AFRICAN COFFEE SECTOR€¦ · INVESTMENT AGENDA FOR THE KENYAN COFFEE SECTOR –EXECUTIVE SUMMARY...

35

AFRICAN COFFEE SECTOR addressing national investment agendas on a continental scale Kenya Case Study 1 SEPTEMBER 16 AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE Sector study conducted by Agri-Logic and Valued Chain by assignment of the Global Coffee Platform Contact: [email protected]

Transcript of AFRICAN COFFEE SECTOR€¦ · INVESTMENT AGENDA FOR THE KENYAN COFFEE SECTOR –EXECUTIVE SUMMARY...

AFRICAN COFFEE SECTORaddressing national investment agendas on a continental scale

Kenya Case Study

1

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Sector study conducted by Agri-Logic and Valued Chain by assignment of the Global Coffee PlatformContact: [email protected]

CHALLENGE:

• Currently Africa only supplies 10% of global

coffee volumes, while coffee was first

discovered in Ethiopia.

• In most African origins, yields are low, quality

is inconsistent, and supply chains are

inefficient.

OPPORTUNITIES:

• Buyers value certain coffees from Africa for

their quality, and there is a potential to

increase volumes to meet growing demand.

• Coffee may contribute to sustainable

development in Africa’s rural areas.

2

INTRODUCING NATIONAL COFFEE INVESTMENT AGENDAS FOR AFRICA

INVESTMENT AGENDAS:

• Greater understanding of challenges and

opportunities in mainstreaming sustainable

coffee production.

• Insight into required funding, return on

investment, and possible public and private

contributions.

• Insight into impact of investment based on

quantitative research and stakeholder

consultation. Benchmarks and analysis are

based on 2015 data.

• Full reports available on the GCP website for

Angola, Burundi, Cameroon, Côte d’Ivoire,

Ethiopia, Kenya, Rwanda, Tanzania and

Uganda.

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

• Executive summary

• Positioning of coffee from origin

• Production areas in origin

• Supply & demand trend and

• Market interest in sustainability

• Value chain structure

• Farm level production systems

• Supply chain efficiency

• Differential competitiveness

3

CONTENT OF THIS REPORT

• Cost of production

• Current farmer business case

• Production and price effects of investments

• Impact, cost and return per intervention

• Effect on farmer business case

• National sector business case

• Proposed public and private contributions

• Conclusion

INVESTMENT OPPORTUNITIES ANALYSIS

• The following slides describe the required investment (cost) and expected returns (revenue), as well

as the expected impact on price, volume, quality and livelihoods.

• Investments are analysed on a sector level: total increased revenue in relation to total additional cost.

On a sector level, all of these opportunities present a positive return on investment.

• Cost and benefits may not be attributed to the same actor in the value chain (e.g. government and

buyers pay for farmer training, while the farmer gains most of the additional revenue from yield

increase).

• Also, specific interventions may not lead to additional value creation, but to a redistribution of value

within the chain (e.g. farmer grouping can lead to higher farm gate price, while export price and GDP

contribution is not affected).

• Investment contributions are indicative based on stakeholder input. Investments and conditions to be

negotiated within national public private platforms taking into account amongst others international

competitiveness, governance, transparency and accountability assurance.

4

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

INVESTMENT AGENDA FOR THE KENYAN COFFEE SECTOR – EXECUTIVE SUMMARY• Coffee volumes in Kenya are declining, and are currently around 45,000 MT per annum, or 0.5% of

global production.

• The sector is dominated by smallholder on less than 0.5ha. These smallholders are required by

law to join cooperatives. Larger estates exist and even though the number of farms is low, these

estates represent about 40-45% of coffee volume. The volume share of smallholders is increasing,

as estates are sold to real estate projects.

• Cost of production are relatively high, and increasing in line with cost in Brazil. This is a competitive

disadvantage for Kenya compared to other African origins. Productivity is average to low, especially

on small farms. Despite high private sector interest from European and American coffee buyers,

farmers are abandoning coffee in favour of other crops.

• The sector is regulated by the Kenyan government, and 85% of coffee is sold through the Nairobi

Coffee Exchange. Levies of 4% are in line with international benchmark, but licensing cost are reported

to be high.

5

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

• There is significant potential to increase coffee sector value in Kenya through selective investment

in farmer training, farm rejuvenation, use of inputs and farmer organisation building.

• Volumes could increase to ~75.000 Mt per annum. The increased value largely flows into rural

economy.

• Coffee alone will not provide sufficient income for a full farmer household, under current conditions it

appears unlikely that the gap to the poverty line can be met with agricultural activities. It is unlikely

that farmers will be lifted out of poverty in the short- to mid-term, despite investments.

• Total programme investment amounts to an estimated 198 million USD over 10 years that would

generate a return across the sector of >1 billion USD at current prices.

