agriculture, forestry & fisheries -...

52

agricul ture, forestry & fisheries Department: Agriculture, Forestry and Fisheries REPUBLIC OF SOUTH AFRICA

Transcript of agriculture, forestry & fisheries -...

agriculture,forestry & fisheriesDepartment:Agriculture, Forestry and FisheriesREPUBLIC OF SOUTH AFRICA

2015

Department: Agriculture, Forestry and FisheriesREPUBLIC OF SOUTH AFRICA

Printed and published by

Department of Agriculture, Forestry and FisheriesDirectorate: Communication ServicesPrivate Bag X144, Pretoria 0001

II

III

CONTENTS

ACRONYMS ................................................................................................................................................................... IV LIST OF TABLES ........................................................................................................................................................... IVLIST OF FIGURES ......................................................................................................................................................... VEXECUTIVE SUMMARY ................................................................................................................................................ VII

Chapter 1: Introduction and background

1.1. Introduction ............................................................................................................................................................. 1 1.2. Goals and key objectives of the report ................................................................................................................... 11.3. Key defi nitions and principles ................................................................................................................................. 1 1.4. Strategic role of sector cooperatives in economic growth ...................................................................................... 2 1.5. Methodological considerations for data collection .................................................................................................. 21.6. Limitations/scope of the report ............................................................................................................................... 31.7. Structure of the report ............................................................................................................................................. 3

Chapter 2: Profi ling of cooperatives in the sector

2.1. Geographic distribution of cooperatives ................................................................................................................. 3 2.2. Cooperatives according to subsector ..................................................................................................................... 42.3. Cooperatives according to commodities ................................................................................................................. 52.4. Cooperatives according to forms/levels .................................................................................................................. 52.5. Post production cooperatives ................................................................................................................................. 62.6 Cooperatives according to operational status ......................................................................................................... 7

Chapter 3: Membership and cooperative management

3.1. Membership in cooperatives ................................................................................................................................... 7 3.2. Gender analysis ...................................................................................................................................................... 83.3. Management in cooperatives ................................................................................................................................. 93.4. Educational level of cooperative managers ............................................................................................................ 10

Chapter 4: Cooperatives and employment

4.1. Introduction ............................................................................................................................................................. 114.2. Defi nition of employment ........................................................................................................................................ 114.3. Cooperative employment estimates (globally, regionally and locally) .................................................................... 114.4. Gender in cooperative employment ........................................................................................................................ 14

Chapter 5: Training support and capacity development

5.1. Introduction ............................................................................................................................................................. 145.2. Types of capacity building programmes for cooperatives ...................................................................................... 15 5.3. Cooperative compliance in the sector .................................................................................................................... 16

Chapter 6: Financial matters related to cooperatives in the sector

6.1. Capitalisation of cooperatives ................................................................................................................................. 186.2. The gearing ratio .................................................................................................................................................... 196.3. Sources of capital for cooperatives in the sector .................................................................................................... 196.4. Financial performance of cooperatives in the sector (annual turnover) .................................................................. 23

Chapter 7: Cooperatives and market access

7.1. Defi ning market access .......................................................................................................................................... 257.2. Challenges with market access ............................................................................................................................... 257.3. Types of markets accessed by cooperatives in the sector ..................................................................................... 26 7.4. Summary of formal markets supplied by sector cooperatives ................................................................................ 30 7.5. Landownership by cooperatives ............................................................................................................................. 30 7.6 Conclusion and recommendation ............................................................................................................................ 31

Annexures

Business analysis sheet (data collecting questionnaire) ............................................................................................... 33

Cooperatives and enterprise development business analysis sheet

IV

ACRONYMSARC Agricultural Research Council CODAS Cooperative Data Analysis System CIPC Companies and Intellectual Property Commission CICOPA International Organization of Industrial, Artisan, Service and Social Producers’ Cooperatives CRDP Comprehensive Rural Development Programme DAFF Department of Agriculture, Forestry and Fisheries DEDEA Department of Economic Development and Environmental Affairs DL Department of Labour DRDLR Department of Rural Development and Land Reform DSD Department of Social Development dti Department of Trade and Industry DWS Department of Water and Sanitation FAO Food and Agriculture Organization GDP Gross Domestic Product ICA International Cooperative Alliance IDC Industrial Development Corporation ILO International Labour Organization IYC International Year of Cooperatives LEDA Limpopo Economic Development Agency LRAD Land Redistribution for Agricultural Development MAFISA Micro Agricultural Financial Institutions of South Africa NDA National Development Agency NYDA National Youth Development Agency PTO Permission to occupy UN United Nations USD United States Dollar VDM Vhembe District Municipality ZAR South African Rand

LIST OF TABLESTable 1: Geographic distribution of cooperatives ......................................................................................................... 3Table 2: Cooperatives according to subsector s .......................................................................................................... 4Table 3: Cooperatives according to commodities ......................................................................................................... 5Table 4: Cooperatives according to forms .................................................................................................................... 5Table 5: Postproduction cooperatives .......................................................................................................................... 6Table 6: Cooperatives according to operational status ................................................................................................ 7Table 7: Global memberships in cooperatives ............................................................................................................. 8Table 8: Membership of cooperatives in provinces ...................................................................................................... 8Table 9: Cooperatives with managers and their gender ............................................................................................... 9Table 10: Level of education of cooperative managers ................................................................................................ 10Table 11: Global membership in cooperatives ............................................................................................................. 12Table 12: Memberships in Sub-Sahara Africa .............................................................................................................. 12Table 13: Job opportunities created by cooperatives in the sector .............................................................................. 13Table 14: Three year analysis of employment in cooperatives .................................................................................... 13Table 15: Type of employment according to gender .................................................................................................... 14Table 16: Institutional support and capacity development in cooperatives .................................................................. 15Table 17: Cooperative compliance in the sector .......................................................................................................... 17Table 18: Equity in cooperatives .................................................................................................................................. 19Table 19: Grants by DAFF ............................................................................................................................................ 20Table 20: Grants by external stakeholders in the Eastern Cape .................................................................................. 21Table 21: Grants by external stakeholders in Free State ............................................................................................. 21Table 22: Grants by external stakeholders in Gauteng ................................................................................................ 21Table 23: Grants by external stakeholders in Limpopo ................................................................................................ 22Table 24: Grants by external stakeholders in Mpumalanga ......................................................................................... 22

V

Table 25: Grants by external stakeholders in North West ............................................................................................ 22Table 26: Grants by external stakeholders in Western Cape ....................................................................................... 22Table 27: Loans by DAFF ............................................................................................................................................. 23Table 28: Loans by external stakeholders .................................................................................................................... 23Table 29: Comparison between grants and loans ........................................................................................................ 23Table 30: Global annual turnover by cooperatives ....................................................................................................... 24Table 31: Financial performance over a three-year period ........................................................................................... 24Table 32: Markets accessed by Eastern Cape cooperatives ....................................................................................... 26Table 33: Markets accessed by Free State cooperatives ............................................................................................. 26Table 34: Markets accessed by Gauteng cooperatives ................................................................................................ 27Table 35: Markets accessed by KwaZulu-Natal cooperatives ...................................................................................... 27Table 36: Markets accessed by Limpopo cooperatives ................................................................................................ 28Table 37: Markets accessed by Mpumalanga cooperatives ......................................................................................... 28Table 38: Markets accessed by Northern Cape cooperatives ...................................................................................... 29Table 39: Markets accessed by North West cooperatives ........................................................................................... 29Table 40: Markets accessed by Western Cape cooperatives ...................................................................................... 29Table 41: Summary of market opportunities for cooperatives ...................................................................................... 30Table 42: Landownership by cooperatives in provinces ............................................................................................... 31

LIST OF FIGURESFIG. 1: Geographical distribution of cooperatives ........................................................................................................ 4FIG. 2: Cooperatives per province according to subsectors ......................................................................................... 4FIG. 3: Graph depicting forms of cooperatives and provinces ..................................................................................... 6FIG. 4: Cooperatives in postproduction ........................................................................................................................ 6FIG. 5: Graphical presentation of cumulative membership in cooperatives ................................................................. 9FIG. 6: Cooperative managers according to gender .................................................................................................... 10FIG. 7: Graphical presentation of level of education of cooperative managers ............................................................ 11FIG. 8: Analysis of three year employment in cooperatives ......................................................................................... 13FIG. 9: Institutional capacity building and support ........................................................................................................ 16FIG.10: Graphical presentation of cooperative compliance in the sector ..................................................................... 18FIG. 11: Members’ contribution in cooperatives ........................................................................................................... 20FIG.12: Comparison between grants and loans ........................................................................................................... 23FIG. 13: Annual turnover in cooperatives ..................................................................................................................... 25FIG. 14: Graphical presentation of formal market opportunities for cooperatives ........................................................ 31FIG. 15: Pie chart of landownership in cooperatives .................................................................................................... 31

VI

VII

EXECUTIVE SUMMARYThe importance of the cooperative sector and its impact round the world continues to be studied and highlighted. However, the economic and social dimensions of this business model are yet to be fully understood and demonstrated. It is very diffi cult to determine how to support or aid cooperative development without reliable data on the size and impact of coop-eratives. The goal of the cooperative annual report, now in its fourth edition, is to increase and enhance the available data on cooperatives in order to present a more detailed account of their actual contribution to the socio-economic development of communities.

