AI & Machine Learning Applied to Investment Management ... · AI & Machine Learning Applied to...

48

AI & Machine Learning Applied to Investment Management: Beyond the Hype October 2018

Transcript of AI & Machine Learning Applied to Investment Management ... · AI & Machine Learning Applied to...

AI & Machine Learning Applied to Investment

Management: Beyond the Hype

October 2018

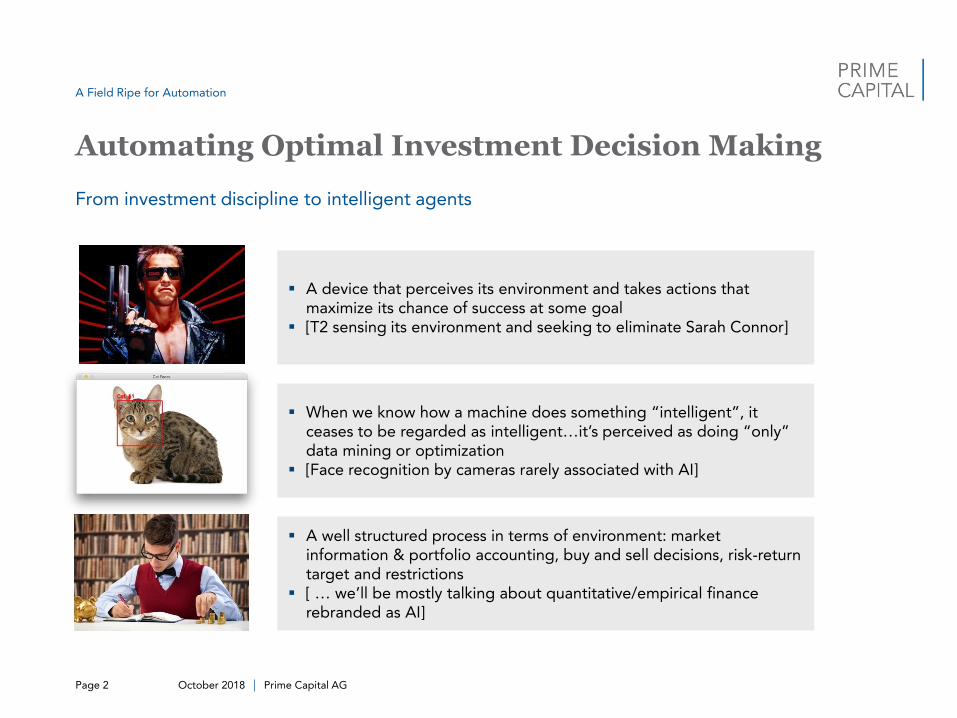

From investment discipline to intelligent agents

A Field Ripe for Automation

Automating Optimal Investment Decision Making

October 2018 Prime Capital AG Page 2

A well structured process in terms of environment: market information & portfolio accounting, buy and sell decisions, risk-return target and restrictions

[ … we’ll be mostly talking about quantitative/empirical finance rebranded as AI]

A device that perceives its environment and takes actions that maximize its chance of success at some goal

[T2 sensing its environment and seeking to eliminate Sarah Connor]

When we know how a machine does something “intelligent”, it ceases to be regarded as intelligent…it’s perceived as doing “only” data mining or optimization

[Face recognition by cameras rarely associated with AI]

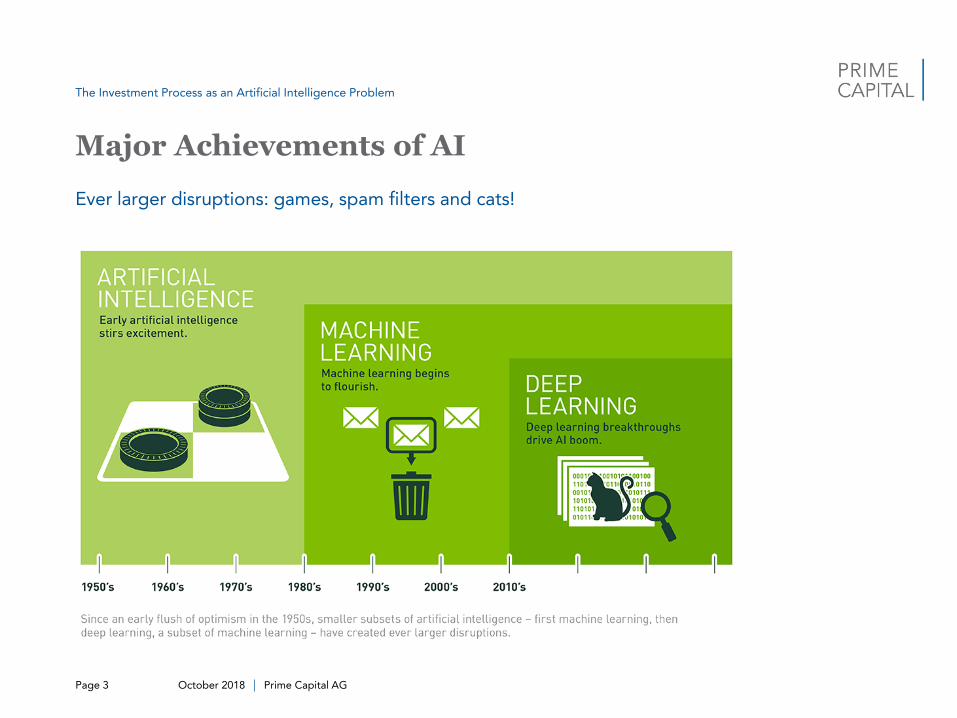

Ever larger disruptions: games, spam filters and cats!

The Investment Process as an Artificial Intelligence Problem

Major Achievements of AI

Page 3 October 2018 Prime Capital AG

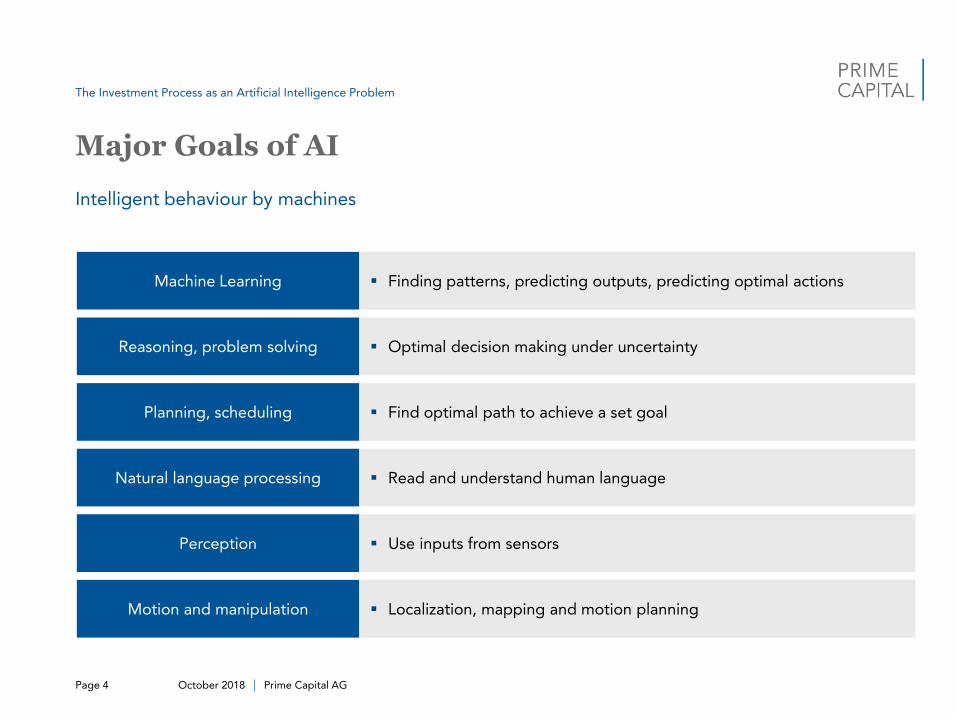

Intelligent behaviour by machines

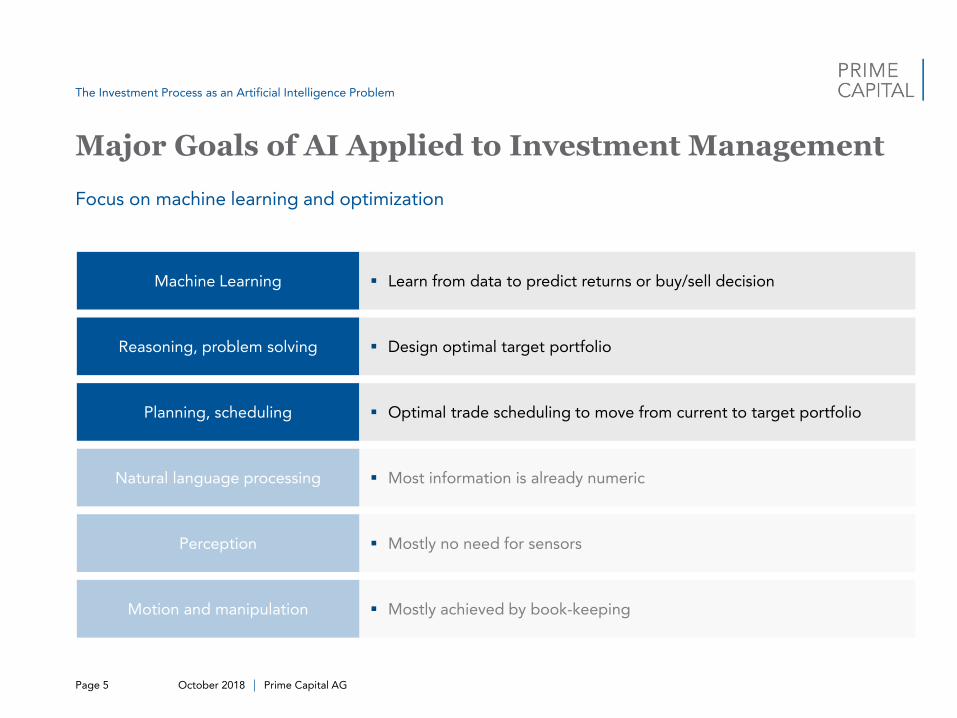

The Investment Process as an Artificial Intelligence Problem

Major Goals of AI

Machine Learning Finding patterns, predicting outputs, predicting optimal actions

Reasoning, problem solving Optimal decision making under uncertainty

Planning, scheduling Find optimal path to achieve a set goal

Natural language processing Read and understand human language

Perception Use inputs from sensors

Motion and manipulation Localization, mapping and motion planning

Page 4 October 2018 Prime Capital AG

Focus on machine learning and optimization

The Investment Process as an Artificial Intelligence Problem

Major Goals of AI Applied to Investment Management

Machine Learning Learn from data to predict returns or buy/sell decision

Reasoning, problem solving Design optimal target portfolio

Planning, scheduling Optimal trade scheduling to move from current to target portfolio

