Affordable Care Act (ACA): What Every Rehab Professional Should Know February 7, 2014 NYU Wasserman...

60

Affordable Care Act (ACA): What Every Rehab Professional Should Know February 7, 2014 NYU Wasserman Center presented by Anthony LaGattuta, MBA, MA, EA

-

Upload

marshall-gray -

Category

Documents

-

view

214 -

download

0

Transcript of Affordable Care Act (ACA): What Every Rehab Professional Should Know February 7, 2014 NYU Wasserman...

Affordable Care Act (ACA):

What Every Rehab Professional Should Know

February 7, 2014 NYU Wasserman Center presented by Anthony

LaGattuta, MBA, MA, EA

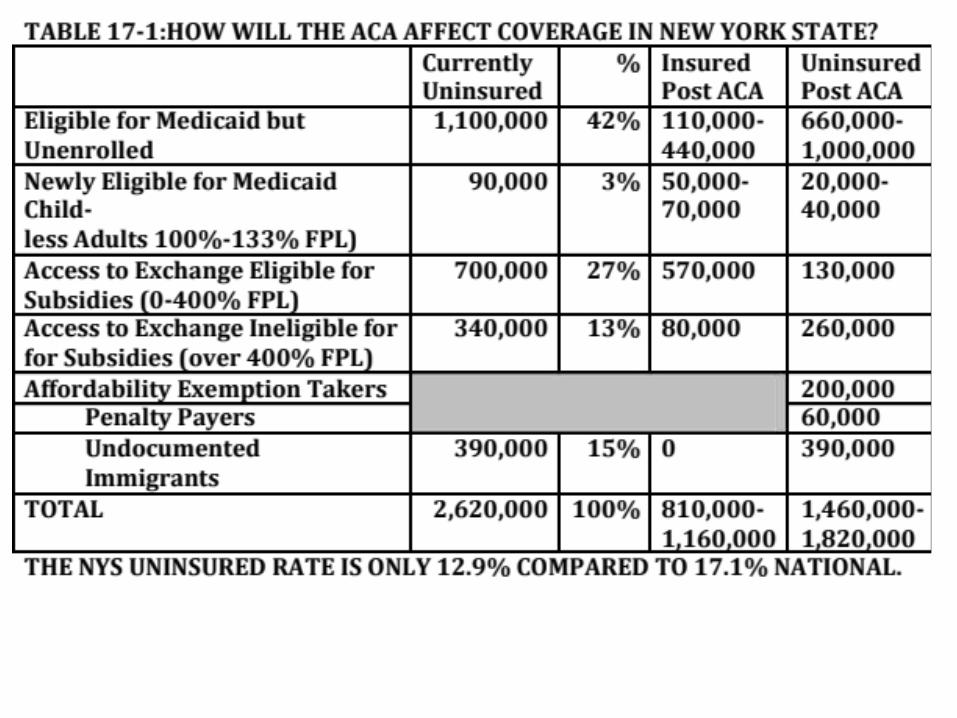

The Affordable Care Act: Impact on NYS

WORK DISINCENTIVES: LOSS OF PUBLIC SUPPORTED HEALTH BENEFITS

4

Today’s Agenda

• Brief History Health Care Reform• The Problem(s): Uninsured and

Unsustainable Costs• Solution:

– Insurance Market Reform & Employer ER Mandate– Individual Responsibility-- Insurance Purchase Subsidies and Public

Programs• Revenue• Quality/Health Care Reform• Help in NYS

Material consulted:Inside National Health Reform by John E. McDonough; Health Care Reform Simplified: What Professionals in Medicine, Government, Insurance, and Business Need to Know by Dave Parks; ObamaCare Survival Guide: The Affordable Act and What It Means for You and Your Healthcare by Nick J. Tate; Why Obamacare is Wrong for America: How the New Health Care Law Drives Up Costs, Puts Government in Charge of Your Decisions, and Threatens Your Constitutional Rights by Grace-Marie Turner, James C. Capretta, Thomas P. Miller and Robert E. MoffitBeating Obamacare: Your Handbook for Surviving the New Health Care Law by Betsy McCaughey; Selected Tax and Other Provisions of the 2010 Health Care by Danny Santucci (A Continuing Education Course for Tax Practitioners);Implementing Federal Health Care Reform: A Roadmap for New York State by the NYS Health Foundation;“System Failure: How Obama Botched Obamacare” by Charles R. Morris and “Health Scare: Obamacare Is Down but Not Out” by J. Peter Nixon—Articles in 12/20/13 edition of Commonwealth; PowerPoint Presentations by: Kaiser Foundation, Empire Justice Center, Legal Aid Society.

