Air Arabia PJSC · Cost-effective distribution network and booking system Drive growth through an...

26

February 2008 -1- Investor Presentation February 2008 Air Arabia PJSC

Transcript of Air Arabia PJSC · Cost-effective distribution network and booking system Drive growth through an...

February 2008- 1 -

Investor Presentation

February 2008

Air Arabia PJSC

February 2008- 2 -

Disclaimer

Information contained in this presentation is subject to change without notice, its accuracy is not

guaranteed and it may not contain all material information concerning the company. Neither we nor

our advisors make any representation regarding, and assumes no responsibility or liability for, the

accuracy or completeness of, or any errors or omissions in, any information contained herein.

In addition, the information contains projections and forward-looking statements that reflect the

company’s current views with respect to future events and financial performance. These views are

based on current assumptions which are subject to various risks and which may change over time.

No assurance can be given that future events will occur, that projections will be achieved, or that the

company’s assumptions are correct. Actual results may differ materially from those projected.

This presentation is strictly not to be distributed without the explicit consent of

Company management under any circumstance.

February 2008- 3 -

� Air Arabia at a Glance

� Investment Highlights

� Financial Highlights

� Strategy and Outlook

Agenda

February 2008- 4 -

Air Arabia at a Glance

- 5 -February 2008

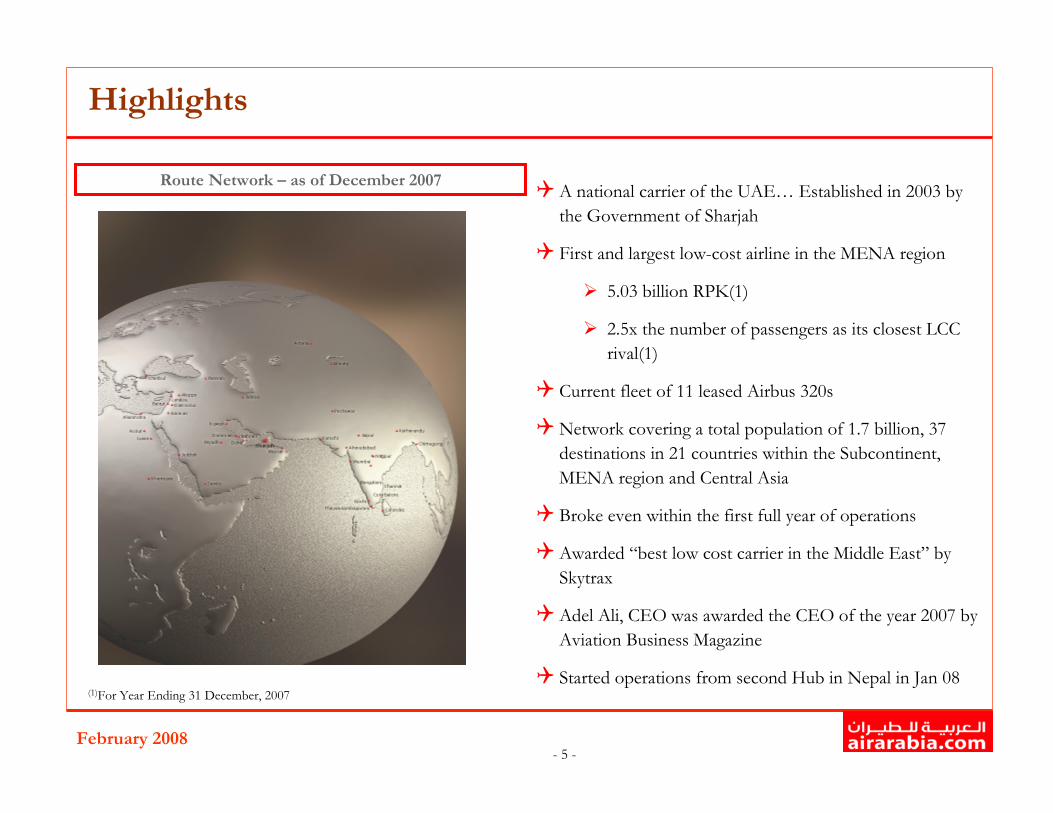

Highlights

�A national carrier of the UAE… Established in 2003 by

the Government of Sharjah

� First and largest low-cost airline in the MENA region

� 5.03 billion RPK(1)

� 2.5x the number of passengers as its closest LCC

rival(1)

� Current fleet of 11 leased Airbus 320s

�Network covering a total population of 1.7 billion, 37

destinations in 21 countries within the Subcontinent,

MENA region and Central Asia

� Broke even within the first full year of operations

�Awarded “best low cost carrier in the Middle East” by

Skytrax

�Adel Ali, CEO was awarded the CEO of the year 2007 by

Aviation Business Magazine

� Started operations from second Hub in Nepal in Jan 08(1)For Year Ending 31 December, 2007

