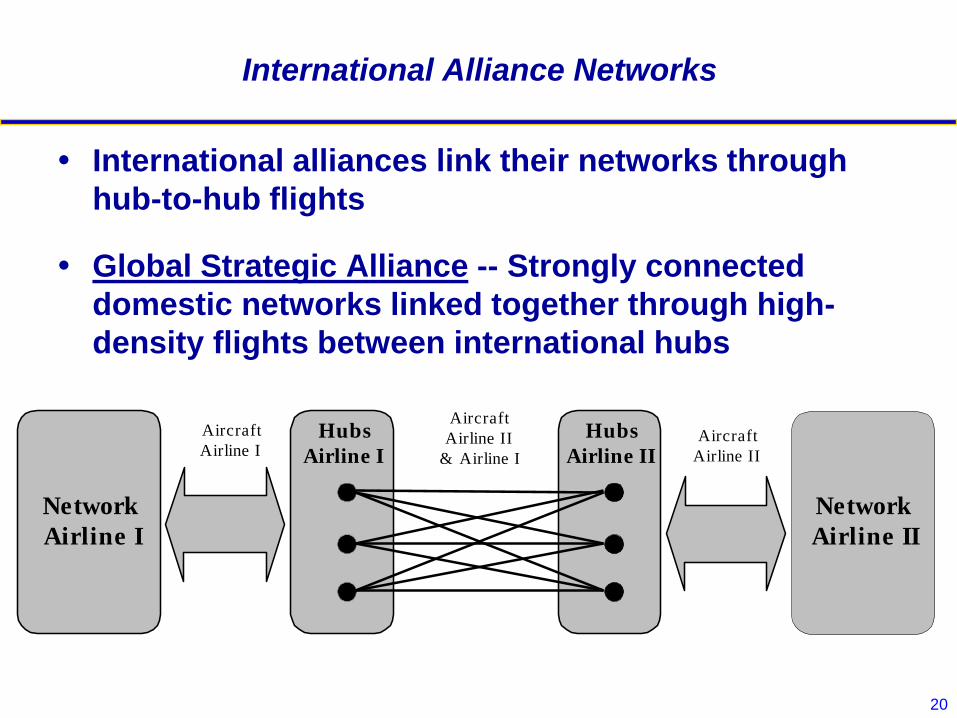

International Alliance Networks

International alliances link their networks through

hub-to-hub flights

Global Strategic Alliance -- Strongly connected

domestic networks linked together through high-

density flights between international hubs

21

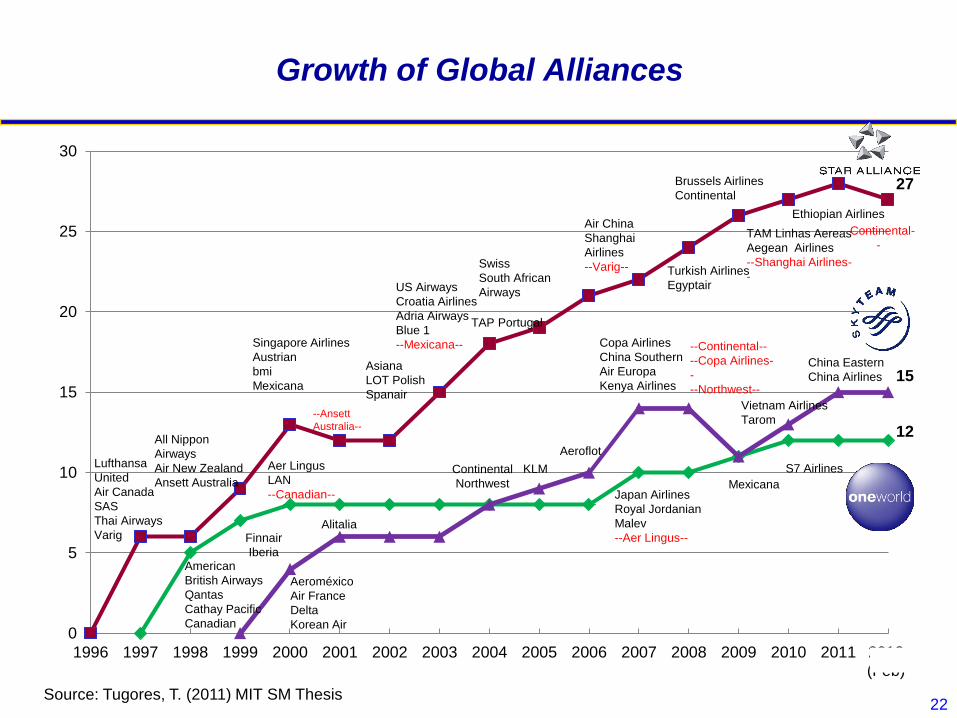

Global Airline Alliances

Airline alliances are strategic partnerships between

several airlines which focus primarily on large scale

code-sharing agreements

KLM – Northwest Alliance in 1989 was the first step in

the establishment of multinational alliances

Anti-trust immunity is a central tenet of airline

alliances

Currently there are 3 large airline alliances:

Star Alliance (1997)

oneworld (1999)

SkyTeam (2000)

22

0

5

10

15

20

25

30

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012(Feb)

