AGENDA - CBRE Vietnam...VIETNAM OFFICE MARKET OVERVIEW & OUTLOOK - IMPLICATIONS FOR OCCUPIERS . 2...

13

1 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY AGENDA 1. 360 DEGREE WORKPLACE STRATEGY -TRENDS AND DRIVERS 2. GOING GREEN - ENTER GREEN LEASES 3. VIETNAM OFFICE MARKET OVERVIEW & OUTLOOK - IMPLICATIONS FOR OCCUPIERS

Transcript of AGENDA - CBRE Vietnam...VIETNAM OFFICE MARKET OVERVIEW & OUTLOOK - IMPLICATIONS FOR OCCUPIERS . 2...

1 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

AGENDA

1. 360 DEGREE WORKPLACE STRATEGY

-TRENDS AND DRIVERS

2. GOING GREEN

- ENTER GREEN LEASES

3. VIETNAM OFFICE MARKET OVERVIEW

& OUTLOOK

- IMPLICATIONS FOR OCCUPIERS

2 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

ENRICHING THE OCCUPIER EXPERIENCES

3 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

CBRE’S RECENT REGIONAL EXPERIENCE

CBRE new office in Singapore

4 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

ENTER A GREEN LEASE

“A green lease is a standard form lease with additional clauses included which provide for the management and improvement of the Environmental Performance of a building by both owner and occupier. Such a document is legally binding and its provisions remain in place for the duration of the term”. - UK Better Buildings Partnership

5 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

Very early days in Asia but signs that will change

• Some successful examples (e.g. Lend Lease in

Singapore)

• A number of large MNC occupiers are now pursuing

green lease strategies

• Singapore BCA just released Office and Retail

Green Lease Schedules for 2014.

• Hong Kong Green Building Council working on

Green Lease guidance

• GRESB is asking for it

GREEN LEASES – THE NEW FRONTIER

6 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

0% 10% 20% 30% 40% 50%0%10%20%30%40%50%$0$5$10$15$20$25$30$35

Rent Stable, Vacancy Down

OFFICE

Source: CBRE Vietnam, YTD 2014.

AVERAGE ASKING RENT

(US$/sm/month)

VACANCY RATE

(%)

