Aim: Money Matters – Credit Cards Course: Math Literacy Aim: How does money matter? Installment...

16

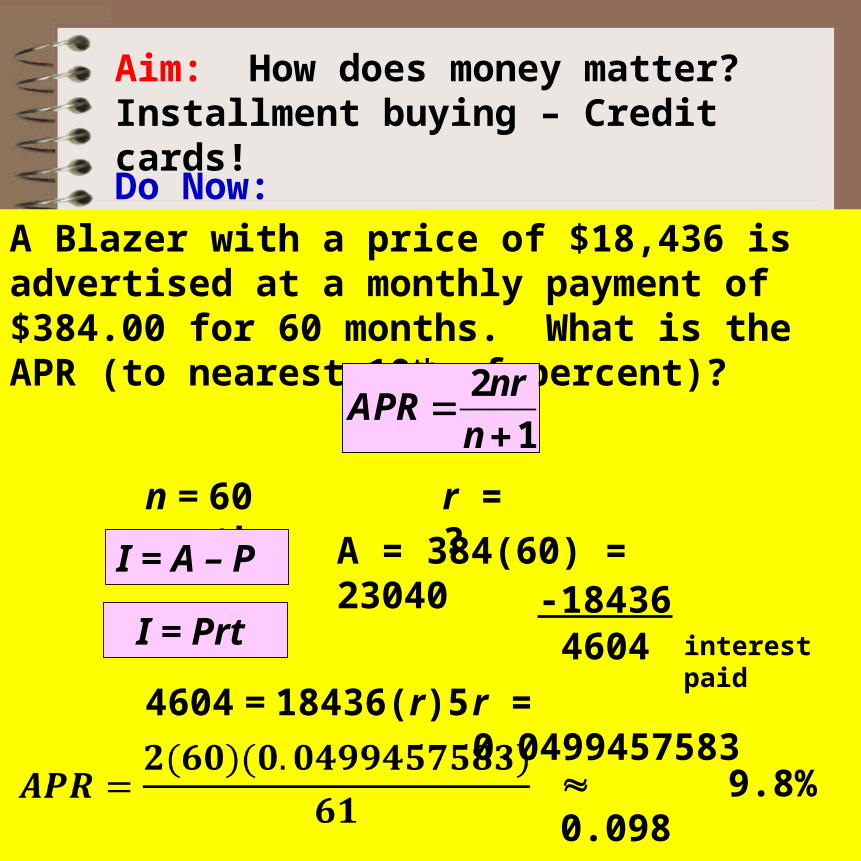

Aim: Money Matters – Credit Cards Course: Math Literacy Aim: How does money matter? Installment buying – Credit cards! Do Now: A Blazer with a price of $18,436 is advertised at a monthly payment of $384.00 for 60 months. What is the APR (to nearest 10 th of percent)? n = 60 months r = ? I = A – P A = 384(60) = 23040 -18436 4604 I = Prt 4604 = 18436(r)5 r = 0.0499457583 0.098 9.8% 2 1 nr APR n interest paid

-

Upload

marshall-goodwin -

Category

Documents

-

view

214 -

download

0

Transcript of Aim: Money Matters – Credit Cards Course: Math Literacy Aim: How does money matter? Installment...

Aim: Money Matters – Credit Cards Course: Math Literacy

Aim: How does money matter? Installment buying – Credit cards!

Do Now:

A Blazer with a price of $18,436 is advertised at a monthly payment of $384.00 for 60 months. What is the APR (to nearest 10th of percent)?

n = 60 months r = ?

