Federal Health Care Reform 2009: Affordable Health Care for All

Upload

careermindsCategory

view

133download

0description

Healthcare Reform Briefing: What HR Should Know

Sponsored by

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

Discussion Topics

• What is happening in 2014?

• Employer interaction with public exchange

• Employer strategies for 2014 and beyond

• Emerging healthcare costs

• Closing thoughts

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

2 December 8, 2013 2 December 8, 2013

Benefits and/or compensation strategy and planning

Recruiting and/or outplacement, I never touch the benefits

HRIS and administration, I have to make sure benefits run

smoothly

All of the above

None of the above, I came for the free shirt

Who is here today? My main focus within HR is…

Choose all that apply.

Please Respond

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

What is happening in 2014

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

2014 is a significant year … Consequences of Affordable Care Act (ACA)

Design &

Marketplace

Changes

No lifetime

dollar limits/ pre-exiting

condition limits

Restricted annual

dollar limits

No waiting period

over 90 days

Out of Pocket Maximum

Wellness Incentives

Exchanges

Employer

mandate

and shared

responsibility

Minimum plan value

and contribution

requirements

(delayed)

Fees

Comparative

effectiveness

research (PCORI)

Fees on

insurers

Manufacturer’s

fees

Temporary

reinsurance

programs

Higher plan

enrollment

Dependents to

age 26

30-hour eligibility

Individual Mandate

Medicaid Expansion

Auto enrollment

(delayed)

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

Employer Mandate and Shared Responsibility High Level Requirements…

Offer cover to “full-time employees” – “Minimum essential coverage”

– Coverage offer to 95% of FT employees and dependent children considered offer to “substantially all”

– FTE is any employee who works on average 30 or more hours per week

– Must offer to FTEs and their dependent children under age 26 (but not required to offer to spouses or domestic partners)

“affordable” health care coverage – An employee’s required contribution for self-only coverage cannot exceed

9.5% of the employee’s household income

with a “minimum value” – The actuarial value of the plan must be at least 60% - The calculation of the

anticipated percentage of the cost of the “essential health benefits” covered by a plan

or, face potential tax “penalties”

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

6

New in 2014: Individual Mandate

All individuals

must have health coverage

Pay penalty

2014

Greater of $95 (single) | $285 cap (family)

or 1% of household income

By 2016

Greater of $695 (single) | $2,085 cap (family)

or 2.5% of household income

OR

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

Single

individual

Family

of four

% of

FPL** Annual household income

Household income >400% of FPL

not eligible for subsidy through

marketplace

400% $45,960 $94,200

300% $34,470 $70,650

200% $22,980 $47,100

150% $17,235 $35,325

138% $15,856 $32,499

100% $11,490 $23,550

* Not all States have agreed to expand Medicaid to 138% of FPL

** Based on 2013 FPL

7

Public Programs in 2014 Medicaid

Expanded to anyone below

138% federal poverty line

Not all states have agreed to expand coverage

• In these states, federal subsidies may be available for certain people to buy coverage

• Those ineligible for Medicaid or federal subsidies may have no option for subsidized coverage other than employer plan (if available)

Insurance plan options available on exchanges that are operated by states or federal government (or a state/federal partnership)

• Exchanges will conduct open enrollment: Oct 1, 2013 to Mar 31, 2014

• If household income is between 100%/138% and 400% of federal poverty level (FPL) – and individual does not have access to affordable employer coverage that provides minimum value– federal government will provide subsidies to buy insurance on exchanges

Medicaid Expansion Public Exchanges

Public Programs in 2014 Medicaid, Public Exchanges and Subsidies

Subsidies

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

Employer Requirements in 2014

8

Ta

xe

s a

nd

Fe

es

• PCORI.

• Temporary Reinsurance Fee.

• Health Insurer Fee.

Co

mm

un

ica

tio

ns • SBCs.

• W-2 reporting of health care costs.

• Exchange Notice.

Pla

n D

es

ign

Re

qu

ire

me

nts

• Maximum 90 day waiting period.

• No limits on pre-existing conditions or essential health benefits.

• Limits on out-of-pocket maximums; counting copayments against OOP max.

• Expansion of Wellness incentives.

• Coverage for clinical trial related services.

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

Interacting with the public exchange

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

10

Healthcare.gov

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

11 December 8, 2013 11 December 8, 2013

1%

10%

20%

40%

What percent of large employers (with over 500 ees) are going

to terminate medical coverage in the next three years?

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

New in 2014: Public Exchange (aka Public Marketplace)

0 5 10 15 20 25 30 35 40 45 50

Employer

Individual

Uninsured

Medicaid/CHIP

Medicare/Gov't

Percent of Population by Current Health Insurance Source*

*Source: U.S. Census, 2011

• Almost all large employers say they will continue to provide health care

benefits in 2014 and beyond.