The 2014/15 edition presents the results of a data analysis on cooperatives in agriculture, forestry and fi sheries, using data of 1 788 cooperatives collected and captured on the Cooperative Data Analysis System (CODAS). The report quantita-tively measured the economic impact of cooperatives in the sector. It describes and quantifi es the magnitude of economic activity accounted for by sector cooperative businesses in the country. It also provides insights into sector cooperative ac-tivities, as well as into effective support measures for these organisations which can be used by farmers , in setting up and strengthening their collective organisation, and by the cooperative movement and government in their effort to encourage the establishment of cooperatives in the sector.

Of the 1 788 cooperatives whose data was used to prepare this report, 95% (1703) are involved in activities relating to agriculture, with only 60 cooperatives involved in fi shery related activities. Forest related cooperatives account for 1, 4% (25) of the total cooperatives. In terms of commodities, the vegetable commodity has been found to be dominant with about 24% of the cooperatives (amounting to 430) involved in vegetable production. This is followed by the livestock commod-ity at 21% (377 cooperatives). The number of cooperatives participating in post-production activities (value adding and agro-processing) has showed a steady increase over a three year period from 27 in 2012 to 60 in 2013 and 96 in 2014.In terms of the level at which the 1 788 cooperatives are formalised, 1 755 have been formalised as primary/producer co-operatives with 42 cooperatives at secondary level primarily to provide support services to producer cooperatives. A total of 41 930 farmers belong to cooperatives in the sector with 55% of these being females. Only 716 of the total cooperatives surveyed have full-time managers, which raises concerns on operational effi ciency and sustainability.

According to analysis performed, an additional 2 697 jobs were created by cooperatives in the sector in 2014/15. The department continues to provide support with training and capacity development to cooperatives in key identifi ed com-petencies such as fi nancial management, business planning, marketing, cooperative governance, etc. In terms of equity, there has been an increase of about R3,5 million invested by members in their cooperatives from 2013. A greater number of cooperatives are benefi ting from the departmental fi nancing support programmes, in particular, the Comprehensive Agricultural Support Programme (CASP), with 185 cooperatives supported to the amount of R120 million in the 2014/15 fi nancial year and one cooperative approved for support with R6,9 million through the AgriBEE Fund. Altogether 16 coop-eratives have been supported with production loans through Mafi sa amounting to R4,3 million. However, the private sector is still lagging behind in terms of providing fi nancial support to cooperatives in the sector.

There has been a slight increase in annual turnover from R134 million in 2013 to R157 million in 2014. Market access continues to be a challenge. Of the 245 cooperatives with access to formal markets, only 30 are selling to the retail chain supermarkets such as Shoprite, Pick n Pay, Boxer, etc. In terms of landownership, 406 cooperatives (23%) have title deeds to their land and 499 cooperatives (28%) use the permission to occupy method. Together all the cooperatives surveyed have a combined ownership of 645 583 ha.

The department continues to promote the establishment of commodity-based cooperatives to ensure a more focused approach by smallholder farmers. Support to existing cooperatives, through training and capacity development will be heightened to improve profi tability and competitiveness. An impact assessment study on the existing support instruments will be conducted in the current fi nancial year to determine the effectiveness thereof and inform future interventions.

VIII

1

CHAPTER 1:INTRODUCTION AND BACKGROUND

1.1 Introduction

Cooperatives are successful in economic development because they are commercial organisations that operate by a broader set of values than those associated with the limited pursuit of profi t alone. Firstly, they are businesses that practise economic fairness by ensuring equal access to markets and services among an open and voluntary membership base. Because they are owned by the consumers of the services they provide, cooperatives tend to make decisions that balance the need for profi tability with the greater interests of the community which they serve.

Taken as a whole, the cooperative movement is Africa’s biggest non-governmental organisation that plays a signifi cant role in many national economies and has created a great number of salaried jobs and self-employment opportunities. Yet, the role of cooperatives in employment creation has been neglected by employment planners, cooperative promotion agen-cies, social partners and donor organisations alike. In many African countries, cooperatives were considered primarily as instruments to execute certain economic or political functions on behalf of the government, not as autonomous, member based organisations that create and consolidate self-employment.

The importance of the cooperative sector and its impact round the world continues to be studied and highlighted. However, the economic and social dimensions are yet to be fully understood and demonstrated. It is very diffi cult to determine how to support or aid the development of cooperatives without reliable data on their size and impact. Despite the much publicised United Nation’s International Year of Cooperatives (IYC), clear, concise and reputable data on the number of cooperatives in the country, number of members, turnover, employees and assets do not exist.

The goal of the ongoing annual publications on the state of cooperatives in the agriculture, Forestry and Fisheries coopera-tives, now in its fourth edition, is to increase and enhance the availability of data on cooperatives in order to present a more detailed view of their actual contribution to the socio-economic development of the country. The Department of Agriculture, Forestry and Fisheries (DAFF) collect available economic and social data on cooperative enterprises in the country with the support of provincial departments of agriculture (PDAs) and other stakeholders in an effort to demonstrate the existence and viability of this model as an alternative to the traditionally dominant for-profi t business model.

The 2014 edition presents results of data analysis of 1 788 sector cooperatives whose data is captured on the Cooperative Data Analysis System (CODAS). As in the previous editions, the report is intended to be exploratory, and does not attempt to be all-inclusive rather, but to be an overview of the signifi cant contribution of cooperatives in the sector to economic growth and job creation imperatives.

The goal is to increasingly move beyond the current cooperatives used for analysis to include all operational cooperatives registered with the Companies and Intellectual Property Commission (CIPC) so as to have a more accurate measure of their impact on the economy. To accomplish this, a more aggressive data collection strategy, which include deepening collaborations with, among others the cooperative movement, commodity associations, CIPC, local government and other community-based organisations operating at local level will have to be explored.

1.2 Goals and key objectives of the report

This report aims at contributing to a better understanding of the contribution of cooperatives in the sector to the key gov-ernment imperatives of food security, job creation and contribution to the economic growth. The report further seeks to highlight some of the key challenges faced by cooperatives, such as access to markets, fi nance, infrastructure, skills, technology, etc. In summary, the report aims to achieve the following:

Raise the awareness and profi le of cooperatives in the sector;

Highlight some of the challenges facing sector cooperatives;

Demonstrate the economic and social importance of cooperatives in the sector; and

Model good practice and highlight successful cooperative business models and innovative approaches.

1.3 Key defi nitions and principles

The International Cooperative Alliance (ICA) defi nes a cooperative as an autonomous association of persons united volun-tarily to meet their mutual economic, social, and cultural needs and aspirations through a jointly-owned and democratical-ly-controlled enterprise. Cooperatives are based on the values of self-help, self-responsibility, democracy, equality, equity and solidarity. In the tradition of their founders, cooperative members believe in the ethical values of honesty, openness, social responsibility and caring for others. The cooperative principles are guidelines by which cooperatives put their values into practice, including voluntary and open membership, democratic member control, member economic participation,

2

autonomy and independence, education, training and information, cooperation among cooperatives and concern for com-munity.

1.3.1. Agricultural cooperatives

An agricultural cooperative is a cooperative that produces, processes or markets agricultural products and supplies agri-cultural inputs and services to its members. Put another way, agricultural cooperatives pool the production and resources of farmers and rural entrepreneurs in order to maximise the benefi ts for their members. Agricultural cooperatives can be classifi ed into service or production cooperatives. Production cooperatives involve farmers who operate the cooperative on jointly owned agricultural plots/farms while service cooperatives are more common and members carry out their activities independently, and the cooperative provides them with a range of services, including machinery, processing, transport, packaging, distribution, marketing and information.

1.3.2. Forest cooperatives

As the name indicates, forest owner cooperatives are owned and democratically controlled by individuals, families and organisations that own forest land. They provide a variety of services to their landowner members, especially forest man-agement and timber marketing services. Forest user cooperatives, often referred to as community forest management groups, comprise local community residents who make use of state-owned or communal forests for fi rewood, charcoal, timber, non-timber forest products, hunting, eco-tourism and other activities.

1.3.3. Fishery cooperatives

These are cooperatives that produce, process, sell and market fi shery products and supply fi shery inputs and services to their members. They do fi shing, extraction of aquatic animals, aquatic plants from oceans, rivers, lakes and dams. Fishing is done on the basis of obtaining fi shing and other related business licences to do business in specifi ed waters or areas.

1.4. Strategic role of sector cooperatives in economic growth

Despite its signifi cant and positive impact on economic and social development, the cooperative form of enterprise con-tinues to be underutilised and poorly understood. Very few people today are aware that an estimated 100 million jobs are provided by cooperatives to salaried employment—which is 20% more than multinational corporations. This is in fact a conservative fi gure considering that cooperatives provide not only direct employment, but also self-employment, indirect and induced employment.