I = A – P A = 384(60) = 23040 -184364604I = Prt

4604 = 18436(r)5 r = 0.0499457583

0.098

9.8%

2

1

nrAPR

n

interest paid

Aim: Money Matters – Credit Cards Course: Math Literacy

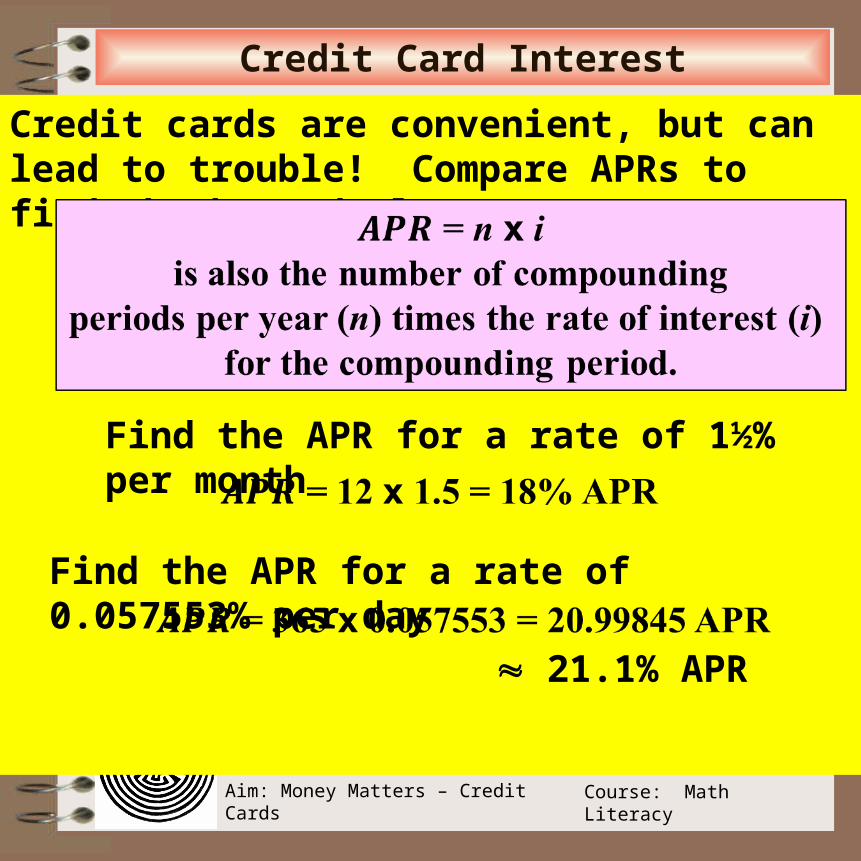

Credit Card Interest

Credit cards are convenient, but can lead to trouble! Compare APRs to find the best deal.