• Created by ACA.

• Structured marketplace to sell and purchase health insurance operated by states or

federal government (or a state/federal partnership).

• Government subsidized medical coverage for low income individuals and families.

• Exchanges will conduct open enrollment: Oct 1, 2013 to Mar 31, 2014.

Will benefit from government programs – Expanded

Medicaid and Public Exchanges in 2014

12

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

What do the public exchanges do?

13 December 8, 2013

Manage Plan Activities

Determine eligibility, enroll individuals

Assist consumers

Provide financial management

Ensure plan accountability

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

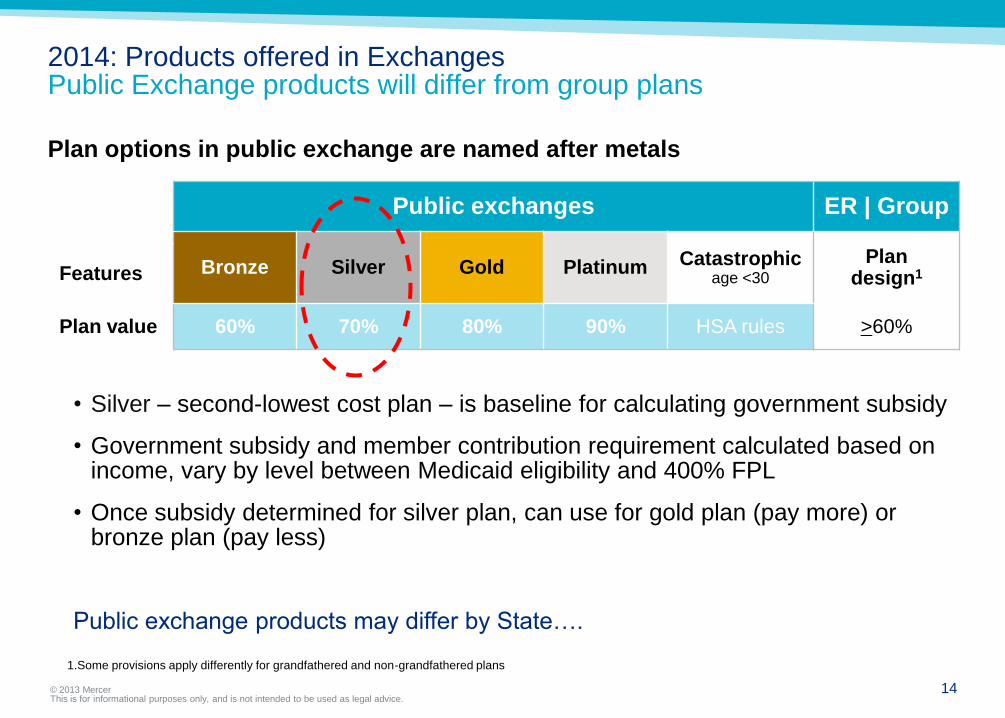

2014: Products offered in Exchanges Public Exchange products will differ from group plans

Plan options in public exchange are named after metals

Public exchanges ER | Group

Bronze Silver Gold Platinum Catastrophic age <30

Plan design1 Features

Plan value 60% 70% 80% 90% HSA rules >60%

14

1.Some provisions apply differently for grandfathered and non-grandfathered plans

• Silver – second-lowest cost plan – is baseline for calculating government subsidy

• Government subsidy and member contribution requirement calculated based on income, vary by level between Medicaid eligibility and 400% FPL

• Once subsidy determined for silver plan, can use for gold plan (pay more) or bronze plan (pay less)

Public exchange products may differ by State….

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

Public Exchanges Status of State Exchanges (as of March 2013)

15 15

Sources: Kaiser Family Foundation (states); HHS, HealthCare.gov (territories)

Default to federal exchange 27 Declared state exchange 22 Planning partnership exchange 7

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

Employers and Public Exchanges How Will It Work When Employees Apply For Subsidies?

Individual applies to Exchange

Provides & attests to certain info including:

• income and family size

• lowest cost employer plan option that meets minimum value (employee only cost)

1 Exchange verification

Verifies income and other info

Verification process for employer coverage (statistical sample only)

Individual can enroll during verification process

2 Exchange Eligibility Notice

• Notice to individual of eligibility determination after verification complete

• Notice to employer if individual determined eligible for exchange subsidies after verification complete

3

Employer Appeal 4 IRS reporting &

reconciliation

After close of calendar year, IRS has at least three sources of info to confirm subsidies were provided correctly:

• Employer reporting

• Exchange reporting

• Individual tax filing

5

16

• Employer requests appeal within 90 days of notice described in step 3

• Exchange tells employee of appeal request

• Written appeal decision w/in 90 days of receipt of appeal request

IRS Employer Shared Resp process

6

IRS has said, after employee tax returns for coverage year are due:

• IRS will contact employer about possible liability

• Employer response

• IRS notice & demand for payment

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

17 December 8, 2013 17 December 8, 2013

Few will be eligible

10%

20%

40%

All employees are eligible

What percent of your organization’s employees are going to

be eligible for the subsidy on the public exchange?

