Agua Caliente Band of Mission Indians v. Cnty. of...

53

Agua Caliente Band of Mission Indians v. Cnty. of Riverside

Transcript of Agua Caliente Band of Mission Indians v. Cnty. of...

Agua Caliente Band of Mission

Indians v. Cnty. of Riverside

•

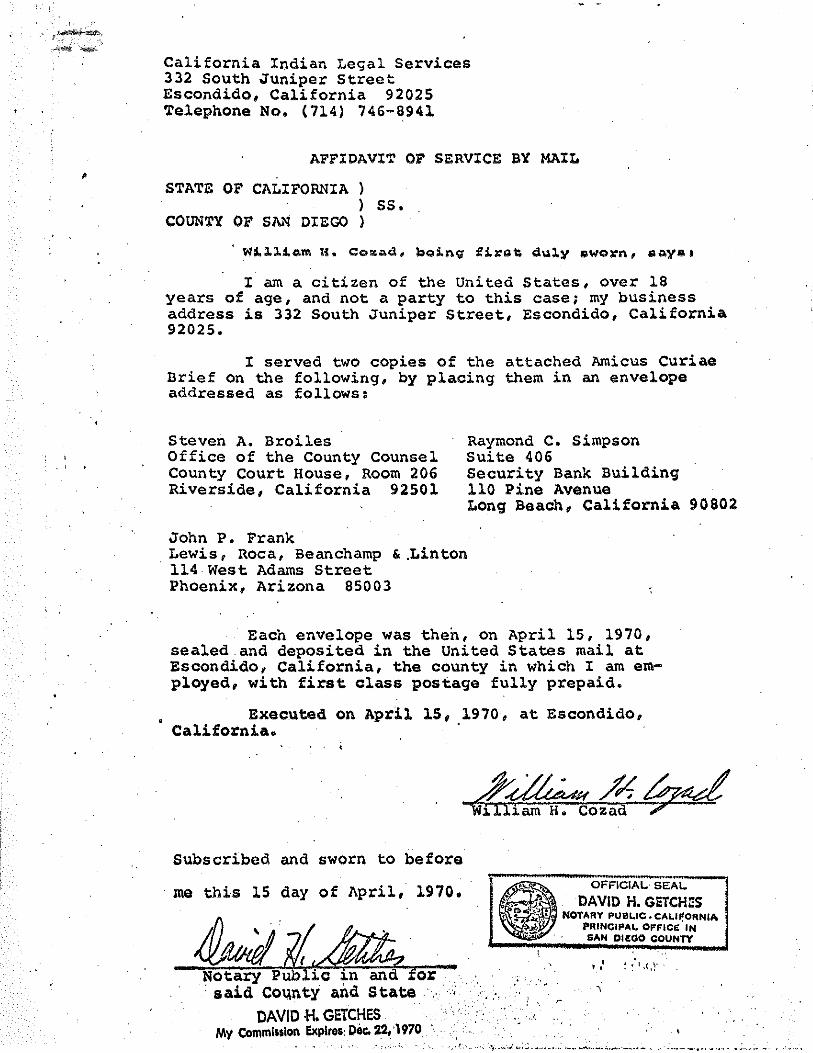

California Indian Legal Services 332 South Juniper Street Escondido, California 92025 Telephone No. (714) 746-8941

AFFIDAVIT OF SERVICE BY MAIL

STATE OF CALIFORNIA ) ) SSe

COUNTY OF SAi'! DIEGO l

I am a citizen of the United States, over 18 years of age, and not a party to this case; my business address is 332 South Juniper Street, Escondido, California 92025.

I served two copies of the attached Amicus Curiae Brief on the following, by placing them in an envelope addressed as follows:

Steven A. Broiles Office of the County Counsel County Court House, Room 206 Riverside, California 92501

John P. Frank

Raymond C. Simpson Suite 406 Security Bank Building 110 Pine Avenue Long Beach, California 90802

Lewis, Roca, Beanchamp &.Linton 114· West Adams Street Phoenix, Arizona 85003

Each envelope was then, on April 15, 1970, sealed and deposited in the United States mail at Escondido, California, the county in which I am employed, with first class postage fully prepaid.

Executed on April 15, .1970, at Escondido, California.

Subscribed and sworn to before

. me this lS day of April, 1970.

vt.~HA~ iiam H. Cozad

.< , •

" " ,.~

r

OFFICIAL SEAL

DAVID H. GETCH!:S NOTARY PUBL-Ie ~ CALIF,ORNIA

PRINCIPAL OFFICE IN SAN DIEOO COUNTY

'. " : ~ 1 ,( ,~'

;

..

•

, \

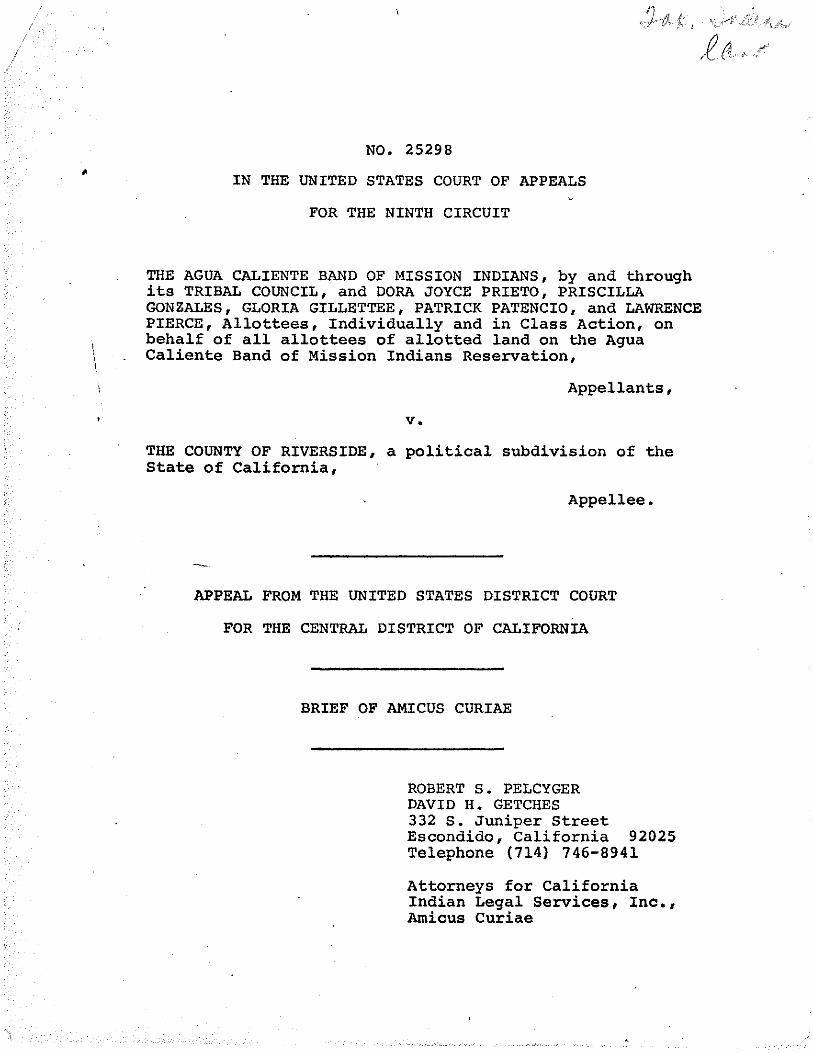

NO. 25298

IN THE UNITED STATES COURT OF APPEALS

FOR THE NINTH CIRCUIT

THE AGUA CALIENTE BAND OF MISSION INDIANS, by and through its TRIBAL COUNCIL, and DORA JOYCE PRIETO, PRISCILLA GONZALES, GLORIA GILLETTEE, PATRICK PATENCIO, and LAWRENCE PIERCE, Allottees, Individually and in Class Action, on behalf of all allottees of allotted land on the Agua Caliente Band of Mission Indians Reservation,

Appellants,

v.

THE COUNTY OF RIVERSIDE, a political subdivision of the State of California,

Appellee.

APPEAL FROM THE UNITED STATES DISTRICT COURT

FOR THE CENTRAL DISTRICT OF CALIFORNIA

BRIEF OF AMICUS CURIAE

ROBERT S. PELCYGER DAVID H. GETCHES 332 S. Juniper Street Escondido, California 92025 Telephone (714) 746-8941

Attorneys for California Indian Legal Services, Inc., Amicus Curiae

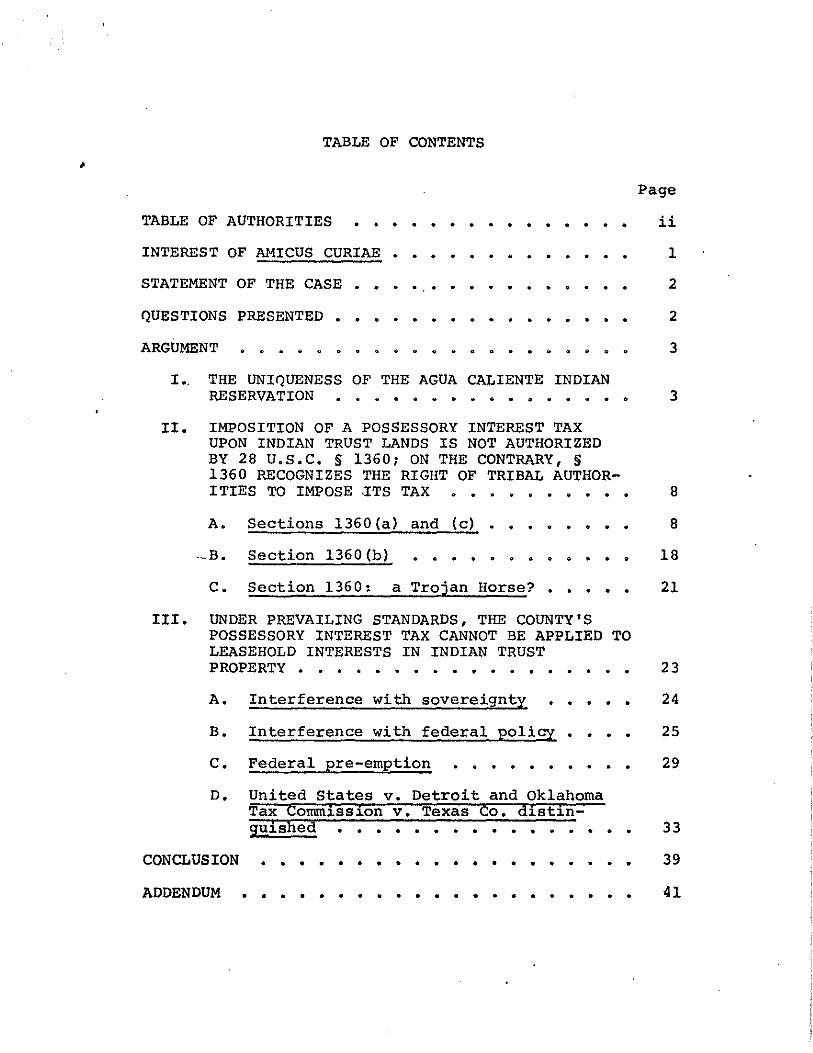

• TABLE OF CONTENTS

TABLE OF AUTHORITIES • • • • • • • • • • • • • • •

INTEREST OF AMICUS CURIAE · • · · • • · · STATEMENT OF THE CASE • . • • • · •

QUESTIONS PRESENTED • • • · • • • • • •

ARGUMENT . • . • . • • • • • • • • •

I •. THE UNIQUENESS OF THE AGUA CALIENTE INDIAN RESERVATION · . • • · • · • · • · · • •

II. IMPOSITION OF A POSSESSORY INTEREST TAX UPON INDIAN TRUST LANDS IS NOT AUTHORIZED BY 28 U.s.C. § 13601 ON THE CONTRARY, § 1360 RECOGNIZES THE RIGHT OF TRIBAL AUTHOR-

· •

•

•

•

Page

ii

1

2

2

3

3

ITIES TO IMPOSE ·ITS TAX • • • • • •• 8

III.

