AIP Costco Executive Summary

8

Applied Investments Program 1 Costco Wholesale Corp. Ticker: COST Change Insider Positions: -0.43% Current Price: $155.92 EV/EBITDA: 13.93 52 Week High: $156.85 Market Cap (mil): $68,683 52 Week Low: $109.50 Shares (mil): 440.5 MStar Fair Value: $135.00 Sector: Consumer Staples EPS T12 $4.82 P/E T12: 32.3 EPS Next Year: $5.18 ROA: 6.4% DuPont ROE 16.44% BEST 12M Target Price: $149.47 Ste wards hip rating: Exemplary Morningstar credit rating: AA- Economic Moat: Wide ROE 2014: 17.79% Dividend Schedule: 02/05/2015 Spec Div. $5.00 11/12/2014 Cash Div. $0.35 07/09/2014 Cash Div. $0.35 05/14/2014 Cash Div. $0.35 Stock type: Classic growth Stock Style: Large growth Wall St. Recommendations Buys 5 Holds 3 Sell 1 Liquidity/Financial Health (Latest Quarter) Current ratio 1.2 Quick ratio 0.55 Financial Leverage 2.8 Debt/Equity 0.41 AIP FCF Costco.xlsx Research Highlights and Investment Thesis Research Highlights Costco has had exceptional growth and cash generation over the past 5 years and will have opened an estimated 65 new stores between 2014 and 2015. The company operates at extremely tight margins and near ly all of the company’s profit is generated through membership subscriptions. There are three main types of subscribers; Gold Star memberships, Business Memberships, and Executive Memberships. Gold Star and Business memberships pay an annual subscription of only $55 per year while Executive memberships pay $110 per year. Costco’s average warehouse is 144,000 square feet, but newly built warehouses are becoming even larger. Costco wields significant buying power by providing access to a large network of repeat consumers. Costco’s buying power coupled with strong supplier relations allows Costco to maintain an efficient supply chain of over 258 suppliers, these key qualities result in lower operating costs where savings are passed on to the customer. The company currently operates around 670 warehouses all over the nation and has recently begun expansion into new global markets including China, Spain, Puerto Rico, Canada, United Kingdom, Mexico, Japan, Australia, Taiwan and Korea. Additionally, the company has recently issued $1 billion in bonds that will be used to fund a special dividend to be paid out on Feb 27, 2015 Investment Thesis I recommend a hold on Costco, when taking into account my DCF analysis, the prior analysts sell target, and my research of the company I find the company near fair value. Although we have held Costco since May 21, 2014 the corporation appears to have some upside coupled with the strong potential for growth. Similarly, our current portfolio positioning would be negatively affected if we were to sell Costco and I find the risk of holding Costco in the short term to be lower than the risk of being seriously underweight within the Consumer staples sector given the substantial negative upsides of CVS health and Molson Coors. Costco has generated strong cash flow and is likely to continue into the foreseeable future, thus supporting the company’s sizeable dividends. Overall, management has performed well and the company is expanding into new markets which will further support their prevailing strong growth rate. 110 120 130 140 150 160

-

Upload

ryan-sopinski -

Category

Documents

-

view

84 -

download

0

Transcript of AIP Costco Executive Summary

Applied Investments Program 1

Costco Wholesale Corp.

Ticker: COST Change Insider Positions: -0.43% Current Price: $155.92 EV/EBITDA: 13.93

52 Week High: $156.85 Market Cap (mil): $68,683 52 Week Low: $109.50 Shares (mil): 440.5 MStar Fair Value: $135.00 Sector: Consumer Staples

EPS T12 $4.82 P/E T12: 32.3

EPS Next Year: $5.18 ROA: 6.4% DuPont ROE 16.44% BEST 12M Target Price: $149.47

Stewardship rating: Exemplary

Morningstar credit rating: AA- Economic Moat: Wide ROE 2014: 17.79%

Dividend Schedule: 02/05/2015 Spec Div. $5.00 11/12/2014 Cash Div. $0.35 07/09/2014 Cash Div. $0.35 05/14/2014 Cash Div. $0.35 Stock type: Classic growth Stock Style: Large growth

Wall St. Recommendations Buys 5 Holds 3 Sell 1

Liquidity/Financial Health

(Latest Quarter) Current ratio 1.2 Quick ratio 0.55 Financial Leverage 2.8 Debt/Equity 0.41

AIP FCF Costco.xlsx

Research Highlights and Investment Thesis Research Highlights

Costco has had exceptional growth and cash generation over the past 5 years and will have opened an estimated 65 new stores between 2014 and 2015.

