AIRLINE ALLIED SERVICES LIMITED - · PDF fileAASL 4 VISION: To be prominent domestic airline...

83

AIRLINE ALLIED SERVICES LIMITED AASL

Transcript of AIRLINE ALLIED SERVICES LIMITED - · PDF fileAASL 4 VISION: To be prominent domestic airline...

AIRLINE ALLIED SERVICES LIMITED

AASL

AASL

CONTENTS

Page No.

1. Board of Directors 1

2. Chairman’s Message 2

3. Directors’ Report 5

4. Comments of the Comptroller & Auditor General of India 31

5. Independent Auditors’ Report 32

6. Balance Sheet as at 31 March 2016 55

7. Statement of Profit & Loss for the year ended 31 March 2016 56

8. Cash Flow Statement 57

9. Notes forming part of the Financial Statements for the year ended 31 March 2016 58

AASL

BOARD OF DIRECTORS (as on 30 DECEMBER 2016)

Shri Ashwani Lohani Chairman

Shri Vinod Hejmadi Director

Shri Pankaj Srivastava Director

Smt. Meenakshi Dua Director

Capt Arvind Kathpalia Director

Dr. (Smt.) Shefali Juneja Director

Chief Executive Officer

Shri C.S. Subbiah

Auditors

M/s. Chandra Gupta & Associates

Chartered Accountant

E-103, Palm Court Apartments

Plot No.-3, Sector-19-B, Dwarka

New Delhi-110 075.

Company Secretary

Shri Gagan Batra

Registered Office

Old Lufthansa Hanger Building,

(Adjacent to ED-NR Office)

I.G.I. Airport, T-1,

New Delhi-110 037

1

AASL

2

CHAIRMAN'S MESSAGE

Dear Shareholders,

It gives me great pleasure to present to you the Thirty Third Annual Report of the Company for the year 2015-16.

Airline Allied Services Ltd. (AASL) is the leading airline in the country providing connectivity to Tier II & Tier III cities in India.

NEW CIVIL AVIATION POLICY – REGIONAL CONNECTIVITY SCHEME

The Ministry of Civil Aviation (MoCA), Government of India released the National Civil Aviation Policy 2016 (NCAP 2016). One of the objectives of NCAP 2016 is to “enhance regional connectivity through fiscal support and infrastructure development”.

In the new Civil Aviation Policy, the Government has capped passenger fares for flight journeys from unserved and underserved airports at Rs 2,500 per hour of flying for approximately 500 kilometres under the regional connectivity scheme.

In this scheme, the gap in costs and revenues, if any, will be compensated through Viability Gap Funding (VGF). No landing charges, parking charges and Terminal Navigation Landing Charges will be imposed for regional connectivity scheme flights. The regional connectivity scheme will be in operation for 10 years with individual route contracts to be for a 3-year span. Limited period exclusive route rights will be allotted to selected operators.

This appears to open up tremendous opportunities and markets for the airline like AASL which are operating with small aircraft and connecting smaller cities.

PERFORMANCE OF THE COMPANY DURING THE YEAR

In the current year, the net loss is higher by Rs.14.83 crores as company registered a net Loss of Rs. 198.75 crores during 2015-16 in comparison with previous year's loss of Rs.183.92 crores. This is mainly attributed to following factors:

1. Increased lease charges by Rs. 43.63 crores due to induction of five new aircraft in the fleet.

2. Upward increase in Maintenance charges by Rs. 37.47 crores due to induction of new aircraft and higher upkeep of old aircraft of the fleet, namely CRJ and ATR- 42.

3. There was upward increase in Landing and Navigation expenses, Catering expenses due to discontinuation of BOB, increase in interest paid to parent company Air India Limited, increase in redelivery charges of returned leased aircraft, appreciation of USD vis-a-vis Indian Rupee.

4. Although the Passenger Revenue increased by Rs.29.61 crores owing to increase in passenger carriage but there was a decline in passenger yield by Rs.558/- per passenger. Thus, growth remaining stunted.

5. Although ATF cost registered a decrease of Rs. 26.31 crores due to fall in average ATF rate but this gain was more than offset by above stated elements of cost. Besides, Sundry Receipts too registered the decline owing to decrease in Maintenance Reserve refunds from the Lessors.

AASL

3

FUTURE PLANS

Company is in process of inducting 10 New ATR 72-600 aircraft in its fleet in the ensuing financial year. With this induction, revenue is likely to increase three times. With additional flights, fixed overhead cost will be apportioned accordingly. This will lead to lowering of operational cost. Plans are afoot to increase the aircraft utilization from 6.5 hrs to 8.4 hrs a day with the planned recruitment of new pilots. Hopefully, the bottom line in the next fiscal will turn black from the red.

ACKNOWLEDGEMENT

I take this opportunity to thank Air India Limited and Ministry of Civil Aviation for their unstinted support. I also acknowledge the support extended by all other authorities including banks and regulatory agencies and assure that we will continue our course on a growth trajectory, taking Airline Allied Services Limited to greater heights. I would like to thank my colleagues on the Board for their valuable guidance.

I would like to thank all employees of Airline Allied Services Limited for exemplary efforts to show the world the strength and resilience of our team spirit in pursuit of excellence. I want to thank each one of our employees for his contribution and everybody in the Airline Allied Services Limited family who had risen to the occasion to uphold the image of the company.

On behalf of the Board, I seek your continued support, as always.

� � � (Ashwani Lohani)Chairman

AASL

4

VISION:

To be prominent domestic airline providing connectivity to Tier 2 and 3 cities and a feeder airline to the network & in complete synergy with Air India.

MISSION & OBJECTIVES :

Prominent domestic airline

Customer

l Provide safe, reliable and on-time services

l Take effective steps to provide high level of customer satisfaction

l Explore new passenger base for airline market

l Provide one-stop connectivity to metros and beyond for seamless travel to main domestic and international destinations.

Processes

l Continuously improve standards of safety and efficiency

l Operate and maintain a young and modern fleet

l Provide the best and most efficient network in conjunction with main network of Air India

l Create economic value

l Enhance its competitive market standing and image as a domestic short haul airline operator.

Route – Network

l Compete with high density train traffic

l Meet regional aspirations of swift connection to metros and beyond

l Provide connectivity to cities so far not air connected.

People

l Build a highly motivated and professional team

l Maintain highest degree of transparency and ethics

l Be a responsible corporate citizen

AASL

5

DIRECTORS’ REPORT

The Shareholders,

The Directors of your company have pleasure in presenting the Thirty Third Annual Report together with audited Statement of Accounts of Airline Allied Services Ltd. for the year ended 31 March 2016.

1 FINANCIAL AND PHYSICAL PERFORMANCE

The Financial and Physical performance for the year under review vis-a-vis the previous year was as under:

Financial Performance :

(Rs. in Crs.)

2015-16 2014-15

Operating Revenue 268.20 226.63 Schedule Revenue 209.13 179.93 Non schedule revenue 58.64 37.64 Incidental Revenue 00.43 09.06

Other Income 5.66 1.32

Total Revenue 273.86 227.95

Total Expenses 472.61 411.87 Net Profit/(Loss) for the year Before Tax (198.75) (183.92) Net Profit/(Loss) for the year After Tax (198.75) (183.92) Share Capital 402.25 2.25

Physical Performance : 2015-16 2014-15 ASKMs (in millions) 342.639 289.614 RPKMs (in millions) 227.984 197.916 Passengers Carried (in millions) 0.400 0.310 Seat Factor (%) 66.5 68.3 Load Factor (%) 61.7 58.5

In current year, the net loss is higher by Rs. 14.83 crore as company registered a net Loss of Rs.198.75 crores during 2015-16 in comparison with previous year's loss of Rs.183.92 crores. This is mainly attributed to following factors:

1. Increased lease charges by Rs. 43.63 crores due to induction of five new aircraft in the fleet.

2. Upward increase in Maintenance charges by Rs. 37.47 crores due to induction of new aircraft and higher upkeep of old aircraft of the fleet, namely CRJ and ATR- 42.

AASL

6

3. There was upward increase in Landing and Navigation expenses, Catering expenses due to discontinuation of BOB, increase in interest paid to parent company Air India Limited, increase in redelivery charges of returned leased aircraft, appreciation of USD vis-a-vis Indian Rupee.

4. Although the Passenger Revenue increased by Rs.29.61 crores owing to increase in passenger carriage but there was a decline in passenger yield by Rs. 558/- per passenger. Thus, growth remaining stunted.

5. Although ATF cost registered a decrease of Rs.26.31 crores due to fall in average ATF rate but this gain was more than offset by above stated elements of cost. Besides, Sundry Receipts too registered the decline owing to decrease in Maintenance Reserve refunds from the Lessors.

2. DETAILS OF REVISION OF FINANCIAL STATEMENTS OR BOARD'S REPORT

The Company has not revised its Financial Statements or Board's Report in respect of any of the three preceding financial years as mentioned in Section 131 (1) of the act.

3. AMOUNT, WHICH THE BOARD PROPOSES TO CARRY TO ANY RESERVES

The Board of the company has decided/proposed to carry “Nil” amount to its reserves.

4. DIVIDEND

The directors are not recommending any dividend as the company has not earned profits.

5. MAJOR EVENTS DURING THE YEAR

a) State of the company's affairs

Fleet Position

As on 31 March 2016 the fleet of the company comprised 11 leased aircraft as under:- Aircraft Type� No. of Aircraft � Owner� ATR-42-320 03 Leased from M/s Abric Leasing Ltd, Ireland

ATR 72-600 05 Leased from different overseas lessors

Bombardier CRJ-700 03 Leased from different overseas lessors Network/ New Links

As at the year end, the network of the company consisted of 29 domestic stations and the Alliance Air operated around (ATR-72-600-132, ATR-42-38 +CRJ-26 & flights/ week) 196 flights per week.