A. Sections 1360(a) and (c) • • • • • • •

·_B. Section 1360 (b) • • " 9 · " . . . .

C. Section 1360: a Trojan Horse? · . . . UNDER PREVAILING STANDARDS, THE COUNTY'S POSSESSORY INTEREST TAX CANNOT BE APPLIED TO LEASEHOLD INTERESTS IN INDIAN TRUST PROPERTY • • • • • • • • • • • • • • • •. •

A. Interference with sovereignty • • •

B. Interference with federal policy • • •

C. Federal pre-emption · . . . . . · . . D. United States v. Detroit and Oklahoma

Tax Commission v. Texas Co. distin-

8

18

21

23

24

25

29

guished • • • • • • • • • • • • • • •• 33

CONCLUSION

ADDENDUM

• • • • • • • • • • • • • • • • • • • •

• • • • • • • • • • • • • • • • • • • •

39

41

28 U.S.C. § 1360 • • • • • • • • • • • • • 3,8,9,12,

• 15,20,21,22, 33,34,39

28 U.S.C. § 1360 (a) • • • • • • • • • • • • 8, 10, 18, 21, 39

28 U.S.C. § 1360 (b) · · • • • • • • • · • 9, 10, 11, 14, 17, 18, 19, 20, 39

28 U.S.C. § 1360(0) • • • • · • • • • • · 8, 9, 10, 17, 18, 39

42 U.S.C. §§ 2001 et seq. • • · • · • • • • 32

Act of January 12, 1891 (Mission Indian Relief Act) (26 Stat. 712) • · · · · • • • · 3, 31

Public Law 280, 67 Stat 589 (August 15, 9, 21, 1953) • • • • • • • 22, 23

Public Law 322, 63 Stat 705 • • • · • • • • 21

_ Public Law 8:6,.326,73 Stat 597 (September 21, 1959)

• ~ • · • · • · • • 30

Public Law 86-505, § 2, 74 Stat 199 (June 11, 1960) • • • • · • · . . • • • 30

Public Law 87-375, 75 Stat 804 (October 4, 1961) • • • • • • • • • • · 30

Public Law 87-785, 76 Stat 8115 (October 10, 1962) • · • · • · • • • · • 30

Public Law 88-167, 77 Stat 301 (November 4, 1963) · • • · • • • • • • • 30

Public Law 89-408, 80 Stat 132 (April 27, 1966) • • • • • • • · • • 30

Public Law 90-182, 81 Stat 559 (December 8, 1967) • • • .. . • • • • • • 30

iii

• Public Law 90-184, 81 Stat. 560 (December

10, 1967)

Public Law 90-335, § l(f), 82 Stat. 175

• • •

(June 10, 1968) • • • • • • • • • • • • •

Public Law 90-355, 82 Stat. 242 (June 20, 1968) • lIP ••••••••

Public Law 90-534, § 6, 82 Stat. 884 (September 28, 1968) ••••••••

· . . . . · . . . .

Public Law 90-570, 82 Stat. 1003 (October 12, 1968) •••••• • • •

o • • • • • • • • • • •

30

30

30

30

30

13 60 Stat. 237, § 4

25 C.F.R. Part 131 Col • • • • Col 110 III eo • • I). 29

30 F. R. 8172 (June 22, 1965). • • • • • • •

30 F.R. 8722 (July 2, 1965) • o • .. • Q •

33 F.R. 17339 (November 21, 1968) • • • • • 0

California

California Civil Code §

California Government Code §

California Government Code §

California Government Code §

California Government Code §§

1114

38660

65850

29088

29100-29102

• •

.. It .. •

. . . "

California Health & Safety Code § 1901.2

California Health & Safety Code § 1920

California Health & Safety Code § 17922

California Health & Safety Code § 17951

iv

· . • •

• • •

• •

13, 14

13

2

18

17

17

16

16

15

15, 17

17

17

• California Revenue & Taxation Code § 102 •

California Revenue & Taxation Code 5 107 •

California Revenue & Taxation Code § 128 •

• •

• •

• •

California Revenue & Taxation Code S 401 • • •

California Revenue & Taxation Code § 1603 • •

California Revenue & Taxation Code § 2151 · . California Revenue & Taxation Code § 2914 • •

Ordinance of San Diego County No. 3444 • • · .

17

15

16

16

16

16

34

15

Proposed Legislation

H. R. 12589, 91st Congress (1969) 33

Hearings

Cases

Hearings before the House Subcommittee on

Appropriations for the Department of the

"- Interior and Related Agencies for Fiscal

Year 1969. "~"."" •• <iI.O ••••• 27

Alabama v. King & Boozer, 314 U.S. 1 (1941).. 35

Alaska Pacific Fisheries v. United States, 248 U.S. 78 (1918) • • • • • • • • • • • • • • 21

Beecher v. Wetherby, 95 U.S. 517 (1877). • •• 7

Buster v. Wright, 135 Fed. 947 (8th Cir. 1905), appeal dismissed 203 U.S. 599 (1906) • • • •• 11

Cherokee Nation v. Georgia,S Pet. (U.S.) 1 (1831) .. .. .. .. .. .. .. .. .... ...... 9

Choate v. Trapp, 224 U.S. 665 (1912) • • • •• 21, 36

Commissioner of Taxation v. Brun, Minn., 174 N.W.2d 120 (1970), .: ••••• --:-:- :-:-.-:- 25, 38

v

• county of San Bernardino v. La Mar, 271 A.C.A. 821, 76 Cal.Rptr. 547 (1969).

Evans v. Faught, 231 Cal.App.2d 698, 42 Cal.Rptr. 133 (1965) ••••••• • •

Fraser v. Bentel, 161 Cal. 390, 119 Pac.

· . . 14, 16

· . . 19

509 (1911) • • • • • • • • • • 19

Graves v. New York, 306 U.S. 466 (1939). • •

Hopkins v. United States, 414 F.2d 464 (9th Cir. 1969) •••••••• o 0 • Go

35

2

Iron Crow v. Oglala Sioux Tribe of Pine Ridge Reservation, 231 F.2d 89 (8th cir. 1956) • •• 11, 25

James v. Dravo Contracting Co., 302 U.S. 134 (1937) .. Go Go • 0 Go ~ • Go • 0 Go. 35

Johnson v. Bridge, 60 Ca1.App. 629, 213 Pac. 512 (1923) • • • • • • • • • • •• 19

Johnson v. Mc Intosh, 8.Wbeat. (U.S.) 543 (1823) • •• • ••••• • • 7

Kirkwood v. Arenas, 243 F.2d 863 (9th Cir. 1957) 9, 19

Makah Indian Tribe v. Clallam County, 73 Wash.2d 667, 440 P.2d 462 (1968) •• • • • •

Mescalero Apache Tribe v. Hickel, 10th Cir.

26

No. 40-70 • • • • • • • • • • 2

Merris v. Hitchcock, 194 U.S. 384 (1904) •

N.L.R.B. v. Wyman-Gordon Co., 394 U.S. 759 (1969) • • • • • • •

Oklahoma Tax Commission v. Texas Co., 336 U.S. 342 (1969) •••••••• • •

Oklahoma Tax Commission v. un~ted States, 319 U.S •. 598 (1943) ••••••••••

, ,

, "

vi

• •

· .

• •

11

13

34, 37, 38, 39

38

• Osuna v. Johnstone, San Diego Superior (civil No. 313438) . . . . . . . PUlalluE Tribe v. De12artrnent of Game, 391 u.s. 392 (1968) . . • . • • •

Seaboard World Airlines v. Gronouski, 230 F.Supp. 44 (D.D.C. 1964) •••

•

•

Court, •. .. • • • • 14

• • • . 9

• • ~ e 14

Selmour:v SUEerintendent, 368 U.S. 351 (1962). 17

Snohomish County v. Seattle Disrosal Co., 70 Wash. 668, 425 P.2d 22 (1967 cert.denied 389 U.S. 1016 (1967) •••••••••••

SohoP12Y v. Smith, 302 F.Supp. 899 (D.Ore. 1969)

Squire v. CaEoeman, 351 U.S. 1 (1956). •• •

Starrv. Long Jim, 227 U.S. 613 (1913)

United States v. Detroit, 355 U.S. 466 (1958).