For example, in agriculture, where the majority of cooperatives are still found, cooperatives maintain farmers’ ability to be self-employed given that for many farmers the fact that they are members of a cooperative and derive income from the ser-vices, allows them to continue to farm and contribute to rural community development. In both urban and rural contexts, the impact of cooperatives in providing income to members creates additional employment through multiplier effects, including enabling other enterprises to grow and, in turn, provide local jobs (the indirect employment capacity of cooperatives).

According to the Food and Agriculture Organization of the United Nations (FAO), agriculture, forestry, fi sheries and live-stock cooperatives are the main sources of employment and income in rural areas, where most of the world’s poor and hungry people live. Agriculture cooperatives play an important role in supporting small agricultural producers and mar-ginalised groups such as young people and women. They empower their members economically and socially and create sustainable rural employment through business models that are resilient to economic and environmental shocks.

Cooperatives offer small agricultural producers opportunities and a wide range of services, including improved access to markets, natural resources, information, communications, technologies, credit, training and warehouses. They also facil-itate smallholder producers’ participation in decision making at all levels, support them in securing land-use rights, and negotiate better terms for engagement in contract farming and lower prices for agricultural inputs such as seeds, fertiliser and equipment. Through this support, smallholder producers can secure their livelihoods and play a greater role in meeting the growing demand for food on local, national and international markets, thereby contributing to poverty alleviation, food security and the eradication of hunger.

1.5. Methodological considerations for data collection

The choice of the many methods for collecting data will depend on the variables to be measured and the source and the resources available. In many cases, there is a natural way to collect particular variables. The choice of method is infl u-enced by the data collection strategy, the type of variable, the accuracy required, the collection point and the skill of the enumerator.

3

For the purposes of this report, a data collecting questionnaire specifi cally designed for this project and which is the core of the process of data collection, was used. The advantage of using a questionnaire lies in its ability to be distributed to a large number of people. It also saves time and money as compared to interviews. People are more truthful while respond-ing to the questionnaires regarding controversial issues in particular owing to the fact that their responses are anonymous. However, they also have drawbacks. The majority of the people who receive questionnaires do not return them and those who do might not be representative of the originally selected sample.

To facilitate its completion among diverse groups of people, the questionnaire is made available to PDAs and other stake-holders. Data collection should be conducted at intervals suffi ciently frequent for management purposes. New data is collected on a regular basis while existing data is reviewed annually. Data collected directly from the primary source make it possible to collect a wider range of data than those available in existing databases.

1.6. Limitations/scope of the report

To stimulate interest and raise awareness on the importance of cooperatives, particularly in the agriculture, forestry and fi sheries sector, greater effort in data collection and reporting on the economic impact of these cooperatives is needed. This report is thus presented to help stimulate interest and raise the profi le of cooperatives in the sector. The report is there-fore only limited to all cooperatives in the sector whose data has been collected and captured on the cooperative database.

1.7. Structure of the report

This report is structured as follows: Chapter 2 provides profi les of cooperatives surveyed in terms of commodities, subsec-tor, forms/levels, level of activity and operational status. The third chapter presents an analysis of membership in coopera-tives as a key ingredient/component of the cooperative model, management of cooperatives and the educational levels of cooperative managers. This is followed by analysis of cooperative employment in chapter 4. Chapter 5 focuses on training and capacity development as a tool towards the successful realisation of goals by cooperatives. Capitalisation and fi nancial performance of cooperatives are dealt with in Chapter 6 and Chapter 7 looks at issues relating to market access. Finally, the last chapter provides the concluding remarks for this report.

CHAPTER 2:PROFILING OF COOPERATIVES IN THE SECTOR

2.1. Number of cooperatives profi led

Chapter 2 of this report focuses on profi ling the cooperatives that formed the basis of analysis performed to generate this report. This include their geographic distribution, classifi cation in terms of subsectors, forms/levels, commodities they are involved in, categorisation in terms of those involved in primary production as well as those in post- production activities as well as their operational status. A profi le of a total of 1 788 sector cooperatives whose data is captured on CODAS is presented in this section.

Province Number of cooperatives

Eastern Cape 212

Free State 89

Gauteng 106

KwaZulu-Natal 383

Limpopo 384

Mpumalanga 224

Northern Cape 107

North West 222

Western Cape 61

Total 1 788

Table 1: Geographic distribution of cooperatives

4

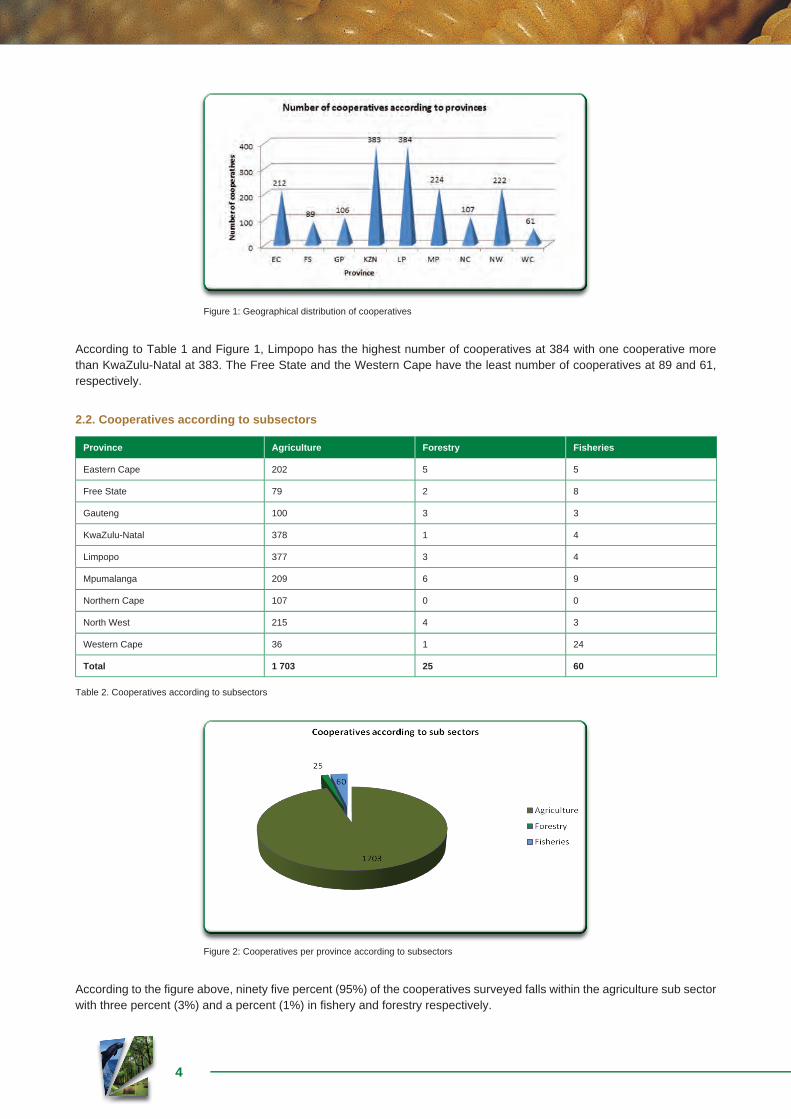

Figure 1: Geographical distribution of cooperatives

According to Table 1 and Figure 1, Limpopo has the highest number of cooperatives at 384 with one cooperative more than KwaZulu-Natal at 383. The Free State and the Western Cape have the least number of cooperatives at 89 and 61, respectively.

2.2. Cooperatives according to subsectors

Province Agriculture Forestry Fisheries

Eastern Cape 202 5 5

Free State 79 2 8

Gauteng 100 3 3

KwaZulu-Natal 378 1 4

Limpopo 377 3 4

Mpumalanga 209 6 9

Northern Cape 107 0 0

North West 215 4 3

Western Cape 36 1 24

Total 1 703 25 60

Table 2. Cooperatives according to subsectors

Figure 2: Cooperatives per province according to subsectors

According to the fi gure above, ninety fi ve percent (95%) of the cooperatives surveyed falls within the agriculture sub sector with three percent (3%) and a percent (1%) in fi shery and forestry respectively.

5

2.3. Cooperatives according to commodities

Commodity Number of cooperatives in a province

EC FS GP KZN LP MP NC NW WC Total

Beekeeping 2 0 1 2 3 2 1 1 1 13

Cotton 0 0 0 0 0 13 0 0 0 13

Crops 61 5 5 73 97 38 4 52 1 336

Fisheries 5 8 3 4 4 9 0 3 24 60

Forestry 5 2 3 1 3 6 0 4 1 25

Flowers 0 0 1 0 1 0 0 0 1 3

Fruit 3 1 1 2 9 0 0 3 1 20

Herbs 0 0 1 0 1 0 0 0 0 2

Input supply 6 6 0 3 10 5 1 6 3 40

Livestock 36 27 5 39 36 25 78 60 9 315

Marketing/value add-ing/processing

7 5 13 2 13 6 0 3 4 53

Mixed farming 10 5 0 18 8 9 5 30 0 85

Poultry 28 15 28 113 103 44 12 30 4 377

Sugar cane 0 0 0 12 0 0 0 0 0 12

Vegetables 47 15 45 114 96 67 6 30 10 430

Wool 2 0 0 0 0 0 0 0 2 4

Total 212 89 106 383 384 224 107 222 61 1788

Table 3: Cooperatives according to commodities

According to Table 3, the highest number of cooperatives (430) constituting 24% are involved in vegetable production and the bulk of these are found in the KwaZulu-Natal. The second dominant commodity is poultry at 21% (377) cooperatives with KwaZulu-Natal still the leading province.

