Airbus Group - media.freecaster.commedia.freecaster.com/doc/cassidian/gif_2014_1.pdf · A350 XWB RC...

141

1 Airbus Group Philippe Balducchi SVP Investor Relations London 10 December 2014

Transcript of Airbus Group - media.freecaster.commedia.freecaster.com/doc/cassidian/gif_2014_1.pdf · A350 XWB RC...

1

Airbus Group Philippe Balducchi

SVP Investor Relations

London

10 December 2014

GLOBAL INVESTOR FORUM 2014

2

Airbus Group Global Investor Forum - Agenda

2

10 December 2014 11 December 2014

14:00 Welcome & Agenda

Philippe Balducchi, SVP Investor Relations

14:05 CEO Speech

Tom Enders, CEO Airbus Group

14:30 Financial Performance

Harald Wilhelm, CFO Airbus Group

15:00 Q&A

15:45 Break

16:00 Group Strategy (including Q&A)

Marwan Lahoud, CSMO Airbus Group

16:45 Airbus Helicopters (including Q&A)

Guillaume Faury, CEO Airbus Helicopters

17:30 Airbus Defence & Space (including Q&A)

Bernhard Gerwert, CEO Airbus Defence & Space

18:15 CEO Wrap Up

19:45 Cocktail and Dinner

Rakesh Gangwal, Co-founder IndiGo

9:00 Airbus

Fabrice Brégier, CEO Airbus

John Leahy, COO Customers Airbus

Didier Evrard, Executive Vice President - Head of A350 Programme

10:00 Q&A

10:45 GIF Wrap Up

Tom Enders, CEO Airbus Group

Harald Wilhelm, CFO Airbus Group

11:00 Group Meeting: 1st Session

12:00 Lunch

13:30 Group Meeting: 2nd Session

14:15 Group Meeting: 3rd Session

15:00 End

Group Meetings Hosts

CEO Airbus Group

CFO Airbus Group

CEO Airbus

1

Airbus Group Harald Wilhelm

Airbus Group, CFO

London

10 December 2014

2

Disclaimer This presentation includes forward-looking statements. Words such as “anticipates”, “believes”, “estimates”, “expects”, “intends”, “plans”, “projects”, “may” and similar expressions are used

to identify these forward-looking statements. Examples of forward-looking statements include statements made about strategy, ramp-up and delivery schedules, introduction of new

products and services and market expectations, as well as statements regarding future performance and outlook. By their nature, forward-looking statements involve risk and uncertainty

because they relate to future events and circumstances and there are many factors that could cause actual results and develop ments to differ materially from those expressed or implied

by these forward-looking statements.

These factors include but are not limited to:

• Changes in general economic, political or market conditions, including the cyclical nature of some of Airbus Group’s businesses;

• Significant disruptions in air travel (including as a result of terrorist attacks);

• Currency exchange rate fluctuations, in particular between the Euro and the U.S. dollar;

• The successful execution of internal performance plans, including cost reduction and productivity efforts;

• Product performance risks, as well as programme development and management risks;

• Customer, supplier and subcontractor performance or contract negotiations, including financing issues;

• Competition and consolidation in the aerospace and defence industry;

• Significant collective bargaining labour disputes;

• The outcome of political and legal processes including the availability of government financing for certain programmes and the size of defence and space procurement budgets;

• Research and development costs in connection with new products;

• Legal, financial and governmental risks related to international transactions;

• Legal and investigatory proceedings and other economic, political and technological risks and uncertainties.

As a result, Airbus Group’s actual results may differ materially from the plans, goals and expectations set forth in such forward-looking statements. For a discussion of factors that

could cause future results to differ from such forward-looking statements, see Airbus Group “Registration Document” dated 4 Apri l 2014.

Any forward-looking statement contained in this presentation speaks as of the date of this presentation. Airbus Group undertakes no obligation to

publicly revise or update any forward-looking statements in l ight of new information, future events or otherwise.

Safe Harbour Statement

GLOBAL INVESTOR FORUM 2014

3

Building Blocks of Airbus Group Shareholder Value

GLOBAL INVESTOR FORUM 2014

Capital Allocation

Financial Flexibility

Cash Generation

Driving Total Shareholder Returns

Operating Profit

Operational Improvement

Top Line Growth

4

Macro Environment

GLOBAL INVESTOR FORUM 2014

Macro environment overall favourable for Airbus Group

GDP

€/$ rate

Air Traffic Oil

Interest Rates Defence Budgets

5

Consistent Topline Growth

GLOBAL INVESTOR FORUM 2014

CAGR = Compound Annual Growth Rate

2008

Airbus

Airbus HC

Airbus DS

42.8bn€

57.6bn€ 7.7%

CAGR

Division 3-5 year

Growth Trend

2009 2010 2011 2012 2013 2014

Airbus Airbus HC Airbus DS

6

Growing Airbus Backlog Supporting Topline Growth

GLOBAL INVESTOR FORUM 2014

5 years of

production

9 years of

production

Airbus backlog # of a/c A320CEO-NEO swaps Airbus deliveries

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 YTD 2014

0%

4% 2%

5% 4% 1% 2%

5% 2% 2%

4%+1%

Cancellations as % total backlog

9m 2014 Airbus Backlog by Units

Asia Pacific

28%

Lessors 19%

Europe 17%

N. America 12%

ME 8%

RoW 16%

1,454

2,177

3,421 3,488

4,437

6,036

320

378

434 453 483 498 510

534

588 626

7

2015 2016 2017 2018 2019 2020

GLOBAL INVESTOR FORUM 2014

A320 rate 46

Ready to adapt production rates on A320 and A330 to market demand

Transitioning Ceos to Neos

neo backlog* ceo backlog*

* Backlog includes MoUs, options, and commitments

A320 Family

2015 2016 2017 2018 Beyond 2018

A330 rate 9

Ongoing Campaigns

A330 Family

8

Product Life Cycle EBIT and Cash Flow Curves

GLOBAL INVESTOR FORUM 2014

New Development Programmes

• Upfront investment

• Learning curve brings down recurring costs

Incremental Upgrades

Extend programme life

Less investment

Less risk

EBIT Contribution

Cashflow Contribution

ILLUSTRATIVE

9

GLOBAL INVESTOR FORUM 2014

A320

A330

A350

A380 CEO

NEO

A350

A380

A320 / A330

2 0 1 4 5 6 7 8 9 0 2

Airbus Product Portfolio Positioned to Produce EBIT and Cash

ILLUSTRATIVE

10

A350 Profitability

10 December 2014

GLOBAL INVESTOR FORUM 2014

PR

ICE

Launch Price

A350

Launch Price

A350 XWB

Serial Price

A350 XWB

RC

– B

uy / M

ake

R

am

p - U

P

PR

OF

ITA

BIL

ITY

Prof itability

IAS 11 Impact

Prof itability

+ LMC

11

Consistently Seeking Competitiveness Across the Group

GLOBAL INVESTOR FORUM 2014

Airbus DS Airbus Helicopters HQ Airbus

Manufacturing / Operations

Procurement

Programme Management

Support Functions

Engineering

Customer Satisfaction

12

Securing EBIT with Hedging Policy

GLOBAL INVESTOR FORUM 2014

Hedging Activity Increasing Hedging and Exposure

Protection and visibility gained with hedging, taking advantage of strengthening $