Aeroméxico

Air France

Delta

Korean Air

Alitalia

Continental

Northwest

KLM

Aeroflot

Copa Airlines

China Southern

Air Europa

Kenya Airlines

--Continental--

--Copa Airlines-

-

--Northwest--

Vietnam Airlines

Tarom

China Eastern

China Airlines

American

British Airways

Qantas

Cathay Pacific

Canadian

Finnair

Iberia

Aer Lingus

LAN

--Canadian-- Japan Airlines

Royal Jordanian

Malev

--Aer Lingus--

Mexicana

S7 Airlines Lufthansa

United

Air Canada

SAS

Thai Airways

Varig

All Nippon

Airways

Air New Zealand

Ansett Australia

Singapore Airlines

Austrian

bmi

Mexicana

--Ansett

Australia--

Asiana

LOT Polish

Spanair

US Airways

Croatia Airlines

Adria Airways

Blue 1

--Mexicana--

Swiss

South African

Airways

Air China

Shanghai

Airlines

--Varig--

TAP Portugal

Turkish Airlines

Egyptair

Brussels Airlines

Continental

TAM Linhas Aereas

Aegean Airlines

--Shanghai Airlines-

-

--Continental-

-

27

15

12

Ethiopian Airlines

Growth of Global Alliances

Source: Tugores, T. (2011) MIT SM Thesis

23

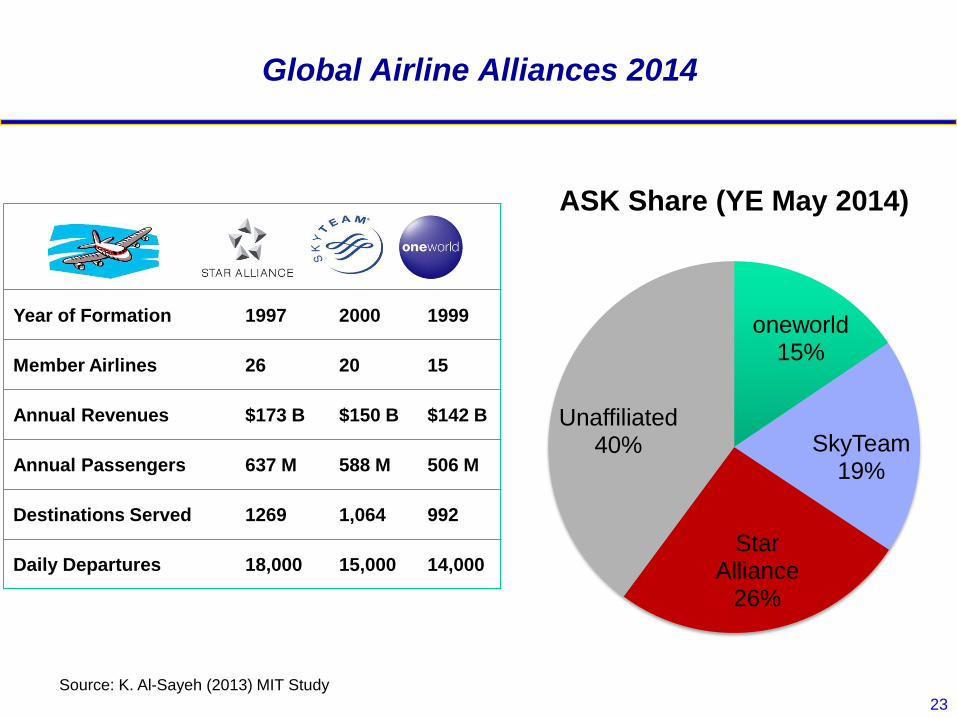

Global Airline Alliances 2014

Year of Formation 1997 2000 1999

Member Airlines 26 20 15

Annual Revenues $173 B $150 B $142 B

Annual Passengers 637 M 588 M 506 M

Destinations Served 1269 1,064 992

Daily Departures 18,000 15,000 14,000

Source: K. Al-Sayeh (2013) MIT Study

oneworld 15%

SkyTeam 19%

Star Alliance

26%

Unaffiliated 40%

ASK Share (YE May 2014)

24

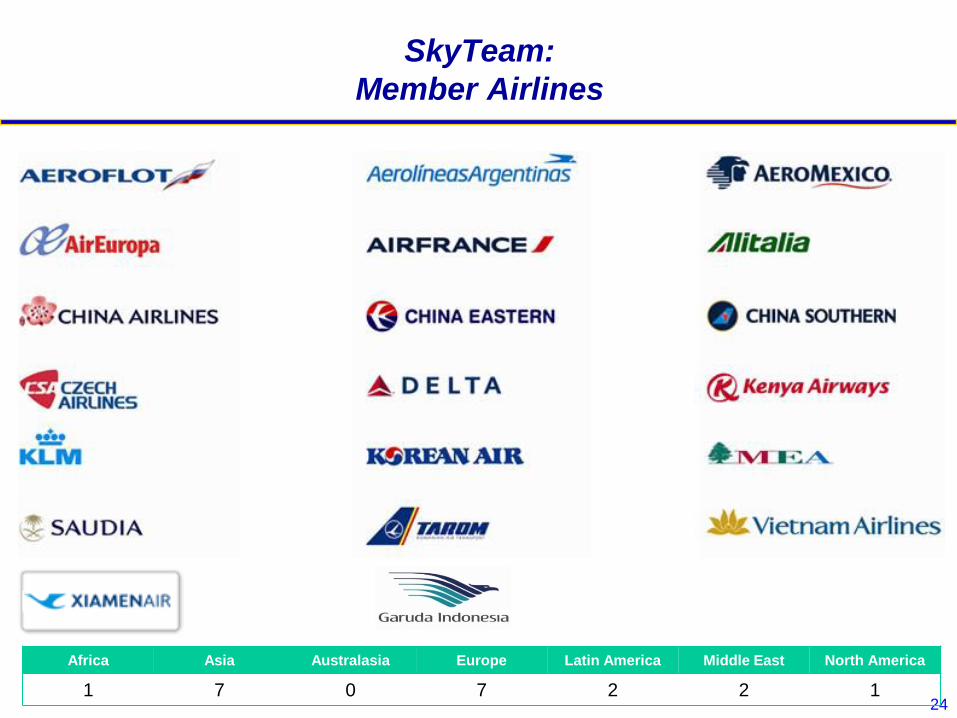

SkyTeam:

Member Airlines

Africa Asia Australasia Europe Latin America Middle East North America

1 7 0 7 2 2 1

25

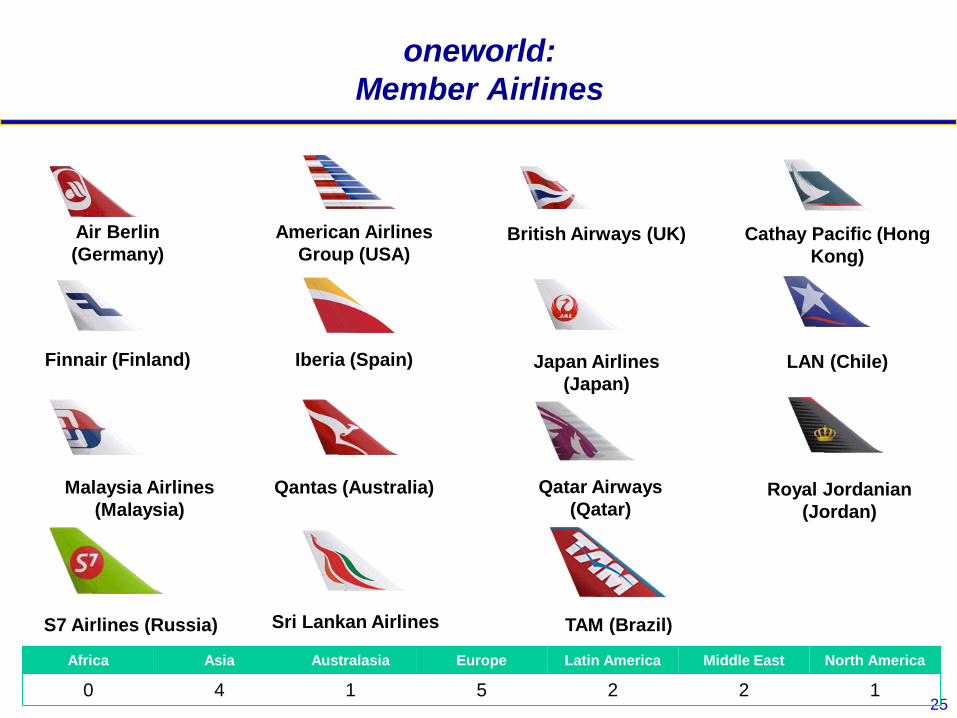

oneworld:

Member Airlines

American Airlines

Group (USA)

Air Berlin

(Germany) British Airways (UK) Cathay Pacific (Hong

Kong)

Iberia (Spain) Finnair (Finland) Japan Airlines

(Japan)

LAN (Chile)

Qantas (Australia) Malaysia Airlines

(Malaysia) Royal Jordanian

(Jordan)

S7 Airlines (Russia)

Qatar Airways

(Qatar)

TAM (Brazil) Sri Lankan Airlines

Africa Asia Australasia Europe Latin America Middle East North America

0 4 1 5 2 2 1

26

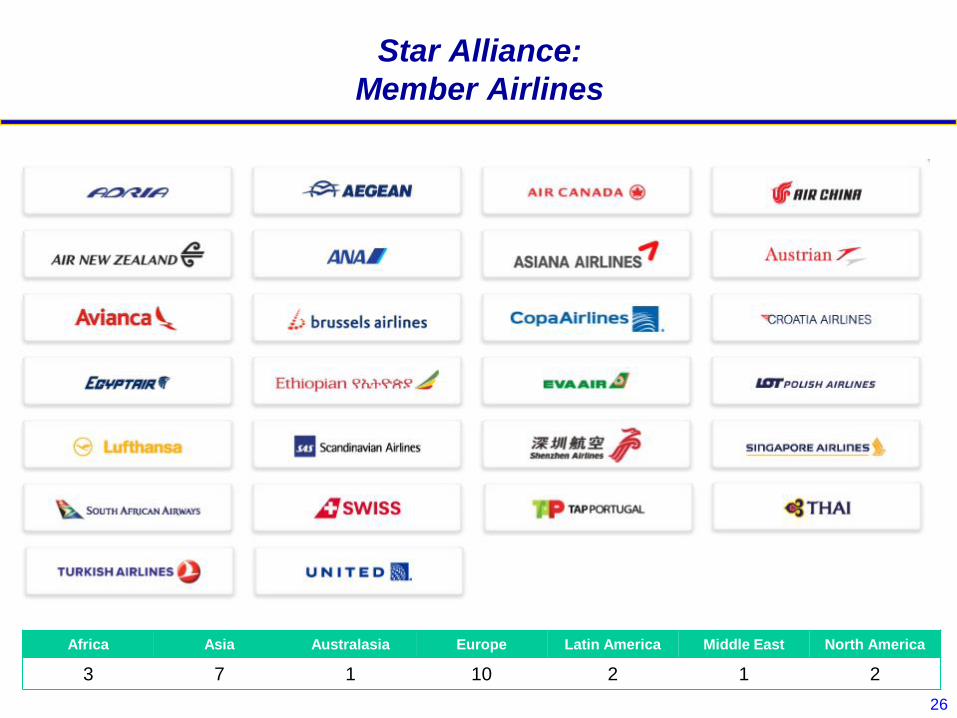

Star Alliance:

Member Airlines

Africa Asia Australasia Europe Latin America Middle East North America

3 7 1 10 2 1 2

27

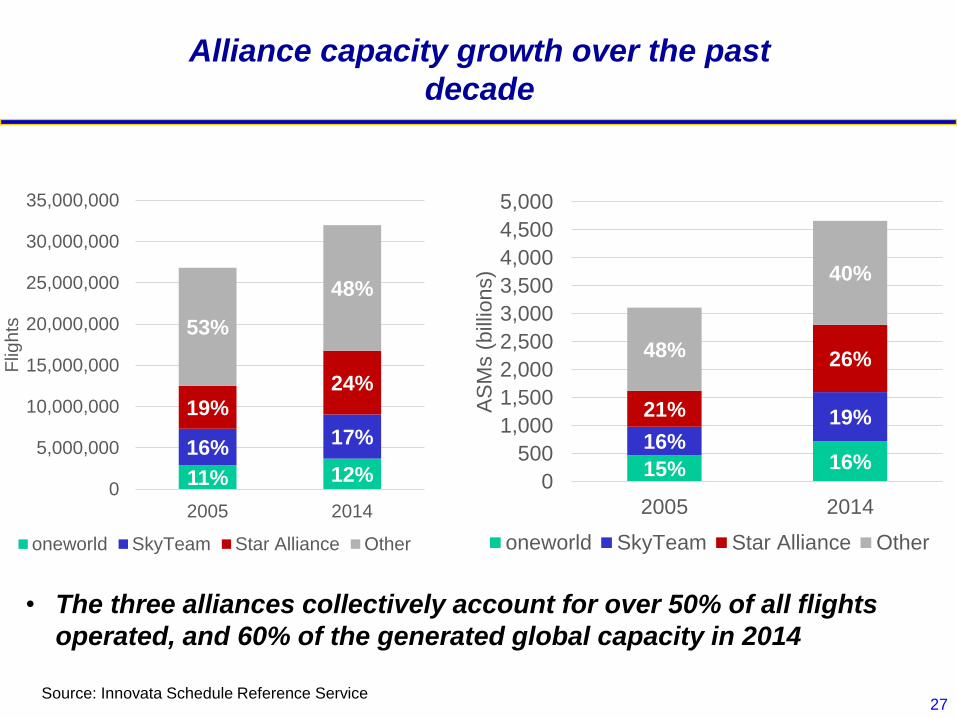

Alliance capacity growth over the past

decade

11% 12%

16% 17%

19% 24%

53%

48%

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

2005 2014

Flig

hts

oneworld SkyTeam Star Alliance Other

15% 16% 16%

19% 21%

26% 48%

40%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2005 2014A

SM

s (

bill

ions)

oneworld SkyTeam Star Alliance Other

• The three alliances collectively account for over 50% of all flights

operated, and 60% of the generated global capacity in 2014

Source: Innovata Schedule Reference Service

28

Advantages of Airline Alliances

Airlines can strengthen networks and market position

against competing alliances:

Expand network coverage with little risk or increased operating

costs, and no new capital required (aircraft or facilities)

Access to new O-D markets and incremental revenues

Increased market shares in existing markets due to greater

presence, meaning increased traffic, revenues, and profit

For consumers, a “seamless” travel experience:

World-wide service with single check-in, consistent passenger

service standards, club rooms and FFP benefits

29

Disadvantages of Airline Alliances

Potential for disagreements among airline partners:

Can be difficult and costly to completely standardize customer

service standards and procedures

Cost savings might not be as great as anticipated

Conflicting network and revenue sharing objectives

Possible for one partner to actually lose revenue as dominant

airline exerts market and RM strengths

Alliance relationships are not permanent, as airlines switch

partners and alliances

For consumers, confusion about code-sharing,

operating carriers and potentially anti-competitive

impacts

30

Airlines choosing bilateral relationships

outside of traditional alliances

Recent activity points to some airlines pursuing

bilateral codeshares as an alternative to alliances:

Alaska Airlines and jetBlue in the U.S. cooperating with various

international flag airlines feeding their domestic hub

In 2013 Qantas and Emirates announced a major partnership

including codesharing on Europe-Australia services (despite

Qantas being a oneworld member)

Hainan Airlines of China effectively “locked out” of alliances has

set up codeshares at its gateways (American, Brussels, Air

Berlin)

New developments raise interesting questions about

the future of the traditional alliance model

31

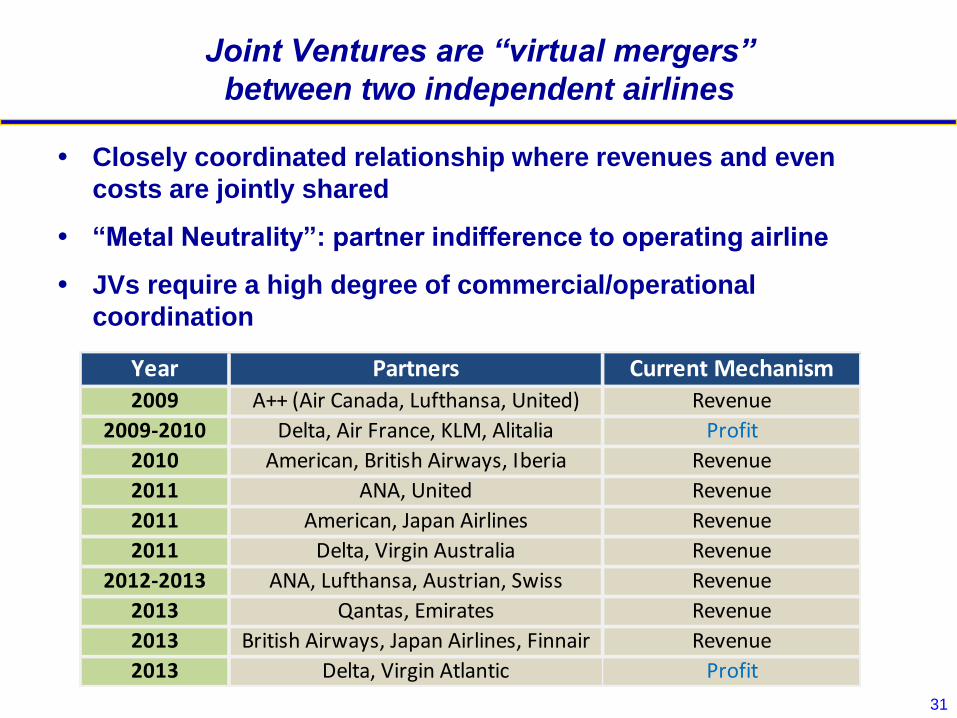

Joint Ventures are “virtual mergers”

