Private Equity Practice 2021 North American Private Equity ...

Upload

asiabuyoutsCategory

view

1.056download

1description

AN N UAL R E PORT 2008

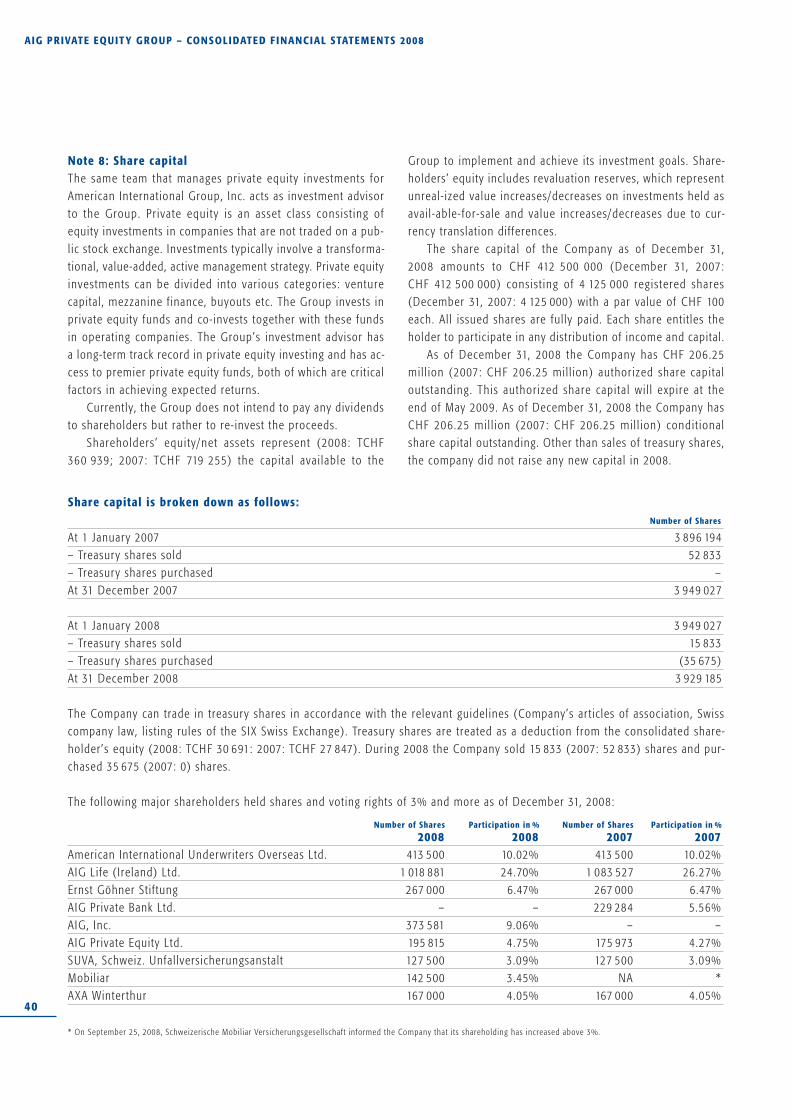

FACTS AND F IGURES

Company profile

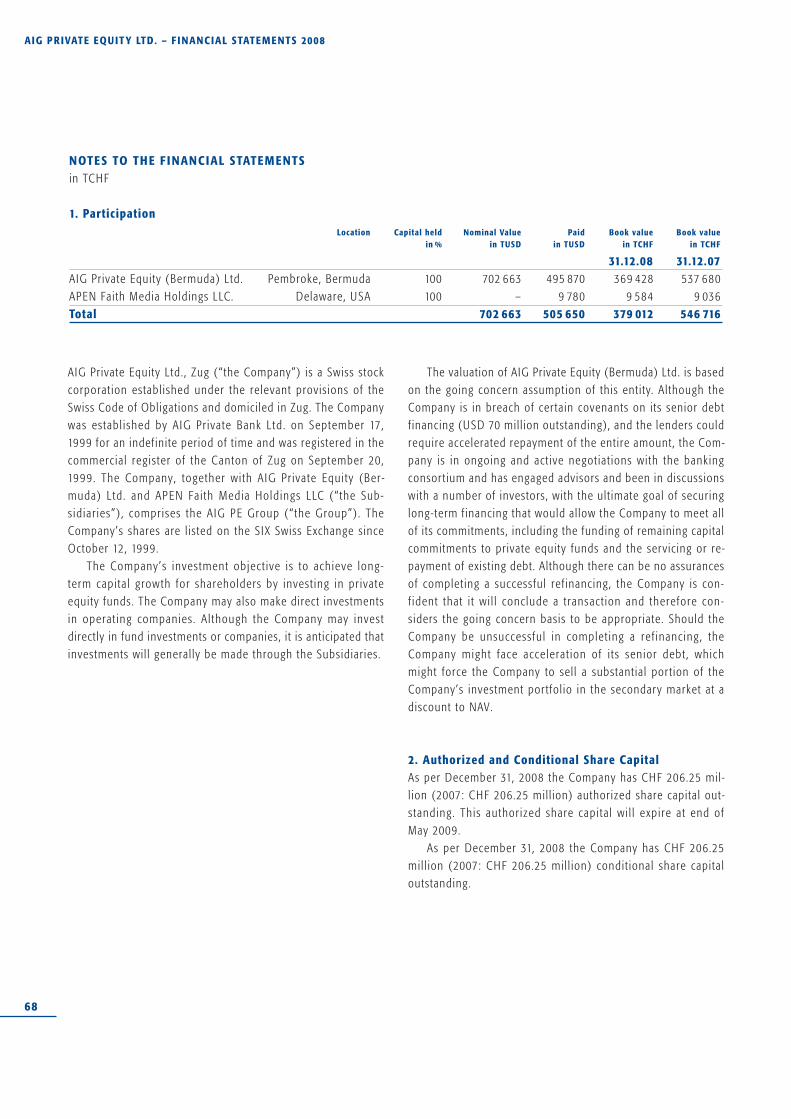

AIG Pr ivate Equity Ltd. is a Swiss investment com-

pany with an object ive to achieve long-term capital

growth for shareholders by investing in a diversif ied

por tfol io of private equity funds and privately held

operat ing companies. The same team that manages

private equity investments for American International

Group, Inc. acts as investment advisor for AIG Private

Equi ty Ltd . With nine years of operat ing his tor y

in a variety of market condit ions, AIG Private Equity

Ltd. has a sol id track record and a mature por tfol io

of funds and direct investments. AIG Private Equity

Ltd. is l is ted on the S IX Swiss E xchange under the

t icker symbol “APEN”.

Valuation as of December 31, 2008

Closing price per share CHF 37.95

Net asset value per share CHF 91.86

(applying fair values)

Exchange rate USD/CHF 1.0673

Exchange rate EUR/CHF 1.4856

Number of shares outstanding 3 929 185

Market capital izat ion CHF 149 112 571

Swiss Security Number

915.331

ISIN: CH0009153310

Ticker: APEN

Trading Information

Reuters: APEZn.S

Bloomberg: APEN

Telekurs: APEN

www.aigprivateequity.com

CONTENTS

Chairman’s Statement 2

Management Report

– Review 2008 and Outlook 4

– Overview of 20 Largest Investments 8

Financial Report

– AIG Private Equity Group 20

Consol idated Financial Statements 2008

– Corporate Governance 57

– AIG Private Equity Ltd. 66

Financial Statements 2008

2

CHAIRMAN’S STATEMENT

valuat ions. The ef fect of th is can be seen in the Company’sNAV, which decl ined substant ia l ly in the four th quar ter. The Company also experienced l iquidity constraints in the four thquar ter as distributions from existing investments dropped dra-mat ica l ly and the Company’s lenders requested ear ly repay-ment of the Company’s USD 100 mi l l ion credi t l ine. F inal ly ,AIG, the Company’s founder, sponsor and investment advisorwas forced to accept a substantial investment by the US fed-eral government and plans to sel l many of i ts operat ing busi-nesses ( inc luding the Company’s investment advisor , AIGInvestments and AIG Private Bank).

Investment income was down sharply as exi ts were scarcewith buyers struggl ing to secure debt f inancing for new deals.At the same t ime the Company recorded substant ia l wr i te-downs from long term assets. The Company is required to per-form an impairment analysis on a quar terly basis . At year-endfund managers marked down the value of por tfol io companiesmainly due to mult iples of public comparables coming down –especial ly in the four th quar ter. This led to signif icantly lowervaluat ions across the por tfol io even for companies that weretracking budget.

With fewer distributions but capital draw downs from fundsremaining at high levels in the f irst three quar ters of 2008, theCompany drew down i ts credi t l ine and issued preference shares from its subsidiary in Bermuda. As per the end of thethird quar ter the Company breached covenants under the cre-dit agreement with the banking consor t ium and a supplemen-tary agreement to the loan agreement was s igned. In returnfor the Company maintaining an early prepayment schedule,the banking syndicate agreed to waive cer ta in f inancia l covenants. In Apri l 2009 the Company proposed to the bank -ing syndicate a s tandst i l l agreement unt i l Ju ly 2009 as i t

Dear Shareholders

2008 was a disappointing year. The global f inancial cr is is thatbegan in 2007 intensif ied sharply fol lowing the bankruptcy ofLehman Brothers in September 2008, and credit markets cameto a near standst i l l , with lenders unwil l ing to assume counter-par ty r isk. Uncer tainty and lack of credit had a signif icant im-pact on an already weak real economy, with most developedeconomies contract ing sharply in the four th quar ter. Publ icequity markets turned in their worst per formance in decades,with many major indices down 30–40% or more for the year.Pr ivate equi ty va luat ions and act iv i ty have been par t icular ly impacted due to the lack of credi t for new transact ions or exi ts and the leveraged nature of buyout investments, whichtends to ampl i fy equi ty losses in per iods of dec l in ing asset

EDUARDO LEEMANN, Chairman of the Board

3

CHAIRMAN’S STATEMENT

Despite the diff iculties faced by the Company, we believe thereare many successful investments in the portfolio that wil l beginto demonstrate their value when markets and the global eco-nomy stabi l ize.