1,240

1,260

1,280

1,300

1,320

1,340

1,360

1,380

1,400

1,420

Monthly hedges

avg. spot rates EUR USD

avg hedge rates EUR USD

Monthly FX Hedging 2013 - YTD 2014

As of 9m 2014

13

Profitability Performance

GLOBAL INVESTOR FORUM 2014

* 2013 f igures are pro forma amended with IFRS 11 restatement

EBIT (bn€) and RoS (%) bef ore one off EBIT Outlook

** Compared to 2013 RoS before restatement at 6%

3.7%

5.2%

6.1%*

Moderate RoS

Growth**

1.8

3.0 3.5

2011 2012 2013 2014

Track record of profitability improvement – 2014 guidance reaffirmed

14

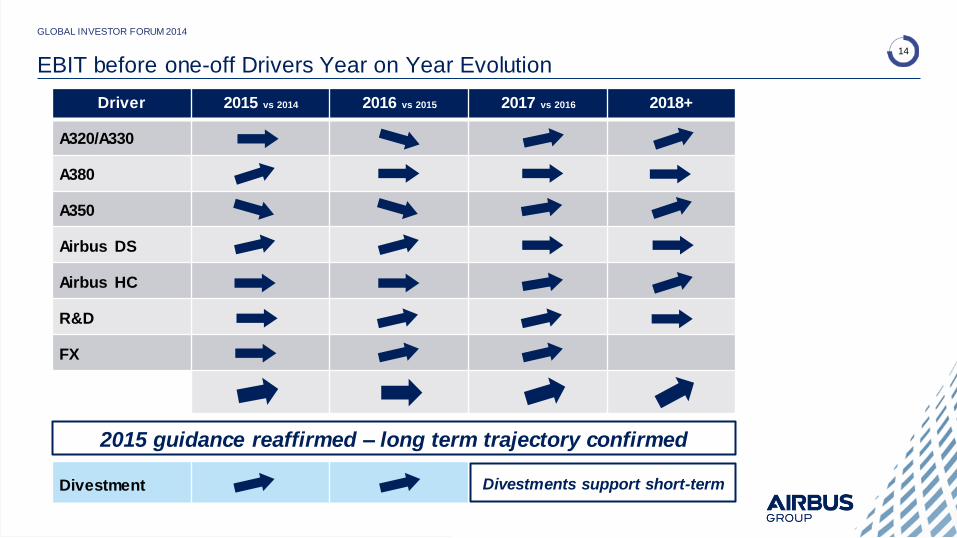

EBIT before one-off Drivers Year on Year Evolution

GLOBAL INVESTOR FORUM 2014

Driver 2015 vs 2014 2016 vs 2015 2017 vs 2016 2018+

A320/A330

A380

A350

Airbus DS

Airbus HC

R&D

FX

Divestment

2015 guidance reaffirmed – long term trajectory confirmed

Divestments support short-term

15

Inventory and PDP Evolution

GLOBAL INVESTOR FORUM 2014

Governmental & Institutional

Commercial

Customer Advances

2014E

33-36bn€

A350

Evolution

Other Inventories

Evolution (A330, A320, A380, Airbus DS,

Airbus HC, etc)

Inventories

2014E

26-28bn€

Including A350 Programme

16

Outlook on Key Cash Drivers

GLOBAL INVESTOR FORUM 2014

Driver 2014 2015 2016 2017 2018+

A320/A330 +++++ ++++ ++++ +++++

A380 - ~ ~ ~

A350 - - - - - - - - - -

A400M - - - - - -

Airbus DS/HC

& HQ + + + +

Summary View ~ ~/- ++ +++

Divestment + + +

2014 guidance reaffirmed – long term trajectory confirmed

Divestments support short-term

17

Financial Policy

GLOBAL INVESTOR FORUM 2014

Robust Net

Cash Level

Shareholders

Deliver on committed

dividend policy

Hedging

Ensure access to

instruments

Credit Rating

Target A- or

better

Business Risks

Program execution and

macro risks

Business Model

Annual cashflow profile,

resource intensive

Opportunities

Keep flexibility to

invest

18

Conclusion: Driving Total Shareholder Returns

GLOBAL INVESTOR FORUM 2014

COMPETITIVENESS AND PROFITABILITY

TOPLINE GROWTH

EPS

Growth

DIVIDEND POLICY

FINANCIAL POLICY

DPS

Growth

1

Airbus Group Marwan Lahoud

Airbus Group, CSMO

London

10 December 2014

2

Disclaimer This presentation includes forward-looking statements. Words such as “anticipates”, “believes”, “estimates”, “expects”, “intends”, “plans”, “projects”, “may” and similar expressions are used

to identify these forward-looking statements. Examples of forward-looking statements include statements made about strategy, ramp-up and delivery schedules, introduction of new

products and services and market expectations, as well as statements regarding future performance and outlook. By their nature, forward-looking statements involve risk and uncertainty

because they relate to future events and circumstances and there are many factors that could cause actual results and develop ments to differ materially from those expressed or implied

by these forward-looking statements.

These factors include but are not limited to:

• Changes in general economic, political or market conditions, including the cyclical nature of some of Airbus Group’s businesses;

• Significant disruptions in air travel (including as a result of terrorist attacks);

• Currency exchange rate fluctuations, in particular between the Euro and the U.S. dollar;

• The successful execution of internal performance plans, including cost reduction and productivity efforts;

• Product performance risks, as well as programme development and management risks;

• Customer, supplier and subcontractor performance or contract negotiations, including financing issues;

• Competition and consolidation in the aerospace and defence industry;

• Significant collective bargaining labour disputes;

• The outcome of political and legal processes including the availability of government financing for certain programmes and the size of defence and space procurement budgets;

• Research and development costs in connection with new products;

• Legal, financial and governmental risks related to international transactions;

• Legal and investigatory proceedings and other economic, political and technological risks and uncertainties.

As a result, Airbus Group’s actual results may differ materially from the plans, goals and expectations set forth in such forward-looking statements. For a discussion of factors that

could cause future results to differ from such forward-looking statements, see Airbus Group “Registration Document” dated 4 Apri l 2014.

Any forward-looking statement contained in this presentation speaks as of the date of this presentation. Airbus Group undertakes no obligation to

publicly revise or update any forward-looking statements in l ight of new information, future events or otherwise.

GLOBAL INVESTOR FORUM 2014

Safe Harbour Statement

3

Positioned as a Leader

3

Exchange rates: US$ to €: 0,776; £ to €: 1,178; CAD$ to €0,729, BRL to €: 0,347, SEK to €:0,115

BAE systems revenues split between BAE Systems Inc. and the rest. UTC includes large share of non Aerospace businesses.

FY13 Group Revenues (€bn) FY13 Defence Revenues (€bn)*

0 20 40 60 80

General Dynamics

Honeywell

Locked Martin

UTC

Airbus Group

Boeing

0 5 10 15 20 25

Safran

Dassault Aviation

Thales

Finmeccanica

Airbus Group

BAE Systems

FY13 Helicopters Revenues (€bn)

0 2 4 6 8

Boeing

Bell

Russian Helicopters

Agusta Westland

Sikorsky

Airbus Helicopters

0 10 20 30 40 50

Embraer

Bombardier Aerospace

Airbus

Boeing Commercial

FY13 Commercial Aircraft Revenues (€bn)

GLOBAL INVESTOR FORUM 2014

4

Keeping Ahead Through Responding to Current Customer Dynamics…

Airbus « Made in USA » tapping large replacement market

Footprint in China to access the biggest future market

Commercial Aircraft

Air traffic to

double next 15 years

New Dynamics

in Space markets

Better organize the European space industry landscape

Upside in Satellite markets

Strong product

modernization demands

from the market

Upgrades in Helicopters (EC 145 T2, EC-135 T3/P3)

Continuous Innovation in commercial aircraft

(A320 NEO, A321neoLR, A330 NEO, A330 242t…)

Evolution in Military (E-Captor, C295 mission systems)

Budget realities

in Defence

Integrate and focus to secure competitiveness

Focus on leadership segments (Tanker, Combat a/c,

Transport, Missiles…) and access global growth

Market Realities Selected Responses

GLOBAL INVESTOR FORUM 2014

5

New Business Models... ...and New Technologies …in the Factory of the Future

E- FAN Humanoid robot

3D printing

Exoskeletons for assembly

SSTL

Electrical Satellites

Zephyr

…while Systematically Planning the Future

GLOBAL INVESTOR FORUM 2014

6

Actively Managing and Reshaping our Portfolio

Unappealing

Attractive

Matches Contradicts

Fin

an

cia

l In

tere

st

Strategic Interest

…and execution ongoing A systematic approach is in place….

Core:

Airbus Safran Launchers

Non-Core:

Dassault Aviation

Non-Core: Airbus DS perimeter reshaping

Focus on profitability, value creation, and market position

GLOBAL INVESTOR FORUM 2014

7 Dassault Aviation – Making an Attractive Financial Asset Liquid

Strong track record and good prospects….

…with no strategic interest for the Group

Influence on business minimal - No industrial logic as long as not in control

Competing in Defence

Good partner for potential European programmes but shareholding not helpful to make it happen

First steps taken

8% sold for 794m€

Further sales in 2015 targeted

Focus is on an orderly exit to maximise value

GLOBAL INVESTOR FORUM 2014

8

36

58 64

41

67

2011A 2012A 2013A 9M 2013 9M 2014

Dassault Aviation – Strong Record, Well Positioned for the Future

Ind

ex

ed

Sto

ck

Pri

ce

0

50

100

150

200

250

300

Dassault Business Jets¹ Military EU²

Strong share price development supported by robust operating

margins and strong cash-flow ...

Book to Bill

Business

Jets

Orders

(Units)

Source: Company disclosure

(1) Business Jets peers include General Dynamics, Embraer, BBA Aviation, Bombardier and Textron.

(2) Military EU peers include BAE Systems, Finmeccanica, Cobham and Tilleul.

10-year stock price performance

x2.3

x1.7

x1.5

Today

Tomorrow

Beyond

... and positioned to benefit from grow th in heavier segment of

business jet market

Option on 2 major sources of upside

1. Rafale export (India, Qatar, UAE)

2. Value uplift embedded in Thales stake

Uniquely positioned to benefit from business jet market

recovery through 2 new product launches

• Falcon 8X – scheduled end 2016

• Falcon 5X – scheduled mid 2017

0.6x 0.9x 0.8x 1.5x 0.9x

+63%

Future Benefit from New Programmes Sustained Value Creation

Strong Business Jet Order Momentum

GLOBAL INVESTOR FORUM 2014

9

JV – Airbus Safran Launchers

Vertically integrating Prime role and Propulsion

provider to gain cost control and competitiveness

Sales and Launch Operations to be integrated

Clear cost and risk sharing principles and

simplified contract management

Market evolving….