2014

Q4

Q3

Q2

Q1

2013

Q4

Q3

Q2

Q1

2012

Q4

Q3

Q2

Q1

2011

Q4

Q3

Q2

Q1

GRADE B GRADE A GRADE B GRADE A

$0 $5 $10 $15 $20 $25 $30 $35

2014

Q4

Q3

Q2

Q1

2013

Q4

Q3

Q2

Q1

2012

Q4

Q3

Q2

Q1

2011

Q4

Q3

Q2

Q1

7 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

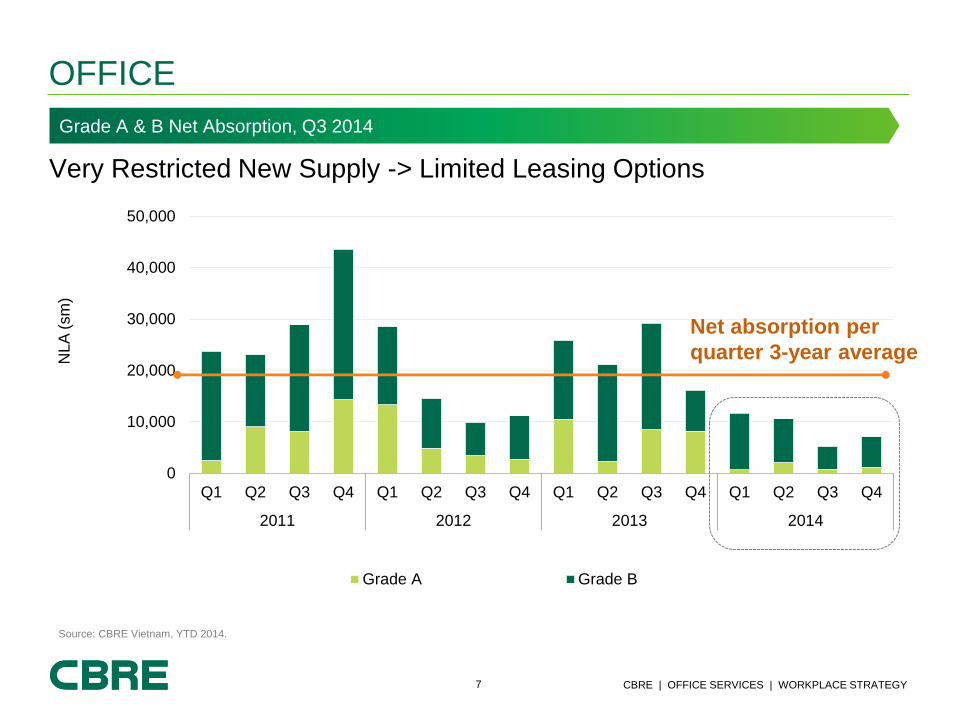

0

10,000

20,000

30,000

40,000

50,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2011 2012 2013 2014

NLA

(sm

)

Grade A Grade B

Very Restricted New Supply -> Limited Leasing Options

OFFICE

Source: CBRE Vietnam, YTD 2014.

Net absorption per

quarter 3-year average

Grade A & B Net Absorption, Q3 2014

8 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

Tenant Categories

OFFICE

Source: CBRE Vietnam, YTD 2014.

Number is calculated based on CBRE’s enquiries only

By Industry, YTD 2014 By Nationality, YTD 2014

By Transaction Types, 2012 – YTD 2014

5%

30%

25%

7%

11%

39%

81%

45%

22%

7%

14%

14%

0% 20% 40% 60% 80% 100%

2012

2013

YTD 2014New letting

Expansion

Relocation

Renewal

19%

13%

5%

12% 12%

39%

Banking/ Finance/ Insurance

Phamarceutical/chemicals/ comestic

Sourcing/ Outsourcing

Technology/Electronic/IT

Manufacturing

Other

29%

25% 8%

6%

6%

26%

Europe

US

Vietnam

Germany

Korea

Other

9 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

-10%

-5%

0%

5%

10%

15%

20%

Ma

nila

Sin

ga

po

re

Ho

Chi M

inh C

ity

Ne

w D

elh

i

Kua

la L

um

pur

Taip

ei

Seo

ul

Auckla

nd

Ban

gkok

Sha

ngh

ai

Gua

ngzh

ou

Beiji

ng

Sydn

ey

To

kyo

Ho

ng

Kon

g

Me

lbou

rne

Hano

i

Mu

mb

ai

Brisb

an

e

Rental Growth, H1 2014 Forecast Rental Growth, 2014

APAC Rental Growth

OFFICE

(*) Forecasted at the end of 2013

Source: CBRE Research, August 2014.

Better than expected In line with expectations Lagging behind expectations

*

10 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

Outlook 2015

OFFICE

Average rent stable in Q1 & Q2 and very likely will be more

competitive in new office supply coming online Q1 & Q2 2015

Against this context, the vacancy rate will rise slightly.

Expansion and new entrants are anticipated to drive office market in 2015 given

improving market conditions and changes in regulatory environment. Active sectors

include Insurance, Sourcing, IT/Technology

Limited new supply CBD supply from large scale, mixed use projects

and from those projects developed partly for owner- occupation

11 CBRE | OFFICE SERVICES | WORKPLACE STRATEGY

4 Best 2 More

The First prize

of

National Energy

Efficiency

Winner 2011

The best

location

The

biggest

shopping

mall

The largest

floor plate

Greener –

More energetic More

convenient

VINCOM CENTER DONG KHOI

For enquiry, please call 0936 299 899

THANK YOU

Please fill in feedback forms

QUESTIONS & ANSWERS