The company operates at extremely tight margins and nearly all of the company’s profit is generated through membership subscriptions. There are three main types of subscribers; Gold Star memberships, Business Memberships, and Executive Memberships. Gold Star and Business memberships pay an annual subscription of only $55 per year while Executive memberships pay $110 per year.

Costco’s average warehouse is 144,000 square feet, but newly built warehouses are becoming even larger.

Costco wields significant buying power by providing access to a large network of repeat consumers. Costco’s buying power coupled with strong supplier relations allows Costco to maintain an efficient supply chain of over 258 suppliers, these key qualities result in lower operating costs where savings are passed on to the customer. The company currently operates around 670 warehouses all over the nation and has recently begun expansion into new global markets including China, Spain, Puerto Rico, Canada, United Kingdom, Mexico, Japan, Australia, Taiwan and Korea.

Additionally, the company has recently issued $1 billion in bonds that will be used to fund a special dividend to be paid out on Feb 27, 2015

Investment Thesis I recommend a hold on Costco, when taking into account my DCF analysis, the prior analysts sell

target, and my research of the company I find the company near fair value. Although we have held

Costco since May 21, 2014 the corporation appears to have some upside coupled with the strong

potential for growth. Similarly, our current portfolio positioning would be negatively affected if

we were to sell Costco and I find the risk of holding Costco in the short term to be lower than the

risk of being seriously underweight within the Consumer staples sector given the substantial

negative upsides of CVS health and Molson Coors. Costco has generated strong cash flow and is

likely to continue into the foreseeable future, thus supporting the company’s sizeable dividends.

Overall, management has performed well and the company is expanding into new markets which

will further support their prevailing strong growth rate.

110

120

130

140

150

160

Applied Investments Program 2

Business Description Notes A 7 Day 69 hour work week

allows for lower labor costs in comparison to other retailers.

Sales, General, and Admin accounted for $10,899,000,000

Costco had $112,640,000,000 in revenue for FY 2014

Selling, General and Admin as a % of Revenue Peer Comparison

Peer Revenue Comparison

Percentage of portfolio consumer

staples sector holdings

Business Description Costco Wholesale Corp is a large wholesaler that operates membership warehouses

in multiple countries. The company began operations in 1983 in Seattle, Washington and is principally engaged in the operation of membership warehouses in the United States and Puerto Rico, Canada, United Kingdom, Mexico, Japan, Australia, Spain, and through majority owned subsidiaries in Taiwan and Korea. Similarly, the company’s stock is traded on the NASDAQ.

Costco’s business model operates approximately 670 membership warehouses with the intent to offer members low prices on a limited selection of nationally branded and select private – label products in a wide range of merchandise categories.

Costco buy’s the majority of their merchandise directly from manufacturers and direct it to a cross-docking consolidation point, essentially a large warehouse, where the merchandise is reallocated and organized to be shipped to individual warehouses that provide stores with inventory. The company’s average warehouse is 144,000 square feet with newer warehouses

being slightly larger. The company’s marketing activities include regularly participating in community

outreach programs to local businesses in new and existing markets. Warehouses owned by the company operate seven days a week between 10:00 am

and 8:30 pm. Due to efficient operations the company is able maintain lower labor costs by

averaging lower hours of operation in comparison to other retailers.

Costco’s core strategy is to provide members with a broad range of high quality merchandise at prices consistently lower than they would be able to obtain anywhere else.

Portfolio Positioning Currently, we are overweight the Consumer Staples sector by 0.54%. Within the consumer

staples sector we have four holdings being: Costco Wholesale Corp (1.28% weight), CVS Health Corp (4.08% weight), Molson Coors Brewing (3.35% weight), and Walmart Stores (1.67% weight).

Costco became a holding of the portfolio May 21, 2014 at a price of $114.52 with a market value of $7,444 making up 65 shares in the company. We now own 35 shares with a market value of $5,205 and a current price per share of $148.70.

Our four holdings within the Consumer Staples sector are highly correlated with each other. In addition, all share a strong correlation with Vanguards Consumer Staples ETF (VDC)

All companies within the consumer staples sector of the portfolio, excluding Molson Coors Brewing, have a wide economic moat, which has a narrow moat.