Eduardo LeemannChairman of the Board

became evident that the prepayment schedule could not be maintained. During that period the Company is exploring var ious ref inancing opt ions . The abi l i ty of the Company to secure s table f inancing to fund ex is t ing investment commit-ments wi l l c lear ly have a mater ia l impact on the out look forreturns to our equity holders.

The global economy has continued to deteriorate in 2009,with large contract ions expected for major economies in thef i rs t quar ter and a substant ia l s lowing of growth in largeremerging economies such as China and India. While there aresome s igns of s tabi l izat ion in credi t and equi ty markets , i tseems l ike ly that any recovery wi l l be a long, s low process . Valuat ions wil l stay under pressure unti l economic confidenceis restored and credit markets begin to function more normally.

DR. CHR ISTIAN WENGER, Vice Chairman

ROBERT THOMPSON, MemberDR. ROGER SCHMID, Member

DR. ERNST MÄDER, Member

4

MANAGEMENT REPORT

The f irst three quar ters ref lected results from a normal weakperiod with NAV decreasing 9.7% and the share price 40.3%.The four th quar ter was characterized by the signif icant turmoilon the f inancial markets. Financial inst i tut ions came under si-gnif icant stress and in some cases were in need of governmentsuppor t . Credit markets froze and the interbank market cameto a standst i l l . Equity markets lost fur ther terrain in the f i rstpar t of the four th quar ter, recovering somewhat towards theyear-end. Al l of the above impacted private equity investmentsand led to a severe contract ion in transact ion volume in thefour th quar ter.

Aside from the signif icant valuation changes,the weakening of the USD (Q4: –4.6%; 2008: –5.8%) and the Euro (Q4: –5.8%; 2008: –10.2%)had a negative impact on NAV as had the l istedpor tfol io investments.

E xi ts were dif f icult to achieve as equity mar-kets were volat i le and weak in 2008 result ing inone of the worst I PO environments in manyyears. Addit ional ly , secondary transact ions, thesale of a por t fol io company to another pr ivateequi ty sponsor , dec l ined s igni f icant ly as debt f inancing was diff icult to secure in the first threequar ters and v i r tual ly imposs ib le to f ind in the four th quar ter. As a result of the restr ictedtransact ion volume, the Company’s investmentincome was substantial ly lower than in the pre-

vious year. The sale of three of the top 20 investments at thebeginning of 2008 at good mult iples contr ibuted strongly toinvestment income. Addit ional ly , the Company unwound thecontractual agreements in the second quar ter. The contractualagreements were entered into in 1999 shor t ly after inceptionof the Company. The agreements provided the Company withinstant e xposure to a mature pr ivate equi ty por t fo l io of 65 private equity funds with vintages ranging from 1986 to 1999.As that por tfol io continued to exi t underly ing por tfol io com-panies, the remaining fair value of the contractual agreementsdecreased continuously to CHF 38.8 mil l ion at the end of thef i rs t quar ter 2008. Near ly hal f of the fa i r va lue was concen-trated in four funds: Doughty Hanson I I I , Palamon EuropeanEquity, Apollo IV and Blackstone I I I . As a result of the unwind-ing of the contractual agreements , the Company received

Rev iew 2008 and Out look

Quarterly Investment Income from 2004 to 2008

Investment Income in TCHF

AIG Private Equity Ltd. (the “Company”) recorded a disappointing result in

a very challenging market environment in 2008. The turmoil in the financial

markets has had a material negative impact on the Company. The frozen

debt markets, weak equity markets and weak global economy impacted

valuations and led to a substantial decrease in distributions from existing

investments. The Company’s net asset value (“NAV”) per share decreased

49.6% from CHF 182.13 to CHF 91.86. The Company’s share price decreased

77.7% and ended the year at CHF 37.95.

Q1

2004

Q2

2004

Q3

2004

Q4

2004

Q1

2005

Q2

2005

Q3

2005

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

5

MANAGEMENT REPORT

direct l imited par tnership interests in these four funds equi-valent to i ts exist ing indirect interests and received cash pro-ceeds equal to NAV for the remaining funds covered by theagreements . Tota l cash proceeds f rom the unwinding of thecontractual agreements were USD20.3 mi l l ion and the fa i rva lue of the four funds t ransferred to the Company’s d i rectownership totaled USD 15.4 mil l ion.

The wr i te-down on non-current assets amounted to CHF 223.0 mil l ion (2007 CHF 10.1 mil l ion). In accordance withI FRS requirements , the Company considers any investment(whether fund or direct investment) wi th a fa i r va lue belowcost for more than twelve months as impaired. In addition, anyinvestment with a fair value more than 30% below cost wil l beconsidered impaired regardless of the leng th the investmentwas held below cost . In contrast to other tests , the majori ty ofthe wr i te-downs were caused by the la t ter category. Lower valuat ion mult iples and the weak economic environment ledto this s i tuat ion. Addi t ional ly , wi th fewer e x i ts , we recordedmore funds that remained below cost for more than twelvemonths. Since impairments are taken automatical ly under thepol ic y , an impairment does not necessar i ly ref lect manage-ment’s opinion that the affected fund or direct investment wil lul t imately return a loss.

Top 20 investments

The Company’s top 20 investments por tfol io recorded anotheryear of h igh turnover , wi th a tota l of ten new investments joining the top 20 in the course of the year. Three ful l saleswere achieved at at t ract ive mult iples in spi te of a very chal-lenging market environment. Overal l we are pleased with the

per formance of the top 20 investments and are aware that atleast one is looking to generate l iquidity for investors in 2009.See page 8 for detai led information on the por tfol io of top 20investments.

Investment Program

The Company added s ix funds and no direct investments to i ts por t fo l io in 2008. The commitments to the s ix funds are divided up into f ive fol low-on funds and one new fund.

The Company made commitments to two new funds in2008 with an investment focus on Nor th America: BlackstoneCapital Par tners VI (USD 25 mil l ion) and Ares Corporate FundI I I (USD 20 mil l ion). Blackstone Capital Par tners V I wi l l pur-sue large-scale private equity focusing on investments in largecap businesses, both in the U.S. and international ly. Targetedsectors include large industr ials , communicat ions and media,and energy among others; with par ticular focus on out-of-favorsectors and under-appreciated industr ies . The Company has invested in numerous prior Blackstone funds. Ares I I I makesmajor i ty and shared-control investments in d is t ressed andunder-capital ized middle market companies. Ares I I I continuesto pursue a wide variety of transact ions including buyouts, re-capi ta l izat ions , growth equi ty , d is t ressed for control invest -ments and investments in debt secur i t ies wi th equi ty- l ikereturns. The Company is already a l imited par tner in Ares I I .

Two European funds were added to the por t fo l io wi th commitments total ing EUR 40 mil l ion: Advent International VI(EUR 20 mil l ion) and CVC European Equity Par tners V (EUR 20mi l l ion) . Advent V I wi l l cont inue to pursue the s t rategy Advent has fol lowed in prior funds, focusing on the fol lowing

ANDREW FLETCHERCONRADIN SCHNE IDER

6

MANAGEMENT REPORT

sectors: Business/Financial Services, Retai l/Consumer, Health-care, Technology/Media/Telecom and Industr ials. Advent’s aimwith fund VI is to invest in control buyout transactions of com-panies in Western Europe (majori ty) and Nor th America. TheCompany has invested in Advent V in 2005 (and sold the stakein the four th quar ter) . CVC V wi l l cont inue the investment s t rategy that CVC has adopted for many years for i ts pr iorfunds; invest ing pr imar i ly in lead, control buyouts on a pan European bas is in deals wi th enterpr ise va lues typica l ly in excess of EUR 1bi l l ion. The Company has invested in a widevariety of funds managed by CVC.

One new fund, TowerBrook Capi ta l Par tners I I I (USD 20mill ion), has its investment focus on both Europe and the USA.TowerBrook I I I pursues control-oriented private equity invest-ments in large and middle market companies, par tnering withhighly capable management teams and seeking s i tuat ions characterized by complexity.

One fund was added to the Rest-of-the-World/Asia por t ionof the por t fo l io : Founta inVest China Growth Capi ta l Fund (USD 7.5 mil l ion). FountainVest wi l l target equity investmentsthat have a strong nexus with China. In par t icular , the Fundwil l target oppor tunit ies to invest in sizable, privately-ownedenterprises in China that are entering high growth stages ledby local entrepreneurs. The Fund wil l target equity investmentsof USD 50 mil l ion to USD 200 mil l ion in 10-15 companies pri-mari ly in the i) consumers & l i festyles, i i) bui lders/developersand i i i) resources & alternat ive energy sectors.

Unfunded commitments as of year end amounted to approximately CHF 744 mil l ion or 117% of total assets. Gen-era l ly , we e xpect funds to invest over a per iod of approx i -mately f ive years.

Direct Investments

In 2008 the Company made no new direct investments butmade three fo l low-on investments in Advanstar Communi-cations, Thomas Nelson Publishing and Falcon Farms for a totalof CHF 1.35 mil l ion. The Company’s por tfol io of direct invest-ments has decl ined fur ther in 2008. The main reason werelower valuat ions recorded for a number of direct investments.Especial ly impacted were CapMark and MVLF. CapMark, act ivein the commerc ia l rea l estate sector , and MVLF, a leverage f inance fund holding a por tfol io of mezzanine and second l ienloans, were par t icular ly hit .

At year end, d i rect investments accounted for 7.1% of invested assets ( including the investments in loans). This re-presents a decrease of nearly f ive percentage points over theprior year.