United States v. Kagama, 118 U.S. 375 (1886)

United States v. Libbl, McNeil and Libbl, - 107 F.Supp •. 697 (D. Alaska 1!}52) •••••••

United States v. Rickert 188 U.S. 432 (1903) • ===~!,

united States v. Santa Fe Pacific R. Co., 314 U.S. 339, reh.den. 314 u.s. 716 (1941) ••

Vitex Manufacturini Co. v. GOvernment of the Virgin Islands, 35 F.2d 313 (3rd. cir 1965) •

Warren Trading Post v. Tax Comm., 380 U.S. 685 (1965) • • • • • ••••

Williams v. Lee, 358 U.S. 217 (1959) •••••

Worcester v. Georgia, 6 Pet. (U.S.) 515 (1832)

Your Food Stores, Inc. v. Vi11a~e of 68 N.Mex. 327, 361 P.2d 950 (19 1), cert.denieQ,. 368 U.S. 915 (1961) ••

vii

ESEanola,

• • • • •

19

9

19, 26

21

34, 35, 36

9

14

25

7

28

24, 26, 29, 30, 36, 37

9, 24, 36, 37

9, 38

25

TREATISES AND LAW REVIEWS

United States Department of the Interior, Handbook of Federal Indian Law (1958) •• • •

Rosenn, "Puerto Rican Land Reform: The History of an Instructive Experiment" 73 Yale L. J. 334 (1963) ••••••• iii iii Q GI

OTHER AUTHORITIES

California State Advisory Commission on Indian Affairs, "Progress Report to the Governor and Legislature: Indians in Rural and Reservation Areas" (February, 1966)

Executive Order of the President No. 11435

11

28

4,5,6

(November 21, 1968) • • • • • • • • • •• 22

Memorandum Opinion of the Deputy Solicitor, No. 36768, (February 7, 1969).,. • • • • • •• 20

Memorandum Opinion of the Sacramento Solicitor (October 22, 1968) •••

Regional • • • • • 20

1969 California County Fact Book • • • • • •• 17

Sacramento Area Office of the Bureau of Indian Affairs, "Tribal Information and Directory" (1970) •••••••••••••••.••• 3, 4

viii

• NO. 25298

IN THE UNITED STATES COURT OF APPEALS

FOR THE NINTH CIRCUIT

THE AGUA CALIENTE BAND OF MISSION INDIANS, by and through its TRIBAL COUNCIL, and DORA JOYCE PRIETO, PRISCILLA GONZALES, GLORIA GILLETTEE, PATRICK PATENCIO, and LAWRENCE PIERCE, Allottees, Individually and in Class Action, on behalf of all allottees of allotted land on the Agua Caliente Band of Mission Indians Reservation,

Appellants,

v.

THE COUNTY OF RIVERSIDE, a political subdivision of the State of California,

Appellee.

APPEAL FROM THE UNITED STATES DISTRICT COURT

"- FOR THE CENTRAL DISTRICT OF CALIFORNIA

BRIEF OF AMICUS CURIAE

INTEREST OF AMICUS CURIAE*

California Indian Legal Services is a non-profit

corporation supported by the Legal Services Program of the

Office of Economic Opportunity. Legal assistance to low

income American Indians and Indian tribes is provided by

*Letters from appellants and appellee consenting to the submission of this brief amicus curiae have been submitted to the Clerk.

-1-

• California Indian Legal Services, particularly in the

specialized area of law related to Indian resources and in

economic development activities. Amicus has submitted a

brief amicus curiae before this court in Hopkins v. United

States, 414 F.2d 464 (9th Cir. 1969) and before the Court

of Appeals for the Tenth Circuit in Mescalero Apache Tribe

v. Hickel (No. 40-70) which is now pending.

The decision in this case will be of great signifi

cance to Indians. Amicus is active in promoting and

assisting in the economic development of Indian reserva

tions and therefore has a vital interest in presenting to

this court the full range of issues raised by this case.

STATEMENT OF THE CASE

Amicus adopts the statement of the case in

Appellants' Brief.

QUESTIONS PRESENTED

This case involves the validity of the imposition

of a possessory interest property tax on lands held in

trust by the United States of America for the Agua Caliente

Band of Mission Indians.

-2-

• ARGUMENT

I. THE UNIQUENESS OF THE AGUA CALIENTE INDIAN RESERVATION.

According to the January, 1970 edition of the

"Tribal Information and Directory" published by the Sacra

mento Area Office of the Bureau of Indian Affairs, there

are seventy-six Indian Reservations or Rancherias in the

State of California (not including the four Reservations

along the Colorado River, which are under the jurisdiction

of the Phoenix Area Office of the Bureau). The State of

California has attempted to assume certain jurisdiction,

the precise nature of which is at issue in this proceeding,

over Indians residing on all of these lands pursuant to

28 U.S.C. § 1360 and 18 U.S.C. § 1162. Of the seventy-six

Reservations and Rancherias listed, the Bureau of Indian

Affairs "Tribal Information and Directory" indicates that

twenty-five Reservations (including Agua Caliente) were

established under authority of the Act of January 12, 1891,

the Mission Indian Relief Act (26 stat. 712). Of these

twenty-five, nine are located in Riverside County, two in

San Bernardino County, thirteen in San Diego County, and

one in Santa Barbara County.

According to the same Bureau of Indian Affairs,

Sacramento Area Office "Tribal Information and Directory,"

the Indian Reservations in California range in size from

less than one acre (Sheep Ranch Rancheria) to more than

-3-

• 85,000 acres (Hoopa Valley Reservation). Bureau of Indian

Affairs, supra at pp. 34 and 67. Agua Caliente (approxi

mately 27,000 acres, T. 39) is the second largest Reserva

tion in Southern California, the largest being the Morongo

Reservation (32,254 acres, ~. at p. 51) and the smallest

being the Santa Ynez Reservation (99 acres, Id. at p. 65).

Populations of California Indian Reservations vary from

zero (La Posta, Cuyapaipe) to more than 850 (Hoopa Valley).

~. at pp. 27, 34 and 39. Obviously, there are very few

statements that are applicable to all of the Indian lands

in California but one generalization does apply, almost

without exception: the. Indians residing in virtually every

Reservation or Rancheria are impoverished. The major

exception is Agua Caliente.

In "Progress Report to the Governor and the Legis

lature by the State Advisory Commission on Indian Affairs

on Indians in Rural and Reservation Areas" (February, 1966),

the California State Advisory Commission on Indian Affairs

made the following findings and recommendations concerning

the social and economic characteristics which define the

position of California's rural Indian population:

1. Two of the major underlying factors which

account for the problems of underdevelopment of reserva

tion economies are the poor quality and remoteness of

Indian lands and the almost complete lack of higher

-4-

• job skills among Indians. "Progress Report," supra

at p. 9.

2. The rate of unemployment in the Commission's

survey of 10 reservations is 25.5 percent; the rate of

unemployment reported by the [questionnaire of the

House Committee on Interior and Insular Affairs in 1963]

is 35 percent. Id. at p. 9.

3. The commission survey finds that over 70 per

cent of the families residing on 10 California

reservations earn, on the average, less than $3,000

annually, with one-half of these earning less than

$1,500 per year. Id. at p. 9.

4. The conditions under which Indians live in

California are the lowest of any minority group.

Housing is grossly inadequate: living quarters are

small, crowded and poorly furnished; existing houses

are structurally unsound; foundations are lacking in

many cases; the building materials used, together with

faulty electrical wiring and the unsafe use of gas,

kerosene, and wood stoves, constitute a constant men

ace to life; houses generally do not provide the mini

mum necessary protection from extreme climatic

conditions. Reports from federal, state and local

agencies agree with the commission's findings: from

30 to 50 percent of the homes need complete replacement

-5-

and 40 to 60 percent need improvements, taken together,

this means that 90 percent of all homes need replace

ment or repairing to provide adequate living quarters

for California Indians. Sewage disposal facilities are

unsatisfactory in 60 to 70 percent of cases. Water

from contaminated sources is used in 38 to 42 percent

of the homes. Water must be hauled, under unsanitary

conditions, by 40 to 50 percent of all Indian families.

Id. at p. 10.

5. The key to the solution of the problems of

Indians, whether in the areas of education, welfare and

health, or living conditions lies in the development of

the employment potential of Indians and in the economic

development of their land resources. Id. at p. 10.

When viewed against this sobering background, the

uniqueness of the Agua Caliente situation is apparent. To

mark the comparison, it is sufficient to point out that 103

of the 150 members of the Agua Caliente tribe each own

interests in trust land (allotments) that had appraised

values of $335,000 in 1959 (T. 38). Undoubtedly, most of

the remaining members of the tribe are the allottees' minor

children.

It may be that the Agua Caliente Indians have

progressed to the point, both economically and in terms of

their competency to manage their own affairs, when it is

-6-

• no longer necessary or desirable for the United States to

hold title to property for the Indians' sole use and

benefit. However, this judgment is not one for the courts

to make but rather for the congress. l United States v.

Santa Fe Pacific R. Co., 314 U.S. 339, reh. den. 314 U.S.

716 (1941); Beecher v. Wetherby, 95 U.S. 517 (1877); Johnson

v. M'Intosh, 8 Wheat (U.S.) 543 (1823). Therefore, in

determining the merits of this litigation, this court should

not be guided by whatever opinions it may have concerning

the wisdom of continuing this nation's trust responsibilities

to the appellant.

The questions to be decided in this proceeding are

not unique to the Agua Caliente-Palm Springs situation.

This court's decision will have a direct impact upon all

Indians residing on or near Indian trust land in California

and throughout the Western United States. what may appear

to be logical or equitable in one set of circumstances may

turn out to be utterly disasterous when applied elsewhere. 2

lFrom the available evidence, Congress has apparently determined that the trust relationship with the Agua Caliente Tribe needs to be strengthened, not weakened. ~ 25 U.S.C. § 954.

2This is not to imply that in the circumstances presented here imposition of the appellee's possessory interest tax is either reasonable or equitable. To the contrary, the uncontradicted evidence shows the severe detrimental consequences of the tax on the economic development of the Indian lands (T. 80).

-7-

• For this reason, we implore this court to consider carefully

not only the impact of its decision on Indians generally,

but also the kind of judicial decision that is best cal-

culated to achieve the flexibility of approach demanded by

the diverse nature of the problems confronting the many

distinct Indian communities in their relations with the

dominant society. While a decision affirming the trial

court mayor may not solve the unique problems involved in

Agua Caliente-Palm Springs-County of Riverside relationship,

it would certainly severely hamper the efforts of other

Indian communities to improve conditions on their reserva-

tions.

II. IMPOSITION OF A POSSESSORY INTEREST TAX UPON INDIAN TRUST LANDS IS NOT AUTHORIZED BY 28 U.S.C. § 1360; ON THE CONTRARY, § 1360 RECOGNIZES THE RIGHT OF TRIBAL AUTHORITIES TO IMPOSE ITS TAX.

A. Sections 1360(a) and (c).

The appellee's authority to impose a possessory

interest tax on leased Indian land is specifically excluded

from the grant of civil jurisdiction to California in 28

U.S.C. § 1360. Title 28 U.S.C. § 1360, far from authorizing

taxation of Indian lands, prohibits any direct tax on Indian

land. The Court of Appeals for the Ninth Circuit said of

§ 1360 that it "negatives the idea that any change in the

law as to 'alienation, encumbrance, or taxation' of Indians'

-8-

• property was intended." Kirkwood v. Arenas, 243 F.2d 863,

865 (9th Cir. 1957).