Natural language processing Most information is already numeric

Perception Mostly no need for sensors

Motion and manipulation Mostly achieved by book-keeping

Page 5 October 2018 Prime Capital AG

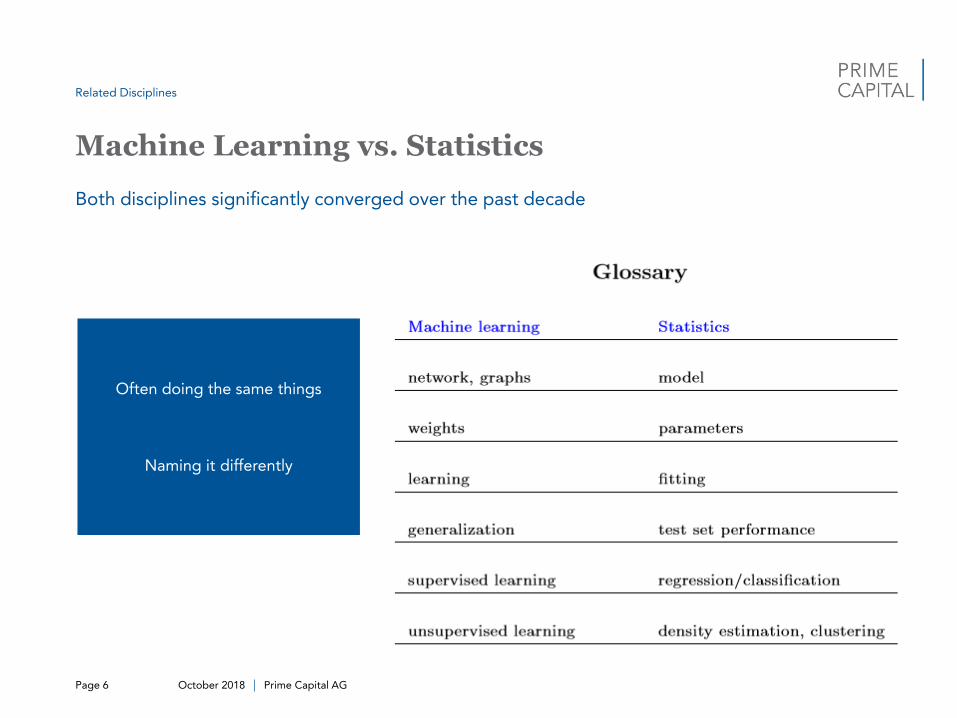

Both disciplines significantly converged over the past decade

Related Disciplines

Machine Learning vs. Statistics

October 2018 Prime Capital AG Page 6

Often doing the same things

Naming it differently

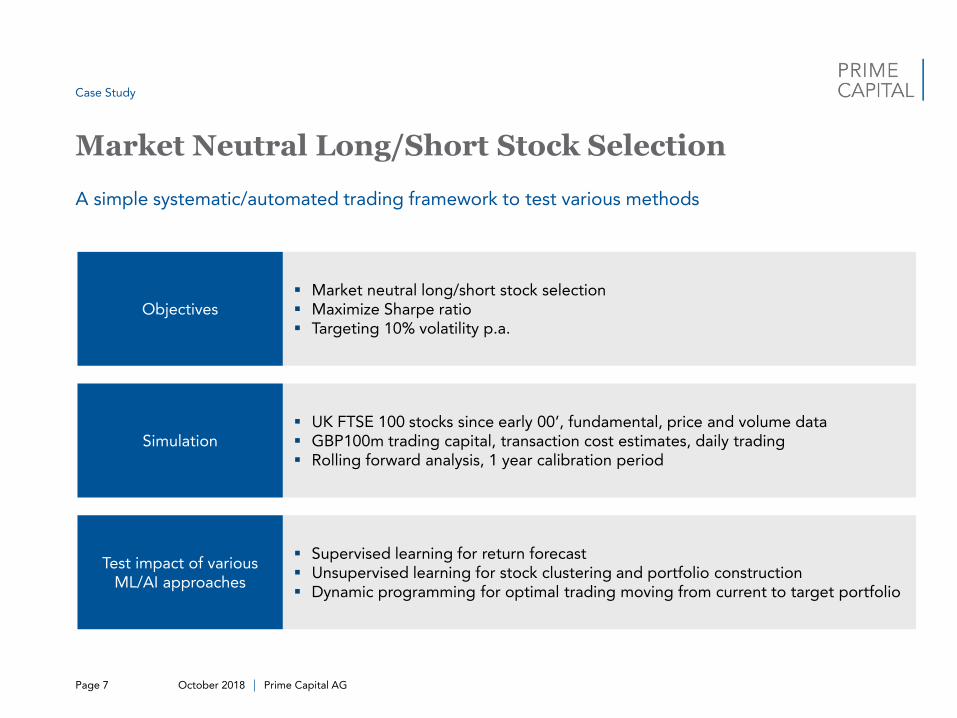

A simple systematic/automated trading framework to test various methods

Case Study

Market Neutral Long/Short Stock Selection

October 2018 Prime Capital AG Page 7

Simulation UK FTSE 100 stocks since early 00’, fundamental, price and volume data GBP100m trading capital, transaction cost estimates, daily trading Rolling forward analysis, 1 year calibration period

Objectives Market neutral long/short stock selection Maximize Sharpe ratio Targeting 10% volatility p.a.

Test impact of various ML/AI approaches

Supervised learning for return forecast Unsupervised learning for stock clustering and portfolio construction Dynamic programming for optimal trading moving from current to target portfolio

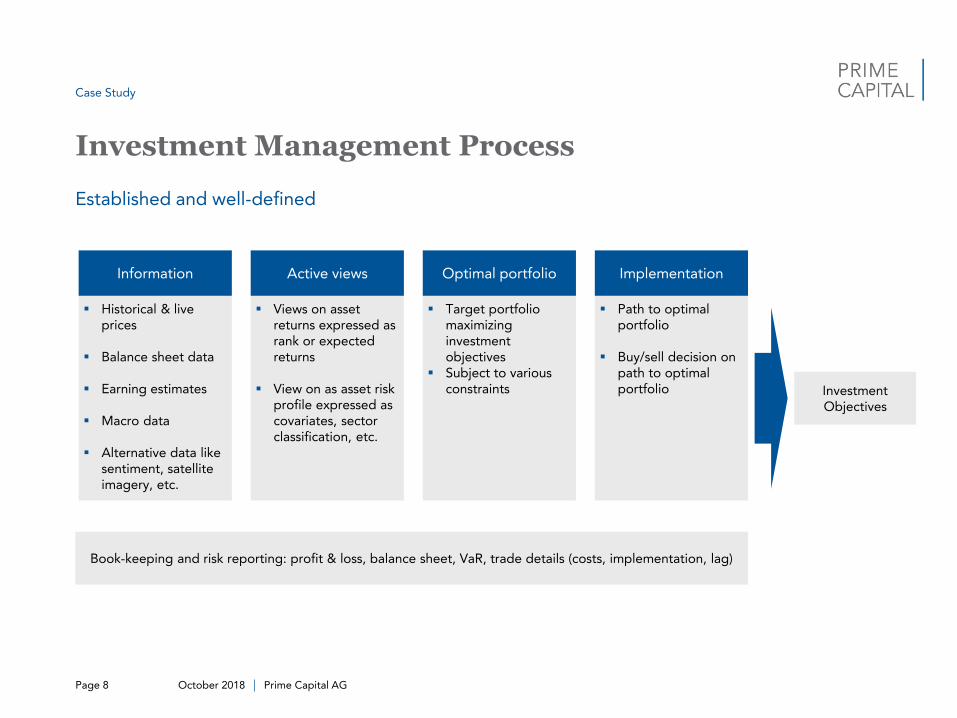

Established and well-defined

Case Study

Investment Management Process

October 2018 Prime Capital AG Page 8

Information

Historical & live prices

Balance sheet data

Earning estimates

Macro data

Alternative data like sentiment, satellite imagery, etc.

Active views

Views on asset returns expressed as rank or expected returns

View on as asset risk profile expressed as covariates, sector classification, etc.

Optimal portfolio

Target portfolio maximizing investment objectives

Subject to various constraints

Implementation

Path to optimal portfolio

Buy/sell decision on path to optimal portfolio Investment

Objectives

Book-keeping and risk reporting: profit & loss, balance sheet, VaR, trade details (costs, implementation, lag)

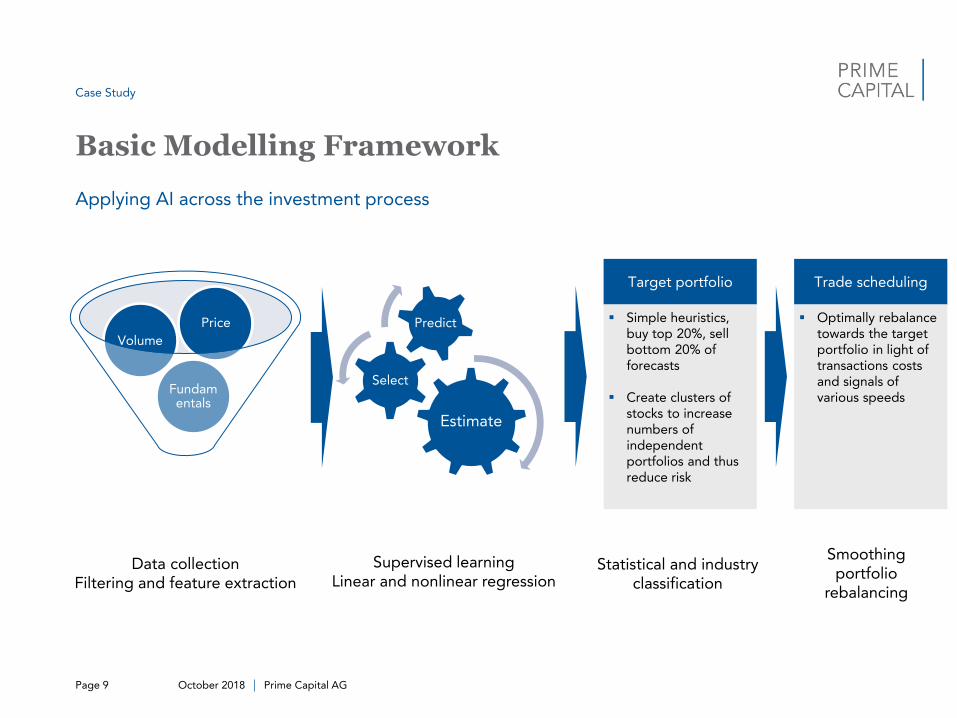

Applying AI across the investment process

Case Study

Basic Modelling Framework

October 2018 Prime Capital AG Page 9

Fundamentals

Volume

Price

Estimate

Select

Predict

Target portfolio

Simple heuristics, buy top 20%, sell bottom 20% of forecasts

Create clusters of stocks to increase numbers of independent portfolios and thus reduce risk

Trade scheduling

Optimally rebalance towards the target portfolio in light of transactions costs and signals of various speeds