6

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

INVESTMENT AGENDA FOR THE KENYANCOFFEE SECTOR – EXECUTIVE SUMMARY

KENYAResilience for improved yields and quality, supply chain efficiency for livelihoods

7

SEPTEMBER 16AFRICAN COFFEE SECTOR: addressing national investment agendas on a continental scale

POSITIONING OF KENYA

Item Value

Total volume (3 year average) 45,800 Mt

% of global production 0.52%

% Arabica – Robusta 100% Arabica

% natural – semi-washed – fully washed 11% natural – 89% washed

Compound Annual Growth Rate of coffee production (2000-2015)

- 4.7%

Main export markets USA, EU

Market segments Rich flavour arabica

GDP 63.4 billion USD

GDP – agriculture 19 billion USD

GDP – coffee 0.22 billion USD

8

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

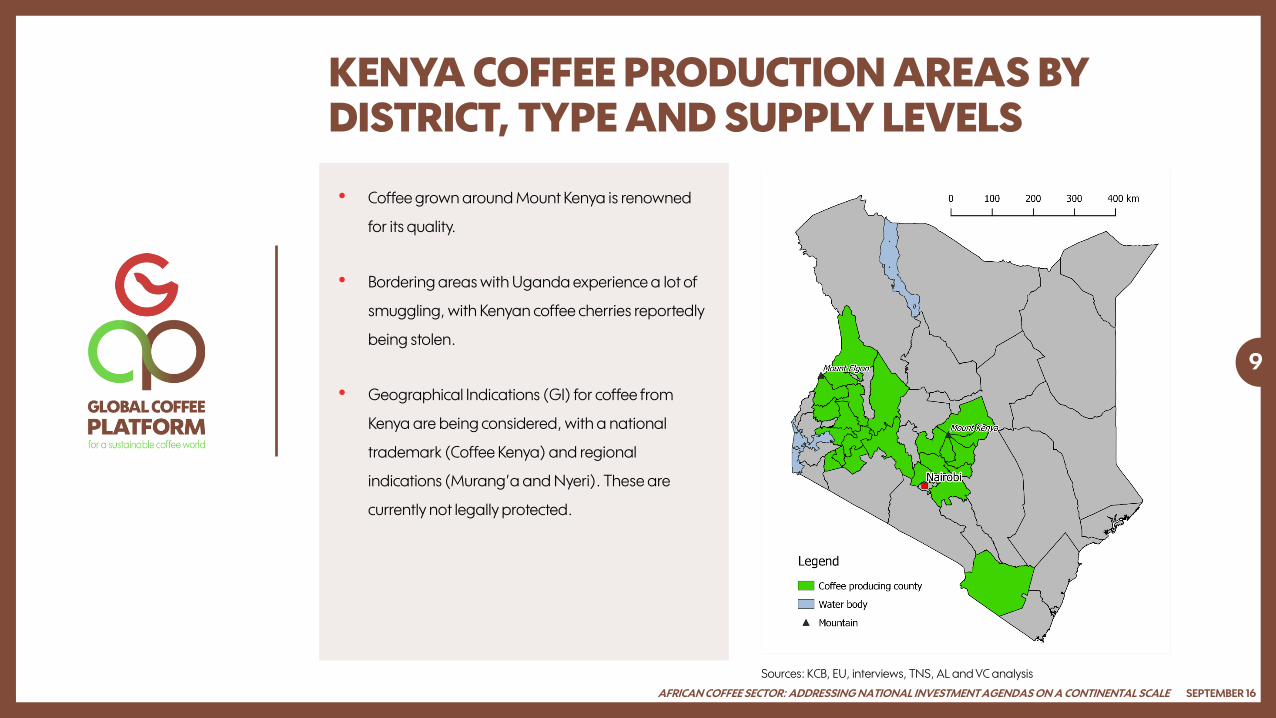

• Coffee grown around Mount Kenya is renowned

for its quality.

• Bordering areas with Uganda experience a lot of

smuggling, with Kenyan coffee cherries reportedly

being stolen.

• Geographical Indications (GI) for coffee from

Kenya are being considered, with a national

trademark (Coffee Kenya) and regional

indications (Murang’a and Nyeri). These are

currently not legally protected.

9

KENYA COFFEE PRODUCTION AREAS BY DISTRICT, TYPE AND SUPPLY LEVELS

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Sources: KCB, EU, interviews, TNS, AL and VC analysis