Route Network – as of December 2007

- 6 -February 2008

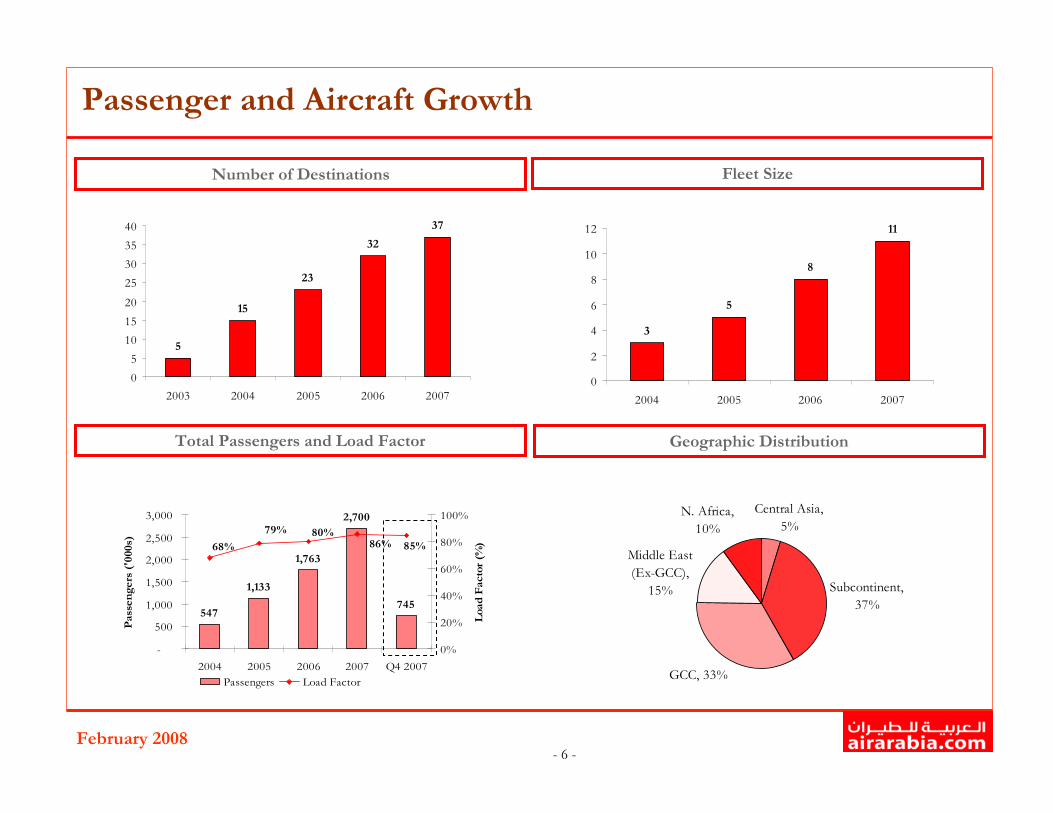

Passenger and Aircraft Growth

Total Passengers and Load Factor Geographic Distribution

Fleet SizeNumber of Destinations

5

15

23

32

37

0

5

10

15

20

25

30

35

40

2003 2004 2005 2006 2007

3

5

8

11

0

2

4

6

8

10

12

2004 2005 2006 2007

547

1,133

1,763

2,700

745

85%86%80%

68%

79%

-

500

1,000

1,500

2,000

2,500

3,000

2004 2005 2006 2007 Q4 2007

Passengers ('000s)

0%

20%

40%

60%

80%

100%

Load Factor (%

)

Passengers Load Factor

Central Asia,

5%

Subcontinent,

37%

GCC, 33%

Middle East

(Ex-GCC),

15%

N. Africa,

10%

February 2008- 7 -

Investment Highlights

- 8 -February 2008

Investment Highlights

� Highly favorable home and regional market dynamics

� Strong air traffic growth projected in our target regions

� Low Cost Carrier (LCC) model highly untapped in the Middle East

� First mover advantage

� Highly profitable Low Cost Carrier business model

� Continue to drive costs lower through operational efficiencies

� Consistently achieved the highest level of aircraft utilization in the A320 family

� Cost-effective distribution network and booking system

� Drive growth through an aggressive expansion plan

� Significant route and fleet expansion planned, supported by Sharjah Airport expansion

� Track record of profitable expansion

� Started operations from second hub in Nepal in Jan 08 and plans for third hub through 2008

� Support from the Sharjah and UAE Government

� Experienced management team

- 9 -February 2008

Highly Favorable Home and Regional Market Dynamics

International Air Traffic Growth by Key Route Area Middle East Passenger Traffic(1)

Source: Airbus

�Strong Air Traffic Growth Projected in Our Target Regions

(1) Airbus Estimate; based on number of passengers of the top 20 airlines in the Middle East

7.1%

5.3%

5.3% 6.0%

Middle East Routes All International Routes

AAGR % 2005A-2010E

Passenger Freight

81

270

2005A 2025E

Passengers in M

M

- 10 -February 2008

Highly Favorable Home and Regional Market Dynamics

LCC Penetration - Middle East(2)

Europe

(1) Source: IBM Business Consulting Services

North America

LCC Penetration – Proven Markets –

2005A(1)

� GCC countries, particularly UAE, have a significant expatriate

population from the Indian Subcontinent, Egypt and the Levant (80%

of UAE population is expatriate)

�Low Cost Carrier (LCC) Model Highly Untapped in the Middle East

(2) Source: Air Arabia – 2005A: based on number of passengers of Air Arabia and Jazeera Airways (1.2m; Source: respective company websites) as a percentage of total passenger traffic in the

Middle East (148m; Source: Zawya.com).