Supervised learning Linear and nonlinear regression

Data collection Filtering and feature extraction

Statistical and industry classification

Smoothing portfolio

rebalancing

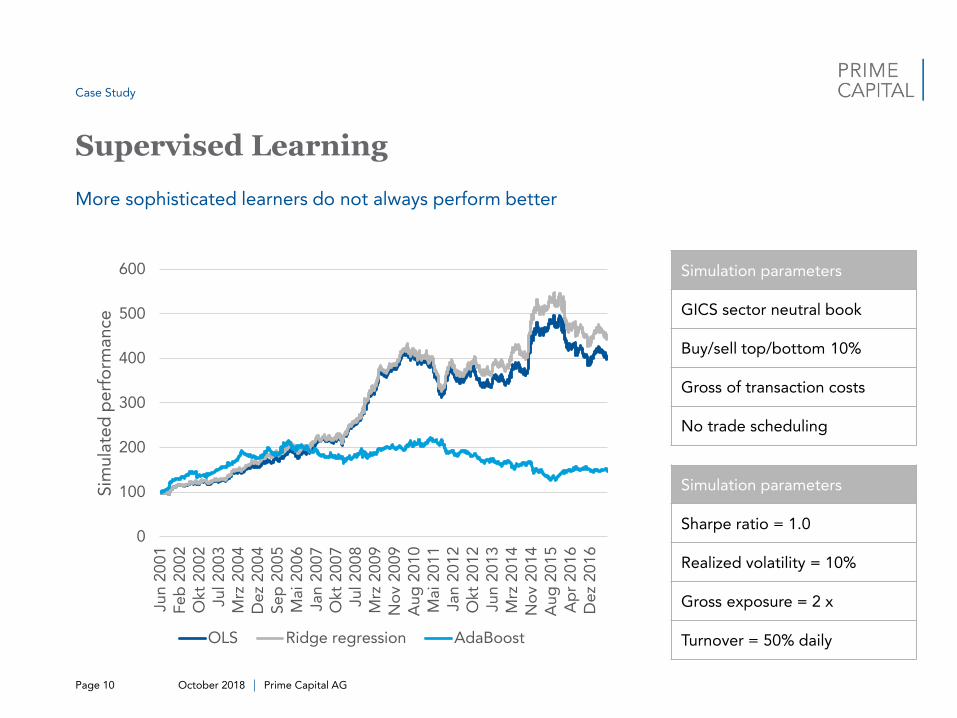

More sophisticated learners do not always perform better

Case Study

Supervised Learning

October 2018 Prime Capital AG Page 10

0

100

200

300

400

500

600

Jun 2

001

Fe

b 2

002

Okt

20

02

Jul 2

00

3M

rz 2

004

Dez

200

4Se

p 2

005

Mai 20

06

Jan 2

007

Okt

20

07

Jul 2

00

8M

rz 2

009

No

v 20

09

Au

g 2

01

0M

ai 20

11

Jan 2

012

Okt

20

12

Jun 2

013

Mrz

20

14

No

v 20

14

Au

g 2

01

5A

pr

2016

Dez

201

6

Sim

ula

ted

pe

rfo

rmance

OLS Ridge regression AdaBoost

Simulation parameters

GICS sector neutral book

Buy/sell top/bottom 10%

Gross of transaction costs

No trade scheduling

Simulation parameters

Sharpe ratio = 1.0

Realized volatility = 10%

Gross exposure = 2 x

Turnover = 50% daily

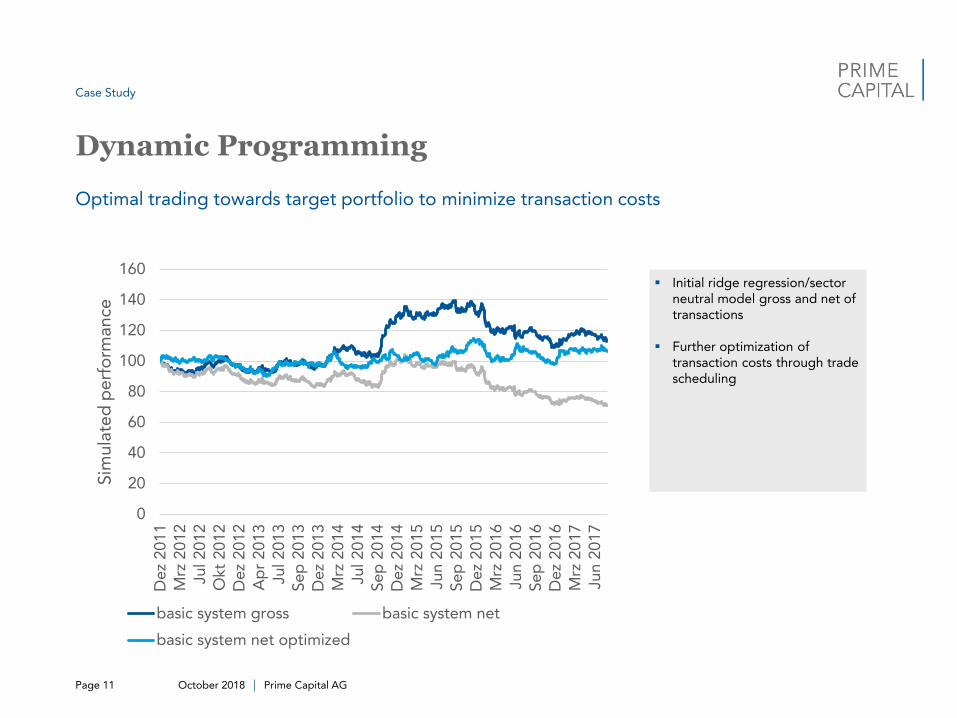

Optimal trading towards target portfolio to minimize transaction costs

Case Study

Dynamic Programming

October 2018 Prime Capital AG Page 11

0

20

40

60

80

100

120

140

160

Dez

201

1

Mrz

20

12

Jul 2

01

2

Okt

20

12

Dez

201

2

Ap

r 2

013

Jul 2

01

3

Se

p 2

013

Dez

201

3

Mrz

20

14

Jul 2

01

4

Se

p 2

014

Dez

201

4

Mrz

20

15

Jun 2

015

Se

p 2

015

Dez

201

5

Mrz

20

16

Jun 2

016

Se

p 2

016

Dez

201

6

Mrz

20

17

Jun 2

017

Sim

ula

ted

pe

rfo

rmance

basic system gross basic system net

basic system net optimized

Initial ridge regression/sector neutral model gross and net of transactions

Further optimization of transaction costs through trade scheduling

Key Takeaways

The Rise of The Machines?

October 2018 Prime Capital AG Page 12

Key Takeaways

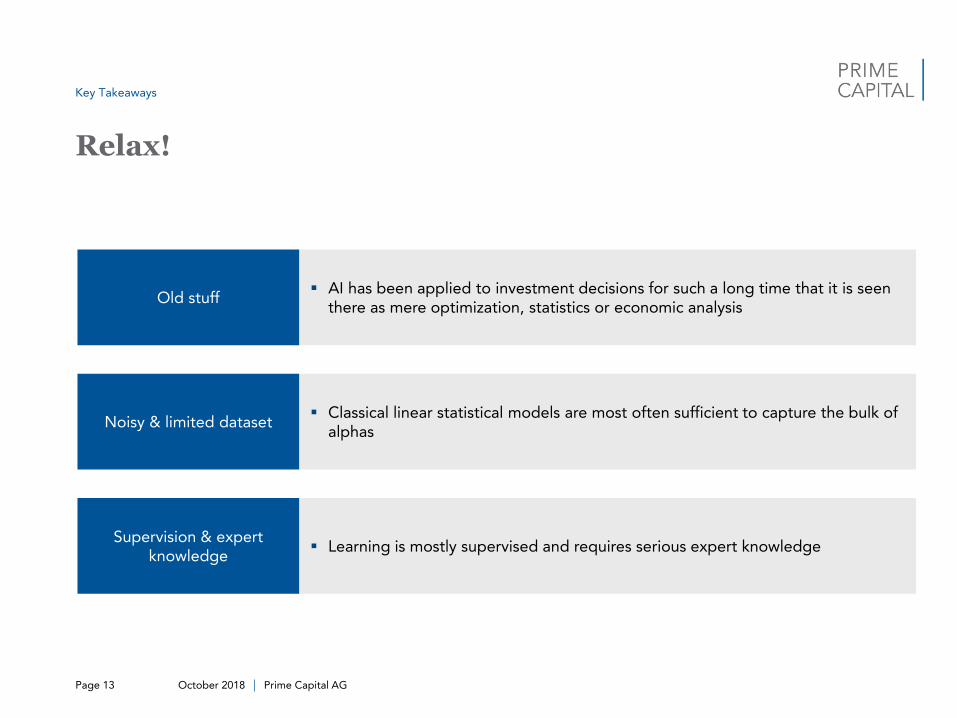

Relax!

October 2018 Prime Capital AG Page 13

Old stuff AI has been applied to investment decisions for such a long time that it is seen

there as mere optimization, statistics or economic analysis

Supervision & expert knowledge

Learning is mostly supervised and requires serious expert knowledge

Noisy & limited dataset Classical linear statistical models are most often sufficient to capture the bulk of

alphas

Key Takeaways

Industry Outlook

October 2018 Prime Capital AG Page 14

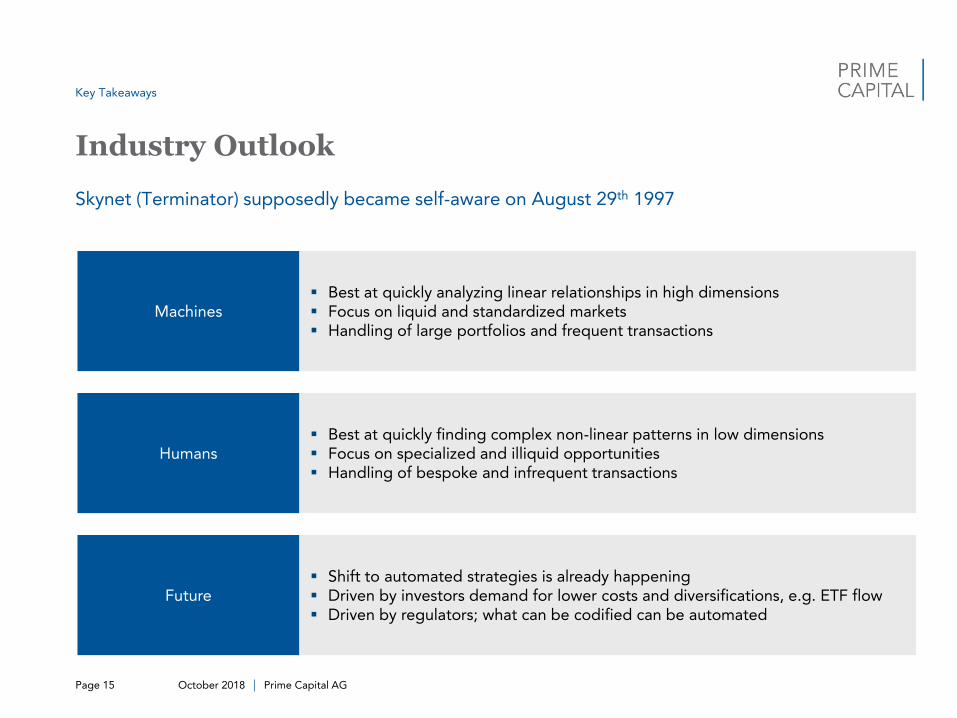

Skynet (Terminator) supposedly became self-aware on August 29th 1997

Key Takeaways

Industry Outlook

October 2018 Prime Capital AG Page 15

Machines Best at quickly analyzing linear relationships in high dimensions Focus on liquid and standardized markets Handling of large portfolios and frequent transactions

Future Shift to automated strategies is already happening Driven by investors demand for lower costs and diversifications, e.g. ETF flow Driven by regulators; what can be codified can be automated

Humans Best at quickly finding complex non-linear patterns in low dimensions Focus on specialized and illiquid opportunities Handling of bespoke and infrequent transactions

Skynet (Terminator) supposedly became self-aware on August 29th 1997

October 2018 Prime Capital AG Page 16

This document does not constitute any advice, recommendation or investment proposal; was issued for information purpose only, has no contractual value; and may contain

errors and/or omissions. This document does not create any legally binding obligations on the part of Prime Capital AG and/or its affiliates (“Prime Capital”) and nothing

contained herein shall in any way constitute any offer by Prime Capital to provide any service or product, or an offer or solicitation of an offer to buy or sell any securities or

other investment product. This document is not intended for distribution or use by any person or entity who is a citizen or resident of or located in any jurisdiction where such

distribution, publication or use would be prohibited. Past performance is not indicative of future results. The value of an investment in the fund may go up as well as down and

can result in losses, up to and including a total loss of the amount initially invested. No representation or warranty, express or implied, is made as to the accuracy,

completeness or correctness of the information contained in this document and Prime Capital assumes no responsibility or liability for any of the contents, errors and/or

omissions herein, nor for any use thereof or reliance placed thereupon by any person. In case of any inconsistency between this document and the latest prospectus pertaining

to the fund, that prospectus shall prevail. A decision to invest in the fund should only be taken after careful consideration of that prospectus and the legal information contained

therein. The prospectus can be obtained from the fund’s Administrator, registered office or representative (where applicable). You should consult a lawyer, an accountant or

other financial advisor as to the fund’s suitability for you, prior to any investment in the fund.

Source of data: Prime Capital AG

Disclaimer

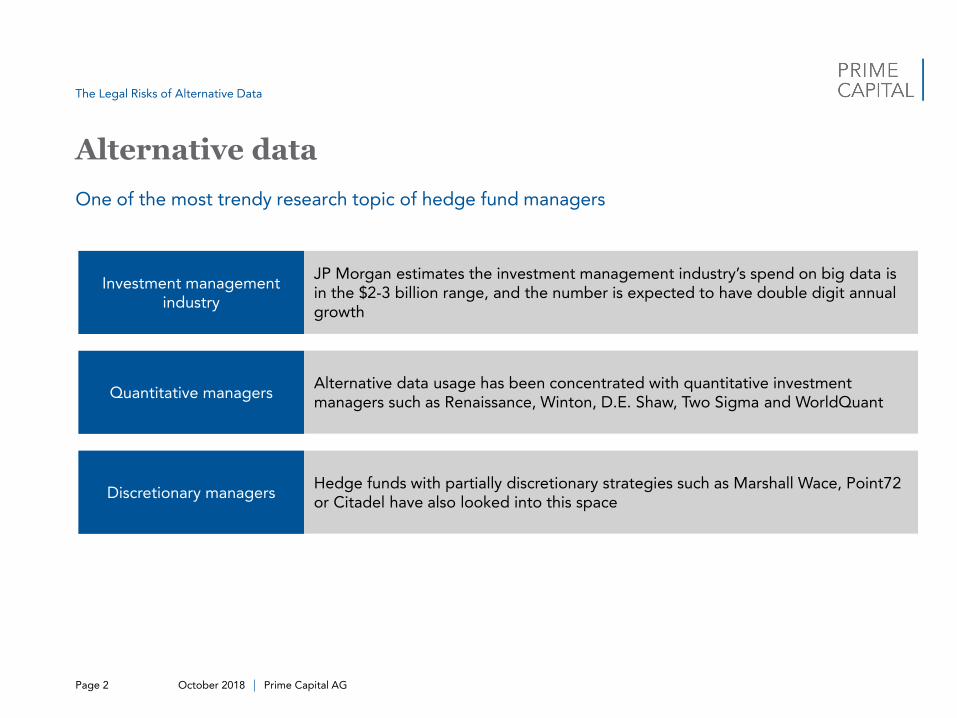

The Legal Risks of Alternative DataOctober 2018

One of the most trendy research topic of hedge fund managers

Alternative data

Prime Capital AGPage 2 October 2018

The Legal Risks of Alternative Data

Investment management industry

JP Morgan estimates the investment management industry’s spend on big data is in the $2-3 billion range, and the number is expected to have double digit annual growth

Quantitative managersAlternative data usage has been concentrated with quantitative investment managers such as Renaissance, Winton, D.E. Shaw, Two Sigma and WorldQuant

Discretionary managersHedge funds with partially discretionary strategies such as Marshall Wace, Point72 or Citadel have also looked into this space