Find the APR for a rate of 1½% per month

Find the APR for a rate of 0.057553% per day

21.1% APR

Aim: Money Matters – Credit Cards Course: Math Literacy

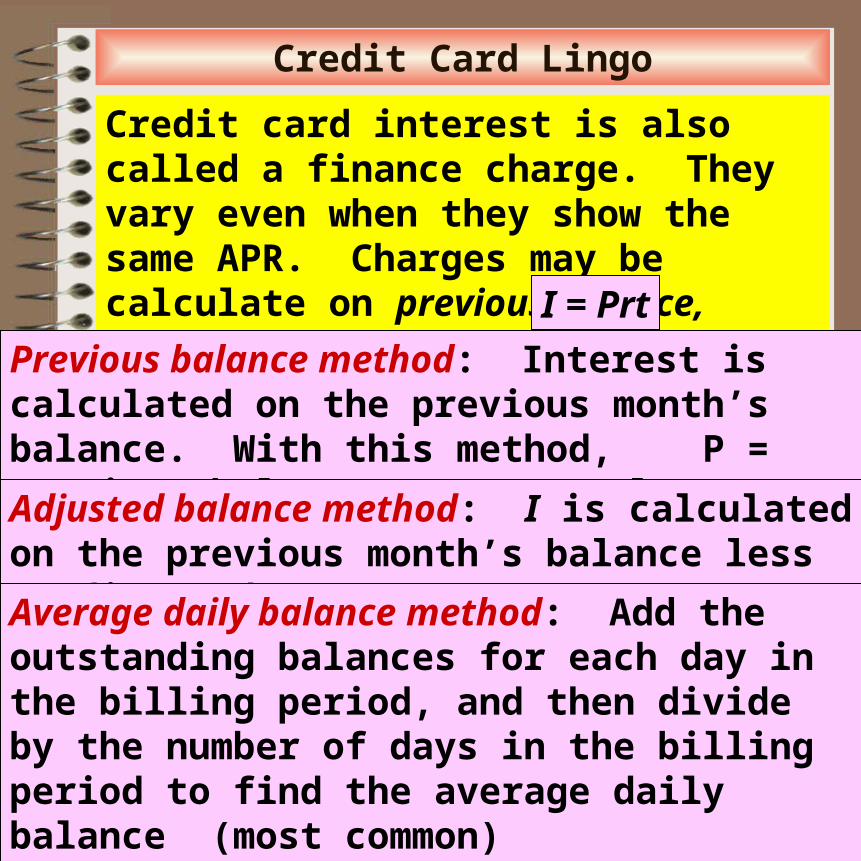

Credit Card Lingo

Credit card interest is also called a finance charge. They vary even when they show the same APR. Charges may be calculate on previous balance, adjusted balance, and/or average daily balance.

Previous balance method: Interest is calculated on the previous month’s balance. With this method, P = previous balance, r = annual rate, and t = 1/12.

I = Prt

Adjusted balance method: I is calculated on the previous month’s balance less credits and payments.

Average daily balance method: Add the outstanding balances for each day in the billing period, and then divide by the number of days in the billing period to find the average daily balance (most common)

Aim: Money Matters – Credit Cards Course: Math Literacy

More Credit Card Lingo

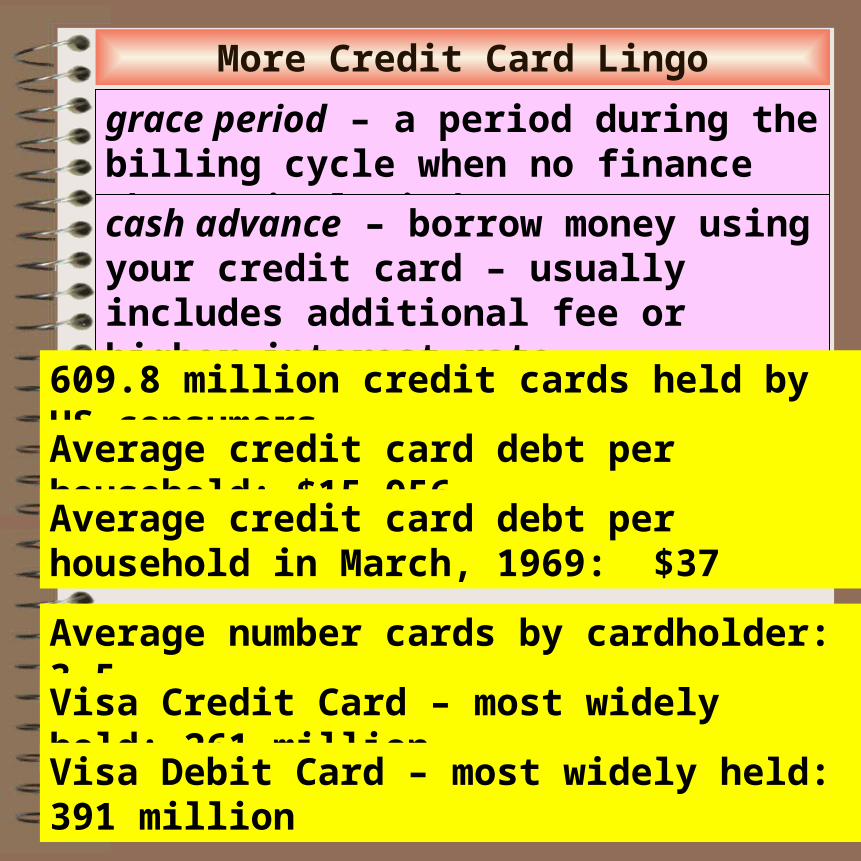

grace period – a period during the billing cycle when no finance charge is levied.

cash advance – borrow money using your credit card – usually includes additional fee or higher interest rate.

609.8 million credit cards held by US consumers

Average credit card debt per household: $15,956

Average number cards by cardholder: 3.5

Visa Credit Card – most widely held: 261 million

Visa Debit Card – most widely held: 391 million

Average credit card debt per household in March, 1969: $37

Aim: Money Matters – Credit Cards Course: Math Literacy

More Credit Card Stuff

How long with it take to pay off a credit card debt of $3000 & interest paying just the minimum 3% of balance each month?