10

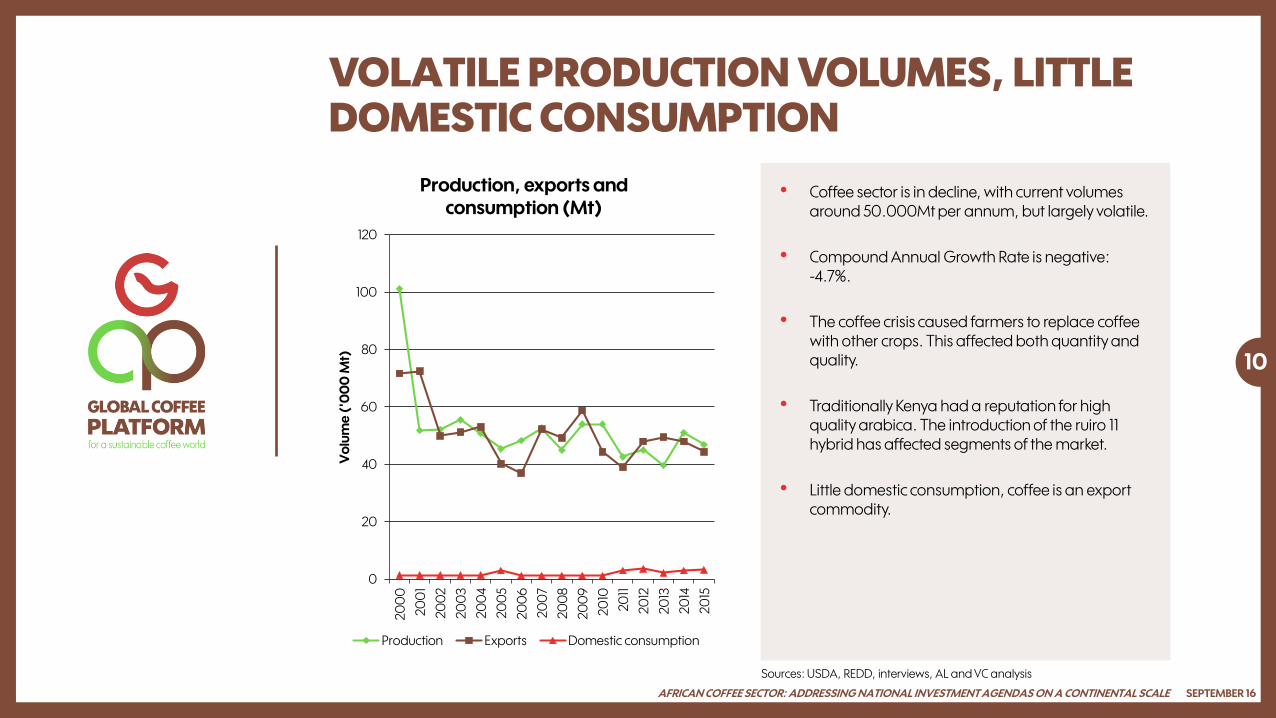

VOLATILE PRODUCTION VOLUMES, LITTLE DOMESTIC CONSUMPTION

• Coffee sector is in decline, with current volumes around 50.000Mt per annum, but largely volatile.

• Compound Annual Growth Rate is negative: -4.7%.

• The coffee crisis caused farmers to replace coffee with other crops. This affected both quantity and quality.

• Traditionally Kenya had a reputation for high quality arabica. The introduction of the ruiro 11 hybrid has affected segments of the market.

• Little domestic consumption, coffee is an export commodity.

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Sources: USDA, REDD, interviews, AL and VC analysis

0

20

40

60

80

100

120

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Vo

lum

e (

'00

0 M

t)

Production, exports and consumption (Mt)

Production Exports Domestic consumption

11

AFRICA LAGGING IN SHARE OF CERTIFIED SUSTAINABLE SUPPLY

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Vo

lum

e (

'00

0 b

ag

s o

f 6

0k

g)

Year

Global supply (‘000 bags)