Liquidity

Capital cal ls remained at high levels in the f irst three quar ters.The st i l l fa i r ly high volume of cal ls goes back to specia l izedfund managers investing in debt securit ies at discounts or fundmanagers buying debt of por t fol io companies at a discount ,and a lso ref lects a large number of t ransact ions that wereagreed in the second half of 2007 and the f irst half of 2008,but that eventual ly closed in 2008.

In order to fund capi ta l ca l l s the Company increased in January 2008 the credit l ine with the banking consor t ium toUSD 100 mil l ion. Due to distr ibutions slowing down and capi-ta l cal ls remaining at high levels for the f i rst three quar ters ,the bank faci l i ty was ful ly ut i l ized and the Company’s subsi-diary in Bermuda issued USD 150 mil l ion in preferred sharesto an AIG group company.

1. Diversification by Investment Focus as of December 31, 2008Expressed as % of invested assets applying fair values

2. Investment Framework as of December 31, 2008Expressed as % of total assets applying fair values

Venture 5.1%

Mezzanine 2.8%

Development Capital 4.7%

Buyout 87.4%

AIG 3rd-Party Direct TotalFunds Funds InvestmentsPortfolio Portfolio Portfolio

Developed MarketsEurope 2.1% 38.0% 2.6% 42.7%Nor th America 5.8% 35.2% 6.4% 47.4%

Other Markets 3.3% 4.1% 0.1% 7.5%Total 11.2% 77.3% 9.1% 97.6%

7

MANAGEMENT REPORT

At the end of th i rd quar ter the Company breached covenants on i ts USD 100 mil l ion credit faci l i ty. Towards year-end the Company and the lenders s igned a supplementar yagreement to the loan agreement. In return for the Companymaintaining an early prepayment schedule, the banking syn -dicate agreed to waive two f inancia l covenants . The prepay-ment schedule provides for var ious payments wi th the f ina lpayment due June 30, 2009.

In order to repay debt and increase l iquidity the Companysold 7 por tfol io funds (CVC I I I , CVC IV, CVC Tandem, Advent V,Sun Capital V, KRG I I I and Avista) in the secondary market. Inreturn for the sale of these funds the Company received pro-ceeds of CHF 76.8 mil l ion. Unfunded commitments that werereleased with the sale of the funds amounted to CHF 39 mil-l ion. The impact on the NAV for the por t fo l io funds was CHF –6.75 per share.

In the four th quar ter debt was reduced by CHF 37.2 mil -l ion, ref lect ing a f i rst repayment under the loan with the ban-k ing syndicate and repaying loan balances wi th AIG Pr ivateBank and HSBC Bank of Bermuda which provided shor t termfaci l i t ies to fund capital cal ls .

Outlook

The f i rs t quar ter 2009 led to a worsening of the overa l l picture. Equity markets per formed poorly before recovering inMarch. While there have been signs of stabi l izat ion in creditmarkets , they are s t i l l not funct ioning at anywhere near the levels of recent years and cer tain lenders (such as CDOs) havedisappeared f rom the scene – perhaps permanent ly. In l inewith i ts impairment pol icy the Company recorded substantialwri te downs on i ts investments. I t is l ikely that there wi l l befur ther pressure on valuat ions as economic weakness affects

operat ing resul ts and publ ic equi ty markets ref lect reduced valuat ion mult iples. There are, however, many profi table com-panies in the por t fol io . Mult ip le expansion from the currentdepressed levels wi l l have a material posit ive impact on valu -at ions as f inancial markets and the global economy stabi l ize.

L iquidi ty remains the key issue for the board and the management, and we are working to streng then and sol idi fythe Company’s balance sheet and f inancial s i tuat ion. Discus -s ions with the banking syndicate are ongoing and a stand st i l lunti l July 15 was proposed. This t ime period al lows the Com-pany to pursue various options to resolve the l iquidity issues.

In 2009 the Company sold fur ther funds (EMP I I , CognetasI I , Berkshire VI I , Doughty Hanson I I I , EQT I I I , EQT IV, EQT V(50%), Lion Capital I I (50%), Calyle IV, Diamond Castle (40%),KRG IV (20%), P lat inum I I (50%)). In return for the sa le ofthese funds the Company received proceeds of CHF 37.9 mil-l ion. Unfunded commitments that were released with the saleof the funds amounted to CHF 78.9 mil l ion. The impact on theNAV for the por tfol io funds was CHF –11.23 per share.

The Company got of f to a chal lenging s tar t in 2009. Management and the board of d i rectors are under tak ing a l lsteps to refinance the Company in a way that provides the bestreturns for shareholders.

3. Diversification by Vintage Year as of December 31, 2008Expressed as % of invested assets applying fair values

4. Diversification by Region as of December 31, 2008Expressed as % of invested assets applying fair values

Nor th America 48.6%

Other regions 7.7%

Europe 43.7%

8

MANAGEMENT REPORT

Por t fo l io turnover was high, wi th a tota l of ten new invest -ments jo ining the top 20. This was due to a mix ture of new investments, secondary sales, and valuat ion changes. Ref lect-ing the por tfol io as a whole, the top 20 investments por tfol iocont inues to be wel l -d ivers i f ied, wi th the fol lowing industr yweightings: 34.1% services, 21.5% energy, 19.2% communica-t ions, 9.3% medical & health, 8.5% industr ial , and 7.4% con-sumer. The F inancia l Ser v ices sector (8 .4% in 2007) is notrepresented in the top 20 investments por tfol io anymore, dueto pressure on valuat ions of por tfol io companies act ive in thefinancial industry. The Semiconductor sector (4.4% in 2007) isalso not represented due to the valuat ion adjustment of Free-scale at year end. The matur i ty of the top 20 investments isgett ing a l i t t le older with the average holding period increas -ing to 22.2 months (30.12.2007: 19.2 months). The minimum

fair value for inclusion in the top 20 investment por tfol io wasaround CHF 3.8 mil l ion (2007: 5.1 mil l ion) with the averageamounting to about CHF 6.6 mil l ion (2007: CHF 8.6 mil l ion).

Top 20 Portfolio Performance

At year end Geoservices , an upstream oi l f ie ld services com-pany with headquar ters located in the Paris suburbs, was thelargest investment for the Group. Nearly 100% of i ts businessact iv i ty takes place outside France on a worldwide basis in atleast 50 different locations spread over al l continents. I ts mainbusiness l ines are Mud Logging, Wel l Intervent ion and FieldSurvei l lance. I t took the top spot from Capmark, which drop-ped f rom the Top 20 a l together. In the second posi t ion is Kinder Morgan , which is up f rom the seventh spot in 2007after sol id per formance and a substant ial add-on investmentin Q3 2008. Kinder Morgan is one of the largest pipeline trans-por ters and terminal operators in Nor th America . Third is Thomas Nelson Publishing , which mainta ins i ts hold on thenumber three spot. Thomas Nelson/Faith Media, is the leadingpublisher of Christ ian-oriented books, Bible reference books,and translat ions of the Christ ian Bible, and also sel ls seculart i t les to mainstream commercial markets. The fastest-growingsegment of the business is the Gospel Music Channel, with agood subscript ion base. Thomas Nelson Publ ishing is one ofthree direct investments the Group has in the Top 20, with theother two being Knowledge Universe Education at number fourand Acosta at number seventeen. Knowledge Universe Edu-cat ion is a leading global education company serving a widerange of s tudents , f rom infants and toddlers to pr imary andsecondary students. At number f ive, up from posit ion seven-

Top 20 Inves tments

As of December 31, 2008, the total fair market value of the Group’s twenty

largest holdings was CHF 131.6 million. While this represents a 23.6%

decrease from the value of the top 20 investments portfolio at the end of

2007, it also represents a larger share (36.5%) of the Group’s NAV due

to the decrease in the overall value of the Group’s assets by 25.3% over

the course of the year.

9

MANAGEMENT REPORT

teen in 2007, rounding out the top f ive is Numéricâble , thenumber one cable operator in France, serving more than 99%of French cable subscribers.

There are ten new entrants into the Top 20 this year withtwo being new investments for the Group. The new invest -ments in 2008 were Ersol Thin Film (Ventizz IV) and Rhythm(Ares I I ) . Ersol Thin F i lm GmbH is par t ia l ly owned by ErsolSolar Energy AG, a German l isted company that produces andmarkets high-qual i ty s i l icon-based photovol ta ic products . InJune 2008, i t was announced that Ersol Energy AG wil l be soldto Rober t Bosch AG. In connection with this transact ion, Ven-t izz’s posit ion in Ersol Thin Fi lm wil l be purchased in 2011 ata f ixed price. (The Company wil l value i ts posit ion in Ersol atthe discounted present value of the expected proceeds fromthe forward sale) . Rhy thm, aka Guitar Center , is the leadingmusical instrument retai ler that is approximately 4 t imes thesize of i ts largest competi tor. The Company operates throughthree business uni ts : Gui tar Center Reta i l S tores (214 reta i l stores), Direct Response (onl ine and catalog businesses), andMusic & Ar ts (97 stores providing rental band and orchestraequipment) . The other new entrants into the Top 20 are HDSupply, Ports America, Ziggo (Dutch Cable Conglomerate),OGF, Spie, Mater Private Care, Applus, and Hygenic . HD Sup-ply is one of the largest and most diversi f ied wholesale distr i -butors in the U.S. and Canada, providing top qual i ty productsand value-added services to professional customers in the In-f ras t ructure and Energy , Maintenance, Repair and Improve-ment and Special ty Construct ion markets. Por ts America pro-v ides independent mar ine terminal operat ions to conta inershipping companies, rol l -on/rol l -off shippers, cruise l ines andgeneral cargo and stevedoring services at 24 locat ions alongthe Atlantic as well as the Gulf and West Coasts including NewYork, New Jersey, Philadelphia, Baltimore, Miami, New Orleans,Tampa and Houston. Ziggo (Dutch Cable) was formed by thecombination of three of the four largest cable operators in theNetherlands. The group is the incumbent analogue televis ionprovider to some 3.3 mil l ion homes, approximately 55% of al lDutch households , and a lso provides broadband, te lephonyand digital TV services. OGF is the leader in the French funeralservices market. I ts posit ion is par t icular ly strong in the high-end segment of the market. The company provides a full scopeof services, from organization of burials and cremations, to themanufactur ing of coff ins (French leadership) and the sel l ingof pre-need funera l contracts through i ts large network , orpar tnerships with banks or insurance companies. Spie is thesecond largest provider of mult i - technical contract ing servicesin France (12% market share behind Vinci) . I ts main act iv i ty