AASL

7

Technical Reliability

Aircraft-wise Technical Reliability during the year 2015-16 was as under:

a) ATR 72-600� � 99.50% b) ATR 42-320� � 99.41% c) CRJ-700� � � 99.21%

Aircraft Utilization

Aircraft utilization during the year 2015-16 was as under:

a) ATR 72-600� � � 7482:58 BH b) ATR 42-320� � � 5816:16 BH c) CRJ-700� � � 2981:21 BH

The company introduced services on the following new routes/additional flights during the year 2015-16:-

New Flights / Links

i) ATR-72 Aircraft

§ Hyderabad/Vijayawada/Hyderabad-4 flights per week w.e.f. 10 July 2015 to 31 October 2015 (flight restructured to operate as Hyderabad/Vijayawada/Vizag & v.v. w.e.f. 02 November 2015)

§ Hyderabad/Tirupati/Hyderabad- 4 flights per week w.e.f. 10 July 2015 to 31 October 2015. Withdrawn as not meeting operating cost.

§ Mumbai/Diu/Mumbai- 4 times per week w.e.f 25 October 2015.

§ Hyderabad/Vijayawada/Vizag & v.v.- 5 times per week w.e.f 2 November 2015.

§ Mumbai/Surat/Mumbai- 3 times per week w.e.f 25 December 2015.

§ Mumbai/Gwalior/Mumbai- 3 times per week w.e.f 25 December 2015.

§ Delhi/Gorakhpur/Delhi- 6 times per week w.e.f 15 January 2016.

§ Frequency increased to Daily instead of 6 times/ week on Delhi/Kullu/Delhi w.e.f. 27 March 2016.

§ Delhi/Surat/Delhi- 2 Flights per week with ATR 72 w.e.f. 18 February 2016 making Delhi/Surat/Delhi a daily flight (5 flights with CRJ aircraft).

ii) ATR-42-320 Aircraft

§ Bangalore/Puducherry/Bangalore - 6 flights per week w.e.f. 14 April, 2015 to 15 October 2015. Flight operated under VGF. Operations withdrawn as VGF limit was exhausted.

AASL

8

§ Kolkata/Durgapur /Kolkata - 6 flights per week w.e.f. 18 May, 2015 to 20 December 2015. Flight operated under VGF. Withdrawn at the request of Durgapur Airport Authorities.

§ Bangalore/Mysore/Bangalore - 6 flights per week w.e.f. 2 September, 2015 to 17 November 2015. Flight operated under VGF. Operations withdrawn as VGF limit was exhausted.

Operation of flights with VGF support/Charters:

During the year 2015-16, the following flights/routes continued to operate regularly under VGF support program with the respective State Governments/Government agencies.

1. Kochi/Agatti/Kochi with ATR-42 aircraft 6 times per week with support from Lakshadweep Administration.

2. With VGF support from North Eastern Council:

a. Kolkata/Silchar/Tezpur & return 3 times per week with ATR-42 aircraft. b. Kolkata/Guwahati/Lilabari & return 4 times per week with ATR-42 aircraft. c. Kolkata/Shillong/Kolkata 6 times per week with ATR-42 aircraft.

3. Bangalore/ Puducherry /Bangalore - 6 flights per week w.e.f. 14 April, 2015 to 15 October 2015. Flight operated under VGF. Operations withdrawn as VGF limit was exhausted.

4. Kolkata/Durgapur /Kolkata - 6 flights per week with ATR- 42 aircraft w.e.f. 18 May, 2015 to 20 December 2015. Flight operated under VGF support provided by Bengal Aetropolis Private Limited (BAPL). Withdrawn at the request of BAPL.

5. Bangalore/Mysore/Bangalore-6 flights per week with ATR-42 aircraft w.e.f. 2 September, 2015 to 17 November 2015. Flight operated under VGF support from Government of Karnataka. Flights were withdrawn as VGF limit was exhausted.

6. Mumbai/Diu/Mumbai- 4 times per week with ATR-72 aircraft w.e.f 25 October 2015. Flights are being operated under VGF support from Diu Administration.

7. Charter operations on Portblair/Car Nicobar/Portblair sectors with CRJ aircraft once a week continued during the year. Charter flight operated for Andaman and Nicobar Administration. The charters operated regularly. The charter flight was withdrawn w.e.f. 1 August 2016.

Human Resources

The staff strength of the company at the close of the year was 455 (664) excluding 14 (17) employees on deputation from the parent Company, Air India. All the employees of the Company are on fixed term contract basis. Out of the 455 contractual employees, 190 (41.75%) were female employees. Cadre-wise, as on 31 March 2016, there were 77 Pilots, 149 cabin crew and remaining 229 were other categories of employees. The Company has been supplementing cabin crew and other manpower as required by Air India. 40 Employees deputed from AIESL to AASL as on 31 March 2016.

AASL

9

AASL had deployed 169 staff (35 cabin crew, 43 Operations, 04 VHF Operators, 58 Ground & Other Commercial & 29 Security Attendants) till 31 March 2016 on deputation to Air India.

Therefore, Company effectively had 340 (286+14+40) employees at close of the year for in its own operations.

Since the Company could not develop in-house expertise in the field, it had recruited 7 employees on contract who were superannuated from AIL, by virtue of their knowledge and long experience to handle some key positions, to satisfy/meet the regulatory requirements.

As on 31 March 2016, there were total 10 expatriate pilots, out of which (9) expatriate commanders on ATR fleet and 1 expatriate commander on CRJ fleet. Out of these 9 on ATR fleet, 4 were Training Captain. The Company's endeavor is to keep the number of expatriate pilots to bare minimum to maintain minimum mandatory strength of commander vis-à-vis aircraft fleet. There is no expatriate pilot in P2 category.

ATR-42-320/ATR-72-600 Aircraft

Air India Engineering Services Ltd. (AIESL), a wholly owned subsidiary of our parent Company, Air India undertakes maintenance of all our aircraft. Its hangar in Kolkata is the main engineering base for maintenance activities on ATR 42-320 aircraft. The Scheduled Line Maintenance and Major Maintenance activities (upto '4C' Check i.e. 16000 FH) are being carried out by AIESL including special inspections, snag rectifications as per trouble shooting / maintenance manuals for continued airworthiness of the aircraft.

The base has capability for carrying out replacement of main elements of the aircraft i.e. engines, landing gears, propellers and Structural Repair etc. which are major maintenance tasks. Infrastructure and capability has been developed to carry out '1C' Check (4000 FH), '2C' Check (8000 FH), '4C' Check (16000 FH) & '8' yearly check. The structural integrity of the aircraft is ensured by carrying out by Environmental Damage (Corrosions) and Fatigue Damage inspections.

ATR 42-320 aircraft is being operated from Bangalore also. AIESL Delhi, Kolkata, Mumbai and Hyderabad base have the capability to carry out maintenance up to 'A' Check on ATR 72-600 aircraft. MRO AIESL, Hyderabad is in the process of developing its facilities to have capability to carry out 'C' check on ATR 72-600 aircraft.

ATR- Engine Repair Facilities

Alliance Air does not have any Repair / Refurbishment / Performance restoration facility for PW121/127M engine of ATR aircraft and CF34-8C engine of CRJ 700 aircraft. The repair of PW 121/127M engine has been outsourced to M/s Pratt and Whitney, (Original Engine Manufacturer) and that of CRJ 34-8C Engine to M/s.GE (Original Engine Manufacturer).

ATR Component Shop Facilities Alliance Air does not have any facilities for repair of components. There is no plan in future to develop any such facility either for component or for engines as it is not cost effective.

Bombardier CRJ 700 Aircraft

Delhi is the main engineering base for maintenance activities on CRJ 700 aircraft. The Main base has infrastructure and capability to carry out checks till '6A' check. Heavy maintenance ('C' check) of CRJ-700 aircraft is outsourced to a FAA/EASA approved MRO as per the requirements of lease arrangements.

AASL

10

Technical Training Type Refresher Course for Engineers both for ATR-42-320 and CRJ-700 are carried out in-

house at Air India Engineering Training School. General refresher for engineers is also conducted in-house at Air India Engineering Training School. Differential type training for some engineers for newly inducted ATR-72-600 was conducted at manufacturer's facility at Toulouse. Now Type training for ATR-72-600 also is being conducted in-house at Air India Engineering Training School.

Future Perspective

The fleet of Alliance Air comprises 11 aircraft (03 ATR-42-320, 05 ATR-72-600 and 03 CRJ 700 aircraft) on lease. 03 CRJ-700 are being prepared for re-delivery to lessors on the expiry of their lease term. As per plan 03 more ATR-72-600 aircraft have been inducted in 2016-17 into AASL on lease of 12 years. Negotiations with L1 bidder, on the lease terms, for induction of new 10 more ATR-72-600 is under process. 01 ATR 42-320 aircraft VT-ABO (MSN 406) was hit by Jet airways bus and the insurance claim and settlement with Jet Airways is under process. The extension of lease of 02 ATR-42-320 aircraft is being considered for a period of 6-12 months (from the date of expiry of their lease term on 31.03.17) to maintain existing operations, including NE and Agatti.

Further, as per Turn Around Plan (TAP) of AIL, Alliance Air shall have a fleet of 40 Turbo prop aircraft by the year 2020.

Flight Safety

The Company has an independent Flight Safety Department which functions as per the DGCA requirements in proactive manner. Flight Safety Department carries out preventive and investigative functions for the Airline. The preventive functions include, the cockpit voice recorder monitoring, flight data recorder monitoring and Internal Safety Audits of the stations, being operated by Airline which includes Airfield Inspection, Spot Checks, Ramp Inspection and Cockpit Surveillance Checks at regular interval.