TABLE 17-2: HISTORY OF HEALTH CARE REFORM

6

• TR, FDR, TRUMAN, JOHNSON, CARTER, CLINTON (S), OBAMA• PRIVATE INSURANCE FOR THE WEALTHY IN THE 1920S• SECTION 106 OF THE INTERNAL REVENUE CODE EXEMPTS HEALTH INSURANCE

ESPECIALLY AFTER WW2 SINCE WAGE CONTROLS. HEALTH INSURANCE PROVIDED PRIMARILY BY EMPLOYERS AND UNIONS. NOW COST OF HEALTH INSURANCE APPEARS ON THE W-2-SUBJECT TO TAX IF IT EXCEEDS CERTAIN THRESHOLDS (“CADILLAC PLANS”)

• MEDICARE/MEDICAID CAME IN UNDER JOHNSON IN 1965; LEADERS HAD HOPED TO EVENTUALLY TO COVER EVERYONE JUST AS SSA ITSELF HAD EXPANDED TO COVER MOST OF THE POPULATION.

• “HILARYCARE” WOULD HAVE REORGANIZED WITH 159 BOARDS THE PRIVATE MARKET AROUND REGIONAL ALLIANCES AND HMOS AND WOULD INSURE AFFORDABLE PREMIUMS . THE PLAN WAS DEVELOPED WITH HER “CABAL” OF 500 BUT KEPT OUT THE PUBLIC. THE INSURANCE CARRIERS AND MOST OF THE MEDICAL PROVIDERS PUSHED BACK. REMEMBER “THELMA AND LOUISE”. EVEN WITH A MAJORITY THE DEMOCRATS COULD NOT AGREE ON A BILL.

• IN 1997 CLINTON PASSED THE CHIP PROGRAM COVERING CHILDREN KENNEDY AND HATCH MANAGED THIS LEGISLATION THRU.• MGRS OF ACA TRIED TO WORK THRU CONGRESS WITH BOTH PARTIES AND

BROUGHT IN THE INSURANCE CARRIERS AND MEDICAL PROVIDERS.• WHAT CHANGED? UNSUSTAINABLE GROWTH OF MEDICAL INSURANCE COSTS

[1/6TH OF ECONOMY) AND THE NUMBER OF THE UNINSURED/BANKRUPTS ESPECIALLY WITH THE GREAT RECESSION. ALSO “ROMNEYCARE”

The Problem

• 50 million people uninsured• Costs rising• Fragmented coverage and care• Insurance company practices

don’t cover “pre-existing conditions” lifetime and annual limits drop people when they get sick

Possible Solutions?

Right

Tax Credits

• free market

• doesn’t solve all the problems

Left

Single payer

• big government

• “non-starter” in this political environment

Solution

• Build on current system

T Mix of public and private

• Fix the problems

T Increase access and affordability

15

ACA Vision

• ACA has a two-fold vision – universal coverage and cost control

• Cost control provisions relate primarily to changing the way we deliver care– Payment reforms– New service delivery models

• Universal coverage provisions utilize a “three-legged stool” approach

The Three-legged Stool

16

• First leg is insurance market reform (affecting employer and individual coverage) – Reforms w/out reductions

• Second leg is individual responsibility• Third leg is insurance purchase subsidies

(individuals and small businesses) and public programs – Eligibility streamlining and expansion – Coordinated enrollment with Exchange– New marketplace (negotiating leverage for

states) with tax subsidies up to 400% FPL

ROCKY ROLL-OUT•Website problems-volume, complexity, language/culture, accessibility•People dropped from plans not meeting guidelines or just being dropped•More doctors dropping out from Medicare/ Advantage (11 States) or not in Medicaid•Few psychiatrists to cover up mental health and behavioral disorders•People don’t want Medicaid-only to purchase on the exchange•Many premiums higher than anticipated•Some people not covered still where Medicaid not expanded or loss of DSH$•Not enough younger workers buying in yet: the “the death spiral”•Using future Medicare cuts to fund unemployment insurance•Confusion about (children’s) dental insurance that is often a separate insurance•The suspending of Title IX (CLASS) and limits on the 1099s for payments of $600+ *•Almost 2000 waivers for large employers for full compliance *one of many unrelated tax measures

Some countervailing positive forces:Health premiums have been leveling off Once people are enrolled especially in Medicaid it will be hard to throw them outŸ Once people choose a health care plan they are likely to stay with despite a change of jobs