2.4. Cooperatives according to forms/levels

In South Africa the structure of cooperatives follow a four-tier pyramidal structure with primary cooperatives at the bottom of the pyramid, followed by secondary cooperatives, tertiary and the apex. The table below indicates the number of coop-eratives in the sector according to levels.

ProvinceTypes of cooperatives

Primary Secondary Tertiary Apex

Eastern Cape 205 7 0 0

Free State 87 2 0 0

Gauteng 104 2 0 0

KwaZulu-Natal 372 11 0 0

Limpopo 379 5 0 0

Mpumalanga 215 9 0 0

Northern Cape 107 0 0 0

North West 218 4 0 0

Western Cape 59 2 0 0

Total 1 746 42 0 0

Table 4: Cooperatives according to types

6

Figure 3: Graph depicting forms of cooperatives and provinces

Fig.3. shows that about 1 746 cooperatives have been formalised at primary level and 42 at secondary level. Primary cooperatives are involved in primary production of goods and services while secondary cooperatives are established by primary cooperatives to provide them with support services that will enhance their sustainability.

2.5. Post-production cooperatives

Province Number of cooperatives per category

Processing Marketing Input supply

Eastern Cape 3 7 3

Free State 5 0 6

Gauteng 6 7 2

KwaZulu-Natal 1 1 3

Limpopo 9 5 10

Mpumalanga 2 5 4

Northern Cape 0 0 1

North West 3 0 6

Western Cape 4 0 3

Total 33 25 38

Table 5: Post-production cooperatives

Figure 4: Cooperatives in postproduction

7

According to Fig 4, of the total number of cooperatives (1 788) only 96 (5%) cooperatives are involved in post-production related activities. This implies that smallholder farmers are unable to derive optimal returns on the production due to lack of value addition and processing.

2.6. Cooperatives according to operational status

ProvinceOperational status

A B C D E F G H I

Eastern Cape 104 63 13 9 21 2 0 0 0

Free State 34 18 5 5 24 3 0 0 0

Gauteng 21 39 13 4 22 6 1 0 0

KwaZulu-Natal 116 124 24 9 59 51 0 0 0

Limpopo 163 96 17 12 68 25 3 0 0

Mpumalanga 118 62 44 0 0 0 0 0 0

Northern Cape 46 30 7 11 5 7 0 0 1

North West 89 52 13 2 46 18 2 0 0

Western Cape 25 9 5 1 18 3 0 0 0

Total 716 493 141 53 263 115 6 0 1

Table 6: Cooperatives according to operational status

A - Operational and expandingB - Operational and stableC - Unstable and have potentialD - unstable with no potentialE - New and operationalF - Dormant with potentialG - Dormant with no potentialH - Liquidation I - Closed

Table 6 shows that 716 (40%) of cooperatives are classifi ed as operational and expanding, while 493 (28%) fall within the operational and stable category.

CHAPTER 3: MEMBERSHIP AND COOPERATIVE MANAGEMENT

3.1 Membership in cooperatives

Cooperatives are voluntary organisations open to all persons able to use their services and willing to accept the respon-sibilities of membership, without gender, social, political, racial or religious discrimination. Inherent in this principle is the idea that cooperatives must allow and tolerate a free exchange of ideas. When discussion is complete, members vote and the majority opinion becomes policy. By extension, it simply means that cooperatives without members who consume their services will not function. Membership, therefore, becomes a critical component without which cooperatives will not get off the ground.

Membership is at the core of cooperative enterprises. Agriculture and food cooperatives represent a signifi cant portion of the global cooperative sector in developed and developing countries. Thirty per cent (30%) of the 300 largest cooperatives are found in the agricultural sector. These can assume a variety of forms, from small, grassroots associations to unions, federations and chambers of agriculture. The FAO estimates global membership of cooperatives to be more than 1 billion as illustrated by Table 7 on the next page with a large proportion in the agricultural sector.

8

Recent statistics show that out of 100 Africans, at least seven people are members of a cooperative and the total number of cooperatives in most countries has continued to grow.

The table below provides a breakdown of cooperative membership according to sectors worldwide as well as the number of cooperatives thereof.

Sector No. of cooperatives No. of members

Banking/credit unions 210,559 703,070,123

Insurance 3,644 248,864

Agriculture 1,224,650 122,120,167

Utilities 1,714 19,858,921

Grocery/consumer 81,437 97,869,940

Worker 84,799 4,369,600

Housing 15,247 16,383,048

Health 1,700 3,441,221

Education and social 87,998 21,876,054

Purchasing or marketing 41,865 26,256,054

Other or undefi ned 760,985 56,296,177

Worldwide total 2,514,598 1,071,790,167

Table 7: Global memberships in cooperatives (Source: UN Secretariat Results of 2014)

3.1.2. Membership of cooperatives in provinces

Province Total Male Female Youth People living with disabilities

Eastern Cape 8 627 3 650 4 977 1 092 115

Free State 1 274 729 545 159 6

Gauteng 1 246 557 689 280 45

KwaZulu-Natal 8 487 3 046 5 441 1 175 73

Limpopo 11 100 5 882 5 218 946 135

Mpumalanga 5 574 2 438 3 136 568 45

Northern Cape 1 765 776 989 237 10

North West 3 160 1 537 1 623 337 33

Western Cape 697 450 247 34 6

Total 41 930 19 065 22 865 4 828 468

Table 8: Membership of cooperatives in provinces

Table 8 indicates that the 1 788 cooperatives have a combined membership of 41 930, of which 19 065 (45%) consist of males and 22 865 (55%) females. Youth and People living with disabilities constitute 12 % (4828) and 1% (468) respec-tively.

3.2. Gender analysis

Gender refers to the social attributes and opportunities associated with being male or female and the relationships between women and men and girls and boys, as well as the relations between women and those between men. These attributes, opportunities and relationships are socially constructed and are learned through socialisation processes. They are context/time-specifi c and changeable. Gender determines what is expected, allowed and valued in a women or a man in a given context. In most societies there are differences and inequalities between women and men in responsibilities assigned,

9

activities undertaken, access to and control over resources, as well as decision-making opportunities. Gender is part of the broader socio-cultural context. Other important criteria for socio-cultural analysis include class, race, poverty level, ethnic group and age.

Gender plays a signifi cant role in cooperatives particularly those in rural areas where culture is still observed and practiced.

Figure 5: Graphical presentation of cumulative membership in cooperatives

3.3. Management in cooperatives

Cooperatives believe that management is not only benefi cial from a human and social point of view, but also a key com-petitive asset for a company. This conviction originates both from real life examples and academic research. One of the challenges facing cooperatives is their inability to attract suitably qualifi ed managers, partly owing to the perceived low or poor remunerations offered by these enterprises.

Management combines ideas, processes, materials, facilities and people to effectively provide needed services to mem-ber-owners. Managing a cooperative can be challenging and diffi cult. It involves not only managing resources and busi-ness operations, as in other businesses, but also dealing with problems stemming from the cooperative’s distinctive char-acteristics. Because the cooperative’s members are both owners and patrons, special relationships and problems arise concerning member and board of director roles and responsibilities. Management in cooperatives involves mobilisation of human skills, processes, as well as fi nancial and technological resources so that the cooperatives’ goals can be reached.

3.3.1 Cooperatives with managers and their gender

Province Total number of co-ops withmanagers

Male Female Youth People livingwithdisabilities

Eastern Cape 124 93 31 2 1

Free State 48 30 18 0 0

Gauteng 73 48 25 0 0

KwaZulu-Natal 147 52 95 2 0

Limpopo 93 92 1 1 1

Mpumalanga 117 50 67 5 0

Northern Cape 12 7 5 0 0

North West 74 52 22 3 0

Western Cape 28 24 4 0 0

Total 716 448 268 13 2

Table 9: Cooperatives with managers and their gender

10

Table 9 shows the total number of cooperatives with managers and an analysis in terms of gender, youth and people living with disabilities. Accordingly, 716 cooperatives have full-time managers. In terms of gender, 448 of the 716 managers are males as compared to their female counterparts at 268. Only 13 managers fall within the youth category and 2 managers are living with disabilities. The fi gure below provide a graphical representation of the gender analysis for cooperative man-agers.