All reported incidents are investigated by the Permanent Investigation Board (PIB) of the Company and the recommendations of PIB are included in the operation procedures and policy to prevent recurrences. The investigations of incidents are carried out along with DGCA representatives and no PIB cases of the financial year 2015-16 are pending.

During the financial Year 2015-16, Alliance Air had no occurrence, classified as serious incident on CRJ-700 aircraft, ATR-42-320 and ATR-72-600 aircraft. To ensure safety of aircraft, following measures are taken up by Flight Safety Department:-

l The procurement of FOQA system for new ATR 72-600 aircraft fleet in the year 2016.

l The flight occurrences which are classified as incidents by the regulatory norms are investigated by the Investigation Board of the Airline in coordination with the Air Safety Directorate of the DGCA.

l The recommendations of Investigation Board are circulated to the respective departments for their compliance to the applicable recommendations.

AASL

11

l The Airline has facility for downloading the data from the flight data recorder and same is monitored by Flight Safety Department.

l Regular Internal Safety Audit is conducted for safety evaluations of the Airline and the findings are reported to the concerned departments and the DGCA.

l Load and Trim Sheet of ATR-72-600, CRJ-700 & ATR 42-320 aircraft fleet are being monitored on monthly basis.

l Ramp Inspection/Spot Check of Base Stations/ Line Stations are carried out randomly.

l Safety inspection of Line stations are being carried out as per direction of DGCA.

l Recommendations of DGCA is Annual Air Safety review meet are being emphasized during counseling of Pilots.

Training

Alliance Air has upgraded 1 ATR co-pilot into Commander and 1 ATR co-pilot is undergoing PIC upgrade training. With our planned training measures and conversion of some of co-pilots into commander, we were able to keep the number of foreigners (Expatriates) commanders/ trainer/examiner to bare minimum level.

Inventory Control

Aircraft inventory consisting of aircraft spare parts and consumable items is monitored and controlled through computerized RAMCO software, which is used for both AIESL and AASL inventories. AIESL exercises its procurement and control procedures for AASL inventories also.

Plan for 2016-17

Out of the fleet of Five ATR 72-600, three new ATR 72-600 aircraft were inducted during the year 2015-16. Three more ATR 72-600 aircraft have been inducted till 15 August, 2016 making it a fleet of 8 ATR 72-600 aircraft as on date. As stated earlier, induction of 10 more ATR 72-600 aircraft is under process. These aircraft are proposed to be deployed on Tier 2 & 3 cities to improve regional connectivity as proposed in the New National Civil Aviation Policy envisaged by Ministry of Civil Aviation.

Use of Hindi

To fulfill the objectives of the Official Language policy of the Government, the Company played its role in promoting the usage of Hindi at all levels. Staff were encouraged to work in Hindi. To promote Hindi, a Hindi Pakhwara is conducted every year, wherein employees participate in various competition categories like essay writing, poem reciting etc. Prizes and awards are distributed during the function.

Contribution to Exchequer

The Company has contributed Rs. 2.18 cores (Rs. 3.32 crores) to Government exchequer by way of Sales Tax and other levies on Aviation Turbine Fuel.

AASL

12

b) Change in the nature of business

The Company has not commenced any new business or discontinued any of its existing business during the year.

c) Material changes and commitments, if any, affecting the financial position of the company which have occurred between the end of the financial year of the company to which the Financial Statements relate and the date of the Report.

� � No such material changes or commitments made affecting the financial position of the Company during the intervening period from April 2016 to December 2016.

6. GENERAL INFORMATION AND FUTURE OUTLOOK

Airline Allied Services Limited which had been set up in 1983 by erstwhile Indian Airlines, started airline operations with B737 aircraft under the brand name of Alliance Air in April 1996. These aircraft were taken on dry lease from erstwhile Indian Airlines.

The passenger aviation market in India has recorded a steady growth of around 20-22% in the last year. This has been possible due to induction of capacity by all airlines and also fares becoming more affordable. The growth in Tier 2 & 3 cities is still largely untapped, as larger airlines have focused on trunk routes and operate larger capacity aircraft which are not suitable for serving in smaller airports.

Alliance Air has the advantage of operating ATR type of aircraft since January 2003. It intends to build on this experience of over a decade of serving to Tier 2 & 3 cities. The average age of the ATR-42 type of aircraft of the fleet is about 20 years. Alliance Air has inducted 04 ATR-72-600 aircraft in its fleet in the year 2015/2016. With the induction of these aircraft. Alliance Air has commenced services on many new routes like Mumbai/Surat, Mumbai/Gwalior, Delhi/Gorakhpur, Mumbai/Diu, Hyderabad/ Vijayawada/ Vizag. We propose to induct more ATR-72 aircraft in the fleet. The Turn Around Plan of Air India approved by Government of India envisages a fleet of 40 turbo prop aircraft to be inducted by year 2020/2021. Addition of more aircraft will enable operations of increased flights to smaller cities, so that it complements the operations of Air India from major cities. Apart from introduction of services to new small routes, ATR-72 will enable up-gradation of existing routes on ATR-42 to this aircraft.

7. CAPITAL STRUCTURE

7.1 Details of equity shares issued

During the financial year, the company has allotted 4,00,00,000 (Four Crores) Equity Shares of Rs. 100/- each at par, aggregating to Rs. 4,00,00,00,000 (Four Hundred Crores) to Air India Ltd on rights basis.

8. MANAGEMENT

8.1 Directors and Key Managerial Personnel (KMP)

The following changes have occurred in the constitution of Directors and KMP of the Company during the FY 2015-16.

AASL

13

S.No Name Designation Date of Date of Appointment Cessation

1. Shri Rohit Nandan Chairman - 31.08.2015

2. Shri Ashwani Lohani Chairman 31.08.2015 -

3. Capt. A.K. Govil Director - 18.08.2015

4. Capt Arvind Kathpalia Director 30.09.2015

5. Shri S Venkat Director - 31.10.2015

6. Shri Vinod S. Hejmadi Director 20.11.2015 -

7. Shri Sunil Dua Chief Finance 24.06.2015 31.10.2016 Officer

Facts Of Resignation Of Director [Section 168(1)]

There was no incident of resignation by any Director of the Company during the FY 2015-16.

8.2 Number of Meetings of the Board of Directors

During the Financial Year 2015-16, the Company held seven meetings (including adjourned & re-adjourned meetings) of the Board of Directors as per Section 173 of Companies Act, 2013 which is summarized below.

S No. Date of Meeting Board Strength No. of Directors Present

1 24.06.2015 7 6

2 07.07.2015 7 5

3 14.08.2015 7 7

4 22.09.2015 6 5

5 08.10.2015 7 7

6 19.11.2015 7 6

7 10.03.2016 7 5

8.3 Composition of Committees and details of changes, if any

AUDIT COMMITTEE

The constitution of Audit Committee as required under the Companies Act, 2013 was approved by the Board of Directors in its 133 Meeting held on 24 December 2014 and following were its members as on 31 March 2016:

AASL

14

Smt. (Dr.) Shefali Juneja � � -� Chairperson*Ms. Puja Jindal� � � -� MemberShri Vinod S. Hejmadi�� -� MemberShri Ashwani Lohani � � -� Permanent Invitee

*Ms. Puja Jindal ceased to be the member of the Committee w.e.f. 8 April 2016 in her ex-officio capacity.

Appointment of Independent Directors & Declaration

As there was no Independent Director on the Board of AASL, the matter had been taken up with the Ministry of Civil Aviation by Air India Limited.

NOMINATION, REMUNERATION AND STAKEHOLDERS RELATIONSHIP COMMITTEE

The Constitution of Nomination and Remuneration Committee shall be taken up after the appointment of Independent Directors by Holding Company/Administrative Ministry.

8.4 Company's Policy on Director's appointment and remuneration

Appointment Policy

The Company being wholly owned subsidiary of Air India Ltd., the appointment of directors is done by Holding Company i.e. Air India in consultation with Administrative Ministry.

Remuneration Policy

Section 197 in respect of remuneration to Directors of the Company is not applicable to AASL, being a Government Company Vide Notification No. G.S.R.463(E) dated 5 June 2015.

8.5 Board Evaluation

It is not applicable to AASL, being a Government Company Vide Notification No. G.S.R. 463(E) Dated 5 June, 2015.

8.6 Remuneration received by Managing / Whole time Director from holding or subsidiary company

There was no whole time Director on the Board of the Company during FY 2015-16.

8.7 Directors' Responsibility Statement

The Board of Directors of the Company confirm:-

(a) That in the preparation of the Annual Accounts, the applicable Accounting Standards have been followed along with proper explanation relating to material departures;

AASL

15

(b) The Directors have selected such accounting policies and applied them consistently and made judgments and estimates that are reasonable and prudent so as to give a true and fair view of the state of affairs of the Company at the end of the financial year and of the profit and loss of the Company for that period;

(c) The Directors have taken proper and sufficient care for the maintenance of adequate accounting records in accordance with the provisions of the Act for safeguarding the assets of the Company and for preventing and detecting fraud and other irregularities;

(d) The Directors have prepared the Annual Accounts on a going concern basis;

(e) Company being unlisted sub clause (e) of section 134(3) is not applicable.

(f) The Directors have devised proper systems to ensure compliance with the provisions of all applicable laws and that such systems are adequate and operating effectively.

8.8 Internal financial controls

AASL appointed M/s MGC & KNAV, Global Risk Advisors LLP to conduct a risk management assessment for the purpose of Internal Financial Control on various process and activities for the year 2015-16 and submitted a fair report with various suggestions and recommendation to be implemented in 2016-17. The report was shared with statutory auditors of the Company for their comments thereon.