Space X and ULA/Blue

Origin in the US

Governments world wide

with ambitions – China,

India…

Price pressure in certain

segments

Ambitions to decrease

launch cost high

…and Airbus Group is creating a one-stop-shop

GLOBAL INVESTOR FORUM 2014

10

Ariane 6

Modular

Two configurations enabling

mission versatility, with single &

dual launch capabilities

Synergetic

Benefits from existing launcher

family and ongoing developments

plus cadence effect

Market driven

Closer link to Arianespace

leveraging brand, unrivalled

commercial reach and proven

service offering

GLOBAL INVESTOR FORUM 2014

11

Streamlining the Airbus DS Portfolio

Rethink structure to address

bottom line performance

Refocus and divest where others

can create more value than us

Orient portfolio on leadership

positions to succeed under any

market conditions

….Solutions for Airbus DS portfolio Guiding Principles….

Disposals ongoing Professional Mobile Radio

Commercial satellite

communications services

Various subsidiaries, JVs,

and participations

Exploring Industrial

Alternatives

Boosts competitiveness

in a core area Missiles*

Revenue split - *Revenues for missiles not consolidated

Military

Aircraft

Space

Systems

Electronics

CIS

Launcher

JV

GLOBAL INVESTOR FORUM 2014

12

Execution of Strategy Well Underway

2013 2014 2015-16

Group Strategy

Revisited

Portfolio

Review Completed

Perimeter Reshaping

Execution

Full strategic review

across the Group

“We make it Fly”

Integrate Defence

and Space

ReBrand to Airbus

Portfolio assessment

across the Group

Core vs. non-core

identified

Disposals and

restructurings

launched

Disposals, asset sales,

and restructurings

Rationalized internal

CAPEX and R&D

Competitiveness

enhanced through

greater focus

Capitalize on greater focus for stronger topline growth

and better bottom-line performance

GLOBAL INVESTOR FORUM 2014

13 Delivering on our Strategy

1

Airbus Helicopters Guillaume Faury

Airbus Helicopters, CEO

London

10 December 2014

2

Disclaimer This presentation includes forward-looking statements. Words such as “anticipates”, “believes”, “estimates”, “expects”, “intends”, “plans”, “projects”, “may” and similar expressions are used

to identify these forward-looking statements. Examples of forward-looking statements include statements made about strategy, ramp-up and delivery schedules, introduction of new

products and services and market expectations, as well as statements regarding future performance and outlook. By their nature, forward-looking statements involve risk and uncertainty

because they relate to future events and circumstances and there are many factors that could cause actual results and develop ments to differ materially from those expressed or implied

by these forward-looking statements.

These factors include but are not limited to:

• Changes in general economic, political or market conditions, including the cyclical nature of some of Airbus Group’s businesses;

• Significant disruptions in air travel (including as a result of terrorist attacks);

• Currency exchange rate fluctuations, in particular between the Euro and the U.S. dollar;

• The successful execution of internal performance plans, including cost reduction and productivity efforts;

• Product performance risks, as well as programme development and management risks;

• Customer, supplier and subcontractor performance or contract negotiations, including financing issues;

• Competition and consolidation in the aerospace and defence industry;

• Significant collective bargaining labour disputes;

• The outcome of political and legal processes including the availability of government financing for certain programmes and the size of defence and space procurement budgets;

• Research and development costs in connection with new products;

• Legal, financial and governmental risks related to international transactions;

• Legal and investigatory proceedings and other economic, political and technological risks and uncertainties.

As a result, Airbus Group’s actual results may differ materially from the plans, goals and expectations set forth in such forward-looking statements. For a discussion of factors that

could cause future results to differ from such forward-looking statements, see Airbus Group “Registration Document” dated 4 Apri l 2014.

Any forward-looking statement contained in this presentation speaks as of the date of this presentation. Airbus Group undertakes no obligation to

publicly revise or update any forward-looking statements in l ight of new information, future events or otherwise.

Safe Harbour Statement

GLOBAL INVESTOR FORUM 2014

3

A Year of Execution and Delivery:

Certification and Entry into Service

• EC175

• EC145 T2

• EC135 P3/T3

Full return to service of EC225

Capitalizing on new brand: Eurocopter

becomes Airbus Helicopters

Year 1 of Transformation Plan delivery

GLOBAL INVESTOR FORUM 2014

Airbus Helicopters – 2014 Achievements

4

GLOBAL INVESTOR FORUM 2014

Civil & Parapublic (C&P) Market: Responding to changing Market Dynamics

Short

term

Long

term

US / Canada

2014 - 23

3,090

2008 - 13

Short

term

Long

term

Western Europe

1,310

2014 - 23 2008 - 13

Short

term

Long

term

Eastern Europe / CIS

1,680

2014 - 23 2008 - 13

Short

term

Long

term

Latin America

2,110

2014 - 23 2008 - 13

Short

term

Long

term

Asia / Pacific

2,240

2014 - 23 2008 - 13

Short

term

Long

term

Africa / Middle East

920

2014 - 23 2008 - 13

2008 – 2013 Airbus Helicopters bookings share 2014 – 2023: new deliveries

5

GLOBAL INVESTOR FORUM 2014

2008 – 2013 Airbus Helicopters bookings share 2014 – 2023: new deliveries

Military Helicopter Market: Addressing a Structural Shift in the Market

Short

term

Long

term

US / Canada

2014 - 23 2008 - 13

2,680

Short

term

Long

term

Western Europe

2014 - 23 2008 - 13

680

Short

term

Long

term

Eastern Europe / CIS

2014 - 23 2008 - 13

1,840

Short

term

Long

term

Latin America

2014 - 23 2008 - 13

380

Short

term

Long

term

Africa / Middle East

2014 - 23 2008 - 13

980

Short

term

Long

term

Asia / Pacific

2014 - 23 2008 - 13

2,470

6

GLOBAL INVESTOR FORUM 2014

Support & Service growth based on

Airbus Helicopters fleet growth…

…and the deployment of new services

to enhance value for our customers

Support & Services: Stable and Consistent Growth driven by Fleet in Service

0,0

0,5

1,0

1,5

2,0

2,5

3,0

2012 2013 2014 2015e 2016e

Re

ve

nu

e €

bn

Stable contribution of services to topline revenues

7

GLOBAL INVESTOR FORUM 2014

Support & Services and Governmental Programmes will drive short term outlook

Airbus Helicopters Business Drivers

Commercial Helicopters

Governmental Helicopters

Support & Services

Commercial Helicopters

Governmental Helicopters

Support & Services

2013 Revenues % Short-Term Revenues %

8

GLOBAL INVESTOR FORUM 2014

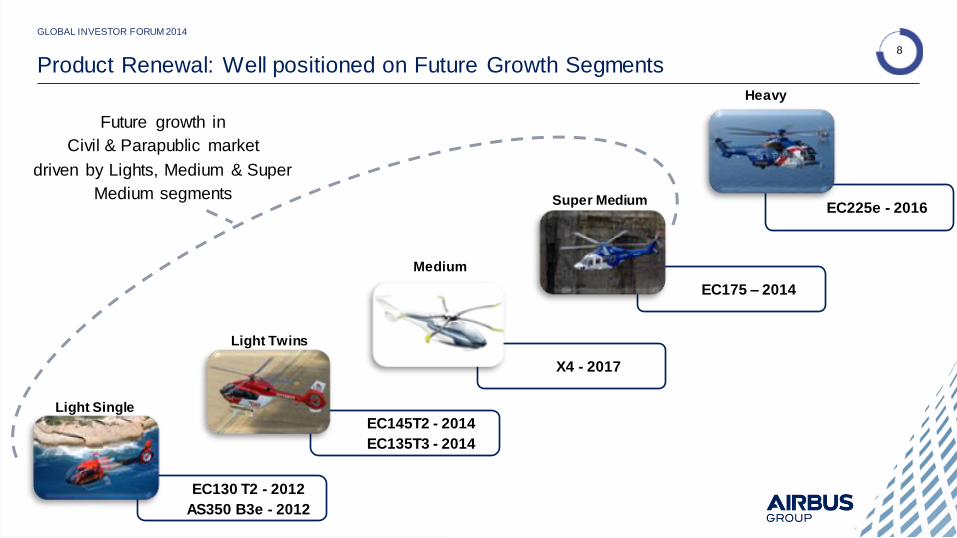

EC130 T2 - 2012

AS350 B3e - 2012

EC225e - 2016

EC175 – 2014

X4 - 2017

EC145T2 - 2014

EC135T3 - 2014

Light Single

Super Medium

Medium

Light Twins

Heavy

Future growth in

Civil & Parapublic market

driven by Lights, Medium & Super

Medium segments

Product Renewal: Well positioned on Future Growth Segments

9

GLOBAL INVESTOR FORUM 2014

Customer

Satisfaction

Quality & Safety

Design &

Production

Cost, Cash &

Competitiveness

Our new ways of

working

Progress

to date

Transformation Plan: On Track

Ensure that Company is driven by customer care

Develop a robust quality and safety management system

Industrialize our operations, from early design to manufacturing

Reduce costs and manage cash in order to create more value

Change the mindset and behaviours in order to fit these commitments

10 L

EAN

E

C2

25

O&

G

Flo

w L

ine

GLOBAL INVESTOR FORUM 2014

Customer

Satisfaction

Quality

& Safety

Design &

Production

Cost, Cash,

Competitiveness

New Ways

of working

Implementation of Transformation Plan

e-S

erv

ices

Sp

are

s

Av

ail

ab

ilit

y

Sy

ne

rgie

s

wit

h A

irb

us

Gro

up

11

Priorities unchanged…

Customer Satisfaction

Quality & Safety

Competiteveness

In a environment of …

A low C&P market

Important on-going military opportunities

Fleet renewal

GLOBAL INVESTOR FORUM 2014

A strong business model and new products to drive our future

Airbus Helicopters in 2015

1

Airbus Defence & Space Bernhard Gerwert

Airbus DS, CEO

London

10 December 2014

2

Disclaimer This presentation includes forward-looking statements. Words such as “anticipates”, “believes”, “estimates”, “expects”, “intends”, “plans”, “projects”, “may” and similar expressions are used

to identify these forward-looking statements. Examples of forward-looking statements include statements made about strategy, ramp-up and delivery schedules, introduction of new

products and services and market expectations, as well as statements regarding future performance and outlook. By their nature, forward-looking statements involve risk and uncertainty

because they relate to future events and circumstances and there are many factors that could cause actual results and developments to differ materially from those expressed or implied

by these forward-looking statements.

These factors include but are not limited to:

• Changes in general economic, political or market conditions, including the cyclical nature of some of Airbus Group’s businesses;

• Significant disruptions in air travel (including as a result of terrorist attacks);

• Currency exchange rate fluctuations, in particular between the Euro and the U.S. dollar;

• The successful execution of internal performance plans, including cost reduction and productivity efforts;

• Product performance risks, as well as programme development and management risks;

• Customer, supplier and subcontractor performance or contract negotiations, including financing issues;

• Competition and consolidation in the aerospace and defence industry;

• Significant collective bargaining labour disputes;

• The outcome of political and legal processes including the availability of government financing for certain programmes and the size of defence and space procurement budgets;

• Research and development costs in connection with new products;

• Legal, financial and governmental risks related to international transactions;

• Legal and investigatory proceedings and other economic, political and technological risks and uncertainties.

As a result, Airbus Group’s actual results may differ materially from the plans, goals and expectations set forth in such forward-looking statements. For a discussion of factors that

could cause future results to differ from such forward-looking statements, see Airbus Group “Registration Document” dated 4 April 2014.

Any forward-looking statement contained in this presentation speaks as of the date of this presentation. Airbus Group undertakes no obligation to

publicly revise or update any forward-looking statements in light of new information, future events or otherwise.

Safe Harbour Statement

GLOBAL INVESTOR FORUM 2014

3

GLOBAL INVESTOR FORUM 2014

Global leader in Space, Military Aircraft, Missiles and related Systems & Services

MB

DA

-MdC

N-©

DG

A

Airbus DS

4

GLOBAL INVESTOR FORUM 2014

Key Achievements: Restructuring

Go Live New Organisation created within 6 months – go-live on 1 July

More than 40,000 employees successfully transferred

1,000 positions already reduced – on track HC Reduction

One HQ for former 3 divisions established in Munich

8 sites closed in 2014; on track for 2016 target Site Optimisation

Leveraging best practices

Eliminating inefficiencies

Streamlining of organisation

Synergies

5

Military Aircraft Space

Ariane 5: launch slots filled

until 2018

Ariane 6: Programme

launched

Satellite : robust demand

GEO Intelligence: double

digit growth

Eurofighter: improved

export capability

A330 MRTT: growing

customer base

Light & Medium Transport:

book-to-bill > 1

A330 MRTT: successful

deployment in operational

missions

A400M: in service with

multiple customers

63rd successful Ariane 5

launch in a row

Rosetta mission: Philae

landing on a comet

GLOBAL INVESTOR FORUM 2014

M51: further development

under contract

Launch of a new Franco-

British missile programme

(FASGW(H)/ANL)*

Naval Cruise Missile:

Last successful development

firing

Key Achievements: Business

Commercial

Momentum

Programme

Execution

Missiles

*FASGW(H)/ANL: Future Anti Surface Guided Weapon (Heavy)/ Anti Navire Léger)

6

Core Business

Competitive business pillars clearly identified

Enhance Value Creation

Reinforce leadership position

Streamline portfolio

GLOBAL INVESTOR FORUM 2014

Execute on Strategy

© J

. G

ietl

7

Validation of Ariane 6 concept

Creation of Airbus Safran Launchers

GLOBAL INVESTOR FORUM 2014

Space - Develop Europe’s Leading Role in the Space Industry

8

Outlook

GLOBAL INVESTOR FORUM 2014

NEAR-TERM LONG-TERM

Ariane

Satellites

Services

MBDA

Eurofighter

A400M

A330 MRTT

A5 maintain leadership/

JV Creation Ariane 6 success

Capitalise on technological

advantage Enhance global market share

Sell new GEO services Prepare next MilSatcom services

Grow export sales Further integration

Secure export orders Focus on capability

enhancement and Services

Programme execution Secure export market

Secure further orders

Military

Aircraft

Missiles

Space

9

GLOBAL INVESTOR FORUM 2014

Defence and Space are stable and predictable businesses

Our bespoke products and programmes address current and future customer challenges and respond to market opportunities

Profitability target for 2015 maintained – future improvement from focusing on our core activities and de-risking our portfolio

Conclusion

1

Airbus Fabrice Brégier

Airbus, CEO

London

11 December 2014

2

Disclaimer This presentation includes forward-looking statements. Words such as “anticipates”, “believes”, “estimates”, “expects”, “intends”, “plans”, “projects”, “may” and similar expressions are used

to identify these forward-looking statements. Examples of forward-looking statements include statements made about strategy, ramp-up and delivery schedules, introduction of new

products and services and market expectations, as well as statements regarding future performance and outlook. By their nature, forward-looking statements involve risk and uncertainty

because they relate to future events and circumstances and there are many factors that could cause actual results and develop ments to differ materially from those expressed or implied

by these forward-looking statements.

These factors include but are not limited to:

• Changes in general economic, political or market conditions, including the cyclical nature of some of Airbus Group’s businesses;

• Significant disruptions in air travel (including as a result of terrorist attacks);

• Currency exchange rate fluctuations, in particular between the Euro and the U.S. dollar;

• The successful execution of internal performance plans, including cost reduction and productivity efforts;

• Product performance risks, as well as programme development and management risks;

• Customer, supplier and subcontractor performance or contract negotiations, including financing issues;

• Competition and consolidation in the aerospace and defence industry;

• Significant collective bargaining labour disputes;

• The outcome of political and legal processes including the availability of government financing for certain programmes and the size of defence and space procurement budgets;

• Research and development costs in connection with new products;

• Legal, financial and governmental risks related to international transactions;

• Legal and investigatory proceedings and other economic, political and technological risks and uncertainties.

As a result, Airbus Group’s actual results may differ materially from the plans, goals and expectations set forth in such forward-looking statements. For a discussion of factors

that could cause future results to differ from such forward-looking statements, see Airbus Group “Registration Document” dated 4 Apri l 2014.

Any forward-looking statement contained in this presentation speaks as of the date of this presentation. Airbus Group undertakes no obligation to

publicly revise or update any forward-looking statements in l ight of new information, future events or otherwise.