Aim: Money Matters – Credit Cards Course: Math Literacy

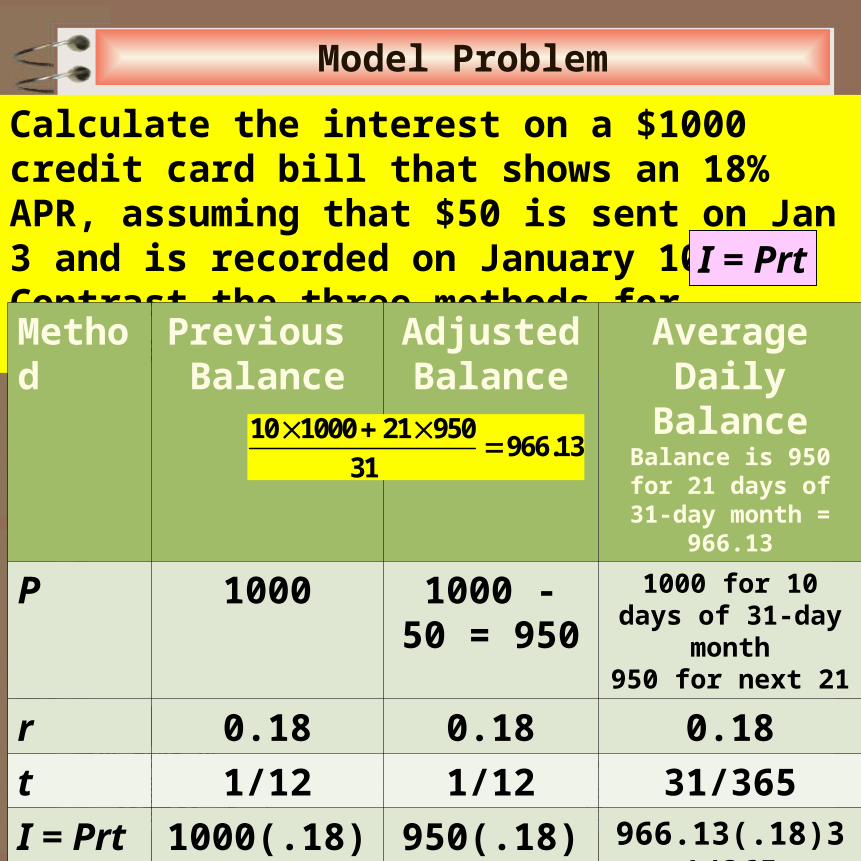

Model Problem

Calculate the interest on a $1000 credit card bill that shows an 18% APR, assuming that $50 is sent on Jan 3 and is recorded on January 10. Contrast the three methods for calculating the interest. I = Prt