8.9 Disclosure regarding frauds

There are no frauds reported by the Auditor to the Audit Committee or to the Board.

9. DISCLOSURES RELATING TO SUBSIDIARIES, ASSOCIATES AND JOINT VENTURES

Company does not have any Subsidiary, Joint Venture or Associate Company.

10. DETAILS OF DEPOSITS The Company has not accepted any public deposits during the year ended 31 March 2016 as covered

under the provisions of Section 76 of the Companies Act, 2013 read with the Companies (Acceptance of Deposits) Rules, 2014.

11. PARTICULARS OF LOANS, GUARANTEES AND INVESTMENTS

Particulars of loans, guarantees and investments have been disclosed in the financial statement.

12. PARTICULARS OF CONTRACTS OR ARRANGEMENTS WITH RELATED PARTIES

All related party transactions that were entered into during the financial year were on an arm's length basis and were in the ordinary course of business. There are no materially significant related party transactions made by the Company with Promoters, Directors, Key Managerial Personnel or other designated persons which may have a potential conflict with the interest of the Company at large and Approval of the Board of Directors was obtained wherever required.

AASL

16

Company does not have any details of transaction entered with the related parties which are required to be attached in Form No. AOC-2.

13. DISCLOSURES PERTAINING TO CORPORATE SOCIAL RESPONSIBILITY

Provisions of Section 135 of Companies Act, 2013 relating to Corporate Social Responsibility is not applicable to the Company as the Company has not earned any profits during the year.

14. DETAILS OF REMUNERATION OF EMPLOYEES

Section 197 read with Rule 5 of The Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014 in respect of employees of the Company is not applicable to AASL, being a Government Company, vide Notification No. G.S.R.463(E) dated 5 June 2015.

15. CONSERVATION OF ENERGY, TECHNOLOGY ABSORPTION, FOREIGN EXCHANGE EARNINGS AND OUTGO

(A) The particulars as required under the provisions of Section 134(3) (m) of the Companies Act, 2013 in respect of conservation of energy and technology absorption have not been furnished considering the nature of activities undertaken by the Company during the year under review.

(B) Foreign exchange earnings and Outgo

(Rs. in Crores)

Earnings NIL

Outgo 167.06

16. RISK MANAGEMENT Since the revenue of AASL is tied up through its parent company Air India and the parent company is

having adequate risk management policy in case of sales through Agents, credit cards etc; by establishing a Capping monitoring policy, Bank Guarantee policy, Risk monitoring through Risk engine attached to web portal, AASL being 100 percent subsidiary is not prone to high business risk. Moreover, the IFCR for AASL for 2015-16 is being done for which AASL is taking necessary steps as recommended in the report.

Therefore, the Company does not have any Risk Management Policy yet as the element of risk

threatening the Company's existence is very minimal.

17. MATERIAL ORDERS OF REGULATORS

No significant and material orders have been passed by the regulators or courts or Tribunals impacting the going concern status and Company's operation in future during the year.

18. DETAILS OF ESTABLISHMENT OF VIGIL MECHANISM

Provisions of Section 177(9) read with rule 7(1) of Companies (Meetings of Board and its powers) Rules 2014 relating to establishment of Vigil Mechanism for directors and employees, to report a genuine concern, are not applicable to the Company as the Company has not accepted any deposits or borrowed any money from banks in excess of specified amount.

AASL

17

19. AUDITORS

The Comptroller & Auditor General of India (CAG), has appointed M/s. Chandra Gupta & Associates, Chartered Accountants as Statutory Auditors of the Company for FY 2015-16.

Qualifications or adverse remarks in the Auditors' Report which require any clarification/ explanation along with reply of management thereto are attached.

The Notes on financial statements are self-explanatory and needs no further explanation.

20. COMMENTS OF COMPTROLLER AND AUDITOR GENERAL OF INDIA

The comments of Comptroller and Auditor General of India (C&AG) as required under Section 143(6)(b)

of the Companies Act, 2013 on the accounts of the Company for the year ended 31 March 2016 are attached.

21. SECRETARIAL AUDIT REPORT

The Company appointed Mr. Jiwan Parkash Saini, Practicing Company Secretary, as Secretarial Auditor to conduct the Secretarial Audit for FY 2015-16. The Secretarial Audit Report (Form No. MR.3) is attached.

The explanations or comments by the Board on every qualification, reservation or adverse remark or disclaimer made by the auditor in his report are also attached.

22. COMPLIANCE WITH SECRETARIAL STANDARDS

The Secretarial Standards issued by ICSI under Section 118(10) of Companies Act, 2013 have been complied with by the Company.

23. DETAILS OF SICKNESS OF THE COMPANY

The Company is not a sick Company. Hence details not applicable.

24. EXTRACT OF ANNUAL RETURN

In compliance with the provisions of Section 92(3) of the Companies Act, 2013 read with Rule 12(1) of the Companies (Management and Administration) Rules, 2014, extract of Annual Return is attached.

25. DISCLOSURES UNDER THE SEXUAL HARASSMENT OF WOMEN AT THE WORKPLACE (PREVENTION, PROHIBITION & REDRESSAL) ACT, 2013

The details of sexual harassment cases reported in the Company during the financial year, are as under:-

1) No complaint of sexual harassment was received during the relevant year.

2) Number of cases pending for more than ninety days are Nil.

AASL

18

Number of workshops or awareness programmes carried out in connection with sexual harassment: General awareness programmes is normally conducted periodically. Besides this, posters on sexual

harassment are being displayed at work places.

Remedial measures taken by the company :

A Committee is being formed to deal with the complaints and also spread awareness in the organization.

26. COMPLIANCE WITH RTI ACT, 2005

The Company being a public sector enterprise has successfully ensured compliance with the provisions of Right to Information Act, 2005 for providing information to the citizens.

The Company has a CPIO (Central Public Information Officer) and Appellate Authority for timely disposal of applications and appeals.

During 2015-16, 20 Requests / Appeals were received and 19 have been disposed off.

27. TRANSFER OF UNCLAIMED DIVIDEND TO INVESTOR EDUCTION AND PROTECTION FUND

The provisions of Section 125(2) of the Companies Act, 2013 do not apply as there was no dividend declared and paid last year.

28. CORPORATE GOVERNANCE

The Company has complied with the requirements of Corporate Governance with the exception of appointment of Independent Directors on the Board. This matter is being pursued by the Holding company i.e. Air India Ltd. with the Administrative Ministry.

A detailed Corporate Governance Report forms part of this Annual Report separately.

29. ACKNOWLEDGEMENTS

Board sincerely acknowledges the support and guidance received from the Ministry of Civil Aviation, Comptroller and Auditor General of India, Ministry of Corporate Affairs and other agencies.

For and on behalf of the Board of Directors

Sd/- ASHWANI LOHANI ChairmanPlace : New DelhiDate : 21 March 2017�

AASL

19

Annexure to Directors' Report for the year 2015-16 Annexure-I

FORM NO. MGT 9 EXTRACT OF ANNUAL RETURN

As on financial year ended 31.03.2016 Pursuant to Section 92 (3) of the Companies Act, 2013 and rule 12(1) of the Companies

(Management & Administration) Rules, 2014.

I. REGISTRATION & OTHER DETAILS:

II. PRINCIPAL BUSINESS ACTIVITIES OF THE COMPANY (All the business activities contributing 10 % or more of the total turnover of the company shall be stated) -

1. CIN U51101DL1983GOI016518

2. Registration Date 13/09/1983

3. Name of the Company AIRLINE ALLIED SERVICES LIMITED (AASL)

4. Category/Sub-category of the Company

Government Company

5. Address of the Registered office & contact details

OLD LUFTHANSA HANGER BUILDING, (ADJECENT TO ED-NR OFFICE), IGI AIRPORT, T-1, NEW DELHI- 110037

6 Whether listed company No

7. Name, Address & contact details of the Registrar & Transfer Agent, if any.

N.A.

Sr No

Name and Description of main products / services NIC Code

of the Product/

service

% to total turnover of

the company

1

To establish, maintain and operate international and domestic air transport services, scheduled and non scheduled, in all the countries of the world for the carriage of passengers, meals and freight and for

any other purposes.

621 100

III. PARTICULARS OF HOLDING, SUBSIDIARY AND ASSOCIATE COMPANY:

Sr. No.

Name and Address of the Company

CIN/GIN

Holding / Subsidiary / Associate

% of Shares

Applicable Section

1 Air India Limited 113, Airlines House, Gurudwara Rakabganj Road, New Delhi, 110 001.

U62200DL2007GOI161431

Holding

100%

2 (46)

AASL

20

IV. SHARE HOLDING PATTERN (Equity Share Capital Breakup as percentage of Total Equity) : Category-wise Share Holding

Category of Shareholders

No. of Shares held at the beginning of the year

[As on 01-04-2015]

No. of Shares held at the end of the year [As on 31-03-2016] %

Change during

the year

Demat

Physical

During the year

% of Total

Shares Demat Physical Total

% of Total

Shares

A. Promoters

(1) Indian

a) Individual/ HUF - - - - - - - - -

b) Central Govt - - - - - - - - -

c) State Govt(s) - - - - - - - - -

d) Bodies Corp. - 2,25,000 4,00,00,000 100 - 40,225,000 40,225,000 100 0.00

e) Banks / FI - - - - - - - - -

f) Any other - - - - - - - - -

Total shareholding of Promoter (A)

- 2,25,000 4,00,00,000 100 - 40,225,000 40,225,000 100 0.00

B. Public Shareholding Not Applicable

1. Institutions

a) Mutual Funds/UTI - - - - - - - - -

b) Banks / FI - - - - - - - - -

c) Central Govt. - - - - - - - - -

d) State Govt.(s) - - - - - - - - -

e) Venture Capital Funds

- - - - - - - - -

f) Insurance Companies

- - - - - - - - -

g) FIIs - - - - - - - - -

h) Foreign Venture Capital Funds

- - - - - - - - -

i) Others (specify) Foreign Banks

- - - - - - - - -

Sub-total (B)(1):- - - - - - - - - -

AASL

21

Category of Shareholders

No. of Shares held at the beginning of the year [As on 01-04-2015]

No. of Shares held at the end of the year [As on 31-03-2016]

% Change during

the year

Demat

Physical

Total

% of Total

Shares

Demat

Physical

Total

% of Total

Shares

2. Non-Institutions Not Applicable

a) Bodies Corp.