Safe Harbour Statement

GLOBAL INVESTOR FORUM 2014

3

Positioned to Deliver Long-Term Profitable Growth

GLOBAL INVESTOR FORUM 2014

Growing market with solid fundamentals

Continuing momentum on operational efficiency improvements

Controlled execution to sustain growth

Product portfolio positioned to capture growth

4

Content

GLOBAL INVESTOR FORUM 2014

Delivering on Commitments

Improving Performance

Clear Path Forward and Conclusion

5

Development Programmes: 2014 Achievements

GLOBAL INVESTOR FORUM 2014

Mastering development programmes

Accelerate time to market of new products

neo

neo

Extension of a profitable programme

Path set to reach EIS in 42 months

Orders and commitments from 8 customers (5 airlines & 3 lessors)

EASA/FAA certification on time

Ready for delivery to Qatar Airways

A350-1000 on track for 2017 EIS

First flight as per initial launch schedule

Flight test underway (150 FT hours, more than 40 flights)

752 net orders YTD Backlog: 3,362 / 63 customers

Backlog: 152* / 8 customers

Backlog: 786 / 41 customers

* Includes MoUs

6

Series Programmes: 2014 Achievements

GLOBAL INVESTOR FORUM 2014

Delivering on series programmes

Production adapting to market demand

Fleet in service: 147 / Operators: 12

Backlog: 171

Delivering ~ 30 aircraft

Dispatch Reliability 98.5%

On path to breakeven in 2015

Fleet in service: 1,112 / Operators: 106*

Backlog: 367 **

Delivering rate 10, adjusting to rate 9 from Q4 2015

Dispatch Reliability 99.4%

First 242t version in FAL

Fleet in service: 6,053 / Operators: 319

Backlog: 4,832

Delivering rate 42, rate 46 from Q2 2016

Dispatch Reliability 99.6%

Robust ramp up of A321 and Sharklets (86% of current production)

*Excludes A340

** Includes MoUs

7

Content

GLOBAL INVESTOR FORUM 2014

Delivering on Commitments

Improving Performance

Clear Path Forward and Conclusion

8

Improving our Products and Services

GLOBAL INVESTOR FORUM 2014

Improved products to meet and anticipate customer needs

A320

• Sharklet retrofit option - EIS 2015

• A321neoLR - 97t variant

• A320neo 20% fuel reduction per seat by 2020 vs today’s A320ceo

A330

• Neo launched

• Versatility: 242t and regional capabilities

A380

• New design weights

• High density cabin

Improved aircraft operations and services

• Time to fix improved by up to 25%

• Service revenues increased by 14%

Innovative products and services which meet Customer needs

9

Enhancing our Industrial Performance

GLOBAL INVESTOR FORUM 2014

Engineering

Production

Faster, cost optimized development

A330neo development time reduced

Design to cost solutions (A350)

First time right (10-15% reduction of corrective modifications)

Culture

Eradicate disturbances and inefficiencies in our work everywhere

Speed, agility, simplicity

Innovation

Stop & fix

Supply

Chain

Maintain tight control through anticipation, collaboration, cost reductions

Joint improvement programmes with main suppliers

Missing parts reduced by >60% on series programmes*

Double sourcing, re-tendering, re-design

Airbus Operating System deployed using lean principles

42 model lines deployed

End-to-end quality gates

Increased use of 3D data

* Airframe

10

Content

GLOBAL INVESTOR FORUM 2014

Delivering on Commitments

Improving Performance

Clear Path Forward and Conclusion

11

Clear Path Forward

GLOBAL INVESTOR FORUM 2014

NEAR-TERM LONG-TERM

Expand customer base Product upgrade Commercial Momentum

Controlled ramp-up Continuous innovation Rate 10

EIS -1000 Further rate increases

A330neo Development Strengthen market positioning

A330neo EIS

Industrial Transition Commercial Transition

A320neo EIS Further Rate increases Controlled ramp-up

Industrial Transition

12

Conclusion

GLOBAL INVESTOR FORUM 2014

Delivering on Commitments

Improving Products and Services

Enhancing Operations

Clear Path Forward

Greater Value

for our

Customers

Enhanced

Financial

Performance

1

Commercial update John Leahy

Chief Operating Officer – Customers

London,

December 11th, 2014

2

Disclaimer This presentation includes forward-looking statements. Words such as “anticipates”, “believes”, “estimates”, “expects”, “intends”, “plans”, “projects”, “may” and similar expressions are used

to identify these forward-looking statements. Examples of forward-looking statements include statements made about strategy, ramp-up and delivery schedules, introduction of new

products and services and market expectations, as well as statements regarding future performance and outlook. By their nature, forward-looking statements involve risk and uncertainty

because they relate to future events and circumstances and there are many factors that could cause actual results and develop ments to differ materially from those expressed or implied

by these forward-looking statements.

These factors include but are not limited to:

• Changes in general economic, political or market conditions, including the cyclical nature of some of Airbus Group’s businesses;

• Significant disruptions in air travel (including as a result of terrorist attacks);

• Currency exchange rate fluctuations, in particular between the Euro and the U.S. dollar;

• The successful execution of internal performance plans, including cost reduction and productivity efforts;

• Product performance risks, as well as programme development and management risks;

• Customer, supplier and subcontractor performance or contract negotiations, including financing issues;

• Competition and consolidation in the aerospace and defence industry;

• Significant collective bargaining labour disputes;

• The outcome of political and legal processes including the availability of government financing for certain programmes and the size of defence and space procurement budgets;

• Research and development costs in connection with new products;

• Legal, financial and governmental risks related to international transactions;

• Legal and investigatory proceedings and other economic, political and technological risks and uncertainties.

As a result, Airbus Group’s actual results may differ materially from the plans, goals and expectations set forth in such forward-looking statements. For a discussion of factors that

could cause future results to differ from such forward-looking statements, see Airbus Group “Registration Document” dated 4 Apri l 2014.

Any forward-looking statement contained in this presentation speaks as of the date of this presentation. Airbus Group undertakes no obligation to

publicly revise or update any forward-looking statements in l ight of new information, future events or otherwise.

Safe Harbour Statement

GLOBAL INVESTOR FORUM 2014

3

Global Market Forecast 2014: Highlights

GLOBAL INVESTOR FORUM 2014

Passenger aircraft (≥ 100 seats)

Jet f reight aircraft (>10 tons)

Source: Airbus GMF 2014

GMF 2014 key numbers and 20-year change

World Fleet Forecast 2013 2033 % change 2013-2033

RPK (trillion) 5.8 14.6 151%

Passenger Aircraft Fleet

16,855 34,818 107%

New passenger aircraft deliveries

30,555

Dedicated Freighters 1,605 2,645 65%

New freighter aircraft deliveries

803

Total New Aircraft Deliveries 31,358

4

Air traffic doubles every 15 years

GLOBAL INVESTOR FORUM 2014

Source: ICAO, Airbus GMF 2014

0

2

4

6

8

10

12

14

16

1973 1978 1983 1988 1993 1998 2003 2008 2013 2018 2023 2028 2033

World annual RPK* (trillion)

5

Global Middle Class to more than double

GLOBAL INVESTOR FORUM 2014

Source: Kharas and Gertz, Airbus

EOY 2013

** Households with daily expenditures between $10

and $100 per person (at PPP)

679 697 673

264 261 252

1 413

2 782

4 450

0

1 000

2 000

3 000

4 000

5 000

2013* 2023 2033

Global Middle Class**

(Millions of people)

Emerging countries

World Population 8,500 7,900 7,200

% of world population 63% 48% 33%

3,740

2,356

5,375

North America

Europe

6

0,01

0,10

1,00

10,00

0 10 20 30 40 50 60

2013 trips per capita

22% of the population of the emerging countries took a trip a year in 2013

GLOBAL INVESTOR FORUM 2014

Source: Sabre (annualized September 2013 data),

IHS Global Insight, Airbus |

*Passengers originating from respective country

Bubble size proportional to population

2013 GDP per capita (thousands $US)

Europe

~1 trip per capita

North America

1.6 trips per capita

China

0.25 trips per capita

India

0.06 trips per capita

7

0,01

0,10

1,00

10,00

0 10 20 30 40 50 60

…but by 2033, 66% of the population of the emerging countries will take a trip a year

GLOBAL INVESTOR FORUM 2014

Source: Sabre (annualized September 2013

data), IHS Global Insight, Airbus |

*Passengers originating from respective country

Bubble size proportional to population

India 2033

0.26 trips per capita

China 2033

0.95 trips per capita

2033 trips per capita

2013 GDP per capita (thousands $US)

8

0

20

40

60

80

100

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Gross order share since 1995

Airbus and Boeing world market share

GLOBAL INVESTOR FORUM 2014

To end Nov ember 2014

Boeing 82%

Airbus 18%

9

Boeing 1,270 55%

Airbus 1,039 45%

Net

2014 market share

GLOBAL INVESTOR FORUM 2014

Data to December 5th 2014

Boeing 1,376 51%

Airbus 1,336 49%

Gross

2,712 industry

orders

2,309 industry

orders

10

2014 market share by category - gross

GLOBAL INVESTOR FORUM 2014

Data to December 5th 2014

1,058 47%

1,173 53%

Single aisle 2,231 orders

A320 737

316 69%

143 31%

Widebody 459 orders

2 9%

20

91%

VLA 22 orders

A330

A350

767

777

777X

787

A380 747-8

A350 57 53%

787 49 47%

11

2014 market share by category - net

GLOBAL INVESTOR FORUM 2014

Data to December 5th 2014

978 50%

970 50%

Single aisle 1,948 orders

A320 737

292 84%

55 16%

Widebody 347 orders

0

14 100%

VLA 14 orders

A330

A350

767

777

777X

787

A380 747-8

A350 -26

787 25 100%

12

Combined industry backlog of over 11,500 aircraft

GLOBAL INVESTOR FORUM 2014

Data to December 5th 2014

Airbus

A320ceo 1,470

A320neo 3,362

A330 215

A330neo 40

A350 XWB 786

A380 171

Boeing

737NG 1,665

737 MAX 2,553

767/787 893

777 232

777X 286

777F 35

747-8 26

747-8F 13

5,703 6,044 New Industry record

13

0

1000

2000

3000

4000

5000

6000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Airbus delivery and backlog comparison