On the other hand, Costco Wholesale Corp. has exceeded its adjusted sell target of $138.23 offering a -7% upside based on past analysis. Further, CVS Health Corp and Molson Coors have also exceeded their adjusted sell targets providing a -15% upside for CVS Health Corp and a -17% upside for Molson Coors. Given, these holdings it will be necessary for the team to try to search for new candidates for the portfolio’s consumer staples sector.

Lastly, our current holdings in consumers staples account for 10.38% of the overall portfolio and 8.71% of the portfolio has exceeded their adjusted sell targets and now have negative upsides. 83.14% of our Consumer Staples holdings have a negative upside.

0.0%5.0%

10.0%15.0%20.0%25.0%30.0%35.0%

Co

stco

Targ

et

Do

llar

Gen

eral

Wal

mar

t

Wal

gree

ns

$0$50,000

$100,000$150,000$200,000$250,000$300,000$350,000$400,000

Cost

co

Targ

et

Do

llar

Gen

eral

Wal

mar

t

Wal

gre

en

s

(IN

MIL

LIO

NS

0.00%0.50%1.00%1.50%2.00%2.50%3.00%3.50%4.00%4.50%

Cost

co

CV

S H

ealt

h

Mo

lson

Coo

rs

Wal

mar

t

Applied Investments Program 3

Costco two-part bond issuance

Initial issue price: 99.704

Yield at pricing: 2.296

Coupon: 2.25%

Coupon freq: semi-annual

Settlement: 02/17/2015

Maturity 02/15/2022

Initial issue price: 99.895

Yield at pricing: 1.772

Coupon: 1.75%

Coupon freq: semi-annual

Settlement: 02/17/2015

Maturity 02/15/2020

Omega “Seamaster” watch

Source: Google images

Consumer Staples Upside to Sell Consumer staples daily returns correlation matrix

Recent News Costco has recently entered the Chinese retail market and was open for business in

November 2014. In addition, Costco has set up a store on the e-commerce giant Alibaba’s mall-like designed global platform. Customers who purchase Costco products through the Alibaba platform can expect to receive products within five to 20 days of purchase.

Deutsche Bank recently downgraded their rating on the company’s stock from a hold to a buy. Deutsche Bank cites the potential for Costco to struggle with negative foreign currency translation and also expects that lower gas prices may pose a negative impact on same store sales because consumers may now have incentive to drive further away than their local Costco in search of better deals.

Costco has recently engaged in the issuance of new debt. The new debt has been granted an A rating and was announced on February 5, 2015. Moreover, the debt will be issued in multiple tranches totaling $1 billion. The $1 billion will be broken up into two large tranches being, one for $500 million 1.75% senior unsecured notes that are due in 2020, and the other being $500 million 2.25% senior unsecured notes that are due in 2022. The debt was distributed as domestic bonds and have combined registration fees in accordance with Rule 457® under the Securities act of 1933 of $115,967. The registration fees have been broken down into $58,039 due for the 1.750% bonds and $57,928 due for the 2.25% bonds.

On February 6, 2015 Costco appeared as one of 36 companies on Bloomberg news that has had the biggest changes in implied volatility based on the options market. All companies on this list had the biggest percentage changes in implied volatility for the previous trading day, are more than 10 days from expiration, have a trading volume of at least 200 contracts and have strike prices within 5% of the underlying security’s price. http://finance.yahoo.com/q/op?s=COST&date=1429228800

Costco has had recent legal battles relating to the sale of Luxury watches. The legal battle stems from manufacturer Omega watches claiming Costco engaged in copyright infringement under the expanded first doctrine when the company (Costco) imported and sold Omega’s bestselling “Seamaster” watch from the gray market. Watches sold by Costco were obtained by ENE limited who purchased the watches from unidentified third parties. Costco then sold 43 of the watches to discount club members at a price significantly below-market retail price. Through multiple appeals the court has ruled in favor of Costco citing the first sale doctrine. The court determined that Costco did not violate the first sale doctrine because Omega authorized the first sale of the watches to its foreign distributors.

**A gray market is and unofficial market where the import and sale of goods by unauthorized

dealers occurs. Such and activity although unofficial is not illegal.