Volume certified Volume conventional

Total volume

Sources: USDA, CTA, AL and VC analysis

0% 20% 40% 60% 80%

Africa

Latin america

Asia

Share of total supply and certified supply

Share of certified and verified supply Share of global supply

12

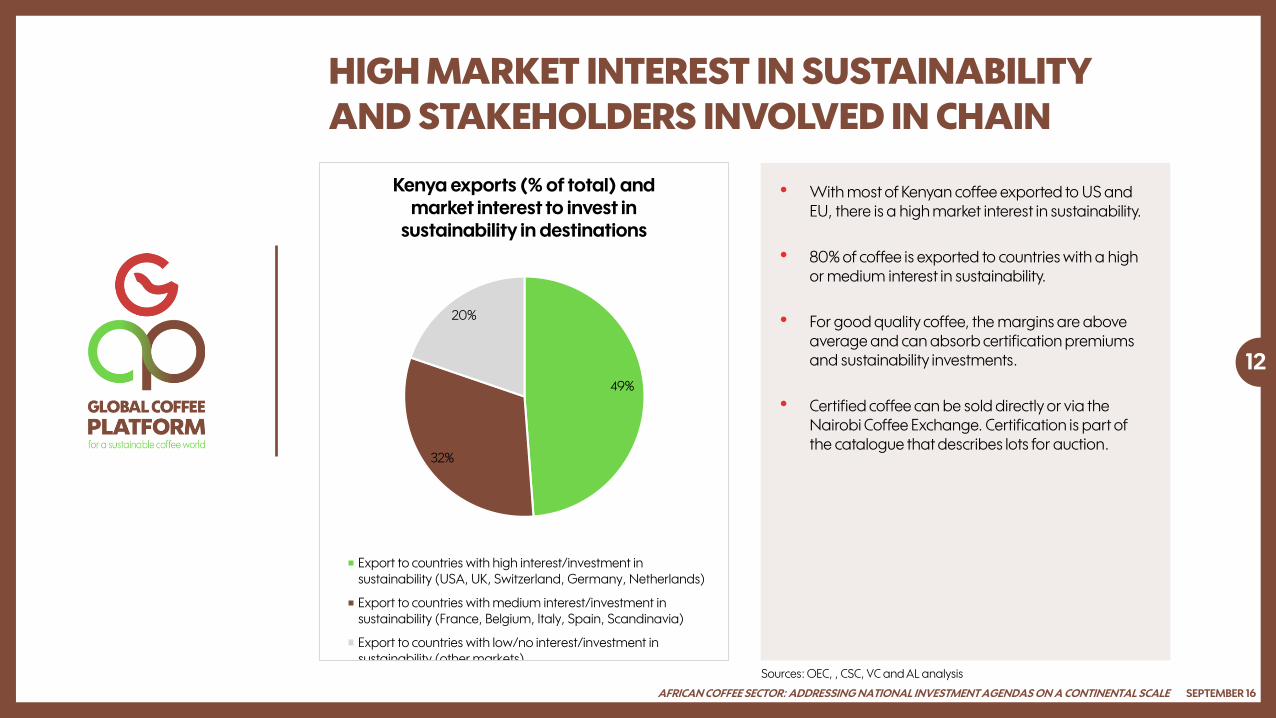

HIGH MARKET INTEREST IN SUSTAINABILITY

AND STAKEHOLDERS INVOLVED IN CHAIN

• With most of Kenyan coffee exported to US and EU, there is a high market interest in sustainability.

• 80% of coffee is exported to countries with a high or medium interest in sustainability.

• For good quality coffee, the margins are above average and can absorb certification premiums and sustainability investments.

• Certified coffee can be sold directly or via the Nairobi Coffee Exchange. Certification is part of the catalogue that describes lots for auction.

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Sources: OEC, , CSC, VC and AL analysis

49%

32%

20%

Kenya exports (% of total) and market interest to invest in

sustainability in destinations

Export to countries with high interest/investment insustainability (USA, UK, Switzerland, Germany, Netherlands)

Export to countries with medium interest/investment insustainability (France, Belgium, Italy, Spain, Scandinavia)

Export to countries with low/no interest/investment insustainability (other markets)