2005A 2007E – Air Arabia EstimateLCC

11%

Traditional

Carriers

89%

LCC

25%

Traditional

Carriers

75%

LCC

0.8%

Traditional

Carriers

99.2%

Traditional

Carriers

98.6%

LCC

1.4%

- 11 -February 2008

Highly Profitable Low Cost Carrier Business Model

CompanyRevenue / ASK

(AED - Fils)

Cost / ASK

(AED - Fils)EBITDAR

Air Asia 13.7 11.2 32.2%

Air Arabia 21.1 13.6 34.3%

Ryan Air 21.5 16.8 30.0%

Jet Blue 20.3 19.1 16.6%

South West 22.6 20.8 15.2%

Vigin Blue 36.8 31.3 19.6%

WestJet 34.0 29.2 23.7%

GOL 29.7 29.8 13.0%

EasyJet 31.1 25.9 16.6%

Vueling Airlines SA 24.4 27.9 3.4%

UAL Corp (US) 29.1 27.6 11.8%

North West Airlines (Corp) 30.6 27.3 17.7%

LCC Median 26.7 26.6 17.2%

Cathy 32.6 29.6 19.8%

Emirates 28.0 25.2 24.7%

SIA 35.7 30.8 25.9%

Qantas 53.4 49.5 19.0%

Air France - KLM 51.1 47.0 17.1%

British Airways 42.8 38.0 21.6%

- 12 -February 2008

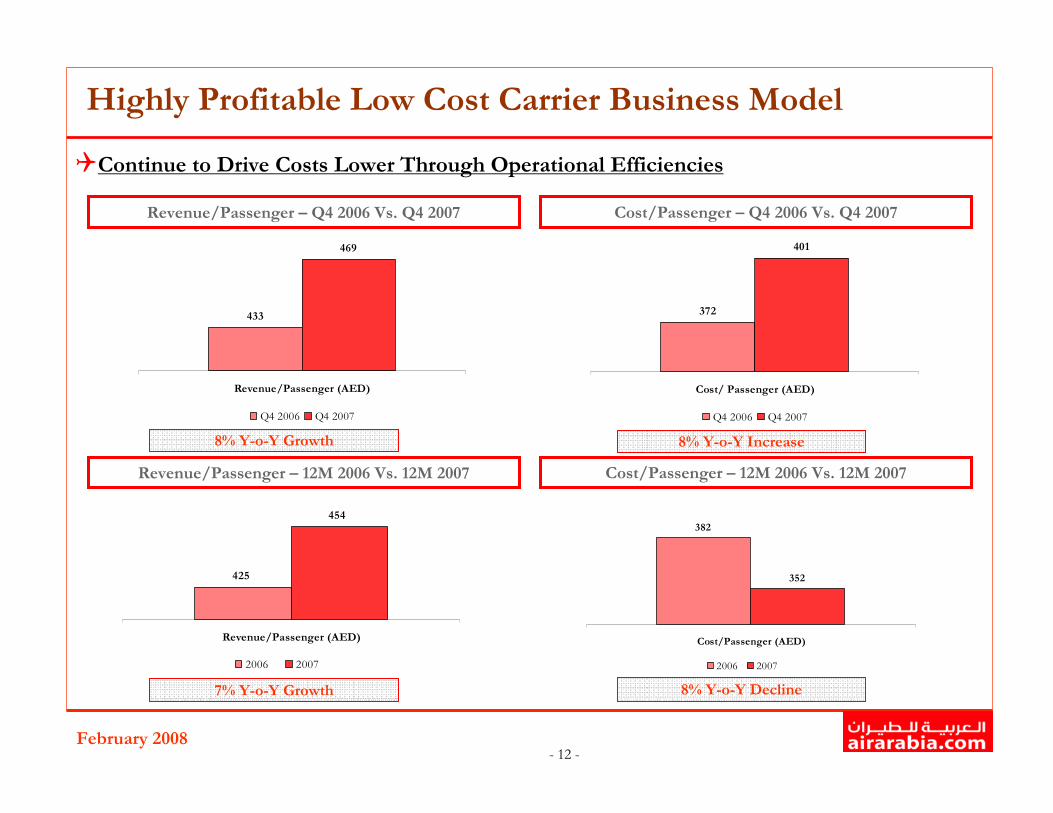

Highly Profitable Low Cost Carrier Business Model

8% Y-o-Y Growth

Revenue/Passenger – Q4 2006 Vs. Q4 2007 Cost/Passenger – Q4 2006 Vs. Q4 2007

8% Y-o-Y Increase

7% Y-o-Y Growth 8% Y-o-Y Decline

Revenue/Passenger – 12M 2006 Vs. 12M 2007 Cost/Passenger – 12M 2006 Vs. 12M 2007

�Continue to Drive Costs Lower Through Operational Efficiencies

433

469

Revenue/Passenger (AED)