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

0% 1% 2% 3% 4%

BO

ND

PR

ICE

YTM

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

0% 1% 2% 3% 4%

BO

ND

PR

ICE

YTM

-15%

-5%

5%

15%

Cost

co

CV

S H

ea

lth

Mo

lson

Coor

s

Wal

ma

rt

Costco WalmartMolson

Coors

CVS

Health

VDC

ETFCostco 1 0.927 0.888 0.957 0.991

Walmart 0.927 1 0.777 0.864 0.961

Molson Coors 0.888 0.777 1 0.934 0.866

CVS Health 0.957 0.864 0.934 1 0.955

VDC ETF 0.991 0.961 0.866 0.955 1

Correlation Matrix

Highest Correlation Lowest Correlation

Applied Investments Program 4

Return on Common Equity FY 2014

Effective Tax Rate FY 2014

Current Ratio FY 2014

Source: Google images

Source: Google images

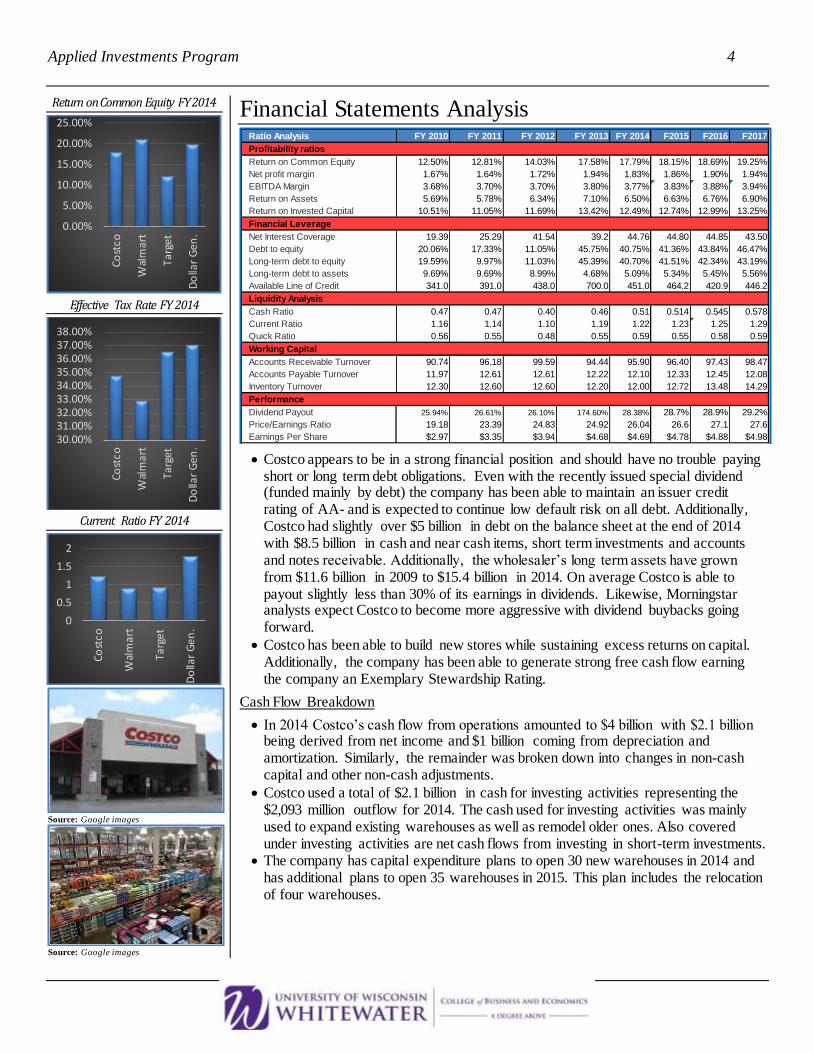

Financial Statements Analysis

Costco appears to be in a strong financial position and should have no trouble paying

short or long term debt obligations. Even with the recently issued special dividend (funded mainly by debt) the company has been able to maintain an issuer credit rating of AA- and is expected to continue low default risk on all debt. Additionally, Costco had slightly over $5 billion in debt on the balance sheet at the end of 2014 with $8.5 billion in cash and near cash items, short term investments and accounts and notes receivable. Additionally, the wholesaler’s long term assets have grown from $11.6 billion in 2009 to $15.4 billion in 2014. On average Costco is able to payout slightly less than 30% of its earnings in dividends. Likewise, Morningstar analysts expect Costco to become more aggressive with dividend buybacks going forward.