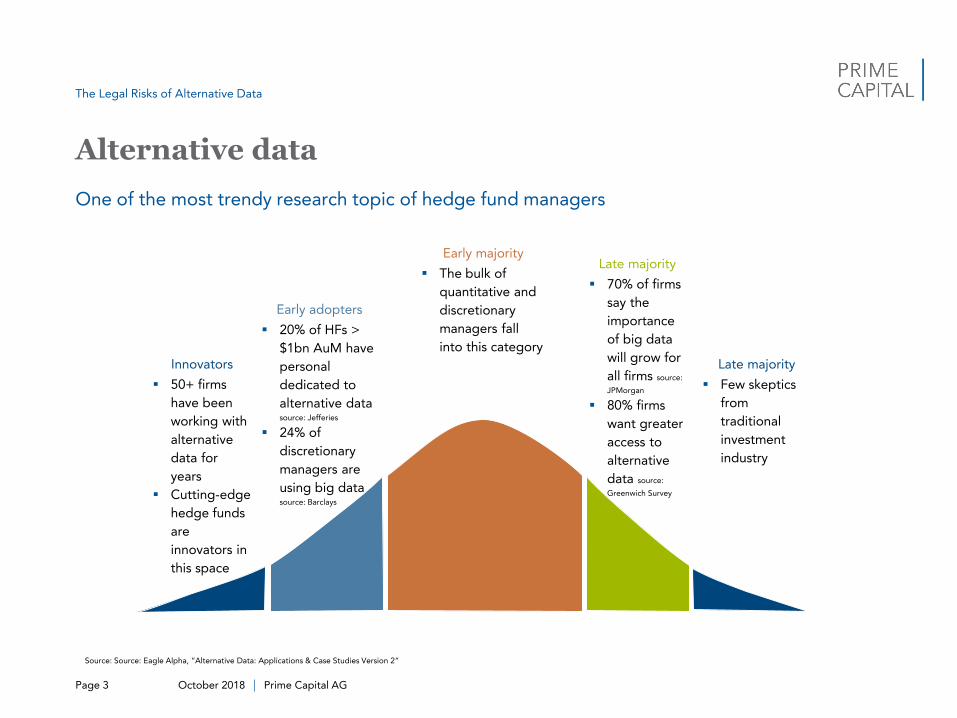

One of the most trendy research topic of hedge fund managers

Alternative data

Prime Capital AGPage 3 October 2018

Innovators

50+ firms

have been

working with

alternative

data for

years

Cutting-edge

hedge funds

are

innovators in

this space

Early adopters

20% of HFs >

$1bn AuM have

personal

dedicated to

alternative data source: Jefferies

24% of

discretionary

managers are

using big data source: Barclays

Early majority

The bulk of

quantitative and

discretionary

managers fall

into this category

Late majority

70% of firms

say the

importance

of big data

will grow for

all firms source:

JPMorgan

80% firms

want greater

access to

alternative

data source:

Greenwich Survey

Late majority

Few skeptics

from

traditional

investment

industry

Source: Source: Eagle Alpha, “Alternative Data: Applications & Case Studies Version 2”

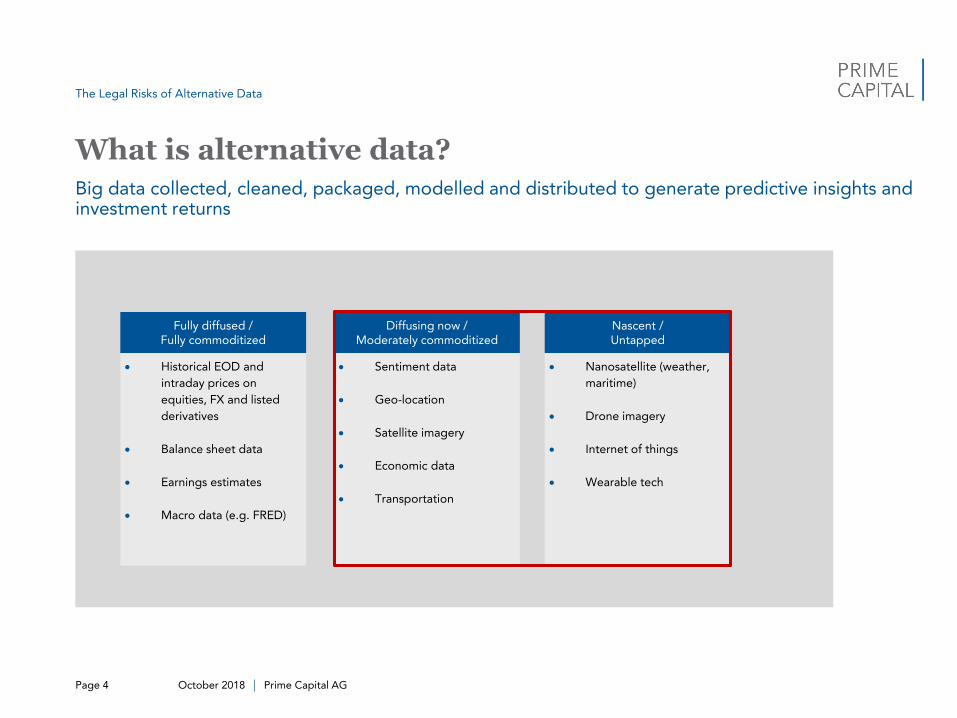

The Legal Risks of Alternative Data

Big data collected, cleaned, packaged, modelled and distributed to generate predictive insights and investment returns

What is alternative data?

Prime Capital AGPage 4 October 2018

Fully diffused /Fully commoditized

Historical EOD and

intraday prices on

equities, FX and listed

derivatives

Balance sheet data

Earnings estimates

Macro data (e.g. FRED)

Diffusing now / Moderately commoditized

Sentiment data

Geo-location

Satellite imagery

Economic data

Transportation

Nascent / Untapped

Nanosatellite (weather,

maritime)

Drone imagery

Internet of things

Wearable tech

The Legal Risks of Alternative Data

Legal risks are less emphasized and potentially overlooked by managers and investors

Legal grey zone

Prime Capital AGPage 5 October 2018

’’

’’

Source: Financial Times.

The Legal Risks of Alternative Data

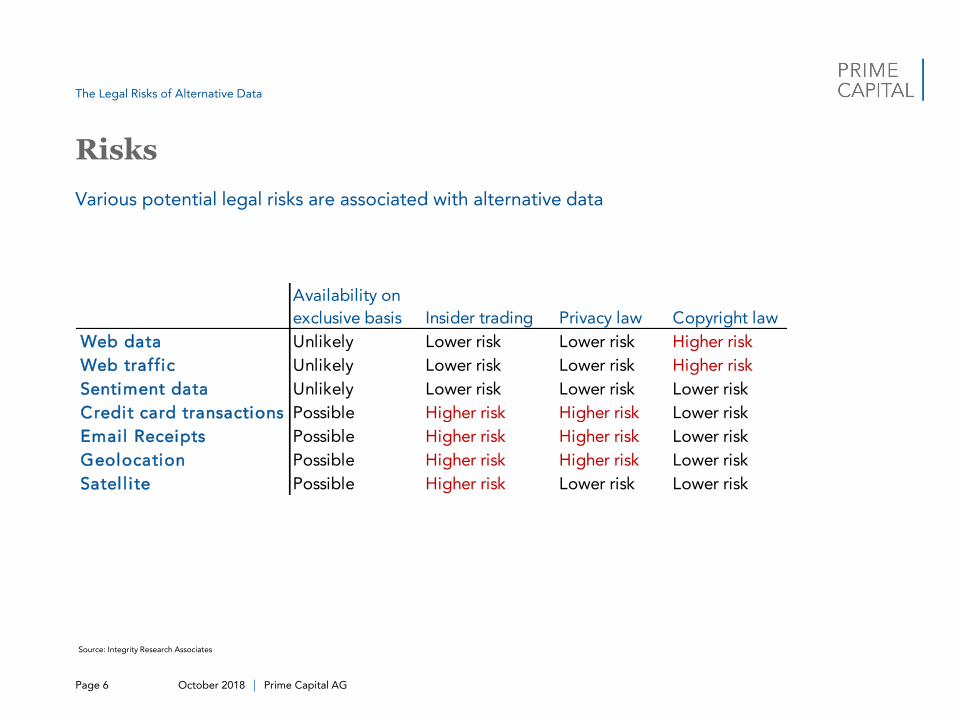

Various potential legal risks are associated with alternative data

Risks

Prime Capital AGPage 6 October 2018

Source: Integrity Research Associates

Availability on

exclusive basis Insider trading Privacy law Copyright law

Web data Unlikely Lower risk Lower risk Higher risk

Web traffic Unlikely Lower risk Lower risk Higher risk

Sentiment data Unlikely Lower risk Lower risk Lower risk

Credit card transactions Possible Higher risk Higher risk Lower risk

Email Receipts Possible Higher risk Higher risk Lower risk

Geolocation Possible Higher risk Higher risk Lower risk

Satel l ite Possible Higher risk Lower risk Lower risk

The Legal Risks of Alternative Data

Facebook – Cambridge Analytica data scandal

Risks: user privacy violation

Prime Capital AGPage 7

Facebook exposed up to 87 million users’ data to Cambridge Analyticathrough a quiz app

Cambridge Analytica gained access to the data of app user’s facebook friends without their knowledge, consent or authorization

Facebook may initially have been misled, but it failed to notify Facebook users about the situation and to ensure that the stolen data was destroyed after learning the true nature of Cambridge Analytica’s work

October 2018

Source: vox.com

The Legal Risks of Alternative Data

Alternative data = material non-public information?

Risks: insider trading

Prime Capital AGPage 8

SEC v. Huang

Two employees of Capital One used the bank’s customers credit card data to predict stock price moves for their personal trading account

The pair made $2.8mn between 2015 and 2017

The court ruled that the credit card transaction data is material non-public information and the use of data is without consent of the bank or the credit card users

The two employees end up paying $4.7mn and $13.5mn fine respectively

October 2018

Source: Integrity Research Associates

The Legal Risks of Alternative Data

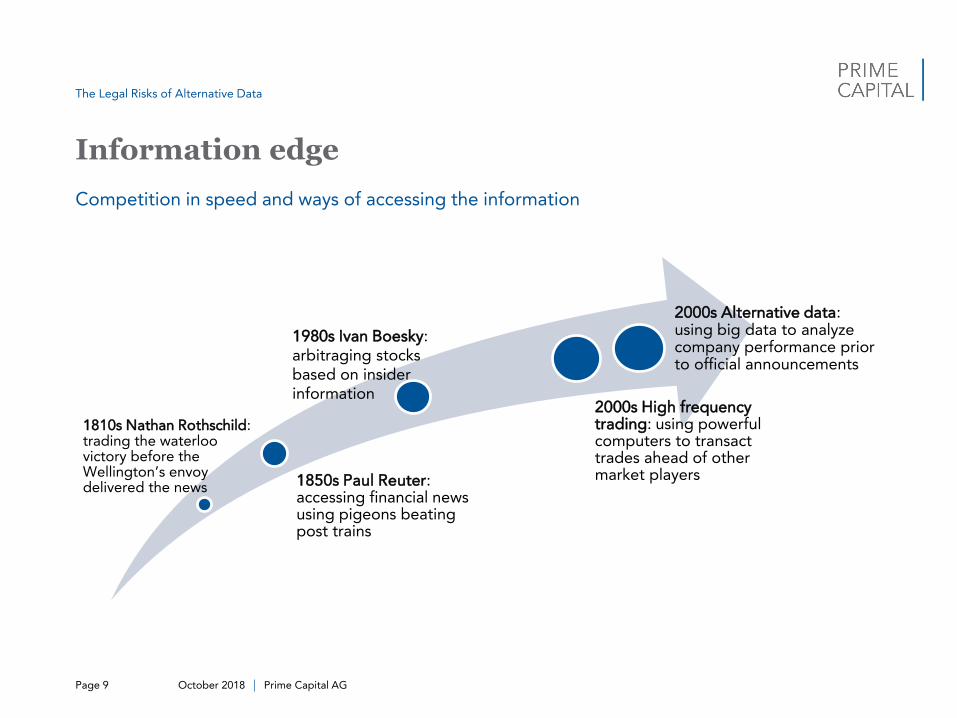

Competition in speed and ways of accessing the information

Information edge

Prime Capital AGPage 9 October 2018

1810s Nathan Rothschild: trading the waterloo victory before the Wellington’s envoy delivered the news 1850s Paul Reuter:

accessing financial news using pigeons beating post trains

2000s High frequency trading: using powerful computers to transact trades ahead of other market players

1980s Ivan Boesky: arbitraging stocks based on insider information

2000s Alternative data: using big data to analyzecompany performance prior to official announcements

The Legal Risks of Alternative Data

As investors, we should be aware of the potential risks associated with alternative data

Conclusion - risk awareness

Prime Capital AGPage 10 October 2018

ManagersAmong the managers we spoke to, the more established ones already take legal risks into consideration while selecting and utilizing alternative data

InvestorsInvestors should be aware of the current legal grey zone/future legal risk while carrying out due diligence with managers who utilize alternative data

The Legal Risks of Alternative Data

Prime Capital AG | Hedge Fund Solutions

Page 1 | April 2016 | Strictly Confidential

The Legal Risks of Alternative Data

November 2018

Prime Capital AG | Hedge Fund Solutions

Page 2 | November 2018 | strictly confidential

Content

Executive Summary ................................................................................................................................................. 3

Background ............................................................................................................................................................. 4

What is Alternative Data? ........................................................................................................................................ 5

Legal Grey Zone ...................................................................................................................................................... 5

Concluding Remarks ............................................................................................................................................... 8

Contact and Disclaimer ........................................................................................................................................... 9

Prime Capital AG | Hedge Fund Solutions

Page 3 | September 2016 | Strictly confidential

Executive Summary This paper aims to discuss the potential legal risks of alternative data and to raise awareness among

investors about the issues which are currently in a legal grey zone and are potentially overlooked by many

market participants. The paper begins with a brief background of alternative data, before reviewing several

most prominent legal risks coupled with legal cases associated with alternative data and concludes with a

historical review showing that market players have always sought to gain an informational edge. All data

provided in this note are from Prime Capital AG if not stated otherwise.