,0 ,20 ,40 ,60 ,80 1,0

0

50

100

150

200

250

Usc

ts/l

b

Share of supply in value chain segment

Value chain structure Kenya Arabica 2015

Farm gate price Auction price Market price

13

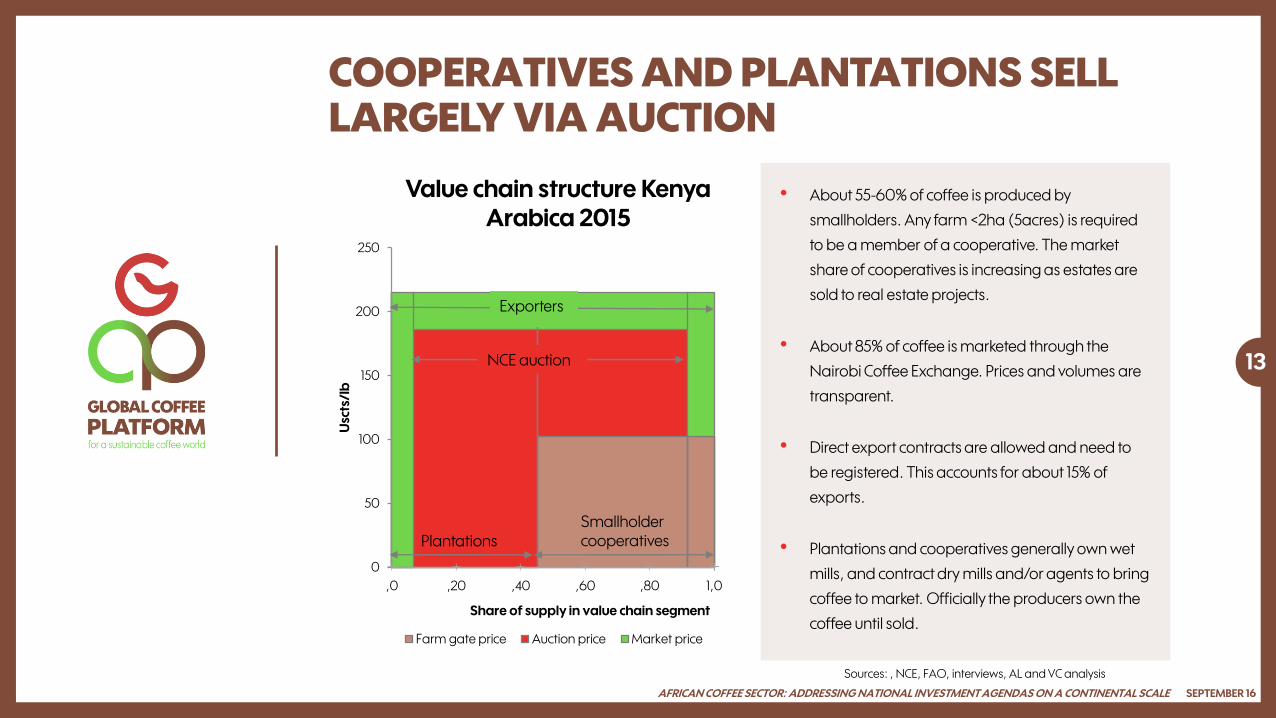

COOPERATIVES AND PLANTATIONS SELL LARGELY VIA AUCTION

• About 55-60% of coffee is produced by

smallholders. Any farm <2ha (5acres) is required

to be a member of a cooperative. The market

share of cooperatives is increasing as estates are

sold to real estate projects.

• About 85% of coffee is marketed through the

Nairobi Coffee Exchange. Prices and volumes are

transparent.

• Direct export contracts are allowed and need to

be registered. This accounts for about 15% of

exports.

• Plantations and cooperatives generally own wet

mills, and contract dry mills and/or agents to bring

coffee to market. Officially the producers own the

coffee until sold.

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Sources: , NCE, FAO, interviews, AL and VC analysis

PlantationsSmallholder cooperatives

NCE auction

Exporters

14

SECTOR CONSISTS PREDOMINANTLY OF SMALL-

SIZED FARMS OF LESS THAN 0.5 HA

• Smallholders with <5 acres (<2ha) are required by law to join a cooperative. KNBS indicates 800.000 smallholders organized in 600 cooperatives.

• Farms >5 acres (>2ha) are called estates and are allowed to market their coffee independently. It is estimated that about 3300 medium estates exist, and about 100 large estates.

• Land shortages are prevalent, farm sizes per household have come down significantly as plots are split between siblings when inherited.

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Sources: KNBS, interviews, AL and VC analysis

0% 20% 40% 60% 80% 100%

Number of farmers

Acreage (ha)

Nr of farmers and acreage distribution

Small <0.5ha Medium acreage >0.5<3ha Plantations >10ha

15

CURRENT PRODUCTIVITY LEVELS ARE LOW- TO

MID-LEVEL AND COULD GROW

• Productivity of Arabica is on average 350-

400kg green coffee per ha. This is far

below market leader Brazil and other

major origins.

• There is a large difference between estates

and smallholders. Yields at estates are

>600kg/ha whereas smallholders

organized in cooperatives produce on

average 300kg/ha.

• Productivity in Kenya could increase further,

up to 1 Mt/ha appears to be feasible at

least for estates. A major challenge

however is the lack of research capacity

and lack of success in developing new

resistant varieties.

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Sources: USDA, FAO, interviews, AL and VC analysis

0.00 0.50 1.00 1.50 2.00

Kenya

Brazil

Colombia

India

Average productivity (Mt/ha)

Arabica productivity (Mt/ha)

16

SUPPLY CHAIN EFFICIENCY BELOW OTHER MAJOR ORIGINS

• Data on farm gate prices is inconsistent, with large variability between sources. Cooperatives and estates receive ~80% of FOB price for processed coffee, but the share that is passed on to the smallholder farmer varies largely between 20-70% of FOB.

• Farm gate price as share of FOB does seem to have increased, but farmers remain dependent on external facilities or cooperatives to process their cherry.

• A 4% levy is applied to all exports. This income is to be used for the marketing bodies, research and infrastructure.

• Several licensing fees apply in order to obtain required permits, which is not visible in displayed value distribution but according to research adds another 2-5% to the cost of supply chain actors. In his April 2016 State of the Nation address, the president announced that licensing fees and levies would be waived.

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Sources: KNBS, NCE, FAO, interviews, AL and VC analysis

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Kenya Brazil Colombia India

Value distribution Arabica (% of FOB price)

Farm gate Supply chain costs Export tax/Cess

17

GOOD DIFFERENTIAL IN LINE WITH INDIA AND

OTHER AFRICAN ORIGINS

• Average differentials for Kenya arabica are +4

USDct/lb.

• Specific grades attract higher differentials.

Consistency in quality could possibly improve

differentials slightly.

• Kenya coffee is valued for quality over Brazil, and

still competitive in price compared to other

Arabica origins.