Distribution of value in Top 20 2008 vs. 2007

Comparison Top 20 by Maturity 2008 vs. 2007

Comparison Top 20 2008 vs. 2007 by Industry

2008 2007 adjusted for currency dif ferences

10

MANAGEMENT REPORT

i s the provis ion of e lect r ica l , heat ing vent i la t ion and a i r condit ioning (“HVAC”) and mechanical engineering to a widerange of industr ial , commercial and public sector customers.Mater Private Healthcare is Ireland’s leading special ist privatehospital , located in Dublin. I t was establ ished by the Sisters ofMercy in 1986 on a s i te adjacent to the Mater Miser icordiaeUniversity Hospital , one of Ireland’s leading academic teachinghospi ta ls , provid ing Mater wi th access to high-qual i ty con-sultants and medical staff . Mater provides a range of medicalspecial ty services and is considered a centre of excel lence forcardiac and cancer re la ted procedures . Applus is Spain’s leading inspect ion, cer t i f i cat ion, and technologica l ser v icescompany, operat ing g lobal ly through four d iv is ions; Auto Vehicle Inspect ion, Inspect ion and Technical Assistance, Engi-neering, Test ing and Cer t i f icat ion, and Non-Destruct ive Testsand Inspect ions . Last ly , Hygenic , based in Akron, Ohio, i s a leading des igner , manufacturer , and marketer of wel l knowbranded, consumable products to therapy, rehabi l i tat ion, andwellness markets.

There are ten companies dropping out of the Top 20 thisyear with two due to ful l e xi ts , one from a return of capital ,and the rest related to per formance and the overal l weak eco-nomic environment. The two exits were Suomen Asiakastietoand Universal Studios Escape . Suomen As iakast ie to is the leading business and credit information company in Finland.GMT Communicat ions Par tners I I I announced the sale of Suo-men Asiakast ieto in Apri l 2008 and returned more than EUR 6mil l ion to the Group in May. Universal Studio Escape, consists of the two theme parks, Universal Studios Florida and Is landsof Adventure , Ci tyWalk , a d in ing, reta i l and enter ta inment complex, and Universal Studios Florida, a movie- based themepark. In February 2008, the Group sold i ts holding – a longstanding top 20 company with initial investment taking place in2000. I-Med Holdings ( formal ly known as DC A Group) hasdropped out of the Group’s top 20 as a result of the sale of

their “Aged Care” business and thus a return of capital . I -MedHoldings is Austral ia’s largest private diagnost ic imaging net-work and was held trough CVC European Equity Par tners IV,CVC European Equity Par tners Tandem Fund and CVC CapitalPar tners Asia Paci f ic I I . Capmark , a global ly divers i f ied com-pany that provides a broad range of f inancia l ser v ices to investors in commercia l rea l estate-re la ted assets , was theGroup’s largest s ingle investment at the end of 2007. Due tothe decline in the financial markets it had a challenging year in2008 and dropped f rom the Top 20 a l together. EMI , a por t -fo l io company of Terra F i rma Investments I I I , i s one of theworld’s largest music companies. 2008 was a tough market thatwas not favorable to the recorded music industry and after avaluat ion adjustment, in spite of sat isfactory operat ional per-formance, EMI dropped out of the Top 20. Hertz , the world’slargest genera l use car renta l company, which is publ ica l ly l i s ted, e xper ienced a s igni f icant drop in share pr ice (–68%)due to weak g lobal equi ty markets in the four th quar ter. Primesight i s a leading outdoor media owner of var ious sheets, backlight bil lboards and exclusive adver tising contracts.In October there was a return of capi ta l f rom br idge f inan-cing. This, coupled with the valuat ion adjustment resulted in Primesight fal l ing out of the Top 20. Freescale Semiconductor ,a global designer, manufacturer , and marketer of broad l inesemiconductors, was reduced in value due to general weaknessin the semiconductor business dur ing 2007 and a reduct ion in orders f rom i ts pr imary customer, Motorola . PBL Media , Austra l ia ’s largest d ivers i f ied media company, a lso droppedfrom the Top 20 due to valuat ion adjustments fol lowing weakoperat ing per formance. Hema dropped of f the l i s t a f ter a secondary sale of 50% of the Group’s holding in Lion CapitalI I brought the value of the investment down.

Outlook

The majori ty of the company’s top 20 investments per formedaccording to their business plan, while some suffered set-backsas they are act ive in industr ies that feel the impact of a re-cession early in the cycle. Three of the top twenty investmentsat the end of 2007 were e x i ted dur ing 2008, provid ing theCompany with substantial distributions and capital gains. Whilewe do not ant ic ipate s igni f icant exi t act iv i ty through at leastthe f irst half of 2009 (i f not considerably longer), a number oftop 20 investments are wel l posit ioned for exi ts when marketsstabi l ize.

11

MANAGEMENT REPORT

TOP 20 INVESTMENTS *Fair Value Percentage

Investment Date Portfolio Company (CHF million) of NAV Type Sector 1 Geography

1 July 2005 Geoservices 14.1 3.9% Buyout Energy Global

2 May 2007 Kinder Morgan 14.1 3.9% Buyout Energy North America

3 June 2006 Thomas Nelson Publishing 13.2 3.6% Buyout Communications North America

4 Jan. 2007 Knowledge Universe Education 10.3 2.9% Buyout Services Global

5 May 2005 Numéricâble 7.0 2.0% Buyout Communications Europe

6 Sept. 2007 HD Supply 6.5 1.8% Buyout Services North America

7 Jan. 2007 Maxam 6.2 1.7% Buyout Industrial Products Europe

8 June 2006 The Nielsen Company (VNU) 6.0 1.7% Buyout Services Global

9 March 2007 Foodvest 5.1 1.4% Buyout Consumer Europe

10 Feb. 2008 Ersol Thin Film 5.1 1.4% Buyout Industrial Europe

11 Nov. 2007 Ports America 5.0 1.4% Buyout Services North America

12 April 2007 Ziggo (f.k.a. Dutch Cable Conglomerate) 5.0 1.4% Buyout Communications Europe

13 July 2008 Rhythm 4.7 1.3% Buyout Consumer North America

14 Oct. 2007 OGF 4.6 1.3% Buyout Services Europe

15 July 2006 Spie 4.5 1.2% Buyout Services Europe

16 Dec. 2007 Mater Private Healthcare 4.5 1.2% Buyout Medical/Health Europe

17 July 2006 Acosta 4.1 1.1% Buyout Services North America

18 Oct. 2007 Ethypharm 4.0 1.1% Buyout Medical/Health Global

19 Nov. 2007 Applus 3.8 1.1% Buyout Services Europe

20 April 2007 Hygenic 3.8 1.1% Buyout Medical/Health North America

Total Fair Value Top 20 Holdings 131.6 36.5%

1 EVCA Definition

* Taking secondary transactions into account that were concluded in 2009

12

MANAGEMENT REPORT

www.geoservices .com

Geoservices is an upstream oi l f ield services company, worldleader on the Mud Logging market with a clear focus on com-plex and offshore projects and the second largest player onthe Wel l Inter vent ion (S l ick l ine) market . Geoserv ices a lso operates on the F ie ld survei l lance market . Company head-quar ters are located near Par is , France. A lmost 100% of i tsbusiness act iv i ty takes place outs ide France on a wor ldwidebas is in at least 50 di f ferent locat ions spread over a l l con-t inents . Geoservices employs over 4 000 people of some 60different nat ional i t ies.

www.kne.com

Kinder Morgan is a leading pipel ine transpor tat ion and energystorage company in Nor th America. Kinder Morgan owns an interest in or operates more than 26 000 miles of pipelines and170 terminals . I t s p ipel ines t ranspor t natura l gas , gasol ine,crude oi l , CO2 and other products , and i ts terminals s tore petroleum products and chemicals and handle bulk materialsl ike coal and petroleum coke.

www.knowledgeu.com

Knowledge Universe Educat ion (KUE) is a leading g lobal educat ion company ser v ing a wide range of s tudents , f rom infants and toddlers to primary and secondary students. TheCompany operates approx imately 1 900 centers in the U.S . ,roughly double the nearest competitor. KUE also offers beforeand after-school tutoring services at approximately 700 schoolsites and an on-l ine education business through its KnowledgeLearning Corporat ion subsid iar y. KUE a lso owns a minor i tystake in k12, a leading operator of web-del ivered curr iculumfor “vir tual char ter schools.”

www.thomasnelson.com

Fai th Media Holdings , LLC, i s a company formed by Inter-Media Advisors to acquire the control l ing interests in ThomasNelson Media , Inc . (“TNM”) and The Gospel Music Channel(“GMC”). TNM is the leading publ isher of Christ ian-or ientedfict ion and non-fict ion books, Bible reference books, and trans-lat ions of the Christ ian Bible. TNM also sel ls secular t i t les tomainstream commercia l markets . GMC is the f i rs t adver t isersuppor ted cable network dedicated to gospel music.