Method Previous Balance

Adjusted Balance

Average Daily Balance

Balance is 950 for 21 days of 31-day month =

966.13

P 1000 1000 - 50 = 950

1000 for 10 days of 31-day month950 for next 21

r 0.18 0.18 0.18

t 1/12 1/12 31/365

I = Prt 1000(.18)1/12

950(.18)1/12 966.13(.18)31/365

= $15 = $14.25 = $14.77

10 1000 21 950966.13

31

Aim: Money Matters – Credit Cards Course: Math Literacy

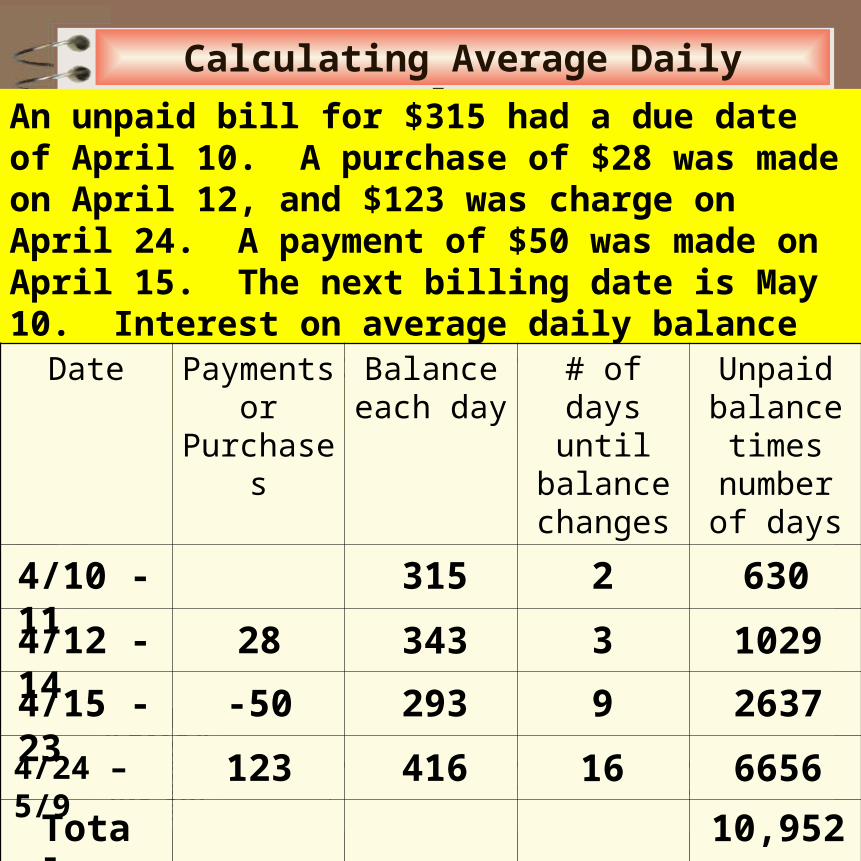

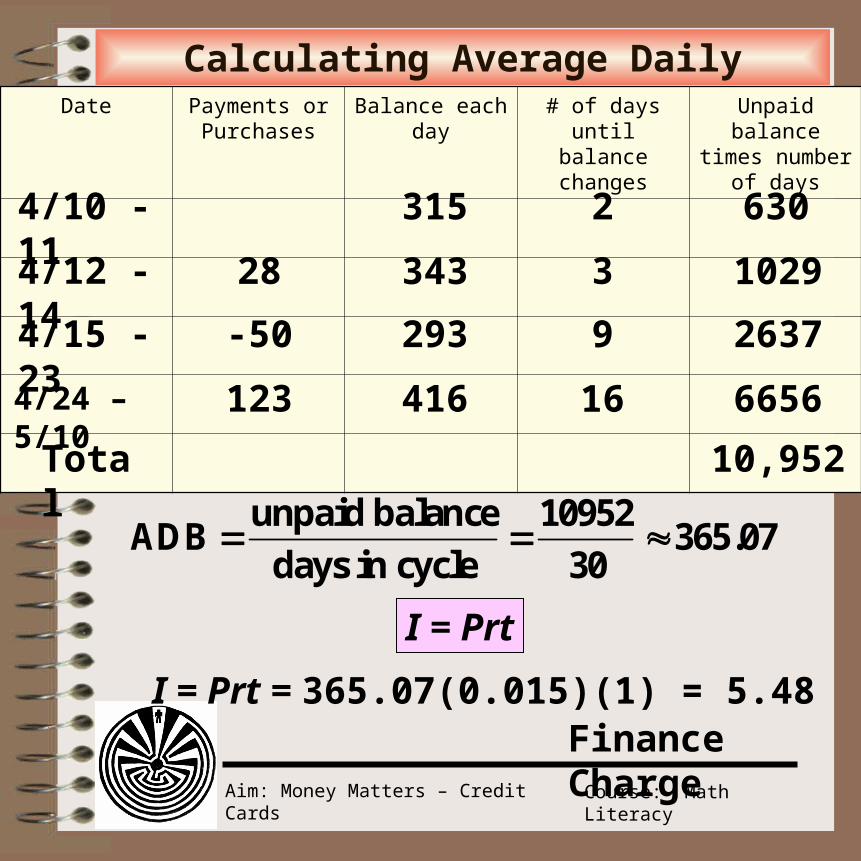

Calculating Average Daily Balance

An unpaid bill for $315 had a due date of April 10. A purchase of $28 was made on April 12, and $123 was charge on April 24. A payment of $50 was made on April 15. The next billing date is May 10. Interest on average daily balance is 1.5%. Find finance charge on May 10 bill.