Q4 2006 Q4 2007

372

401

Cost/ Passenger (AED)

Q4 2006 Q4 2007

425

454

Revenue/Passenger (AED)

2006 2007

382

352

Cost/Passenger (AED)

2006 2007

- 13 -February 2008

Highly Profitable Low Cost Carrier Business Model

* Other Costs include insurance and other operating costs

Operating Costs as a Percentage of Revenues

7.6% 4.3% 2.7% 4.2%

6.5%5.1% 4.2% 2.9%

32.4%31.2% 31.7%

14.4% 13.5%13.9% 11.8%

11.4% 10.9%9.9% 11.0%

14.4%11.4%

9.1% 8.9%

13.6%12.5%

14.3% 11.9%

4.6%

3.7%3.7%

2.3%

28.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2004 2005 2006 2007

G&A Expenses Sales & Marketing Fuel Aircraft LeaseDirect Staff Maintenance Airport Charges Others*

101.0%% of Revenue 93.8% 84.7%89.0%

- 14 -February 2008

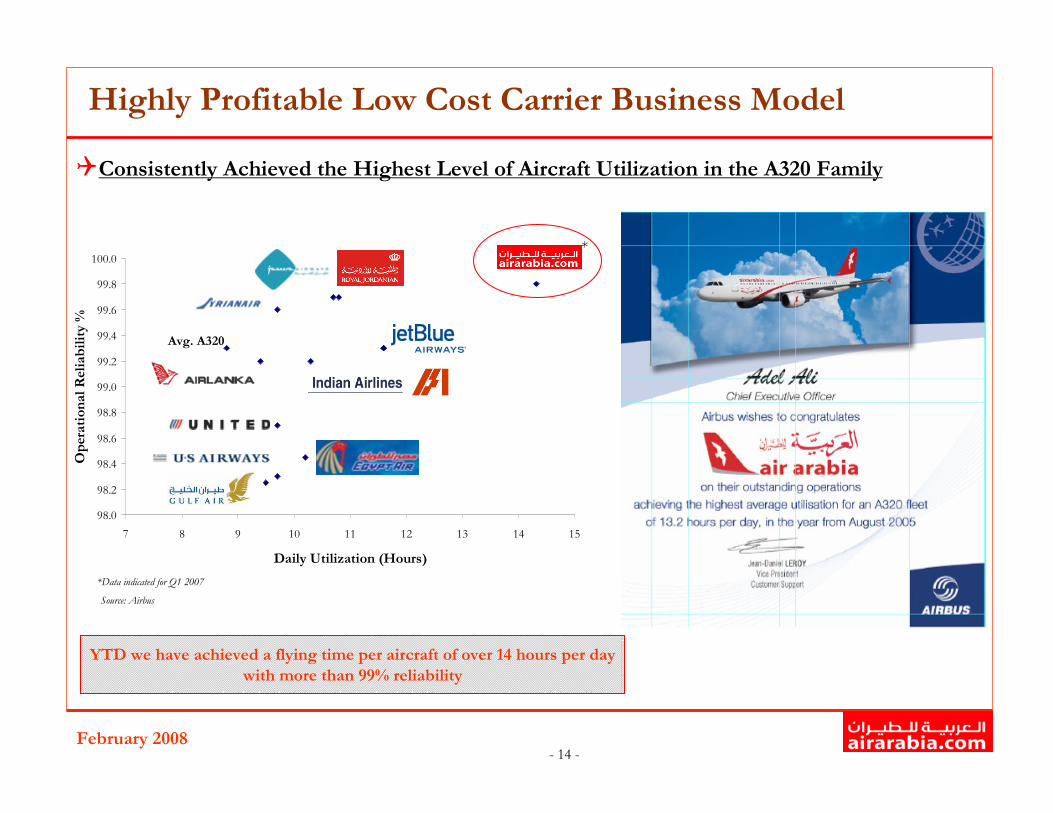

Highly Profitable Low Cost Carrier Business Model

98.0

98.2

98.4

98.6

98.8

99.0

99.2

99.4

99.6

99.8

100.0

7 8 9 10 11 12 13 14 15

Daily Utilization (Hours)

Operational Reliability %

Source: Airbus

YTD we have achieved a flying time per aircraft of over 14 hours per day

with more than 99% reliability

*

*Data indicated for Q1 2007

Avg. A320

�Consistently Achieved the Highest Level of Aircraft Utilization in the A320 Family