1

2

3 4

13

www.numericable . f r

Numéricâble is the result of a consol idat ion of several cableoperators . The new ent i ty covers 9 mi l l ion households and al l of the largest French urban areas. I t offers a ful l range ofanalogue and dig i ta l pay T V, internet broadband (up to 100Mega) and telephony services. Completel which was acquiredin September 2007, is the third largest business to businessinfrastructure-based telecommunications operator in France. I thas both a nat ional backbone and a DSL network wi th 600 exchanges covering 110 ci t ies in France.

MANAGEMENT REPORT

www.maxam-corp.com

Founded in 1872 by Al f red Nobel , Maxam is a Spanish indu-str ial group with production centers in over 20 countr ies andcommercia l presence in more than 90 countr ies . Maxam is the leader in the development, manufacture and sale of civi le xplosives and ini t iat ion systems for the mining, quarry and infrastructure industr ies in addit ion to a leading producer ofhunting car tr idges and powders for spor t ing use, and demil i -tar izat ion serv ices . Fur thermore, Maxam is a key suppl ier ofraw mater ia ls to the Nitrochemical sector , both for Maxam’s internal needs and for sale to third par t ies.

www.hdsupply.com

HD Supply is one of the largest and most diversif ied wholesaledistr ibutors in the U.S. and Canada, providing top qual i ty pro-ducts and value-added services to professional customers inthe Infrast ructure and Energy , Maintenance, Repair and Im-provement and Specialty Construction markets. The company’spor tfol io of industry- leading businesses special izes in del iver-ing supplies and services to a wide range of customers, with a focus on contractors , bui lders , maintenance profess ionals , government and municipal enti t ies and industr ial businesses.Hal f of the company’s businesses have earned leading posi-t ions in the markets they serve.

5

6

7

2

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

14

MANAGEMENT REPORT

www.nielsen.com

The Nielsen Company is a global information and media com-pany with leading market posit ions in marketing and consumer

8

www.ersol .de

Ersol Thin Fi lm GmbH, a subsidiary of ersol Solar Energy AG,is a thin f i lm producer of solar modules based on amorphousand microcrystal l ine si l icon. The Thin Fi lm technology is anti-cipated to win significant market shares within the photovoltaicmarket by both allowing for market expansion on the one handand by par t ia l ly subst i tut ing the e x is t ing cr ysta l l ine P V pro-ducts . One major reason for this market development is thereduced requirement for rare s i l icon supply in the th in f i lmtechnology with perspect ives of increasing i ts eff ic iency.

10

www.portsamerica .com

Por ts America provides independent mar ine terminal oper-at ions to container shipping companies, rol l -on/ rol l -off ship-pers, cruise l ines and general cargo and stevedoring services at23 locat ions along the Atlantic and Gulf Coasts including NewYork, New Jersey, Philadelphia, Baltimore, Miami, New Orleans,Tampa and Houston.

11

www.foodvest .co .uk

Foodvest is one of the largest food groups in Europe. Foodvestis a UK registered business and was created in 2006 with themerger of Young’s Seafood in the UK and Findus in Sweden.Today the business is run by a s ingle management team.Young’s Seafood is based in Grimsby, England. Young’s is theUK’s leading seafood producer, with a 40% share of both thefrozen and chi l led seafood market. Findus is based in Malmo,Sweden. Findus is the leading frozen food brand in Sweden,Norway, F in land and France. F indus produces a wide range of products inc luding seafood, vegetables , ready meals andfrozen bakery products.

9

information, televis ion and other media measurement, onl ineintel l igence, mobile measurement, trade shows and businesspublications (Bil lboard, The Hollywood Reporter, and Adweek).The company is act ive in approx imately 100 countr ies , wi thheadquar ters in New York.

15

MANAGEMENT REPORT

www.ziggo.nl

Dutch Cable (since rebranded as Ziggo), is the market leadingcable T V operator in the Netherlands, and was created in 2006through the acquisi t ion of three exist ing cable operators witha combined value of EUR 5.45 bi l l ion.

www.guitarcenter.com

Guitar Center is the leading musical instrument retai ler and isapproximately four t imes the size of i ts largest competitor. TheCompany operates through three business units: Guitar Cen-ter Reta i l Stores (214 reta i l s tores) , Direct Response (onl ineand catalog businesses), and Music & Ar ts (97 stores providingrental band and orchestra equipment).

12

13 R H Y T H M

www.pfg. fr

OGF is the leader of the French funeral services market, withan approximate 2006 market share of 25% in value, and 23%in volumes. I ts posit ion is par t icular ly strong in the high endsegment of the market. The company provides a ful l scope ofservices, from organizat ion of burials and cremations, to themanufactur ing of coff ins (French leadership) and the sel l ingof pre-need funera l contracts through i ts large network , orpar tnerships with banks or insurance companies.

14

Ziggo was created f rom the combinat ion of Kabelcom, Casema and Mult ikabel , which were respect ively the second,th i rd and four th largest cable operators in the Nether lands. Together, the businesses provide cable to over half of all Dutchhouseholds. In 2006, they generated revenues of EUR 989 mil-l ion from 3.3 mil l ion subscribers.

www.spie .eu

Spie is the second largest provider of mul t i - technica l con-tract ing services in France. I ts main act iv i ty is the provision ofelectr ical , heating venti lat ion and air condit ioning and mecha-nical engineering to a wide range of industrial, commercial andpublic sector customers. In addit ion, Spie has developed spe-c ia l i sed business uni ts cover ing Oi l and Gas ser v ices , Com-municat ions and Nuclear act iv i t ies . I t i s a lso act ive outs ideFrance through subsid iar ies in Benelux , Morocco, Germany,Spain and Por tugal . Spie has revenues of around EUR 3.6 bi l -l ion and over 29 000 employees.

15

www.materprivate. ie

Mater Private Healthcare (“Mater”) is Ireland’s leading specia-l ist private hospital , located in Dublin. I t has 202 beds, 5 oper-at ing theatres ( increasing to 7 this year) , 178 special is t con-

16 sultants and over 700 staf f . I t was establ ished by the Sisters of Mercy in 1986 on a si te adjacent to the Mater MisericordiaeUniversity Hospital , one of Ireland’s leading academic teachinghospi ta ls , provid ing Mater wi th access to high-qual i ty con-sultants and medical staff . Mater provides a range of medicalspecial ty services and is considered a centre of excel lence forcardiac and cancer related procedures.

16

MANAGEMENT REPORT

www.ethypharm.com

Ethypharm is one of the world’s leading drug del ivery systems(DDS) companies that provide a range of effect ive solut ionsto opt imize the del iver y of pharmaceut ica l products . The use of Ethypharm’s DDS technologies del ivers impor tant benef i ts inc luding improving the drug’s ef f icacy , enhancing pat ient compliance and comfor t , ex tending the l i fe cycles ofexist ing pharmaceutical products, and reducing the total costof t reatment . E thypharm has launched 50 products in over 70 countr ies.

18

www.acosta.com

Acosta, Inc. is the leading sales and marketing agency (“SMA”)serv ic ing consumer packaged goods (“CPG”) companies in the U.S. and Canada. I ts customer base comprises over 1 300cl ients and includes top t ier global food and beverage manu-facturers . Acosta has roughly 11 000 non-unionized sales as-soc iates deployed at 120 000+ reta i l locat ions to ser ve theGrocery Channel and Strategic Channels, which include mass/c lub, natura l/specia l ty , convenience s tores and drug s tores .Acosta generates revenues through sales commission fees paidby CPGs for in-store merchandising and retai l execut ion ser-vices as well as category management and headquar ter sel l ingservices.

17

www.applus.com

Headquar tered in Barcelona, Applus is Spain’s leading test ing,inspect ion and cer t i f icat ion company and no. 10 in the world,employing over 8 500 people and operat ing in over 25 marketsubsegments in 32 countr ies across 5 cont inents . Applus operates global ly through four divis ions; Auto Vehicle Inspec-t ion, Inspection and Technical Assistance, Engineering, Test ingand Cer t i f icat ion, and Non-Destruct ive Tests and Inspect ions.

19www.hygenic .com

The Hygenic Corporat ion is a leading designer, manufacturer,and marketer of branded, consumable products sold to the-rapy, rehabi l i tat ion, and wellness professionals under the wellknown Thera-Band® and Bio-Freeze® brand names. The Com-pany’s core products inc lude res is tance bands and tubing, topical analgesics, and a broad range of therapy and exerciseproducts used by physical therapists, chiropractors, podiatrists,physical trainers and massage therapists to promote streng th,f lexibi l i ty , and provide pain rel ief for their pat ients.

20

F I NANC IAL R E PORT 2008

20

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

CONSOLIDATED BALANCE SHEET AS OF DECEMBER 31, 2008 AND DECEMBER 31, 2007in TCHF

Note 2008 2007Assets

Current assets

– Cash and cash equivalents 2 14 930 26

– Derivat ive instruments 4 – 1 645

– Receivables and prepayments 5 345 1 826

Total current assets 15 275 3 497

Non-current assets

– Loans 1 14 049 18 655

– Investments held as avai lable-for-sale

Direct Investments 1 43 864 101 788

Funds 1, 17 562 891 685 997

Contractual agreements 1, 16 – 41 425

Total non-current assets 620 804 847 865

Total Assets 20 636 079 851 362

Liabilities and Shareholders’ EquityCurrent Liabi l i t ies

– Payables and accrued charges 6 9 479 24 008

– Loans 7 101 947 107 954

– Deferred tax l iabi l i ty 13 – 145

Total current liabilities 111 426 132 107

Preferred shares 7 163 714 –

Total liabilities 275 140 132 107

Shareholders’ Equity

– Share capital 412 500 412 500

– Share capital premium 149 090 149 116

– Treasury stock (at cost) (30 691) (27 847)

– Reserve for stock option plan 18 – 182

– Total Revaluat ion reserve 10 (56 574) 26 772

– Accumulated surplus 158 532 77 948

– Net profi t for the period (271 918) 80 584

Total Shareholders’ Equity 360 939 719 255

Total Liabilities and Shareholders’ Equity 636 079 851 362

Net asset value per shareNumber of shares outstanding at year-end 8 3 929 185 3 949 027

Net asset value per share ( in CHF) 91.86 182.13

The accompanying notes on pages 24 to 52 form an integral par t of these consol idated f inancial statements.