Date Payments or

Purchases

Balance each day

# of days until

balance changes

Unpaid balance times

number of days

4/10 - 11

4/12 - 14

4/15 - 23

4/24 – 5/9

Total

28

-50

123

315

343

293

416

2

3

9

16

630

1029

2637

6656

10,952

Aim: Money Matters – Credit Cards Course: Math Literacy

Calculating Average Daily BalanceDate Payments or

PurchasesBalance each day # of days until

balance changesUnpaid balance times number of

days

4/10 - 11

4/12 - 14

4/15 - 23

4/24 – 5/10

Total

28

-50

123

315

343

293

416

2

3

9

16

630

1029

2637

6656

10,952

unpaid balance 10952ADB 365.07

days in cycle 30

I = Prt

I = Prt = 365.07(0.015)(1) = 5.48Finance Charge

Aim: Money Matters – Credit Cards Course: Math Literacy

Aim: How does money matter? Installment buying – Credit cards!

Do Now:

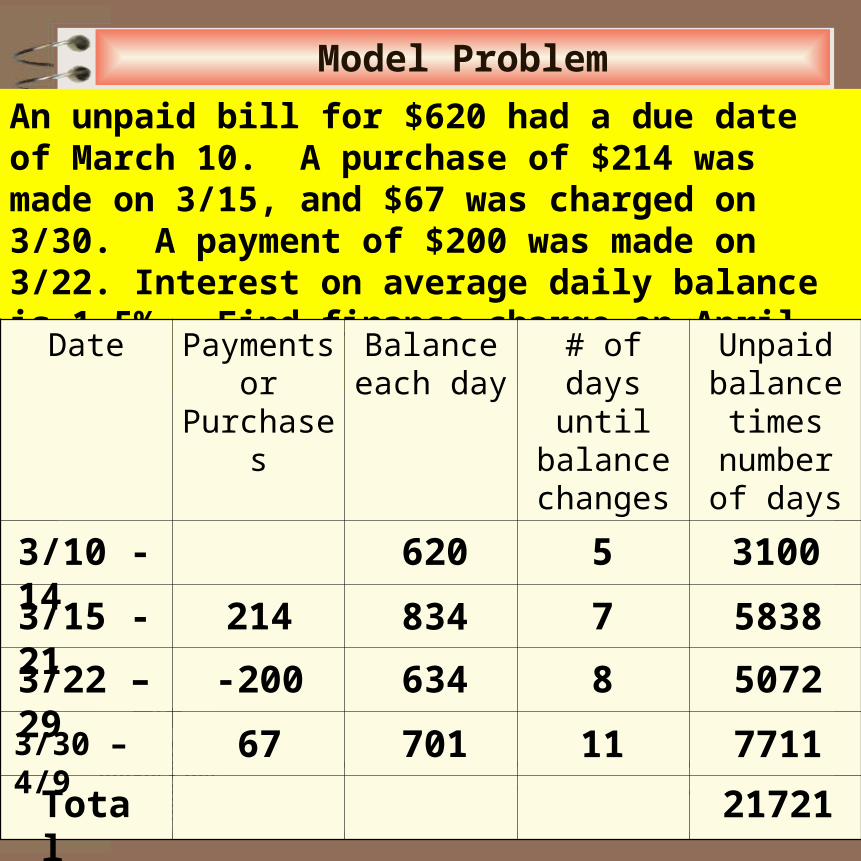

An unpaid bill for $620 had a due date of March 10. A purchase of $214 was made on 3/15, and $67 was charged on 3/30. A payment of $200 was made on 3/22. Interest on average daily balance is 1.5%. Find finance charge on April 10 bill.

Aim: Money Matters – Credit Cards Course: Math Literacy

Model Problem

An unpaid bill for $620 had a due date of March 10. A purchase of $214 was made on 3/15, and $67 was charged on 3/30. A payment of $200 was made on 3/22. Interest on average daily balance is 1.5%. Find finance charge on April 10 bill.