- 15 -February 2008

Highly Profitable Low Cost Carrier Business Model

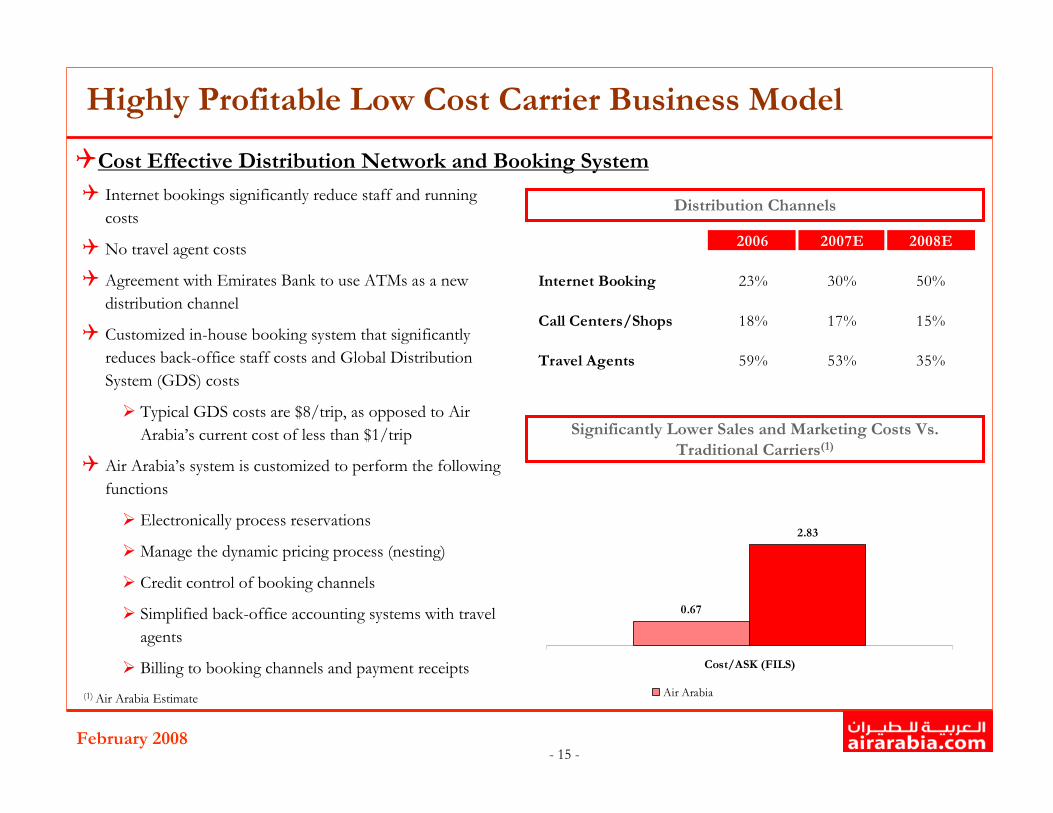

� Internet bookings significantly reduce staff and running

costs

� No travel agent costs

� Agreement with Emirates Bank to use ATMs as a new

distribution channel

� Customized in-house booking system that significantly

reduces back-office staff costs and Global Distribution

System (GDS) costs

� Typical GDS costs are $8/trip, as opposed to Air

Arabia’s current cost of less than $1/trip

� Air Arabia’s system is customized to perform the following

functions

� Electronically process reservations

� Manage the dynamic pricing process (nesting)

� Credit control of booking channels

� Simplified back-office accounting systems with travel

agents

� Billing to booking channels and payment receipts

Distribution Channels

Significantly Lower Sales and Marketing Costs Vs.

Traditional Carriers(1)

2006 2007E 2008E

Internet Booking 23% 30% 50%

Call Centers/Shops 18% 17% 15%

Travel Agents 59% 53% 35%

�Cost Effective Distribution Network and Booking System

(1) Air Arabia Estimate

0.67

2.83

Cost/ASK (FILS)

Air ArabiaTraditional M.E. network Carrier

- 16 -February 2008

Drive Growth Through an Aggressive Expansion Plan

4

8.5

2007 2008P

PAssengers (in M

M)

Fleet Expansion (Sharjah Hub)

We currently serve only 37 out of the potential 200 airports within 5-hours flying radius

Source: Sharjah Airport Website

�Significant Route and Fleet Expansion Planned, Supported by Sharjah Airport Expansion

Sharjah Airport Expansion

5 Hour Flying Radius (Sharjah Hub)

Target

Destinations32 50 85

811

19

34

2006 2007 2010P 2015P

Aircrafts

- 17 -February 2008

Drive Growth Through an Aggressive Expansion Plan

# of Destinations vs. Net Profit Margin Breakeven Load Factor vs. Actual Load Factor*

�Track Record of Profitable Expansion

(1)Two destinations added in October; Net income excluding interest on IPO funds

15

23

32

37

0.0%

7.6%

13.5%

30.2%

0

5

10

15

20

25

30

35

40

2004A 2005A 2006A 2007A

Destinations

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Net profit margin (%)