Prime Capital AG | Hedge Fund Solutions

Page 4 | November 2018 | strictly confidential

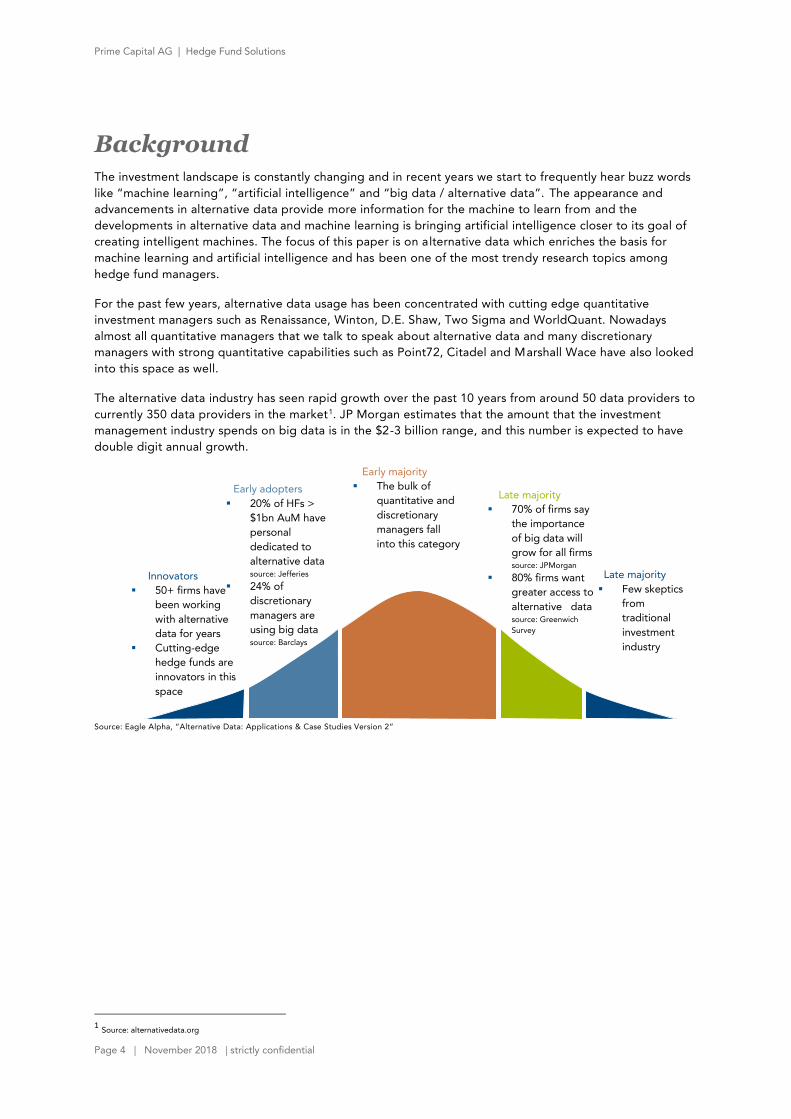

Background The investment landscape is constantly changing and in recent years we start to frequently hear buzz words

like “machine learning”, “artificial intelligence” and “big data / alternative data”. The appearance and

advancements in alternative data provide more information for the machine to learn from and the

developments in alternative data and machine learning is bringing artificial intelligence closer to its goal of

creating intelligent machines. The focus of this paper is on alternative data which enriches the basis for

machine learning and artificial intelligence and has been one of the most trendy research topics among

hedge fund managers.

For the past few years, alternative data usage has been concentrated with cutting edge quantitative

investment managers such as Renaissance, Winton, D.E. Shaw, Two Sigma and WorldQuant. Nowadays

almost all quantitative managers that we talk to speak about alternative data and many discretionary

managers with strong quantitative capabilities such as Point72, Citadel and Marshall Wace have also looked

into this space as well.

The alternative data industry has seen rapid growth over the past 10 years from around 50 data providers to

currently 350 data providers in the market1. JP Morgan estimates that the amount that the investment

management industry spends on big data is in the $2-3 billion range, and this number is expected to have

double digit annual growth.

Source: Eagle Alpha, “Alternative Data: Applications & Case Studies Version 2”

1 Source: alternativedata.org

Innovators

50+ firms have

been working

with alternative

data for years

Cutting-edge

hedge funds are

innovators in this

space

Early adopters

20% of HFs >

$1bn AuM have

personal

dedicated to

alternative data source: Jefferies

24% of

discretionary

managers are

using big data source: Barclays

Early majority

The bulk of

quantitative and

discretionary

managers fall

into this category

Late majority

70% of firms say

the importance

of big data will

grow for all firms source: JPMorgan

80% firms want

greater access to

alternative data source: Greenwich

Survey

Late majority

Few skeptics

from

traditional

investment

industry

Prime Capital AG | Hedge Fund Solutions

Page 5 | November 2018 | strictly confidential

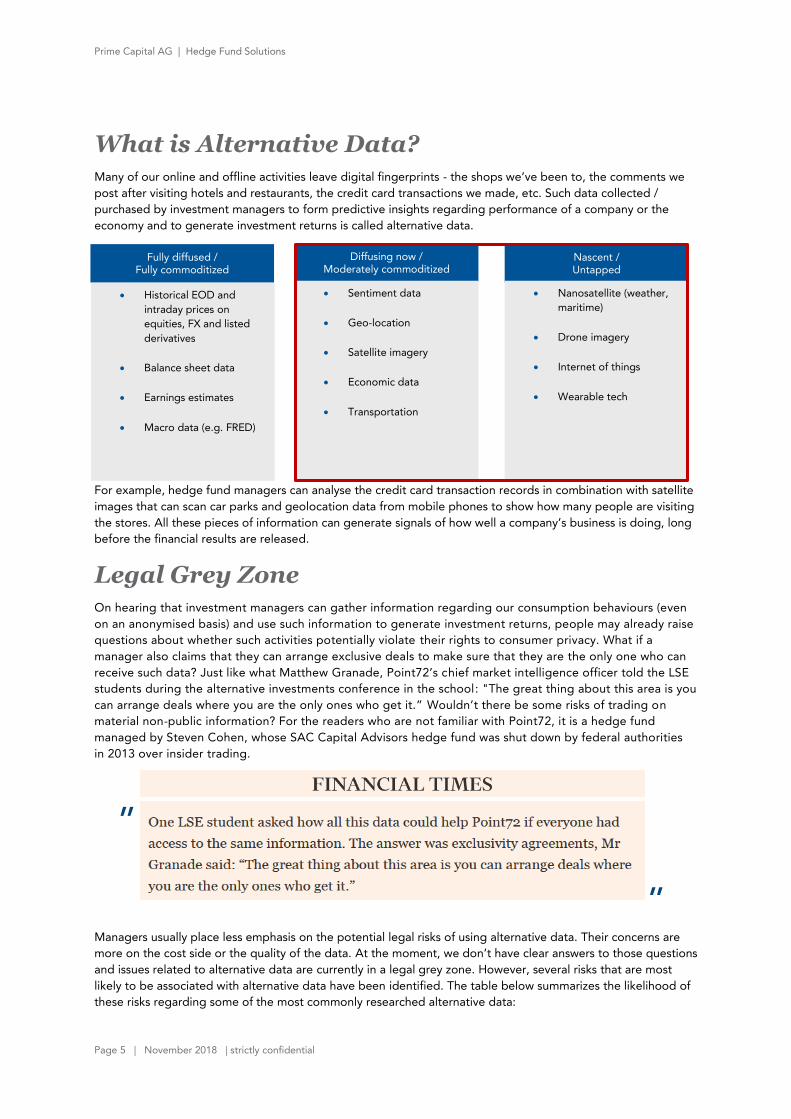

What is Alternative Data? Many of our online and offline activities leave digital fingerprints - the shops we’ve been to, the comments we

post after visiting hotels and restaurants, the credit card transactions we made, etc. Such data collected /

purchased by investment managers to form predictive insights regarding performance of a company or the

economy and to generate investment returns is called alternative data.

For example, hedge fund managers can analyse the credit card transaction records in combination with satellite

images that can scan car parks and geolocation data from mobile phones to show how many people are visiting

the stores. All these pieces of information can generate signals of how well a company’s business is doing, long

before the financial results are released.

Legal Grey Zone On hearing that investment managers can gather information regarding our consumption behaviours (even

on an anonymised basis) and use such information to generate investment returns, people may already raise

questions about whether such activities potentially violate their rights to consumer privacy. What if a

manager also claims that they can arrange exclusive deals to make sure that they are the only one who can

receive such data? Just like what Matthew Granade, Point72’s chief market intelligence officer told the LSE

students during the alternative investments conference in the school: "The great thing about this area is you

can arrange deals where you are the only ones who get it.” Wouldn’t there be some risks of trading on

material non-public information? For the readers who are not familiar with Point72, it is a hedge fund

managed by Steven Cohen, whose SAC Capital Advisors hedge fund was shut down by federal authorities

in 2013 over insider trading.

Managers usually place less emphasis on the potential legal risks of using alternative data. Their concerns are

more on the cost side or the quality of the data. At the moment, we don’t have clear answers to those questions

and issues related to alternative data are currently in a legal grey zone. However, several risks that are most

likely to be associated with alternative data have been identified. The table below summarizes the likelihood of

these risks regarding some of the most commonly researched alternative data:

Fully diffused / Fully commoditized

Historical EOD and

intraday prices on

equities, FX and listed

derivatives

Balance sheet data

Earnings estimates

Macro data (e.g. FRED)

Diffusing now / Moderately commoditized

Sentiment data

Geo-location

Satellite imagery

Economic data

Transportation

Nascent / Untapped

Nanosatellite (weather,

maritime)

Drone imagery

Internet of things

Wearable tech

’’

’’