Date Payments or

Purchases

Balance each day

# of days until

balance changes

Unpaid balance times

number of days

3/10 - 14

3/15 - 21

3/22 – 29

3/30 – 4/9

Total

214

-200

67

620

834

634

701

5

7

8

11

3100

5838

5072

7711

21721

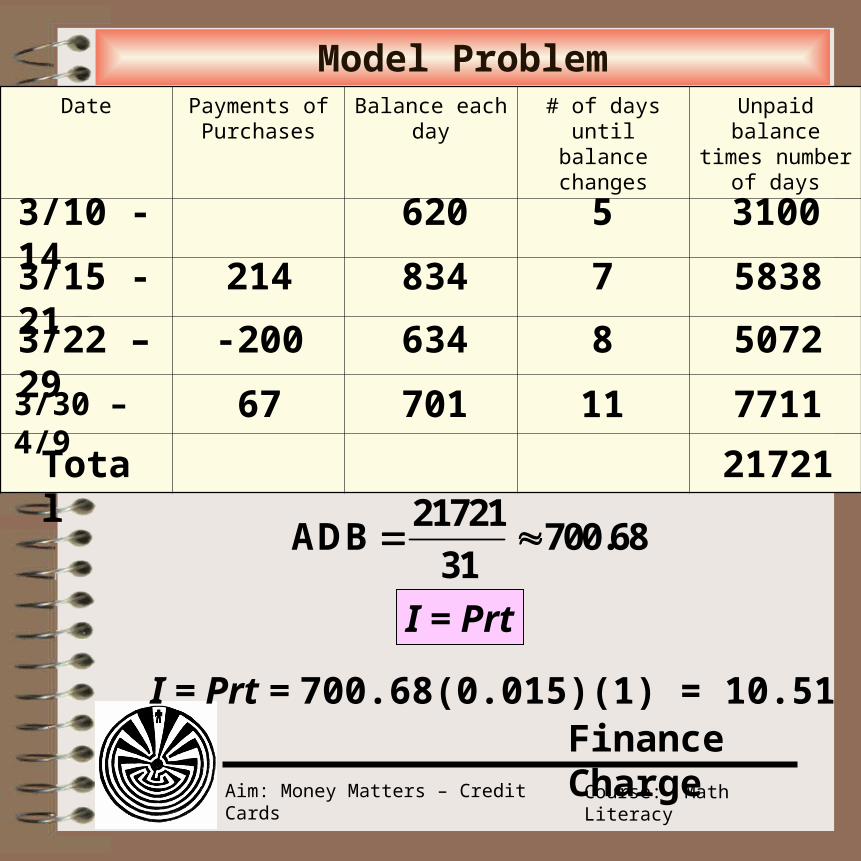

Aim: Money Matters – Credit Cards Course: Math Literacy

Model ProblemDate Payments of

PurchasesBalance each day # of days until

balance changesUnpaid balance times number of

days

21721ADB 700.68

31

I = Prt

I = Prt = 700.68(0.015)(1) = 10.51Finance Charge

3/10 - 14

3/15 - 21

3/22 – 29

3/30 – 4/9

Total

214

-200

67

620

834

634

701

5

7

8

11

3100

5838

5072

7711

21721

Aim: Money Matters – Credit Cards Course: Math Literacy

More Credit Card Stuff

36 percent of respondents said they didn't know the interest rate on the card they use most often.The national average default rate as January 2010 stood at 27.88 percent and the mean default rate is 28.99 percent.Slightly more than half of Americans -- 51 percent -- said that in the past 12 months, they carried over a balance and was charged interest on a credit card.93 percent of cards allowed the issuer to raise any interest rate at any time by changing the account agreement. Only eight percent of cards with penalty rate conditions offered to restore the original rate terms when payments are made on-time, usually after 12 months. 72 percent of cards included offers of low promotional rates which issuers could revoke after a single late payment. Among 39 credit cards Consumer Action looked at from 22 financial institutions, the average interest rate for purchases was 12.83 percent. That's a drop of more half a point from the 2008 survey results. Interest rates on purchases ranged from 4.25 percent to 22.99 percent, with the fixed rate credit cards averaging an interest rate of 10.03 percent and the variable rate credit cards averaging 13.20 percent. Average APR on new credit card offer: 14.10 percent