Figure 6: Cooperative managers according to gender

3.4. Educational level of cooperative managers

Education is a central principle of the cooperative movement, enshrined in the 5th principle of the cooperative identity, which states, “Cooperatives provide education and training for their members, elected representatives, managers, and employees so they can contribute effectively to the development of their cooperatives,” The need for higher education and training in business management, and specifi cally for programs that refl ect the unique character of the cooperative model, has been recognised as a challenge for the movement.

Cooperative managers, fi nding themselves in a completely new context, must be trained to acquire appropriate skills, enabling them to manage rather than simply execute orders handed down from above and to take initiatives aimed at strengthening the cooperative. Training should cover business skills, accounting, and raising more investment capital from internal and member sources (rather than counting on external (usually government) sources, and looking to the members and the Board for guidance). Managers will also have to learn that they are working for the member-owners of the cooper-ative and not directing docile peasants. All managers will eventually have to be reconfi rmed by the membership. Training will be more effective if it places more stress on improving business effi ciency and member services and if trainees have a say in determining the content of programmes, and in assessing the trainers.

Level of education of cooperative managers

Education level Number of managers

Primary 79

Secondary 327

Tertiary 122

Specialised 49

Unknown 139

Total 716

Table 10: Level of education of cooperative managers

In terms of the level of education of cooperative managers, 327 of the 716 managers have studied up to secondary level viz. Grade 12 while 122 possesses post-matric qualifi cations. Forty nine (49) managers have specialised skills such as poultry production, farm management, plant production, etc.

11

Figure 7: Graphical presentation of level of education of cooperative managers

CHAPTER 4:COOPERATIVES AND EMPLOYMENT

4.1. Introduction

Cooperatives have a comparative job creation advantage over other types of enterprises for the following reasons:

they are labour intensive by nature;

they are cost-effective because of member commitment and participation;

they generate economies of scale and scope through horizontal and vertical integration;

they establish links between the informal and the formal sectors; and

they put economic and social development on a broader base.

Worker-owned cooperatives provide their members with decent, permanent jobs while client-owned cooperatives, which are predominant in the agricultural sector, can stabilise existing self-employment in rural areas. Financial cooperatives can mobilise savings among the poorest and therefore accumulate capital for productive investment while social cooperatives provide self-employed workers with a minimum of social security and create jobs in the social service sector.

4.2. Defi nition of employment

The meaning of the term employment used in this study follows the International Labour Organisation’s (ILO) defi nition, according to which “employment covers any work, be it for wage or salary, profi t or family gain”, and includes both “paid employment” and “self-employment”, taking into consideration that “employers, own-account workers and members of producers’ cooperatives should be considered as in self-employment”.

Rural employment is any activity, occupation, work, business or service performed by rural people by force or for remuner-ation, profi t, social or family gain, in cash or kind, including under a contract of hire, written or oral, expressed or implied and without regard to whether the service is performed on a self-directed, part-time, full-time or casual basis. This defi nition in-cludes farmers, fi shers, forest users, pastoralists, those performing domestic work, and other self-employed rural peoples, temporary, casual, piece-rate, own-account, migrant, and home-based workers (vegetable market vendors, day labourers, artisans, etc.) in the informal sector; part or full-time contract workers, farmers, sharecroppers, and tenants; small, medium and large farm, food processing, and off-farm enterprises; and both unionised and unorganised workers.

4.3. Cooperative employment estimates (globally, regionally and locally)

4.3.1 Global estimates

Presented for the fi rst time at the Second International Summit of Cooperatives held in Quebec, Canada from 06 to 09 October 2014, the study “Cooperatives and employment: a global report” carried out by the ICA’s International Organisa-tion of Industrial, Artisanal and Service Producers’ Cooperatives (CICOPA), the Alliance›s sector for industrial and service cooperatives, discusses the signifi cance of cooperative employment globally, both quantitatively and qualitatively. It shows

12

how cooperatives contribute to resilient employment, a sustainable economy and the well-being of people at work, making up almost 12% of the entire employed population of the G20 countries.

Together cooperatives employ over twelve (12) million persons or roughly 0,2% of the world’s population. In relative terms, this is slightly larger than the entire adult population of Ecuador. The summit illustrated more clearly how important the cooperative movement is to the world economy. As cited in various studies that were presented during the summit, there are 2,6 million cooperatives worldwide, with 1 billion members and 12,6 million jobs. Within the G20 nations, cooperatives account for 12% of all jobs and annual revenue of US$3 000 billion.

Sector No. of cooperatives No. of members No. of employees

Banking/credit unions 210 559 703 070 123 2 452 130

Insurance 3 644 248 864 961 409

Agriculture 1 224650 122 120 167 1 181 682

Utilities 1 714 19 858 921 94 882

Grocery/consumer 81 437 97 869 940 875 181

Worker 84 799 4 369 600 1 218 751

Housing 15 247 16 383048 102 823

Health 1 700 3 441 221 153 180

Education and social 87 998 21 876 054 497 445

Purchasing or marketing 41 865 26 256 054 3 402 008

Other or undefi ned 760 985 56 296 177 1 671 257

Total worldwide 2 514 598 1 071 790 167 12 610 748

Table 11: Global membership in cooperatives (Source: UN Secretariat Results of 2014)

4.3.2. Regional estimates

Region Co-ops Membership Employee

Africa-Sub Sahara 85 260 18 509 605 10 914

Table 12: Memberships in Sub-Sahara Africa (Source: UN Secretariat Results of 2014)

Table 12 above indicates that Africa-Sub-sahara accounts for about ten thousand jobs from eighty fi ve thousand cooper-atives with a combined membership of over eighteen million (Statistics of South African cooperatives are not included in these fi gures).

13

4.3.3. Employment opportunities created by cooperatives in the sector (South Africa)

ProvinceNature of employment

Permanent Part time

2013/14 2014/15 Variance 2013/14 2014/15 Variance

Eastern Cape 1504 1 738 234 318 318 0

Free State 128 814 686 46 83 37

Gauteng 463 651 188 58 61 3

KwaZulu-Natal 702 868 166 542 988 446

Limpopo 694 1 056 362 611 798 187

Mpumalanga 722 855 133 264 293 29

Northern Cape 42 46 4 15 60 45

North West 461 561 100 196 205 9

Western Cape 170 170 6 82 150 68

Total 4 886 6 759 1 879 2 132 2 956 824

Table 13: Job opportunities created by cooperatives in the sector

4.3.3.1. Three-year analysis of employment in cooperatives.

Employment type 2012/13 2013/14 2014/15

Permanent 2 885 4 886 6 759

Casual 2 104 2 132 2 956

Total 4 989 7 018 9 715

Table 14: Three-year analysis of employment in cooperatives

The summary above refl ects a cumulative job opportunities created by cooperatives over a three year period (both perma-nent and seasonal) of 9715 jobs.

Figure 8 : Analysis of three-year employment in cooperatives

14

4.4. Gender in cooperative employment

Province

Type of employment

Permanent Casual

Male Female Male Female

Eastern Cape 747 1 013 147 149

Free State 423 394 48 32

Gauteng 267 387 18 40

KwaZulu-Natal 364 497 407 588

Limpopo 391 665 321 477

Mpumalanga 309 546 117 176

Northern Cape 31 12 37 26

North West 262 299 115 90

Western Cape 127 49 105 39

Total 2 921 3 862 1315 1 617

Table 15: Type of employment according to gender

The outcome of gender analysis as depicted by the table 15 above indicates that more females are employed by the coop-eratives than their male counterparts.

CHAPTER 5:TRAINING SUPPORT AND CAPACITY DEVELOPMENT

5.1. Introduction

The increasingly competitive environment requires cooperative enterprises to develop their capacity to continually re-invent themselves and offer new goods and better services. Otherwise, their chances of maintaining and increasing their share of the market are limited. Cooperatives often function in a tough business environment where previous state-maintained protection no longer applies. It is in this context that cooperative entrepreneurship becomes a key enabler for cooperatives to successfully meet the challenges they face.

The core tools cooperatives need in order to fl ourish are advice on capacity building, entrepreneurship development, leadership training, market research, fi nancial management, inter-cooperative networking and federation building. In all cooperative endeavours, members’ mobilisation and sensitisation is a central issue. The sustainability of a cooperative enterprise, as well as its failure, is very much connected with the understanding and sense of ownership members have in respect of their enterprises. The development of capacities in cooperative organisations should leave behind some tradi-tional indicators of success in private enterprises, although they also operate in the same market environments.