Destinations Net profit margin

73%67%

79% 80%86%

77%

0%

20%

40%

60%

80%

100%

2005 2006 2007

Breakeven load factor Actual load factor

Months to Recent Route

Start of

OperationsLoad Factors

Months to

Profitability

Chittagong - Bangladesh Jun - 07 95% 1

Peshwar - Pakistan Mar - 07 85% 2

Chennai - India Nov - 06 74% 2

Thiruvananthapuram - India Nov - 06 89% 2

Kochi - India May 06 95% 1

- 18 -February 2008

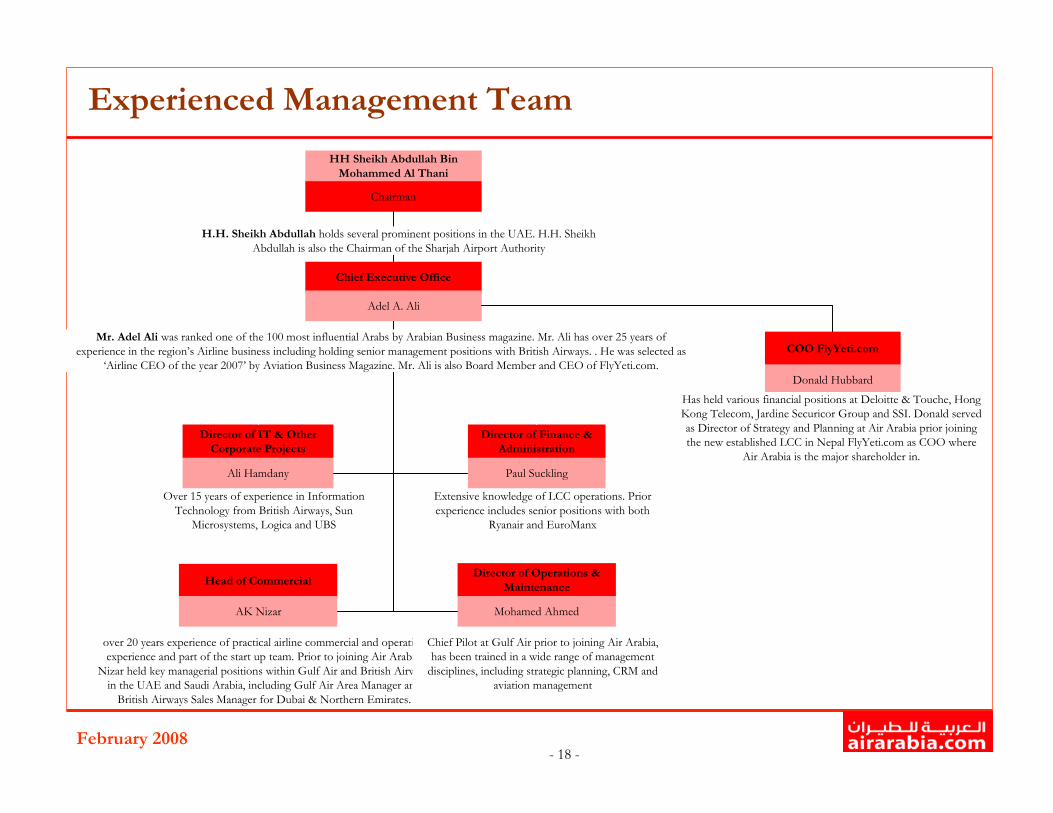

Experienced Management Team

Chief Executive Office

Adel A. Ali

Director of IT & Other

Corporate Projects

Ali Hamdany

Head of Commercial

AK Nizar

Director of Operations &

Maintenance

Mohamed Ahmed

COO FlyYeti.com

Donald Hubbard

Director of Finance &

Administration

Paul Suckling

HH Sheikh Abdullah Bin

Mohammed Al Thani

Chairman

H.H. Sheikh Abdullah holds several prominent positions in the UAE. H.H. Sheikh

Abdullah is also the Chairman of the Sharjah Airport Authority

Over 15 years of experience in Information

Technology from British Airways, Sun Microsystems, Logica and UBS

Extensive knowledge of LCC operations. Prior

experience includes senior positions with both Ryanair and EuroManx

Has held various financial positions at Deloitte & Touche, Hong Kong Telecom, Jardine Securicor Group and SSI. Donald served

as Director of Strategy and Planning at Air Arabia prior joiningthe new established LCC in Nepal FlyYeti.com as COO where

Air Arabia is the major shareholder in.

over 20 years experience of practical airline commercial and operating experience and part of the start up team. Prior to joining Air Arabia,

Nizar held key managerial positions within Gulf Air and British Airways in the UAE and Saudi Arabia, including Gulf Air Area Manager and

British Airways Sales Manager for Dubai & Northern Emirates.

Chief Pilot at Gulf Air prior to joining Air Arabia, has been trained in a wide range of management

disciplines, including strategic planning, CRM and aviation management

Mr. Adel Ali was ranked one of the 100 most influential Arabs by Arabian Business magazine. Mr. Ali has over 25 years of

experience in the region’s Airline business including holding senior management positions with British Airways. . He was selected as ‘Airline CEO of the year 2007’ by Aviation Business Magazine. Mr. Ali is also Board Member and CEO of FlyYeti.com.