In enacting "Public Law 280" (28 U.S.C. § 1360 and

18 U.S.C. § 1162, 67 Stat. 589), which authorized assumption

of limited civil and criminal jurisdiction of certain named

states (including California) and territories over the

"Indian country" within their boundaries, Congress care

fully preserved areas of immunity from state jurisdiction

(28 U.S.C. § 1360(b) and 18 U.S.C. § 1162(b» and acknowledged

the traditional authority of Indian tribes and communities

to govern themselves. 28 U.S.C. § 1360(c); ~. William v.

~, 358 U.S. 217(1959). In carefully carving out an area

of exclusive tribal jurisdiction and erecting legal barriers

to prevent the state:'s. political subdivisions from assuming

dominion and control over Indian Reservations, Congress

recognized not only the traditional sovereignty of Indian

communities, but also the history of strained, indeed at

times hostile, relations between Indians and surrounding

localities. Cf. Worcester v. Georgia, 6 Pet. (U.S.) 515

(1832); Cherokee Nation v. Georgia, 5 Pet. (U.S.) 1 (1831);

and more recently, Puyallup Tribe v. Department of Game,

391 U.S. 392 (1968); and Sohappyv. Smith, 302 F.Supp. 899

(D. Ore. 1969). In United States v. Kagama', 118 U.S. 375

(1886), a criminal case arising on an Indian Reservation in

California, the court observed: "Because of the local ill

-9-

• feeling, the people of the States where the [Indian Tribes]

are found are often their deadliest enemies."

Section 1360(a) makes applicable to all "Indian

country" within the State of California those civil laws

"that are of general application to private persons or pri

vate property· and provides further that such laws "shall

have the same force and effect within such Indian country

as they have elsewhere within the State." (emphasis added)

The law thereby draws an important distinction between the

civil laws of state-wide application on the one hand and

the civil law promulgated by the state's various political

subdivisions on the other. While the "Indian country"

described in the act was to be subject to the state-wide

civil laws of general application (except for the limita

tions set forth in § l360(b», the law specifically excluded

such "Indian country" from the jurisdiction of local

political subdivisions.

This distinction is also embodied in § 1360(c)

which specifically recognizes the authority of Indian tribes

within the affected states to govern themselves and their

property subject to only one limitation. The section reads:

Any tribal ordinance or custom heretofore or hereafter

adopted by an Indian tribe, band, or community in the

exercise of any authority which it may possess shall,

-10-

• if not inconsistent with any applicable civil law of

the State, be given full force and effect in the deter-

mination of civil causes of action pursuant to this

section. (emphasis supplied)

The authority of tribal governing communities

recognized in this section is at least equal to the author

ity of the state's political subdivisions. Obviously, a

city or county is not permitted to enact ordinances incon-

sistent with applicable civil law of the state. See Cal. ---Const. Art. II, § 11. The same limitation applies to

Indian governing authorities (subject to the limitations

on state jurisdiction in § l360(b». However, in all other

respects Indian tribes, bands, and communities are free to

govern themselves and this authority necessarily entails

the collection of revenue. 3

As the discussion, infra, of the assessment, levy,

and collection of the possessory interest tax will show,

appellant Agua Caliente Tribe, by and through its Tribal

Council, has the right, power, and authority to impose a

3Merris v. Hitchcock, 194 U.S. 384 (1904); Iron Crow v. 0hIaIa sioux Tribe of Pine Ridge Reservation;--231 F.2d 9, 96 (8th C~r. 1956); Buster v. Wright, 135

. Fed. 947 (8th Cir. 1905), appeal dismissed 203 U.S. 599 (1906). See generall¥ United States Department of the Interior, Federal Ind~an Law (1958), pp. 435 et seq.

-11-

• possessory interest tax, or for that matter, any kind of

tax, property or otherwise, consistent with applicable

state civil laws of general application. Once it is

clear that the Tribe has such authority (which is specifi

cally recognized and affirmed by § 1360), it is manifest

that the lands within so-called "Indian country" are immune

from the appellee's possessory interest tax, just as the

appellee is without authority to assess, levy, or collect

property taxes on lands outside the County of Riverside.

There is no overlapping jurisdiction shared by the appellant

Tribe and the appellee County because the political sub

divisions of the state are specifically excluded by Congress

from applying their local laws, ordinances, etc. to the

"Indian country" within their exterior boundaries.

This obvious distinction between jurisdiction con

ferred on the state and jurisdiction withheld from the

state's political subdivision has been recognized by the

Secretary of the Interior, by the California courts, and by

the state's political subdivisions themselves.

Thus, in purporting to adopt and make applicable

the laws of the State of California relating to the use of

land leased from Indians, the regulation promulgated by

the Secretary of the Interior specifically provided:

This adoption and application does not include the

-12-

• laws, ordinances, codes, resolutions, rules, or other

regulations of the various counties and cities within

the State of California which will be adopted and

applied by separate action with such exceptions as

are determined to be appropriate. 30 F.R. 8722 (July

2, 1965).

To the knowledge of amicus, the only regulation issued by

the Secretary purporting to adopt and apply the laws and/or

other regulations of any of the political subdivisions in

California to leased Indian land involved the unique cir

cumstances of the Agua Caliente Reservation and the City of

Palm Springs, 30 F.R. 8172 (June 22, 1965). Although these

regulations (both 30 F.R. 8722 and 30 F.R. 8172) made appli-

cable to leased Indian land state and local laws "limiting,

zoning, or otherwise governing, regulating, or controlling

[its] use or development," state and local tax laws were

specifically excluded. 4

4Amicus cites these regulations for two purposes: first, to demonstrate governmental awareness of the different status accorded state and local laws under Public Law 280, and second, to point out that although the regulations purportedly authorize some state or local control of the use or development of leased Indian land, state or local taxation of leased Indian land was clearly not authorized. However, amicus has grave doubts concerning the meaning and/or validity of the regulations. The proposed regulations were not published in the Federal Register in advance of their promulgation as required by 5 U.S.C. § 553(b) (3) and its predecessor 60 Stat. 237, § 4, and is therefore void. NLRB v. Wyman-Gordon Co., 394 U.S. 759 (1969); Seaboard Worl~

-13-

• In County of San Bernardino v. La Mar, 271 A.C.A.

821, 76 Cal.Rptr. 547 (1969), the State Mobile Home Parks

Act was found to be applicable to leased Indian land

pursuant to 30 F.R. 8172 and, since enforcement power was

specifically delegated to the counties by the state law,

the County of San Bernardino was permitted to enforce the

provisions of the state law of general application.

However, the county could not enforce its own mobile park

ordinance. In fact, San Bernardino County conceded on

appeal its lack of authority to apply its ordinance (as

opposed simply to enforcing the state law) to land leased

from Indians.

In Osuna v. Johnstone (San Diego Superior Court,

civil No.31343B), Indians residing on the Barona Indian

Reservation in San Diego County brought a class action

challenging the application of the county's dog licensing

Airlines v. Gronouski, 230 F.Supp. 44 (D. D.C. 1964); United States v. Libby, r4cNeil and Libby, 107 F.Supp. 697 (D. Alaska 1952). Further, the July 2,1965 regulation (purporting to make certain state laws applicable to leased Indian land) provides: "Nothing contained in this notice shall be construed to in any way alter or limit the provisions of" 28 U.S.C. § 1360(b) and 18 U.S.C. § l162(b). The subsequent rulings of the Solicitor~p Office of the

JDepartment of the Interior, infra fn. 8, holding that these sections conferred jurisdiction upon the State of California only to the extent its laws operate upon the person, but that state laws may not be applied if their enforcement, directly or indirectly, would involve the regulation of trust property, would appear to undercut completely the effect of these purported regulations.

-14-

•

· ... _.

ordinance to dogs kept on the Reservation. In granting

plaintiffs' motion for a preliminary injunction, the court

held that S 1360 does not grant jurisdiction for the

application of laws, regulations and ordinances which are

local in nature. Because California Health and Safety

Code S 1920 does not require the County of San Diego to

collect a dog license fee, the county ordinance imposing

a dog license tax was found to be an ordinance local in

nature which could not be applied to dogs kept on the

Indian Reservation. The remainder of S 1920, to the extent

its enforcement by the county was made mandatory by state

law, in "rabies areas" .such as San Diego County (Cal.

Health and Safety Code S 1901.2), was held to be enforcible

by the county. Following the issuance of this preliminary

injunction, the County Board of Supervisors adopted an

ordinance (No. 3444) accepting this decision by formally

recognizing the exemption.. of. the owners of dogs kept on

federal Indian trust land from the county's license fee.

The tax here assessed, levied, and collected by , appellee County is clearly local in nature and non-mandatory,

and is decidedly not a civil law of general application

throughout the State of California. California Revenue and

Taxation Code S 107 merely defines the meaning of

"possessory interests." Pursuant to the state statutory

-15-

• state law.is not self-executing here, nor is it mandatory •

state law does no more than provide basic guidelines on

the model of enabling legislation. 6 The result is a

pattern of property taxation that differs markedly among

the counties. See 1969 California County Fact Book, p. 31.

From the nature of the state statutory scheme, it

is readily apparent that, pursuant to the Tribe's inherent

authority, supra fn. 1, and 2B U.S.C. § l360(c), the

appellant tribe has the authority to impose a possessory

interest tax consistent with applicable state laws of

general applicatio~. State law, however, does bar double <

taxation. 7 Cal. Const. Art. XIII, § 1 and Cal. Rev. and

Tax. Code § 102. B The two possessory interest taxes

imposed, respectively, by the appellee and the appellant

6For other examples of state legislation enabling its political subdivisions to enact certain kinds of ordinances, see, ~., Cal. Health and Safety Code § 1920 (dog licenseSfT C~ Govt. Code § 65B50 (zoning); Cal. Govt. Code § 3B660, and Cal. Health and Safety Code-§§ 17922,17951 (building codes).

7The taxing authority of the tribe clearly extends to the interests of non-Indian lessees. See Seymour v. Superintendent, 36B U.S. 351 (1962), and cases cited in footnote 3.

BWe assume, arguendo, that the state law proscribing double taxation is not within the limitation of state civil jurisdiction in § l360(b). If it is included with the limitations of that section, so, too, must the rest of the state tax·scheme, including the tax challenged in the instant case. See infra.