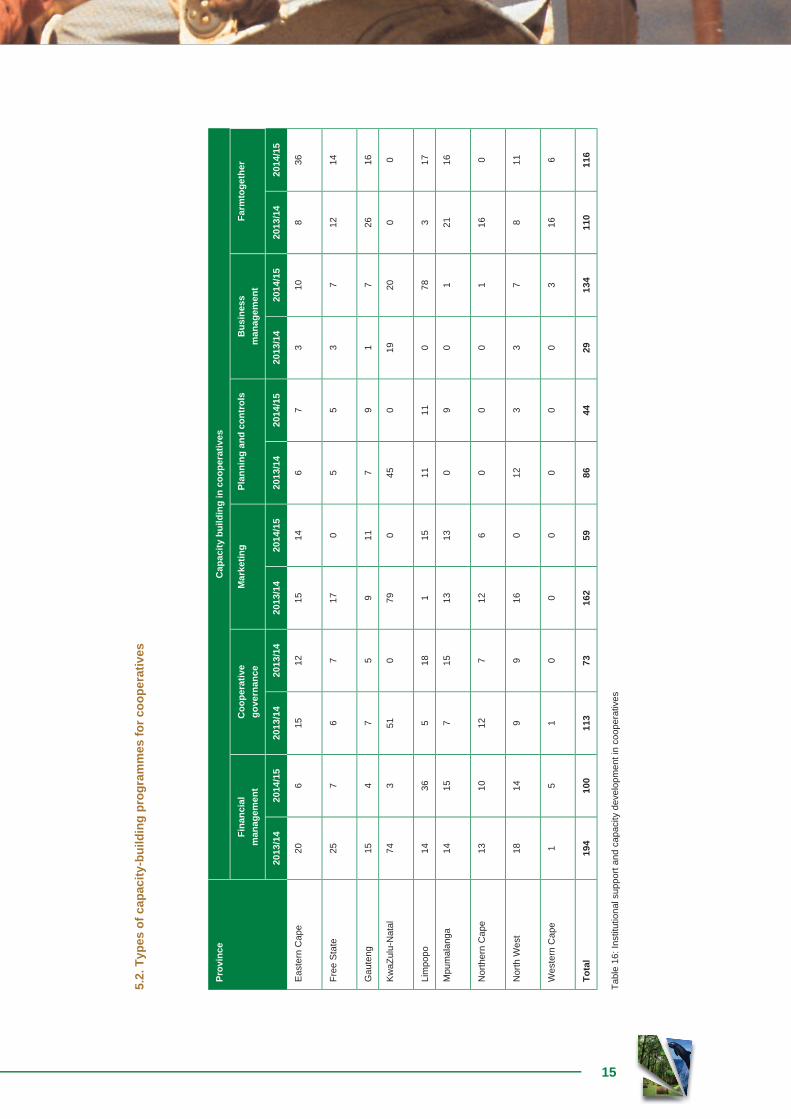

In order to appraise capacity in sector cooperatives, key competency areas were identifi ed as crucial for a cooperative to be able to manage its affairs effectively. The table on the next page lists these competencies and the number of coopera-tives that were exposed through training.

15

Tab

le 1

6: In

stitu

tiona

l sup

port

and

cap

acity

dev

elop

men

t in

coop

erat

ives

5.2.

Typ

es o

f ca

pac

ity-

bu

ildin

g p

rog

ram

mes

fo

r co

op

erat

ives

Pro

vin

ceC

apac

ity

bu

ildin

g in

co

op

erat

ives

Fin

anci

alm

anag

emen

tC

oo

per

ativ

eg

ove

rnan

ceM

arke

tin

gP

lan

nin

g a

nd

co

ntr

ols

Bu

sin

ess

man

agem

ent

Far

mto

get

her

20

13/1

420

14/1

520

13/1

420

13/1

420

13/1

420

14/1

520

13/1

420

14/1

520

13/1

420

14/1

520

13/1

420

14/1

5

Eas

tern

Cap

e20

615

1215

146

73

108

36

Fre

e S

tate

257

67

170

55

37

1214

Gau

teng

15

47

59

117

91

726

16

Kw

aZul

u-N

atal

743

510

790

450

1920

00

Lim

popo

1436

518

115

1111

078

317

Mpu

mal

anga

1415

715

1313

09

01

2116

Nor

ther

n C

ape

1310

127

126

00

01

160

Nor

th W

est

1814

99

160

123

37

811

Wes

tern

Cap

e1

51

00

00

00

316

6

To

tal

194

100

113

7316

259

8644

2913

411

011

6

16

Figure 9: Institutional capacity building and support

According table 16 and fi gure 9 above, the number of cooperatives supported with training in the identifi ed areas is in-creasing.

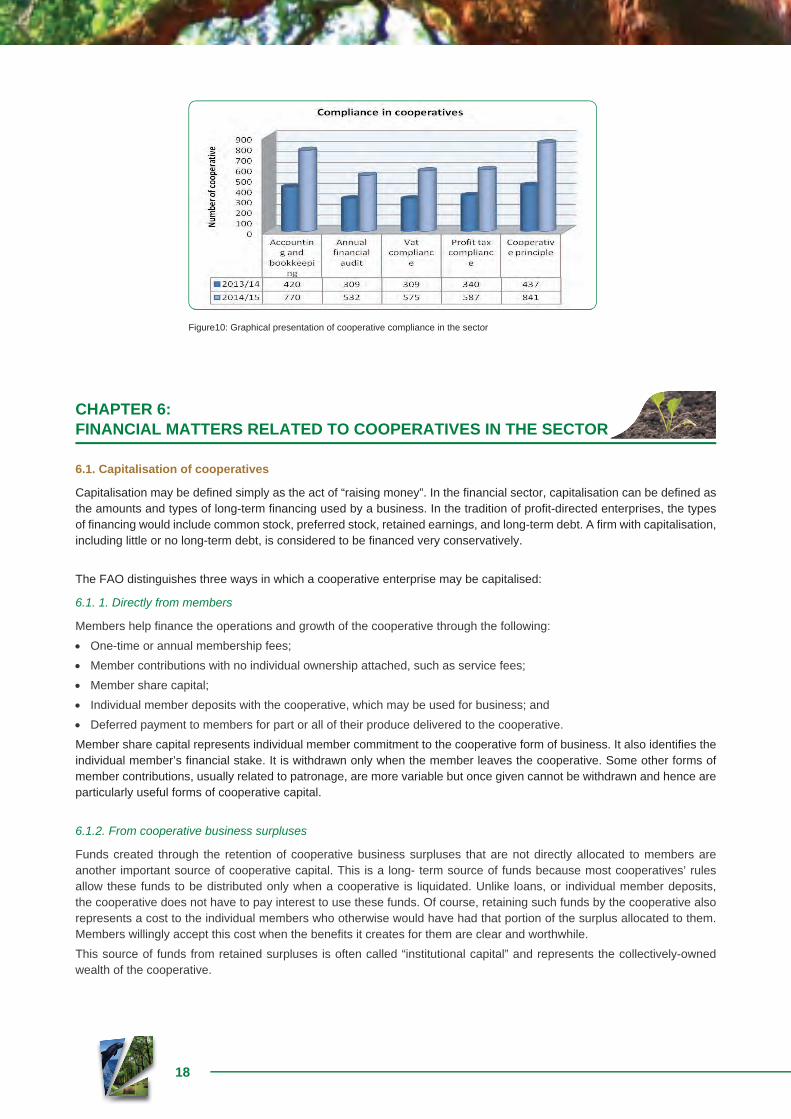

5.3. Cooperative compliance in the sector

When measuring the level of compliance in cooperatives, fi ve major factors are being used, which are as follows, account-ing and record keeping, annual fi nancial audit, VAT compliance, profi t tax compliance and cooperative principles. Table 17 and fi gure 10 indicate the number of cooperatives complying with the fi ve selected key compliance areas. Compared with 2013/14 fi nancial year, the level of compliance has improved in 2014/15 fi nancial year.

17

Pro

vin

ce

Co

mp

lian

ce a

rea

Acc

ou

nti

ng

an

db

oo

kkee

pin

gA

nn

ual

fi n

anci

alau

dit

Vat

com

plia

nce

Pro

fi t

tax

com

plia

nce

Co

op

erat

ive

pri

nci

ple

s

2013

/14

2014

/15

2013

/14

2014

/15

2013

/14

2014

/15

2013

/14

2014

/15

2013

/14

2014

/15

Eas

tern

Cap

e37

9421

5421

5722

4128

38

Fre

e S

tate

2760

1730

3335

1633

2452

Gau

teng

18

149

2110

2110

2823

61

Kw

aZul

u-N

atal

7699

5267

5375

5168

6210

8

Lim

popo

9319

670

134

6311

581

152

103

232

Mpu

mal

anga

108

145

9612

176

133

115

129

118

167

Nor

ther

n C

ape

819

311

78

85

1538

Nor

th W

est

4399

4062

4290

3792

4510

8

Wes

tern

Cap

e10

441

324

410

3919

37

Tot

al

420

770

309

532

309

575

340

587

437

841

Com

plia

nce

in c

oope

rativ

es

Tab

le 1

7: C

oope

rativ

e co

mpl

ianc

e in

the

sect

or

18

Figure10: Graphical presentation of cooperative compliance in the sector

CHAPTER 6: FINANCIAL MATTERS RELATED TO COOPERATIVES IN THE SECTOR

6.1. Capitalisation of cooperatives

Capitalisation may be defi ned simply as the act of “raising money”. In the fi nancial sector, capitalisation can be defi ned as the amounts and types of long-term fi nancing used by a business. In the tradition of profi t-directed enterprises, the types of fi nancing would include common stock, preferred stock, retained earnings, and long-term debt. A fi rm with capitalisation, including little or no long-term debt, is considered to be fi nanced very conservatively.