Costco has been able to build new stores while sustaining excess returns on capital. Additionally, the company has been able to generate strong free cash flow earning the company an Exemplary Stewardship Rating.

Cash Flow Breakdown

In 2014 Costco’s cash flow from operations amounted to $4 billion with $2.1 billion being derived from net income and $1 billion coming from depreciation and amortization. Similarly, the remainder was broken down into changes in non-cash capital and other non-cash adjustments.

Costco used a total of $2.1 billion in cash for investing activities representing the $2,093 million outflow for 2014. The cash used for investing activities was mainly used to expand existing warehouses as well as remodel older ones. Also covered under investing activities are net cash flows from investing in short-term investments.

The company has capital expenditure plans to open 30 new warehouses in 2014 and has additional plans to open 35 warehouses in 2015. This plan includes the relocation of four warehouses.

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%Co

stco

Wal

mar

t

Ta

rge

t

Do

llar

Gen

.

30.00%31.00%32.00%33.00%34.00%35.00%36.00%37.00%38.00%

Cost

co

Wal

ma

rt

Targ

et

Do

llar

Gen

.

0

0.5

1

1.5

2

Cost

co

Wal

mar

t

Targ

et

Do

llar

Gen

.

Ratio Analysis FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 F2015 F2016 F2017

Profitability ratios

Return on Common Equity 12.50% 12.81% 14.03% 17.58% 17.79% 18.15% 18.69% 19.25%

Net profit margin 1.67% 1.64% 1.72% 1.94% 1.83% 1.86% 1.90% 1.94%

EBITDA Margin 3.68% 3.70% 3.70% 3.80% 3.77% 3.83% 3.88% 3.94%

Return on Assets 5.69% 5.78% 6.34% 7.10% 6.50% 6.63% 6.76% 6.90%

Return on Invested Capital 10.51% 11.05% 11.69% 13.42% 12.49% 12.74% 12.99% 13.25%

Financial Leverage

Net Interest Coverage 19.39 25.29 41.54 39.2 44.76 44.80 44.85 43.50

Debt to equity 20.06% 17.33% 11.05% 45.75% 40.75% 41.36% 43.84% 46.47%

Long-term debt to equity 19.59% 9.97% 11.03% 45.39% 40.70% 41.51% 42.34% 43.19%

Long-term debt to assets 9.69% 9.69% 8.99% 4.68% 5.09% 5.34% 5.45% 5.56%

Available Line of Credit 341.0 391.0 438.0 700.0 451.0 464.2 420.9 446.2

Liquidity Analysis

Cash Ratio 0.47 0.47 0.40 0.46 0.51 0.514 0.545 0.578

Current Ratio 1.16 1.14 1.10 1.19 1.22 1.23 1.25 1.29

Quick Ratio 0.56 0.55 0.48 0.55 0.59 0.55 0.58 0.59

Working Capital

Accounts Receivable Turnover 90.74 96.18 99.59 94.44 95.90 96.40 97.43 98.47

Accounts Payable Turnover 11.97 12.61 12.61 12.22 12.10 12.33 12.45 12.08

Inventory Turnover 12.30 12.60 12.60 12.20 12.00 12.72 13.48 14.29

Performance

Dividend Payout 25.94% 26.61% 26.10% 174.60% 28.38% 28.7% 28.9% 29.2%

Price/Earnings Ratio 19.18 23.39 24.83 24.92 26.04 26.6 27.1 27.6

Earnings Per Share $2.97 $3.35 $3.94 $4.68 $4.69 $4.78 $4.88 $4.98

Applied Investments Program 5

Costco’s global diversification

has added to their ability to

compete with other

multinational corporations such

as Walmart and Target Revenue Growth 2009-2015

Source: Bloomberg data analyst developed chart

Net Income Growth 2009-2015

Source: Bloomberg data analyst developed chart

Profit Margin 2009-2015

Source: Bloomberg data analyst developed chart

Costco relies on over 258 suppliers to fulfill the needs of warehouse

stocking

Lastly, the company’s cash flow from financing activities accounted for $1.2 billion in

2014. Net cash used in financing activities grew drastically from $44 million up to $786

million the primary uses of cash were the issuance of dividends common stock

repurchases, and payment of withholding taxes on stock-based awards. Throughout 2013

and 2014 Costco underwent a stock repurchases program and repurchased 357,000 and

2,915,000 common shares respectively. In 2013 the average price being $96.41 per share

and $114.45 per share in 2014. In April of 2014 the board of directors increased the

company’s quarterly cash dividend from $0.31 to $0.355 per share totaling $1.33 per

share in 2014.