between two independent airlines

Closely coordinated relationship where revenues and even

costs are jointly shared

“Metal Neutrality”: partner indifference to operating airline

JVs require a high degree of commercial/operational

coordination

Year Partners Current Mechanism2009 A++ (Air Canada, Lufthansa, United) Revenue

2009-2010 Delta, Air France, KLM, Alitalia Profit

2010 American, British Airways, Iberia Revenue

2011 ANA, United Revenue

2011 American, Japan Airlines Revenue

2011 Delta, Virgin Australia Revenue

2012-2013 ANA, Lufthansa, Austrian, Swiss Revenue

2013 Qantas, Emirates Revenue

2013 British Airways, Japan Airlines, Finnair Revenue

2013 Delta, Virgin Atlantic Profit

32

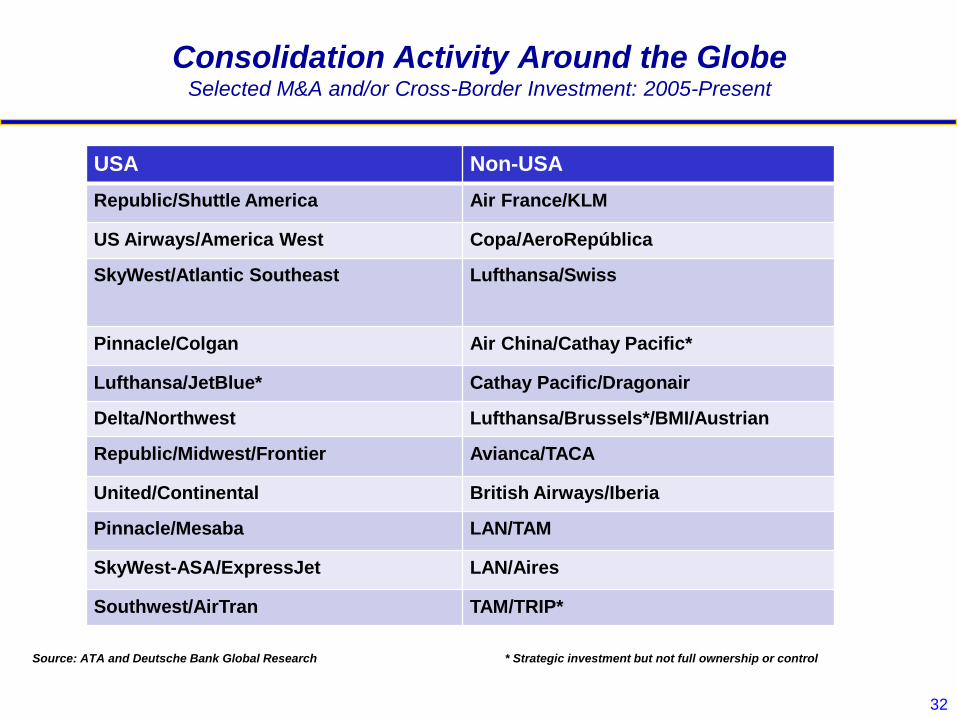

Consolidation Activity Around the Globe Selected M&A and/or Cross-Border Investment: 2005-Present

USA Non-USA

Republic/Shuttle America Air France/KLM

US Airways/America West Copa/AeroRepública

SkyWest/Atlantic Southeast Lufthansa/Swiss

Pinnacle/Colgan Air China/Cathay Pacific*

Lufthansa/JetBlue* Cathay Pacific/Dragonair

Delta/Northwest Lufthansa/Brussels*/BMI/Austrian

Republic/Midwest/Frontier Avianca/TACA

United/Continental British Airways/Iberia

Pinnacle/Mesaba LAN/TAM

SkyWest-ASA/ExpressJet LAN/Aires

Southwest/AirTran TAM/TRIP*

Source: ATA and Deutsche Bank Global Research * Strategic investment but not full ownership or control