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Sources: interviews, AL and VC analysis

Kenya

Colombia

India

Brazil

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7

-20

-15

-10

-5

0

5

10

15

20

Dif

fere

nti

al (

US

Dct

/lb

)

Share of global supply

Arabica differentials (USDct/lb over ICE) and share of supply (%)

18

PRODUCTION COST ARE HIGH AND INCREASING, SPECIFICALLY ON FARM

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

• Increasing cost, especially labour and fertiliser, put cost of production in line with Brazil, and set cost above other East

African Arabica origins.

• Cost increase is attributed to high labour cost and climatic challenges affecting both inputs use and yields.

Sources: Rozimina, GroIntel, interviews, AL and VC analysis

0

20

40

60

80

100

120

140

160

2008 2009 2010 2011 2012 2013 2014 2015

Va

lue

(U

SD

ct/l

b)

Arabica cost of production (USDct/lb, ex household labour)

Kenya Brazil

0

50

100

150

2008 2015 2008 2015

Kenya Brazil

Va

lue

(U

SD

ct/l

b)

Arabica cost breakdown (USDct/lb)

Arabica trade export cost

Arabica export processing cost

Arabica farm processing cost

Arabica labor cost

Arabica planting cost

Arabica fertiliser cost

19

COFFEE FARMING IS NOT PROFITABLE FOR SMALLHOLDER FARMERS

• Coffee farmers in most cases just reach break-even on their coffee crop.

• Supply chain actors (cooperatives and agents) absorb most of the profit.

• With an average family-size of 4.4 people per household, net coffee income is far below the poverty line of 1.9 USD/capita/day (adjusted for purchasing power parity).

• Currently coffee is abandoned in favour of other activities.

• Farmer business case can be improved by passing on higher share of price to farmers, as well as increasing yields.

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Sources: Interviews, AL and VC analysis

87

0

132

44

200

244

0

200

400

600

800

1,000

1,200

1,400

0

50

100

150

200

250

300

Po

ve

rty

lin

e (

US

D/h

ou

seh

old

)

US

D/y

ea

r

Average farmer business case for Arabica in comparison to poverty

line

Cost Value Poverty line (USD1.9/day)

• Modelling 4 opportunities:

• Farmer training

• Rejuvenation/replanting

• Increasing input application

• Farmer organisation building

• A combination of first 3 interventions could increase total production to ~75.000 Mt.

• These productivity interventions are interrelated and can not be implemented separately.

20

MODELLING INVESTMENT OPPORTUNITIES – PRODUCTION EFFECTS

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Vo

lum

e (

Mt)

Production effect of investment opportunities

Increase inputs application - net production impact

Rejuvenation/replanting - net production impact

Farmer training - net production impact

Base level

• Assuming weighed average base price stable over time.

• Farmer organisations, if well managed, can add significant value to the farm gate price as a result of improved efficiency.

• Export price would not be affected by these interventions.

• Detailed models for the first 4 opportunities which show a positive business case are shown on the following pages

21

MODELLING INVESTMENT OPPORTUNITIES – PRICE EFFECTS

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

2,240

2,250

2,260

2,270

2,280

2,290

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Va

lue

(U

SD

/Mt)

Farm gate price effect of investment opportunities

Farmer organisation building - farm gate price impact

Base level

0

1,000

2,000

3,000

4,000

5,000

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Va

lue

(U

SD

/Mt)

Export price effect of investment opportunities

Base level

22

FARMER TRAINING INVESTMENT CAN GROW CURRENT SUPPLY BY 15%

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

0

100,000

200,000

300,000

400,000

500,000

600,000

Nu

mb

er

of

farm

ers

Number of farmers enrolled in training program

Annual nr farmers in training programme

Cumulative nr farmers trained -

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Ad

dit

ion

al s

up

ply

(M

t)

Additional supply from farmer training programme (Mt)

• For training on Good Agricultural Practices to be

effective it needs to be participatory, intensive and

should run for at least 4 years.

• Farmer training can build on existing cooperatives

structure, although training capacity is not currently

present in cooperatives so capacity building would be

part of this investment.

• Against this background we budget 75

USD/farmer/year in training costs, assuming 60% of the

farmers to be motivated, the investment would total 145

million USD over 10 years.

23

FARMER TRAINING OFFERS GOOD RETURNS ON INVESTMENT

Indicator Value (10 years)

Cumulative nr of farmers reached 482,040

Additional volume coffee per annum in steady state (Mt)

7,408

Total investment $ 144,612,000

Total return $ 293,814,698

NPV (10%) $ 74,896,890

NPV (20%) $ 42,127,717

Investment per farmer $ 300

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

24

REJUVENATION INVESTMENT TAKES A WHILE TO SHOW EFFECTS...

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

-

1,000

2,000

3,000

4,000

5,000

6,000

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Ad

dit

ion

al s

up

ply

(M

t)

Additional supply from rejuvenation (Mt)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Vla

ue

(h

a)

Acreage rejuvenated (ha)

• Replanting is necessary, especially with estates moving away from coffee. However with current low farmer incomes, the investment is not likely coming from the farmers and adoption rate is estimated at 20%.