Choose all that apply.

Please Respond

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

18

What household income is needed to receive subsidized government insurance?

May be eligible for subsidy

Single

individual

Family

of four

% of

FPL** Annual household income

Household income >400% of FPL

not eligible for subsidy through marketplace

400% $45,960 $94,200

300% $34,470 $70,650

200% $22,980 $47,100

150% $17,235 $35,325

138% $15,856 $32,499

100% $11,490 $23,550

* Not all States have agreed to expand Medicaid to 138% of FPL ** Based on 2013 FPL

Medicaid eligible*

Income segments

under health reform

No government subsidy

© 2013 Mercer This is for informational purposes only and is not intended to be used as legal advice.

Employer Strategies – 2014 and Beyond

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

*Projected

Source: Mercer’s National Survey of Employer-Sponsored Health Plans; Bureau of Labor Statistics, Consumer Price Index, U.S. City Average of Annual

Inflation (April to April) 1990-2013; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey (April to April)

1990-2013.

The Good News: employers expect to hold per-employee health benefit cost growth to 4.8% in 2014 But the increase in per-employee cost does not reflect rising enrollment

17.1%

12.1%

10.1%

8.0%

-1.1%

2.5%

0.2%

6.1%

8.1%

11.2%

14.7%

10.1%

7.5%

5.5% 4.8%*5.0%*

4.1%

6.1%6.9%

6.3%6.1%6.1%6.1%7.3%

2.1%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Workers' earnings

Annual change in total health benefit cost per employee

Overall inflation

© 2013 Mercer This is for informational purposes only and is not intended to be used as legal advice.

21

Issues That Are Top of Mind for Employers as They Look Beyond 2014

Continued cost increase due to Affordable Care Act.

Educating employees about their choices and supporting informed

decisions.

Handling employee questions about the public exchange.

Administrative issues (tracking employee hours, look-back period).

Staying on top of all the Affordable Care Act requirements.

Anticipation of the excise tax in 2018.

Source: Mercer Survey, HCR Road to Implementation, June 2013

© 2013 Mercer This is for informational purposes only, and is not intended to be used as legal advice.

Employers React to Affordable Care Act in 2014 & Make the News…

UPS drops coverage for working

spouses and estimates covering

children to age 26 will cost $60M

Starbucks announced that it will not be

cutting benefits for spouses/partners or

reducing hours for workers so that they do

not qualify for benefits

Darden and Sears joined a fully insured

private exchange and Darden stopped

offering full time qualifying hours to many

employees

Delta Airlines faces an increase of $100M

in medical costs in 2014 between normal

trend and ACA requirements (appears to

be at least 38% of the increase)

Xerox is increasing their working

spouse surcharge to $1,500 annually in

2014

Walmart has been focusing on hiring

temporary employees to manage

healthcare costs under ACA

The Hamilton School District in

Trenton, NJ will be limiting substitute

teachers to 4 days per week to avoid

30 hour per week threshold

Clothing retailer Forever 21 (27,000

employees total) announced

reclassification of non-management

positions from FT to PT effective Sept. 1,

2013 based on a reduction of hours to a

maximum 29.5 hours per week

22

© 2013 Mercer This is for informational purposes only and is not intended to be used as legal advice.

23 December 8, 2013 23 December 8, 2013

Status quo – perhaps tweak the current approach and monitor

Introducing High Deductible Health Plans (HDHPs)

Adding a 60% plan or “low” option

Focusing on health management or wellness incentives

Other changes such as adjusting eligibility for spouses, etc.

Is your organization thinking or considering any of the

following to manage costs?

Choose all that apply.

Please Respond

© 2013 Mercer This is for informational purposes only and is not intended to be used as legal advice.

December 8, 2013

Employers’ responses are all over the board!

24

24% Make all

employees

eligible for

the FTE plan

17% Offer the FTE plan

to some, but not

all, newly eligible

employees

27% Add a

lower-cost

plan for

newly

eligible

hourly

employees

31% Add a low-

cost plan

as the

default for

auto-

enrollment

13% Where contributions

are “unaffordable”

add a less

expensive plan

51% Change workforce strategy so fewer employees work 30+ hours/week

© 2013 Mercer This is for informational purposes only and is not intended to be used as legal advice.

Public Vs. Private Exchanges What is the Difference?