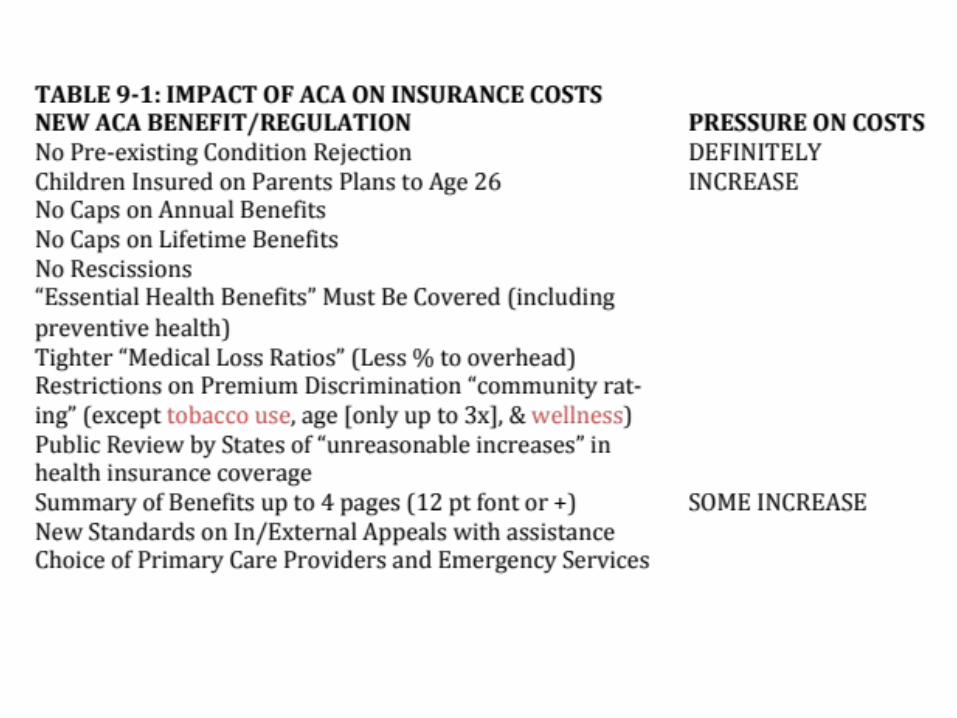

TEN “ESSENTIAL BENEFITS”**Ambulatory patient services**Emergency services **Hospitalization**Maternity and newborn care**Mental health and substance use disorder services (including behavioral health treatment)**Prescription drugs**Rehabilitation and habilitative services and devices**Laboratory services**Preventive and wellness and chronic disease management**Pediatric services, including oral(dental) and vision care Note: grandfathered plans temporarily exempt from these requirements.

Income (cont’d)MAGI

MAGI is Modified Adjusted Gross Income is

based on IRS rules.

Section 36B(d)(2) of Internal Revenue code of 1986; 42 C.F.R. § 435.603(d); 42 C.F.R. § 435.603(e)

Gross Income

Gross income = wages, SS income, investment income, unemployment, pensions, IRA distribution, alimony, and income from self-employment,

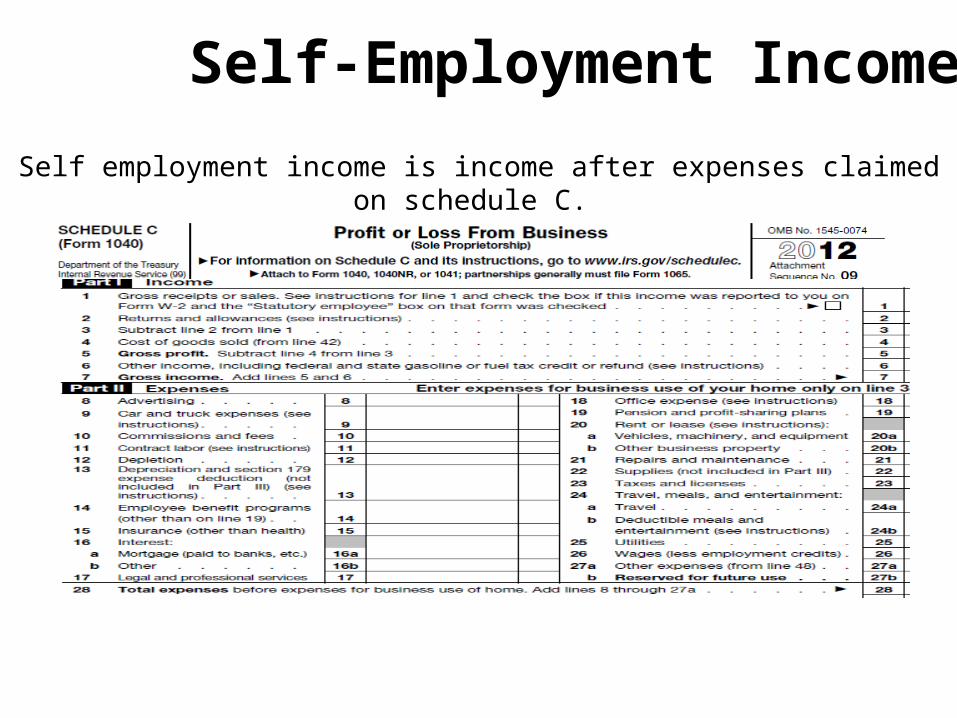

Self-Employment Income

Self employment income is income after expenses claimed on schedule C.