• Some existing projects have realized good results with community or cooperative nurseries, and grafting support. These are relatively cost efficient methods of rejuvenation.

• Return on investment is excellent for those producers that can afford or get access to finance, but due to low expected adoption rates the overall volume effect is ~10%.

• Replanting can also increase resilience with resistant varieties.

25

RETURN ON INVESTMENT IS POSITIVE FOR THOSE THAT CAN AFFORD

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Indicator Value (10 years)

Cumulative acreage replanted (ha)

13,620

Additional volume coffee per annum in steady state (Mt)

5,407

Total investment $ 2.451,600

Total return $ 142,081,653

NPV (10%) $ 67,943,544

NPV (20%) $ 36,018,641

Investment per ha $ 180

26

INPUT SUPPLY INVESTMENT HAS LARGE IMPACT

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

vla

ue

(h

a)

Acreage with enhanced input use (ha)

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Ad

dit

ion

al s

up

ply

(M

t)

Additional supply from input use (Mt)

• Small-scale farmers tend to be risk averse as one failed crop is enough to undermine their living conditions.

• Fertiliser investment can be risky, but farmers would have to finance 20%-30% from equity.

• Limited extra use of inputs can be promoted to match risk appetite of farmers and generate additional production.

• Only farmers that are part of the training programme should make use of the additional input supply investment to ensure optimal use.

• Several projects in Kenya have successfully demonstrated use of organic fertilizer from on farm livestock.

27

INPUT USE STILL LOW, BUT COULD GROW AS FARMERS’ EQUITY INCREASES

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Indicator Value (10 years)

Acreage using additional inputs in steady state (ha)

34,050

Additional volume coffee per annum in steady state (Mt)

17,228

Total investment $ 20,217,188

Total return $ 632,833,365

NPV (10%) $ 336,917,079

NPV (20%) $ 204,195,305

Investment per ha per year $ 75

28

STRENGTHENING COOPERATIVES IMPROVES

SUPPLY CHAIN EFFICIENCY

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

• Smallholders with <5 acres (<2ha) are required by law to join a cooperative. KNBS indicates 800.000 smallholders organized in 600 cooperatives. We estimate that about 50% of these cooperatives has the need and potential to improve.

• Main objective of the farmer organisation building program is to improve supply chain efficiency: better utilization of processing assets and increase of farmer share of coffee price.

0

100,000

200,000

300,000

400,000

500,000

0

200,000

400,000

600,000

800,000

1,000,000

Baseline 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Nu

mb

er

of

farm

ers

in p

rog

ram

Nu

mb

er

of

farm

ers

org

an

ize

d

Number of farmers in farmer organisations

Cumulative nr of farmers in organisation building programme

Membership of farmer organisations with limited improvement potential

Baseline membership base

Annual nr of farmers in organisation building programme

29

COOPERATIVES WILL INCREASE VOLUMES

FOLLOWING INCREASED FARM YIELDS

• Expert judgements from the sector set the

investment in improving farmer organisations at

around 20USD/farmer/year.

• Since smallholder are currently only allowed to sell

through cooperatives, the supply rate is not

expected to change.

• Productivity improvements from other

interventions help to grow supply through

cooperatives.

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

0%

10%

20%

30%

40%

50%

60%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1 2 3 4 5 6 7 8 9 10

Fa

rme

rs'

sup

ply

ra

te (

%)

Vo

lum

e (

Mt)

Volume marketed through farmer organisations (Mt) and farmers'

supply rate (%)

Annual volume marketed through farmer organisations

Baseline volume farmer organisations

Share of farmers' supply exported through farmerorganisations

30

COMMERCIALLY, INVESTMENT IN FARMER

ORGANISATIONS IS NOT VIABLE

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Indicator Value (10 years)

Number of farmers in improved farmer organizations in steady state

800,000

Volume of coffee marketed through farmer organizations in steady state (Mt)

46,872

Additional farm gate value per annum in steady state

$ 507,163

Total investment $ 31,131,750

Total value redistribution $ 3,745,785

NPV (10%) $ -20,168,346

NPV (20%) $ -15,266,565

• Improved supply chain efficiency through

cooperatives can significantly increase farm gate

price.

• This investment does not create additional value

at sector level, but rather redistributes existing

value in the chain with improved farm gate prices

as a result.

• Donors that do not seek a commercial return on

their investment would be required for this type of

intervention.

• The 4 combined interventions show a positive impact on the farmer business case, improving revenues by 64% from both price and yield improvement, and increasing profit by factor 2.6.

• Total producer income would then increase to 318 USD/household per year.

• This however is still not sufficient for a full farming family in relation to the poverty line (value of home consumption of other crops not factored in).

• To lift farmers out of poverty, further income is needed but seems currently unlikely.

• The business case for medium to large estates is significantly better than the business case for smallholder farmers.