December 8, 2013 25

Medical,

prescription

Dental, vision, life,

voluntary, plus more

Government

sponsored

Employer, broker,

TPA, association

Actives, retirees

PUBLIC PRIVATE

Open Closed

Single or

multiple carrier

Individuals Group plans

Insured or

self-funded

Standalone

dental

Insured only

© 2013 Mercer This is for informational purposes only and is not intended to be used as legal advice.

Private Exchanges In a Picture

EXCHANGE

Ven

do

rs

& c

arr

iers

Medical Dental Ancillary

Ben

efi

ts

ad

min

Eligibility &

enrollment

Consolidated

billing

Additional

features

Co

ns

um

er

ex

pe

rie

nc

e

Full product suite with choice of plans

Health Life, accident

& disability Voluntary

26

$

$

Employer

contribution

Consumer

enrollment portal

Decision tools

&/or call center

Multiple payment

models

27 December 8, 2013

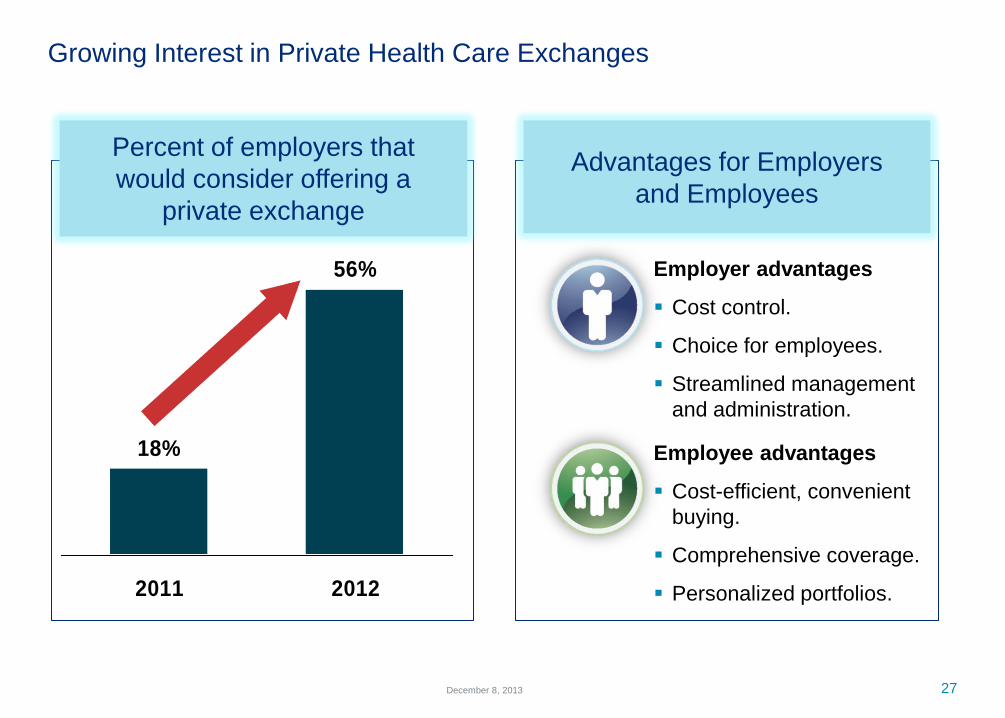

Growing Interest in Private Health Care Exchanges

18%

56%

2011 2012

Percent of employers that

would consider offering a

private exchange

Employer advantages

Cost control.

Choice for employees.

Streamlined management

and administration.

Employee advantages

Cost-efficient, convenient

buying.

Comprehensive coverage.

Personalized portfolios.

Advantages for Employers

and Employees

© 2013 Mercer This is for informational purposes only and is not intended to be used as legal advice.

Closing thoughts

© 2013 Mercer This is for informational purposes only and is not intended to be used as legal advice.

Closing Thoughts…

• Short term – Employers focused on cost management

and ACA compliance

– Expanded eligibility, minimum plan design, and affordable

contributions in 2015.

– Excise tax in 2018.

• Still some unknowns about the ACA

– Auto-enrollment.

– Reporting and disclosure.

– Could there be more delays?

• Longer term – things will change!

– New products/approaches.

– Funding changes.

– Delivery system transformations.

29

MERCER

Services provided by Mercer Health & Benefits LLC.

Thank You

MERCER

Mercer is not engaged in the practice of law and this presentation, which

may include commenting on legal issues or regulations, does not

constitute and is not a substitute for legal advice. Accordingly, Mercer

recommends that employers secure the advice of competent legal

counsel with respect to any legal matters related to this report or

otherwise.

The information contained in this document and in any attachments is

not intended by Mercer to be used, and it cannot be used, for the

purpose of avoiding penalties under the Internal Revenue Code or

imposed by any legislative body on the taxpayer or plan sponsor.