-17-

• tribe cannot be allowed to stand together; the county tax

must fail. Title 28 U.S.C. § l360(c) protects the ability

of the tribe to impose its tax in that it is a tribal law

"not inconsistent" with state law. On the other hand, 28

U.S.C. § l360(a) prohibits collection of the county tax-

a law which is local and not general in nature.

B. Section l360(b).

In Part II B of their opening brief, appellants

argue persuasively that 28 U.S.C. § l360(b) specifically

precludes imposition of the tax in question by appellee.

As they correctly point out, the trial court's distinction

between taxing Indian property and taxing the property of

the non-Indian lessee (the former being proscribed, the

latter permissible), a distinction which is essential to

sustain the holding of the court below, leads to impossible

difficulties because state courts are specifically denied

jurisdiction to adjudicate the right to possession of

Indian property. Yet state courts cannot possibly escape

that very undertaking if the tax here in question is

permitted.

The trial court's purported distinction must fail

for another reason. Section l360(b) precludes not only

the taxation of Indian trust property, but also its "encum

brance." section 1114 of the Cal. Civil Code provides that

-18-

• the term "incumbrances" "includes taxes, assessments, and

all liens upon real property." Interpreting this statute,

the California Supreme Court declared in Johnson v. Bridge,

60 Cal.App. 629, 213 Pac. 512 (1923) incumbrance was

defined to include "whatever charges, burdens, obstructs, or

impairs" the use of an estate in land, or "impedes its 9

transfer." Similarly, in Snohomish County v. Seattle

Disposal Co., 70 Wash. 668, 425 P.2d 22 (1967), cert.

denied 389 U.S. 1016 (1967), zoning ordinances were held to

be "encurnbrances,"(defined as "a burden on land deprecia-

tive of its value, such as a lien, easement, or servitude,

which, though adverse ,to the interests of the landowner,

does not conflict with his conveyance of the land in fee")

within the meaning of S 1360(b). And most importantly,

the United States Supreme Court and the Court of Appeals

for the Ninth Circuit have held the clause "free of all

charge or incumbrance whatsoever" to preclude imposition of

taxes on trust land. In Squire v. Capoeman, 351 U.S. 1

(1956) the taxation of income from the sale of timber on

allotted (Indian trust) lands was proscribed. In Kirkwood

v. Arenas, supra, the imposition of an inheritance tax on

the transfer of an allotment to one's heirs was invalidated.

9See also Fraser v. Bentel, 161 Cal. 390, 119 Pac. 509 (1911), and Evans v. Faught, 231 Ca1.App.2d 698, 42 Ca1.Rptr. 133 (1965) and cases therein cited.

-19-

• Clearly, the imposition of appellee's possessory

interest tax constitutes an "elncumbrance" within existing

judicial definitions, on the estate of the Indian bene-

ficiary. The uncontradicted evidence in this case shows

that the tax operates to "impair" and "burden" the trust

property, preventing or obstructing its use. The tax is

depreciative of the land's value. Needless to say, the tax

is an "encumbrance" whether or not the land is actually

leased because the threatened or potential application of

the tax is itself a burden that depreciates the value of

the land and obstructs or impairs its use. Therefore,

even if imposition of appellee's possessory interest tax

does not constitute taxation of Indian trust property

(because the tax is formally imposed on the non-Indian's

leasehold interest) the tax operates as an encumbrance on

the Indian trust property and is outside the scope of

jurisdiction conveyed by § 1360. 10

lOIn interpreting § 1360(b), the Solicitor of the Department of the Interior has ruled: (1) That 28 U.S.C. § 1360 conferred jurisdiction upon the State of California to apply its laws to Indians only to the extent such laws operate upon the person, but state laws may not be aPplied to Indians if their enforcement, directly or indirectly, would have an impact on or involve the regulation of trust property in any significant way (Memorandum Opinion of the Deputy Solicitor No. M36768 [February 7,1969]). (2) That § 1360 did not authorize the imposition of the state sales tax on Indian trading activities on Indian Reservations in California (Memorandum Opinion of the Sacramento Regional Solicitor [October 22,1968]).

-20-

• If there is any doubt about what Congress intended

by the language it used, the rule of construction of laws

relating to Indians that doubtful expressions are to be

resolved in favor of the Indians should be invoked.

Alaska Pacific Fisheries v. United States, 248 U.S. 78 (1918);

Choate v. Trapp, 224 U.S. 665 (1912); starr v. Long Jim,

227 U.S. 613 (1913).

C. Section 1360: a Trojan Horse?

There are policy considerations which also compel

this court to reject appellee's argument that their posses

sory interest tax is authorized by § 1360. Appellant tribe,

even before the enactment of Public Law 280, recognized the

"law and order" problems resulting from the absence of state

jurisdiction within the Indian Reservation, and joined with

local authorities in requesting Congress to pass Public Law

322 (63 Stat. 705), applicable only to the Agua Caliente

Reservation. Many tribal authorities, including appellant,

also p~rticipated in the deliberations which led to the

enactment of § 1360. See generally plaintiffs' Trial Brief

and Points and Authorities in Support Thereof, pp. 23-26.

Congressional willingness to consider the opinions of such

tribal authorities is apparent from the exceptions to state

jurisdiction ennumerated in § 1360(a). The entire statute

seems to have been drafted to assure the affected Indian

-21-

, tribes that there would be no adverse consequences to the

assumption of the limited state jurisdiction conferred by

the act. Obviously, no tribal authority would have con-

sented to the assumption of state jurisdiction if they had

thought that this legislation would have allowed the imposi-

tion of a possessory interest tax upon their lessees. To

construe Public Law 280 as authorizing the imposition of

such a tax would not only be a cruel irony (since the Indians

had helped to procure its passage) but yet another breach of

trust.

Further, in 1968 Congress amended Public Law 280

to require the consent.of the tribe before any state not

previously granted civil jurisdiction over Indians could

acquire such jurisdiction. 25 U.S.C. § 1322.11

Insofar as

llAt the same time, Congress provided for the retrocession of the jurisdiction conferred by 28 U.S.C. § 1360 and 18 U.S.C. § 1162. 25 U.S.C. § 1323 and Executive Order of the President No. 11435 (November 21, 1968), 33 F.R. 17339. This is an indication that Congress was less than completely satisfied with the fifteen years of experience under Public Law 280. In view of this congressional policy to retreat from the old policy of encouraging the states to assume civil jurisdiction over Indian country, manifested in both §§ 1322 and 1323 of 25 U.S.C., it would be unwise and counter productive for the courts to expand p.L •. 280 jurisdiction to anything beyond that which was clearly in the contemplation of the Congress at the time of its enactment.

-22-

, it still remains a congressional policy to provide for the

assumption of state civil and criminal jurisdiction over

Indians, with the consent of the appropriate tribal

authorities, that policy will be undermined considerably,'

if indeed it is not dealt the death below, by a holding

that Public Law 280 authorizes the imposition of a posses-

sory interest tax on lessees of Indian land. It is not

very likely that tribal authorities will consent to the

assumption of state civil jurisdiction if they know in

advance that the state will thereby acquire authority to

control the use of their land through the imposition of a

possessory interest tax.

III. UNDER PREVAILING STANDARDS, THE COUNTY'S POSSESSORY INTEREST TAX CANNOT BE APPLIED TO LEASEHOLD INTERESTS IN INDIAN TRUST PROPERTY.

In recent years, the Supreme Court has set forth

three related tests for determining the applicability

of state law to Indian lands and Indian affairs, under

anyone of which appellee's possessory interest tax would

be invalid. 12 They are:

1. Whether the state action infringes on the right

of Indian Reservations to make their own laws and be ruled

l2This discussion assumes that Congress has not specifically authorized imposition of the appellee's possessory interest tax. ~ Part II, supra.

-23-

• by them, i.e., wKether the state action interferes with

tribal sovereignty; Williams v. Lee, 358 U.S. 217, 220

(1959) •

2. Whether the state laws interfere with federal

policies concerning the reservations; Warren Trading Post

v. Arizona Tax Comm., 380 U.S. 685, 687 (1965).

3. Whether the federal government has pre-empted

the field so that no room remains for any state action;

Warren Trading Post v. Arizona Tax Comm., supra at 690-91.

A. Interference with sovereignty.

The imposition of the County's tax prevents the

tribe' from imposing its. own tax on the lessees of Indian

land. Even if imposition of both the tribe's and the

County's tax does not constitute double taxation,13 as a

practical matter, as the facts in this case clearly demon

strate, taxing by the County renders ineffective the

possibility of a tax by the tribe. If the tribe were to

insist that its tax be paid, along with the County's, it

would completely undermine the economic desirability of

leasing Indian land.

It is not necessary, however, for the court to find

that the tribe would not be able to levy and collect its

tax if the County's tax is imposed in order to find an

l3~ p. 17, supra.

-24-

• interference with tribal sovereignty. It is sufficient

interference with the Tribe's right to make its own laws

and to be ruled by them for the County to levy a tax on

property that is within the jurisdiction of the Tribe and

potentially subject to the Tribe's tax. "Two self-governing

bodies cannot have dual and co-existent jurisdiction and

control within the same territory at the same time." Your

Foods stores, Inc. v. Village of Espanola, 68 N.M. 327, 361

P.2d 950,956 (1961), cert. denied 368 U.S. 915 (1961).

See also Iron Crow v. Oglala Sioux Tribe of Pine Ridge

Reservation, supra.

In Commissioner of Taxation v. Brun, Minn.

--'0' 174 N.W.2d 120 (1970), the Supreme Court of Minnesota

held that the state lacked authority to impose an income

tax on Indians residing on the Red Lake Reservation stating,

"It cannot be argued that siphoning off part of the earnings

from employees of a sawmill operated for the benefit and

welfare of enrolled members of the tribe does not interfere

with the tribal right of self-government." 174 N.W.2d at

126.

B. Interference with federal pOlicy.

There is an express federal policy to encourage the

economic development of Indian land and to encourage Indians

to become economically self-sufficient. United States v.

-25-

,

.... -' .

Rickert, 188 U.S. 432 (1903). Squire v. Capoeman, supra.

In Makah Indian Tribe v. Clallam County, 73 wash.2d

667, 440 p.2d 462 (1968), the Supreme Court of Washington

held that personal property of an Indian kept on the

reservation is exempt from a county's personal property

tax. The personal property in question was utilized in a

commercial enterprise which did business with non-Indians.