The FAO distinguishes three ways in which a cooperative enterprise may be capitalised:

6.1. 1. Directly from members

Members help fi nance the operations and growth of the cooperative through the following:

One-time or annual membership fees;

Member contributions with no individual ownership attached, such as service fees;

Member share capital;

Individual member deposits with the cooperative, which may be used for business; and

Deferred payment to members for part or all of their produce delivered to the cooperative.

Member share capital represents individual member commitment to the cooperative form of business. It also identifi es the individual member’s fi nancial stake. It is withdrawn only when the member leaves the cooperative. Some other forms of member contributions, usually related to patronage, are more variable but once given cannot be withdrawn and hence are particularly useful forms of cooperative capital.

6.1.2. F rom cooperative business surpluses

Funds created through the retention of cooperative business surpluses that are not directly allocated to members are another important source of cooperative capital. This is a long- term source of funds because most cooperatives’ rules allow these funds to be distributed only when a cooperative is liquidated. Unlike loans, or individual member deposits, the cooperative does not have to pay interest to use these funds. Of course, retaining such funds by the cooperative also represents a cost to the individual members who otherwise would have had that portion of the surplus allocated to them. Members willingly accept this cost when the benefi ts it creates for them are clear and worthwhile.

This source of funds from retained surpluses is often called “institutional capital” and represents the collectively-owned wealth of the cooperative.

19

6.1.3. From outsiders

I n addition to institutional capital and member capital, cooperatives often make use of external sources of funds to run their operations or to fi nance investments. These non-member sources of funds may include cooperative or commercial banks, suppliers, government or donor agencies. External funding may be provided in different ways:

as a grant,

as a short term-loan,

as a long-term loan, and

as a trade credit offered by a supplier.

Commercial providers of funds, such as banks, generally provide credit or loans that are legally secured by collateral (pledged assets of the cooperative). They are motivated by profi t and seek to minimise risk. Non-commercial providers, such as governments or donors, generally provide credit on more generous terms at below market rates of interest or pro-vide grants. Their motivations may be social, political or economic and often a combination of all three.

6.2. The gearing ratio

T he more assets the cooperative owns and has fully paid for (buildings, equipment, stock and fi nancial reserves) the more others are willing to lend additional funds. Also, the greater the amount of the cooperative’s institutional plus member cap-ital, the higher the amount that can safely be borrowed from outside sources. Financial leverage, or gearing, is expressed by a percentage ratio which gives an indication of the degree of risk involved in borrowing funds. The higher the gearing ratio, the higher the risk the cooperative runs in losing its assets in the event of inability to repay a loan. The gearing ra-tio relates to the amount of externally borrowed capital to the total capital employed by the cooperative (institutional and member capital plus borrowed funds).

6.3. Sources of capital for cooperatives in the sector

6.3.1. Equity

Equity in this context refers to amounts contributed by members of cooperatives in a form of membership/joining fees pre-scribed by the constitution of each cooperative. Table 18 below shows an increase of R3,5 million in member contributions in their cooperatives. An increase in the amount of money invested by members in a cooperative result in an improved fi nancial leverage or gearing.

Province Number of cooperatives/fi nancial year Amount (ZAR)/fi nancial year

2013/14 2014/15 Variance 2013/14 2014/15 Variance

R’000 R’000 R’000

Eastern Cape 169 212 43 460 319 141

Free State 64 89 25 99 22 121

Gauteng 71 106 35 62 862 800

KwaZulu-Natal 362 383 21 1 932 1 947 15

Limpopo 268 384 116 1 619 2 112 493

Mpumalanga 171 224 53 411 1 109 698

Northern Cape 105 107 2 267 325 58

North West 193 222 29 1 292 2 552 1 261

Western Cape 40 61 21 2 367 2 367 0

Total 1443 1788 345 8 510 11 616 3 106

Table 18: Equity in cooperatives

20

Figure 11: Members contribution in cooperatives

6.3.2. Investment by DAFF through grants

As indicated in 6.1 above, in addition to institutional capital and member capital, cooperatives often make use of external sources of funds to run their operations or to fi nance their business activities. These non-member sources of funds may include cooperative or commercial banks, suppliers, government or donor agencies. This section presents the results of analysis undertaking on external sources of fi nance for sector cooperatives in a form of grants mainly from the Department (DAFF), provinces (PDA’s) and other government departments. The table below shows a cumulative amount of R178 mil-lion invested in sector cooperatives by DAFF in the form of grants over a period of two years.

Province Number of cooperatives Grant amount (ZAR) Cumulative amount

2013/14 2014/15 2013/14 2014/15

R’000 R’000 R’000

Eastern Cape 32 17 9 654 7 126 9 829

Free State 20 5 990 13 805 14 795

Gauteng 8 21 460 638 1 098

KwaZulu-Natal 22 27 0 12 655 12 655

Limpopo 15 28 8 788 40 683 49 471

Mpumalanga 8 12 179 34 275 34 454

Northern Cape 5 4 0 685 685

North West 40 61 27 631 47 944 75 575

Western Cape 2 11 3 300 10 033 13 333

Total 152 186 51 002 127 162 178 164

Table 19: Grants by DAFF

21

6.3.3. Investment by other intuitions through grants

6.3.3.1. Eastern Cape

Name of institution Number of cooperatives Grant amount (ZAR)

R’000

Municipality 10 35 441

Shell SA 1 150

DSD 2 32 606

DRDLR 2 637

DWS 1 150

NDA 1 2 000

DEDEA 1 350

NETS AFRICA 10 4 000

ARC 1 180

TINA SINAKO 1 2 000

Total 30 77 513

Table 20: Grants by external stakeholders in the Eastern Cape

6.3.3.2. Free State

Name of institution Number of cooperatives Grant amount (ZAR)

R’000

Harmony gold mine 2 3 000

Total 2 3 000

Table 21: Grants by external stakeholders in the Free State

6.3.3.3. Gauteng

Name of institution Number of cooperatives Grant amount (ZAR)

R’000

dti 5 574

DRDLR 1 390

DSD 1 920

DL 1 200

NDA 1 250

Total 9 2 334

Table 22: Grants by external stakeholders in Gauteng

22

6.3.3.4. Limpopo

Name of institution Number of cooperatives Grant amount (ZAR)

R’000

dti 4 1 400

AFGRI 1 700

LEDA 1 177

DSD 1 500

NDA 1 1 800

VDM 1 1 500

DRDLR 1 2 500

Total 10 8 577

Table 23: Grants by external stakeholders in Limpopo

6.3.3.5. Mpumalanga

Name of institution Number of cooperatives Grant amount (ZAR)

R’000

CRDP 1 2 000

NYDA 1 27

Total 2 2 027

Table 24: Grants by external stakeholders in Mpumalanga

6.3.3.6. North West

Name of institution Number of cooperatives Grant amount (ZAR)

R’000

IDC 1 2 200

Total 1 2 200

Table 25: Grants by external stakeholders in the North West

6.3.3.7. Western Cape Province

Name of institution Number of cooperatives Grant amount (ZAR)

R’000

DRDLR 2 2 500

Total 2 2 500 000

Table 26: Grants by external stakeholders in the Western Cape

6.3.4. Investment through loans

External funding to cooperatives does not only come in the form of grants but also in the form of loans either from the department or other stakeholders. This section presents the results of analysis of external funding in the form of loans.

6.3.4.1. Investment by DAFF through loans

DAFF provides loan funding to cooperatives for production purposes through the Micro agricultural Financial Institutions of South Africa (Mafi sa). These funds are disbursed through accredited service providers authorised to retail the funds.

23

Province Number of cooperatives Loan amount (ZAR)

R’000

Eastern Cape 11 3 486

KwaZulu-Natal 5 870

North West 1 2

Total 16 4 358

Table 27: Loans by DAFF

6.3.4.2. Investment by other institutions through loans

Province Institution Number of cooperatives Loan amount (ZAR)