Prime Capital AG | Hedge Fund Solutions

Page 6 | November 2018 | strictly confidential

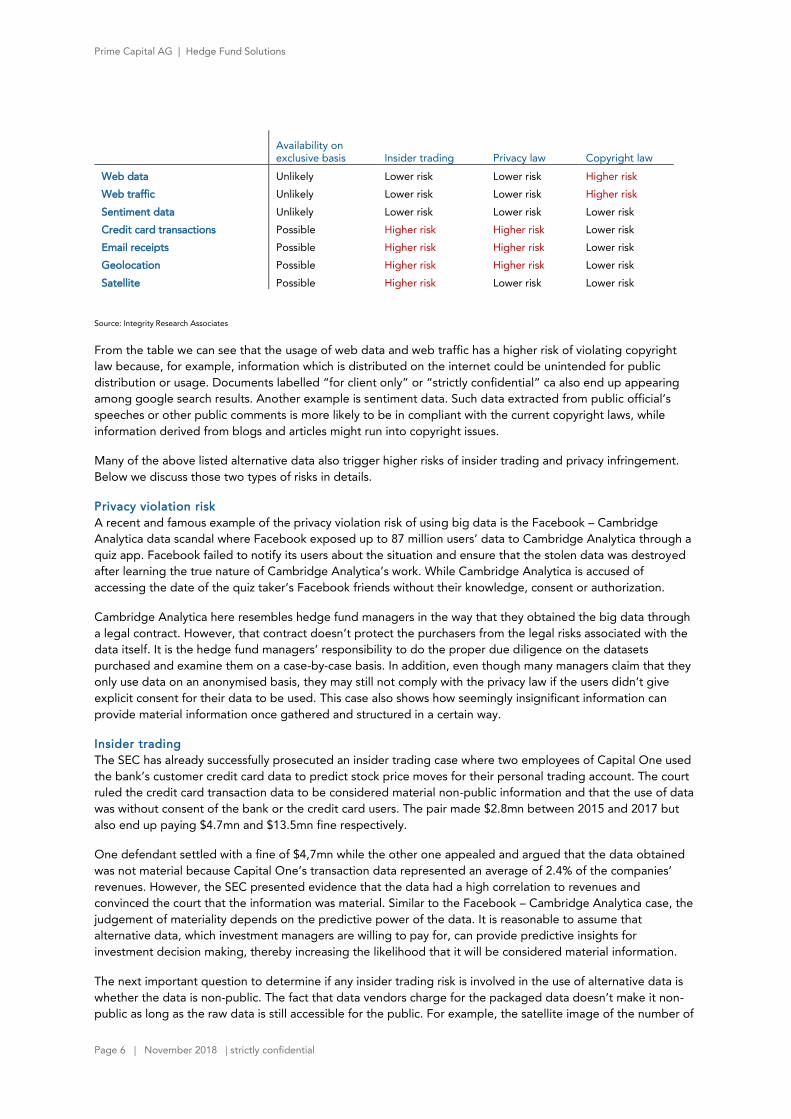

Availability on exclusive basis Insider trading Privacy law Copyright law

Web data Unlikely Lower risk Lower risk Higher risk

Web traffic Unlikely Lower risk Lower risk Higher risk

Sentiment data Unlikely Lower risk Lower risk Lower risk

Credit card transactions Possible Higher risk Higher risk Lower risk

Email receipts Possible Higher risk Higher risk Lower risk

Geolocation Possible Higher risk Higher risk Lower risk

Satellite Possible Higher risk Lower risk Lower risk

Source: Integrity Research Associates

From the table we can see that the usage of web data and web traffic has a higher risk of violating copyright

law because, for example, information which is distributed on the internet could be unintended for public

distribution or usage. Documents labelled “for client only” or “strictly confidential” ca also end up appearing

among google search results. Another example is sentiment data. Such data extracted from public official’s

speeches or other public comments is more likely to be in compliant with the current copyright laws, while

information derived from blogs and articles might run into copyright issues.

Many of the above listed alternative data also trigger higher risks of insider trading and privacy infringement.

Below we discuss those two types of risks in details.

Privacy violation risk A recent and famous example of the privacy violation risk of using big data is the Facebook – Cambridge

Analytica data scandal where Facebook exposed up to 87 million users’ data to Cambridge Analytica through a

quiz app. Facebook failed to notify its users about the situation and ensure that the stolen data was destroyed

after learning the true nature of Cambridge Analytica’s work. While Cambridge Analytica is accused of

accessing the date of the quiz taker’s Facebook friends without their knowledge, consent or authorization.

Cambridge Analytica here resembles hedge fund managers in the way that they obtained the big data through

a legal contract. However, that contract doesn’t protect the purchasers from the legal risks associated with the

data itself. It is the hedge fund managers’ responsibility to do the proper due diligence on the datasets

purchased and examine them on a case-by-case basis. In addition, even though many managers claim that they

only use data on an anonymised basis, they may still not comply with the privacy law if the users didn’t give

explicit consent for their data to be used. This case also shows how seemingly insignificant information can

provide material information once gathered and structured in a certain way.

Insider trading The SEC has already successfully prosecuted an insider trading case where two employees of Capital One used

the bank’s customer credit card data to predict stock price moves for their personal trading account. The court

ruled the credit card transaction data to be considered material non-public information and that the use of data

was without consent of the bank or the credit card users. The pair made $2.8mn between 2015 and 2017 but

also end up paying $4.7mn and $13.5mn fine respectively.

One defendant settled with a fine of $4,7mn while the other one appealed and argued that the data obtained

was not material because Capital One’s transaction data represented an average of 2.4% of the companies’

revenues. However, the SEC presented evidence that the data had a high correlation to revenues and

convinced the court that the information was material. Similar to the Facebook – Cambridge Analytica case, the

judgement of materiality depends on the predictive power of the data. It is reasonable to assume that

alternative data, which investment managers are willing to pay for, can provide predictive insights for

investment decision making, thereby increasing the likelihood that it will be considered material information.

The next important question to determine if any insider trading risk is involved in the use of alternative data is

whether the data is non-public. The fact that data vendors charge for the packaged data doesn’t make it non-

public as long as the raw data is still accessible for the public. For example, the satellite image of the number of

Prime Capital AG | Hedge Fund Solutions

Page 7 | November 2018 | strictly confidential

cars parked outside a supermarket is public data because one can always go to the parking lot and count how

many cars are parked there. However, availability of data on an exclusive basis potentially heightens the risk of

insider trading by making the information not accessible to the general public.

Prime Capital AG | Hedge Fund Solutions

Page 8 | November 2018 | strictly confidential

Concluding Remarks Throughout the history of finance, people have always sought to gain access to information faster than the

other market participants so as to trade ahead of them. Beginning with the famous story of Nathan Rothschild

trading on the waterloo victory before Wellington’s envoy delivered the news, and then again where Paul

Reuter transferred financial news using pigeons which were faster than the post trains. Then in the 80s we had

Ivan Boesky arbitraging stocks based on insider information and in 2000s where people started to utilize high

frequency trading and alternative data to gain an informational edge in the market competitions.

In this pursuit of gaining a leg up in the market, some engaged in taking advantage of technological advances

while some employed means that were ex-post proven to be illegal. In the cases of the illegal practices, there

has always been a gap between these practices and the regulations that are set in place. Though there are

currently no clear rules or regulations to define the legal risks regarding alternative data and some managers

might put less emphasis on it or overlook the potential legal risks here, but we feel that investors should have

the awareness of this issue and take it into consideration in the due diligence process.

Prime Capital AG | Hedge Fund Solutions

Page 9 | November 2018 | strictly confidential

Contact and Disclaimer

Prime Capital AG

Bockenheimer Landstr. 51-53

60325 Frankfurt am Main

GERMANY

Tel: +49 (0)69 9686 984 0

Fax: +49 (0)69 9686 984 61

21, rue Philippe II

L-2340 Luxemburg

LUXEMBURG

Tel: +352 278 610 84

Fax: +352 278 612 95

Internet: www.primecapital-ag.com

This document is issued and approved by Prime Capital AG, Frankfurt. This information is intended solely for the use of

the person to whom it is given and may not be reproduced or given to any other person. It is not an offer or solicitation

to subscribe for shares in any fund and is by way of information only. Please note that the price of shares and the income

from any fund may go down as well as up and may be affected by the changes in rates of exchange. Past performance is

not indicative of future performance. An investor may not get back the amount invested.

Source of data: Prime Capital AG.

Seite Seite Ausschließlich zur Information für "Professionelle Kunden" und "Geeignete Gegenparteien" gemäß §31a Abs. 2 und 4 WpHG. © 2017 Privat & vertraulich.

Tungsten Capital Management GmbH, Hochstraße 35 – 37, 60313 Frankfurt, Germany. Tungsten Capital Management GmbH verfügt über die erforderliche Erlaubnis derBundesanstalt für Finanzdienstleistungsaufsicht ("BaFin") und unterliegt deren Aufsicht.

Gewinnbringende Strategien in turbulenten Märkten

Frankfurt am Main 23.10.2018

Seite Seite

Disclaimer

Dieses Dokument richtet sich ausschließlich an Kunden der Kundengruppe „Professionelle Kunden“ gem. § 31 a Abs. 2 WpHG und/oder „Geeignete Gegenparteien“ gem. § 31 a Abs. 4 WpHG und ist nicht für

Privatkunden bestimmt. Die Verteilung an Privatkunden ist nicht beabsichtigt. Es dient ausschließlich Informationszwecken und stellt keine Finanzanalyse im Sinne des §34b WpHG, keine Anlageberatung,

Anlageempfehlung oder Aufforderung zum Kauf oder Verkauf von Finanzinstrumenten dar. Historische Wertentwicklungen lassen keine Rückschlüsse auf ähnliche Entwicklungen in der Zukunft zu. Diese sind

nicht prognostizierbar. Alleinige Grundlage für den Anteilerwerb sind die Verkaufsunterlagen zum Sondervermögen. Verkaufsunterlagen zu allen Sondervermögen der Universal-Investment sind kostenlos bei

Ihrem Berater / Vermittler der zuständigen Depotbank oder bei Universal-Investment unter www.universal-investment.de erhältlich. Alle angegebenen Daten sind vorbehaltlich der Prüfung durch die

Wirtschaftsprüfer zu den jeweiligen Berichtsterminen. Die Ausführungen gehen von unserer Beurteilung der gegenwärtigen Rechts- und Steuerlage aus. Für die Richtigkeit der hier angegebenen Informationen

übernimmt Tungsten Capital Management keine Gewähr. Änderungen vorbehalten. Quellen: Bloomberg, eigene Berechnungen.

Wertentwicklungen der Vergangenheit sind kein verlässlicher Indikator für die künftige Wertentwicklung.

Stand: 31. Januar 2018

Ausschließlich zur Information für "Professionelle Kunden" und "Geeignete Gegenparteien" gemäß §31a Abs. 2 und 4 WpHG.2