The court stated,

The reasons for such a ruling lie almost exclusively

in the discernable federal policy of encouraging

Indians to become economically self-sufficient on

their reservations •• . . That the Makahs will, while receiving most of the

benefits of taxpayers and citizenship, escape some

of the correlative responsibilities of citizenship

is a problem for the Congress and the President to

solve. (440 p.2d at 447-48)

This is consistent with the reasoning of the Supreme Court

in invalidating the State of Arizona's sales tax on the

.gross income of a retail business on the Navajo Indian

Reservation partly because of the added financial burden

such a tax would impose on the Indian purchasers. Warren

Trading Post v. Arizona TaxComm., supra at 691.

Every year, as part of its proposed budget for the

-26-

• coming fiscal year, the Bureau of Indian Affairs makes

the following statement to the House and Senate Appropria

tion Subcommittees considering its budget request:

The ultimate goals of the Bureau of Indian Affairs

for the Indian people are maximum economic se1f

sufficiency, equal participation in American life and

equal citizenship privileges and responsibilities.

The Bureau is working toward the attainment of these

goals through two basic programs, one of which is

education, and the other is the economic development

of reservation resources.

See, ~., Hearings before the House Subcommittee

on Appropriation for the Department of the Interior

and Related Agencies for Fiscal Year 1969 at p. 744.

That exemption from the County's tax is an effec

tive means of increasing the development of the trust

land to accomplish this federal policy was shown conclusively

in the court below (T. 207-8). Exemption adds to the value

of the Indians' land by providing them with the possibility

of a greater net return on their land (T. 202). As was

established in the District Court, the tax sought to be

imposed by appellee clearly frustrates this federal policy.

The tax has caused rent arrearages (T. 129-30) and lease

defaults (T. 107, 139). Because of the tax lower rentals

-27-

• must be accepted (T. 109); in fact, fewer leases are made

because of the tax (T. SO). The effect of the tax is to

frustrate severely the federal goal of encouraging Indians

to utilize their land to become economically self-sufficient

(T.70). The tax has had this effect on the Agua Caliente

Band of Mission Indians, a band of Indians who are, as was

pointed out above, in a far better financial position than

the vast majority of Indians in the state of California.

If the tax can be so damaging to Agua Calientes, it is not

hard to comprehend the devastating effects similar taxes

would have on less fortunate Indians (~T. 196, et seq.).

Many communities offer tax incentives to attract

commerce. See generally Rosenn, "Puerto Rican Land Reform:

The History of an Instructive Experiment," 73 Yale L.J. 334

(1963) and Vitex Manufacturing Co. v. Government of the

Virgin Islands, 351 F.2d 313 (3rd Cir. 1965). The federal

government has established the Indians' tax-exemption to

provide for the maximum economic benefit to the Indians.

The imposition of the County's possessory interest tax on

lessees of Indian land destroys the tribe's right and

authority to offer such incentives and thus is another

way in which tribal sovereignty is invaded. On many Indian

reservations in California, the presence of even one

industry would eliminate most of the unemployment and would

-2S-

• tend to help alleviate the omnipresent poverty. See

Part I, supra. If, as the record reveals in this case, it

is difficult to attract commerce to the Agua Caliente

Reservation in the Palm Springs area because of the County's

tax, what chance do the other reservations in far less

desirable areas have to bring industry to their localities

unless they are able to offer some kind of tax incentive?

C. Federal pre-emption.

In Warren Trading Post v. Arizona Tax Comm., supra,

imposition of Arizona's state sales tax on federally

licensed traders with respect to sales made to reservation

Indians on the~reservation was held to be precluded by the .-comprehensive federal scheme regulating reservation trading.

"There-is no room for the States to legislate on the

subject." 380 U.S. at 391, fn. 18.

The federal statutes and regulations concerning the

leasing of Indian trust land evidence the same intention to

pre-empt the field. The purpose of 25 U.S.C. § 415 and the

comprehensive regulations promulgated to interpret and

apply the leasing statutes, 25 C.F.R. Part 131, is obviously

to encourage the leasing of Indian lands as one means to

effectuate federal Indian policy by generating jobs and

income on the reservations. Prior to the enactment of §

415 in 1955, Congress had not authorized long term leasing

-29-

• of IndJ."an 1ands.14 S b ue t dm t t 25 USC § u seq n amen en so. • •

415 extending the terms for which leases on the lands of

certain tribes would be authorized to 99 year leases (in

1959 Agua Caliente was the first tribe so authorized,

P.L. 86-326, 73 Stat. 597 (Sept. 21, 1959» show the

popularity of the leasing device with both the Congress and

many Indian tribes. P.L. 90-570, 82 Stat. 1003 (Oct. 12,

1968); P.L. 90-534 § 6, 82 Stat. 884 (sept. 28, 1968);

P.L. 90-355, 82 Stat. 242 (June 20, 1968); P.L. 90-335

§ l(f), 82 Stat. 175 (June 10, 1968); P.L. 90-184, 81 Stat.

560 (Dec. 10, 1967); P.L. 90-182, 81 Stat. 559 (Dec. 8,

1967); P.L. 89-408, 80 Stat. 132 (April 27,1966); P.L.

88-167, 77 Stat. 301 (Nov. 4, 1963) ; P.L. 87-785, 76 Stat.

805 (Oct. 10, 1962) ; P.L. 87-375, 75 Stat. 804 (Oct. 4,

1961); P.L. 86-505 § 2, 74 Stat. 199 (June 11, 1960) ;

P.L. 86-326, 73 Stat. 597 (Sept. 21, 1959) •

In view of the federal government's paramount trust

responsibilities to Indians and Indian tribes, it is

inconceivable that Congress intended to leave to the County

the privilege of levying this tax. Warren Trading Post v.

140wing to the vast bureaucracy of the federal Indian establishment, and the period of time it takes for Indians to adjust to the vagaries of federal policy, in Indian affairs fifteen years is a very short time in which to even begin to implement the purposes of a statute.

-30-

--"--

•

C_·' ___ .... v·~·, _ ___.~ ..... ~~ "',. _ ..... -'-'_~ ';1( ... •

Arizona Tax Comrn., supra at 691. To do so would make

the implementation of national Indian policy dependent upon

fluctuating local tax rates.

Two other kinds of congressional enactments also

demonstrate congressional intent to exclude states from

exercising taxing authority within Indian country. First,

the Congress has given the Secretary of the Interior

authority to issue fee patents to Indian allottees "whenever

he shall be satisfied that any Indian allottee is competent

and capable of managing his or her affairs." 25 U.S.C.

§ 349. This statute expressly provides that after the

issuance of a fee paten,t, all restrictions as to sale, in

cumbrance, or taxation of the allotted land shall be removed

but that until the fee patent is issued,"all allottees to

whom trust patents shall be issued shall be subject to the

exclusive jurisdiction of the United States." Id. See also

§§ 4 and 5 of the Act of January 12, 1891, the Mission

Indian Relief Act. 26 Stat. 712 and 25 U.S.C. § 483. If

the Agua Caliente Indian allottees are, in the judgment of

the Secretary of the Interior (not the County of Riverside)

financially and otherwise competent, and if the Secretary

(not the County) concludes that the tax exemption is no

longer warranted, the Secretary is authorized to issue a

fee patent, thereby subjecting the land to state and local

taxation.

-31-

• Other statutes indicative of congressional intent

to pre-empt the field are the acts providing for certain

services at federal expense to Indian reservations and

Indian people that would otherwise be provided by the state

or its subdivisions. These statutes are a recognition that

the welfare of Indians is primarily a federal responsibility.15

The federal government contributes funds either directly or

indirectly (through the states or local school districts)

for reservation roads (25 U.S.C. § 318(a», Indian education

(20 u.s.c. §§ 236, et ·seg. and 244 et seg., and 25 U.S.C.

§§ 452-54) and Indian health (42 U.S.C. §§ 2001, et seg.).

If the state or its political subdivisions believe that

the minuses outweigh the pluses, the appropriate remedy is

an application to Congress or the Executivel6 for greater

contributions through existing channels or for the creation

15It bears emphasis that the property tax is only one of the state's sources of revenue and that California Indians do contribute to the state's revenue in many other ways. For example, California Indians pay sales taxes, excise taxes, taxes in their income from non-exempt property, gasoline taxes, etc.

160ne of the most obvious advantages of proceeding through the Congress or Executive branches is that they have ·the flexibility to look at the unique circumstances of each case and act accordingly. If the state or its subdivision is allowed to impose its tax, the tax will fall across the board upon those who might be able to afford it and upon those who will not. In the past, Congress has acted to authorize the state and local authorities to tax the output and improvements of oil, gas, and mining lessees of Indian lands. 25 U.S.C. § 398(c). See Part II A of Appellants' Opening Brief. ---

-32-

•

17 of new channels. Through the enactment of such legisla-

tion, Congress has indicated that the funds to provide

essential services for Indians and Indian Reservations

will come from sources that will not impose additional

burdens on the Indians and that the determination of the

appropriate source is exclusively within the province of

Congress.

Taken together, the federal statutes and regulations

authorizing and encouraging the leasing of Indian land, the

federal statutes authorizing the Secretary of the Interior

to issue allottees taxable fee patents under certain cir-

cumstances, and the federal statutes providing, either

directly or indirectly, for the services required by Indians,

show as clearly as any federal regulatory scheme could that

there is simply no room for the County to impose its posses

sory interest tax on Indian lands.

D. United States v. Detroit and Oklahoma Tax Commis-

sion v. Texas Co. distinguished.

In addition to finding authority for the County's

possessory interest tax in 28 U.S.C. § 1360, the trial

17congressman Tunney of Riverside County has recently introduced legislation in the House of Representatives which would authorize the Secretary of the Interior to pay the states or counties, upon their request, an amount equal to any tax or levy which would be imposed on Indian lands if they were not held in trust by the United States. H.R. 12589, 91st Congress.

-33-

• court's holding rests largely on a line of cases culminating

in United states v. Detroit, 355 U.S. 466 (1958) and

Oklahoma Tax Commission v. Texas Co., 336 U.S. 342 (1949).

These cases are clearly distinguishable under the principles

discussed in the preceding three sections.

In United states v. Detroit, supra, the Supreme

Court upheld a possessory interest tax imposed on a lessee

of government land pursuant to a Michigan statute. The case

does stand for the proposition that a state tax that is

eventually borne in some measure by the United States is not

invalid for that reason alone.

The case at bar is distinguishable in several respects.

First, in Detroit, the Court recognized that Congress could

confer immunity by statute (355 U.S. at 474), and Congress

did precisely that with respect to the County's tax at issue

in this case by enacting 28 U.S.C. § 1360. See Part II.