(Market Maker +

LLP)

i) I Indian - - - - - - - - - ii) Overseas - - - - - - - - - b)

Individuals

i)

Individual

shareholders

holding nominal

share capital upto

Rs. 1 lakh

-

-

-

-

-

-

-

-

-

ii)

Individual

shareholders

holding nominal

share capital in

excess of Rs.

1 lakh

-

-

-

-

-

-

-

-

-

c)

Others (specify)

i)

Non Resident

Indians

-

-

-

-

-

-

-

-

-

ii)

Non Resident

Indians -

Non

Repatriable

-

-

-

-

-

-

-

-

-

iii)

Office Bearers

-

-

-

-

-

-

-

-

-

iv)

Directors

-

-

-

-

-

-

-

-

-

v)

HUF

-

-

-

-

-

-

-

-

-

vi)

Overseas

Corporate Bodies

-

-

-

-

-

-

-

-

-

vii)

Foreign Nationals

-

-

-

-

-

-

-

-

-

viii)

Clearing

Members

-

-

-

-

-

-

-

-

-

ix)

Trusts

-

-

-

-

-

-

-

-

-

x)

Foreign Bodies -

D R

-

-

-

-

-

-

-

-

-

Sub-total (B)(2):-

-

-

-

-

-

-

-

-

-

Total Public Shareholding (B) = (B)(1)+ (B)(2)

-

-

-

-

-

-

-

-

-

C.

Shares held by

Custodian for

GDRs & ADRs

-

-

-

-

-

-

-

-

-

Grand Total (A+B+C)

2,25,000

4,00,00,000

100

-

40,225,000

40,225,000

100

0.00

AASL

22

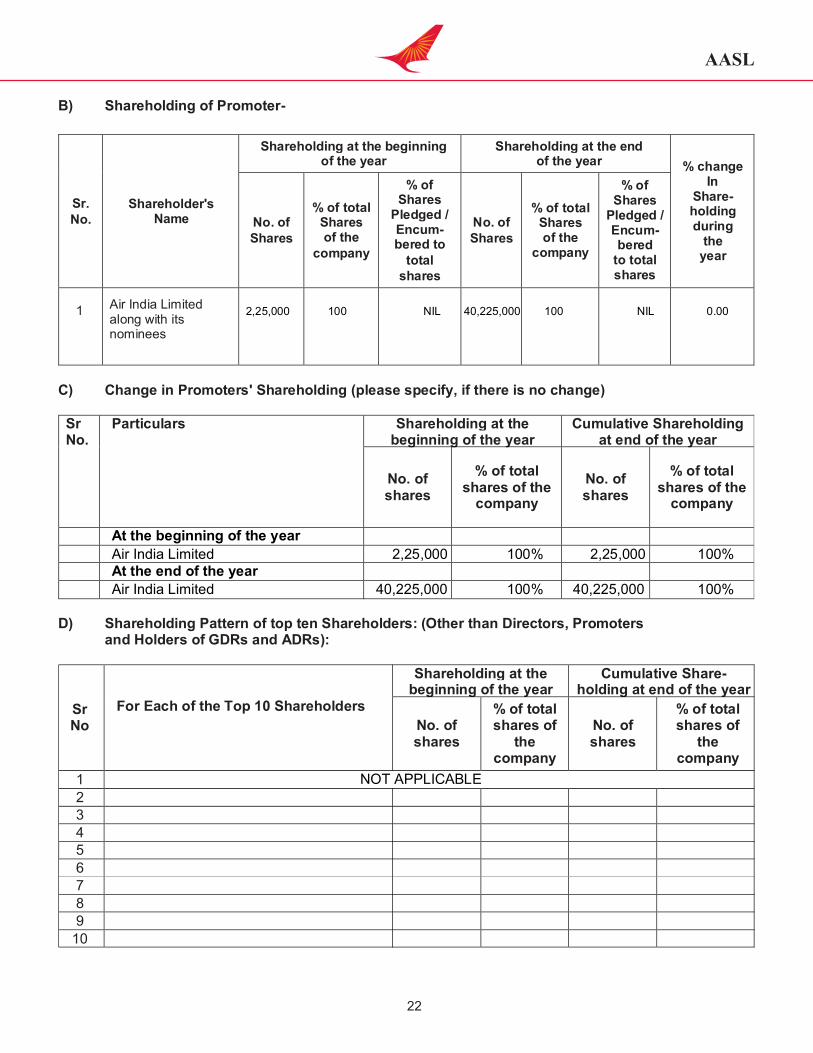

B) Shareholding of Promoter-

C) Change in Promoters' Shareholding (please specify, if there is no change)

Sr No.

Particulars Shareholding at the beginning of the year

Cumulative Shareholding at end of the year

No. of shares

% of total shares of the

company

No. of shares

% of total shares of the

company

At the beginning of the year

Air India Limited 2,25,000 100% 2,25,000 100% At the end of the year

Air India Limited 40,225,000 100% 40,225,000 100%

D) Shareholding Pattern of top ten Shareholders: (Other than Directors, Promoters and Holders of GDRs and ADRs):

Sr. No.

Shareholder's Name

Shareholding at the beginning of the year

Shareholding at the end of the year % change

In Share- holding during

the year

No. of Shares

% of total Shares of the

company

% of Shares

Pledged / Encum- bered to

total shares

No. of Shares

% of total Shares of the

company

% of Shares

Pledged / Encum- bered

to total shares

1 Air India Limited

along with its

nominees

2,25,000

100

NIL

40,225,000

100

NIL

0.00

Sr No

For Each of the Top 10 Shareholders

Shareholding at the beginning of the year

Cumulative Share-holding at end of the year

No. of shares

% of total shares of

the company

No. of shares

% of total shares of

the company

1 NOT APPLICABLE

2

3

4 5

6

7

8

9

10

AASL

23

E) Shareholding of Directors and Key Managerial Personnel:

S. No.

Shareholding of each Directors and each Key Managerial Personnel

Shareholding at the beginning of the year

Cumulative Shareholding at the end of year

No. of shares

% of total shares of

the company

No. of shares

% of total shares of

the company

NIL

Total

V. INDEBTEDNESS -Indebtedness of the Company including interest outstanding/accrued but not due for payment.

(Rs. in Crore)

Secured Loans

excluding deposits

Unsecured Loans

Deposits Total

Indebtedness

Indebtedness at the beginning of the financial year

i) Principal Amount

ii) Interest due but not paid

iii) Interest accrued but not due

Total (i+ii+iii)

Change in Indebtedness during the financial year

* Addition

* Reduction

Net Change

Indebtedness at the end of the financial year

i) Principal Amount

ii) Interest due but not paid

iii) Interest accrued but not due

Total (i+ii+iii)

- 10,551,004,433 - 10,551,004,433

- - - -

- - - -

- 10,551,004,433 - 10,551,004,433

33,572,817 -

- -

33,572,817 -

- 10,584,577,250 - 10,584,577,250

- - - -

- - - -

- 10,584,577,250 - 10,584,577,250

AASL

24

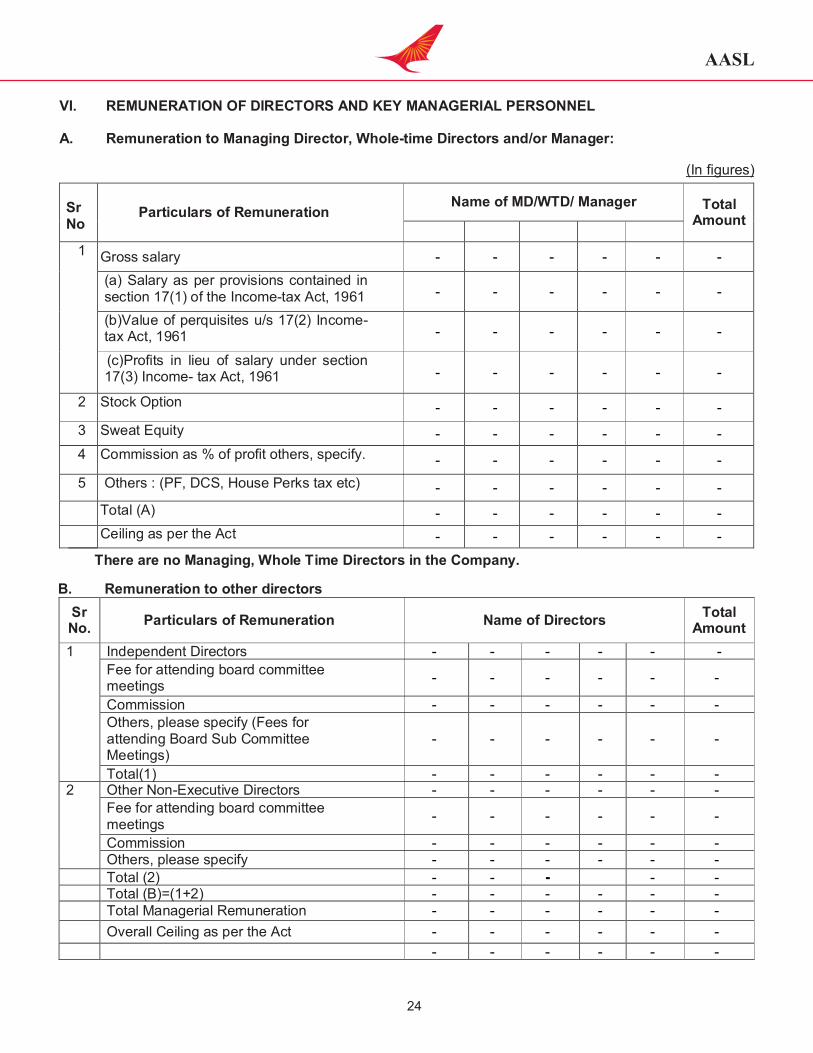

VI. REMUNERATION OF DIRECTORS AND KEY MANAGERIAL PERSONNEL A. Remuneration to Managing Director, Whole-time Directors and/or Manager:

(In figures)

Sr No

Particulars of Remuneration Name of MD/WTD/ Manager Total

Amount

1 Gross salary - - - - - -

(a) Salary as per provisions contained in section 17(1) of the Income-tax Act, 1961 - - - - - -

(b)Value of perquisites u/s 17(2) Income-tax Act, 1961 - - - - - -

(c)Profits in lieu of salary under section 17(3) Income- tax Act, 1961 - - - - - -

2 Stock Option - - - - - -

3 Sweat Equity - - - - - -

4 Commission as % of profit others, specify. - - - - - -

5 Others : (PF, DCS, House Perks tax etc) - - - - - -

Total (A) - - - - - -

Ceiling as per the Act - - - - - -

There are no Managing, Whole Time Directors in the Company.

B. Remuneration to other directors

Sr No.

Particulars of Remuneration Name of Directors Total

Amount

1 Independent Directors - - - - - -

Fee for attending board committee meetings

- - - - - -

Commission - - - - - - Others, please specify (Fees for attending Board Sub Committee Meetings)

- - - - - -

Total(1) - - - - - - 2 Other Non-Executive Directors - - - - - -

Fee for attending board committee meetings

- - - - - -

Commission - - - - - - Others, please specify - - - - - -

Total (2) - - - - - Total (B)=(1+2) - - - - - - Total Managerial Remuneration - - - - - -

Overall Ceiling as per the Act - - - - - -

- - - - - -

AASL

25

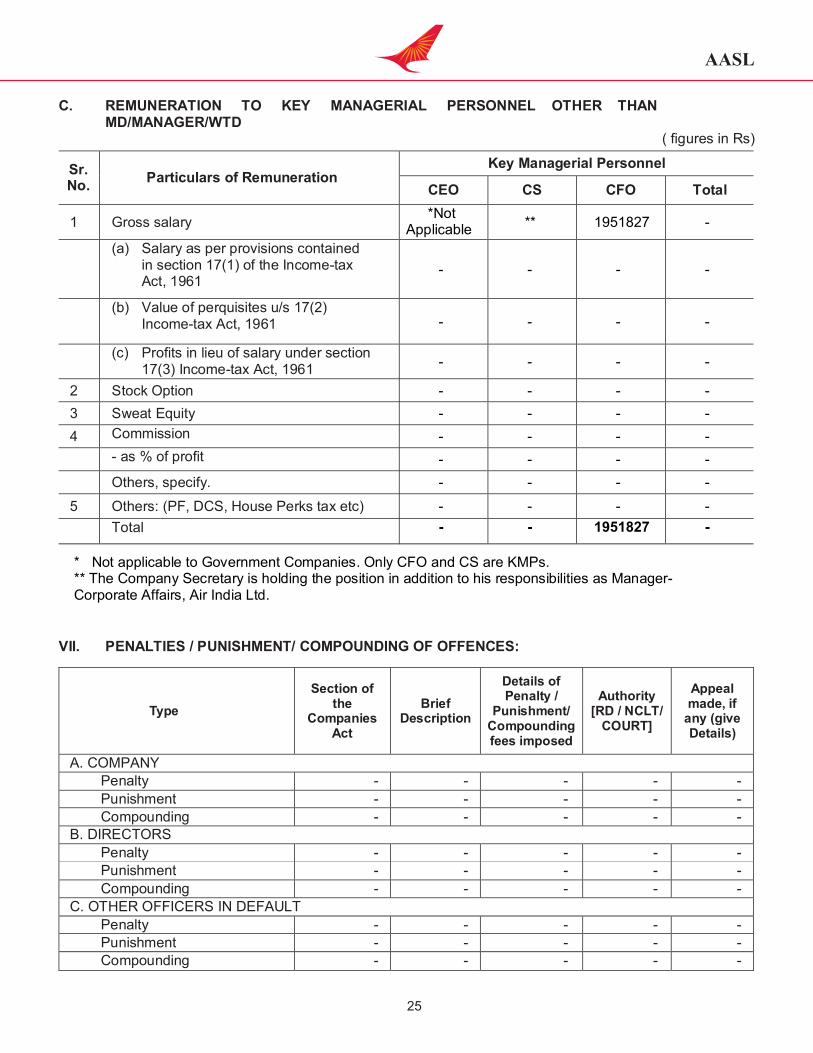

VII. PENALTIES / PUNISHMENT/ COMPOUNDING OF OFFENCES:

Type

Section of the

Companies Act

Brief Description

Details of Penalty /

Punishment/ Compounding fees imposed

Authority [RD / NCLT/

COURT]

Appeal made, if

any (give Details)

A. COMPANY

Penalty - - - - -

Punishment - - - - -

Compounding - - - - - B. DIRECTORS

Penalty - - - - -

Punishment - - - - -

Compounding - - - - -

C. OTHER OFFICERS IN DEFAULT

Penalty - - - - -

Punishment - - - - -

Compounding - - - - -

C. REMUNERATION TO KEY MANAGERIAL PERSONNEL OTHER THAN MD/MANAGER/WTD

* Not applicable to Government Companies. Only CFO and CS are KMPs. ** The Company Secretary is holding the position in addition to his responsibilities as Manager-Corporate Affairs, Air India Ltd.

( figures in Rs)

Sr. No.

Particulars of Remuneration Key Managerial Personnel

CEO CS CFO Total

1 Gross salary *Not

Applicable ** 1951827 -

(a) Salary as per provisions contained in section 17(1) of the Income-tax Act, 1961

- - - -

(b) Value of perquisites u/s 17(2)

Income-tax Act, 1961 - - - -

(c) Profits in lieu of salary under section

17(3) Income-tax Act, 1961 - - - -

2 Stock Option - - - -

3 Sweat Equity - - - -

4 Commission - - - -

- as % of profit - - - -

Others, specify. - - - -

5 Others: (PF, DCS, House Perks tax etc) - - - -

Total -

-

1951827

-

AASL

26

SECRETARIAL AUDIT REPORTFOR THE FINANCIAL YEAR ENDED 31ST MARCH, 2016

(Pursuant to Section 204 (1) of the Companies Act, 2013 and rule No.9 of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014)

To,The Members,Airline Allied Services LimitedOld Lufthansa Hanger Building, (Adjacent To Ed-Nr Office), IGI Airport, T-1,New Delhi – 110037.

I have conducted the secretarial audit of the compliance of applicable statutory provisions and the adherence to good corporate practices by Airline Allied Services Limited (CIN:U51101DL1983GOI016518) (hereinafter called the Company). Secretarial Auditwas conducted in a manner that provided me a reasonable basis for evaluating the corporate conducts / statutory compliances and expressing my opinion thereon.

Based on my verification of the Airline Allied Services Limited's books, papers, minute books, forms and returns filed and other records maintained by the company and also the information provided by the company, its officers, agents and authorised representatives during the conduct of secretarial audit and as per the explanations given to me and the representations made by the Management, I hereby report that in my opinion, the Company has, during the audit period covering the financial year ended on 31st March, 2016 generally complied with the statutory provisions listed hereunder and also that the Company has proper Board processes and compliance mechanism in place to the extent, in the manner and subject to the reporting made hereinafter:

A. I have examined the books, papers, minute books, forms and returns filed and other records made available to me and maintained by the company for the financial year ended on 31st March, 2016 according to the applicable provisions of:

i. The Companies Act, 1956 and the Companies Act, 2013 ('the Act') and the rules made there under;

During the period under review the Company has complied with the provisions of the Companies Act, 1956 and the Companies Act, 2013 ('the Act') and the rules made there under, as applicable, subject to the following observations:

a) There were few instance of delay in filing of e-forms under the Companies Act, 1956 and the Companies Act, 2013 ('the Act') and the rules made there under, but they were regularised by payment of additional fees under the Act.

b) Company has not appointed Independent directors pursuant to sub-section 4 of section 149 of Companies Act, 2013 , hence no meeting of independent directors could be held during the period under audit. Since, the company has not appointed independent directors , the company has not complied with the provisions of section 177(2) and 178 of Companies Act, 2013 read with Rule 6 of Companies( Meetings of Board and its Power) Rules, 2014 as regard the appointment of Independent directors in composition of the Audit Committee.

c) Company has not constituted Remuneration and Nomination Committee of the Board pursuant to 178of Companies Act, 2013 read with Rule 6 of Companies( Meetings of Board and its Power) Rules, 2014 as it meets the prescribe criteria as mentioned in Rule 6.

AASL

27

Queries raised by Statutory auditors of the company in Audit Observations in relation to compliance of Companies Act, 2013 which has been replied by the Management in Directors Report have not been reproduced here.