33

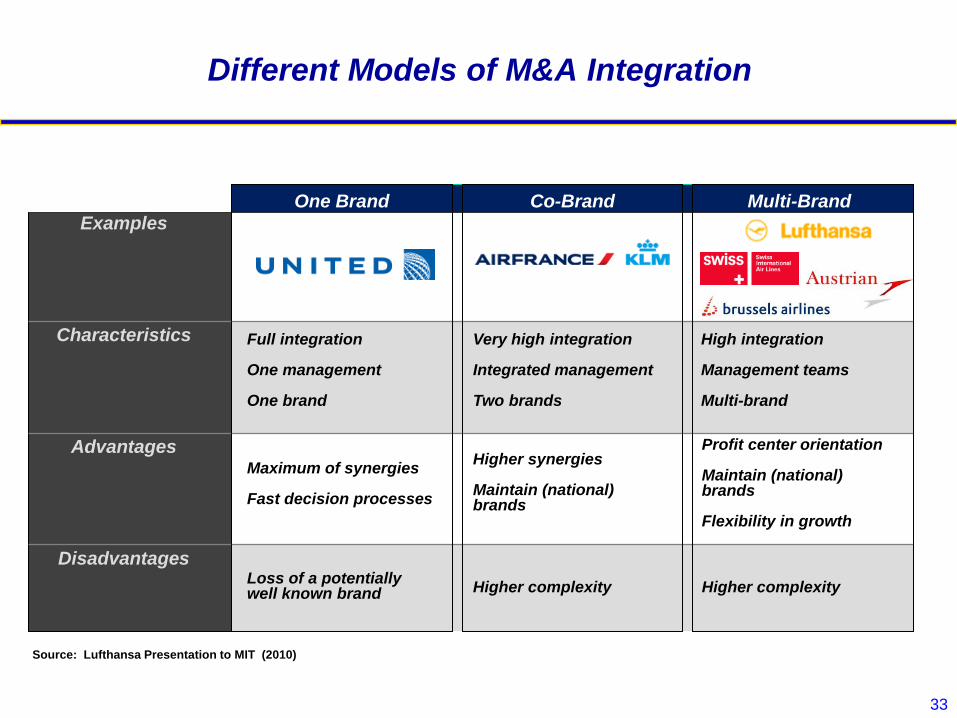

Different Models of M&A Integration

Examples

Characteristics

Advantages

Disadvantages

One Brand Co-Brand Multi-Brand

Full integration One management One brand

Maximum of synergies Fast decision processes

Loss of a potentially well known brand

Very high integration Integrated management Two brands

Higher synergies Maintain (national) brands

Higher complexity

High integration Management teams Multi-brand

Profit center orientation Maintain (national) brands Flexibility in growth

Higher complexity

Source: Lufthansa Presentation to MIT (2010)

34

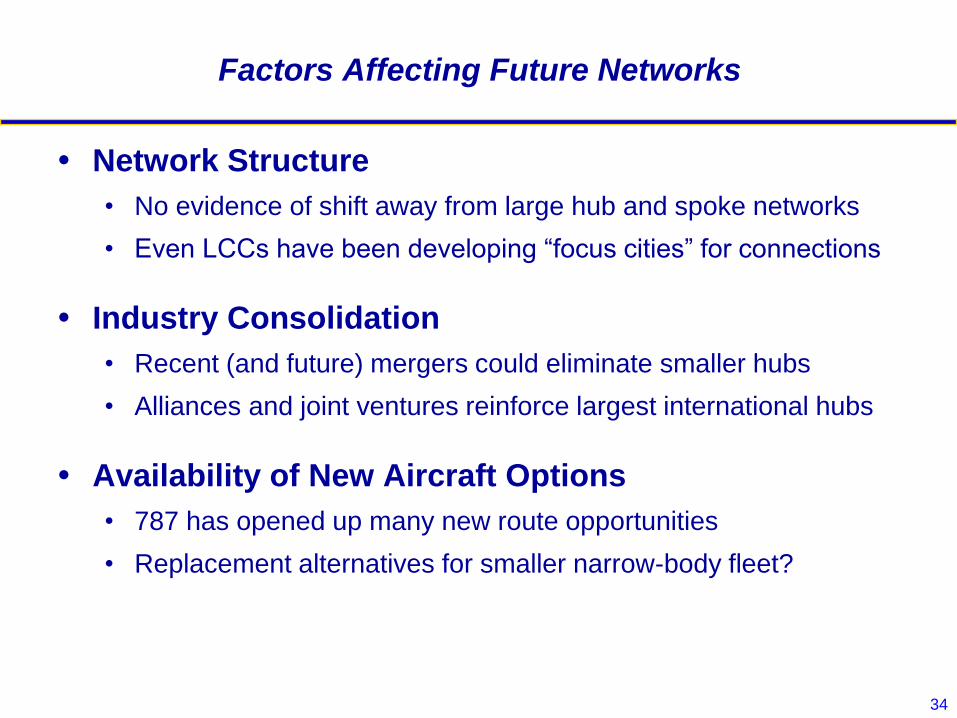

Factors Affecting Future Networks

Network Structure

• No evidence of shift away from large hub and spoke networks

• Even LCCs have been developing “focus cities” for connections

Industry Consolidation

• Recent (and future) mergers could eliminate smaller hubs

• Alliances and joint ventures reinforce largest international hubs

Availability of New Aircraft Options

• 787 has opened up many new route opportunities

• Replacement alternatives for smaller narrow-body fleet?

![the role of the airline transportation network · arXiv:q-bio/0507029v1 [q-bio.OT] 18 Jul 2005 Prediction and predictability of global epidemics: the role of the airline transportation](https://static.fdocuments.in/doc/165x107/5eb7e40b15e49a3fcf0366d5/the-role-of-the-airline-transportation-network-arxivq-bio0507029v1-q-bioot.jpg)