Second, the Supreme Court expressly noted that the Michigan

tax could not be enforced against the property. 355 U.S. at

467, n.l, 469. Possessory interest taxes imposed in the

State of California are, by contrast, collectable by seizure

and sale. Cal. Rev. and Tax. Code §§ 107 and 2914. Third,

there was no claim that Congress had excluded the state from

imposing its tax because the federal government had pre

empted the field to such a degree that there was no room

-34-

• left for state legislation. Fourth, the County's tax

imposed on the lessees of Indian land is inconsistent with

federal policy objectives while in Detroit the tax resulted

only in slightly increased cost to the government. As set

forth above, Part III B, there is a discernable and express

federal policy to encourage economic development on Indian

land and Indian economic self-sufficiency with which the

County's tax interferes and undermines. In the cases relied

upon by the trial court the tax did not strike at the

government's overriding goal as it does here.

In James v. Dravo Contracting Co., 302 U.S. 134

(1937), the government sought to have dams built, and con

tracted with the plaintiff to construct them. The tax on

the contractor which the Supreme Court sustained had as its

burden on the government the increased cost of construction;

it did not frustrate its primary purpose of having the dam

built. In Alabama v. King and Boozer, 314 U.S. 1 (1941),

the tax also resulted in a higher cost to the government,

but it did not frustrate its purpose--the acquisition of

building materials. In both Graves v. New York, 306 U.S.

466 (1939) and Detroit, the tax simply had an adverse

financial effect on the federal government. The taxes in

these cases resulted only in a degree of financial burden

on the federal government. Faced with deciding whether

-35-

• they should afford a private party a tax benefit which

would interfere with the state's power to tax or to impose

a financial burden on the federal government, the courts

have chosen the latter. However, when the very purpose of

the tax exemption is to provide an economic incentive to

develop Indian lands and to enable Indians to derive income

from their lands in order to become self-sufficient,

government interests of an entirely different magnitude are

involved. ~., Choate v. Trapp, supra, and Part II B

supra. Instead of merely imposing a financial burden on the

government, the County's tax contravenes the underlying

federal policy and, in.addition, directly conflicts with the

tribe's sovereignty.

Fifth, the Supreme Court has held in Williams v. Lee,

supra, and Warren Trading Post v. Arizona Tax Comm., supra,

that the presumptions operative in Indian cases are exactly

the reverse of the presumptions applied in Detroit. In

Detroit the court said;

Wise and flexible adjustment of inter-governmental tax

immunity calls for political and economic considera

tions of the greatest difficulty and delicacy. Such

complex problems are ones which Congress is best

qualified to resolve. (355 u.S. at 474)

In the absence of such congressional action, the state's

tax was upheld. By contrast, in Williams v. Lee, supra,

-36-

• the court held that state jurisdiction over Indian reserva

tions would be permitted only when specifically authorized

by Congress. 358 U.S. at 223. In the absence of congres

sional action, the state would not be permitted to exercise

its authority. Similarly, in Warren Trading Post v. Arizona

Tax Comm., supra, the presumption operated against the state

imposed tax in the absence of congressional authorization.

380 U.S. at 691. In fact, in Warren Trading Post it was held

that a general statute permitting states to levy sales or

use taxes within certain federal areas did not apply to

Indian reservations because there was no suggestion that

Congress meant to give.states new power to tax federally

licensed Indian traders. 380 U.S. at 391, n.18. The

court's holding establishes that state taxation on Indian

reservations is an altogether different matter than state

taxation within other federal areas.

Oklahoma Tax Commission v. Texas Co., supra upheld

the validity of two Oklahoma taxes, a tax on the gross

value of petroleum production and an excise tax on each

barrel of petroleum produced, as applied to lessees of

Indian land. The taxes were expressly found to have an

"insubstantial" effect on the lessees. 336 U.S. at 351.

There was no claim that the federal government had occupied

the field to the exclusion of Oklahoma's authority to tax.

• The case simply marks the demise of the "federal instru

mentality" doctrine as applied to the lessees of Indian

land. The interests of the Indian owners were neither

presented to nor considered by the court. Nor was the

issue of the possible infringement of tribal sovereignty

before the court. The Supreme Court noted earlier, in

Oklahoma Tax Commission v. United States, 319 U.S. 598

(1943) (cited in Oklahoma Tax Commission v. Texas Co.,

supra fn. 37),

Worcester v. Georgia, 6 Pet (U.S.) 515, held that

a state might not regulate the conduct of persons in

Indian territory on the theory that the Indian tribes

were separate political entities with all the rights

of. independent status--a condition which has not existed

for many years in the State of Oklahoma. (319 U.S. at

602)

The court later stated that the Oklahoma Indians possessed

but a "remnant" of their former tribal sovereignty and

"have no effective tribal antonomy." 319 U.S. at 603.

See also Commissioner of Taxation v. Brun, supra.

In the case at bar, the allottees and the tribe

are represented and have asserted their rights and interests

protected and fostered by federal law. The Agua Caliente

Tribe is alive and well, and has imposed its own tax, which

-38-

• directly conflicts with the County's tax, pursuant to its

authority recognized in 28 U.S.C. § 1360(c). As the record

clearly shows, the County's tax has had a substantial impact

on the economic development of the Reservation. Oklahoma

Tax Commission v. Texas Co., supra is inapplicable because

Oklahoma's tax had no substantial effect, was not pre-empted

by comprehensive federal regulation, and did not interfere

with tribal sovereignty.

CONCLUSION

Imposition of Riverside County's possessory interest

tax upon lessees of the Indian trust lands of the Agua

Caliente Band of Mission Indians is proscribed by 28 U.S.C.

§§ 1360(a), 1360(b), and 1360(c). Furthermore, such taxa

tion would frustrate the federal Indian policy of fostering

economic development, would interfere with an area pre

empted by federal regulation, and would infringe upon the

tribal sovereignty of the Agua Caliente Band. The County's

tax is invalid on anyone of these grounds. The three

subsections of § 1360 provide three entirely separate grounds

for prohibiting the County from such taxation.

These legal principles governing this case must not

be obscured by the relative wealth of many members of the

Agua Caliente Band among their Indian brethren, nor by the

-39-

• attractiveness of the property which is theirs due to the

accidents of history. The Agua Calientes are the extra

ordinary case, but their fate in this case will be of pro

found influence upon all Indian tribes throughout California

and indeed, throughout the nation.

Congress and the Executive are best qualified to

resolve the complex problems involving the relations of

all the various, widely divergent Indian communities with

their surrounding localities.

Dated: April 15, 1970

Respectfully submitted,

ROBERT S. PELCYGER DAVID H. GETCHES California Indian Legal Services

By Robert S. pelcyge~ \

(Law Clerks William H. Cozad and Richard L. Perez assisted on the Brief.)

-40~

• ADDENDUM

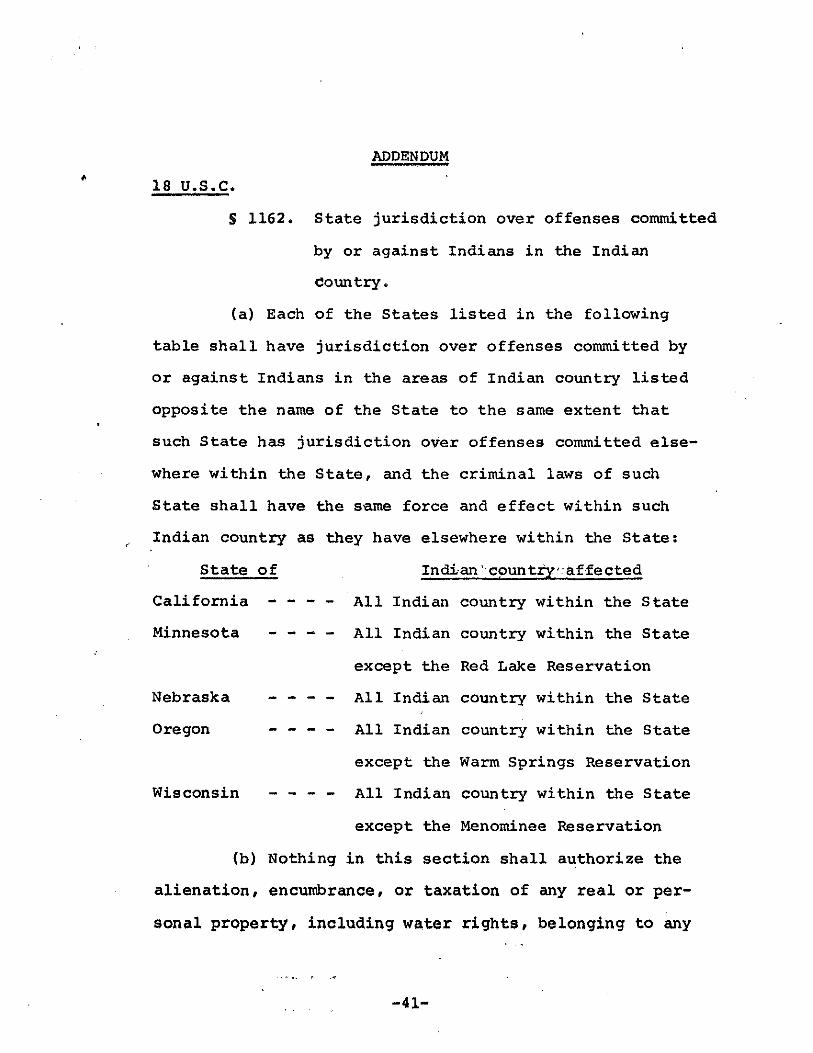

18 U.S.C.

§ 1162. State jurisdiction over offenses committed

by or against Indians in the Indian

Country.