B. In aviation sector, following laws are specifically applicable to the Company:

l Aircraft Act, 1934

l Carriage by Air Act, 1972

l Tokyo Convention Act, 1975

l Anti-Hijacking Act, 1982

l Suppression of Unlawful Acts against Safety of Civil Aviation Act, 1982

l Civil Aviation Requirements issued by DGCA

Director General of Civil Aviation vide circular dated 21.12.2011 in connection with regulatory audit policy and programme under which regulatory audit are being carried out with an aim to carry out to ascertain the internal control of a organisation in its activities and to ensure compliance of regulatory requirements. It is explained by the company that the Regulatory audit of the company is done by the audit team of DGCA as per the audit programme and audit procedure as prescribed under regulatory audit policy of DGCA .

The Regulatory Audit Program (RAP) has been developed to promote conformance with the aviation regulations and standards that collectively prescribe an acceptable level of aviation safety. It also ensures that Civil Aviation audit policies and procedures are applied uniformly.

Regulatory Audits are conducted for the grant of approvals for Initial Certification, Additional Approval, Routine Conformance and Special Purpose Audit pursuant to the Aircraft Act1934. The Director General of Civil Aviation or any other officer specially empowered in his behalf by the Central Government shall perform the safety oversight functions in respect of matters specified in this Act or the Rules made there under.

The Joint Director General Civil Aviation nominated by the Director General is responsible for all regulatory audits and inspections and is normally the Convening Authority.

The type of audits are Initial Certification Audit , Additional Approval Audit, Routine Conformance Audit and Special-Purpose Audit and is determined by the circumstances under which the audit is convened.

Regulatory audit includes Check Lists for of Airworthiness Audit policy and procedures and Operations audit policy and procedures .

DGCA has issued Civil Aviation Requirements ( CAR ) under section 4 of Aircraft Act, 1934 read with Rule 133A of Aircraft Rules, 1937 and the company is required to comply such requirements under DGCA check systems . While the broad principles of law are contained in the Aircraft Rules, 1937, Civil Aviation Requirements are issued to specify the detailed requirements and compliance procedures.

I further report, that the company is generally regular in compliance of aforesaid aviation laws and the compliance by the Company of such aviation laws have not been reviewed in this Audit which have been subject to review by DGCA and other designated professionals/authorities.

AASL

28

C. I have also examined compliance with the applicable clauses of the following:

(i) Secretarial Standards issued by The Institute of Company Secretaries of India. and

D) I have examined the framework, processes and procedures of compliance with respect to following laws applicable to the company on test basis.

Apprentices Act, 1961; Employees State Insurance Act, 1948; Payment of Wages Act,1948; Minimum Wages Act, 1948; Industrial Disputes Act, 1947; Payment of Bonus Act, 1965; Payment of Gratuity Act, 1972; Contract Labour (Regulation and Abolition) Act, 1970; Maternity Benefit Act, 1961; The Child Labour (Prohibition & Regulation) Act, 1986; Equal RemunerationAct,1976; The Employment Exchange (Compulsory Notification of Vacancies) Act,1956,

Company has created separate Trusts to administer Provident Fund Contributions named Airline Allied Services Employees Provident Fund Trust Regulations, 1996.

Sexual Harassment of Women at Workplace( Prevention, Prohibition and Regulation ) Act, 2013: The Company has in place an Anti Sexual Harassment Policy in line with the requirements of The Sexual Harassment of Women at the Workplace (Prevention, Prohibition & Redressal) Act, 2013. Internal Complaints Committee (ICC) has been set up to redress complaints received regarding sexual harassment.

In connection with aforesaid laws, adequate systems and processes are in place to monitor and ensure compliance with such laws .

During the audit, it is observed that the Compliance Management System needs to be further strengthen by taking the following actions:

a) To establish Corporate Compliance Committee and designate a Chief Compliance officer and maintain centralised mechanism to ensure compliance with all applicable laws;

b) To establish and maintain effective co-ordination of functional units and the compliance department under the overall supervision of the Board;

c) To establish mechanisms to prevent, detect, report and to respond to non-compliances;

d) To present Quarterly compliance Report to the Board;

e) Identification and classification of various compliance risks;

f) Organisation of compliance Check list, Audit, feed back, remedies.

E) I further report, that the compliance by the Company of applicable financial laws, like direct and indirect tax laws, has not been reviewed in this Audit since the same have been subject to review by statutory financial audit and other designated professionals.

During the period under review and as per the explanations and clarifications given to me and there presentations made by the Management, the Company has generally complied with the provisions of the Act, Rules, Regulations, Guidelines, etc. mentioned above subject to the observation made therein.

I further report that:

AASL

29

The Board of Directors of the Company is duly constituted with proper balance of Executive Directors, Non-Executive Directors and Nominee Directors. The changes in the composition of the Board of Directors that took place during the period under review were carried out in compliance with the provisions of the Act.

Adequate notice is given to all directors to schedule the Board Meetings at least seven days in advance and where the Board meetings are called at shorter notice ,presence of at least one Nominee director is ensured, agenda and detailed notes on agenda were sent and a system exists for seeking and obtaining further information and clarifications on the agenda items before the meeting and for meaningful participation at the meeting.

Decisions at the Board Meetings, as represented by the management, were taken unanimously.

I further report that as per the explanations given to me and the representations made by the Management and relied upon by me there are adequate systems and processes in the Company commensurate with the size and operations of the Company to monitor and ensure compliance with applicable laws, rules, regulations and guidelines. It is informed that the Company has responded to notices for demands, claims, penalties etc. levied by various statutory / regulatory authorities and initiated actions for corrective measures, wherever necessary.

I further report that during the audit period the company has:

i) During the financial year, the company has allotted 4,00,00,000 (Four Crores) Equity Shares of Rs. 100/- each at par, aggregating to Rs. 4,00,00,00,000 (Four Hundred Crores) to Air India Ltd vide Board Meeting dated22.09.2015.

Sd/-(Jiwan Parkash Saini)

Company Secretary in practice

December21, 2016FCS No: 3671 CP No: 2100

Note-1: Specific non compliances / observations / audit qualification, reservation or adverse remarks has been reported in respect of the above at appropriate place .

Note-2: This Report is to be read with my letter of even date which is annexed as Annexure A and forms an integral part of this report.

'Annexure A’

To,The Members,Airline Allied Services LimitedOld Lufthansa Hanger Building, (Adjacent To Ed-Nr Office), IGI Airport, T-1,New Delhi – 110037.

I report of even date is to be read along with this letter.

1. Maintenance of Secretarial record is the responsibility of the management of the Company. My responsibility is to express an opinion on these secretarial records based on my audit.

2. I have followed the audit practices and process as were appropriate to obtain reasonable assurance about the correctness of the contents of the Secretarial records. The verification was done on test basis to ensure that correct facts are reflected in Secretarial records. I believe that the process and practices, we followed provide a reasonable basis for my opinion.

3. I have not verified the correctness and appropriateness of financial records and Books of Accounts of the Company.

4. Where ever required, I have obtained the Management representation about the Compliance of laws, rules and regulations and happening of events etc.

5. The Compliance of the provisions of Corporate and other applicable laws, rules, regulations, standards is the responsibility of management. My examination was limited to the verification of procedure on test basis.

6. The Secretarial Audit report is neither an assurance as to the future viability of the Company nor of the efficacy or effectiveness with which the management has conducted the affairs of the Company.

Sd/-(Jiwan Parkash Saini)

Company Secretary in practice

December 21, 2016FCS No: 3671 CP No: 2100

AASL

30

AASL

31

COMMENTS OF THE COMPTROLLER AND AUDITOR GENERAL OF INDIA UNDER SECTION 143(6)(b) OF THE COMPANIES ACT, 2013 ON THE FINANCIAL STATEMENTS OF THE AIRLINES ALLIED SERVICES LIMITED FOR THE YEAR ENDED 31 MARCH 2016

The preparation of financial statements of the Airlines Allied Services Limited for the year ended 31 March 2016 in accordance with the financial reporting framework prescribed under the Companies Act, 2013 (Act) is the responsibility of the management of the company. The statutory auditor appointed by the Comptroller and Auditor General of India under section 139(5) of the Act is responsible for expressing opinion on the financial statements under section 143 of the Act based on independent audit in accordance with the standards on auditing prescribed under section 143(10) of the Act. This is stated to have been done by them vide their Audit Report dated 21 December 2016.

I, on the behalf of the Comptroller and Auditor General of India, have decided not to conduct the supplementary audit of the financial statements of Airline Allied Services Limited for the year ended 31 March 2016 under section 143(6)(a) of the Act.

For and on the behalf of the Comptroller & Auditor General of India

Sd/-Place : New Delhi (Neelesh Kumar Sah)Dated : 20 February 2017 Principal Director of Commercial Audit

& ex-officio Member, Audit Board-I, New Delhi.

AASL

32

INDEPENDENT AUDITOR'S REPORT TO THE MEMBERS OF AIRLINE ALLIED SERVICES LIMITED

Report on the Financial Statements

We have audited the accompanying financial statements of M/s Airline Allied Services Limited, (the “Company”), which comprises the Balance Sheet as at March 31, 2016, the Statement of Profit and Loss and Cash Flow Statement for the year then ended, and a summary of significant accounting policies and other explanatory information.

Management's Responsibility for the Financial Statements

The Company's Board of Directors is responsible for the matters stated in Section 134(5) of the Companies Act, 2013 (“the Act”) with respect to the preparation of these financial statements that give a true and fair view of the financial position, financial performance and cash flows of the company in accordance with the accounting principles generally accepted in India, including the Accounting Standards specified under Section 133 of the Act, read with Rule 7 of the Companies (Accounts) Rules, 2014. This responsibility also includes maintenance of adequate accounting records in accordance with the provisions of the Act for safeguarding the assets of the Company and for preventing and detecting frauds and other irregularities; selection and application of appropriate accounting policies; making judgements and estimates that are reasonable and prudent; and design, implementation and maintenance of adequate internal financial controls, that were operating effectively for ensuring the accuracy and completeness of the accounting records, relevant to the preparation and presentation of the financial statements that give a true and fair view and are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We have taken into account the provisions of the Act, the accounting and auditing standards and matters which are required to be included in the audit report under the provisions of the Act and the Rules made there under.