GLOBAL INVESTOR FORUM 2014

To December 5th 2014

Airbus backlog 6,044

14

0

1000

2000

3000

4000

5000

6000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

0

200

400

600

800

1000

1200

Airbus delivery and backlog in-synch at 5:1 1990-2006

GLOBAL INVESTOR FORUM 2014

To December 5th 2014

Airbus backlog Airbus deliveries (scale 1/5 x backlog)

15

0

1000

2000

3000

4000

5000

6000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

0

200

400

600

800

1000

1200

Airbus delivery and backlog at 9:1 in 2014 with conservative delivery ramp-up

GLOBAL INVESTOR FORUM 2014

To December 5th 2014

Airbus backlog Airbus deliveries (scale 1/5 x backlog)

16

0

200

400

600

800

1000

1200

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Production policy results in smooth ramp-up. No troughs and peaks

GLOBAL INVESTOR FORUM 2014

To end Nov ember 2014

Annual deliveries

Airbus

17

0

200

400

600

800

1000

1200

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Delivery comparison

GLOBAL INVESTOR FORUM 2014

Annual deliveries

Boeing

-55% -59% +140%

+130%

18

Airbus product line

GLOBAL INVESTOR FORUM 2014

250 seats

300 seats

350 seats

400 seats

500 seats

150 seats

200 seats

100 seats

A380

747-8

A330 Family

A350 Family

787 Family

777/777X

A320 Family 737 Family

Seat capacity

19

Over 11,000 A320 Family sales

GLOBAL INVESTOR FORUM 2014

Data to December 5th 2014

6,331 4,832

Orders Deliveries Backlog

11,163

20

NEO leads the MAX in orders and customers

GLOBAL INVESTOR FORUM 2014

Data to December 5th 2014

Source: Airbus Orders & Deliveries,

Boeing.com

A320neo

3,362 orders

737 MAX

2,553

orders

63 Customers

46 Customers

Including

12 customers converting

243 737NG

(9% conversions)

Including

6 customers converting

102 A320ceo

(3% conversions)

21

GLOBAL INVESTOR FORUM 2014

22

At launch, A320neo lowered fuel burn per seat by 15%

GLOBAL INVESTOR FORUM 2014

800 nm sector

High density configuration

A319ceo A319neo A320ceo A320neo A321ceo A321neo

156 seats 156 seats

-15% -15%

180 seats 180 seats 220 seats

-16%

220 seats

At launch

23

With increased exit limits, A320neo lowers fuel burn per seat by 20%

GLOBAL INVESTOR FORUM 2014

800 nm sector

High density configuration

Airbus Cabin Flex (ACF) is an optional

f eature

A319ceo A319neo A320ceo A320neo A321ceo A321neo

-17% -18% -21%

Exit limit increase

156 seats 160 seats 180 seats 189 seats 220 seats 240 seats

24

In 2020 A320neo Family fuel burn per seat will be up to 23% lower

GLOBAL INVESTOR FORUM 2014

800 nm sector

High density configuration

Airbus Cabin Flex (ACF) is an optional

f eature

A319ceo A319neo A320ceo A320neo A321ceo A321neo

-19% -20% -23%

156 seats 160 seats 180 seats 189 seats 240 seats

Exit limit increase plus PW 2% PIP from 2019

220 seats

25

0

20

40

60

80

100

120

140

160

180

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

Nominal $US

High oil prices here for the long-term

GLOBAL INVESTOR FORUM 2014

Source: IHS Energy, Airbus

Brent oil price (US$ per bbl) Forecast History

26

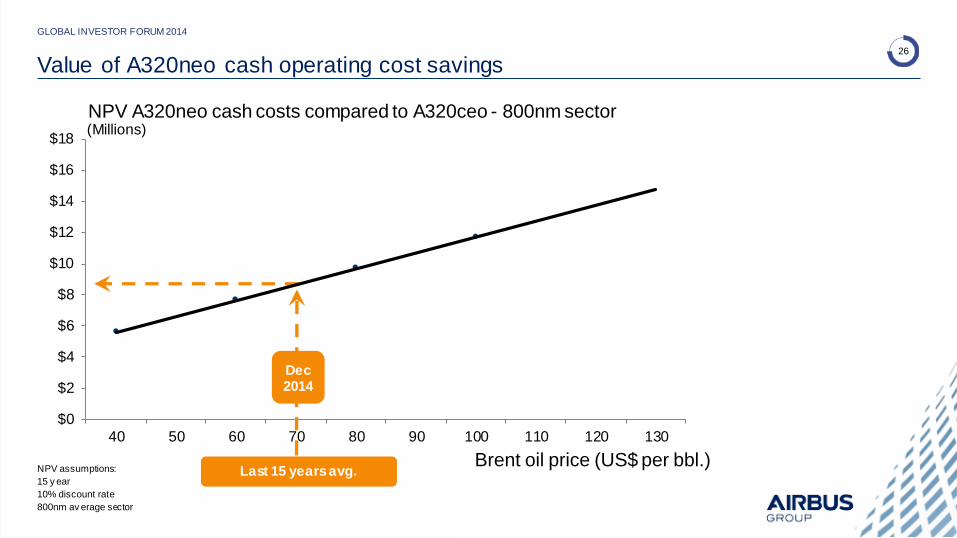

Value of A320neo cash operating cost savings

GLOBAL INVESTOR FORUM 2014

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

40 50 60 70 80 90 100 110 120 130

Brent oil price (US$ per bbl.)

Dec 2014

Last 15 years avg.

NPV A320neo cash costs compared to A320ceo - 800nm sector

NPV assumptions:

15 y ear

10% discount rate

800nm av erage sector

(Millions)

27

A321neo with more range than a 757-200 for longer range markets

GLOBAL INVESTOR FORUM 2014

Product Development Study

A321neo Airbus Cabin-Flex configuration

for business class layout flexibility

MTOW 97t

ACT#2-3

28

0

5000

10000

15000

20000

25000

0 1000 2000 3000 4000 5000 6000

Distance (nm)

A321neo with 97t MTOW flies farther than a 757-200W

GLOBAL INVESTOR FORUM 2014

97t A321 with 3 ACTs

Product Development Study

Aircraft MTOW Pax Range

757-200W 115t 169 3800nm

A321neo 97t 164 3900nm

Payload (kg)

29

97t A321neo extends market reach

GLOBAL INVESTOR FORUM 2014

ASCEND data

North - South routes

special focus on Brazil

East coast - Europe

Europe -

Middle East Europe -

West Africa Australia –

South-east Asia

North-Europe -

Asia

469 Boeing 757 aircraft in passenger service

8

45

103

310

3

30

Airbus Widebody Family: matching market demand

GLOBAL INVESTOR FORUM 2014

31

159

786 750

152

66

286

634 616

141

0

100

200

300

400

500

600

700

800

900

A380 A350 A330 A330neo 747-8 777X 777 787 767

Airbus leads in Passenger and freighter widebody orders since A350 XWB launch

GLOBAL INVESTOR FORUM 2014

Net widebody passenger and freighter orders

since A350 XWB launch in December 2006

Net orders + A330neo commitments

December 2006 to December 5th 2014

Airbus 1,847 Boeing 1,743

32

1,127 255

Orders Deliveries Backlog

1,394

~1,500 A330 sales and commitments

GLOBAL INVESTOR FORUM 2014

At end Nov ember 2014.

Sales/backlog include 40 firm A330neo

33

A330 Family has the largest operator base of any widebody

0

20

40

60

80

100

120

2004 2006 2008 2010 2012 2014

Year

A330

787

777

GLOBAL INVESTOR FORUM 2014

Commercial airline operators with passenger aircraft

in-serv ice and / or on order as at end each year.

Unidentified operators excluded.