February 2008- 19 -

Financial Highlights

- 20 -February 2008

Historical Financial Performance

Revenues Gross Profit

EBITDAR Net Profit

2465

130

318

12.5%

17.4%

25.9%

15.8%

0

50

100

150

200

250

300

350

2004 2005 2006 2007

Gross Profit (AED in M

M)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

% M

argin

Gross profit Margin

2984

182

421

34.4%24.3%20.4%

15.1%

0

100

200

300

400

500

2004 2005 2006 2007

EBITDAR (AED in M

M)

0.0%

5.0%

10.0%

15.0%20.0%

25.0%

30.0%

35.0%

40.0%% M

argin

EBITDAR EBITDAR Margin

031

101

370

30.2%

13.5%

0.0%7.5%

0

50

100

150

200

250

300

350

400

2004 2005 2006 2007

Net Profit (AED in M

M)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

% M

argin

Net Profit Net Margin

192

411

749

1,225

-

200

400

600

800

1,000

1,200

1,400

2004 2005 2006 2007

Revenues (AED in M

M)

- 21 -February 2008

Q4 2007 Financial Highlights

Revenues

Net Income(1)

EBITDAR Margin

Net Income Margin(1)

Growth Rate

Q4 06 – Q4 07: 62%

Q3 07 – Q4 07: -5%

(1)Including interest on cash proceeds from the recent IPO (AED 44m in Q3 2007)

215

369349

0

50

100

150

200

250

300

350

400

Q4 2006 Q3 2007 Q4 2007

AED in Millions

24.3%

34.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

FY 2006 FY 2007

15%

45%

26%

15%

33%

14%

0%

10%

20%

30%

40%

50%

Q4 2006 Q3 2007 Q4 2007

Including Interest Excluding Interest

33

165

90

0

50

100

150

200

Q4 2006 Q3 2007 Q4 2007

AED in M

illions

February 2008- 22 -

Strategy and Outlook

- 23 -February 2008

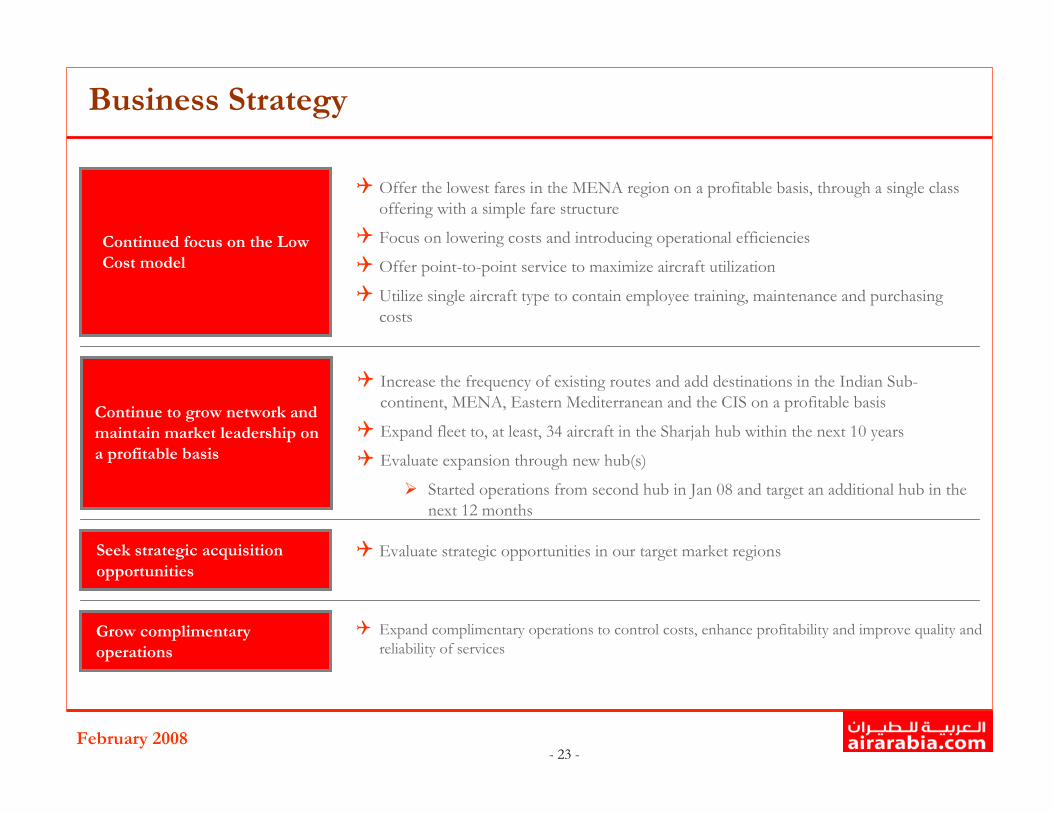

Business Strategy

Continue to grow network and

maintain market leadership on

a profitable basis

� Offer the lowest fares in the MENA region on a profitable basis, through a single class

offering with a simple fare structure

� Focus on lowering costs and introducing operational efficiencies

� Offer point-to-point service to maximize aircraft utilization

� Utilize single aircraft type to contain employee training, maintenance and purchasing

costs

� Increase the frequency of existing routes and add destinations in the Indian Sub-

continent, MENA, Eastern Mediterranean and the CIS on a profitable basis

� Expand fleet to, at least, 34 aircraft in the Sharjah hub within the next 10 years

� Evaluate expansion through new hub(s)

� Started operations from second hub in Jan 08 and target an additional hub in the

next 12 months

� Evaluate strategic opportunities in our target market regions

Continued focus on the Low

Cost model

Seek strategic acquisition

opportunities…………………

Grow complimentary

operations…………………….