Gewinnbringende Strategien in turbulenten Märkten

Seite Seite

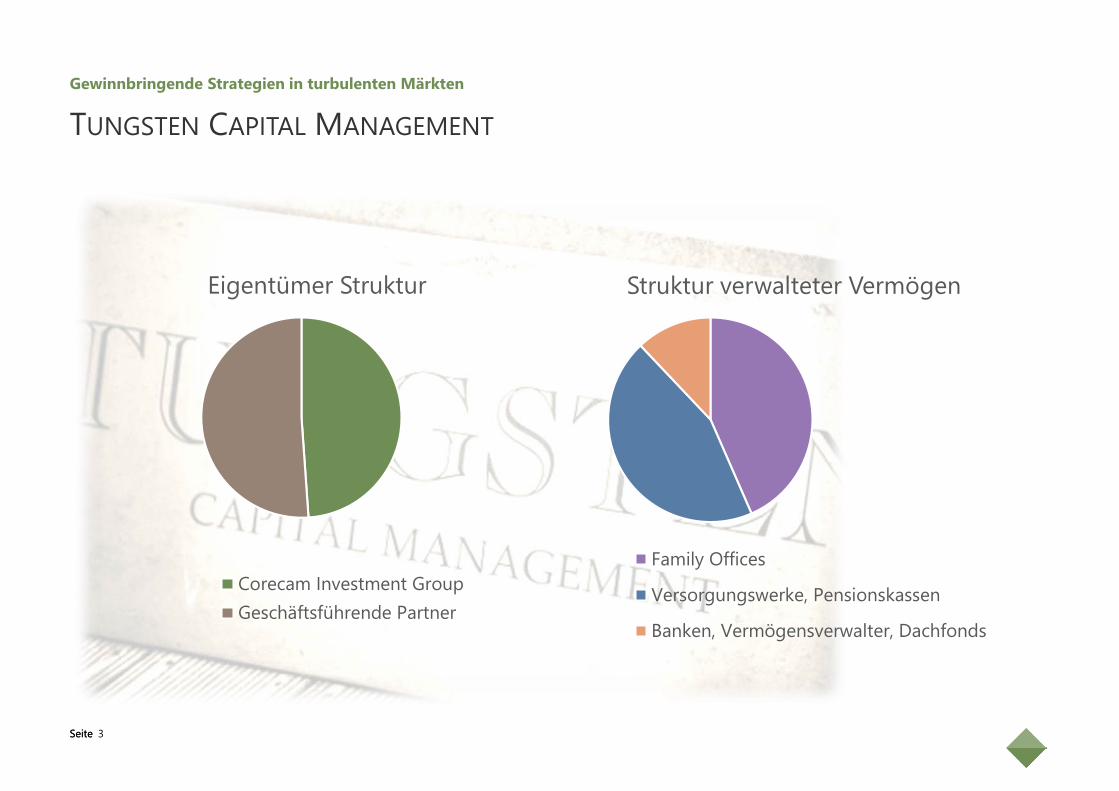

TUNGSTEN CAPITAL MANAGEMENT

3

Eigentümer Struktur

Corecam Investment GroupGeschäftsführende Partner

Struktur verwalteter Vermögen

Family Offices

Versorgungswerke, Pensionskassen

Banken, Vermögensverwalter, Dachfonds

Gewinnbringende Strategien in turbulenten Märkten

Seite Seite

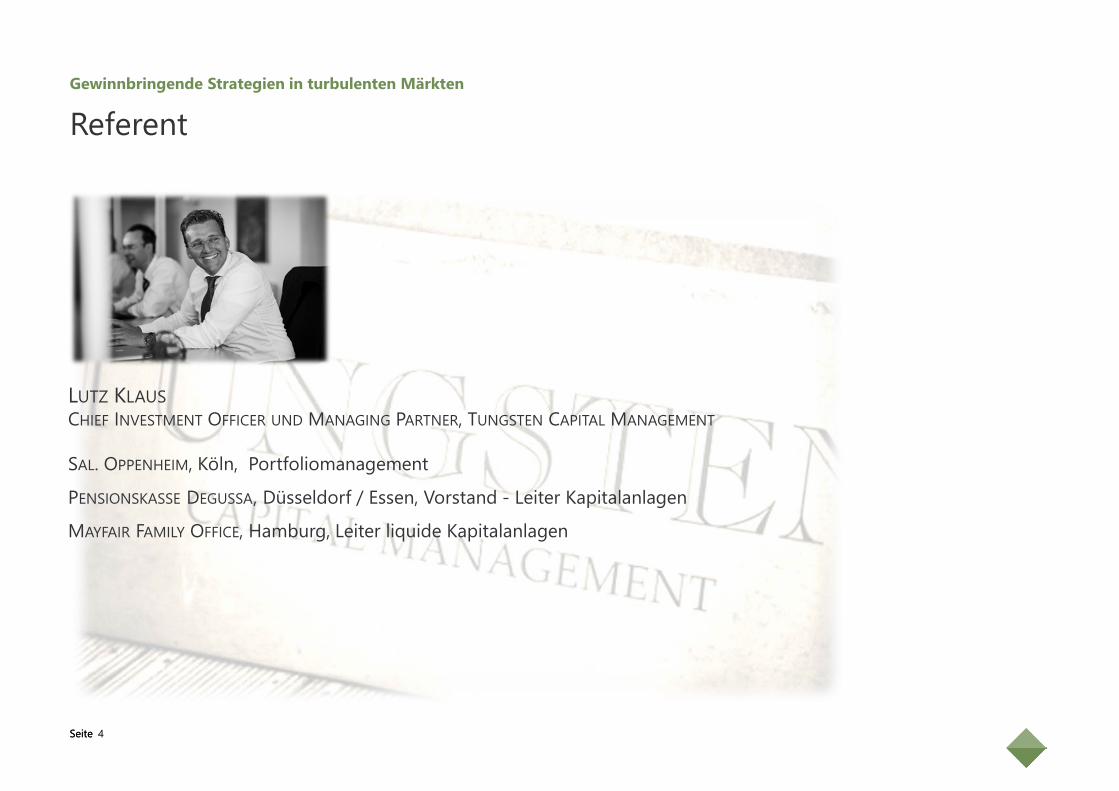

Referent

LUTZ KLAUSCHIEF INVESTMENT OFFICER UND MANAGING PARTNER, TUNGSTEN CAPITAL MANAGEMENT

SAL. OPPENHEIM, Köln, Portfoliomanagement

PENSIONSKASSE DEGUSSA, Düsseldorf / Essen, Vorstand - Leiter Kapitalanlagen

MAYFAIR FAMILY OFFICE, Hamburg, Leiter liquide Kapitalanlagen

4

Gewinnbringende Strategien in turbulenten Märkten

Seite Seite 5

Gewinnbringende Strategien in turbulenten Märkten

Seite Seite

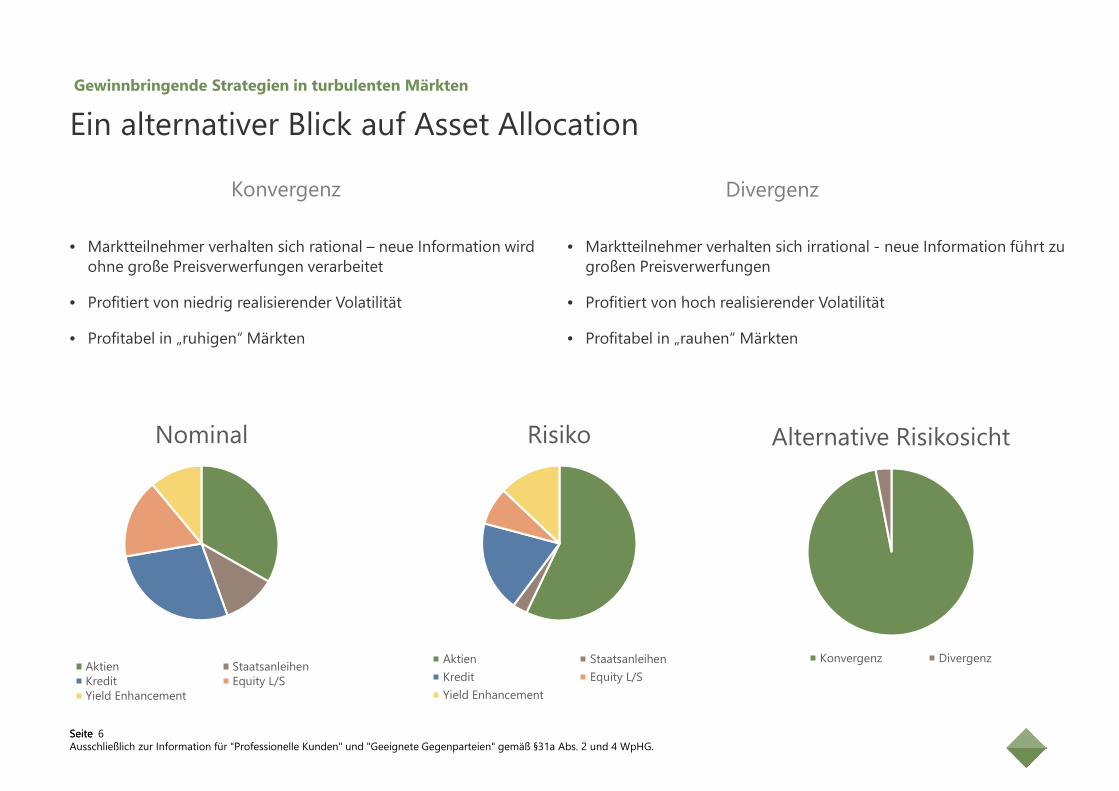

Ein alternativer Blick auf Asset AllocationGewinnbringende Strategien in turbulenten Märkten

Ausschließlich zur Information für "Professionelle Kunden" und "Geeignete Gegenparteien" gemäß §31a Abs. 2 und 4 WpHG.6

Konvergenz Divergenz

• Marktteilnehmer verhalten sich rational – neue Information wird ohne große Preisverwerfungen verarbeitet

• Profitiert von niedrig realisierender Volatilität

• Profitabel in „ruhigen“ Märkten

• Marktteilnehmer verhalten sich irrational - neue Information führt zu großen Preisverwerfungen

• Profitiert von hoch realisierender Volatilität

• Profitabel in „rauhen“ Märkten

Nominal

Aktien StaatsanleihenKredit Equity L/SYield Enhancement

Risiko

Aktien StaatsanleihenKredit Equity L/SYield Enhancement

Alternative Risikosicht

Konvergenz Divergenz

Seite Seite

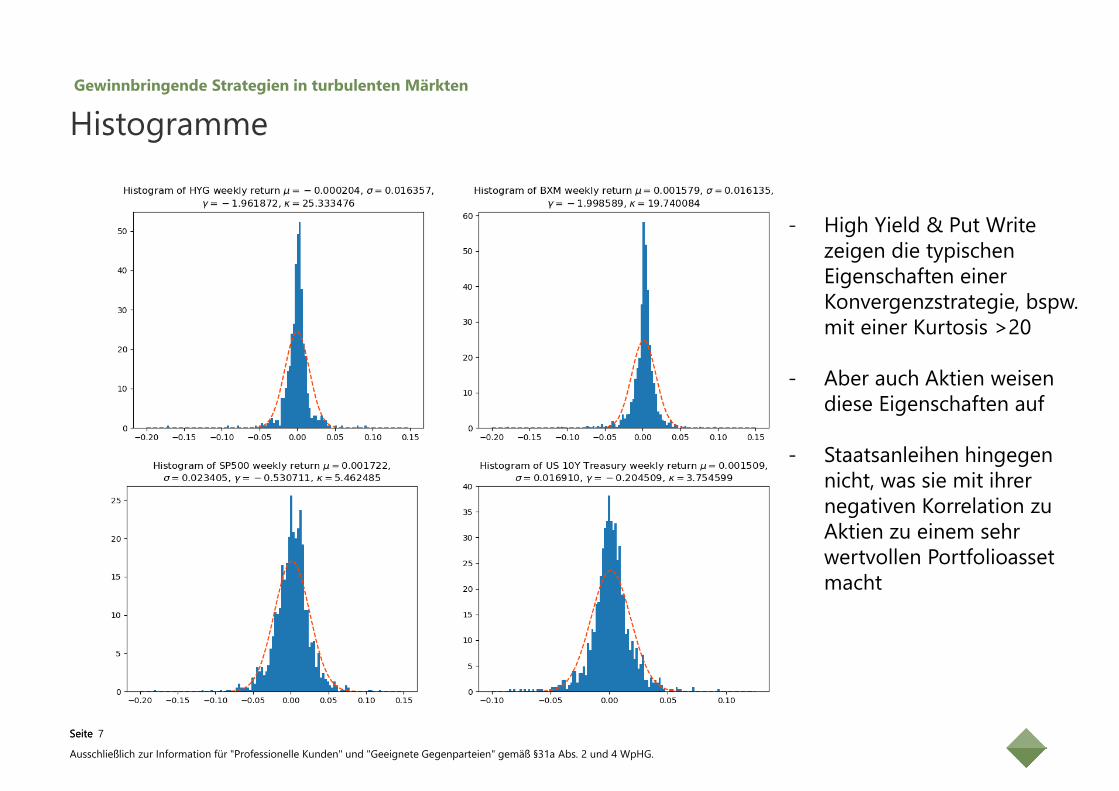

Histogramme

7

Gewinnbringende Strategien in turbulenten Märkten

- High Yield & Put Write zeigen die typischen Eigenschaften einer Konvergenzstrategie, bspw. mit einer Kurtosis >20

- Aber auch Aktien weisen diese Eigenschaften auf

- Staatsanleihen hingegen nicht, was sie mit ihrer negativen Korrelation zu Aktien zu einem sehr wertvollen Portfolioassetmacht

Ausschließlich zur Information für "Professionelle Kunden" und "Geeignete Gegenparteien" gemäß §31a Abs. 2 und 4 WpHG.

Seite Seite

Was kann man tun?

I. Reduktion aggressiver Carry Strategien

Gerade in diesen Strategien erhält man eine attraktive Vergütung für das eingegangene Risiko

II. Kauf von Staatsanleihen mit langer Laufzeit

Einziges long-only Asset mit Divergenz Eigenschaften und positiver Ertragserwartung

III. Tail Risk Hedging

Short Volatility wahrscheinlich attraktivste Risikoprämie am Kapitalmarkt – Wirklich dagegen stellen?

IV. Long Vol-biased Strategies

CTAs, Global Macro und long-biased Volatility Trading – profitieren von hoch realisierender Vol

Ausschließlich zur Information für "Professionelle Kunden" und "Geeignete Gegenparteien" gemäß §31a Abs. 2 und 4 WpHG.8

Gewinnbringende Strategien in turbulenten Märkten

Seite Seite

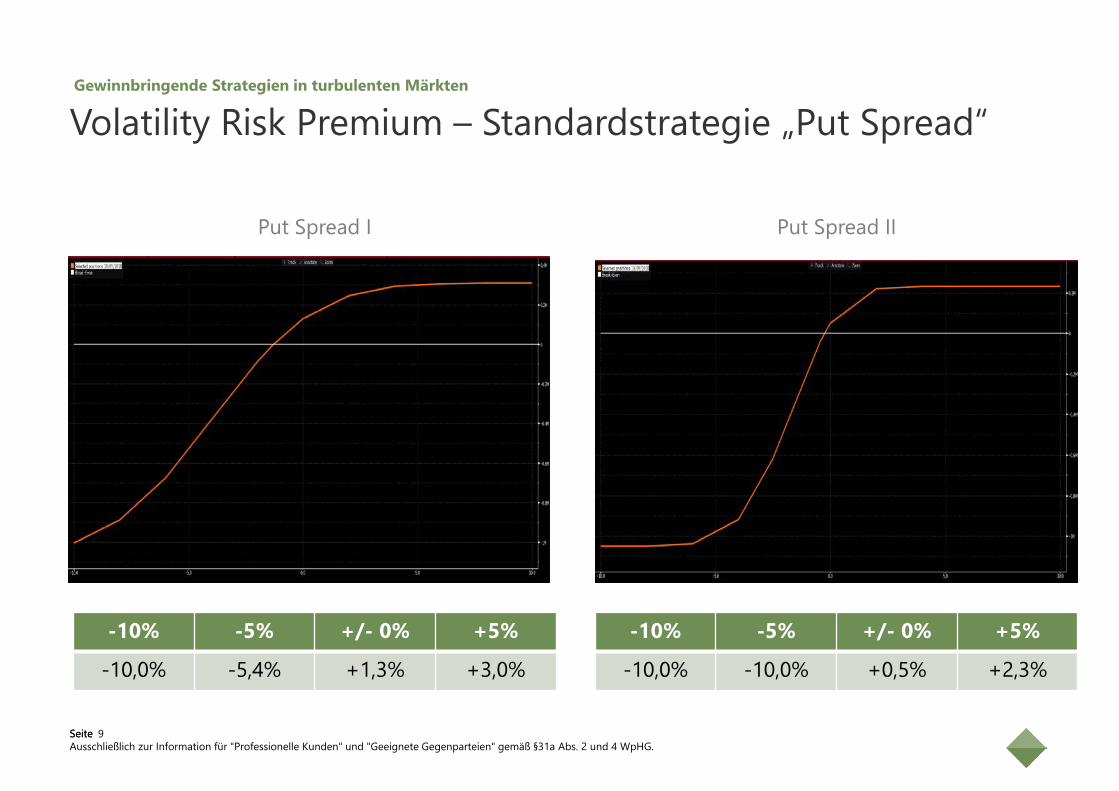

Volatility Risk Premium – Standardstrategie „Put Spread“

Ausschließlich zur Information für "Professionelle Kunden" und "Geeignete Gegenparteien" gemäß §31a Abs. 2 und 4 WpHG.9