Source: ASCEND

Number of passenger operators

34

242t A330ceo EIS in May 2015

GLOBAL INVESTOR FORUM 2014

35

Delta orders 25 A350-900 and 25 A330-900neo

GLOBAL INVESTOR FORUM 2014

14% lower fuel/seat than A330ceo - Delta’s most profitable aircraft

10% larger than 787-9 - more revenue on growing Pacific routes

An optimized solution for trans-Atlantic and trans-Pacific Markets

A350-900

350 seats

7,500nm range

A330-900neo

310 seats

6,000nm range

36

A330neo 18in economy seating

GLOBAL INVESTOR FORUM 2014

37

1m 64m

Aerodynamic improvement

GLOBAL INVESTOR FORUM 2014

Modified upper belly fairing

Wing re-twist Composite winglet extension

Increased wing span to 64m

(+3.7m)

Wingspan stays within Code E category

38

- 14% fuel per seat

A330neo 14% lower fuel burn per seat

GLOBAL INVESTOR FORUM 2014

*ICE : increased Cabin Efficiency

A330 RR Trent 772B – 2014 deliv eries

Max passenger Payload – 4,00nm mission

A330ceo

Airframe Powerplant

RR Trent

772B

RR Trent

7000

A330neo

- 4%

Aerodynamic

Improvements

(shark lets and

optimisation)

-11%

Fuel

burn

+2%

Powerplant

weight

+1%

Engine

integration

Wing

modifications - 12% fuel per trip

A330neo

+ 6-10 seats*

39

Total Operating

Cost per seat

+7%

787-9

304 seats

Cash Operating

Cost per seat

Datum

787-9

304 seats

$1.3m/month

1%

A330-900neo cost efficiency

GLOBAL INVESTOR FORUM 2014

Airbus standard economic rules

787 (253t) with GE engines,,

4000nm route, JAR 3%, 200nm diversion,

f uel price 3 US$/Usg

Operating cost

Lease rate

A330-900neo

310 seats

$1.1m /month

40

A330neo deliveries start in December 2017

GLOBAL INVESTOR FORUM 2014

41

A350 XWB: 786 aircraft to deliver to 41 customers

GLOBAL INVESTOR FORUM 2014

Orders and deliv eries to December 5th 2014

42

A350 XWB: designed to reduce cash operating costs by 25%

GLOBAL INVESTOR FORUM 2014

Latest generation Trent XWB

offers up to 10% lower

SFC than the GE-90

Highly tapered planform

Variable camber / Differential flap setting

Optimum fuselage cross-section

Lightweight material airframe

Engines

Aerodynamics

Weight

43

A350-1000: 35 tonnes lighter than the stretched 777-9X

GLOBAL INVESTOR FORUM 2014

777-300ER 175t OWE

-20t

+15t

A350-1000 155t OWE

Clean sheet design

777-9X

777-300ER 777-9X

5th derivative

• 4-frame stretch

• Frame sculpting

• Bigger wing with folding wings

• Engine upsize

44

A380 takes off or lands every 4 minutes

GLOBAL INVESTOR FORUM 2014

Orders and deliv eries to end November 2014

147 171

Orders Deliveries Backlog

318

45

A380 dominates the very large aircraft market with almost 90% market share

GLOBAL INVESTOR FORUM 2014

Data to end November 2014

Source: Airbus Orders & Deliveries,

Boeing.com

VIP not included

747-8 42

orders 12%

747-8 5

airlines 21%

Net orders and airlines customers for passenger aircraft

A380

318 orders

88%

A380

19 airlines

79%

46

42 Mega-Cities worldwide

GLOBAL INVESTOR FORUM 2014

90%+ Of long-haul

traffic on routes

to/from/via 42

cities

Handling more than 10,000 long haul passengers per day

Source: GMF 2013; Cities with more than 10,000 daily passengers, Long haul traffic: flight distance >2,000nm, excl. domestic traffic

47

71 Mega-Cities worldwide by 2023

Source: GMF 2013; Cities with more than 10,000 daily passengers, Long haul traffic: flight distance >2,000nm, excl. domestic traffic

GLOBAL INVESTOR FORUM 2014

95%+ Of long-haul

traffic on routes

to/from/via 42

cities

Handling more than 10,000 long haul passengers per day

48

Over 70 million passengers have now enjoyed the A380 experience

GLOBAL INVESTOR FORUM 2014

Data to end August 2014

Revenue flight hours 1,660,000 flight hours in 196,000 revenue flights

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

49

A380 dispatch reliability

95%

96%

96%

97%

97%

98%

98%

99%

99%

2010 2011 2012 2013 2014

GLOBAL INVESTOR FORUM 2014

2014 y ear to end September

15 minute delay criteria

50

A380 developments have increased market reach

GLOBAL INVESTOR FORUM 2014

Improved SFC

Trent 900\ GP 7000

Aircraft weight reduction

New Design Weights

payload

+500nm

+8t

Optimised wing twist

-1%

Fuel burn

51

The world’s longest routes are operated with A380

GLOBAL INVESTOR FORUM 2014

The longest

A380 flights > 16 hours

Los Angeles

Dubai Dallas

Sydney

52

4 new A380 operators in 2014-2015

GLOBAL INVESTOR FORUM 2014

ASIANA AIRLINES

QATAR AIRWAYS TRANSAERO

ETIHAD

53

Premium A380 cabin experience

GLOBAL INVESTOR FORUM 2014

54

A380 cabin: 19” wide,10-abreast, seating

GLOBAL INVESTOR FORUM 2014

55

A380 cabin: Revenue maximisation with 18” wide,11-abreast, seating

GLOBAL INVESTOR FORUM 2014

56

Undisputed

industry

Flagship The winning combination

Strong market recognition

of complementary roles Single aisle

leader

GLOBAL INVESTOR FORUM 2014

1

A350 XWB Achievements & Path Forward Didier Evrard, Head of A350 XWB Programme

London

11 December 2014

2

Disclaimer This presentation includes forward-looking statements. Words such as “anticipates”, “believes”, “estimates”, “expects”, “intends”, “plans”, “projects”, “may” and similar expressions are used

to identify these forward-looking statements. Examples of forward-looking statements include statements made about strategy, ramp-up and delivery schedules, introduction of new

products and services and market expectations, as well as statements regarding future performance and outlook. By their nature, forward-looking statements involve risk and uncertainty

because they relate to future events and circumstances and there are many factors that could cause actual results and develop ments to differ materially from those expressed or implied

by these forward-looking statements.

These factors include but are not limited to:

• Changes in general economic, political or market conditions, including the cyclical nature of some of Airbus Group’s businesses;

• Significant disruptions in air travel (including as a result of terrorist attacks);

• Currency exchange rate fluctuations, in particular between the Euro and the U.S. dollar;

• The successful execution of internal performance plans, including cost reduction and productivity efforts;

• Product performance risks, as well as programme development and management risks;

• Customer, supplier and subcontractor performance or contract negotiations, including financing issues;

• Competition and consolidation in the aerospace and defence industry;

• Significant collective bargaining labour disputes;

• The outcome of political and legal processes including the availability of government financing for certain programmes and the size of defence and space procurement budgets;

• Research and development costs in connection with new products;

• Legal, financial and governmental risks related to international transactions;

• Legal and investigatory proceedings and other economic, political and technological risks and uncertainties.

As a result, Airbus Group’s actual results may differ materially from the plans, goals and expectations set forth in such forward-looking statements. For a discussion of factors that

could cause future results to differ from such forward-looking statements, see Airbus Group “Registration Document” dated 4 Apri l 2014.

Any forward-looking statement contained in this presentation speaks as of the date of this presentation. Airbus Group undertakes no obligation to

publicly revise or update any forward-looking statements in l ight of new information, future events or otherwise.

Safe Harbour Statement

GLOBAL INVESTOR FORUM 2014

3

GLOBAL INVESTOR FORUM 2014

Learn lessons to meet delivery commitments

A350-900 certified & ready for EIS

Preparing the future by boosting competitiveness

4

A350 XWB is Certified on Time (as Committed in 2012) and Ready for EIS

EASA Type Certification

- Awarded on 30th September 2014

FAA approval on the 12th Nov

On track for first

customer delivery end-2014

GLOBAL INVESTOR FORUM 2014

5

A350-900 Certification in a Record Time:14.5 months after First Flight

Functional &

Reliability tests done

with mature systems

at certification

standard

Route proving On time

departure for 20 days

26 flights,14 airports

>180 FH

81,700 nm

Cabin comfort

validated through

early tests on MSN2

Positive passenger

feedback throughout

Early Long Flights and

route proving. Wide

spacious cabin. Low cabin

noise

Certification tests

passed first time

thanks to airframe &

engine maturity

Flight envelope fully

opened (Stalls, Flutter

testing, VMU, …)

External noise, HIRF

testing MERTO test.