We conducted our audit in accordance with the Standards on Auditing specified under section 143(10) of the Act. Those Standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal financial control relevant to the Company's preparation of the financial statements that give a true and fair view in order to design audit procedures that are appropriate in the circumstances. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of the accounting estimates made by Company's Directors, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion on the financial statements.

AASL

33

Basis for Qualied Opinion

(i) The nancial statements of the Company under report are drawn up on a 'Going concern basis'. thThe company has informed vide Board Meeting dated 11 April, 2016, the Revenue and Capital

Budget Estimates for the year 2016-17. The Assumptions are made on the budget estimates of 2016-17 though not satisfactory yet the contention of the company is accepted since Air India Ltd., the holding company of the AASL has assured its nancial support to the Company and had converted ̀ 40,000 lakhs of amount advanced to the Company into equity.

(ii) Statement of Prot and Loss includes Trafc Revenue of ̀ 20,912.86 lakhs of current year and ̀ 9.04 lakhs pertain to previous year. (other than grant from NEC Shilong and Agati) accounted for on the basis of ledger account of Air India Limited and expenditure on Service charges of ` 170.37 Lakhs and Other Operating and Administration expenses of ̀ 11913.15 lakhs [which includes ` 265.09 lakhs on account of delayed payments to oil companies] accounted for only on the basis of credit and debit notes raised by Air India Limited. The Company is annually providing liability in respect of delayed payments to OIL companies on the basis of advice given by Air India Ltd. In absence of basic records / vouchers / supporting documents and relevant details, the revenue and expenditure stated above remained unveried to that extent.

(iii) System of Inventory Accounting followed by the company is not proper/complete. In this respect our observations are as below -

a) In respect of ATR / CRJ aircraft inventories, procurement is made by Air India Limited and later transferred to the company without any invoice and charging of applicable sales tax (VAT) - amount and its impact on accounts is unascertainable. Moreover, sufcient control does not exist to ensure that all inventory transactions are authorized, processed and accounted completely.

b) Custom Duty and Freight on aircraft spare parts which form part of aircraft inventories, comprise of freight, duties, incidentals etc. on aircraft inventories owned by the company as well as those taken on lease from the manufacturers and also include freight, incidentals etc. on aircraft components and spares exported for repairs. In the absence of its item wise segregation and loading, the balance of custom duty and freight on aircraft spares amounting to ̀ 522.20 lakhs lying at the end of the year under Current Assets and ` 36.79 lakhs charged to material consumed during the year remained unveried and hence correctness of these amounts and their impact on nancials could not be commented upon.

c) The company is not maintaining any record of Inventories at its stores in Delhi, Hyderabad and Kolkata and the nancial gures are incorporated in its books at the year end on the basis of abstract received from Air India Limited showing the values of different categories of inventories. In absence of details, correctness of Inventory could not be veried and its impact on accounts could not be commented upon. Further in absence of complete details, adequacy of obsolence provision for aircraft stores and spares cannot be commented upon.

d) The consumption of inventory is booked at the year end on the basis of balance arrived at from opening stock plus purchases made during the year less closing stock (advised by Air India Limited) at the end of the year instead of accounting on the basis of actual consumption and disclosing the shortages or excesses, if any, separately. Thus, it is not in accordance with the accepted inventory accounting practices and AS-2 (revised) on valuation norms issued by the ICAI. Hence, the consumption of inventory amounting to

AASL

34

`416.44 lakhs could not be veried and impact on accounts for variance, if any, cannot be commented.

e) Non-compliance of Accounting Standard AS-2 (Revised) on "Valuation of Inventories"-

(i) Inventories have been valued without complete identication and allocation of freight, duties, incidentals etc. with respect to individual items (also refer sub-para (b) above).

(ii) Further, inventories have been valued at cost as against lower of cost and net realizable value.

Impact of the above on the accounts remained unascertained.

(iv) The accounts with the Airport Authority of India Ltd., HPCL and Air India Engineers Services Limited (AIESL) are unconrmed and unreconciled which may impact elements of

stexpenditure/income as well. In absence of conrmation and reconciliation as on 31 March, 2016, we are unable to comment on the impact thereon.

(v) Accounting of certain transactions on settlement basis (Refer Accounting Policy disclosed in Note No. 1.4 and 1.11 are not in accordance with accrual method of accounting prescribed under the Act, Accounting Standard AS-I on "Disclosure of Accounting Policies" and AS-6 (Revised) on "Net Prot or Loss for the period, prior period items and changes in Accounting Policies" issued by ICAI. Amount and impact on accounts unascertained by the Company.

(vi) Accounting policy of the company with respect to accounting of prior period items and prepaid / accrued expenses upto ̀ 10,000/- for Individual items(refer Accounting Policy disclosed in Note No. 1.8 in the year of receipt / payment is not in accordance with accrual method of accounting prescribed under the Act and Accounting Standards AS-1 and AS-5 (Revised)Issued by the ICAI. Amount and impact on accounts is unascertained by the Company.

(vii) The company has not provided liability for leave encashment to the employees for year-end leave balance as required by AS-15 (revised) issued by the ICAI (Refer Accounting Policy disclosed in Note No 1.6). Amount and impact on accounts unascertained by the Company.

(viii) Non-conrmation of balances in respect of Other Long Term Liabilities, Trade Payables, Other Current Liabilities, Long Term. Loans & Advances, Other Noncurrent Assets, Trade Receivables, Short Term Loans & Advances and Other Current Assets. We are unable to comment on the impact of adjustments arising out of non-conrmation of such balances on the nancial statements.

(ix) The company has shown contingent liability amounting to ` 33,612.54 lakhs in respect of income tax demands and ` 62.63 Lakh stowards unsettled legal claims, for which no provision has been made as these demands are said to be disputed by the company in appeals (refer Note No. 25 (I)), In view of pending appeals and legal opinion obtained by the company, we are unable to comment upon the liability of the company and its impact on accounts currently is not ascertainable. Further, based on information available there is an additional liability of tax, interest & penalty on account of TDS ̀ 75.88 lakhs.

(x) Debtors include ̀ 2940.35 lakhs recoverable from M/s Gati Limited outstanding since Feb'2009 for aircrafts operated by the Company. Air India Limited had invoked their bank guarantee and recovered ̀ 3000 Lakhs which was transferred to the Company and the same has been kept by the Company in a separate account of “Security Deposit - Gati” under 'Other Long Term

AASL

35

Liabilities'. The matter is stated to be in dispute between Air India Limited and M/s Gati Ltd. wherein the Arbitral Tribunal has given award of ̀ 2672.95 lakhs (including interest etc.) against Air India Limited. An appeal has been led by Air India Limited before the Hon'ble Delhi High Court against the arbitral award which also upheld the decision of Arbitral Tribunal. To le an appeal in Delhi High court (double bench) against the order, AIL has deposited ` 2200 Lakhs with Hon'ble High Court as deposit money on 17.11.2015 and same has been debited by AIL. Accordingly, we are unable to express our opinion on the impact on the company's accounts for non-recoverability of outstanding dues or amount to be refunded for guarantee invoked or payment of awarded amount.

(xi) The physical verication of assets for the biennial period ended 2014-15 was done in 2015-16. The verication report has reported shortage of ` 96.73 lakhs. The shortage in verication report has been sent to stations/regions for verication. The necessary adjustments will be passed on conrmation from the regions/stations. The adjustment on account of said shortage has not been accounted for in books.

(xii) Company is not accounting for TDS on expenses accounted for on provisional basis. The company is also not accounting for TDS on interest paid to Air India Limited. The same is accounted for at the time of providing of actual expenses. The tax and interest liability on the same have not been accounted for in the books.

(xiii) The company has accounted for interest expense amounting to ̀ 11,131.80 lakhs on account of delayed payment of amount payable to Air India Limited and accounted interest income of ` 243.24 lakhs on account of delayed receipts from AIESL. The company has failed to provide any agreement, and justication for providing the said interest.

We are unable to comment on the impact on the financial statements referred to in this report for paras stated in 'Basis for Qualified Opinion' herein above for the reasons given in each paragraph.

Qualified Opinion

In our opinion and to the best of our information and according to the explanations given to us, except for the effect of the matters described in the Basis for Qualified Opinion paragraph, the aforesaid financial statements read together with the significant accounting policies and notes thereon give the information required by the Act in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India:

sta) in the case of the Balance Sheet, of the state of affairs of the Company as at 31 March'2016;

b) in the case of the Statement of Profit and Loss, of the “Loss” of the Company for the year ended on that date; and

c) in the case of the Cash Flow Statement, of the cash flows for the year ended on that date,

Report on Other Legal and Regulatory Requirements

1. As required by 'the Companies (Auditor's Report) Order, 2016 (“the Order”) issued by the Central Government of India in term of section 143(11) of the Act, we give in the Annexure “A” a statement on the matters specified in paragraph 3 and 4 of the order.

2. We are enclosing our report in terms of Section 143(5) of the Companies Act, 2013, on the basis of such checks of the books and records of the Company as we considered appropriate and according to the

AASL

36

information and explanations given to us, in the Annexure “B” on the directions/ sub-directions issued by the Comptroller and Auditor- General of India.

3. As required by Section 143 (3) of the Act we report that