� Expand complimentary operations to control costs, enhance profitability and improve quality and

reliability of services

- 24 -February 2008

Business Outlook

ST Outlook Long-term Outlook

2007 2008 outlook 2010E

Aircraft 11 14 ~ 19

Destinations 37 40 ~ 50

Passengers 2.7 Million 3.3 Million ~ 4.5 Million

Revenue Y-o-Y Growth 64%

Growth expected to

be at ~ 30% p.a.

Growth expected to

be maintained at ~

20%-25% p.a. for the

next 3 years

Profitability

EBITDAR margin at

34%

EBITDAR margin

level (~30%)

EBITDAR margin

level (~30%)

Aircraft --- 2 ~6

Destinations --- 6 ~ 20

Passengers ~ 1.4 Million

qWe target a 15% return on investments in our complimentary operations, in the long-term

Sharjah Hub

Nepal Hub

Complimentary

Operations

February 2008- 25 -

Appendix

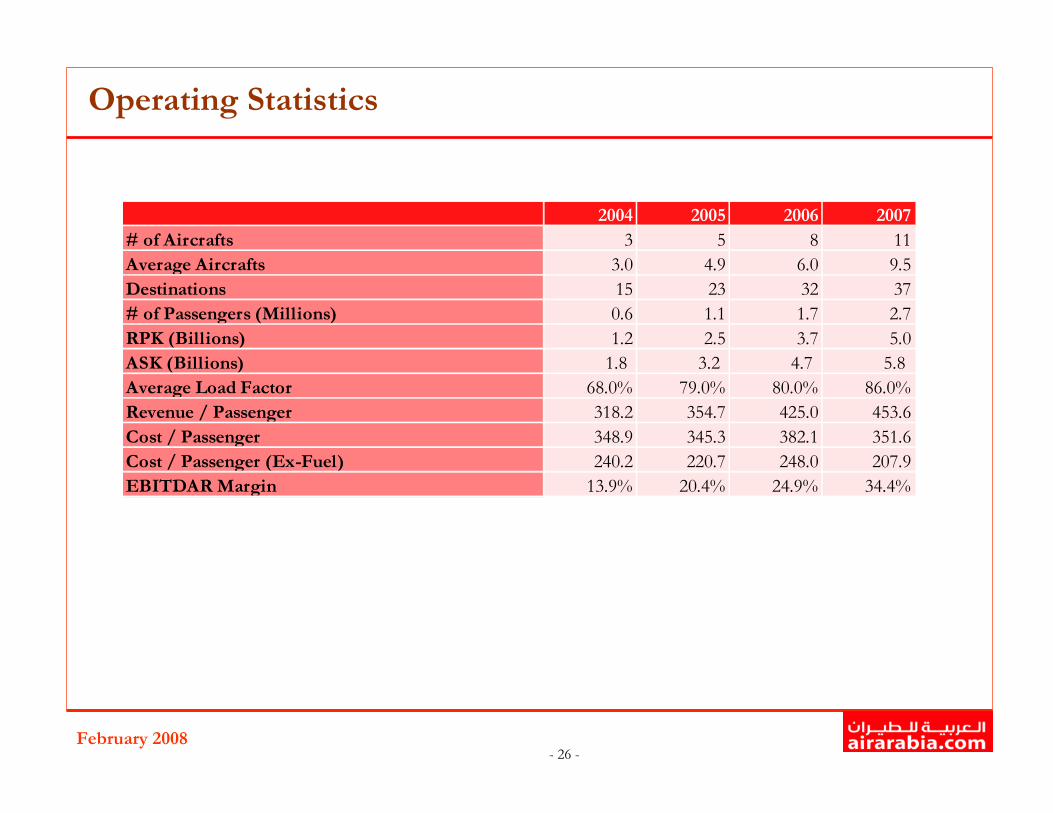

- 26 -February 2008

Operating Statistics

2004 2005 2006 2007

# of Aircrafts 3 5 8 11

Average Aircrafts 3.0 4.9 6.0 9.5

Destinations 15 23 32 37

# of Passengers (Millions) 0.6 1.1 1.7 2.7

RPK (Billions) 1.2 2.5 3.7 5.0

ASK (Billions) 1.8 3.2 4.7 5.8

Average Load Factor 68.0% 79.0% 80.0% 86.0%

Revenue / Passenger 318.2 354.7 425.0 453.6

Cost / Passenger 348.9 345.3 382.1 351.6

Cost / Passenger (Ex-Fuel) 240.2 220.7 248.0 207.9

EBITDAR Margin 13.9% 20.4% 24.9% 34.4%