High Altitude : Cold,

Hot & Dry, Hot & Humid

+45°C to -40°C in the

McKinley chamber

Flight test hours for certification as planned

Consistently ahead of plan

Aircraft availability very good from day 1

2,600 FH flown in 680 flights for

Type Certificate

0

500

1000

1500

2000

2500

3000

3501

01/06/2013 01/12/2013 01/06/2014 01/12/2014

A350 Flight Hour evolution

ALL A350

TARGET AVG A350

ALL A380 (RR)

Ty pe Certification

VMU : Minimum unstick speed - MERTO: Maximum Energy Rejected Take-Off test

GLOBAL INVESTOR FORUM 2014

6

Demonstrating Reliability at Certification Enabling ETOPS

1st A/C type certified

“Beyond 180 min”

180 minutes ETOPS in basic

specification

300 or 370 minutes ETOPS

available as options

GLOBAL INVESTOR FORUM 2014

7

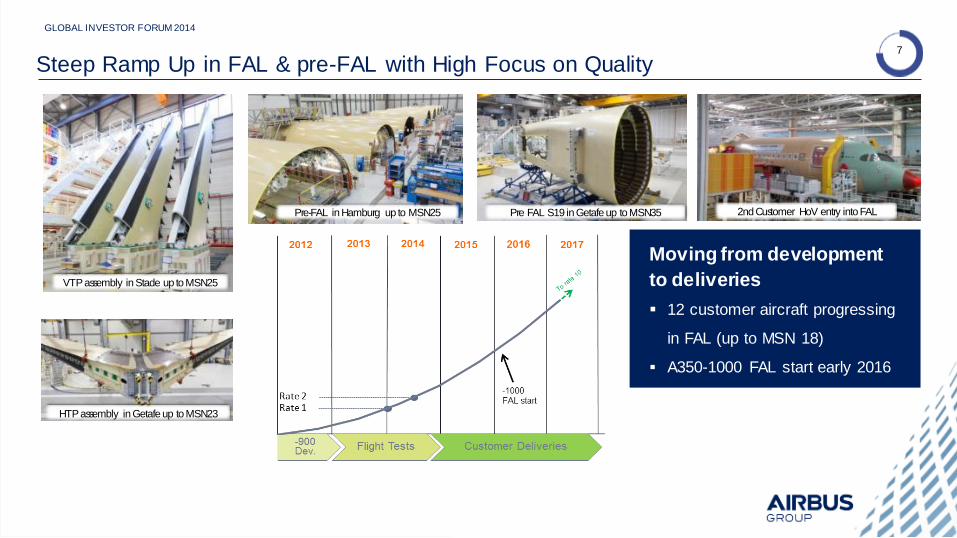

Steep Ramp Up in FAL & pre-FAL with High Focus on Quality

Moving from development

to deliveries

12 customer aircraft progressing

in FAL (up to MSN 18)

A350-1000 FAL start early 2016

2nd Customer HoV entry into FAL Pre-FAL in Hamburg up to MSN25

VTP assembly in Stade up to MSN25

HTP assembly in Getafe up to MSN23

Pre FAL S19 in Getafe up to MSN35

GLOBAL INVESTOR FORUM 2014

8

Learn lessons to meet delivery commitments

GLOBAL INVESTOR FORUM 2014

A350-900 certified & ready for EIS

Preparing the future by boosting competitiveness

9

Airbus Programmes Industry

Lessons Learned from Airbus Programmes and Industry

Plan a quick but achievable ramp-up

Ensure highest possible level of maturity

at certification

(e.g. techno issue)

Use best practices from outside aerospace

(e.g. automotive)

Flexible customisation appreciated by

customers but can have negative

industrial impact

(e.g. A380)

Travelled work volume can be difficult to

reduce

Complex Supply chain with bottlenecks

and performance issue

GLOBAL INVESTOR FORUM 2014

10

What Makes the Difference on A350 XWB? Applying Lessons Learned

Alignment programme / functions with trust of Top Management => Speed

Risks & opportunities led at head of Programme level => Anticipation

Continuous de-risking of contracts with customers => Customer confidence

Program management

Planning transparency to enable alignment => Efficiency

Very regular communication with customers, markets and suppliers with explanations => Trust

Communication

New technology risks (stringers, root joints) identified and mitigated

Quality Gates and Stop & Fix approach to gain speed in FAL

Airline-like environment during flight test campaign to accelerate operability

Technology & Maturity

GLOBAL INVESTOR FORUM 2014

11

Airline like Environment: AIRLINE1 & Airline Office – Key Enabler for Maturity

Providing the airlines’ experience

Participating in flight test a/c operations

Ensuring direct feedback to Airbus

Contribute to validation of customer support system

Contribute to on-aircraft verification activities

AIRLINE Office – Voice of Customer

Aircraft Maturity

Product Maturity Items (PMI)

Operational Test Campaign (OTC)

Tech Pub & Ground Support Equipment (GSE)

Aircraft Operability

Dispatch Operations

Built In Test (BITE)

Maintenance Efficiency

Component removal

AIRLINE1 – Mirror airline operations

Focus on delivering an A/C with the highest dispatch reliability:

Prepare rapid solving of in-service issues (TTGF*)

* TTGF: Time To Get a Fix

GLOBAL INVESTOR FORUM 2014

12

What Makes the Difference on A350 XWB? Applying Lessons Learned

Catalogue policy with Enabling platform: => High Reuse / Leadtime reduction

Qualified BFE suppliers

Customer Definition Center for definition freeze

Customisation

& Industrial

Requirements

Reconciliation

Reliable Extended Enterprise using common development tools & process

Industrial harmonisation across Extended Enterprise

Steep ramp-up but limited aircraft in FAL at certification => Limits Retrofits

Pro-active development of critical suppliers

Supply Chain, Methods &

Rools

GLOBAL INVESTOR FORUM 2014

13

Galleys

Models

• Wide range of galley models

• Hundreds of distinct galley configurations

G1C Galley Configurations

SFE(Supplier Furnished Equipment)

Modular Offering with almost limitless combinations

Customisation & Industrial Requirements Reconciliation

Catalogue with Mix of Pre-developed Modules Fitted for Flex Zones

GLOBAL INVESTOR FORUM 2014

14

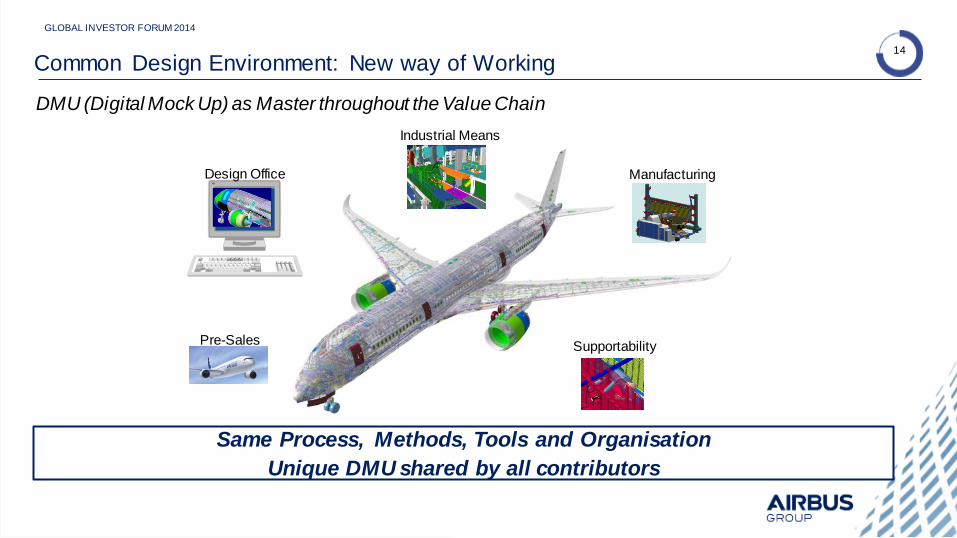

Common Design Environment: New way of Working

Same Process, Methods, Tools and Organisation

Unique DMU shared by all contributors

Pre-Sales

Design Office

Industrial Means

Manufacturing

Supportability

GLOBAL INVESTOR FORUM 2014

DMU (Digital Mock Up) as Master throughout the Value Chain

15

GLOBAL INVESTOR FORUM 2014

Learn lessons to meet delivery commitments

A350-900 certified & ready for EIS

Preparing the future by boosting competitiveness

16

Profitability Protection through Production Costs Convergence

Buy Subsidiaries Make

Design changes (Design to Cost)

Commercial levers on Buy

Simplification of manufacturing processes

RC

– B

uy / M

ake

RC

Convergence

Early a/c

learning curve

Control

Concession Flow

Simplification,

Design to Cost,…

Current

Target set Q4 2014

Initial

Target

GLOBAL INVESTOR FORUM 2014

17

A350-1000 Design Benefits from A350-900 Experience

A350-900 Flight Test data continuously analyzed for A350-1000

design optimization

A350-900 static tests results used to optimize A350-1000 structure

A350-1000 incorporates latest innovations

• CFRP Doors surrounds

• Pylon composite spar

Building on A350-900 experience and successful platform

Extensive use of simulation on A350-1000 to reduce tests

GLOBAL INVESTOR FORUM 2014

18

Preparing A350-1000 Industrialisation On Time

TrentXWB-97 engine ran for 1st time

Centre Wing Box – 1st Metal cut // 1st Ply

CFRP Doors Surrounding

structure - Barrel 1B

Wing Covers - 1st Ply

UTAS MLG manufacturing

started and Scale 1 Mockup

GLOBAL INVESTOR FORUM 2014

19

Next Steps

Successful start of operations with Qatar

Deliver ramp up within cost targets

Continue to apply lessons learnt to keep A350-1000 on track

A350 XWB: boosting Airbus competitiveness

GLOBAL INVESTOR FORUM 2014

20

A350 XWB Achievements & Path Forward Didier Evrard, Head of A350 XWB Programme

London

11 December 2014