(a) Each of the States listed in the following

table shall have jurisdiction over offenses committed by

or against Indians in the areas of Indian country listed

opposite the name of the State to the same extent that

such State has jurisdiction over offenses committed else

where within the State, and the criminal laws of such

State shall have the same force and effect within such

Indian country as they have elsewhere within the State:

State of Indian 'countiy':af·fected

California All Indian country within the State

Minnesota

Nebraska

Oregon

Wisconsin

- - - - All Indian country within the State

except the Red Lake Reservation

- - - - All Indian country within the State

- - - - All Indian country within the State

except the Warm Springs Reservation

- - - - All Indian country within the State

except the Menominee Reservation

(b) Nothing in this section shall authorize the

alienation, encumbrance, or taxation of any real or per

sonal property, including water rights, belonging to any

-41-

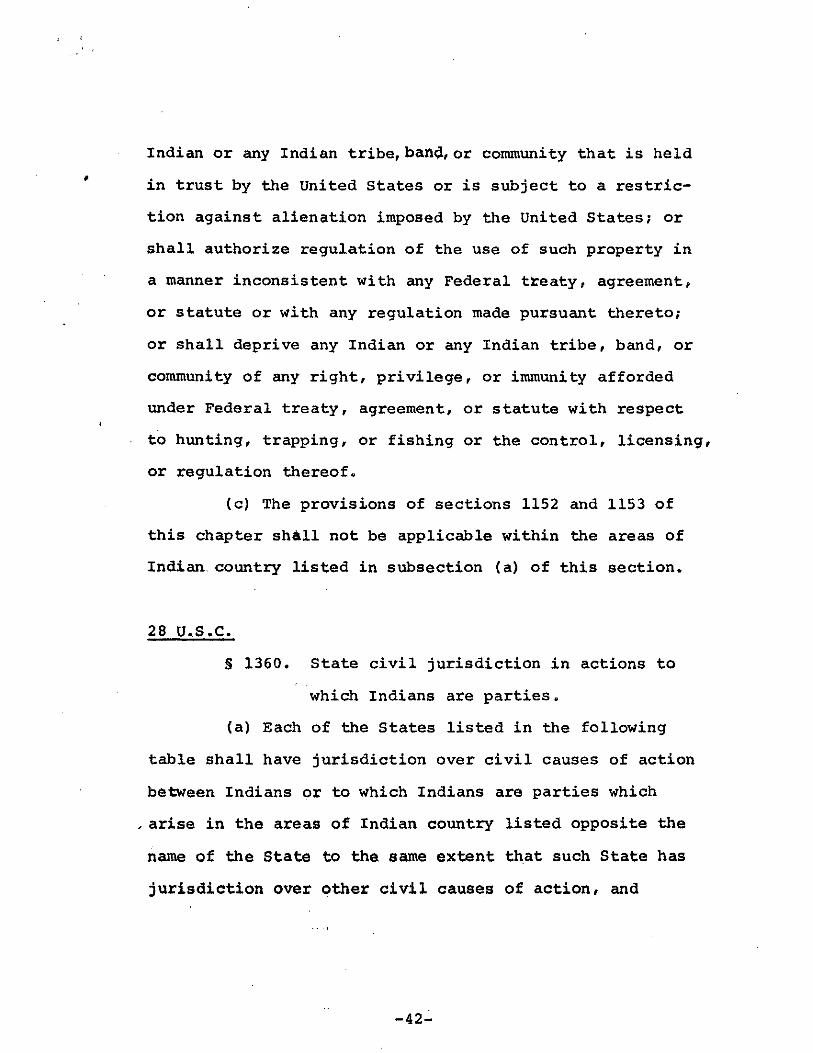

• Indian or any Indian tribe,ban~,or community that is held

in trust by the united States or is subject to a restric

tion against alienation imposed by the United States; or

shall authorize regulation of the use of such property in

a manner inconsistent with any Federal treaty, agreement,

or statute or with any regulation made pursuant thereto;

or shall deprive any Indian or any Indian tribe, band, or

community of any right, privilege, or immunity afforded

under Federal treaty, agreement, or statute with respect

to hunting, trapping, or fishing or the control, licensing,

or regulation thereof.

(c) The provisions of sections 1152 and 1153 of

this chapter shall not be applicable within the areas of

Indian. country listed in subsection (a) of this section.

28 U •. S.C.

S 1360. State civil jurisdiction in actions to

which Indians are parties.

(a) Each of the States listed in the following

table shall have jurisdiction over civil causes of action

between Indians or to which Indians are parties which

,arise in the areas of Indian country listed opposite the

name of the State to the same extent that such State has

jurisdiction over other civil causes of action, and

-42-

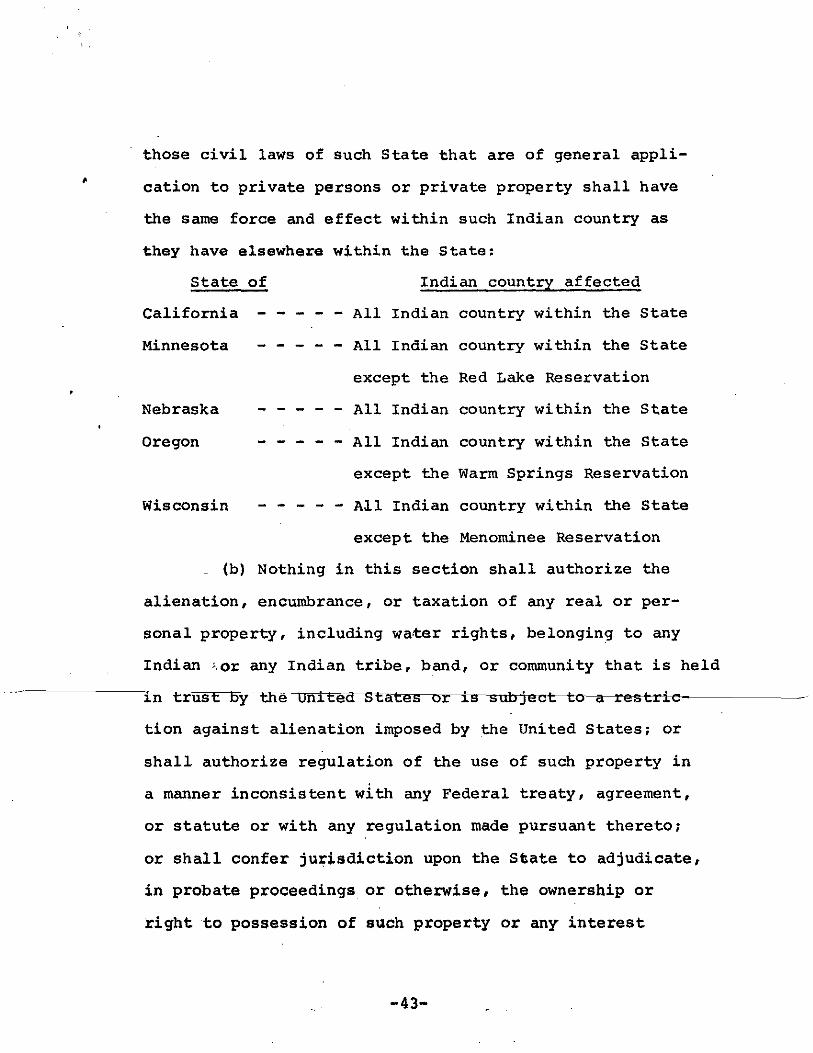

• those civil laws of such State that are of general appli

cation to private persons or private property shall have

the same force and effect within such Indian country as

they have elsewhere within the State:

State of Indian country affected

California - - - - - All Indian country within the State

Minnesota

Nebraska

Oregon

Wisconsin

- All Indian country within the State

except the Red Lake Reservation

- All Indian country within the State

- - - All Indian country within the State

except the Warm Springs Reservation

- - - - - All Indian country within the State

except the Menominee Reservation

_ (b) Nothing in this section shall authorize the

alienation, encumbrance, or taxation of any real or per

sonal property, including water rights, belonging to any

Indian '.or any Indian tribe, band, or community that is held

1n trust by the United States or is subject to a restrie

tion against alienation imposed by the United States; or

shall authorize regulation of the use of such property in

a manner inconsistent with any Federal treaty, agreement,

or statute or with any regulation made pursuant thereto;

or shall confer jurisdiction upon the State to adjudicate,

in probate proceedings or otherwise, the ownership or

right to possession of such property or any interest

-43-

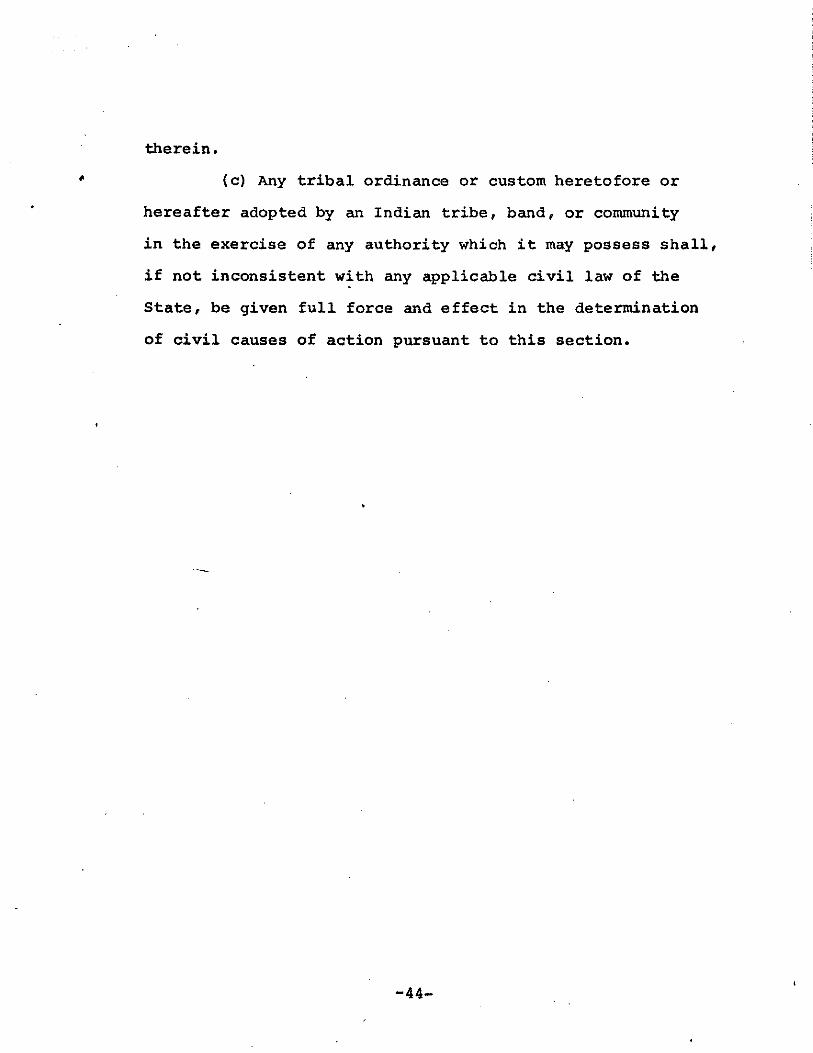

• therein.

(c) Any tribal ordinance or custom heretofore or

hereafter adopted by an Indian tribe, band, or community

in the exercise of any authority which it may possess shall,

if not inconsistent w~th any applicable civil law of the

State, be given full force and effect in the determination

of civil causes of action pursuant to this section.

-44-