21

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

CONSOLIDATED INCOME STATEMENT FOR THE PER IOD JANUARY 1 TO DECEMBER 31, 2008 AND JANUARY 1 TO DECEMBER 31, 2007in TCHF

Note 2008 2007Income

Interest income from non-current assets 12 3 268 11 130

Dividend income from non-current assets 12 352 3 165

Net real ized gains on investments 12 16 124 112 053

Interest income from current assets 80 671

Net gain on derivat ive instruments – 2 642

Total Income 20 19 824 129 661

ExpensesManagement fees 14 (11 595) (14 205)

Per formance fees 14 – (13 049)

Service fees 14 (404) (409)

Write-down of non-current assets 11 (223 015) (10 144)

Other operat ing expenses (4 534) (2 764)

Interest expense from loans (7 963) (1 898)

Dividend expense on preferred shares (3 811) –

Net loss on foreign currency exchange (39 616) (5 718)

Net loss on derivat ive instruments (266) –

Total Expenses (291 204) (48 187)

Income before tax expense (271 380) 81 474

Tax expenses 13 (538) (890)

Net profit for the period (271 918) 80 584

Earnings per shareWeighted average number of shares outstanding during the period 9 3 945 028 3 927 921

Net profi t/( loss) per share ( in CHF) – basic 9 (68.93) 20.52

Net profi t/( loss) per share ( in CHF) – di luted 9 (68.93) 20.49

The accompanying notes on pages 24 to 52 form an integral par t of these consol idated f inancial statements.

22

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

CONSOLIDATED STATEMENT OF CASH FLOWS FOR THE PER IOD JANUARY 1 TO DECEMBER 31, 2008 AND JANUARY 1 TO DECEMBER 31, 2007in TCHF

Note 2008 2007Cash Flows from Operating Activities

Purchase of non-current assets * 1 (281 658) (413 270)

Proceeds from return of invested capital in non-current assets * 1 166 125 146 121

Interest income received from current assets 80 673

Net interest income from non-current assets 12 3 432 13 193

Dividends received from non-current assets 12 352 3 165

Net real ized gains on investments 12 9 390 110 863

Proceeds from derivat ive instruments 1 378 1 942

Operat ing costs (4 910) (3 892)

Management & Per formance fees 14 (24 261) (14 662)

Total Cash Flows from Operating Activities (130 073) (155 867)

Cash Flows from Financing ActivitiesProceeds from loans 67 177 107 954

Repayment of loans (68 641) –

Interest paid on l ine of credit (8 057) (1 586)

Proceeds from issuance of preferred shares 157 618 –

Treasury share purchase (5 350) –

Treasury share sale 2 104 8 454

Total Cash Flows generated by/(used in) Financing Activities 144 851 114 822

Foreign Exchange Effect 126 3 892

Increase (decrease) in Cash and Cash Equivalents 14 904 (37 153)

Cash and Cash Equivalents as of January 1 2 26 37 179

Cash and Cash Equivalents as of December 31 2 14 930 26

* The dif ferences to the totals shown in note 1 are explained by currency effects and distr ibution in kind in respect to the unwinding of the contractual agreements

The accompanying notes on pages 24 to 52 form an integral par t of these consol idated f inancial statements.

23

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

STATEMENT OF CHANGES IN CONSOLIDATED SHAREHOLDERS’ EQUIT Y AS OF DECEMBER 31, 2008

AND DECEMBER 31, 2007in TCHF

Share Share Less Reserve Revaluation Accumulated Total

Capital Capital treasury for stock Reserve Surplus Equity

Premium stock option (Deficit)

(at cost) plan

Shareholders’ EquityBalance January 1, 2007 412 500 148 770 (36 207) 156 22 679 77 948 625 846

Transaction in reserve for stock option plan 26 26

Value increase on investments 20 078 20 078

Value decrease on investments due to currency differences (15 985) (15 985)

Transaction in treasury shares 346 8 360 8 706

Total of results included in shareholders’ equity 346 8 360 4 093 12 825Net profit for the period 80 584 80 584

Total Result 346 8 360 26 4 093 80 584 93 409

Total Shareholders’ Equity as of December 31, 2007 412 500 149 116 (27 847) 182 26 772 158 532 719 255

Balance January 1, 2008 412 500 149 116 (27 847) 182 26 772 158 532 719 255Transaction in reserve for stock option plan (182) (182)

Value decrease on investments – – (96 254) (96 254)

Value increase on investments due to currency differences – – 12 908 12 908

Transaction in treasury shares (26) (2 844) – (2 870)

Total of results included in shareholders’ equity (26) (2 844) (83 346) (86 216)Net profit for the period – – (271 918) (271 918)

Total Result (26) (2 844) (83 346) (271 918) (358 134)

Total Shareholders’ Equity as of December 31, 2008 412 500 149 090 (30 691) – (56 574) (113 386) 360 939

The accompanying notes on pages 24 to 52 form an integral par t of these consol idated f inancial statements.

24

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

CORPORATE INFORMATION

AIG Private Equity Ltd. , Zug (“the Company”) is a Swiss stockcorporat ion establ ished under the relevant provis ions of theSwiss Code of Obligations and domiciled in Zug. The Company,together wi th AIG Pr ivate Equi ty (Bermuda) Ltd . and APENFaith Media Holdings LLC (“the Subsidiar ies”), comprises theAIG PE Group (“the Group”). The Company’s shares are l istedon the SIX Swiss E xchange.

The Company’s investment object ive is to achieve longterm capi ta l growth for shareholders by invest ing in pr ivateequity funds. The Company may also make direct investmentsin operat ing companies . A l though the Company may invest directly in fund investments or companies, it is anticipated thatinvestments wil l general ly be made through the Subsidiar ies.

The Company’s Board of Directors is responsible for thepolicies and management of the Company as well as valuationsand the appointment of the investment committee. The sub-s id iar y ’s investment commit tee is responsib le for assess ing the investment oppor tunit ies presented by the manager andthe investment advisor and subsequently making investmentrecommendat ions to the Bermuda Board of Directors for approval . As of December 31, 2008 the Company par t ial ly em-ployed one employee (2007: one) . For informat ion on theGroup’s management p lease refer to Note 14, Managementand Advisory Agreement.

The consol idated f inancia l s tatements are author ized forissue on Apri l 29, 2009 by the Board of Directors. The annualgeneral meeting cal led for June 2, 2009 wil l vote on the f inalacceptance of the consol idated f inancial statements.

ACCOUNTING POLICIES

Basis of preparationThe accompanying consol idated f inancia l s ta tements of theGroup for the year ended December 31, 2008 have been pre-pared in accordance wi th Internat ional F inancia l Repor t ingStandards (IFRS) formulated by the Internat ional AccountingStandards Board (IASB), and comply with Swiss Law and theaccounting provisions of the addit ional rules for the l ist ing ofinvestment companies of the SIX Swiss E xchange.

In prepar ing these f inancia l s tatements management as -sumed the use of the going concern assumption to be appro-priate. The appropriateness of that assumption is disclosed innote 15 (l iquidity r isk).

The consol idated f inancial statements are prepared underthe historical cost convention, except that investments avai l -able- for-sa le and der ivat ive f inancia l inst ruments are s tated at their fair value as disclosed in the accounting pol ic ies here-after.

Basis of consolidationThe consol idated f inancia l s ta tements of the Group inc ludeAIG Private Equity Ltd. and the companies that i t controls. Thiscontrol i s normal ly ev idenced when the Group owns, e i ther direct ly or indirect ly , more than 50% of the voting r ights of acompany’s share capi ta l or i t i s able to govern the f inancia land operating policies of an enterprise so as to benefit from itsactivit ies. Consolidated financial statements are prepared usinguni form account ing pol ic ies for l ike t ransact ions and otherevents in similar circumstances. Subsidiar ies are consol idatedfrom the date on which effect ive control is transferred to theGroup and are no longer consol idated from the date that con-trol ceases. The consolidation is per formed using the purchasemethod. Al l intercompany transact ions and balances are el i -minated. Al l Group companies have a December 31 year end.The scope of consol idat ion current ly inc ludes AIG Pr ivateEqui ty (Bermuda) Ltd . and APEN Fai th Media Holdings LLC,which both are owned 100% by the Company.

NOTES TO THE CONSOLIDATED F INANCIAL STATEMENTS

AIG Pr ivate Equi ty Ltd .

AIG Pr ivate Equi ty (Bermuda) Ltd .

APEN Fai th Media Holdings LLC

100% 100%

25

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

• The investments of the Group are held as par t of theGroup’s por t fo l io sole ly for the purpose of capi ta l ga insupon sale in the near future.

• As of December 31, 2008 the Group holds ownership in-terests of 20% or more in AIG Hor izon Par tners Fund(36.57%; 20.50% inc luding s ide-by-s ide vehic le ; 2007:36.57%; 20.50% including side-by-side vehicle). Accordingto the l imi ted par tnership agreement of th is fund, theGroup does not have the power to par t ic ipate in the f inancial and operat ing pol icy of the fund. Therefore, thisinvestment is excluded from equity accounting.