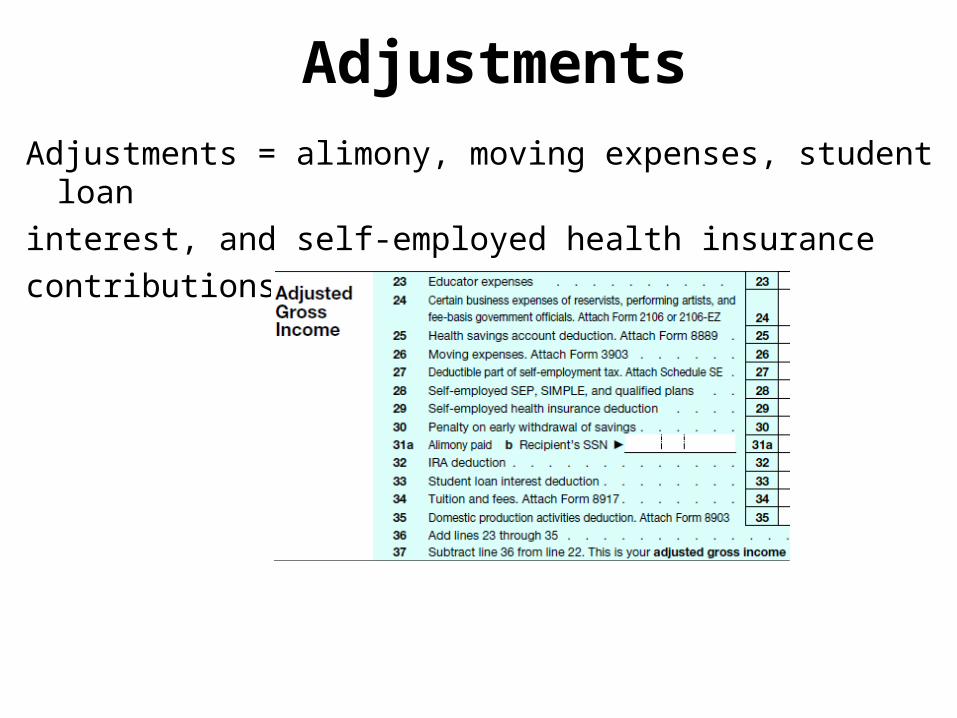

AdjustmentsAdjustments = alimony, moving expenses, student loan interest, and self-employed health insurance contributions

Income Disregards

Old Rule = Many disregard rules.

New Rule = Only 1 disregard: 5% of your Modified Adjusted Gross Income. 133% becomes 138%

42 U.S.C. § 1396a(14)(I)(i); 42 C.F.R. § 435.603(d)(1)

ResourcesOld Rule – No Resource Test

New Rule – NO CHANGE. No Resource Test

42 U.S.C. § 1396a(C); 42 C.F.R. § 435.603(g)

Alignment is not perfect in NYS…

Traditional Eligibility Categories

MAGINew Eligibility Group

41

42

Coordinated Enrollment

• Single application for tax subsidies, Medicaid and Child Health Plus

• Applications must have on line, in person, mail and telephone options

• Data matching through SSA, State Labor, Treasury & Homeland Security

• Both Exchange & Medicaid agency must screen for all programs &, if agreement:– Governmental Exchange can enroll in Medicaid– Medicaid agency can enroll in subsidies

HEALTH CARE REFORMNOT EVERY CHANGE THAT OCCURS FROM NOWON IS “OBAMACARE,” BUT PRETTY NEARLY SO.THE FOLLOWING TWO SLIDES CONTAIN SOME

72 KEY PROVISIONS.

Navigators

While there is plenty of assistance available, we should recommend consumers to seek our “Navigators,” who counsel applicants and submit applications directly. Referral should be made to the Centers for Independent Living (such as CIDNY) and other advocacy groups. Undocumented immigrants still may be able to get some assistance for their children and, thus, should be recommended to go to agencies serving immigrants (such as Catholic Charities).

More Information

• www.healthcare.gov• https://nystateofhealth.ny.gov• http://obamacarefacts.com• healthreform.kff.org/the-animation.aspx• www.nymetronra.org