Aim: Money Matters – Credit Cards Course: Math Literacy

More Credit Card Stuff

Penalty fees from credit cards will add up to about $20.5 billion in 2009, From 1989 to 2004, the percentage of cardholders incurring fees due to late payments of 60 days or more increased from 4.8 percent to 8.0 percent. One-fourth of the students surveyed in US PIRG's 2008 Campus Credit Card Trap report said that they have paid a late fee, and 15 percent have paid an "over the limit" fee. In the first 3 months of 2009, 27 percent of card offers carried an annual fee, up from 18 percent in 2008,The average late fee was found to have risen to $28.19, way up from $25.90 in 2008. Consumer Action reported that late fees reached up to $39 per incident. 92 percent of cards included a fee for exceeding the credit limit, including 100 percent of all student cards. The amount of the overlimit fee is $39 on most accounts. 64 percent of respondents said having "no annual fee" was an important reason why they chose the credit card they did the last time they got a new card.95 percent of surveyed issuers have over-limit fees. The average over-limit fee, among institutions with over-limit fees, is $29.13.

Aim: Money Matters – Credit Cards Course: Math Literacy

More Credit Card Stuff

The average person under the age of 35 got both their first credit card and their first debit card when they were about 21 years old. 41 percent of cardholders from the ages of 18 to 29 made only the minimum required payment on a credit card in some of the past 12 months. Only 2 percent of undergraduates had no credit history. Eighty-four percent of the student population overall have credit cards, an increase of approximately 11 percent since the fall of 2004. Undergraduates are carrying record-high credit card balances. The average (mean) balance grew to $3,173, the highest in the years the study has been conducted. Median debt grew from 2004’s $946 to $1,645. Twenty-one percent of undergraduates had balances of between $3,000 and $7,000, also up from the last study. Half of college undergraduates had four or more credit cards in 2008. That's up from 43 percent in 2004 and just 32 percent in 2000. Since 2004, students who arrived on campus as freshmen with a credit card already in-hand have increased from 23 percent to 39 percent. In spring of 2008, only 15 percent of freshmen had a zero balance, down dramatically from 69 percent in the fall of 2004. The median debt freshmen carried was $939, nearly triple the $373 in 2004. Seniors graduated with an average credit card debt of more than $4,100, up from $2,900 almost four years ago. Close to one-fifth of seniors carried balances greater than $7,000.

Aim: Money Matters – Credit Cards Course: Math Literacy

More Credit Card Stuff

Nine in 10 undergraduates reported paying for direct education expenses with credit cards—and the average amount they charged more than doubled since the last study. Ninety-two percent of undergraduate credit cardholders charged textbooks, school supplies, or other direct education expenses, up from 85 percent when the study was last conducted, in 2004. Nearly one-third (30 percent) put tuition on their credit card, an increase from 24 percent in the previous study. Students who used credit cards to pay for direct education expenses estimated charging $2,200, more than double 2004’s average of $942. Sixty percent of undergrads experienced surprise at how high their balance had reached, and 40 percent said they have charged items knowing they didn’t have the money to pay the bill. Only 17 percent said they regularly paid off all cards each month, and another 1 percent had parents, a spouse, or other family members paying the bill. The remaining 82 percent carried balances and thus incurred finance charges each month. Two-thirds of survey respondents said they had frequently or sometimes discussed credit card use with their parents. The remaining one-third who had never or only rarely discussed credit cards with parents were more likely to pay for tuition with a credit card and were more likely to be surprised at their credit card balance when they received the invoice.

Aim: Money Matters – Credit Cards Course: Math Literacy

More Credit Card Stuff

Eighty-four percent of undergraduates indicated they needed more education on financial management topics. In fact, 64 percent would have liked to receive information in high school and 40 percent as college freshmen. One-fourth of the students surveyed in US PIRG's 2008 Campus Credit Card Trap report said that they have paid a late fee, and 15 percent have paid an "over the limit" fee. 74 percent of monthly college spending is with cash and debit cards. Only 7 percent is with credit cards. The average college graduate has nearly $20,000 in debt; average credit card debt has increased 47 percent between 1989 and 2004 for 25-to 34-year-olds and 11 percent for 18- to 24-year-olds. Nearly one in five 18- to 24-year-olds is in "debt hardship," up from 12 percent in 1989.