Significant accounting judgments and estimatesThe preparat ion of f inancial statements requires managementto make est imates and assumptions that af fect the repor tedamounts of assets and l iabi l i t ies and disclosure of contingentassets and l iabi l i t ies at the date of the f inancia l s ta tements and the repor ted amounts of revenues and expenses duringthe repor t ing per iod. Actual resul ts could di f fer f rom thoseest imates.

The areas involving a higher degree of judgment or com-plexity, or areas where assumptions and est imates are signif i -cant to the f inancial statements are the fol lowing:

• Fair value of f inancial instrumentsThe fair value of f inancial instruments that are not tradedin an active market are determined by using valuation tech-niques. The Group uses i ts judgment to select a variety ofmethods and make assumptions that are not always sup-por ted by observable market pr ices or rates . The use of valuat ion techniques requires management to make est i -mates. Changes in assumptions could affect the repor tedfair value of these investments. The carry ing amounts ofinvestments for which fair values were determined usingvaluat ion techniques amounted to CHF 539.0 mi l l ion(2007: CHF 691.6 mil l ion).

• Share-based paymentsThe Group measures the cost of equity-sett led transactionswith management by reference to fair value of the equityat the date at which they are granted. Est imating fair valuefor share-based payments requires determining the mostappropriate valuat ion model for a grant of equity instru-ments, which is dependent on the terms and condit ions ofthe grant. This also requires determining the most appro-priate inputs to the valuation model including the expectedl i fe of the option, volat i l i ty and dividend yield and makingassumptions about them. The assumptions and model usedfor est imat ing fa i r va lue of share-based payments are

disclosed under “share-based compensation plans” (page30) . The carr y ing amounts of share-based payments forwhich fair values were determined using valuation techniquesamounted to TCHF 0 (2007: TCHF 182).

• ImpairmentManagement per forms an impairment assessment quar terlyto assess prolonged or s ignif icant decl ines in fair value onf inancia l assets avai lable for sa le . Management uses i ts judgement to determine which investments are consideredto be impaired. Changes in assumptions used could affectthe amount of impairments repor ted.

Change in accounting policiesThe accounting pol ic ies adopted are consistent with those ofthe previous f inancial year except as fol lows:

The following interpretation to published standards is man-datory for accounting periods beginning on or after 1 January2008. Adoption of these revised standards and interpretat ionsdid not have any effect on the f inancial per formance or posi-t ion of the Group:• IFR IC 12, ‘Service concession arrangements’ ; and• IFR IC 11, ‘ I FRS 2 – Group and treasury share transact ions’• IFRIC 14, ‘IAS 19 – The limit on a defined benefit asset, mini-

mum funding requirements and their interact ion’ ,• IAS 39 (amended), ‘Financial Instruments: Recogit ion and

Measurement’ .

Summary of significant accounting policiesForeign Currency Transactions– Functional and presentat ion currencyThe group’s investments are mainly held in foreign currenciesdif ferent from the presentat ion currency. Therefore, proceedsfrom these investments are also received in foreign currencies.Investments are general ly held in the Subsidiar ies which areaccounted for in USD. Fur ther, per formance management andcash f low project ions are based on investment currency (pri-mari ly USD and EUR). Accordingly, the Board of Directors con-siders the USD as the currency that most fai thful ly representsthe economic ef fects of the under ly ing t ransact ions , eventsand condit ions of the Group, and the USD is considered to bethe funct ional currency of the Company and i ts subsidiar ies.The presentat ion currency of the f inancial statements is CHF.

26

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

– Transact ions and balancesForeign currency transactions are translated into the functionalcurrency using the exchange rates prevai l ing at the dates ofthe transact ions. Foreign exchange gains and losses result ingfrom the sett lement of such transact ions and from the trans-la t ion at year-end exchange rates of monetar y assets and l iabi l i t ies denominated in fore ign currencies are recognized in the income statement. Translat ion dif ferences on monetaryitems, such as derivat ives held at fair value through profi t orloss, are repor ted as par t of the fair value gain or loss. Trans-la t ion di f ferences on non-monetar y i tems, such as equi t iesclassi f ied as avai lable-for-sale f inancial assets, are recognizedin equity (reserve from foreign currency translat ion).

– Translat ion to presentat ion currencyThe resul ts and f inancia l pos i t ions of Group companies aretranslated from the funct ional currency into the presentat ioncurrency as fol lows:

• assets and l iabi l i t ies for each balance sheet presented aretranslated at the c los ing rate at the date of that balancesheet;

• income and expenses for each income statement are trans-lated at effect ive exchange rates; and

• al l resul t ing e xchange di f ferences are recognized as a separate component of equity.

Cash and Cash EquivalentsCash includes cash on hand and cash with banks. Cash equi-valents are shor t-term, highly l iquid investments that are rea-di ly conver t ib le to known amounts of cash wi th or ig inalmaturi t ies of three months or less, and that are subject to aninsignificant risk of change of value. Cash and cash equivalentsare recorded at nominal value.

Financial Instruments – Initial recognition and subsequent measurement– Financial assets – Init ia l recognit ionFinancial assets within the scope of IAS 39 are classi f ied as f i -nancial assets at fair value through profit or loss, loans and re-ceivables , held- to-matur i ty investments or avai lable for sa leassets. The Group determines the classi f icat ion of i ts f inancialassets at ini t ia l recognit ion.

Financial assets are recognized init ial ly at fair value plus, inthe case of investments not held at fa ir value through prof i tor loss, direct ly attr ibutable transact ion costs.

Purchases or sales of f inancial assets that require del iveryof assets within a t ime frame establ ished by regulat ion or con-vention in the marketplace (regular way purchases) are recog-nized on the set t lement date , i .e . , the date that the Groupcommits to purchase or sel l the asset . The Group’s f inancialassets include cash and shor t-term deposits , trade and otherreceivables, loan and other receivables, quoted and unquotedfinancial instruments, and derivat ive f inancial instruments.

Financial assets – Subsequent measurementThe subsequent measurement of f inancial assets depends ontheir c lassi f icat ion as fol lows

• Loans and receivables Al l loans and receivables are subsequent ly measured atamor t ized cost using the effect ive interest method. Gainsand losses are recognized in the consol idated incomestatement when the loans and receivables are derecogni-zed or impaired, as wel l as through the amor t izat ion pro-cess.

• Avai lable-for-sale f inancial assets Available-for-sale f inancial assets are subsequently re-mea-sured at fair value with unreal ized gains or losses recogni-zed direct ly in equity unti l the investment is derecognizedor determined to be impaired, at which t ime the cumula-t ive gain or loss recorded in equity is recognized in the in-come statement.

Direct Investments and Fund InvestmentsUnder IAS 39, the Group has designated al l i ts investmentsand secur i t ies as avai lable- for-sa le . This category was chosen as the most appropriate for an investment companyas the Group manages net asset value. An investment, in-c luding contractual agreements , is recognized where theGroup deems i t probable that future economic benef i ts associated with an investment wil l f low to the enti ty , and i t has a cost or value that can be measured rel iably. Thefuture economic benef i t of an investment is i ts potent ia lto contr ibute, direct ly or indirect ly, to the f low of cash andcash equivalents to the enti ty. Al l purchases and sales ofinvestments are recognized when the capital is cal led or adistr ibut ion is received. Cost of purchase includes trans -act ion costs . Interest income and div idend income is recognized in the income statement upon the receipt ofsuch dividends.

27

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

Contractual AgreementsOn December 22, 1999 the Group entered into three con-tractual agreements with American International Group Inc.that enti t le the Group to receive payments equal to a prorata share of al l distr ibutions from a specif ied l ist of funds,whi le obl i gat ing the Group to make payments equal to apro rata share of al l draw-downs of committed capital tothe same underlying funds. Interest income, dividends andcapital gains relat ing to the contractual agreement are re-cognized in the income statement on a monthly basis whencash is received f rom the counterpar ty. The contractualagreements were wound-up in 2008.

• Financial assets at fair value through profi t or loss Financial assets at fair value through profi t or loss includefinancial assets held for trading and f inancial assets desi-gnated upon init ia l recognit ion at fair value through profi tor loss. Financial assets are classi f ied as held for trading i fthey are acquired for the purpose of se l l ing in the nearterm. This category inc ludes der ivat ive f inancia l inst ru-ments entered into by the Group. Financial assets at fa irva lue through prof i t and loss are carr ied in the balancesheet at fair value. Changes in the fair value of derivat ivef inancial instruments are recorded into the income state-ment.

• Derivat ive Financial InstrumentsThe Company enters into foreign exchange forwards or op-t ion contracts to par t ial ly macro-hedge i ts net exposure inprivate equity investments denominated in foreign curren-cies. These derivative f inancial instruments are held by theCompany and i ts Subsidiar ies.

Financial liabilities – Initial recognitionFinancial l iabi l i t ies within the scope of IAS 39 are classi f ied asf inancia l l iabi l i t ies at fa i r value through prof i t or loss , loansand borrowings, or as der ivat ives des ignated as hedging in-struments in an effective hedge, as appropriate. The Group de-termines the c lass i f icat ion of i ts f inancia l l iabi l i t ies at in i t ia lrecognit ion. Financial l iabi l i t ies are recognized init ia l ly at fairvalue and in the case of loans and borrowings, direct ly attr i -butable transact ion costs.

The Group’s f inancia l l iabi l i t ies inc lude t rade and otherpayables, bank overdraft , loans and borrowings and derivat ivef inancial instruments.

Financial liabilities - Subsequent measurementThe measurement of f inancial l iabi l i t ies depends on their c las-si f icat ion as fol lows:

• Financial l iabi l i t ies at fair value through profi t or lossFinancial l iabi l i t ies at fair value through prof i t or loss in-clude f inancial l iabi l i t ies held for trading and f inancial l ia-bi l i t ies designated upon init ia l recognit ion as at fair valuethrough prof i t or loss . This category inc ludes der ivat ive f inancial instruments entered into by the Group. Gains orlosses on l iabi l i t ies held for trading are recognized in theincome statement . The Group has not des ignated any f inancial l iabi l i t ies as at fair value through profi t or loss.