Income statement analysis

Costco’s revenue has grown significantly from 2009 to 2014 and has kept the strong pace

of 9.53% per year on average. In 2009 Costco had $71.4 billion in revenue growing to

$112.6 billion in 2014.

Similarly, Costco has seen even stronger growth in net income over the same time period

growing at an average rate of 14% over the 5 year period.

Although Costco has be able to generate over $112.6 billion in revenue for FY 2014, the

company is still operating at razor thin profit margins. Net income margins for the fiscal

year ending in 2014 were only 1.83% these small margins are one of the main drivers of

Costco’s ability to stay extremely competitive in terms of pricing. Supply chain

management and strong supplier relationships are also strong contributors to success.

0

20000

40000

60000

80000

100000

120000

140000

2009

2011

2013

2015

ACTUAL PROJECTED

10001200140016001800200022002400

2009

2010

2011

2012

2013

2014

2015

ACTUAL PROJECTED

0

0.5

1

1.5

2

2.5

2009

2010

2011

2012

2013

2014

Applied Investments Program 6

EV/EBITDA Comparisons

Source: Bloomberg data analyst developed chart

Source: Bloomberg data analyst developed chart

Source: Bloomberg data analyst developed chart

DCF Analysis Discount Rate 8.0%

Discount Rate 9.0%

Discount Rate 10.0%

Valuation

Peer relative

Based on a peer relative valuation comparing Costco to Walmart, Target, and Dollar General the DCF model computes an implied fair value of $102.02, I found this value to be low based on my own estimations and further refined the valuation model to retail consumer staples companies with similar market caps. An EQS screening of companies within the consumer staples sector, market caps between $50 billion and $70 billion, and a country of domicile within the United States yielded three results; Mondelez International (MDLZ), Colgate Palmolive (CL), and Costco Wholesale(COST). These two additional companies were then analyzed against Costco with the addition of CVS health. The analysis showed a more comparable scenario in terms of EV/EBITDA, but offered a lower implied fair value of $94.95. A final analysis comparing Costco to Walmart, Dollar General, and CVS health yielded an implied fair value of $113.19. The average of the three results would imply a fair value of ~$103/share.

DCF Analysis

Inputs Sales growth: 7.8%, 8.0%, 9.6%, 9.4%

My estimates of company growth are slightly higher than consensus in the short term

but at or below consensus in the long term. I believe the company will continue to

maintain strong growth rates in the short as they continue to open new stores, but may

face hardship over the long haul when opening more stores starts to become difficult

due to market saturation. My 2015-2017 estimates are slightly over consensus, yet

below the 5 year average.

Cogs: 88.1%

Cogs of good sold will likely remain relatively stable, Costco relies on small margins

and low pricing to maintain a competitive advantage and the company cannot afford to

have higher COGS in the long run. I expect that management will continue to maintain

strong relations with suppliers and the company will continue to have significant

buying power over their many suppliers.

SGA: 10.0%

Costco may face a slight uptick in SGA as the company continues to open new stores

and hire new staff. Costco opened 30 new stores in 2014 and is planning to open an

additional 35 in 2015.

Taxes: 35.2%

Taxes may increase slightly as the Obama administration has recently proposed a large

tax increase on American companies, specifically relating to overseas profits. 14 of the

30 warehouses developed in 2014 were overseas.

Debt 22.5%

Costco’s recent $1 billion special dividend will be funded mostly by debt through the

issuance of two tranches of bonds at $500 million each. The shorter of the two debt

issuance’s will be $500 million of 1.750% notes due February 15, 2015, with the longer

of the two being $500 million of 2.250% notes due February 15, 2022.