R’000

Gauteng Land Bank 1 120

ABSA Bank 1 85

Total 2 205

Table 28: Loans by external stakeholders

6.3.5. Comparison between grants and loans

Grants Loans

R’000 R’000

225 313 4 379

Table 29: Comparison between grants and loans

Figure 12: Comparison between grants and loans

6.4. Financial performance of cooperatives in the sector (annual turnover)

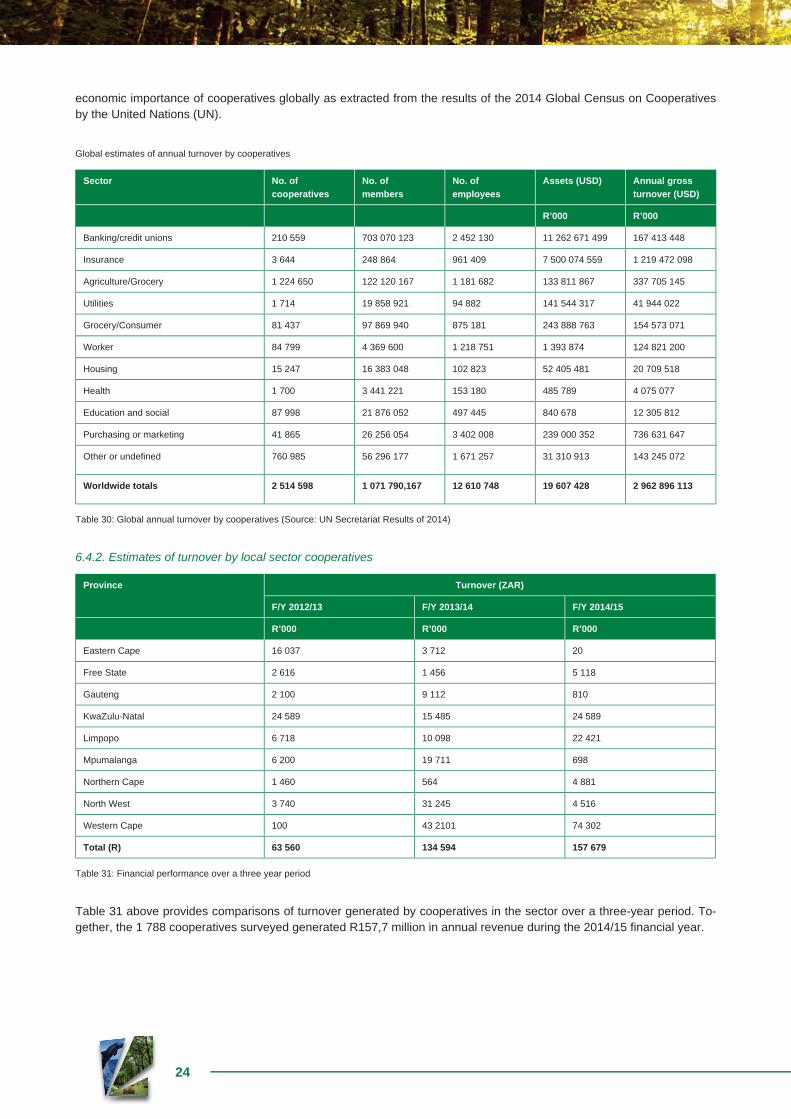

6.4.1. Global estimates

The new World Cooperative Monitor launched this week, reveals that together cooperatives around the world generated US$2,96 trillion in national revenue. This is done through leveraging of their combined asset base of US$ 19,6 trillion. It is further estimated that combined, the global cooperative economy is larger than France’s economy and places it right behind Germany’s economy as the 5th largest economic unit if it were a united country. The table that follows illustrates the

24

economic importance of cooperatives globally as extracted from the results of the 2014 Global Census on Cooperatives by the United Nations (UN).

Global estimates of annual turnover by cooperatives

Sector No. of cooperatives

No. of members

No. of employees

Assets (USD) Annual grossturnover (USD)

R’000 R’000

Banking/credit unions 210 559 703 070 123 2 452 130 11 262 671 499 167 413 448

Insurance 3 644 248 864 961 409 7 500 074 559 1 219 472 098

Agriculture/Grocery 1 224 650 122 120 167 1 181 682 133 811 867 337 705 145

Utilities 1 714 19 858 921 94 882 141 544 317 41 944 022

Grocery/Consumer 81 437 97 869 940 875 181 243 888 763 154 573 071

Worker 84 799 4 369 600 1 218 751 1 393 874 124 821 200

Housing 15 247 16 383 048 102 823 52 405 481 20 709 518

Health 1 700 3 441 221 153 180 485 789 4 075 077

Education and social 87 998 21 876 052 497 445 840 678 12 305 812

Purchasing or marketing 41 865 26 256 054 3 402 008 239 000 352 736 631 647

Other or undefi ned 760 985 56 296 177 1 671 257 31 310 913 143 245 072

Worldwide totals 2 514 598 1 071 790,167 12 610 748 19 607 428 2 962 896 113

Table 30: Global annual turnover by cooperatives (Source: UN Secretariat Results of 2014)

6.4.2. Estimates of turnover by local sector cooperatives

Province Turnover (ZAR)

F/Y 2012/13 F/Y 2013/14 F/Y 2014/15

R’000 R’000 R’000

Eastern Cape 16 037 3 712 20

Free State 2 616 1 456 5 118

Gauteng 2 100 9 112 810

KwaZulu-Natal 24 589 15 485 24 589

Limpopo 6 718 10 098 22 421

Mpumalanga 6 200 19 711 698

Northern Cape 1 460 564 4 881

North West 3 740 31 245 4 516

Western Cape 100 43 2101 74 302

Total (R) 63 560 134 594 157 679

Table 31: Financial performance over a three year period

Table 31 above provides comparisons of turnover generated by cooperatives in the sector over a three-year period. To-gether, the 1 788 cooperatives surveyed generated R157,7 million in annual revenue during the 2014/15 fi nancial year.

25

Figure 13: Annual turnover in cooperatives

CHAPTER 7:COOPERATIVES AND MARKET ACCESS

7.1. Defi ning market access

Jonathan Creese (2009) defi nes market access as it refers to the technical and non-technical measures for the entry of goods into markets. Market access for all smallholder farmers means that every farmer can participate in the market for trade. By having access to a market farmers` standard of living will be uplifted and their productivity will increase. Market access is important for agriculture and rural development in South Africa. However, to be able to access markets, farmers have to be aware of the requirements which include but not limited to competitiveness, quality, variety/breed, understand-ing consumers, understanding local culture, customs and tastes, effi cient value chain function, retailer requirements, infra-structure, packaging, building and maintaining relationships and address information asymmetries.

7.2. Challenges with market access

Lara Barlow and Niek van Dijk (2013) summarised the following as some of the challenges facing smallholder farmers and cooperatives with regard to access to markets:

7.2.1. Product quality

Product inspections are undertaken to ensure that products meet quality requirements. Most farmers have their produce declined as a result of poor quality. These usually result in profi t losses to farmers because of the unmarketable products.

7.2.2. Product pricing

Break even is diffi cult to be reached by farmers because they feel that their produce do not fetch high prices. Prices farmers get for their produce are low according them. End users of the products, be it communities, are not willing to pay more for organic produce and they do not put any premium on organic produce.

7.2.3. Market knowledge and business skills

Farmers have a limited ability to look for new markets or negotiate successfully good deals because farmers in this fi eld have limited or no market knowledge and poor business skills. Smallholder farmers have a high level of illiteracy; as such, they feel that they lack ways of dealing with supermarkets.

26

Other challenges with market access include lack of appropriate infrastructure, limited access and high cost to improve farm inputs and production technology, insuffi cient agricultural services, lack of access of facilities for agricultural credit and the ownership and control of productive land.

7.3. Types of markets accessed by cooperatives in the sector

7.3.1 Eastern Cape

Institutions supplied Number of cooperatives supplying

Spar 3

Hoppsin & Karen 1

Boxer 2

East London market 1

Shepstone 1

Steers 1

Total 9

Table 32: Markets accessed by Eastern Cape cooperatives

7.3.2 Free State

Institutions supplied Number of cooperatives supplying

Albert Boarding School 1

BKB 1

Mangaung Fresh Produce Market 2

Boxer Supermarket 1

Cambridge Supermarket 1

Local government 1

Econo Fish 4

J.S Poultry 1

Overland 1

Pick n Pay Supermarket 1

Ponelopele 1

Tshwane Fresh Produce Market 1

Senwes Kooperasie 1

Shoprite Supermarket 1

Sky country 1

Supreme Chicken 1

Thabanchu Butchery 1

Veriland 1

Welkom 1

Grain SA 1

Total 24

Table 33: Markets accessed by Free State cooperatives

27

7.3.3 Gauteng Province

Institutions supplied Number of cooperatives supplying

Joburg Fresh Produce Market 1

Hospitals 1

Hotel Swazi Inn 1

Hawkers Association 1

Pick n Pay 1

Retailers 1

Total 6

Table 34: Markets accessed by Gauteng cooperatives

7.3.4 KwaZulu-Natal

Institutions supplied Number of cooperatives supplying

Hospitals 7

Supermarkets 3

Aheers Greytown 1

Pietermaritzburg market 1

Spar 4

Dundee milling 3

Safgri 1

Boxer 2

Natalia market 1

Richards Bay Minerals 2

Mkhondeni market 1

School feeding scheme 1

Pills Honey Pty 1

Triangle Supermarket 1

University of Zululand 1

Sisonke Morning Market 1

Nkanyezi supermarket 1

G.J. Crooks 1

Vryheid Greengrocer 1

Total 34

Table 35: Markets accessed by KwaZulu-Natal cooperatives

28

7.3.5 Limpopo Province

Institutions supplied Number of cooperatives supplying

Afgri 1

Am-pak 1

Boxer Supermarket 1

Durban market 1

Golden Good 1

City Deep 8

Tshwane market 1

Pick n Pay Supermarket 4

Potatoes SA 1

Pioneer 1

Tiger Brand 2