• Loans and borrowingsAfter ini t ia l recognit ion, interest bearing loans and borro-wings are subsequently measured at amor t ized cost usingthe effect ive interest rate method. Gains and losses are re-cognized in the income statement when the l iabi l i t ies arederecognized as wel l as through the amor t izat ion process.Preference shares, which are mandatori ly redeemable ona specif ic date, are classi f ied as l iabi l i t ies.

Financial Instruments – DerecognitionA f inancia l asset i s derecognized i f , and only i f , the Group either transfers the contractual r ights to receive the cash f lowsof the f inancial asset , or i t retains the contractual r ights to re-ceive the cash f lows of the f inancial asset , but assumes a con-t ractual obl igat ion to pay the cash f lows to one or morerec ip ients , and in doing so t ransfers substant ia l ly a l l of therisks and rewards of the asset .

A f inancia l l iabi l i ty i s derecognized when the obl igat ionunder the l iabi l i ty is discharged, is cancel led or has expired.When an exist ing f inancial l iabi l i ty is replaced by another fromthe same lender on substantial ly dif ferent terms, or the termsof an exist ing l iabi l i ty are substantial ly modif ied, such an ex-change or modi f icat ion is t reated as a derecogni t ion of the original l iabi l i ty and the recognit ion of a new l iabi l i ty , and thedifference in the respect ive carrying amounts is recognized inthe income statement.

28

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

Financial Instruments – Determination of fair valueThe Group’s investments are pr imar i ly non-current f inancia lassets and market quotat ions are not readi ly avai lable, there-fore these investments are measured at their fair value usingthe most appropriate valuat ion techniques as described in de-ta i l below. The responsibi l i ty for determining the fa ir valuesl ies with the Board of Directors. Although general par tners offunds in which the Group invests and sponsors of the Group’sdirect investments provide valuations of these investments, noindependent ex ternal valuat ion of these investments was con-ducted. Al l fair valuat ions may dif fer s ignif icantly from valuesthat would have been used had ready markets existed. Suchdifferences could be material .

– Direct InvestmentsDirect investment valuations are reviewed on a quar terly basisby the investment advisor. The investment advisor uses infor-mation provided by the lead sponsor of the direct investment.Financial and market per formance is compared with budget in-format ion, data obta ined f rom compet i tors and subsequentrounds of f inancing. The Company reviews and discusses thevaluations with the investment advisor and may independentlyapply adjustments to determine the valuat ion. In determiningthe fair value of an unquoted direct investment, al l appropriateand applicable factors relevant to their value, including but notl imited to the fol lowing are considered:

• Venture capital investments:A new f inancing round that is material in s ize for the com-pany and having new, sophist icated inst i tut ional investorsmaking up a s igni f icant piece of the f inancing round. Aninside round of f inancing does not qual i fy.

• Buy-out/later stage investments for which subsequentrounds of f inance are not antic ipated:Once an investment has been held for one year, an analy-sis of the fair market value of the investments wil l be per-formed. This analysis wi l l typical ly be based on one of thefol lowing methods (depending on what is appropriate forthat par t icular company/industry):– Result of mult iple analysis;– Result of discounted cash f low analysis;– Reference to transact ion prices ( including subsequent

f inancing rounds);– Reference to the valuat ion of other investors;– Reference to comparable companies.

Based on a composite assessment of a l l appropriate andapplicable indicators of fair value, the Group determines thefair values as of the valuat ion date.

– Fund InvestmentsIn determining the fair value of fund investments, the Groupreviews the most recent repor t provided by the fund manager.The Group reviews the valuat ions and fol lowing year-end dis-cusses por t fo l io company per formance wi th each indiv idualfund manager. The fund managers determine fair values of theunder ly ing investments by us ing the same valuat ion techni -ques as for direct investments.

Investments in securit ies and in other f inancial instrumentst raded on recognized exchanges ( inc luding bonds, equi t ies , futures contracts , opt ions, and funds), are valued at the lastrepor ted bid price on the valuat ion date. Investments in secu-rit ies and in other f inancial instruments traded in the over-the-counter market and l i s ted secur i t ies for which no t rade isrepor ted on the valuat ion date are valued at the last repor tedbid and ask price for long and shor t posit ions, respect ively.

– Contractual AgreementsThe contractual agreements are va lued us ing the la test re-por ted net asset value available from the General Par tners andadding or subtract ing subsequent cash f lows.

– Derivat ive Financial InstrumentsFair va lues for der ivat ive f inancia l instruments are obta inedfrom quoted market pr ices, discounted cash f low models, oroption pric ing models as appropriate.

Financial Instruments – Impairment of financial assetsFinancia l inst ruments are rev iewed for impairment at each balance sheet date . For avai lable- for-sa le investments , the cumulat ive gain or loss prev ious ly recognized in equi ty is inc luded in net prof i t or loss for the per iod when there is object ive evidence that the asset is impaired.

An impairment is recorded when there is a s igni f icant (> 30%) or prolonged (> 1 year) decrease in fair value belowcost. Impairments are reflected in revaluation reserves (equity)and in the write-down of long-term assets (income statement).

The avai lable- for-sa le investments are categor ized intothree dis t inct categor ies . The appl icat ion of the impairment pol icy to the individual category of investments is appl ied asfol lows:

29

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

– Direct InvestmentsDirect investment valuations are reviewed on a quar terly basisby the investment advisor. Financial and market per formanceis compared with budget information, data obtained from com-peti tors and subsequent rounds of f inancing. In case of s igni-f icant deviat ions , va luat ions are adjusted to ref lect currentmarket va lues . I f a d i rect investment has had a fa i r marketvalue below cost for at least a year or in excess of 30%, i t wi l lbe deemed to be impaired and the cumulat ive loss previouslyrecognized in equity wil l be transferred to profit or loss for theperiod.

– Fund InvestmentsFunds where the Company is a direct l imited par tner wi l l bereviewed at each balance sheet date. I f a fund investment hashad a fair market value below cost for at least a year or in ex-cess of 30%, i t wi l l be deemed to be impaired and the cumu-lat ive loss previously recognized in equity wi l l be transferredto profi t or loss for the period.

– Contractual AgreementsAt each balance sheet date the reference funds are reviewedby the Company and investment advisor. I f a reference fundhas l iquidated al l of i ts por tfol io companies and is beyond i tsinvestment period, the Company wil l el iminate the referencefund from the contractual agreements and expense any resi-dual value through the profi t and loss accounts. Addit ional ly ,the Company wi l l inc lude the cumulat ive loss previously re-cognized in equi ty in net prof i t or loss for the per iod i f i tcomes to the conclusion that the future cash f lows of the con-tractual agreements wil l not cover i ts costs. Refer to Note 16for fur ther detai ls on the contractual agreements.

Net Asset Value per Share and Earnings per ShareThe net asset value per share is calculated by dividing the netassets included in the balance sheet by the number of par t ic i -pating shares outstanding at the repor ting date. Basic earningsper share are calculated by dividing the net prof i t attr ibutableto the ordinary shareholders by the weighted average numberof ordinary shares outstanding during the period. Diluted earn-ings per share are ca lculated by adjust ing the weighted average number of ordinary shares outstanding assuming con-version of al l di lut ive potential ordinary shares.

TaxesTax provisions are based on repor ted income. Taxes are calcu-lated in accordance with the tax regulat ions in force in eachcountry where the Group has investments.

– Swit zerlandThe Company is taxed as a holding company in the Canton ofZug. Income, including dividend income and capital gains fromits par t ic ipat ions, is exempt from taxat ion at the cantonal andcommunal level . For Swiss federal tax purposes, income tax atan effect ive tax rate of approximately 7.8% is levied. However,div idend income qual i f ies for the par t ic ipat ion exemption i fthe re lated investment represents at least 20% of the othercompany’s share capital or has a value of not less than CHF 2mi l l ion. The par t ic ipat ion e xempt ion is e x tended to capi ta lga ins on the sa le of a substant ia l par t ic ipat ion ( i .e . a t least20%), which was acquired after January 1, 1997, and was heldfor a minimum holding period of one year. The result of thepar t ic ipat ion exempt ion pursuant to the aforement ioned re-quirements is that d iv idend income and capi ta l ga ins are almost ful ly exempt from taxat ion. In cases where the par t ic i -pat ion exemption is not appl icable, a deferred tax l iabi l i ty wi l lbe calculated for Swiss federal tax purposes.

Provisions for taxes payable on profits earned in the Groupcompanies are calculated and recorded based on the applica-ble tax rate in Swit zerland.

– USAPEN Faith Media Holdings LLC is subject to income and capi-tal gains taxes in the US.

Tax expenses shown in the profi t and loss accounts repre-sent wi thholding taxes paid in var ious jur isdic t ions that theGroup can not rec la im and may inc lude direct taxes paid inSwit zerland or the US. Capital taxes charged to the Companyby the Canton of Zug are included in the operat ing expenses.

Shareholders EquityOrdinary shares are classi f ied as equity. Mandatori ly redeem-able preference shares are classi f ied as l iabi l i t ies . The trans-act ion costs of an equity transact ion, other than in the contex tof a business combination, are accounted for as a deductionfrom equi ty. Equi ty t ransact ion costs are comprised of onlythose incrementa l e x ternal costs d i rect ly a t t r ibutable to theequity transact ion, which would otherwise have been avoided.Equity is comprised of the fol lowing:

30

AIG PR IVATE EQUIT Y GROUP – CONSOLIDATED F INANCIAL STATEMENTS 2008

• Share capital and Share capital premiumRefer to Note 8 for a descript ion and fur ther detai ls on theshare capital and share capital premium.