31

SIGNIFICANT POSITIVE IMPACT ON FARMERS, BUT POVERTY PERSISTS

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

0

200

400

600

800

1,000

1,200

1,400

0

50

100

150

200

250

300

350

400

Va

lue

(U

SD

/ye

ar)

Improved farmer business case for Arabica in comparison to poverty

line

Programme effect

Income

Cost

Poverty line (USD1.9/day/person, PPP adjusted)

• Investment in coffee can significantly increase the

sector value for all actors in the value chain. The

majority of value flows into the rural economy.

• As productivity improves, local supply chains

benefit, primarily from additional supply.

• Additionally, an improved supply chain efficiency

should bring additional value to farmers.

32

NATIONAL BUSINESS CASE: SIGNIFICANT INCREASE IN SECTOR VALUE FOR ALL

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Summary USD over 10 years

Total investment $ 198,412,538

Total return $ 1,068,729,715

NPV (10%) $ 457,561,793

NPV (20%) $ 265,866,332

0

50

100

150

200

250

300

350

400

Baseline sector value Target sector value

Va

lue

(m

illio

n U

SD

)

Impact of investment on national sector value in steady state (M$)

Farmers Local supply chain Government tax revenue

• A large share (54%) of the investment should come from grants.

• This could also be invested by Kenyan government in addition to reserving part of export tax.

• This will be initial seed funding to fill the funding gap and allow investment in farmer organisation building.

• This can however leverage industry funding by attracting roasters and banks.

• Due to low profitability, only a small portion of farmers would be able to invest.

33

INVESTMENT SHARED BY NATIONAL GOVERNMENT, PRIVATE SECTOR, GRANTS

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

Summary Value

ACF revolving fund size $ 16,731,420

Required grant funding $ 106,716,206

Required grant funding % 54%

Required national budget (% export tax)

50% Co

ntr

ibu

tion

s a

re in

dic

ativ

e b

ase

d o

n s

take

ho

lde

r in

pu

t. In

vest

me

nts

an

d c

on

diti

on

s to

be

n

eg

otia

ted

with

in n

atio

na

l pu

blic

priv

ate

pla

tfo

rms

taki

ng

into

acc

ou

nt a

mo

ng

st o

the

rs

inte

rna

tion

al c

om

pe

titiv

en

ess

, go

vern

an

ce, t

ran

spa

ren

cy a

nd

acc

ou

nta

bili

ty a

ssu

ran

ce.

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

Vla

ue

(U

SD

)

Public and private programme contributions

Required seed funding grants

Export tax earmarked for programme

Private sector investment

Farmer investment via fund

Annual programme cost

Required cumulative grants

Required total revolving fund

CONCLUSIONS

• The coffee sector in Kenya is in decline, and would need investments of both private and public sector

if it is to be revived. Currently farmers are abandoning coffee is favour of other crops.

• There is significant potential to increase coffee sector value in Kenya through selective investment in

farmer training, farm rejuvenation, use of inputs and farmer organisation building. Volumes could

increase to ~75.000 Mt per annum. The increased value largely flows into rural economy.

• Coffee alone will not provide sufficient income for a full farmer household, under current conditions it

appears unlikely that the gap to the poverty line can be met with agricultural activities. It is unlikely that

farmers will be lifted out of poverty in the short- to mid-term, despite investments.

• Total programme investment amounts to an estimated 198 million USD over 10 years that would

generate a return across the sector of >1 billion USD at current prices.

34

SEPTEMBER 16AFRICAN COFFEE SECTOR: ADDRESSING NATIONAL INVESTMENT AGENDAS ON A CONTINENTAL SCALE

35

SEPTEMBER 16AFRICAN COFFEE SECTOR: addressing national investment agendas on a continental scale

SourcesGlobal Coffee Platform, Olam, GroIntelligence, The Economist, Coffee Sustainability Catalogue, Varqa, Rozimina

DataKenya National Bureau of Statistics, Nairobi Coffee Exchange, US Department of Agriculture, Food and Agriculture Organisation, International Coffee Organisation, USAID, 4C Association, UTZ Certified, Agri-Logic

About the Global Coffee PlatformThe GCP is a collaboration between the 4C Association and the Sustainable Coffee Program of IDH – The Sustainable Trade Initiative. The Global Coffee Platform is an inclusive multi-stakeholder sustainability platform aligning the activities of a diverse network of stakeholders to set into action the global commitments made through Vision 2020 and create a thriving and sustainable coffee sector.

About Agri-LogicAgri-Logic – management, consultancy and research - operates where agricultural production, development, international trade and consumer markets intersect. We combine a thorough understanding of farm level reality and commodity trade with scientific research skills and a track record in sustainability strategy design and implementation, to help clients deal with sustainability challenges and market requirements.

About Valued ChainValued Chain is an independent consultancy. We support organizations in understanding their value chain and stakeholders, identification and mitigation of risks, and realization of opportunities. We believe in integrating commercial objectives with sustainability of the business and its stakeholders. Working from Amsterdam and Lagos, we connect Europe and Africa.