Although we have been invested in Costco for quite some time, after performing the DCF analysis it appears that there may still be some upside left the company, the team must be aware of the fact that all companies within the Consumer staples sector including Costco, excluding Walmart have exceeded their adjusted sell target. The team should consider companies within the consumer staples sector when searching for a company to research that could replace our current holdings within that sector. Based on a discount rate of 9.0% Costco has an estimated NPV per share of $170.18

02468

10121416

CO

ST

CO

WH

OL

ES

AL

E

WA

L-M

AR

TS

TO

RE

S

CV

S H

EA

LT

HC

OR

P

DO

LLA

RG

EN

ER

AL

C

02468

1012141618

CO

ST

CO

WH

OL

ES

AL

E

MO

ND

ELE

ZIN

TE

R-A

CV

S H

EA

LT

HC

OR

P

CO

LGA

TE

-P

AL

MO

LIV

02468

10121416

CO

ST

CO

WH

OLE

SA

LE

WA

L-M

AR

TST

OR

ES

TA

RG

ET

CO

RP

DO

LLA

RG

ENER

AL

Applied Investments Program 7

Upside to Sell Consumer Staples current holdings

Source: AIP price watch list

Crude Oil production in millions of barrels per day forecast to 2030

Source: U.S. Energy Information Administration

Natural gas plant liquids production in millions of barrels

per day forecast to 2030

Source: U.S. Energy Information Administration

Applied Investment Portfolio Sector holdings by weight

Investment Risks Portfolio Positioning

Our current portfolio positioning poses some risk based on our current holdings within

the consumer staples sector. We currently have four holdings, three of which have

exceeded their adjusted sell targets. The three that have exceeded their sell targets are

CVS health, Molson Coors, and Costco by -15%, -8%, and -6% respectively. Currently,

Walmart appears to contain some upside. Recently issued debt

The recently issued debt of $1 billion could pose some risk if Costco were unable to

maintain current levels of annual revenue. If the company were to see a decrease in sales

due to macroeconomic conditions or serious systematic risks they may be unable to make

timely debt payments. I perceive this risk to be quite small considering that Costco lies

within the Consumer Staples sector providing essential products such as food, beverages,

tobacco, and household items. Consumer Staples is generally considered a safe haven

during economic downturns and it is likely that Costco would not be as adversely

affected during an economic depression as other companies from external sectors. Changes in accounting standards

Within the company’s 10k management offers some comment on risks associated with

changes in accounting standards. The company relies heavily on current accounting

standards and would face some significant risk if assumptions that management currently

has and operates on were to change. Changes in legal standards

Changes in current legal interpretations and judgments could pose some additional risks.

If Costco continues to operate based on assumptions of current laws and regulations and

those laws and regulations change the company could face some legal risk, especially if

laws relative to purchasing items through the gray market to distribute through

warehouses would become illegal in all cases. Components of Climate change

Components relevant to climate change could negatively impact Costco’s business as the

company uses natural gas, diesel fuel, gasoline, and electricity in their distribution centers

and warehouse operations. Increased government regulations on these types of energy

sources could result in higher operating costs depleting Costco’s ability to operate at

current price levels and remain competitive. Moreover, the company sells a large amount

of gasoline as a portion of their revenue source and could be negatively affected if

consumers shift demand to more environmentally friendly sources of energy for

transportation.

Conclusion and Recommendation In conclusion, I recommend a weak hold on Costco based on a multitude of factors. First, I find the company almost fairly valued when taking into account my DCF analysis, the prior analysts sell target, Morningstar research, and lastly my research of the company. Based on these factors I offer a fair value of $160.00/share. On the other hand, Costco appears to have some upside remaining coupled with a strong potential for continued growth. Similarly, our current portfolio positioning would be adversely affected if eliminated our Costco holdings and I find the risk of holding Costco to be lower than the risk of being seriously underweight the Consumer staples sector given the substantial negative upsides of CVS health and Molson Coors. Costco has been able to generate strong cash flow and is likely to continue into the future which will support their ability to issue sizeable dividends. Overall, management has performed well earning a Morningstar management rating of exemplary and the company is expanding into new markets which will further support their strong growth rate.

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

CVS

Hea

lth

Mo

lson

Coo

rs

Cost

co

Wal

mar

t

6

7

8

9

10

2013

2016

2019

2022

2025

2028

2.2

2.4

2.6

2.8

3

3.2

2013

2016

2019

2022

2025

2028

$2%

CD12%

CS

10%

Ene.

12%

Fin.13%Funds

6%

HC10%

Ind.11%

IT16%

Mat.Tele.1%

Uti l.3%

Applied Investments Program 8

Tables and Exhibits

Costco vs Vanguard Consumer Staple ETF ( = 0.991 )

Costco Historical Price Chart (May 2013-Jan 2015)

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

160

180Costco vs. Consumer Staples ETF

Costco (VDC) ETF