Gewinnbringende Strategien in turbulenten Märkten

Put Spread I

-10% -5% +/- 0% +5%

-10,0% -5,4% +1,3% +3,0%

Put Spread II

-10% -5% +/- 0% +5%

-10,0% -10,0% +0,5% +2,3%

Seite Seite

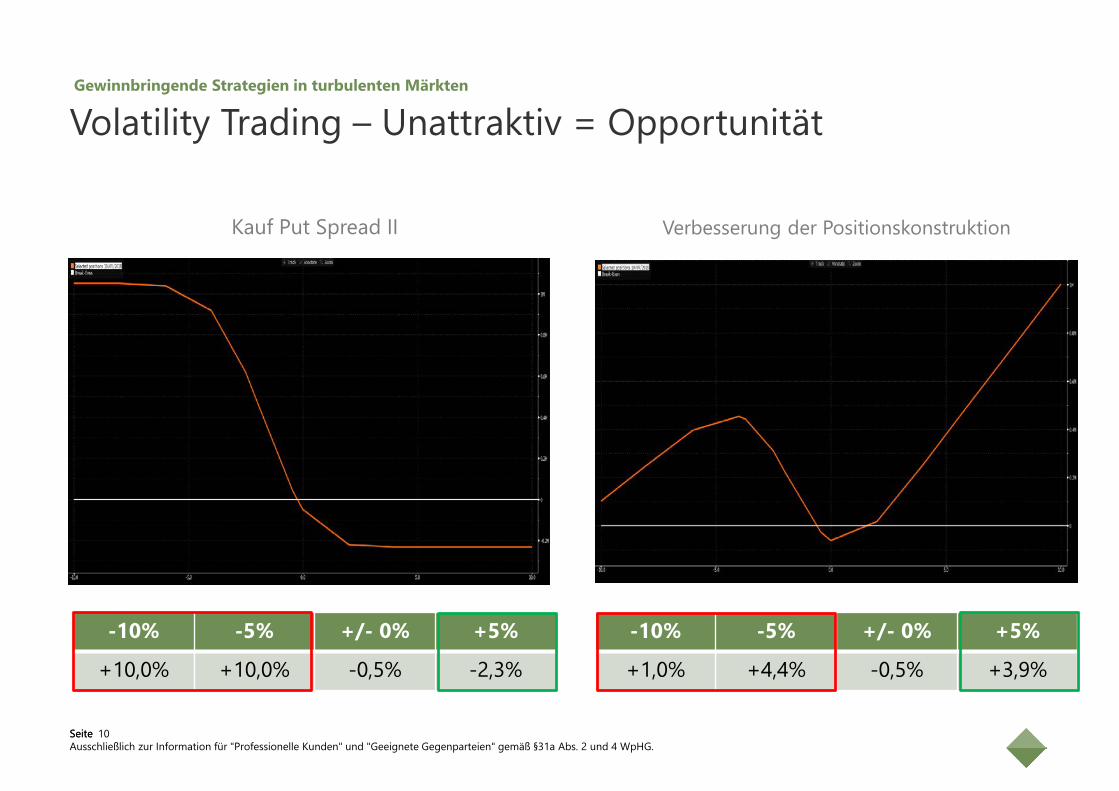

Volatility Trading – Unattraktiv = Opportunität

Ausschließlich zur Information für "Professionelle Kunden" und "Geeignete Gegenparteien" gemäß §31a Abs. 2 und 4 WpHG.10

Gewinnbringende Strategien in turbulenten Märkten

Kauf Put Spread II

-10% -5% +/- 0% +5%

+10,0% +10,0% -0,5% -2,3%

Verbesserung der Positionskonstruktion

-10% -5% +/- 0% +5%

+1,0% +4,4% -0,5% +3,9%

Seite Seite

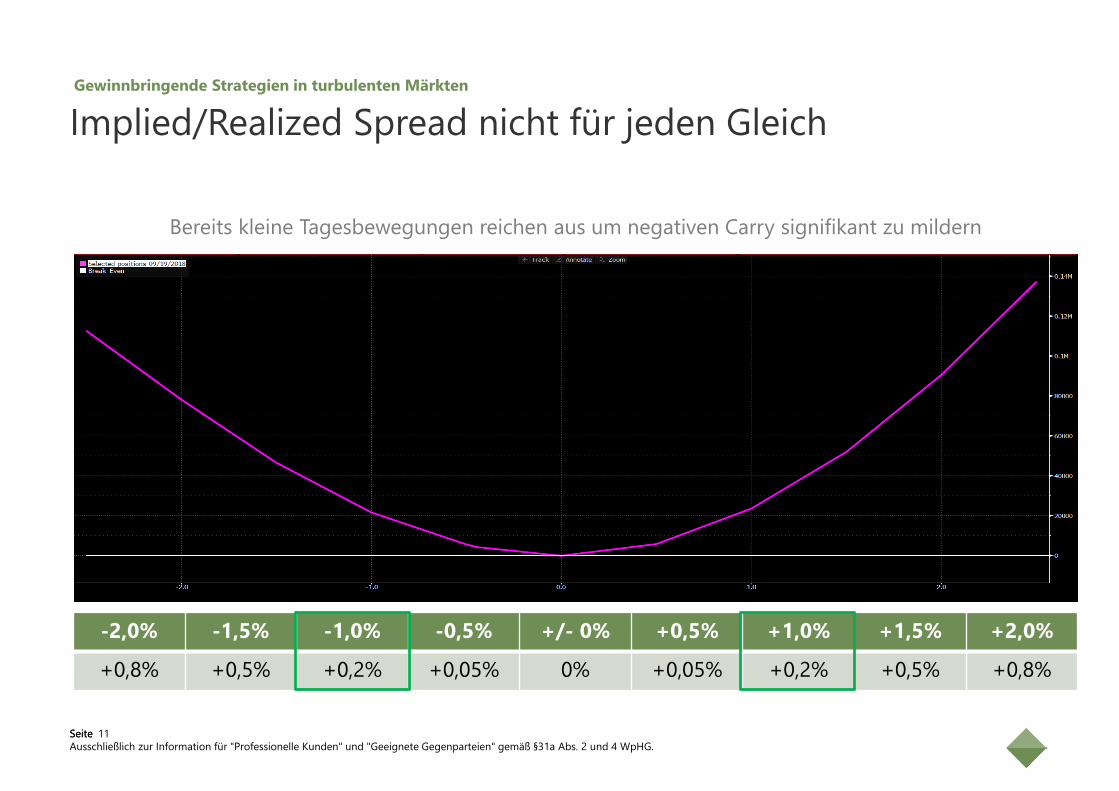

Implied/Realized Spread nicht für jeden Gleich

Ausschließlich zur Information für "Professionelle Kunden" und "Geeignete Gegenparteien" gemäß §31a Abs. 2 und 4 WpHG.11

Gewinnbringende Strategien in turbulenten Märkten

-2,0% -1,5% -1,0% -0,5% +/- 0% +0,5% +1,0% +1,5% +2,0%

+0,8% +0,5% +0,2% +0,05% 0% +0,05% +0,2% +0,5% +0,8%

Bereits kleine Tagesbewegungen reichen aus um negativen Carry signifikant zu mildern

Seite Seite

Volatility Trading Cross Asset – Fixed Income Future

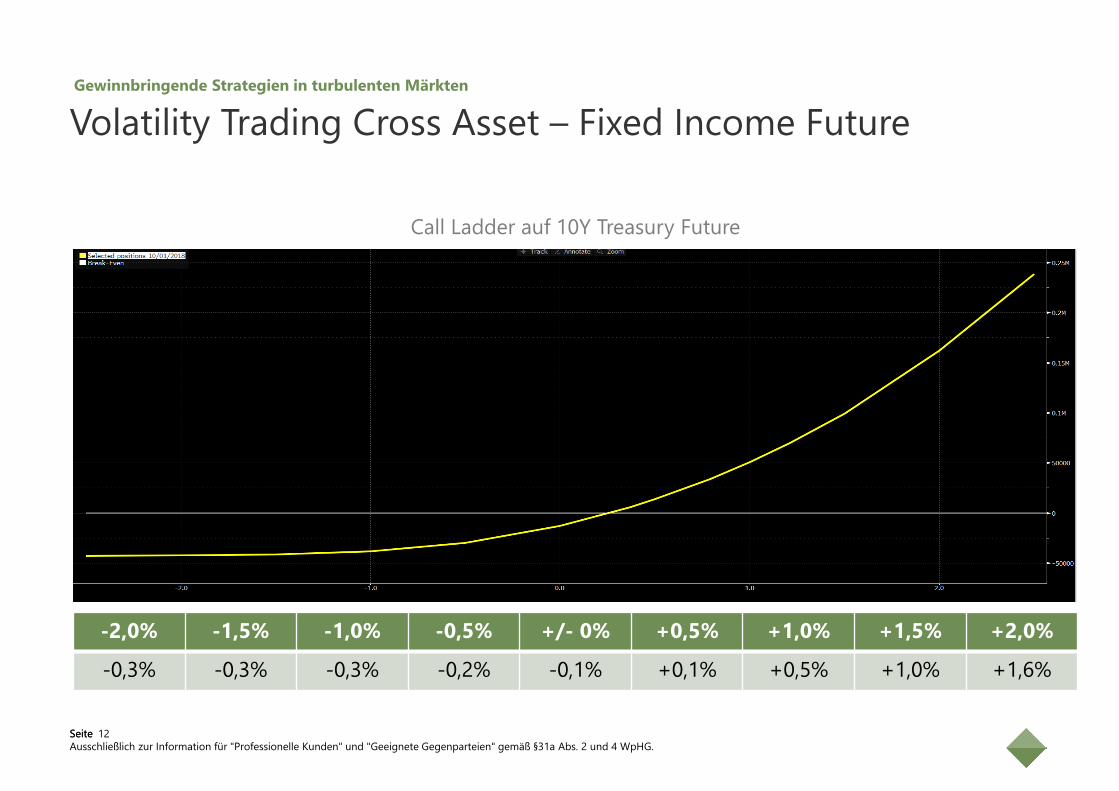

Ausschließlich zur Information für "Professionelle Kunden" und "Geeignete Gegenparteien" gemäß §31a Abs. 2 und 4 WpHG.12

Gewinnbringende Strategien in turbulenten Märkten

-2,0% -1,5% -1,0% -0,5% +/- 0% +0,5% +1,0% +1,5% +2,0%

-0,3% -0,3% -0,3% -0,2% -0,1% +0,1% +0,5% +1,0% +1,6%

Call Ladder auf 10Y Treasury Future

Seite Seite

Zusammenfassung

Ausschließlich zur Information für "Professionelle Kunden" und "Geeignete Gegenparteien" gemäß §31a Abs. 2 und 4 WpHG.

Long-biased Volatility Trading bietet eine Alternative

Es gibt eine hohe Anzahl an Einzelstrategien im Volatilitätsmarkt, jedoch funktioniert keine in jeder Marktphase

Risikoprämie aus Volatilität wahrscheinlich attraktivste strukturelle Prämie am Markt

Systematisch, passives long Exposure zu Volatilität als Hedge extrem teuer

Investmentportfolios sollen eine Risikoprämie verdienen

Hohe Allokation zu Konvergenz Strategien sinnvoll

13

Gewinnbringende Strategien in turbulenten Märkten

Aktives Management ist der Schlüssel zur Reduktion des negativen Carry

Manager die alle Strategien beherrschen und richtig einsetzen schaffen einen hohen Mehrwert